Embed Size (px)

Citation preview

Market Outlook

June 2018

EQUITY MARKET

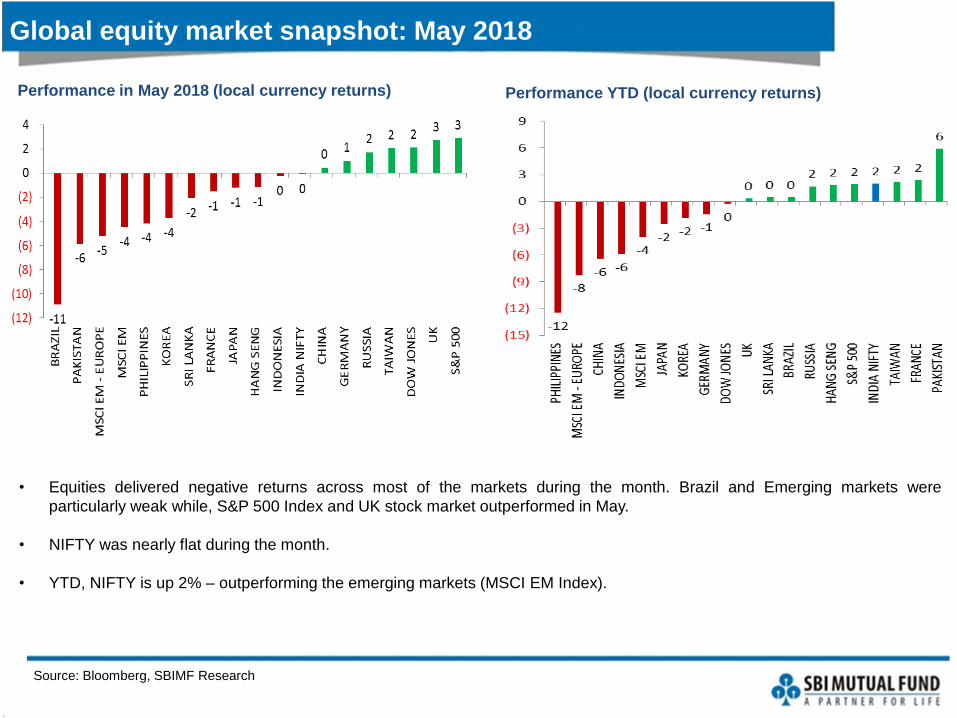

Global equity market snapshot: May 2018

Source: Bloomberg, SBIMF Research

• Equities delivered negative returns across most of the markets during the month. Brazil and Emerging markets were

particularly weak while, S&P 500 Index and UK stock market outperformed in May.

• NIFTY was nearly flat during the month.

• YTD, NIFTY is up 2% – outperforming the emerging markets (MSCI EM Index).

Performance in May 2018 (local currency returns) Performance YTD (local currency returns)

Indian stock market snapshot: May 2018

Source: Bloomberg, SBIMF Research

Performance in May 2018 (local currency returns) Performance YTD (local currency returns)

• Indian equity market delivered negative returns across most of the sectors (barring Banks) in May after delivering positive

returns in the last month. Pharma and Real Estate were the worst performers during the month.

• Sensex is up by 0.5% and Nifty is down up 0.03% in May.

• Both Mid-cap index and small-cap index were down by 6% each. YTD, small and mid-caps have under-performed NIFTY.

• YTD, Nifty is up 2% and Sensex is up 4%. Sector-wise performance has been negative across most of the sectors on a YTD

basis (barring IT, FMCG and Bank index). Real Estate and PSUs are the laggards (down 14% each respectively).

Source: CMIE economic outlook, SBIMF Research,

Growth recovery seen in last three quarters

• GDP showed 3rd consecutive quarter of growth recovery. 4Q FY18 GDP growth surged to 7.7% y-o-y

vs. downwardly revised 7.0% in 3Q (previous figure was 7.2%).

• GVA grew by 7.6% in Q4 FY18 vs. 6.6% in 3Q FY18.

India's growth continued to recover for 3rd consecutive quarter

Source: CMIE economic outlook, SBIMF Research,

Supply and demand side break-up of growth

Supply side (% growth)% share in

GDPFY17

Q1 FY18

Q2 FY18

Q3 FY18

Q4 FY18

FY18

Real GVA 100 7.1 5.6 6.1 6.6 7.6 6.5

Agriculture, forestry and fishing 16.5 6.3 3.0 2.6 3.1 4.5 3.4

Industry 31.6 6.8 0.1 6.1 7.1 8.8 5.5

Mining and quarrying 3.1 13.0 1.7 6.9 1.4 2.7 2.9

Manufacturing 17.7 7.9 -1.8 7.1 8.5 9.1 5.7

Utilities 2.2 9.2 7.1 7.7 6.1 7.7 7.2

Construction 8.6 1.3 1.8 3.1 6.6 11.5 5.7

Services 51.9 7.5 9.5 6.8 7.7 7.7 7.9

Demand side (% growth)% share in GDP

FY17Q1

FY18Q2

FY18Q3

FY18Q4

FY18FY18

Real GDP 100 7.1 5.6 6.3 7.0 7.7 6.7

Private Consumption 56.1 7.3 6.9 6.8 5.9 6.7 6.6

Government Consumption 10.3 12.2 17.6 3.8 6.8 16.8 10.9

Gross Capital Formation 35.2 4.7 5.1 8.0 10.1 14.9 9.6

Investment 31.8 10.1 0.8 6.1 9.1 14.4 7.6

Exports of G&S 1.6 5.0 5.9 6.8 6.2 3.6 5.6

Imports of G&S 1.8 4.0 18.5 10.0 10.5 10.9 12.4

Both supply side and demand side growth accelerated in Q4 FY18

• 4Q FY18 GDP growth surged to 7.7% y-o-y (vs. 7.0% in 3Q) and 6.7% for the full year. Implying that even though economic

momentum picked up in 2H, it wasn’t enough to offset the sharply reduced growth in 1H.

• This growth can primarily be explained by rise in investment and pick-up in government spending. Consumption picked up too.

Exports growth was flat while imports moderated leading to lower negative contribution to growth.

• On the supply side, GVA grew by 7.6% (vs. 6.6% in 3Q) and at 6.5% for the full year.

• Agriculture posted a strong growth while, growth in industry and services were flat. Surprisingly, all engines of industry (mining,

manufacturing, utilities and construction) picked momentum. Services were primarily supported by government spending.

• The momentum in Indian economy is picking up. While part of it stems from fading of demonetization and GST effects, other

part rests on government spending (both revex and infrastructure capex). To our dismay, India is not participating fully in the

global growth. Exports made an even lower contribution to growth this quarter.

• For FY19, we expect Real GDP growth rate to increase 7.6%.

Source: CMIE economic outlook, SBIMF Research,

High Frequency indicators point to improving growth

We track 40-50 high frequency indicators to gauge economic health. Increasing number of high frequency indicators are pointing

to improved growth. Interestingly, apart from bank credit, all indicators used to track the investment trends are encouraging.

Goods exports are languishing, but services exports is rising fast. While the agri-prices are low, rural wage growth is tepid and

there is an incessant cry of farm loan waiver, perhaps the increased access to roads, electricity, and finance is leading to

increased rural oriented demand in select segment. Weak bank credit to industry is a major constraint.

Pink denotes deterioration in growth than previous month Green denotes improvement in growth than previous month

% growth Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 5yr average (May13-Apr18)

Sale of Commercial Vehicles 50.4 52.6 39.7 31.1 24.6 76.0 3.9

Domestic Sale of two-wheelers 23.5 41.5 33.4 23.8 18.3 16.9 8.6

Foreign tourist arrivals 14.4 15.2 8.4 10.1 13.4 4.4 9.8

Domestic air traffic 16.5 17.4 18.2 23.3 26.9 N/A 16.5

Bank personal loans 17.3 18.9 20.0 20.4 17.8 19.1 16.0

Currency in circulation 39.7 80.0 75.5 57.1 37.0 32.9 9.7

Production of consumer non-durables 23.7 16.8 11.0 7.3 10.9 N/A 5.7

Aluminium production 8.8 9.0 9.1 8.3 4.3 8.0 1.9

Cement production 16.9 17.7 19.6 23.0 13.0 16.6 4.3

Bitumen consumption 15.5 9.4 12.1 15.2 10.2 16.4 6.7

AUM of Mutual Funds 38.1 29.8 29.0 24.1 21.7 20.7 23.2

Production of consumer durables 3.1 2.1 7.8 7.5 2.9 N/A 3.4

Services exports 15.4 15.9 20.4 20.3 18.7 N/A 4.0

Capital goods imports 15.6 9.8 28.1 28.1 26.2 12.4 -1.2

Coal production 0.7 0.3 3.8 1.4 9.1 16.0 4.2

Rural wage growth -0.6 -1.0 -2.1 N/A N/A N/A 1.1

Good exports 29.2 12.5 11.6 4.3 -0.4 4.4 1.0

Bank industrial credit 1.0 2.1 1.1 1.0 0.7 N/A 5.1

Bank credit to infrastructure sector -2.3 -0.7 -2.9 -1.9 -1.7 N/A 5.7

Production of crude oil -0.1 -0.8 -1.7 -2.6 -2.4 -1.6 -1.1

Production of Natural Gas 2.4 1.2 -1.2 -1.5 0.9 7.4 -3.7

Indicators that are Robust

Indicators that have recently showed stronger growth

Indicators that have recently showed weaker growth

Indicators that are weak for long

Source: IMD, SBIMF Research,

IMD predicts a normal south-west monsoon in 2018

CategoryRainfall Range (%

of LPA)Forecast

probability (%)Climatological Probability (%)

Deficient < 90 13 16

Below Normal 90 - 96 28 17

Normal 96 - 104 43 33

Above Normal 104 - 110 13 16

Excess > 110 3 17

Meteorological Sub-Divisions

IMD 2nd stage forecasts for South-West Monsoon 2018

East & North-East India 93% of LPA

North West India 100% of LPA

Central India 99% of LPA

South Peninsula 95% of LPA

July 101% of LPA, error +/- 9%

August 94% of LPA, error +/- 9%

September 97% of LPA, error +/- 4%

South-West Monsoon 2018 is most likely to be normal North-West and Central India are predicted to be normal

• IMD has predicted 43% probability of a normal monsoon (97% of LPA) in their second stage forecast of south-west

monsoon 2018.

• South Peninsula and North-east India are predicted to receive below normal rainfall while it is likely to be normal for

Central and North-West India.

• July to receive good rainfall, problems might rise during crucial sowing month of August.

• All in all, monsoon is predicted to be normal that said, spatial distribution could be a risk.

Source: CMIE economic outlook, Ministry of Agriculture, SBIMF Research, NB: ***Average Wage Rates in Rural India for

Men: Adjusted Series; *2016-17 figures are Final Estimates, **2017-18 Kharif and Rabi figures are 3rd advance estimates respectively.

Rural demand has strengthened

…but agriculture output has improved for 3rd consecutive

season…Rural wage growth is moderating***…

…leading to increased tractor and two-wheeler demand• Rural economy appears to have strengthened

• While the rural wage growth is still muted, the farm output

has been healthy for 3rd consecutive season. The rural

access to formal sector lending channel has increased.

• Focus of budget (both center and state) in last 3 years have

shifted towards rural population and outlay on rural road

development, housing, irrigation, electricity penetration and

employment has increased.

• Some of the indicators like sales of two-wheelers, FMCG

goods, tractors and fertilizer – which provides a gauge to

rural demand have picked up in last two-three quarters.

Source: CMIE economic outlook, SBIMF Research, NB: * As per April 2018 data

Manufacturing sector is on the recovery path

PMI Manufacturing indicates expansion since September 2017Manufacturing production is on the recovery path

Imports are growing faster than exports • In FY18, IIP manufacturing witnessed a marginal

improvement in the growth (4.6% in FY18 vs. 4.3% in FY17)

primarily contributed by pharmaceuticals, metals and motor-

vehicles.

• PMI manufacturing has been expanding for last 9 months on

account of improvement in the new orders, output and

purchases.

• Imports are growing faster than exports. Imports of capital

goods, in particular, are buoyant. On the exports front, 28%*

of the total exports are coming from engineering goods alone.

• Going forward, we expect manufacturing sector to remain

above trend for most part of the year, barring growth

intermittent aberrations.

