Embed Size (px)

Citation preview

MARKET CITY AND THE WA HORTICULTURE VALUE CHAIN

Stephen Ward

CEO Perth Markets Limited

16th August 2018

CONTENTS

Stephen Ward, CEO Perth Markets LimitedAugust 2018

The Horticulture Industry Value Chain in WA.• Value Chain Participants, and Market Changes over the Last 2 Years

• WA Grown Produce

• Exports

• Economics and Demographics

The Market City Complex• Key Statistics & Facts

• Market City Competitive Strategic Position

• Corporate History

• Transition from Government Ownership

• Financial Results

• New Cool Chain Warehouse and Site Development

Perth Markets Limited (PML) has commissioned independent research group

freshlogic to map and define the total WA Horticulture Market. This includes

determining the wholesale market share of tenants operating from the Market

City site.

The analysis was undertaken for the year ending 30 June 2017 and 2018 and

has been undertaken since 2011 giving 8 years of consistent data.

WA HORTICULTURE VALUE CHAIN

• The total WA market volume increased but value decreased marginally over the two years in review with a number of +ve & -veevents effectively almost balancing out at a State level.

• This indicates that fruit and vegetable volumes increased marginally more than market values for the years in review.

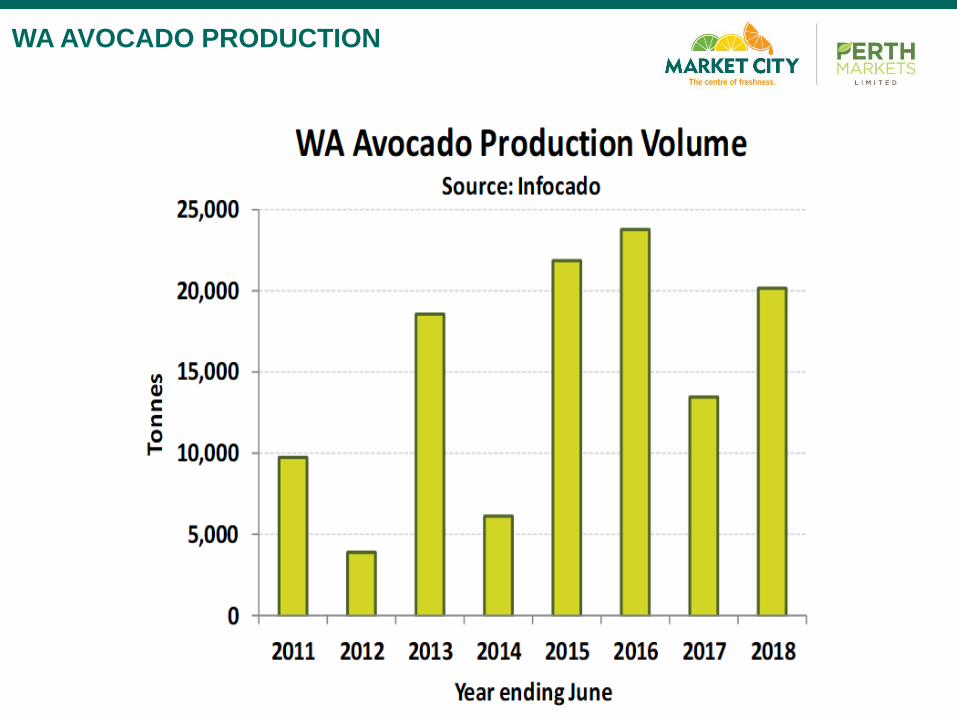

• The WA wholesale market is now marketing an additional 12-14,000 t of avocados per annum. At the national avocado wholesale price of $5.50 per kg that is generating an additional $66 - $77 million in wholesale value annually.

• Pest & disease challenges led to constraints for interstate exports. This left more product in the WA market and combined with improving Carnarvon output to increase supply and pressure down wholesale prices.

