Embed Size (px)

Citation preview

MARKET ENVIRONMENT REPORT April 2015

MERCER Market Environment Report April 2015 2

About Mercer

Mercer is a global provider of investment services, and offers customized guidance at each stage of the investment

decision, risk management, and investment monitoring process. We have been dedicated to meeting clients’ needs for

more than 40 years, and work with the fiduciaries of retirement funds, foundations, endowments, wealth management

firms and other investors in more than 60 countries. We offer clients a continuum of services in order to tailor solutions

specific to their unique requirements and governance objectives. Our services include:

For further information contact:

Chris Kohler, Endowments and Foundations, [email protected] or at 630 750 8017

John Nussbaumer, Retirement Plans and Health Care, [email protected] or at 404 442 3280

David Eisenberg, Wealth Management Providers, [email protected] or at 617 747 9454

Missed our recent publications? These materials are available on Mercer.com.

Setting an Appropriate Liquidity Budget: Making the Most of a Long Investment Horizon

Global REITs - A Mercer Point of View

Hedge Fund Managers and the Swiss Black Swan

Defined Contribution - Customizing Target Date Funds

Defined Benefit - Best Ideas for the Hibernation Portfolio

Not-for-Profit - Is A Stronger Dollar Good For Your Investment Portfolio?

MERCER Market Environment Report April 2015 3

Overview

Table of Contents

Performance

International equities outperformed domestic equities in Q1 4

Macro environment

Oil prices stabilized 5

The dollar extended its rally 6-7

Has the Eurozone economy turned the corner? 8

Another first quarter slump for the US economy 10

Weak commodity prices and a slowing China weigh 11

on emerging economies

The Fed dialed back tightening expectations 12-13

Financial markets

Equities remain attractive relative to bonds 14-15

US equities: Earnings face near-term headwinds 16-17

Small-caps expensive, but less exposed to dollar strength 18

Emerging market equities face near-term risks 19

International equities have better earnings growth prospects

than the US 20-21

Treasury yields declined further in Q1 22-23

High yield bonds rebounded in Q1 24

Depreciating currencies hurt returns for local emerging

market debt 25

Dollar strength and excess oil supply weigh on commodities 26

Valuations and interest rate sensitivity are concerns for 27

Global REITs

Hedge funds 28

Liability driven investing: Maintain tactical underhedge, 29

favor credit

Executive Summary

Global equities got off to a solid start in 2015 as easy monetary conditions and

improving growth helped drive European and Japanese equities higher. US

equities, in contrast, posted muted returns. The MSCI ACWI index earned

4.9% in local currencies and 2.3% in US$.

While US growth disappointed in Q1, data for other developed markets was

encouraging. The IMF projects advanced economies will expand by 2.4% this

year, which would be the strongest year since 2010 and a solid improvement

from the 1.8% rate in 2014.

Diverging monetary policies seem to be the primary driver of currency markets.

The trade-weighted dollar continued its ascent during the first quarter, rising by

8.1%. We believe the dollar is likely to continue to rise, although at a slower

pace than it did during the last six months.

The Fed reined in tightening expectations at its March meeting, but still

appears likely to lift rates in 2015, which could introduce more volatility into

asset prices and lead to the long-awaited correction in equity markets.

Nevertheless, global monetary policy will remain extremely easy for the

foreseeable future due to policies in Europe and Japan.

While equity valuations are elevated and prospective returns are below

average, we continue to favor them relative to bonds. The prospective equity

risk premium on equities remains attractive, and low bond yields could put

further upward pressure on valuations.

We continue to favor non-US developed equities over US equities. Non-US

stocks are more reasonably priced than US equities. Furthermore, weak

currencies and improving growth should help Eurozone and Japanese

companies grow earnings. Meanwhile, the strong dollar and the potential for

wage increases have dampened the outlook for US profits.

We are cautious on the near-term outlook for emerging market stocks relative

to developed stocks and would not be surprised to see them continue to

underperform. Nevertheless, we continue to favor strategic overweights.

Given current spreads and yields, we maintain a preference for high yield

bonds over Treasuries, but favor global equities to high yield bonds.

With traditional assets priced to provide lower returns going forward, we

continue to suggest investors seek additional return drivers, such as manager

alpha, illiquidity and other non-traditional risk factors.

MERCER Market Environment Report April 2015 4

International equities outperformed domestic equities in Q1

1.0

4.9 3.5

10.2

3.1 2.2

1.0

10.9

11.6

10.2

8.0

4.9

0

2

4

6

8

10

12

14

US (S&P500)

MSCI EAFE Europe Japan Pacific ExJapan

EmergingMkts

(%)

First Quarter Returns for Global Markets US $

Local Currency

Source: MSCI, Datastream

Non-US equities substantially

outperformed in Q1 benefiting

from an improved growth

outlook.

Dollar strength

weighed on US$

returns, although

internationals still

outperformed in

unhedged terms.

3.1

-2.1

5.4

2.4

6.6

2.0

0.5

2.7

-4

-2

0

2

4

6

8

Gro

wth

Va

lue

Gro

wth

Va

lue

Gro

wth

Va

lue

De

fen

siv

e

Dyna

mic

Russell Top 200 Russell Midcap Russell 2000 Russell 1000

(%)

First Quarter Style Performance

Source: Datastream

Growth outperformed value

across all capitalizations in Q1.

Defensive indexes lagged

during the quarter.

-5.9

-4.4

-4.0

-1.5

0.0

1.0

1.1

1.4

1.6

2.2

2.3

2.5

2.5

4.0

4.2

4.3

4.9

5.6

-10 -5 0 5 10

Commodity Futures

Intl Fixed

Emerg Mkt Debt (Local)

Natural Res Stks

T-Bills

US Large-Cap Stks

US MBS

US TIPS

US Treasuries

Emerg Mkt Stks

US I/G Corp Bonds

Fund of Hedge Funds

US High Yield Bonds

US Mid-Cap Stks

Global REITs

US Small-Cap Stks

Intl Large-Cap Stks

Intl Sm-Cap Stks

First Quarter Performance (%)

Source: Datastream

Small-caps outperformed large-caps

in Q1. Dollar strength may have

weighed on multinational large-cap

firms, while small-caps are more

domestically focused.

Funds of hedge funds

outperformed global

stocks and US bonds.

The MSCI ACWI index earned

2.3% and the Barclays Aggregate

index returned 1.6%.

Credit outperformed

Treasuries.

The real yield on 5-

year TIPS fell from

0.52% to –0.14%.

LCEMD losses were due to currency

declines. $US-denominated debt

returned 1.9%.

The yield on the 10-year

Treasury dropped from

2.17% to 1.94% in Q1.

The S&P 500 lagged most

markets in Q1.

MERCER Market Environment Report April 2015 5

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

4

5

6

7

8

9

10

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

Rig

Co

un

t

Millio

n B

arr

els

per

Day

US Oil Production

Barrels per Day (MM, Smoothed, LHS) US Oil Rig Count (RHS)

The US rig count measures the number of rigs actively drilling

oil wells. The count has declined by nearly 50%, driven by

idling of low efficiency rigs. New supply from active, high

productivity rigs is still outpacing the production decline from

existing wells. Supply could continue to rise in the near-term,

but a sustained drop in rig count should eventually lead to

lower production as existing wells are depleted.

Oil prices stabilized

Oil fell from $53 to $48 a barrel in Q1, although prices recovered to the

mid-$50s in early April. Rising inventories suggest continued

oversupply. However, the estimated global excess supply of 1M

barrels per day represents only about 1% of total demand. Lower

prices and improving global economic growth should help lift demand,

absorbing some of the current excess supply. Going forward, supply

dynamics will likely be a key factor in determining future prices.

