Embed Size (px)

Citation preview

Marketing: Responsibility for Profit and Growth

Dr. Dirk Buchta, Senior Partner May 17th, 2011

PwC Success Formulas

PwC

Agenda

PwC Engagement in Strategy & Marketing Consulting

Marketing – The Top Issue on the CEO Agenda

PwC Success Formulas

Seven Key Levers of Marketing for Profit and Growth

Marketing Roadmap

2

PwC

PwC Engagement in Strategy & Marketing Consulting

3

PwC

We are a global consulting leader

Global

PwC People: 161,718

PwC Advisory: 32. 344

Countries: 154

Locations: 766

4

PwC Advisory Services generate $6,1 billion revenues with 32.344 consultants .

PwC

We provide strategy and marketing consulting services to global leaders across industries

5

Industry Key global clients (examples)

Automotive General Motors, Volkswagen, Daimler, Ford Motor Company, Toyota Motor Corporation

Energy utilities &

mining

E.ON, RWE, MOL, Eni, Chevron Corporation, Royal Dutch Shell, KazMunaiGaz

National Company, CEZ, Gazprom, SOCAR, PKN Orlen, Petrochina, Federal Grid,

RusHydro, Statoil

Healthcare &

pharma Johnson & Johnson, AstraZeneca, Bayer, Sanofi-Aventis, Hoffman La Roche,

GlaxoSmithKline

Industrial

products General Electric, ThyssenKrupp, Linde, Sumitomo Corporation, Arcelor-Mittal, System

Capital Management,

Retail &

consumer Unilever, Pepsi, P&G, SAB Miller, BAT, Philip Morris, Metro, OBI, Central European

Distribution Corporation, Robert Bosch, Kraft Foods,

Financial

Services

Société Générale, Vienna Insurance Group, Generali, Commerzbank, ING, Aviva, AXA,

Deutsche Bank, Banco Santander, P KO BP, International Bank of Azerbaijan, Sberbank

TICE France Telecom, Deutsche Telecom, Vodafone, Vivendi, Telefonica, Nokia, IBM,

Siemens, Samsung, Sony, Mobilnye Telesistemy, Svyazinvest

Private equity Blackstone Group, Macquarie Group, Intermediate Capital Group, Advent International

Corporation, Samruk - Kazyna National Fund

Government EBRD, World Bank, European Union (EU), Sochi Olympic Committee

PwC

We have a strong presence in Central & Eastern Europe

Geography Revenues ($ mil) Asia 2,935

Australasia and Pacific 1,293

Central & Eastern Europe 726

Western Europe 11,062

Middle East & Africa 823

North America & Caribbean 8,952

South & Central America 778

Total 26,569

No. of employees in 2010 32,225

6,850

6,837

57,702

10,033

37,643

10,428

161,718

6

PwC

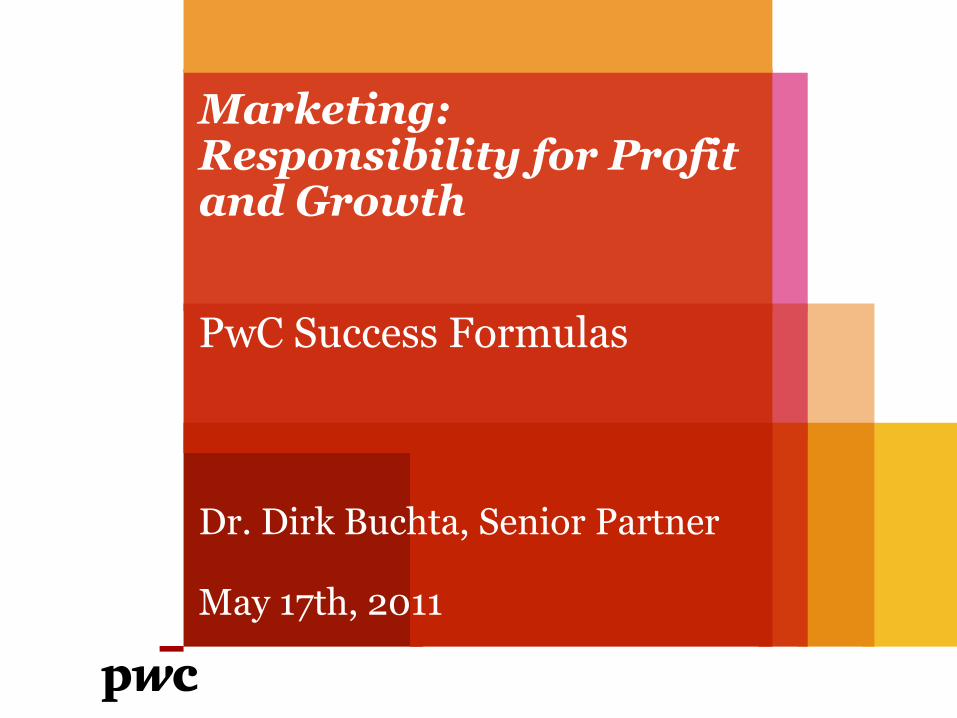

We employ more than 1.000 employees in South Eastern Europe’s and are constantly growing

