Embed Size (px)

Citation preview

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

Market Input: Interest Rates

Joint Vienna Institute, Vienna, Austria

February 23 – 27, 2015

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

(Market) Interest rates

• The cash flows as well as the cost and risk of a given debt management strategy will depend on the future path of interest (and exchange rates), which are unknown

• How to determine them?– Assume constant rates

– Ask analysts to prepare forecasts and take an average

– Link to projections for policy rates, inflation, and GDP growth

– Use market information, perhaps even data from more developed markets

2

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

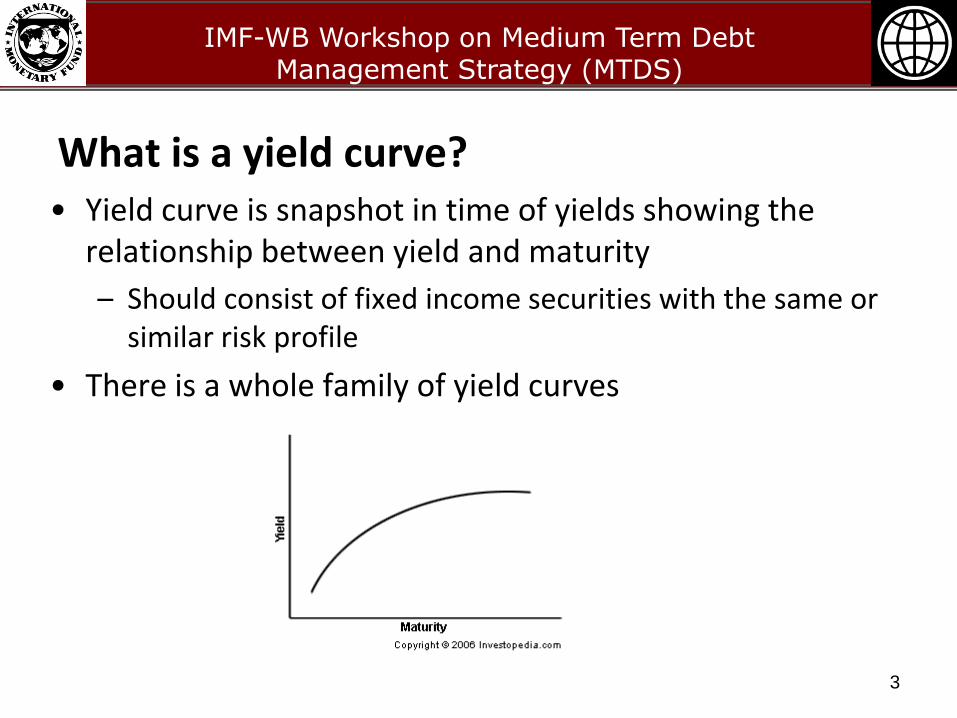

What is a yield curve?• Yield curve is snapshot in time of yields showing the

relationship between yield and maturity

– Should consist of fixed income securities with the same or similar risk profile

