Embed Size (px)

Citation preview

Investor visit AkzoNobel Brazil

Rob Frohn

Member of the Board of Management and the Executive Committee responsible for Specialty Chemicals

May 18, 2011

• AkzoNobel & strategic ambitions – Rob Frohn

• Brazil & AkzoNobel – Jaap Kuiper

• Specialty Chemicals in Brazil - Antonio Carlos

Francisco

• Performance Coatings in Brazil - Almir Gozzi

• Decorative Paints in Brazil - Jaap Kuiper

• Questions

Agenda

1Investor visit AkzoNobel Brazil

AkzoNobel key facts

2

2010

• Revenue €14.6 billion

• 55,590 employees

• EBITDA: €2.0 billion*

• Net income: €0.8 billion

• 39 percent of revenue from high-growth markets

• A leader in sustainability

* Before incidentals

Revenue by business area EBITDA* by business area

Investor visit AkzoNobel Brazil

Our strategic ambition is to be

3Investor visit AkzoNobel Brazil

Our medium term strategic goals

4

• Grow to €20 billion revenues

• Increase EBITDA each year,

maintaining 13-15% margin

• Reduce OWC/revenues by 0.5

p.a. towards a 12% level

• Pay a stable to rising dividend

• Top quartile safety

performance

• Top position in sustainability

• Top quartile performance in

diversity, employee engagement,

and talent development

• Top quartile eco-efficiency

improvement rate

Investor visit AkzoNobel Brazil

Aspirations for high-growth markets

5

Double revenues in China

• Grow from $1.5 to $3 billion of revenues

• Make a step change in people development

Create significant footprint in India

• Grow from €0.25 to €1 billion of revenues

• Increasing footprint for all business areas

Outgrow the competition in Brazil

• Grow from €0.75 to €1.5 billion of revenues

• Become clear market leader in all our activities

Expand in Middle East and Sub-Saharan Africa

Investor visit AkzoNobel Brazil

High-growth markets will become significantly more important

6

% of revenue, indicative

High-growth markets will be around 50% of revenue in this decade

32%

„Mature‟ Europe

25%

Asia Pacific5%

ME&A

11%

Latin America

18%

North America

9%

„Emerging‟ Europe

Investor visit AkzoNobel Brazil

Brazil & AkzoNobel

Jaap Kuiper, Managing Director Decorative Paints Latam

AkzoNobel |

AkzoNobel |9

Do you know Brazil?

