Embed Size (px)

Citation preview

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Forecasting Realized VolatilityUnivariate and Multivariate Heterogeneous Autoregressive

Model of Realized Volatility with Jump processes

A. Nabbi

Department of Quantitative EconomicsSchool of Business and Economics

Maastricht University

April 22, 2016

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Outline

1 IntroductionFinancial Data, Models and IssuesVolatility EstimatorsVolatility Components

2 Long-Memory Models of RVHeterogeneous AR and AR Quarticity Models

3 Proposed Models

4 Forecast Measure

5 Univariate Models on S&P500Model EstimationsIn-sample Forecast Performance

6 What’s Next

ForecastingRealizedVolatility

A. Nabbi

Introduction

Financial Data,Models andIssues

VolatilityEstimators

VolatilityComponents

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

IntroductionFinancial Data, Models and Issues

Financial Data Characteristics:

Persistent Autocorrelation of square returns.

Return Distribution: fat-tailed and leptokurtic.

Slow convergence to Normal distribution.

Volatility Models:

Short-Memory Models: GARCH and SV Models.

Long-Memory Models: FIGARCH and ARFIMA.

Issues in Modeling:

Unable to reproduce data characteristics, Loss ofObservations, Lack of Economic interpretation.

Under-performance to estimate high-frequent data.

ForecastingRealizedVolatility

A. Nabbi

Introduction

Financial Data,Models andIssues

VolatilityEstimators

VolatilityComponents

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

IntroductionFinancial Data, Models and Issues

Financial Data Characteristics:

Persistent Autocorrelation of square returns.

Return Distribution: fat-tailed and leptokurtic.

Slow convergence to Normal distribution.

Volatility Models:

Short-Memory Models: GARCH and SV Models.

Long-Memory Models: FIGARCH and ARFIMA.

Issues in Modeling:

Unable to reproduce data characteristics, Loss ofObservations, Lack of Economic interpretation.

Under-performance to estimate high-frequent data.

ForecastingRealizedVolatility

A. Nabbi

Introduction

Financial Data,Models andIssues

VolatilityEstimators

VolatilityComponents

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

IntroductionFinancial Data, Models and Issues

Financial Data Characteristics:

Persistent Autocorrelation of square returns.

Return Distribution: fat-tailed and leptokurtic.

Slow convergence to Normal distribution.

Volatility Models:

Short-Memory Models: GARCH and SV Models.

Long-Memory Models: FIGARCH and ARFIMA.

Issues in Modeling:

Unable to reproduce data characteristics, Loss ofObservations, Lack of Economic interpretation.

Under-performance to estimate high-frequent data.

ForecastingRealizedVolatility

A. Nabbi

Introduction

Financial Data,Models andIssues

VolatilityEstimators

VolatilityComponents

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

IntroductionVolatility Estimators

Daily Realized Variance

Let rt,i be high-frequency intraday return, then:

RV(d)t = RVt ≡

M∑i=1

r2t,i (1)

where ∆ = 1d/M and ∆-frequency return is defined byrt,i = log(Pt−1+i .∆)− log(Pt−1+(i−1).∆).

Jump robust estimators:

Bipower Variation: BPVt ≡ π2

(M−1M

)∑Mi=2 |rt,i ||rt,i−1|.

Median Truncated Realized Variance:MedRVt ≡ π

π−2

(M

M−1

)∑M−1i=2 Med(|rt,i+1|, |rt,i |, |rt,i−1|)2.

ForecastingRealizedVolatility

A. Nabbi

Introduction

Financial Data,Models andIssues

VolatilityEstimators

VolatilityComponents

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

IntroductionVolatility Estimators

Daily Realized Variance

Let rt,i be high-frequency intraday return, then:

RV(d)t = RVt ≡

M∑i=1

r2t,i (1)

where ∆ = 1d/M and ∆-frequency return is defined byrt,i = log(Pt−1+i .∆)− log(Pt−1+(i−1).∆).

Jump robust estimators:

Bipower Variation: BPVt ≡ π2

(M−1M

)∑Mi=2 |rt,i ||rt,i−1|.

