Embed Size (px)

Citation preview

Market Overview for Corrugated Paper and Boxes

Presented by Don Crossley, Advance Packaging Corporation’s President & Owner

Advance Packaging Corporation

• Started in 1966

• Independent Corrugator and Box Plant

• Market: Domestic US, primarily Midwest

• 80,000 tons of corrugated paper consumed annually, $53,000,000 spend

• Crossley: 38 years industry experience

• Paper buyer for 20 years

Industry Metrics

Shipment Statistics

• Corrugated industry shipments totaled more

than 376.4 billion square feet in 2016 an

increase of 2.1% from 2015

• The value of industry shipments increased

to $30.8 billion

• 80% of industry shipments came from

corrugator plants and 20% came from sheet

plants

Source: Numera, FBA

End-use markets - 2016

Food manufacturing31%

Wholesale trade16%Paper manufacturing*

9%

Agriculture, forestry, fishing and hunting

8%

Beverage manufacturing

6%

Plastics and rubber products

manufacturing5%

Chemicals manufacturing

5%

Other manufacturing10%

E-Commerce4%

Other3%

Retail trade (excl. e-commerce)

3%

*Pre-2015 this held a larger market share, but manufacture of corrugated sheets has not been included in the 2015 or 2016 reports

Source: 2016 Fibre Box Association Industry Annual Report

30370.0

30067.9

31763.4

31350.6

31902.4 31800.7

30210.6

27592.9

29794.430005.4 30079.5

30287.1

30648.7

31020.831238.7

25000.0

26000.0

27000.0

28000.0

29000.0

30000.0

31000.0

32000.0

33000.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Total Industry Consumption of Liner and Medium (Thousands of Tons)

Source: Alternative Paper Solutions

Total Capacity for North

American Producers

(Thousands of Tons)

1. IP 12667

2. WestRock 7336

3. Georgia-Pacific 4155

4. PCA 3762

5. Kapstone 1700

6. Pratt 1465

7. All Others 8797

Year Acquirer Target Assets OwnerEstimated Capacity

(ktpy)

2007 Georgia-Pacific Brewton Smurfit-Stone 275

2007 KapStone P&P Roanoke Rapids International Paper 105

2008 International Paper Weyerhaeuser (8 mills) Weyerhaeuser 5 700

2008 RockTenn Co SolvaySouthern Container

Corp730

2008 Temple-Inland NewportPremier Boxboard

Limited195

2008 KapStone P&P North Charleston MeadWestvaco 405

2011 KapStone P&P Cowpens U.S. Corrugated 220

2011 RockTenn Smurfit-Stone (12 mills) Smurfit-Stone 5 875

2012 International Paper Temple-Inland (7 mills) Temple-Inland 3 655

2012 Hood Container Corp. New Johnsonville IP /Temple-Inland 340

Market consolidation since 2007

Source: Numera, FBA

Market consolidation since 2007

Year Acquirer Target Assets OwnerEstimated Capacity

(ktpy)