10 Reasons to Believe in Brazil

13

1. Strong Democracy

Investor visit AkzoNobel Brazil

14

2. Diversity

Investor visit AkzoNobel Brazil

15

3. Demographic DevelopmentMonthly Family Income

Source: IBGE / FGV

Investor visit AkzoNobel Brazil

16

4. Unemployment Rate (%)

Source: IBGE / BSL / Eurostat

8,8

5,6

9,5

Investor visit AkzoNobel Brazil

17

Source: Brazil Central Bank

5. Credit Expansion (€ Billion)

748

Investor visit AkzoNobel Brazil

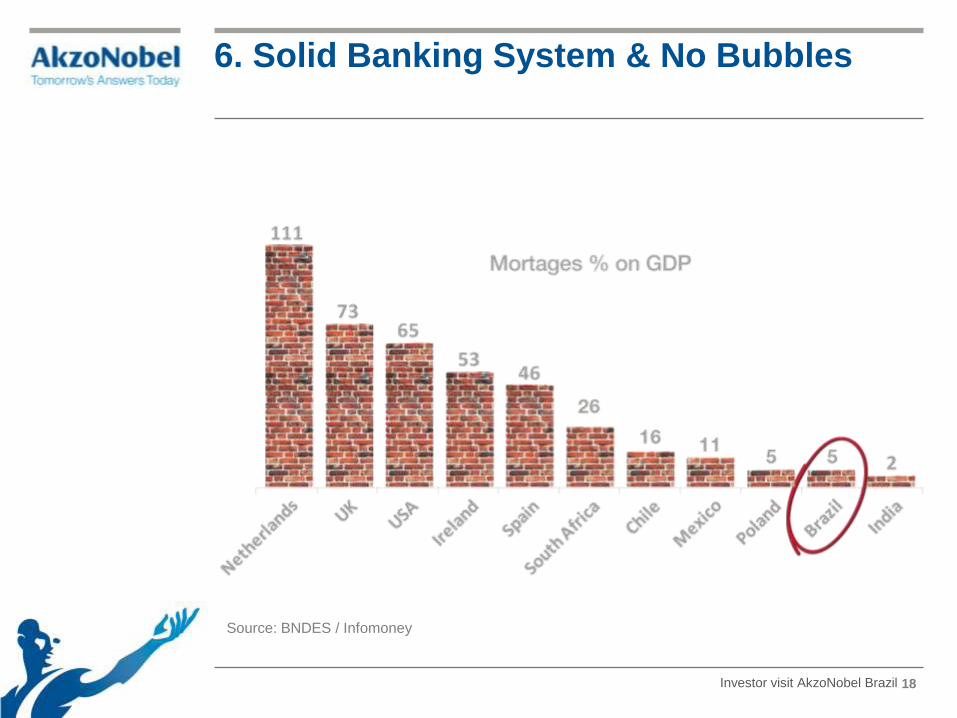

18

6. Solid Banking System & No Bubbles

Source: BNDES / Infomoney

Investor visit AkzoNobel Brazil

19

7. Inflation at bay(%)

Source: Brazil Central Bank

… relatively

Investor visit AkzoNobel Brazil

20

7. Inflation Projection (%)

2010 2011 2012

Central Bank 5.9 5.6 4.2

IMF 5.9 5.9 4.5

OECD 5.9 5.3 5.1

Latin Focus 5.9 5.8 4.8

Investor visit AkzoNobel Brazil

21

8. Brazil International Reserves

Source: Brazil Central Bank

289

Investor visit AkzoNobel Brazil

22

9. Brazil: Commodity King

Exports

No 1 in Iron Ore

No 1 in Meat

No 1 in Coffee

No 1 in Sugar

No 1 in Tobacco

No 1 in Orange Juice

No 1 in Ethanol&Biodiesel

No 2 in Soy

No 4 in Cellulose

Investor visit AkzoNobel Brazil

23

10. Big Opportunities

Investor visit AkzoNobel Brazil

24Business Unit | Title

Attention Points

1. Education System

25

- Investments in basic education – but without quality:

- 1 in 5 Brazilians are functional illiterates

- Lack of investments in Medium and Superior education

Source: IBGE

Investor visit AkzoNobel Brazil

2.Taxes

26

Source: IBGE / FGV

- 85 different taxes

- 36% of GDP are taxes

- An average company spends 1,5% of revenues in dealing

with tax requirements

Investor visit AkzoNobel Brazil

3. Interest Rate (%)

27

Source: Brazil Central Bank

Interbank (Selic)

Individuals

Companies

45,0

31,3

12,0

Investor visit AkzoNobel Brazil

4. Legal System

28

Source: Jus Navigandi Portal/Exame Magazine

- Arcaic structure

- Brazilian law allows almost limitless appeals

- Extremely slow process – average time is 10 years;

- Excess of demands and assignments – 3,4K process per judge

waiting closure.

Investor visit AkzoNobel Brazil

29

Savings and Investment Rates (%GDP)

Source: World Bank

China India Russia

54%

45%

38% 40%

32%

26%18% 20%

Savings (% GDP) Investments (% GDP)

Brazil

Investor visit AkzoNobel Brazil

30

Investment acceleration surpasses other emerging countries

Investment Growth (%)

Investm

ent

Rate

over

GD

P (

%)

Source: IMF and Credit Suisse

Investor visit AkzoNobel Brazil

31

Long Term Challenges

Low Standard or costly infrastructure including

telephones, transport networks, utilities

Failure to honour contracts, bribery, corruption,

weak corporate governance

Lack of key skills including management

Poor quality control

Rising wages / low productivity

Underdeveloped retail and distribution systems

Credit risk

Availability of credit

Difficult relations with organised labour

Saturated markets

Source: EIU, HSBC

Investor visit AkzoNobel Brazil

Let‟s come back to inflation

32

Inflation expectation in 2011

Source: Tendências Consultoria

Investor visit AkzoNobel Brazil

Brazil is like the Amazon

BeautifulRich

Vibrant

Attractive...

…But it can be dangerous!

AkzoNobel in Brazil

Who we are…

• 3 legal entities in Brazil:

• 2 Pulp&Paper;

• 1 Other BUs;

•2010 revenues of € 887M

•2.701 employees

•9 BUs

•14 manufacturing sites

• listed in the main Brazilian

business ranking

• Exame

• The 181st in 2010

and 390th 2009

36Investor visit AkzoNobel Brazil

…and what make us proud

1st Place at Social Responsibility / Sustainability Rank

Source: Isto e Dinheiro - 2010

37Investor visit AkzoNobel Brazil

Great national projects...

1.Sustainability

2.Dialogue

38Investor visit AkzoNobel Brazil

...and local community projects

1.Social Responsibility

2.Engagement

39Investor visit AkzoNobel Brazil

41%

83%

17%

42%

80%

20%

17%

81%

19%

Total Employees

Male

Female

Performance Coatings Decorative Paints Specialty Chemicals

Our people…

• 2.701 employees in Brazil

(April 2011)

• 70 handicapped people work

in AkzoNobel

• EUR 2,5 MM of training

investments in 2010

40Investor visit AkzoNobel Brazil

…building the local talent base.

