Embed Size (px)

Citation preview

Master Thesis

The Potential of Fresnel Reflectors for Process HeatGeneration in the MENA Region

AJ �®KQ @ ÈAÖÞ�� ð ¡�

B@ ��Qå��Ë @ �é�®¢JÓ ú

�èP@QmÌ'@ YJËñ�K ú ÉJ �KQ �» @ñ« Ð@Y j�J�@

�éJ K A¾Ó@

ByMartin Haagensubmitted to

Faculty of Electrical Engineering and Computer Science (University of Kassel)and Faculty of Engineering (University of Cairo) in partial fulfilment of the

requirements for M.Sc. degree in Renewable Energy and Energy Efficiency forthe MENA Region REMENA

Kassel, February 2012

1. Corrector Prof. Dr. Klaus Vajen (University of Kassel, Faculty of Mechanical Engineering,Department of Thermal Engineering)

2. Corrector Prof. Dr. Sayed Kaseb (University of Cairo, Faculty of EngineeringDepartment of Mechanical Power Engineering)

3. Corrector Prof. Dr. Dirk Dahlhaus (University of Kassel, Faculty Electrical Engineering andComputer Sciences, Department of Telecommunications

Academic supervisor: Christoph LauterbachIndustrial supervisor: Tobias Schwind, Christian Zahler (Industrial Solar GmbH)

Martin Haagen Matriculation: 30253827 Sprollstr. 85 70597 Stuttgart [email protected]

Master Thesis

The Potential of Fresnel Reflectors for Process HeatGeneration in the MENA Region

AJ �®KQ @ ÈAÖÞ�� ð ¡�

B@ ��Qå��Ë @ �é�®¢JÓ ú

�èP@QmÌ'@ YJËñ�K ú ÉJ �KQ �» @ñ« Ð@Y j�J�@

�éJ K A¾Ó@

ByMartin Haagensubmitted to

Faculty of Electrical Engineering and Computer Science (University of Kassel)and Faculty of Engineering (University of Cairo) in partial fulfilment of the

requirements for M.Sc. degree in Renewable Energy and Energy Efficiency forthe MENA Region REMENA

Kassel, February 2012

Approved by the Examining Committee:

1. Corrector Prof. Dr. Adel Khalil

2. Corrector Dr. Hany Nokrashy

3. Corrector Prof. Dr. Dirk Dahlhaus

Academic Supervisor Christoph Lauterbach

Martin Haagen Matriculation: 30253827 Sprollstr. 85 70597 Stuttgart [email protected]

Abstract

This study assesses the potential of generating solar heat for industrialprocesses with linear Fresnel collectors in the Middle East and NorthAfrica to be around 460 TWh. Based on a comprehensive top-down ap-proach Morocco and Tunisia are identified as most promising. Withinthe bottom-up approach 10 companies in Morocco and 7 companies inTunisia were visited and their potential assessed in more detail. More-over, the most promising industries were examined on potential benefitsand challenges. Furthermore, the major legislations and institutions ofthe countries are included in the assessment. A single variable sensitivityanalysis examines the factors which influence the internal rate of returnand thermal energy costs of solar process heat systems. A reference sce-nario shows that currently solar process heat systems with linear Fresnelcollectors are not feasible in Morocco or Tunisia. An institutional com-parison identifies most suitable support schemes for solar process heatsystems. Based on the results the study provides recommendations forpolicy makers and the private sector.

I thank my correctors, Prof. Dr. Klaus Vajen, Dr. Sayed Kaseb,Prof. Dr. Dirk Dahlhaus and especially my academic supervisorChristoph Lauterbach, as well as all the staff from Industrial Solar,especially Christian Zahler and Tobias Schwind for the constantsupport, helpful advice and inspiration. Without them, the thesiscould not have been completed.

Contents1. Introduction 7

1.1. Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81.2. Literature review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2. Fundamentals 102.1. Basic solar energy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102.2. Collection of solar energy with linear Fresnel collectors . . . . . . . . . . . . . . 12

2.2.1. Optical and thermal analysis . . . . . . . . . . . . . . . . . . . . . . . . 132.2.2. Components of linear Fresnel collectors . . . . . . . . . . . . . . . . . . . 152.2.3. Specific advantages of linear Fresnel collectors . . . . . . . . . . . . . . . 162.2.4. Cost and yields of linear Fresnel collectors . . . . . . . . . . . . . . . . . 17

2.3. Integration of solar heat in industrial processes . . . . . . . . . . . . . . . . . . 192.3.1. Basic concepts for integration . . . . . . . . . . . . . . . . . . . . . . . . 192.3.2. Storage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212.3.3. Further effects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

2.4. Tools for financial analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 252.4.1. Investment appraisal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 252.4.2. Further financial tools . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

3. Top down approach - energy situation in Middle East and North Africa 303.1. Energy supply and demand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 303.2. Potential for renewable energies . . . . . . . . . . . . . . . . . . . . . . . . . . . 313.3. Overview of countries and selection for bottom up assessment . . . . . . . . . . 313.4. Industrial heat demand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 323.5. Solar process heat at medium temperatures in Middle East and North Africa . . 353.6. Suitable sectors for process heat generation at medium temperatures . . . . . . 363.7. Challenges for solar heat in industrial processes . . . . . . . . . . . . . . . . . . 40

4. Bottom up assessment 424.1. Morocco . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

4.1.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 424.1.2. The potential and rationale for renewable energies . . . . . . . . . . . . . 434.1.3. Institutional framework for renewable energies . . . . . . . . . . . . . . . 444.1.4. Industry in Morocco . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

5

4.1.5. Qualitative assessment of solar process heat in Morocco . . . . . . . . . 494.2. Tunisia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

4.2.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 524.2.2. The potential and rationale for renewable energies . . . . . . . . . . . . . 534.2.3. Institutional framework for renewable energies . . . . . . . . . . . . . . . 544.2.4. Industry in Tunisia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 564.2.5. Qualitative assessment of solar process heat in Tunisia . . . . . . . . . . 57

4.3. Comparison of countries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

5. Economic and institutional assessment of solar process heat in Middle East andNorth Africa 615.1. Variables and sensitivity analysis . . . . . . . . . . . . . . . . . . . . . . . . . . 615.2. Reference scenarios . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 655.3. Institutions for solar industrial process heat in the Middle East and North Africa 67

5.3.1. Support schemes in Middle East and North Africa . . . . . . . . . . . . 685.3.2. Analysis of support schemes . . . . . . . . . . . . . . . . . . . . . . . . . 68

6. Summary and conclusions 71

References 74

List of Abbreviations 85

Appendix 92

A. Energy tariffs in Morocco and Tunisia 92

B. Gasgrid in Tunisia 93

C. Food companies listed at the Moroccan and Tunisian stock exchange 94

D. Exemplary calculation for reference case 95

E. Economic potentials for renewable energies in Middle East and North Africa andfurther energy data 97

6

1. IntroductionToday´s society is more than ever dependant on energy. Yet, within the last decades challengesof the current energy supply system became apparent. Global reserves of fossil fuels are on de-cline and the strong increase of energy prices impedes social and economic development. At thesame time increasing emissions are responsible for the anthropogenic part of climate change.Since the publication of the Stern report (Stern, 2007), also the economic dimensions of climatechange are acknowledged. Furthermore, the extraction and combustion of fossil fuels have se-vere impacts on human health and the environment. Thus, major changes in the energy supplysystem are necessary. In the last years the use of renewable energies (RE) increased. Yet, theystill play only a minor role in industrial production, although industry is responsible for around33 % of total energy demand according to the United Nations Industrial Development Organi-zation (UNIDO) (UNIDO, 2011). The same study also expects that the industrial productiongrows by a factor of four until 2050, which highlights the crucial importance to address REin industry. As will be shown in Section 3.4 heat is the dominant energy form in industrialproduction. Several studies (see Section 1.2) already assessed the potential of solar heat forindustrial processes (SHIP) and all found that application is far behind the potential. Whilemost SHIP assessments were restricted to non-concentrating solar collectors and regionally fo-cussed on Europe this study differs in three aspects. First, it takes not only a pure technicalapproach (e.g. energy characteristics) but also considers industrial and socio-economic datawhich are crucial for industrial decision makers.Second, it examines Middle East and North Africa1 (MENA), this region was so far studied onlyonce (Reiners, 2011). The total energy demand of MENA is small compared to other regionsbut sufficiently large, and the countries similar enough, to justify a focussed examination.Third, due to the high share of direct irradiation in MENA, as well as the continuous develop-ment of concentrating technologies, it focuses on SHIP at higher temperatures with concentrat-ing collectors (SHIPc) . In respect to the technology, the focus is on linear Fresnel collectors(LFC), under the hypothesis that they have inherent advantages for SHIPc (see Section 2.2.3).Expanding the scope to higher temperatures allows to include more processes. Moreover, whensteam is considered in comparison to hot water, the overall potential further raises due to thehigh energy needed for evaporation2.Thus, it is the objective to identify countries and industries within MENA which are most

1This study covers Algeria, Bahrain, Egypt, Jordan, Lebanon, Libya, Kuwait, Morocco, Oman, Qatar, SaudiArabia, Syria, Tunisia, Turkey, the United Arab Emirates and Yemen. The Palestinian Territories and Israelare not considered.

