Embed Size (px)

Citation preview

MarketSentiment Survey

H2 2014

Portfolio–RICS–ELTINGAMarket Sentiment Survey | H2 2014

01 Highlights 02 Explanation 03 Index 05 Office sector 09 Retail sector 13 Industrial sector 16 General sentiment

Portfolio–RICS–ELTINGA Market Sentiment Survey | H2 2014

1

– Responses from this round of the Sentiment Survey have underpinned the improved situation

on both the investment and occupational markets. This is mainly driven by the office sector.

Tangible results in the retail and industrial sectors remain to be seen, however the situation is

clearly bottoming out in these sectors as well.

– According to RICS professionals, the Hungarian commercial real estate sector has become more

valuable as a result of the last six months. It is even better news that 79% of the respondents

expect investment appetite to improve further. Optimism permeates the office and retail sec-

tors, too.

– The Budapest Commercial Property Index has registered an increase of over 4 points since H1,

resulting from both rental growth and a slight yield compression reported by respondents.

– Office yield levels have shifted inwards by at least 25 basis points in all office categories, thus

reaching the softest yields in the history of this survey (from H2 2011). Typical rents in the

office sector are almost stable.

– The retail sector has shown improvement in the sentiment towards yield expectations and bot-

toming out towards rents. For Mall-type retail parks and Big Box retail we have observed yield

compression, but the resulting yields have rather caught up with H2 2013 levels.

– The optimism characterising the core markets is not observable in the industrial sector.

– More than two thirds of the respondents expect yield compression in the next 3-6 months

across.

Highlights

Yield (%)Rent (€/sqm/month)

Typical Minimum Maximum

Top CBD office building 7.3 14.0 12.5 18.0

Prime non-CBD office building 7.8 12.0 10.3 13.5

Good quality non-central office building 8.4 10.0 9.0 12.0

Prime out-of-town logistics center 9.0 3.1 2.5 4.0

Small Business Unit 9.0 4.0 3.5 4.5

Top 5 shopping malls 7.3 40.0 25.0 55.0

Mall-type retail park 8.3 10.0 8.0 13.0

Big box retail 8.4 7.0 5.5 9.0

All median figures for H2 2014

H2 2014 | Portfolio–RICS–ELTINGA Market Sentiment Survey

2

Rent (€ / sqm / month)

Distribution oftypical rent responses

median of typicalrent responses

median of maximumrent responses

median of minimumrent responses

Rati

o of

res

pons

es (

%)

Explanatory example chart

The most important output resulting from our research is the rental rates and yields data

(presented in charts similar to the one below). As this publication is based on the opinions

of individuals, these charts reflect the distribution of responses received in respect to a given

variable, i.e. rental rates or yields related to a type of property. Extreme values were removed

and the ranges of the remaining answers were then divided into subsections. The charts

indicate the percentage of responses falling into each subsection, with the median value

marked with a red vertical line (the median is the middle value of the data set when it has

been arranged in ascending order, i.e. the numeric value separating the higher half of the data

from the lower half).

The survey included questions regarding the realistic minimum, maximum, and typical

rental rates in respect to a particular type of property. While we also present all of these in

a tabular format, the rate charts only include the responses to the question of typical rental

rate levels.

Explanation

Portfolio–RICS–ELTINGA Market Sentiment Survey | H2 2014

3

The starting value of the Buda-

pest Commercial Property

Index was set to 100.00 based

on survey data collected in

the second half of 2011. By

H1 2013, it had decreased to

the region of 90.00, where it

has been floating ever since.