Developing our

People

MEP/AMP

100% of leader

population by 2011

Recognizing Talent

POC Program to

provide 100 of the new

jobs needed until 2015

BU Synergies

HAY will produce a new

design for a job

structure that have both

consistency and

respect BU singularities

41Investor visit AkzoNobel Brazil

31% 27% 27% 27%

40% 43% 44% 44%

30% 30% 29% 29%

2008 2009 2010 Colunas2 2015

Performance Coatings Decorative Paints Specialty Chemicals

2010 revenue €887 million

Source: BUs

Brazilian Sales. It includes export but not local intercompany sales

AkzoNobel Brazil – Revenue

42Investor visit AkzoNobel Brazil

Our achievements

• Robust growing business

• Leadership positions in

EKA, Packaging, Marine

• Strong Position in Deco and

Car Refinishes

• Good reputation in social

responsibility and

sustainability

• Leadership position in PR -

Ad Equivalence and Social

Media Activation

• Platform for shared services

focused in country

approach

43Investor visit AkzoNobel Brazil

Our challenges

• Leverage the business

and process synergies

over 9 BUs

• To have only nº 1 or nº 2

positions in all business

• Increase diversity:

women and handicapped

people

• Top quartile for employee

engagement

44Investor visit AkzoNobel Brazil

Specialty Chemicalsin Brazil

Antonio Carlos Francisco

General Manager Pulp and Paper Chemicals Brazil

The chemical industry value chain

Industrial Chemicals

Surface Chemistry

Pulp and Paper Chemicals

Functional Chemicals

Mining, oil,

biomaterials

Base

chemicals

Chemical

inter-

mediates

Performance/

functional

chemicals

‘End’

products

Investor visit AkzoNobel Brazil 46

Our Specialty Chemicals market positions in Brazil

47

Functional

Chemicals

Pulp

and Paper

Surface

Chemistry

3

1

4

AgriculturalHome &

Personal care

Sulfur derivatives

High polymers

1

Sizing

chemicals

Investor visit AkzoNobel Brazil

Bleaching

and retention

chemicals

12

2

Business approaches

Pulp and Paper Chemicals

• Strategy: Grow through innovation and

unique know-how using “Chemical Islands”

and energy from customers

Surface Chemistry

• Strategy: We will deliver sustainable surface

chemistry solutions to achieve profitable

growth

Functional Chemicals

• Strategy: Grow in existing markets as well as

other Functional Chemicals products

(Bermocoll, Cellulosic's, Elotex)

Investor visit AkzoNobel Brazil 48

Investor visit AkzoNobel Brazil 49

Pulp and Paper Chemicals

Agenda

• Pulp and Paper

industry

• Eka Chemicals

• Chemicals Island

• Future Ahead

Investor visit AkzoNobel Brazil 50

Brazilian Pulp and Paper Industry

• 4th largest pulp producer in the world and with

potential to be the 2nd by 2020, from 13 mtpy to 30 mtpy,

below USA and above China and Canada.

• 9th largest paper producer

• Exports 60% of the pulp and 20% of tpaper production

• Majority of the companies are Brazilian companies

Investor visit AkzoNobel Brazil 51

Brazilian Pulp Industry

• Modern mills, 1,5 Mtpy capacity

• 100% planted forests, 70 - 80% certified (FSC, Cerflor)

• Concentrated market, around 15 companies

• Sustainable industry

Investor visit AkzoNobel Brazil 52

Brazilian Pulp Industry continuation

• Self sufficient and exporter of green energy

• For each 1 ton of CO2 produced, 3 tons are collected

• 40% of their properties (forests) are preserved, including

natural species plantation

• 70% of the forests are certified (FSC, Cerflor, etc)

• Fibria is the only company in the world forest sector

listed in the DJSI

Investor visit AkzoNobel Brazil 53

Brazilian Paper Industry

• Fragmented market, around 130 companies

• Low paper consumption per capita

SELECTED COUNTRIES

kg/inhab./year

341.7

265.9

247.4

241.5

208.8

190.8

184.9

167.6

79.5

59.6

59.5

44.6

Finland

USA

Germany

Japan

Canada

Italy

United Kingdom

France

Chile

Mexico

Argentina

Brazil

World Average

57.8 kg/inhab./year

Paper consumption per capita

Investor visit AkzoNobel Brazil 54

Competitiveness of Pulp IndustryEucaliptus productivity

Eucalyptus planted forests with high productivity and future potential

REASONS FOR HIGH PRODUCTIVITY LEVELS

Climate and Soil

Research

Organized private sector

High qualified labor force

TECHNOLOGICAL ADVANCES

Genetics

Biotechnology

High Quality raw material

Socio-envirnmental planning

Rotation

WOOD FOR PULP PRODUCTION

Productivity (m3/ha/year)

