Embed Size (px)

Citation preview

1

07-2014

Rmb – the next chapter

China had large capital inflows last year, with foreign exchange accumulation reaching $98 billion and $131 billion in the third and fourth quarters of 2013, respectively1. Going into 2014, the RMB reversed its upward trend against the USD and effectively depreciated by 2.7% in the first quarter, in contrast with a cumulative gain of about 40% since 2005.

The decline of the RMB over this period was largely due to the intervention of China’s central bank to dampen “hot money” inflows. Market participants with access to both the onshore and offshore markets have profited from arbitraging between the high onshore RMB interest rates and low dollar borrowing rates. Expectations of continued RMB appreciation combined with low volatility incentivized firms that operate in both mainland China and Hong Kong to move funds on- and offshore to borrow dollars at low interest rates and invest the funds in China, which resulted in the large capital inflows.

Since then, the “managed” currency depreciation served its purpose to shake the broadly held view on “main street” of one-way appreciation over the past few years. The People’s Bank of China (PBoC) widened the daily onshore USD/RMB trading band by 1.0% to +/-2.0% on March 17. Furthermore, the government stated in a recent monetary report that in future the RMB exchange rate will increasingly be determined by market forces and the central bank will gradually back off from regular intervention. Recent initiatives by the PBoC are encouraging and have paved the way for two-way fluctuation of the currency as part of the reform required to bring about a more flexible exchange rate regime.

A future global currency

The Chinese government is committed to making capital account liberalization a reform priority in 2014, which will not only further enable Chinese residents and corporates to broaden their investments globally, but also help offshore RMB markets to become more diversified and developed to appeal to a wider range of international investors.

Against that backdrop, trade settlement and cross-border payments denominated in RMB continue to grow as more corporates switch to RMB invoicing. According to SWIFT data, RMB is now the seventh-biggest currency for global payments, accounting for 1.43% of payments in April.

Fundamentals of offshore Rmb bonds remain favourable. Rmb appreciation previously was one of the major incentives for overseas investors to accumulate the currency in key offshore centres such as Hong Kong. While this market perception has changed, resilient risk adjusted returns and sustained demand for Rmb deposits will continue to support this asset class. With increasing globalization of the Rmb, it is arguably the most under allocated currency in the world today.

Market Perspective

At a glance

n Offshore RMB bonds (also known as Dim Sum) is one of the most attractive asset classes today.

n Demand for RMB deposits in offshore centres continues to grow.

n Recent RMB volatility highlights no such thing as one-way appreciation.

n Dim Sum bonds have posted positive returns YTD.

n New Dim Sum bond issuance continues to diversify as the market expands.

n RMB bonds offer relatively low correlation and volatility to other asset classes.

n Investment grade stays in focus.

n RMB is an increasingly important asset class for global investors.

n RMB is arguably the most under allocated currency in the world today.

RMB Bonds: Beyond a Currency Play

In Focus: Fixed Income

1 Report to Congress on International Economic and Exchange Rate Policies, U.S. Department of the Treasury Office of International Affairs, April 15, 2014

