Embed Size (px)

Citation preview

by Split Screen Data Ltd. for German Films July 2013

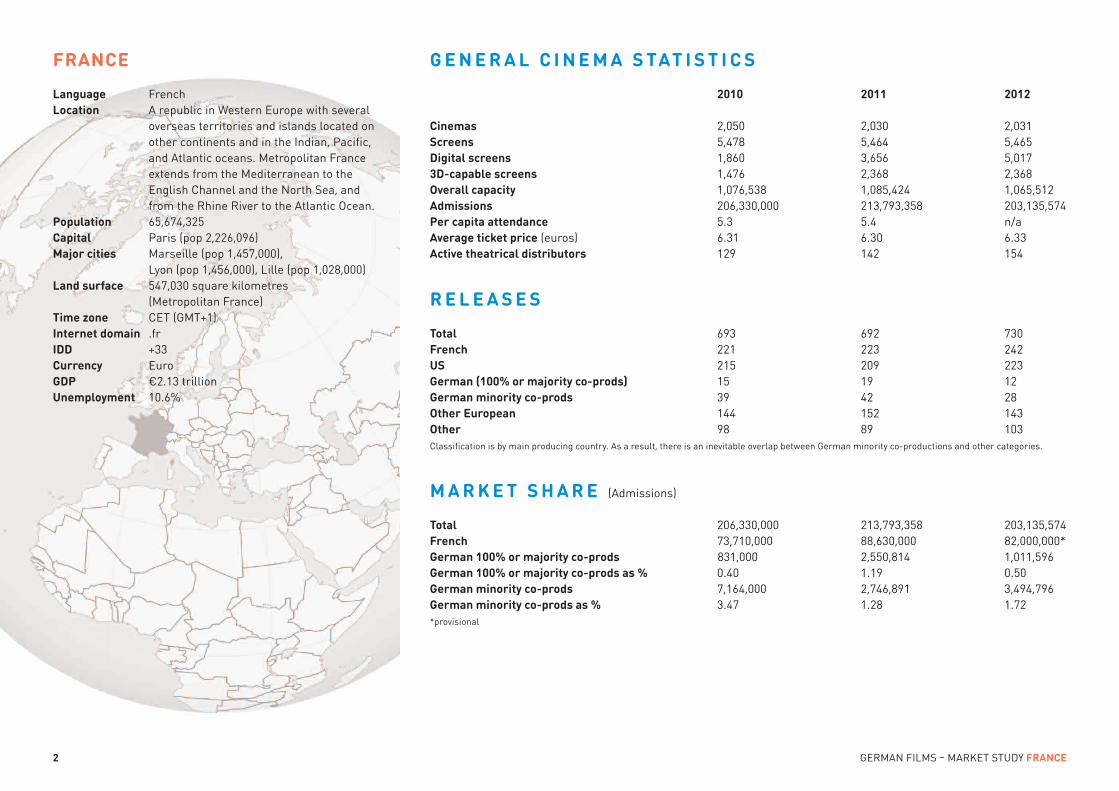

Market StudyFRANCE

2 GerMaN FILMS – Market Study FRANCE

GENERAL C INEMA STAT IST ICS

2010 2011 2012

Cinemas 2,050 2,030 2,031Screens 5,478 5,464 5,465Digital screens 1,860 3,656 5,0173D-capable screens 1,476 2,368 2,368Overall capacity 1,076,538 1,085,424 1,065,512Admissions 206,330,000 213,793,358 203,135,574Per capita attendance 5.3 5.4 n/aAverage ticket price (euros) 6.31 6.30 6.33Active theatrical distributors 129 142 154

RELEASES

Total 693 692 730French 221 223 242US 215 209 223German (100% or majority co-prods) 15 19 12German minority co-prods 39 42 28Other European 144 152 143Other 98 89 103Classification is by main producing country. as a result, there is an inevitable overlap between German minority co-productions and other categories.

MARKET SHARE (admissions)

Total 206,330,000 213,793,358 203,135,574French 73,710,000 88,630,000 82,000,000*German 100% or majority co-prods 831,000 2,550,814 1,011,596German 100% or majority co-prods as % 0.40 1.19 0.50German minority co-prods 7,164,000 2,746,891 3,494,796German minority co-prods as % 3.47 1.28 1.72*provisional

FRANCE

Language FrenchLocation a republic in Western europe with several

overseas territories and islands located on other continents and in the Indian, Pacific, and atlantic oceans. Metropolitan France extends from the Mediterranean to the english Channel and the North Sea, and from the rhine river to the atlantic Ocean.

Population 65,674,325Capital Paris (pop 2,226,096)Major cities Marseille (pop 1,457,000),

Lyon (pop 1,456,000), Lille (pop 1,028,000)Land surface 547,030 square kilometres

(Metropolitan France)Time zone Cet (GMt+1)Internet domain .frIDD +33Currency euroGDP €2.13 trillionUnemployment 10.6%

TITLE

2010 TOP 10

*aVatar (uS) Harry POtter aNd tHe deatHLy HaLLOWS: Part 1 (uS/uk) LeS PetItS MOuCHOIrS (Fr) INCePtION (uS/uk) SHrek FOreVer aFter (uS) aLICe IN WONderLaNd (uS) tOy StOry 3 (uS) CaMPING 2 (Fr) tHe tWILIGHt SaGa: eCLIPSe (uS)tHe PrINCeSS aNd tHe FrOG (uS) * released in previous year(s)

2010 GERMAN F I LMS (100% or majority co-productions in red)

La raFLe (Fr/Ger) tHe GHOSt (Fr/Ger/uk) reSIdeNt eVIL: aFterLIFe (uk/Ger/uS) La PrINCeSSe de MONtPeNSIer (Fr/Ger)tOurNÉe (Fr/Ger)SOuL kItCHeN (Ger/Fr/It) FLICkaN SOM Lekte Med eLdeN (SWe/Ger) WÜSteNBLuMe (Ger/aut)taNZtrÄuMe (Ger) Mr. NOBOdy (BeL/Fr/CaN/Ger) aJaMI (ISr/Ger/uk)uNCLe BOONMee WHO CaN reCaLL HIS PaSt LIVeS (tHaI/Ger/Fr/SP/uk)tHe COuNteSS (Fr/uS/Ger) SturM (Ger/deN/NL) WIr SINd dIe NaCHt (Ger) eNter tHe VOId (Fr/Ger/It) NINJa aSSaSSIN (uS/Ger) BaL (tur/Ger) CarLOS (Fr/Ger) NOStaLGIa de La LuZ (CHILe/Fr/Ger) WICkIe uNd dIe StarkeN MÄNNer (Ger)

RELEASE DETAILSDISTRIBUTOR

twentieth Century Fox France Warner Bros. Pictures FranceeuropaCorp distributionWarner Bros. Pictures France Paramount Pictures FranceWalt disney Studios Motion Pictures (France)Walt disney Studios Motion Pictures (France)Pathé distribution SNd Walt disney Studios Motion Pictures (France)

GaumontPathé distribution Metropolitan FilmexportStudioCanalLe PactePyramide distribution uGC distributionBac FilmsJour2FêtePathé distributionad Vitam Pyramide distribution Bac FilmseuropaCorp distributionMetropolitan FilmexportWild Bunch distributionStudioCanalBodega FilmsMk2 diffusionPyramide distributionMetropolitan Filmexport

RELEASE DATE

16.12.0924.11.1020.10.10 21.07.10 30.06.10 24.03.1014.07.10 21.04.1007.07.10 27.01.10

10.03.10 03.03.1022.09.1003.11.10 30.06.1017.03.10 30.06.1010.03.1013.10.10 13.01.10 07.04.1001.09.1021.04.1017.03.10 29.12.1005.05.1010.02.1022.09.10 07.07.1027.10.1021.07.10

ADMISSIONS

9,185,3375,506,3045,249,3454,933,5514,625,1184,533,4144,353,253 3,978,1143,940,3013,842,600

2,895,8101,048,701

911,560733,237507,406281,017273,459162,486159,369142,536140,792132,511121,31872,25660,11753,37352,91749,50045,75847,29241,244

