Embed Size (px)

Citation preview

October 9, 2007

MasterCard PayPass® Time & Motion Study Effect of merchant deployment quality on payment times (December 2006 & April-Sep 2007) Final

M. Kathryn (Kate) Peterson

October 9, 2007 © MasterCard. All rights reserved. 2

Author’s Note

• While quantitative measures have been gathered and analyzed, they should be considered directional and not predictive as the number of observations cannot be calculated to be statistically significant.

• Please refer to the Application of Results on slide 14.

October 9, 2007 © MasterCard. All rights reserved. 3

Executive Summary

• Research conducted to understand impact on retail purchase time of various types of PayPass deployments; methodology involved comparing purchase times of various ways to pay

• Eleven merchants of various categories were grouped by the quality of their PayPass POS (point-of-sale) deployment: high/medium/low*

– 2 pharmacy chains (New York metro) – 52 transactions

– 2 grocery chains (regional/metro) – 60 transactions

– 2 convenience store chains (1 national, 1 regional) – 60 transactions

– 3 national quick service restaurant chains – 86 transactions

– 2 movie theater chains (New York metro) – 26 transactions

• 10 of 11 merchants had integrated PayPass terminals/readers with cash register systems; 1 merchant setup required dual entry**

* See page 13 for a definition of high, medium and low quality deployments **A dual entry setup requires the cashier to setup the terminal to receive payment card information, and is not ideal

October 9, 2007 © MasterCard. All rights reserved. 4

Executive Summary (cont.)

• High quality PayPass deployments were:

– 52% (or 15 seconds) faster than cash payments

– 33% (or 6.86 seconds) faster than payment cards

• Medium quality PayPass were:

– 56% (or 7.87 seconds) slower than high quality PayPass setup

– 26% (or 7.74 seconds) faster than cash in this set-up

• Low quality PayPass deployments were

– 172% (or 24.10 seconds) slower than those in high quality setups, and were 83% (or 17.35 seconds) slower than cash in low quality setups.

• See the table on the following page

October 9, 2007 © MasterCard. All rights reserved. 5

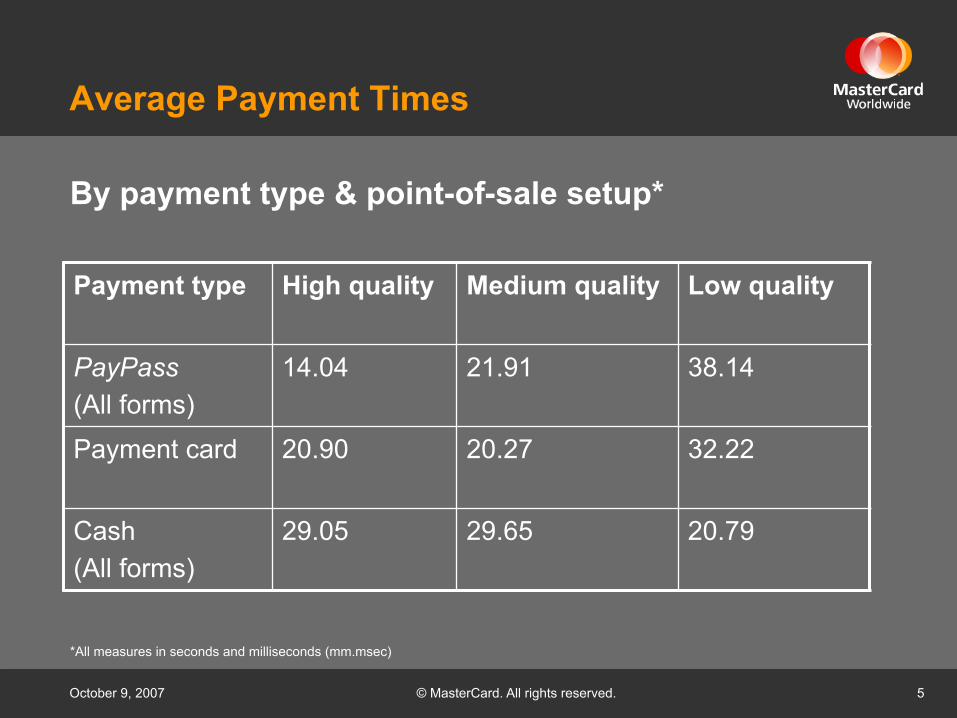

Average Payment Times

Payment type High quality Medium quality Low quality

PayPass (All forms)

14.04 21.91 38.14

Payment card 20.90 20.27 32.22

Cash (All forms)

29.05 29.65 20.79

*All measures in seconds and milliseconds (mm.msec)