However, H2 2014 brought

a positive change: the Index

rose by over 4 points within

the last half-year period. The

index is made up of a com-

pound value that traces senior

real estate professionals’

assessments of current yields

and rental rates for the com-

mercial real estate market. A

measure of value is created

by dividing the median typi-

cal yearly rent by the current

yield for each of the eight sub-

segments present in the sur-

vey, and attributing weights to

these values in order to reflect

the relative volume of each

sub-segment. The results are

then added up and compared

against the other surveys. The

overall decrease since 2011

has been produced by a com-

bination of rents perceived to

be shrinking and yields seen

as growing. Similarly, the cur-

rent improvement is a result

of both factors partially coun-

tering their earlier changes at

the same time. Rents made a

stronger impact than yields in

both cases. The market sector

to have made the most sig-

nificant impact on the Index

in the last six months is the

Top-5 Malls where a slight

increase in yields was not suf-

ficient to counter a perceived

rental growth. All other sub-

markets have contributed pos-

itively to a lesser extent with

the exception of Top CBD

Offices. The overall picture

since 2011 is more colourful:

Big-Box and Mall-Type Retail

have driven the Index down

along with Prime Logistics,

while the Top-5 Malls made a

positive contribution over the

entire period..

BCP Index

93.74

BCP Index(H2 2011=100)

H2 2014 93.74

H1 2014 89.67

H2 2013 90.74

H1 2013 90.35

H2 2012 96.53

H1 2012 95.21

H2 2011 100

H2 2014 | Portfolio–RICS–ELTINGA Market Sentiment Survey

4

The survey uses eight hypothetical properties intended to represent major segments of the

Budapest commercial property market. Their descriptions include typical characteristics in

terms of location, quality, size, and occupancy, making them suitable investment products.

When asking about rental rates, hypothetical lease transactions were defined to reflect an

average exchange on the given market in terms of both size and basic conditions. The pho-

tos accompanying each detailed description of buildings are of properties that do not actu-

ally exist on the Hungarian market. However, they have been selected to create the right

impressions of the scenario at hand and to ensure that all respondents consider the same

property categories when answering the questions.

1. Top CBD office building

2. Prime non-CBD office building

3. Good quality non-central office building

4. One of the Top 5shopping malls

5. Mall-type retail park

6. Big box retail

7. Prime out-of-town logistics center

8. Small Business Unit

Categories

Portfolio–RICS–ELTINGA Market Sentiment Survey | H2 2014

5

In comparison with the

results of the previous sur-

veys, yield levels have

shifted inwards by at least

25 basis points in all office

categories, thus reaching

the softest yields in the his-

tory of this survey (since H2

2011). This shows an opti-

mistic view of how the mar-

ket has evolved in the last 6

months and reflects the lat-

est transactional evidence.

Rents show a more complex

picture. Typical rents for the

‘Top CBD Office’ category

decreased by 1 euro after a

peak in H1 2014, while typ-

ical rents in the other two

categories remained the

same. The biggest change is

also shown in the ‘Top CBD

Office’ category where max-

imum rents decreased by

1.75 euros after a peak in

H1 2014. Interestingly, sen-

timent towards minimum

rents has increased by 0.5

euro in this office category.

We have to note that the

variance in the responses is

relatively high in the first

office category with a high

number of responses falling

into the 15-18 euro range.

However, as a result of the

observed movements in all

office categories, rent lev-

els have not moved signifi-

cantly from the level they

were at in H1 2011. On

average, typical rents still

continue to displaya ten-

dency of approximating

minimum rents.

Office sector

Yield levels have decreased by at least 25 basis points in all office categories.

H2 2014 | Portfolio–RICS–ELTINGA Market Sentiment Survey

6

1. Top CBD office 2. Prime non-CBD office

20%

0%

4%

8%

12%

16%

5-6

7-8

9-10

11-1

2

13-1

4

15-1

6

17-1

8

19-2

0

21-2

2

23-2

4

median=14

0% 4% 8%

12% 16% 20% 24%

6-7

8-9

10-1

1

12-1

3

14-1

5

16-1

7

18-1

9

20-2

1

22-2

3

24-2

5

median=12

Rent opinions (€/sqm/m)Rent opinions (€/sqm/m)

0% 5%

10% 15% 20% 25% 30% 35% 40%

5-5.

25

5.5-

5.75

6-

6.25

6.

5-6.

75

7-7.

25

7.5-

7.75

8-

8.25

8.

5-8.

75

9-9.

25

9.5-

9.75

10

-10.

25

10.5

-10.

