Embed Size (px)

Citation preview

8/4/2019 Market Outlook 26th August 2011

http://slidepdf.com/reader/full/market-outlook-26th-august-2011 1/3

1

Market OutlookIndia Research August 26, 2011

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

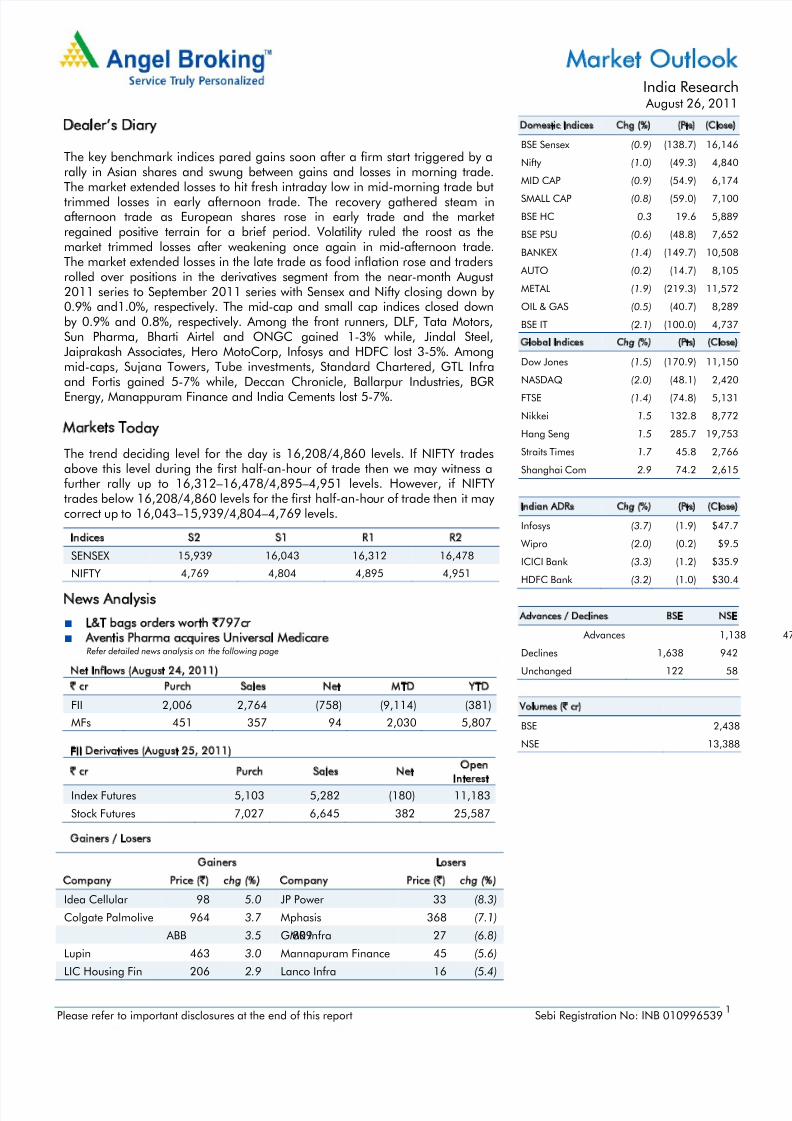

Dealer’s Diary

The key benchmark indices pared gains soon after a firm start triggered by arally in Asian shares and swung between gains and losses in morning trade.

The market extended losses to hit fresh intraday low in mid-morning trade buttrimmed losses in early afternoon trade. The recovery gathered steam inafternoon trade as European shares rose in early trade and the marketregained positive terrain for a brief period. Volatility ruled the roost as themarket trimmed losses after weakening once again in mid-afternoon trade.The market extended losses in the late trade as food inflation rose and tradersrolled over positions in the derivatives segment from the near-month August2011 series to September 2011 series with Sensex and Nifty closing down by 0.9% and1.0%, respectively. The mid-cap and small cap indices closed downby 0.9% and 0.8%, respectively. Among the front runners, DLF, Tata Motors,Sun Pharma, Bharti Airtel and ONGC gained 1-3% while, Jindal Steel,Jaiprakash Associates, Hero MotoCorp, Infosys and HDFC lost 3-5%. Among

mid-caps, Sujana Towers, Tube investments, Standard Chartered, GTL Infraand Fortis gained 5-7% while, Deccan Chronicle, Ballarpur Industries, BGR Energy, Manappuram Finance and India Cements lost 5-7%.

Markets Today

The trend deciding level for the day is 16,208/4,860 levels. If NIFTY tradesabove this level during the first half-an-hour of trade then we may witness afurther rally up to 16,312–16,478/4,895–4,951 levels. However, if NIFTYtrades below 16,208/4,860 levels for the first half-an-hour of trade then it may correct up to 16,043–15,939/4,804–4,769 levels.

