Embed Size (px)

Citation preview

Market in MinutesHotels and Leisure Q1 2018

Savills Research Ireland

Economic Overview Ireland’s economy continues to perform remarkably well with total output now rising at a faster annual rate than any other country in the EU. Growth in consumer spending is contributing positively to this having accelerated to a five-quarter high of 2.7%. Jobs growth is the driving force behind this. Ireland is currently creating nearly 50,000 additional jobs per annum. As a result, unemployment has fallen to 6.1%, leading to a more competitive labour market and a sustained period of modest but meaningful earnings growth. Greater numbers at work, coupled with increased earnings and modest tax cuts, have led to over 5% growth in real aggregate disposable incomes over the past twelve months. Adding to this, sustained growth in consumer loans has further boosted spending power.

The economic outlook for Ireland’s main tourism partners remains positive too, in spite of Brexit uncertainties and the protectionist policies adopted in America. The global recovery is continuing to gather momentum with the IMF pencilling in growth of 3.9% for 2018 and 2019. At the same time, the ECB is planning to continue its bond buying programme to September and no interest rate increases are expected until 2019 at the earliest. As well as ensuring cheap consumer credit, this should help to keep the Euro competitive.

Table 1: Consumer Economy Dashboard

Indicator % Change Y/Y

Unemployment Rate -17.6

Core Retail Sales (ex. Motors) +7.3

Consumer Sentiment (3mma) +6.8

Real VAT Receipts +5.5

Real Household Disposable Incomes +5.3

Consumer Credit Outstanding Balances +4.4

Overseas Trips to Ireland +3.6

Real Personal Consumption Expenditure +2.7

Total Employment +2.2

Real Average Gross Earnings +1.5

Sources: CSO, CBI, KBC Bank Ireland/ESRI, Dept. of Finance.