75

11-1

1.25

median = 7.25

0% 5%

10% 15% 20% 25% 30% 35%

5.25

-5.5

5.75

-6

6.25

-6.5

6.75

-7

7.25

-7.5

7.75

-8

8.25

-8.5

8.75

-9

9.25

-9.5

9.75

-10

10.2

5-10

.5

10.7

5-11

median = 7.75

Yield opinions (%)Yield opinions (%)

A-category (according to BRF) office building

located within the CBD of Budapest:

– represents the highest standard in

the market in terms of technical

specifications and prestige

– It has an underground garage

– The building is at least 95% let to

multiple tenants,

– at least 80% of the tenants are

international companies

– the average unexpired lease term

is at least 4 years

Market headline rental rate for a specific

letting transaction:

– 500 sqm office space

– 5-year lease term

– strong international tenant

A-category (according to BRF) office building

located in an established, but non-CBD office

location:

– represents high standard in the market

in terms of technical specifications and

prestige

– it has an underground garage

– the building is at least 95% let to

multiple tenants

– at least 80% of the tenants are

international companies

– the average unexpired lease term is at

least 4 years

Market headline rental rate for a specific letting

transaction:

– 500 sqm office space

– 5-year lease term

– strong international tenant

Portfolio–RICS–ELTINGA Market Sentiment Survey | H2 2014

7

6%

12%

18%

24%

30%

6-7

8-9

10-1

1

12-1

3

14-1

5

16-1

7

18-1

9

20-2

1

22-2

3

24-2

5

median = 10 Rent opinions (€/sqm/m)

0%

5%

10%

15%

20%

25%

5.25

-5.5

5.75

-6

6.25

-6.5

6.75

-7

7.25

-7.5

7.75

-8

8.25

-8.5

8.75

-9

9.25

-9.5

9.75

-10

10.2

5-10

.5

10.7

5-11

median = 8.375 Yield opinions (%)

A-category (according to BRF) office building

located in a non-central office location:

– built no more than 10 years ago

– it has an underground garage

– good public transportation

– the building is at least 95% let to

multiple tenants, not necessarily of

international covenant

– the average unexpired lease term is at

least 3 years

Market headline rental rate for a specific

letting transaction:

– 500 sqm office space

– 4-year lease term

– reliable and financially stable tenant

3. Good quality non-central offices

Strong interest from owner occupiers

and more liquidity from local HUF

funds. Banks are willing to borrow.

Increased state interest in strategic

real estate assets with continual

investment into infrastructure. Poten-

tial for office vacancy to drop further.

Growing interest from foreign funds

to consider Hungary but global uncer-

tainty as such could cool the market

quite quickly.

Hamish White MRICS, CIB Bank

Occupational markets are showing

healthy improvements, however

Q2 results were more optimistic than

Q3 results.

Jaroslav Kopac MRICS, JLL

H2 2014 | Portfolio–RICS–ELTINGA Market Sentiment Survey

8

Distribution of responses in 'CBD office rent' category

Distribution of responses in 'Prime Non-CBD office rent' category

0%

2%

4%

6%

8%

10%

12%

14% 6-

7

7-8

8-9

9-10

10-1

1

11-1

2

12-1

3

13-1

4

14-1

5

15-1

6

16-1

7

17-1

8

18-1

9

19-2

0

20-2

1

21-2

2

22-2

3

23-2

4

Typical rent frequency (2014 H2) (MA) Typical rent frequency (2014 H1) (MA)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

5-6

6-7

7-8

8-9

9-10

10-1

1

11-1

2

12-1

3

13-1

4

14-1

5

15-1

6

16-1

7

17-1

8

18-1

9

19-2

0

Typical rent frequency (2014 H2) (MA) Typical rent frequency (2014 H1) (MA)

