Embed Size (px)

Citation preview

Rich Blackman, Vice President, State Street Securities Finance Mary Ellen Mullen, CFA, Principal, Bridgebay Consulting, LLC

Maximizing Portfolio Returns Through Securities Lending

26

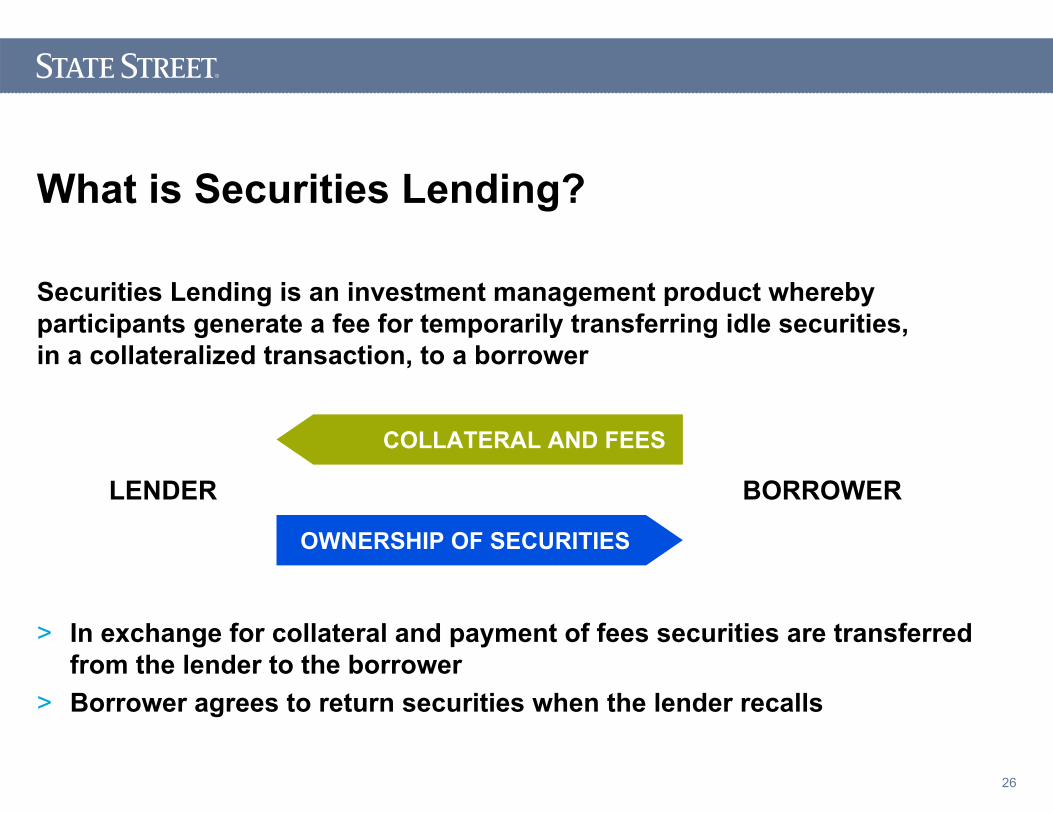

What is Securities Lending?

> In exchange for collateral and payment of fees securities are transferred from the lender to the borrower

> Borrower agrees to return securities when the lender recalls

Securities Lending is an investment management product wherebyparticipants generate a fee for temporarily transferring idle securities,in a collateralized transaction, to a borrower

LENDER BORROWER

OWNERSHIP OF SECURITIES

COLLATERAL AND FEES

27

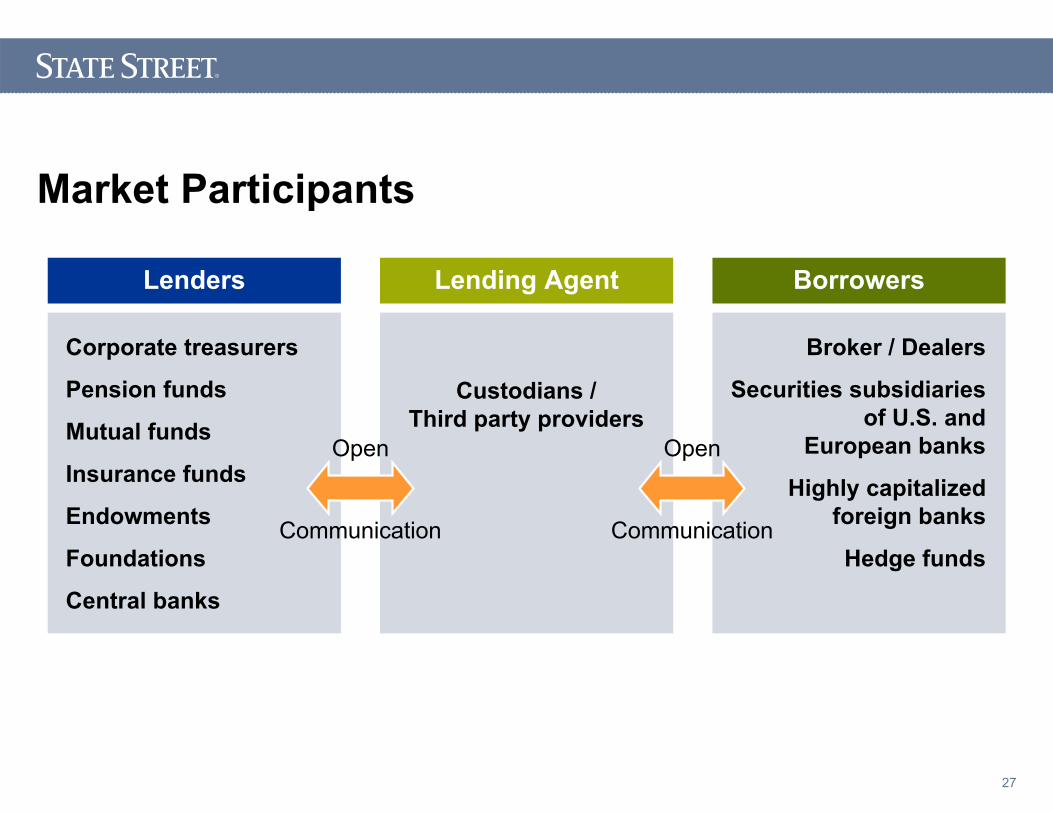

Lenders Lending Agent

Custodians /Third party providers

Borrowers

Broker / Dealers

Securities subsidiariesof U.S. and

European banks

Highly capitalizedforeign banks

Hedge funds

Market Participants

Open

Communication

Open

Communication

Corporate treasurers

Pension funds

Mutual funds

Insurance funds

Endowments

Foundations

Central banks

28

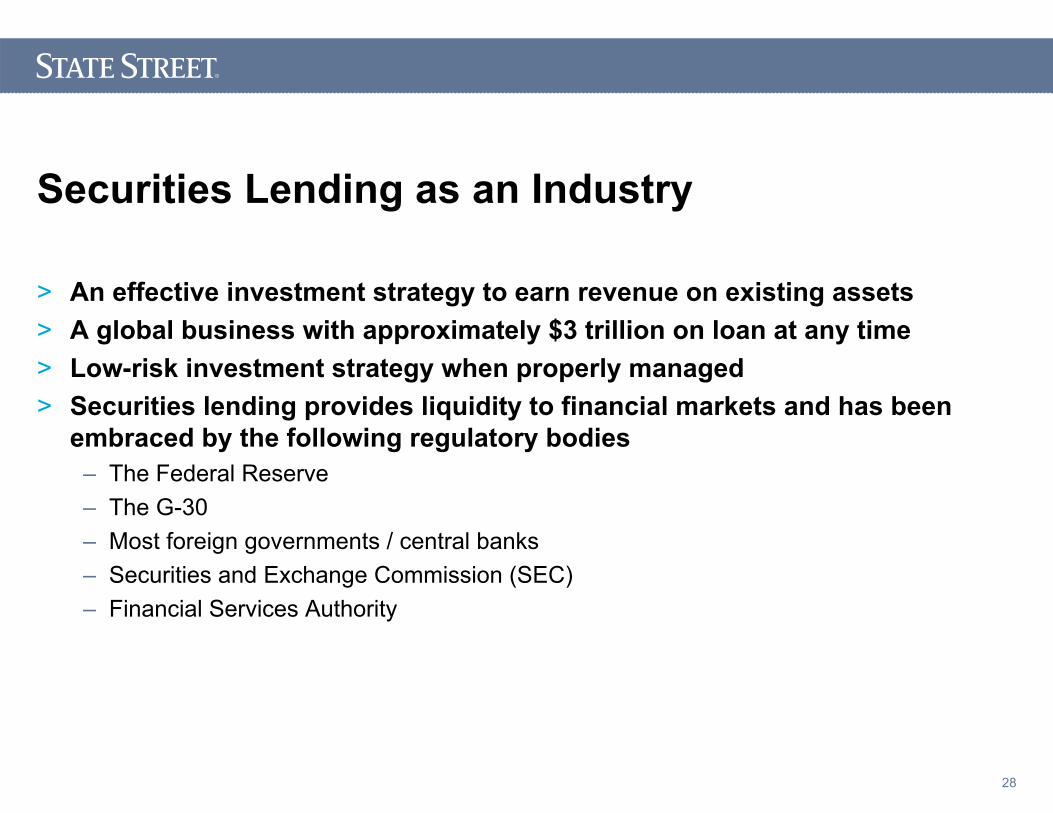

Securities Lending as an Industry

> An effective investment strategy to earn revenue on existing assets> A global business with approximately $3 trillion on loan at any time> Low-risk investment strategy when properly managed> Securities lending provides liquidity to financial markets and has been

embraced by the following regulatory bodies– The Federal Reserve– The G-30– Most foreign governments / central banks– Securities and Exchange Commission (SEC)– Financial Services Authority