2Energy demand to heat water from 20◦C to 100◦C without evaporation is around 340 kJ/kg. To evaporateit at 100◦C it needs an additional 2200 kJ/kg.

7

promising for SHIPc taking social, economic, industrial and institutional aspects into account.Sometimes SHIP and SHIPc can be treated analogously, sometimes differentiation is crucial.

Social dimensionEven though the topic is mainly technical and economical it also has an important social di-mension. First, fossil fuel combustion causes health and environmental problems which effecthuman development. Moreover, with ongoing technical development and raising energy pricesRE will be the cheaper energy source in the mid-term. If a country lacks behind in this tran-sition process (technical know how, awareness, human capacities, institutions) it will have acompetitive disadvantage in the future which impedes social and economic development.

1.1. MethodologyThis section discusses the methodology applied within this study. The analytical part is com-prised of five different approaches.First, within the top-down approach 16 MENA countries are compared and the countries withcomparatively high potential for SHIP, whereas a variety of factors is taken into account, areidentified. Moreover, industries are compared in respect to the temperature levels applied.Second, within the bottom-up approach the countries with high potential are studied in moredetail. 17 companies from promissing industries were assessed on key criteria like: (i) roofstructure, (ii) solar share, (iii) process temperature, (iv) supply temperature, (v) heat carrier,(vi) capital, (vii) annual days of production, (viii) hours of reduction per day. For some of thecriteria the result can only be estimated3. The selection of companies was mainly based oninternet research of websites for industrial development4. There was no strict methodology forthe selection of companies but size was a key criteria5(e.g. turnover, employees). For this studythe companies were made anonymous. The approach used within the bottom up part of thisstudy is sampling - examining a small number of enterprises and drawing conclusions aboutthe population. For statistically valid results the sampling has to adhere to several conditions,as discussed in (Freedman et al., 1997). Since they could not be fulfilled within this study theresults are not statistically sound but provide a confined insight.Third, within the sensitivity analysis eleven input factors are assessed on their relative impact.Forth, within the reference scenarios several scenarios are discussed which are based on actual

3The solar share for example depends on a varying demand. Moreover, often not all area which theoreticallycan be covered will be be available for installation.

4for Morocco: http://www.emergence.gov.ma, for Tunisia: http://www.tunisianindustry.nat.tn5as shown in Figure 6 the technology is only suitable for comparatively big installations

8

country data but not on specific companies. This allows to compare focus countries and dif-ferent systems (steam, cooling). Finally, within an institutional comparison the countries areassessed and good institutional frameworks identified.

1.2. Literature reviewWithin the literature on SHIP there are two major approaches. Some studies use a bottom upapproach, extrapolating a total potential from some assessed companies. Others use a top downapproach, based on aggregated industrial figures. UNIDO found that solar thermal energy cancontribute 1,556 TWh/y (≈ 3%) to industrial energy demand by 20506 (UNIDO, 2011). Astudy on the ”Potential Of Solar Heat for Industrial Processes” (POSHIP) (Schweiger et al.,2001) estimated the potential for solar heat at medium temperatures for Spain and Portugal asaround 5.8 TWh/year. Another study, ”PROduzieren MIt SOlar Energie” (Engl.: ”Producingwith Solar Energy” - PROMISE)(Müller et al., 2004) found a potential of 1.5 TWh/year inAustria. The European Solar Thermal Industry Federation (ESTIF) identified the potential forEurope and the key challenges for SHIP (ESTIF, 2006). The Ecoheatcool report(Ecoheatcooland Euroheat and Power, 2006) studied the total European heat market, also for Industry. Aspart of Task 33/IV of the International Energy Agency (IEA) a report (Vannoni et al., 2008)summarized the studies mentioned above. In 2009 another study estimated the total solarthermal potential for Europe (Weiss and Biermayr, 2009). A recent study assessed the totalpotential for SHIP in Germany (Lauterbach et al., 2011b) and examined nine sectors in moredetail. It found a potential of 15.6 TWh/year (3.1 % of the total industrial heat demand). Theresults of the various studies (e.g. potential in TWh) can not be directly compared since theydiffer, inter alia, in the temperature range and the country size. Nevertheless, they all founda potential of around 3-4.5 % of the total industrial heat demand (Lauterbach et al., 2011b),and that the installed capacity is far behind the potential. Some papers also deal with specificprojects and technical challenges like (Krüger et al., 2010). There are two studies examiningthe MENA region. Solaterm found great potential for solar thermal energy collection, but littleusage (Drück et al., 2007). Reiners estimated the total potential for solar steam production inindustry for the Mediterranean region7 to be 325 – 373 TWh (Reiners, 2011). Despite smallerdifferences all studies found similar results. First, there is a large potential for SHIP. Second,the most promising industries are (i) food and beverages, (ii) textile, (iii) plastics, (iv) pulpand paper as well as (v) chemical. Third, there are still major challenges, the most importantones are listed below in Section 3.7.

6Biomass contributes around 8 % today and is expected to continue its dominant role.7Including MENA and southern Europe

9

2. FundamentalsThis chapter provides fundamental knowledge necessary for this study. Section 2.1 introducesthe principles of solar energy collection. Section 2.2 describes the technology of the LFCcollector and Section 2.3 lists basic concepts for the integration of solar thermal energy inindustrial processes. Finally, Section 2.4 introduces financial tools for the economic analysis.

2.1. Basic solar energyThe radiation at the earth surface is determined by the geometrical relation of the earth surfaceto the sun as well as absorption and scattering processes within the atmosphere. Their effectdepends on atmospheric particles (aerosols8) and the distance within the atmosphere whichthe sun beams have to cross. The later is usually expressed as the atmospheric mass (AM),the distance relative to the path vertically upward. The global irradiance (G) is divided intothe beam irradiance (Gb) and the diffuse irradiance (Gd) . Due to its diurnal and seasonalvariation the irradiance is commonly expressed as the integrated value over one year9. Withinthe MENA region Gb can reach up to 2, 800kWh/m2/y according to a study by the DeutschesZentrum für Luft- und Raumfahrt10 (DLR, 2005).

Solar GeometryThe incidence angle of solar beams on the earth can be fully described by two angles.

• zenith angle = ΘZ between the beam and the surface normal

• azimuth angle = γ between the projection beam on the horizontal plane and south

In order to derive them, the solar declination angle and the hour angle are necessary. Since theearth axis of rotation is always tilted by 23.45◦ relative to the axis normal to the ecliptic plane,the solar declination angle - the angle between the sun earth center line and its projection onthe equator - changes between ±23.5 % over the year. Moreover, the hour angle - the angle theearth would have to turn to bring a specific spot directly under the sun - provides the positionof the earth to the sun independet of our local times. Thus, the incidence angle depends on aspecific spot, date and time.

8Liquid or solid particles in the air (e.g. water vapour, dust, combustion products, volcano particles)9To reduce variations between the years data is sometimes provided for a typical meteorological year (TMY).

