Embed Size (px)

Citation preview

Discrete random variablesExpectation and variance

Standard discrete probability distributions

MAS113 Introduction to Probability and

Statistics

Dr Jonathan Jordan

School of Mathematics and Statistics, University of Sheffield

2017–18

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Random variables

Informally, we think of a random variable as any quantitythat is uncertain to us. For example:

the number of emergency call-outs received by a firestation in a given week;

the price of a barrel of oil in one month’s time;

the number of gold medals won by Great Britain at thenext summer Olympics.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Random variables

Informally, we think of a random variable as any quantitythat is uncertain to us. For example:

the number of emergency call-outs received by a firestation in a given week;

the price of a barrel of oil in one month’s time;

the number of gold medals won by Great Britain at thenext summer Olympics.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Random variables

Informally, we think of a random variable as any quantitythat is uncertain to us. For example:

the number of emergency call-outs received by a firestation in a given week;

the price of a barrel of oil in one month’s time;

the number of gold medals won by Great Britain at thenext summer Olympics.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Random variables

Informally, we think of a random variable as any quantitythat is uncertain to us. For example:

the number of emergency call-outs received by a firestation in a given week;

the price of a barrel of oil in one month’s time;

the number of gold medals won by Great Britain at thenext summer Olympics.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Random variables continued

We cannot say with certainty what any of these quantities are,but probability theory gives us a framework for describing howlikely different values are.

Whereas elements of a sample space may not be numerical,random variables are always numerical quantities, and so,when defining a random variable, we need a rule for gettingfrom the random outcome in the sample space to the value ofthe random variable.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Random variables continued

We cannot say with certainty what any of these quantities are,but probability theory gives us a framework for describing howlikely different values are.

Whereas elements of a sample space may not be numerical,random variables are always numerical quantities, and so,when defining a random variable, we need a rule for gettingfrom the random outcome in the sample space to the value ofthe random variable.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Random variables continued

Definition

Given a sample space S , we define a random variable X tobe a mapping from S to the real line R.

We sometimes write a random variable as X (s), where s ∈ S .We define the range of X to be the set of all possible valuesof X :

RX := {x ∈ R; x = X (s) for some s ∈ S}.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Random variables continued

Definition

Given a sample space S , we define a random variable X tobe a mapping from S to the real line R.We sometimes write a random variable as X (s), where s ∈ S .

We define the range of X to be the set of all possible valuesof X :

RX := {x ∈ R; x = X (s) for some s ∈ S}.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Random variables continued

Definition

Given a sample space S , we define a random variable X tobe a mapping from S to the real line R.We sometimes write a random variable as X (s), where s ∈ S .We define the range of X to be the set of all possible valuesof X :

RX := {x ∈ R; x = X (s) for some s ∈ S}.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Discrete random variables

In this chapter, we consider discrete random variables, inwhich the number of possible values is either finite orcountably infinite.

Example

Counting heads in coin tosses

Example

Share portfolio

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Discrete random variables

In this chapter, we consider discrete random variables, inwhich the number of possible values is either finite orcountably infinite.

Example

Counting heads in coin tosses

Example

Share portfolio

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Discrete random variables

In this chapter, we consider discrete random variables, inwhich the number of possible values is either finite orcountably infinite.

Example

Counting heads in coin tosses

Example

Share portfolio

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Summation notation

Before continuing with the discussion of random variables, wedefine some new summation notation, and recap some resultsregarding manipulations of sums.

Let X be a discrete random variable with rangeRX = {x1, x2, . . . , xn}.

For any function g(x), we define

∑x∈Rx

g(x) :=n∑

i=1

g(xi) = g(x1) + g(x2) + . . . + g(xn).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Summation notation

Before continuing with the discussion of random variables, wedefine some new summation notation, and recap some resultsregarding manipulations of sums.

Let X be a discrete random variable with rangeRX = {x1, x2, . . . , xn}.

For any function g(x), we define

∑x∈Rx

g(x) :=n∑

i=1

g(xi) = g(x1) + g(x2) + . . . + g(xn).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Summation notation

Before continuing with the discussion of random variables, wedefine some new summation notation, and recap some resultsregarding manipulations of sums.

Let X be a discrete random variable with rangeRX = {x1, x2, . . . , xn}.

For any function g(x), we define

∑x∈Rx

g(x) :=n∑

i=1

g(xi) = g(x1) + g(x2) + . . . + g(xn).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Summation notation continued

For any two constants a and b, we have

n∑i=1

(a + bg(xi)) = (a + bg(x1)) + . . . + (a + bg(xn))

= na + bn∑

i=1

g(xi).

Note thatn∑

i=1

a = na,

(so the sum is not equal to a).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Summation notation continued

For any two constants a and b, we have

n∑i=1

(a + bg(xi)) = (a + bg(x1)) + . . . + (a + bg(xn))

= na + bn∑

i=1

g(xi).

Note thatn∑

i=1

a = na,

(so the sum is not equal to a).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Summation notation continued

For any two constants a and b, we have

n∑i=1

(a + bg(xi)) = (a + bg(x1)) + . . . + (a + bg(xn))

= na + bn∑

i=1

g(xi).

Note thatn∑

i=1

a = na,

(so the sum is not equal to a).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Summation notation continued

For any two constants a and b, we have

n∑i=1

(a + bg(xi)) = (a + bg(x1)) + . . . + (a + bg(xn))

= na + bn∑

i=1

g(xi).

Note thatn∑

i=1

a = na,

(so the sum is not equal to a).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Summation notation continued

For any two constants a and b, we have

n∑i=1

(a + bg(xi)) = (a + bg(x1)) + . . . + (a + bg(xn))

= na + bn∑

i=1

g(xi).

Note thatn∑

i=1

a = na,

(so the sum is not equal to a).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Probability mass functions

Definition

For a discrete random variable X , we define the probabilitymass function (p.m.f. for short) pX to be

pX (x) := P(X = x),

where x can be any real number.Note that P(X = x) = P(A) where

A = {s ∈ S ; X (s) = x}.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Probability mass functions

Definition

For a discrete random variable X , we define the probabilitymass function (p.m.f. for short) pX to be

pX (x) := P(X = x),

where x can be any real number.Note that P(X = x) = P(A) where

A = {s ∈ S ; X (s) = x}.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Probability mass functions

Definition

For a discrete random variable X , we define the probabilitymass function (p.m.f. for short) pX to be

pX (x) := P(X = x),

where x can be any real number.