• There is a whole family of yield curves

3

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

Building a yield curve

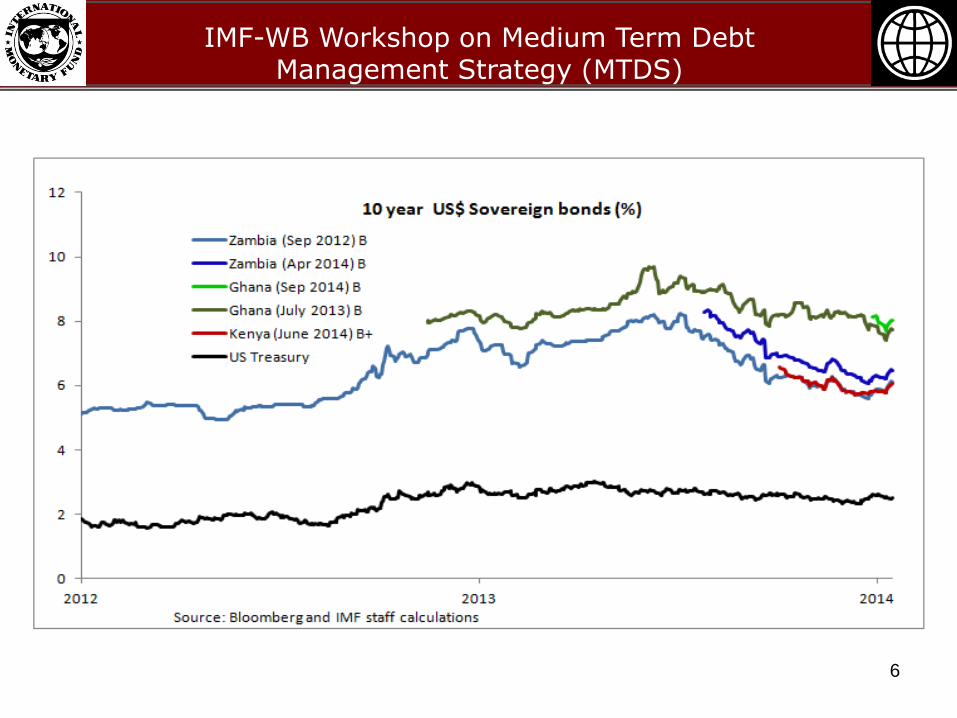

• Begin with foreign currency debt

– Build on mature market curves: any international bonds will be issued at a spread to a benchmark (e.g., a US 10-year Treasury)

– Determine likely credit premia to derive implied FX sovereign curve:

• May need to use peers to set plausible spreads

• Presumes that rating has been established

4

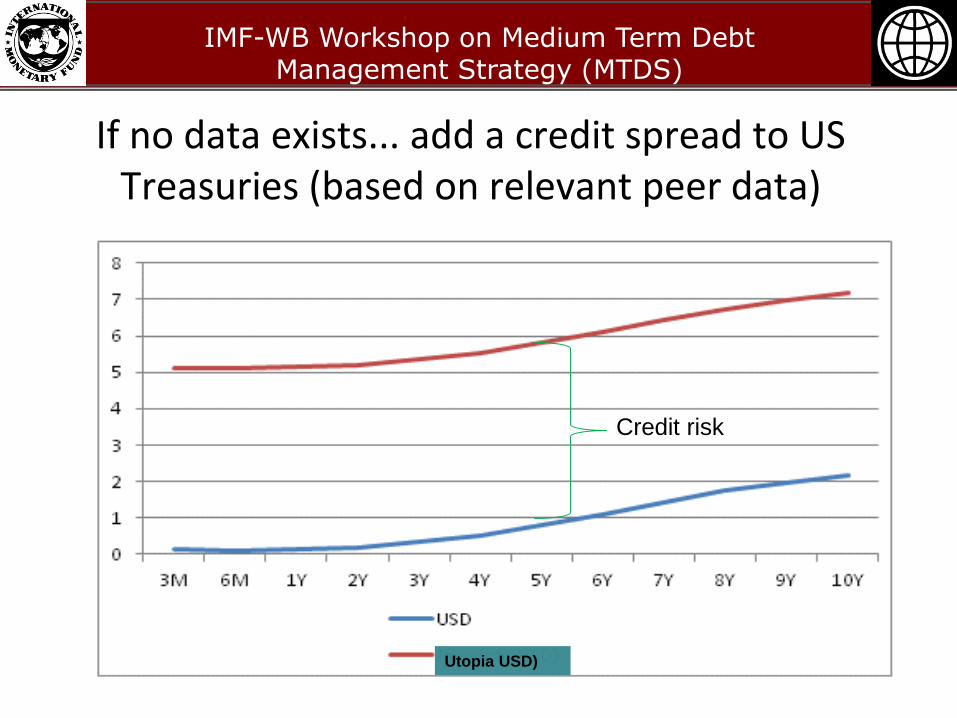

For many countries access to market data is limited

The domestic market for government securities is thin and short

Interest rates are not market determined

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

If no data exists... add a credit spread to US Treasuries (based on relevant peer data)

Utopia USD)

