Embed Size (px)

Citation preview

cushmanwakefield.com

Market ReportSuburban Maryland | 4th Quarter 2017

Cushman & Wakefield | 2

DC Metropolitan Area Overview..............................................................................3

Suburban Maryland & Map...................................................................................4-6

Bethesda/Chevy Chase...............................................................................................7

Rock Spring Park..........................................................................................................8

Pike Corridor..................................................................................................................9

I-270/Rockville..............................................................................................................10

Gaithersburg/Germantown.......................................................................................11

Silver Spring....................................................................................................................12

Prince George’s County..............................................................................................13

Frederick County..........................................................................................................14

Appendix.........................................................................................................................15

Tables..........................................................................................................................18-25

Methodology & Definitions......................................................................................26

About Cushman & Wakefield.................................................................................27

Contents

cushmanwakefield.com | 3

Washington, DC Metropolitan Area

WASHINGTON, DC METRO

Q4 16 Q4 17 12-Month Forecast

DC Metro Employment 3.2M 3.3M

DC Metro Unemployment 3.8% 3.6%

U.S. Unemployment 4.6% 4.1%

Economic Indicators

Market IndicatorsQ4 16 Q4 17 12-Month

Forecast

Overall Vacancy 17.8% 17.8%

Net Absorption 1.4M 1.9M

Under Construction 8.4M 10.0M

Average Asking Rent (FS) $35.85 $37.54

Net Absorption/Asking Rent 4Q TRAILING AVERAGE

Washington, DC Metropolitan Area NET ABSORPTION - DELIVERIES - VACANCY

The past 12 months proved to be another strong year for economic performance in the Washington, DC metropolitan region (DC metro). For a third straight year, job growth far exceeded the historical average, adding 56,300 nonfarm payroll positions in 2017 – only slightly off the 2015 and 2016 totals of 57,000 per year. Job growth was led by the office-intensive Professional and Business Services sector, which grew by 16,300 jobs in 2017. Job creation in other office-using sectors was flat to negative: employment in Financial Services ended the year up 700, in Federal Government down 500 and in Information down 2,500 jobs. Among non-office-using sectors, the Education and Healthcare, and Leisure and Hospitality sectors experienced strong gains of over 13,000 positions each. The District of Columbia (DC) added 10,000 jobs while Northern Virginia (NoVA) and Suburban Maryland (SMD) both added 23,000.

While job growth and the overall economy continued to surge, overall net absorption continued to erode compared to historical averages. The DC metro region absorbed 1.9 million square feet (msf) of space in 2017, well off the 2.6 msf that the region has averaged every year since 2001. The regional vacancy rate was 17.8%, relatively unchanged from year-end 2016. DC accounted for 600,000 square feet (sf) of absorption and a 12.4% vacancy rate, NoVA registered 1.0 msf of absorption and a vacancy rate of 21.5% and SMD had 130,000 sf of absorption with vacancy ending the year at 19.4%.

While technology, consumer goods and real estate firms executed several notable new leases in 2017, most large new transactions were executed by organizations that are typically on the “top deals” list in the DC metro region: federal agencies, law firms, not-for-profits and federal contractors. The federal government’s leasing arm – the General Services Administration (GSA) – was responsible for the largest lease of the year in each of the three DC metro jurisdictions, with the Federal Communications Commission leasing 473,000 sf in DC, the Transportation Security Administration leasing 625,000 sf in Northern Virginia, and the Department of Homeland Security leasing 575,000 sf in Suburban Maryland. These three cases demonstrate that the government will continue to consolidate large requirements in submarkets that offer quality development at a relative value compared to pricier, traditional government enclaves.

New supply in the core downtown submarkets of DC continues to be a concern for overall market fundamentals looking forward. The Central Business District (CBD), East End, and Capitol Hill/NoMa are expected to deliver over 7.0 msf of office space in the next 24 months, 4.8 msf of which is currently under construction. Among those projects that are currently under construction, 2.5 msf—51%—is already preleased. Expect vacancy rates and concessions to rise in these submarkets as tenants continue to seek the top floors while velocity on lesser space in new developments remains modest, at best.

On the flipside, the transit-oriented suburban submarkets have been relatively supply-constrained with under-construction projects nearing 80.0% preleased. This supply constraint is subject to change as a plethora of high-profile, large tenants are currently active in the market with limited existing quality space options left to accommodate them. This will benefit developers like Carr Properties, The Meridian Group and JBG Smith, all of whom have risked spec development. The next 12 to 18 months should see two or more developments getting underway in Reston/Herndon, one likely in Tysons, and an active market for projects that recently broke ground in Bethesda.

$36

$37

$37

$38

$38

$39

$39

-1,000

-500

0

500

1,000

1,500

2011 2012 2013 2014 2015 2016 2017Net Absorption, SF (thousands) Asking Rent, $ PSF

0%

4%

8%

12%

16%

20%

-6-4-202468

10

05 06 07 08 09 10 11 12 13 14 15 16 17

Vaca

ncy R

ate

MSF

Net Absorption Deliveries

Cushman & Wakefield | 4

Suburban Maryland

Overall Vacancy

Net Absorption/Asking Rent FOUR QUARTER TRAILING AVERAGE

Market IndicatorsQ4 16 Q4 17 12-Month

Forecast

Vacancy 20.6% 19.4%

YTD Absorption (sf) 747k 130k

Under Construction (sf) 0 1,106,787

Average Asking Rent $26.33 $26.85

$25.00$25.50$26.00$26.50$27.00$27.50$28.00$28.50$29.00

-3

-2

-1

0

1

2

3

2011 2012 2013 2014 2015 2016 Q2 2017

x 100

000

Net Absorption, MSF Asking Rent, $ PSF

Suburban Maryland Office Q4 2017

MARKETBEAT

cushmanwakefield.com

Economic Indicators

Market Indicators (Overall, All Classes)

Overall Net Absorption/Overall Asking Rent4-QTR TRAILING AVERAGE

Overall Vacancy

EconomyJob growth in Suburban Maryland remained strong in 2017, but themajority of job gains were in non-office-using sectors. From Januarythrough November, the local economy generated just over 15,700 netnew, nonfarm payroll jobs. Leading job growth year-over-year were theEducation and Healthcare sector with 5,400 jobs, and Leisure andHospitality with 5,300 jobs. For the office-using sectors there was a lossof about 1,350 jobs in Information, Financial, and Federal employment,and a small gain of 370 jobs in the Professional Business Servicessector.

Market OverviewFollowing headline-making headquarters relocations by the GeneralServices Administration (GSA) for the Department of HomelandSecurity’s (DHS) Citizenship and Immigration Services (CIS) to PrinceGeorge’s County, and by Marriott International to Bethesda/ChevyChase, Suburban Maryland once again captured two notable leases bythe close of the fourth quarter of 2017. JBG Smith secured two morepreleases (also the second and third largest leases of the quarter) at4747 Bethesda Avenue: Booz Allen Hamilton preleased 65,000 squarefeet (sf) and Host Hotels preleased 55,000 sf, bringing the Class Abuilding to 71.0% committed. These two leases helped new leasingactivity close the fourth quarter of 2017 at 3.7 million square feet (msf)—the highest level since 2007.

Such healthy leasing activity resulted in positive overall year-to-date netabsorption of 130,658 sf, 90,173 sf of which occurred in the fourthquarter. There was a handful of small to midsized tenants andexpansions that helped bolster overall net absorption. The GSAexpanded to take 12,000 sf at 20030 Century Boulevard, and the Makea Wish Foundation moved into 11,000 sf at 4451-4459 ForbesBoulevard. The largest move-in of the quarter was Bank of America/Merrill Lynch which occupied 23,500 sf at 7501 Wisconsin Avenue.Given positive absorption, overall vacancy declined 140 basis points(bps) year-over-year, closing the fourth quarter of 2017 at 19.4%. Withdeclining vacancy—particularly in the Bethesda/Chevy Chase submarketwhere vacancy remained among the lowest in the region—landlordshave begun to push overall asking rents upward. Overall asking rents forall classes in Suburban Maryland closed the fourth quarter of 2017 at$26.85 per square foot (psf).

Throughout 2017, headlines focused on the development story ofBethesda/Chevy Chase, particularly as several buildings are expected togo spec over the next 12 to 18 months. But other areas of the SuburbanMaryland market have also continued to attract tenants with build to-suitopportunities, including Kaiser Permanente’s building at 4000 GardenCity Drive, and the DHS/CIS headquarters at One Town Center.

OutlookWith the pipeline of new construction coming to the Bethesda/ChevyChase submarket and the Purple Line finally underway, excitementcontinues to build in the Suburban Maryland market. The area’s strongdemographics, exceptional amenities and growing range oftransportation options position Suburban Maryland for revitalization inthe Metro-accessible submarkets. With the increasing trend towardthe live-work-play environment, these new multipurpose developmentswill appeal strongly to companies that are looking to attract and retaintop talent in their workforce. However, vacancies in non-Metro servedlocations are likely to remain elevated as tenants gravitate towards moreamenitized options.

