Embed Size (px)

Citation preview

Market shifts shaping LNG shippingAnita Odedra, Director - LNG Supply & Commercial Operations Association of Ship Brokers & Agents (U.S.A.), Inc.

28 – 30 September 2011

Legal disclaimer

The following presentation contains forward-looking statements concerning BG Group plc strategy,operations, financial performance or condition, outlook, growth opportunities or circumstances in thecountries, sectors or markets in which BG Group plc operates. By their nature, forward-lookingstatements involve uncertainty because they depend on future circumstances and relate to eventsthat cannot always be controlled or predicted. Although the Company believes that the expectationsreflected in such forward-looking statements are reasonable, no assurance can be given that suchexpectations will prove to have been correct. Actual results could differ materially from the guidancegiven in this presentation for a number of reasons. For a detailed analysis of the factors that mayaffect our business, financial performance or results of operations, we urge you to look at the“Principle risks and uncertainties” included in the BG Group plc Annual Report & Accounts 2010.Nothing in this presentation should be construed as a profit forecast and no part of this presentationconstitutes, or shall be taken to constitute, an invitation or inducement to invest in BG Group plc orany other entity, and must not be relied upon in any way in connection with any investment decision.BG Group plc undertakes no obligation to update any forward-looking statements.

No representation or warranty, express or implied, is or will be made in relation to the accuracy orcompleteness of the information in this presentation and no responsibility or liability is or will beaccepted by BG Group plc or any of its respective subsidiaries, affiliates and associated companies(or by any of their respective officers, employees or agents) in relation to it.

2

Industry context

• 2010 global trade up 22% YoY

• UK is now a global LNG balancing market

• Australia gearing up for significant supply growth mid-decade

– 4 Australian LNG projects made FID in 2010-2011

– Project delivery challenge

• North American unconventional gas emerging as potential LNG supply

– US Gulf Coast

– Canada West Coast

3Markets tightening – pulling new supply

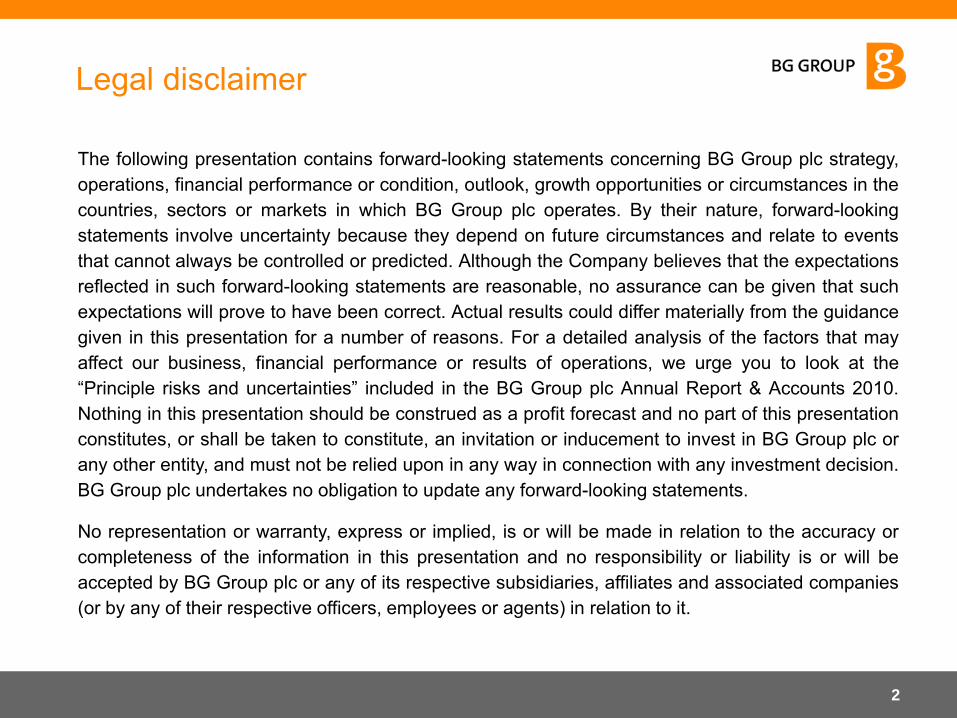

Global LNG supply outlook

4New supplies and prices 2014+ still highly uncertain

0

100

200

300

400

500

600

700

2000 2005 2010 2015 2020 2025

mtp

a

Existing Under Construction Probable PossibleSpeculative Global Demand Global Supply

Develop-mentdelay

Future growth uncertainty

Project start-up slippage

• Contractor capacity

• Costs• Partner

alignment• NOC capacity• Environment• Export vs

domestic

• All of the previous, plus• Geopolitical• Reserves access• Market?