GerMaN FILMS – Market Study FRANCE 3

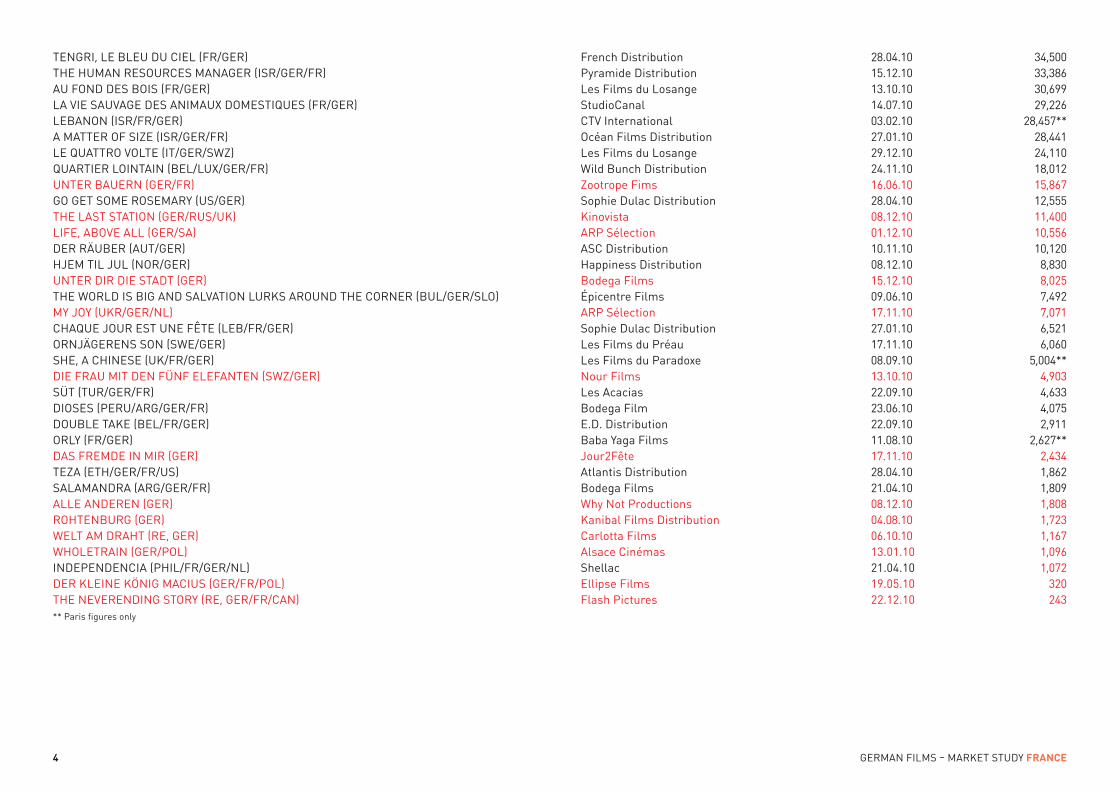

teNGrI, Le BLeu du CIeL (Fr/Ger) tHe HuMaN reSOurCeS MaNaGer (ISr/Ger/Fr) au FONd deS BOIS (Fr/Ger) La VIe SauVaGe deS aNIMauX dOMeStIQueS (Fr/Ger) LeBaNON (ISr/Fr/Ger) a Matter OF SIZe (ISr/Ger/Fr) Le QuattrO VOLte (It/Ger/SWZ) QuartIer LOINtaIN (BeL/LuX/Ger/Fr) uNter BauerN (Ger/Fr) GO Get SOMe rOSeMary (uS/Ger) tHe LaSt StatION (Ger/ruS/uk)LIFe, aBOVe aLL (Ger/Sa) der rÄuBer (aut/Ger) HJeM tIL JuL (NOr/Ger) uNter dIr dIe Stadt (Ger) tHe WOrLd IS BIG aNd SaLVatION LurkS arOuNd tHe COrNer (BuL/Ger/SLO) My JOy (ukr/Ger/NL) CHaQue JOur eSt uNe FÊte (LeB/Fr/Ger) OrNJÄGereNS SON (SWe/Ger) SHe, a CHINeSe (uk/Fr/Ger) dIe Frau MIt deN FÜNF eLeFaNteN (SWZ/Ger) SÜt (tur/Ger/Fr) dIOSeS (Peru/arG/Ger/Fr) dOuBLe take (BeL/Fr/Ger) OrLy (Fr/Ger) daS FreMde IN MIr (Ger) teZa (etH/Ger/Fr/uS) SaLaMaNdra (arG/Ger/Fr) aLLe aNdereN (Ger) rOHteNBurG (Ger) WeLt aM draHt (re, Ger) WHOLetraIN (Ger/POL) INdePeNdeNCIa (PHIL/Fr/Ger/NL) der kLeINe kÖNIG MaCIuS (Ger/Fr/POL) tHe NeVereNdING StOry (re, Ger/Fr/CaN)** Paris figures only

French distributionPyramide distributionLes Films du LosangeStudioCanalCtV International Océan Films distributionLes Films du LosangeWild Bunch distributionZootrope FimsSophie dulac distributionkinovistaarP SélectionaSC distributionHappiness distributionBodega FilmsÉpicentre FilmsarP Sélection Sophie dulac distributionLes Films du PréauLes Films du ParadoxeNour FilmsLes acaciasBodega Filme.d. distributionBaba yaga Films Jour2Fêteatlantis distributionBodega FilmsWhy Not Productionskanibal Films distribution Carlotta Films alsace CinémasShellacellipse FilmsFlash Pictures

28.04.1015.12.1013.10.1014.07.1003.02.1027.01.1029.12.10 24.11.1016.06.10 28.04.1008.12.1001.12.1010.11.1008.12.1015.12.1009.06.1017.11.10 27.01.1017.11.10 08.09.1013.10.1022.09.1023.06.1022.09.1011.08.10 17.11.1028.04.1021.04.1008.12.1004.08.1006.10.1013.01.1021.04.10 19.05.10 22.12.10

34,50033,38630,69929,226

28,457**28,44124,11018,01215,86712,55511,40010,55610,1208,8308,0257,4927,0716,5216,060