By payment type & point-of-sale setup*

October 9, 2007

Research Objectives

October 9, 2007 © MasterCard. All rights reserved. 7

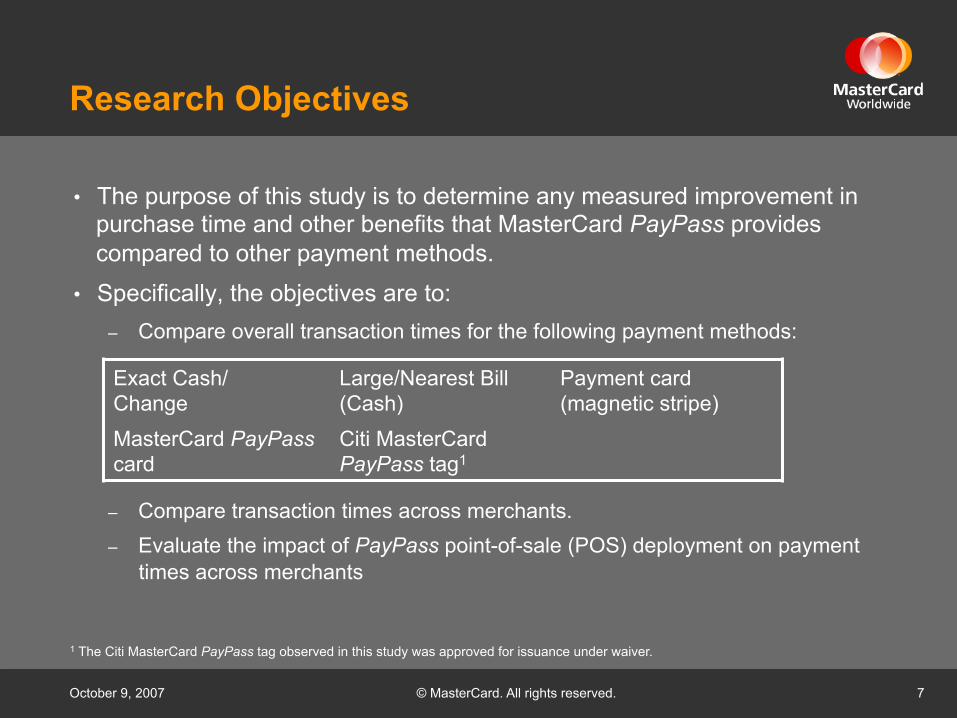

Research Objectives

• The purpose of this study is to determine any measured improvement in purchase time and other benefits that MasterCard PayPass provides compared to other payment methods.

• Specifically, the objectives are to: – Compare overall transaction times for the following payment methods:

– Compare transaction times across merchants. – Evaluate the impact of PayPass point-of-sale (POS) deployment on payment

times across merchants

Exact Cash/ Change

Large/Nearest Bill (Cash)

Payment card (magnetic stripe)

MasterCard PayPass card

Citi MasterCard PayPass tag1

1 The Citi MasterCard PayPass tag observed in this study was approved for issuance under waiver.

October 9, 2007

Methodology

October 9, 2007 © MasterCard. All rights reserved. 9

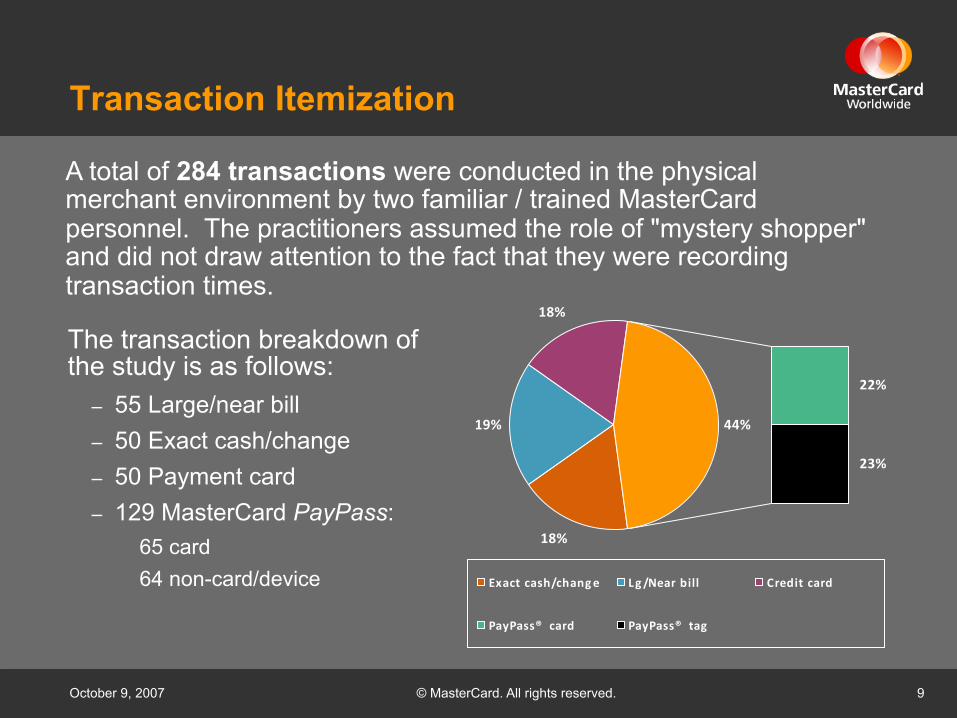

Transaction Itemization

The transaction breakdown of the study is as follows:

– 55 Large/near bill – 50 Exact cash/change – 50 Payment card – 129 MasterCard PayPass:

65 card 64 non-card/device

A total of 284 transactions were conducted in the physical merchant environment by two familiar / trained MasterCard personnel. The practitioners assumed the role of "mystery shopper" and did not draw attention to the fact that they were recording transaction times.

18%

19%

18%

22%

23%

44%

Exact cash/change Lg /Near bill Credit card

PayPass® card PayPass® tag

October 9, 2007 © MasterCard. All rights reserved. 10

General Quality & Control

• The general quality and control criteria for the study provided that: – At least one transaction of each payment type was conducted at 4 different

locations for each merchant.*

– Merchants were visited at varied times throughout the day.