Q4 16 Q4 17 12-Month Forecast

D.C. Metro Employment 3.2M 3.3M

D.C. Metro Unemployment 3.8% 3.6%

U.S. Unemployment 4.7% 4.1%

Q4 16 Q4 17 12-Month Forecast

Vacancy 20.6% 19.4%

YTD Net Absorption (sf) 747k 130k

Under Construction (sf) 0 1,106,787

Average Asking Rent* $26.33 $26.85

*Rental rates reflect gross asking $psf/year

$25.00$25.50$26.00$26.50$27.00$27.50$28.00$28.50$29.00

-300-250-200-150-100-50

050

100150200250

2011 2012 2013 2014 2015 2016 Q4 2017

Thou

sand

s

Net Absorption, MSF Asking Rent, $ PSF

12%

14%

16%

18%

20%

22%

24%

2011 2012 2013 2014 2015 2016 2017

Historical Average = 19.5%

SUBURBAN MARYLAND OFFICE

Suburban Maryland Office Q4 2017

MARKETBEAT

cushmanwakefield.com

Economic Indicators

Market Indicators (Overall, All Classes)

Overall Net Absorption/Overall Asking Rent4-QTR TRAILING AVERAGE

Overall Vacancy

EconomyJob growth in Suburban Maryland remained strong in 2017, but themajority of job gains were in non-office-using sectors. From Januarythrough November, the local economy generated just over 15,700 netnew, nonfarm payroll jobs. Leading job growth year-over-year were theEducation and Healthcare sector with 5,400 jobs, and Leisure andHospitality with 5,300 jobs. For the office-using sectors there was a lossof about 1,350 jobs in Information, Financial, and Federal employment,and a small gain of 370 jobs in the Professional Business Servicessector.

Market OverviewFollowing headline-making headquarters relocations by the GeneralServices Administration (GSA) for the Department of HomelandSecurity’s (DHS) Citizenship and Immigration Services (CIS) to PrinceGeorge’s County, and by Marriott International to Bethesda/ChevyChase, Suburban Maryland once again captured two notable leases bythe close of the fourth quarter of 2017. JBG Smith secured two morepreleases (also the second and third largest leases of the quarter) at4747 Bethesda Avenue: Booz Allen Hamilton preleased 65,000 squarefeet (sf) and Host Hotels preleased 55,000 sf, bringing the Class Abuilding to 71.0% committed. These two leases helped new leasingactivity close the fourth quarter of 2017 at 3.7 million square feet (msf)—the highest level since 2007.

Such healthy leasing activity resulted in positive overall year-to-date netabsorption of 130,658 sf, 90,173 sf of which occurred in the fourthquarter. There was a handful of small to midsized tenants andexpansions that helped bolster overall net absorption. The GSAexpanded to take 12,000 sf at 20030 Century Boulevard, and the Makea Wish Foundation moved into 11,000 sf at 4451-4459 ForbesBoulevard. The largest move-in of the quarter was Bank of America/Merrill Lynch which occupied 23,500 sf at 7501 Wisconsin Avenue.Given positive absorption, overall vacancy declined 140 basis points(bps) year-over-year, closing the fourth quarter of 2017 at 19.4%. Withdeclining vacancy—particularly in the Bethesda/Chevy Chase submarketwhere vacancy remained among the lowest in the region—landlordshave begun to push overall asking rents upward. Overall asking rents forall classes in Suburban Maryland closed the fourth quarter of 2017 at$26.85 per square foot (psf).

Throughout 2017, headlines focused on the development story ofBethesda/Chevy Chase, particularly as several buildings are expected togo spec over the next 12 to 18 months. But other areas of the SuburbanMaryland market have also continued to attract tenants with build to-suitopportunities, including Kaiser Permanente’s building at 4000 GardenCity Drive, and the DHS/CIS headquarters at One Town Center.

OutlookWith the pipeline of new construction coming to the Bethesda/ChevyChase submarket and the Purple Line finally underway, excitementcontinues to build in the Suburban Maryland market. The area’s strongdemographics, exceptional amenities and growing range oftransportation options position Suburban Maryland for revitalization inthe Metro-accessible submarkets. With the increasing trend towardthe live-work-play environment, these new multipurpose developmentswill appeal strongly to companies that are looking to attract and retaintop talent in their workforce. However, vacancies in non-Metro servedlocations are likely to remain elevated as tenants gravitate towards moreamenitized options.

Q4 16 Q4 17 12-Month Forecast

D.C. Metro Employment 3.2M 3.3M

D.C. Metro Unemployment 3.8% 3.6%

U.S. Unemployment 4.7% 4.1%

Q4 16 Q4 17 12-Month Forecast

Vacancy 20.6% 19.4%

YTD Net Absorption (sf) 747k 130k

Under Construction (sf) 0 1,106,787

Average Asking Rent* $26.33 $26.85

*Rental rates reflect gross asking $psf/year

$25.00$25.50$26.00$26.50$27.00$27.50$28.00$28.50$29.00

-300-250-200-150-100-50

050

100150200250

2011 2012 2013 2014 2015 2016 Q4 2017

Thou

sand

s

Net Absorption, MSF Asking Rent, $ PSF

12%

14%

16%

18%

20%

22%

24%

2011 2012 2013 2014 2015 2016 2017

Historical Average = 19.5%

SUBURBAN MARYLAND OFFICE

EconomyJob growth in Suburban Maryland remained strong in 2017, but the majority of job gains were in non-office-using sectors. From January through November, the local economy generated just over 15,700 net new, nonfarm payroll jobs. Leading job growth year-over-year were the Education and Healthcare sector with 5,400 jobs, and Leisure and Hospitality with 5,300 jobs. For the office-using sectors there was a loss of about 1,350 jobs in Information, Financial, and Federal employment, and a small gain of 370 jobs in the Professional Business Services sector.

Market OverviewFollowing headline-making headquarters relocations by the General Services Administration (GSA) for the Department of Homeland Security’s (DHS) Citizenship and Immigration Services (CIS) to Prince George’s County, and by Marriott International to Bethesda/Chevy Chase, Suburban Maryland once again captured two notable leases by the close of the fourth quarter of 2017. JBG Smith secured two more preleases (also the second and third largest leases of the quarter) at 4747 Bethesda Avenue: Booz Allen Hamilton preleased 65,000 square feet (sf) and Host Hotels preleased 55,000 sf, bringing the Class A building to 71.0% committed. These two leases helped new leasing activity close the fourth quarter of 2017 at 3.7 million square feet (msf)—the highest level since 2007.

Such healthy leasing activity resulted in positive overall year-to-date net absorption of 130,658 sf, 90,173 sf of which occurred in the fourth quarter. There was a handful of small to midsized tenants and expansions that helped bolster overall net absorption. The GSA expanded to take 12,000 sf at 20030 Century Boulevard, and the Make a Wish Foundation moved into 11,000 sf at 4451-4459 Forbes Boulevard. The largest move-in of the quarter was Bank of America/Merrill Lynch which occupied 23,500 sf at 7501 Wisconsin Avenue. Given positive absorption, overall vacancy declined 140 basis points (bps) year-over-year, closing the fourth quarter of 2017 at 19.4%. With declining vacancy—particularly in the Bethesda/Chevy Chase submarket where vacancy remained among the lowest in the region—landlords have begun to push overall asking rents upward. Overall asking rents for all classes in Suburban Maryland closed the fourth quarter of 2017 at$26.85 per square foot (psf).

Throughout 2017, headlines focused on the development story of Bethesda/Chevy Chase, particularly as several buildings are expected to go spec over the next 12 to 18 months. But other areas of the Suburban Maryland market have also continued to attract tenants with build to-suit opportunities, including Kaiser Permanente’s building at 4000 Garden City Drive, and the DHS/CIS headquarters at One Town Center.

OutlookWith the pipeline of new construction coming to the Bethesda/Chevy Chase submarket and the Purple Line finally underway, excitement continues to build in the Suburban Maryland market. The area’s strong demographics, exceptional amenities and growing range of transportation options position Suburban Maryland for revitalization in the Metro-accessible submarkets. With the increasing trend toward the live-work-play environment, these new multipurpose developments will appeal strongly to companies that are looking to attract and retain top talent in their workforce. However, vacancies in non-Metro served locations are likely to remain elevated as tenants gravitate towards more amenitized options.

cushmanwakefield.com | 5

Maryland Office Submarkets

cushmanwakefield.com | 5

Maryland Office Submarkets

270

28

340

85

190

495 395

95

95

210 51

295

9529

695

795

83

32

27 26

236

FREDERICK

GERMANTOWN

GAITHERSBURG

I-270/ROCKVILLE

PIKE CORRIDOR

ROCK SPRINGPARK

BETHESDA/CHEVY CHASE SILVER

SPRING

NORTHSILVER SPRING

LAUREL

BELTSVILLE/COLLEGE PARK

GREENBELT

BOWIE

OXON HILL/SUITLAND

LANDOVER/LANHAM

Cushman & Wakefield | 6

Suburban Maryland Office MarketInventory & Vacancy by Submarket, Fourth Quarter 2017

Top Transactions

Suburban Maryland Office MarketNet Absorption - Deliveries - Vacancy, Fourth Quarter 2017

Key Lease Transactions Q4 2017

2

Suburban MarylandNet Absorption – Deliveries – Vacancy

0%

4%

8%

12%

16%

20%

24%

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

05 06 07 08 09 10 11 12 13 14 15 16 17

Vaca

ncy

Rat

e

MSF

Net Absorption Deliveries Vacancy Rate

PROPERTY SF TENANT TRANSACTION TYPE SUBMARKET

2115 East Jefferson Street 89,708 GSA - National Institutes of Health Renewal Pike Corridor

4747 Bethesda Avenue 65,000 Booz Allen Hamilton Direct Bethesda/Chevy Chase

4747 Bethesda Avenue 55,050 Host Hotels Direct Bethesda/Chevy Chase

6511 America Boulevard 54,000 GSA - Federal Emergency Management Agency Renewal Bethesda/Chevy Chase

4600 Powder Mill Road 40,000 Virginia College Renewal Bethesda/Chevy Chase

4

Suburban Maryland Office Market Inventory & Vacancy by Submarket, Fourth Quarter 2017

