Embed Size (px)

Citation preview

MAS Notice 610/1003 Regulatory Reporting

15 May 2015

Executive Briefing

1

Content

© 2015 Deloitte & Touche LLP. All rights reserved. 2

Background on revisions What’s new in 610/1003? Reporting requirements Key challenges in reporting Share your views

Background on revisions

3 © 2015 Deloitte & Touche LLP. All rights reserved.

Background on revisions

4

- Current set of returns are dated, and needed to be revised to reflect feedback and common challenges observed, and developments in product types and businesses of banks/merchant banks.

- Data collated on ad-hoc basis, now consolidated in the proposed revisions to the returns.

- Reporting Obligations to IMF and other global organisations - Regulators seek to obtain more detailed financial data and improve the data quality

submitted by banks. This provides regulators with more ‘useful’ data for analysis.

MAS Closed Consultation with selected

banks, merchant banks and audit firms

on Notice 610/1003

Final MAS Notice

610/1003

Jan 2014 Dec 2014 (CP closed on 5 February 2015)

When?

© 2015 Deloitte & Touche LLP. All rights reserved.

What’s new in

610/1003?

5 © 2015 Deloitte & Touche LLP. All rights reserved.

6

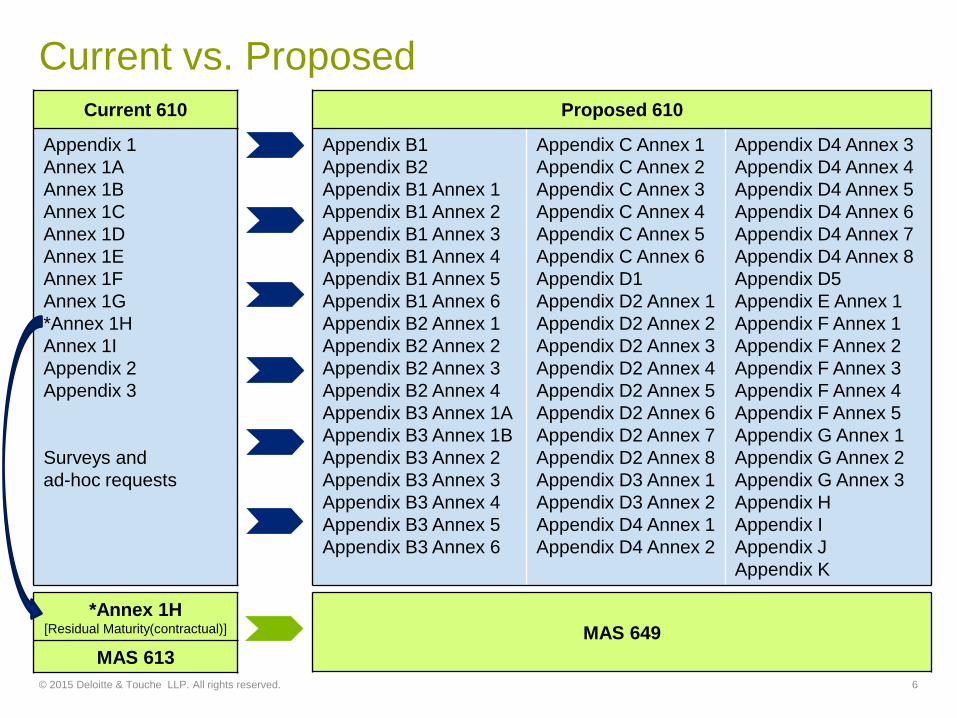

Current 610

Appendix 1 Annex 1A Annex 1B Annex 1C Annex 1D Annex 1E Annex 1F Annex 1G *Annex 1H Annex 1I Appendix 2 Appendix 3 Surveys and ad-hoc requests

*Annex 1H [Residual Maturity(contractual)]

MAS 613

Proposed 610

Appendix B1 Appendix B2 Appendix B1 Annex 1 Appendix B1 Annex 2 Appendix B1 Annex 3 Appendix B1 Annex 4 Appendix B1 Annex 5 Appendix B1 Annex 6 Appendix B2 Annex 1 Appendix B2 Annex 2 Appendix B2 Annex 3 Appendix B2 Annex 4 Appendix B3 Annex 1A Appendix B3 Annex 1B Appendix B3 Annex 2 Appendix B3 Annex 3 Appendix B3 Annex 4 Appendix B3 Annex 5 Appendix B3 Annex 6

Appendix C Annex 1 Appendix C Annex 2 Appendix C Annex 3 Appendix C Annex 4 Appendix C Annex 5 Appendix C Annex 6 Appendix D1 Appendix D2 Annex 1 Appendix D2 Annex 2 Appendix D2 Annex 3 Appendix D2 Annex 4 Appendix D2 Annex 5 Appendix D2 Annex 6 Appendix D2 Annex 7 Appendix D2 Annex 8 Appendix D3 Annex 1 Appendix D3 Annex 2 Appendix D4 Annex 1 Appendix D4 Annex 2

Appendix D4 Annex 3 Appendix D4 Annex 4 Appendix D4 Annex 5 Appendix D4 Annex 6 Appendix D4 Annex 7 Appendix D4 Annex 8 Appendix D5 Appendix E Annex 1 Appendix F Annex 1 Appendix F Annex 2 Appendix F Annex 3 Appendix F Annex 4 Appendix F Annex 5 Appendix G Annex 1 Appendix G Annex 2 Appendix G Annex 3 Appendix H Appendix I Appendix J Appendix K

MAS 649

© 2015 Deloitte & Touche LLP. All rights reserved.