KEY FINDINGS

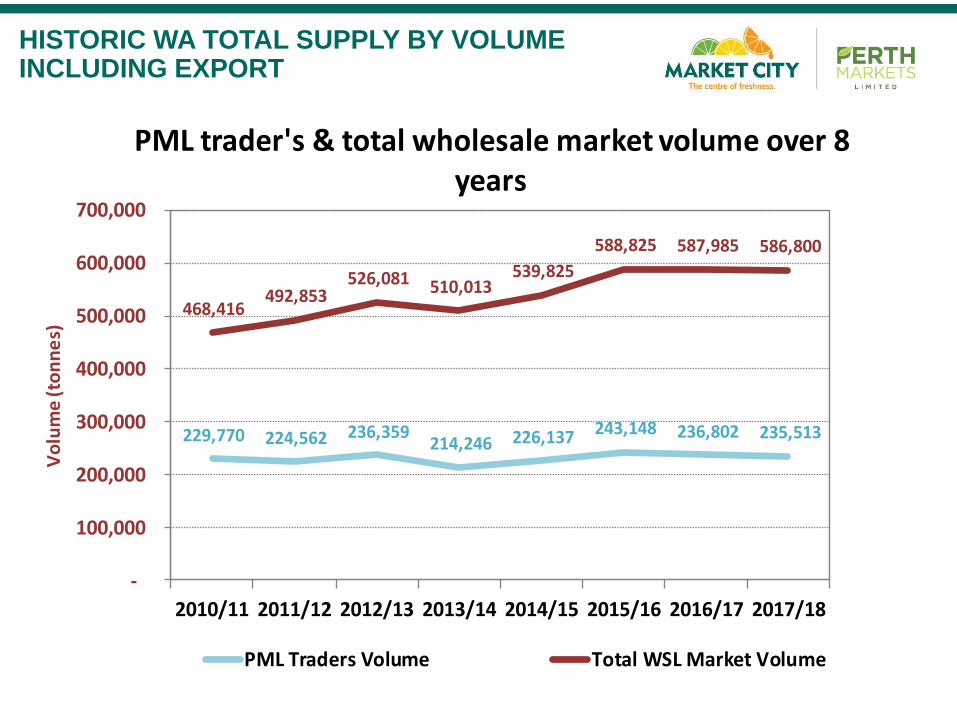

HISTORIC WA TOTAL SUPPLY BY VOLUME INCLUDING EXPORT

229,770 224,562 236,359 214,246 226,137 243,148 236,802 235,513

468,416 492,853

526,081 510,013 539,825

588,825 587,985 586,800

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 2017/18

Vo

lum

e (t

on

ne

s)

PML trader's & total wholesale market volume over 8 years

PML Traders Volume Total WSL Market Volume

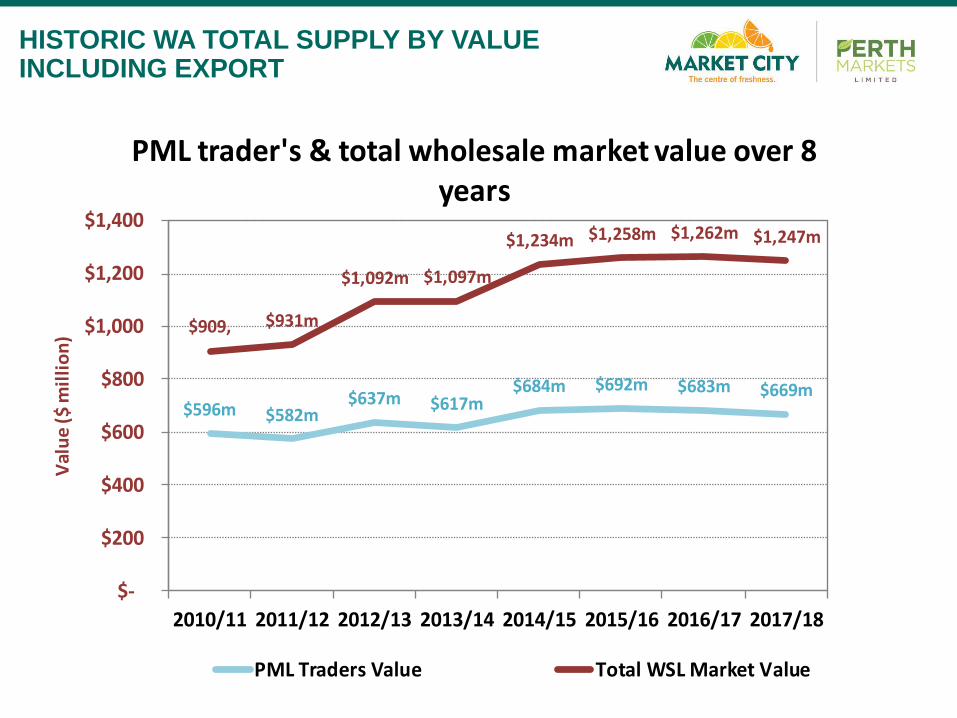

HISTORIC WA TOTAL SUPPLY BY VALUE INCLUDING EXPORT

$596m $582m$637m $617m

$684m $692m $683m $669m

$909, $931m

$1,092m $1,097m

$1,234m $1,258m $1,262m $1,247m

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 2017/18

Val

ue

($ m

illi

on

)

PML trader's & total wholesale market value over 8 years

PML Traders Value Total WSL Market Value

WA AVOCADO PRODUCTION

• Positive, expanding exports volumes have continued and help reduce the reliance on the domestic market consumption, but impacted PML traders’ volume market share due to lower exposure to these channels.