Portfolio–RICS–ELTINGA Market Sentiment Survey | H2 2014

9

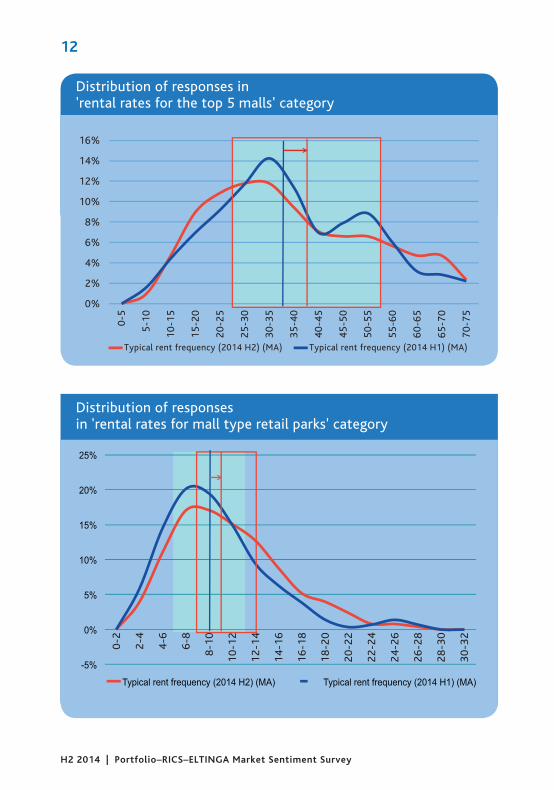

Compared to the last results,

the retail sector has shown

improvement in sentiment

towards yield expectations

and a stability/bottoming

out towards rents. Yields for

Top-5 Malls have been oscil-

lating in the 7-7.25% range

since the introduction of this

survey, and therefore the

outward movement of 25bp

in this round should be per-

ceived as stable. For Mall-

type Retail Parks and Big-

Box Retail we have observed

yield compression, but the

resulting yields have rather

caught up with H2 2013 lev-

els. Rents are stable.

Retail sector

The results of the survey are supportingthe general news on improved activity among investors as well as reports on rising retail sales volumes.

H2 2014 | Portfolio–RICS–ELTINGA Market Sentiment Survey

10

4. One of the Top 5 shopping malls

0%

4%

8%

12%

16%

20%

0-5

10-1

5

20-2

5

30-3

5

40-4

5

50-5

5

60-6

5

70-7

5

80-8

5

90-9

5

100-

105

median = 40

0%

5%

10%

15%

20%

25%

30%

35%

5-5.

25

5.5-

5.75

6-6.

25

6.5-

6.75

7-7.

25

7.5-

7.75

8-8.

25

8.5-

8.75

9-9.

25

9.5-

9.75

10-1

0.25

10.5

-10.

75

11-1

1.25

median = 7.25

Prime shopping center located in Budapest,

at a metro station or central location:

– GLA is at least 40,000 sqm, no vacancy

– the property accommodates at least

2 major anchor tenants

– the average unexpired lease term is

at least 5 years

Market headline rental rate for a specific

letting transaction:

– 200 sqm retail unit

– 5-7 year lease term

– strong international brand

– well-positioned unit within the centre

5%

10%

15%

20%

25%

30%

0-2

2-4

4-6

6-8

8-10

10

-12

12-1

4 14

-16

16-1

8 18

-20

20-2

2 22

-24

24-2

6 26

-28

28-3

0 30

-32

median = 10

0%

5%

10%

15%

20%

25%

5.25

-5.5

5.75

-6

6.25

-6.5

6.75

-7

7.25

-7.5

7.75

-8

8.25

-8.5

8.75

-9

9.25

-9.5

9.75

-10

10.2

5-10

.5

10.7

5-11

median = 8.25

Retail park located in Budapest, in an

established location:

– GLA is approx. 12,000 sqm, no

vacancy

– the property accommodates at

least 1 major anchor tenant

– the average unexpired lease term is

at least 5 years

Market headline rental rate for a specific

letting transaction:

– 300-400 sqm

– 5-year lease term

– local company / strong international

brand

5. Mall-type retail parks

Rent opinions (€/sqm/m)

Yield opinions (%)

Rent opinions (€/sqm/m)

Yield opinions (%)

Portfolio–RICS–ELTINGA Market Sentiment Survey | H2 2014

11

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

5-5.

25

5.5-

5.75

6-

6.25

6.