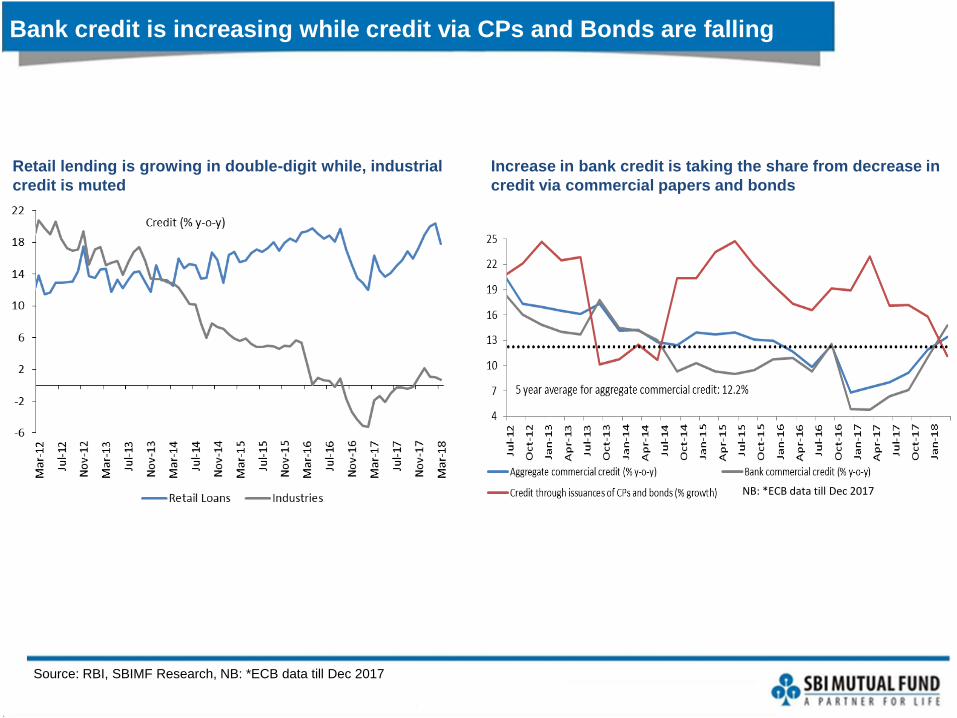

Source: RBI, SBIMF Research, NB: *ECB data till Dec 2017

Bank credit is increasing while credit via CPs and Bonds are falling

Retail lending is growing in double-digit while, industrial

credit is muted

Increase in bank credit is taking the share from decrease in

credit via commercial papers and bonds

NB: *ECB data till Dec 2017

Source: CMIE economic outlook, SBIMF Research,

Outlook: FY19 growth is expected to surge to 7.6%

Growth is likely to improve further to 7.6% y-o-y in FY18

• FY19 growth is expected to surge to 7.6% y-o-y.

• Higher oil prices, widening of trade deficit and any shortfall in monsoon pose downward risk, while government infrastructure

push, fading away of GST disruptions, rising global growth and improved business sentiments will provide the positive support.

5.5

6.4

7.4

8.2

7.1

6.7

7.6

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

FY13 FY14 FY15 FY16 FY17 FY18 FY19 E

% growth

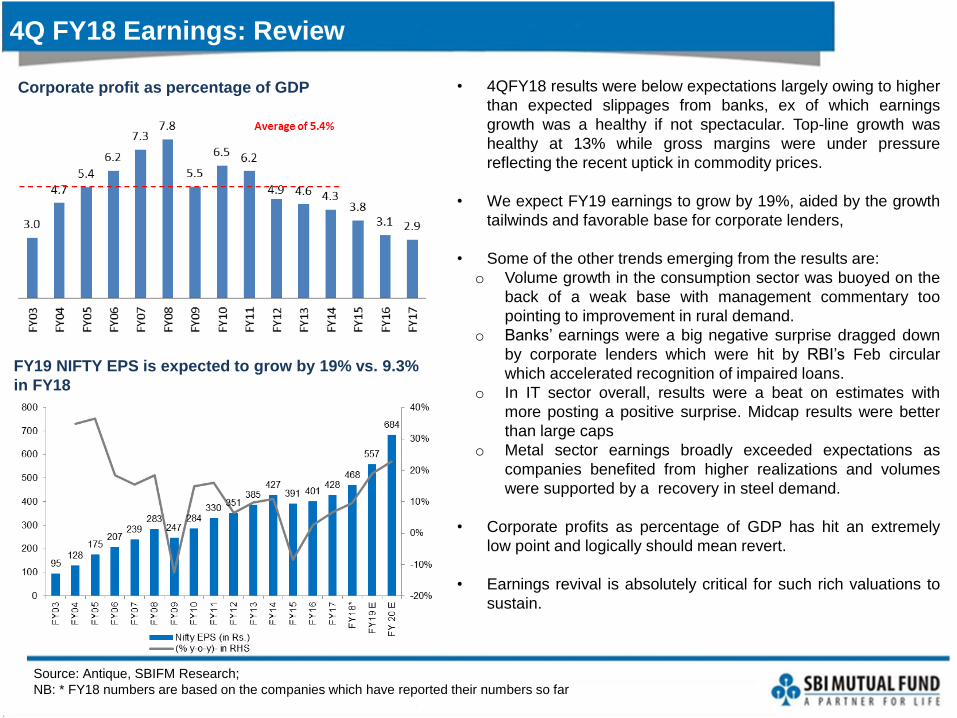

Source: Antique, SBIFM Research;

NB: * FY18 numbers are based on the companies which have reported their numbers so far

FY19 NIFTY EPS is expected to grow by 19% vs. 9.3%

in FY18

Corporate profit as percentage of GDP

4Q FY18 Earnings: Review

• 4QFY18 results were below expectations largely owing to higher

than expected slippages from banks, ex of which earnings

growth was a healthy if not spectacular. Top-line growth was

healthy at 13% while gross margins were under pressure

reflecting the recent uptick in commodity prices.

• We expect FY19 earnings to grow by 19%, aided by the growth

tailwinds and favorable base for corporate lenders,

• Some of the other trends emerging from the results are:

o Volume growth in the consumption sector was buoyed on the

back of a weak base with management commentary too

pointing to improvement in rural demand.

o Banks’ earnings were a big negative surprise dragged down

by corporate lenders which were hit by RBI’s Feb circular

which accelerated recognition of impaired loans.

o In IT sector overall, results were a beat on estimates with

more posting a positive surprise. Midcap results were better

than large caps

o Metal sector earnings broadly exceeded expectations as

companies benefited from higher realizations and volumes

were supported by a recovery in steel demand.

• Corporate profits as percentage of GDP has hit an extremely

low point and logically should mean revert.

• Earnings revival is absolutely critical for such rich valuations to

sustain.

Liquidity: FIIs pulled out while DIIs were net investors in May

FIIs sold US$ 1.2 billion during the month

Source: MOSL, SBIMF Research

Mutual funds continue to invest in Indian equities Insurance companies were net buyers during the month

-0.1

-1.0

0.9

-2.6

-0.9

0.8

-1.1

0.0

-1.7

-1.2

4.1

0.60.40.8

1.71.51.4

-0.7

-2.6

-1.2

0.0

1.6

5.1

-0.3

1.5

0.60.4

-2.0-1.7

0.3

3.0

-0.7

2.0

-1.9

2.0

-0.9-1.2M

ay-1

5

Au

g-1

5

No

v-1

5

Feb

-16

May

-16

Au

g-1

6

No

v-1

6

Feb

-17

May

-17

Au

g-1

7

No

v-1

7

Feb

-18

May

-18

US$ billion

0.7

1.6

0.9

1.61.4

0.51.00.7

1.1

0.9

-1.5

-0.1

1.1

0.00.0

0.40.6

1.4

2.0

1.4

0.80.3

0.7

1.71.51.4

1.8

2.82.7

1.51.9

1.31.4

2.5

1.4

1.71.8

May

-15

Au

g-1

5

No

v-1

5

Feb

-16

May

-16

Au

g-1

6

No

v-1

6

Feb

-17

May

-17

Au

g-1

7

No

v-1

7

Feb

-18

May

-18

US$ billion 0.7

0.3

-0.7

0.9

0.1

-0.7

0.30.3

0.80.7

-1.0

-0.3

0.0

-0.3

-0.9-1.1

-0.3-0.2

0.7

0.0-0.1 -0.2

-1.3

-0.3

-0.8

-0.4

-1.1

-0.3

0.5

0.0

-0.4

0.0

-1.4

0.3

-0.4-0.4

0.4

May

-15

Au

g-1

5

No

v-1

5

Feb

-16

May

-16

Au

g-1

6

No

v-1

6

Feb

-17

May

-17

Au

g-1

7

No

v-1

7

Feb

-18

May

-18

US$ billion

Source: Morgan Stanley, SBIMF Research,

Indian Equity Valuations relative to emerging markets

India’s valuation relative to other EMs is slightly above

historical average

…and the relative return on equity (RoE) has fallen

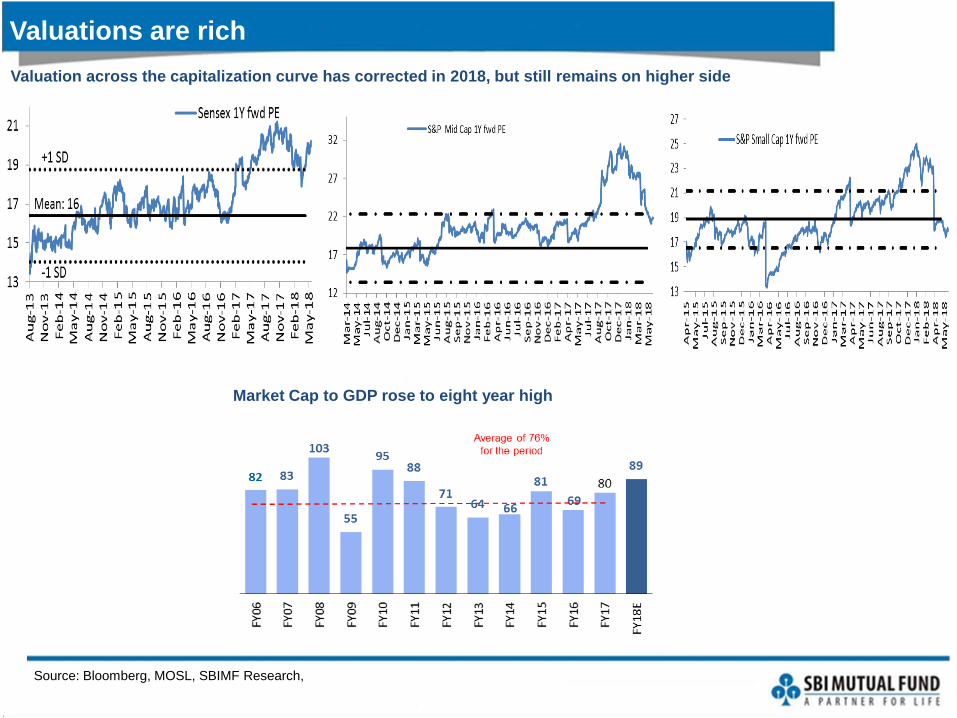

Valuations are rich

Valuation across the capitalization curve has corrected in 2018, but still remains on higher side

Source: Bloomberg, MOSL, SBIMF Research,

Market Cap to GDP rose to eight year high

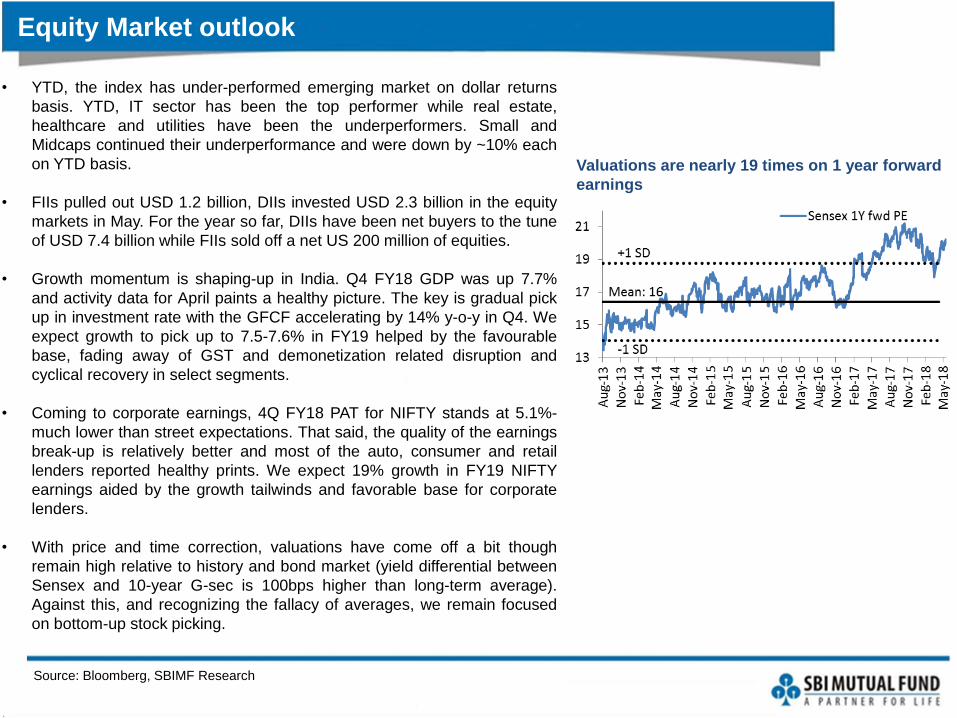

Equity Market outlook

Valuations are nearly 19 times on 1 year forward

earnings

Source: Bloomberg, SBIMF Research

• YTD, the index has under-performed emerging market on dollar returns

basis. YTD, IT sector has been the top performer while real estate,

healthcare and utilities have been the underperformers. Small and

Midcaps continued their underperformance and were down by ~10% each

on YTD basis.