Credit risk

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

6

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

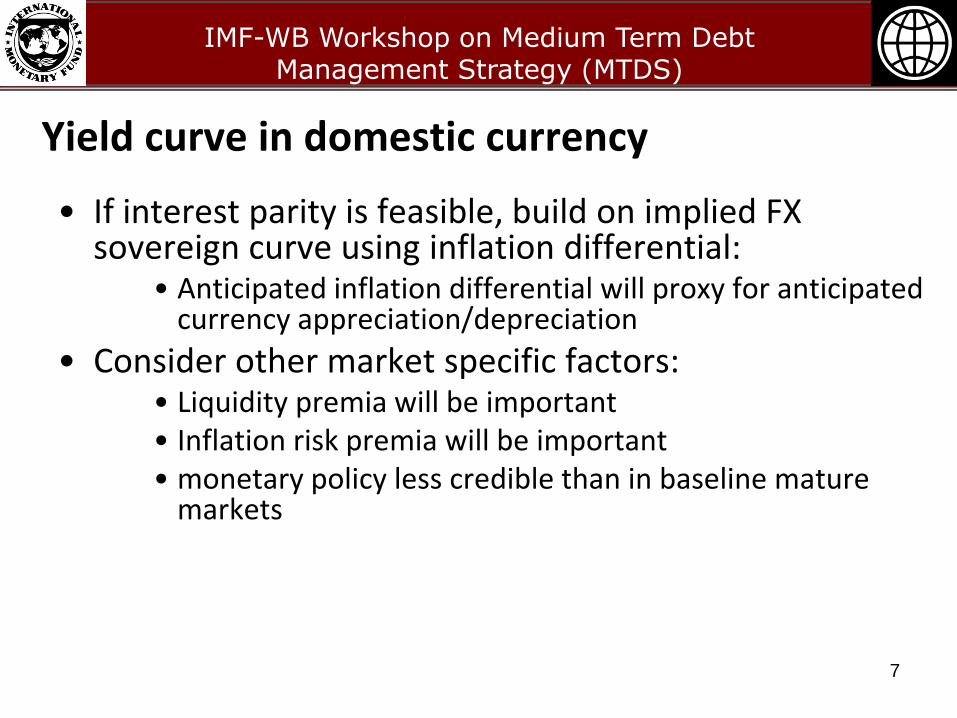

Yield curve in domestic currency

• If interest parity is feasible, build on implied FX sovereign curve using inflation differential:

• Anticipated inflation differential will proxy for anticipated currency appreciation/depreciation

• Consider other market specific factors:• Liquidity premia will be important• Inflation risk premia will be important • monetary policy less credible than in baseline mature