5-6.

75

7-7.

25

7.5-

7.75

8-

8.25

8.

5-8.

75

9-9.

25

9.5-

9.75

10

-10.

25

10.5

-10.

75

11-1

1.25

median = 8.375

0%

5%

10%

15%

20%

25%

30%

0-1

1-2

2-3

3-4

4-5

5-6

6-7

7-8

8-9

9-10

10

-11

11-1

2 12

-13

13-1

4 14

-15

15-1

6

median = 7

Stand alone hypermarket located within

an established retail park:

– GLA is at least 5,000 sqm and

single let to a reliable and

financially stable tenant

– the remaining lease duration is at

least 10 years

Market headline rental rate for a specific

letting transaction:

– 5,000 sqm big-box, 10-year lease term

– reliable and financially stable tenant

6. Big box retail

Yield opinions (%)

Rent opinions (€/sqm/m)

There is increasing invest-

ment activity mostly from

Hungarian investors but also

on behalf of international

companies who already have

a local track record. Both core

and value-added products are

sought after. Rents are still

under pressure which mostly

translates into the provision

of big incentives.

György Lindwurm MRICS,DTZ Hungary

Low risk opportunities now

attract increasing interest

resulting in a phenomenon

that was rarely seen in recent

years: competitive situa-

tions gradually driving yields

down. However, financing

remains tight and Hungary

must continue to be seen as

a cheap investment location

- these factors limit the room

for yield compression in the

foreseeable future.

Krisztián Hornok MRICS,Indotek Group

H2 2014 | Portfolio–RICS–ELTINGA Market Sentiment Survey

12

Distribution of responses in 'rental rates for mall type retail parks' category

Distribution of responses in'rental rates for the top 5 malls' category

0%

2%

4%

6%

8%

10%

12%

14%

16%

0-5

5-10

10-1

5

15-2

0

20-2

5

25-3

0

30-3

5

35-4

0

40-4

5

45-5

0

50-5

5

55-6

0

60-6

5

65-7

0

70-7

5

Typical rent frequency (2014 H2) (MA) Typical rent frequency (2014 H1) (MA)

-5%

0%

5%

10%

15%

20%

25%

0-2

2-4

4-6

6-8

8-1

0

10

-12

12

-14

14

-16

16

-18

18

-20

20

-22

22

-24

24

-26

26

-28

28

-30

30

-32

Typical rent frequency (2014 H2) (MA) Typical rent frequency (2014 H1) (MA)

Portfolio–RICS–ELTINGA Market Sentiment Survey | H2 2014

13

The optimism characteris-

ing the core markets is not

observable in the indus-

trial sector. Respondents are

still cautious when consider-

ing rents. The results of the

survey show hesitation in

each category with a slight

increase compared to the

June figures, but rather pres-

sure compared to prior esti-

mates. Typical rents are a

little above €3 per square

metre per month in the case

of logistics schemes and

around €4 in the case of SBU.

There has been no transac-

tion in this sector to influ-

ence yield opinions, conse-

quently the 9% has remained

unchanged ever since the

survey started. Confidence in

this sector is still low, both as

development and as invest-

ment products.

Industrial sector

Still no sign of optimism in the industrial sector.

H2 2014 | Portfolio–RICS–ELTINGA Market Sentiment Survey

14

7. Small Business Units

0% 5%

10% 15% 20% 25% 30% 35% 40% 45% 50% 55%

0-0.

5 0.

5-1

1-1.

5 1.

5-2

2-2.

5 2.

5-3

3-3.

5 3.

5-4

4-4.

5 4.

5-5

5-5.

5 5.

5-6

6-6.

5 6.

5-7

7-7.

5 7.

5-8

median = 3.125

Rent opinions (€/sqm/m)

0%

5%

10%

15%

20%

25%

30%

35%

40%

5.25

-5.5

5.75

-6

6.25

-6.5

6.75

-7

7.5-

7.75

8-8.

25

8.5-

8.75

9-9.