• Competitive intensity in the retail market is now at the level in other states. The core driver being the expansion of the lower prices ALDI network and the compounding impact or competing retailer responses.

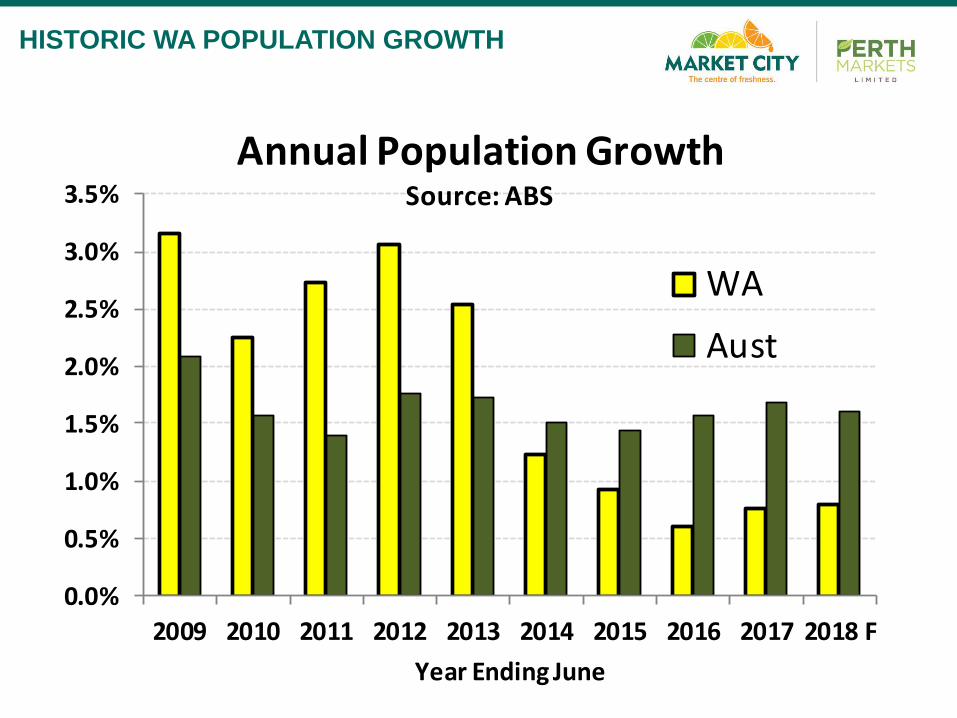

• Population driven growth in the WA market for fresh fruit and vegetables continues to be lower than the national levels

KEY FINDINGS

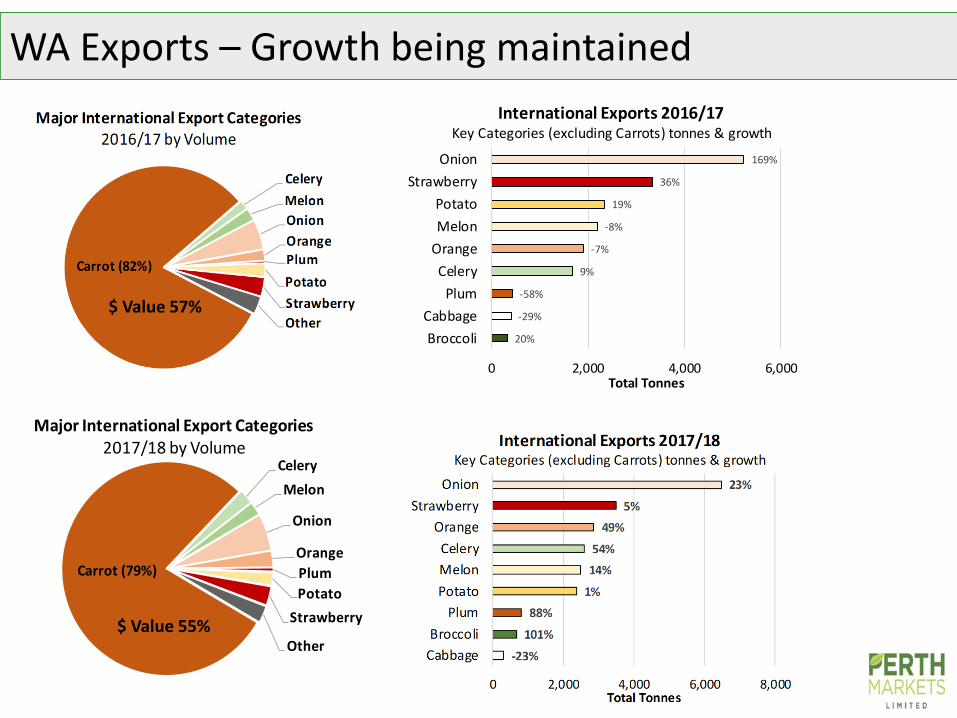

WA Exports – Growth being maintained

Carrot (79%)