29

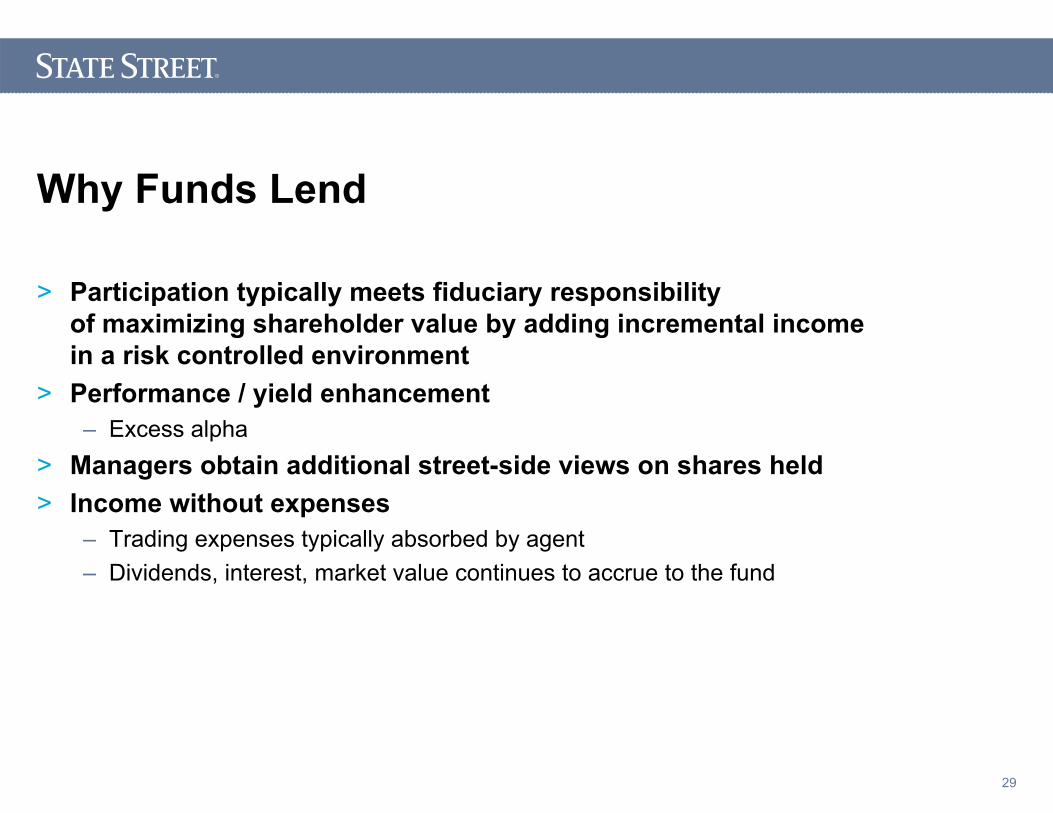

Why Funds Lend

> Participation typically meets fiduciary responsibilityof maximizing shareholder value by adding incremental incomein a risk controlled environment

> Performance / yield enhancement– Excess alpha

> Managers obtain additional street-side views on shares held> Income without expenses

– Trading expenses typically absorbed by agent– Dividends, interest, market value continues to accrue to the fund

30

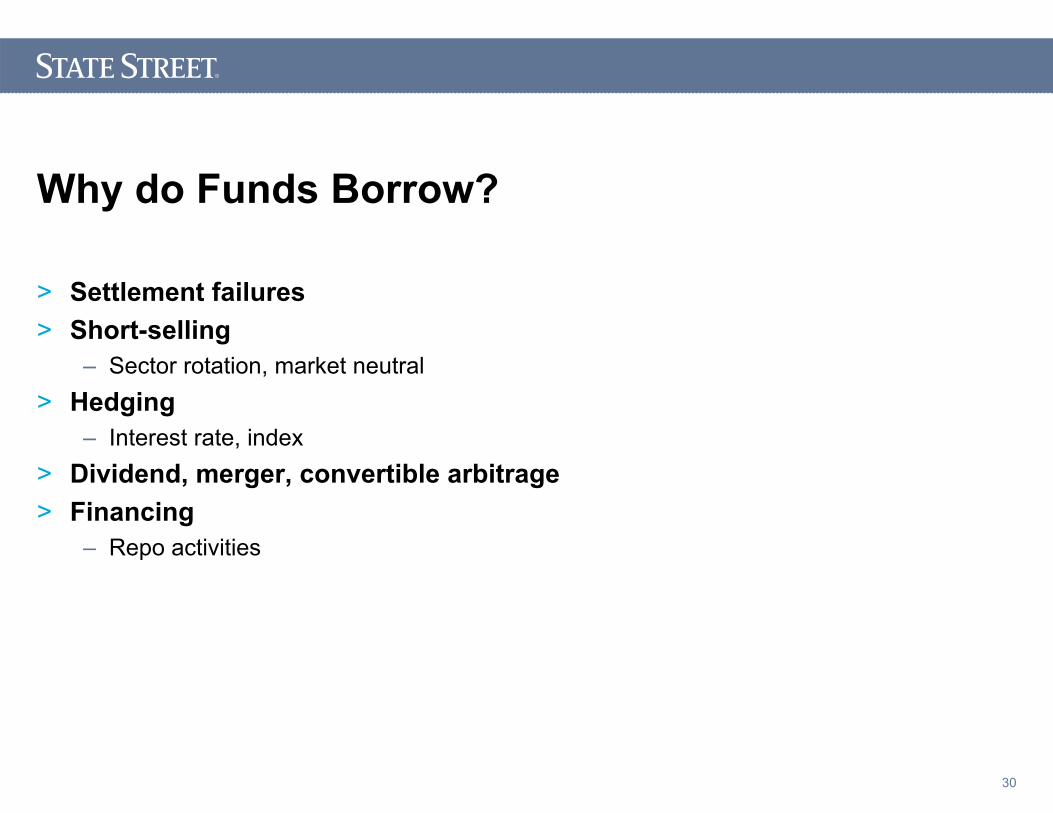

Why do Funds Borrow?