• FIIs pulled out USD 1.2 billion, DIIs invested USD 2.3 billion in the equity

markets in May. For the year so far, DIIs have been net buyers to the tune

of USD 7.4 billion while FIIs sold off a net US 200 million of equities.

• Growth momentum is shaping-up in India. Q4 FY18 GDP was up 7.7%

and activity data for April paints a healthy picture. The key is gradual pick

up in investment rate with the GFCF accelerating by 14% y-o-y in Q4. We

expect growth to pick up to 7.5-7.6% in FY19 helped by the favourable

base, fading away of GST and demonetization related disruption and

cyclical recovery in select segments.

• Coming to corporate earnings, 4Q FY18 PAT for NIFTY stands at 5.1%-

much lower than street expectations. That said, the quality of the earnings

break-up is relatively better and most of the auto, consumer and retail

lenders reported healthy prints. We expect 19% growth in FY19 NIFTY

earnings aided by the growth tailwinds and favorable base for corporate

lenders.

• With price and time correction, valuations have come off a bit though

remain high relative to history and bond market (yield differential between

Sensex and 10-year G-sec is 100bps higher than long-term average).

Against this, and recognizing the fallacy of averages, we remain focused

on bottom-up stock picking.

Fixed Income Market

Global rates snapshot for May 2018

Source: Bloomberg, SBIMF Research

• US bond yields inched down by 9 bps during the month due to rekindling fears of trade war.

• Italy and Spain witnessed an increase in the bond yields by 100 bps and 22 bps respectively during the month as political

concerns have risen.

• Bonds yields decreased in other key developed markets.

• Bond yields inched up or remained same across all of the emerging markets in May (barring South Korea).

10 Year Gsec Yield (% mth end)

2015 end 2016 end 2017 end Feb-18 Mar-18 Apr-18 May-18m-o-m change

(in bps)3m Change (in

bps)% change in YTD (in bps)

Developed market

US 2.27 2.44 2.41 2.86 2.74 2.95 2.86 -9 0 45

Germany 0.63 0.21 0.43 0.66 0.50 0.56 0.34 -22 -32 -9

Italy 1.35 1.82 1.75 1.71 1.53 1.53 2.53 100 82 78

Japan 0.27 0.05 0.05 0.05 0.05 0.06 0.04 -2 -1 -1

Spain 1.77 1.38 1.57 1.54 1.16 1.28 1.50 22 -4 -6

Switzerland -0.06 -0.19 -0.15 0.09 0.03 0.09 -0.07 -15 -16 8

UK 1.96 1.24 1.19 1.50 1.35 1.42 1.23 -19 -27 4

Emerging Market

Brazil 16.51 11.40 10.26 9.61 9.49 9.84 11.46 162 185 120

China 2.83 3.03 3.88 3.84 3.74 3.63 3.63 0 -21 -25

India 7.76 6.52 7.33 7.73 7.40 7.77 7.83 6 10 50

Indonesia 8.69 7.91 6.29 6.59 6.65 6.88 6.95 7 36 66

Korea 2.08 2.07 2.47 2.74 2.63 2.74 2.70 -5 -4 23

Malaysia 4.19 4.19 3.91 4.03 3.94 4.12 4.19 6 16 28

Philippines 3.95 4.64 4.93 4.93 4.93 6.05 6.24 19 132 132

Russia 9.62 8.36 7.49 7.02 7.05 7.27 7.35 8 33 -14

Taiwan 1.02 1.20 1.03 0.97 0.97 0.97 0.97 0 0 -6

Thailand 2.49 2.65 2.32 2.39 2.40 2.44 2.60 16 22 28

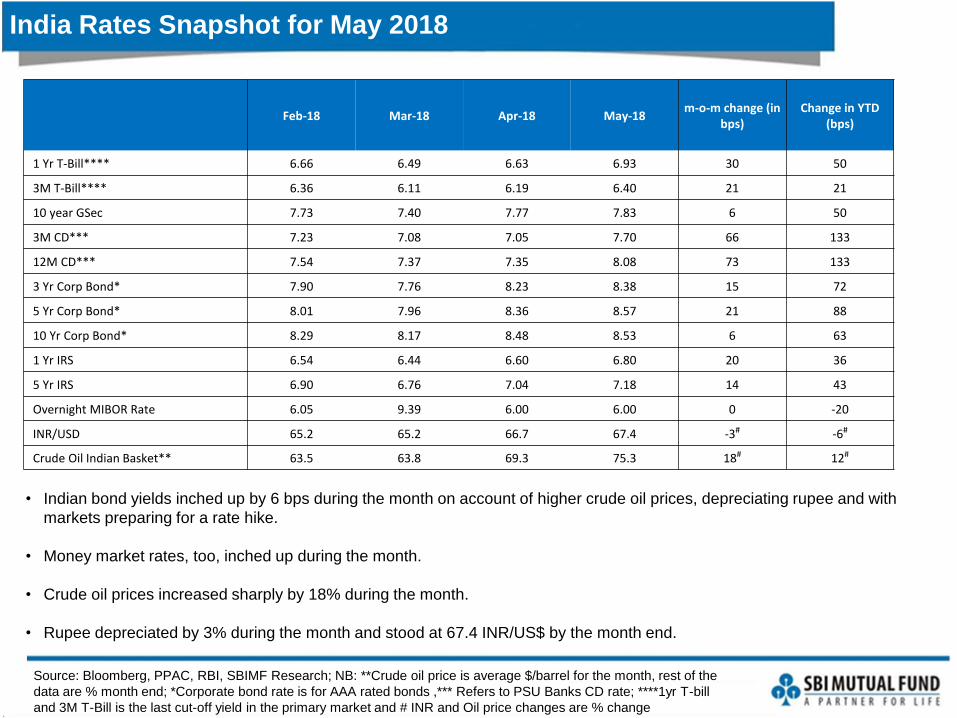

India Rates Snapshot for May 2018

Source: Bloomberg, PPAC, RBI, SBIMF Research; NB: **Crude oil price is average $/barrel for the month, rest of the

data are % month end; *Corporate bond rate is for AAA rated bonds ,*** Refers to PSU Banks CD rate; ****1yr T-bill

and 3M T-Bill is the last cut-off yield in the primary market and # INR and Oil price changes are % change

• Indian bond yields inched up by 6 bps during the month on account of higher crude oil prices, depreciating rupee and with

markets preparing for a rate hike.

• Money market rates, too, inched up during the month.

• Crude oil prices increased sharply by 18% during the month.

• Rupee depreciated by 3% during the month and stood at 67.4 INR/US$ by the month end.

Feb-18 Mar-18 Apr-18 May-18m-o-m change (in

bps)Change in YTD

(bps)

1 Yr T-Bill**** 6.66 6.49 6.63 6.93 30 50

3M T-Bill**** 6.36 6.11 6.19 6.40 21 21

10 year GSec 7.73 7.40 7.77 7.83 6 50

3M CD*** 7.23 7.08 7.05 7.70 66 133

12M CD*** 7.54 7.37 7.35 8.08 73 133

3 Yr Corp Bond* 7.90 7.76 8.23 8.38 15 72

5 Yr Corp Bond* 8.01 7.96 8.36 8.57 21 88

10 Yr Corp Bond* 8.29 8.17 8.48 8.53 6 63

1 Yr IRS 6.54 6.44 6.60 6.80 20 36

5 Yr IRS 6.90 6.76 7.04 7.18 14 43

Overnight MIBOR Rate 6.05 9.39 6.00 6.00 0 -20

INR/USD 65.2 65.2 66.7 67.4 -3# -6#

Crude Oil Indian Basket** 63.5 63.8 69.3 75.3 18# 12#

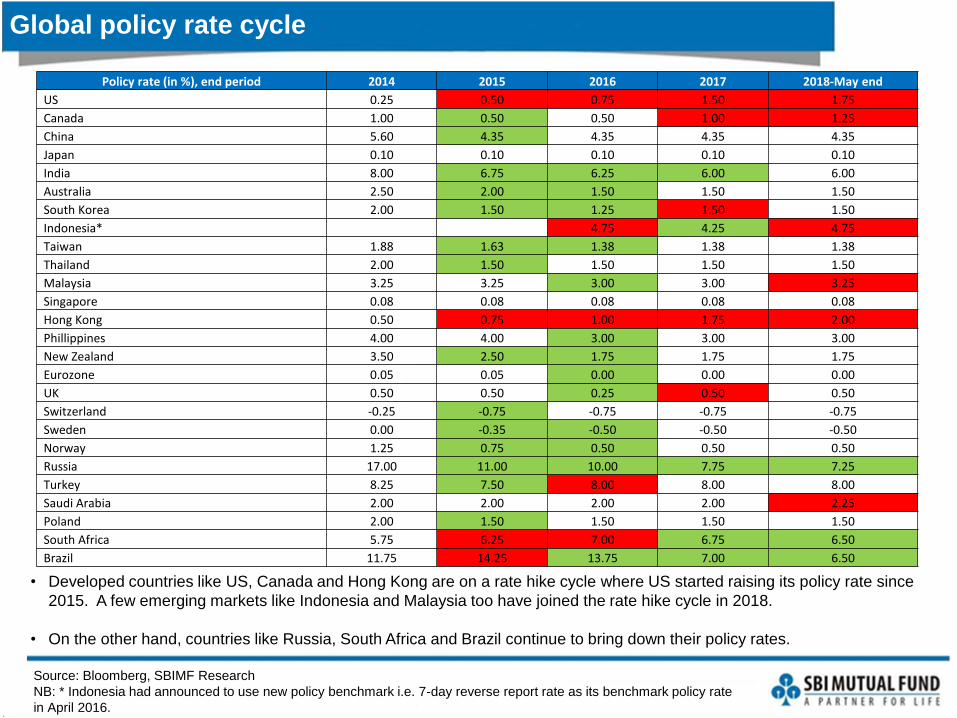

Global policy rate cycle

Source: Bloomberg, SBIMF Research

NB: * Indonesia had announced to use new policy benchmark i.e. 7-day reverse report rate as its benchmark policy rate

in April 2016.

• Developed countries like US, Canada and Hong Kong are on a rate hike cycle where US started raising its policy rate since

2015. A few emerging markets like Indonesia and Malaysia too have joined the rate hike cycle in 2018.

• On the other hand, countries like Russia, South Africa and Brazil continue to bring down their policy rates.