2

07-2014

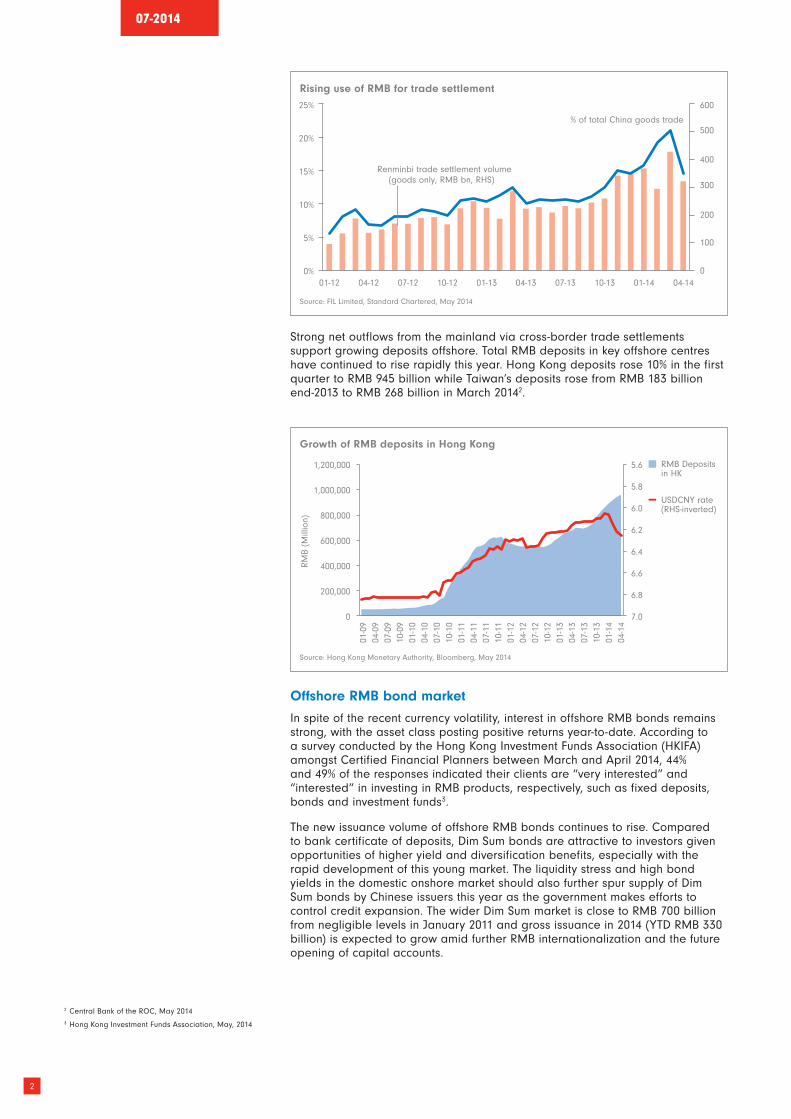

Strong net outflows from the mainland via cross-border trade settlements support growing deposits offshore. Total RMB deposits in key offshore centres have continued to rise rapidly this year. Hong Kong deposits rose 10% in the first quarter to RMB 945 billion while Taiwan’s deposits rose from RMB 183 billion end-2013 to RMB 268 billion in March 20142.

Rising use of Rmb for trade settlement

Source: FIL Limited, Standard Chartered, May 2014

Offshore Rmb bond market

In spite of the recent currency volatility, interest in offshore RMB bonds remains strong, with the asset class posting positive returns year-to-date. According to a survey conducted by the Hong Kong Investment Funds Association (HKIFA) amongst Certified Financial Planners between March and April 2014, 44% and 49% of the responses indicated their clients are “very interested” and “interested” in investing in RMB products, respectively, such as fixed deposits, bonds and investment funds3.

The new issuance volume of offshore RMB bonds continues to rise. Compared to bank certificate of deposits, Dim Sum bonds are attractive to investors given opportunities of higher yield and diversification benefits, especially with the rapid development of this young market. The liquidity stress and high bond yields in the domestic onshore market should also further spur supply of Dim Sum bonds by Chinese issuers this year as the government makes efforts to control credit expansion. The wider Dim Sum market is close to RMB 700 billion from negligible levels in January 2011 and gross issuance in 2014 (YTD RMB 330 billion) is expected to grow amid further RMB internationalization and the future opening of capital accounts.