Note that P(X = x) = P(A) where

A = {s ∈ S ; X (s) = x}.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Probability mass functions

Definition

For a discrete random variable X , we define the probabilitymass function (p.m.f. for short) pX to be

pX (x) := P(X = x),

where x can be any real number.Note that P(X = x) = P(A) where

A = {s ∈ S ; X (s) = x}.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Notation

In the notation, we use X to represent the random variable,and x to represent a possible value of X

Whereas X refers to a specific random variable, the use of theletter x is arbitrary; we could just as well writepX (a) := P(X = a).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Notation

In the notation, we use X to represent the random variable,and x to represent a possible value of X

Whereas X refers to a specific random variable, the use of theletter x is arbitrary; we could just as well writepX (a) := P(X = a).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Properties

A probability mass function must have the following twoproperties.

1 pX (x) ≥ 0∀x ∈ R.

2 Probability mass functions must ‘sum to 1’:∑x∈RX

pX (x) = 1.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Properties

A probability mass function must have the following twoproperties.

1 pX (x) ≥ 0∀x ∈ R.

2 Probability mass functions must ‘sum to 1’:∑x∈RX

pX (x) = 1.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Properties

A probability mass function must have the following twoproperties.

1 pX (x) ≥ 0∀x ∈ R.

2 Probability mass functions must ‘sum to 1’:∑x∈RX

pX (x) = 1.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Proofs of properties

Property 1 follows from the definition of pX (x).

To prove property 2, first write RX = {x1, x2, . . . , xn}, and letAi = {s ∈ S ; X (s) = xi}.

You should now convince yourself that A1, . . . ,An is apartition of S .

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Proofs of properties

Property 1 follows from the definition of pX (x).

To prove property 2, first write RX = {x1, x2, . . . , xn}, and letAi = {s ∈ S ; X (s) = xi}.

You should now convince yourself that A1, . . . ,An is apartition of S .

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Proofs of properties

Property 1 follows from the definition of pX (x).

To prove property 2, first write RX = {x1, x2, . . . , xn}, and letAi = {s ∈ S ; X (s) = xi}.

You should now convince yourself that A1, . . . ,An is apartition of S .

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

In a simple lottery, two numbers are drawn at random, withoutreplacement, from the numbers 1,2,3,4.You choose two numbers: 1 and 3.

If both 1 and 3 are drawn, you win £10. If either 1 or 3 isdrawn (but not both), you win £5. Otherwise, you winnothing.Let X be the amount in pounds that you win. Tabulate pX (x).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

In a simple lottery, two numbers are drawn at random, withoutreplacement, from the numbers 1,2,3,4.You choose two numbers: 1 and 3.If both 1 and 3 are drawn, you win £10. If either 1 or 3 isdrawn (but not both), you win £5. Otherwise, you winnothing.

Let X be the amount in pounds that you win. Tabulate pX (x).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

In a simple lottery, two numbers are drawn at random, withoutreplacement, from the numbers 1,2,3,4.You choose two numbers: 1 and 3.If both 1 and 3 are drawn, you win £10. If either 1 or 3 isdrawn (but not both), you win £5. Otherwise, you winnothing.Let X be the amount in pounds that you win. Tabulate pX (x).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Measure

Note that a probability mass function can be thought of asdefining a probability measure on the range space RX .

For a subset A ⊆ RX , define mX (A) := P(X ∈ A).

It is not hard to check that mX satisfies the definition of aprobability measure, and it is called the law or distribution ofX .

We generally think in terms of the probability mass functionrather than of the measure, but the measure idea is usefulwhen we come to generalise beyond discrete random variables.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Measure

Note that a probability mass function can be thought of asdefining a probability measure on the range space RX .

For a subset A ⊆ RX , define mX (A) := P(X ∈ A).

It is not hard to check that mX satisfies the definition of aprobability measure, and it is called the law or distribution ofX .

We generally think in terms of the probability mass functionrather than of the measure, but the measure idea is usefulwhen we come to generalise beyond discrete random variables.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Measure

Note that a probability mass function can be thought of asdefining a probability measure on the range space RX .

For a subset A ⊆ RX , define mX (A) := P(X ∈ A).

It is not hard to check that mX satisfies the definition of aprobability measure, and it is called the law or distribution ofX .

We generally think in terms of the probability mass functionrather than of the measure, but the measure idea is usefulwhen we come to generalise beyond discrete random variables.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Measure

Note that a probability mass function can be thought of asdefining a probability measure on the range space RX .

For a subset A ⊆ RX , define mX (A) := P(X ∈ A).

It is not hard to check that mX satisfies the definition of aprobability measure, and it is called the law or distribution ofX .

We generally think in terms of the probability mass functionrather than of the measure, but the measure idea is usefulwhen we come to generalise beyond discrete random variables.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Cumulative distribution function

Definition

We define the cumulative distribution function,abbreviated to c.d.f., FX of a random variable X to be

FX (x) := P(X ≤ x),

where x can be any real number.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Cumulative distribution function

Definition

We define the cumulative distribution function,abbreviated to c.d.f., FX of a random variable X to be

FX (x) := P(X ≤ x),

where x can be any real number.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Cumulative distribution function

Definition

We define the cumulative distribution function,abbreviated to c.d.f., FX of a random variable X to be

FX (x) := P(X ≤ x),

where x can be any real number.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

C.d.f. and p.d.f.

The cumulative distribution function can be written in termsof the probability mass function:

FX (x) := P(X ≤ x) =∑

a≤x ,a∈RX

pX (a). (1)

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

C.d.f. and p.d.f.

The cumulative distribution function can be written in termsof the probability mass function:

FX (x) := P(X ≤ x) =∑

a≤x ,a∈RX

pX (a). (1)

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

Suppose England are to play the West Indies in a 3 match testseries. Let X be the number of matches won by England. Ifmy probability mass function for X is

pX (0) = 0.05, pX (1) = 0.2, pX (2) = 0.6, pX (3) = 0.15,

tabulate my cumulative distribution function.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Quantile function

The quantile function is related to the inverse of thecumulative distribution function.