Policy rate (in %), end period 2014 2015 2016 2017 2018-May end

US 0.25 0.50 0.75 1.50 1.75

Canada 1.00 0.50 0.50 1.00 1.25

China 5.60 4.35 4.35 4.35 4.35

Japan 0.10 0.10 0.10 0.10 0.10

India 8.00 6.75 6.25 6.00 6.00

Australia 2.50 2.00 1.50 1.50 1.50

South Korea 2.00 1.50 1.25 1.50 1.50

Indonesia* 4.75 4.25 4.75

Taiwan 1.88 1.63 1.38 1.38 1.38

Thailand 2.00 1.50 1.50 1.50 1.50

Malaysia 3.25 3.25 3.00 3.00 3.25

Singapore 0.08 0.08 0.08 0.08 0.08

Hong Kong 0.50 0.75 1.00 1.75 2.00

Phillippines 4.00 4.00 3.00 3.00 3.00

New Zealand 3.50 2.50 1.75 1.75 1.75

Eurozone 0.05 0.05 0.00 0.00 0.00

UK 0.50 0.50 0.25 0.50 0.50

Switzerland -0.25 -0.75 -0.75 -0.75 -0.75

Sweden 0.00 -0.35 -0.50 -0.50 -0.50

Norway 1.25 0.75 0.50 0.50 0.50

Russia 17.00 11.00 10.00 7.75 7.25

Turkey 8.25 7.50 8.00 8.00 8.00

Saudi Arabia 2.00 2.00 2.00 2.00 2.25

Poland 2.00 1.50 1.50 1.50 1.50

South Africa 5.75 6.25 7.00 6.75 6.50

Brazil 11.75 14.25 13.75 7.00 6.50

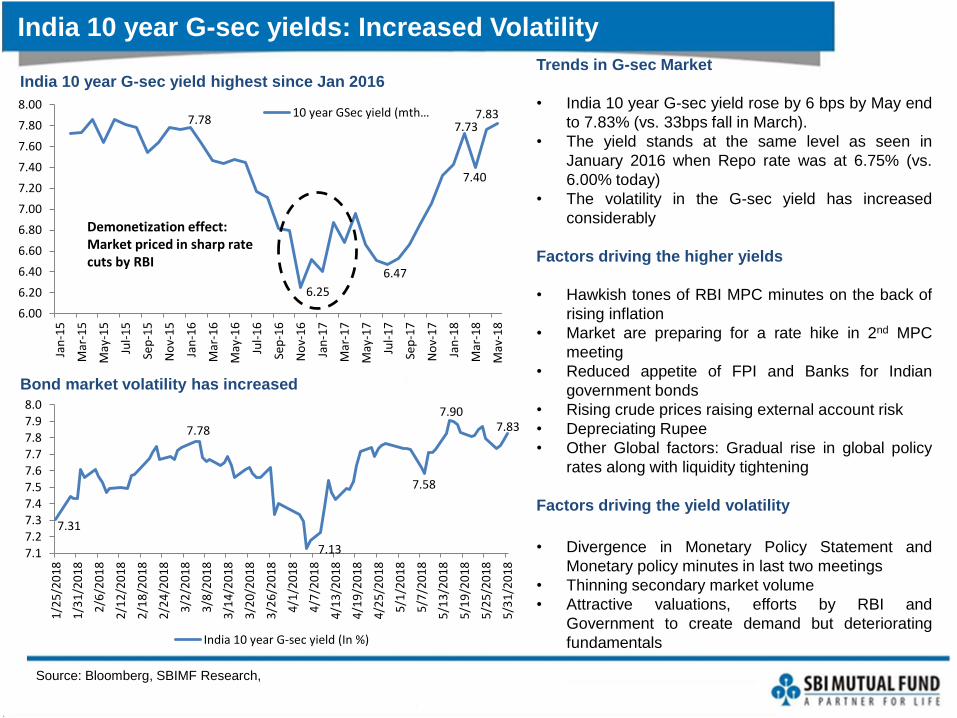

India 10 year G-sec yields: Increased Volatility

Source: Bloomberg, SBIMF Research,

Trends in G-sec Market

• India 10 year G-sec yield rose by 6 bps by May end

to 7.83% (vs. 33bps fall in March).

• The yield stands at the same level as seen in

January 2016 when Repo rate was at 6.75% (vs.

6.00% today)

• The volatility in the G-sec yield has increased

considerably

Factors driving the higher yields

• Hawkish tones of RBI MPC minutes on the back of

rising inflation

• Market are preparing for a rate hike in 2nd MPC

meeting

• Reduced appetite of FPI and Banks for Indian

government bonds

• Rising crude prices raising external account risk

• Depreciating Rupee

• Other Global factors: Gradual rise in global policy

rates along with liquidity tightening

Factors driving the yield volatility

• Divergence in Monetary Policy Statement and

Monetary policy minutes in last two meetings

• Thinning secondary market volume

• Attractive valuations, efforts by RBI and

Government to create demand but deteriorating

fundamentals

India 10 year G-sec yield highest since Jan 2016

Bond market volatility has increased

7.78

6.25

6.47

7.73

7.40

7.83

6.00

6.20

6.40

6.60

6.80

7.00

7.20

7.40

7.60

7.80

8.00

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

May

-16

Jul-

16

Sep

-16

No

v-1

6

Jan

-17

Mar

-17

May

-17

Jul-

17

Sep

-17

No

v-1

7

Jan

-18

Mar

-18

May

-18

10 year GSec yield (mth…

Demonetization effect: Market priced in sharp rate cuts by RBI

7.31

7.78

7.13

7.58

7.907.83

7.17.27.37.47.57.67.77.87.98.0

1/2

5/2

01

8

1/3

1/2

01

8

2/6

/20

18

2/1

2/2

01

8

2/1

8/2

01

8

2/2

4/2

01

8

3/2

/20

18

3/8

/20

18

3/1

4/2

01

8

3/2

0/2

01

8

3/2

6/2

01

8

4/1

/20

18

4/7

/20

18

4/1

3/2

01

8

4/1

9/2

01

8

4/2

5/2

01

8

5/1

/20

18

5/7

/20

18

5/1

3/2

01

8

5/1

9/2

01

8

5/2

5/2

01

8

5/3

1/2

01

8

India 10 year G-sec yield (In %)

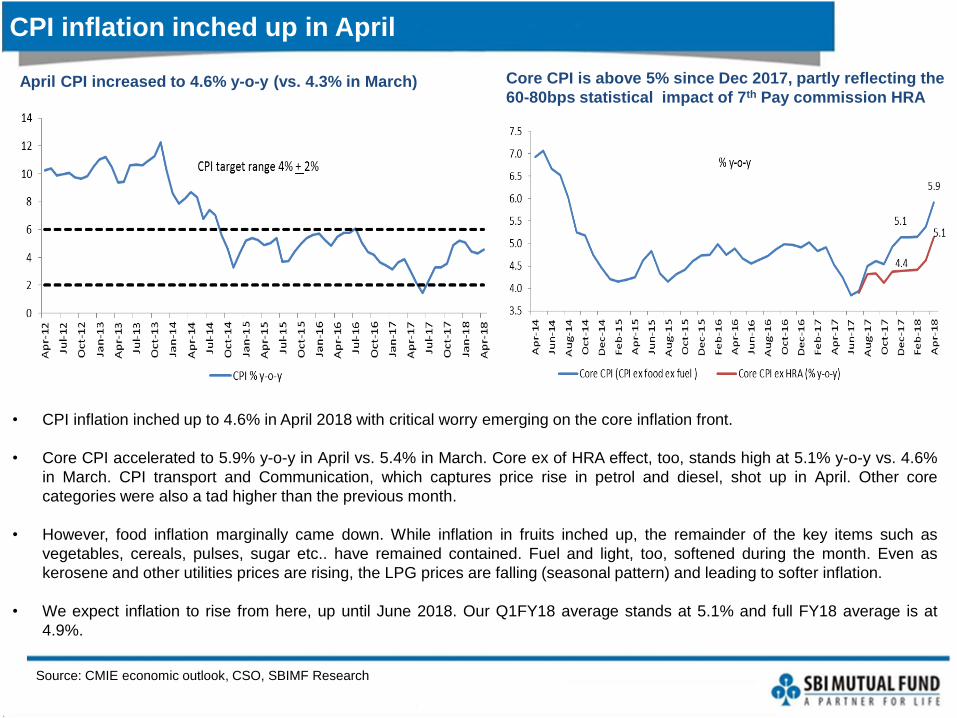

CPI inflation inched up in April

Source: CMIE economic outlook, CSO, SBIMF Research

April CPI increased to 4.6% y-o-y (vs. 4.3% in March) Core CPI is above 5% since Dec 2017, partly reflecting the

60-80bps statistical impact of 7th Pay commission HRA

• CPI inflation inched up to 4.6% in April 2018 with critical worry emerging on the core inflation front.

• Core CPI accelerated to 5.9% y-o-y in April vs. 5.4% in March. Core ex of HRA effect, too, stands high at 5.1% y-o-y vs. 4.6%

in March. CPI transport and Communication, which captures price rise in petrol and diesel, shot up in April. Other core

categories were also a tad higher than the previous month.

• However, food inflation marginally came down. While inflation in fruits inched up, the remainder of the key items such as

vegetables, cereals, pulses, sugar etc.. have remained contained. Fuel and light, too, softened during the month. Even as

kerosene and other utilities prices are rising, the LPG prices are falling (seasonal pattern) and leading to softer inflation.

• We expect inflation to rise from here, up until June 2018. Our Q1FY18 average stands at 5.1% and full FY18 average is at

4.9%.

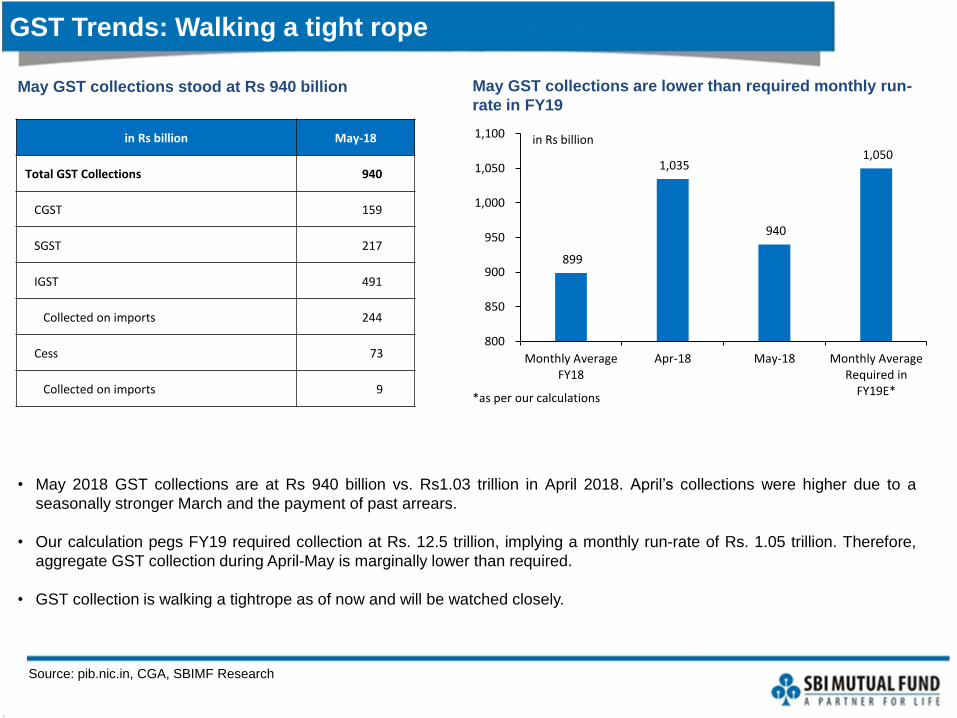

GST Trends: Walking a tight rope

Source: pib.nic.in, CGA, SBIMF Research

May GST collections stood at Rs 940 billion

• May 2018 GST collections are at Rs 940 billion vs. Rs1.03 trillion in April 2018. April’s collections were higher due to a

seasonally stronger March and the payment of past arrears.

• Our calculation pegs FY19 required collection at Rs. 12.5 trillion, implying a monthly run-rate of Rs. 1.05 trillion. Therefore,

aggregate GST collection during April-May is marginally lower than required.

• GST collection is walking a tightrope as of now and will be watched closely.