Species 1980 2008 Grow Rate Potential Grow Rate

Eucalyptus 24 41 71% 70 192%

Pine 19 36 89% 40 111%

Investor visit AkzoNobel Brazil 55

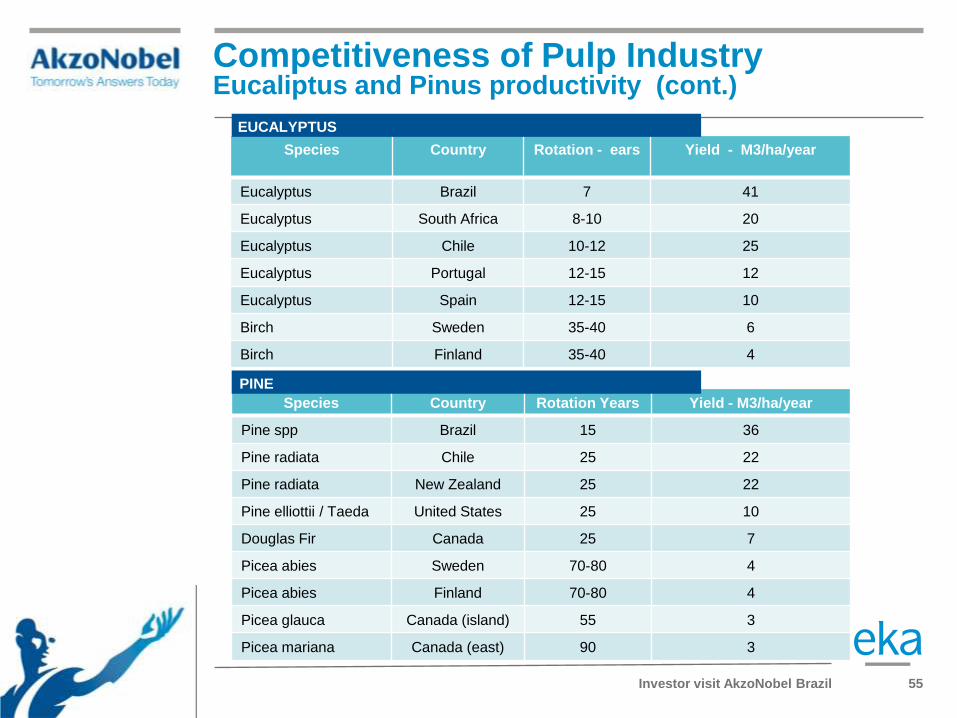

Competitiveness of Pulp Industry Eucaliptus and Pinus productivity (cont.)

PINUS

Species Country Rotation - ears Yield - M3/ha/year

Eucalyptus Brazil 7 41

Eucalyptus South Africa 8-10 20

Eucalyptus Chile 10-12 25

Eucalyptus Portugal 12-15 12

Eucalyptus Spain 12-15 10

Birch Sweden 35-40 6

Birch Finland 35-40 4

Species Country Rotation Years Yield - M3/ha/year

Pine spp Brazil 15 36

Pine radiata Chile 25 22

Pine radiata New Zealand 25 22

Pine elliottii / Taeda United States 25 10

Douglas Fir Canada 25 7

Picea abies Sweden 70-80 4

Picea abies Finland 70-80 4

Picea glauca Canada (island) 55 3

Picea mariana Canada (east) 90 3

EUCALYPTUS

PINE

Investor visit AkzoNobel Brazil 56

Competitiveness of Pulp Industry Land Availability

Forest Area (ha) Required for a1,000,000 tons/year Pulp Mill

2007 Million Hectares

%

Federal and State Conservation Areas 176 20.7

Grazing Areas (Comprising Pasture) 172 20.2

“Devolutionary” and other uses 171 20.1

Indigenous Areas 107 12.6

Rural Settlements 77 9.0

Unexplored Areas available for agriculture (not comprising Amazon forest)

71 8.3

Temporary Agriculture 55 6.5

Permanent Agriculture 17 2.0

Planted Forest 5 0.6

BRAZIL 851 100.0

Source: IBGE, MAPA, Conab, ABRAF, INCRA and MMA

57

Brazilian Pulp Market

19 YEARS WITHOUT LOSING ANY ClO2 PLANT COMPETITION

LAST DECADE (2001-2010)