Celery

Melon

Onion

Orange

Plum

Potato

Strawberry

Other

Major International Export Categories 2017/18 by Volume

20%

-29%

-58%

9%

-7%

-8%

19%

36%

169%

0 2,000 4,000 6,000

Broccoli

Cabbage

Plum

Celery

Orange

Melon

Potato

Strawberry

Onion

Total Tonnes

International Exports 2016/17Key Categories (excluding Carrots) tonnes & growth

$ Value 57%

$ Value 55%

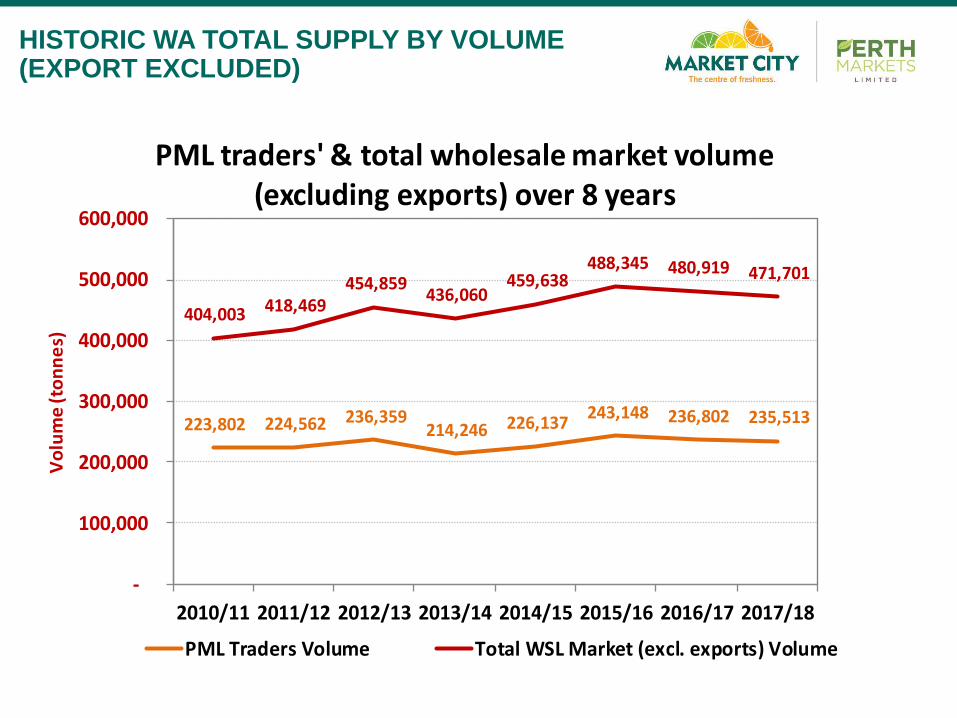

HISTORIC WA TOTAL SUPPLY BY VOLUME (EXPORT EXCLUDED)

223,802 224,562 236,359 214,246 226,137

243,148 236,802 235,513

404,003 418,469 454,859

436,060 459,638

488,345 480,919 471,701

-

100,000

200,000

300,000

400,000

500,000

600,000

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 2017/18

Vo

lum

e (t

on

ne

s)