Gibson Hotel - Sold Q4 2017

02 savills.ie/research

Hotels and Leisure Market in Minutes

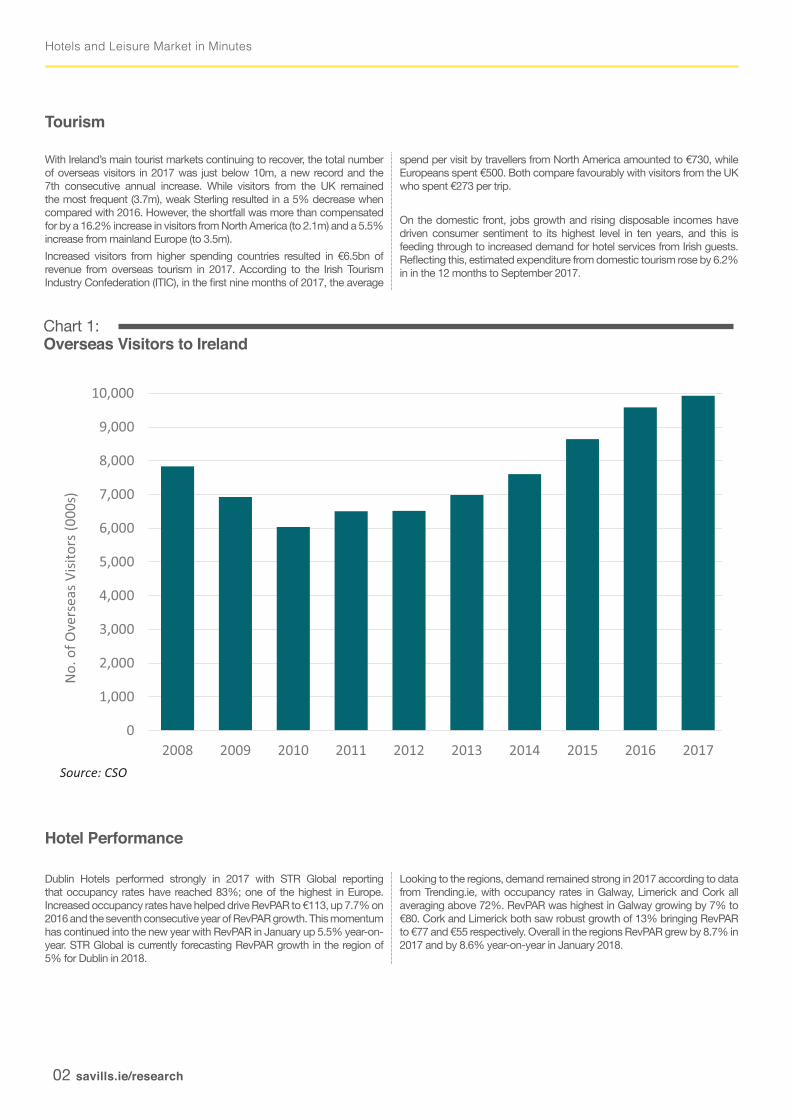

With Ireland’s main tourist markets continuing to recover, the total number of overseas visitors in 2017 was just below 10m, a new record and the 7th consecutive annual increase. While visitors from the UK remained the most frequent (3.7m), weak Sterling resulted in a 5% decrease when compared with 2016. However, the shortfall was more than compensated for by a 16.2% increase in visitors from North America (to 2.1m) and a 5.5% increase from mainland Europe (to 3.5m).Increased visitors from higher spending countries resulted in €6.5bn of revenue from overseas tourism in 2017. According to the Irish Tourism Industry Confederation (ITIC), in the first nine months of 2017, the average

spend per visit by travellers from North America amounted to €730, while Europeans spent €500. Both compare favourably with visitors from the UK who spent €273 per trip.

On the domestic front, jobs growth and rising disposable incomes have driven consumer sentiment to its highest level in ten years, and this is feeding through to increased demand for hotel services from Irish guests. Reflecting this, estimated expenditure from domestic tourism rose by 6.2% in in the 12 months to September 2017.

