Embed Size (px)

Citation preview

Market Liquidity, Private Information, and the Cost of Capital:

Microstructure Studies on Family Firms in Japan*

Takashi Ebihara

Faculty of Economics, Musashi University

Keiichi Kubota

Graduate School of Strategic Management, Chuo University

Hitoshi Takehara

Graduate School of Finance, Accounting, and Law, Waseda University

Eri Yokota

Faculty of Business and Commerce, Keio University

October 21, 2012

JEL Classifications: G14, G32, G12, M21 Keywords: information asymmetry, market liquidity, family management, cost of equity, cost of debt *) This paper was presented at the 2012 World Finance Conference held in Rio de Janeiro, the 2012 Nippon Finance Association Annual Meeting in Tokyo, the 1st Workshop on Finance and Accounting Research in the Asia Pacific Region in Nagoya, and the International Conference on Business Groups and Family Business: India, Japan, and Thailand in Delhi. The authors thank Takato Hiraki, Rosy Locorotondo, Vikas Mehrotra, Wataru Ota, Krishnamurthy Subramanian, and Yupana Wiwattanakantang for useful comments and suggestions. The authors also thank Yasuhiro Arikawa, Shigeu Asaba, Tai-Yuan Chen, Joseph Fan, Zhaoyang Gu, Roger King, Matao Miyamoto, David Reeb, Carlo Salvato, Jay Shanken, and Jun Uno for helpful discussion. The authors acknowledge financial support from the Grant-in-Aid for Scientific Research ((A) 21243029) from the Ministry of Education, Culture, Sports, Science and Technology of Japan. All remaining errors are our own.

1

Market Liquidity, Private Information, and the Cost of Capital:

Microstructure Studies on Family Firms in Japan

Abstract

We investigate market liquidity, distribution of private information-based trades, and the

cost of capital of publicly traded family firms in Japan. First, we find that Japanese family

firms have a lower cost of debt, lower market liquidity, and higher information asymmetry.

We did not find any difference in the cost of equity, however, although it is slightly higher

for family firms. Accordingly, the WACC of family firms is higher than that for

non-family firms although it is significant only for the conventional t-test. As for

estimation of information asymmetry and illiquidity, we use the private information flow

(Adjusted PIN) and the symmetric order inflow shock (PSOS). In addition, we estimate

several conventional measures of market liquidity and illiquidity as used in microstructure

studies. We find that the PSOS is a good measure of market illiquidity for our sample of

family firms and control non-family firms. In conclusion, we claim that more voluntary

disclosure is called for among Japanese family firms; first, to decrease the cost of equity,

and second, to increase market liquidity of traded stocks as well as reduce the probability

of private information-based trades. This is the first study to use asymmetric information

related variables in family business research, which is a new contribution to the literature.

2

1. Introduction

In the past, family business research focused on ownership structure and productive

efficiency of founding families, as well as the efficacy of second and later generation CEOs.

Empirical evidence on family businesses is abundant for U.S. firms as well as European

and East Asian countries. Claessens et al. (2000) investigated the ownership and control

structure of East Asian countries, and La Porta, et al. (1999) conducted similar tests for 27

developed nations. The evidence for efficiency of family-controlled businesses in the U.S.

is found by Anderson and Reeb (2003) and Villalonga and Amit (2006), and for Japanese

firms by Saito (2008) and Allouche et al. (2008). Mazzi (2011) also extensively surveys

family business literature from the viewpoint of financial performance of family firms.

Masulis et al. (2011) investigates the cost and benefits of the pyramid structure of 45

countries including Japan, and finds that group firms underperform counterpart non-group

firms, although the pyramid structure helps internal financing of affiliate firms inside the

group. From another perspective, Gomez-Mejia and Nunez-Nickel (2001) investigate the

efficacy of the CEO and the editor, for a sample of both family and non-family firms, of

Spanish newspaper companies. They find that the tenure of descendent CEOs is tied to firm

performance and risk-taking within the framework of agency theory, and demonstrate that

family descendent CEOs are not necessarily less efficient.

For investigation into information quality of accounting numbers, Ali et al. (2007) finds

that a sample of U.S. family firms show better quality financial disclosure, are followed by

more analysts, and trade their stocks with smaller bid-ask spreads. Wang (2006) also finds

that earnings quality is better for family than non-family firms. For Japanese data, Ebihara

3

et al. (2012) finds that the quality of earnings is higher for family firms in terms of

abnormal accruals and earnings persistence.

In this paper we investigate liquidity and the degree of information asymmetry of stocks

in family versus non-family firms listed on the Tokyo Stock Exchange, as well as measure

the cost of capital in the two types of firms to resolve the difference. Note that O’Hara

(2003) argues that the cost of capital will be higher when there is more information

asymmetry in capital markets and less liquidity among traded stocks and this is also why

we investigate the differences in the cost of capital. On the other hand, McConaughy

(1999, pp. 356-357) argues that cost of equity can be lower for family firms due to the

“family effect,” which means that their investment is generally more patient and better-run

with less risk. Accordingly, one of the main objectives of this study is to investigate

whether there is more information asymmetry and lower liquidity among traded stocks of

family firms in Japan at the same time as exploring source of differences in cost of equity,

cost of debt, and WACC.

The foregoing observations lead us to raise our core research questions on the degree of

information asymmetry and liquidity of family firms in Japan, and we investigate these

with the help of a Poisson arrival microstructure model of information as well as the use of

several alternative liquidity measures. Simultaneously, we investigate cost of equity, debt,

and WACC, and associate our findings from microstructure studies with conventional cost

of capital measures.

Section 2 motivates our study and explains the research method we employ. Section 3

establishes the maintained hypotheses. Section 4 explains the estimation method and

4

Section 5 explains our data. Section 6 reports basic characteristics of family businesses in

Japan, market liquidity, information asymmetry of stocks and the estimated cost of capital.

Section 7 reports regression results and identifies the source of differences in the cost of

capital and information asymmetry between family and non-family firms. Section 8

concludes.

2. Motivation and Research Methods

2.1 Family Firms Research and Information Asymmetry

Although there are abundant previous studies investigating cost of equity and debt for

family firms (McConaughty, 1999 and Anderson et al. 2003, among others), the results vary

and are not conclusive. In this paper, we look at the source of the difference in the cost of

capital from the viewpoint of information asymmetry. For that purpose, we employ the

measures developed by Duarte and Young (2009). As far as the authors are aware, only in

Anderson et al. (2009) has an investigation been conducted by utilizing microstructure

studies in financial economics to investigate information asymmetry for family firms with

Japanese data. They also investigated family firm opacity and found that stocks of

heir-controlled firms have higher bid-ask spreads than founder-controlled family firms or

non-family diffuse shareholder firms. However, they did not use the tick-based PIN

measure which we use in this study. Furthermore, Anderson et al. (2012) report that

stocks of family-controlled firms experience higher abnormal short sales, suggesting the

existence of more informed trades. For U.S. firms, this implies there may be more private

information-based trades among family firms.

5

A priori, we expect that there will be higher concentrations of stock held by family

firms which would result in a lower proportion of floating stocks traded. However, how this

affects liquidity and/or information asymmetry of family firm stocks is an empirical

question to be quantitatively measured. For that, we utilize theoretical constructs developed

in the microstructure field of financial economics, in particular, the Adjusted PIN and the

PSOS by Duarte and Young (2009).

Moreover, if we find that family firms stocks are traded with higher information

asymmetry and less liquidity, it will imply a higher cost of equity as Easley and O’Hara

(2004) demonstrated for U.S. data. On the other hand, if we observe that stocks of family

firms are more liquid than non-family firms, and there is less information asymmetry, it will

imply a lower cost of equity. If this is the case, it might be because of a higher level of

voluntary disclosure released by founding family management, whose personal reputation

may be more strongly tied to their company reputation (Bolton and Dewatripont, 2005,

Chapter. 5).

As for cost of debt, note that the larger fraction of debt for Japanese family firms is

bank loans instead of corporate bonds, and it is not a priori clear whether cost of debt is

higher or lower for family firms. It may be lower because the lending banks might have

more confidence in stable management and ownership of family firms, or higher because

lenders might be more concerned with the entrenchment effect caused by founding families

and family or non-family CEOs (Gomez-Mejia and Nunez-Nickel, 2001). The argument

and evidence from U.S. firms is presented by Anderson et al. (2003, p. 267) from the

6

viewpoint of agency cost, claiming that family firms are more concerned with survival and

reputations, and that lenders have more confidence in lending to family firms.

2.2 Family Firms in Japan

Claessens et al. (2000) is the most widely cited article in Asian family business research

which investigated ownership structure among East Asian countries including Japan. They

cover 1240 listed firms in Japan (ibid. p.104) and point out that 13.1% of firms are

controlled by families with a 10% shareholding cutoff level of founding families, and that

only 9.7% of firms are controlled by families with a 20% cutoff level. Their study is also

important in the sense that it illuminates the differences of Japan and Korea relative to other

East Asian countries. In Korea there exists the Chaebol relationship and formerly in Japan

there was the Zaibatsu relationship, both of which form a “Konzern” of firms based on

family relationships. In Japan, however, Zaibatsu was forcefully resolved after World War

II and founding families had to liquidate large portions of their family stocks. Then

Zaibatsu groups formed cross-shareholdings among firms such as Mitsubishi, Mitsui and

Sumitomo. In Korea massive mergers are now occurring among Chaebol firms, and

separate studies of these consolidation effects are needed.1

The database by Claessens et al. (2000) for Japan is based on data from 1996, and it

needs to be updated for the following reasons. First, big changes in ownership structure for

Japanese stocks occurred in the past 15 years and a larger fraction of stocks listed on the

1 L&G is one example of such a consolidation between two different Chaebol groups. See Almeida et al. (2010) for the most recent analyses on Chaebol groups in Korea. They also emphasize the role of cross-shareholdings like in Japan. See Yafeh (2000) for recent changes in corporate governance in Japan after the degree of cross-shareholdings decreased.

7

exchange are currently owned by fund trusts, pension funds, mutual funds and foreign

individual and institutional investors. Second, cross-shareholdings among Japanese firms

have decreased substantially in recent years (Eoyang, 1998). Thus we infer that both the

weight of shareholdings by founding families and the fraction of floating stocks are smaller,

which we attempt to quantify in the current study.

A priori we classify Japanese family firms into three types. The first is small business

that has survived for over 200 years. The majority of these firms is private and is not

publicly traded, such as Toraya, a 16th century pastry producer from Kyoto, as well as many

independent hotels, restaurants, and craft makers. These are not included in our sample.