US production has accounted for nearly 60% of global crude oil supply

growth since 2011. While production has continued to increase due to

projects started before the price collapse, energy companies are

slashing capital expenditures. US production could potentially level-off

later this year due to the rapid depletion rate of shale wells.

Technological enhancements continue to drive the cost of US shale

drilling lower, which means prices may not have to rise much to get

investment flowing again.

A nuclear deal with Iran could release more supply, but a supply

disruption is a constant risk in the Middle East.

The decline in oil prices should help global growth because

consuming countries generally have a higher propensity to spend than

producing countries. However, a renewed downturn could destabilize

some regimes, leading to greater geopolitical risks.

Source: Bloomberg

200

250

300

350

400

450

500

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

Millio

n B

arr

els

US Crude Oil Inventory

20

40

60

80

100

120

Jan

-14

Fe

b-1

4

Mar-

14

Ap

r-1

4

May-1

4

Jun

-14

Jul-

14

Au

g-1

4

Se

p-1

4

Oct-

14

No

v-1

4

De

c-1

4

Jan

-15

Fe

b-1

5

Mar-

15

Ap

r-1

5

$ P

er

Barr

el

WIT Oil Futures Prices

1M

12M

36M

Source: Bloomberg

Source: Bloomberg

US inventory has jumped by 25% since the start of the year,

suggesting oversupply in the US. With the futures prices

trading higher than spot, there is an incentive to hold oil for

sale at higher prices in later months.

Following the free-fall in 2H14 and

January, prices stabilized in the

remainder of Q1 and have rebounded in

early April.

MERCER Market Environment Report April 2015 6

-35

-30

-25

-20

-15

-10

-5

0

5

Sw

iss F

ran

c

Ta

iwa

n D

olla

r

India

n R

upe

e

Ch

inese Y

ua

n

Jap

an

ese

Ye

n

Ko

rea

n W

on

Mexic

an P

eso

Ne

w Z

eala

nd $

GB

Pou

nd

Au

str

alia

n D

olla

r

Ca

na

dia

n D

olla

r

Eu

ro

Bra

zili

an

Re

al

(%)

Performance of Foreign Currencies Versus the Dollar Q1

1-Year

The trade-weighted dollar continued its ascent during the first quarter,

rising by 8.1%. It advanced by as much as 9.7%, but pared gains after

the March FOMC meeting. The euro tumbled 11.3%, and most

commodity sensitive currencies and emerging market currencies also

declined. We believe the dollar is likely to continue to rise, although at

a slower pace than it did during the last six months.

Monetary policy seems the primary driver of currency markets. The

dollar has a significant yield advantage on intermediate- and long-

term bonds. With many European cash rates now negative and the

Fed likely to begin lifting rates in 2015, the gap should widen on the

short-end as well.

The 10-year US Treasury ended the quarter yielding 1.9%

compared to 0.2% in Germany and 0.4% in Japan. With global

savings running high, the dollar should continue to benefit from

foreign capital inflows.

Some of the liquidity from the ECB’s €1.1T QE program could leak

into the US due to relatively attractive yields.

The dollar’s surge over the last nine months has pushed it into

overvalued territory. While not at unprecedented levels, the dollar is

rich against most major currencies based on purchasing power parity

(PPP). A widening current account deficit is another intermediate-term

bearish factor for the dollar. While both valuations and the current

account deficit suggest the dollar has already run too far, they are not

likely to prevent an overshoot over the short-term.

Perhaps the biggest risk for the dollar is if the Fed proves less

aggressive in hiking rates than the market expects. A strong dollar

impedes US growth and reduces inflation, which could potentially

keep the Fed on the sideline for longer. Calculations by the IMF

suggest that a 10% appreciation in the real trade-weighted dollar has

an equivalent effect as a 100 basis-point rate hike. A perceived

change in the outlook for interest rate differentials could cause a

stampede out of the dollar as speculators have record long exposure.

The dollar extended its rally

Source: Bloomberg

The Swiss Franc surged 20% in

mid-January as the central bank

abandoned its cap relative to the

euro, but has since given back

most of those gains.

The euro fell by 11.3% against the

dollar in Q1, the largest quarterly

decline in the history of the

common currency.

The yen had a quite quarter, falling just 0.3%

-20

-10

0

10

20

30

40

50

197

3

197

6

197

9

198

2

198

5

198

8

199

1

199

4

199

7

200

0

200

3

200

6

200

9

201

2

201

5

Rela

tiv

e t

o G

eo

metr

ic M

ean

(%

)

US Dollar - Real Effective Exchange Rate

The real trade-weighted

dollar would need to

appreciate another 12%

to return to the 2002

high.

Source: Bloomberg

The dollar pulled back

8% in 1998, before

continuing to trend

higher.

MERCER Market Environment Report April 2015 7

-40

-30

-20

-10

0

10

20

30

40

50

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

(%)

Currency Valuation Versus US Dollar

(Based on Relative PPP)

Euro UK Pound

Yen Australian$

The yen trades at a 27% discount

to the dollar, while the euro is at a

10% discount.

50

150

250

350

450

550

650

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

Jul-

16

(1/2

008=

100)

Central Bank Balance Sheet Growth

US EMU UK Japan

The dollar extended its rally (cont.)

The Fed’s and the Bank of England’s balance

sheets are expected to remain flat going

forward, while the ECB and the Bank of Japan

are expected to expand their balance sheets.

The ECB’s QE program should take its balance

sheet back to 2012 levels.

Projections >>>

Source: Bloomberg, Mercer

Source: Bloomberg

Dollar Expensive

Dollar Cheap

-6

-4

-2

0

2

4

6

8

Sw

itzerl

an

d

Eu

rozo

ne

Ch

ina

Jap

an

India

Mexic

o

US

Ca

na

da

Bra

zil

Au

str

alia UK

Current Account Balances

(2015 estimates, % of GDP)

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

US

UK

Germ

any

Sp

ain

Sw

itzerl

an

d

De

nm

ark

Sw

ede

n

Jap

an

(%)

Selected Government Bond Yields

Target 5-year 10-year

Source: Bloomberg

Source: IMF

5y German bonds

finished the quarter with

a negative yields.

Switzerland and Denmark

have lowered policy target

rates to -0.75% to discourage

exchange rate appreciation

against the euro.

Current account balances argue against further

deprecation of the euro/USD. The Eurozone’s

current account surplus exceeds 3% of GDP,

compared to a 2% deficit for the US. This is

likely to widen further in 2016 at current

exchange rates.

The weak euro has mostly

benefitted the exports of

Germany, which is not in need of

the subsidy.