Slovenia 69 Strategy 11 Deals 4 Tax & Legal 14 Assurance 40

Total SEE 1084 Strategy 60 Deals 87 Tax & Legal 354 Assurance 583

Croatia 83 Strategy 3 Deals 4 Tax & Legal 19 Assurance 57

Serbia 115 Strategy 9 Deals 14 Tax & Legal 25 Assurance 67

Bulgaria 155

Strategy 6 Deals 11 Tax & Legal 45 Assurance 93

Other SEE 86 Albania 32 Macedonia 35 Bosnia 19 Montenegro - Kosovo -

Romania 576 Strategy 31 Deals 51 Tax & Legal 224 Assurance 270

Source: iReporter YTD May 15, 2011 7

PwC

Marketing – The Top Issue on the CEO Agenda

The environment in which you have spent most, if not all of your careers, has changed.

8

PwC

Recently we have published our 14th Annual Global CEO Survey on company growth

• 1,201 global interviews were conducted between September and November 2010

• 70 countries

• Industry cuts for 15 sectors

• Quantitative research supplemented with face-to-face CEOs interviews

• You can find more insights on: http://www.pwc.com/gx/en/ceo-survey

1.201 CEOs

9

Source: PwC14th Annual Global CEO Survey

PwC

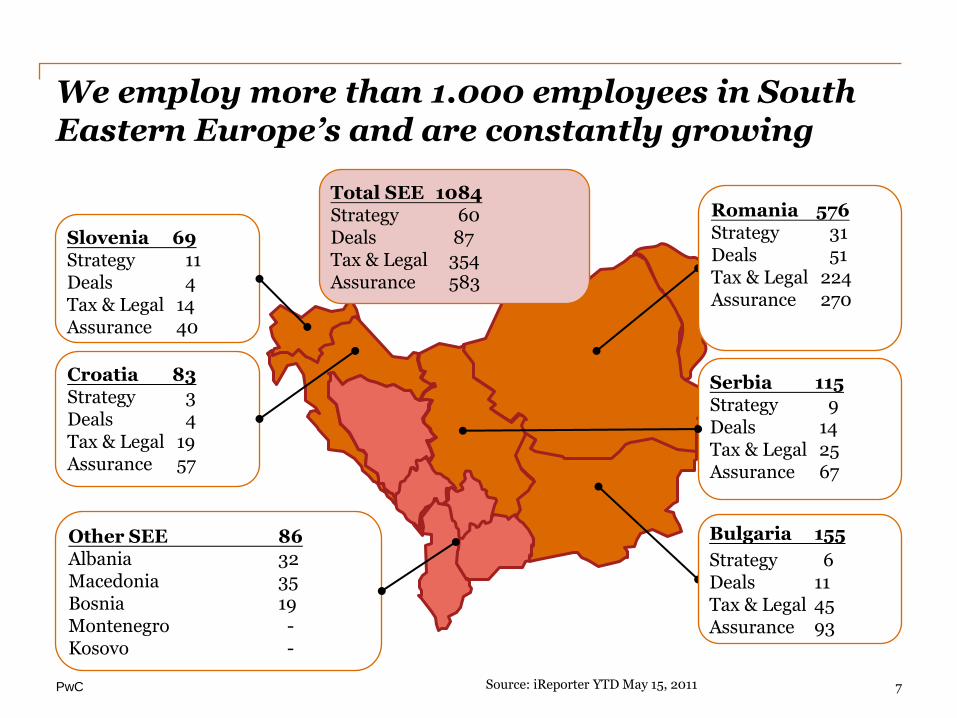

The survey proves an increasing confidence of CEOs in future growth

10

• CEO’s globally are steadily regaining their short-term confidence to near pre-crisis levels

• CEOs operating in the CEE region are slightly more optimistic regarding future growth

PwC

Most global CEOs expect Marketing to drive this growth by customer focus and innovation

78% CEOs expect their development efforts to generate ‘significant’ new revenue opportunities

11

39% CEOs expect the majority of their innovation to be co-developed with partners outside their organisation

64% CEOs view the development of environmentally friendly products and services as important part of their innovation strategy

Source: PwC14th Annual Global CEO Survey

PwC

Procter & Gamble knocks downs the barriers between organizations

Source: PwC14th Annual Global CEO Survey

‘Today, nearly every new item we bring out was produced with at least one partner somewhere in the world. For example, we co-locate scientists from partner organisations and from our organisation in the same laboratory. It’s amazing what you can do when you knock down the barriers in an organisation or the barriers between organisations.’