Growth of Rmb deposits in Hong Kong

Source: Hong Kong Monetary Authority, Bloomberg, May 2014

2 Central Bank of the ROC, May 2014 3 Hong Kong Investment Funds Association, May, 2014

25%

20%

15%

10%

5%

0%

600

500

400

300

200

100

0 01-12 04-12 07-12 10-12 01-13 04-13 07-13 10-13 01-14 04-14

% of total China goods trade

Renminbi trade settlement volume(goods only, RMB bn, RHS)

5.6

5.8

6.0

6.2

6.4

6.6

6.8

7.0

1,200,000

RM

B (M

illio

n)

1,000,000

800,000

600,000

400,000

200,000

0

01-0

904

-09

07-0

910

-09

01-1

004

-10

07-1

010

-10

01-1

104

-11

07-1

110

-11

01-1

204

-12

07-1

210

-12

01-1

304

-13

07-1

310

-13

01-1

404

-14

RMB Deposits in HK

USDCNY rate (RHS-inverted)

#"!

#"!

#"!

#"!

##!

##!

##!

##!

#$!

#$!

#$!

#$!

#%!

#%!

#%!

#%!

#&!

#&!

3

07-2014

The asset class has swiftly diversified since inception - from being dominated by sovereign and Chinese bank issuance to including more Chinese blue chip companies, quasi-sovereigns and foreign multinationals. The market now consists of over 330 different bonds from nearly 200 issuers, with 32% from outside China, including institutions such as McDonald’s, Volvo and KfW.

Dim Sum Issuances (outstanding since market inception)

Source: BofA Merrill Lynch Dim Sum Bond Index, Bloomberg, 2014

The resilience of offshore RMB bonds amid the recent heightened foreign exchange volatility indicates this market can offer attractive opportunities independent of any currency bias. With the PBoC gravitating towards easing monetary policy while the Fed is tightening by unwinding QE, investors are increasingly being drawn to offshore RMB bonds as a safe-haven and alternative investment option, with lower duration at a reasonably attractive effective yield level.

Dim Sum Index Universe – by country Dim Sum Index Universe – by Sector

Source: FIL Limited, Bloomberg, BoA Merrill Lynch Dim Sum Index as at May 2014

Dim Sum bonds – attractive yield, high quality, low duration and less exposed to USD rate risk

Source: FIL Limited, BoA Merrill Lynch Indices, Bloomberg, May 2014

With the low correlation between RMB and other Asian currencies, offshore RMB-denominated investment grade bonds are less closely linked with the broader Asian universe. The Dim Sum market is not heavily influenced by US Treasuries or credit spread volatility, and thus remains relatively insulated from onshore liquidity conditions given restricted onshore access.

“We expect the Chinese government to allow more local entities including SOEs to issue offshore Rmb bonds in 2014, which will boost offshore supply and further improve liquidity. Increasing depth and turnover of the CNH asset market will also encourage faster product innovation.”

bryan Collins portfolio manager of

Fidelity WorldWide Fund - RMB Bond Fund Fidelity Funds - Asian High Yield Fund

“Rmb securities can offer attractive opportunities independent of any currency bias, and in addition, total return is further supported by income and currency components.”

Bryan Collins portfolio manager of

Fidelity WorldWide Fund - RMB Bond Fund Fidelity Funds - Asian High Yield Fund

9

8

7

6

5

4

3

2

1

00 1 2 3 4 5 6 7 8

Yiel

d to

Matu

rity

(%)

Duration (years)

Offshore RMB

Asian HY

Euro HY

US HY

Euro IG

Asian IG US IG

EM Bonds

Size

(RM

B m

m)

600 800

700

600

500

400

300

200

100

0

500

400

300

200

100

0

2009

03-11

07-11

11-11

03-12

07-12

11-12

03-13

07-13

11-13

03-14

IG

HY

No. of issues (RHS)

18.9% Sovereign15.9% Banking12.7% Real Estate8.9% Agency7.2% Services6.4% Financial Services5.3% Basic Industry4.4% Utility4.0% Capital Goods3.4% Automotive2.6% Consumer Non‐Cyclical2.3% Insurance2.0% Technology & Electronics 1.9% Energy1.9% Consumer Cyclical0.9% Supranational0.6% Government Guaranteed0.6% Telecommunications