25

9.5-

9.75

10-1

0.25

0.5-

10.7

5

11-1

1.25

median = 9

Yield opinions (%)

A-category industrial property located within

Budapest, close to main arterial road:

– GLA is at least 10,000 sqm (could be in

multiple buildings)

– the property is approx. 100% let to

multiple tenants

– the average unexpired lease term is at

least 3 years

Market headline rental rates for a specific

letting transaction:

– 500 sqm warehouse space

– 3-year lease term

– reliable and financially stable tenant

A-category industrial property located

approx 5 minutes from a motorway:

– GLA is at least 25,000 sqm (could be in

multiple buildings)

– The property is approx. 100% let to

multiple tenants

– the average unexpired lease term is at

least 4 years

Market headline rental rates for a specific

letting transaction:

– 3,000 sqm warehouse space

– 5-year lease term

– strong international tenant

8. Prime out-of-town logistics centers

0% 3% 6% 9%

12% 15% 18% 21% 24% 27% 30%

0-0.

5 0.

5-1

1-1.

5 1.

5-2

2-2.

5 2.

5-3

3-3.

5 3.

5-4

4-4.

5 4.

5-5

5-5.

5 5.

5-6

6-6.

5 6.

5-7

7-7.

5 7.

5-8

median = 4

Rent opinions (€/sqm/m)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

5.5-

5.75

6-

6.25

6.

5-6.

75

7-7.

25

7.5-

7.75

8-

8.25

8.

5-8.

75

9-9.

25

9.5-

9.75

10

-10.

25

0.5-

10.7

5 11

-11.

25

median = 9 Yield opinions (%)

Portfolio–RICS–ELTINGA Market Sentiment Survey | H2 2014

15

Distribution of responses in category 'rent of out-of-town logistics buildings'

0%

5%

10%

15%

20%

25%

0-0.

5

0.5-

1

1-1.

5

1.5-

2

2-2.

5

2.5-

3

3-3.

5

3.5-

4

4-4.

5

4.5-

5

5-5.

5

5.5-

6

6-6.

5

6.5-

7

Typical rent frequency (2014 H2) (MA) Typical rent frequency (2014 H1) (MA)

It really seems like that the ice is

finally melting in our markets as

well!

Valter Kalaus MRICS, VLK Consulting

I expect only a slight yield

compression.

László Vas, Diófa Asset Management

New movemenents on the hori-

zon: Asian investors are active in

the industrial sector.

Name not given

H2 2014 | Portfolio–RICS–ELTINGA Market Sentiment Survey

16

Which commercial segment do you think currently offers the best conditions for an Investor?

How do you think investment appetite for property will change over the next six months?

Which commercial segment do you think currently offers the best conditions for a Developer?

Office 60%

Retail 21%

Industrial 11%

Other 2%

I don't know 6%

Office 60%

Retail 15%

Industrial

13%

Other 8%

I don't know 4%

Improve 79%

Same 13%

Worse 0%

I don’t know 8%

General sentiment

A majority now expects yield compression for the next 3-6 months across sectors.

Do you expect yield compression for the next 3-6 months across sectors?

no 29%

yes 71%

Portfolio–RICS–ELTINGA Market Sentiment Survey | H2 2014

17

Median yields (%)

Top CBD offices, rents (euro / sqm / month)

7

7.25

7.5

7.75

8

8.25

8.5

8.75

9

9.25

9.5

2011H2

2012H1

2012H2

2013H1

2013H2

2014H1

2014H2

SMALL BUSINESS UNIT

PRIME OUT OF TOWNLOGISTICS

GOOD QUALITYNON-CENTRAL OFFICE

MALL TYPE RETAIL PARK

BIG BOX RETAIL

PRIME NON-CBD OFFICE

TOP CBD OFF

TOP 5 MALL

0

5

10

15

20

25

2011 H2 2012 H1 2012 H2 2013 H1 2013 H2 2014 H1 2014 H2

typical

maximum

minimum

H2 2014 | Portfolio–RICS–ELTINGA Market Sentiment Survey

18

Out of town logistics, rents (euro / sqm / month)

Top five malls, rents (euro / sqm / month)