10%

12%

14%

16%

18%

20%

22%

24%

0

2

4

6

8

10

12

14

16

Vaca

ncy

Rat

e

MSF

Class A Class B Class C Vacancy % MD Overall Vacancy

cushmanwakefield.com | 7

Bethesda/Chevy Chase

The Bethesda/Chevy Chase submarket closed the fourth quarter of 2017 with generally healthy market fundamentals. Year-to-date new leasing activity registered just over 1.2 million square feet (msf)—a record high due in large part to Marriott International, Inc.’s prelease for its future headquarters at 7750 Wisconsin Avenue committed to earlier in the year. Additionally, fourth-quarter leasing activity was bolstered by two preleases secured by JBG Smith at 4747 Bethesda Avenue: Booz Allen Hamilton preleased 65,000 square feet (sf) and Host Hotels preleased 55,050 sf. Combined with JBG Smith’s previously announced commitment to take approximately 100,000 sf at the property, the Class A building is currently 71.0% preleased. The third-largest lease of the fourth quarter of 2017 was that executed by WTOP for 30,612 sf at 5425 Wisconsin Avenue.

Despite record new leasing activity, year-to-date net absorption closed the fourth quarter of 2017 at negative 91,454 sf—a year-over-year (YOY) decline of 67.0%. The decline was primarily a result of limited near-term availabilities for tenants. The first new construction building is not scheduled to deliver until mid-2019, leaving few existing options in the Bethesda/Chevy Chase submarket. However, given that new leasing activity has been buoyed by a number of large preleases from new-to-the-submarket tenants, once those new buildings deliver, net absorption will certainly spike upward.

The overall vacancy rate in the Bethesda/Chevy Chase submarket closed the fourth quarter of 2017 at 10.8%. While that is up slightly year-over-year by 110 basis points (bps), it is still among the lowest in the region.

Given the relatively low vacancy in the submarket, overall asking rents have continued to hold steady, closing the fourth quarter of 2017 at $36.89 per square foot (psf) for all classes. Class A rental rates closed the quarter at $41.08 psf—a 4% decline quarter-over-quarter—primarily due to a large block of space with above-average asking rents leasing up in the fourth quarter, and increasingly limited quality options remaining on the market.

OutlookOverall, the Bethesda/Chevy Chase submarket is positioned for a market resurgence, with multiple buildings in the construction pipeline and healthy preleasing at very strong rents already underway for many of them. Given the submarket’s strong amenity base, Metro access to both the existing Red Line and a future Purple Line station, and a broad tenant base of professional and business services, the new deliveries will continue to attract tenants from across the region. This is evident in Marriott’s decision to relocate its headquarters to the market, and Booz Allen Hamilton and Host Hotels committing to leases in Bethesda from other submarkets. Additionally, with one of the lowest vacancy rates in the region and no new deliveries set to hit the market until mid-2019, the Bethesda/Chevy Chase submarket is expected to remain landlord-favorable for the next 12 to 18 months.

Market Indicators*Arrows = Current Qtr Trend

Asking Rent

Net Absorption – Deliveries – Vacancy

New Leasing Activity

Asking Rent$36.89

Net Absorption(91,454 SF)

Vacancy10.3%

Deliveries0 SF

Under Construction626,020 SF

5

Bethesda/Chevy Chase Net Absorption – Deliveries - Vacancy

0%

2%

4%

6%

8%

10%

12%

14%

-0.2-0.1-0.10.00.10.10.20.20.30.30.4

09 10 11 12 13 14 15 16 17

Vaca

ncy

Rat

e

MSF

Net Absorption Deliveries Vacancy Rate

6

Bethesda/Chevy ChaseNew Leasing Activity

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

MSF

Q1 Q2 Q3 Q4

7

Bethesda/Chevy Chase

$25

$30

$35

$40

$45

$50

$55

2009 2010 2011 2012 2013 2014 2015 2016 Q4 2017

Full

Serv

ice

PSF

Class A Class B, $ PSF

Asking Rent

Cushman & Wakefield | 8

Rock Spring Park

8

Rock Spring ParkNet Absorption – Deliveries - Vacancy

0%

5%

10%

15%

20%

25%

30%

35%

-0.2-0.2-0.1-0.10.00.10.10.20.20.3

09 10 11 12 13 14 15 16 17

Vaca

ncy

Rat

e

MSF

Net Absorption Deliveries Vacancy Rate

As it did during the first half of the year, Rock Spring Park continued to see improving, albeit still soft, market fundamentals through the fourth quarter of 2017. New leasing activity for the quarter was comprised of small and mid-sized tenants. The largest lease of the quarter was that of the Make a Wish Foundation, which signed for 11,464 square feet (sf) at 10401 Fernwood Road. In all, total new leasing activity for the fourth quarter of 2017 totaled 19,342 sf, which helped bring the year-to-date new leasing to 68,151sf. That wasn’t quite enough, however, to top 2016’s total of 128,116 sf, registering a 39% decrease year-over-year.

Year-to-date overall net absorption remained positive, closing the year at 188,515 sf. Most of that absorption was due to the National Institutes of Health (NIH) vacating from 5635 Fishers Lane and relocating to 6700 Rockledge Drive in the first quarter.

The substantial positive absorption in the market contributed to a decline in overall vacancy rates which closed the fourth quarter of 2017 at 24.8% —down 430 basis points (bps) year-over-year. With Suburban Maryland as a whole posting an average overall vacancy rate of 19.4%, however, Rock Spring Park continued to face market softness, particularly as older, less-amenitized office parks struggle to compete against the Metro-accessible locations tenants continue to seek.

Given elevated vacancy rates, overall asking rents dipped 1.8%, closing the fourth quarter of 2017 at $29.80 per square foot (psf). Despite above market vacancy, asking rents in Rock Spring Park remained on par with Montgomery County’s average of $29.20 psf, and well above Suburban Maryland’s average of $26.85 psf. Overall Class A asking rents in Rock Spring Park averaged $30.58 psf for the fourth quarter, slightly below the county average of $31.52 psf, signaling an opportunity for tenants to find quality space at competitive price points.

Outlook

Overall, the Rock Spring Park submarket continues to tighten, though slowly, as small and mid-sized tenants help to chip away at remaining vacancy. With the Marriott Headquarters slated for residential, the risk of new office vacancy coming online following the hotelier’s relocation to the Bethesda/Chevy Chase submarket is mitigated. Additionally, the market should see an increase in the population base as the new residential comes along, and along with it, more amenities to further attract tenants from both the public and private sectors. With no new construction in the pipeline vacancy rates should remain in check and asking rents holding.

Market Indicators*Arrows = Current Qtr Trend

Net Absorption – Deliveries – Vacancy

9

Rock Spring ParkNew Leasing Activity

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.18

0.20

2012 2013 2014 2015 2016 2017

MSF

Q1 Q2 Q3 Q4

10

Rock Spring Park

$20

$22

$24

$26

$28

$30

$32

$34

$36

2011 2012 2013 2014 2015 2016 Q4 2017

Full

Serv

ice

PSF

Class B, $ PSFClass A, $ PSF

Asking Rent

Asking Rent$29.70

Net Absorption188,515 SF

Vacancy24.8%

Deliveries0 SF

Under Construction0 SF

Asking Rent

New Leasing Activity

cushmanwakefield.com | 9

Pike Corridor

11

Pike CorridorNet Absorption – Deliveries - Vacancy

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

-1.5

-1.0

-0.5

0.0

0.5

1.0

10 11 12 13 14 15 16 17

Vaca

ncy

Rat

e

MSF

Net Absorption Deliveries Vacancy Rate

Market fundamentals in the Pike Corridor submarket were varied throughout the fourth quarter of 2017. Year-to-date new leasing activity picked up during the quarter, closing at just under 338,943 square feet (sf) —a 75.7% increase from the third quarter. The largest lease of the quarter was signed by the General Services Administration (GSA) on behalf of the National Institutes of Health for a 90,000-sf renewal at 2115 East Jefferson Street. The largest new lease was executed by The American Physiological Society (APS), which committed to just over 30,000 sf at 6120 Executive Boulevard.

Despite strong leasing activity, year-to-date net absorption still registered at negative 96,725 sf at the close of the fourth quarter of 2017. It should be noted, however, that this was due to several tenants vacating the submarket during the first half of the year: Dixon Hughes vacated 24,849 sf at Rockville Pike, the FDA vacated 10,000 sf at 1 Church Street, and Montgomery County’s consolidation from 47,322 sf at 40 West Gude Drive.

Overall vacancy rates closed the fourth quarter of 2017 at 17.9%—a 110-basis-point (bps) increase year-over-year. Pike Corridor’s fourth quarter vacancy matched the overall average vacancy for Montgomery County, and 150 bps lower than Suburban Maryland’s average as a whole. While vacancy has declined, overall asking rents for all classes have remained in check, closing the fourth quarter of 2017 at $28.30 per square foot (psf). The overall average rent for Class A product closed the quarter at $30.05 psf, in line with Suburban Maryland’s overall Class A average of $30.16 psf.