5,004**4,9034,6334,0752,911

2,627**2,4341,8621,8091,8081,7231,1671,0961,072

320243

4 GerMaN FILMS – Market Study FRANCE

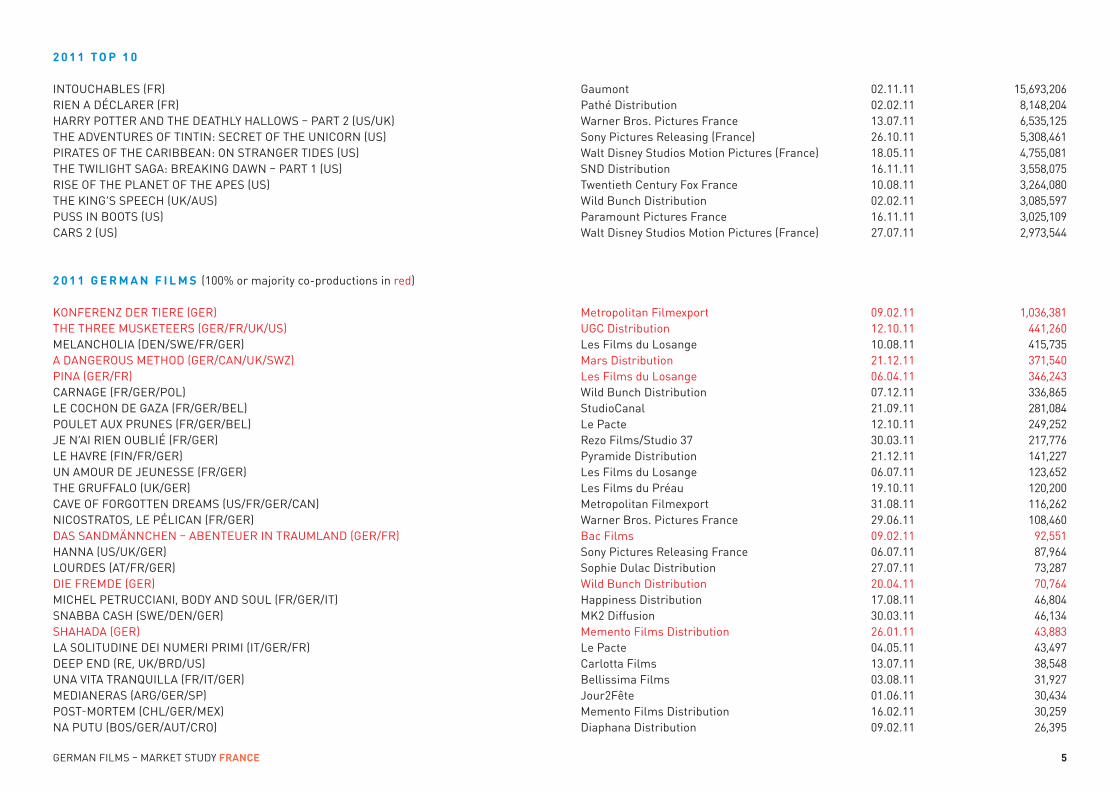

2011 TOP 10

INtOuCHaBLeS (Fr)rIeN a dÉCLarer (Fr)Harry POtter aNd tHe deatHLy HaLLOWS – Part 2 (uS/uk)tHe adVeNtureS OF tINtIN: SeCret OF tHe uNICOrN (uS) PIrateS OF tHe CarIBBeaN: ON StraNGer tIdeS (uS)tHe tWILIGHt SaGa: BreakING daWN – Part 1 (uS)rISe OF tHe PLaNet OF tHe aPeS (uS)tHe kING’S SPeeCH (uk/auS)PuSS IN BOOtS (uS)CarS 2 (uS)

2011 GERMAN F I LMS (100% or majority co-productions in red)

kONFereNZ der tIere (Ger)tHe tHree MuSketeerS (Ger/Fr/uk/uS) MeLaNCHOLIa (deN/SWe/Fr/Ger) a daNGerOuS MetHOd (Ger/CaN/uk/SWZ) PINa (Ger/Fr) CarNaGe (Fr/Ger/POL) Le COCHON de GaZa (Fr/Ger/BeL) POuLet auX PruNeS (Fr/Ger/BeL) Je N’aI rIeN OuBLIÉ (Fr/Ger) Le HaVre (FIN/Fr/Ger) uN aMOur de JeuNeSSe (Fr/Ger) tHe GruFFaLO (uk/Ger) CaVe OF FOrGOtteN dreaMS (uS/Fr/Ger/CaN) NICOStratOS, Le PÉLICaN (Fr/Ger) daS SaNdMÄNNCHeN – aBeNteuer IN trauMLaNd (Ger/Fr) HaNNa (uS/uk/Ger) LOurdeS (at/Fr/Ger) dIe FreMde (Ger) MICHeL PetruCCIaNI, BOdy aNd SOuL (Fr/Ger/It) SNaBBa CaSH (SWe/deN/Ger) SHaHada (Ger) La SOLItudINe deI NuMerI PrIMI (It/Ger/Fr) deeP eNd (re, uk/Brd/uS) uNa VIta traNQuILLa (Fr/It/Ger) MedIaNeraS (arG/Ger/SP) POSt-MOrteM (CHL/Ger/MeX) Na Putu (BOS/Ger/aut/CrO)

GaumontPathé distributionWarner Bros. Pictures FranceSony Pictures releasing (France)Walt disney Studios Motion Pictures (France)SNd distribution twentieth Century Fox FranceWild Bunch distributionParamount Pictures FranceWalt disney Studios Motion Pictures (France)

Metropolitan Filmexport uGC distributionLes Films du Losange Mars distributionLes Films du LosangeWild Bunch distributionStudioCanalLe Pacterezo Films/Studio 37Pyramide distributionLes Films du LosangeLes Films du Préau Metropolitan Filmexport Warner Bros. Pictures France Bac FilmsSony Pictures releasing FranceSophie dulac distributionWild Bunch distribution Happiness distributionMk2 diffusionMemento Films distribution Le PacteCarlotta FilmsBellissima FilmsJour2FêteMemento Films distributiondiaphana distribution

02.11.1102.02.1113.07.1126.10.1118.05.1116.11.1110.08.1102.02.1116.11.1127.07.11

09.02.1112.10.1110.08.1121.12.1106.04.1107.12.1121.09.11 12.10.1130.03.11 21.12.1106.07.11 19.10.11 31.08.1129.06.11 09.02.11 06.07.11 27.07.11 20.04.11 17.08.1130.03.11 26.01.1104.05.1113.07.1103.08.1101.06.11 16.02.1109.02.11

15,693,2068,148,2046,535,1255,308,4614,755,0813,558,0753,264,0803,085,5973,025,1092,973,544

1,036,381441,260415,735371,540346,243336,865281,084249,252217,776141,227123,652120,200116,262108,46092,55187,96473,28770,76446,80446,13443,88343,49738,54831,92730,434 30,25926,395