10German Aerospace Centre

10

Solar resource assessment for concentrating collectorsConcentrating collectors only work with Gb, which is also called direct normal irradtion (DNI),whereas non-concentrating collectors or photovoltaic cells can use direct and diffuse irradiation.Their input resource is the global irradiance. The annual variability of Gb compared to G ismuch higher since the first is strongly affected from clouds (absorption or reflection) and aerosols(scattering) (Lohmann et al., 2006). For measuring DNI data there are various approaches. Itcan be measured with pyrheliometers from the ground, with satellite images or in a hybridmethod where the advantages of the ground data (spatial accurateness) and the satellite data(availability of long time series) are combined. Today various institutions offer DNI data11 whichdiffer in measurements and / or their analysis. Suri et al. compared six spatial databases andfound the differences in global irradiation to be 7 % on average (Suri, 2008). For DNI it can beexpected to be higher, as mentioned above. Moreover, they also found higher differences in areaswith low quality and density of data. Thus, for the MENA region were data is scarce and often oflow quality high variations between different sources are expected12 and examples can be seen inTable 1. This is a major obstacle for solar projects with concentrating collectors. Furthermore,

Table 1: Differences in DNI data from various institutions for MENA12

Location DLR Meteonorm UNEP (SWERA) Max Diff in %DNI in kWh/m2/y

Cairo, Eypt 2300 2041 2117 11Casablanca, Morocco 2100 1798 1570 25Tunis, Tunisia 1900 1805 1642 14

satellite data should be validated with ground measurements; Masdar overestimated the DNI fortheir Shams 1 project by more than 10 % with satellite images (Deign, 2012). While validationcan be done for concentrated solar power (CSP) projects it can be an obstacle for SHIPc sincevalidation costs (≈ 30.000 e) are comparatively higher due to lower investments. As a firststep for country classification DLR published CSP performance indicators for MENA countries(Trieb et al., 2005). It is an average yield per area for a specific country. It is based on theDNI on the ground (after correcting for atmospheric disturbances) on a 5km*5km spatial and0.5 h temporal resolution. All areas which are unsuitable for CSP power generation (e.g. slope,restricted areas, water bodies etc.) are excluded. However, the differences in DNI within a11for example: Mines-ParisTech (http://www.helioclim.org), DLR (http://www.solemi.de), or Meteonorm

(http://www.meteonorm.com)12A DLR project (2010 – 2012) produces a solar atlas for the Mediterranean to address this issue.12Data from (Trieb et al., 2005) and (UNEP, 2005) is read from maps which is less exact. SWERA = Solar

and Wind Energy Resource Assessment

11

country are often as a large as between countries. Looking at Morocco for example, the CSPperformance indicator is 2600 kWh/m2/a while the irradiation in the major industrial areasis around 1800 kWh/m2/a (Meteonorm 6.1). Even taking into account that there are majoruncertainties with both measurements there is still a vast difference. Thus, aggregated valuesare not a good indicator to identify potential for SHIPc.

2.2. Collection of solar energy with linear Fresnel collectorsThe principle of LFC13 is to concentrate the sunlight on an absorber tube that is fixed abovethe collector field. However, unlike in parabolic trough collectors (PTC), this is done by severallinearly aligned reflectors (see Figure 1), each with a characteristic curvature.

Figure 1: Model of a linear Fresnel collector (Industrial Solar GmbH)

Like all concentrating solar collectors LFC can only use direct irradiation. LFC have twocharacteristic planes – the longitudinal plane standing vertically on the collector field andrunning parallel to the absorber and the transversal plane standing vertically on the collectorfield but crossing it (see Figure 2). The three crucial angles in a LFC are defined in Table 2.

Table 2: Characteristic angles in linear fresnel collectors

Angle DefinitionθT The transversal angle between the z-axis and the pro-jection of the solar position in the transversal plane.

θT = arctan(| sin(γ)| tan(θZ))

θL The longitudinal angle between the z-axis and theprojection of the solar position in the longitudinal plane.

θL = arctan(cos(γ) tan(θZ))

θI The incidence angle between the solar position andthe transversal plane.

θI = arctan(cos(γ) sin(θZ))

13The name of this technology dates back to Augustin-Jean Fresnel (1788 – 1827). First demonstrations weredone by Giovanni Francia (1911-1980) in Italy.

12

Figure 2: Crucial planes in linear Fresnel collectors (Mertins, 2009)

TrackingSince the absorber is fixed above the collector field all reflectors have a different inclinationtowards the sun. The inclination angle ϕpr (Equation 1) of the primary receivers depends onthe horizontal (Xpr) and vertical distance (Hrc+Z) from the absorber as well as on the transversalangle θT. All mirrors turn with the same angular speed (15◦/ h) and can be operated by a singlemotor. However, they are commonly operated individually or in smaller groups for reasons ofcontrolling and to avoid a complete break down.

ϕpr =θT − arctan( Xpr

Hrc+Z)

2(1)

2.2.1. Optical and thermal analysis

Optical effectsIn LFC the primary reflectors are slightly bend in order to focus the radiation on the absorber.Thus, radiation parallel to the main axis of the reflectors causes a single focal line. However,since the mirrors are not normal14 to the incoming radiation LFC always suffer from an astigma-tism (Mertins, 2009) (see Figure 3), which reduces efficiency. Moreover, further effects reducethe optical efficiency (ηth).

• Cosine losses due to low positions of the sun14If the central mirror is normal to the incoming radiation it is in the shade of the secondary reflector.

13

Figure 3: Astigamatism in linear Fresnel collectors (Mertins, 2009)

• Shading due to absorber, structure or secondary reflector

• Occultation of reflected radiation at the back of other mirrors

• Line end losses when the reflection misses the absorber in the longitudinal axis

• Optical errors due to material, construction or tracking

• Absorption of radiation in the primary / secondary reflector or the outer absorber skin

The optical efficiency ηopt takes all theses effects into accounts and sets the thermal outputin relation to the incoming energy. Since the reflectors change their position to the sun theaperture area is not constant in LFC. Thus, the area of the primary receiver Apr is used as inEquation 2.

ηopt =q

GbApr(2)

Effects of orientationThe yield of LFC depend on their orientation, whereas north – south orientated collectors havehigher yields over the year (roughly 5 - 8 %) while east – west orientated collectors have longeroperating hours and thereby higher yields in winter times. For the application in industry bothorientations have advantages (see Section 2.3.3) and thus orientation is not a decisive factor.Two exemplary yield profiles are shown in Figure 4.

Thermal effectsThe energy yield of solar thermal collectors can be approximated by Equation 3. Concentratingcollectors bundle the radiation on the absorber in order to achieve higher temperatures (T) ofthe heat fluid. The concentration ratio (CR) is defined as the ratio of the aperture (Aap) to

14

.....

Jan

.

Feb

.

Mar

.

Apr

.

May

.

Jun

.

Jul

.

Aug

.

Sep

.

Oct

.

Nov

.

Dec

.

Year

.

0

.

5

.

10

.

averageyields

inMW

th/da

y

.

. ..North – South . ..East – West

Figure 4: Monthly average daily yields of a collector with 2816 m2 apperture area in Korba, Tunisia(DNI 1898 W/m2) (data: Meteonorm 6.1, simulation: Industrial Solar GmbH)

the absorber area (Aabs), CR =AapAabs

. It is ultimately limited by the relation of the sun to theearth15. Heat losses depend on the temperatur difference between the heat fluid (T) and theambient temperature (Ta).

qth = ηoptGb −Aap

Aabs[ϵσ(T 4 − T a

4) + α(T − T a)] (3)

The collected energy ηopt ∗ Gb is reduced by thermal losses due to convection and radiation.Both effects depend on the operating temperature of the system and the specific materialproperties (emissivity, conductivity). With higher temperature differences or lower irradiationthe collector efficiency ηcol drops, as can be seen in Figure 5.

2.2.2. Components of linear Fresnel collectors

For the primary reflectors of LFC flat mirrors can be used, which are bended mechanically.This is possible due to the comparatively large distance of the primary reflector to the absorberand can drive down the costs. The collector field is defined by the number of primary receivers,their width and length as well as the distance between the reflectors. The glass of the mirrorsshould be thin and with a low iron content to reduce absorption16. At the same time, the glassand the reflective layer have to withstand harsh environmental conditions.In LFC secondary reflectors are used since not all the reflected radiation hits the absorber15CRmax (2 dimensional) = 212 whereas CRmax(3 dimensional) = 45,033. Commercial LFCs have a CR ≈ 3016Flabeg specifications for flat mirrors for CSP: thickness 0.95 mm – 4 mm, minimal reflectivity 93.5 % – 95 %

15

... ..0

.100

.200

.300

.400

.500

.0 .

20

.

40

.

60

.

temperature difference (T - Ta) in ◦K

.

ηth

in%

.

. ..200 W/m2 . ..400 W/m2 . ..800 W/m2 . ..1000 W/m2

Figure 5: Thermal efficiency of LFC (aperture width = 26 m, ηopt = 0.669) (Mertins, 2009)

directly. Thereby more reflectors can be installed per receiver. Furthermore, the secondaryreflector reduces convection losses at the absorber.The absorber pipe collects the incoming radiation and conveys it to the heat carrier. There-fore, its selective coating should have a low emittance and high absorptance17. Moreover, it hasto withstand high temperatures. Sometimes the absorber pipe is protected with a glass coverfrom below. In other installations vacuumised tubes are used as in PTC. In order to avoidclogging only treated water can be used.