Outlook

The Pike Corridor submarket started to experience some improvements in its market fundamentals through the fourth quarter of 2017. The area remains well-positioned to attract tenants, particularly as construction of the Pike & Rose mixed-use development comes to an end, bringing with it retail and residential options to the area. With the growing demand for amenity-heavy and Metro-accessible locations, vacancy rates are expected to continue decreasing over the next 18 to 24 months, which will help to keep asking rents elevated.

Market Indicators*Arrows = Current Qtr Trend

Net Absorption – Deliveries – Vacancy

12

Pike CorridorNew Leasing Activity

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

2010 2011 2012 2013 2014 2015 2016 2017

MSF

Q1 Q2 Q3 Q4

13

Pike CorridorAsking Rent

$20

$22

$24

$26

$28

$30

$32

$34

$36

2012 2013 2014 2015 2016 Q4 2017

Full

Serv

ice

PSF

Class A Class B, $ PSF

Asking Rent$28.30 FS

Net Absorption(96,725 SF)

Vacancy17.9%

Deliveries0 SF

Under Construction0 SF

Asking Rent

New Leasing Activity

Cushman & Wakefield | 10

I-270/Rockville

Similar to trends in the first half of the year, the 1-270/Rockville submarket continued to see diverging market fundamentals throughout the fourth quarter of 2017. New leasing activity decreased by 43.0% year-over-year, with year-to-date new leasing closing the fourth quarter of 2017 at 372,206 square feet (sf). There were, however, several noteworthy leases greater than 10,000 square feet (sf). The largest new lease of the quarter was signed by Oil Price Information Service (OPIS) for 36,599 sf at 2099 Gaither Road; the second-largest signed by Skanska for 14,918 sf at 700 King Farm.

Despite the decline in new leasing activity, year-to-date net absorption remained positive, closing the fourth quarter of 2017 at 250,494 sf. This was particularly noteworthy given that the I-270/Rockville submarket registered 50,471 sf of positive absorption in 2016.

Given the significant positive absorption, vacancy rates declined 150 basis points (bps) from the fourth quarter of 2016, closing the fourth quarter of 2017 at 23.0%. Vacancy in the I-270/ Rockville submarket was 510 bps higher than Montgomery County’s vacancy rate of 17.9%.

With vacancy rates declining and positive net absorption, landlords have continued to push asking rents. Overall asking rents closed the fourth quarter at $28.35 per square foot (psf)—a 3.0% increase year-over-year.

Outlook

New construction remains limited in the I-270/Rockville submarket which will help keep vacancy rates in check. However, with increasing consumer demand for walkable, mixed-use environments and Metro-proximate locations, the I-270/Rockville submarket could be a competitive alternative for tenants seeking large blocks of space in amenitized locations while seeking cost-effective options.

Market Indicators*Arrows = Current Qtr Trend

Asking Rent$28.34

Net Absorption250,494 SF

Vacancy23.0%

Deliveries0 SF

Under Construction0 SF

14

I-270/Rockville Net Absorption – Deliveries - Vacancy

0%

5%

10%

15%

20%

25%

30%

-0.5-0.4-0.3-0.2-0.10.00.10.20.30.4

09 10 11 12 13 14 15 16 17

Vaca

ncy

Rat

e

MSF

Net Absorption Deliveries Vacancy Rate

Net Absorption – Deliveries – Vacancy

15

I-270/RockvilleNew Leasing Activity

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

MSF

Q1 Q2 Q3 Q4

16

I-270/Rockville

$20

$22

$24

$26

$28

$30

$32

$34

$36

2009 2010 2011 2012 2013 2014 2015 2016 Q4 2017

Full

Serv

ice

PSF

Class A Class B, $ PSF

Asking Rent

Asking Rent

New Leasing Activity

cushmanwakefield.com | 11

Gaithersburg/Germantown

Market fundamentals in the Gaithersburg and Germantown submarkets remained stable through the fourth quarter of 2017. Both submarkets experienced sluggish new leasing activity during the quarter. Year-to-date new leasing activity in Gaithersburg closed the quarter at 35,062 square feet (sf)—a 31.0% decrease year-over-year. With no new leasing activity recorded in Germantown during the quarter, new leasing activity year-to-date was unchanged from that in the third quarter of the year at 18,924 sf. Indeed, the majority of new leasing activity for Germantown during 2017 occurred in the third quarter. The most notable lease of the quarter was signed by Deleon Stang for 9,000 sf at 100 Lakeforest Boulevard in Gaithersburg.

Despite Gaithersburg’s quiet leasing activity in the fourth quarter of 2017, overall net absorption remained stable, closing the quarter with positive 15,504 sf and accounting for 20.3% of Montgomery County’s total absorption in 2017. Vacancy rates continued to hold, closing the fourth quarter of 2017 at 21.6%, 220 basis points (bps) above Suburban Maryland’s overall average vacancy rate of 19.4%. As office parks continue to struggle with the increasing demand for Metro-proximate locations, vacancy rates could continue to rise. Rental rates remained in check, with overall asking rents for all classes closing the fourth quarter of 2017 at $24.37 per square foot (psf).

Germantown closed the fourth quarter of 2017 with 5,084 sf of positive absorption, resulting in 51,545 sf of positive absorption year-to-date, most of which was registered in the third quarter. Given positive absorption, overall vacancy declined 370 bps year-over-year, locking in the fourth quarter of 2017 at 18.7%. Germantown vacancy remains 70 bps lower than Suburban Maryland’s overall average vacancy of 19.4%. With vacancy rates declining, rental rates increased, closing the fourth quarter of 2017 at $24.66 psf—a 1.0% uptick from the fourth quarter of 2016. In comparison to Montgomery County’s overall average asking rent of $29.20, average rents in Germantown remain among the lowest in the County.

Outlook

Leasing activity remained slow in both submarkets throughout 2017. Vacancy rates in Germantown declined and remained flat in Gaithersburg; however, with new leasing activity remaining stagnant and no new construction in the pipeline, vacancy rates should remain in check for both submarkets. As the demand continues to shift towards more amenitized, Metro-proximate locations, market fundamentals in the Gaithersburg and Germantown submarkets could struggle. But for those tenants that are looking for space at a lower price point in Montgomery County, Germantown and Gaithersburg are competitive options.

Market Indicators*Arrows = Current Qtr Trend

Asking Rent$24.02

Net Absorption20,588 SF

Vacancy20.2%

Deliveries0 SF

Under Construction0 SF

17

Gaithersburg/GermantownNet Absorption – Deliveries - Vacancy

0%

5%

10%

15%

20%

25%

-0.2

-0.1

-0.1

0.0

0.1

0.1

0.2

0.2

0.3

09 10 11 12 13 14 15 16 17

Vaca

ncy

Rat

e

MSF

Net Absorption Deliveries Vacancy Rate

Net Absorption – Deliveries – Vacancy

18

Gaithersburg/GermantownNew Leasing Activity

0.00

0.05

0.10

0.15

0.20

0.25

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

MSF

Q1 Q2 Q3 Q4

19

Gaithersburg/Germantown

$15

$17

$19

$21

$23

$25

$27

$29

2011 2012 2013 2014 2015 2016 Q42017

Full

Serv

ice

PSF

Class A Class B, $ PSF

Asking Rent

Asking Rent

New Leasing Activity

Cushman & Wakefield | 12

Silver Spring

Silver Spring experienced mixed market fundamentals throughout the fourth quarter of 2017. Year-to-date new leasing activity registered 173,727 square feet (sf), an uptick of 11.5% year-over-year, although the majority of new leasing was recorded in the first half of the year. Small and mid-sized tenants accounted for all the leasing activity during the fourth quarter, as there were no leases executed for more than 10,000 sf. There were, however, a couple of small and mid-sized tenants that relocated from the submarket, resulting in negative year-to-date absorption which closed the fourth quarter of 2017 at a barely audible negative 512 sf.

Overall vacancy rates closed the fourth quarter of 2017 at 12.6%—a 110-basis-point (bps) increase year-over-year. Despite the increase, Silver Spring still registered the second-lowest vacancy rate among all Suburban Maryland submarkets: 530 bps lower than Montgomery County’s overall vacancy of 17.9% and 680 bps lower than Suburban Maryland’s vacancy of 19.4%. Overall asking rents, which continued to hold near the $29.00 per square foot (psf) mark, closed the fourth quarter of 2017 at $29.35 psf.

Outlook

With the noteworthy announcement of Discovery Communications relocating its headquarters to New York City in 2019, the Silver Spring submarket could see a significant increase in vacancy and a decline in absorption with the 545,000 sf of vacant space coming online. But with Silver Spring’s strong amenity base and Metro-accessibility, as well as proximity to the District of Columbia, it will remain an attractive option for tenants that begin to be pushed out of the more landlord-favorable Bethesda/Chevy Chase submarket. With the addition of Metro’s now-underway Purple Line, Silver Spring will be further connected to the western Suburban Maryland submarket, continuing to provide tenants the accessibility that they currently demand. This, combined with a rare very large block of existing quality space, will add the Discovery headquarters space to the short list of any large tenant requirements looking for space regionally.