2012 New-Indy Containerboard Ontario IP /Temple-Inland 330

2012 New-Indy Containerboard Oxnard International Paper 185

2012 Smurfit Kappa ForneyOrange County

Container290

2013 KapStone P&P Longview Longview Fiber 640

2013 PCA DeRidder and Wallula Boise 685

2014 RockTenn Tacoma Simpson Paper 330

2015 WestRock Newberg and Dublin SP Fiber 225

2015 Hood Container St. FrancisvilleAmzak Capital/

KPAQ145

2017 McKinley Paper (Bio-Pappel) Port Angeles Nippon Paper 200

2017 DS Smith Buyout (80% equity purchase) Interstate Resources 425

Market consolidation since 2007

Market consolidation since 2007

Source: Numera, FBA

Source: 2016 Fibre Box Association Industry Annual Report

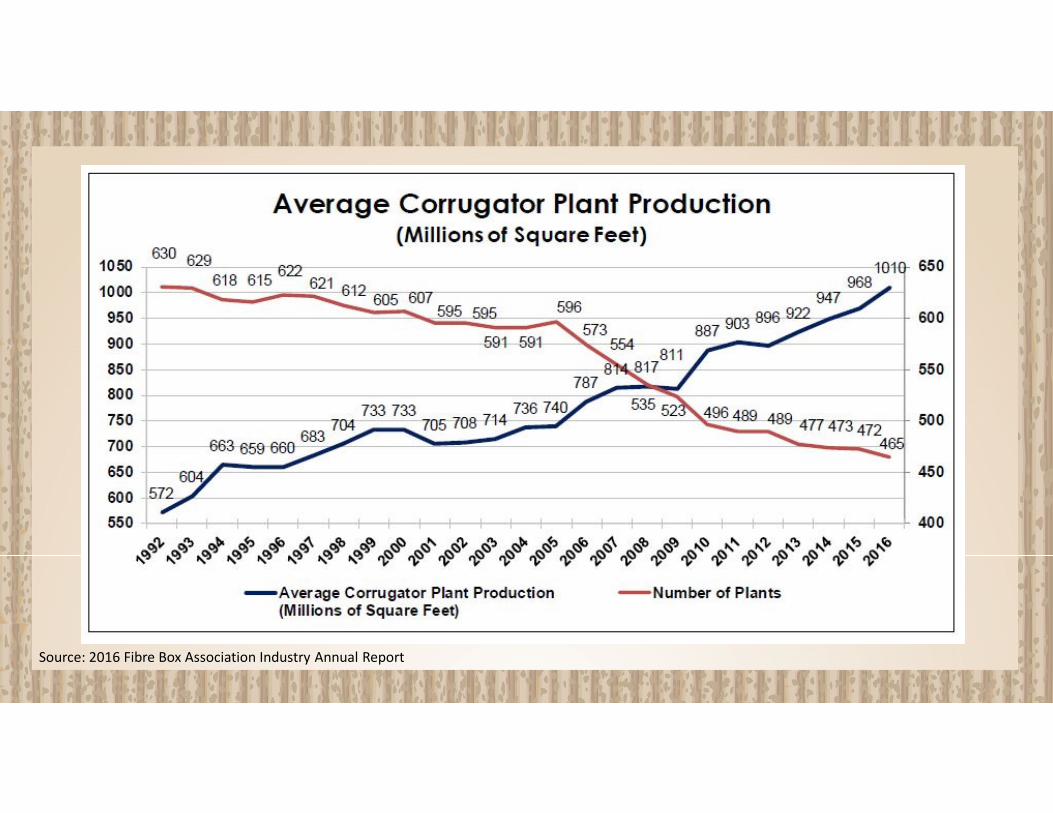

806 806

775761 755

738 743733

694 690

554535

523

496 489 489477 473 472 465

400

500

600

700

800

900

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Plant Consolidation over the Last 10 Years

Sheet Plants Corrugator Plants

Major capacity changes since 2014

Source: Numera, FBA

Source: Numera, FBA

Major capacity changes since 2014

Going forward, six major expansions are expected in the North American containerboard market. Three of these

(Wallula WA, Port Angeles WA , and DeRidder LA) are considered certain and should start up in 2018.

Three more mill projects remain on the horizon (Milwaukee WI, a SAICA project, and Fitchburg MA), but are still being

considered “uncertain” for now. We are currently considering the SAICA project as highly unlikely, given that it has been

some time since any updates were released.

Source: 2016 Fibre Box Association Industry Annual Report

17481.7

16186

14694

15485.6 15518.7 15668.1 15696.7 15506.8 15487.2 15593.4

4481.9 45134166.5

5037.5 5047.6 4816.55109.9

5511.1 5638.2 5510.1

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Domestic Consumption Kraft and Recycled Liner (Thousands of Tons)

Kraft Liner Recycled Liner

Source: 2016 Fibre Box Association Industry Annual Report

Source: 2016 Fibre Box Association Industry Annual Report

Source: 2016 Fibre Box Association Industry Annual Report

Is Cost or demand driving prices increases over the past year?