MERCER Market Environment Report April 2015 8

-100

-75

-50

-25

0

25

50

75

100

125

De

c-1

2

Mar-

13

Jun

-13

Se

p-1

3

De

c-1

3

Mar-

14

Jun

-14

Se

p-1

4

De

c-1

4

Mar-

15

Citigroup Economic Surprise Index US

Eurozone

Japan

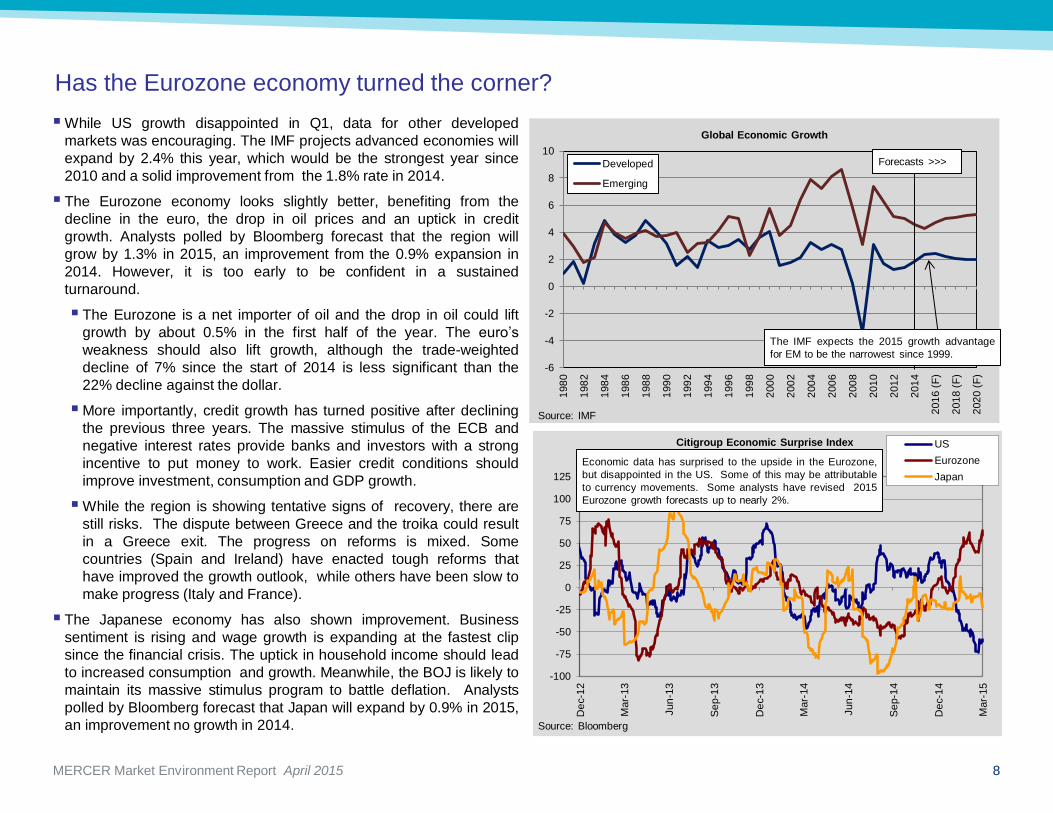

Has the Eurozone economy turned the corner?

While US growth disappointed in Q1, data for other developed

markets was encouraging. The IMF projects advanced economies will

expand by 2.4% this year, which would be the strongest year since

2010 and a solid improvement from the 1.8% rate in 2014.

The Eurozone economy looks slightly better, benefiting from the

decline in the euro, the drop in oil prices and an uptick in credit

growth. Analysts polled by Bloomberg forecast that the region will

grow by 1.3% in 2015, an improvement from the 0.9% expansion in

2014. However, it is too early to be confident in a sustained

turnaround.

The Eurozone is a net importer of oil and the drop in oil could lift

growth by about 0.5% in the first half of the year. The euro’s

weakness should also lift growth, although the trade-weighted

decline of 7% since the start of 2014 is less significant than the

22% decline against the dollar.

More importantly, credit growth has turned positive after declining

the previous three years. The massive stimulus of the ECB and

negative interest rates provide banks and investors with a strong

incentive to put money to work. Easier credit conditions should

improve investment, consumption and GDP growth.

While the region is showing tentative signs of recovery, there are

still risks. The dispute between Greece and the troika could result

in a Greece exit. The progress on reforms is mixed. Some

countries (Spain and Ireland) have enacted tough reforms that

have improved the growth outlook, while others have been slow to

make progress (Italy and France).

The Japanese economy has also shown improvement. Business

sentiment is rising and wage growth is expanding at the fastest clip

since the financial crisis. The uptick in household income should lead

to increased consumption and growth. Meanwhile, the BOJ is likely to

maintain its massive stimulus program to battle deflation. Analysts

polled by Bloomberg forecast that Japan will expand by 0.9% in 2015,

an improvement no growth in 2014.

Economic data has surprised to the upside in the Eurozone,

but disappointed in the US. Some of this may be attributable

to currency movements. Some analysts have revised 2015

Eurozone growth forecasts up to nearly 2%.

-6

-4

-2

0

2

4

6

8

10

198

0

198

2

198

4

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

201

6 (

F)

201

8 (

F)

202

0 (

F)

Global Economic Growth

Developed

Emerging

Source: IMF

Source: Bloomberg

The IMF expects the 2015 growth advantage

for EM to be the narrowest since 1999.

Forecasts >>>

MERCER Market Environment Report April 2015 9

Has the Eurozone economy turned the corner? (cont.)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Mar-

10

Se

p-1

0

Mar-

11

Se

p-1

1

Mar-

12

Se

p-1

2

Mar-

13

Se

p-1

3

Mar-

14

Se

p-1

4

Mar-

15

(%)

Eurozone 2-Year Inflation Expectations 2-Years Forward

-8

-6

-4

-2

0

2

4

De

c-1

0

Mar-

11

Jun

-11

Se

p-1

1

De

c-1

1

Mar-

12

Jun

-12

Se

p-1

2

De

c-1

2

Mar-

13

Jun

-13

Se

p-1

3

De

c-1

3

Mar-

14

Jun

-14

Se

p-1

4

De

c-1

4

(%)

Eurozone Growth in Household and Non-financial Corporate Loans

(Rolling 3-month annualized)

-4

-3

-2

-1

0

1

2

3

199

1

199

3

199

5

199

7

199

9

200

1

200

3

200

5

200

7

200

9

201

1

201

3

201

5

(%)

Japanese Wage Growth

BCA estimates that from 2012 to

2014 credit in the Eurozone shrank

by around €300B a year,

substantially weighing on growth.

Credit growth turned positive in early

2012, but quickly plummeted as the

debt crisis intensified. Today, Eurozone

yields are at record lows, and the ECB

is expanding its balance sheet by

€720B a year.

Inflation expectations made a welcome move upwards in the

first quarter. Still, they remain below the ECB’s target of 2%,

with the market pricing in inflation of only 1.2% between 2017

and 2019. This suggests that the ECB is likely to maintain its

QE program until the end of 2016 at the earliest.

Nominal wage growth in Japan is at

its highest level since before the

financial crisis. Higher wage growth

could translate into increased

consumption and higher GDP growth.

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Fe

b-1

3

Ap

r-1

3

Jun

-13

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Jun

-14

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

(%)

2015 GDP Growth

Consensus Expectations

US Eurozone

UK Japan

US growth expectations will likely

decline further if Q1 growth is as

low as expected.

The Eurozone’s growth outlook has

been revised upward this year and

may improve further.

Source: Bloomberg

MERCER Market Environment Report April 2015 10

-6

-4

-2

0

2

4

6

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

(%)

Year-Over-Year Growth in Employment and Hourly Wages

Non-farm Payrolls

Average Hourly Wages

Another first quarter slump for the US economy

The US economy sputtered in the first quarter. Economists forecasted

2.8% growth at the start of the quarter, but now predict growth of only

1.3% (which could be too optimistic). Some temporary factors

contributed to this, including the weather and the West Coast ports

strike. The strength of the dollar and the decline in energy investment

were also drags. The decline in energy prices should be a positive for

growth in 2015, but the benefits were only partially realized in Q1

because households saved much of the windfall.

Employment growth in the quarter was disappointing relative to recent

history, although solid in absolute terms. Payrolls increased by an

average of 197k per month in Q1, down from 324k in 4Q14, while

unemployment slipped from 5.6% to 5.5%. Household income is

growing at a solid pace, which should continue to support spending.