The second are those in heavy industries, transportation, transportation equipment, or

electric appliances. Most of these firms were started before World War II and Tobu

Railroad, Toyota, and Nakayama Steel are examples. The third are firms in newer high tech

industries, where founding families are still running them (entrepreneurship stage), or are

retired and the second generation is in charge, either a family member or an outsider

(descendent stage). Square-Enix, Omron, and Kyocera are examples. Among these

three types, the latter two are larger firms and most are listed, which is the sample we use

for the current study.

In previous research on Japanese family businesses, Asaba (2012) investigated

investment behavior of the electric machinery industry from 1995-2006 and found that his

sample of 184 family firms demonstrated a more aggressive and enduring investment than

non-family firms. Saito (2008) found that family firms slightly out-performed non-family

firms between 1990 and 1998, and superiority was limited to the founders’ reign. Allouche

8

et al. (2008) found that financial performance of family firms in Japan from 1998-2003, as

measured by accounting ratios, was better than non-family firms. Finally, Mehrotra et al.

(2011) investigated the succession problem of Japanese family businesses and

demonstrated that adopted heirs could avoid the succession problem. They studied firms

between 1949 and 1970 and followed the observation up to 2000.

The current paper adopts a different angle in order to investigate family businesses in

Japan and focuses on liquidity and information asymmetry with the use of measurement

from microstructure studies as well as cost of debt and equity. If we can find any

difference in these variables between family and non-family firms, in particular,

microstructure variables, this evidence would be the first in family business research.

2.3 The Cost of Capital

To estimate cost of equity in this study we use the Fama and French three factor model

(2003). This model is composed of the following factors; value-weight excess market

returns, the size factor spread portfolio (SML), and the book-to-price ratio factor spread

portfolio (HML). The model is denoted as follows: )( mRE is the expected return of

market, )( SMBRE is the expected return of the “small minus big” factor portfolio,

)( HMLRE is the “high book-to-price ratio minus the low book-to-price ratio” factor

portfolio, and fR is the risk-free interest rate. Each beta coefficient in (1) is the

corresponding factor loading for each stock or portfolio.

)()())(()( 321 HMLiSMBifmifi RERERRERRE (1)

9

The reason we use this model to measure cost of equity is because the Fama and French

model better fits Japanese data than the one-factor CAPM (Jagannathan et al., 1998).

For the cost of debt, we use the average past five years of interest paid to total interest

bearing debt. Although Anderson et al. (2003) use the yield-to-bond for U.S. data, the

corporate bond market in Japan is basically an over-the-counter market and a price quote

will be different between investment banks which give offers even if quotes are available.

Also, Kubota and Takehara (2007) use this measure of cost of debt to estimate WACC for

Japanese data.

The estimates for WACC of firms are computed in a standard fashion as the weighted

sum of cost of equity and after-tax cost of debt. We use actual tax rates during the fiscal

year, computed as the ratio of net income after-tax to net income before-tax. The

weightings for cost of equity and cost of debt multiplied by 1 minus effective tax rate are

conducted by the market value of equity and the book value of all interest-bearing debt.

2.4 Measures of Information Asymmetry and Symmetric Order Flow

In her review article, O’Hara (2003) emphasized the importance of exploring the price

discovery process before investigating the equilibrium price of assets in asset pricing theory.

Studies by Easley et al. (1996, 2002) are examples which explored this price discovery

process using tick-by-tick U.S. data. They estimated the so-called “PIN” variable, which is

a variable related to the probability of information-based trades among all trades, based on

the Poisson process of private information arrival. For example, Duarte et al. (2008), utilize

this PIN variable to assess the impact of Regulation Fair Disclosure for U.S. firms. They

10

use the PIN variable as a proxy to measure the degree of information asymmetry and find

that Regulation Fair Disclosure affects the cost of capital using the PIN along with other

control variables. In Duarte et al. (2008) the estimated PIN and other variables are used as

independent variables to predict changes in the cost of capital of firms after Regulation FD

was introduced in 2000. Their main finding was that NASDAQ firms were more strongly

affected and costs of capital for these firms increased, suggesting that smaller firms bear

more increased costs due to the new disclosure rule. Kubota and Takehara (2009) estimated

PIN values for Tokyo Stock Exchange firms and reported that parameter values for Japan

were comparable to U.S. ones originally estimated by Easley et al. (2002).

In Easley’s original model there are three types of market participants: market makers,

informed traders, and uninformed traders. Other markets in the rest of the world, however,

are usually not equipped with market makers, and an electronically-driven order market

system is the dominant form of trading. Based on comparable parameter estimates derived

from Tokyo Stock Exchange firms by Kubota and Takehara (2009) and Paris Bourse firms

by Aktas et al. (2003), we directly apply the PIN and Adjusted PIN estimation methods to

the electronically-driven order market of the TSE and investigate the relative weight of

private and public information trades.2

Based on the original model by Easley et al. (2002), Duarte and Young (2009) further

extend the original PIN model to disentangle measures of private information-based trades,

2 We thank Maureen O’Hara for discussing this point. Kubota and Takehara (2009, p. 321) discuss why limit orders can play the role of market makers for Tokyo Stock Exchange data. When Foucault (1999) analyzes the nature of dynamic limit order markets, he refers to the Tokyo Stock Exchange as a representative market of this kind. Moreover, Back and Baruch (2004) prove the equivalence of the floor market and the market with market makers under suitable regularity conditions.

11

which they call Adjusted PIN, and the unconditional probability of trade occurrences

arising from symmetric order flow shocks, which hit both buy and sell orders at the same

time. These are two measures we use for our study. They call this latter variable PSOS, the

probability of symmetric order flow shocks. According to Duarte and Young (2009, p. 126)

this measure comes about from “occurrence of a public news event about whose

implications traders disagree,” and/or “that traders simply coordinate on certain days to

reduce trading costs.” In our investigation of family firms in Japan, we use Duarte and

Young’s version of the PIN, the so-called Adjusted PIN and the PSOS, and test our

hypotheses. We employ this version of the information asymmetry variable because Kubota

et al. (2012) found that the Duarte and Young version of the PIN model can well describe

the behavior of recent Japanese stock return data.

In the original model by Easley et al. (2002) there are two types of risk-neutral traders in

the market: informed and uninformed traders. First, nature chooses once each day whether

there is a new private information event with probability a , or not, with probability )1( a .

The orders arrive according to the Poisson process and uninformed traders send orders with

a buying order rate of b and a selling order rate of s . The probability of being a good

signal is denoted as d and the probability of being a negative signal is 1-d. While the

extra order arrival rate by the informed trader is the same for both good and bad signals,

Duarte and Young (2009) extend this stochastic process, where the buy rate is denoted as

bu and the sell rate su . They further introduce the parameter θ which is a probability of a

symmetric order flow shock event occurring. The extra order rate based on the occurrences

12

of this symmetric order flow shock is b or s dependent on whether it is a good or bad

signal.

Assuming each day’s independent drawing is from the Poisson process and thus the

likelihood function is represented by the product of each day’s likelihood function, we can

numerically maximize this function using daily observations of the number of buyer and

seller-initiated transactions. Based on these parameter estimates, the Adjusted PIN and

PSOS variables are derived from Bayes’s rule, as follows:

sbsbsb

sb

dd

ddPINAdjusted

)())1((

))1((( (2)

sbsbsb

sb

ddPSOS

)())1((

)( (3)

Both variables represent the ex post probability that trades are triggered by private

information among all tick-by-tick trades for (2) and that trades are triggered by symmetric

order flow shocks for (3). In (2), the numerator denotes the joint probability of orders

composed of information-based order arrival rate times the occurrence of the information

event and the denominator is the total joint probability of trades. Similarly in (3), the

numerator denotes the joint probability of orders composed of those orders triggered by

symmetric order flow shocks and the denominator is the total joint probability of trades.

3. Hypotheses

13

Family firms are generally expected to have a management team congruent with the

family norm, whether the CEO is from the family or not. Thus, we expect that inside the

firm the management team possesses stronger real authority by the definition of Aghion and

Tirole (1997). Family firms may also suffer less from agency cost problems that arise

between managers and share owners (Jensen and Meckling, 1976) either because a large

fraction of shares are owned by founding families, or the CEO has real authority emanating

from the family owner. Thus these elements will lead to higher firm efficiency with less

agency cost.

As for the quality of disclosure, when the reputation of a company is strongly tied to the

reputation of the family, management may be strongly motivated to disclose that their

company is indeed a good one. On the other hand, when blocks of stock are owned by

family members but ownership is not large enough to have family reputation strongly tied

to a higher stock price, they may be less motivated to voluntary disclose the state of the

firm to minority shareholders, and will only stick to the minimum level of disclosure.

Then there will be more information asymmetry in stock trading.

Our primary research interests are the effect of family ownership structure and the role

played by family members in financial management decisions; that is, the operating and

financial risk of the firm as revealed in cost of capital estimates and the degree of private

information trade and liquidity in their stock trading.

For information asymmetry, traders on every trading day cannot be denied, even if we

accept the notion that the efficient market hypothesis eventually holds its existence. 3 For

3 We thank George Constantinides for discussing this point.

14

U.S. data, Easley et al. (1996, 2002) estimate parameter values of the probability of private

information-based trades for each trading day by using tick-by-tick quote and transaction

data, and report that about 20 percent of daily trading is based on private information.

Similarly, Kubota and Takehara (2009) report comparable estimates for Japanese data using

tick-by-tick data. These estimated values support our initial belief that there exists

information asymmetry in everyday trading of U.S. and Japanese stock markets.4

In this paper we use the adjusted PIN variable by Duarte and Young (2009) to

disentangle

the information asymmetry measure, the Adjusted PIN, and the illiquidity measure of firm

stocks’ PSOS to investigate family firm data. We can control for general information flow

shocks coming into the stock price and can pinpoint the degree of information asymmetry

between informed and uninformed trades.5 Moreover, the variable PSOS can identify

illiquidity of the stock. In addition, we estimate several alternative measures of liquidity

used in conventional financial research, which we will formally introduce in Section 4.2

because the PSOS is a rather new concept and the behavior of this variable is less known.

Next, when the degree of information asymmetry is higher, cost of equity will be higher

(O’Hara 1996).6 The motivation to voluntarily disclose may come from management’s

desire to signal to capital market participants that their firm should be classified as a good 4 In Holden and Subrahmanyam (1992) private information is revealed immediately when the trading interval approaches zero in their microstructure model, but empirical results for U.S. and Japanese stock markets indicate that is not the case for every trading day. 5 Anderson et al. (2009) distinguish between internal component (founder, heir or firm) in their family business research, and an external component (market) to assess the degree of opacity of firms. The former is more related to information asymmetry and the latter to market liquidity according to our interpretation. 6 Whether there is significant difference, however, depends on the degree of competitiveness of the stock market according to the recent theoretical model of Lambert et al. (2012).