GerMaN FILMS – Market Study FRANCE 5

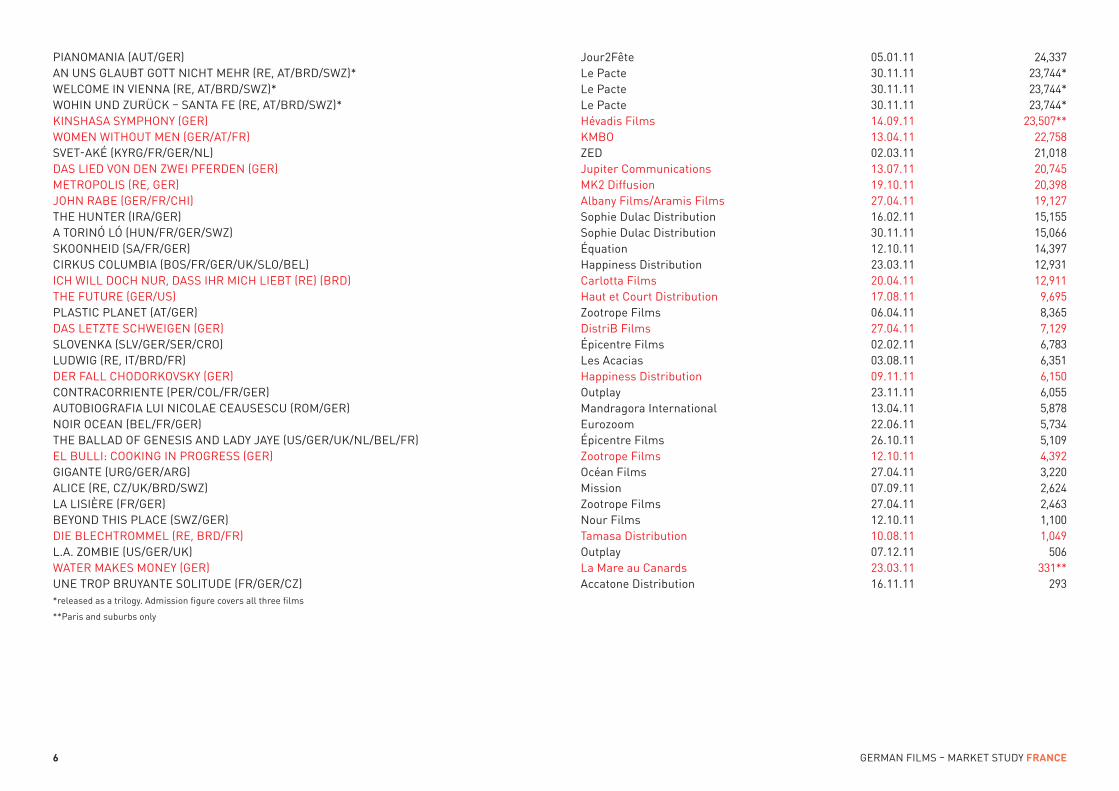

PIaNOMaNIa (aut/Ger) aN uNS GLauBt GOtt NICHt MeHr (re, at/Brd/SWZ)* WeLCOMe IN VIeNNa (re, at/Brd/SWZ)* WOHIN uNd ZurÜCk – SaNta Fe (re, at/Brd/SWZ)* kINSHaSa SyMPHONy (Ger) WOMeN WItHOut MeN (Ger/at/Fr) SVet-akÉ (kyrG/Fr/Ger/NL) daS LIed VON deN ZWeI PFerdeN (Ger) MetrOPOLIS (re, Ger) JOHN raBe (Ger/Fr/CHI) tHe HuNter (Ira/Ger) a tOrINÓ LÓ (HuN/Fr/Ger/SWZ) SkOONHeId (Sa/Fr/Ger) CIrkuS COLuMBIa (BOS/Fr/Ger/uk/SLO/BeL) ICH WILL dOCH Nur, daSS IHr MICH LIeBt (re) (Brd) tHe Future (Ger/uS) PLaStIC PLaNet (at/Ger) daS LetZte SCHWeIGeN (Ger) SLOVeNka (SLV/Ger/Ser/CrO) LudWIG (re, It/Brd/Fr) der FaLL CHOdOrkOVSky (Ger) CONtraCOrrIeNte (Per/COL/Fr/Ger) autOBIOGraFIa LuI NICOLae CeauSeSCu (rOM/Ger) NOIr OCeaN (BeL/Fr/Ger) tHe BaLLad OF GeNeSIS aNd Lady Jaye (uS/Ger/uk/NL/BeL/Fr)eL BuLLI: COOkING IN PrOGreSS (Ger) GIGaNte (urG/Ger/arG) aLICe (re, CZ/uk/Brd/SWZ) La LISIÈre (Fr/Ger) BeyONd tHIS PLaCe (SWZ/Ger) dIe BLeCHtrOMMeL (re, Brd/Fr) L.a. ZOMBIe (uS/Ger/uk) Water MakeS MONey (Ger) uNe trOP BruyaNte SOLItude (Fr/Ger/CZ) *released as a trilogy. admission figure covers all three films

**Paris and suburbs only

Jour2Fête Le PacteLe PacteLe PacteHévadis Films kMBOZed Jupiter CommunicationsMk2 diffusionalbany Films/aramis FilmsSophie dulac distributionSophie dulac distributionÉquation Happiness distribution Carlotta FilmsHaut et Court distributionZootrope FilmsdistriB FilmsÉpicentre FilmsLes acaciasHappiness distributionOutplay Mandragora International eurozoom Épicentre FilmsZootrope FilmsOcéan FilmsMissionZootrope FilmsNour Filmstamasa distributionOutplay La Mare au Canards accatone distribution

05.01.1130.11.1130.11.1130.11.1114.09.1113.04.1102.03.11 13.07.1119.10.1127.04.1116.02.1130.11.1112.10.1123.03.1120.04.1117.08.1106.04.1127.04.1102.02.1103.08.1109.11.1123.11.1113.04.1122.06.1126.10.1112.10.1127.04.1107.09.1127.04.1112.10.1110.08.1107.12.1123.03.1116.11.11

24,33723,744*23,744*23,744*

23,507**22,75821,01820,74520,39819,12715,155 15,06614,39712,93112,9119,6958,3657,1296,7836,3516,1506,0555,8785,7345,1094,3923,2202,6242,4631,1001,049

506331**

293

6 GerMaN FILMS – Market Study FRANCE

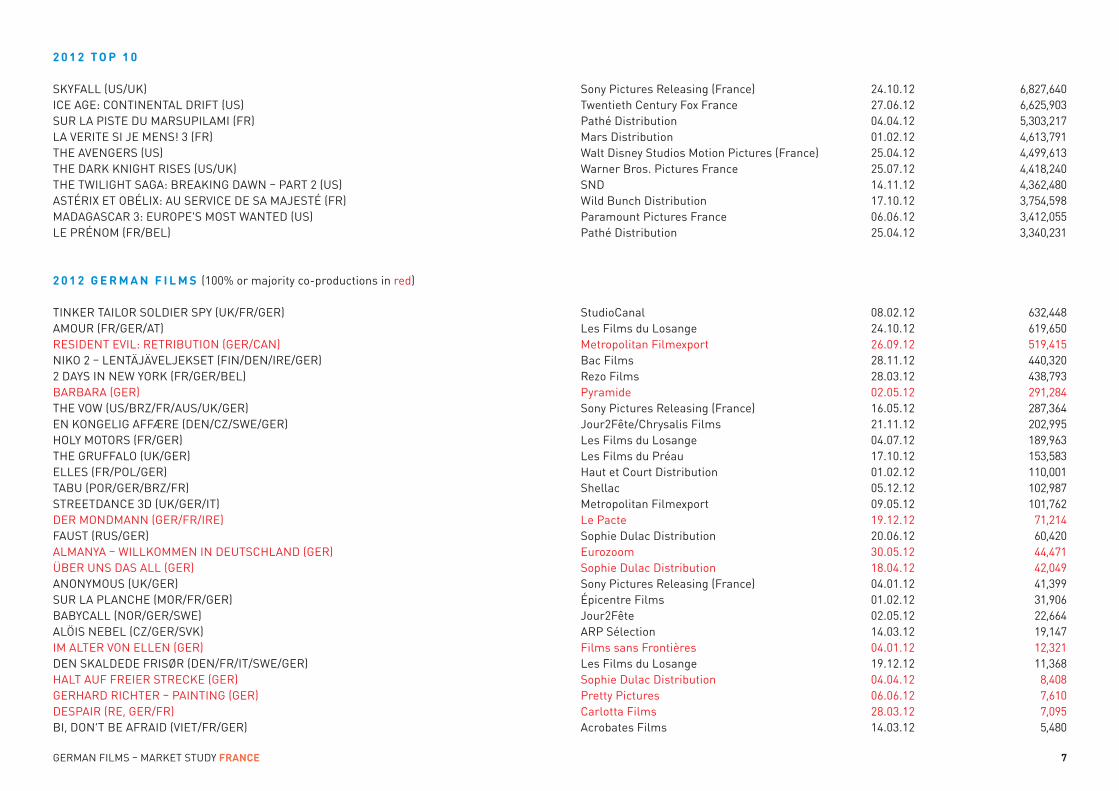

2012 TOP 10

SkyFaLL (uS/uk) ICe aGe: CONtINeNtaL drIFt (uS) Sur La PISte du MarSuPILaMI (Fr) La VerIte SI Je MeNS! 3 (Fr) tHe aVeNGerS (uS) tHe dark kNIGHt rISeS (uS/uk) tHe tWILIGHt SaGa: BreakING daWN – Part 2 (uS) aStÉrIX et OBÉLIX: au SerVICe de Sa MaJeStÉ (Fr) MadaGaSCar 3: eurOPe'S MOSt WaNted (uS) Le PrÉNOM (Fr/BeL)

2012 GERMAN F I LMS (100% or majority co-productions in red)

tINker taILOr SOLdIer SPy (uk/Fr/Ger) aMOur (Fr/Ger/at) reSIdeNt eVIL: retrIButION (Ger/CaN) NIkO 2 – LeNtÄJÄVeLJekSet (FIN/deN/Ire/Ger) 2 dayS IN NeW yOrk (Fr/Ger/BeL) BarBara (Ger) tHe VOW (uS/BrZ/Fr/auS/uk/Ger) eN kONGeLIG aFFÆre (deN/CZ/SWe/Ger) HOLy MOtOrS (Fr/Ger) tHe GruFFaLO (uk/Ger) eLLeS (Fr/POL/Ger) taBu (POr/Ger/BrZ/Fr) StreetdaNCe 3d (uk/Ger/It) der MONdMaNN (Ger/Fr/Ire) FauSt (ruS/Ger) aLMaNya – WILLkOMMeN IN deutSCHLaNd (Ger) ÜBer uNS daS aLL (Ger) aNONyMOuS (uk/Ger) Sur La PLaNCHe (MOr/Fr/Ger) BaByCaLL (NOr/Ger/SWe) aLÖIS NeBeL (CZ/Ger/SVk) IM aLter VON eLLeN (Ger) deN SkaLdede FrISØr (deN/Fr/It/SWe/Ger) HaLt auF FreIer StreCke (Ger) GerHard rICHter – PaINtING (Ger) deSPaIr (re, Ger/Fr) BI, dON’t Be aFraId (VIet/Fr/Ger)

Sony Pictures releasing (France) twentieth Century Fox FrancePathé distributionMars distributionWalt disney Studios Motion Pictures (France)Warner Bros. Pictures FranceSNd Wild Bunch distribution Paramount Pictures France Pathé distribution

StudioCanalLes Films du Losange Metropolitan FilmexportBac Films rezo FilmsPyramideSony Pictures releasing (France) Jour2Fête/Chrysalis Films Les Films du LosangeLes Films du Préau Haut et Court distributionShellacMetropolitan FilmexportLe PacteSophie dulac distributioneurozoomSophie dulac distributionSony Pictures releasing (France)Épicentre FilmsJour2FêtearP SélectionFilms sans Frontières Les Films du LosangeSophie dulac distributionPretty PicturesCarlotta Filmsacrobates Films