Bob McDonald Chairman of the Board, President and CEO, The Procter & Gamble Company, US

12

PwC

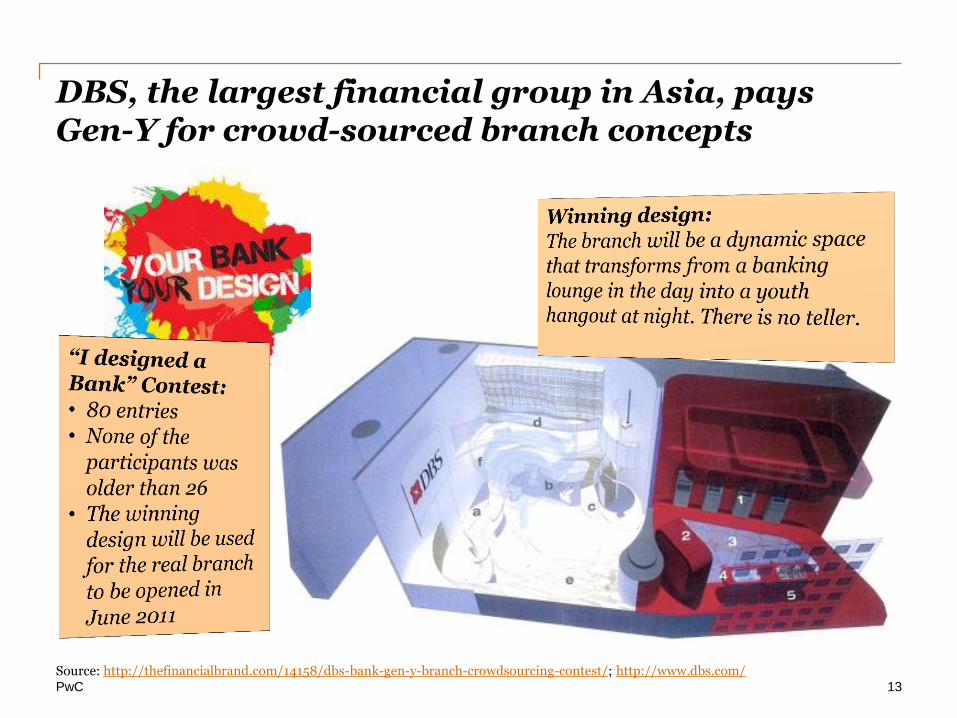

DBS, the largest financial group in Asia, pays Gen-Y for crowd-sourced branch concepts

13

Source: http://thefinancialbrand.com/14158/dbs-bank-gen-y-branch-crowdsourcing-contest/; http://www.dbs.com/

PwC

PwC Success Formulas

What are the Top Performers’ success formulas for profit and growth?

14

PwC

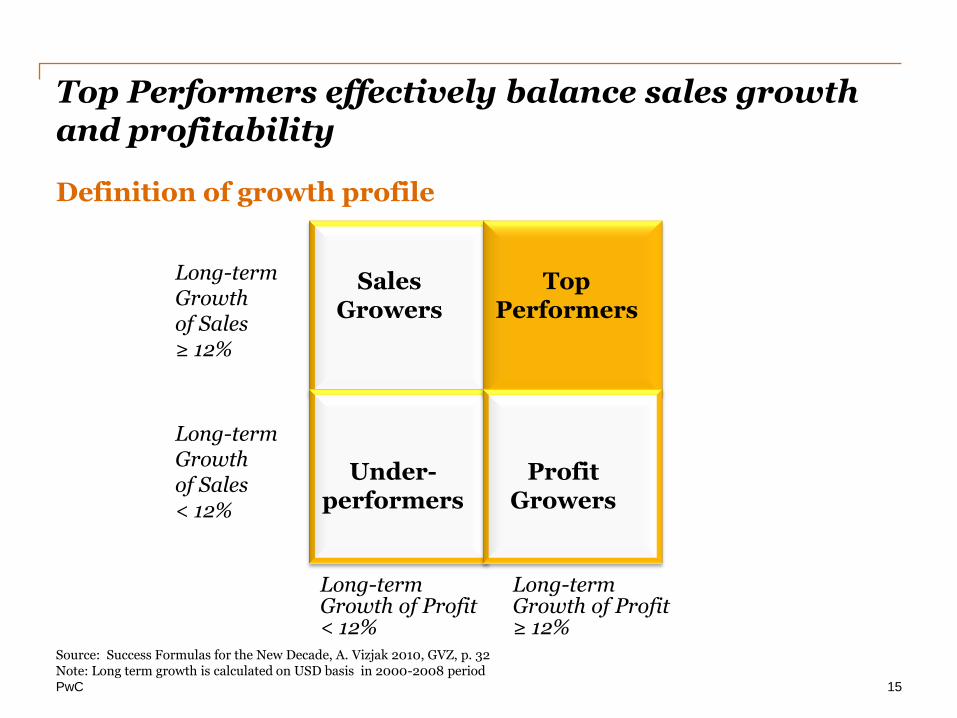

Top Performers effectively balance sales growth and profitability

15

Sales Growers

Top Performers

Profit Growers

Under- performers

Long-term Growth of Sales ≥ 12%

Long-term Growth of Sales < 12%

Long-term Growth of Profit ≥ 12%

Long-term Growth of Profit < 12%

Source: Success Formulas for the New Decade, A. Vizjak 2010, GVZ, p. 32 Note: Long term growth is calculated on USD basis in 2000-2008 period