Current vs. Proposed

Proposed structure

7

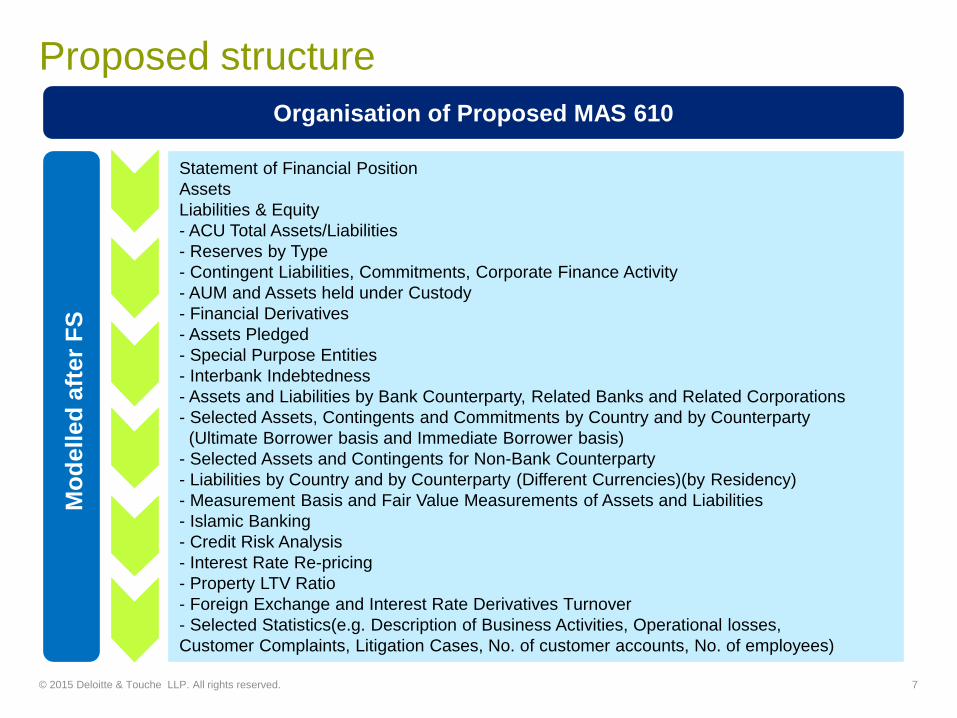

Statement of Financial Position Assets Liabilities & Equity - ACU Total Assets/Liabilities - Reserves by Type - Contingent Liabilities, Commitments, Corporate Finance Activity - AUM and Assets held under Custody - Financial Derivatives - Assets Pledged - Special Purpose Entities - Interbank Indebtedness - Assets and Liabilities by Bank Counterparty, Related Banks and Related Corporations - Selected Assets, Contingents and Commitments by Country and by Counterparty (Ultimate Borrower basis and Immediate Borrower basis) - Selected Assets and Contingents for Non-Bank Counterparty - Liabilities by Country and by Counterparty (Different Currencies)(by Residency) - Measurement Basis and Fair Value Measurements of Assets and Liabilities - Islamic Banking - Credit Risk Analysis - Interest Rate Re-pricing - Property LTV Ratio - Foreign Exchange and Interest Rate Derivatives Turnover - Selected Statistics(e.g. Description of Business Activities, Operational losses, Customer Complaints, Litigation Cases, No. of customer accounts, No. of employees)

Organisation of Proposed MAS 610

Mo

del

led

aft

er F

S

© 2015 Deloitte & Touche LLP. All rights reserved.

Proposed format and content of the reporting forms

• Modelled after FS to reflect reporting banks’ financial condition • Prepare reporting forms in accordance with Singapore FRS

Proposed revisions highlighted in MAS response to Consultation Paper

Proposed structure

8

Reporting frequency for forms

• Monthly, quarterly, half-yearly and yearly • Extension of submission deadline for a number of returns

except for the monthly reporting forms

Implementation of changes following Notice issuance

• Extended to 18 months • Provide 2 six-monthly updates of implementation status to

MAS prior to final implementation.

© 2015 Deloitte & Touche LLP. All rights reserved.

1.Consolidated reporting for SG operations Pertinent proposed revisions

9

Reduced reporting requirements based

on ACU and DBU

Preparation of consolidated reports

for SG operations

For the purpose of reporting under this Notice, the Domestic Banking Unit ("DBU") and Asian Currency Unit (“ACU”) operations of merchant banks in Singapore are to be

considered as "banks" and transactions with them should be classified under "Banks in Singapore".

Appendices requiring separate reporting of ACU and DBU • Appendix B2 Annex 2 – Deposits by Size and Deposit Rate of Non-Bank Customers • Appendix B2 Annex 3 Parts I,II,III – Capital Funds and Adjusted Capital Funds, ACU

Total Assets/Liabilities

© 2015 Deloitte & Touche LLP. All rights reserved.

2. Removal of amounts due from/to banks Pertinent proposed revisions

10

Vostro accounts & interbank takings to report under

“Deposits and Balances”

Nostro accounts & interbank lending/placements to report under

“Cash and Balances”

Loans to banks to report under

"Loans and Advances"

Reporting should instead be guided by nature of transactions in financial reporting

© 2015 Deloitte & Touche LLP. All rights reserved.

3. Accrued interest receivable and payable

Pertinent proposed revisions

11

Current

610

Proposed

610

Accrued interest usually recorded and classified separately in “Other

Assets” and “Other

Liabilities” in Statement

of Financial Position

Accrued interest to be included in the outstanding amounts of the underlying assets or liabilities

MAS Response This approach would result in uniform treatment of accrued interest across all interest-bearing assets and liabilities.

© 2015 Deloitte & Touche LLP. All rights reserved.