> Settlement failures> Short-selling

– Sector rotation, market neutral> Hedging

– Interest rate, index> Dividend, merger, convertible arbitrage> Financing

– Repo activities

31

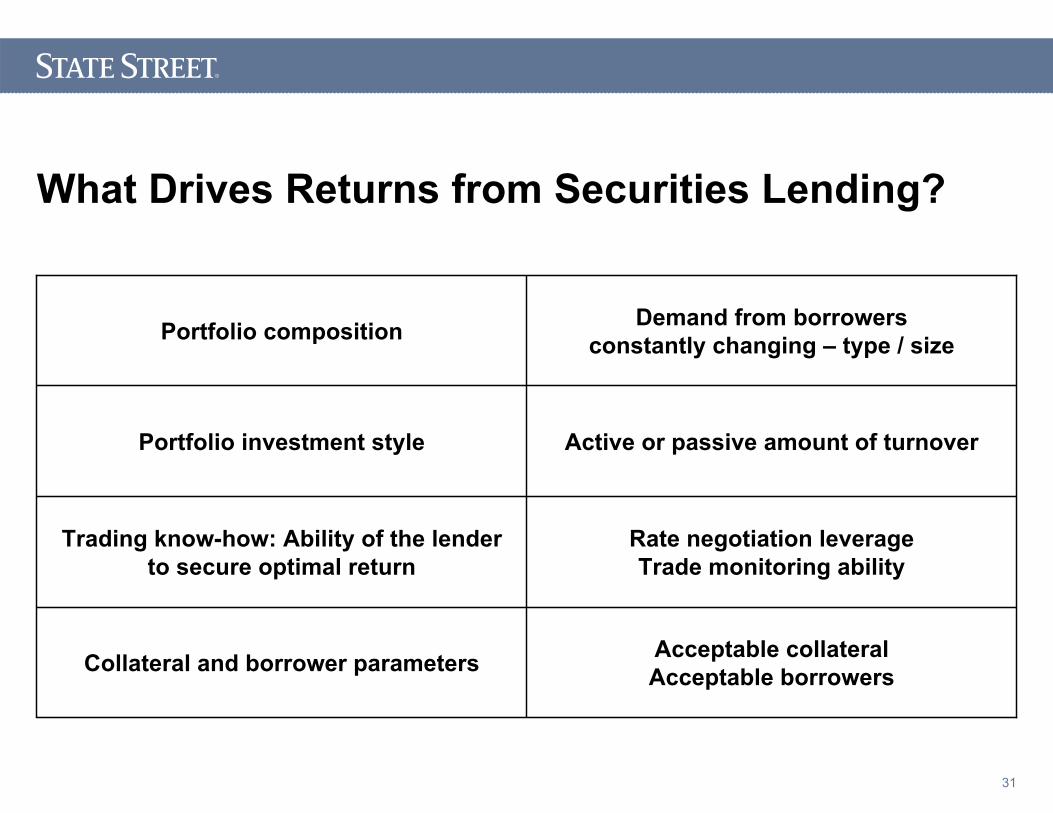

Acceptable collateralAcceptable borrowersCollateral and borrower parameters

Rate negotiation leverageTrade monitoring ability

Trading know-how: Ability of the lenderto secure optimal return

Active or passive amount of turnoverPortfolio investment style

Demand from borrowersconstantly changing – type / sizePortfolio composition

What Drives Returns from Securities Lending?