0

1

2

3

4

5

6

2011 H2 2012 H1 2012 H2 2013 H1 2013 H2 2014 H1 2014 H2

typical

maximum

minimum

0

5

10

15

20

25

30

35

40

45

50

55

60

65

2011 H2 2012 H1 2012 H2 2013 H1 2013 H2 2014 H1 2014 H2

typical

maximum

minimum

Portfolio–RICS–ELTINGA Market Sentiment Survey | H2 2014

19

A biannual publication, the Market Sentiment Survey is a collaboration between the ELT-

INGA Centre for Real Estate Research, Portfolio and RICS Hungary. It has been designed to

provide a clear picture of how Hungary’s senior real estate professionals see current yield

and rental rates, as well as general market expectations. The purpose of the Market Senti-

ment Survey is to improve transparency on the Hungarian real estate market by establish-

ing a benchmark for sentiment drawing on a wide professional basis. All Hungarian RICS

members (both full members and candidates for membership) were invited to fill in a ques-

tionnaire prepared by RICS and Portfolio.hu. They were asked for their opinions on current

market yields and rental rates, as well as on future market expectations. A total of nearly 50

real estate professionals participated actively in the current Market Sentiment Survey. Of

the respondents, 70% were full RICS members and more than 75% have over 10 years of

professional experience. The completed surveys indicate that around 65% of respondents

work for international companies. Respondents were asked to provide information on their

industry and their personal specialty within their organisation. Nearly 60% of respondents

work for consultancy firms. However, developers and asset management professionals also

weighed in heavily within the survey. The respondents’ fields of specialisation were fairly

diverse: valuation, investment, development and asset management were the best repre-

sented categories in the survey.

About the survey

Ratio of respondents own work specialism

0%

5%

10%

15%

20%

25%

30%

35%

Assetmanagement

Develop-ment

Financing Investment Valuation Letting Research Other

H2 2014 | Portfolio–RICS–ELTINGA Market Sentiment Survey

20

Definitions

Market Yield: The current net annual income divided by the purchase price received by the

Vendor in a transaction where the asset has been traded at Market Value as of today. Mar-

ket Value is the estimated amount for which a property should exchange on a certain date;

between a willing buyer and a willing seller; in an arm’s length transaction; after proper mar-

keting; when both parties had each acted knowledgeably, prudently and without compulsion.

Market Headline Rent: The estimated amount for which a property, or part of a property

should lease on appropriate lease terms between a willing landlord and a willing tenant; on

a certain date; in an arm’s length transaction; after proper marketing; when both parties had

each acted knowledgeably, prudently and without compulsion.

Category ‘A’: A building that either conforms to all the „hard criteria“ and at least 6 of the

„soft criteria“ or certified by Breeam / LEED. Hard criteria: modern cable management, a mod-

ern air handling system, adequate provision of secure dedicated parking (at least parking ratio

of 1/75 not applying to refurbishments and periphery sub-market), a high quality standard

finish, 24-hour access and security. Soft criteria: high speed modern lifts, clear ceiling

height of at least 2.70 m, prestige/quality reception area, flexible partitioning, high quality

architectural design, services in the building / immediate vicinity, power-supply back-up, dou-

ble-glazed windows / anti-glare glass, restaurant/canteen, quality finish to working areas.

Budapest Research Forum (BRF): It was established in 2000 and currently include the fol-

lowing members: CB Richard Ellis, Colliers, Cushman & Wakefield, DTZ, Eston, GVA Robertson,

Jones Lang LaSalle. The aim of BRF is to represent a regulated framework where the leading

property advisors can discuss the problems related to the Budapest property market, share

and analyse market information.

RIRIRICSCSCS ––– tttthehehehe RRRRoyoyoyoyoyalalalalal IIIIInsnsnsnsnstitititititutututututititt on of f Chhararartetetetetererererer ddddd SuSuSuSuSurrrveyororororors s s s s –– was created in 181818686868 iiinnn thttheee UnUnUnititittedededee KKKKKinininningdgdgdgdgdomoomomom. ItItt receceiiveveved d d d d a a a a a rorororooyayyyy l l l chchchchcharaaaa ter in 1881.