Chart 1: Overseas Visitors to Ireland

Tourism

36%

11%

3%

22%

3%

8%

3%

11%

3%Fashion & Footwear

Health & Beauty

Jewellery

Food & Beverage

Food Grocery

Sta�onery / Cards / Confec�onery

Lifestyle

Homeware

Kids

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

)s000( srotisiV saesrevO fo .o

N

Source: CSO

Hotel Performance

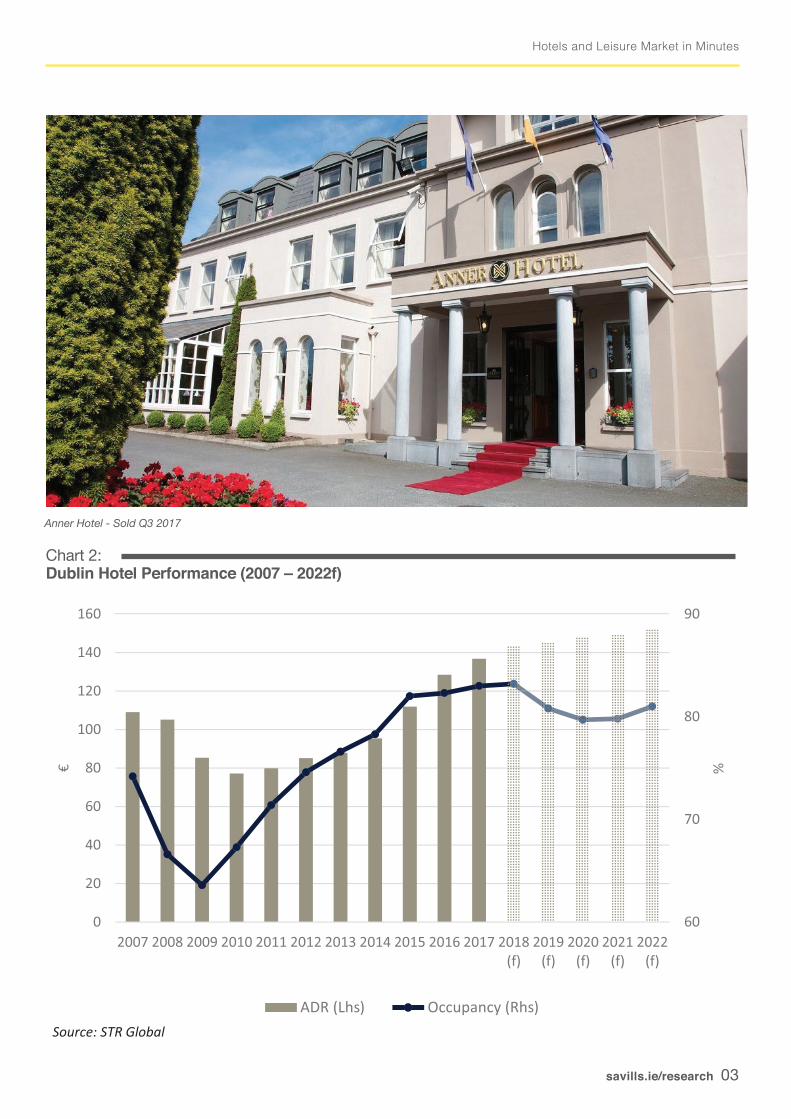

Dublin Hotels performed strongly in 2017 with STR Global reporting that occupancy rates have reached 83%; one of the highest in Europe. Increased occupancy rates have helped drive RevPAR to €113, up 7.7% on 2016 and the seventh consecutive year of RevPAR growth. This momentum has continued into the new year with RevPAR in January up 5.5% year-on-year. STR Global is currently forecasting RevPAR growth in the region of 5% for Dublin in 2018.

Looking to the regions, demand remained strong in 2017 according to data from Trending.ie, with occupancy rates in Galway, Limerick and Cork all averaging above 72%. RevPAR was highest in Galway growing by 7% to €80. Cork and Limerick both saw robust growth of 13% bringing RevPAR to €77 and €55 respectively. Overall in the regions RevPAR grew by 8.7% in 2017 and by 8.6% year-on-year in January 2018.

savills.ie/research 03

Hotels and Leisure Market in Minutes

Chart 2: Dublin Hotel Performance (2007 – 2022f)

60

70

80

90

0

20

40

60

80

100

120

140

160

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018(f)

2019(f)

2020(f)

2021(f)

2022(f)

%€

ADR (Lhs) Occupancy (Rhs)Source: STR Global

36%

11%

3%

22%

3%

8%

3%

11%

3%Fashion & Footwear

Health & Beauty

Jewellery

Food & Beverage

Food Grocery

Sta�onery / Cards / Confec�onery

Lifestyle

Homeware

Kids

Source: Savills Research

60

70

80

90

0

20

40

60

80

100

120

140

160

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018(f)

2019(f)

2020(f)

2021(f)

2022(f)

