Embed Size (px)

Citation preview

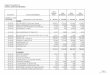

Market Developments3Q 2016

Data source: IHS Fairplay

(Production in CGT)

Europe

Japan

South Korea

China

RoW

1990 2000 2010 2015 2018

Evolution of Shipbuilding Capacity

Data source: Clarkson, European Commission

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

New orders

Deliveries

Quelle: IHS Fairplay 08/2016

2016: Projection based

on 1st HY

12,4% 3,4%

Global Shipbuilding Development in 1.000 GT

GDP / trade growth elasticity changing

6

5.China Shipbuilding Employment

553

374

0

100

200

300

400

500

600

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016.6

1,000 persons

With the adjustment of the shipbuilding market, the employment of shipbuilding

industry has been declining since 2011.

Till the end of Jun. 2016, the employment of China shipbuilding industry was about

374 thousands, fell by 32% compared with the 2011 peak of 553 thousands.

Data Source: CANSI

Shipbuilding Employment & Wage

- The number of employees and wage level of the industry in Korea had been in upward trend except the year 2009, but this trend is likely to decline in the years to come due to ongoing industry restructuring.

0

20

40

60

80

100

120

140

160

180

200

1998 2001 2004 2007 2010 2013 2016.1H

Thousands

Subcontractors Technical & Skilled Workers

Engineers Management &

Administration

(Thousand

Workers)

Average Monthly Wages in Manufacturing

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2008 2009 2010 2011 2012 2013 2014 2015 2016.

2Q

CAGR : 4.4%

(Thousand

KRW)

Shipbuilding Employment Trend

* Note : As of end of each year (KOSHIPA members only) * Source : Korean Ministry of Employment & Labor

-3-

8

Workforce in SAJ

0%

10%

20%

30%

40%

50%

60%

0

20

40

60

80

100

120

140

160

180

75 80 85 90 95 00 05 10 15

Staff Factory Worker Subcontract Worker % of Subcontract Worker (right axis)

as of April

2016

Staff 9.8

Factory Worker 13.5

Subcontract Worker 31.0

Total 54.3

(1,000 persons)

Source: SAJ

Shipyard Employment & Turnover in Germany

9

0

1

2

3

4

5

6

7

8

9

0

10

20

30

40

50

60

70

80

90

1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

Um

sätz

e in

Mrd

. €

Bes

chäf

tigt

e in

10

00

Employment

Turnover (in current prices)

ab 2007 Beschränkung auf Betriebe ab 50 Beschäftigte (bisher 20 Beschäftigte)

Quelle: Statistisches Bundesamt, Darstellung: VSM

Data source: IHS Fairplay

Data source: IHS Fairplay

Data source: IHS Fairplay

Data source: IHS Fairplay

Value of New Contracts (in US bn $)

0

5

10

15

20

25

30

35

40

45

50

2013 2014 2015 3Q 2016

KOREA

CHINA

EUROPE

JAPAN

RoW

Source: Clarkson

Data source: IHS Fairplay

Data source: IHS Fairplay

Data source: IHS Fairplay

Data source: IHS Fairplay

Data source: IHS Fairplay

Data source: IHS Fairplay

Data source: IHS Fairplay

• Total global investment from Jan to Oct = 26 bn $ • 12.9 bn invested on new Cruise ships

Data source: Clarksons

Relative Development of Marketsegments

19.01.2017

0

50

100

150

200

250

2013 2014 2015 2016 Hj.1

Ind

ex 2

01

3=1

00

Tanker

Bulker

Container/Dry Cargo

Passengerships

NCCV

Datasource: IHS FairplayIndex based on new ordersin CGT

= Non Cargo Carrying Vessels

Data source: Clarksons

Data source: Clarksons

Data Source: X-rates

Data source: Meps.co.uk

Thank You!

More info: www.seaurope.eu

TRADE

TTIP: Negotiations of the Jones Act

• 15th Round of EU-US Negotiation

• To be noted.

• Consolidated version of market assessment of different business segments in the context of TTIP negotiations

• Comments

• ECORYS’ Trade Sustainability Impact Assessment (TSIA) final Interim Technical Report on TTIP

• Comments

• US elections: quid nunc?

International WG on Export Credit

• Next steps?

EU-South Korea • South-Korean state subsidies

• Suggestions for Board discussion on 17.11.2016

• OECD WP6 and South-Korea• SEA Europe position at WP6 on 2 December 2016• Input to 6 questions raised by DG Trade • Answer to question from South Korea• Actions and/or positions expected from the European

Commission towards South-Korea during the WP 6 meeting on 2 December 2016.

• IMF Working Paper • Discuss findings

• Draft inception report of the evaluation of the EU South Korea FTA implementation• SEA Europe position

EU- China • Shipbuilding Dialogue

• Suggestions for discussion items

• EU-China Investment Agreement negotiations • Next steps

• Market economy status of China• Implications • Next steps• Meeting in EP

• Outcome of the 6th EU China High-level Economic and Trade Dialogue• To be noted

ANTI-DUMPING DUTIES ON IMPORTS OF CERTAIN CHINESE STEEL PRODUCTS

• Commission anti-dumping duties

• Impact for our industry

• Commission Communication towards a robust trade policy for the EU in the interest of jobs and growth

• Discuss content + possible SEA position

• Commission proposal

• New proposal issued on 9.11.2016

COMMISSION PROPOSAL – DUAL USE

• Comments on content of the proposal

• Next steps

AOB

• CETA

• SEA Europe meeting with trade experts

• TiSA

• SEA Europe strategy paper on trade issues

• Other topics of interest?

MEETINGS IN 2017

THE END