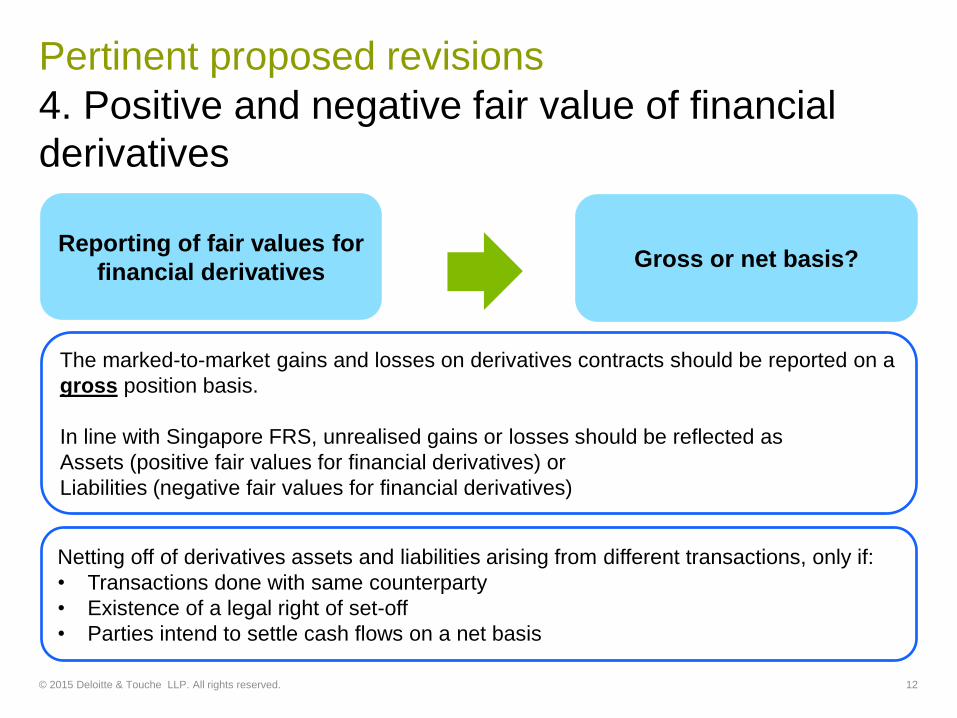

4. Positive and negative fair value of financial derivatives

Pertinent proposed revisions

12

Reporting of fair values for financial derivatives Gross or net basis?

The marked-to-market gains and losses on derivatives contracts should be reported on a gross position basis. In line with Singapore FRS, unrealised gains or losses should be reflected as Assets (positive fair values for financial derivatives) or Liabilities (negative fair values for financial derivatives)

Netting off of derivatives assets and liabilities arising from different transactions, only if: • Transactions done with same counterparty • Existence of a legal right of set-off • Parties intend to settle cash flows on a net basis

© 2015 Deloitte & Touche LLP. All rights reserved.

5. Reporting of immediate vs ultimate borrower basis (Appendix D1 vs D2)

Pertinent proposed revisions

13

Immediate borrower

Ultimate borrower

• Direct counterparty that the bank deals/transacts with

• The party bearing the ultimate risk and control of the counterparty dealt with

* No specific definitions provided in MAS sources and above definitions are based on DT’s interpretation.

© 2015 Deloitte & Touche LLP. All rights reserved.

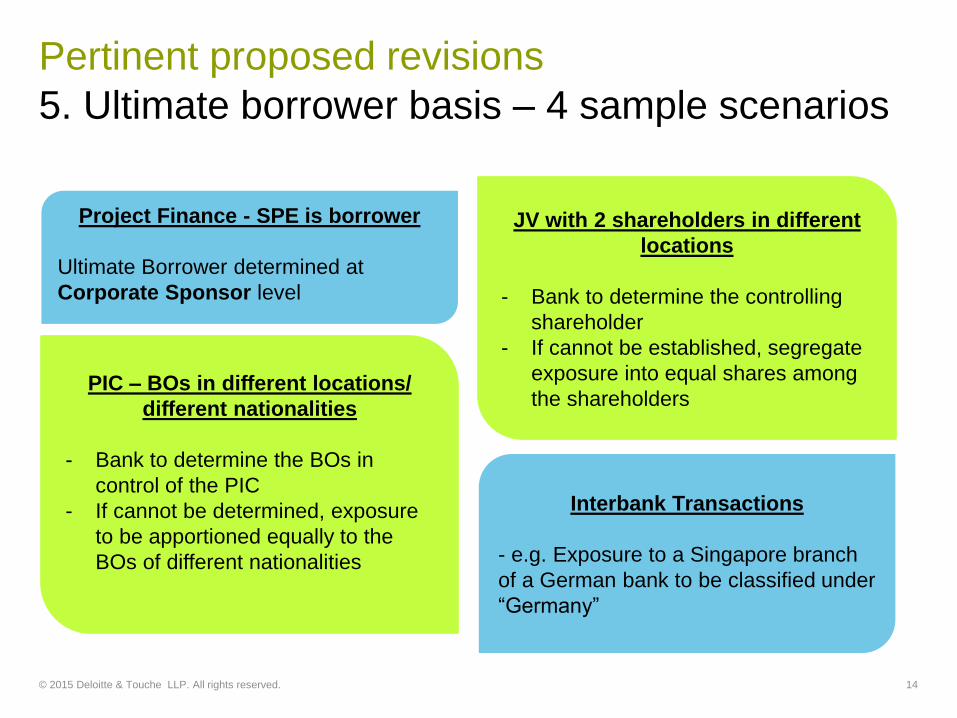

5. Ultimate borrower basis – 4 sample scenarios Pertinent proposed revisions

14

Project Finance - SPE is borrower Ultimate Borrower determined at Corporate Sponsor level

Interbank Transactions - e.g. Exposure to a Singapore branch of a German bank to be classified under “Germany”

PIC – BOs in different locations/ different nationalities

- Bank to determine the BOs in

control of the PIC - If cannot be determined, exposure

to be apportioned equally to the BOs of different nationalities

JV with 2 shareholders in different locations

- Bank to determine the controlling

shareholder - If cannot be established, segregate

exposure into equal shares among the shareholders

© 2015 Deloitte & Touche LLP. All rights reserved.

5. Immediate borrower basis – 4 transaction-type classification scenarios

Pertinent proposed revisions

15

All transactions unless specifically stated

- Classified by Residency of the

counterparty

Equity and bond investments - Based on the country of

incorporation and registration of the issuer.

Bills

- Based on the residence of the drawee of the bills as the drawee is the final recipient of the credit extended.

Positions vis-à-vis international organisations

- To report separately as distinct

geographical group

© 2015 Deloitte & Touche LLP. All rights reserved.

5. Reporting of immediate vs ultimate borrower basis (Appendix D1 vs D2)

Pertinent proposed revisions

16

For Ultimate Borrower(country where the ultimate risk resides) basis, to report exposures by country and by counterparty in one Appendix D1, on all currencies basis. Additional requirement to identify exposures to state owned banks.