Market Indicators*Arrows = Current Qtr Trend

Asking Rent$29.35

Net Absorption(-512 SF)

Vacancy12.6%

Deliveries0 SF

Under Construction0 SF

20

Silver SpringNet Absorption – Deliveries - Vacancy

8%

9%

10%

11%

12%

13%

-0.50

0.00

0.50

1.00

1.50

2.00

10 11 12 13 14 15 16 17

Vaca

ncy

Rat

e

MSF

Net Absorption Deliveries Vacancy Rate

Net Absorption – Deliveries – Vacancy

21

Silver SpringNew Leasing Activity

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

MSF

Q1 Q2 Q3 Q4

22

Silver SpringAsking Rent

$20$22$24$26$28$30$32$34$36$38

2009 2010 2011 2012 2013 2014 2015 2016 Q4 2017

Full

Serv

ice

PSF

Class A Class B, $ PSF

Asking Rent

New Leasing Activity

cushmanwakefield.com | 13

Prince George’s County

The Prince George’s County submarket experienced healthy market fundamentals throughout the fourth quarter of 2017. Year-to-date new leasing activity closed the quarter at just over 1.7 million square feet (msf) —a 47.1% increase from the fourth quarter of 2016, although the majority of new leasing activity occurred in the first three quarters of the year. Throughout the fourth quarter, there were a handful of renewals and mid-sized leases. The largest new lease of the quarter was that of the National Center for Children and Families (NCCF) which signed for 12,616 square feet (sf) at 6404 Ivy Lane. The United States Federal Emergency Management Agency (FEMA) captured the largest renewal of the quarter for 54,000 sf at 6511 American Boulevard. Such healthy leasing activity resulted in positive overall year-to-date- net absorption of 205,054 sf—a year-over-year increase of 31.6%—75,165 sf of which occurred in the fourth quarter.

Given such positive absorption, overall vacancy closed the fourth quarter of 2017 at 24.5%—a 380-basis-point (bps) decrease year-over-year. Overall vacancy in Prince George’s County was 510 bps higher than Suburban Maryland’s overall vacancy rate of 19.4%. The two tightest submarkets in Prince George’s County were Landover/Landham and Bowie which had vacancy rates of 19.6% and 18.4%, respectively, in the fourth quarter. At the close of the quarter the highest vacancy rates were in Beltsville/College Park (27.5%) and Greenbelt (30.7%), 300 bps and 620 bps higher, respectively, than the County’s overall average.

Overall asking rents in Prince George’s County, which continued to hold near the $21.00 per square foot (psf) mark, closed the fourth quarter of 2017 at $21.40 psf. The County’s overall average asking rate fell $5.45 below Suburban Maryland’s overall average asking rent of $26.85 psf for the quarter. The overall average asking rent for Class A buildings closed the quarter at $23.57 psf, a 4.9% increase year-over-year. Beltsville/College Park boasts the highest rental rate in the County, closing the fourth quarter at $22.26 psf, but rents could continue to rise since construction on Metro’s Purple Line has begun.

There were no new deliveries in the fourth quarter of the year; however, there are a couple buildings in the pipeline. Construction continues at 5801 Research Court in College Park: a 75,000-sf, Class A speculative project slated to deliver in the fourth quarter of 2018. Built-to-suit opportunities have continued to attract tenants, as is evident with Kaiser Permanente’s 176,000 sf building at 4000 Garden City drive and the DHS/CIS headquarters at One Town Center, both currently underway.

OutlookWith the pipeline of new construction and the Metro Purple Line underway, Prince George’s County is well-positioned to attract tenants. When the Purple Line delivers in 2020 it will connect College Park to the western Suburban Maryland submarket. As tenants seek out Metro-proximate locations, College Park becomes a new viable option for tenants that are looking to leave the more landlord-favorable Bethesda/ Chevy Chase submarket. As 5801 University Research Court gets closer to delivering and no preleasing occurs, the market can expect to see a rise in vacancy with 75,000 sf of inventory coming online. In addition, it is clear that as the federal government continues to seek locations that offer a value compared to traditional enclaves, Prince George’s County should continue to be a net beneficiary of GSA consolidations.

Market Indicators*Arrows = Current Qtr Trend

Asking Rent$21.40

Net Absorption205,054 SF

Deliveries251,000 SF

Under Construction825,464 SF

23

Prince George's CountyNet Absorption – Deliveries - Vacancy

0%

4%

8%

12%

16%

20%

24%

28%

32%

-0.6-0.5-0.4-0.3-0.2-0.10.00.10.20.30.4

07 08 09 10 11 12 13 14 15 16 17

Vaca

ncy

Rat

e

MSF

Net Absorption Deliveries Vacancy Rate

Net Absorption – Deliveries – Vacancy

24

Prince George's CountyNew Leasing Activity

0.00

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

THSF

Q1 Q2 Q3 Q4

25

Prince George's County

$18

$19

$20

$21

$22

$23

$24

$25

2011 2012 2013 2014 2015 2016 Q4 2017

Full

Serv

ice

PSF

Class A Class B, $ PSF

Asking RentAsking Rent

New Leasing Activity

Vacancy24.5%

Cushman & Wakefield | 14

Frederick County

Frederick County continued to experience diverse market fundamentals through the fourth quarter of 2017. Year-to-date new leasing activity closed the quarter at 128,016 square feet (sf). Most new leasing activity was recorded in the first two quarters of 2017—thanks in large part to CSRA leasing 33,360 sf at 110 Thomas Johnson Drive and Asbury Communities taking 26,380 sf at 5285 Westview Drive. The largest lease of the fourth quarter was signed by an undisclosed tenant for 2,020 sf at 5301 Buckeystown Pike.

Given sluggish leasing activity, quarter-to-date absorption closed the fourth quarter of 2017 at a slightly negative 3,430 sf. There were a handful of small move-outs that contributed, and with limited, large new-to-market tenant’s future absorption activity is expected to remain relatively flat.

Overall vacancy closed the fourth quarter of 2017 at 17.3%—a 10-basis-point (bps) increase quarter-over-quarter. Class A vacancy remained significantly tighter, closing the fourth quarter at 13.0%—500 bps lower than Class A vacancy in Montgomery County and 720 bps lower than Class A vacancy in Prince George’s County. Average rents for all classes in Frederick County closed the fourth quarter of 2017 at $15.21 per square foot (psf) —a 1.4% increase quarter-over-quarter. Class A overall average asking rent was $22.00 psf at the close of the quarter, $8.16 lower than Suburban Maryland’s overall Class A average of $30.16 psf.

Outlook

With the growing trend toward live-work-play environments, and considering Frederick County’s lack of accessibility to Metro as well as its distance from Washington, DC, the market could see vacancy rates increase as tenants look to seek out more amenity rich submarkets. However, Frederick County’s affordable rental rates make the submarket a viable option for tenants looking to lease a large amount of space at low rental rates.

Market Indicators*Arrows = Current Qtr Trend

Asking Rent$15.21

Net Absorption(420,919 SF)