May GST collections are lower than required monthly run-

rate in FY19

in Rs billion May-18

Total GST Collections 940

CGST 159

SGST 217

IGST 491

Collected on imports 244

Cess 73

Collected on imports 9

899

1,035

940

1,050

800

850

900

950

1,000

1,050

1,100

Monthly AverageFY18

Apr-18 May-18 Monthly AverageRequired in

FY19E*

in Rs billion

*as per our calculations

Prices for most commodities have been on the rise

Source: Bloomberg, SBIMF Research

Commodities prices have been on a broad ascending path since 2016

Energy prices have witnessed a broad-based rise, agriculture commodities, precious metals and basic metals

show mixed trends

129.3

154.0

126

136

146

156

166

176M

ar-1

3

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

May

-16

Jul-

16

Sep

-16

No

v-1

6

Jan

-17

Mar

-17

May

-17

Jul-

17

Sep

-17

No

v-1

7

Jan

-18

Mar

-18

May

-18

CRB Commodity Index

-18

-10

-6 -5 -5 -4 -20

2 2 3 3 47

9 11 1214 14 15

1720 21

23 24

-20

-15

-10

-5

0

5

10

15

20

25

30

Sugar Coffee Palladium Copper Silver Iron Ore NaturalGas

Corn Coal Gasoline Heating Oil WTI Nickel

% Change YTD

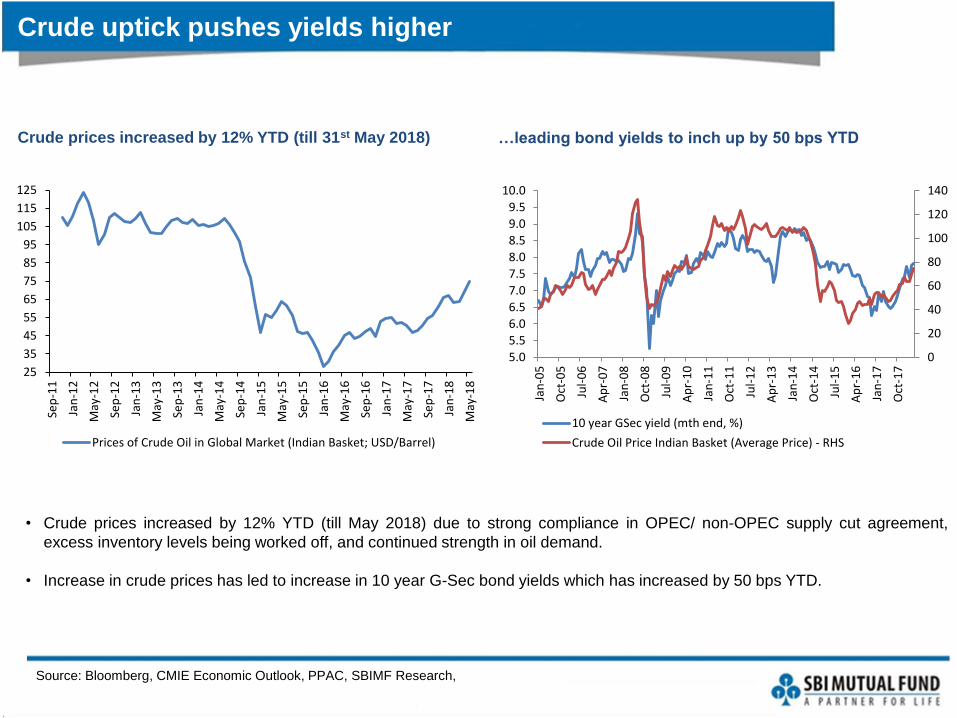

Crude uptick pushes yields higher

Source: Bloomberg, CMIE Economic Outlook, PPAC, SBIMF Research,

25

35

45

55

65

75

85

95

105

115

125

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Sep

-15

Jan

-16

May

-16

Sep

-16

Jan

-17

May

-17

Sep

-17

Jan

-18

May

-18

Prices of Crude Oil in Global Market (Indian Basket; USD/Barrel)

0

20

40

60

80

100

120

140

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

Jan

-05

Oct

-05

Jul-

06

Ap

r-0

7

Jan

-08

Oct

-08

Jul-

09

Ap

r-1

0

Jan

-11

Oct

-11

Jul-

12

Ap

r-1

3

Jan

-14

Oct

-14

Jul-

15

Ap

r-1

6

Jan

-17

Oct

-17

10 year GSec yield (mth end, %)

Crude Oil Price Indian Basket (Average Price) - RHS

Crude prices increased by 12% YTD (till 31st May 2018) …leading bond yields to inch up by 50 bps YTD

• Crude prices increased by 12% YTD (till May 2018) due to strong compliance in OPEC/ non-OPEC supply cut agreement,

excess inventory levels being worked off, and continued strength in oil demand.

• Increase in crude prices has led to increase in 10 year G-Sec bond yields which has increased by 50 bps YTD.

Source: : International Energy Statistics, PPAC, SBIMF Research

India is the third largest importer of Crude Oil…

India accounts for 10% of global crude import

2015 Net import of Crude Oil

2015 Net import of Crude Oil (In billion barrel)

% share

US 2.4 17.1

China 2.3 16.3

India 1.4 9.9

Japan 1.2 8.1

Korea 1.0 6.8

Germany 0.6 4.5

Italy 0.5 3.3

Spain 0.5 3.2

Netherlands 0.4 2.9

France 0.4 2.8

Others 3.6 25.2

Total 14.3 100.0

100

205

0

2

4

6

8

10

12

14

0

50

100

150

200

250

19

97

-98

19

98

-99

19

99

-00

20

00

-01

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

20

17

-18

India Total Consumption of Petreolum Products (Billion Litre)

% growth- RHS

…and imports 86% of its consumption needs

Source: PPAC, SBIMF Research

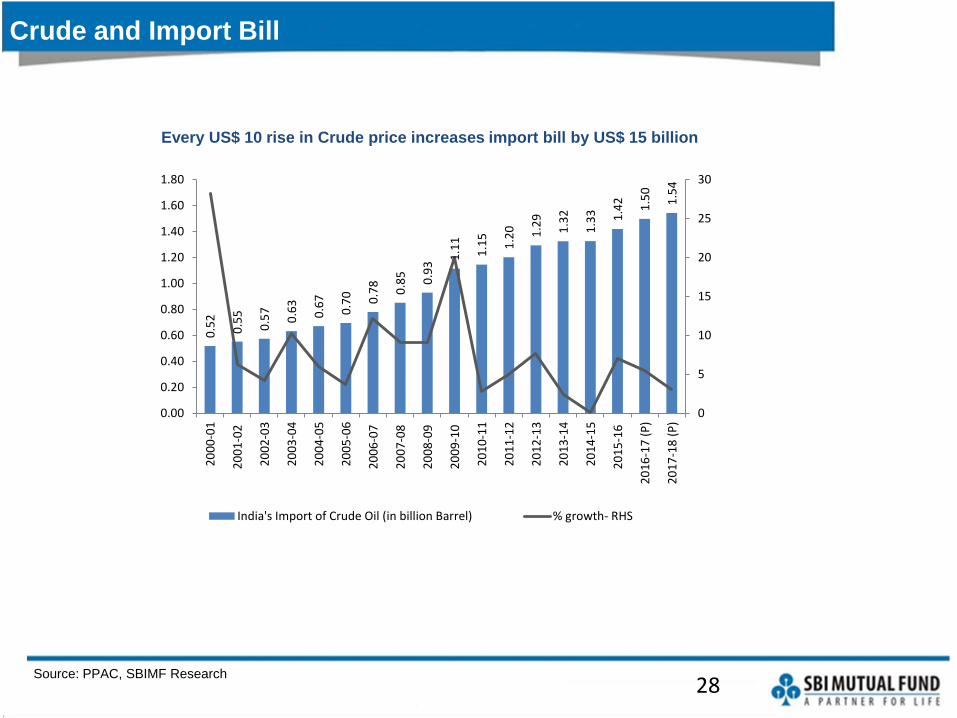

Crude and Import Bill

Every US$ 10 rise in Crude price increases import bill by US$ 15 billion

28

0.5

2

0.5

5

0.5

7

0.6

3

0.6

7

0.7

0 0.7

8

0.8

5

0.9

3

1.1

1

1.1

5

1.2

0 1.2

9

1.3

2

1.3

3 1.4

2

1.5

0

1.5

4

0

5

10

15

20

25

30

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

20

00

-01

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

(P

)

20

17

-18

(P

)

India's Import of Crude Oil (in billion Barrel) % growth- RHS

Source: PPAC, SBIMF Research

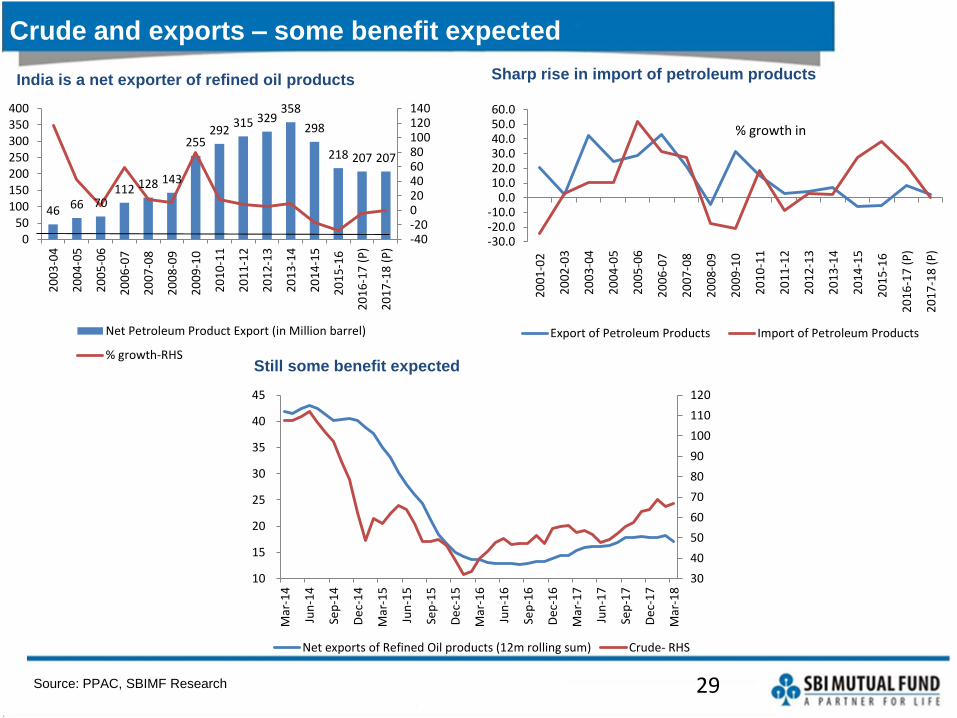

Crude and exports – some benefit expected

India is a net exporter of refined oil products

29

30

40

50

60

70

80

90

100

110

120

10

15

20

25

30

35

40

45

Mar

-14

Jun

-14

Sep

-14

De

c-1

4

Mar

-15

Jun

-15

Sep

-15

De

c-1

5

Mar

-16

Jun

-16

Sep

-16

De

c-1

6

Mar

-17

Jun

-17

Sep

-17

De

c-1

7

Mar

-18

Net exports of Refined Oil products (12m rolling sum) Crude- RHS

46 66 70112 128 143

255292

315 329358

298

218 207 207

-40-20020406080100120140

050

100150200250300350400

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

(P

)

20

17

-18

(P

)

Net Petroleum Product Export (in Million barrel)

% growth-RHS

-30.0-20.0-10.0

0.010.020.030.040.050.060.0

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

20

16

-17

(P

)

20

17

-18

(P

)

Export of Petroleum Products Import of Petroleum Products

% growth in

Sharp rise in import of petroleum products

Still some benefit expected

Source: Bloomberg, RBI, SBIMF Research

Rising crude prices: Positive bearing on Remittances

Rising oil leads to increased remittances from Indian workers in oil-exporting countries

30

1315 16

22 21

24

30

4245

52 53

63 64 65 6663

5759

20

30

40

50

60

70

80

90

100

110

120

10

20

30

40

50

60

70

FY0

1

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8E

Remittances (US$ billion) Brent (US$/barrel)- RHS

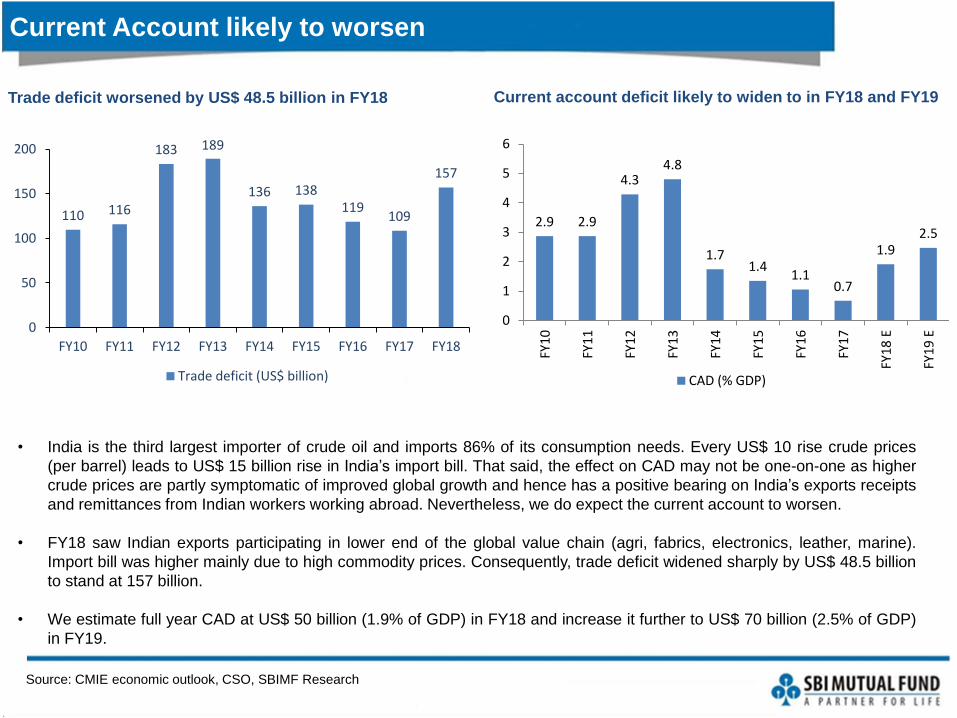

Current Account likely to worsen

Source: CMIE economic outlook, CSO, SBIMF Research

Trade deficit worsened by US$ 48.5 billion in FY18

• India is the third largest importer of crude oil and imports 86% of its consumption needs. Every US$ 10 rise crude prices

(per barrel) leads to US$ 15 billion rise in India’s import bill. That said, the effect on CAD may not be one-on-one as higher

crude prices are partly symptomatic of improved global growth and hence has a positive bearing on India’s exports receipts

and remittances from Indian workers working abroad. Nevertheless, we do expect the current account to worsen.