15

one within the framework of signaling theory. Bolton and Dewatripont (2006, p. 24), for

example, state that “One of the main ideas emerging from the analysis of contracting

problems with private but verifiable information is that incentives for voluntary disclosure

can be very powerful.” If that were the case, there would be a group of firms which disclose

voluntarily, and another group which do not, and consequently a separating equilibrium will

hold.

Hence, our main research agenda is the quality of information dissemination and

consequent differences in the cost of capital between family and non-family firms, and we

construct the following six hypotheses, H1 to H6, and an accompanying corollary.

First, if private information shared by family members is revealed to a lesser extent to

capital market participants, we expect that private information-based trades have heavier

weight, and accordingly, cost of equity for family firms will be higher than non-family

firms (Easley and O’Hara, 2004). For non-family public firms we expect that the

diversified management team may talk more openly about their management strategies to

analysts and the media, while managers of family firms may show less opaqueness of

strategies shared solely among family members. The evidence by Anderson et al. (2009)

confirms this point for a recent large sample of U. S. data and finds that family firms are

more opaque than non-family firms.

Second, outside lenders who have more personal ties with founding families may have

more confidence in the reliability of family management. If the proportion of shares held

among family members is high, lenders will consider that management is more concerned

with firm value maximization, and hence have less chance of defaulting. Moreover, even if

16

the proportion of family-held shares is low, the descendent management team may have

inherited the management style from the founder, and may still share close personal

relationships.7 Thus, we expect the cost of debt, mainly bank loans for Japanese firms, will

be lower for family than non-family firms.

It is not clear how this will affect the overall weighted average cost of capital (WACC)

of family firms. It is widely known that the Japanese corporate tax is one of the highest in

the world next to the U.S., with an effective statutory tax rate of 40.87%. The use of tax

shields helps reduce WACC values. However, we infer that family firms will be less open

to outside borrowing because a family does not lose control of the firm to banks. For

example, the high WACC for family firms in Japan due to the non-use of debt can be seen

in the Toyota Motor Co., where the WACC value is as high as 8%.8

How family-controlled firms perform financing decisions following the pecking order

theory by Myers (1977) is another question, although it is outside the scope of this research.

If family businesses tend not to borrow, the WACC will be higher, but if they borrow more

because of their financial constraints, it will be lower, ceteris paribus the level of cost of

equity of our compared firms.

With these considerations we state our first three hypotheses regarding the cost of

capital.

7 These arguments probably apply more to regional banks than to megabanks in Japan. When we had a chance to interview Wacoal Holdings Corp., we asked about their relationship with the Bank of Kyoto and confirmed this point. Note that Wacoal Holding Corp. has little debt, while the firm highly values of their relationship with the Bank of Kyoto, and vice versa. 8 Toyota Motor Co. is now classified as a family business, according to our definition, after a family member took over as CEO in June 2010.

17

H1: Family-controlled firms have a higher cost of equity than non-family firms.

H2: Family-controlled firms have a lower cost of debt than non-family firms.

H3: In view of H1 and H2, there is no difference in weighted average cost of capital

between family-controlled and non-family firms.

Next, in order to explain the above three hypotheses, we formulate three additional

hypotheses and collect microstructure evidence to test them. In particular, we explore how

disclosure decisions adopted by family firms and the attention paid by outside analysts and

investors affect the degrees of information asymmetry, and thus, to what extent private

information is impounded into stock prices. Accordingly, our question is whether there is

any difference or similarity with that regard between family and non-family firms. To

answer these queries, we first state two hypotheses:

H4: Stocks of family-controlled firms are traded with a higher probability of symmetric

order flow shocks than non-family firms.

H5: Stocks of family-controlled firms are traded with a higher degree of information

asymmetry than non-family firms

Furthermore, we claim that degrees of information asymmetry and stock liquidity are

entangled in the above framework because the existence of information asymmetry implies

that there is wider disagreement among traders about the true quality of the firm, which

18

may then produce wider bid-ask spreads of limit price orders. Our PSOS variable can

purportedly extract the symmetric order flow shocks apart from information asymmetry, the

Adjusted PIN, and we expect that this PSOS variable contains separate illiquidity-related

information of stock trading. Note that Duarte and Young (2009) claim that the probability

of symmetric order flows can measure the illiquidity of stock. Thus, in H6 we investigate

the liquidity of stock trading, simultaneously utilizing other alternative measures of

liquidity as formally defined in Section 4.2 below. Note that H4 forms a subset of the

hypothesis H6.

H6: Stocks of family-controlled firms are traded with less liquidity than stocks of

non-family firms.

Finally, we set forth the final reasoning on the condition that H5 and H6, as well as H4,

are supported with data from our microstructure evidence. If these observations are indeed

true, we will have succeeded in explaining one of the reasons why H1 holds. Moreover,

H2 holds when lenders are in the position of insiders relative to outside stock investors and

give more generous lending terms to family firms. Thus, we state this as an empirical

proposition.

Proposition: If both hypotheses H5 and H6 hold, we infer that the illiquidity of stock and

information asymmetry cause hypotheses H1 and H2 to hold.

19

In order to compare this PSOS variable with other liquidity-related variables to test H5,

we compute Amihud’s (2002) illiquidity measure, Liu’s (2004) zero-trading volume day

measure, the marginal transaction costs estimated by the LDV model of Lesmond et al.

(1999 ), the standard turnover ratio, and bid-ask spreads as defined in Section 4.2.

4. Estimation Methods Used

4.1 Adjusted PIN and PSOS

We use tick-by-tick quotes and transaction records for all traded stocks, and classify each

transaction as either a buyer or seller-initiated transaction without ambiguity using the

following method.9 That is, all previous and current maximum bid-price and minimum

ask-price are recorded in our dataset, and based on these quotes we classify all transactions

as either buyer or seller-initiated depending on whether each transaction price is determined

above or below the mid-point of the most recent bid-ask price. We impose further

conditions that at least 180 days of trading data are available to compute the Adjusted PIN

annually for each firm using tick data from July 2007 to June 2010. To make sure the

publicly available data is available for trading investors, we estimate these variables with

transaction data from July 1st after financial data becomes publicly available by the end of

June for our March fiscal year-end firm sample.

To estimate the parameter vector with tick-by-tick data we numerically maximize the

product of likelihood functions with exterior penalty functions for inequality constraints

9 We do not have to use the conventional “tick test” which is the case for markets with specialists.

20

using a standard computing procedure and choose estimated parameter values from the

largest maximum likelihood function out of 10 optimizations for each firm and each year.10

4.2 Alternative Liquidity Measures

To construct alternative liquidity measures, we use three measures as well as turnover

ratio, average bid-ask spreads and average effective spreads. One measure is illiquidity,

ILLIQ, devised by Amihud (2002) as shown in (4), one is the zero-trading volume day

measure by Liu (2004), and the last is marginal cost for trades, estimated using the limited

dependent variable (LDV) model by Lesmond et al. (1999).

The “illiquidity” measure proposed by Amihud (2002) is defined as the average ratio of

the daily absolute return to trading volume on that day. Let Dj,t denote number of days in

which trading volume of firm j is strictly positive, rj,d,t denote daily return of stock, and vj,d,t

denote trading volume in million yen. Then, ILLIQj,t, Amihud’s illiquidity measure for firm

j in year t is defined as follows.

tjD

d tdj

tdj

tjtj

r

DILLIQ

,

1 ,,

,,

,,

||1

(4)

This measure is widely used in asset pricing theory tests in financial economics, such as

Avramov et al. (2006) for U.S. data, and Kubota et al. (2012) for Japanese data.

The zero-trading day measure proposed by Liu (2006) is constructed as follows. Let

ZeroTDj,t, be the number of days on which there were no trades for security j in the past 12

10 We estimate the parameters by using the function "min_uncon_mulvar" in the IMSL CMATH Library. This function uses a quasi-Newton method to minimize the multivariate function and details of our algorithm are explained in Dennis and Schnabel (1983).

21

months t. Let NoTDj,t be the number of trading days in the past 12 months. Then the

zero-trading day measure, LM12, is defined as follows.

M

TurnZeroTD

NoTDLM tj

tj

tj

tj

,

,

,

,

/112211 (5)

where M is the constant large enough to satisfy the following inequality.

1/)/1(0 , MTurn tj (6)

The marginal transaction cost estimation method developed by Lesmond et al. (1999) is

the method to use the limited dependent variable model, which assumes that the real return

r*j,d,t after subtracting the transaction cost satisfies the following unconditional CAPM (7)

with respect to benchmark return, rM,d,t, Their estimation method tries to compute both the

marginal costs to buy and sell the security at the same time estimating the beta and

volatility by the maximum likelihood method.

tdjtdftdMjtdftdj rrrr ,,,,,,,,*

,, )( (7)

Finally, as candidates for other liquidity-related measures, in addition to standard

turnover ratios, we use conventional bid-ask spreads and the effective spread, which is an

absolute value of the difference between transaction price and the mid-point of bid and ask

price, all measured in basis points.

These are the measures we use as proxies for stock liquidity and to compare with the

symmetric order flow: the PSOS variable (which measures the illiquidity of the stock

separately from Adjusted PIN) and the degree of information asymmetry constructed by

Duarte and Young (2009).

5. Data

22

Ownership and CEO data to identify family firms was extracted predominantly from the

Major Shareholders Database and Directors’ Database (from Toyo Keizai, Inc.) while

financial statement and stock price data was extracted from the Nikkei NEEDS Financial

Quest Database published by Nikkei Digital Media, Inc.

We construct our database for the current study as follows. Based on surveys by Toyo

Keizai Shinpousha we have data for the largest 30 stockholders and detailed descriptions of

board members, including the CEO and chairperson with endowed executive authority.

Simultaneously, we use data from our questionnaire responses explained below as well as

old company handbooks by Toyo Keizai to identify founding family members. To

confirm family names and kinship, in 2009 we sent a questionnaire to all 3527 listed firms

to collect family ownership and management information. In total, 406 listed firms

responded.1112 For firms who did not respond, corporate histories and Toyo Keizai’s Top 30

Major Shareholders List were examined to identify ownership and management

information.

Based on data from March 2007, 2008, and 2009 we constructed a database for family

businesses based on two criteria: the founding family owns more than 10% of equity

shares; and the CEO, president, or chairperson is from the founding family, which we call

“CEO criterion,” for brevity. The former 10% criteria is used in Asaba (2012) and Mehrotra

et al. (2010) for reasons that, in Japan, the inheritance tax is quite hefty at over 50%,

leading to the dilution of family-owned shares, and main banks tend to hold stable shares of

11 The response rate of the questionnaire was 11.5%, which is close to the average rate of or higher than normal response rates for questionnaires to Japanese companies. 12 Financial firms were excluded due to the fundamental differences in their financial reporting structure.