1 VCP JACAREI New Line

2 ARACRUZ LINE C New Line

3 CENIBRA New Line

4 RIPASA New Line

5 VERACEL Green Field

6 BAHIA SUL New Line

7 KLABIN New Line

8 BAHIA PULP New Line

9 FIBRIA TRÊS LAGOAS Green Field

Around $20 billion invested

NEXT DECADE 2011- 2020

1 ELDORADO Green Field

2 SUZANO MA Green Field

3 CMPC GUAIBA New Line

4 FIBRIA TRES LAGOAS New Line

5 SUZANO PI Green Field

6 VERACEL New Line

7 KLABIN Green Field

8 CENIBRA New Line

9 ELDORADO New Line

Around $20 billion to be invested

Investor visit AkzoNobel Brazil

Investor visit AkzoNobel Brazil 58

AkzoNobel Pulp and Paper business unit

• Eka is the brand we use to go to market

•5 sites distributed in the Brazilian territory

•New site under construction

•Following the pace of the pulp industry

Investor visit AkzoNobel Brazil 59

AkzoNobel Pulp and Paper sites

Investor visit AkzoNobel Brazil 60

Chemical Island Concept

• Lay out flexibility

• Strong safety approach on chemicals, instead pulp

• Optimization of the transportation, labor etc

• Improvement of the synergies

Investor visit AkzoNobel Brazil 61

Chemical Island Concept continuation

• Reducing the duplicity in equipments

• Stronger relationship between supplier ans customer

• Higher commitment with the community

• Development of local infrastructure

• Delivering a chemical solution

3D Movie – Eldorado Pulp Mill

Investor visit AkzoNobel Brazil 62

Investor visit AkzoNobel Brazil 63

Eldorado Pulp Mill ProjectSite view

3D view of Eldorado Pulp Mill and Eka site

Investor visit AkzoNobel Brazil 64

Eka future 6th site in Brazil3D view - Tres Lagoas - Eldorado Cellulose

Investor visit AkzoNobel Brazil 65

ELDORADO Pulp MillActual site conditions

Investment of around €90 million

Construction to start June 2011

Operational from October 2012

66

Future Ahead 2010-2015Growth Drivers

2010

Chlorate market growth Increasing share in PCH

RevenueSales

2015

80%

2010

High Profitability in Chlorate Recovering profitability in PCH

EBITDA Sales

EBITDA

2015

160%

Investor visit AkzoNobel Brazil

Revenue

Investor visit AkzoNobel Brazil 67

Summary Brazilian Pulp and Paper business

• Fast growing industry

• Great underlying economics and competitive strength

for pulp industry in Brazil

• We will leverage our global scale combined with our

leadership in bleaching and chemical islands

• Ideal circumstances for further growth in Brazil in the

decade to come

Performance Coatings

in Brazil

Almir Gozzi

Managing Director Latin America

Automotive & Aerospace Coatings

Our Performance Coatings market positions in Brazil

69

Wood Finishes

and Adhesives

Powder

Coatings

Marine and

Protective

Coatings

Automotive &

Aerospace

Coatings

Industrial

Coatings

21

25

Vehicle Refinish

& Automotive

Plastic CoatingsOEM Comm.

Vehicles

ProtectiveMarine

1 Beer &

Beverage

Packaging

Food cans

Investor visit AkzoNobel Brazil

2

2

Powder

2Coil coatings

Specialty

Plastics

coatings

4

Wood

1

Aerospace

coatings

Business approaches

Marine & Protective Coatings

• Strategy: to continue strong No.1 position in Marine Coatings;

there is good opportunity for Protective Coatings in

Geographical and market segment expansion.

Wood Finishes & Adhesives

• Strategy: expanding into the Brazilian market and introducing

new technology.

Automotive & Aerospace Coatings

• Strategy: focus primarily on mid-market growth and leverage our

leading global technology and innovations in Brazil.

Powder Coatings

• Strategy: to maintain profitable growth ahead of the market by

leading the development of new market segments for Powder

Coatings; at the same time we compete with innovative

propositions in the traditional ones.

Industrial Coatings

• Strategy: to expand our leading position in the packaging

coatings end markets in Brazil.

Investor visit AkzoNobel Brazil 70

Investor visit AkzoNobel Brazil 71

Automotive and Aerospace Coatings in brief

• AkzoNobel A&AC is one of the world’s leading suppliers of paints

and services for vehicle repair, OEM commercial vehicles,

automotive plastics and aerospace coatings markets

• We provide coatings for original equipment and refinishing

applications to bodyshops, aircraft manufacturers, fleet owners,

automotive suppliers and major bus and truck producers

• Our portfolio includes strong brands such as: Sikkens®,

Lesonal®, Dynacoat®, Wanda®, Sikkens Autocoat® BT,

Aerowave®, Aerobase® and Aerodur®

• We are operating in more than 60 countries and offer

outstanding customer service, top-notch training, full technical

and logistical support, and detailed local knowledge.

Investor visit AkzoNobel Brazil 72

A&AC Business Segments

AkzoNobel A&AC

OEM Commercial Vehicles

Automotive Plastic Coatings

Aerospace CoatingsVehicle Refinish

Investor visit AkzoNobel Brazil 73

Worldwide Operations

% of 2010 global revenue (€994 million)

Americas

35%

Europe

50%

Asia Pacific

15%

Investor visit AkzoNobel Brazil 74

Some of the global customers we serve

Investor visit AkzoNobel Brazil 75

Color Excellence

Investor visit AkzoNobel Brazil 76

Global excellence in Color: Getting color right!

• Objective: the right colors, first time, every time, to help our

customers maximize their performance

• Our own color development centers and a globally accessible

color database provide a perfect color match for any customer

anywhere in the world

• Worldwide 38 training centers, 600 color courses are held each

year for approx 4000 students

• Large color offer (more than 800,000 color formulas) and high

consistency in quality and application

• More than 40,000 mixing machines installed

• Benchmark for the Automotive industry for color digitization

Investor visit AkzoNobel Brazil 77

Innovation

Investor visit AkzoNobel Brazil 78

Latest Innovations

• Mixit Pro: Sikkens online color formula retrieval software that is easy to use and offers different reporting functions and inventory management

• Stickerfix™: The smart do-it-yourself solution for minor paint damage. Easy to use, eco-friendly and color-matched to your car.