For Immediate Borrower(country of residence of borrower) basis, to report exposures by country and by counterparty in 8 different Annexes of Appendix D2. Annex 1 : all currencies basis Annex 2 – 8 : SGD, USD, EUR, JPY, GBP, CHF & RMB respectively Further industry classification required for exposures to Corporates via Loans & Advances and Bills Discounted or Purchased

© 2015 Deloitte & Touche LLP. All rights reserved.

5. Guidance provided Pertinent proposed revisions

17 © 2015 Deloitte & Touche LLP. All rights reserved.

New annexes with entirely new reporting requirements

18 © 2015 Deloitte & Touche LLP. All rights reserved.

Entirely new annexes

19

Annexes Significant effort Moderate effort

1 Appendix B1 Annex 5 Intangible Assets

2 Appendix B2 Annex 3 Part III ACU Total Assets/Liabilities

3 Appendix B2 Annex 4 Reserves by Type

4 Appendix B3 Annex 5 Assets Pledged

5 Appendix B3 Annex 6 Special Purpose Entities

6 Appendix E Annex 1 Islamic Banking

7 Appendix F Annex 1 Asset Ageing Analysis by Counterparty and by Purpose

8 Appendix I Part VI Turnover by Execution Method – G10, Non-G10, SGD

*Assumption: FIs carry out activities which require reporting for the above returns

© 2015 Deloitte & Touche LLP. All rights reserved.

1. Appendix B1 Annex 5 – Intangible assets Proposed revisions

Extraction from GL

Moderate effort ?

© 2015 Deloitte & Touche LLP. All rights reserved. 20

2. Appendix B2 Annex 3 Part III – ACU Total Assets/Liabilities

Proposed revisions

21

Requires expansion of existing reporting requirement – Contingent Liabilities and Commitments

Requires expansion of existing reporting requirement – Contingent Liabilities

and Commitments

Moderate effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

3. Appendix B2 Annex 4 – Reserves by type Proposed revisions

22

Required extraction from GL

Moderate effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

4. Appendix B3 Annex 5 – Assets pledged Proposed revisions

© 2015 Deloitte & Touche LLP. All rights reserved. 23

Further work is required to be performed from the FS

disclosure

Moderate effort ?

5. Appendix B3 Annex 6 – Special purpose entities

Proposed revisions

24

- Identify parties with the information to be reported

- Additional processes required to obtain the information

Significant effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

6. Appendix E Annex 1 – Islamic banking Proposed revisions

25

Information in this return supplements the information already submitted in Appendix B1 & B2

Requires banks to track related information

Moderate effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

7. Appendix F Annex 1 – Asset ageing analysis Proposed revisions

26

Ageing by days

Significant effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

8. Appendix I Part VI - FX & IRD execution method

Proposed revisions

27

Requires reporting for G10, non-G10

currencies and SGD

More onerous reporting elements, how are banks going to capture these

data?

Are banks even tracking this currently?

Significant effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

New annexes with expanded scope

28 © 2015 Deloitte & Touche LLP. All rights reserved.

29

Annexes Significant Effort Moderate Effort

1 Appendix B1 Annex 6 Properties and Equipment

2 Appendix B3 Annex 2 Corporate Finance Activity

3 Appendix B3 Annex 3 AUM and Assets Held Under Custody

4 Appendix G Annexes 1,2,3 Interest Rate Re-pricing

5 Appendix H Property Loan to Value Ratio

Annexes with expanded scope

© 2015 Deloitte & Touche LLP. All rights reserved.

1. Appendix B1 Annex 6 – Properties and equipment

Proposed revisions

30

Required extraction from FS

Moderate effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

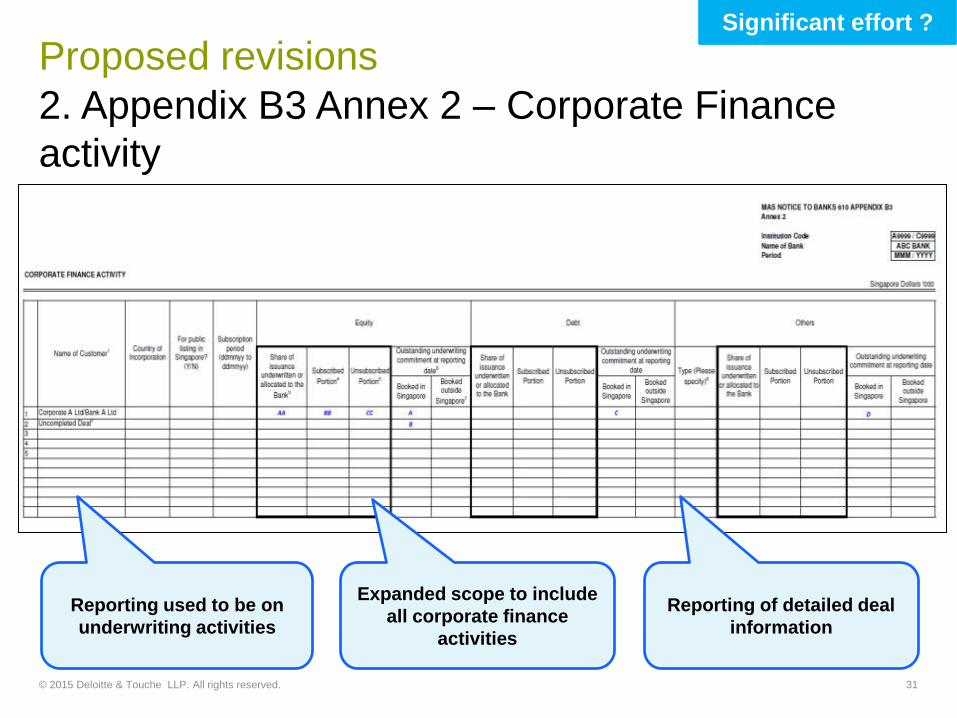

2. Appendix B3 Annex 2 – Corporate Finance activity

Proposed revisions

31

Expanded scope to include

all corporate finance activities

Reporting of detailed deal

information

Reporting used to be on underwriting activities

Significant effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

3. Appendix B3 Annex 3 – AUM and assets held under custody

Proposed revisions

32

Only required categorisation by discretionary/non-discretionary in

the past. More effort required to segregate the information that is required for the

reporting

Significant effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

4. Appendix G – Interest rate re-pricing Proposed revisions

33

Requires identification interest rate sensitive value to be reported in more

granular time buckets

Line items expanded

Significant effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

5. Appendix H – Property loan to valuation ratio Proposed revisions

34

Expanded LTV buckets

Separate reporting for different property types: • Residential • Commercial • Industrial • Others

Moderate effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

Annexes with additional dimensions on existing reported data

35 © 2015 Deloitte & Touche LLP. All rights reserved.