Source: BG Group interpretation of Wood Mackenzie (May 2011) data

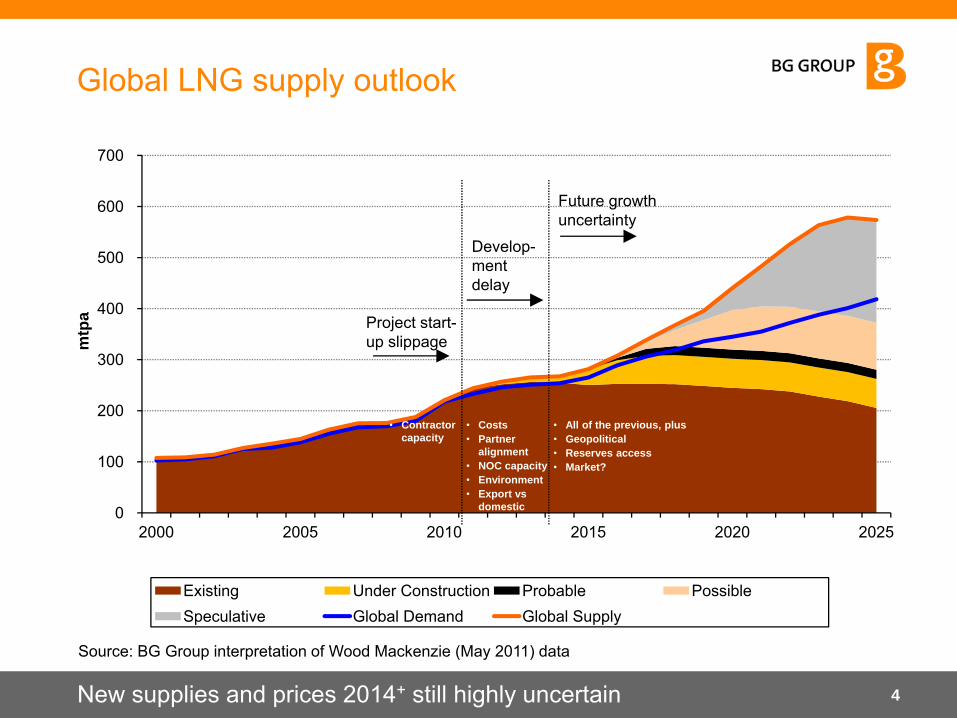

Existing and potential LNG importing countries

Demand robust – a rapid increase in aspiring importers

Existing (25)

Under consideration (30+)Under construction (1)

Uruguay

Jamaica

El Salvador

Hawaii (US) Mexico

US

Dom. Rep

Chile

Canada

Canary Is. (Sp)

Argentina

Source: BG Group (Aug 2011)