– One researcher did all PayPass card transactions, another all exact change payments, etc. This provided control in the amount of time to locate money or card, get receipt or change, etc.

– Purchases were similar in nature, but not exactly the same (i.e. one small item per transaction, one food or beverage at Burger King, etc).

– Detailed tracking sheets were completed for each transaction to provide detailed documentation for future reference.

– Most transactions were audio taped to provide additional documentation.

* We conducted the study at 6 CVS pharmacy locations in New York City. Four had implemented the HHP terminal and reader; 2 implemented the Hypercom terminal and reader.

October 9, 2007 © MasterCard. All rights reserved. 11

Time Measurement

• The time measurement quality and control criteria for the study provided that:

– Measurements were taken in seconds accurate to the nearest hundredth of a second (00:00:00.00).

– The same researcher timed all transactions to ensure consistency of measurements, using a Sportline brand stopwatch.

• Measurements included: 1. Overall Purchase Time

The total time involved in the transaction, from when the customer is greeted by the cashier until the customer receives the receipt.

2. Payment Time* The time involved from when the cashier tells the customer the final price until the customer receives the receipt.

*Measurement of grocery self-checkout machine transactions differ from above, due to their unique characteristics (described in detail on following page).

October 9, 2007 © MasterCard. All rights reserved. 12

Time Measurement (cont.)

• Time measurements techniques differed for self checkout due to its unique characteristics:

Self-Checkout Payment Time – For PayPass form factors & payment cards. The total time, starting

with the start of payment portion of the self-scan, until the machine confirms that payment is complete and customer can take receipt and remove groceries.

October 9, 2007 © MasterCard. All rights reserved. 13

Definitions

• PayPass Point-of-Sale Deployment Quality* – To analyze the impact of the deployment context on

transaction times, we grouped the merchant deployments into three levels of quality:

High: Integrated PayPass reader & payment terminal with the cash register. Minimal cashier involvement needed to make card payments. Some training for cashiers; or instructions at point-of-sale. Implemented for 1-2 years, or more. Generally follows MasterCard PayPass deployment best practices. Medium: Integrated card terminal and register; PayPass reader can be stand-alone. Some cashier involvement needed to finish card payment steps. Little or no training. Implemented 6-12 months. Low: PayPass reader & payment terminal separate from register; dual entry required. Cashier required to setup terminal and complete payment steps on card terminal. No training provided. Recently implemented.

*The levels were set by the PayPass merchant deployment team after a high-level review of various POS contexts.

October 9, 2007 © MasterCard. All rights reserved. 14

Application of Results

• This study is intended to provide a general, qualitative report of the time metrics for purchases at PayPass merchants selected for this study—the limited number of trials conducted is not statistically relevant.

• As such, the results are only applicable to this limited sample and cannot be directly applied to merchants outside the scope of this trial.

October 9, 2007

General Conclusions

October 9, 2007 © MasterCard. All rights reserved. 16

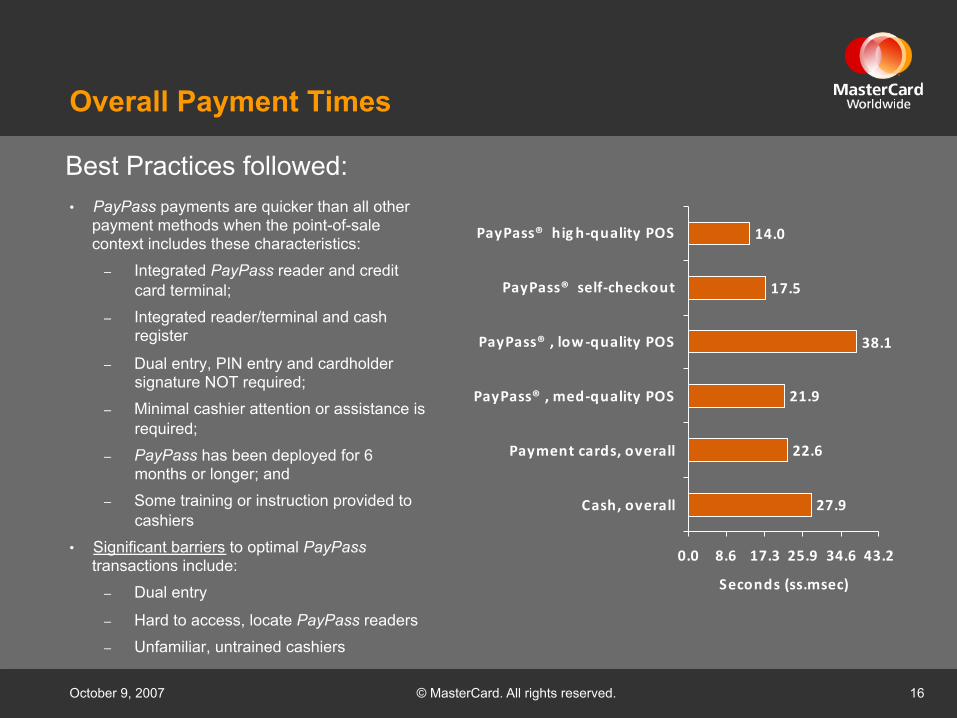

Overall Payment Times

• PayPass payments are quicker than all other payment methods when the point-of-sale context includes these characteristics:

– Integrated PayPass reader and credit card terminal;

– Integrated reader/terminal and cash register

– Dual entry, PIN entry and cardholder signature NOT required;

– Minimal cashier attention or assistance is required;

– PayPass has been deployed for 6 months or longer; and

– Some training or instruction provided to cashiers

• Significant barriers to optimal PayPass transactions include:

– Dual entry

– Hard to access, locate PayPass readers

– Unfamiliar, untrained cashiers

Best Practices followed:

27.9

22.6

21.9

38.1

17.5

14.0

0.0 8.6 17.3 25.9 34.6 43.2

Cash, overall

Payment cards, overall

PayPass® , med-‐quality POS

PayPass® , low-‐quality POS

PayPass® self-‐checkout

PayPass® hig h-‐quality POS

Seconds (ss.msec)

October 9, 2007 © MasterCard. All rights reserved. 17

Overall Payment Times (cont.)