2.2.3. Specific advantages of linear Fresnel collectors

The selection of the optimal solar thermal collector depends on the intended application, mainlyprocess temperature. LFC are suitable for medium temperatures (100◦C – 400◦C). Below themajor advantages of LFC are listed, following a study on the Solarmundo project (Häberleet al., 2002). Most of them have to be understood in comparison to PTC.

• The usage of flat mirrors offers great potential for cost reduction (Kalogirou, 2004),(Häberle et al., 2002).

• Low wind-loads reduce breaking of mirrors and reduce costs for motors and gears (Morinet al., 2006).

• LFC can have lower investment cost and longer life time since no flexible high pressurejoints are needed like in PTC (Häberle et al., 2002).

17Specifications of Schott PTR® 70: emittance ≤ 10 % and absorptance of ≥ 95 %

16

• Higher land use efficiency compared to PTC since collector field can be more densilypacked (Häberle et al., 2002).

• Low operation and maintenance cost due to easy access and cleaning (Häberle et al.,2002), (Morin et al., 2012).

• Multiple land use since collectors can be installed on rooftops (Häberle et al., 2002).

• Advantages in direct steam generation (DSG) since most radiation hits absorber frombelow.

However, also PTC have major advantages. They can achieve even higher temperatures dueto greater concentration and there is much more experience in the operation. Which technologyis most suitable for a specific application has to be seen case by case, nevertheless for SHIPc

there are several advantages of LFC.

2.2.4. Cost and yields of linear Fresnel collectors

Even tough PTC is the dominant technology for concentrated solar energy in the last yearsmore companies started to work on LFC18. Despite the same operating principle the designsof the systems differ. For electricity generation LFC are usually bigger (greater CR to reachhigher temperatures). Moreover, costs depend on system size as shown in Figure 6.

..... 0.

200

.

400

.

600

.

800

.

1,000

.0.5 MW

.1 MW

.10 MW

.

Capacity

.

Costs

perm

2

Figure 6: Cost function of linear Fresnel collectors (Industrial Solar GmbH)

18For example Areva (France), CNIM (France), Fera (Italy), Ferrostaal (Germany), Novatec Solar (Germany),Solar Power Group (Germany), Soltigua (Italy)

17

In an attempt to compare the break even of LFC with PTC for electricity generation Morinet al. found that ”little cost data for commercial LFC is published today” (Morin et al., 2012).Apart from the uncertainties of absolute prices, projects below a certain size (e.g. 1 MW) arenot reasonable due to the cost structure. At the same time, bigger projects become increasinglyeconomical. The reason for the great drop in prices is the high amount for fixed costs (pumps,control, planning). To compare prices with other technologies it is important to use the correctvariable, for energy it is usually the CSHG (see Section 2.4). Total installation costs of projectsare misleading since they also include costs for the power block, an absorption chiller or steamstorage. Also the costs per m2 for SHIPc can not compared directly with costs of power plantssince the later are usually of a size of 50 MW and above.

Yields of Linear Fresnel CollectorsDue to the course of the sun and the various impacts on DNI (see Section 2.1) the yields ofLFC vary during the day and over the year. The objectives, when applying SHIP, are low costsper solar generated thermal energy (CSHG) and a reasonable internal rate of return (IRR).Therefore, the solar share should be high and wastes at peak times reduced. Average monthlyyields of a collector are shown in Figure 4, Figure 7 shows some exemplary daily productioncurves.

... ..5

.6

.7

.8

.9

.10

.11

.12

.13

.14

.15

.16

.17

.18

.19

.0 .

500

.

1,000

.

1,500

.

Hour of the day

.

Powe

rin

kWth

.

. ..Summar day (north - south) . ..Summer day (east - west)

. ..Spring day (north - south) . ..Spring day (east - west)

. ..Winter day (north - south) . ..Winter day (east - west)

Figure 7: Daily yield profile of a collector with 2816 m2 apperture area in Korba, Tunisia(DNI 1898 W/m2) (data: Meteonorm 6.1, simulation: Industrial Solar GmbH)

18

2.3. Integration of solar heat in industrial processesApart from the general challenges of solar energy a major obstacle for SHIP is the integrationin industrial processes. For industry a reliable supply of energy at constant specifications(pressure, temperature) is crucial. Even short disruptions within the production process cancause great losses. A fossil fired back-up boiler is always available. The integration of SHIPc

depends on the demands of the specific processes (e.g. heat carrier), the circumstances at thesite (e.g. area for installations), the current energy supply system (e.g. centralized system) andthe load. Moreover, due to their fluctuations at least some storage is beneficial for application.Complex integration can drive up the costs substantially in both design and investment. Asplanning and know how were already identified as major obstacles for SHIP in Europe (ESTIF,2006) this will be even more severe in MENA. In order to identify suitable applications forSHIPc in MENA, integration has to be taken into account. This chapter briefly describes themain concepts.

2.3.1. Basic concepts for integration

Process or system level integrationIn most industrial installations with thermal energy demand at higher temperatures there is acentral steam supply (companies with parallel supply of steam and hot water are not consideredhere). For the integration of solar thermal energy there are three different possibilities, (i) steamgeneration on the system level, (ii) direct coupling to a specific process and (iii) pre-heating ofboiler fed water, as shown in Figure 8.

Figure 8: Integration of solar collectors in processes (Schweiger et al., 2001)

19

The later is not considered since it is rather suitable for low temperature collectors. Froman energetic point of view it is reasonable to provide the processes directly with heat at theneeded temperature. This is repeatedly stressed in the studies on SHIP.

”... one should look at the actual temperature needed by the process itself andnot at the temperature of the heat carrier being used...”(Vannoni et al., 2008)

This statement holds on a macro level. When heat is generated at higher temperatures thanneeded at the process energy is wasted (thermal losses increase with the temperature differenceT - Ta). However, the situation differs from the perspective of the individual firm. First, heav-ing only one central heat supply at the maximum temperature is easier than running variouscircuits. Second, supplying heat at temperatures well above the actual process reduces themass flow rate as well as the dimensions of the heat exchangers and thereby investment costs.Third, if the process is running already or will be changed in the future there might be spaceconstraints which undermine the installation of additional equipment (or larger hat exchang-ers). Forth, various different cycles make the system more complex. Finally, a centralized andstandardized system is also more flexible for changes within the facility over time. Yet, if theheat is supplied centrally the system is dominated by the process with the highest temperaturesand thermal losses increase. Schweiger et all. assessed whether integration on the system levelis possible and found that ”in almost all industries, the coupling of the solar system to thecentral heat supply system is possible” (Schweiger et al., 2001). Nevertheless, when a processhas large energy requirements at low temperatures it might well be reasonable to take it off thecentral system and supply the energy efficiently at low temperatures.

Direct steam generation or heat fluidConcentrating solar collectors are capable to achieve temperatures high enough for steam gen-eration. Yet, while steam is difficult to handle, high temperatures (e.g. up to 200◦C) can alsobe achieved with pressurized water. Adding a blend to the water can further increase the evap-oration temperature. In industry steam is a common heat carrier, thus efficient direct steamgeneration (DSG) is very beneficial for SHIPc. It reduces investment costs (heat exchanger,thermo-oil) and the use of environmental harmful substances. The three solar steam generationconcepts are listed below (Kalogirou, 2009).

• steam-flash – Pressurized water is circulated through the collector and afterwards flashedto steam. In order to prevent evaporation high pressures are needed in the system.Moreover, temperature differences to the ambient are higher since there is only sensibleheat. The higher temperatures also increase thermal losses.

20

• direct steam – A two phase flow circulates in the collector. It needs less energy for pumpingand the thermal losses are also reduced. However, air bubbles can cause flow instabilitiesand high local temperature / pressure gradients which increase material stresses. Alsothe operation becomes more difficult, especially in large collector fields.

• indirect steam – A heat fluid is circulated through collector while steam is generatedusing a heat exchanger. While this concept is comparatively easy to operate the heatexchanger and fluid increase the investment costs. Moreover, thermo-oils have otherinherent deficits. They are often toxic and easy flammable, especially when startingdecomposition. Furthermore, they have poorer heat transfer characteristics than water.Thus, higher flow rates and temperature differences are necessary which decrease overallefficiency.