• Autoclear LV Exclusive: Self healing clearcoat that offers excellent scratch resistance and gloss retention by making minor scratches disappear when exposed to (sunlight) heat

• UV LED gun: Innovative spraying device that enables you to spray and cure Autoclear UV. It offers increased process efficiency, flexibility and energy savings

• Automatchic 3: Hand-held color checking device which allows you to measure the car’s exact color and find the right color formula in matter of seconds

• Next Generation Basecoat / Clearcoat system in Aerospace: reduced process cycle times, extended durability and excellent cleanability. The system provides significant savings to both paint shops and the life cycle of an aircraft.

StickerFix Video

Investor visit AkzoNobel Brazil 79

Investor visit AkzoNobel Brazil 80

How we are doing in BrazilHow we are doing in Brazil

Automotive & Aerospace Coatings

Our four key areas Our key stakeholders

OEMs, insurance companies,

fleets/lease companies, body shops,

vendors, suppliers, internal AN

customers

Employees

Global Community

AkzoNobel

81

Automotive & Aerospace Coatings

Market Size

2%

65%

18%

15%

AEROSPACE

VR

CV

APC

Euro 6 mln

Euro 196 mln

Euro 53 mln

Euro 45 mln

82

Total Market: Eur 300 mln

Investor visit AkzoNobel Brazil 83

Vehicle Refinish marketStrategy is oriented toward trade growth

Top

Segment

Middle Market

Low-end

Premium ~5% Typical focus for

AkzoNobel

(and other

multinationals)