24.10.12 27.06.1204.04.1201.02.12 25.04.1225.07.12 14.11.12 17.10.1206.06.1225.04.12

08.02.12 24.10.1226.09.1228.11.12 28.03.12 02.05.1216.05.12 21.11.12 04.07.12 17.10.1201.02.12 05.12.1209.05.1219.12.1220.06.1230.05.1218.04.1204.01.12 01.02.1202.05.1214.03.1204.01.12 19.12.12 04.04.1206.06.1228.03.1214.03.12

6,827,6406,625,9035,303,2174,613,7914,499,6134,418,2404,362,4803,754,5983,412,0553,340,231

632,448619,650519,415440,320438,793291,284287,364202,995189,963153,583110,001 102,987101,76271,21460,42044,47142,04941,39931,90622,66419,14712,32111,3688,4087,6107,0955,480

GerMaN FILMS – Market Study FRANCE 7

BLaCk ButterFLIeS (NL/Ger/Sa) SHarQIya (ISr/Fr/Ger) GeLeCek uZuN Surer (tur/Ger/Fr) tÖte MICH (Ger/Fr/SWZ) PLayOFF (Ger/ISr/Fr) HOuSe OF BOyS (LuX/Ger) tHe GreeN WaVe (Ger) GIrIMuNHO (BrZ/SP/Ger) SeNtadOS FreNte aL FueGO (CHILe/Ger) aurOra (rOM/Fr/SWZ/Ger) MarIeke, MarIeke (BeL/Ger) ICH BIN eINe terrOrIStIN (Fr/POL/Ger) ParaISO (Peru/Ger/SP)

SALES AGENTS FOR GERMAN F I LMS RELEASED IN FRANCE (not including re-releases)

aLLe aNdereN Global ScreenaLMaNya – WILLkOMMeN IN deutSCHLaNd Beta CinemaBarBara the Match Factorya daNGerOuS MetHOd HanWay FilmseL BuLLI: COOkING IN PrOGreSS autlook Filmsalesder FaLL CHOdOrkOVSky rezo FilmsdIe FreMde Global ScreendaS FreMde IN MIr Global ScreentHe Future the Match FactoryGerHard rICHter – PaINtING the Match FactorytHe GreeN WaVe Visit FilmsHaLt auF FreIer StreCke the Match FactoryIM aLter VON eLLeN the Match FactoryJOHN raBe Beta CinemakINSHaSa SyMPHONy C Major entertainmentder kLeINe kÖNIG MaCIuS Global ScreenkONFereNZ der tIere timeless FilmstHe LaSt StatION the Little Film CompanydaS LetZte SCHWeIGeN Global ScreendaS LIed VON deN ZWeI PFerdeN atrix FilmsLIFe, aBOVe aLL Global Screender MONdMaNN Le PactePINa HanWay FilmsPLayOFF Wild BunchreSIdeNt eVIL: retrIButION Sony Pictures GlobalrOHteNBurG Lightning entertainmentdaS SaNdMÄNNCHeN – aBeNteuer IN trauMLaNd Bac FilmsSHaHada Memento Films InternationalSOuL kItCHeN the Match Factory

Zootrope FilmsaSC distribution arizona FilmsLes Films du LosangeWild Bunch distributionOutplaydistrib Films damned distribution arizona FilmsShellackMBO kanibal Films distributionJML distribution

22.02.1207.11.1218.04.1225.04.1204.07.1207.11.1218.01.1215.08.1222.08.1221.03.1229.08.1206.06.1225.07.12

8 GerMaN FILMS – Market Study FRANCE

5,2144,4383,3152,7952,7502,657 2,1842,0561,8001,6351,025

33086

SturM trustNordisktaNZtrÄuMe Films BoutiquetHe tHree MuSketeerS Summit entertainmenttÖte MICH Les Films du LosangeÜBer uNS daS aLL Global ScreenuNter BauerN recreationuNter dIr dIe Stadt the Match FactoryWater MakeS MONey kern Filmproduktion*WHOLetraIN Global ScreenWICkIe uNd dIe StarkeN MÄNNer timeless PicturesWIr SINd dIe NaCHt Celluloid dreamsWOMeN WItHOut MeN Coproduction OfficeWÜSteNBLuMe the Match Factor* production company

TELEV IS ION AND V IDEO

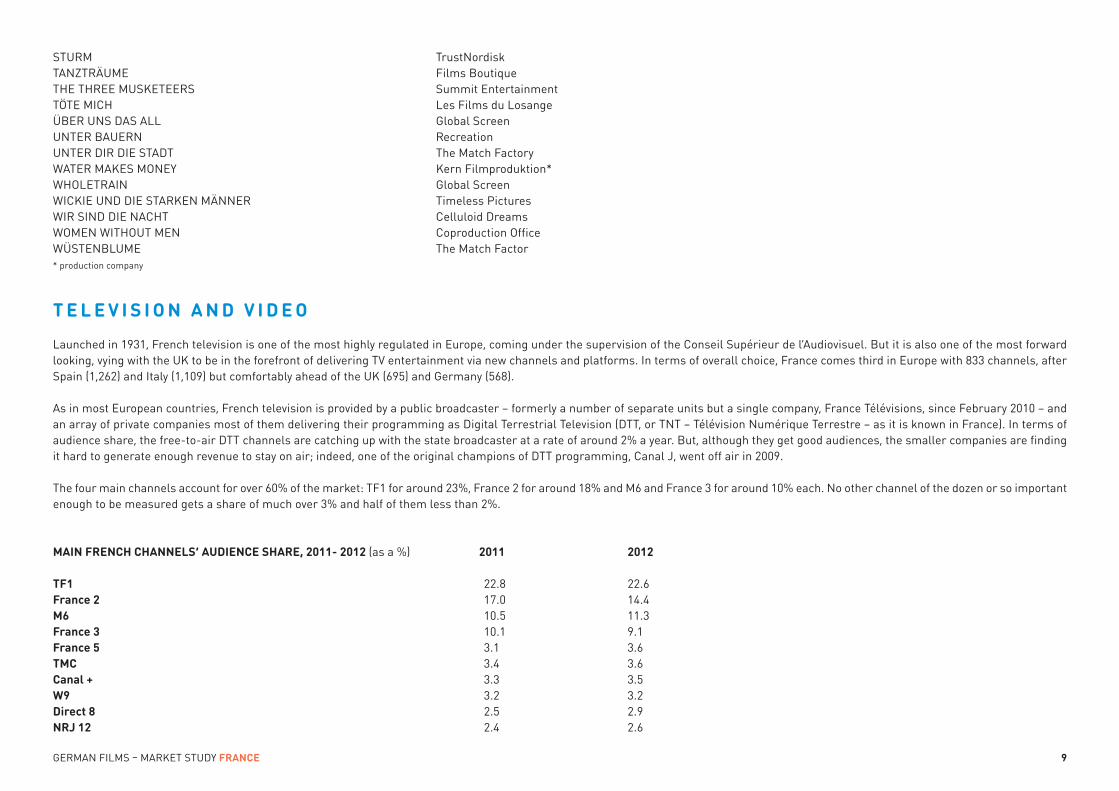

Launched in 1931, French television is one of the most highly regulated in europe, coming under the supervision of the Conseil Supérieur de l’audiovisuel. But it is also one of the most forwardlooking, vying with the uk to be in the forefront of delivering tV entertainment via new channels and platforms. In terms of overall choice, France comes third in europe with 833 channels, afterSpain (1,262) and Italy (1,109) but comfortably ahead of the uk (695) and Germany (568).

as in most european countries, French television is provided by a public broadcaster – formerly a number of separate units but a single company, France télévisions, since February 2010 – andan array of private companies most of them delivering their programming as digital terrestrial television (dtt, or tNt – télévision Numérique terrestre – as it is known in France). In terms ofaudience share, the free-to-air dtt channels are catching up with the state broadcaster at a rate of around 2% a year. But, although they get good audiences, the smaller companies are findingit hard to generate enough revenue to stay on air; indeed, one of the original champions of dtt programming, Canal J, went off air in 2009.

the four main channels account for over 60% of the market: tF1 for around 23%, France 2 for around 18% and M6 and France 3 for around 10% each. No other channel of the dozen or so importantenough to be measured gets a share of much over 3% and half of them less than 2%.