markets

7

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

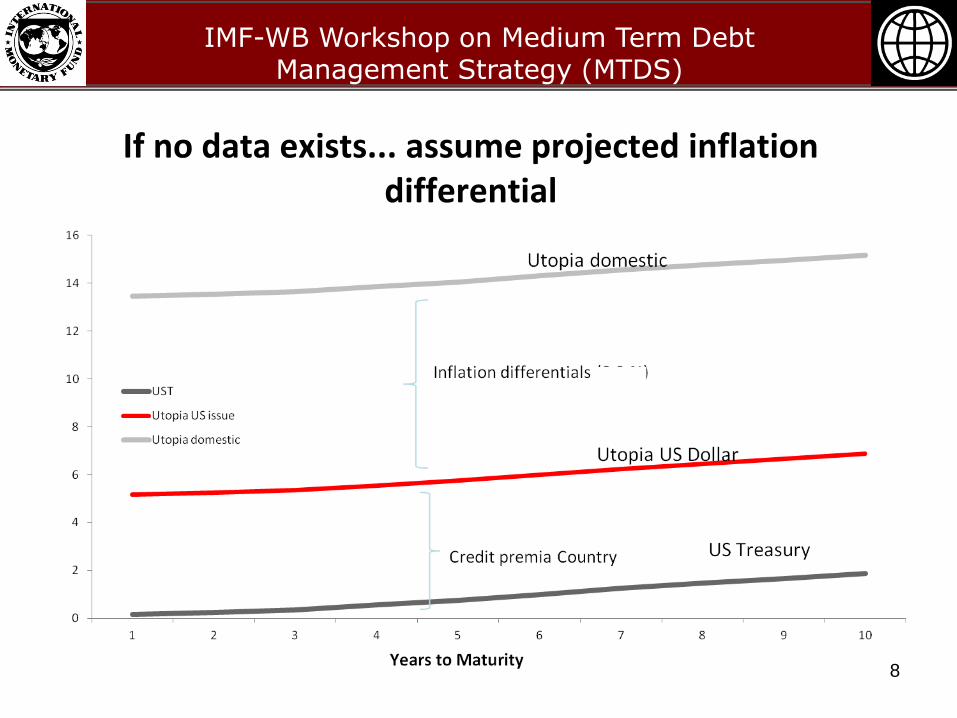

If no data exists... assume projected inflation differential

8

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

Is this the best approach?

• For many countries access to market data is limited– The domestic market for government securities is thin and short

– Interest rates are not market determined

– Fixed exchange rate policy

• Macroeconomic projections can provide a reasonable alternative– MoF, CB, IFIs or investment banks

– But still need assumptions about term structure

9

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

What if a market curve exists?

• Compare existing curve to that implied by covered interest parity

– Difference? Explained by liquidity and other risk premia

• May not extend sufficiently

– If want to consider introducing longer tenors need to make assumptions about term premia or build on interest parity determined curve (e.g., by holding liquidity and other premia constant at last observed point)

10

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

Forward Yield Curves

• Are we done yet?

– Not quite. We now have the relevant yield curves for current period, but need yield curves for each year within the time horizon

• What can we do?

– Can determine the market’s expectations of future rates from current/spot yield curves