Direct steam generation has a great potential since it increases efficiency and reduces invest-ment costs (no heat exchanger or thermo-oil), yet the technique is still in its infancy. On thepower plant level there is a research project in Almeria, for SHIPc there is a pilot project in aGerman aluminium factory (Dunst, 2011).

Open or Closed SystemsThe differentiation between open and closed systems refers more to low temperature collectors(especially for air) but is mentioned here for completeness. Within open systems the heatcarrier is released to the process (e.g. in drying). For wet systems one application could bewashing. In SHIPc this is not reasonable due to high thermal energy losses. Moreover, in mostapplications and locations the water for the collectors need purification, which is also energyintensive.

2.3.2. Storage

Fluctuations over seconds to seasons are an intrinsic feature of solar energy. At the same timealso industrial production varies (e.g. batches). Fitting supply to demand is a major challengefor SHIP which can be eased by applying storage systems. Moreover, in hybrid systems (solarand fossil) it can allow the boiler to run at optimal efficiency. Compared to electricity, heat iscomparatively easy to store. Nevertheless in practice an appropriate storage system can driveup the costs of a SHIP installation substantially. Figure 9 provides an overview of the variousheat storage concepts following Fisch (Fisch et al., 2005).

21

heat storage system

thermal storage

sensible heat

liquid solid

latent heat

solid – liquid liquid – gaseous

chemical storage

reaction heat

Figure 9: Thermal storage concepts (Fisch et al., 2005)

In direct storage the heat carrier is stored directly while in indirect storage the heat is storedin a separate medium. Steam accumulators (see Figure 10) are well suited for short storagetimes. They are charged by raising the temperature in a pressurized vessel and discharged byreleasing steam with lowering the pressure. By their very nature, steam characteristics changesince there is a pressure drop while releasing - this can further complicate the integration in anindustrial process if the steam is needed in a narrow temperature range.

Figure 10: Steam accumulator (Steinmann and Eck, 2005)

The latent heat concept overcomes this problem by applying phase change materials. Therebylarge amounts of energy can be stored at constant temperatures (Hirn and Mexer, 2011), andsteam at constant characteristics can be released. For temperatures with several hundreddegrees alkaline salt systems are used. However, today all the storage systems are still veryexpensive. All storage systems drive up investment costs. Thus, it is reasonable to identify

22

applications where no storage is necessary. Smaller amounts of heat can often be stored in aprocess - e.g. heating a bath or in the boiler. For solar cooling hot water tanks are sufficientwhich are much cheaper compared to steam storage systems. Moreover, for industry cold roomscan also be used as a storage to a certain degree if the temperature can be lowered beyondthe normal operation point. Even though storage is a crucial issue for extensive application ofSHIP today there is still large potential where no storage is needed.

2.3.3. Further effects

Orientation of the solar field As was shown in Figure 4 the orientation of the collectorfield effects the annual yield. Thus, for concentrating systems the orientation is already acrucial question in system integration. If the solar field is oriented east – west, the annualyyield is lower compared to north – south, but the yields in winter are higher. In respect tothe integration, especially if a process is fed directly, there can be good reasons to install east– west. This question was discussed on an actual plant in Switzerland (Marty and Frank, 2011).

Effects of a solar field on the boiler efficiencyEven though, with a sufficient big storage, a solar only production is technically possible thisis not feasible. The realistic option for the integration of SHIPc is to operate as a fuel saver,where the conventional boiler produces steam during the night and when the irradiation isinsufficient. The boiler efficiency depends inter alia on the flue gas temperature and stacklosses, radiation and convection losses, the air-fuel ratio and the operating conditions (∆T).Moreover, when comparing boilers it is also important to consider their operation principle19.If a boiler operates at a lower capacity the absolute thermal losses remain constant and raiserelative to the steam produced. Also, if the boiler has to be turned on and off more oftenthis reduces the overall efficiency. Thus, integrating SHIPc can reduce boiler efficiency. Atthe same time, in large industries with several boilers efficiency might be raised if one boilercan be switched of completely. It is not possible to define the impacts of the integration of asolar field on a boiler in general, however, they can be severe and have to be taken into account.

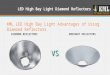

Boiler conceptsThere are mainly two different types of boiler in industry. In fire-tube boilers (see Figure 11),the predominant type, the exhaust gases are circulated several times through a large vesselfilled with water at the bottom and steam at the top. In high speed steam generators, water iscirculated in a coil which is placed in the flame (see Figure 12). The mere presence of different19For example, condensing water boilers have by their operation principle a higher efficiency.

23

Figure 11: Fire-tube boiler (Viessmann GmbH,2010) Figure 12: High speed steam generator

(Spirax Sarco, 2011)

concepts shows that neither is superior. Also in respect to the integration of SHIPc both havespecific strengths and weaknesses which are summarized in Table 3.

Table 3: Comparison of boiler concept (Spirax Sarco, 2011)

Fire-tube boilers High speed steam generatorsAdvantages: Advantages:+ easy to connect several boilers + smaller investment+ dry steam + little area+ integrated storage + can be installed everywhere

+ less water treatment necessaryDisadvantages: Disadvantages:- high investment - wet steam- large secured area needed - no constant pressure- trained staff necessary - maintenance intensive pump- long heat up time - losses in start up

Poly-generationA measure which is commonly proposed to increase energy efficiency is poly-generation, theproduction of two or more useful outputs (see Table 4). In industry the potential for poly-generation is very high due to the demand of various types of energy (mechanical, electrical,thermal). Poly-generation has environmental and economic advantages. First, it reduces fuelconsumption by making use of waste heat. Second, it allows to optimize output for prices - for

24

Table 4: Outputs in poly-generation at various temperature levels

Temperature level Process250◦C – 400◦C electricity generation in conventional steam turbine

electricity generation in organic Rankine cycleindustrial process heat

100◦C – 250◦C industrial process heatsea water desalination with multi-effect distillationmulti-stage absorption chillerregeneration of steam after turbine

40◦C – 100◦C industrial process heatsingle-stage absorption chillerdistrict heating

example to produce electricity only during peak hours. Third, energy can be stored in the easiestform. Yet, at the same time there are also inherent disadvantages. It increases the investmentcosts and if the fuel (solar energy) is constrained the machines can not run under full capacitysimultaneously. Moreover, installations become much more complex - both for planning andoperation. For industrial purposes the combined use of heat and cooling is especially reasonablesince chillers are often run by expensive electricity. Yet, of course poly-generation can also beapplied with conventional fuel fired boilers.

2.4. Tools for financial analysisFor assessing and comparing the situation in companies energy yields have to be transferredin monetary units. Within this part major approaches for investment appraisal are discussed,later further financial tools are introduced.

2.4.1. Investment appraisal

For assessing whether an investment in SHIP is reasonable a financial analysis has to be done.This section presents the major dynamic20 approaches for investment appraisal, and brieflytouches on their underlying assumptions as well as inherent strengths and weaknesses. This isnecessary, since within the literature on accounting there is no unanimity (Hering, 2008). Thethree approaches are (i) capital value method, (ii) annuity method and the (iii) internal rate ofreturn (IRR) (Kruschwitz, 2011). Since the first two bring the same investment decision the

20Static approaches do not respect the time when a cash flow occurs and are thus not considered here.

25

annuity method is not discussed.For the net present value (NPV), a capital value method, all cash flows are discounted totime t = 0. An investment should be realized if the NPV is positive and higher than all otheralternatives. It can be calculated with Equation (4), whereas LT is the the lifetime, t a specificyear, r the discounting factor and CF the cash flow (returns – expenditures).

NPV =LT∑t=1

CFt

(1 + r)t(4)

The major problem of the NPV is to select an appropriate discount rate r. Often the interestrate is used under the rigid assumption of a perfect and unrestricted21 capital market (Götzeet al., 2008). The major advantages of the NPV are that it is an absolute evaluation and allowsa straight forward interpretation (Crundwell, 2008).The internal rate of return is another investment appraisal method. The basic approach isto ask, under which discount rate the NPV becomes 0, as shown in Equation (5).