Indices S2 S1 R1 R2

SENSEX 15,939 16,043 16,312 16,478NIFTY 4,769 4,804 4,895 4,951

News Analysis

L&T bags orders worth `797cr Aventis Pharma acquires Universal Medicare

Refer detailed news analysis on the following page

Net Inflows (August 24, 2011)

` cr Purch Sales Net MTD YTD

FII 2,006 2,764 (758) (9,114) (381)

MFs 451 357 94 2,030 5,807

FII Derivatives (August 25, 2011)

` cr Purch Sales NetOpen

Interest

Index Futures 5,103 5,282 (180) 11,183

Stock Futures 7,027 6,645 382 25,587

Gainers / Losers

Gainers Losers

Company Price (`) chg (%) Company Price (`) chg (%)

Idea Cellular 98 5.0 JP Power 33 (8.3)

Colgate Palmolive 964 3.7 Mphasis 368 (7.1)

ABB 8093.5 GMR Infra 27 (6.8)

Lupin 463 3.0 Mannapuram Finance 45 (5.6)

LIC Housing Fin 206 2.9 Lanco Infra 16 (5.4)

Domestic Indices Chg (%) (Pts) (Close)

BSE Sensex (0.9) (138.7) 16,146

Nifty (1.0) (49.3) 4,840

MID CAP (0.9) (54.9) 6,174

SMALL CAP (0.8) (59.0) 7,100

BSE HC 0.3 19.6 5,889

BSE PSU (0.6) (48.8) 7,652

BANKEX (1.4) (149.7) 10,508

AUTO (0.2) (14.7) 8,105

METAL (1.9) (219.3) 11,572

OIL & GAS (0.5) (40.7) 8,289

BSE IT (2.1) (100.0) 4,737

Global Indices Chg (%) (Pts) (Close)

Dow Jones (1.5) (170.9) 11,150

NASDAQ (2.0) (48.1) 2,420

FTSE (1.4) (74.8) 5,131

Nikkei 1.5 132.8 8,772

Hang Seng 1.5 285.7 19,753

Straits Times 1.7 45.8 2,766

Shanghai Com 2.9 74.2 2,615

Indian ADRs Chg (%) (Pts) (Close)

Infosys (3.7) (1.9) $47.7

Wipro (2.0) (0.2) $9.5

ICICI Bank (3.3) (1.2) $35.9

HDFC Bank (3.2) (1.0) $30.4

Advances / Declines BSE NSE

Advances 1,138

Declines 1,638 942

Unchanged 122 58

Volumes (` cr)

BSE 2,438

NSE 13,388

8/4/2019 Market Outlook 26th August 2011

http://slidepdf.com/reader/full/market-outlook-26th-august-2011 2/3

August 26, 2011 2

Market Outlook | India Research

L&T bags orders worth `797cr

Larsen & Toubro’s (L&T) building and factories division has bagged orders aggregating to ` 797cr from one of the leading developers. The order is for mixed use constructioncomprising predominantly of residential, including retail and commercial developments atMumbai. With these order the outstanding order book stands at ~ ` 1.38 trillion (3.1x

FY2011 revenues) providing revenue visibility for next couple of years.

At the CMP of ` 1,547, the stock is trading at 19.4x FY2013E earnings and 3.3x FY2013EP/BV, on a standalone basis. We have used the sum-of-the-parts (SOTP) methodology tovalue the company to capture all its business initiatives and investments/stakes in thedifferent businesses. Ascribing separate values to its parent business on a P/E basis andinvestments in subsidiaries on P/E, P/BV and mcap basis, our target price works out to ` 1,946, which provides 25.8% upside from current levels. We recommend a Buy on thestock and maintain L&T as our top pick in the sector.

Aventis Pharma acquires Universal Medicare

Aventis has acquired Universal Medicare, a nutraceutical formulation company. Accordingto the deal, the products that Aventis Pharma will be acquiring on mutually agreed termsand the manufacturing rights of the company would be retained by the UniversalMedicare. Mumbai-based Universal Medicare manufactures markets and distributesbranded nutraceutical formulations in India through its sales and marketing infrastructure.For the year ended 31 March 2011, the company's turnover of branded nutraceuticalformulations was approximately Rs110cr. The latest acquisition, the company will advanceits sustainable growth strategy in India and facilitate the creation of a consumer healthcareand wellness platform. This move is also synergetic with the growth strategy of Sanofi, amajority stakeholder in Aventis Pharma. The transaction is expected to close by 4QDec’2011. While the details of the deal are not know, we believe that the earnings

would increase by 7%. Thus after factoring in the possible upsides from the deal, the stockwould trade at 21.6xCY2012E earnings, and hence remain Neutral on the stock.

Economic and Political News

Citigroup cuts global, India growth view

Food inflation soars to 9.8% from 9.03%

Government to relax equity dilution norms for insurance firms

India, China enjoy 68% of emerging market PE investment

Corporate News

ONGC looks to drill eight wells in KG gas block

Srei Infra Finance to raise ` 4,600cr infra fund

Tata Power to invest ` 1,000cr to lay cables in Mumbai

Telcos under TRAI scanner for hiking mobile tariffs

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

8/4/2019 Market Outlook 26th August 2011

http://slidepdf.com/reader/full/market-outlook-26th-august-2011 3/3

August 26, 2011 3

Market Outlook | India Research

Research Team Tel: 022-3935 7800 E-mail: [email protected] Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits andrisks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss ordamage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or inconnection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to thelatest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may haveinvestment positions in the stocks recommended in this report.

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

Address: 6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai - 400 093.Tel: (022) 3935 7800

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)Reduce (-5% to 15%) Sell (< -15%)