%€

ADR (Lhs) Occupancy (Rhs)Source: STR Global

36%

11%

3%

22%

3%

8%

3%

11%

3%Fashion & Footwear

Health & Beauty

Jewellery

Food & Beverage

Food Grocery

Sta�onery / Cards / Confec�onery

Lifestyle

Homeware

Kids

Source: Savills Research

Anner Hotel - Sold Q3 2017

04 savills.ie/research

Hotels and Leisure Market in Minutes

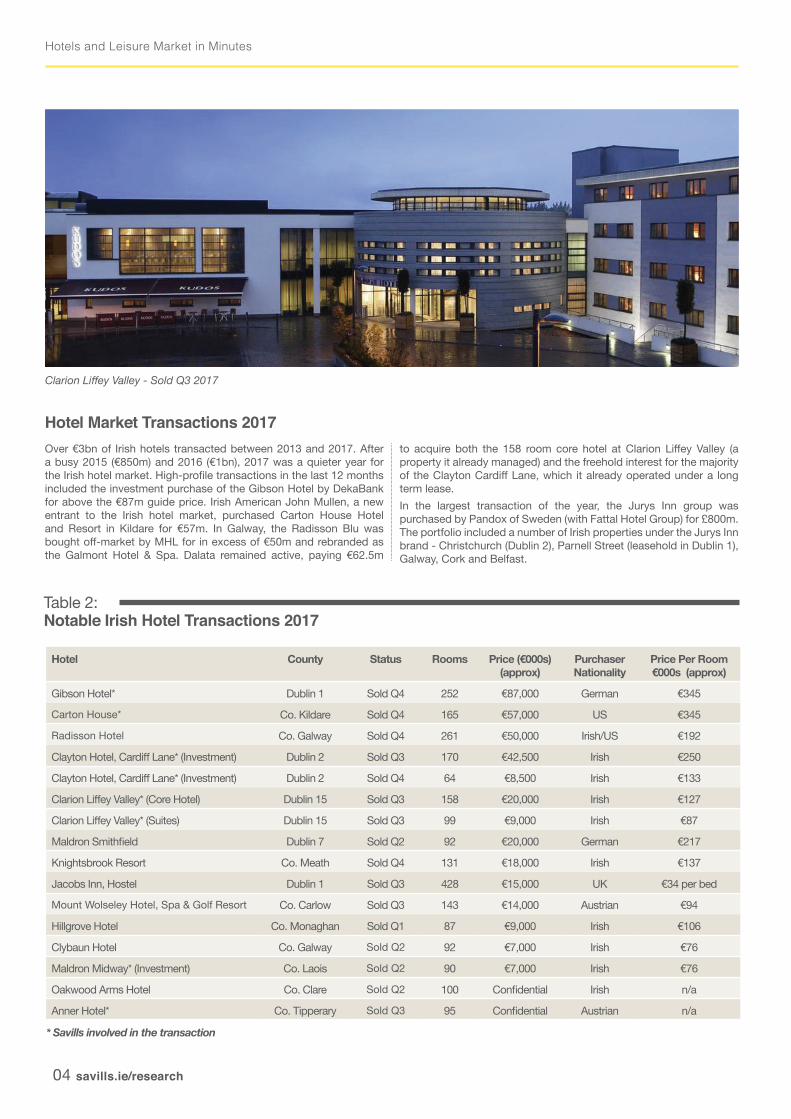

Hotel Market Transactions 2017Over €3bn of Irish hotels transacted between 2013 and 2017. After a busy 2015 (€850m) and 2016 (€1bn), 2017 was a quieter year for the Irish hotel market. High-profile transactions in the last 12 months included the investment purchase of the Gibson Hotel by DekaBank for above the €87m guide price. Irish American John Mullen, a new entrant to the Irish hotel market, purchased Carton House Hotel and Resort in Kildare for €57m. In Galway, the Radisson Blu was bought off-market by MHL for in excess of €50m and rebranded as the Galmont Hotel & Spa. Dalata remained active, paying €62.5m

to acquire both the 158 room core hotel at Clarion Liffey Valley (a property it already managed) and the freehold interest for the majority of the Clayton Cardiff Lane, which it already operated under a long term lease. In the largest transaction of the year, the Jurys Inn group was purchased by Pandox of Sweden (with Fattal Hotel Group) for £800m. The portfolio included a number of Irish properties under the Jurys Inn brand - Christchurch (Dublin 2), Parnell Street (leasehold in Dublin 1), Galway, Cork and Belfast.

Table 2: Notable Irish Hotel Transactions 2017

Hotel County Status Rooms Price (€000s) (approx)

Purchaser Nationality

Price Per Room €000s (approx)

Gibson Hotel* Dublin 1 Sold Q4 252 €87,000 German €345

Carton House* Co. Kildare Sold Q4 165 €57,000 US €345

Radisson Hotel Co. Galway Sold Q4 261 €50,000 Irish/US €192

Clayton Hotel, Cardiff Lane* (Investment) Dublin 2 Sold Q3 170 €42,500 Irish €250

Clayton Hotel, Cardiff Lane* (Investment) Dublin 2 Sold Q4 64 €8,500 Irish €133

Clarion Liffey Valley* (Core Hotel) Dublin 15 Sold Q3 158 €20,000 Irish €127

Clarion Liffey Valley* (Suites) Dublin 15 Sold Q3 99 €9,000 Irish €87

Maldron Smithfield Dublin 7 Sold Q2 92 €20,000 German €217

Knightsbrook Resort Co. Meath Sold Q4 131 €18,000 Irish €137

Jacobs Inn, Hostel Dublin 1 Sold Q3 428 €15,000 UK €34 per bed

Mount Wolseley Hotel, Spa & Golf Resort Co. Carlow Sold Q3 143 €14,000 Austrian €94

Hillgrove Hotel Co. Monaghan Sold Q1 87 €9,000 Irish €106

Clybaun Hotel Co. Galway Sold Q2 92 €7,000 Irish €76

Maldron Midway* (Investment) Co. Laois Sold Q2 90 €7,000 Irish €76

Oakwood Arms Hotel Co. Clare Sold Q2 100 Confidential Irish n/a

Anner Hotel* Co. Tipperary Sold Q3 95 Confidential Austrian n/a

* Savills involved in the transaction

Clarion Liffey Valley - Sold Q3 2017

savills.ie/research 05

Hotels and Leisure Market in Minutes

Hotel Market Transactions - 2018 YTDHilton branded hotels account for much of the early 2018 activity - the Hilton Garden Inn Dublin sold to LRC as part of the Amaris portfolio for £600m, the Hilton Belfast has also been sold and the Hilton Dublin Airport is currently on the market. The Citywest Hotel change of ownership was cleared by the CCPC (Competition Authority) and Davy (acting for Austrian investor Thomas Röggla) was confirmed as the preferred purchaser for the 103 room McWilliam Park in Co. Mayo for a reported €9m, its ninth hotel purchase in Ireland.