Definition of growth profile

PwC

Among the top performers we have identified four success formulas

16

Sales Growers

Profit Growers

Under- performers

Source: Success Formulas for the New Decade, A. Vizjak 2010, GVZ

Pr

od

uc

t D

ive

rs

ific

ati

on

Internationalisation

Regional Hero

Industry Shark

Local Specialist

International Champion

Top Performers

PwC

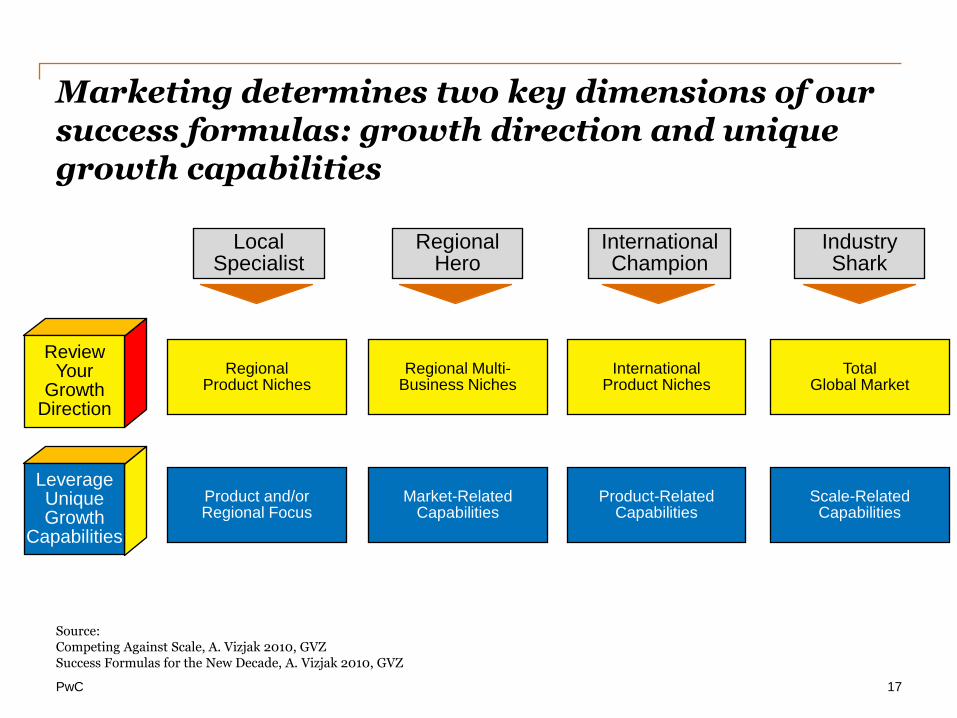

Marketing determines two key dimensions of our success formulas: growth direction and unique growth capabilities

17

Source: Competing Against Scale, A. Vizjak 2010, GVZ Success Formulas for the New Decade, A. Vizjak 2010, GVZ

Industry Shark

Local Specialist

Regional Hero

International Champion

Review Your

Growth Direction

Leverage Unique Growth

Capabilities

Regional Product Niches

Regional Multi- Business Niches

International Product Niches

Total Global Market

Product and/or Regional Focus

Market-Related Capabilities

Product-Related Capabilities

Scale-Related Capabilities

PwC

The excellent financial results of the analysed sample prove the success of all four formulas

18

Regional Heroes

Local Specialists

Industry Sharks

International Champions

Revenue growth: 10 percent

Profit growth:

11 percent

Profitability: 10 percent

Revenue growth: 19 percent

Profit growth:

22 percent

Profitability: 9 percent

Revenue growth: 18 percent

Profit growth:

17 percent

Profitability: 9 percent

Revenue growth: 16 percent

Profit growth:

19 percent

Profitability: 11 percent

KPI’s: Median values of the formula clusters Revenue growth = Sales CAGR 2000 – 2008 Profit growth =EBIT CAGR 2000 – 2008 Profitability = EBIT on Assets 2008

Source: Success Formulas for the New Decade, A. Vizjak 2010, GVZ

PwC

Seven Key Levers of Marketing for Profit & Growth

What are the marketing success drivers we learned from success formula examples?

19

PwC

Seven key levers operationalize the responsibility of Marketing for profit and growth