RIRIRICSCSCS mmmemememmbebebebersrsrsrs aaaaarerererere kkkkknononononownwnwnwnw aaaaasss s s chchchhhaararara teteterereeddd suuuurvrvrvvveyeyeyeyeyororororors,s,s, and are recececece ogogogogogogninininin sesesesesesedddddddbybyby ttthehehe dddesesesigigignanananatitittionononn aaaaftftftf ererer tttheheheeeiriririr nnnnnamamamamame ee ––– FRFRFRICICICS S S (f(f(f(f(fororororo FFFFFeleeeelloloow ww w w ofofofofof RRRRRICICICICCS)S)S)S)S) or MRMRMRICICICS S S (f(f(fororor MMMMemememembebebebeer rrrr ofofofff RRICCCS)S)S)...

ToToTodadaday y y RIRIRICSCSCS iiisss aaa glglglglobobobbal pprororororopepepertrrrr y profoffffesesesesessisisisis onononoo alaa bboddody y y y y wwiwiwiw ththththth 110000 ,000quququalalalifififieieied d d mememembmbmbererers ss ininin oovevevevever r rr 10100000 cooountrrrtrrieieeieesss.ss TTThehehe kkkeyeyey rrrrrolololololeseseses ooooof ff RICS are tototo rrregegegulululatatatee e anananddd pprp omomomomototototteeeee tthththt e prprprofesesessis ononononon, , , mamamamm ininintataaininn ttthehehehehe hhhhhigigigiggheheheheheststststt eeeeedududududu---cacacatititionononalalal aaandndnd ppprororofefefessssssioioioionanananallll stststandards, ppprororororotetetetetectctct ccclililienee tststss aaaandndndndnd ccconononononsus mersthththrororougugugh h h a a a stststriririctctct cccododode e e off eeeethththt ici s and dd prrovvovovvididdiddeeeee imimimpapapartrtrtiaii l adadadddvivvivivicecececec , ,, , , anaaaa alysis anananddd guguguidididananancecece

ChChChararartetetererereddd sususurvrvrveyeyeyorororss s hehehelpplp ttttoo sususuusuststss aiaiaia nnn ththhthheeee ususussse e e e e ofofof lllanannd dd ana d d unnnnunlololololockckckkk the lololongngng tttererermmm vavavalululueee ofofof ppprororopepepertrtrty.y. TTThehehehehey yy y y arararrreeeee kkekekekey y y totototoo eeeffffficicciieientn mmarkeeetststss iiiin nnn nlalalandndnd, , , prprpropopopererertytyty aaandndnd ttthehehe eeenvnvnvirrrrononononmemeemementntntntnt wwwwwiititithohohoutututtt wwhihh ch importantntn wwwwworororororldldldldld ecece onononomomomieieies s s wowowoulululddd nononot tt bebebe aaablblblb e eee totototo ffffunununununctctctcc ioioionnn efefeffeffefefffectc ivvely.yy

AnAnA nanana OOOrcrcrcsisisik,k,k, RRRegegegioioionananal l l MaMaManananagegeg r r r ––– RIRIRIRICSCSCSS CCCCenenenee trtrtrttralalaalal & Eastern EuropeE:E:E aaaororo cscssikikk@r@[email protected] g g W:W:W: wwwwwwwww.r.r.ricicicsss.orororg/g//eueueuurororopepepepep

Portfolio.hu–RICS–ELTINGA Market Sentiment Survey | H2 2014

• Csanád Csűrös – Portfolio, Business Development Director

• Krisztián Hornok MRICS – Transaction Director, Indotek Group

• Áron Horváth – ELTINGA

• Jaroslav Kopac MRICS – Jones Lang LaSalle Kft. National Director – Head of Valuation Hungary

• György Lindwurm MRICS – DTZ Hungary Kft. Associate Director – Investment

• Aliz McLean – ELTINGA

• Edina Winkler MRICS – DTZ Hungary Kft. Senior Surveyor – Valuation, RICS Hungary Board Member

Contributors