• FY18 saw Indian exports participating in lower end of the global value chain (agri, fabrics, electronics, leather, marine).

Import bill was higher mainly due to high commodity prices. Consequently, trade deficit widened sharply by US$ 48.5 billion

to stand at 157 billion.

• We estimate full year CAD at US$ 50 billion (1.9% of GDP) in FY18 and increase it further to US$ 70 billion (2.5% of GDP)

in FY19.

Current account deficit likely to widen to in FY18 and FY19

110 116

183 189

136 138119

109

157

0

50

100

150

200

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Trade deficit (US$ billion)

2.9 2.9

4.34.8

1.71.4

1.10.7

1.92.5

0

1

2

3

4

5

6

FY1

0

FY1

1

FY12

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8 E

FY1

9 E

CAD (% GDP)

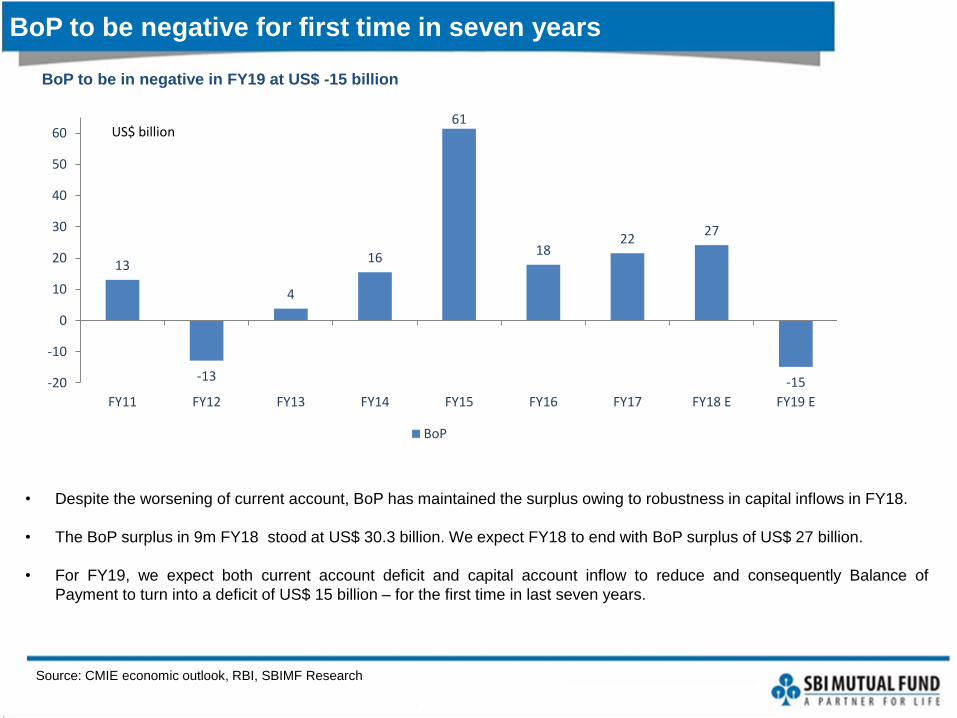

BoP to be negative for first time in seven years

Source: CMIE economic outlook, RBI, SBIMF Research

BoP to be in negative in FY19 at US$ -15 billion

• Despite the worsening of current account, BoP has maintained the surplus owing to robustness in capital inflows in FY18.

• The BoP surplus in 9m FY18 stood at US$ 30.3 billion. We expect FY18 to end with BoP surplus of US$ 27 billion.

• For FY19, we expect both current account deficit and capital account inflow to reduce and consequently Balance of

Payment to turn into a deficit of US$ 15 billion – for the first time in last seven years.

13

-13

4

16

61

1822

27

-15-20

-10

0

10

20

30

40

50

60

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 E FY19 E

BoP

US$ billion

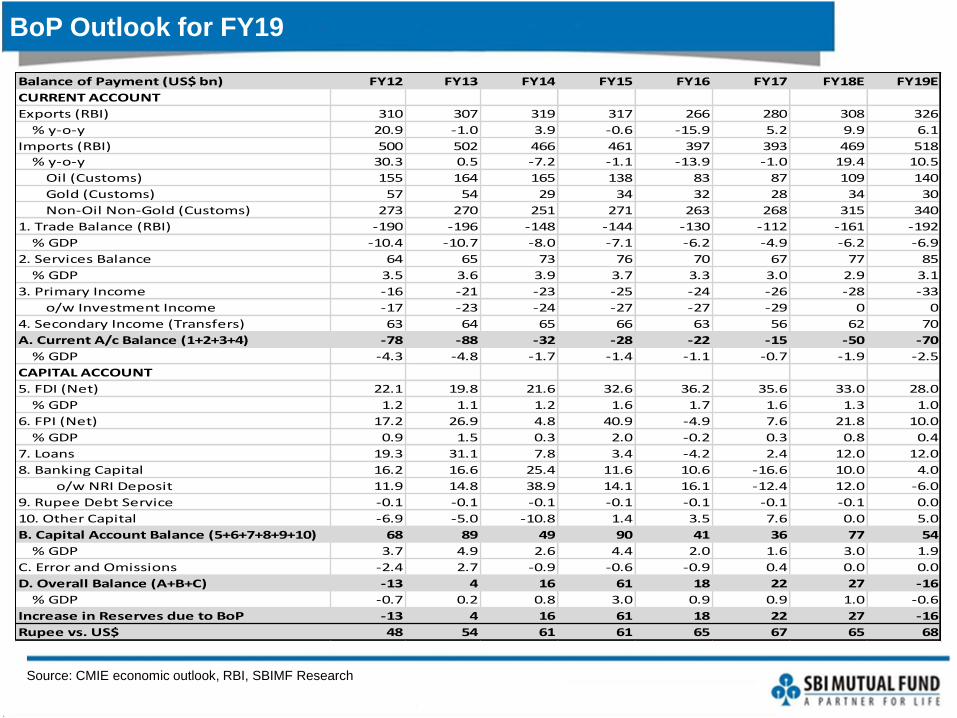

BoP Outlook for FY19

Source: CMIE economic outlook, RBI, SBIMF Research

Balance of Payment (US$ bn) FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E