20 Full impact on profit drivers

Brand Management

Category Management

Customer Centricity

Product Complexity

Value Innovation

Channel Management

Cross Selling

Profit Price Volume Costs = * -

7

6

5

4

3

2

1

Partial impact on profit drivers

PwC

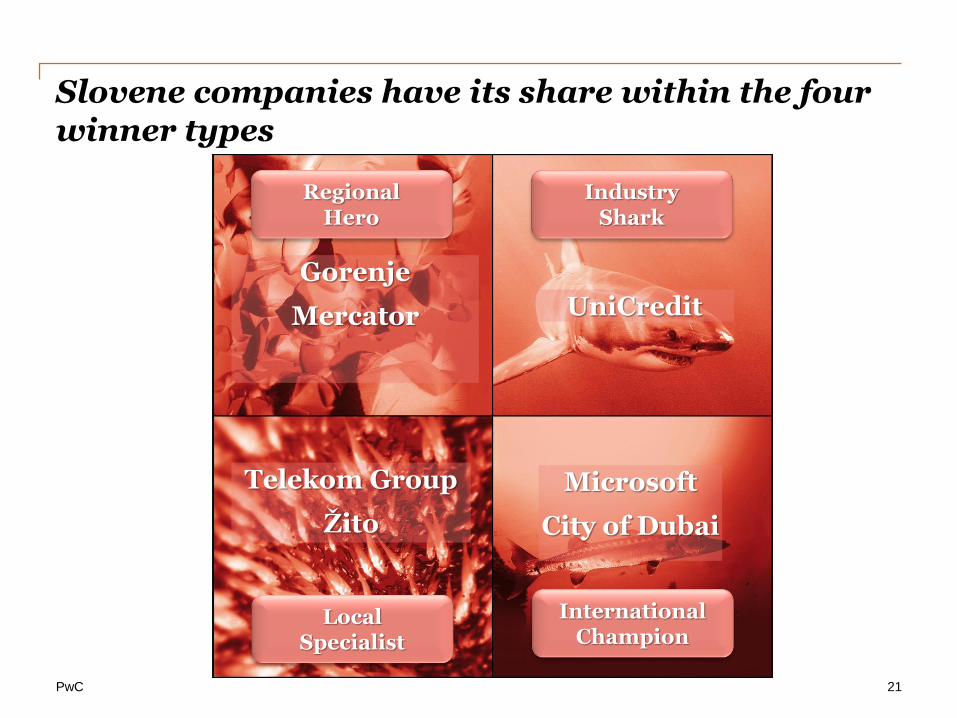

Slovene companies have its share within the four winner types

21

Regional Hero

Industry Shark

Local Specialist

International Champion

Microsoft

City of Dubai

UniCredit

Telekom Group

Žito

Gorenje

Mercator

PwC

Key Marketing Levers of a Local Specialist

22

Product Complexity

Cross Selling

Profit Price Volume Costs = * -

7

4 Telekom Group

Žito

PwC

Market segment Fixed

Telephony

Company

Market share

Market position in Slovenija

Mobile System

Solutions Internet

Marketing

Telekom Mobitel Najdi

Planet9

56 % of active users

S76 % in fixed telephony

46 % in broadband

#1

Avtenta

#1 #1

Pay TV

TS/Planet9

26 %

#2 #5

45 % 11 %

Telekom Group has a leading position in Slovenia

23

Source: APEK, Annual Report Skupine TS 2009

Cross Selling

PwC

Žito reduced the product complexity with direct impact on manufacturing and overhead costs

24

Brands/ Products

Understand Complexity

Drivers

Set Complexity

Rules

Calculate Impact

Product revenues per channel

Product revenues

Profitability targets

# channels per product

Manufacturing costs

Labour costs

Product features

Channels

Manufacturing

# SKU

# SKU

# SKU

# SKU

Product Complexity

Grajske pekarne

Zlato polje

Maestro

Gorenjka

Source: Žito

PwC

Key Marketing Levers of a Regional Hero

25

Category Management

Channel Management

Profit Price Volume Costs = * -

6

5 Gorenje

Mercator

PwC

Final Consumers

Gorenje offers home appliances & furniture: Large Household appliances, Small household appliances & kitchenwear, consumer electronics,

other home appliances (water heaters, radiators, heathing systems), furniture

Retail Shops

& E-Com- merce

of Producer

Sales to

OEMs

(original equip- ment

manu- facturers)

Independent electrical

goods specialist

retail shops

Whole- Sale

Kitchen specialist

retail shops

Kitchen manufac-

turers

Mail order

retailers

Sales force & key account managers of Producers

Hyper- markets, Depart-

ment stores

Building construc-

tion / architects

Sales agents of

Producers

Electrical goods spe- cialist re- tail chains

Do-it- yourself

Retail chains

Gorenje developed the entire range of sales channels by customizing products to individual retailers’ requirements

Channel Management

26

Source: Success Formulas for the New Decade, A. Vizjak 2010, GVZ

PwC

Source: Gorenje Annual Report 2010

Gorenje is a Regional Hero and remains a sales and profit grower even in a stagnating market