11

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

12

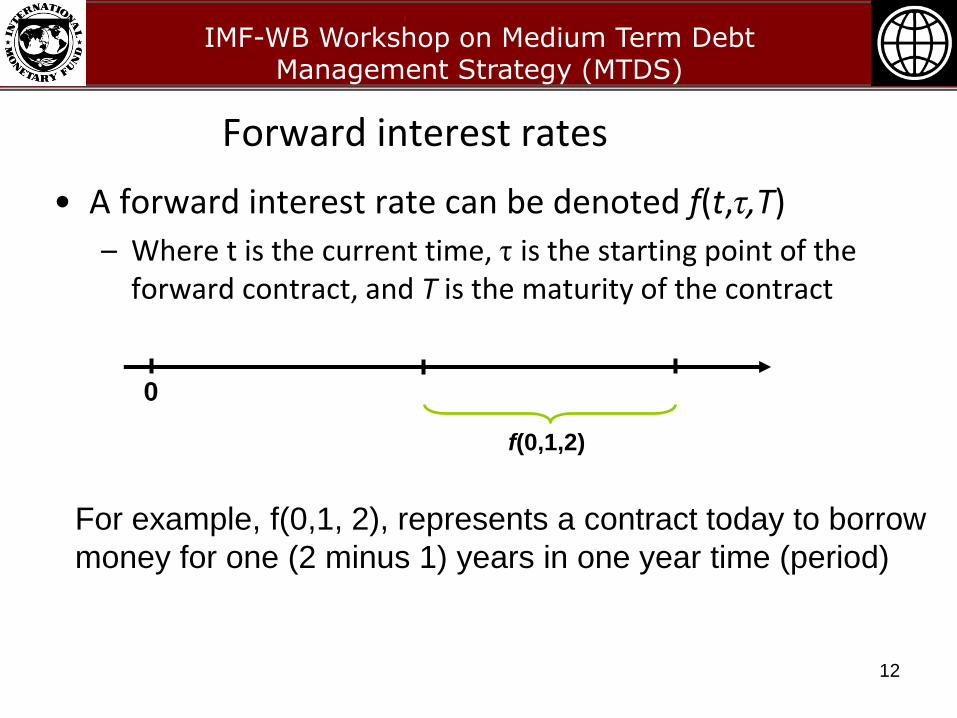

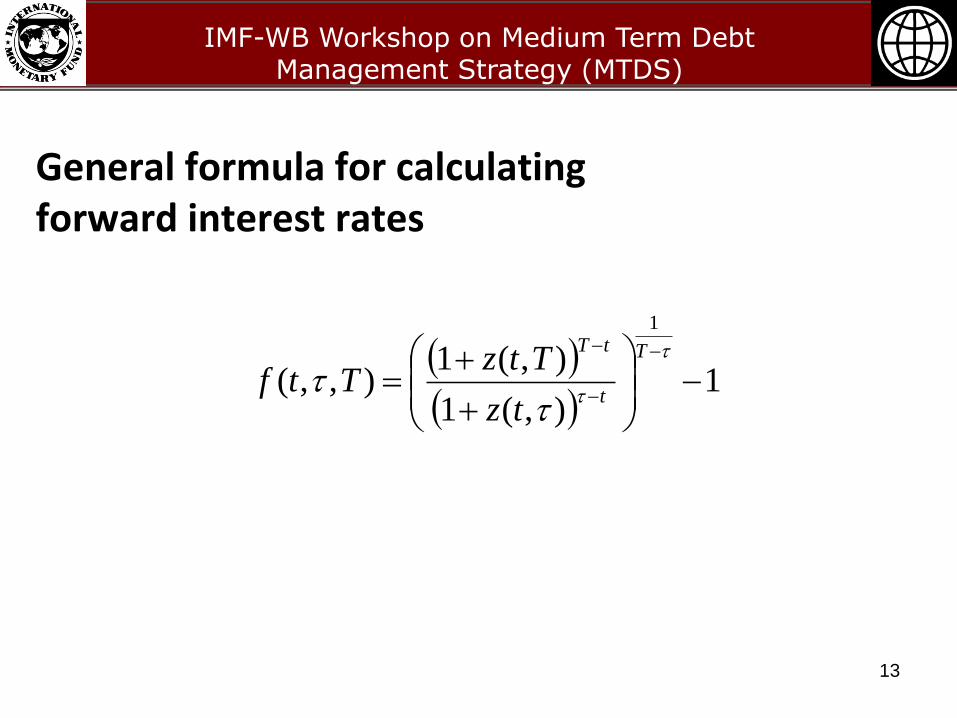

Forward interest rates

• A forward interest rate can be denoted f(t,τ,T)

– Where t is the current time, τ is the starting point of the forward contract, and T is the maturity of the contract

Time0 1 2

f(0,1,2)

For example, f(0,1, 2), represents a contract today to borrow

money for one (2 minus 1) years in one year time (period)