Definition

For α ∈ [0, 1] the α quantile (or 100× α percentile) is thesmallest value of x such that

FX (x) ≥ α

The median is the 0.5 quantile.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Quantile function

The quantile function is related to the inverse of thecumulative distribution function.

Definition

For α ∈ [0, 1] the α quantile (or 100× α percentile) is thesmallest value of x such that

FX (x) ≥ α

The median is the 0.5 quantile.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Quantile function

The quantile function is related to the inverse of thecumulative distribution function.

Definition

For α ∈ [0, 1] the α quantile (or 100× α percentile) is thesmallest value of x such that

FX (x) ≥ α

The median is the 0.5 quantile.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Independence of random variables

We say that two random variables X and Y are independentof each other if any event defined only using the value of X isindependent of any event defined only using the value of Y .

More specifically, we can make the following definition fordiscrete random variables:

Definition

Two discrete random variables X and Y are independent if

P(X = x ,Y = y) = P(X = x)P(Y = y),

for all x and y , or, equivalently, . . .

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Independence of random variables

We say that two random variables X and Y are independentof each other if any event defined only using the value of X isindependent of any event defined only using the value of Y .

More specifically, we can make the following definition fordiscrete random variables:

Definition

Two discrete random variables X and Y are independent if

P(X = x ,Y = y) = P(X = x)P(Y = y),

for all x and y , or, equivalently, . . .

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Independence continued

Definition. . .

P(X = x |Y = y) = P(X = x).

If two random variables are not independent, then we say thatthey are dependent.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

Independence of random variables

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation and variance

The probability mass function gives a complete description ofthe uncertainty we have about a random variable X .

It tells us how likely each possible value of X is.

However, there are other quantities that can tell us usefulthings about a random variable, which we can derive from theprobability mass function. We consider here the expectationand variance of a random variable.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation and variance

The probability mass function gives a complete description ofthe uncertainty we have about a random variable X .

It tells us how likely each possible value of X is.

However, there are other quantities that can tell us usefulthings about a random variable, which we can derive from theprobability mass function. We consider here the expectationand variance of a random variable.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation and variance

The probability mass function gives a complete description ofthe uncertainty we have about a random variable X .

It tells us how likely each possible value of X is.

However, there are other quantities that can tell us usefulthings about a random variable, which we can derive from theprobability mass function. We consider here the expectationand variance of a random variable.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation I

On a European roulette wheel, the ball can land on one of theintegers 0 to 36.

A bet of one pound on odd returns one pound (plus theoriginal stake) if the ball lands on any odd number from 1 to35.

Assuming the ball is equally likely to land anywhere, if you betone pound on odd a large number of times, how much moneyper game are you likely to win (or lose)?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation I

On a European roulette wheel, the ball can land on one of theintegers 0 to 36.

A bet of one pound on odd returns one pound (plus theoriginal stake) if the ball lands on any odd number from 1 to35.

Assuming the ball is equally likely to land anywhere, if you betone pound on odd a large number of times, how much moneyper game are you likely to win (or lose)?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation I

On a European roulette wheel, the ball can land on one of theintegers 0 to 36.

A bet of one pound on odd returns one pound (plus theoriginal stake) if the ball lands on any odd number from 1 to35.

Assuming the ball is equally likely to land anywhere, if you betone pound on odd a large number of times, how much moneyper game are you likely to win (or lose)?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation II

Informally, if you bet on odd 10000 times, we might supposethat you will win 18

37× 10000 = 4865 times and lose

1937× 10000 = 5135 times, so you will lose 270 pounds overall,

or 2.7 pence per game.

Formally, we define the expected profit (or loss) per game.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

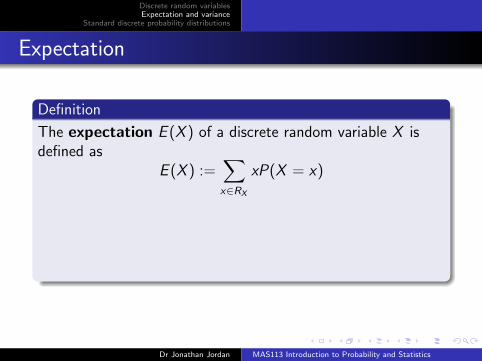

Expectation

Definition

The expectation E (X ) of a discrete random variable X isdefined as

E (X ) :=∑x∈RX

xP(X = x)

We refer to the expectation of X as the mean of X and writeµX to represent the mean:

µX := E (X ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation

Definition

The expectation E (X ) of a discrete random variable X isdefined as

E (X ) :=∑x∈RX

xP(X = x)

We refer to the expectation of X as the mean of X and writeµX to represent the mean:

µX := E (X ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

In the roulette example, let X be your net winnings after asingle bet of one pound on odd. What is E (X )?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

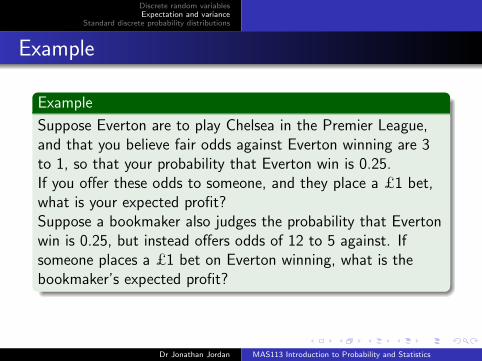

Suppose Everton are to play Chelsea in the Premier League,and that you believe fair odds against Everton winning are 3to 1, so that your probability that Everton win is 0.25.

If you offer these odds to someone, and they place a £1 bet,what is your expected profit?Suppose a bookmaker also judges the probability that Evertonwin is 0.25, but instead offers odds of 12 to 5 against. Ifsomeone places a £1 bet on Everton winning, what is thebookmaker’s expected profit?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

Suppose Everton are to play Chelsea in the Premier League,and that you believe fair odds against Everton winning are 3to 1, so that your probability that Everton win is 0.25.If you offer these odds to someone, and they place a £1 bet,what is your expected profit?