Panama

New Zealand

Brazil

S. Africa

Kenya

Japan

S. Korea

Indonesia

Philippines

SingaporeSri Lanka

Pakistan

Vietnam

Bangladesh

TaiwanMorocco

Belgium

NetherlandsDenmark

China

India

Portugal

PolandGermany

Ireland

France

Thailand

UkraineTurkey

Greece

Romania

Lebanon

CyprusKuwaitSpain

DubaiBahrain

UK

ItalyIsrael

Albania

Croatia

Colombia

FinlandLithuania/Belarus

Slovenia

Malaysia

Martinique & Guadeloupe

Aruba

Puerto Rico

5

Ghana

+8%

+8%

+8%+67%

+40%+48%

-89%

+∞

-1

+0

+1

+2

+3

Japan Korea Taiwan Chile China India Mexico W Thailand

mt

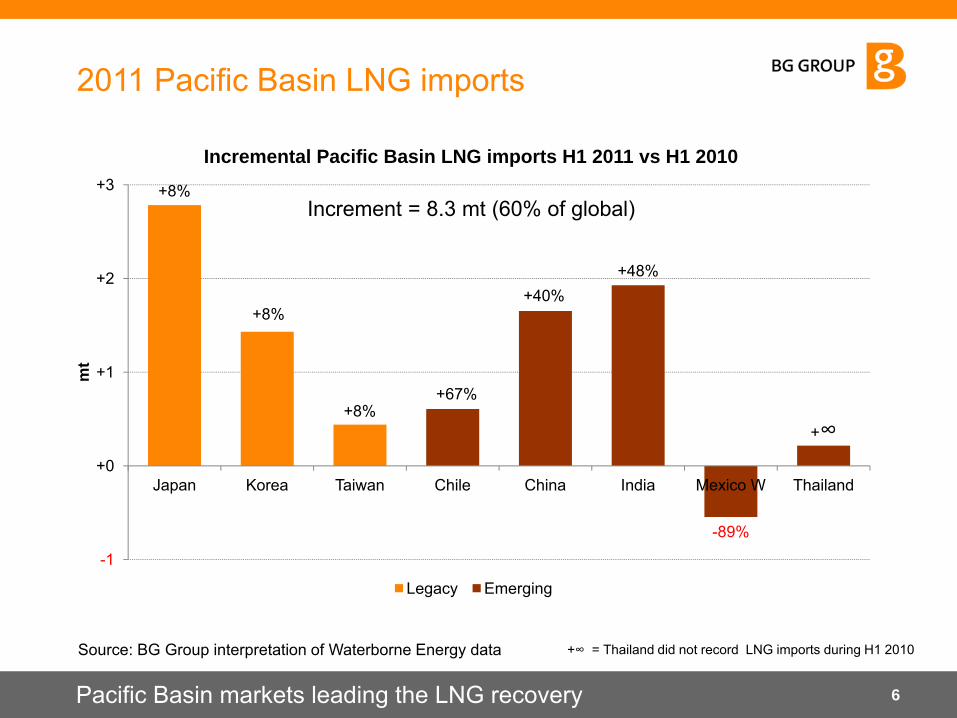

Incremental Pacific Basin LNG imports H1 2011 vs H1 2010

Legacy Emerging

Pacific Basin markets leading the LNG recovery

2011 Pacific Basin LNG imports

6

Increment = 8.3 mt (60% of global)

Source: BG Group interpretation of Waterborne Energy data +∞ = Thailand did not record LNG imports during H1 2010