23

lending partners as well as investment trusts related to those bank groups.13 In this paper

we want a continuous explanatory variable for cross-sectional regressions, and thus we use

a continuum of shareholding ratios at the estimation stage. The second criterion, “CEO

criterion,” implies the management authority is still in the hands of the founding family

either as a CEO or board chair. In this study we dichotomously classify family-controlled

and non-family-controlled firms with the 10 % holding and CEO criterion.14

The particular sample for this microstructure study is firms listed on the first and second

sections of the Tokyo Stock Exchange as of March 2007, 2008 and 2009, and we use

individual financial statements to find original shareholders’ holdings.15 To estimate the

PIN variable we use tick-by-tick quote and transaction data provided by Nikkei Media

Marketing Co., Ltd. For financial data, the source is again Nikkei Media Marketing.

Two control variables we use are lnMV, which is a natural logarithm of market value of

equity (in million yen), and B/M, which is the book-to-market ratio of the firm in percent.

These financial attributes of the firm, lnMV and B/M, are computed from the Nikkei

Portfolio-Master Database. Cost of equity is estimated from the aforementioned

unconditional Fama and French three factor model of equation (1).

We do not include in our sample firms which PIN and Adjusted PIN could not be

computed numerically, which accounts for less than 12 percent of the total sample. Thus

our total observations are 4303 firm-years. Also note that we have not included financial

13 Another country with a hefty inheritance tax rate was Taiwan, but is no longer the case. 14 Thus, our classification scheme is somewhat different from the one used by Allouche et al. (2008) for Japanese firms and similar to the one used by Saito (2008). We plan to test robustness between these two criteria in an extension of the current research. 15 Although in Japan, family firms in general have many subsidiaries and related companies, the pyramid structure is not so common, and, accordingly, we focus only on parent companies.

24

firms because we use cost-of-capital estimates, which cannot be unambiguously defined for

these firms.

6. Basic Observations

6.1 Basic Statistics

We explore the information dissemination process of our sample of family firms

through daily stock trading data. These firms disclose compulsory financial statements as

publicly-listed firms, conduct voluntary PR activities, and most often solicit their own CSR

activities on their web pages. 16 We claim that the Adjusted PIN and PSOS can

quantitatively identify degrees of information asymmetry as well as stock liquidity. We

suspect substantial shareholdings by families with less floating stocks will affect both

information asymmetry and stock liquidity, which will in turn affect the level of the cost of

capital.

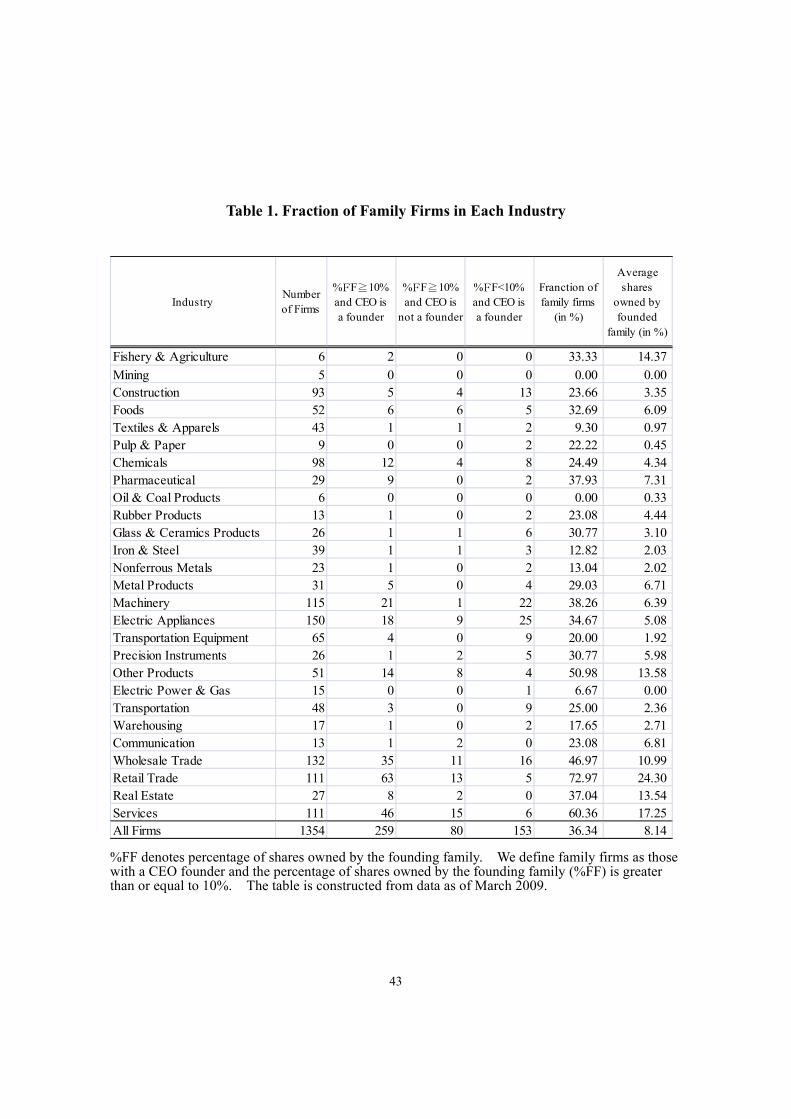

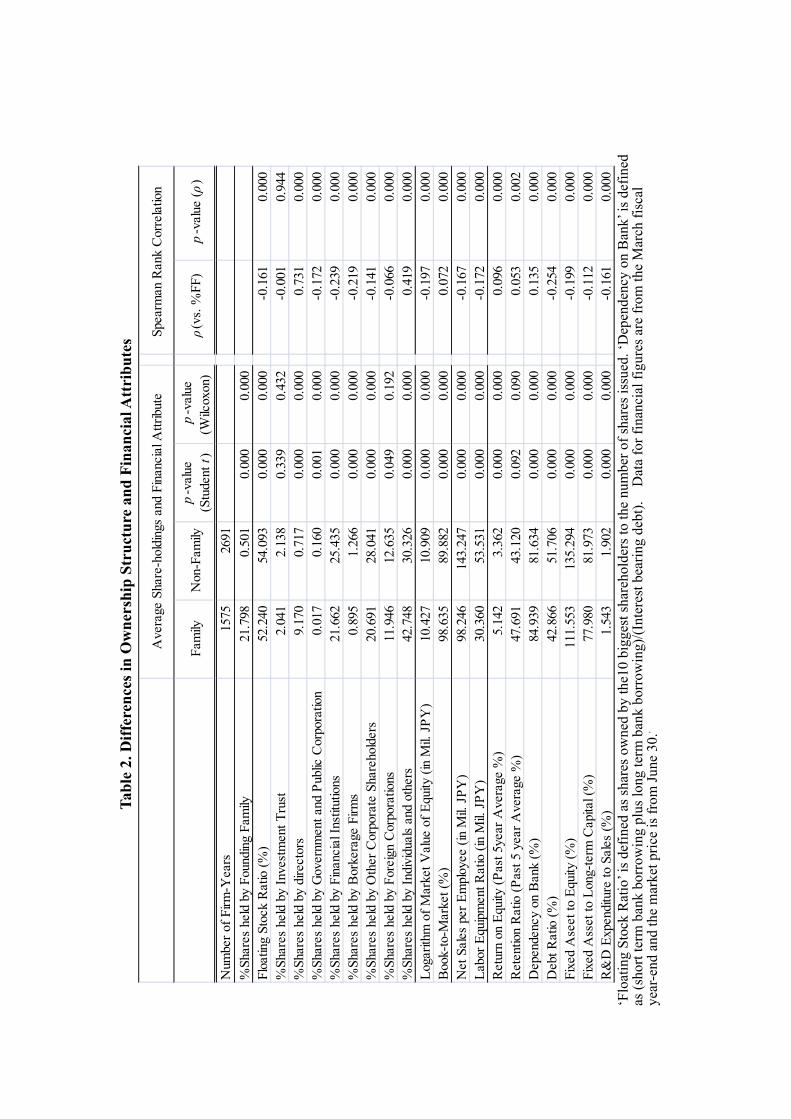

We present the basic statistics in Tables 1 and 2. Table 1 identifies the weight of family

businesses in Japan among Tokyo Stock Exchange listed firms.

TABLE 1 ABOUT HERE

The first column is the number of total sample firms, for which the Adjusted PIN and PSOS

could be computed with suitable convergence criteria. The number of firm samples as of

March 2009 is 1354. In the first column the number of firms for each industry is listed. In

the second column we report the number of firms where the ratio of shareholding by the 16 The level of CSR activities conducted by family firms in Japan is investigated in Aoi, et al. (2012).

25

founding family exceeds 10% and either the CEO, president, or chairperson is from the

founding family; the second row is the number of firms, for which only the first criterion of

10% shareholdings is satisfied; and the third column is where only the second CEO

criterion is satisfied.17 The fourth column computes the percentage of family firms when at

least one of the three criteria is met, and the fifth column reports average shares owned by

families whose companies are classified as family firms in the fourth column.

From the table we find that 36.34% of our sample firms are classified as family firms

and average shareholdings are 8.14%. The percent of firms is higher for Retail Trade with

72.97%, Services with 60.36%, and Other Products with 50.98%. The lowest are Mining

and Oil and Coal Products with 0%, meaning there are no family firms in these industries.

The rankings of average shareholdings are also the same with the percentage of the number

of family firms for each industry.

The average percent of 36.34% is comparable to that reported by Anderson and Reeb

(2003) for U.S. firms. Note that these two economies distinguish themselves as a

developed economy where there is more separation of management and ownership, and yet

we find one-third of the listed firms in both countries are family businesses.18

Table 2 reports ownership distributions and basic firm characteristics of our sample

firms. We show the result both for family firms (second column) and for non-family firms

17 We use the 10% criteria based on findings by Asaba (2012) where there were not significant differences using either the 10% or 20% criteria for Japanese family firms in the electronics industry. 18 It has been said that the majority of firms in other Eastern Asian countries are family firms (Morck et al., 2005). Also, the percentage of shares held by families is larger in European countries, and the 30% or 50% shareholdings criteria is oftentimes used to distinguish family firms in these countries in family business research.

26

(third column). The fourth and fifth columns report p-values of the significance of

differences by the Welch test and the Wilcoxon rank test, and the sixth column reports the

Spearman rank correlation between the ranking of each variable and the percentage of

shares owned by founding families. The total sample is 4261 where three years of pooled

observations from 2007 through 2009 are used.