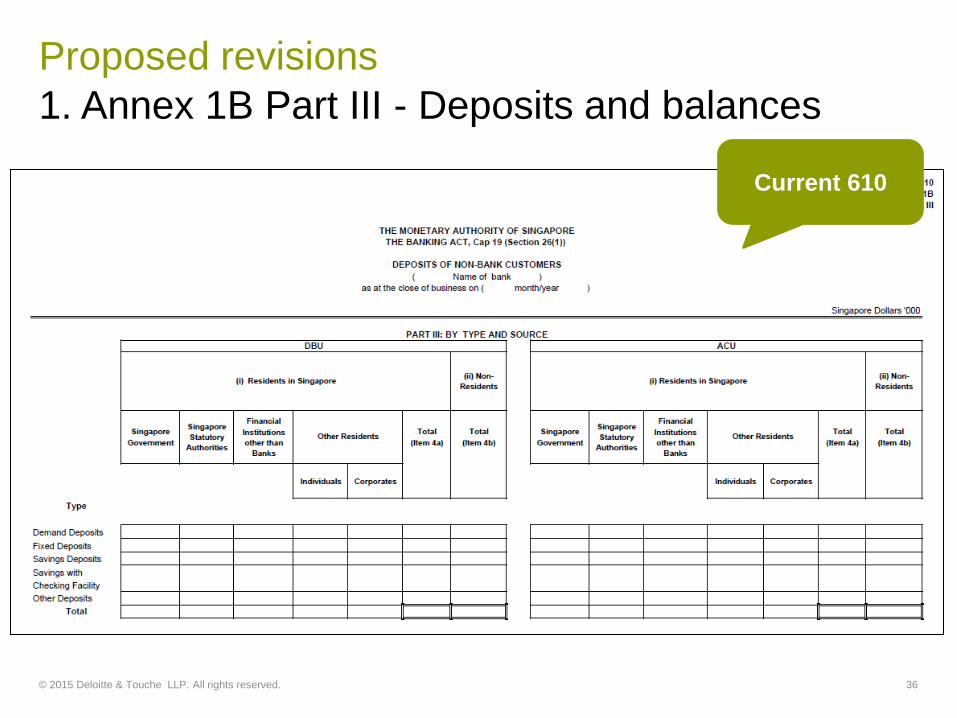

1. Annex 1B Part III - Deposits and balances Proposed revisions

36

Current 610

© 2015 Deloitte & Touche LLP. All rights reserved.

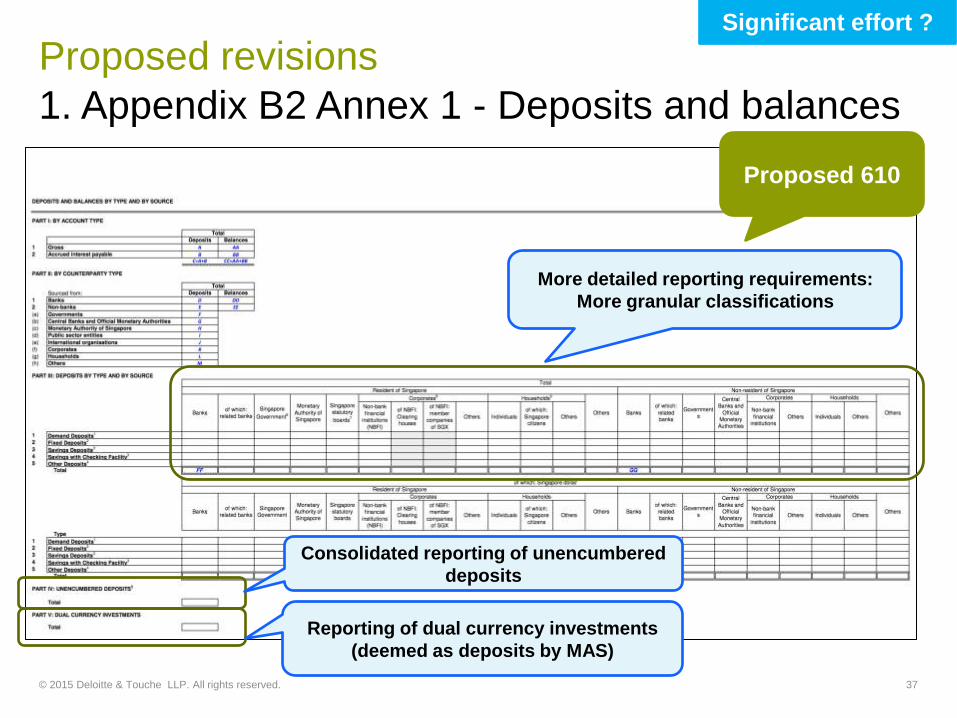

1. Appendix B2 Annex 1 - Deposits and balances Proposed revisions

37

More detailed reporting requirements: More granular classifications

Consolidated reporting of unencumbered deposits

Reporting of dual currency investments (deemed as deposits by MAS)

Proposed 610

Significant effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

2. Annex 1B Part I,II - Deposits and balances Proposed revisions

38

Current 610

© 2015 Deloitte & Touche LLP. All rights reserved.