66.0% China3.0% Germany2.5% France2.2% United Kingdom11.8% Hong Kong0.8% India0.9% Japan2.5% Korea1.7% Russia0.5% Sweden1.6% Singapore0.9% Supernational0.6% Taiwan1.9% United States3.1% Others

4

07-2014

Offshore RMB bonds are now one of the most attractive asset classes in fixed income space globally. Whilst the Dim Sum market has seen impressive growth, prudent investors may want to focus on investment grade issues which provide higher credit quality, enhanced liquidity, better diversity, and higher risk-adjusted returns.

The rising Rmb asset class

The striking growth of the offshore RMB market has incentivised the domestic market to speed up the pace of reform and liberalization as it remains less developed in terms of market visibility, liquidity, transparency and credit rating consistency.

China has made efforts to remove excessive restrictions and improve the infrastructure and efficiency of the onshore bond market. According to the PBoC, the total amount of outstanding bonds in the onshore market in China reached RMB 29.6 trillion by the end of 2013, up by 13% YoY. As of May 21, 152 overseas financial institutions have gained approval to enter China’s interbank bond market, becoming a significant participating force4.

Global institutional investors are increasing their allocation in China’s domestic bond market, with the amount of domestic RMB bonds held by overseas entities up 28% during the first quarter this year, reaching RMB 512.4 billion5. The number of central banks that have swap lines with PBoC continues to rise – as do their interests and needs to diversify foreign reserves by investing in Chinese government bonds. For example, Qatar’s central bank recently signed a deal with the PBoC to invest in China’s interbank bond market to diversify its foreign exchange reserves6. In fact, if Chinese government bonds were included in the World Government Bond Index (WGBI), RMB would be the fourth-largest currency, surpassing sterling. The size and significance of the asset class will catch the attention of a wider range of global investors, leading to further focus on the RMB with internationalization.

Asset class annualized volatility

Source: FIL Limited, April 2014

4 PBoC, China Bond5 PBoC6 Qatar to Enter China’s Interbank Bond Market, Wall Street

Journal, April 18, 2014

Based on 10 years to April 2014

**Indicative RMB profile based on Jan 2011 - Apr 2014

23.0%

14.6%

6.9%

5.9%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

2.57%

Asian Equities

Asian HY

Asian Govt. Bonds

Asian IG

Offshore RMB Bonds**

5

07-2014

China’s domestic financial markets have become much more accessible in the past few years though channels such as the QFII (qualified foreign institutional investor) programme. Strong motivation in the market place and high level government endorsement will also help financial innovation bring forward more financial instruments denominated in RMB, such as futures contracts on commodities traded in RMB in Hong Kong. All of these potential developments towards the liberalization of China’s capital account will continue to bring new and exciting investor opportunities, making RMB a future global leading asset class for all investors.

FIL Limited and its subsidiaries are commonly referred to as Fidelity or Fidelity Worldwide Investment. Fidelity only gives information about its products and services. Any person considering an investment should seek independent advice on the suitability or otherwise of the particular investment. Reference to companies mentioned within this document should not be construed as a recommendation to the investor to buy or sell the same, but is included for the purpose of illustration. Performance of the stock is not a representation of the Fund’s performance. Fidelity, Fidelity Worldwide Investment, the Fidelity Worldwide Investment logo and F symbol are trademarks of FIL Limited. The material is issued by FIL Investment Management (Hong Kong) Limited and it has not been reviewed by the Securities and Futures Commission (“SFC”).

market value of World government bond index (if Chinese government bonds included) (USD bn)

Source: FIL Limited, Citigroup, April 2014

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

EUR

6,895

5,8545,238

1,250 1,201

352 257 164 126 113 85 79 75 63 55 54

USD JPY CNY GBP CAD AUD MXN DKK PLN SEK MYR ZAR CHF NOK SGD0