Trade/Value ~65% Intense battle

between global multi-

nationals „moving

down‟and local

companies „moving

up‟

Low price ~30% Low cost local value

propositions, low end

technology

Investor visit AkzoNobel Brazil 8484

Opportunities and threats

Opportunities

• Car park increasing

• Distribution expansion

• Exploit advantages in colors

Threats

• Informal Market

• Ready mix increasing

• Price pressure

Investor visit AkzoNobel Brazil 86

Strategic Ambition

We will challenge for the number 1 position in the

vehicle refinishes market, strengthen our number 1

position in aerospace coatings and grow selectively in

the APC market

Decorative Paints

Jaap Kuiper, Managing Director Decorative Paints Latam

88

Decorative Paints

Agenda

•Mission

•Market Segments

•Channels

•Competitive Position

•Growth Evolution

•Future Ahead

Investor visit AkzoNobel Brazil

89

Markets

Investor visit AkzoNobel Brazil

90

Competitive Position

CR Brand 1

CR Company 0,77

Investor visit AkzoNobel Brazil

60% 25%

15%

Channels

60%25%

15%Paint Shops

Builder Merchants

Home Centres

Investor visit AkzoNobel Brazil 91

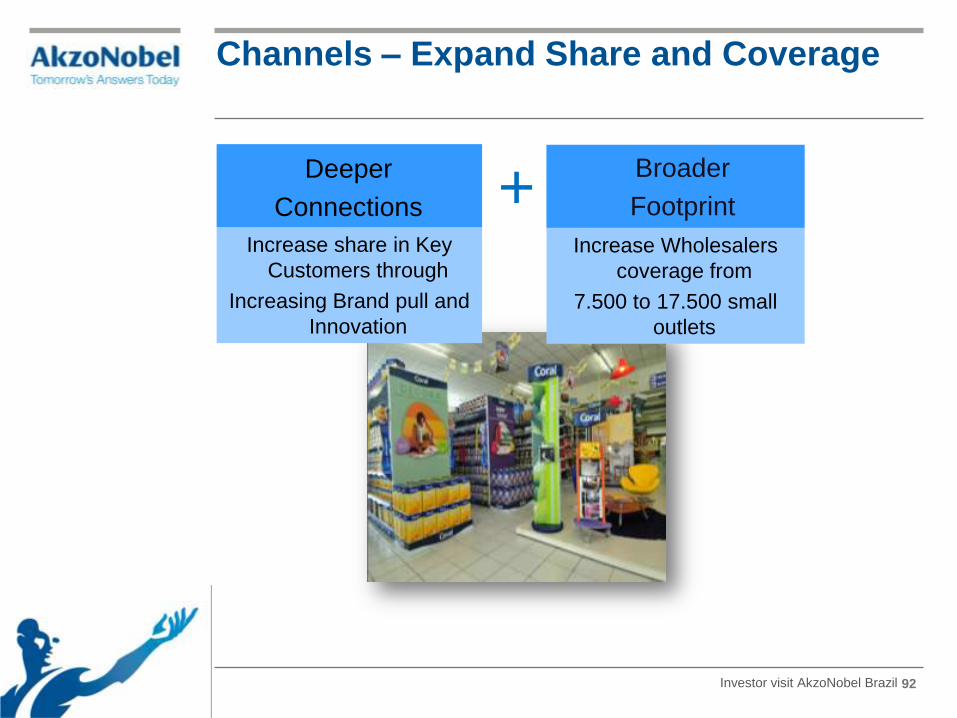

Channels – Expand Share and Coverage

Increase Wholesalers

coverage from

7.500 to 17.500 small

outlets

Increase share in Key

Customers through

Increasing Brand pull and

Innovation

+Deeper

Connections

Broader

Footprint

Investor visit AkzoNobel Brazil 92

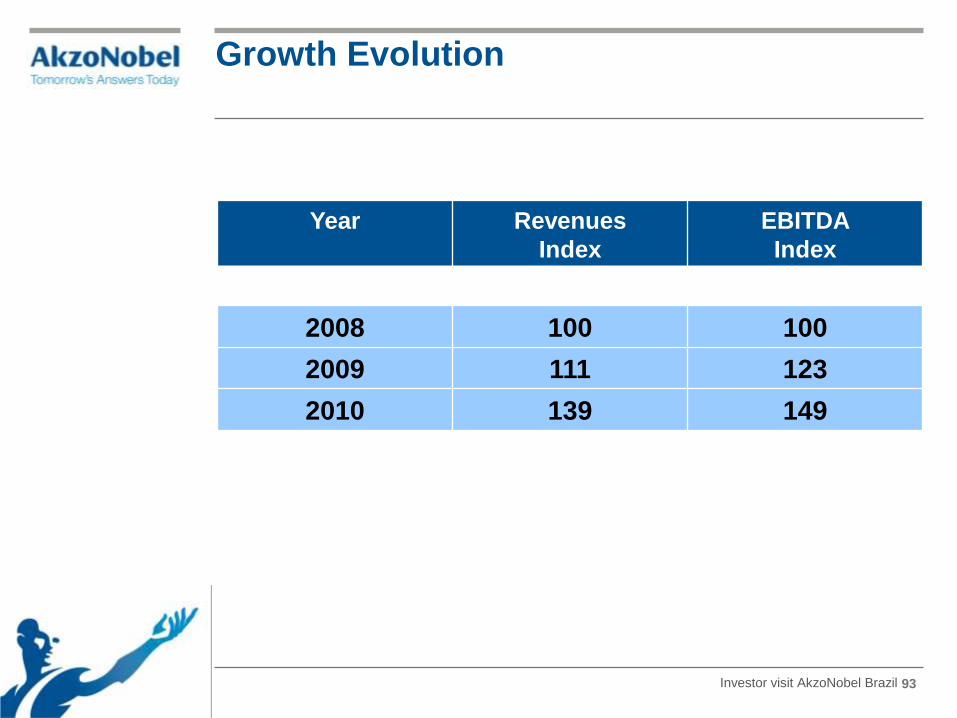

Growth Evolution

Year RevenuesGrowth vs

previousEBITDA

Grow th vs

previousEBITDA %

Year Revenues

Index

EBITDA

Index

2008 100 100

2009 111 123

2010 139 149

Investor visit AkzoNobel Brazil 93

Growth Projection until 2015

Decorative Paints Business - MMEU

Year RevenuesGrowth vs

previousEBITDA

Grow th vs

previousEBITDA %

Revenues EBITDA

Growth 10 - 15 121% 151%

Investor visit AkzoNobel Brazil 94

Revenue Growth Drivers 2010-2015Indexed

100

221

55

22

22

22

Market

Growth

Market Share

Gain

Innovation

Construction

Investor visit AkzoNobel Brazil 95

2008 Acquisition of Coral

96Investor visit AkzoNobel Brazil

97

Decorative Paints Mission

Adding Colour to

People´s Lives

Investor visit AkzoNobel Brazil

2009 New Brand logo and tag line

98Investor visit AkzoNobel Brazil

The Blue Village - Chaouen (Morocco)