TABLE 2 ABOUT HERE

In the third row from the top we report the percentage of overall floating stocks and find

that it is significantly lower for family firms with a ratio of 52% vs. 54% for both

significance tests. By “floating stocks” we mean the fraction not owned by the largest top

10 shareholders.19 The differences in shares owned by investment trusts are not significant,

but other fractions of owned shares are, at the 1% level. In particular, for shares held by

directors, individuals, and others, family firms show significantly higher figures than

non-family firms, which is quite an intuitive result. Even though a fraction of stocks owned

by institutional investors dramatically increased over the past 15 years, we find that a

substantial portion of family firm stock is still owned by individuals and/or family members.

Thus, we expect that the alignment between shareholders and management will be closer,

more so by judging from the portion owned by directors, whose major shares must belong

to founding families because the number of shares held by executives is much lower in

Japan than the U.S. The result of foreign corporation ownership is interesting but not 19 Our data is based on the top 30 shareholders and examination of shareholders 21 to 30 reveal that the top 10 are quite fixed overall and so our proxy measure is a good variable to assess actively traded stocks.

27

significant with the Wilcoxon rank test, which we rely on due to the possible non-normality

of empirical distributions.20 For listed firms in Korea, Oh and Chang (2011) find that

foreign ownership has significant and positive influences on firms’ CSR activities, in

particular, among Chaebol firms. Based on our results for Japan, however, we are able to

safely ignore the influence of foreign corporate ownership on listed family versus

non-family firms because the difference is not significant.

Note that in Table 1 the size of family firms (10.427 in log of million yen) was

significantly smaller than that of non-family firms (10.909 in log of million yen). Family

firms make up more of the value firms according to the book-to-market ratio where those

ratios are higher. In our sample the net sales per employee and labor equipment ratio as

measured by the ratio of tangible assets to number of workers are all significantly smaller

for family firms.

From the seventh row from the bottom we report financial characteristics of firms. From

the top, we find that the ROE, which is computed as a five-year average for each firm, is

significantly higher for family than non-family firms with 5.142% and 3.362%,

respectively.21 In terms of the ROE, which measures the ultimate return to shareholders for

founding families, it seems that family businesses are serving their ultimate purpose. Also,

Japanese family firms retain a larger fraction of earnings, which may show stronger

pecking order behavior. The reason may be that families do not want to lose control of their

firms to lenders and outside shareholders.

20 We thank Jay Shanken for discussion on this point. 21 Recently, Reinking et al. (2011) reported that family firms show a lower ROE than non-family firms with U.S. data.

28

When we look at borrowing-related variables, we find that family firms are more

dependent on banks among debt, while the debt ratio, debt-to-total assets, is much lower

than non-family firms with 42.866% to 51.706%, respectively. These differences are all

significant.

In terms of investment in fixed assets, however, family firms are more lightly equipped

judging from the figures of fixed assets to equity and long-term capital. It may be due to

particular industry distributions between the two types of firms. Note we report that there

are more family firms in services, retail, and other products industries. As for R&D

expenditures, we find that family firms invest less than non-family ones (1.543% vs.

1.902%), but, again, it may be due to distributions of family business industries. Note that

Asaba (2012), in his electronic industry sample, finds that family firms have a tendency not

to decrease investment during recessions and keep a patient investment level.

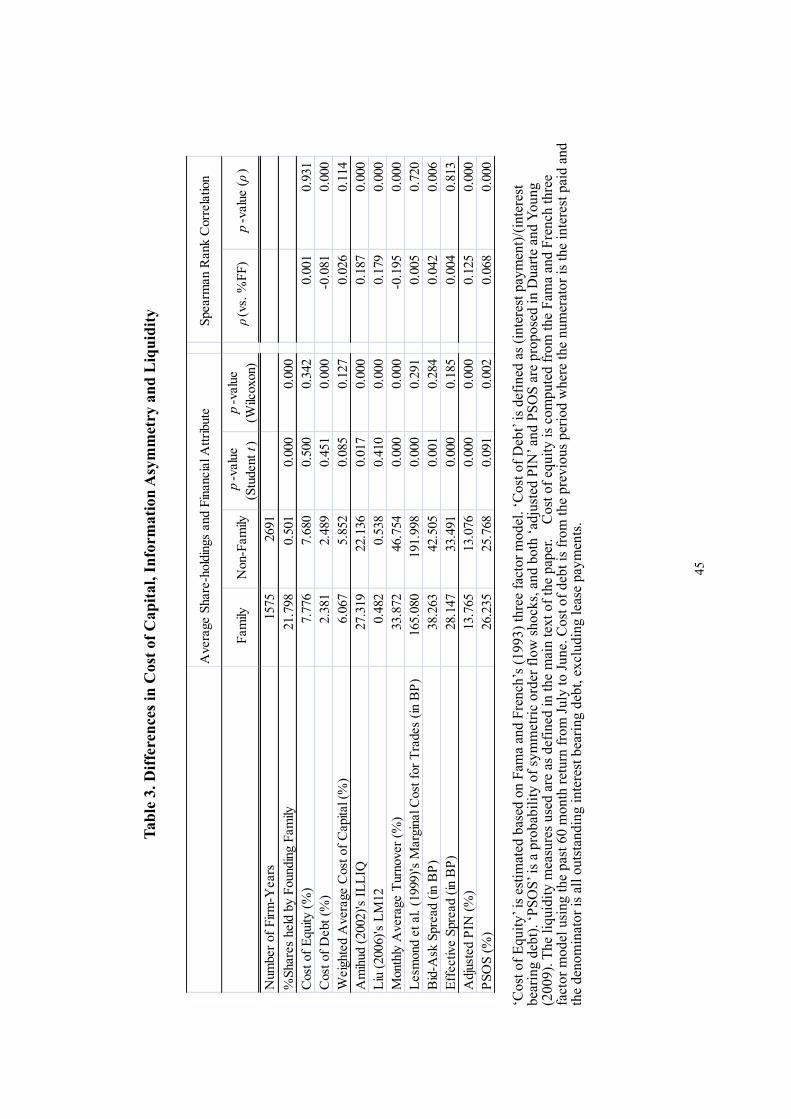

6.2 Cost of Capital Estimates

Table 3 reports the main results on cost of capital estimation and selected liquidity

measures. The first column is for family firms, the second for non-family firms and the

third and fourth columns report p-values for significance of differences. The fifth column

shows the Spearman rank correlation between reported variables and the fraction of shares

owned by family firms. The sixth column reports its significance.

TABLE 3 ABOUT HERE

29

We find that the cost of equity is higher for family businesses (7.776% vs. 7.680%), but

not significant. The correlation with fraction of shares owned by founding families is

positive, but not significant. Accordingly, we cannot conclude whether the cost of capital is

higher for family than non-family firms. So, hypothesis H1 was not confirmed at this stage.

Because our sample is all listed firms, we can safely assume that the asset pricing model

can be applied to these firms, and thus, the result indicates that cash flow of family firms is

not significantly lower than non-family firms. This is contrary to the view raised in

previous literature like McConaughy (1999, p.356), who claim that the benefits of “family

effects,” arising from dedication of families may lower the cost of equity.

As for cost of debt, which is computed from data of all interest bearing debt in the

previous fiscal year, it is lower for family versus non-family businesses (2.381% vs.

2.489%), and the differences are significant for the Wilcoxon test, which we rely on more

because of the possible non-normality of empirical distributions. Moreover, the correlation

between cost of debt and fraction of shares owned by founding families is negative at

-0.081 and significant. In Table 2 we reported that family firms borrow mainly from banks

and the result complements the initial story that lenders have more confidence in some

family firms and require lower interest rates. Consequently, we support hypothesis H2 and

in the next section will try to obtain further confirmation from the cross-sectional

regression. Note our finding for Japan is on par with findings for the U.S. by Anderson et al.

(2003), except they use yield spread and we use the interest paid variable.

Given cost of equity and cost of debt we find that the WACC is slightly higher for

family versus non-family firms (6.067% vs. 5.852%). However, the result is only

30

significant with the conventional t-test with a 10% significance level, and it is not

significant with the Wilcoxon test. In Table 2 we reported that the debt ratio is significantly

lower for family firms. With a high 40.87% statutory corporate tax rate for Japan applicable

to large and profitable listed firms of our sample,22 less use of debt by family firms will

force them to sacrifice the interest tax shield, which may be one reason why WACC is not

significantly different between family and non-family firms, although cost of debt is lower

for family firms and cost of equity is not significantly different. Considering that good

firms in the U.S. are in general less leveraged (Graham, 2000), and also in Japan (Kubota

and Takehara, 2007), family firms may be adopting a strategy of utilizing less debt for

signaling purposes. Thus, we do not reject hypothesis H3.

6.3 Estimates of Information Asymmetry and Liquidity Measures

In the next six rows of Table 3 we report estimation results of several liquidity

measures as explained in Section 3.2. We find the Amihud (2002) illiquidity measure is

significantly higher for family firms with 27.319 vs. 22.136, and the correlation with the

fraction of shares held is positive and significant. Also, in the case of Liu’s (2006) liquidity

measure LM12, liquidity is higher for non-family than family firms and significant.

Moreover, the correlation is significantly positive and does not coincide with the result for

the Amihud measure. Monthly turnover is significantly higher for non-family firm stocks

and the correlation is also significantly positive, which coincides with the result for the

Amihud measure.

22 Kubota and Takehara (2007) report profitable firms are paying corporate tax at the rate close to the statutory tax rate.

31

The other three measures are all insignificant with the Wilcoxon test. As far as

inequality is concerned, in the case of the marginal transaction cost measure by Lesmond et

al. (1999), estimated costs are higher for non-family firms, while the correlation is positive

though not significant. As for the bid-ask and effective spreads, they are lower for family

than non-family firms. However, we find the correlation between the bid-ask spread and the

fractions of shares owned by families is positive and significant.

Overall, in spite of some conflicting results among alternative liquidity measures, we

conclude that family firm stocks are less liquid than non-family stocks. We decided to put

more weight on the result from Amihud’s illiquidity measure because it is one of the most

extensively used measures as a proxy for liquidity in the financial economics literature. We

conclude that hypothesis H6 holds.

Finally, we report the results for the Adjusted PIN and the PSOS. As for the Adjusted

PIN, we find that the probability of private information is significantly higher for family

firms with 13.765% vs. 13.076 % for non-family firms, and moreover, the correlation is

significantly positive. The same is true for the PSOS where family firms report a

significantly higher percentage of symmetric order inflow than non-family firms at a 5%

significance level for the Wilcoxon test. The correlation number also supports this result.