MAIN FRENCH CHANNELS’ AUDIENCE SHARE, 2011- 2012 (as a %) 2011 2012

TF1 22.8 22.6France 2 17.0 14.4M6 10.5 11.3France 3 10.1 9.1France 5 3.1 3.6TMC 3.4 3.6Canal + 3.3 3.5W9 3.2 3.2Direct 8 2.5 2.9NRJ 12 2.4 2.6

GerMaN FILMS – Market Study FRANCE 9

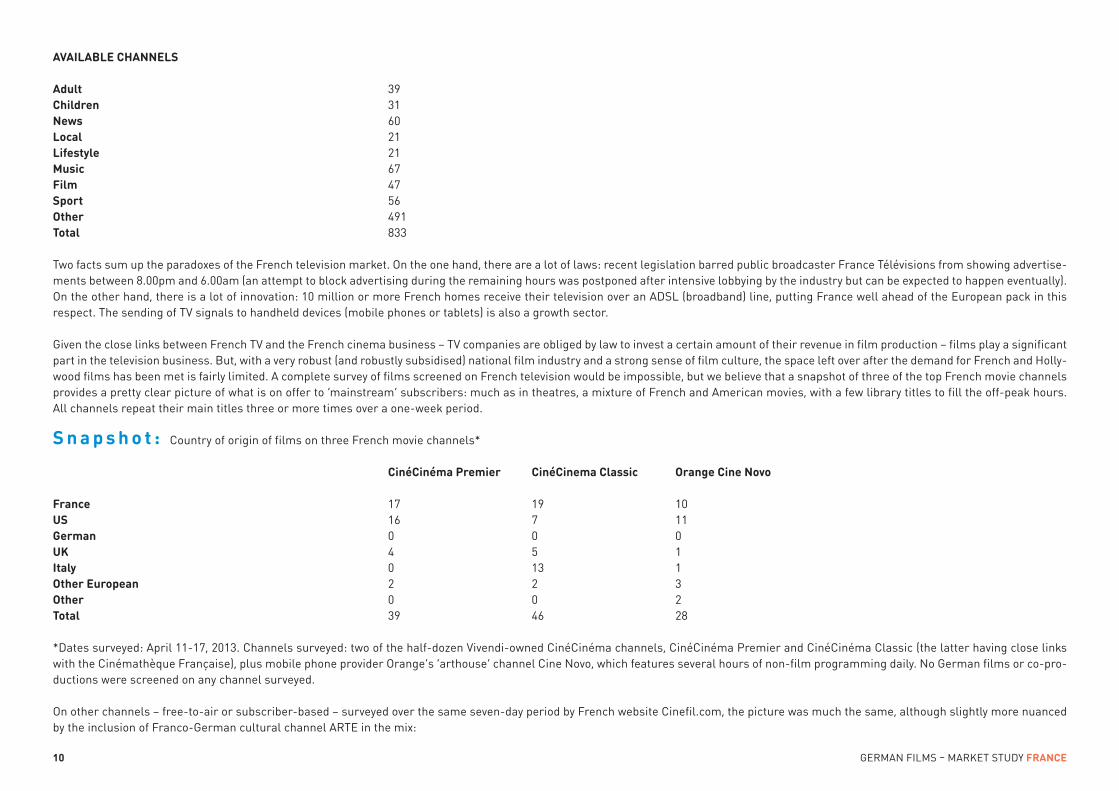

AVAILABLE CHANNELS

Adult 39Children 31 News 60Local 21Lifestyle 21Music 67Film 47Sport 56Other 491Total 833

two facts sum up the paradoxes of the French television market. On the one hand, there are a lot of laws: recent legislation barred public broadcaster France télévisions from showing advertise -ments between 8.00pm and 6.00am (an attempt to block advertising during the remaining hours was postponed after intensive lobbying by the industry but can be expected to happen eventually).On the other hand, there is a lot of innovation: 10 million or more French homes receive their television over an adSL (broadband) line, putting France well ahead of the european pack in thisrespect. the sending of tV signals to handheld devices (mobile phones or tablets) is also a growth sector.

Given the close links between French tV and the French cinema business – tV companies are obliged by law to invest a certain amount of their revenue in film production – films play a significantpart in the television business. But, with a very robust (and robustly subsidised) national film industry and a strong sense of film culture, the space left over after the demand for French and Holly -wood films has been met is fairly limited. a complete survey of films screened on French television would be impossible, but we believe that a snapshot of three of the top French movie channelsprovides a pretty clear picture of what is on offer to ‘mainstream’ subscribers: much as in theatres, a mixture of French and american movies, with a few library titles to fill the off-peak hours.all channels repeat their main titles three or more times over a one-week period.

Snapsho t : Country of origin of films on three French movie channels*

CinéCinéma Premier CinéCinema Classic Orange Cine Novo

France 17 19 10US 16 7 11German 0 0 0UK 4 5 1Italy 0 13 1Other European 2 2 3Other 0 0 2Total 39 46 28

*dates surveyed: april 11-17, 2013. Channels surveyed: two of the half-dozen Vivendi-owned CinéCinéma channels, CinéCinéma Premier and CinéCinéma Classic (the latter having close linkswith the Cinémathèque Française), plus mobile phone provider Orange’s ‘arthouse’ channel Cine Novo, which features several hours of non-film programming daily. No German films or co-pro-ductions were screened on any channel surveyed.

On other channels – free-to-air or subscriber-based – surveyed over the same seven-day period by French website Cinefil.com, the picture was much the same, although slightly more nuancedby the inclusion of Franco-German cultural channel arte in the mix:

10 GerMaN FILMS – Market Study FRANCE

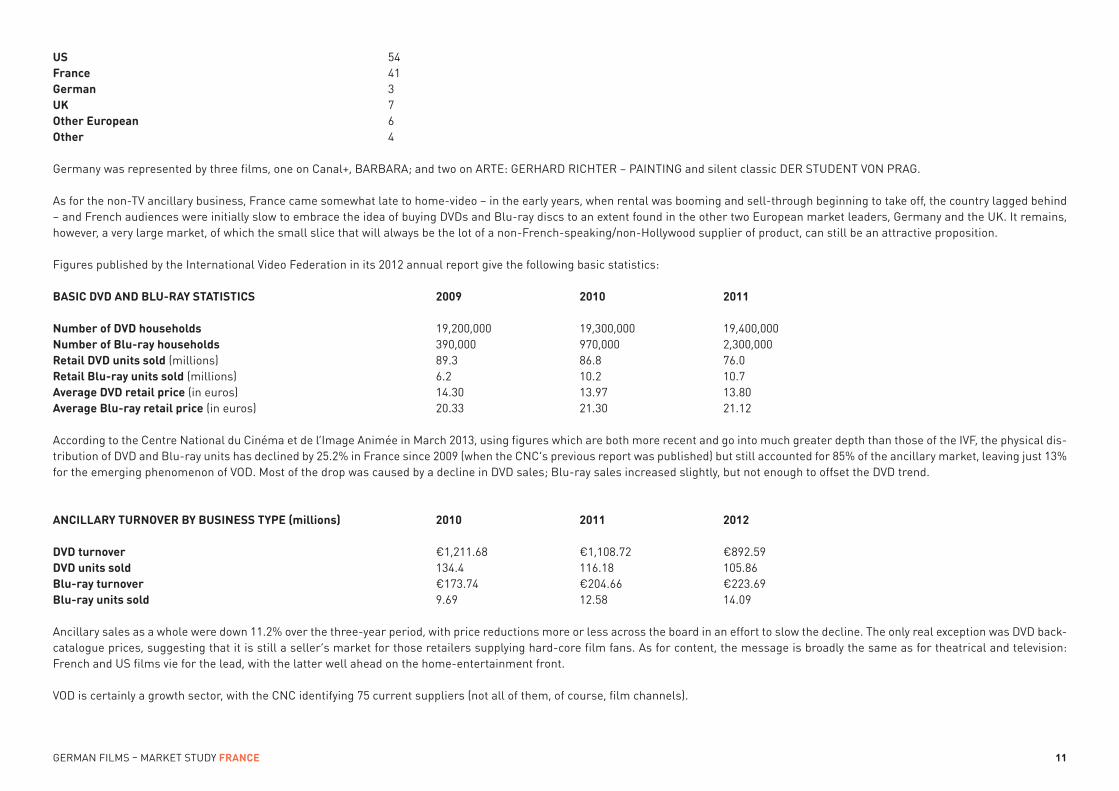

US 54France 41German 3UK 7Other European 6Other 4

Germany was represented by three films, one on Canal+, BarBara; and two on arte: GerHard rICHter – PaINtING and silent classic der StudeNt VON PraG.

as for the non-tV ancillary business, France came somewhat late to home-video – in the early years, when rental was booming and sell-through beginning to take off, the country lagged behind– and French audiences were initially slow to embrace the idea of buying dVds and Blu-ray discs to an extent found in the other two european market leaders, Germany and the uk. It remains,however, a very large market, of which the small slice that will always be the lot of a non-French-speaking/non-Hollywood supplier of product, can still be an attractive proposition.