99Investor visit AkzoNobel Brazil

Taking our mission off the wall…

100Investor visit AkzoNobel Brazil

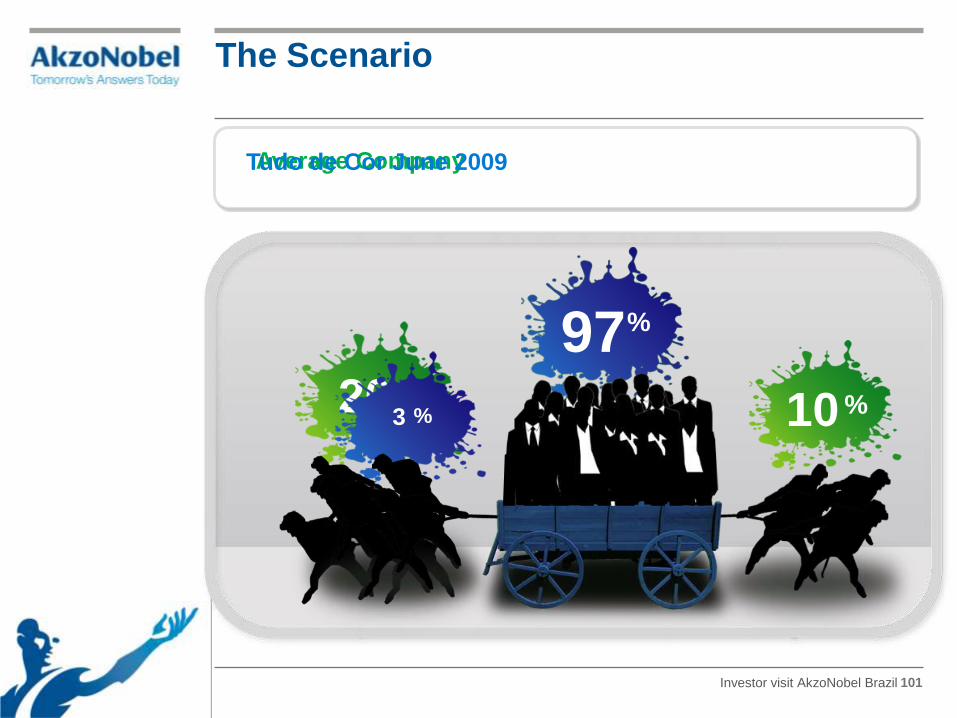

The Scenario

20%3 %

70%97%

Average Company

10%

Tudo de Cor June 2009

101Investor visit AkzoNobel Brazil

Mr. Walter

102Investor visit AkzoNobel Brazil

Bixiga neigbourhood São PauloAugust 2009

103Investor visit AkzoNobel Brazil

Bixiga neigbourhood São PauloAchievements

São Paulo Major

104Investor visit AkzoNobel Brazil

What “Tudo de Cor” is about?

105Investor visit AkzoNobel Brazil

•Visibility

•Relevant for the community•Architectonic/Historic Value

106Investor visit AkzoNobel Brazil

• Community inputs

• Traditions• Local authorities

107Investor visit AkzoNobel Brazil

• Locals apprentices training

• Employees and customers volunteer• TV commercial recording

108Investor visit AkzoNobel Brazil

• Big party to celebrate

• Formal protocol with authorities• Apprentices graduation

109Investor visit AkzoNobel Brazil

Where we've been?

Bixiga-SP - Ago/09 Salvador-BA -Jan/10

Sta. Marta-RJ -Abr/10

Ouro Preto-MG -Out/10

Fundição ProgressoRJ - Nov/09

Olinda-PE - Mar/10 Porto Alegre-RS -Ago/10

Porto Seguro – BA Fev/11

110Investor visit AkzoNobel Brazil

Pillars

The Results

Equity

Building/

Sales Boost

Employee

Engagement

Sustainability

111Investor visit AkzoNobel Brazil

112Investor visit AkzoNobel Brazil

Brand EquityPre test

Recall Index

Persuasion Index

138.0

187.0

93.0

66.0

Tudo de

Cor Film

Paint Market

Average

No

rma

tive

Ran

ge

Copy Effectiveness Index Pre-Test

113Investor visit AkzoNobel Brazil

Sales Boost

2008 2009 2010

20,9%

23,3%

24%

Market ShareTotal

114Investor visit AkzoNobel Brazil

Employee Engagement

115Investor visit AkzoNobel Brazil

1%97%

Employee Engagement

3 %

June 2009

116Investor visit AkzoNobel Brazil

99 % 1%

Today

Employee Engagement

117Investor visit AkzoNobel Brazil

Community Sustainability

118Investor visit AkzoNobel Brazil

Community Sustainability

119Investor visit AkzoNobel Brazil

Edimar

120Investor visit AkzoNobel Brazil

Let's Color Film Wins TED Award

“Color has the power to inspire all of us and I’m delighted that

the positive impact we are having on markets and communities

around the world has been so strongly communicated through

this commercial.”

Tex Gunning (CEO AkzoNobel for Decorative Paints.)

122Investor visit AkzoNobel Brazil

Tudo de Cor for Santa Marta

123Investor visit AkzoNobel Brazil

Tudo de Cor for Santa Marta

Santa Marta Community

6 thousand residents

1500 houses

4

7

124Investor visit AkzoNobel Brazil

www.coral.com.br

www.tudodecorparavoce.com.br

www.twitter.com/TintasCoral

www.youtube.com/TintasCoral

www.facebook.com/TintasCoral

www.flickr.com/photos/coral-brasil/

Questions

125Investor visit AkzoNobel Brazil

Thank you

Safe Harbor Statement

Investor visit AkzoNobel Brazil 127

This presentation contains statements which address such key issues as

AkzoNobel’s growth strategy, future financial results, market positions, product

development, products in the pipeline, and product approvals. Such statements

should be carefully considered, and it should be understood that many factors could

cause forecasted and actual results to differ from these statements. These factors

include, but are not limited to, price fluctuations, currency fluctuations, developments

in raw material and personnel costs, pensions, physical and environmental risks, legal

issues, and legislative, fiscal, and other regulatory measures. Stated competitive

positions are based on management estimates supported by information provided by

specialized external agencies. For a more comprehensive discussion of the risk

factors affecting our business please see our latest Annual Report, a copy of which

can be found on the company’s corporate website www.akzonobel.com.