Thus, the evidence supports hypotheses H4, H5, and H6. However, as we mentioned

earlier, H1 was not conclusive, and so we could not find the direct channel from H5 and H6

to H1 and cannot confirm the plausibility of the corollary. Overall, we conclude that stocks

of family firms are less liquid with a higher probability of private information-based trades

with our initial univariate difference tests.

32

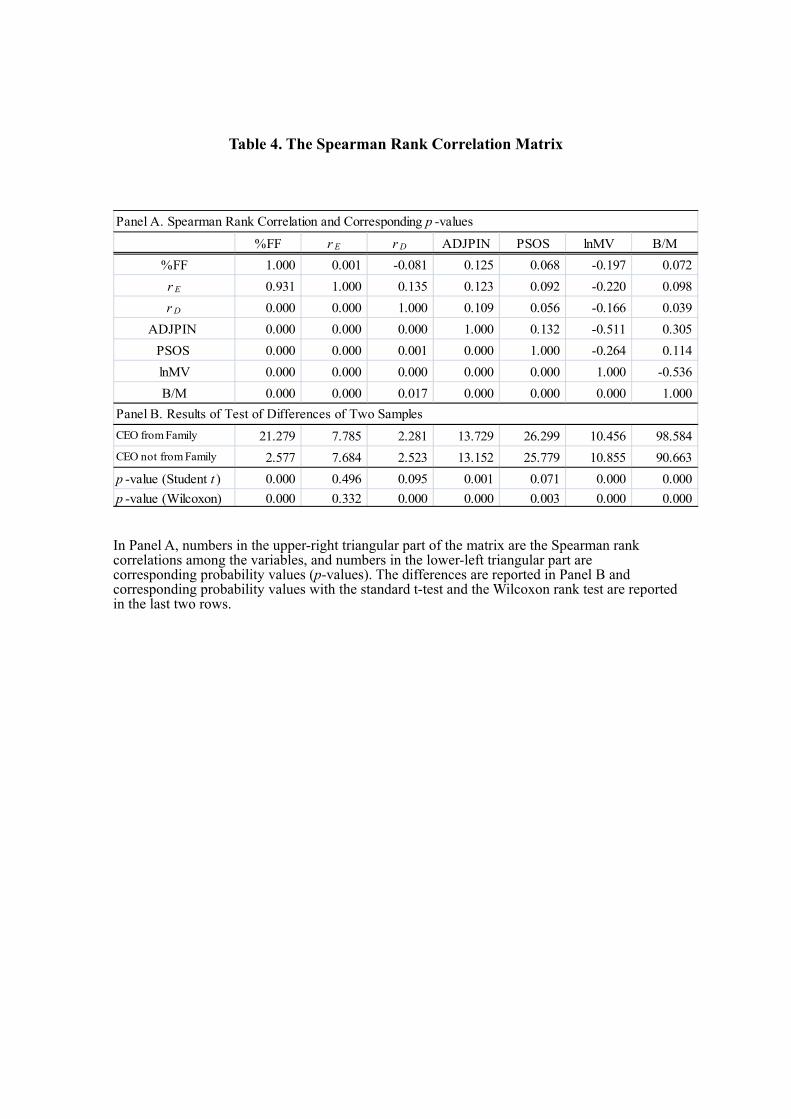

6.4 Correlations of Family-Related Characteristic Variables

Panel A of Table 4 reports the correlations of selected variables, the percent of shares

held by families, cost of equity, cost of debt, Adjusted PIN, PSOS, size, and book-to-market

ratios. The matrix contains Spearman rank correlation numbers in the upper right diagonal

and corresponding p-values in the lower left.

TABLE 4 ABOUT HERE

As for correlations between percent of shares held by families and other variables, the cost

of equity is insignificant, but cost of debt is significant with -0.081, which was reported in

Table 2. The results with the Adjusted PIN and PSOS are positive and significant, as shown

in Table 3. Moreover, cost of equity and the Adjusted PIN and PSOS are all positive and

significant.

In conjunction with the prediction by O’Hara (2000) and Easley and O’Hara (2004)

higher asymmetric information will cause the cost of capital to be higher. The correlation of

cost of equity and debt with size is negative and significant and shows that larger firms

have smaller risk premium ceteris paribus. Also, we find the existence of so-called value

effects found among depressed firms, that value firms have a higher cost of equity and cost

of debt.

In Panel B of the table we report the additional result for Welch’s t test by dichotomizing

the same data depending on whether or not the CEO is from a founding family. The upper

row is a family CEO, and the lower row a non-family CEO. Once again, we do not find a

33

significant result for cost of equity, but find that cost of debt is significantly higher when

the CEO is from a family firm than not (2.281% vs. 2.523%). We also find that the

Adjusted PIN and PSOS are significantly higher when the CEO is from the founding family,

and it may indicate that a family CEO possesses more private information than a CEO

from outside the family. We consider this an illuminating result, which we could not have

obtained without utilizing the theoretical constructs of the microstructure study. As to size,

family firms with family CEOs are smaller than family firms with non-family CEOs, which

are more value firms.

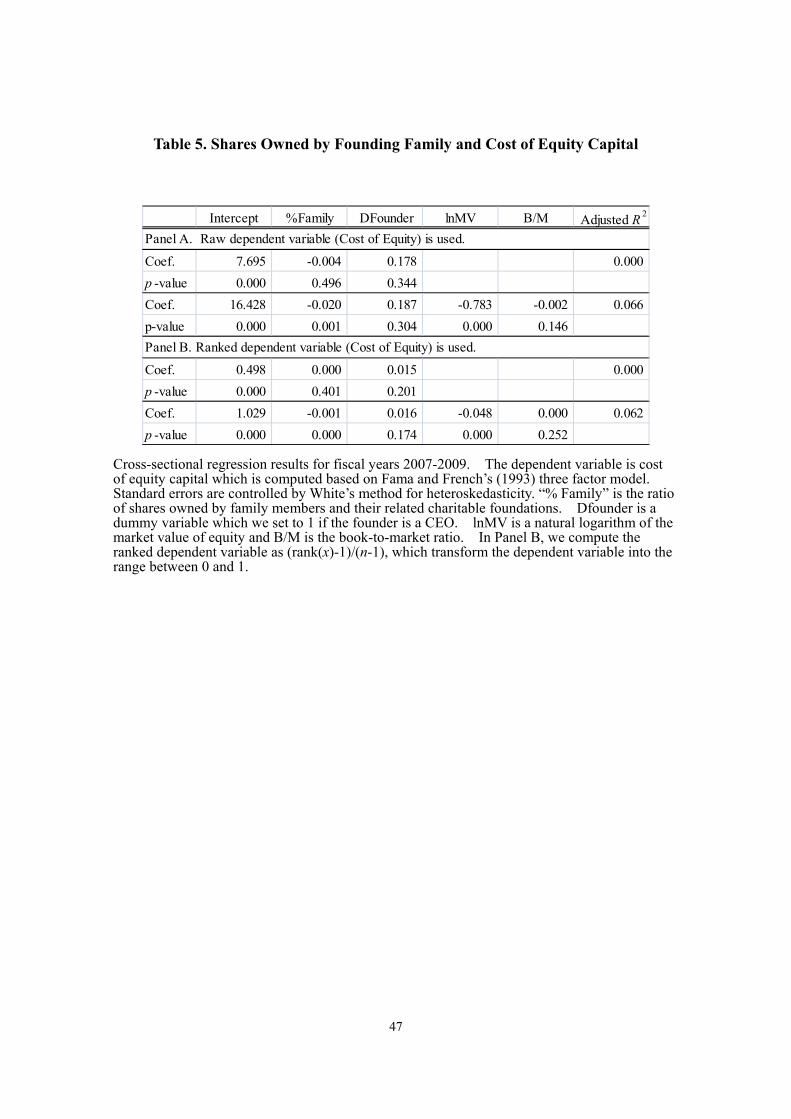

7. Cross-Section Regression Results on Information Asymmetry and Liquidity

Table 5 reports the results for cost of equity regressed on family firm-related variables,

that is, the fraction of shares owned by founding families and the CEO dummy as well as

control variables of size and book-to-market ratios.23 In Panel A, the dependent variable

is the raw variable, and Panel B the dependent variable is the ranked variable; i.e., let x

denote the n-dimensional real vector and rank(x) denote a function which returns the rank

of the elements in x, and the ranked version of x is defined as (rank(x)-1)/(n-1).

TABLE 5 ABOUT HERE

We find that coefficients of the fraction of shares owned by founding families are negative

in all four cases. The coefficients are significant for cases with control variables with

23 We also included an interactive term in the regression between fraction of shares held by founding families and the CEO dummy. The coefficients were all insignificant and we report the cases without interactive terms.

34

p-values 0.001 and 0.000. It means that shares are held more by families less cost of equity.

On the other hand, the CEO dummy is positive, but not significant. Note that hypothesis H1

in Section 5.2 is not conclusive. With our four-panel regression results, we do not reject the

hypothesis that family firms have a higher cost of equity, and, since the magnitude of the

sensitivity is small (-0.020 for raw variables and -0.001 for ranked variables), we conclude

that shares held by families will very weakly lower the cost of equity, or are indifferent.