32

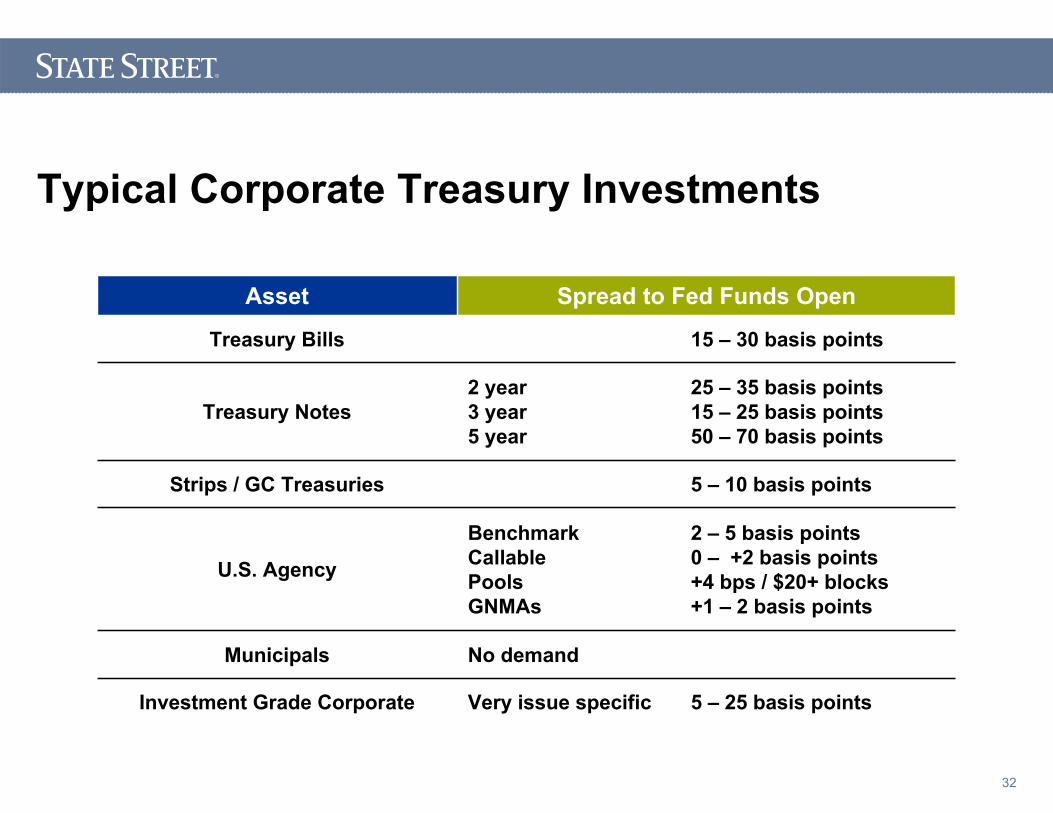

Typical Corporate Treasury Investments

5 – 10 basis points

15 – 30 basis points

5 – 25 basis points

2 – 5 basis points0 – +2 basis points+4 bps / $20+ blocks+1 – 2 basis points

25 – 35 basis points15 – 25 basis points50 – 70 basis points

Strips / GC Treasuries

BenchmarkCallablePoolsGNMAs

U.S. Agency

No demandMunicipals

Very issue specificInvestment Grade Corporate

2 year3 year5 year

Treasury Notes

Treasury Bills

Spread to Fed Funds OpenAsset

33

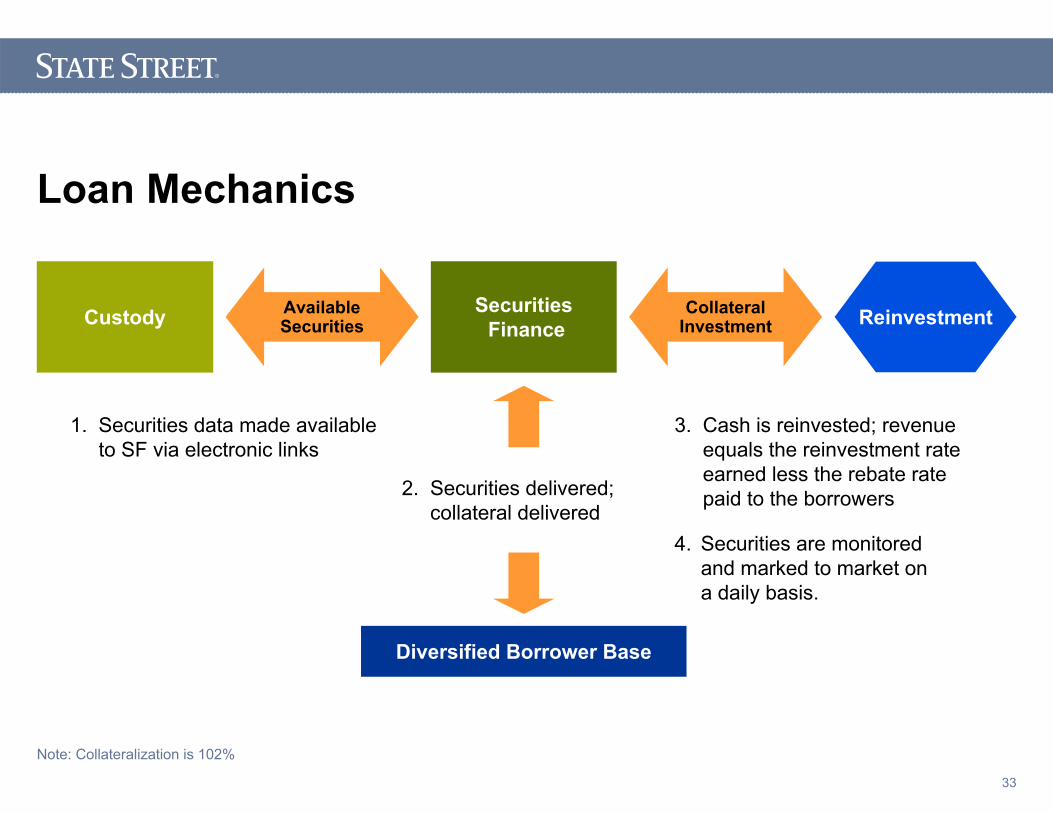

Loan Mechanics

Reinvestment

2. Securities delivered;collateral delivered

AvailableSecurities

1. Securities data made availableto SF via electronic links

3. Cash is reinvested; revenueequals the reinvestment rateearned less the rebate rate paid to the borrowers

Note: Collateralization is 102%

Custody CollateralInvestment

SecuritiesFinance

Diversified Borrower Base

4. Securities are monitored and marked to market on a daily basis.

34

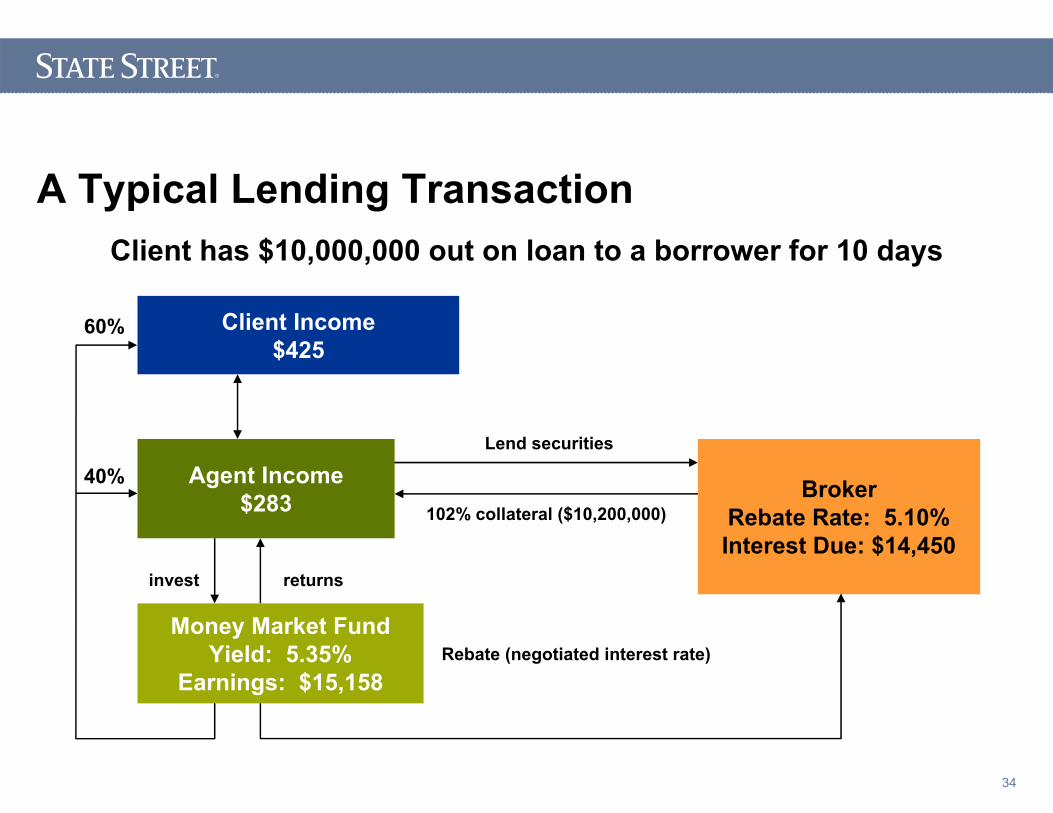

A Typical Lending TransactionClient has $10,000,000 out on loan to a borrower for 10 days

40%

Client Income$425

Agent Income$283 Broker

Rebate Rate: 5.10%Interest Due: $14,450

Rebate (negotiated interest rate)

invest returns

60%

Money Market FundYield: 5.35%

Earnings: $15,158

Lend securities

102% collateral ($10,200,000)

35

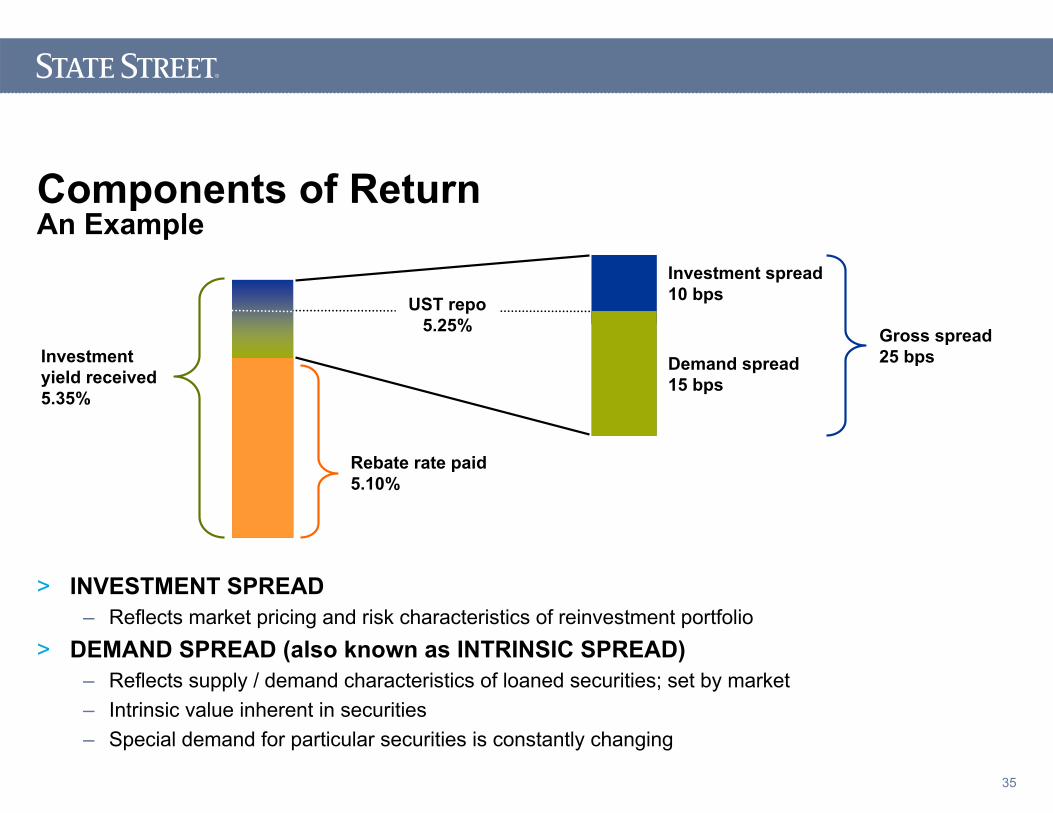

Components of ReturnAn Example

> INVESTMENT SPREAD – Reflects market pricing and risk characteristics of reinvestment portfolio

> DEMAND SPREAD (also known as INTRINSIC SPREAD) – Reflects supply / demand characteristics of loaned securities; set by market– Intrinsic value inherent in securities– Special demand for particular securities is constantly changing

Rebate rate paid 5.10%

Investment spread10 bps

Demand spread15 bps

Gross spread25 bps

UST repo5.25%

Investmentyield received5.35%

36

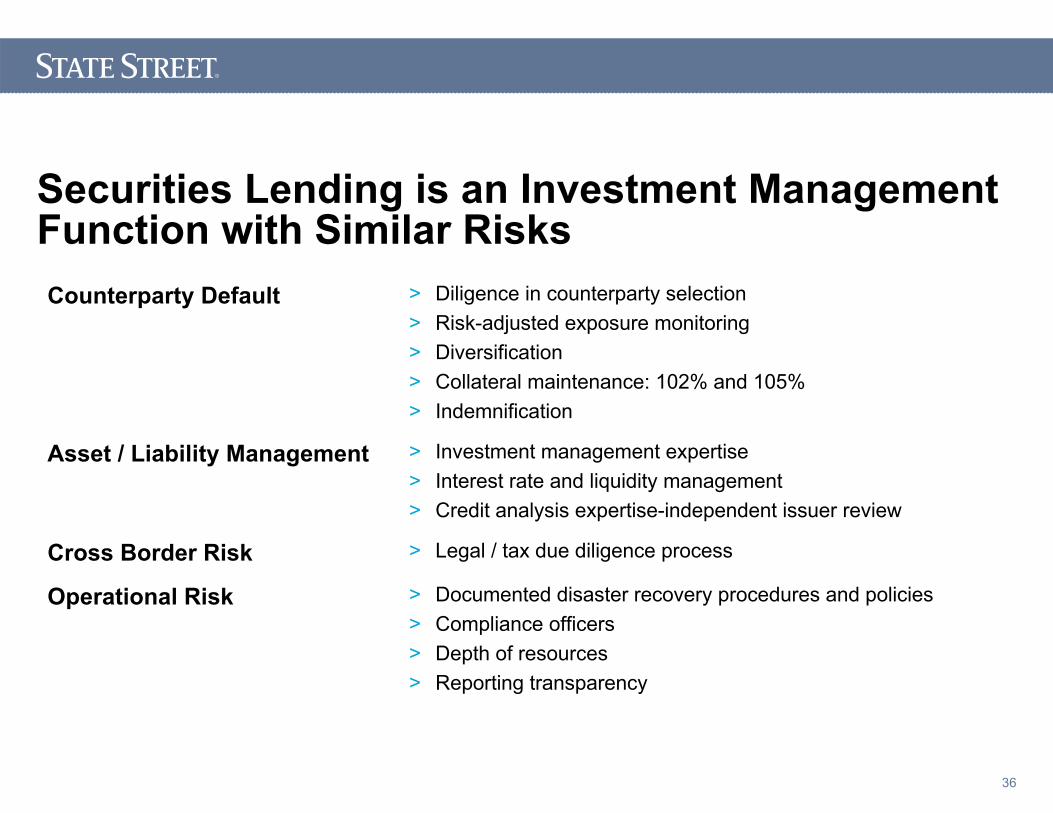

Securities Lending is an Investment Management Function with Similar Risks

> Documented disaster recovery procedures and policies> Compliance officers> Depth of resources> Reporting transparency