Figures published by the International Video Federation in its 2012 annual report give the following basic statistics:

BASIC DVD AND BLU-RAY STATISTICS 2009 2010 2011

Number of DVD households 19,200,000 19,300,000 19,400,000Number of Blu-ray households 390,000 970,000 2,300,000Retail DVD units sold (millions) 89.3 86.8 76.0Retail Blu-ray units sold (millions) 6.2 10.2 10.7Average DVD retail price (in euros) 14.30 13.97 13.80Average Blu-ray retail price (in euros) 20.33 21.30 21.12

according to the Centre National du Cinéma et de l’Image animée in March 2013, using figures which are both more recent and go into much greater depth than those of the IVF, the physical dis-tribution of dVd and Blu-ray units has declined by 25.2% in France since 2009 (when the CNC’s previous report was published) but still accounted for 85% of the ancillary market, leaving just 13%for the emerging phenomenon of VOd. Most of the drop was caused by a decline in dVd sales; Blu-ray sales increased slightly, but not enough to offset the dVd trend.

ANCILLARY TURNOVER BY BUSINESS TYPE (millions) 2010 2011 2012

DVD turnover €1,211.68 €1,108.72 €892.59DVD units sold 134.4 116.18 105.86Blu-ray turnover €173.74 €204.66 €223.69Blu-ray units sold 9.69 12.58 14.09

ancillary sales as a whole were down 11.2% over the three-year period, with price reductions more or less across the board in an effort to slow the decline. the only real exception was dVd back-catalogue prices, suggesting that it is still a seller’s market for those retailers supplying hard-core film fans. as for content, the message is broadly the same as for theatrical and television:French and uS films vie for the lead, with the latter well ahead on the home-entertainment front.

VOd is certainly a growth sector, with the CNC identifying 75 current suppliers (not all of them, of course, film channels).

GerMaN FILMS – Market Study FRANCE 11

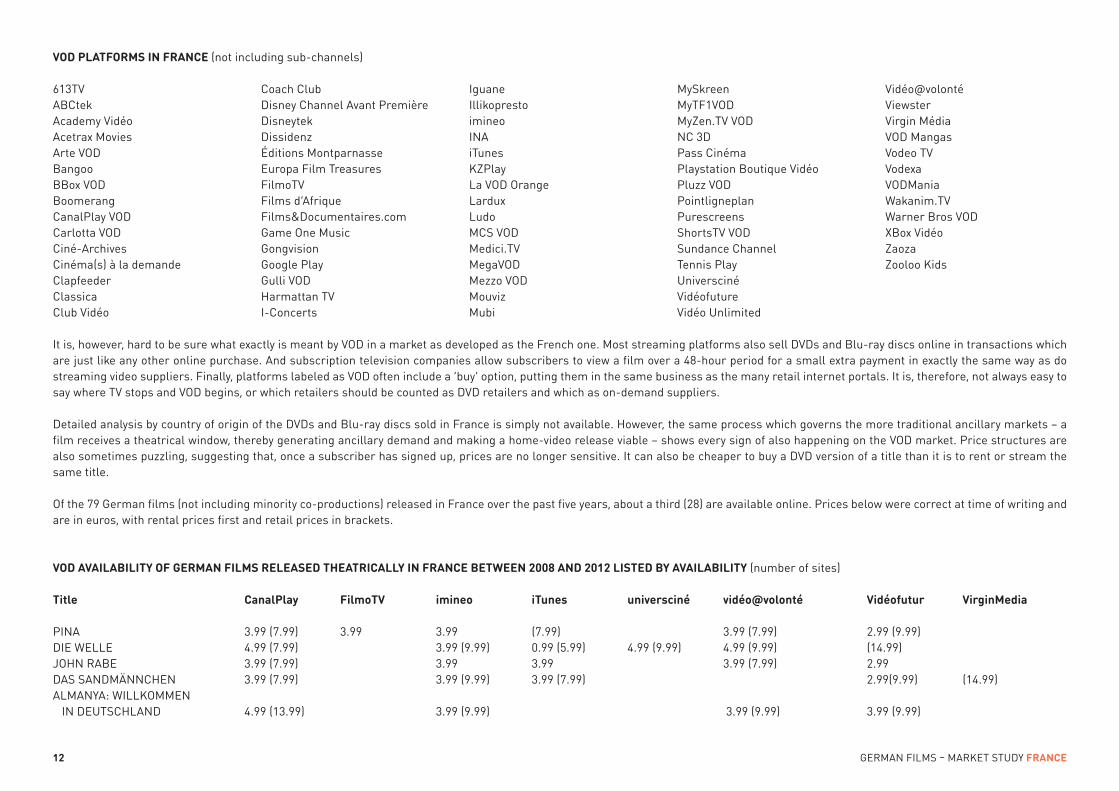

VOD PLATFORMS IN FRANCE (not including sub-channels)

It is, however, hard to be sure what exactly is meant by VOd in a market as developed as the French one. Most streaming platforms also sell dVds and Blu-ray discs online in transactions whichare just like any other online purchase. and subscription television companies allow subscribers to view a film over a 48-hour period for a small extra payment in exactly the same way as dostreaming video suppliers. Finally, platforms labeled as VOd often include a ‘buy’ option, putting them in the same business as the many retail internet portals. It is, therefore, not always easy tosay where tV stops and VOd begins, or which retailers should be counted as dVd retailers and which as on-demand suppliers.

detailed analysis by country of origin of the dVds and Blu-ray discs sold in France is simply not available. However, the same process which governs the more traditional ancillary markets – afilm receives a theatrical window, thereby generating ancillary demand and making a home-video release viable – shows every sign of also happening on the VOd market. Price structures arealso sometimes puzzling, suggesting that, once a subscriber has signed up, prices are no longer sensitive. It can also be cheaper to buy a dVd version of a title than it is to rent or stream thesame title.

Of the 79 German films (not including minority co-productions) released in France over the past five years, about a third (28) are available online. Prices below were correct at time of writing andare in euros, with rental prices first and retail prices in brackets.

VOD AVAILABILITY OF GERMAN FILMS RELEASED THEATRICALLY IN FRANCE BETWEEN 2008 AND 2012 LISTED BY AVAILABILITY (number of sites)