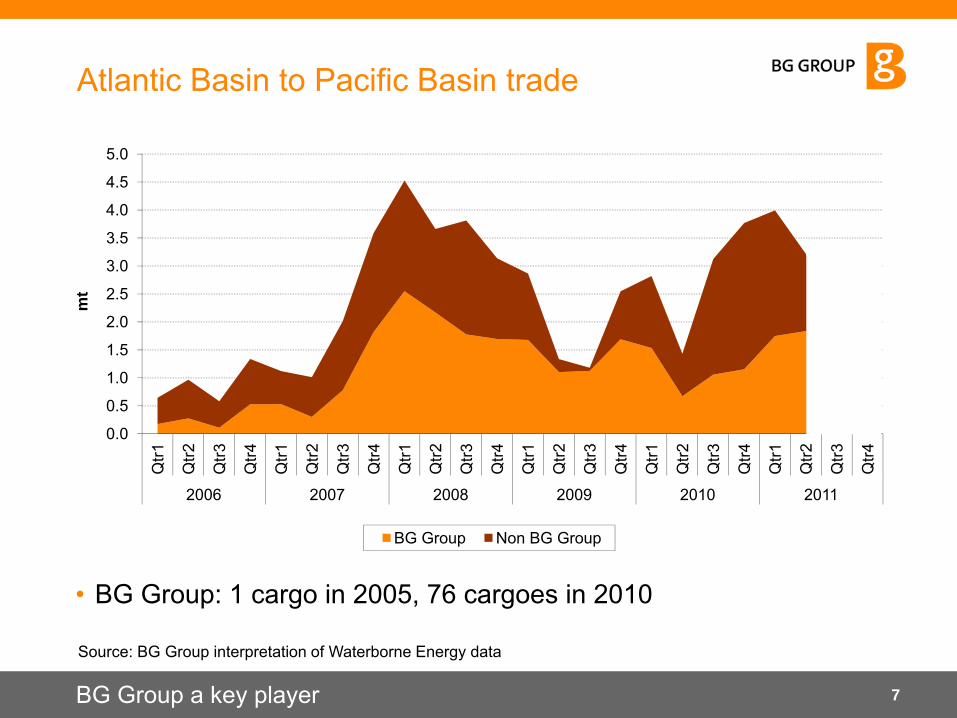

Atlantic Basin to Pacific Basin trade

• BG Group: 1 cargo in 2005, 76 cargoes in 2010

7

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0Q

tr1

Qtr2

Qtr3

Qtr4

Qtr1

Qtr2

Qtr3

Qtr4

Qtr1

Qtr2

Qtr3

Qtr4

Qtr1

Qtr2

Qtr3

Qtr4

Qtr1

Qtr2

Qtr3

Qtr4

Qtr1

Qtr2

Qtr3

Qtr4

2006 2007 2008 2009 2010 2011

mt

BG Group Non BG Group

Source: BG Group interpretation of Waterborne Energy data

BG Group a key player

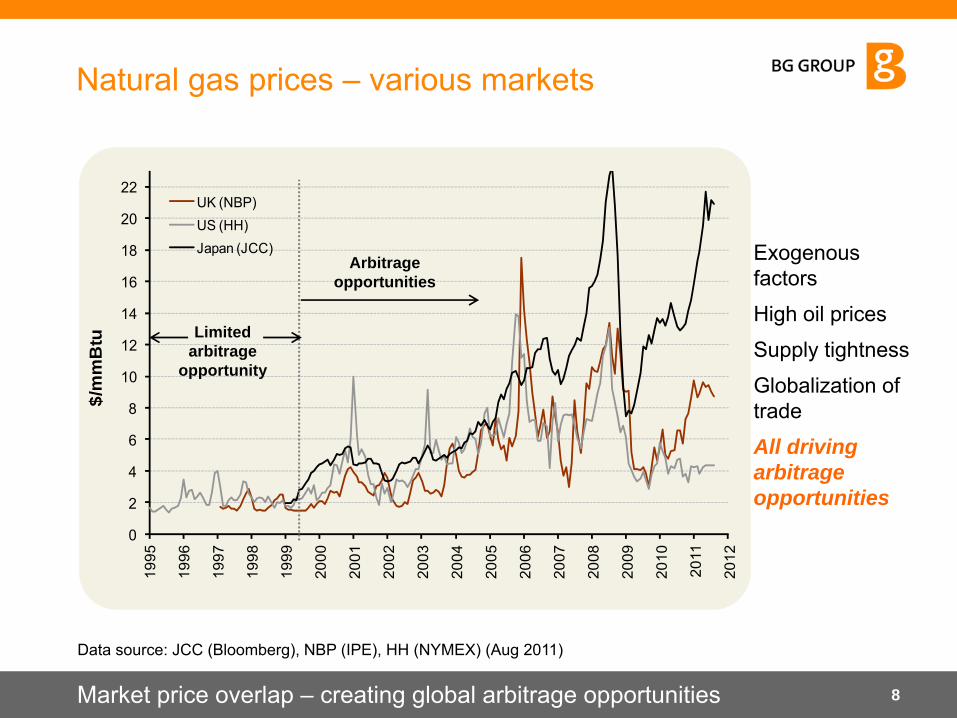

• Exogenous factors

• High oil prices

• Supply tightness

• Globalization of trade

All driving arbitrage opportunities

Natural gas prices – various markets

Market price overlap – creating global arbitrage opportunities

Data source: JCC (Bloomberg), NBP (IPE), HH (NYMEX) (Aug 2011)

8

0

2

4

6

8

10

12

14

16

18

20

22

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

$/m

mB

tu

UK (NBP)US (HH) Japan (JCC)