CURRENT ACCOUNT

Exports (RBI) 310 307 319 317 266 280 308 326

% y-o-y 20.9 -1.0 3.9 -0.6 -15.9 5.2 9.9 6.1

Imports (RBI) 500 502 466 461 397 393 469 518

% y-o-y 30.3 0.5 -7.2 -1.1 -13.9 -1.0 19.4 10.5

Oil (Customs) 155 164 165 138 83 87 109 140

Gold (Customs) 57 54 29 34 32 28 34 30

Non-Oil Non-Gold (Customs) 273 270 251 271 263 268 315 340

1. Trade Balance (RBI) -190 -196 -148 -144 -130 -112 -161 -192

% GDP -10.4 -10.7 -8.0 -7.1 -6.2 -4.9 -6.2 -6.9

2. Services Balance 64 65 73 76 70 67 77 85

% GDP 3.5 3.6 3.9 3.7 3.3 3.0 2.9 3.1

3. Primary Income -16 -21 -23 -25 -24 -26 -28 -33

o/w Investment Income -17 -23 -24 -27 -27 -29 0 0

4. Secondary Income (Transfers) 63 64 65 66 63 56 62 70

A. Current A/c Balance (1+2+3+4) -78 -88 -32 -28 -22 -15 -50 -70

% GDP -4.3 -4.8 -1.7 -1.4 -1.1 -0.7 -1.9 -2.5

CAPITAL ACCOUNT

5. FDI (Net) 22.1 19.8 21.6 32.6 36.2 35.6 33.0 28.0

% GDP 1.2 1.1 1.2 1.6 1.7 1.6 1.3 1.0

6. FPI (Net) 17.2 26.9 4.8 40.9 -4.9 7.6 21.8 10.0

% GDP 0.9 1.5 0.3 2.0 -0.2 0.3 0.8 0.4

7. Loans 19.3 31.1 7.8 3.4 -4.2 2.4 12.0 12.0

8. Banking Capital 16.2 16.6 25.4 11.6 10.6 -16.6 10.0 4.0

o/w NRI Deposit 11.9 14.8 38.9 14.1 16.1 -12.4 12.0 -6.0

9. Rupee Debt Service -0.1 -0.1 -0.1 -0.1 -0.1 -0.1 -0.1 0.0

10. Other Capital -6.9 -5.0 -10.8 1.4 3.5 7.6 0.0 5.0

B. Capital Account Balance (5+6+7+8+9+10) 68 89 49 90 41 36 77 54

% GDP 3.7 4.9 2.6 4.4 2.0 1.6 3.0 1.9

C. Error and Omissions -2.4 2.7 -0.9 -0.6 -0.9 0.4 0.0 0.0

D. Overall Balance (A+B+C) -13 4 16 61 18 22 27 -16

% GDP -0.7 0.2 0.8 3.0 0.9 0.9 1.0 -0.6

Increase in Reserves due to BoP -13 4 16 61 18 22 27 -16

Rupee vs. US$ 48 54 61 61 65 67 65 68

Source: CMIE Economic Outlook, Bloomberg, SBIMF Research

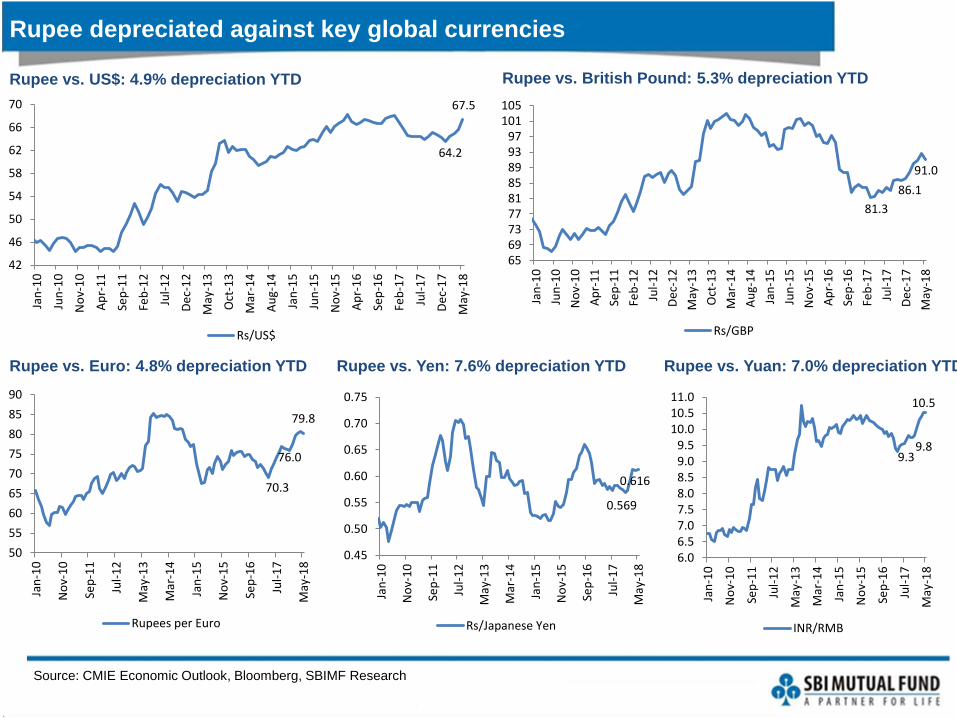

Rupee depreciated against key global currencies

Rupee vs. Yuan: 7.0% depreciation YTD

Rupee vs. British Pound: 5.3% depreciation YTD

Rupee vs. Euro: 4.8% depreciation YTD

70.3

76.0

79.8

50

55

60

65

70

75

80

85

90

Jan

-10

No

v-1

0

Sep

-11

Jul-

12

May

-13

Mar

-14

Jan

-15

No

v-1

5

Sep

-16

Jul-

17

May

-18

Rupees per Euro

Rupee vs. Yen: 7.6% depreciation YTD

9.39.8

10.5

6.06.57.07.58.08.59.09.5

10.010.511.0

Jan

-10

No

v-1

0

Sep

-11

Jul-

12

May

-13

Mar

-14

Jan

-15

No

v-1

5

Sep

-16

Jul-

17

May

-18

INR/RMB

81.3

86.1

91.0

656973778185899397

101105

Jan

-10

Jun

-10

No

v-1

0

Ap

r-1

1

Sep

-11

Feb

-12

Jul-

12

De

c-1

2

May

-13

Oct

-13

Mar

-14

Au

g-1

4

Jan

-15

Jun

-15

No

v-1

5

Ap

r-1

6

Sep

-16

Feb

-17

Jul-

17

De

c-1

7

May

-18

Rs/GBP

0.569

0.616

0.45

0.50

0.55

0.60

0.65

0.70

0.75Ja

n-1

0

No

v-1

0

Sep

-11

Jul-

12

May

-13

Mar

-14

Jan

-15

No

v-1

5

Sep

-16

Jul-

17

May

-18

Rs/Japanese Yen

64.2

67.5

42

46

50

54

58

62

66

70

Jan

-10

Jun

-10

No

v-1

0

Ap

r-1

1

Sep

-11

Feb

-12

Jul-

12

De

c-1

2

May

-13

Oct

-13

Mar

-14

Au

g-1

4

Jan

-15

Jun

-15

No

v-1

5

Ap

r-1

6

Sep

-16

Feb

-17

Jul-

17

De

c-1

7

May

-18

Rs/US$

Rupee vs. US$: 4.9% depreciation YTD

DXY strengthened; ADXY weakened; Rupee is an under-performer

Source: Bloomberg, SBIMF Research

94.9

89.4

94.1

87

90

93

96

99

102

Ap

r-1

6M

ay-1

6Ju

n-1

6Ju

l-1

6A

ug-

16

Sep

-16

Oct

-16

No

v-1

6D

ec-

16

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7M

ay-1

7Ju

n-1

7Ju

l-1

7A

ug-

17

Sep

-17

Oct

-17

No

v-1

7D

ec-

17

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8M

ay-1

8

DXY Index

Dollar strengthened by 4.3% FYTD

112.1

109.4

102

107

112

117

122

Jan

-13

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Sep

-15

Jan

-16

May

-16

Sep

-16

Jan

-17

May

-17

Sep

-17

Jan

-18

May

-18

ADXY Index

Asian currencies weakened by 1.9% FYTD

-15.7

-11.2

-7.2-5.6 -5.3 -5.2 -5.0

-2.3 -1.5 -0.8 -0.7 -0.5

1.6 1.7 1.8 3.9

-20

-15

-10

-5

0

5

Turk

ey

Lira

Bra

zil R

eal

Ru

ssia

n R

ou

ble

Po

lish

Zlo

ty

Ind

ian

Ru

pe

e

Hu

nga

rian

Fo

rin

t

Ph

ilip

pin

e P

eso

Ind

on

esi

an R

up

iah

Afr

ican

Ran

d

Me

xica

n P

eso

Ko

rean

Wo

n

Taiw

anes

e D

olla

r

Ch

ine

se r

enm

inb

i

Mal

aysi

an R

ingi

tt

Thai

Bah

t

Co

lom

bia

n P

eso

% change YTD

Rupee has been an under-performer in the EM currency Basket YTD

2013 and today: Definitely better

May-13 May-18 Better or Worse Comments

Fiscal Situation- Worse

Central Fiscal Deficit (% GDP) 4.9% 3.5% Better FY13 vs. FY18 figure

State Fiscal Deficit (% GDP) 2.0% 3.0% Worse FY13 vs. FY18 figure

Total Bond Supply Rs. Tril l ion 7.6 11.5 Worse FY14 vs. FY19; A major buyer PSU Banks are out of market

Inflation- Better

CPI % y-o-y 10.4 4.7 Better Preceeding 6 month avg

CPI- Outlook % y-o-y 10.0 5.0 Better FY14 vs. FY19

External Account- Better

CAD US$ bn 88 50 Better FY13 vs. FY18E

CAD % GDP 4.8 1.9 Better FY13 vs. FY18E

BoP US$ bn 4 27 Better FY13 vs. FY18E

FX Reserves US$ bn 259 420 Better May 2013 vs. May 2018

Import Cover months 7.2 10.9 Better May 2013 vs. Latest as of Mar 2018

FX Reserves/St Debt Ratio 3.1 4.1 Better May 2013 vs. Latest as of Mar 2018

FX Reserves/ (1 yr CAD+ ST Debt) Ratio 1.6 2.9 Better May 2013 vs. Latest as of Mar 2018

FX Reserves/ Outstanding FII Stock Ratio 0.6 0.6 Same May 2013 vs. Latest as of Mar 2018

Gold Imports US$ bn 54 34 Better FY13 vs. FY18

Growth- Better

GDP % y-o-y 4.8 6.8 Better 2H FY13 vs. 2H FY18

GDP- Outlook % y-o-y 6.5 7.6 Better FY14 vs. FY19

External Situation- Better

Crude Oil - Brent US$ bbl 103 78 Better During the month

DXY % Change 4.0 0.0 Better In preceeding 6 months

Rs./US$ % Change -4.0 -5.2 Same In preceeding 6 months

REER Trade wt 6 ccy 121 125 Same May 2013 vs. Latest as of Mar 2018

Rates- Better

India Real Rate (Policy rate- CPI) bps -120 130 Better April 2018 vs. May 2013

India-US Real Rate Differential (10 yr-CPI) bps -190 270 Worse April 2018 vs. May 2013

Proximity to Election

General election months 12 12 Same

Source: CMIE Economic Outlook, RBI, Bloomberg, SBIMF Research

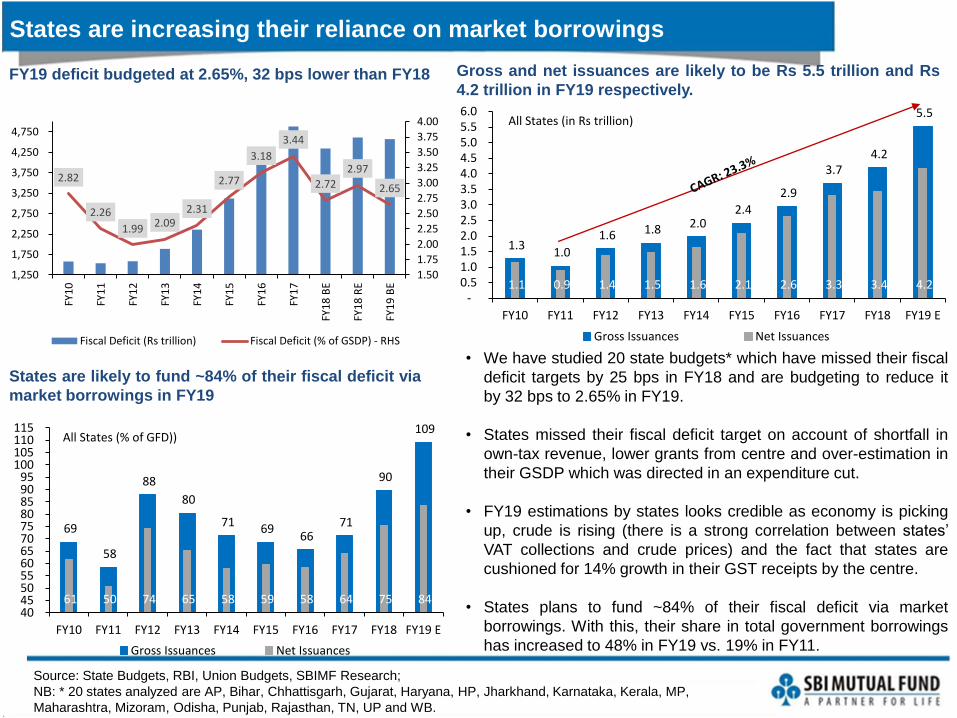

Source: State Budgets, RBI, Union Budgets, SBIMF Research;

NB: * 20 states analyzed are AP, Bihar, Chhattisgarh, Gujarat, Haryana, HP, Jharkhand, Karnataka, Kerala, MP,

Maharashtra, Mizoram, Odisha, Punjab, Rajasthan, TN, UP and WB.

States are increasing their reliance on market borrowings

FY19 deficit budgeted at 2.65%, 32 bps lower than FY18

2.82

2.26

1.99 2.092.31

2.77

3.18

3.44

2.72

2.97

2.65

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

3.75

4.00

1,250

1,750

2,250

2,750

3,250

3,750

4,250

4,750

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8 B

E

FY1

8 R

E

FY1

9 B

E

Fiscal Deficit (Rs trillion) Fiscal Deficit (% of GSDP) - RHS

1.3 1.0

1.6 1.8 2.0 2.4

2.9

3.7 4.2

5.5

1.1 0.9 1.4 1.5 1.6 2.1 2.6 3.3 3.4 4.2 -

0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5 6.0

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 E

All States (in Rs trillion)

Gross Issuances Net Issuances

69

58

88

80

71 69 66

71

90

109

61 50 74 65 58 59 58 64 75 84 40 45 50 55 60 65 70 75 80 85 90 95

100 105 110 115

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 E

All States (% of GFD))

Gross Issuances Net Issuances

Gross and net issuances are likely to be Rs 5.5 trillion and Rs

4.2 trillion in FY19 respectively.

States are likely to fund ~84% of their fiscal deficit via

market borrowings in FY19

• We have studied 20 state budgets* which have missed their fiscal

deficit targets by 25 bps in FY18 and are budgeting to reduce it

by 32 bps to 2.65% in FY19.

• States missed their fiscal deficit target on account of shortfall in

own-tax revenue, lower grants from centre and over-estimation in

their GSDP which was directed in an expenditure cut.

• FY19 estimations by states looks credible as economy is picking

up, crude is rising (there is a strong correlation between states’

VAT collections and crude prices) and the fact that states are

cushioned for 14% growth in their GST receipts by the centre.

• States plans to fund ~84% of their fiscal deficit via market

borrowings. With this, their share in total government borrowings

has increased to 48% in FY19 vs. 19% in FY11.

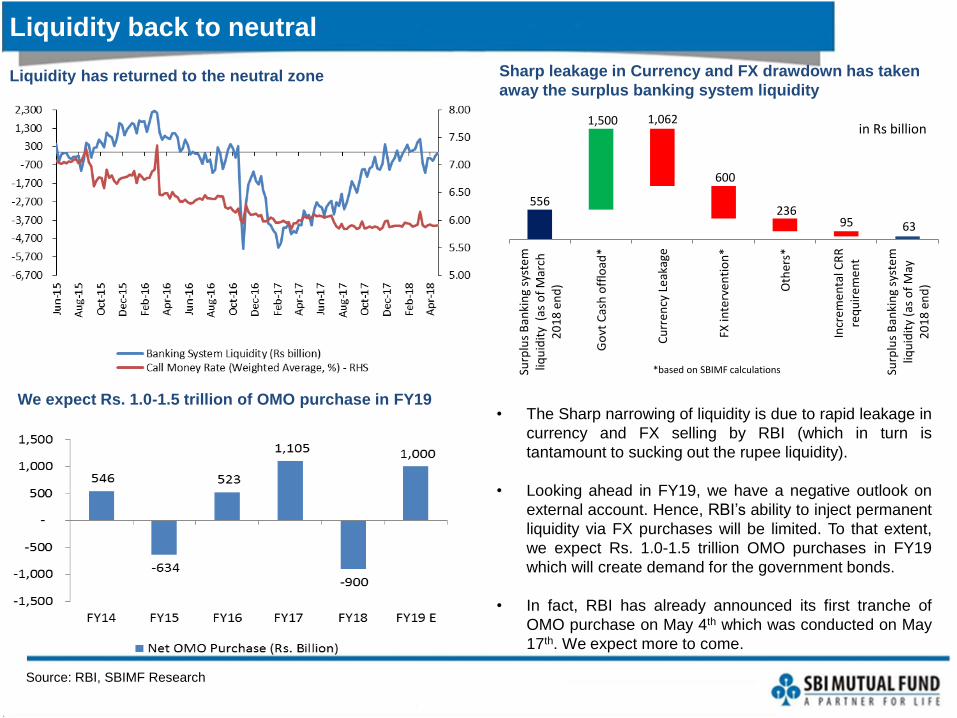

Liquidity back to neutral

Source: RBI, SBIMF Research

Sharp leakage in Currency and FX drawdown has taken

away the surplus banking system liquidity

• The Sharp narrowing of liquidity is due to rapid leakage in

currency and FX selling by RBI (which in turn is

tantamount to sucking out the rupee liquidity).