Median Truncated Realized Variance:MedRVt ≡ π

π−2

(M

M−1

)∑M−1i=2 Med(|rt,i+1|, |rt,i |, |rt,i−1|)2.

ForecastingRealizedVolatility

A. Nabbi

Introduction

Financial Data,Models andIssues

VolatilityEstimators

VolatilityComponents

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

IntroductionVolatility Components

Highly persistent process and consistent.

No access to Intraday data.

True long-memory processes versus simple componentmodels.

Volatility components: Short-, medium- and long-term.

Realized Variance over different time horizon

RV over time horizon h is defined by,

RV(h)t−i = RVt−i |t−h ≡ 1

h

h∑k=i

RVt−k (2)

For time horizons daily, weekly and monthly: h = 1, 5, 22.

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

HeterogeneousAR and ARQuarticityModels

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Long-Memory Models of Realized VolatilityHeterogeneous AR and AR Quarticity Models

Heterogeneous Autoregressive (HAR) - Corsi(2009)

The following model labeled as HAR(3)-RV which captures theapproximate long-memory dynamic dependencies conveniently.

RVt = β0 + β1RV(d)t−1 + β2RV

(w)t−1 + β3RV

(m)t−1 + ϵt (3)

RV refers to Realized Volatility.

Extensions to HAR:

HAR-J:

RVt = β0 + β1RV(d)t−1 + β2RV

(w)t−1 + β3RV

(m)t−1 + β4Jt−1 + ϵt

(4)

Continuous HAR:

RVt = β0+β1BPV(d)t−1+β2BPV

(w)t−1 +β3BPV

(m)t−1 + ϵt (5)

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

HeterogeneousAR and ARQuarticityModels

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Long-Memory Models of Realized VolatilityHeterogeneous AR and AR Quarticity Models

Consider drt = µtdt + σtdWt then QVt = IVt + ηt whereIVt =

∫ tt−1 σ

2s ds.

RVt as consistent estimator of QVt .

In absence of jumps:√M(RV − IV )

D−→ N(0, 2IQ) whereIQt =

∫ tt−1 σ

4s ds.

RQt =M3

∑Mi=1 r

4t,i as consistent estimator of IQt .

Autoregressive Quarticity(ARQ) - Bollerslev (2015)

RVt = β0 +(β1 + β1QRQ

1/2t−1

)RVt−1 + ϵt (6)

which has a time-varying parameter.

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

HeterogeneousAR and ARQuarticityModels

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Long-Memory Models of Realized VolatilityHeterogeneous AR and AR Quarticity Models

Consider drt = µtdt + σtdWt then QVt = IVt + ηt whereIVt =

∫ tt−1 σ

2s ds.

RVt as consistent estimator of QVt .

In absence of jumps:√M(RV − IV )

D−→ N(0, 2IQ) whereIQt =

∫ tt−1 σ

4s ds.

RQt =M3

∑Mi=1 r

4t,i as consistent estimator of IQt .

Autoregressive Quarticity(ARQ) - Bollerslev (2015)

RVt = β0 +(β1 + β1QRQ

1/2t−1

)RVt−1 + ϵt (6)

which has a time-varying parameter.

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

HeterogeneousAR and ARQuarticityModels

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Long-Memory Models of Realized VolatilityHeterogeneous AR and AR Quarticity Models

Demeaned RQ1/2 results in comparable interpretation toautoregressive coefficient in AR(1)-RV.

RQ is highly imprecise and requires forth moments.

Non-robustness.

In presence of jumps: RV is not consistent and RQdiverges as M grows.

HAR on Realized Volatility and ARQ on Realized Variance.

ARQ models extensions:

Can be extended to Heterogeneous ARQ.

HARQ Full model.

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

HeterogeneousAR and ARQuarticityModels

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Long-Memory Models of Realized VolatilityHeterogeneous AR and AR Quarticity Models

Demeaned RQ1/2 results in comparable interpretation toautoregressive coefficient in AR(1)-RV.