Suppose a bookmaker also judges the probability that Evertonwin is 0.25, but instead offers odds of 12 to 5 against. Ifsomeone places a £1 bet on Everton winning, what is thebookmaker’s expected profit?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

Suppose Everton are to play Chelsea in the Premier League,and that you believe fair odds against Everton winning are 3to 1, so that your probability that Everton win is 0.25.If you offer these odds to someone, and they place a £1 bet,what is your expected profit?Suppose a bookmaker also judges the probability that Evertonwin is 0.25, but instead offers odds of 12 to 5 against. Ifsomeone places a £1 bet on Everton winning, what is thebookmaker’s expected profit?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

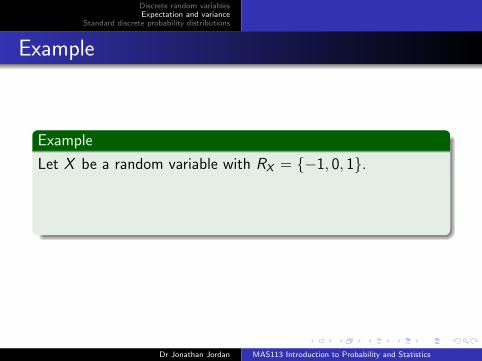

Let X be a random variable with RX = {−1, 0, 1}.

Define Y = g(X ) = X 2.Then Y is another random variable, with RY (y) = {0, 1}.What is E{g(X )}?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

Let X be a random variable with RX = {−1, 0, 1}.Define Y = g(X ) = X 2.

Then Y is another random variable, with RY (y) = {0, 1}.What is E{g(X )}?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

Let X be a random variable with RX = {−1, 0, 1}.Define Y = g(X ) = X 2.Then Y is another random variable, with RY (y) = {0, 1}.What is E{g(X )}?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation of a function of X

Sometimes it is useful to calculate the expectation of afunction of X . The following result generalises the previousexample to tell us how.

Theorem

(The expectation of g(X ))For any function g of a random variable X , with probabilitymass function pX (x),

E{g(X )} =∑x∈RX

g(x)pX (x).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation of a function of X

Sometimes it is useful to calculate the expectation of afunction of X . The following result generalises the previousexample to tell us how.

Theorem

(The expectation of g(X ))For any function g of a random variable X , with probabilitymass function pX (x),

E{g(X )} =∑x∈RX

g(x)pX (x).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation of a function of X

Sometimes it is useful to calculate the expectation of afunction of X . The following result generalises the previousexample to tell us how.

Theorem

(The expectation of g(X ))For any function g of a random variable X , with probabilitymass function pX (x),

E{g(X )} =∑x∈RX

g(x)pX (x).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

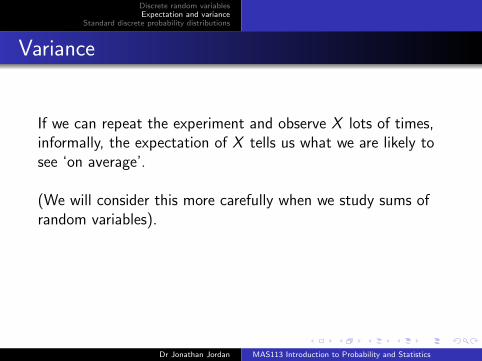

Variance

If we can repeat the experiment and observe X lots of times,informally, the expectation of X tells us what we are likely tosee ‘on average’.

(We will consider this more carefully when we study sums ofrandom variables).

It will also be useful to consider how far X might be from itsexpectation.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Variance

If we can repeat the experiment and observe X lots of times,informally, the expectation of X tells us what we are likely tosee ‘on average’.

(We will consider this more carefully when we study sums ofrandom variables).

It will also be useful to consider how far X might be from itsexpectation.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Variance

If we can repeat the experiment and observe X lots of times,informally, the expectation of X tells us what we are likely tosee ‘on average’.

(We will consider this more carefully when we study sums ofrandom variables).

It will also be useful to consider how far X might be from itsexpectation.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

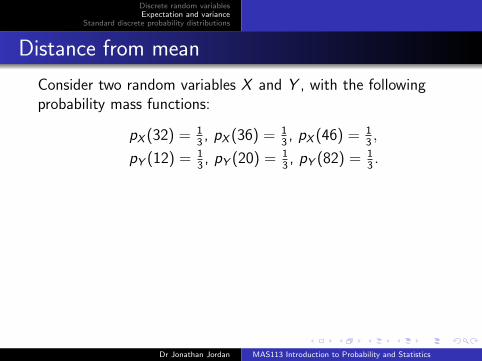

Distance from mean

Consider two random variables X and Y , with the followingprobability mass functions:

pX (32) = 13, pX (36) = 1

3, pX (46) = 1

3,

pY (12) = 13, pY (20) = 1

3, pY (82) = 1

3.

Then

E (X ) = 32× 1

3+ 36× 1

3+ 46× 1

3= 38,

E (Y ) = 12× 1

3+ 20× 1

3+ 82× 1

3= 38.

Both X and Y have the same expected value, but forwhatever values of X and Y we observe, X will be closer toE (X ) than Y will be to E (Y ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Distance from mean

Consider two random variables X and Y , with the followingprobability mass functions:

pX (32) = 13, pX (36) = 1

3, pX (46) = 1

3,

pY (12) = 13, pY (20) = 1

3, pY (82) = 1

3.

Then

E (X ) = 32× 1

3+ 36× 1

3+ 46× 1

3= 38,

E (Y ) = 12× 1

3+ 20× 1

3+ 82× 1

3= 38.

Both X and Y have the same expected value, but forwhatever values of X and Y we observe, X will be closer toE (X ) than Y will be to E (Y ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Distance from mean

Consider two random variables X and Y , with the followingprobability mass functions:

pX (32) = 13, pX (36) = 1

3, pX (46) = 1

3,

pY (12) = 13, pY (20) = 1

3, pY (82) = 1

3.