2. Appendix B2 Annex 2 – Deposits and balances Proposed revisions

39

Proposed 610

Reporting of deposit rate of SGD-denominated deposits

Reporting range broadened

New!

Moderate effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

3. Current 610 Section C Proposed revisions

40

Current 610

© 2015 Deloitte & Touche LLP. All rights reserved.

3. Appendix B3 Annex 1A – Definition of “Contingent liabilities”

Proposed revisions

41

“Bills for collection” no longer

required to be reported in the proposed 610

Expanded, specific categories

MAS has clarified and items listed on the left (Appendix B3 Annex 1A)

are defined as “Contingent

Liabilities”

Proposed 610

Moderate effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

3. Appendix B3 Annex 1B – Definition of “Commitments”

Proposed revisions

42

MAS has clarified items listed on the left (Appendix B3 Annex 1B)

defined as “Commitments”

Reporting by maturity dates

Proposed 610

Moderate effort ?

© 2015 Deloitte & Touche LLP. All rights reserved. 42

4. Current 610 Derivatives Contracts (Annex 1G) Proposed revisions

43

Current 610

© 2015 Deloitte & Touche LLP. All rights reserved.

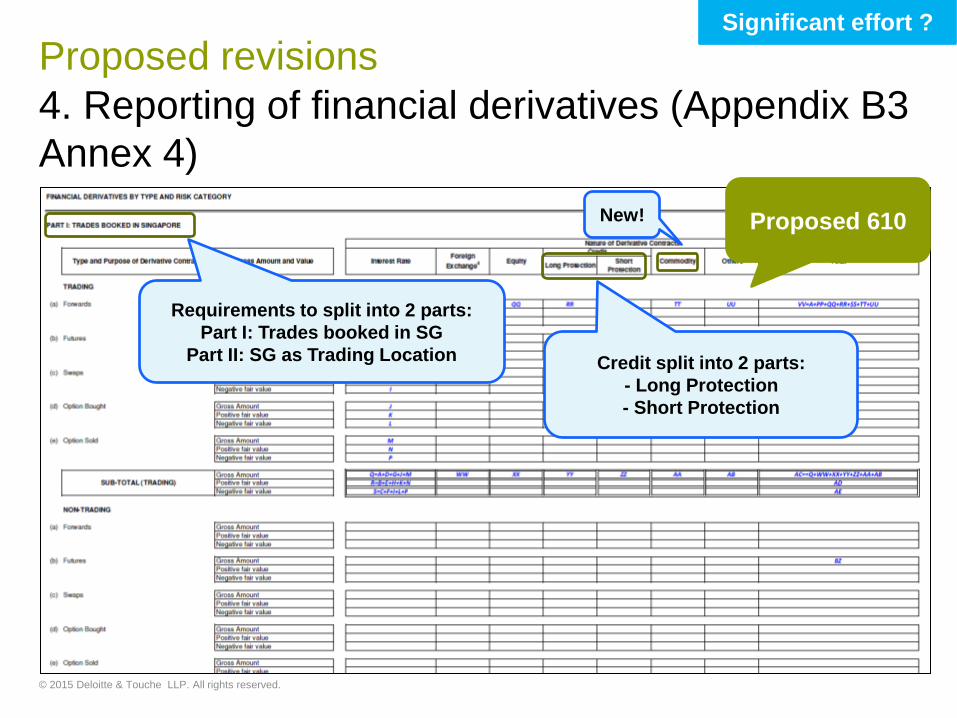

4. Reporting of financial derivatives (Appendix B3 Annex 4)

Proposed revisions

44

Proposed 610

Credit split into 2 parts: - Long Protection - Short Protection

New!

Requirements to split into 2 parts: Part I: Trades booked in SG

Part II: SG as Trading Location

Significant effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

5. Classification of exposures (Appendix 3) Proposed revisions

45

Current 610

© 2015 Deloitte & Touche LLP. All rights reserved.

5. Assets classification (Appendix F Annex 2) Proposed revisions

46

10

Proposed 610

Reporting by asset classes

NEW!

Significant effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

6. Assets by MAS 612 Classification (Appendix F Annex 3)

Proposed revisions

47

Proposed 610

Multi-dimensional reporting requirements

Significant effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

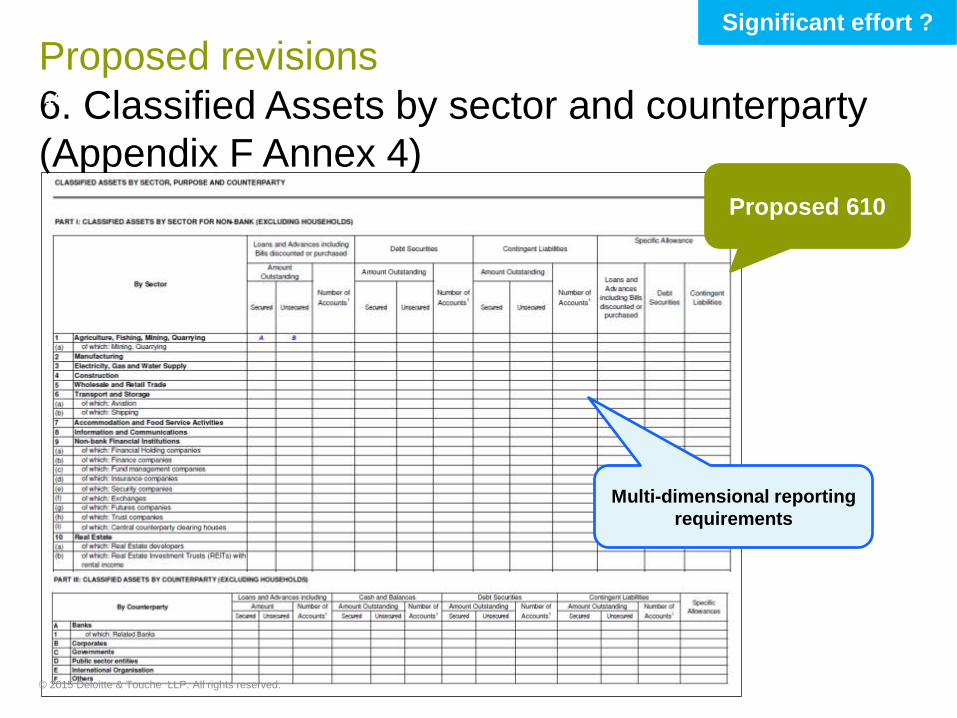

6. Classified Assets by sector and counterparty (Appendix F Annex 4)

Proposed revisions

48

10

Proposed 610

Multi-dimensional reporting requirements

Significant effort ?