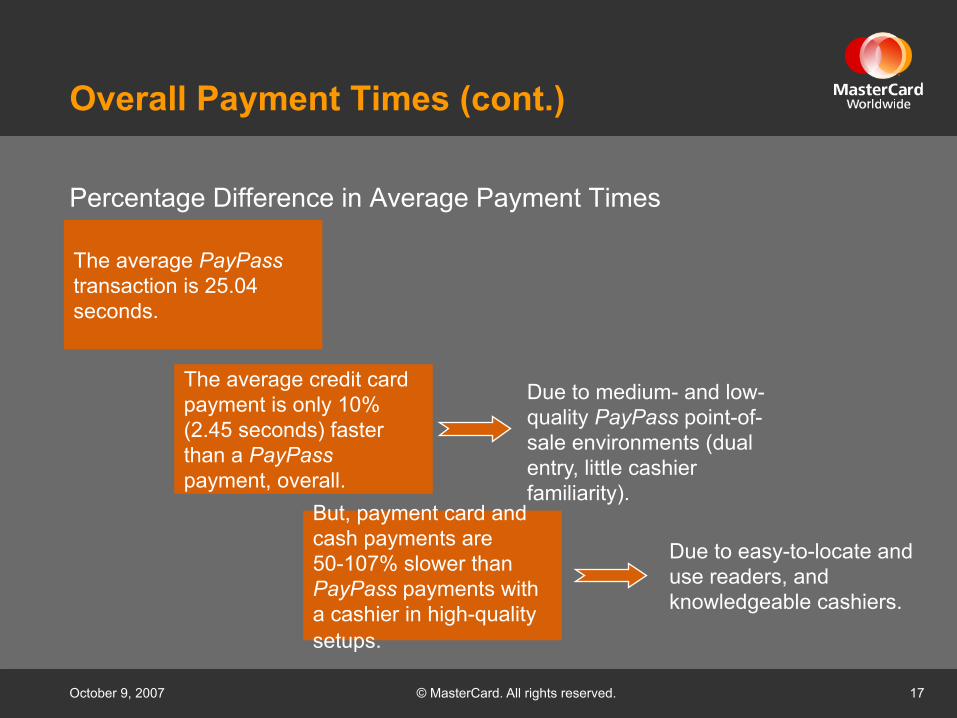

Percentage Difference in Average Payment Times

The average PayPass transaction is 25.04 seconds.

Due to easy-to-locate and use readers, and knowledgeable cashiers.

But, payment card and cash payments are 50-107% slower than PayPass payments with a cashier in high-quality setups.

Due to medium- and low-quality PayPass point-of-sale environments (dual entry, little cashier familiarity).

The average credit card payment is only 10% (2.45 seconds) faster than a PayPass payment, overall.

October 9, 2007 © MasterCard. All rights reserved. 18

PayPass Payment Times

• The pharmacies, grocery stores & convenience stores that we studied had a high level of integrated readers and terminals making these locations our fastest, “high” quality deployed locations.

• The QSR and movie locations we studied had either a dual entry set up or the readers were in awkward locations making it more difficult to easily use leading to their lower scores.

PayPass payment times across all merchants locations in study:

34.9

32.9

23.0

20.2

12.2

0.0 8.6 17.3 25.9 34.6 43.2

Theater

QSR

Convenience

Grocery

Pharmacy

Seconds (ss.msec)