RQ is highly imprecise and requires forth moments.

Non-robustness.

In presence of jumps: RV is not consistent and RQdiverges as M grows.

HAR on Realized Volatility and ARQ on Realized Variance.

ARQ models extensions:

Can be extended to Heterogeneous ARQ.

HARQ Full model.

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Proposed Models

Time-varying Autoregressive Model + Jump component

RVt = β0 + (β1 + β1J .Jt−1)RVt−1 + ϵt (7)

We term this specification the ARJ for short.

Heterogeneous ARJ

RVt = β0+(β1+β1J .Jt−1)RV(d)t−1+β2RV

(w)t−1+β3RV

(m)t−1+ϵt (8)

And respectively, HARJ full model is considered as a candidate.

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

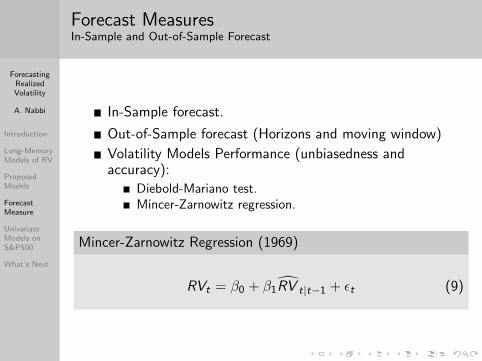

Forecast MeasuresIn-Sample and Out-of-Sample Forecast

In-Sample forecast.

Out-of-Sample forecast (Horizons and moving window)

Volatility Models Performance (unbiasedness andaccuracy):

Diebold-Mariano test.Mincer-Zarnowitz regression.

Mincer-Zarnowitz Regression (1969)

RVt = β0 + β1R̂V t|t−1 + ϵt (9)

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

ModelEstimations

In-sampleForecastPerformance

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Univariate Models on S&P500Model Estimation

HAR(3) on Realized Variance:

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

ModelEstimations

In-sampleForecastPerformance

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Univariate Models on S&P500Model Estimation

HAR(3)-J on Realized Variance:

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

ModelEstimations

In-sampleForecastPerformance

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Univariate Models on S&P500Model Estimation

CHAR on Realized Variance:

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

ModelEstimations

In-sampleForecastPerformance

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Univariate Models on S&P500Model Estimation

ARJ on Realized Variance:

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

ModelEstimations

In-sampleForecastPerformance

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Univariate Models on S&P500Model Estimation

HARJ on Realized Variance:

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

ModelEstimations

In-sampleForecastPerformance

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Univariate Models on S&P500Model Estimation

HARJ Full model on Realized Variance:

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

ModelEstimations

In-sampleForecastPerformance

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Univariate Models on S&P500Model Estimation

Autocorrelation and Partial Autocorrelation:

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

ModelEstimations

In-sampleForecastPerformance

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Univariate Models on S&P500In-sample Forecast Performance

Models R2 MAE RMSE

HAR(3) 0.5308 0.5968 1.7874HAR-J 0.5528 0.5764 1.7454CHAR 0.5575 0.5781 1.7359ARJ 0.5329 0.6206 1.7791HARJ 0.5649 0.5845 1.7216HARJ-F 0.5769 0.5893 1.6980

Table: In-sample forecast performance

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

What’s Next

Out-of-sample forecast performance.

HAR Realized Variance vs. Realized Volatility

Multivariate Models.

Missing values in multivariate case.

Volatility signals, Timezones.

Granger-Causality and Cointegration.

Partial prediction of jumps from other indexes.

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Q&A

ForecastingRealizedVolatility

A. Nabbi

Introduction

Long-MemoryModels of RV

ProposedModels

ForecastMeasure

UnivariateModels onS&P500

What’s Next

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Thank youfor

your attention

ForecastingRealizedVolatility

A. Nabbi

Appendix

References

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

References I

F. CorstA simple approximation Long-memory model of realizedvolatility, 2009.

T. Bollerslev, A.J. Patton and R. Quaedvlieg.Exploiting the Errors: A simple approach for improvedvolatility forecasting, 2015.