© 2015 Deloitte & Touche LLP. All rights reserved.

Reporting requirements

49 © 2015 Deloitte & Touche LLP. All rights reserved.

General submission deadline

Reporting requirements

© 2015 Deloitte & Touche LLP. All rights reserved. 50

Reporting forms Submission deadline

Monthly T+10

Quarterly T+30

Half-Yearly T+30

Yearly T+30

For the quarterly/half-yearly/yearly consolidated and standalone reporting forms for locally-incorporated banks (other than foreign-owned)

T+45

Reporting forms – Proposed 610

Reporting requirements

51

Total number of reportable annexes

Foreign Banks

Local Banks

Bank Level Group Level SG

Operations Overseas

Subsidiaries Overseas Branches

Fre

qu

ency

of

Rep

ort

ing

Monthly 23 - - 21

Quarterly 33 23 26 33 19 15

Half-Yearly

8 9 9 8 1 1

Yearly - 4 4 9 10

56

64

32

36

35

39

54

62

20

29

16

26

© 2015 Deloitte & Touche LLP. All rights reserved.

Key challenges in reporting

52 © 2015 Deloitte & Touche LLP. All rights reserved.

Banks are under increasing pressure to reassess their approach

Key challenges in delivering regulatory reporting

© 2015 Deloitte & Touche LLP. All rights reserved. 53

Regulator driven

challenges

Automation & data

challenges

Organisation & governance

challenges

• Requirements of regulators are evolving rapidly, constant changes and updates will be the new norm

• Inconsistent regulatory guidelines across countries makes regulatory reporting a complex task for global and regional banks

• Regulator becoming more specific and granular to the calculations done behind each number

• Readily available data in order to meet regulator requirements

• Disparate data sources and inconsistent data

• Increasing appetite for more granular and traceability of data

• Temporary tactical solutions and non-scalable manual and fragmented processes

• Lack of coordinated and common response across LOBs, products and geographies

• Lack of integration between risk, finance and operational function areas

• Lack of capacity within regulatory reporting teams to fulfill demands of regulator requirements

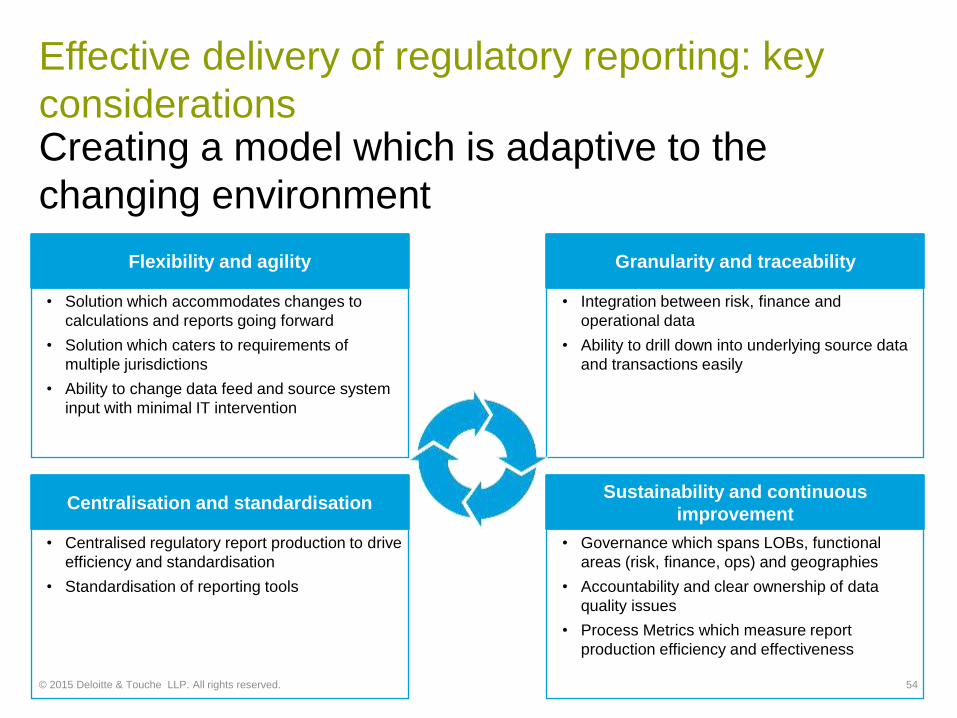

Creating a model which is adaptive to the changing environment

Effective delivery of regulatory reporting: key considerations

© 2015 Deloitte & Touche LLP. All rights reserved. 54

Flexibility and agility

• Solution which accommodates changes to calculations and reports going forward

• Solution which caters to requirements of multiple jurisdictions

• Ability to change data feed and source system input with minimal IT intervention

Centralisation and standardisation

• Centralised regulatory report production to drive efficiency and standardisation

• Standardisation of reporting tools

Granularity and traceability

• Integration between risk, finance and operational data

• Ability to drill down into underlying source data and transactions easily

Sustainability and continuous improvement

• Governance which spans LOBs, functional areas (risk, finance, ops) and geographies

• Accountability and clear ownership of data quality issues

• Process Metrics which measure report production efficiency and effectiveness

Centralising and standardising regulatory reporting efforts

Evolution of regulatory reporting service delivery models

© 2015 Deloitte & Touche LLP. All rights reserved. 55

1. Regulatory reporting relationship management

• Dedicated function which faces off to the regulator

• Manages the expectations of regulators and their requests for adhoc reporting and queries

2. Local regulatory reporting team

• Onshore team focused primarily on report adjustments and reconciliations

• Responds to adhoc reporting queries from regulators

• Gathers requirements for new reports

3. Regional regulatory reporting production team

• Centre of Excellence which manages the production and delivery of regulatory reports for multiple legal entities and lines of business.