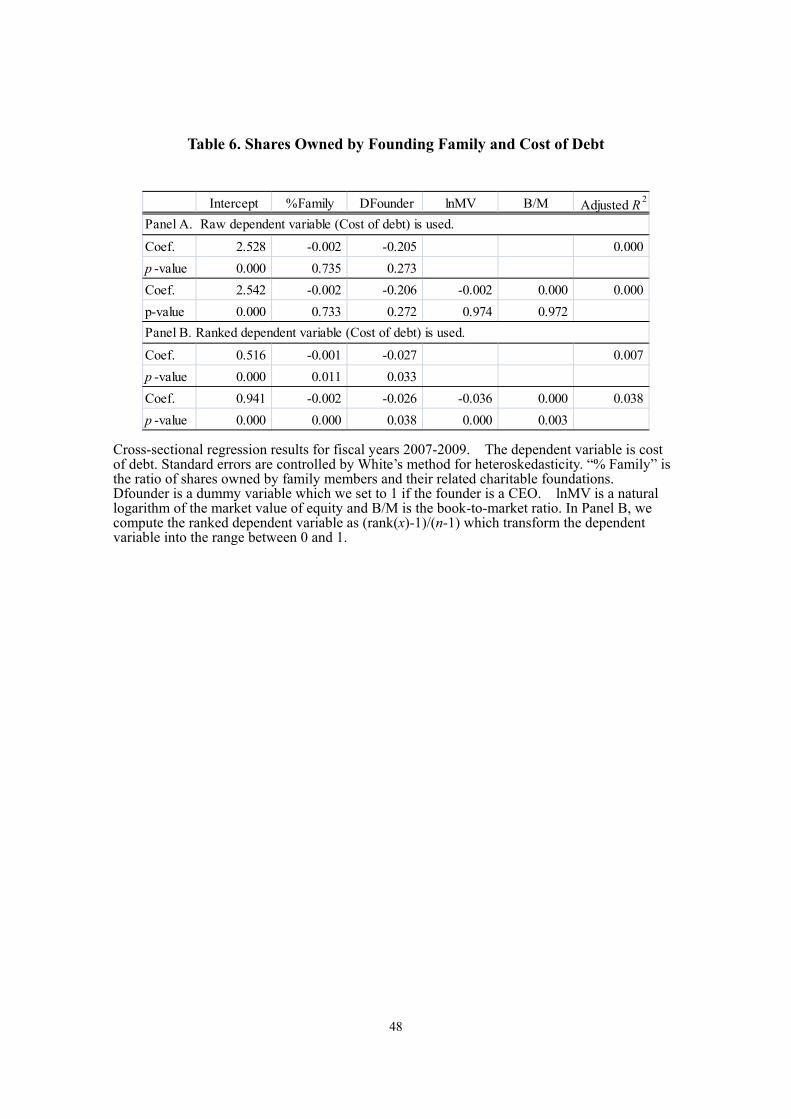

Table 6 reports the regression results for cost of debt, and independent and dependent

variables are the same as in Table 5.

TABLE 6 ABOUT HERE

For cost of debt, as hypothesis H2 purports, all coefficients for the fraction of shares owned

by founding families are negative, which is significant for ranked dependent variables.

Moreover, all the coefficients for the CEO dummy are negative although they are not

significant except for the ranked dependent variable with control variables with p-value

0.038. The result is overall on par with hypothesis H2 and we conclude that cost of debt is

lower for family firms and more so where the CEO is from the family. It supports our

initial view that the lender has more confidence in the family CEO when reaching the

lending decision. Note in the last regression the sensitivity of the CEO dummy, -0.026, is

ten times larger than the fraction of shares owned by founding families, -0.002. So the fact

that the incumbent CEO is from the family really helps explain the lower cost of debt,

which we have addressed in building hypothesis H2; i.e., lenders put a higher trust in

founding family management.

35

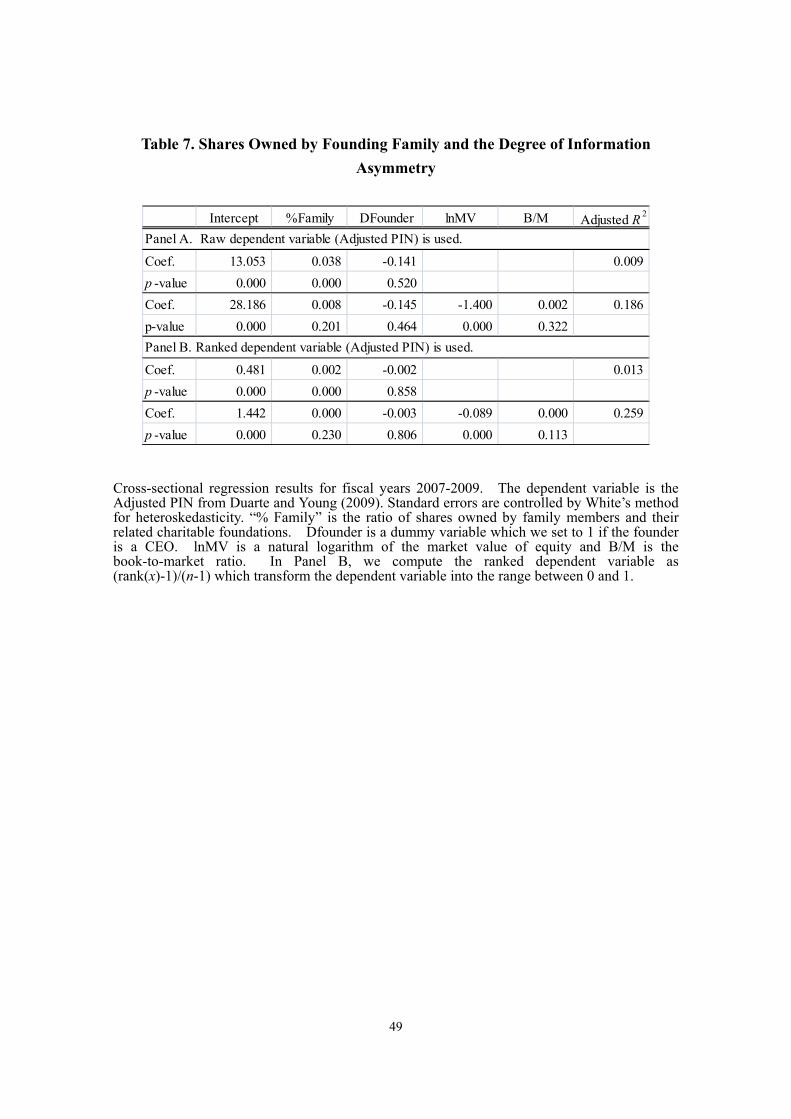

Table 7 reports the results of cross section regressions in which the dependent variable

is the Adjusted PIN. Once again, the set of independent variables is the same in Tables 5

and 6, and the lower Panel B shows results where dependent variables are ranked variables.

TABLE 7 ABOUT HERE

We find that all coefficients are positive (zero for the last case) for the fraction of shares

owned by founding families, suggesting that the higher the fraction of family-held shares,

the higher the probability of private information trades and information asymmetry.

However, the results are weaker because coefficients are significant only for the case when

control variables are not included. Moreover, for the CEO dummy variable, coefficients are

negative and not significant. Hence, we conclude that the fraction of shares owned by

founding families can explain the degree of information asymmetry, but it may be that it

behaves as if it were just a proxy for firm size. Accordingly, the evidence weakly supports

hypothesis H5.

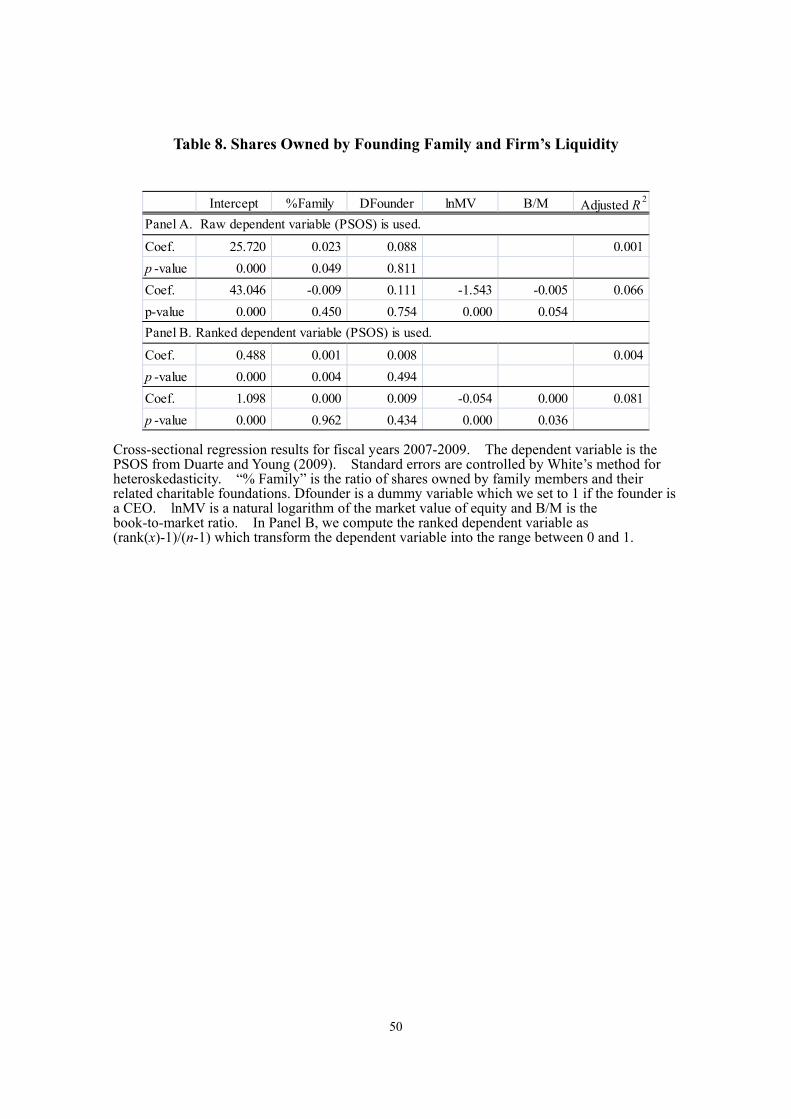

Table 8 reports the result from cross-sectional regressions in which the dependent

variable is the PSOS, the proxy measure of market liquidity.

TABLE 8 ABOUT HERE

We find that most of the coefficients for the fraction of founding family owned shares

are positive, as are all CEO dummy variables. However, coefficients for the fraction of

family shares are significant only for cases where control variables are not used. All the

36

coefficients for CEO dummy variables are not significant. Accordingly, we again weakly

support hypothesis H4 as well as H6, particularly when we use the PSOS as a proxy

variable for the measure of liquidity, as we observed in Table 3.

In sum, from both our univariate difference tests and cross-section regression tests, we

support hypotheses H2, H3, and H6, and weakly support H4 and H5, but are not conclusive

on H1, and thus the Corollary is not supported either. That is, we found evidence that

family firms in Japan have a lower cost of debt, lower market liquidity, and higher

information asymmetry, but the difference on cost of equity cannot be found.24 Although

family firms have less debt, we could not find conspicuous significant differences in the

WACC between family and non-family firms, although it was slightly higher for family

firms and the conventional t-test had a 10% significance level.

Policy implications for financial managers of family businesses are as follows. First, they

can resort to more debt to utilize the tax shield if they want to borrow from outside sources.

However, it may be difficult for firms which want to stick with inside financing in fear of

losing family control. Second, if they want to decrease the cost of equity, and accordingly,

WACC, one open channel is an effort to increase stock liquidity and decrease information

asymmetry at the same time. Family firms can attain this by enhancing their voluntary

disclosing effort and/or increasing floating stocks, which will lead to a lower cost of equity

and WACC. As a result, this will help family firms to implement more projects with

24 Recently Lambert et al. (2012) derived a model where they showed under perfect competition that the degree of information asymmetry does not affect cost of equity, and otherwise, if the market is under imperfect competition. Note that their theoretical model is based on the assumption of exponential utility and normal distributions. Whether the traded stocks of our family firm sample correspond to which case is an empirical question for future scrutiny.