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

General formula for calculating forward interest rates

1),(1

),(1),,(

1

T

t

tT

tz

TtzTtf

13

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

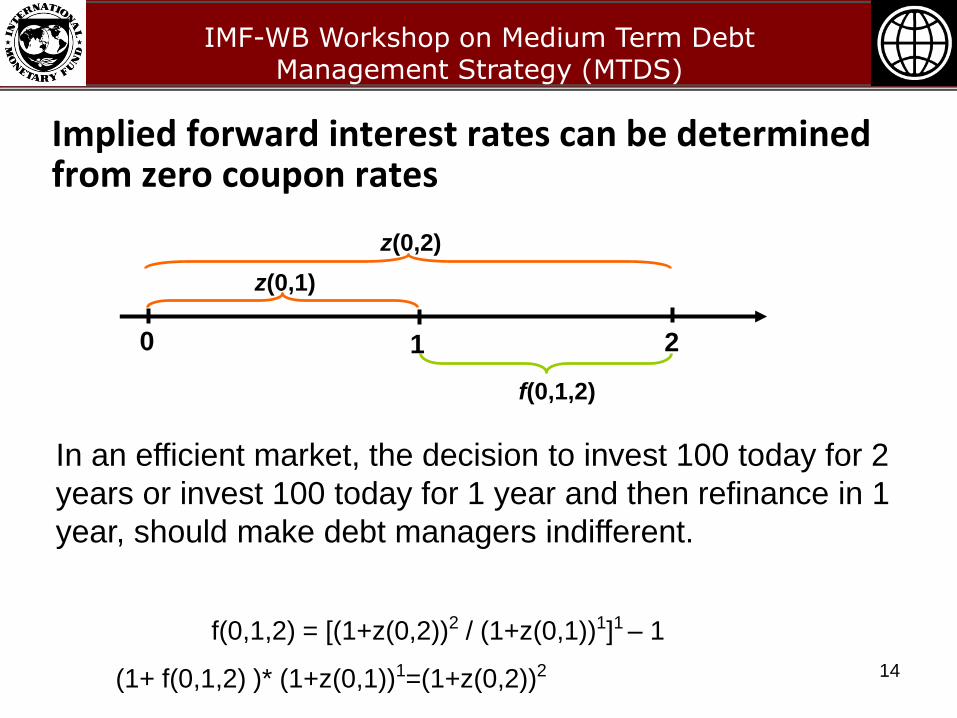

Implied forward interest rates can be determined from zero coupon rates

14

Time0 1 2

z(0,1)

z(0,2)

f(0,1,2)

In an efficient market, the decision to invest 100 today for 2

years or invest 100 today for 1 year and then refinance in 1

year, should make debt managers indifferent.

f(0,1,2) = [(1+z(0,2))2 / (1+z(0,1))1]1 – 1

(1+ f(0,1,2) )* (1+z(0,1))1=(1+z(0,2))2

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

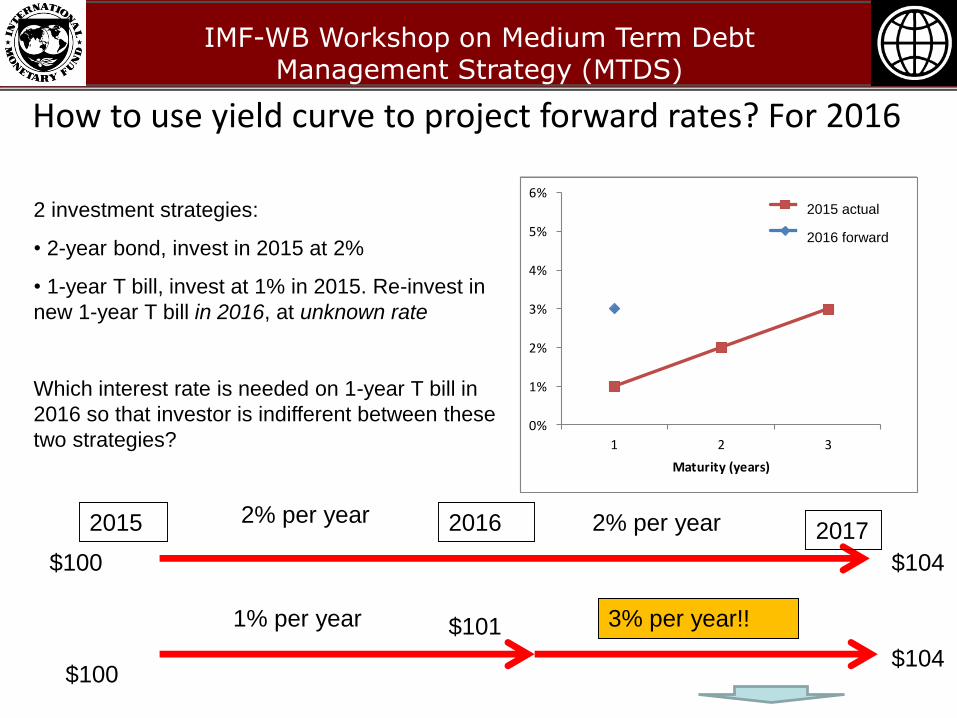

How to use yield curve to project forward rates? For 2016

2 investment strategies:

• 2-year bond, invest in 2015 at 2%

• 1-year T bill, invest at 1% in 2015. Re-invest in

new 1-year T bill in 2016, at unknown rate

Which interest rate is needed on 1-year T bill in

2016 so that investor is indifferent between these

two strategies?

2015 2016 2017

$100 $104

$104

$101

$100

2% per year 2% per year

1% per year ???% per year3% per year!!