Limited arbitrage

opportunity

Arbitrage opportunities

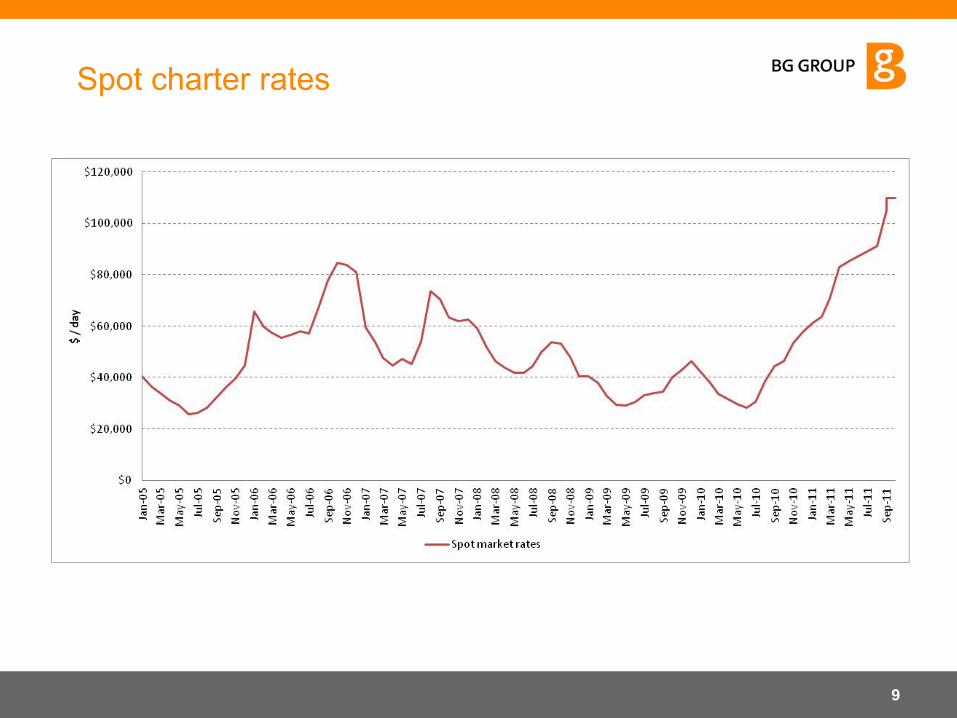

Spot charter rates

9

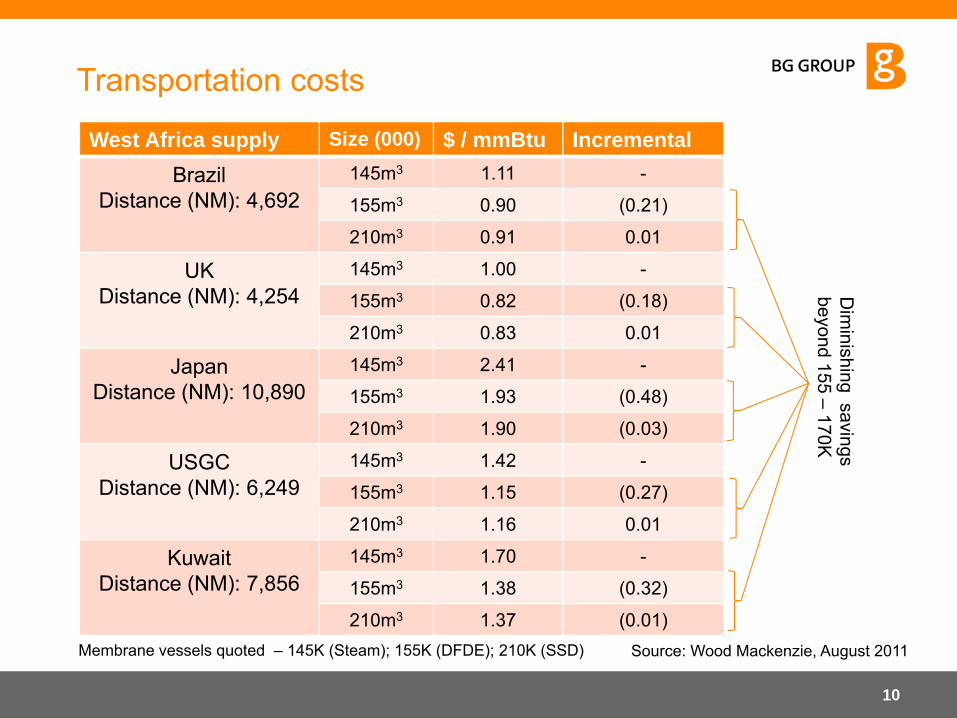

Transportation costs

West Africa supply Size (000) $ / mmBtu IncrementalBrazil

Distance (NM): 4,692145m3 1.11 -

155m3 0.90 (0.21)