Then

E (X ) = 32× 1

3+ 36× 1

3+ 46× 1

3= 38,

E (Y ) = 12× 1

3+ 20× 1

3+ 82× 1

3= 38.

Both X and Y have the same expected value, but forwhatever values of X and Y we observe, X will be closer toE (X ) than Y will be to E (Y ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Distance from mean

Consider two random variables X and Y , with the followingprobability mass functions:

pX (32) = 13, pX (36) = 1

3, pX (46) = 1

3,

pY (12) = 13, pY (20) = 1

3, pY (82) = 1

3.

Then

E (X ) = 32× 1

3+ 36× 1

3+ 46× 1

3= 38,

E (Y ) = 12× 1

3+ 20× 1

3+ 82× 1

3= 38.

Both X and Y have the same expected value, but forwhatever values of X and Y we observe, X will be closer toE (X ) than Y will be to E (Y ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Distance from mean

Consider two random variables X and Y , with the followingprobability mass functions:

pX (32) = 13, pX (36) = 1

3, pX (46) = 1

3,

pY (12) = 13, pY (20) = 1

3, pY (82) = 1

3.

Then

E (X ) = 32× 1

3+ 36× 1

3+ 46× 1

3= 38,

E (Y ) = 12× 1

3+ 20× 1

3+ 82× 1

3= 38.

Both X and Y have the same expected value, but forwhatever values of X and Y we observe, X will be closer toE (X ) than Y will be to E (Y ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

We use the concept of variance to describe how close arandom variable is likely to be to its expected value.

Definition

The variance Var(X ) of a discrete random variable X isdefined as

Var(X ) : = E[{X − E (X )}2

]= E{(X − µX )2}

=∑x∈RX

(x − µX )2pX (x).

We denote the variance by σ2X :

σ2X := Var(X ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

We use the concept of variance to describe how close arandom variable is likely to be to its expected value.

Definition

The variance Var(X ) of a discrete random variable X isdefined as

Var(X ) : = E[{X − E (X )}2

]= E{(X − µX )2}

=∑x∈RX

(x − µX )2pX (x).

We denote the variance by σ2X :

σ2X := Var(X ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

We use the concept of variance to describe how close arandom variable is likely to be to its expected value.

Definition

The variance Var(X ) of a discrete random variable X isdefined as

Var(X ) : = E[{X − E (X )}2

]= E{(X − µX )2}

=∑x∈RX

(x − µX )2pX (x).

We denote the variance by σ2X :

σ2X := Var(X ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

We use the concept of variance to describe how close arandom variable is likely to be to its expected value.

Definition

The variance Var(X ) of a discrete random variable X isdefined as

Var(X ) : = E[{X − E (X )}2

]= E{(X − µX )2}

=∑x∈RX

(x − µX )2pX (x).

We denote the variance by σ2X :

σ2X := Var(X ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Why squared?

If you are wondering why the variance is defined asE [{X − E (X )}2] rather than E{X − E (X )}, the latterexpression will not tell us anything useful about X :

Theorem

(The expected difference between a random variable and itsmean)

E{X − E (X )} = 0,

for any random variable X .

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Why squared?

If you are wondering why the variance is defined asE [{X − E (X )}2] rather than E{X − E (X )}, the latterexpression will not tell us anything useful about X :

Theorem

(The expected difference between a random variable and itsmean)

E{X − E (X )} = 0,

for any random variable X .

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Standard deviation

As the variance is defined as an expected squared difference,the variance will be expressed in units that are the square ofthe units of X .

If we want a measure of spread that is in the same units as X ,we take the square root of the variance.

Definition

The standard deviation of a random variable X , denoted byσX , is the square root of the variance of X .

σX :=√

Var(X ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Standard deviation

As the variance is defined as an expected squared difference,the variance will be expressed in units that are the square ofthe units of X .

If we want a measure of spread that is in the same units as X ,we take the square root of the variance.

Definition

The standard deviation of a random variable X , denoted byσX , is the square root of the variance of X .

σX :=√

Var(X ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Standard deviation

As the variance is defined as an expected squared difference,the variance will be expressed in units that are the square ofthe units of X .

If we want a measure of spread that is in the same units as X ,we take the square root of the variance.

Definition

The standard deviation of a random variable X , denoted byσX , is the square root of the variance of X .

σX :=√

Var(X ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The variance identity

The following result is useful for calculating variances:

Theorem

Var(X ) = E (X 2)− E (X )2,

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The variance identity

The following result is useful for calculating variances:

Theorem

Var(X ) = E (X 2)− E (X )2,

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Calculating the variance

To calculate a variance, if we already have E (X ), we just needto calculate E (X 2).

(Alternatively, if we know the mean and variance, this gives usa quick way of calculating E (X 2)).

Note that as long as Var(X ) > 0 we can see that

E (X 2) 6= E (X )2.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Calculating the variance

To calculate a variance, if we already have E (X ), we just needto calculate E (X 2).

(Alternatively, if we know the mean and variance, this gives usa quick way of calculating E (X 2)).

Note that as long as Var(X ) > 0 we can see that

E (X 2) 6= E (X )2.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Calculating the variance

To calculate a variance, if we already have E (X ), we just needto calculate E (X 2).

(Alternatively, if we know the mean and variance, this gives usa quick way of calculating E (X 2)).

Note that as long as Var(X ) > 0 we can see that

E (X 2) 6= E (X )2.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

Let X be the random variable defined in the roulette example,with E (X ) = −1/37. What is Var(X )?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The expectation and variance of aX + b

Theorem

Let X be a random variable, and a and b be any twoconstants. Then

E (aX + b) = aE (X ) + b,

Var(aX + b) = a2 Var(X ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The expectation and variance of aX + b

Theorem

Let X be a random variable, and a and b be any twoconstants. Then

E (aX + b) = aE (X ) + b,

Var(aX + b) = a2 Var(X ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Special cases

If we set a = 0, then we can see that for any constant b,

E (b) = b,

Var(b) = 0.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation of a sum

It is often useful to consider expectations of sums of randomvariables:

Theorem

Given any two random variables X and Y

E (X + Y ) = E (X ) + E (Y ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation of a product

We might hope that the same was true for variance, so thatthe variance of X + Y was the sum of the variances of X andY .