Vacancy17.3%

Deliveries0 SF

Under Construction0 SF

26

Frederick CountyNet Absorption – Deliveries - Vacancy

0%

4%

8%

12%

16%

20%

24%

28%

-0.5

-0.4

-0.3

-0.2

-0.1

0.0

0.1

11 12 13 14 15 16 17

Vaca

ncy

Rat

e

MSF

Net Absorption Deliveries Vacancy Rate

Net Absorption – Deliveries – Vacancy

27

Frederick CountyNew Leasing Activity

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

400.00

450.00

500.00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

THSF

Q1 Q2 Q3 Q4

28

Frederick County

$0

$5

$10

$15

$20

$25

$30

2011 2012 2013 2014 2015 2016 Q4 2017

Full

Serv

ice

PSF

Class A Class B, $ PSF

Asking Rent

Asking Rent

New Leasing Activity

cushmanwakefield.com | 15

Appendix

Table Summaries

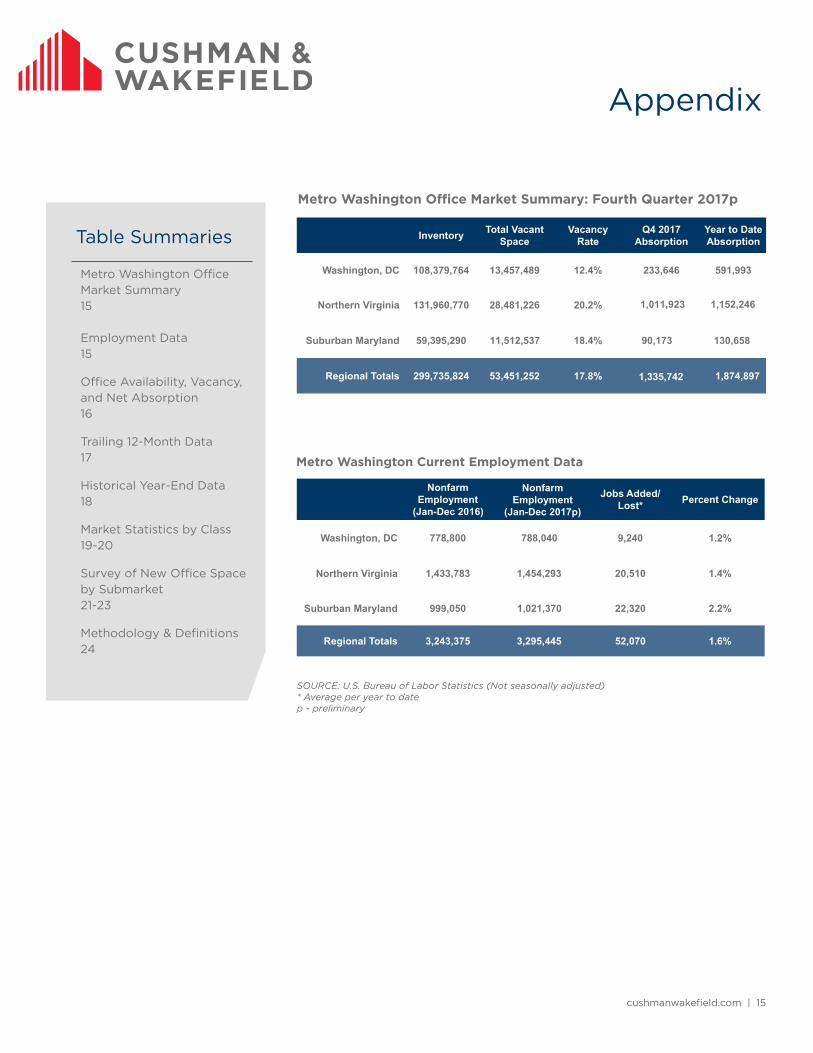

Metro Washington Office Market Summary: Fourth Quarter 2017p

cushmanwakefield.com | 13

Appendix

Table Summaries

Metro Washington Office Market Summary13

Employment Data13

Office Availability, Vacancy, and Net Absorption14

Trailing 12-Month Data15

Historical Year-End Data16

Market Statistics by Class17-18

Survey of New Office Space by Submarket19-22

Methodology & Definitions23

Metro Washington Current Employment Data

Metro Washington Office Market Summary: Second Quarter 2017p

SOURCE: U.S. Bureau of Labor Statistics (Not seasonally adjusted)* Average per year to datep - preliminary

Inventory Total Vacant Space

Vacancy Rate

Q 2017Absorption

Year to Date Absorption

Washington, DC 13, 12. %

Northern Virginia 2 20. %

Suburban Maryland 59, 1 %

Regional Totals 5 17. %

NonfarmEmployment

(Jan- 2016)

NonfarmEmployment

(Jan- 2017p)

Jobs Added/ Lost* Percent Change

Washington, DC 78 1. %

Northern Virginia 1,433,7 1. %

Suburban Maryland 9 1,0 2. %

Regional Totals 3 3,2 1.6%

Metro Washington Office Market Summary15

Employment Data15

Office Availability, Vacancy, and Net Absorption16

Trailing 12-Month Data17

Historical Year-End Data18

Market Statistics by Class19-20

Survey of New Office Space by Submarket21-23

Methodology & Definitions24

Cushman & Wakefield | 16

AppendixO

ffice

Ava

ilab

ility

, Vac

ancy

, and

Net

Ab

sorp

tio

n, F

our

th Q

uart

er 2

017

p

Tota

l Inv

ento

ryN

ew/R

elet

Sp

ace

Vaca

ntSu

blet

Spa

ce

Vaca

ntTo

tal S

pace

Va

cant

Vaca

ncy

Rat

e (%

)N

ew/R

elet

Spa

ce

Abs

orpt

ion

Subl

et S

pace

A

bsor

ptio

nTo

tal N

et A

b-so

rptio

n

Beth

esda

/Che

vy C

hase

(2

2)8,

523,

023

709,

536

211,

072

920,

608

10.8

%24

,240

(1

15,6

94)

(91,

454)

Roc

k Sp

ring

Park

(23

)4,

165,

404

1,01

8,67

113

,809

1,03

2,48

024

.8%

181,

591

6,92

4 18

8,51

5

Pike

Cor

ridor

(1)

11,1

03,0

611,

875,

697

112,

562

1,98

8,25

917

.9%

(90,

447)

(6,2

78)

(96,

725)

I-270

Roc

kville

(20

)9,

345,

162

2,03

0,88

112

1,42

72,

152,

308

23.0

%28

4,89

6 (3

4,40

2)25

0,49

4

Gai

ther

sbur

g (2

4)2,

187,

015

470,

072

1,28

247

1,35

421

.6%

36,2

29

34,1

31

70,3

60

Ger

man

tow

n (2

1)1,

852,

930

342,

662

3,00

034

5,66

218

.7%

49,9

29

1,61

6 51

,545

Silv

er S

prin

g (2

)4,

877,

684

565,

815

47,0

0461

2,81

912

.6%

12,6

88

(13,

200)

(512

)

Nor

th S

ilver

Spr

ing

(25)

1,05

5,12

720

0,11

60

200,

116

19.0

%(2

5,70

0)0

(25,

700)

Mon

tgom

ery

Cou

nty

43,1

09,4

067,

213,

450

510,

156

7,72

3,60

617

.9%

473,

426

(126

,903

)34

6,52

3

Prin

ce G

eorg

e's

Cou

nty

13,4

24,1

603,

256,

351

33,5

083,

289,

859

24.5

%16

5,65

6 39

,398

20

5,05

4

Fred

eric

k C

ount

y2,

861,

724

462,

341

33,5

0849

5,84

917

.3%

(387

,411

)(3

3,50

8)(4

20,9

19)

Tota

l59

,395

,290

10,9

32,1

4258

0,39

511

,512

,537

19.4

%25

1,67

1(1

21,0

13)

130,

658

p -

pre

limin

ary

cushmanwakefield.com | 17

AppendixTr

ailin

g 1

2-M

ont

h D

ata

Tota

l Inv

ento

ryVa

canc

y R

ate

(%)

Tota

l Abs

orpt

ion

1st Q

tr

2017

2nd

Qtr

20

173r

d Q

tr

2017

4th

Qtr

20

171s

t Qtr

20

172n

d Q

tr

2017

3rd

Qtr

20

174t

h Q

tr

2017

1st Q

tr

2017

2nd

Qtr

20

173r

d Q

tr

2017

4th

Qtr

20

17

Beth

esda

/Che

vy

Cha

se8,

641,

418

8,64

1,41

88,

523,

023

8,52

3,02

39.

5%10

.4%

9.8%

10.8

%8,

246

(125

,061

)55

,407

(3

0,04

6)

Roc

k Sp

ring

Park

4,18

9,00

14,

189,

001

4,16

5,40

44,

165,

404

25.8

%25

.1%

25.0

%24

.8%

151,

052

28,4

16

(50)

9,09

7

Pike

Cor

ridor

11,0

79,4

6411

,079

,464

11,1

03,0

6111

,103

,061

17.0

%18

.5%

18.4

%17

.9%

(64,

902)

(65,

525)

14,5

30

19,1

72

I-270

/Roc

kville

9,38

8,90

09,

340,

900

9,34

5,16

29,

345,

162

23.3

%23

.3%

23.2

%23

.0%

294,

020

(58,

368)

(1,0

20)

15,8

62

Gai

ther

sbur

g2,

022,

113

2,18

7,01

52,

187,

015

2,18

7,01

515

.2%

21.7

%22

.3%

21.6

%69

,921

(3

,808

)(1

1,25

7)15

,504

Ger

man

tow

n1,

908,

759

1,85

2,93

01,

852,

930

1,85

2,93

021

.1%

20.9

%18

.9%

18.7

%6,

952

3,13

5 36

,374

5,

084

Silv

er S

prin

g4,

877,

684

4,87

7,68

44,

877,

684

4,87

7,68

411

.0%

12.1

%12

.1%

12.6

%14

,648

(1

3,57

2)22

,252

(2

3,84

0)

Nor

th S

ilver

Spr

ing

1,05

5,12

71,

055,

127

1,05

5,12

71,

055,

127

21.2

%18

.4%

19.7

%19

.0%

(48,

993)

29,1

69

(13,

481)

7,60

5

Mon

tgom

ery

Cou

nty

43,1

62,4

6643

,223

,539

43,1

09,4

0643

,109

,406

17.2

%18

.1%

17.9

%17

.9%

430,

944

(205

,614

)10

2,75

5 18

,438

Prin

ce G

eorg

e's

Cou

nty

13,4

23,6

4513

,423

,745

13,4

23,6

4513

,424

,160

27.2

%25

.4%

25.1

%24

.5%

102,

993

(3,6

93)

30,5

89

75,1

65

Fred

eric

k C

ount

y2,

745,

520

2,79

6,42

02,

861,

724

2,86

1,72

419

.3%

19.0

%17

.2%

17.3

%(4

56,6

91)

351

38,8

51

(3,4

30)

Subu

rban

Mar

ylan

d59

,331

,631

59

,443

,704

59

,394

,775

59

,395

,290

19

.6%

19.8

%19

.5%

19.4

%77

,246

(2

08,9

56)

172,

195

90,1

73

p -

pre

limin

ary

Cushman & Wakefield | 18

AppendixH

isto

rica

l Yea

r-E

nd D

ata

Tota

l Inv

ento

ryVa

canc

y R

ate

(%)

Tota

l Abs

orpt

ion

2014

20

15

2016

20

17

2014

20

15

2016

20

17

2014

20

15

2016

20

17

Beth

esda

/Che

vy

Cha

se8,

612,

795

8,61

2,79

58,

612,

795

8,52

3,02

312

.9%

13.1

%9.