Operational Risk

> Legal / tax due diligence processCross Border Risk

> Investment management expertise> Interest rate and liquidity management> Credit analysis expertise-independent issuer review

Asset / Liability Management

> Diligence in counterparty selection> Risk-adjusted exposure monitoring> Diversification> Collateral maintenance: 102% and 105%> Indemnification

Counterparty Default

37

Items to Consider in Selectinga Securities Lending Partner> Look for partner who will optimize risk-adjusted performance, not just $

– This is an investment activity and should be reviewed as such> Look to leverage your entire portfolio

– Maximize intrinsic value vs. volume of loans– Reduce volatility of earnings

> Manage program through diligence and transparency– Risk management should be integral part of any program– This should not be a black box activity – these are your assets

> Partner with you to meet goals

38

Our Securities Finance Division

> Leading provider of securities finance services, includingsecurities lending

– The largest securities lending agent in the world– $2.6 trillion in lendable assets– $500+ billion assets on-loan

– Providing securities lending for 32 years– Experience in all market environments

> Global Collateral Management is one of the largest short-term cash managers in the world – over $500 billion

> 300+ employees worldwide – fully integrated business line– Trading, market / credit risk management, tax, operations, client service, reinvestment

> 450+ clients worldwide from 35+ countries, 60+ asset managers> Lending in over 30 markets

39

Reporting CapabilitiesIndustry Leading, Next Generation Online Reporting and Risk Measurement Tools

> SL PerformanceReporter® – accessible online. Sample reports include– Daily loan activities report, daily earnings report, monthly earnings statement, monthly

income attribution analysis, monthly market commentary> SL PerformanceAnalyzer® – risk-adjusted performance measurement tool

is designed to quantify, manage and communicate the risk / return relationship in securities lending programs. It provides clients with arisk-adjusted context in which to effectively evaluate their securities lending program.

> PerformanceExplorer® – securities lending performance measurement tool with the ability to evaluate lending returns against a broad universe of industry peers

40

Corporate Cash Considerations

> SFAS-140 requires disclosure on the balance sheet of lending transactions – cash only

> Determine impact, if any, of gross up with tax, analysts> Options

– Maximize earnings opportunity by keeping loans outstanding across quarter ends– Reduce cash loans to $0 and convert non-cash loans where possible– Reduce all loans to $0 for quarter end

41

FASB-140

> FASB Statement No. 140 (Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities) provides accounting and reporting guidance for transfers of financial assets, including accounting for securities lending activities

> FASB Statement No. 140 addresses– Whether the transaction is a sale of the loaned securities for financial

reporting purposes – If the transaction is not a sale, how the lender should report the loaned securities – Whether and how the lender should report the collateral – How the lender should record income earned as a result of securities

lending transactions

42

SFAS-140

> If the securities lending transaction includes an agreement that entitles and obligates the client to repurchase the transferred securities under which the company maintains effective control over those securities, then the client must account for those transactions as secured borrowings (not sales) and continue to report the securities on the statement of net assets. The client should record the cash collateral received as an asset — along with the obligation to return the cashas a liability.

> Generally, if the client receives securities (instead of cash) that may be sold or repledged, the client accounts for those securities in the same way as it would account for cash received. In this case the lender has no right to the collateral unless there is a default, so no accounting of the non-cash collateral is required.

> Reporting– “Cash” collateral received reported as an asset– Obligation to return cash collateral reported as a liability– MV of loans outstanding reclassified under cash and marketable securities– Income typically recorded under “other interest income”