0%

1%

2%

3%

4%

5%

6%

1 2 3

Maturity (years)

2011 actual

0%

1%

2%

3%

4%

5%

6%

1 2 3

Maturity (years)

2011 actual

2012 forward

2015 actual

2016 forward

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

• Upward-sloping yield curve: – Expectation is that future rates will be higher:

• Higher central bank policy rates (tighter policy)• Higher inflation in future• Anticipate stronger economic growth in future

• Downward-sloping yield curve (“inverted yield curve”):– Expectation that future rates will be lower

• Lower central bank policy rates • Lower inflation in future• Strongly inverted curves have historically preceded recessions

• Flat yield curve:– Expectation that future rates will remain the same

• Note: Maturity premium typically results in upward-sloping yield curve regardless of market expectations. Liquidity premium and other structural factors also influence shape

Market interpretation (expectations)

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

Forecasting exchange rates

• Two methodologies– Uncovered interest rate parity

– Purchasing power parity

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

• “The rate at which the currency of one country would have to be converted into that of another country to buy the same amount of goods and services in each country”. Source: IMF, 2012

• the theory that exchange rates should eventually adjust to make the price of identical baskets of tradable goods the same in each country

• put another way how much money would be needed to purchase the same goods and services in two countries, and uses that to calculate an implicit foreign exchange rate

• among other uses, PPP rates facilitate international comparisons of income, as market exchange rates are often volatile

• the economist publishes (daily) Big Mac index, a fun guide to whether currencies are at their correct level. However, any meaningful comparison of prices across countries must consider a wide range of goods and services.

Purchasing power parity (1)

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

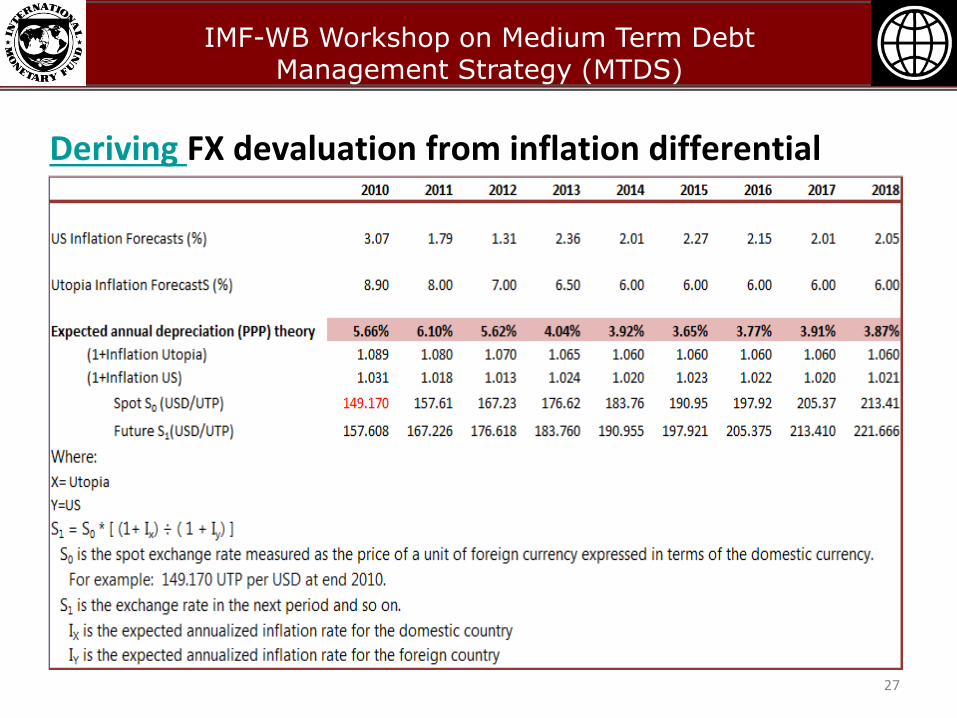

Deriving FX devaluation from inflation differential

27

IMF-WB Workshop on Medium Term Debt Management Strategy (MTDS)

Thank You