• Looking ahead in FY19, we have a negative outlook on

external account. Hence, RBI’s ability to inject permanent

liquidity via FX purchases will be limited. To that extent,

we expect Rs. 1.0-1.5 trillion OMO purchases in FY19

which will create demand for the government bonds.

• In fact, RBI has already announced its first tranche of

OMO purchase on May 4th which was conducted on May

17th. We expect more to come.

We expect Rs. 1.0-1.5 trillion of OMO purchase in FY19

Liquidity has returned to the neutral zone

556

1,500 1,062

600

236 95 63

Surp

lus

Ban

kin

g sy

stem

liqu

idit

y (

as o

f M

arch

20

18

en

d)

Go

vt C

ash

off

load

*

Cu

rre

ncy

Le

akag

e

FX in

terv

en

tio

n*

Oth

ers*

Incr

em

en

tal C

RR

req

uir

em

en

t

Surp

lus

Ban

kin

g sy

stem

liqu

idit

y (a

s o

f M

ay2

01

8 e

nd

)

in Rs billion

*based on SBIMF calculations

Thinning Volume in the secondary market

Source: CEIC, CCIL, RBI, SBIMF Research

Trading activity in secondary Market has fallen considerably in

last one year

• Markets turned jittery over concerns of diminishing appetite for government securities and poor participation by banks.

• In FY18, average monthly trading volume for G-sec has fallen considerably (16% of total outstanding securities vs. 26% in

FY17).

• Treasury bills and State Development Loans (SDLs) also witnessed weaker traction during the year.

• Bank CDs and Corporate Bonds, however, saw some pick-up in volumes.

• Thinning volumes for government papers has also added to volatility in the bond market space.

All government papers (G-sec, T-Bill and SDL) saw

weaker volumes in FY18

Total Monthly Traded Volume (% Outstanding)

G-sec T Bill SDL CPs CDsCorp

Bonds

FY13 16.0 14.5 1.2 18.8 22.7 5.4

FY14 18.6 19.7 1.3 31.8 41.0 5.9

FY15 19.1 17.7 1.3 30.6 43.5 5.4

FY16 16.1 17.8 1.9 24.6 48.4 4.1

FY17 26.4 17.9 2.7 25.8 45.9 4.3

FY18 15.8 15.8 2.1 23.3 51.8 4.4

Debt Market Valuations: attractive

Source: Bloomberg, SBIMF Research

3.2% is an attractive real returns for foreign investors Differential between 10-year yield and Repo rate is higher

than average

G-sec yield relative to equity earnings yield higher than long-term trend

10 Year Gsec Yield

(% mth end)-May

2018

CPI Inflation-April 2018

2018

Real Rate (in %)

Sovereign Credit

Rating by Moody’s

Sovereign Credit

Rating by S&P

Brazil 11.46 2.8 8.7 Ba2- BB-

Russia 7.35 2.4 4.9 Ba1 BB+

South Africa 8.72 4.5 4.2 Baa3- BB+

Indonesia 6.95 3.4 3.6 Baa3 BBB-

India 7.83 4.6 3.2 Baa2 BBB-

China 3.63 1.8 1.8 A1 A+

Thailand 2.60 1.1 1.5 Baa2 BBB

Korea 2.70 1.6 1.1 Baa1 BBB+

Malaysia 4.19 1.4 2.8 Aa2 AA

Philippines 6.24 4.5 1.7 A3 A-

US 2.86 2.5 0.4 Aaa AA+

Taiwan 0.97 2.0 -1.0 Aa3 AA-

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

No

v-0

5

May

-06

No

v-0

6

May

-07

No

v-0

7

May

-08

No

v-0

8

May

-09

No

v-0

9

May

-10

No

v-1

0

May

-11

No

v-1

1

May

-12

No

v-1

2

May

-13

No

v-1

3

May

-14

No

v-1

4

May

-15

No

v-1

5

May

-16

No

v-1

6

May

-17

No

v-1

7

May

-18

India Earnings Yield (in %) India 10 Year G-sec (in %)

-150-100

-500

50100150200250300350

Oct

-01

Ap

r-0

2O

ct-0

2A

pr-

03

Oct

-03

Ap

r-0

4O

ct-0

4A

pr-

05

Oct

-05

Ap

r-0

6O

ct-0

6A

pr-

07

Oct

-07

Ap

r-0

8O

ct-0

8A

pr-

09

Oct

-09

Ap

r-1

0O

ct-1

0A

pr-

11

Oct

-11

Ap

r-1

2O

ct-1

2A

pr-

13

Oct

-13

Ap

r-1

4O

ct-1

4A

pr-

15

Oct

-15

Ap

r-1

6O

ct-1

6A

pr-

17

Oct

-17

Ap

r-1

8

India 10 year minus Repo Rate (in bps)

Long Period Average: 88 bps

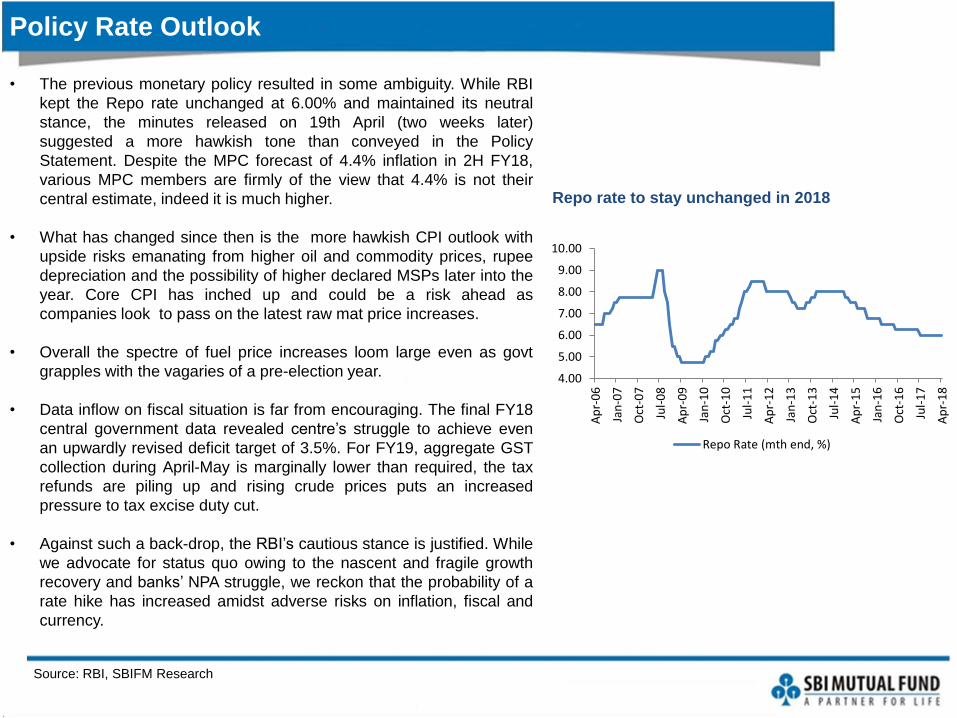

Policy Rate Outlook

Source: RBI, SBIFM Research

Repo rate to stay unchanged in 2018

• The previous monetary policy resulted in some ambiguity. While RBI

kept the Repo rate unchanged at 6.00% and maintained its neutral

stance, the minutes released on 19th April (two weeks later)

suggested a more hawkish tone than conveyed in the Policy

Statement. Despite the MPC forecast of 4.4% inflation in 2H FY18,

various MPC members are firmly of the view that 4.4% is not their

central estimate, indeed it is much higher.

• What has changed since then is the more hawkish CPI outlook with

upside risks emanating from higher oil and commodity prices, rupee

depreciation and the possibility of higher declared MSPs later into the

year. Core CPI has inched up and could be a risk ahead as

companies look to pass on the latest raw mat price increases.

• Overall the spectre of fuel price increases loom large even as govt

grapples with the vagaries of a pre-election year.

• Data inflow on fiscal situation is far from encouraging. The final FY18

central government data revealed centre’s struggle to achieve even

an upwardly revised deficit target of 3.5%. For FY19, aggregate GST

collection during April-May is marginally lower than required, the tax

refunds are piling up and rising crude prices puts an increased

pressure to tax excise duty cut.

• Against such a back-drop, the RBI’s cautious stance is justified. While

we advocate for status quo owing to the nascent and fragile growth

recovery and banks’ NPA struggle, we reckon that the probability of a

rate hike has increased amidst adverse risks on inflation, fiscal and

currency.

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Ap

r-0

6

Jan

-07

Oct

-07

Jul-

08

Ap

r-0

9

Jan

-10

Oct

-10

Jul-

11

Ap

r-1

2

Jan

-13

Oct

-13

Jul-

14

Ap

r-1

5

Jan

-16

Oct

-16

Jul-

17

Ap

r-1

8

Repo Rate (mth end, %)

Debt Market Outlook

Source: Bloomberg, SBIFM Research

Valuations look attractive at G-sec vs. Repo rate

• Bond market has been particularly volatile with 10 year G-sec gyrating

55bps within a fortnight. The yield hugged 7.13% on the day of monetary

policy (5th April) and shot past 7.75% on release of monetary policy

minutes on 19th April.

• In the policy statement, RBI appeared sanguine on inflation and even

revised their inflation projections lower. However, the minutes released two

weeks later seemed relatively hawkish. Market participants are finding it

difficult to decipher the forward guidance given the divergence between the

Policy Statement and the minutes.

• Our call is that we are in the phase of a prolonged pause, but for the risks

arising from higher commodity prices and any untoward actions by the

government in an election year.

• With crude flanking above US$ 70 per barrel, some familiar problems,

namely budget shortfalls, high inflation, current-account deficits and

pressure on rupee have and could make an unwelcome return.

• Thinning volumes and higher volatility create a vicious cycle with potential

ramifications on risk premium.

• RBI has announced an OMO purchase (due on 17th May), have spelled

out some relaxation in the FPI debt inflow as well as ECB norms so as to

attract foreign capital. We believe, the unfolding fiscal dynamics, MSP

announcements, bank credit demand and global developments remain

important variables where considerable uncertainties persist.

• Looking ahead, given the mix of attractive valuations and prospects of

favourable demand-supply in second half (we expect OMO purchase) but

concerning fundamentals, we would be tactical in taking duration exposure.

6.006.507.007.508.008.509.009.50

May

-11

No

v-1

1

May

-12

No

v-1

2

May

-13

No

v-1

3

May

-14

No

v-1

4

May

-15

No

v-1

5

May

-16

No

v-1

6

May

-17

No

v-1

7

May

-18

10 year GSec yield (mth end, %)

Repo Rate (mth end, %)

Thank you

Disclaimer

This presentation is for information purposes only and is not an offer to sell or a solicitation to buy anymutual fund units/securities. These views alone are not sufficient and should not be used for thedevelopment or implementation of an investment strategy. It should not be construed as investmentadvice to any party. All opinions and estimates included here constitute our view as of this date and aresubject to change without notice. Neither SBI Funds Management Private Limited, nor any personconnected with it, accepts any liability arising from the use of this information. The recipient of thismaterial should rely on their investigations and take their own professional advice.

Mutual Funds investments are subject to market risks, read all scheme related documentscarefully.

Asset Management Company: SBI Funds Management Private Limited (A joint venture with SBI andAMUNDI). Trustee Company: SBI Mutual Fund Trustee Company Private Limited.

Contact Details

SBI Funds Management Private Limited

(A joint venture between SBI and AMUNDI)

Corporate Office:

9th Floor, Crescenzo, C-38 & 39, G Block,Bandra Kurla Complex,Bandra (East), Mumbai - 400 051Tel: +91 22 6179 3000Fax: +91 22 6742 5687/88/89/90/91

Website: www.sbimf.com

Call: 1800 425 5425

Visit us @ www.youtube.com/user/sbimutualfund

SMS: “SBIMF” to 56161

Email: [email protected]

Visit us @ www.facebook.com/SBIMF