43

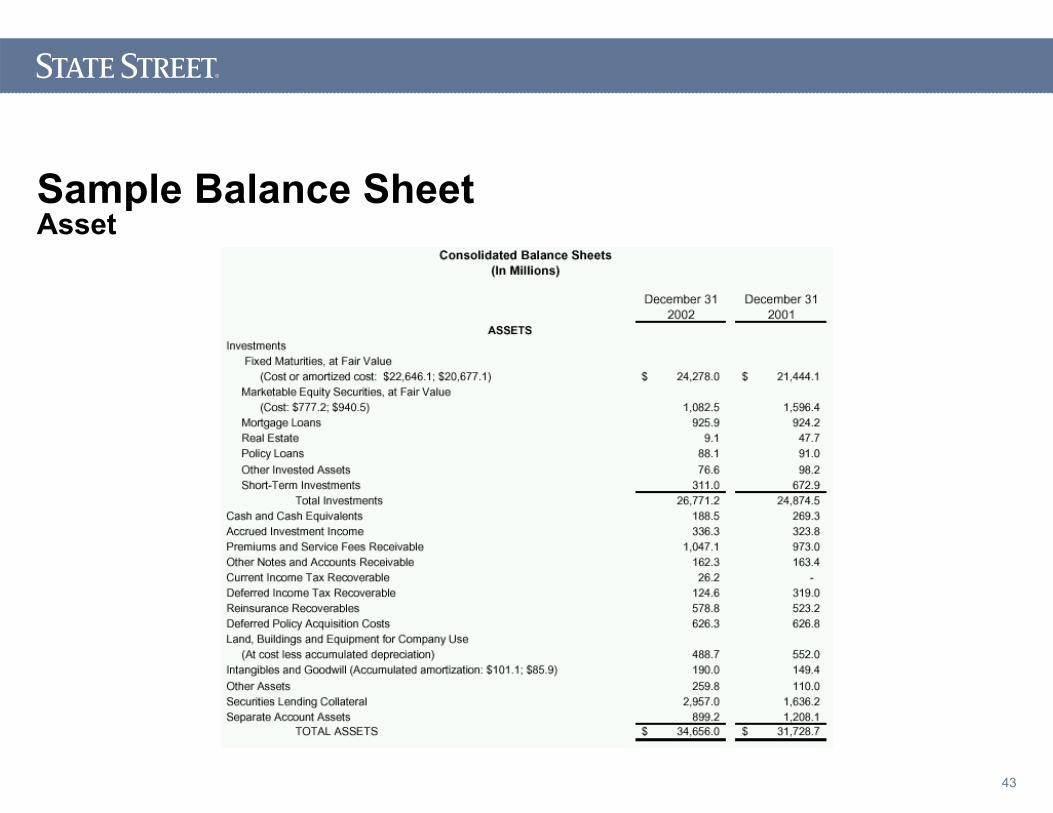

Sample Balance SheetAsset

44

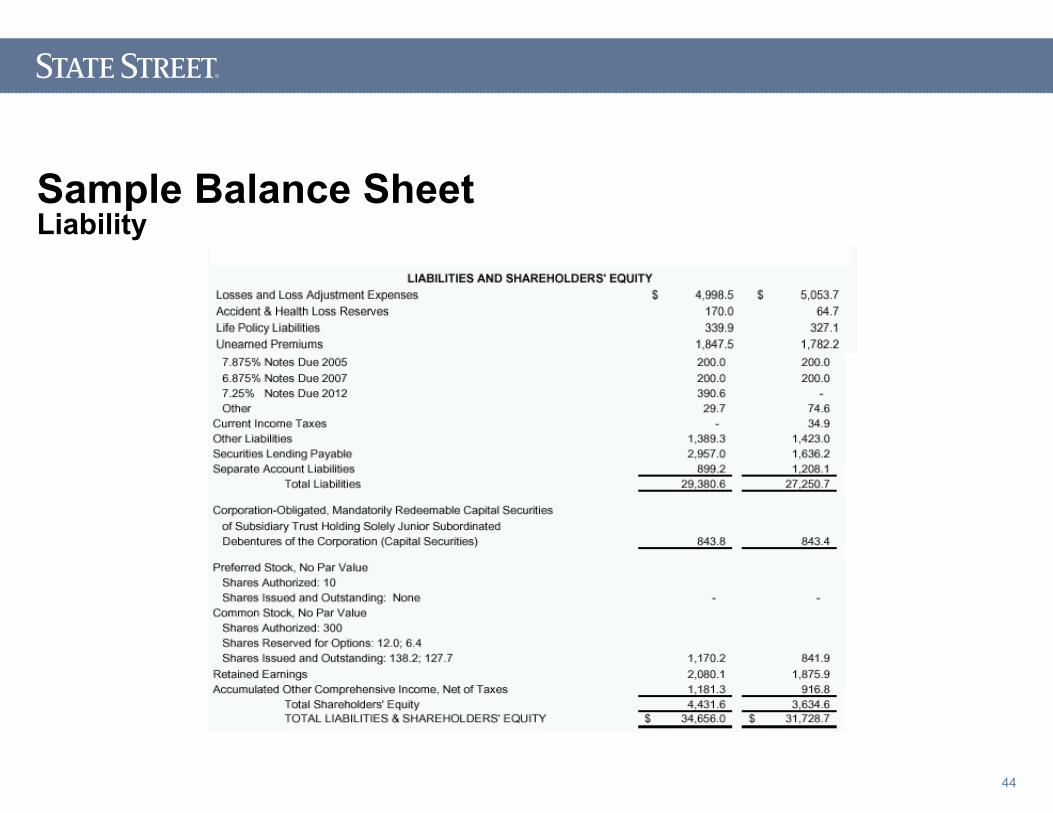

Sample Balance SheetLiability

45

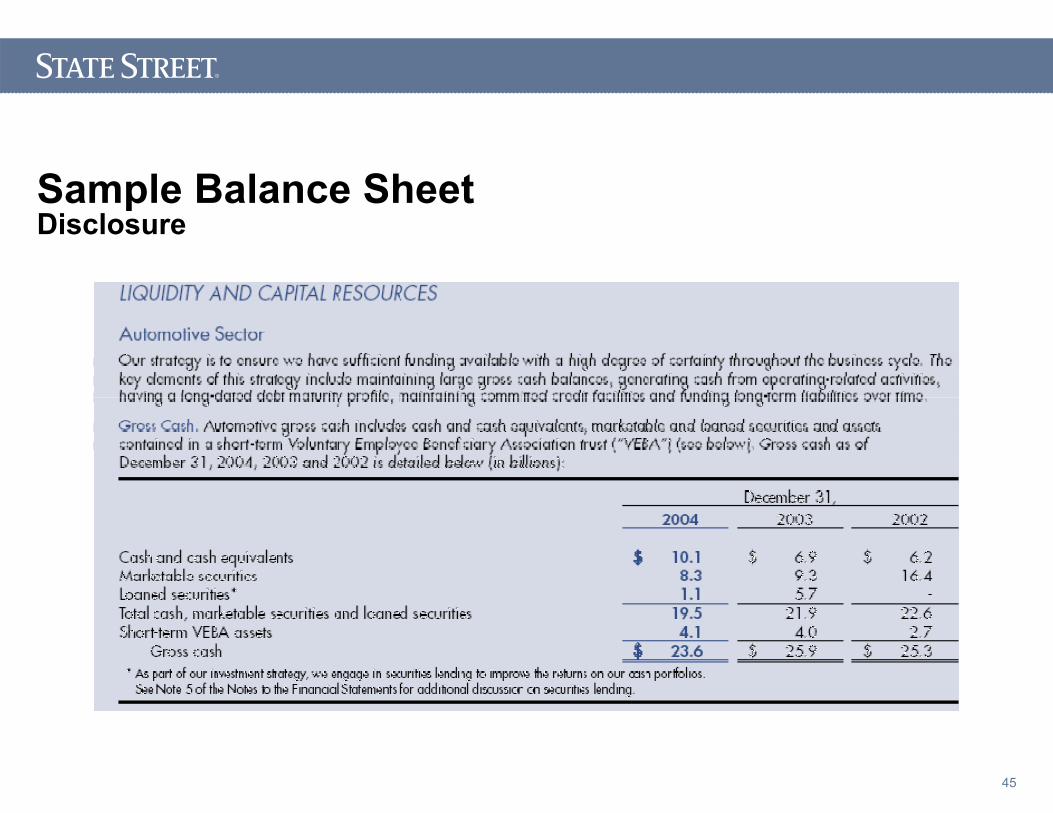

Sample Balance SheetDisclosure

46

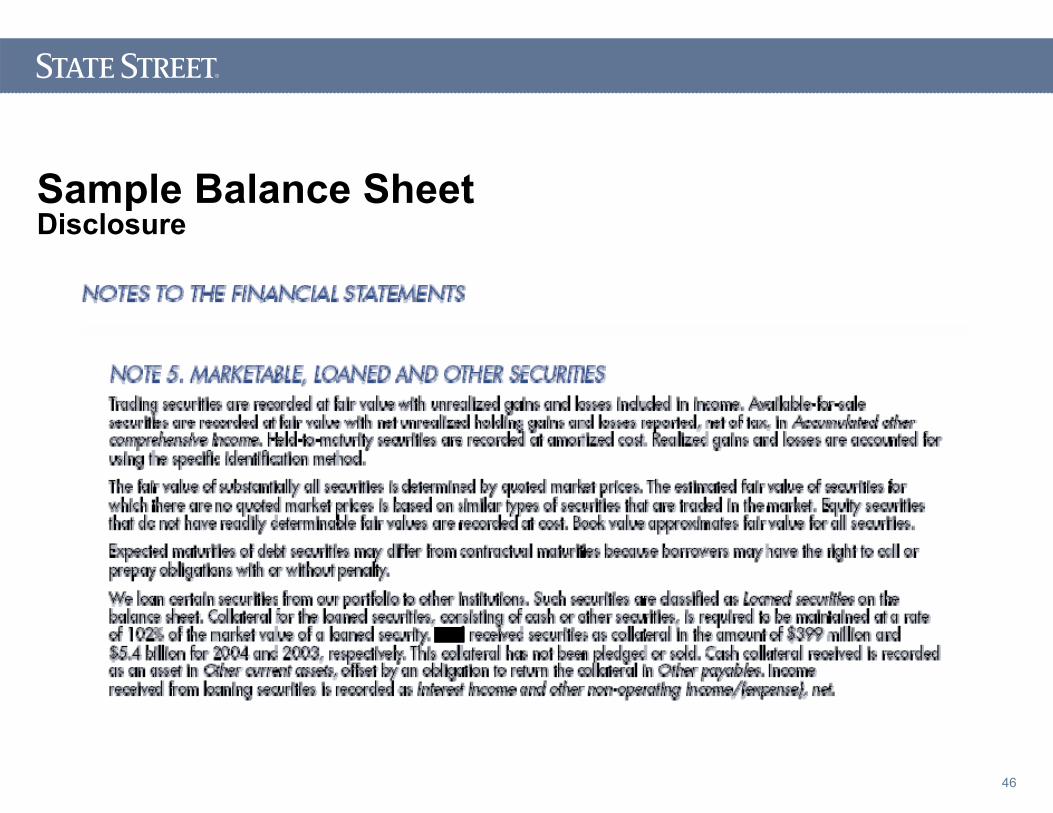

Sample Balance SheetDisclosure

Best Practices forSecurities Lending

Mary Ellen Mullen, CFAPrincipal

Bridgebay Consulting, LLC425-747-1924

Copyright © 2001-2006 by Bridgebay Financial, Inc. All rights reserved.48

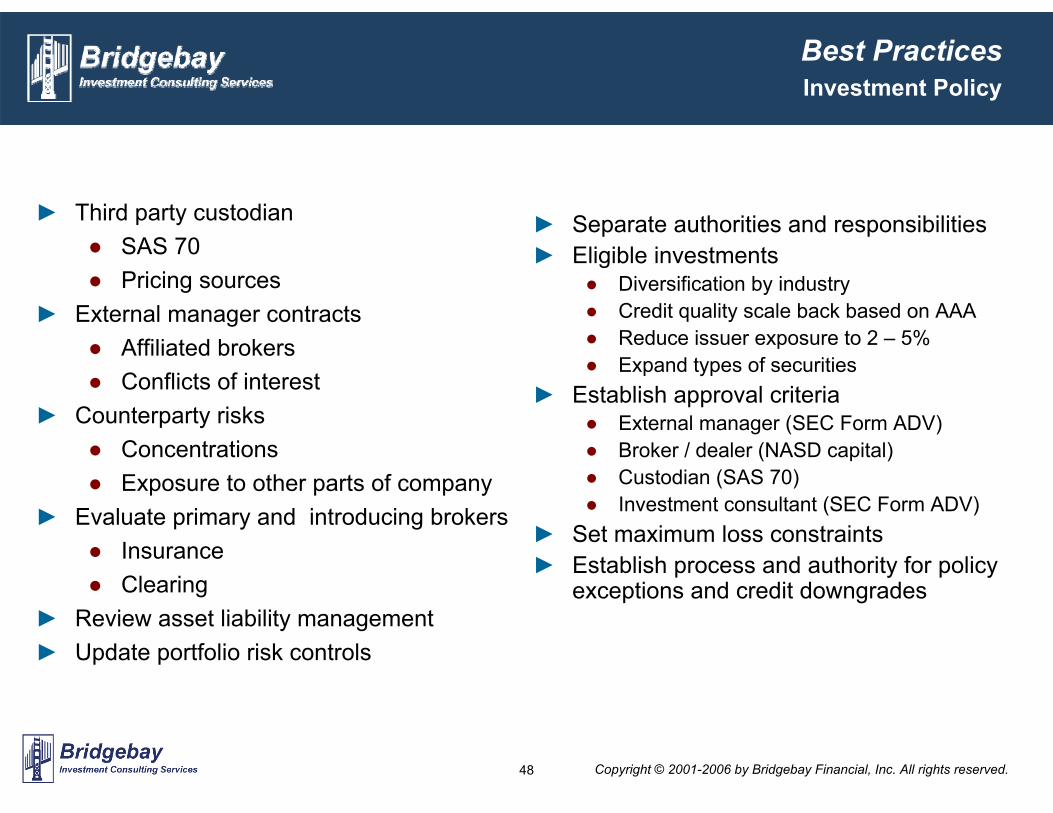

► Separate authorities and responsibilities ► Eligible investments

● Diversification by industry● Credit quality scale back based on AAA● Reduce issuer exposure to 2 – 5%● Expand types of securities