October 9, 2007 © MasterCard. All rights reserved. 19

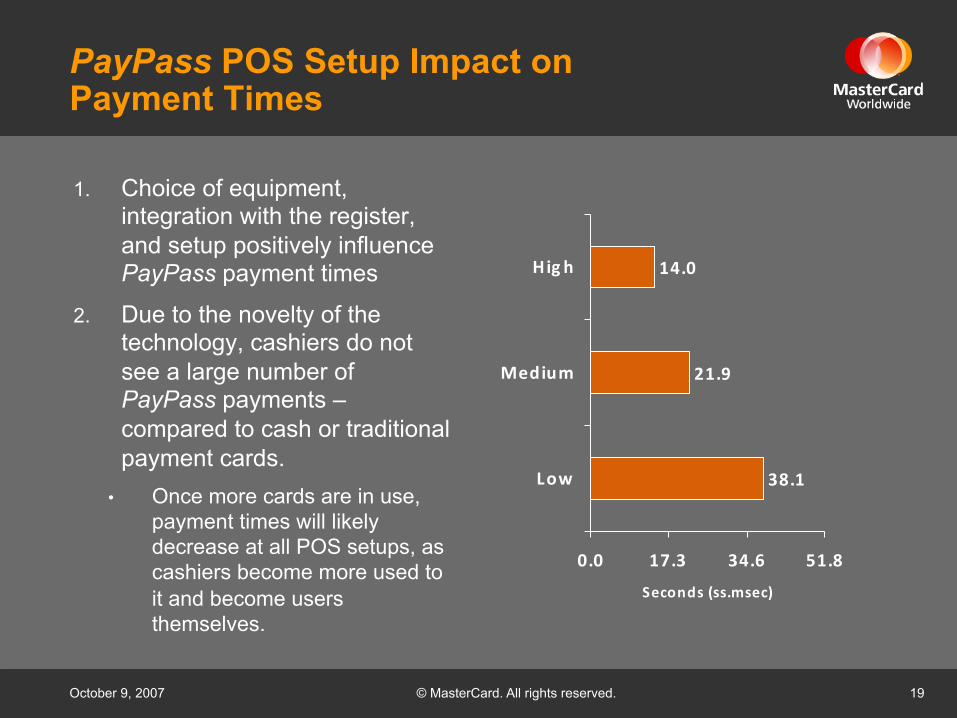

PayPass POS Setup Impact on Payment Times

1. Choice of equipment, integration with the register, and setup positively influence PayPass payment times

2. Due to the novelty of the technology, cashiers do not see a large number of PayPass payments – compared to cash or traditional payment cards.

• Once more cards are in use, payment times will likely decrease at all POS setups, as cashiers become more used to it and become users themselves.

38.1

21.9

14.0

0.0 17.3 34.6 51.8

Low

Medium

Hig h

Seconds (ss.msec)

October 9, 2007 © MasterCard. All rights reserved. 20

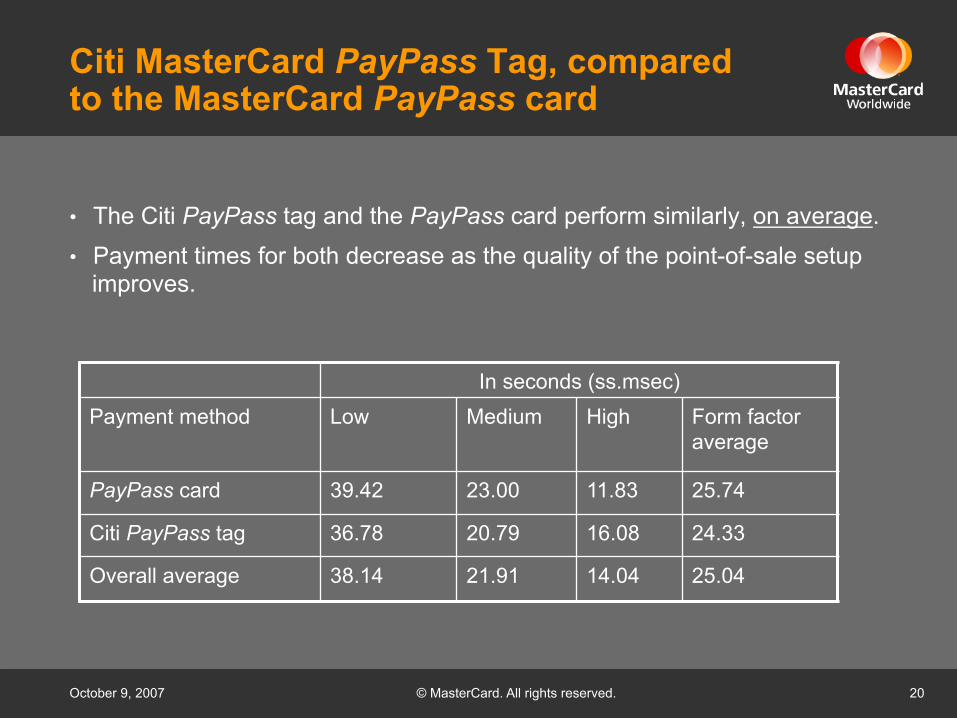

Citi MasterCard PayPass Tag, compared to the MasterCard PayPass card

In seconds (ss.msec) Payment method Low Medium High Form factor

average

PayPass card 39.42 23.00 11.83 25.74

Citi PayPass tag 36.78 20.79 16.08 24.33

Overall average 38.14 21.91 14.04 25.04

• The Citi PayPass tag and the PayPass card perform similarly, on average.

• Payment times for both decrease as the quality of the point-of-sale setup improves.