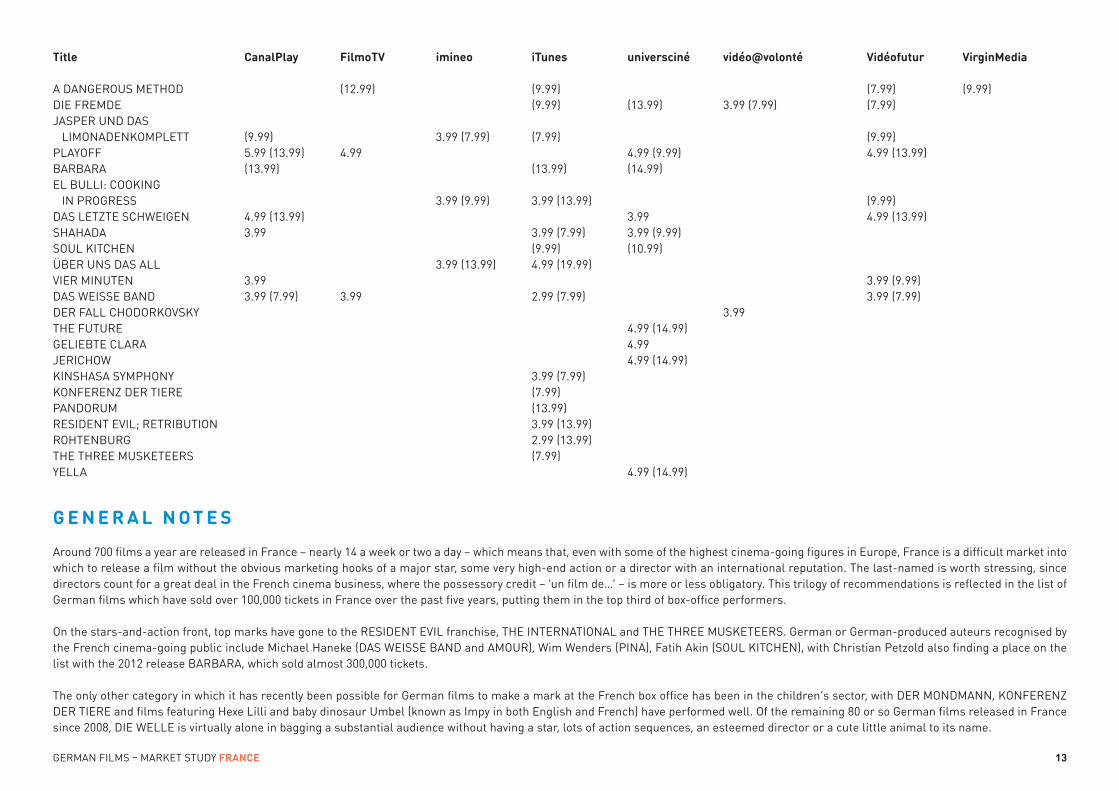

Title CanalPlay FilmoTV imineo iTunes universciné vidéo@volonté Vidéofutur VirginMedia

PINa 3.99 (7.99) 3.99 3.99 (7.99) 3.99 (7.99) 2.99 (9.99)dIe WeLLe 4.99 (7.99) 3.99 (9.99) 0.99 (5.99) 4.99 (9.99) 4.99 (9.99) (14.99)JOHN raBe 3.99 (7.99) 3.99 3.99 3.99 (7.99) 2.99daS SaNdMÄNNCHeN 3.99 (7.99) 3.99 (9.99) 3.99 (7.99) 2.99(9.99) (14.99)aLMaNya: WILLkOMMeN

IN deutSCHLaNd 4.99 (13.99) 3.99 (9.99) 3.99 (9.99) 3.99 (9.99)

613tVaBCtekacademy Vidéoacetrax Moviesarte VOdBangooBBox VOdBoomerangCanalPlay VOdCarlotta VOdCiné-archivesCinéma(s) à la demandeClapfeederClassicaClub Vidéo

Coach Clubdisney Channel avant PremièredisneytekdissidenzÉditions Montparnasseeuropa Film treasuresFilmotVFilms d’afriqueFilms&documentaires.comGame One MusicGongvisionGoogle PlayGulli VOdHarmattan tVI-Concerts

IguaneIllikoprestoimineoINaituneskZPlayLa VOd OrangeLarduxLudoMCS VOdMedici.tVMegaVOdMezzo VOdMouvizMubi

MySkreenMytF1VOdMyZen.tV VOdNC 3dPass CinémaPlaystation Boutique VidéoPluzz VOdPointligneplanPurescreensShortstV VOdSundance Channeltennis PlayuniverscinéVidéofutureVidéo unlimited

Vidéo@volontéViewsterVirgin MédiaVOd MangasVodeo tVVodexaVOdManiaWakanim.tVWarner Bros VOdXBox VidéoZaozaZooloo kids

12 GerMaN FILMS – Market Study FRANCE

Title CanalPlay FilmoTV imineo iTunes universciné vidéo@volonté Vidéofutur VirginMedia

a daNGerOuS MetHOd (12.99) (9.99) (7.99) (9.99)dIe FreMde (9.99) (13.99) 3.99 (7.99) (7.99)JaSPer uNd daS

LIMONadeNkOMPLett (9.99) 3.99 (7.99) (7.99) (9.99)PLayOFF 5.99 (13.99) 4.99 4.99 (9.99) 4.99 (13.99)BarBara (13.99) (13.99) (14.99)eL BuLLI: COOkING

IN PrOGreSS 3.99 (9.99) 3.99 (13.99) (9.99)daS LetZte SCHWeIGeN 4.99 (13.99) 3.99 4.99 (13.99)SHaHada 3.99 3.99 (7.99) 3.99 (9.99)SOuL kItCHeN (9.99) (10.99)ÜBer uNS daS aLL 3.99 (13.99) 4.99 (19.99)VIer MINuteN 3.99 3.99 (9.99)daS WeISSe BaNd 3.99 (7.99) 3.99 2.99 (7.99) 3.99 (7.99)der FaLL CHOdOrkOVSky 3.99tHe Future 4.99 (14.99)GeLIeBte CLara 4.99JerICHOW 4.99 (14.99)kINSHaSa SyMPHONy 3.99 (7.99)kONFereNZ der tIere (7.99)PaNdOruM (13.99)reSIdeNt eVIL; retrIButION 3.99 (13.99)rOHteNBurG 2.99 (13.99)tHe tHree MuSketeerS (7.99)yeLLa 4.99 (14.99)

GENERAL NOTES

around 700 films a year are released in France – nearly 14 a week or two a day – which means that, even with some of the highest cinema-going figures in europe, France is a difficult market intowhich to release a film without the obvious marketing hooks of a major star, some very high-end action or a director with an international reputation. the last-named is worth stressing, sincedirectors count for a great deal in the French cinema business, where the possessory credit – ‘un film de…’ – is more or less obligatory. this trilogy of recommendations is reflected in the list ofGerman films which have sold over 100,000 tickets in France over the past five years, putting them in the top third of box-office performers.

On the stars-and-action front, top marks have gone to the reSIdeNt eVIL franchise, tHe INterNatIONaL and tHe tHree MuSketeerS. German or German-produced auteurs recognised bythe French cinema-going public include Michael Haneke (daS WeISSe BaNd and aMOur), Wim Wenders (PINa), Fatih akin (SOuL kItCHeN), with Christian Petzold also finding a place on thelist with the 2012 release BarBara, which sold almost 300,000 tickets.

the only other category in which it has recently been possible for German films to make a mark at the French box office has been in the children’s sector, with der MONdMaNN, kONFereNZder tIere and films featuring Hexe Lilli and baby dinosaur umbel (known as Impy in both english and French) have performed well. Of the remaining 80 or so German films released in Francesince 2008, dIe WeLLe is virtually alone in bagging a substantial audience without having a star, lots of action sequences, an esteemed director or a cute little animal to its name.

GerMaN FILMS – Market Study FRANCE 13

Given the close ties between French television and the French film industry (see above), television is a difficult market for non-French and non-Hollywood film to crack. as a result, German filmsare more or less absent from the main free-to-air channels (with the exception of arte), and sparsely represented on the key pay-to-view ones. the French dVd market is, like that in mostdeveloped countries, in decline, while VOd in all its forms is still responsible for less than 15% of the non-theatrical market. What is more, the VOd market is close to saturation, with 75 differentplatforms on offer. the most likely outcome seems to be a polarisation which will mirror the theatrical market. a few major distributors are likely to account for most of the market – the top 18theatrical distributors sold 90% of the tickets in 2012, leaving the remaining 138 companies, many of them distinctly boutique operations, to divide up the rest.

On the VOd market, establishing a name seems to have been the main priority, with those that are already recognisable – such as Canal+, Orange and itunes – having a clear advantage. Interestingly,this seems more important than price competitiveness, suggesting that customers sign on for one or perhaps two platforms, rather than shop around for the one with the cheapest titles. It isprobably this combination of saturation and major player dominance that led uS VOd giant Netflix to conclude that the French VOd market was of little interest.

Sources: Institute National de la Statistique et des Études Économiques (National Institute of Statistics and economic Studies), World Bank, tradingeconomics.com, european audiovisual Observatory, Médiametrie, Centre National du Cinéma et de

l’Image animée (CNC), allocine.fr, Le Film Français, voirunfilm.com, cinefil.com, International Video Federation, Ciné-chiffres, Split Screen data Ltd., Picture credits page 1 and 2: tuBS europe on the globe/wikimedia

14 GerMaN FILMS – Market Study FRANCE