210m3 0.91 0.01

UKDistance (NM): 4,254

145m3 1.00 -

155m3 0.82 (0.18)

210m3 0.83 0.01

JapanDistance (NM): 10,890

145m3 2.41 -

155m3 1.93 (0.48)

210m3 1.90 (0.03)

USGCDistance (NM): 6,249

145m3 1.42 -

155m3 1.15 (0.27)

210m3 1.16 0.01

KuwaitDistance (NM): 7,856

145m3 1.70 -

155m3 1.38 (0.32)

210m3 1.37 (0.01)

10

Dim

inishing savings beyond 155 –

170K

Source: Wood Mackenzie, August 2011Membrane vessels quoted – 145K (Steam); 155K (DFDE); 210K (SSD)

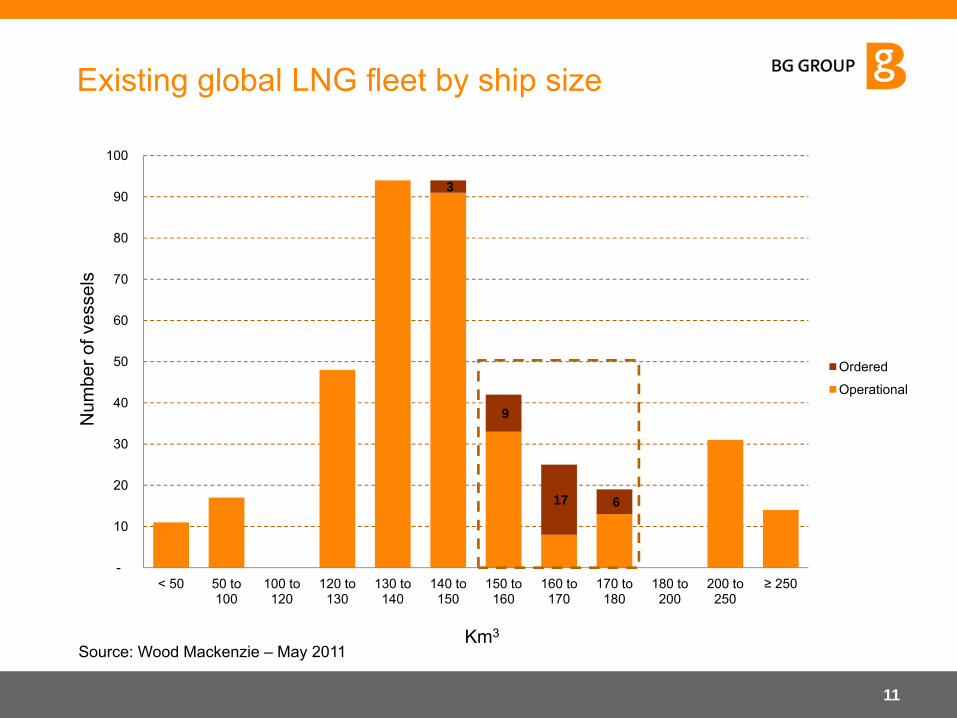

Existing global LNG fleet by ship size

11

3

9

17 6

-

10

20

30

40

50

60

70

80

90

100

< 50 50 to 100

100 to 120

120 to 130

130 to 140

140 to 150

150 to 160

160 to 170

170 to 180

180 to 200

200 to 250

≥ 250

Ordered

Operational

Source: Wood Mackenzie – May 2011

Num

ber o

f ves

sels

Km3

Challenges

• Low sulfur fuel requirements

• New entrants

• Crewing

• Low liquidity and volatility

• Cost management

12

Thank you