October 9, 2007

Merchant-Specific Conclusions

October 9, 2007 © MasterCard. All rights reserved. 22

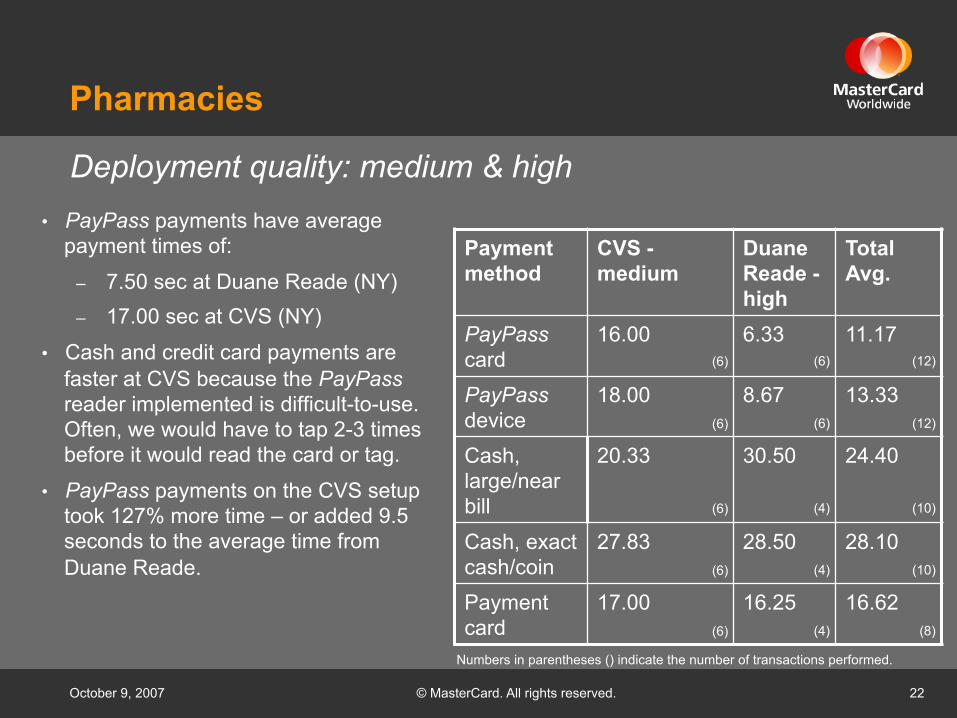

Pharmacies

Payment method

CVS - medium

Duane Reade - high

Total Avg.

PayPass card

16.00 6.33 11.17

PayPass device

18.00 8.67 13.33

Cash, large/near bill

20.33 30.50 24.40

Cash, exact cash/coin

27.83 28.50 28.10

Payment card

17.00 16.25 16.62

• PayPass payments have average payment times of:

– 7.50 sec at Duane Reade (NY) – 17.00 sec at CVS (NY)

• Cash and credit card payments are faster at CVS because the PayPass reader implemented is difficult-to-use. Often, we would have to tap 2-3 times before it would read the card or tag.

• PayPass payments on the CVS setup took 127% more time – or added 9.5 seconds to the average time from Duane Reade.

Deployment quality: medium & high

(6)

(6)

(6)

(6)

(6)

(6)

(6)

(4)

(4)

(4)

(12)

(12)

(10)

(10)

(8)

Numbers in parentheses () indicate the number of transactions performed.

October 9, 2007 © MasterCard. All rights reserved. 23

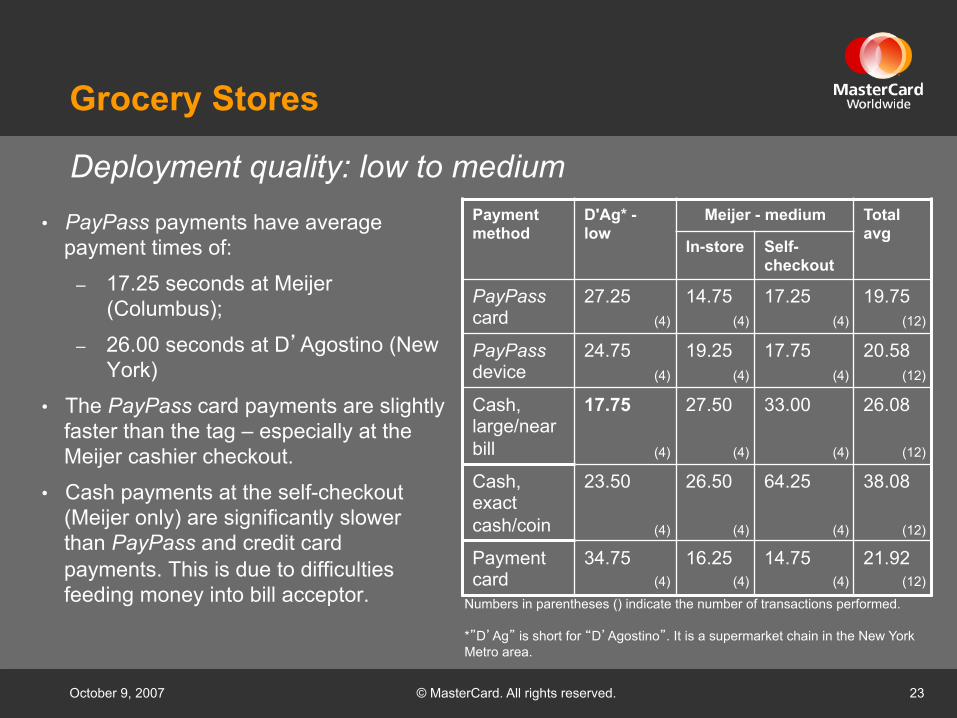

Grocery Stores

Payment method

D'Ag* - low

Meijer - medium Total avg

In-store Self-checkout

PayPass card

27.25 14.75 17.25 19.75

PayPass device

24.75 19.25 17.75 20.58

Cash, large/near bill

17.75 27.50 33.00 26.08

Cash, exact cash/coin

23.50 26.50 64.25 38.08

Payment card

34.75 16.25 14.75 21.92

• PayPass payments have average payment times of:

– 17.25 seconds at Meijer (Columbus);

– 26.00 seconds at D’Agostino (New York)

• The PayPass card payments are slightly faster than the tag – especially at the Meijer cashier checkout.

• Cash payments at the self-checkout (Meijer only) are significantly slower than PayPass and credit card payments. This is due to difficulties feeding money into bill acceptor.