With the reduction in energy investment, business investment is a wild

card. Energy represents 10% to 15% of total business investment, but

that drag could be overcome by other sectors of the economy.

Given the temporary factors, it is probably a mistake to read too much

into Q1 results. Indeed, it is reminiscent of 1Q14 when the economy

contracted 2.1% due largely to poor weather. The economy

rebounded strongly in subsequent quarters. Economists expect a

similar pattern in 2015. Forecasts for full year growth for 2015 have

only come down slightly, from 3.0% to 2.9%.

0

4

8

12

16

20

195

0

195

3

195

6

195

9

196

2

196

5

196

8

197

1

197

4

197

7

198

0

198

3

198

6

198

9

199

2

199

5

199

8

200

1

200

4

200

7

201

0

201

3

(%)

Trade as % of GDP Exports

Imports

30

35

40

45

50

55

60

65

70

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

ISM Business Activity Indexes

Manufacturing

Services

The Q1 hiring represents 1.7% annualized

employment growth, significantly faster

than working-age population growth

(~0.5%), meaning labor market slack

would continue to be absorbed.

Hourly wage growth of

2.1% over the last year

was modest, but positive

in inflation-adjusted terms.

Wage growth should

improve further in 2015 as

more labor slack is

absorbed

Source: Bloomberg, BLS

Source: Bloomberg Source: Bureau of Economic Analysis

Trade is a fairly small portion of the US economy,

but higher than in the previous two periods of

dollar strength.

Exports’ share of GDP fell by 2 percentage points

during the mid-80s dollar bull market and by a

similar amount in the late-90s/early-00s bull

market.

The manufacturing index fell to 51.5 in

March, but the services index remains at

healthy levels.

MERCER Market Environment Report April 2015 11

Weak commodity prices and a slowing China weigh on emerging economies

While developed economic growth continues to show signs of

improvement, emerging market growth is decelerating. However,

there were wide divergences across EM economies due to the varying

impact of weak commodity prices (good for importers, bad for

exporters) and the willingness to implement structural reforms.

The outlook in India has continued to improve as inflation has fallen

and investment has expanded, with growth forecasted to rise to

7.4% this year versus 4.7% in 2014.

In contrast, the sharp decline in oil prices and a stalled political

environment have weighed on the Russian and Brazilian

economies, both of which are forecasted to shrink in 2015.

The strength of the dollar continues to be a concern. While it should

help EM exports, tighter US monetary policy could lead to instability

for countries reliant on capital inflows and those with large external

(particularly US$) debt. The decline in commodities amplifies these

pressures for exporters. While the risk of a widespread EM crisis is

low, some countries appear vulnerable, which could have a contagion

impact.

Chinese growth slowed in Q1 as credit and investment activity fell

further. China is also hampered by its managed peg to the US dollar,

which means its currency is appreciating on a trade-weighted basis.

The manufacturing PMI fell below 50 in Q1, suggesting contracting

activity in that sector. While economists polled by Bloomberg expect

7% growth this year, some analysts believe growth is running well

behind the official statistics.

The slowdown in growth has a silver lining as it is being driven by

structural reforms to transition the economy away from credit-led

investment and towards consumption. This should pay dividends

over the long-term.

The slowdown has caused policy makers to loosen monetary

policy, which has contributed to a run in Chinese equities.

7.4

4.7 5.0

1.5 0.2 0.6

3.0

7.0

7.4

5.3

2.2

-0.7

-4.0

3.5

-6

-4

-2

0

2

4

6

8

10

12

14

Ch

ina

India

Indo

ne

sia

So

uth

Afr

ica

Bra

zil

Ru

ssia

Tu

rkey

(%)

Economic Growth

2014 2015 (F)

-6

-4

-2

0

2

4

6

8

10

Mar-

13

Jun

-13

Se

p-1

3

De

c-1

3

Mar-

14

Jun

-14

Se

p-1

4

De

c-1

4

Mar-

15

(%)

2015 GDP Growth

Consensus Expectations China India

Brazil Russia

There is a wide divergence in

growth expectations across EM

countries. EM importers and

reformers are faring well, while

energy exporters and those with

stalled political environments are

struggling.

Chinese growth

has not fallen

below 7% since

1990.

2015 would represent the

worst year for Brazilian

growth since 1990 and since

2009 in Russia.

Brazilian and Russian

growth forecasts continue to

be slashed with both

economies in recession.

Chinese growth estimates

may be revised downward,

while expectations in India

could rise further.

Source: Bloomberg

Source: Bloomberg

MERCER Market Environment Report April 2015 12

The Fed reined in tightening expectations at its March meeting. The

FOMC members’ average target rate expectation for the end of 2015

fell from 1% to 0.6%, which hints the first rate hike could occur at the

September or October meeting. Longer-term bond yields continued to

fall in Q1 with the yield on the 10-year Treasury declining by 23 bps to

1.94%.

While the Fed’s rate forecasts have moved closer to market

expectations, there remains a wide gap, especially beyond 2015. The

Fed projects the target rate will hit 3% by the end of 2017, while Fed

funds futures price a rate of only 1.5%.

Weak Q1 growth notwithstanding, economic conditions suggest the

market’s expectations are too dovish. The unemployment rate is near

its historical average, suggesting wage growth pressures should

increase. While the headline CPI was essentially flat over the last year

due to falling energy prices, core inflation is edging higher.

European monetary policies likely explain the disconnect between US

economic conditions and rates. The yields on US Treasuries appear

very attractive to European investors facing negative rates. As such,

liquidity from European QE could find its way to the US bond market.

This might keep intermediate- and long-term yields depressed even

when the Fed starts to lift short-term rates, flattening the yield curve.

The allure of US bonds could put the Fed in a difficult position. If the

Fed sets interest rates appropriately for US conditions, it could lead to

more foreign inflows and a further strengthening in the dollar, hurting

exporters. Conversely, if the Fed keeps rates low to discourage

inflows, it risks an overheating economy and inflation.

The Fed still appears likely to lift rates in 2015, which is a concern

given the support zero rates have provided to capital markets since

2009. Higher short-term rates are likely to lead to higher volatility and

perhaps even a correction; however, global monetary policies remain

very accommodative on balance. Furthermore, the process of rate

normalization in the US is likely to be gradual and dependent on an

improving economy. As such, we think markets should be able to

overcome this headwind.

The Fed dialed back tightening expectations

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Cu

rren

t 1 2 3 4 5 6 7 8 9

10

Implie

d F

orw

ard

Tre

asury

Yie

ld (

%)

Years

10-Year Treasury Forward Rates

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

3/31/2015 12/31/2015 12/31/2016 12/31/2017 Long-Run

Expectations for Fed Funds Target Rate

Fed Fund Futures (Dec. 2014)

Fed Fund Futures (April 2015)

FOMC Average (Dec. 2014)

FOMC Average (Mar. 2015)

Economic theory and history suggest that Treasury yields should approximate

nominal GDP growth over the long-term. Consensus forecasts project long-term

nominal GDP growth of 4.6%. However, the yield curve has the 10-year Treasury

rising to only 2.5% by 2025. Bond yields are well below where they should be

unless one has a very pessimistic view of growth prospects, or a dovish view of

Fed policy. An alternate explanation is that monetary policies overseas are

driving funds into US Treasuries, keeping rates low.

The Fed revised its growth expectations

downward in Q1, although it continues

to envision more rapid tightening than

the bond market.