Hotel Development

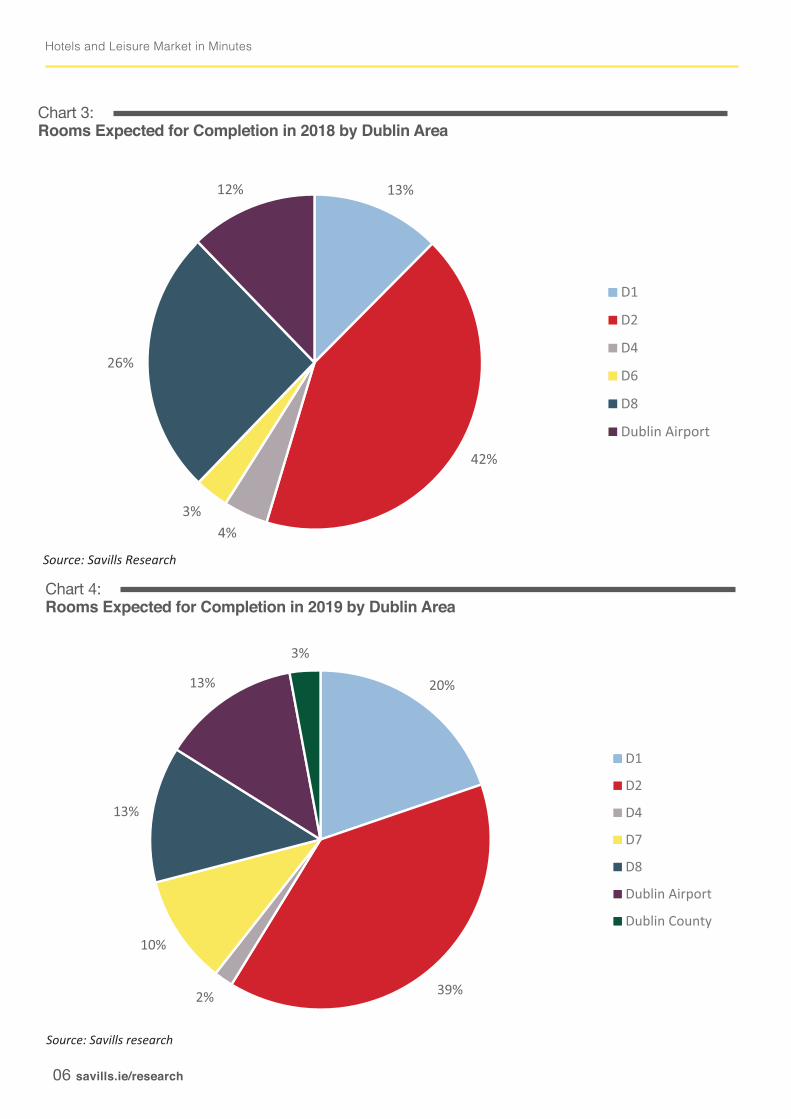

Given the positive economic environment there is now genuine momentum towards delivering additional Dublin hotel room stock. In 2017, 159 additional rooms were delivered in Dublin as a result of extensions. Most notably, the 75 room extension at the North Star Hotel in Dublin 1, accounted for 47% of new stock. Much of current hotel development is concentrated in Dublin 1, Dublin 2 and the emerging Dublin 8 areas. Eighty one percent of the 1,200 additional new rooms in 2018 and 72% of the 2,000 potential additional new rooms in 2019 are planned for delivery in these areas.2018 will see new hotels of scale open. These include the Iveagh Garden Hotel (152 rooms) on Harcourt Street (February), the Dalata owned Maldron Hotel on Kevin Street (140 rooms) and the Clayton Hotel in Charlemont (181 rooms) which will open in June and October respectively. The first Aloft Hotel in Ireland, will open in Blackpitts, Dublin 8 in July and the first hotel in Ranelagh, Dublin 6 (The Devlin) owned by Paddy McKillen Jnr is also nearing completion. The Morgan Hotel in Temple Bar was closed for refurbishment and extension (40 additional rooms) and is due to reopen in mid-2018. Radisson Blu Galway - Sold Q4 2017