7%10

.8%

(44,

478)

(26,

319)

128,

324

(91,

454)

Roc

k Sp

ring

Park

4,05

5,40

44,

079,

001

4,24

0,00

14,

165,

404

25.0

%28

.2%

29.1

%24

.8%

(58,

558)

(4,6

08)

19,7

22

188,

515

Pike

Cor

ridor

10,6

93,2

7010

,772

,914

10,8

76,4

6411

,103

,061

21.8

%16

.9%

16.8

%17

.9%

(30,

994)

93,9

69

(137

,641

)(9

6,72

5)

I-270

/Roc

kville

9,48

8,71

09,

536,

528

9,62

0,13

99,

345,

162

24.5

%24

.2%

24.5

%23

.0%

29,0

88

134,

427

282,

841

250,

494

Gai

ther

sbur

g2,

122,

113

2,15

7,11

32,

157,

113

2,18

7,01

521

.9%

21.0

%21

.3%

21.6

%30

,895

16

,517

(3

1,55

0)70

,360

Ger

man

tow

n1,

908,

759

1,90

8,75

91,

908,

759

1,85

2,93

023

.6%

24.2

%21

.4%

18.7

%24

,654

13

,268

8,

920

51,5

45

Silv

er S

prin

g4,

806,

040

4,80

6,04

04,

877,

684

4,87

7,68

410

.5%

12.2

%11

.5%

12.6

%3,

421

(3,3

32)

21,6

57

(512

)

Nor

th S

ilver

Spr

ing

1,05

5,12

71,

055,

127

1,05

5,12

71,

055,

127

23.2

%24

.9%

19.6

%19

.0%

(7,5

18)

1,25

9 20

,653

(2

5,70

0)

Mon

tgom

ery

Cou

nty

42,7

42,2

1842

,928

,277

43,3

48,0

8243

,109

,406

19.8

%19

.0%

18.2

%17

.9%

(53,

490)

225,

181

312,

926

346,

523

Prin

ce G

eorg

e's

Cou

nty

13,4

17,8

9013

,515

,386

13,4

23,6

4513

,424

,160

24.7

%28

.2%

28.3

%24

.5%

(57,

646)

(6,1

24)

145,

440

205,

054

Fred

eric

k C

ount

yN

/AN

/AN

/A2,

861,

724

N/A

N/A

N/A

17.3

%N

/AN

/AN

/A(4

20,9

19)

Subu

rban

M

aryl

and

56,1

60,1

0856

,443

,663

56,7

71,7

2759

,395

,290

21.0

%21

.2%

20.6

%19

.4%

(111

,136

)21

9,05

7 45

8,36

6 13

0,65

8

p -

pre

limin

ary

cushmanwakefield.com | 19

Suburban Maryland – 4th Quarter 2017 Market Statistics

Market Statistics

Cushman & Wakefield | 18

Suburban Maryland – 2nd Quarter 2017 Market Statistics

BuildingsTotal

Inventory(SF)

New/ReletVacancy (%)

SubletVacancy (%)

Total Vacancy* (%)

Net Absorption Current QTR

(SF)

UnderConstruction

(SF)

Average Asking Rent

(FS)

Bethesda/Chevy Chase

Class

A 22 5,177,706 24.5% 2.6% 9.4% 35,416( ) 626,020 $41.08

B 26 2,640,140 11.7% 2.6% 13.1% 3,518 0 $33.97

C 15 705,177 10.7% 0.4% 12.1% 1,852 0 $30.20

TOTAL 64 8,523,023 8.3% 2.5% 10.8% (30,046) 626,020 $41.08

Rock Spring Park

Class

A 13 3,050,815 24.5% 0.5% 25.0% (4,230) 0 $30.58

B 8 953,589 26.4% 0.0% 26.4% 13,327 0 $27.56

C 1 161,000 11.0% 0.0% 11.0% 0 0 $20.00

TOTAL 22 4,165,404 24.5% 0.3% 24.8% 9,097 0 $28.34

Pike Corridor

Class

A 33 5,294,799 19.0% 0.1% 19.1% (3,492) 0 $31.05

B 46 4,947,208 15.8% 2.1% 17.9% 349 0 $26.66

C 16 861,054 10.5% 0.0% 10.5% 22,315 0 $18.41

TOTAL 95 11,103,061 16.9% 1.0% 17.9% 19,172 0 $28.30

I-270/Rockville

Class

A 46 6,608,313 20.6% 1.6% 22.2% 15.982( ) 0 $30.73

B 31 2,567,028 24.2% 0.7% 24.9% 29,190 0 $22.59

C 3 169,821 27.2% 0.0% 27.2% 2,654 0 $24.66

TOTAL 80 9,345,162 21.7% 1.3% 23.0% 15,862 0 $28.34

Gaithersburg

Class

A 6 605,663 17.8% 0.1% 18.0% (129) $24.37

B 16 1,021,105 16.0% 0.0% 16.1% 15,304 0 $23.62

C 11 560,247 35.4% 0.0% 35.4% 329 0 $15.94

TOTAL 34 2,187,015 21.5% 0.1% 21.6% 15,504 0 $23.47Germantown

ClassA 5 662,740 17.9% 0.5% 18.4% 0 0 $27.86

B 17 1,190,190 18.8% 0.0% 18.8% 5,084 0 $22.32

C 0 0 0.0% 0.0% 0.0% 0 0 N/A

TOTAL 22 1,852,930 18.5% 0.2% 18.7% 5,084 0 $24.66

* Total Vacancy - the vacancy rate is calculated using the combined total of relet, sublet and new vacant space.

Market Statistics

0

Cushman & Wakefield | 20

Suburban Maryland – 4th Quarter 2017 Market Statistics

Market Statistics

cushmanwakefield.com | 19

Suburban Maryland – 2nd Quarter 2017 Market Statistics

Market Statistics

BuildingsTotal

Inventory(SF)

New/ReletVacancy (%)

SubletVacancy (%)

Total Vacancy* (%)

Net Absorption Current QTR

(SF)

UnderConstruction

(SF)

Average Asking Rent

(FS)

Silver Spring

Class

A 14 2,901,148 13.6% 1.5% 15.1% 18,109( ) 0 $30.52

B 7 973,764 7.7% 0.0% 7.7% 6,994 0 $26.96

C 16 1,002,772 9.6% 0.5% 10.0% (12,725) 0 $23.89

TOTAL 37 4,877,684 11.6% 1.0% 12.6% (23,840) 0 $29.35

North Silver Spring

Class

A 4 222,322 2.3% 0.0% 2.3% 0 0 N/A

B 16 832,805 23.4% 0.0% 23.4% 7,605 0 $24.21

C 0 0 0.0% 0.0% 0.0% 0 0 N/A

TOTAL 20 1,055,127 19.0% 0.0% 19.0% 7,605 0 $24.21

Prince George’s County

Class

A 39 4,592,560 20.2% 0.0% 20.2% 47,964 825,767 $23.57

B 135 7,200,545 27.7% 0.5% 27.7% 12,832 0 $20.53

C 54 1,631,055 22.5% 0.0% 22.5% 14,369 0 $19.82

TOTAL 228 13,424,160 24.3% 0.2% 24.5% 75,165 825,767 $21.40

Frederick County

Class

A 14 1,737,465 13.0% 0.0% 13.0% (1,520) $22.00

B 20 1,124,259 21.0% 3.0% 24.0% (1,910) $12.81

C 0 0 0.0% 0.0% 0.0% 0 N/A

TOTAL 34 2,861,724 16.2% 1.1% 17.3% (3,430) $15.21

Suburban Maryland

ClassA 196 30,853,531 17.0% 1.0% 18.0% 30,914( ) 1,451,787 $30.16

B 322 23,450,633 20.4% 1.1% 21.5% 92,293 0 $23.66

C 122 5,091,126 17.7% 0.1% 17.8% 28,794 0 $22.02

TOTAL 640 59,395,290 18.4% 1.0% 19.4% 90,173 1,451,787 $26.85

* Total Vacancy - the vacancy rate is calculated using the combined total of relet, sublet and new vacant space.