Deployment quality: low to medium

*”D’Ag” is short for “D’Agostino”. It is a supermarket chain in the New York Metro area.

(4)

(4)

(4)

(4)

(4)

Numbers in parentheses () indicate the number of transactions performed.

(4)

(4)

(4)

(4)

(4)

(4)

(4)

(4)

(4)

(4)

(12)

(12)

(12)

(12)

(12)

October 9, 2007 © MasterCard. All rights reserved. 24

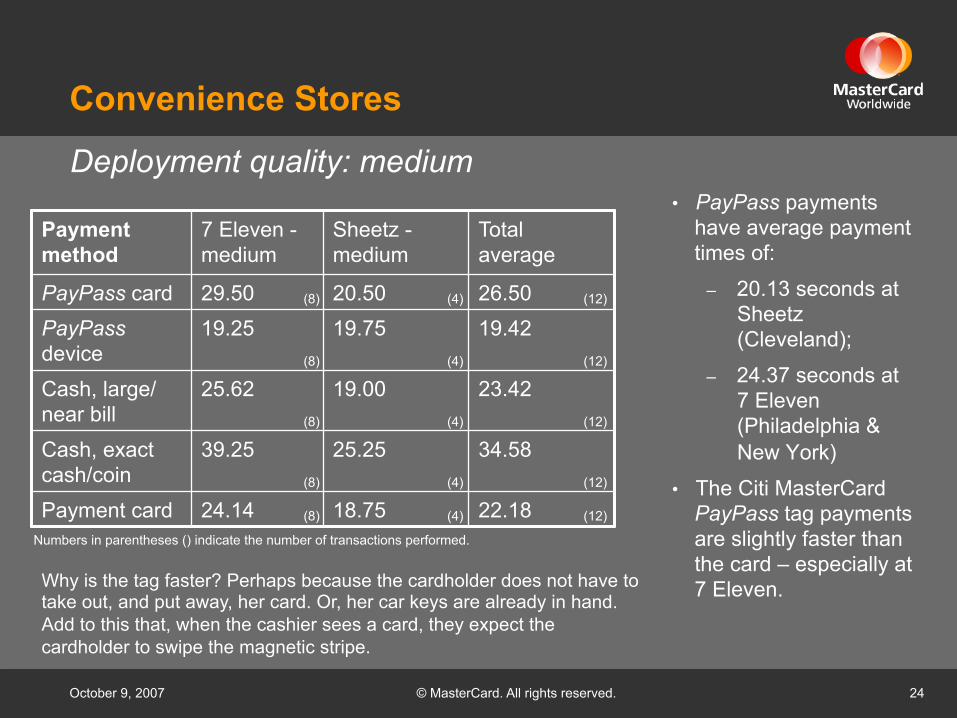

Convenience Stores

Payment method

7 Eleven - medium

Sheetz - medium

Total average

PayPass card 29.50 20.50 26.50 PayPass device

19.25 19.75 19.42

Cash, large/near bill

25.62 19.00 23.42

Cash, exact cash/coin

39.25 25.25 34.58

Payment card 24.14 18.75 22.18

• PayPass payments have average payment times of:

– 20.13 seconds at Sheetz (Cleveland);

– 24.37 seconds at 7 Eleven (Philadelphia & New York)

• The Citi MasterCard PayPass tag payments are slightly faster than the card – especially at 7 Eleven.

Deployment quality: medium

Why is the tag faster? Perhaps because the cardholder does not have to take out, and put away, her card. Or, her car keys are already in hand. Add to this that, when the cashier sees a card, they expect the cardholder to swipe the magnetic stripe.

Numbers in parentheses () indicate the number of transactions performed.

(8)

(8)

(8)

(8)

(8)

(4)

(4)

(4)

(4)

(4)

(12)

(12)

(12)

(12)

(12)