Paper mills have been running greater than 95% operating rates. When you are running at that benchmark percentage or higher it is the supply demand that is driving the prices to increase. It also means that there is a strong possibility that a price increase could be on the horizon.

Source: Ralph Young, AICC

Price increase December 2016 Price increase May 2017 Just announced a $50/Ton Price

increase potentially for Fall 2017

Operating Rates

July 2017

• Linerboard Mills 97.3%

• Medium Mills 99.4%

Source: RISI Info Friday August 18th 2017 issue & RISI Info Tuesday August 22th, 2017

Projected 2018

• Linerboard Mills 96.6%

• Medium Mills 97.3%

Projected 2019

• Linerboard Mills 96.2%

• Medium Mills 96.3%

Mill Cost Structure and what drives it? What is a typical mill cost per ton for production of liner and medium?

Mill Cost per ton for Liner Production

Kraft $328

Recycled $362

Mill Cost per ton for

Medium Production

Virgin $325

Recycled $351

Source: Ralph Young, AICC

OCC Pricing and impact on final paper and box pricing. China OCC purchases impact on OCC domestic pricing.

• OCC is currently at $165/ton up 55.7% from July 2016

• DLK currently at $195/ton up from $105/ton in July 2016

• OCC price has declined by $2/ton in August and $14/ton in September

• OCC sold to China dropped by $40/ton because of a continued lack of imported license being issued by the Chinese government.

Source: RISI Info Friday August 18th 2017 issue and KeyBanc Capital Markets

Inventory Levels for Industry

Source: 2016 Fibre Box Association Industry Annual Report and Fibre Box Association 2017

2420.7

2182.9

2107

2181.92232.1 2223.3

2432.1

2324.2

2511

2357.92391.1

2341.3

2578.9

2489.3

2664.3

2546.6

2672.3

2426.12392.1

2301.5

1500

1700

1900

2100

2300

2500

2700

2900

Containerboard Inventory Levels for Liner and Medium (Thousands of Tons)

Weeks Supply for Industry

Source: 2016 Fibre Box Association Industry Annual Report and Fibre Box Association 2017

3.7

3.2

3.5

3.7

3.93.8

4.1

3.9

4.3

4 4

3.8

4.4

4.2

4.4

4.2

4.5

4

3.8

3.53.4

3.2

2.5

3

3.5

4

4.5

5

Weeks of Supply (Thousands of Tons)

Source: 2016 Fibre Box Association Industry Annual Report

2017 Richard Storat & Associates, Inc

Anatomy Of A Price Increase

• February, 2017 Kapstone Paper and Packaging announces a $50/ton increase in containerboard, 10% on finished goods and 12% on sheets effective March 13, 2017

• Within a few days all of the 4 major integrated producers of paper announced the same price increase on paper on the same date.

• RISI’s Pulp and Paper Week does not increase index prices in March Price Watch.

• Pulp and Paper Week shows a $50/ton increase in April Price Watch siting that “producers easily passed on this increase to non-contract buyers of paper.

Public Company Performance

Source: http://financials.morningstar.com/ratios/r.html?t=KS

1217

1748

2301

2789

3077 3143

0

500

1000

1500

2000

2500

3000

3500

4000

2012 2013 2014 2015 2016 2017 (est)

Kapstone Revenue (Millions)

63

127

172

106

86

75

0

20

40

60

80

100

120

140

160

180

200

2012 2013 2014 2015 2016 2017 (est)

Kapstone Net Income (Millions)

Summary And Recommendations

• Growing demand, low new capacity coming on line and continued consolidation for the industry points to continued upward pressure on pricing in next few years.

• Demand could spike further if Trump vow to bring more manufacturing back to US materializes.

• Opportunities now for further lightweighting of packaging becoming available. Make sure you are not over packing your goods.

• Have your vendor conduct a full packaging audit. This should tell you if your packaging styles, grades and quantities are appropriate.

• Make sure to align yourself with the right vendor model (sheet plant or corrugator) based on your annual packaging spend.

• For improved efficiencies, invest in tooling short term for long term savings.

• Look for alternative pricing trigger than tying price changes to Pulp and Paper Index.

Questions