Source: Federal Reserve, Bloomberg

Source: Bloomberg

MERCER Market Environment Report April 2015 13

0

1

2

3

4

5

6

0

2

4

6

8

10

12

198

4

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

Ch

an

ge i

n A

vera

ge H

ou

rly

Earn

ing

s (

12M

, %

)

Un

em

plo

ym

en

t R

ate

(%

)

Wage Growth and Unemployment

Unemployment Rate (LHS)

Average Hourly Earnings (RHS)

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Dec-13 Feb-14 Apr-14 Jun-14 Aug-14 Oct-14 Dec-14 Feb-15

10-Year Yields on Select Government Bonds

Germany Swiss

UK US

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Mar-

09

Se

p-0

9

Mar-

10

Se

p-1

0

Mar-

11

Se

p-1

1

Mar-

12

Se

p-1

2

Mar-

13

Se

p-1

3

Mar-

14

Se

p-1

4

Mar-

15

(%)

Inflation Breakeven Rate on TIPS

5-year

5-yr / 5 yrs Forward

The Fed dialed back tightening expectations (cont.)

While the Fed directly controls short-term rates, it has only indirect control over

intermediate-term rates, which are also closely linked to supply/demand. Low rates

overseas suggest strong demand for Treasuries, which should act as an anchor on

intermediate rates.

There is a strong link between the unemployment rate and

wage growth, which suggests high wage growth in 2015.

However, the unemployment rate may understate labor

market tightness given the decline in participation rates.

The 5y/5y inflation breakeven rate is

currently below the Fed’s target.

Source: Bloomberg

Source: Bloomberg, BLS Source: Bloomberg

-4

-2

0

2

4

6

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

(%)

Rolling 12-Month Inflation

CPI

CPI Core

The CPI is down slightly over 12

months. It will rebound towards the

core CPI unless oil prices keep falling.

Core inflation is edging higher and is

not far from the Fed’s target.

Source: Bloomberg

MERCER Market Environment Report April 2015 14

Global equities got off to a solid start in 2015 as easy monetary

conditions and improving growth helped drive European and

Japanese equities higher. US equities, in contrast, posted muted

returns. The MSCI ACWI index earned 4.9% in local currencies and

2.3% in US$.

The global growth outlook is favorable, especially compared to the

recent past, which should be supportive of equity earnings. While

some EM economies continue to struggle, US growth should recover

from its Q1 disappointment, and the prospects for the Eurozone and

Japan are improving.

A Fed rate hike in 2015 and the evolution of forward guidance could

introduce more volatility into asset prices and finally lead to the long-

awaited correction in equity markets. Nevertheless, global monetary

policy will remain extremely easy for the foreseeable future due to

policies in Europe and Japan.

With yet another strong quarter driven mostly by valuation expansion,

most indicators suggest global equity valuations are rich on an

absolute basis, but not alarmingly so.

While equity valuations are elevated and prospective returns are

below average, we continue to favor them relative to bonds. More than

half of outstanding Eurozone debt trades at negative yields, with

German yields negative out to 9 years. The prospective equity risk

premium on equities remains attractive, and low bond yields could put

further upward pressure on valuations.

We continue to favor non-US developed equities over US equities.

Non-US stocks are more reasonably priced than US equities.

Furthermore, weak currencies and improving growth should help

Eurozone and Japanese companies grow earnings. Meanwhile, the

strong dollar and the potential for wage increases have dampened the

outlook for US profits.

With equity valuations high and bond yields absurdly low, the

prospective absolute return on balanced portfolios is low. We continue

to suggest investors seek additional return drivers, such as manager

alpha, illiquidity and other non-traditional risk factors.

Equities remain attractive relative to bonds, but more caution warranted

The P/E ratio on the MSCI World

index is near the long-term median.

Source: Datastream

0

5

10

15

20

25

30

35

40

197

5

197

7

197

9

198

1

198

3

198

5

198

7

198

9

199

1

199

3

199

5

199

7

199

9

200

1

200

3

200

5

200

7

200

9

201

1

201

3

201

5

MSCI World P/E Ratio

Normalized Earnings

Reported Earnings

`

-4

-2

0

2

4

6

8

10

12

14

16

18

195

0

195

4

195

8

196

2

196

6

197

0

197

4

197

8

198

2

198

6

199

0

199

4

199

8

200

2

200

6

201

0

201

4

(%)

Real Expected Returns on Stocks and Bonds

Real Yield on 10-yr Treasuries

Normalized Earnings Yield on S&P 500

60/40 Blend Expected Real Return

Source: Datastream, Mercer

Source: Datastream, Bloomberg, S&P, Federal Reserve, Mercer

The trailing P/E ratio on the MSCI World index has risen

from 15 to 19 since the start of 2013.

Theory suggests the

earnings yield provides a

rough estimate of the

future real return on

equities.

With real interest rates near

zero and elevated equity

valuations, the real expected

return on a 60/40 portfolio is

less than 2.5% (assuming no

changes in valuation).

MERCER Market Environment Report April 2015 15

3.8 3.8 6.4

10.7

17.5

25.9 25.6

6.3

0

5

10

15

20

25

30

<-4

0

-40 to

-30

-30 to

-20

-20 to

-10

-10 to

0

0 to

10

10 to

20

>2

0

Pro

babili

ty (

%)

S&P 500 Returns (%)

S&P 500 - One Year Expected Return Distribution Curve

0

1

2

3

4

5

6

7

8

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

(%)

Cost of One-Year Put Options on the S&P 500

Protection Beyond 20% Loss

-2

-1

0

1

2

3

4

5

6

7

8

199

0

199

4

199

8

200

2

200

6

201

0

201

4

(%)

S&P 500 - Equity Risk Premium Versus Long-Term Treasuries

This calculation uses normalized earnings,

which assumes earnings are 26% less than

current levels. Based on reported

earnings, the risk premium was 4.1%.

Based on normalized earnings, the equity risk premium

on the S&P 500 stands at 3%. Due to lower valuations

on non-US stocks, the risk premium on global developed

equities is higher. We estimate that the risk premium on

the MSCI World index is 3.5%.

Source: Mercer, S&P, Bloomberg

Median

since 1956

The cost of one-year tail risk

insurance fell from 2.5% to 2.2%, but

remains above the long-term median.

Source: Parametric, Bloomberg

Equities remain attractive relative to bonds, but more caution warranted (cont.)

The options market prices a 14%

probability of a 20% or worse

decline in 2015, which is above the

historical occurrence of 8%. The expected distribution curve is

negatively skewed (large losses more

likely than large gains), suggesting

option buyers are still willing to pay-up

for downside protection.

S&P 500 Performance Around the

Beginning of Tightening Cycles

-20

-10

0

10

20

30

40

50

May-5

8

Jul-61

Jul-67

Feb-7

2

Jan-7

7

Jul-80

Feb-8

3

Oct-

86

Jan-9

4

Jun-9

9

Jun-0

4

May-5

8

Jul-61

Jul-67

Feb-7

2

Jan-7

7

Jul-80

Feb-8

3

Oct-

86

Jan-9

4

Jun-9

9

Jun-0

4

Six Months Prior 12 Months After

(%)

Historically, the market has earned an

average of 6% in the twelve months following

an interest rate increase. This is below the

overall average of 11%, but the market only

fell in two of eleven observations.

Source: Mercer, Bloomberg

The market has performed well in the 6

months prior to tightening. With a more

transparent Fed, the market could act

before the Fed in the coming cycle.