October 9, 2007 © MasterCard. All rights reserved. 25

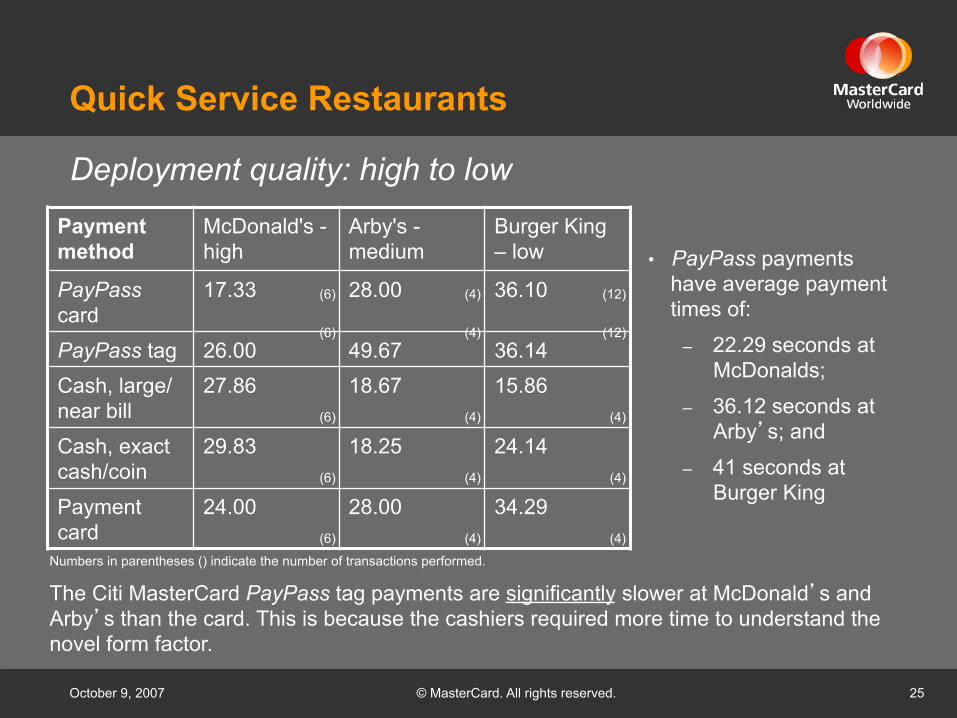

Quick Service Restaurants

Payment method

McDonald's - high

Arby's - medium

Burger King – low

PayPass card

17.33 28.00 36.10

PayPass tag 26.00 49.67 36.14 Cash, large/near bill

27.86 18.67 15.86

Cash, exact cash/coin

29.83 18.25 24.14

Payment card

24.00 28.00 34.29

• PayPass payments have average payment times of:

– 22.29 seconds at McDonalds;

– 36.12 seconds at Arby’s; and

– 41 seconds at Burger King

Deployment quality: high to low

The Citi MasterCard PayPass tag payments are significantly slower at McDonald’s and Arby’s than the card. This is because the cashiers required more time to understand the novel form factor.

Numbers in parentheses () indicate the number of transactions performed.

(6)

(6)

(6)

(6)

(6)

(4)

(4)

(4)

(4)

(4)

(12)

(12)

(4)

(4)

(4)

October 9, 2007 © MasterCard. All rights reserved. 26

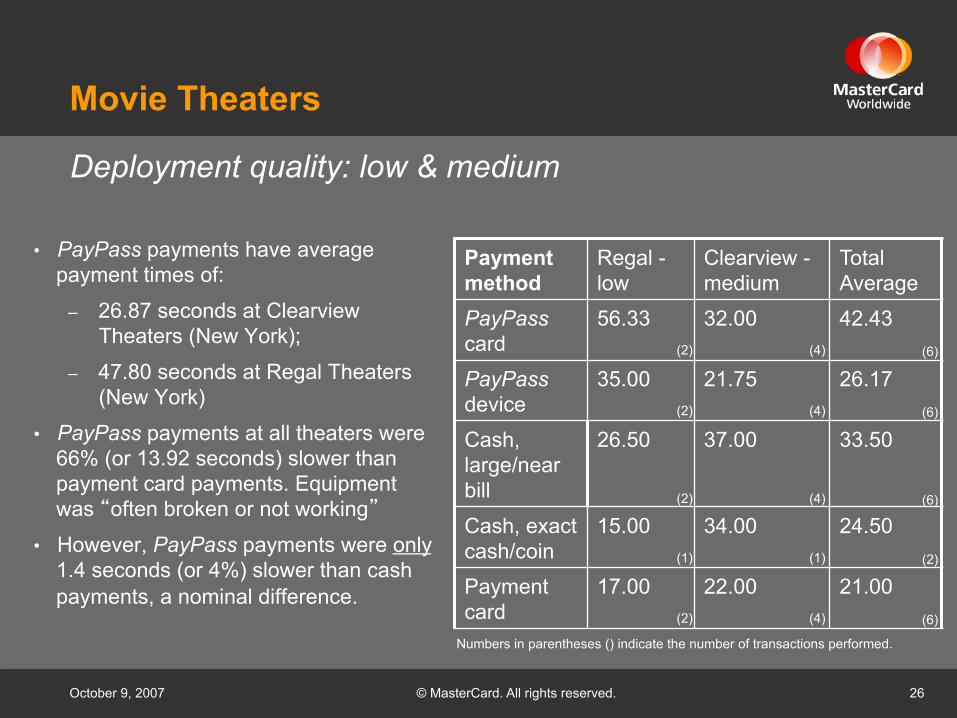

Movie Theaters

Payment method

Regal - low

Clearview - medium

Total Average

PayPass card

56.33 32.00 42.43

PayPass device

35.00 21.75 26.17

Cash, large/near bill

26.50 37.00 33.50

Cash, exact cash/coin

15.00 34.00 24.50

Payment card

17.00 22.00 21.00

• PayPass payments have average payment times of:

– 26.87 seconds at Clearview Theaters (New York);

– 47.80 seconds at Regal Theaters (New York)

• PayPass payments at all theaters were 66% (or 13.92 seconds) slower than payment card payments. Equipment was “often broken or not working”

• However, PayPass payments were only 1.4 seconds (or 4%) slower than cash payments, a nominal difference.

Deployment quality: low & medium

Numbers in parentheses () indicate the number of transactions performed.

(2)

(2)

(2)

(1)

(2)

(4)

(4)

(4)

(1)

(4)

(6)

(6)

(6)

(2)

(6)

Thank you.

![PayPass Personalization Data Specificationsdata.cardzone.cz/contactless/PayPass PDS (V1.3).pdf · 2010-03-14 · viii PayPass Personalization Data Specifications ... [PPMCHIP4] PayPass](https://img.pdfslide.us/doc/110x75/5b29370f7f8b9ae6748b4ab6/paypass-personalization-data-pds-v13pdf-2010-03-14-viii-paypass-personalization.jpg)