Channel Management

27

EUR million

2009 2010

Consolidated revenues

1.185,9 1.382,2

EBIT 12,1 56,4

PwC

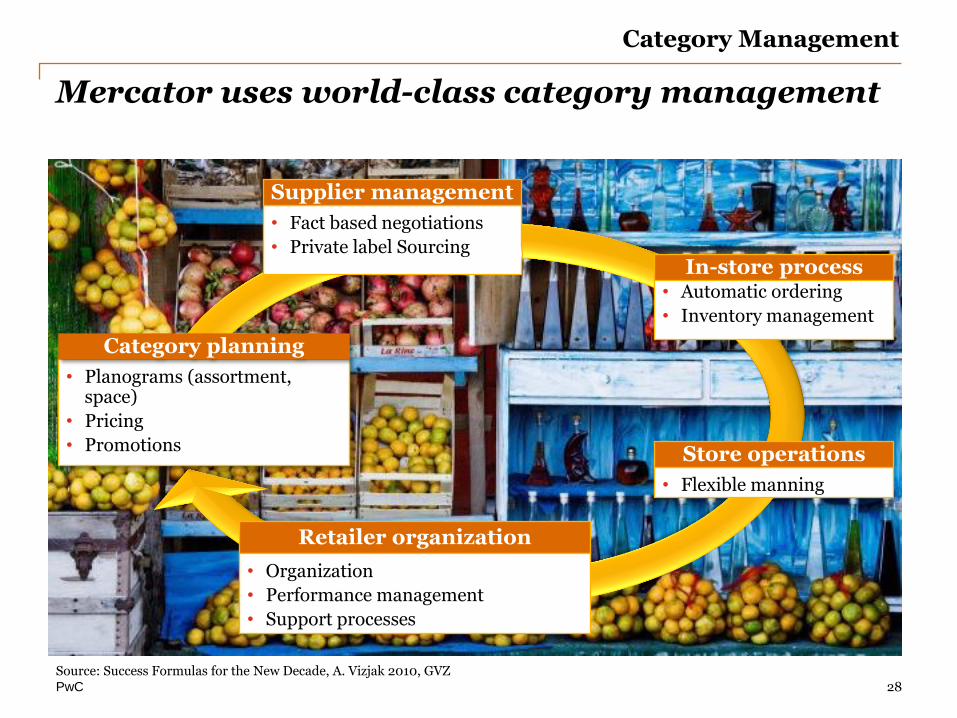

Mercator uses world-class category management

28

Retailer organization

• Fact based negotiations

• Private label Sourcing

Supplier management

• Planograms (assortment, space)

• Pricing

• Promotions

Category planning

• Organization

• Performance management

• Support processes

• Automatic ordering

• Inventory management

In-store process

• Flexible manning

Store operations

Category Management

Source: Success Formulas for the New Decade, A. Vizjak 2010, GVZ

PwC

Key Marketing Levers of an International Champion

29

Brand Management

Value Innovation

Profit Price Volume Costs = * -

3

2 City of Dubai

Microsoft

PwC

Microsoft has always been an innovation pioneer in the IT industry

Social networks, cloud computing Products > Solutions > Services

Browsers, e-mail, eCommerce, Hosting, Wi-Fi, Web 2.0

Distributed Computing

Text editor, spreadsheets DOS, graphical user interface, Windows

early 80’s mid 80’s mid 90’s 2000+

Value Innovation

30

Source: Microsoft

PwC

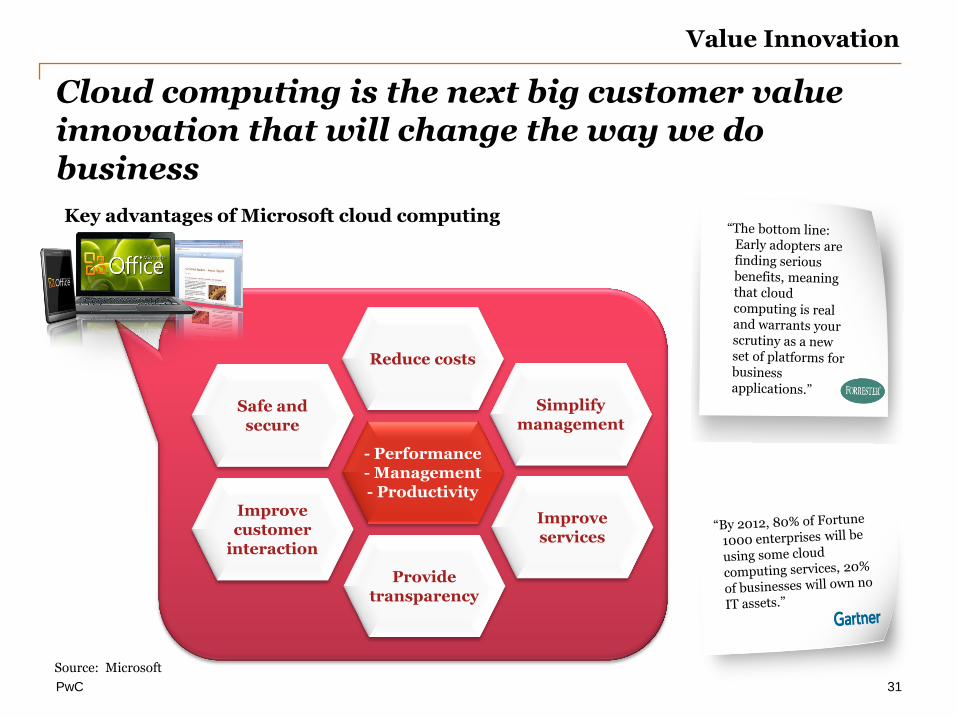

Cloud computing is the next big customer value innovation that will change the way we do business