Source: Bloomberg, Mercer

MERCER Market Environment Report April 2015 16

0

10

20

30

40

50

60

195

6

196

0

196

4

196

8

197

2

197

6

198

0

198

4

198

8

199

2

199

6

200

0

200

4

200

8

201

2

US Shiller's P/E Ratio

S&P 500

MSCI US

US equities: Earnings face near-term headwinds

US equities ended a choppy first quarter up 1.0%. The P/E ratio on

trailing earnings moved from 19.4 to 20.2, which is above the median

of 17.4 since 1956. Valuations continue to appear elevated, especially

on measures that adjust for record profit margins. The P/E ratio based

on average 10Y real earnings (Shiller’s methodology) finished the

quarter at 26.6, compared to a median of 19.3 since 1956.

US earnings are facing mounting downward pressures. Quarterly S&P

500 earnings fell 13.8% year-over-year in Q4. Low oil prices have

gutted energy earnings. Furthermore, the strong dollar has meant a

negative translation effect on foreign sales. Analysts have slashed

2015 EPS estimates by 11% in the last 6 months and now expect a

decline in 2015. While healthy economic growth should support

revenue growth, the earnings growth prospects over intermediate-

term are mixed.

While lower energy prices have had a negative short-term impact

on earnings, they should ultimately reduce input costs, resulting in

a net positive impact. The dollar is a wildcard. Further weakness

will erode profits, but the marginal impact will fade when the dollar

stabilizes. Companies also continue to buyback their own equities,

which increases earnings per share.

With the economy approaching full employment, wage growth

could begin to accelerate, eroding profitability. There are already

signs of a margin squeeze as wage costs are rising faster than

productivity and core consumer prices.

The combination of weak earnings and high valuations are worrisome,

especially with the potential for a Fed rate hike in 2015. Nevertheless,

interest rates remain extremely low and valuations remain fairly

attractive against bonds. While we expect stocks to outperform bonds,

current valuations leave little margin for error.

Source: S&P, MSCI, Bloomberg, Mercer

Shiller’s P/E based on S&P 500 EPS finished the quarter at 26.6, which is 38%

above its historical median. The ratio based on MSCI EPS stood at a more

reasonable 24.2, which is 24% above the historical median.

Introduced in 2001, FAS 142, requires

annual testing of goodwill for impairment

as opposed to amortizing it over 40 years.

FAS 142 impacted S&P 500 (GAAP)

earnings, but not MSCI earnings.

80

90

100

110

120

130

140

Dec-09 Jul-10 Feb-11 Sep-11 Apr-12 Nov-12 Jun-13 Jan-14 Aug-14 Mar-15

(EP

S)

S&P 500 Operating Earnings Estimates

2012

2013

2014

2015

Source: Bloomberg

2015 estimates have fallen sharply.

Earnings estimates for the energy sector

have been cut by over 60% in the last 6

months and the strong dollar has led to

further negative revisions.

MERCER Market Environment Report April 2015 17

-3

-2

-1

0

1

2

3

4

5

6

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

(%)

Productivity and Hourly Wage Growth

Rolling 4 Quarters

Real Compensation Per Hour

Non Farm Business Output

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

1%

2%

3%

4%

Mar-02 Mar-04 Mar-06 Mar-08 Mar-10 Mar-12 Mar-14

(Yo

Y C

han

ge)

Wage Growth vs. Small Business Sentiment

ECI Private Wages & Salaries (LHS)

NFIB planning to raise compensation (RHS, 3Q Advanced)

0%

2%

4%

6%

8%

10%

12%

14%

16%

50%

52%

54%

56%

58%

60%

62%

64%

66%

68%

196

0

196

3

196

6

196

9

197

2

197

5

197

8

198

1

198

4

198

7

199

0

199

3

199

6

199

9

200

2

200

5

200

8

201

1

201

4

Aft

er-

Tax

Pro

fits

Com

pensation o

f E

mplo

ye

es

Employee Compensation and Profits

Share of Non-financial Corporate GDP

Employee Compensation (LS) Corporate Profits (RS)

US equities: Earnings face near-term headwinds (cont.)

Source: Bloomberg

Wage growth has been stubbornly low

since the financial crisis. However, as

the labor market improves, wages

should increase, pressuring margins.

High profit margins have mostly come at the

expense of salaries. Employees currently

receive 57% of corporate value-added (a

proxy for revenues), versus a median of 63%.

A further uptick in

compensation will

likely pressure profits.

Source: Bureau of Economic Analysis

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

-20%

-10%

0%

10%

20%

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

Ro

llin

g 1

2-M

on

th C

han

ge

An

nu

al

Ch

an

ge

S&P 500 Cost of Goods Sold (COGS) and Oil

S&P 500 COGS per Share (LHS) WTI Oil (RHS)

Source: Bloomberg, Mercer

The BEA estimates that energy input costs equate to more than 2% of US

private industry revenues. A decline in oil prices of over 50% should

therefore lower costs and support margins.

More businesses are planning on

raising compensation, a sign that

there is less slack in the labor

market.

Productivity growth has been sluggish

for the last few years. Recently, real

wages have exceeded productivity,

suggesting margin squeeze.

Source: Bloomberg

MERCER Market Environment Report April 2015 18

-20

-15

-10

-5

0

5

10

15

-4

-3

-2

-1

0

1

2

3

1980 1983 1986 1988 1991 1994 1996 1999 2002 2004 2007 2010 2012

Ru

ssell 2

000 -

S&

P 5

00 5

y

(%)

Sta

nd

ard

Dev

iati

on

s f

rom

Mean

Small-caps / Large-caps Valuation and Subsequent Excess Return

(Based on P/E, P/B and P/S)

Relative Valuation (LHS) Subsequent 5y Excess Return (RHS)

18.9

15.7

12.4

16.8

2.1

8.2

25.1

21.6

15.2

19.7

1.5

8.5

35.3

27.8

18.9 19.1

1.3

6.2

0

10

20

30

40

P/E - TrailingReported

P/E - 5 YrAverage

Earnings

P/CF P/E - 1Yr.Forward

(I/B/E/S)

Dividend Yield EPS Growth -Last 10 Yrs

US Equity Valuations by Capitalization

Russell Top 200

Russell Midcap

Russell 2000

Small-caps expensive, but less exposed to dollar strength

In a continuation of Q4 performance, small-cap equities outperformed

large-caps during the first quarter (4.3% vs. 1.0%). Dollar strength and

an active M&A environment are fundamental factors that could benefit

small-caps relative to large-caps. However, small-cap valuations

remain very stretched and large-caps are better positioned to profit

from improving conditions in developed economies overseas.

The performance of small-caps vs. large-caps tends to move in multi-

year cycles. While large-caps have lagged over the past two quarters,

they have outperformed small-caps by 450 bps over the past year.

With valuations on small-caps remaining rich and less scope for

further dollar appreciation, we expect large-caps to maintain a

performance edge over the intermediate-term.

Growth stocks outperformed value equities during Q1 across all

capitalizations. Value stocks were negatively impacted by larger

exposure to the financial, energy and utility sectors, which finished the

quarter in the red. While segments of the growth stock universe

(biotech, social media) are overvalued, growth stocks more broadly

appear fairly valued relative to value stocks, and we continue to

recommend no style bias versus the strategic policy.

Small-caps underperformed

for this full period, which

means valuations should have

been lower. We estimate fair

value at -0.4 to -0.7.

Small-caps still appear

expensive based on this blend

of valuation measures.

Small-caps Unattractive

Small-caps attractive

Source: Russell

Source: NDR, Datastream, Mercer

Mid-caps are expensive

relative to large-caps, but less

so than small-caps.

The valuation of growth

to value is near the long-

term mean.