0

0

0

0

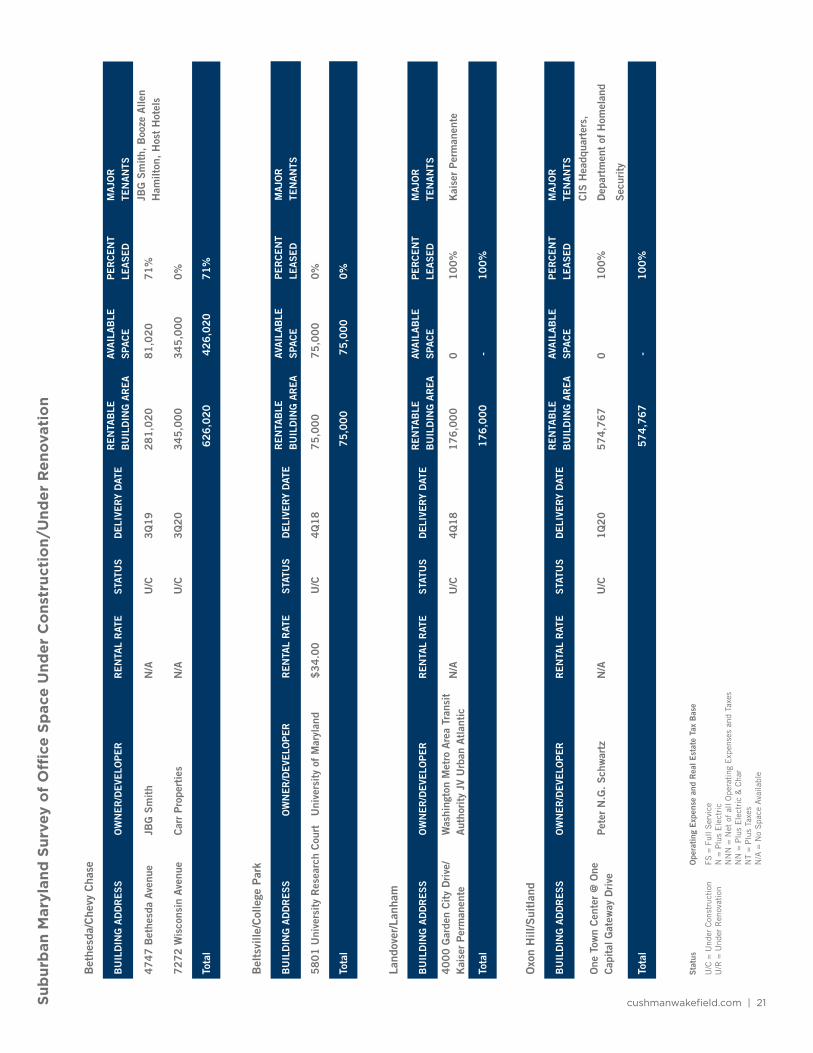

cushmanwakefield.com | 21Sub

urb

an M

aryl

and

Sur

vey

of

Offi

ce S

pac

e U

nder

Co

nstr

ucti

on/

Und

er R

enov

atio

n

Bet

hesd

a/C

hevy

Cha

se

BU

ILD

ING

AD

DR

ES

SO

WN

ER

/DE

VELO

PE

RR

EN

TAL

RAT

ES

TATU

SD

ELI

VER

Y D

ATE

RE

NTA

BLE

B

UIL

DIN

G A

RE

AAV

AIL

AB

LE

SPA

CE

PE

RC

EN

T

LEA

SE

DM

AJO

R

TEN

AN

TS

47

47

Bet

hesd

a Av

enue

JB

G S

mit

hN

/AU

/C3

Q1

92

81

,02

08

1,0

20

71

%JB

G S

mit

h, B

ooze

Alle

n H

amilt

on,

Hos

t H

otel

s

72

72

Wis

cons

in A

venu

eC

arr

Pro

pert

ies

N/A

U/C

3Q

20

34

5,0

00

34

5,0

00

0%

Tota

l 6

26

,02

0

42

6,0

20

7

1%

Bel

tsvi

lle/C

olle

ge P

ark

BU

ILD

ING

AD

DR

ES

SO

WN

ER

/DE

VELO

PE

RR

EN

TAL

RAT

ES

TATU

SD

ELI

VER

Y D

ATE

RE

NTA

BLE

B

UIL

DIN

G A

RE

AAV

AIL

AB

LE

SPA

CE

PE

RC

EN

T

LEA

SE

DM

AJO

R

TEN

AN

TS

58

01

Uni

vers

ity

Res

earc

h C

ourt

Uni

vers

ity

of M

aryl

and

$3

4.0

0U

/C4

Q1

87

5,0

00

75

,00

00

%

Tota

l 7

5,0

00

7

5,0

00

0

%

Land

over

/Lan

ham

BU

ILD

ING

AD

DR

ES

SO

WN

ER

/DE

VELO

PE

RR

EN

TAL

RAT

ES

TATU

SD

ELI

VER

Y D

ATE

RE

NTA

BLE

B

UIL

DIN

G A

RE

AAV

AIL

AB

LE

SPA

CE

PE

RC

EN

T

LEA

SE

DM

AJO

R

TEN

AN

TS

40

00

Gar

den

Cit

y D

rive

/ K

aise

r P

erm

anen

te

Was

hing

ton

Met

ro A

rea

Tran

sit

Aut

hori

ty J

V U

rban

Atl

anti

cN

/AU

/C4

Q1

81

76

,00

00

10

0%

Kai

ser

Per

man

ente

Tota

l 1

76

,00

0

-

1

00

%

Oxo

n H

ill/S

uitl

and

BU

ILD

ING

AD

DR

ES

SO

WN

ER

/DE

VELO

PE

RR

EN

TAL

RAT

ES

TATU

SD

ELI

VER

Y D

ATE

RE

NTA

BLE

B

UIL

DIN

G A

RE

AAV

AIL

AB

LE

SPA

CE

PE

RC

EN

T

LEA

SE

DM

AJO

R

TEN

AN

TS

One

Tow

n C

ente

r @

One

C

apit

al G

atew

ay D

rive

Pet

er N

.G.

Sch

war

tzN

/AU

/C1

Q2

05

74

,76

70

10

0%

CIS

Hea

dqua

rter

s,

Dep

artm

ent

of H

omel

and

Sec

urit

y

Tota

l 5

74

,76

7

-

1

00

%

Sta

tus

Ope

rati

ng E

xpen

se a

nd R

eal E

stat

e Ta

x B

ase

U/C

= U

nder

Con

stru

ctio

nU

/R =

Und

er R

enov

atio

nFS

= F

ull S

ervi

ceN

= P

lus

Ele

ctri

cN

NN

= N

et o

f al

l Ope

rati

ng E

xpen

ses

and

Taxe

sN

N =

Plu

s E

lect

ric

& C

har

NT

= P

lus

Taxe

sN

/A =

No

Spa

ce A

vaila

ble

Cushman & Wakefield | 22

SU

MM

AR

YR

EN

TAB

LE

BU

ILD

ING

AR

EA

AVA

ILA

BLE

S

PAC

EP

ER

CE

NT

LE

AS

ED

20

17

Del

iver

ies

00

0%

20

18

Del

iver

ies

25

1,0

00

75

,00

03

0%

20

19

Del

iver

ies

28

1,0

20

81

,02

07

1%

20

20

Del

iver

ies

91

9,7

67

34

5,0

00

60

%

TOTA

L 1

,45

1,7

87

5

01

,02

0

35

%

Sta

tus

Ope

rati

ng E

xpen

se a

nd R

eal E

stat

e Ta

x B

ase

U/C

= U

nder

Con

stru

ctio

nU

/R =

Und

er R

enov

atio

nFS

= F

ull S

ervi

ceN

= P

lus

Ele

ctri

cN

NN

= N

et o

f al

l Ope

rati

ng E

xpen

ses

and

Taxe

sN

N =

Plu

s E

lect

ric

& C

har

NT

= P

lus

Taxe

sN

/A =

No

Spa

ce A

vaila

ble

Surb

urb

an M

aryl

and

Sum

mar

y o

f O

ffice

Sp

ace

Und

er C

ons

truc

tio

n/U

nder

Ren

ovat

ion

cushmanwakefield.com | 23

Sta

tus

Ope

rati

ng E

xpen

se a

nd R

eal E

stat

e Ta

x B

ase

U/C

= U

nder

Con

stru

ctio

nU

/R =

Und

er R

enov

atio

nFS

= F

ull S

ervi

ceN

= P

lus

Ele

ctri

cN

NN

= N

et o

f al

l Ope

rati

ng E

xpen

ses

and

Taxe

sN

N =

Plu

s E

lect

ric

& C

har

NT

= P

lus

Taxe

sN

/A =

No

Spa

ce A

vaila

ble

Surb

urb

an M

aryl

and

Sur

vey

of

New

Offi

ce S

pac

e

20

17

Del

iver

ies

BU

ILD

ING

AD

DR

ES

SO

WN

ER

/DE

VELO

PE

RS

TATU

SR

EN

TAL

RAT

ES

UB

MA

RK

ET

RE

NTA

BLE

B

UIL

DIN

G A

RE

AN

EW

AVA

ILA

BLE

S

PAC

E

VAC

AN

CY

RAT

E

(AS

OF

CU

RR

EN

T Q

UA

RTE

R)

PE

RC

EN

T LE

AS

ED

UP

ON

D

ELI

VER

Y

20

16

Del

iver

ies

BU

ILD

ING

AD

DR

ES

SO

WN

ER

/DE

VELO

PE

RS

TATU

SR

EN

TAL

RAT

ES

UB

MA

RK

ET

RE

NTA

BLE

B

UIL

DIN

G A

RE

AN

EW

AVA

ILA

BLE

S

PAC

E

VAC

AN

CY

RAT

E

(AS

OF

CU

RR

EN

T Q

UA

RTE

R)

PE

RC

EN

T LE

AS

ED

UP

ON

D

ELI

VER

Y

12

35

8 P

arkl

awn

Dri

veG

reen

cour

t P

orpe

rty

Gro

upD

eliv

ered

4Q

16

N/A

Pik

e C

orri

dor

10

3,5

50

10

3,5

02

87

%0

%

12

43

5 P

ark

Pot

omac

Ave

Foul

ger

Pra

tt/F

oulg

er P

ratt

C

ompa

nies

Del

iver

ed 1

Q1

6N

/AI-

27

0/R

ockv

ille

15

6,0

00

84

,10

75

0%

13

%

Tota

l2

59

,55

01

87

,60

97

2%

63

%

20

15

Del

iver

ies

BU

ILD

ING

AD

DR

ES

SO

WN

ER

/DE

VELO

PE

RS

TATU

SR

EN

TAL

RAT

ES

UB

MA

RK

ET

RE

NTA

BLE

B

UIL

DIN

G A

RE

AN

EW

AVA

ILA

BLE

S

PAC

E

VAC

AN

CY

RAT

E

(AS

OF

CU

RR

EN

T Q

UA

RTE

R)

PE