IRR = {r | NPV =LT∑t=1

CFt

(1 + r)t!= 0} (5)

The IRR is highly controversial and some textbooks argue to abandon it completely due to itsinherent deficiencies (Kruschwitz, 2011). First, the equation to find the IRR can not directlybe solved22. Second, and more important, it is only a relative measure23. The most criticalissue, however, refers to the re-investment. The IRR can not be used to calculate the final valueafter the projects lifetime. This would imply, that ”financial investments yielding the IRR canbe made without limit. This assumption is often unrealistic, because IRR reflects cash flowsof the investment under consideration and not the opportunities in the capital market” (Götzeet al., 2008)24. For investments in SHIPc, with long lifetimes and increasing cash flows thisassumption is especially unrealistic.The modified internal rate of return (IRRM) is a variation of the IRR where the cash flowsare not reinvested with the IRR, but with the interest rate at the capital market (ibar). It can

21Perfect: debt rate = credit rate; unrestricted: money can always be invested and borrowed22There can be none, one, or several mathematical solutions.23If there are two investments, A and B, with the following cash flows A:(-1, 10) and B: (-100, 200) A has a

higher IRR even though most investors would favour B.24An investment will only be realized if the expected IRR is above the interest rate at the market. If there

is the possibility to invest with the same interest rate at the capital market there is no reason to take theinvestment risk at all.

26

be calculated with Equation (6).

IRRM = (1 + ibar) ∗LT

√√√√∑LTt=0

(CFt)(1+r)t

CINV

+ 1− 1 (6)

A complete discussion whether this assumption is completely suitable for investments in SHIPc

can not be done here. Since the Verband Deutscher Ingenierure25 (VDI) proposes this approachfor large solar thermal systems (VDI, 2011) the IRRM is used in the financial analysis below.

2.4.2. Further financial tools

Apart from the methods mentioned above other financial tools can provide further information.The payback period (PP), or amortization time, provides the time until an investment is paidback. It is not an indicator of the profitability of an investment and should only be used inaddition to other methods. For investments with long life time, like in RE, it is importantto use a dynamic amortization where cash flows vary over time. The PP can be found withEquation (7)

PP = min{t | NPV (t) = −CINV +LT∑t=1

CFt

(1 + r)t} (7)

As described above the PP is not an indicator about the profitability of investments. Neverthe-less, a study by the German Ministry of Environment found that 80 % of the assessed Germancompanies use the PP as an investment criteria (Jochem et al., 2008). This is a systemic biasagainst projects with long life times, even if they are highly profitable and especially impedesinvestments in RE.The costs for solar heat generation (CSHG) provide the costs per unit of solar generatedthermal energy, including the pay back of the investment over the lifetime. They can becalculated with Equation (8) (VDI, 2011). The investment costs (CINV) are the total instal-lation costs (including piping etc.) subtracted by subsidies. The operation and maintenancecosts (CO&M) are for labour and material, whereas the consumption costs (CCons) are the costsfor the electricity consumed by the installation. For large installations it is suggested to useCCons = CkWh(el)/50 (VDI, 2011). Qsol is the annual energy yield. The annuity factor (fa) canbe found with Equation (9) (VDI, 2011). However, it has to be considered that the CSHG riseover the lifetime due to increasing costs for O&M and electricity.

CSHG =CINV ∗ fa + CO&M

Qsol

+ CCons (8)

25German Engineer Association

27

fa =(1 + ibar)

LT ∗ ibar(1 + ibar)LT − 1

(9)

The Greenhouse gas abatement costs, see Equation (10), (McKinsey, 2009) are an im-portant tool to compare different investments. They express the additional costs which arenecessary to reduce the emission of CO2eq. Thus, they are rather used by policy makers tocompare efficiency of environmental investments, for example whether to invest in CSP, inSHIP or in forestation26. For the calculation of abatements costs the NPVs of an investmentand an alternative (base case) have to be compared. However, this is restricted to direct finan-cial costs. Indirect benefits like the creation of jobs, or the reduction of electrical peak loadsthrough solar cooling are commonly not included even though they also have great influenceon policy making.

Abatement costs = (Full costs of CO2eq efficient alternative)− (Full costs of reference solution)(CO2eq from reference solution)− ( CO2eq from efficient alternative)

(10)

A sensitivity analysis (SA) can help to deal with uncertainties. Investments in RE arecharacterized by high front up costs and when estimating the feasibility major uncertaintiescan not be avoided, for example the development of fossil fuel prices. A SA asks ”what if”questions and allows to assess the impact of varying factors and on a model. It is done in fourmajor steps (Kruschwitz, 2011).

1. Selection of uncertain input factors and output function

2. Formulation of a mathematical model of the output function

3. Definition of an interval of variation

4. Analytical determination of the intervals of the output function for each input factor

From the perspective of an investor the objective of a SA is not no identify the factors withthe largest absolute impact, but rather the ones with the largest impact within an appropriateinterval27. In Section 5.1 the IRRM as well as the CSHG are examined as objective functionsin a single varying input analysis. Afterwards, the two most important factors are variedsimultaneously in respect to the IRRM.26McKinsey published various national and international reports comparing abatement measures (McKinsey,

2009)27The collector efficiency as well as the CAAGR of fossil fuels are unknown, however, in estimating the latter

there is much more uncertainty.

28

Summing up, the following was found. First, there are a variety of assessment tools whichdiffer in their assumptions and approaches. Thus, also the evaluation of SHIP depends on thechoice of the appraisal tool. Second, companies often base their investment decisions on thePP (Jochem et al., 2008), a method which is not suitable for evaluation and which systemicallybias RE investments.

29

3. Top down approach - energy situation in Middle East andNorth Africa

This chapter discusses the energy supply and demand in MENA, and the potential for RE.Afterwards the potential for SHIPc in MENA is assessed and suitable sectors identified. In theend, the major challenges for SHIP are mentioned.

3.1. Energy supply and demandEnergy demand and CO2 emissions in MENA are growing strongly for the last two decades asshown in Table 5. According to the IEA the total primary energy demand (TPED) in MENAgrew from 378 Mtoe in 2000 to 546 Mtoe28 in 2007 and is expected to raise to 1030 Mtoe in2030 (IEA, 2009). The main drivers are growth of the population29 (World Bank, 2011b) andthe gross domestic product (GDP)30.

Table 5: Energy demand and CO2 emissions in MENA (IEA, 2009)

Indicator Unit 1990 2007 2030 CAAGR in %(2007–2030)

TPED Mtoe 220 546 1030 2.8CO2 emissions Mt 588 1375 2495 2.6

The rising energy consumption poses great challenges on the countries. In addition to theones mentioned in Section 1 there are two more severe issues in MENA. Many governmentssupport energy consumption by subsidies. In times of rising energy prices this is an increasingburden on governmental budgets. Moreover, in some countries there are temporal or regionalenergy shortages (fuel, electricity at peak times) with high economic costs. Thus, the energychallenge is severe in MENA, but differs between the countries. Some MENA countries haveabundant fossil fuels and can continue their current extraction for more than 100 years31. Inothers resources are expected to deplete within the next two decades. In many countries thepoor can not afford rising energy prices and the the energy situation thereby also increases therisk of social unrest. It is clear that major changes are necessary to achieve social, economicand environmental sustainability of the energy system in MENA. Following an approach for the

28Not exactly the same countries are covered as in this study.29The CAAGR for population in MENA between 2000 and 2010 is 2 %.30The CAAGR for the GDP in MENA between 2000 and 2007 is 5 %.31Exact predictions are not possible, especially since with raising prices new extraction methods become feasible.

30

Clean Development Mechanism (CDM) (Sutter, 2003) dimensions of sustainability are depictedin Table 6. All challenges mentioned above can be overcome by RE in the mid term. Whereasthe break even point of different RE varies, they all become cheaper while fossil fuels rise.

Table 6: Sustainability criteria (Sutter, 2003)

Energy demandSocial Development Environmental Development Economic DevelopmentStakeholder participation Fossil energy resources Technology transferImproved services Land resources Regional economyCapacity development Air quality Microeconomic efficiencyEqual distribution Water quality Employment generation

3.2. Potential for renewable energiesEven though RE only play a minor role today, the MENA region has great resources for windand solar energy. The MED-CSP study (Trieb et al., 2005) assessed the potential for varioustechnologies and found that MENA can not only satisfy all its energy demand with RE buteven generate income by the export of clean energy. The Red Sea for example belongs to themost promising regions for wind power in the world. Currently hydro power still accountsfor the largest share of RE in MENA32 while solar energy has by far the largest potential.Still, only a well balanced mix of technologies can ensure a sustainable energy supply33. In theappendix (E) there is an overview over the total economic potential for the various technologiesin the MENA region. This study focuses solely on LFC for SHIPc, whereas the DLR studiedpower generation with concentrating technologies (Trieb et al., 2005). They estimated thetotal economic potential (defined as those areas with a DNI of more than 2,000 kWh/m2/a)as 632,099 TWhel/a. Even though this number can not be transferred directly it indicates thepotential.