37

positive NPVs.

8. Conclusion and Implications

In this paper we investigated market liquidity, distributions of private information-based

trades, and the cost of capital of publicly traded family firms in Japan. The database is

recent as of March 2009, and it covers three years of observations for all listed firms in

Japan.

This is the first study in the literature to use the Adjusted PIN and PSOS for family firm

data. These findings, which are new for Japanese family firms from 2007 through 2009,

have important implications for future family firm financial strategies and disclosure

policies.

Our overall findings are that family firms in Japan have a lower cost of debt, lower

market liquidity, and higher information asymmetry. However, the inference on the

difference in cost of equity is inconclusive. We also did not find whether the WACC for

family firms was significantly different from that for non-family firms with the Wilcoxon

test, although it was significant with the conventional t-test at a 10% level.

Given the evidence, we propose that more transparent voluntary disclosure among

Japanese family firms is called for, primarily for equity investors rather than lenders, in

order to increase market liquidity and reduce information asymmetry of their traded stocks,

and, accordingly, to reduce cost of equity and WACC. Another quick treatment is to

increase their leverage level to utilize the interest tax shield, but considering there is more

information asymmetry among family firms, lower debt may be a signal to inform outside

38

investors that their companies are good. (Graham, 2000). 25 So the latter may not be an

outright solution for firms which want to be classified as good ones in a signaling

equilibrium.

25 The extensive interview conducted in 2011 with Yamazaki Mazak Co. in Nagoya, which is one of the largest and best precision machine tool manufacturing companies in the world, revealed that the company does not utilize debt at all. However, this company is private. Hence, a signaling purpose may not be the direct reason in this case. We conjecture the reason might be congruent control of the company by the founding family in order to sustain long term goals.

39

References:

Aghion, P., Tirole, J., 1997. Formal and real authority in organizations. Journal of Political

Economy 105, 1-29.

Aktas, N., de Bodt, E., Declerck, F., Oppens, H. V., 2007. PIN anomaly around M&A

announcements. Journal of Financial Markets10, 169-191.

Ali, A., Chen, T-Y, Radhakrishnan, S., 2007. Corporate disclosure by family firms. Journal

of Accounting and Economics 44, 238-286.

Allouche, J., Amann, B., Jaussaud, J., Kurashina, T., 2008. The impact of family control on

the performance and financial characteristics of family versus nonfamily businesses in

Japan: A matched-pair investigation. Family Business Review 21, 315-329.

Almeida, H., Park, S. Y., Subrahmanyam, A. S. G., & Wolfenzon, D., 2010. The structure

and formation of business groups: Evidence from Korean Chaebols. Working Paper, Stern

School of Business, New York University.

Amihud, Y., 2002. Illiquidity and stock returns: Cross-section and time-series effects.

Journal of Financial Markets 5, 31-56.

Anderson, R. C., Reeb, D. M., 2003. Founding-family ownership and firm performance:

Evidence from the S&P 500. Journal of Finance 58, 1301-1328.

Anderson, R. C., Mansi, S.A., Reeb, D. M., 2003. Founding family ownership and the

agency cost of debt. Journal of Financial Economics 68, 263-285.

Anderson, R. C., Duru, A., Reeb, D. M., 2009. Founders, heirs, and corporate opacity in the

United States. Journal of Financial Economics 92, 205-222.

Anderson, R. C., Reeb, D. M., Zhao, W., 2012. Family-controlled firms and informed

trading: Evidence from short sales. Journal of Finance, forthcoming.

Aoi, M., Asaba, S, Kubota, K., Takehara, H., 2012. Corporate social performance and

family firms: A case of Japanese firms. Paper presented at International Family Enterprise

Academy Annual Congress, Bordeaux.

Asaba, S. 2012. Patient investment: A study on the behavior of the listed family business in

the Japanese electric machinery industry. Asia Pacific Journal of Management, on line first,

August 26.

Back, K., Baruch, S., 2004. Limit-order market and floor exchanges: An irrelevance

proposition. Manuscript. Texas A&M, and University of Utah.

Bolton, P., Dewatripont, M., 2005. Contract Theory. The MIT Press, Cambridge, MA.

Claessens, S., Djankov, S., Lang, L. H. P., 2000. The separation of ownership and control in

40

East Asian corporations. Journal of Financial Economics 58, 81-112.

Dennis, J. E. Jr., Schnabel, R. B., 1983. Numerical Methods for Unconstrained

Optimization and Nonlinear Equations. Prentice-Hall, Princeton, NJ.

Duarte, J., Han, X. Harford, J., & Young, L., 2008. Information asymmetry, information

dissemination and the effect of regulation FD on the cost of capital. Journal of Financial

Economics, 87, 24-44.

Duarte, J., Young, L., 2009. Why is PIN priced? Journal of Financial Economics 91,

119-138.

Easley, D., Hvidkjaer, S., O’Hara, M., 2002. Is information risk a determinant of asset

returns? Journal of Finance 57, 2185-2222.

Easley, D., Kiefer, N. M., O’Hara, M., Paperman, J. B., 1996. Liquidity, information, and

infrequently traded stocks. Journal of Finance 51, 1405-1436.

Easley, D., O’Hara, M., 2004. Information and the cost of capital. Journal of Finance 59,

1553-1583.

Ebihara, T., Kubota, K., Takehara, H., Yokota, E., 2012. Quality of accounting disclosure

by family firms in Japan. Paper available at ssrn.com;

http://dx.doi.org/10.2139/ssrn.1996505

Eoyang, C., 1998. The liquefaction of Japanese crossholding: Analyzing the unwinding

process. Goldman Sachs Equity Derivative Research, Goldman Sachs and Co, New York.

Fama, E. F., French, K. R., 1993. Common risk factors in the returns on stock and bonds.

Journal of Finance 48, 427-465.

Gomez-Mejia, L. R., Nunez-Nicker, M., 2001. The role of family ties in agency contracts.

Academy of Management Journal 44, 81-95.

Graham, J. R., 2000. How big are the tax benefits of debt? Journal of Finance 55,

1901-1942

Holden, C. W., Subrahmanyam, A., 1992. Long-lived information and imperfect

competition. Journal of Finance 47, 247-270.

Jagannathan, R., Kubota, K., Takehara, H.,1998, Relationship between labor-income risk

and average return: Evidence from the Japanese Stock Market. Journal of Business 71,

319-347.

Jensen, M. C., Meckling, W. H., 1976. Theory of the firms: Managerial behavior, agency

cots, and ownership structure. Journal of Financial Economics 3, 305-360.

Kaul, G., Lei, Q., Stoffman, N., 2008. AIMing at PIN: Order flow, information, and

41

liquidity. Working Paper, Southern Methodist University.

Kubota, K., Takehara, H., 2007. Effects of tax rate changes on the cost of capital: The case

of Japanese firms. Finanz/Archiv Public Finance Analysis 63, 163-185.

Kubota, K., Takehara, H., 2009. Information-based trade, the PIN variable, and portfolio

style differences: Evidence from Tokyo Stock Exchange firms. Pacific-Basin Finance

Journal 17, 295-318.

Kubota, K., Suda, K., Takehara, H., 2012. Impact of quarterly disclosure on information

asymmetry: Evidence from Tokyo Stock Exchange firms. Paper presented at the 2012

Econometric Society European Meeting, Malaga.

Lambert, R.A., Leuz, C., Verrecchia, R. E., 2012. Information asymmetry, information

precision, and the cost of capital. Review of Finance 16, 1-29.

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., 1999. Corporate ownership around the

world. Journal of Finance 54, 471-517.

Lesmond, D. A., Ogden, J. P., Trzcinka, C. A., 1999. A new estimate of transaction costs.

Review of Financial Studies 12, 1113-1141.

Liu W., 2006. A liquidity augmented capital asset pricing model. Journal of Financial

Economics 82, 631-671.

Masulis, R.W., Pham, P. K., Zein, J., 2011. Family business groups around the world: Costs

and benefits of pyramids. Review of Financial Studies 24, 3556-3600.

Mazzi, C., 2011. Family business and financial performance: Current state of knowledge

and future research challenges. Journal of Family Business Strategy 2, 166-181.

McConaughty, D. L. (1999). Is the cost of capital different for family firms? Family

Business Review, 12, 353-360.

Mehrotra, V., Morck, R., Shim, J., Wiwattananakantang, Y., 2011. Adoptive expectations:

Rising sun tournaments in Japanese firms. NBER Working Paper No. 16874.

Morck, R., Wolfenzon, D., Yeung, B., 2005. Corporate governance, economic entrenchment,

and growth. Journal of Economic Literature 43, 655-720.

Myers, S. C., 1977. Determinants of corporate borrowing. Journal of Financial Economics

5,146-175.

Odders-White, E.R., Ready, M. J, 2003. Credit ratings and stock liquidity. Working Paper,

University of Wisconsin-Madison.

Oh, W. Y., Chang, Y. K., 2011. The effect of ownership structure on corporate social

responsibility: Empirical evidence from Korea. Journal of Business Ethics 104, 283-297.

42

O’Hara, M., 2003. Liquidity and price discovery. Journal of Finance 58, 1335-1354.

Pastor L., & Stambaugh, R. (2003). Liquidity risk and expected stock returns. Journal of

Political Economy, 111, 642-685.

Reinking, J. F., Robb, S. W. G., Roberts, R. W., 2011. Family firm’s corporate social

responsibility and financial performance. Paper presented at the 2011 American Accounting

Association Annual Meeting, Denver.

Saito, T., 2008. Family firms and firm performance: Evidence from Japan. Journal of the

Japanese and International Economic, 22, 620-646.

Venter, J. H., de Jongh, D. C. J., 2005. Extending the EKOP model to estimate the

probability of informed trading.

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=648403, (October 20, 2011).

Villalolonga, B., Amit, R., 2006. How do family ownership, control and management affect

firm value? Journal of Financial Economics 80, 385- 417

Wang, D., 2006. Founding family ownership and earnings quality. Journal of Accounting

Research 44, 619-655.

Yafeh, Y., 2000. Corporate governance in Japan: Past performance and future prospects.

Oxford Review of Economic Policy 26, 74-84.

43

Table 1. Fraction of Family Firms in Each Industry

IndustryNumberof Firms

%FF≧10%and CEO isa founder

%FF≧10%and CEO is

not a founder

%FF<10%and CEO isa founder

Franction offamily firms

(in %)

Averageshares

owned byfounded

family (in %)