Reduce costs

Simplify management

Safe and secure

- Performance - Management - Productivity

Improve customer

interaction

Improve services

Provide transparency

Key advantages of Microsoft cloud computing

Value Innovation

31

Source: Microsoft

PwC

Dubai established the leading global lifestyle brand of the Arab world

32

Elements of Dubai’s premier lifestyle brand

• Fun & Entertainment

• Broad variety of hotels

• Best airline (Emirates Airlines)

• Iconic buildings (Burj Al Arab, Burj Khalifa)

• Innovative approaches (e.g. Palm Island)

• Best infrastructure (e.g. Dubai Metro, electronic border control)

Brand Management

Source: Dubai Statistics Department; Gulfnews

PwC

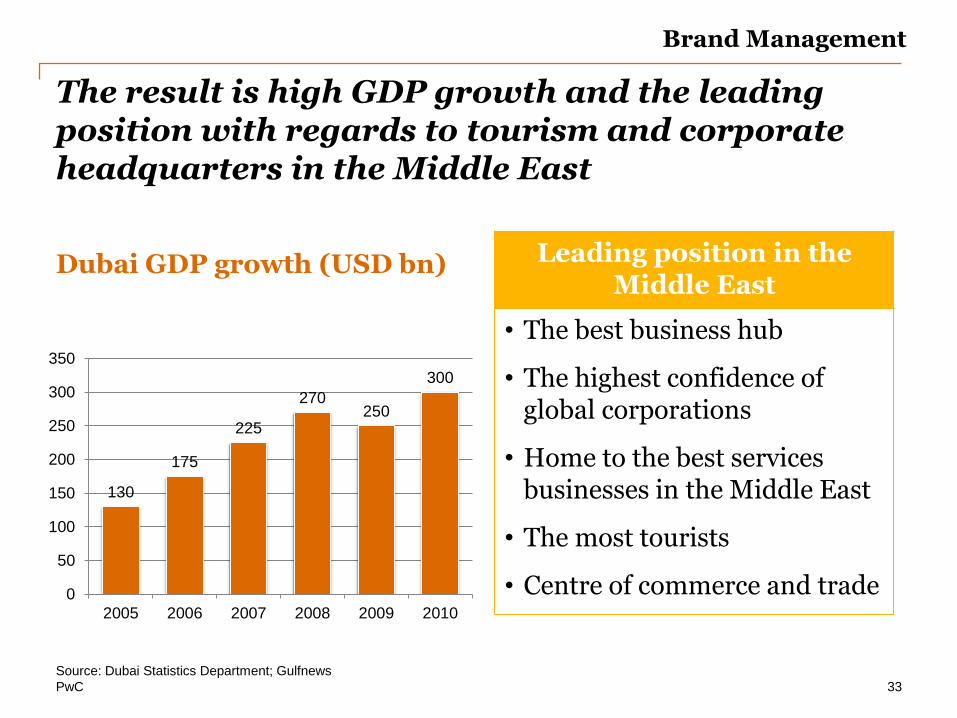

The result is high GDP growth and the leading position with regards to tourism and corporate headquarters in the Middle East

Leading position in the Middle East

• The best business hub

• The highest confidence of global corporations

• Home to the best services businesses in the Middle East

• The most tourists

• Centre of commerce and trade

Source: Dubai Statistics Department; Gulfnews

33

130

175

225

270 250

300

0

50

100

150

200

250

300

350

2005 2006 2007 2008 2009 2010

Dubai GDP growth (USD bn)