This is not true in general, but it is true when X and Y areindependent. To prove this we will first of all prove animportant result about the expectation of a product ofindependent random variables.

Theorem

For any two random variables X and Y which are independent,

E (XY ) = E (X )E (Y ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation of a product

We might hope that the same was true for variance, so thatthe variance of X + Y was the sum of the variances of X andY .

This is not true in general, but it is true when X and Y areindependent. To prove this we will first of all prove animportant result about the expectation of a product ofindependent random variables.

Theorem

For any two random variables X and Y which are independent,

E (XY ) = E (X )E (Y ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Expectation of a product

We might hope that the same was true for variance, so thatthe variance of X + Y was the sum of the variances of X andY .

This is not true in general, but it is true when X and Y areindependent. To prove this we will first of all prove animportant result about the expectation of a product ofindependent random variables.

Theorem

For any two random variables X and Y which are independent,

E (XY ) = E (X )E (Y ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Variance of independent sum

Corollary

For any two random variables X and Y which are independent,

Var(X + Y ) = Var(X ) + Var(Y ).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Example

Example

Let X and Y be independent random variables withVar(X ) = 9 and Var(Y ) = 16. What is Var(X − Y )?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Standard probability distributions

We now consider some standard probability distributions fordiscrete random variables, that can be used in a variety ofdifferent applications.

By “distribution”, we mean a particular choice of probabilitymass function, which may be specified in terms of someparameters.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Standard probability distributions

We now consider some standard probability distributions fordiscrete random variables, that can be used in a variety ofdifferent applications.

By “distribution”, we mean a particular choice of probabilitymass function, which may be specified in terms of someparameters.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The Bernoulli distribution

A Bernoulli random variable X can take one of two values: 0and 1.

Examples of ‘experiments’ that we might describe using aBernoulli random variable are

a patient is given a drug, and the drug either ‘works’:X = 1, or does not: X = 0;

a tennis player either wins a match: X = 1, or loses:X = 0;

in one year, a house is either burgled: X = 1, or not:X = 0.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The Bernoulli distribution

A Bernoulli random variable X can take one of two values: 0and 1.

Examples of ‘experiments’ that we might describe using aBernoulli random variable are

a patient is given a drug, and the drug either ‘works’:X = 1, or does not: X = 0;

a tennis player either wins a match: X = 1, or loses:X = 0;

in one year, a house is either burgled: X = 1, or not:X = 0.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The Bernoulli distribution

A Bernoulli random variable X can take one of two values: 0and 1.

Examples of ‘experiments’ that we might describe using aBernoulli random variable are

a patient is given a drug, and the drug either ‘works’:X = 1, or does not: X = 0;

a tennis player either wins a match: X = 1, or loses:X = 0;

in one year, a house is either burgled: X = 1, or not:X = 0.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The Bernoulli distribution

A Bernoulli random variable X can take one of two values: 0and 1.

Examples of ‘experiments’ that we might describe using aBernoulli random variable are

a patient is given a drug, and the drug either ‘works’:X = 1, or does not: X = 0;

a tennis player either wins a match: X = 1, or loses:X = 0;

in one year, a house is either burgled: X = 1, or not:X = 0.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The Bernoulli distribution

A Bernoulli random variable X can take one of two values: 0and 1.

Examples of ‘experiments’ that we might describe using aBernoulli random variable are

a patient is given a drug, and the drug either ‘works’:X = 1, or does not: X = 0;

a tennis player either wins a match: X = 1, or loses:X = 0;

in one year, a house is either burgled: X = 1, or not:X = 0.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

Definition

If a random variable X has a Bernoulli distribution, then itsprobability mass function is

pX (1) = p,

pX (0) = 1− p,

and pX (x) = 0 otherwise, with 0 ≤ p ≤ 1.We write

X ∼ Bernoulli(p),

to mean “X has a Bernoulli distribution with parameter p’(the probability that X = 1)”.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

Definition

If a random variable X has a Bernoulli distribution, then itsprobability mass function is

pX (1) = p,

pX (0) = 1− p,

and pX (x) = 0 otherwise, with 0 ≤ p ≤ 1.We write

X ∼ Bernoulli(p),

to mean “X has a Bernoulli distribution with parameter p’(the probability that X = 1)”.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

Definition

If a random variable X has a Bernoulli distribution, then itsprobability mass function is

pX (1) = p,

pX (0) = 1− p,

and pX (x) = 0 otherwise, with 0 ≤ p ≤ 1.We write

X ∼ Bernoulli(p),

to mean “X has a Bernoulli distribution with parameter p’(the probability that X = 1)”.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

Definition

If a random variable X has a Bernoulli distribution, then itsprobability mass function is

pX (1) = p,

pX (0) = 1− p,

and pX (x) = 0 otherwise, with 0 ≤ p ≤ 1.

We writeX ∼ Bernoulli(p),

to mean “X has a Bernoulli distribution with parameter p’(the probability that X = 1)”.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

Definition

If a random variable X has a Bernoulli distribution, then itsprobability mass function is

pX (1) = p,

pX (0) = 1− p,

and pX (x) = 0 otherwise, with 0 ≤ p ≤ 1.We write

X ∼ Bernoulli(p),

to mean “X has a Bernoulli distribution with parameter p’(the probability that X = 1)”.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

Definition

If a random variable X has a Bernoulli distribution, then itsprobability mass function is

pX (1) = p,

pX (0) = 1− p,

and pX (x) = 0 otherwise, with 0 ≤ p ≤ 1.We write

X ∼ Bernoulli(p),

to mean “X has a Bernoulli distribution with parameter p’(the probability that X = 1)”.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Mean and variance

Theorem

(Expectation and variance of a Bernoulli random variable)For the expectation of a Bernoulli random variableX ∼ Bernoulli(p), we have

E (X ) = p,

Var(X ) = p(1− p).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Mean and variance

Theorem

(Expectation and variance of a Bernoulli random variable)For the expectation of a Bernoulli random variableX ∼ Bernoulli(p), we have

E (X ) = p,

Var(X ) = p(1− p).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The binomial distribution