3.3. Overview of countries and selection for bottom up assessmentSo far MENA was described on an aggregated level. However, the countries are extremelyheterogeneous in resource endowments and economic development. While Qatar has one of thehighest GDP per capita in the world (29,460 US$), Yemen belongs to the poorest (558 US$).

32For example the Aswan dam in Egypt with a capacity of 2.1GW33In additon to Table 6 grid stability is also of major importance.

31

Some countries (e.g. Kuwait) export 5 times more energy than they consume while others (e.g.Morocco) can only satisfy 4 % of their demand by local production. Table 7 below provides anoverview of relevant energy and socio-economic indicators. Within Appendix E more detailsare given for each country. The solar resource is very high for all MENA countries and the CSPperformance indicator (see Section 2.1) is used for comparison. The same index was also used tocalculate the ”annual earnings per m2”34. The results are aggregated on a national level and cannot be used to predict a specific site due to DNI variances within the countries. Nevertheless,the ”annual earnings per m2” are an indicator combining solar resource and energy costs whichcan be used for a ranking. The resource to production ratio (R/P) gives the remaining time inyears under which resources are available under the current rate of exploitation. Within thisanalysis coal is not considered since it has a minor role in MENA and in industry especially.It is important to stress that there are more crucial variables, especially institutions for thesupport of RE. They are not included in the top-down analysis but will be mentioned later oncountry level. Various criteria exist to identify promising countries. On the one hand countrieswith high energy prices and little resources have the greatest need for RE. On the other hand,resource rich countries with high GDP per capita can more easily afford to shift their energysupply system or realize pilot projects. For the present analysis focus was on high energy(diesel) prices35, a reasonable DNI and a sufficient size of industry (population and GDP percapita). Based on these criteria the following two countries are identified.

• Morocco; (diesel = 0.83 US$ / liter, Production / TPES < 5 %)

• Tunisia; (diesel = 0.84 US$ /liter, Production / TPES < 85 %)

3.4. Industrial heat demandSince there are no detailed studies on industrial energy demand in MENA and the structure ofindustrial energy demand (relative distribution of energy forms, temperatures etc.) is expectedto be similar between regions this section is based on European and German data. It is assumedthat the results can be reasonably transferred to MENA37. According to Eurostat (see Figure13) the industry accounts for 27 % of total energy demand. This demand can further be34How much money would have to be spent on diesel to obtain the same amount of energy as can be harvested

annually per m2. Prices for heating oil would be better for industry, however, data was not available.35Diesel prices are used since there is no source on heating oil prices for industry.36The cost for diesel necessary to obtain the same amount of energy per m2 with an assumed efficiency of 40

%. Diesel prices were used instead of heavy fuel oil costs in order to have consistent data for all countriesfor the same year.

37Despite differences, for example in efficiency, industrial energy demand is determined by the technical process.

32

Table 7: Crucial indicators for country selection

Country Popu

latio

nin

million

GDP

incurrentbillion

US$

GDP

/capita

incurrentUS$

Indu

stry

as%

ofGDP

CSP

perfo

rman

ceindicator

Prod

uctio

n/TPE

Sin

%

R/P

ratio

oilinyears

R/P

ratio

gasin

years

Dieselp

ricein

US$

annu

alearnings

perm

2ine

36

Algeria 35.5 159 4,495 62 2,700 437 18 55 0.2 27Bahrain 1.2 20.6 17,606 n.a. 2,050 189 7 n.a. 0.13 13.3Egypt 81.1 219 2,699 38 2,800 123 16 35 0.2 28Jordan 6.1 27.6 4,557 33 2,700 4 n.a. n.a. 0.61 82.3Kuwait 2.6 109.5 41,463 n.a. 2,100 581 >100 >100 0.2 21Lebanon 4.2 39.2 9,262 21 2,000 4 n.a. n.a. 0.76 76Lybia 6.4 62.4 9,805 78 2,700 569 73 100 0.12 16.2Morocco 31.9 91.2 2,802 30 2,600 4 n.a. n.a. 0.83 107.9Oman 2.7 46.9 17,293 n.a. 2,200 386 19 40 0.38 41.8Qatar 1.6 98.3 61,445 n.a. 2,000 517 55 >100 0.19 19Saudi Arabia 27.5 434.7 15,834 70 2,500 358 75 >100 0.09 11.3Syria 20.5 59.1 2,891 35 2,200 119 18 49 0.53 58.3Tunisia 10.5 44.3 4,199 32 2,400 82 n.a. n.a. 0.84 100.8Turkey 72.8 735.3 10,106 28 2,000 29 n.a. n.a. 1.62 162UAE 6.9 230.3 33,183 61 2,200 309 >100 >100 0.62 68.2Yemen 23.3 26.4 1,130 n.a. 2,200 203 25 >100 0.17 18.7

divided into the various forms of energy, whereas process heat has the largest share. Therelative distribution for Germany is shown in Figure 14. The relative heat demand differsbetween industries whereas the iron and steel, as well as the chemical sector have the highestenergy demand as shown in Figure 15. Due to high temperatures of sometimes more than800◦C the iron and steel, as well as glass industry can not be covered with LFC.

33

...

Transport

.32%..

Industry

.27% ..

Services & households

.

41%

Figure 13: Energy consumption in different sectors (Eurostat, 2011)

...

Mechanical energy

.23%

..

HVAC & warm water

.

10%

..

Process heat

.64%

..Lightning & IT

. 3%

Figure 14: Industrial energy demand in Germany (BMWi, 2011), IT = information technology;HVAC = heating, ventilation and air conditioning

... ..1998

.2000

.2002

.2004

.2006

.2008

.

20

.

40

.

60

.

Year

.

Mtoe

.

. ..Iron & steel . ..Chemical . ..Textile & leather . ..Glass

. ..Paper & printing . ..Food & tobacco . ..Engineering & other metal . ..Other

Figure 15: Final energy consumption of industrial sectors in Europe (Eurostat, 2010)

34

In the chemical sector processes covers a very broad temperature range, thus, the sector cannot be classified at whole. For the next step of the analysis temperature levels will be introduced.Afterwards industry can be classified according to the temperature of their dominant heatdemand. The exact limits are somewhat arbitrary, here the levels of the Ecoheatcool study(Ecoheatcool and Euroheat and Power, 2006) (Ecoheatcool2006) will be used. Their relativeshares are shown in Figure 16.

...

> 400◦C

.43%..

< 100◦C

.30%

..

100◦C – 400◦C

.

27%

Figure 16: Temperature distribution for European industry (Ecoheatcool and Euroheat and Power,2006)

Of course, most industries have processes at different temperatures. Within this analysis thefocus is on SHIPc with LFC. As shown above they are reasonable at medium temperatures.Nevertheless, for calculating the potential of SHIPc both segments, <100◦C and 100◦C – 400◦Care added. Even in companies where all processes are below 100◦C steam is a common heatcarrier. Furthermore, in companies with several processes the temperature of a central steamsupply is determined by the highest temperature. On the other hand, if the demand of hightemperatures is great, the potential is reduced since waste heat can be recovered easily.

3.5. Solar process heat at medium temperatures in Middle East andNorth Africa

When transferring the data of industrial energy consumption from Germany and Europe toMENA there are two major mistakes. First, industry is not equally distributed (not all countrieshave heavy industries). Second, energy efficiency is much higher in Europe. Nevertheless, forthe objective of this study the results can be transferred. According to the IEA the MENAcountries (all 16 mentioned above) had an industrial energy demand of 1,263 TWh in 2009(IEA, 2011). Assuming that 64 % is process heat, of which 57 % is in the range up to 400◦Cthe total demand is around 460 TWh. Even when only a fraction of this amount can be covered

35

by LFC (due to temperature) the potential is huge. Reiners used a more sophisticated approachbased on production and employment data. He estimated the total demand for process heat(up to 250◦C) in the Mediterranean38 to be in the range of 325 to 373 TWh (Reiners, 2011).