Brand Management

PwC

Key Marketing Levers of an Industry Shark

34

Customer Centricity

Profit Price Volume Costs = * -

1 UniCredit

PwC

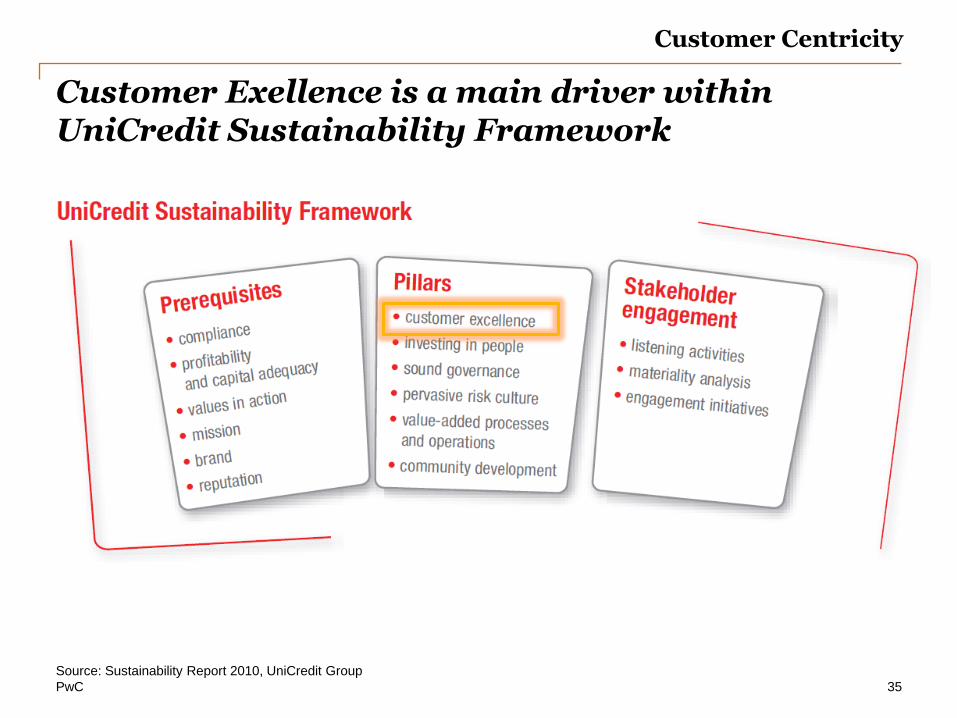

Customer Exellence is a main driver within UniCredit Sustainability Framework

Source: Sustainability Report 2010, UniCredit Group

35

Customer Centricity

PwC

UniCredit established the leading position in the region also due to its focus on customer centricity

Source: Sustainability Report 2010, UniCredit Group; Presentation to Investors, London 2010

36

Customer Centricity

UniCredit Approach to Customer Centricity

• Measured with Customer Satisfaction Index, directly linked to the incentive system for relationship managers

• Roughly 461,000 Customers interviewed in 2010

• Almost all countries in CEE scored above 70 points which is considered Excellent

PwC

Marketing Road Map

By focusing on success drivers and deploying the right capabilities, marketers can position their companies for profitable growth.

37

PwC

Regional Hero

Industry Shark

Local Specialist

International Champion

CROSS SELING

CATEGORY MANAGEMENT

CHANNEL MANAGEMENT

PRODUCT COMPLEXITY MANAGEMENT

CUSTOMER CENTRICITY

VALUE INNOVATON

BRAND MANAGEMENT

1

7

4

5

6

3

2

PwC

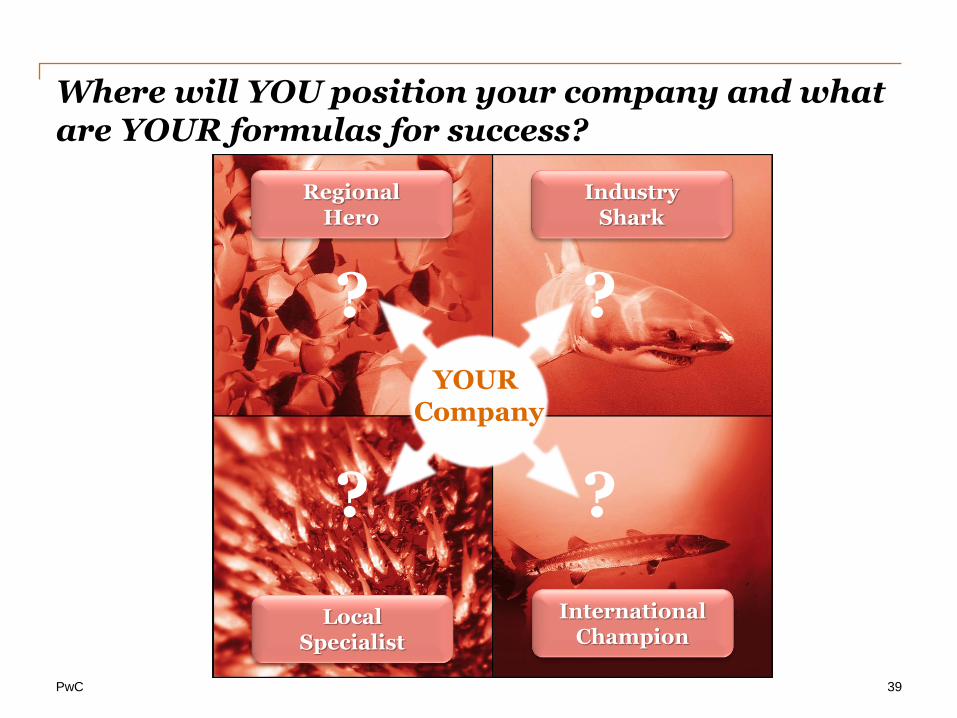

Where will YOU position your company and what are YOUR formulas for success?

39

Regional Hero

Industry Shark

Local Specialist

International Champion

YOUR Company

? ?

? ?

Thank you! Feel free to contact me at: [email protected]

This presentation has been prepared for general guidance on matters of interest only, and

does not constitute professional advice. You should not act upon the information contained in

this publication without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy or completeness of the information contained

in this publication, and, to the extent permitted by law, PricewaterhouseCoopers d.o.o., its

members, employees and agents do not accept or assume any liability, responsibility or duty of

care for any consequences of you or anyone else acting, or refraining to act, in reliance on the

information contained in this publication or for any decision based on it.

© 2011 PricewaterhouseCoopers d.o.o.. All rights reserved. In this document, “PwC” refers to

PricewaterhouseCoopers d.o.o., which is a member firm of PricewaterhouseCoopers

International Limited, each member firm of which is a separate legal entity.