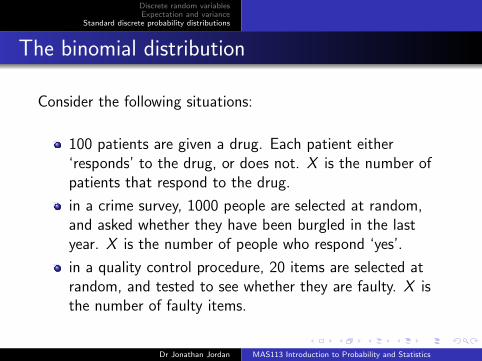

Consider the following situations:

100 patients are given a drug. Each patient either‘responds’ to the drug, or does not. X is the number ofpatients that respond to the drug.

in a crime survey, 1000 people are selected at random,and asked whether they have been burgled in the lastyear. X is the number of people who respond ‘yes’.

in a quality control procedure, 20 items are selected atrandom, and tested to see whether they are faulty. X isthe number of faulty items.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The binomial distribution

Consider the following situations:

100 patients are given a drug. Each patient either‘responds’ to the drug, or does not. X is the number ofpatients that respond to the drug.

in a crime survey, 1000 people are selected at random,and asked whether they have been burgled in the lastyear. X is the number of people who respond ‘yes’.

in a quality control procedure, 20 items are selected atrandom, and tested to see whether they are faulty. X isthe number of faulty items.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The binomial distribution

Consider the following situations:

100 patients are given a drug. Each patient either‘responds’ to the drug, or does not. X is the number ofpatients that respond to the drug.

in a crime survey, 1000 people are selected at random,and asked whether they have been burgled in the lastyear. X is the number of people who respond ‘yes’.

in a quality control procedure, 20 items are selected atrandom, and tested to see whether they are faulty. X isthe number of faulty items.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Bernoulli trials

In each case we have a fixed number of “trials”, each of whichcan have two possible outcomes (often called “success” and“failure”).

(Each trial can be considered an example of a Bernoullidistribution, with “success” corresponding to 1 and “failure”to 0, so they are often referred to as Bernoulli trials.)

In each of these situations it is reasonable to assume that theprobability of a “success”, which we will call p, is constantfrom from one trial to the next, and that the trials areindependent.

In each case we are counting the total number of successes.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Bernoulli trials

In each case we have a fixed number of “trials”, each of whichcan have two possible outcomes (often called “success” and“failure”).

(Each trial can be considered an example of a Bernoullidistribution, with “success” corresponding to 1 and “failure”to 0, so they are often referred to as Bernoulli trials.)

In each of these situations it is reasonable to assume that theprobability of a “success”, which we will call p, is constantfrom from one trial to the next, and that the trials areindependent.

In each case we are counting the total number of successes.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Bernoulli trials

In each case we have a fixed number of “trials”, each of whichcan have two possible outcomes (often called “success” and“failure”).

(Each trial can be considered an example of a Bernoullidistribution, with “success” corresponding to 1 and “failure”to 0, so they are often referred to as Bernoulli trials.)

In each of these situations it is reasonable to assume that theprobability of a “success”, which we will call p, is constantfrom from one trial to the next, and that the trials areindependent.

In each case we are counting the total number of successes.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Bernoulli trials

In each case we have a fixed number of “trials”, each of whichcan have two possible outcomes (often called “success” and“failure”).

(Each trial can be considered an example of a Bernoullidistribution, with “success” corresponding to 1 and “failure”to 0, so they are often referred to as Bernoulli trials.)

In each of these situations it is reasonable to assume that theprobability of a “success”, which we will call p, is constantfrom from one trial to the next, and that the trials areindependent.

In each case we are counting the total number of successes.Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

n = 2

To think about the form of the probability mass function of X ,consider the case n = 2. The possible outcomes are

(on board)

Consider calculating pX (1).

We are not interested in which trials are successes, only thetotal number of successes

There are two ways of achieving one success in total, and foreach of these possibilities, the corresponding probability isp(1− p), so we have pX (1) = 2p(1− p).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

n = 2

To think about the form of the probability mass function of X ,consider the case n = 2. The possible outcomes are

(on board)

Consider calculating pX (1).

We are not interested in which trials are successes, only thetotal number of successes

There are two ways of achieving one success in total, and foreach of these possibilities, the corresponding probability isp(1− p), so we have pX (1) = 2p(1− p).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

n = 2

To think about the form of the probability mass function of X ,consider the case n = 2. The possible outcomes are

(on board)

Consider calculating pX (1).

We are not interested in which trials are successes, only thetotal number of successes

There are two ways of achieving one success in total, and foreach of these possibilities, the corresponding probability isp(1− p), so we have pX (1) = 2p(1− p).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

General formula

In general for n trials, the number of possible sequences thatcontain x successes in total will be

(n

x

)=

n!

x!(n − x)!,

and the probability of any individual sequence with x successesin total will be px(1− p)n−x .

So we will have pX (x) =(nx

)px(1− p)n−x .

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

General formula

In general for n trials, the number of possible sequences thatcontain x successes in total will be(

n

x

)=

n!

x!(n − x)!,

and the probability of any individual sequence with x successesin total will be px(1− p)n−x .

So we will have pX (x) =(nx

)px(1− p)n−x .

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

General formula

In general for n trials, the number of possible sequences thatcontain x successes in total will be(

n

x

)=

n!

x!(n − x)!,

and the probability of any individual sequence with x successesin total will be px(1− p)n−x .

So we will have pX (x) =(nx

)px(1− p)n−x .

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

General formula

In general for n trials, the number of possible sequences thatcontain x successes in total will be(

n

x

)=

n!

x!(n − x)!,

and the probability of any individual sequence with x successesin total will be px(1− p)n−x .

So we will have pX (x) =(nx

)px(1− p)n−x .