► Establish approval criteria● External manager (SEC Form ADV)● Broker / dealer (NASD capital)● Custodian (SAS 70)● Investment consultant (SEC Form ADV)

► Set maximum loss constraints► Establish process and authority for policy

exceptions and credit downgrades

Best PracticesInvestment Policy

► Third party custodian● SAS 70● Pricing sources

► External manager contracts ● Affiliated brokers● Conflicts of interest

► Counterparty risks● Concentrations● Exposure to other parts of company

► Evaluate primary and introducing brokers● Insurance ● Clearing

► Review asset liability management► Update portfolio risk controls

Copyright © 2001-2006 by Bridgebay Financial, Inc. All rights reserved.49

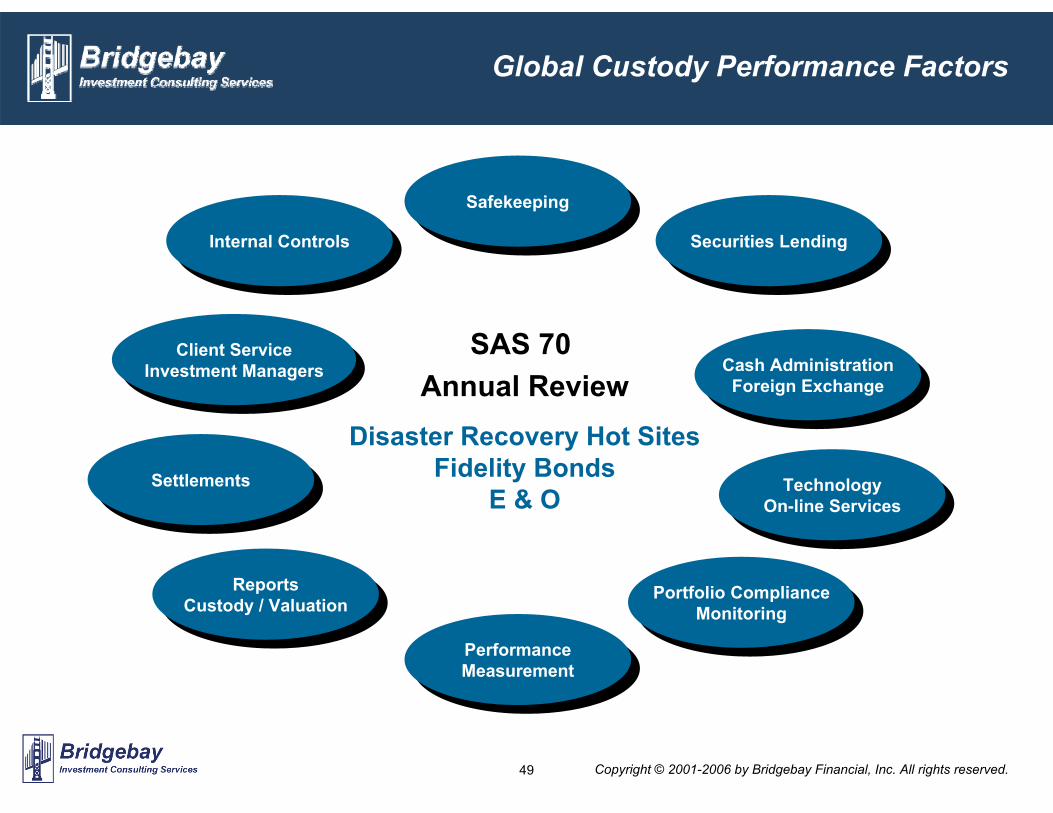

Global Custody Performance Factors

Internal ControlsInternal Controls

Client ServiceInvestment Managers

Client ServiceInvestment Managers

SettlementsSettlements

ReportsCustody / Valuation

ReportsCustody / Valuation Portfolio Compliance

MonitoringPortfolio Compliance

Monitoring

TechnologyOn-line Services

TechnologyOn-line Services

Cash AdministrationForeign Exchange

Cash AdministrationForeign Exchange

Securities LendingSecurities Lending

PerformanceMeasurement

PerformanceMeasurement

SafekeepingSafekeeping

SAS 70 Annual Review

Disaster Recovery Hot SitesFidelity Bonds

E & O

Copyright © 2001-2006 by Bridgebay Financial, Inc. All rights reserved.50

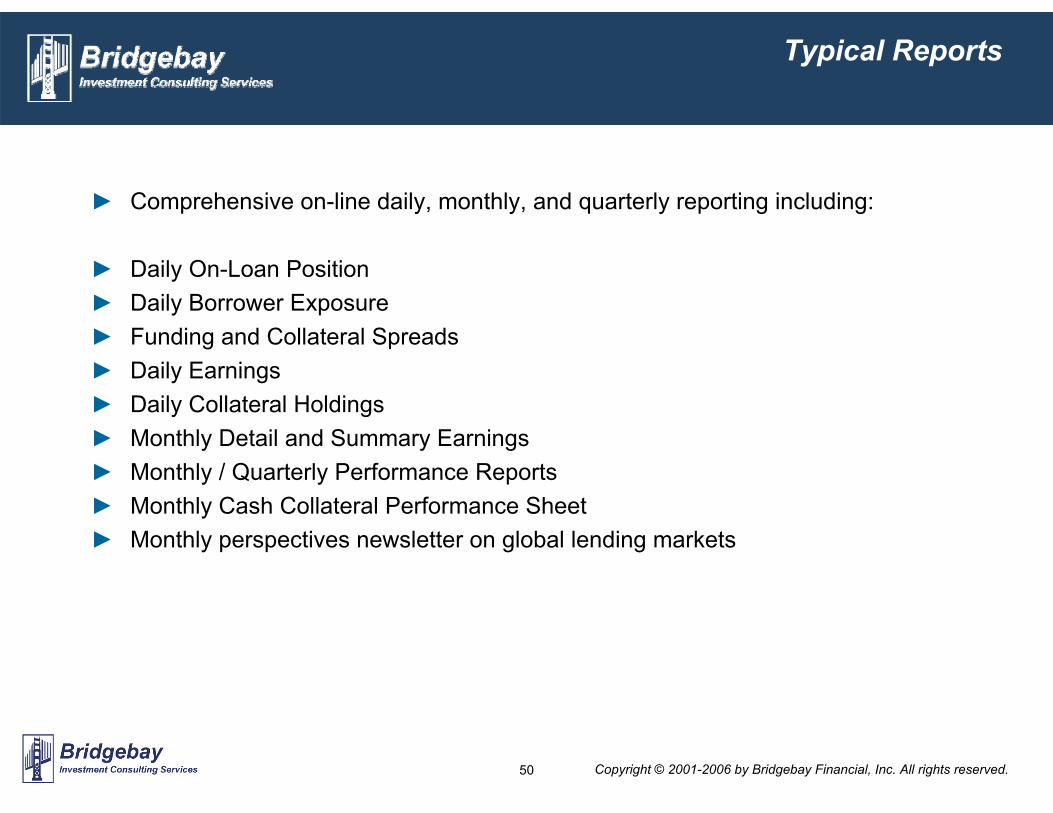

Typical Reports

► Comprehensive on-line daily, monthly, and quarterly reporting including:

► Daily On-Loan Position► Daily Borrower Exposure► Funding and Collateral Spreads► Daily Earnings► Daily Collateral Holdings► Monthly Detail and Summary Earnings► Monthly / Quarterly Performance Reports► Monthly Cash Collateral Performance Sheet► Monthly perspectives newsletter on global lending markets