Knightsbrook Resort - Sold Q4 2017

06 savills.ie/research

Hotels and Leisure Market in Minutes

Chart 4: Rooms Expected for Completion in 2019 by Dublin Area

20%

39%2%

10%

13%

13%

3%

D1

D2

D4

D7

D8

Dublin Airport

Dublin County

Source: Savills research

36%

11%

3%

22%

3%

8%

3%

11%

3%Fashion & Footwear

Health & Beauty

Jewellery

Food & Beverage

Food Grocery

Sta�onery / Cards / Confec�onery

Lifestyle

Homeware

Kids

Source: Savills Research

Chart 3: Rooms Expected for Completion in 2018 by Dublin Area

13%

42%

4%3%

26%

12%

D1

D2

D4

D6

D8

Dublin Airport

Source: Savills Research

36%

11%

3%

22%

3%

8%

3%

11%

3%Fashion & Footwear

Health & Beauty

Jewellery

Food & Beverage

Food Grocery

Sta�onery / Cards / Confec�onery

Lifestyle

Homeware

Kids

Source: Savills Research

savills.ie/research 07

Hotels and Leisure Market in Minutes

OutlookThe tourism sector remains a vital component of the Irish economy and the retention of the 9% VAT rate on tourism in Budget 2018, along with the continued suspension of Air Travel Tax, continue to make Ireland an attractive travel destination. These measures have undoubtedly aided the recovery of the tourism sector, particularly in the regions. Since Q3 2012 the sector has added 42,000 jobs – accounting for just under 12% of total jobs growth in the economy. 2018 looks to be another positive year for the tourism industry as airlines continue to expand seat capacity to Irish airports from North America and mainland Europe, while direct flights from Hong Kong start in June. Irish Ferries announced it will be doubling sailings to and from France during the key summer months.

With rapid economic expansion and the international flavour of Dublin’s corporate sector the demand for hotel beds from business travellers is also rising. Dublin’s office stock has increased by approximately 133,000 sq m over the last three years – enough to accommodate 11,000 extra workers, and a further

400,000 sq m is currently under construction which will create still further business demand for hotels in the city.

Looking further ahead, the Government’s recently published vision for Ireland in 2040, lays out a significant plan for growth in the regions of Ireland in terms of population, jobs and infrastructure. This will benefit regional commerce and tourism. The plan also lays out a new brand for the Midlands to complement the Ancient East and Wild Atlantic Way. Green tourism also features with new Greenways, Blueways and Peatways planned.

For the remainder of the year we expect to see a similar level of single asset transaction volumes to 2017. However, unlike previous years, where deal flow was predominantly on-market driven by institutional de-leveraging, 2018 will be led by re-sales with a preference for off-market deals. As brands continue to seek a foothold in Dublin, we expect the announcement of a number of leased hotels, which will create much sought after long income investment properties.

Clayton Cardiff Lane - Sold Q3 2017

08 savills.ie/research

Hotels and Leisure Market in Minutes

Savills ResearchPlease contact us for further information

Savills is a leading global real estate service provider listed on the London Stock Exchange. The company established in 1855, has a rich heritage with unrivalled growth. It is a company that leads rather than follows, and now has over 180 offices and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East. A unique combination of sector knowledge and entrepreneurial flair give clients access to real estate expertise of the highest calibre. We are regarded as an innovative-thinking organisation backed up with excellent negotiating skills. Savills chooses to focus on a defined set of clients, therefore offering a premium service to organisations with whom we share a common goal. Savills takes a longterm view to real estate and works hard to invest in long term and strategic relationships and is synonymous with a high quality service offering and a premium brand. This bulletin is for general informative purposes only. Whilst every effort has been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. All references to space and floor areas are approximate and apply to the greater Dublin area. The bulletin is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Savills Research. (c) Savills Ltd.

Tom Barret Head of Hotels and Leisure+353 (0) 1 618 [email protected]

Henry RoeSurveyor+353 (0) 1 663 [email protected]

John McCartneyDirector of Research+353 (0)1 618 [email protected]

Aaron SpringAssociate Director+353 (0) 1 618 [email protected]

Gillian GoreAssistant+353 (0) 1 618 [email protected]

Carton House - Sold Q4 2017

Jarlath QuinnAssociate Director, Valuations+353 (0) 618 [email protected]