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

Motivated by this, we make the following definition:

Definition

If a random variable X has a binomial distribution, withparameters n (the number of trials) and p (the probability ofsuccess in each trial), then the probability mass function of Xis given by

pX (x) =n!

x!(n − x)!px(1− p)n−x ,

for x ∈ RX = {0, 1, 2, . . . , n}, and 0 otherwise.We write X ∼ Bin(n, p), to mean “X has a binomialdistribution with parameters n (the number of trials) and p(the probability of success in each trial)”.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

Motivated by this, we make the following definition:

Definition

If a random variable X has a binomial distribution, withparameters n (the number of trials) and p (the probability ofsuccess in each trial), then the probability mass function of Xis given by

pX (x) =n!

x!(n − x)!px(1− p)n−x ,

for x ∈ RX = {0, 1, 2, . . . , n}, and 0 otherwise.We write X ∼ Bin(n, p), to mean “X has a binomialdistribution with parameters n (the number of trials) and p(the probability of success in each trial)”.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

Motivated by this, we make the following definition:

Definition

If a random variable X has a binomial distribution, withparameters n (the number of trials) and p (the probability ofsuccess in each trial), then the probability mass function of Xis given by

pX (x) =n!

x!(n − x)!px(1− p)n−x ,

for x ∈ RX = {0, 1, 2, . . . , n}, and 0 otherwise.We write X ∼ Bin(n, p), to mean “X has a binomialdistribution with parameters n (the number of trials) and p(the probability of success in each trial)”.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

Motivated by this, we make the following definition:

Definition

If a random variable X has a binomial distribution, withparameters n (the number of trials) and p (the probability ofsuccess in each trial), then the probability mass function of Xis given by

pX (x) =n!

x!(n − x)!px(1− p)n−x ,

for x ∈ RX = {0, 1, 2, . . . , n}, and 0 otherwise.

We write X ∼ Bin(n, p), to mean “X has a binomialdistribution with parameters n (the number of trials) and p(the probability of success in each trial)”.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

Motivated by this, we make the following definition:

Definition

If a random variable X has a binomial distribution, withparameters n (the number of trials) and p (the probability ofsuccess in each trial), then the probability mass function of Xis given by

pX (x) =n!

x!(n − x)!px(1− p)n−x ,

for x ∈ RX = {0, 1, 2, . . . , n}, and 0 otherwise.We write X ∼ Bin(n, p),

to mean “X has a binomialdistribution with parameters n (the number of trials) and p(the probability of success in each trial)”.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Definition

Motivated by this, we make the following definition:

Definition

If a random variable X has a binomial distribution, withparameters n (the number of trials) and p (the probability ofsuccess in each trial), then the probability mass function of Xis given by

pX (x) =n!

x!(n − x)!px(1− p)n−x ,

for x ∈ RX = {0, 1, 2, . . . , n}, and 0 otherwise.We write X ∼ Bin(n, p), to mean “X has a binomialdistribution with parameters n (the number of trials) and p(the probability of success in each trial)”.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Link to binomial theorem

Note that the binomial theorem confirms that the binomialprobability mass function is valid (ie it sums to 1):

It tells us that

(a + b)n =n∑

x=0

(n

x

)axbn−x .

and if we now choose a = p and b = 1− p, we have

n∑x=0

pX (x) =n∑

x=0

(n

x

)px(1− p)n−x = (p + (1− p))n = 1,

as we should have.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Link to binomial theorem

Note that the binomial theorem confirms that the binomialprobability mass function is valid (ie it sums to 1):

It tells us that

(a + b)n =n∑

x=0

(n

x

)axbn−x .

and if we now choose a = p and b = 1− p, we have

n∑x=0

pX (x) =n∑

x=0

(n

x

)px(1− p)n−x = (p + (1− p))n = 1,

as we should have.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Link to binomial theorem

Note that the binomial theorem confirms that the binomialprobability mass function is valid (ie it sums to 1):

It tells us that

(a + b)n =n∑

x=0

(n

x

)axbn−x .

and if we now choose a = p and b = 1− p, we have

n∑x=0

pX (x) =n∑

x=0

(n

x

)px(1− p)n−x = (p + (1− p))n = 1,

as we should have.

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Link to binomial theorem

Note that the binomial theorem confirms that the binomialprobability mass function is valid (ie it sums to 1):

It tells us that

(a + b)n =n∑

x=0

(n

x

)axbn−x .

and if we now choose a = p and b = 1− p, we have

n∑x=0

pX (x) =n∑

x=0

(n

x

)px(1− p)n−x = (p + (1− p))n = 1,

as we should have.Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Mean and variance

Theorem

(Expectation and variance of a binomial random variable)For X ∼ Bin(n, p) we have

E (X ) = np

Var(X ) = np(1− p).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Mean and variance

Theorem

(Expectation and variance of a binomial random variable)For X ∼ Bin(n, p) we have

E (X ) = np

Var(X ) = np(1− p).

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Proportion of successes

As well as being interested in the total number of ‘successes’X , we may also be interested in the proportion of success X/n.

We have

E

(X

n

)= p,

Var

(X

n

)=

p(1− p)

n.

What do you think will happen to X/n as n→∞?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Proportion of successes

As well as being interested in the total number of ‘successes’X , we may also be interested in the proportion of success X/n.

We have

E

(X

n

)= p,

Var

(X

n

)=

p(1− p)

n.

What do you think will happen to X/n as n→∞?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Proportion of successes

As well as being interested in the total number of ‘successes’X , we may also be interested in the proportion of success X/n.

We have

E

(X

n

)= p,

Var

(X

n

)=

p(1− p)

n.

What do you think will happen to X/n as n→∞?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

Proportion of successes

As well as being interested in the total number of ‘successes’X , we may also be interested in the proportion of success X/n.

We have

E

(X

n

)= p,

Var

(X

n

)=

p(1− p)

n.

What do you think will happen to X/n as n→∞?

Dr Jonathan Jordan MAS113 Introduction to Probability and Statistics

Discrete random variablesExpectation and variance

Standard discrete probability distributions

The cumulative distribution function

The cumulative distribution function is given by

FX (x) = P(X ≤ x) =x∑

a=0

pX (a)

=x∑

a=0

n!

a!(n − a)!pa(1− p)n−a.

We cannot simplify this expression, and so calculating thec.d.f. by hand can be tedious.

Fortunately, we can do this and other calculations related tothe binomial distribution very easily in R.