Source: Russell

-20

-15

-10

-5

0

5

10

15

20

0.0

0.3

0.5

0.8

1.0

1.3

1.5

1.8

2.0

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

Su

bseq

uen

t 5-Y

r R

ela

tiv

e P

erf

orm

an

ce

(%)

R1000G

/R1000V

Rela

tiv

e t

o M

ean

Valuation of Russell 1000 Growth to Value

and Subsequent Performance

Valuation of R1000G/R1000V

Subsequent 5-Yr Relative Return (R1000G - R1000V)

Source: Russell, Bloomberg

Value attractive

Growth attractive

MERCER Market Environment Report April 2015 19

0

5

10

15

20

25

30

35

He

alth C

are

Co

ns. S

tap

les

Indu

str

ials

Mate

rials

Te

lecom

Co

ns. D

isc.

Utilit

ies

Info

Te

ch

Fin

ancia

ls

En

erg

y

(%)

P/E By Sector

MSCI Emerging Markets

MSCI World

Emerging market equities face near-term risks

Emerging market stocks rose 4.9% in local currency terms and 2.2%

in US$ during Q1. There was wide dispersion in US$ returns across

countries. Chinese and Indian stocks gained 8.1% and 5.4%,

respectively, while Brazilian stocks fell 14.6%. Russian stocks

rebounded 18.6%, but are 25.1% lower for 12 months.

Valuations on emerging market stocks are mixed. With a trailing P/E

of 14, they appear fairly attractive on the surface. However, this is

largely because of energy and financials, which are arguably cheap

for a reason. The median sector in the EM index trades at a less

appealing P/E of 16. Valuations vary widely across countries. Indian

stocks trade at a P/E of 20, as investors have priced-in the improved

outlook. Chinese stocks, with a 38% weight to financials, trade a P/E

of 11. Russia appears to be a bargain, but has serious geopolitical

risks and is sensitive to energy prices.

We are cautious on the near-term outlook for EM stocks and would

not be surprised to see them continue to underperform developed

markets. Earnings are likely decline in 2015 due to the concentration

in commodity sectors. Slowing growth in China, the largest export

market for many EM countries, represents another risk. Finally, Fed

tightening could lead to capital flight. We anticipate that the wide

divergence in economic conditions across countries, and valuations

and earnings across sectors will persist. As such, we continue to

advocate for the use of active management.

0

5

10

15

20

25

30

Se

p-9

5

Mar-

97

Se

p-9

8

Mar-

00

Se

p-0

1

Mar-

03

Se

p-0

4

Mar-

06

Se

p-0

7

Mar-

09

Se

p-1

0

Mar-

12

Se

p-1

3

Mar-

15

P/E on MSCI Emerging Markets

Cap-Weighted

Median

The median P/E is at a 17% premium

to the cap-weighted P/E. Historically,

the median P/E has been at a 9%

premium.

-60

-50

-40

-30

-20

-10

0

10

20

1996 1997 1998 2000 2001 2003 2004 2005 2007 2008 2010 2011 2013 2014

(%)

Valuation of MSCI Emerging Markets to Developed Markets

(Based on an average of P/E, P/B and P/CF)

Source: Datastream

Source: Datastream Source: Bloomberg

Emerging energy and financial stocks trade

at more attractive valuations than in

developed economies; however, health care,

consumer staples and industrials trade at

substantial premiums.

MERCER Market Environment Report April 2015 20

International equities have better earnings growth prospects than the US

International developed equities posted strong returns in Q1. The

MSCI EAFE index returned 10.9% in local terms, outperforming the

S&P 500 by nearly 10 percentage points, although the strength of the

dollar slashed the return to 4.9% in US$.

European stocks surged 11.6% in local terms in Q1 and 3.5% in US$.

European equities are now fully-valued on trailing earnings, trading at

comparable levels to the US. Profits are likely to be a key driver of

absolute and relative performance.

The profit outlook for Europe is promising. The weaker euro will

have a positive impact on earnings. Furthermore, European

companies tend to have high operating leverage, so the uptick in

economic growth (if sustained) could lead to much higher EPS.

Easy monetary policy should also support equities. European

equities yield nearly 300 bps more than 10Y German bunds (3.1%

vs. 0.2%), so there is a powerful incentive for European investors to

step further out on the risk spectrum.

Potential risks for Eurozone stocks include a left-tail event in

Greece, another fizzled economic recovery and a failure in

earnings to come through.

Japanese stocks jumped 10.2% in US$ (the yen was flat). It was

encouraging to see Japanese equites perform strongly in the absence

of yen weakness. Valuations on Japanese stocks appear relatively

attractive at a P/E of 17 on trailing earnings. Furthermore, companies

still have ample capacity to grow earnings as management teams

slowly become more focused on shareholder value.

The strong local currency gains posted by the MSCI EAFE index over

the last year has closed some of the valuation gap to the US. We still

view international developed stocks as more attractive than US stocks

due to better earnings growth potential. Additionally, looser monetary

policy should provide a nice tailwind, while US stocks could face a

headwind from Fed tightening.

Further dollar strength is a risk due to the divergence in monetary

policies. As such, investors could consider hedging a portion of their

international developed allocation to guard against a dollar overshoot.

European stocks are trading at

29% discount to US stocks versus

a historical average of 12%.

-50

-40

-30

-20

-10

0

10

20

30

40

50

No

v-7

9

Jan

-82

Mar-

84

May-8

6

Jul-

88

Se

p-9

0

No

v-9

2

Jan

-95

Mar-

97

May-9

9

Jul-

01

Se

p-0

3

No

v-0

5

Jan

-08

Mar-

10

May-1

2

Jul-

14

(%)

Discount of MSCI Europe to MSCI US

(Based on Shiller's PE)

Europe trades at a 29% discount to

US equities based on average 10-

year real earnings versus a historical

median of 13%.

Source: Datastream, Mercer

20.0 19.5

17.3

13.7

24.2

16.1

25.3

13.1 12.5

10.0 8.9

8.2

2.9 1.9 1.4 1.6 2.0 3.1 1.7

2.6

0

5

10

15

20

25

30

MSCI US MSCI Europe MSCI Japan MSCI EM

Global Valuations

P/E Trailing

Shiller's P/E

P/CF

P/B

Dividend Yield

ROE in Japan is 21% below its 2007-peak.

Stronger domestic growth, the drop in oil

prices and a weak yen should help lift

profitability.

European equities are

yielding 3.1%, while US

stocks yield only 2.0%.

Source: Bloomberg, Mercer

MERCER Market Environment Report April 2015 21

International equities have better earnings growth prospects than the US (cont.)

0

20

40

60

80

100

120

140

197

0

197

3

197

6

197

9

198

2

198

5

198

8

199

1

199

4

199

7

200

0

200

3

200

6

200

9

201

2

201

5

EP

S i

n l

ocal

cu

rren

cy

term

s

Growth in Earnings Per Share US

Europe

0

5

10

15

20

25

30

35

40

45

No

v-7

9

Jan

-82

Mar-

84

May-8

6

Jul-

88

Se

p-9

0

No

v-9

2

Jan

-95

Mar-

97

May-9

9

Jul-

01

Se

p-0

3

No

v-0

5

Jan

-08

Mar-

10

May-1

2

Jul-

14

P/E Ratio on MSCI Europe

Trailing P/E

Shiller P/E

Over the long-term, European and US firms have grown profits at a

similar pace. The gap in earnings since 2011 likely reflects cyclical

rather than structural factors. The outlook for European shares are

dependent on this gap closing, which may happen as the Eurozone

economy improves.

Historically, European firms have

experienced stronger earnings

growth during bull markets,

reflecting their higher operating

leverage and larger exposure to

cyclical sectors.

Based on Shiller’s PE, European

stocks are trading at a 2%

discount to their historical average

since 1979. US stocks are trading

at a 24% premium.