Copyright © 2001-2006 by Bridgebay Financial, Inc. All rights reserved.51

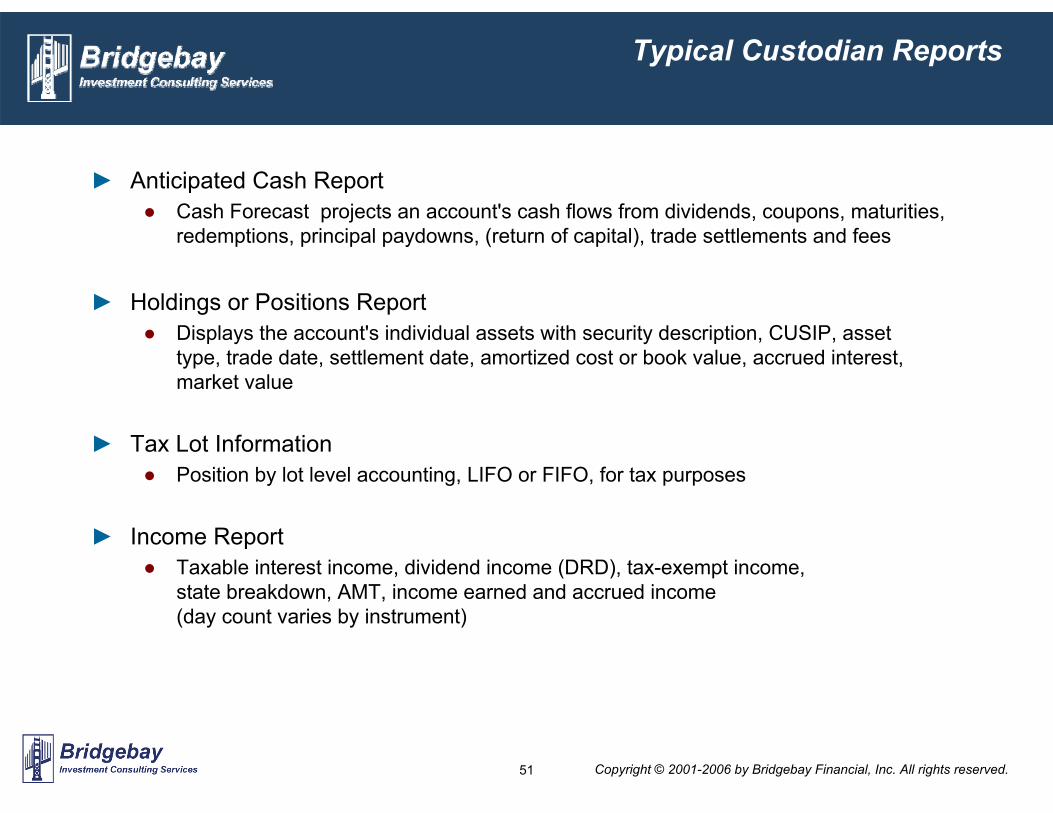

Typical Custodian Reports

► Anticipated Cash Report● Cash Forecast projects an account's cash flows from dividends, coupons, maturities,

redemptions, principal paydowns, (return of capital), trade settlements and fees

► Holdings or Positions Report ● Displays the account's individual assets with security description, CUSIP, asset

type, trade date, settlement date, amortized cost or book value, accrued interest, market value

► Tax Lot Information● Position by lot level accounting, LIFO or FIFO, for tax purposes

► Income Report ● Taxable interest income, dividend income (DRD), tax-exempt income,

state breakdown, AMT, income earned and accrued income(day count varies by instrument)

Copyright © 2001-2006 by Bridgebay Financial, Inc. All rights reserved.52

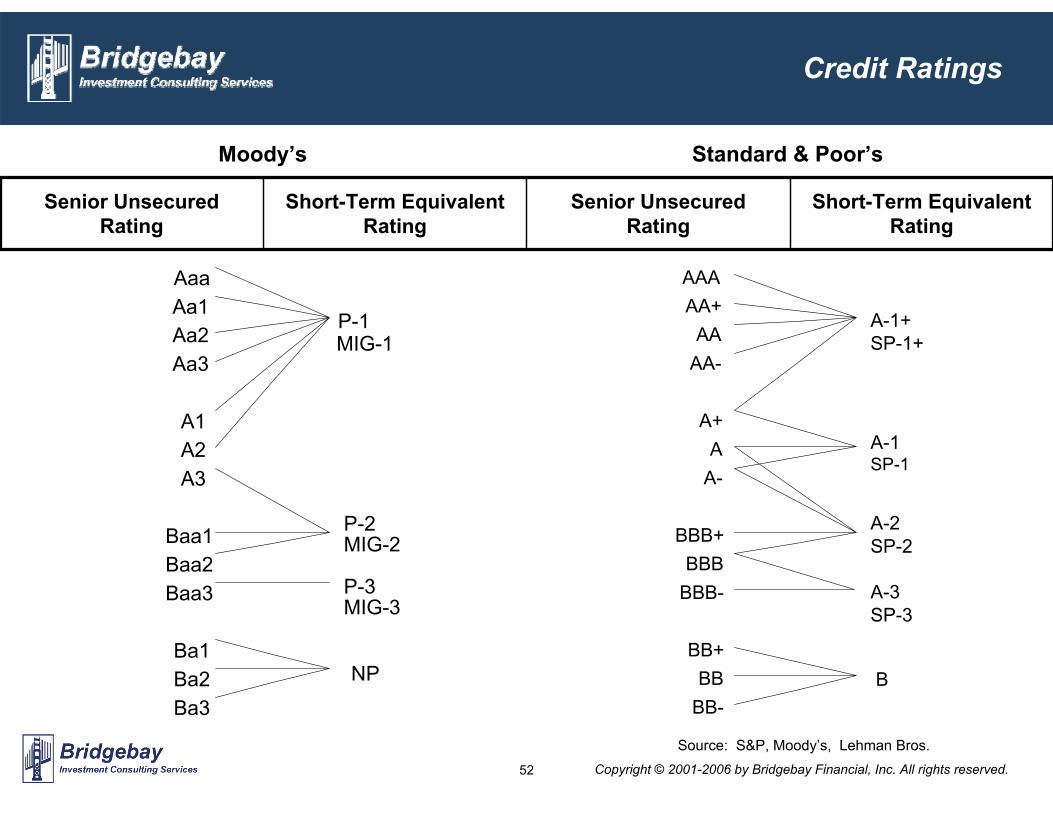

Moody’s Standard & Poor’s

AaaAa1Aa2Aa3

A1A2A3

Baa1Baa2Baa3

Ba1Ba2Ba3

P-1MIG-1

P-2MIG-2

P-3MIG-3

NP

AAAAA+

AAAA-

A+A

A-

BBB+BBB

BBB-

BB+BB

BB-

A-1+SP-1+

A-1SP-1

A-2SP-2

A-3SP-3

B

Source: S&P, Moody’s, Lehman Bros.

Credit Ratings

Short-Term Equivalent Rating

Senior Unsecured Rating

Short-Term Equivalent Rating

Senior Unsecured Rating

Copyright © 2001-2006 by Bridgebay Financial, Inc. All rights reserved.53

Securities Lending ProgramsIssues to Consider

► Years of lending experience► Number of active lending clients► Lendable base of assets► Amount of assets on loan daily► 24 hour trading capabilities globally or U.S. only► Amount of non-custody lending volume► Commitment to business, % of bank’s total revenue from this business► Custodian assets gained / lost ► Array of cash collateral investment programs available

● Reinvestment expertise internal or outsourced to third party● Number of investment professionals, credit and structure expertise● Assets under management in short-term assets

Copyright © 2001-2006 by Bridgebay Financial, Inc. All rights reserved.54

Securities Lending ProgramsRisk Assessment

► How is Counterparty Risk evaluated ● Independent Credit Policy Group● Credit Approval Process ● Frequency and ongoing review of borrowers● Depth and breadth of credit analysis of borrowers● Diversification of approved borrowers

► Collateral Management● Short-term investment manager AUM● Disciplined investment process● Expertise and track record ● Acceptable forms of collateral – Cash / LOCs / Securities● Daily mark-to-market (margins)● Conservative / High-Quality instruments● Ratings by S&P / NAIC Class 1 Rating● Number and Size of Liquidity Pools – the more the better● Commingled / separate account structures● Your portfolio size as % of collateral pool

Copyright © 2001-2006 by Bridgebay Financial, Inc. All rights reserved.55

Securities Lending ProgramsRisk Management Elements

► Borrower Default Indemnification● Full indemnification against a borrower’s failure to return securities● Strength of the Agent

► Compliance Program● Contractual / regulatory reviews● Front-end trade compliance● Continuous self-testing and monitoring● Internal / external examinations● Active liquidity management – Asset / Liability critical to minimize liquidity risk● Administrative oversight of investment vehicles

Copyright © 2001-2006 by Bridgebay Financial, Inc. All rights reserved.56

Securities Lending ProgramsRisk Management Elements

► Proactive interaction with Client● Product development● Addition / approval of borrowers

► Operations – Loan recalls● Importance of integrated systems ● Reallocation of loans● Recall from borrower● Contractual settlement of sales – discretionary

► Transparency – On-line systems