• Centralised reporting is underpinned by common data sets and regulatory reporting applications

4. Finance technology & data • Cross functional reporting data

governance

• Report specification and design

• Report build and test

• Report maintenance

• Data extraction for adhoc queries

Building flexible data and reporting infrastructure Data and reporting infrastructure

© 2015 Deloitte & Touche LLP. All rights reserved. 57

• Map out common data sets that are leveraged as input across different regulatory reports

• Single source of data for risk and finance, utilising a single risk and finance data warehouse

• In-memory computing

• Rules engine driven report generation takes into account, regime specific, asset class specific or event specific rules to generate reports

• Automated reconciliation of recurring standard adjustments

• Intelligent and flexible routing of automated reports means they can be submitted to multiple regulators in appropriate formats

Strengthening governance to meet increasing data requirements

Data and reporting governance

© 2015 Deloitte & Touche LLP. All rights reserved. 58

Data ownership

Data quality

Data timeliness

• Identification of data sets which are common across regulatory reports and normalise to the most trusted source

• Classification of key data elements to inform priority

• Creation of consistent data definitions

• Enterprise data governance across risk, finance and operations with linkage back to LOBs

• Clear accountabilities for data ownership from contributing functional areas

• Governance adapts to new regulations and engage new data stakeholders

• Data validation pushed upstream to data contributors

• Implement data quality metrics upstream

• Determine the frequency of data required based on nature of what is being measured

Promoting service delivery excellence through process metrics

Monitoring and continuous improvement

© 2015 Deloitte & Touche LLP. All rights reserved. 59

Volume and productivity

Timeliness

Effort (Cost)

Quality

Level 3 Metrics Level 2 Metrics Level 4 Metrics Driver

% of units produced overdue: Volume of local entity (regulatory and non-regulatory) reports submitted post required deadline

Volume of local entity regulatory reports submitted post required deadline, by regulatory body: MAS

Volume of local entity regulatory reports submitted post required deadline, to MAS by entity: wholesale bank

Volume of local entity regulatory reports submitted post required deadline

Level 5 Metrics

CFO process metrics

dashboard

EXAMPLE

The transformation journey ahead

Implementation approach

© 2015 Deloitte & Touche LLP. All rights reserved. 60

Medium term Long term Strategic

• Centralisation of risk and regulatory report production across countries

• Establishment of standard reporting and data governance

• Definition of consistent data definitions

• Development of common control framework

• Standardisation of reporting processes through common reporting applications

• Continuous improvement through process metrics

• Data-warehouse for risk and finance

Speakers’ profile

61 © 2015 Deloitte & Touche LLP. All rights reserved.

Risk & Regulatory Advisory Leader, Deloitte Singapore +65 6224 8288 [email protected] Ei Leen is an Assurance and Advisory Partner with Deloitte’s Financial Services

practice in Singapore and leads the Regulatory Advisory team. Ei Leen has more than 19 years of experience in public accounting in Singapore and the US, providing assurance and advisory services to clients in the financial services industry. She has also provided regulatory advisory services to clients in the financial services industry, including banking, capital markets and insurance sectors, and has worked on numerous projects pertaining to compliance reviews as well as review of remediation of regulator’s inspection

findings.

Giam Ei Leen

Speaker’s profile

© 2015 Deloitte & Touche LLP. All rights reserved. 62

Carene Siew, Senior Manager, Risk & Regulatory Compliance Advisory, Deloitte Singapore +65 6224 8288 [email protected] Carene is a Senior Manager with the Risk and Regulatory Advisory Services within the Financial Services practice in Deloitte Singapore. Carene brings with her 17 years of experience in the banking industry, with 15 years spent in MAS. While in MAS, Carene was responsible for on-going regulatory and prudential supervision of a portfolio of banking institution, in which she had identified and supervised problematic banks and instituted corrective actions. She has also performed on-site inspection on a wide portfolio of financial institutions and in the process shared best practices with them on their risk management and control framework.

Carene Siew

Speaker’s profile

© 2015 Deloitte & Touche LLP. All rights reserved. 63

Speaker’s profile

64

Senior Manager, Consulting, Deloitte Southeast Asia +65 6224 8288 [email protected] Simon is a Senior Manager from our consulting practice and has over 13 years of Financial Services Management Consulting experience across Asia and Australia. His focus is on operational excellence and has managed end-to-end delivery of key business transformation initiatives including changes to banking operating models to achieve growth, efficiency and risk/regulatory outcomes. Simon guides and advises clients on making the right decisions for their future business operating model and investments in future business capabilities whilst working with multiple stakeholders to ensure alignment and a common direction.

Simon Tong

© 2015 Deloitte & Touche LLP. All rights reserved.

65

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/sg/about for a more detailed description of DTTL and its member firms. Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 210,000 professionals are committed to becoming the standard of excellence. About Deloitte Southeast Asia Deloitte Southeast Asia Ltd – a member firm of Deloitte Touche Tohmatsu Limited comprising Deloitte practices operating in Brunei, Cambodia, Guam, Indonesia, Lao PDR, Malaysia, Myanmar, Philippines, Singapore, Thailand and Vietnam – was established to deliver measurable value to the particular demands of increasingly intra-regional and fast growing companies and enterprises. Comprising over 270 partners and 6,300 professionals in 24 office locations, the subsidiaries and affiliates of Deloitte Southeast Asia Ltd combine their technical expertise and deep industry knowledge to deliver consistent high quality services to companies in the region. All services are provided through the individual country practices, their subsidiaries and affiliates which are separate and independent legal entities. About Deloitte Singapore In Singapore, services are provided by Deloitte & Touche LLP and its subsidiaries and affiliates. This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte network”) is, by

means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication. Deloitte & Touche LLP (Unique entity number: T08LL0721A) is an accounting limited liability partnership registered in Singapore under the Limited Liability Partnerships Act (Chapter 163A). © 2015 Deloitte & Touche LLP