Source: Datastream, MSCI Source: Datastream, Mercer

0

5

10

15

20

25

30

0.0

1.0

2.0

3.0

4.0

5.0

6.0

197

5

197

8

198

1

198

4

198

7

199

0

199

3

199

6

199

9

200

2

200

5

200

8

201

1

201

4

P/C

F

P/B

Japanese Equity Valuations

P/B

P/CF

Japan trades at a 25% discount

on P/B and a 4% premium based

on P/CF.

Source: Datastream

-3

-2

-1

0

1

2

3

4

198

2

198

4

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

Sta

nd

ard

Dev

iati

on

s f

rom

Mean

Valuation of US$ Based on Relative PPP

(Avg CPI and PPI)

EAFE Basket

EUR

JPY

The dollar appears 12% overvalued

relative to EAFE currencies, but

remains about 10% below the

average level of 2001-02.

Source: Bloomberg, Mercer

MERCER Market Environment Report April 2015 22

-2

-1

0

1

2

3

4

5

3 mo 6 mo 1 yr 2 Yr 3 Yr 5 yr 7 yr 10 yr 20 yr 30 yr

(%)

Treasury Yield Curve

Treasuries at 12/31/13 TIPS at 12/31/13

Treasuries at 12/31/14 TIPS at 12/31/14

Treasuries at 03/31/15 TIPS at 03/31/15

2.5

1.4

3.3 3.3

5.6

3.2

6.8

2.2

1.4

2.6 3.1

6.6

2.1

6.5

2.1

1.3

2.4 2.9

6.2

2.0

6.3

0

3

6

9

Agg. Treas GSE MBS I/G Corp HY Corp Munis Local EMD

(%)

Bond Yields

Dec-13 Dec-14 Mar-15

Treasury yields declined further in Q1

Source: Federal Reserve, Bloomberg

The curve shifted down and modestly flattened in Q1. During

the quarter, the 2-year yield declined by 11 bps to 0.56, while

the 10- and 30-year yields fell by 23 and 21 bps to 1.94%

and 2.54%, respectively.

Source: Barclays, JPMorgan

Yields across all fixed

income sectors

moved lower in Q1.

The Barclays Treasury index rose 1.7% in Q1, as the yields on 10-

and 30-year Treasuries fell by 23bps and 21bps to 1.94% and 2.54%,

respectively. The Barclays Long Treasury index returned 4.0% in Q1

and is up over 21% for the last 12 months.

TIPS slightly underperformed Treasuries during Q1, advancing 1.4%.

For investors with inflation sensitive liabilities, TIPS have appeal

relative to Treasuries. There is a risk of an inflation surprise if the Fed

is too slow to normalize policy. The 1.8% 10-yr breakeven rate on

TIPS provides cheap insurance for this.

We expect interest rates will edge higher, but not expect a sharp

move. The Fed is likely to raise short-term rates at a slow, measured

pace, and the excess supply of global savings should keep a lid on

the long end of the curve. With the ECB and BOJ likely to keep

nominal rates near zero for years to come, demand for relatively high

yielding Treasuries should remain significant.

The Barclays Corporate index gained 2.3% in Q1. During the quarter,

the yield on the Corporate index declined by a modest 20 bps to

3.1%. The option-adjusted spread to Treasuries was unchanged at

1.3%, which is near the long-term median.

Given average spreads and favorable economic conditions, we

maintain a slight preference for investment-grade corporate bonds

over Treasuries. Downside risk for corporates relative to Treasuries

is limited over the short-term.

Over the intermediate-term, credit quality trends are important to

monitor. While interest coverage ratios are high, the credit quality

of the IG corporate bond universe has declined. The tendency of

companies to buyback equities with debt is increasing balance

sheet risks.

While the expected return on government bonds is unattractive, we

don’t expect a significant increase in rates due to overseas demand.

However, the downward shift in the long end of the yield curve makes

the risk of duration exposure very asymmetrical.

The real yield on 5-year TIPS

fell below zero in Q1. The

inflation breakeven rate on 5-

and 10-year TIPS finished at

just 1.5% and 1.8%.

Following a tough

second half of

2014, junk bonds

faired well in the

first quarter.

The yield on local EMD declined,

but currency depreciation led to

losses.

MERCER Market Environment Report April 2015 23

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

199

1

199

3

199

5

199

7

199

9

200

1

200

3

200

5

200

7

200

9

201

1

201

3

201

5

Spread on 10Y US Treasuries to German Bunds

0

10

20

30

40

50

60

70

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

(%)

of

I/G

Bonds O

uts

tandin

g

Quality of Investment Grade Bonds

Aaa Aa

A Baa

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

198

9

199

1

199

3

199

5

199

7

199

9

200

1

200

3

200

5

200

7

200

9

201

1

201

3

(%)

Investment-Grade Corporate Bond Credit Spread

OAS

Median OAS

Quality Adjusted Median OAS

Treasury yields declined further in Q1(cont.)

The spread on investment-grade bonds was flat in Q1.

When factoring in the decline in the quality of the

universe, the current spread is 11 bps above the long-

term median. Given the favorable US economic outlook,

the current spread appears attractive.

Source: Barclays, Mercer

The adjusted

median reflects

the decline in the

credit quality of

the index.

Source: Bloomberg, Mercer

Relatively high bond yields in the US could

continue to attract money from overseas

investors.

The yield advantage of 10y

Treasuries over German

bunds is the highest since

1989.

Source: Bloomberg

The quality of the investment-grade bond

universe is trending lower. The share of the

universe in Baa-rated bonds has reached 44%.

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

0

50

100

150

200

250

300

350

2001 2002 2003 2005 2006 2007 2008 2009 2010 2012 2013 2014

($ T

rillio

n)

($ B

illio

n)

Corporate Bonds Outstanding and Dealer Inventory

Primary Dealer Inventory of Corporate Bonds (LHS)

US Corporate Bonds Outstanding (RHS)

Some analysts worry that

dealers have pulled away

from the corporate market

due to tighter regulations,

making them less likely to

provide liquidity in times of

stress.

While this could result in gap-

down moves in prices, investors

who do not sell into a panic

would likely only suffer temporary

mark-to-market losses.

Source: Federal Reserve, Bloomberg

MERCER Market Environment Report April 2015 24

0% 2%

6% 9%

12%

70%

0% 2% 4% 5%

10%

79%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2015 2016 2017 2018 2019 2020+

(% M

ark

et

Valu

e)

High Yield Bonds by Maturity

High Yield

HY Energy

25

50

75

100

1252

4

6

8

10

30-Jun-14 31-Aug-14 31-Oct-14 31-Dec-14 28-Feb-15

($ p

er

Bbl)

(%)

High Yield OAS vs. Oil Prices High Yield (LHS)

HY Energy (LHS)

HY ex. Energy (LHS)

WTI Oil (RHS, Inverted)

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

0

2

4

6

8

10

12

14

16

18

20

1994 1997 2000 2003 2006 2009 2012 2015

(%)

High Yield OAS vs. 10-year Treasury Yield

High yield OAS 10-yr Treasury Yield

The yield on the Barclays High Yield index declined from 6.6% to

6.2% during the first quarter, leading the index to a 2.5% gain. The

option adjusted spread narrowed by 17 bps and finished the quarter at

4.7%, which is modestly below the long-term median.

Despite a 10.6% drop in oil prices, the energy sector stabilized in Q1

and returned 2.4%. A sustained period of low oil prices will likely lead

to a spike in defaults for energy firms. Given our expectation of a

strengthening economy, the risk of broad systemic defaults appears