3.6. Suitable sectors for process heat generation at medium temperaturesAs explained in Section 3 the medium temperature range (100◦C – 400◦C) is promising forSHIPc with concentrating solar technologies like LFC. Below some sectors, where a large frac-tion for their process heat demand is in the medium level, are described, namely: (i) food andbeverages, (ii) textile and (iii) plastic and chemical. Furthermore, solar cooling is another in-teresting application. Of course there is also potential in other sectors. For example paper andpulp industry with temperatures of 120 – 150◦C is often mentioned as suitable. However, it isexcluded from a more detailed analysis for two reasons. First, it is characterized by very largefacilities which often generate their own electricity and have waste heat available (EPA, 2002)(Vannoni et al., 2008). Second, even though there are some facilities within MENA, the regionas such is rather unsuitable for paper industry due to the lack of wood. Also the desalinationof seawater is very promising for concentrating solar collectors, especially in combination withpower generation. A study by the DLR (Trieb et al., 2007) assessed that the renewable waterresources in MENA are already completely in use, that the demand grows by more than 100 %until 2050. Still,this topic goes beyond the scope of this study39.

ChemicalThe chemical industry has a great energy demand and is often considered as one of the sectorswith the biggest potential for SHIP (Lauterbach et al., 2011b). Since the industry is veryheterogeneous the processes have to be considered individually. The plastic industry, despitesuitable temperature ranges, is not promising for SHIP since heat is commonly provided withelectricity to ensure an accurate temperature distribution within the work-piece40 (Müller et al.,2004). Moreover, according to a study by Eikmeier et al. (2005) more than 50 % of the heatdemand in the German chemical sector is above 500◦C (Lauterbach et al., 2011b). Thus, thereis often waste heat available from higher processes or combined heat dn power (CHP) units.Finally, in MENA the industry is strongest were it is supplied with very cheap raw materialsand energy, which also does not favour the application of SHIP. Still there are very interesting38Reiners included the following countries: Albania, Algeria, Croatia, Egypt, Bosnia and Herzegovina, Greece,

Israel, Jordan, Lebanon, Libya, Morocco, Portugal, Slovenia, Spain, Tunisia and Turkey3950 % of the countries under examination have a higher water consumption than renewable freshwater avail-

ability, as can be seen in the country data in Appendix E.40This was confirmed in the visit of various plastic and cable producing companies in Tunisia.

36

processes. Within the Moroccan analysis for example a factory producing bitumen roofs wasassessed. Bitumen is a residue from oil processing. Due to its chemical properties it is com-monly used in the construction industry to make light, durable and waterproofed roofs. Anoverview of the production process of these roofs can be found in (CDC, 2001). The productionprocess has three inherent advantages for the application of SHIPc. First, temperatures are inthe range between 160 – 270◦C (BWA, 2011). Second, due to the necessary investment in theplant companies commonly have an installed capacity of several MW. Third, before processingthe product has to be stored in hot tanks at temperatures beyond 200◦C. These storage tankscan provide an excellent possibility for short term storage at peak times.

TextileAlso the textile industry is commonly identified as suitable for SHIP (Müller et al., 2004),(ESTIF, 2006), (Schweiger et al., 2001) and energy is one of its major cost factors (Hasanbeigi,2010). At the same time, it is also ”one of the most complicated manufacturing industries be-cause it is a fragmented and heterogeneous sector dominated by small and medium enterprises”(Hasanbeigi, 2010). According to Kalogirou (Kalogirou, 2009) drying (100◦C – 130◦C) and fix-ing (160◦C – 180◦C) have suitable temperatures. Drying is normally done in a mechanical anda thermal step. Müller (Müller et al., 2004) found that in Austria almost all companies areequipped with a central steam system (around 200◦C) to supply heat to the various processes.An overview of the total final energy use for the US textile industry is provided by Hasan-beigi (Hasanbeigi, 2010), which confirms that the textile industry is very suitable for SHIPc

(see Figure 17). Within the POSHIP study (Schweiger et al., 2001) various textile companieswere assessed for the application of compound parabolic concentrating (CPC) collectors, yetno studies are available for higher concentrating technologies.

...

Steam

.28%

..

Motor driven systems

.28%

..

Fired Heaters

.

20%

..

Facilities

.

18%

..

Process cooling

.4%

..Others

. 2%

Figure 17: Energy demand in US textile industry (Hasanbeigi, 2010)

37

Food and beveragesMost studies on SHIP identified food and beverage industries as very promising for SHIP(Schweiger et al., 2001), (Vannoni et al., 2008), (Müller et al., 2004), (Lauterbach et al., 2011b),(ESTIF, 2006). UNIDO even estimates that ” the food and tobacco sector has almost half ofthe potential,” (UNIDO, 2011). Moreover, food industry is present in all countries since it iscrucial for food sovereignty41. Reducing the impact of volatile energy costs on food productionalso contributes to stable food prices in the long run. The processes with high thermal energydemand are (i) cooking, (ii) drying and (iii) sterilization (Kalogirou, 2001). Depending on theproduct the exact temperature levels differ. A challenge for SHIP in food industries is that theannual load curve depends on harvest times and some processes can rest completely for severalweeks to months (e.g. sugar beet processing). Still, large companies are sufficiently diverseand produce often 365 days a year. Within Europe, the beer industry is commonly mentionedas especially suitable, and first projects have been realized already (Schneider, 2010). It is notmentioned in this study since it can well be covered with low temperature collectors and sincebeer industry is not strong in MENA.Also the dairy industry is very interesting due to daily production and high energy demand.Details on the processes in the food and beverage sector can be found in a study by theEuropean Commission (2006) (European Commission, 2006) and are summarized in Table 8.Furthermore, there is also a constant demand for cooling which can ease small fluctuations aswill be discussed below. One of the first SHIPc projects was installed in the dairy sector inPortugal in 1985 (Schweiger et al., 2001).

Table 8: Thermal processes in the dairy sector (European Commission, 2006)

Process Temperatures DescriptionPasteurization 74◦C This process deactivates most micro-organisms and

enzymes with minimized impact on the milk itself.Drying 120◦C – 180◦C Evaporators and spray driers are applied in

multi-stage process.Ultra-high treatment 130◦C – 150◦C By applying very high temperatures for a short time

the shelf life is extended for up to 1 year (uncooled)Sterilization 130◦C – 150◦C In addition to ultra-high treatment sterilized milk is

heated another time to 130◦C for 20 – 40 minutesafter filling and sealing. This can extend shelf lifeup to three years.

41Food sovereignty does not only consider calories per capita but also domestic production.

38

Solar coolingSolar cooling is not mentioned in most studies on SHIP, even though industry often has substan-tial cooling demands (especially the food sector). In MENA the demand for cooling increasesstrongly due to population growth, raising living standards and more developed industries.Since cooling is very energy intensive it is responsible for high CO2eq emissions. Moreover elec-tric HVAC systems also cause grid challenges due to high peak loads. Solar cooling addressesboth challenges simultaneously. While today it is still a niche product the potential is great,especially in the MENA region (Weiss and Mauthner, 2011). Two additional advantages arethat its output fits well to the demand curve (peak load at noon in summer) and that itsproduct can easily be stored (compared to electricity and steam for example). An overview ofthe technical solutions is provided in Table 9.

Table 9: Overview of solar cooling technologies; source: Solair-project41

Method Closed cycle Open cycle

Cycle Closed refrigerant cycle Open refrigerant cycle

Phase of sorbent Solid Liquid Sorbent Liquid

Refrigerant pairs H2O – SiO2 H2O – LiBr H2O – SiO2 H2O – CaCl2Ammonia – H2O H2O – LiCl H2O – LiCl

Capacity 50 kW – 430 kW 15 kW – 5 MW 20 kW – 350 kW not available

COP 0.5 – 0.7 0.6 – 0.75 (single–effect) 0.5 – 1 > 1

Driving temp 60◦C – 90◦C 80◦C – 110◦C (single–effect) 45◦C – 95◦C 45◦C – 70◦C

Closed-cycle absorption systems are most common (more than 60 % market share). Theycan be further differentiated between single stage and multi-effect systems. The later needhigher input temperatures of up to 180◦C, which fits well to LFC, and reuse the rejected heatof the first stage. Therefore multi stage systems have also higher coefficient of performance(COP), which makes them especially suitable for larger systems. The operating temperature ofa chiller depends on the refrigerant. For thermal driven cooling refrigeration–pairs have to befound with suitable properties (e.g. evaporation temperature). Currently the application rangeis still small and commercial products can only cool to around 7◦C. Still there are various inter-esting applications. Lokurlu examined the possibility of using multi-effect absorption machinesin combination with PTC for hotels in Turkey and found them capable of high efficient solarchilling (Lokurlu et al., 2005). Yet, they did not compare costs with alternative technologies.Due to investment costs the application of solar thermal powered cooling machines is only41see: http://www.solair-project.eu/114.0.html (last accessed 01.02.2012)

39