PML traders' & total wholesale market volume (excluding exports) over 8 years

PML Traders Volume Total WSL Market (excl. exports) Volume

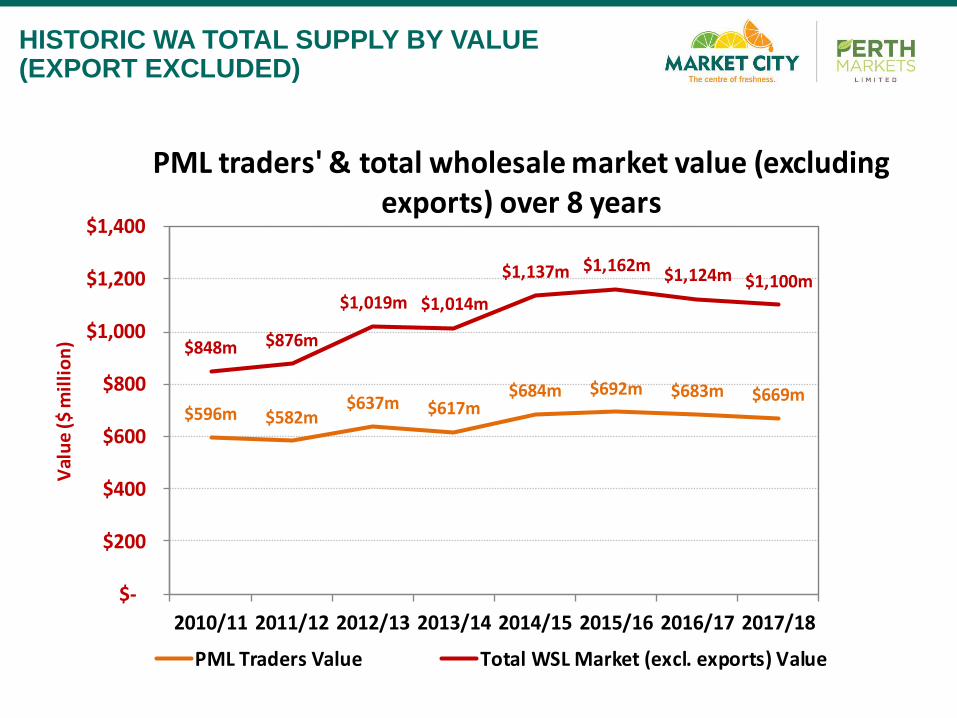

HISTORIC WA TOTAL SUPPLY BY VALUE (EXPORT EXCLUDED)

$596m $582m$637m $617m

$684m $692m $683m $669m

$848m $876m

$1,019m $1,014m

$1,137m $1,162m$1,124m $1,100m

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 2017/18

Val

ue

($ m

illi

on

)

PML traders' & total wholesale market value (excluding exports) over 8 years

PML Traders Value Total WSL Market (excl. exports) Value

HISTORIC WA POPULATION GROWTH

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 F

Year Ending June

Annual Population GrowthSource: ABS

WA

Aust

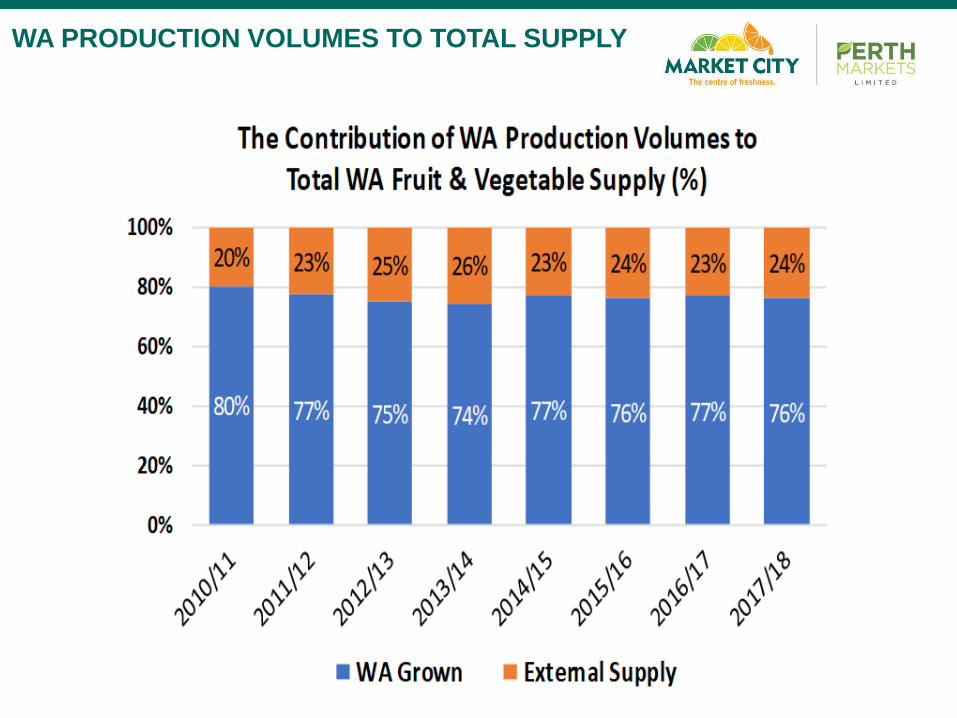

WA PRODUCTION VOLUMES TO TOTAL SUPPLY

Over the last two years, the Wholesale Traders at Market City have retained almost the same market share with only a <1% change demonstrating a flattening out of the previous slow decline.

MARKET CITY TRADERS IMPACT

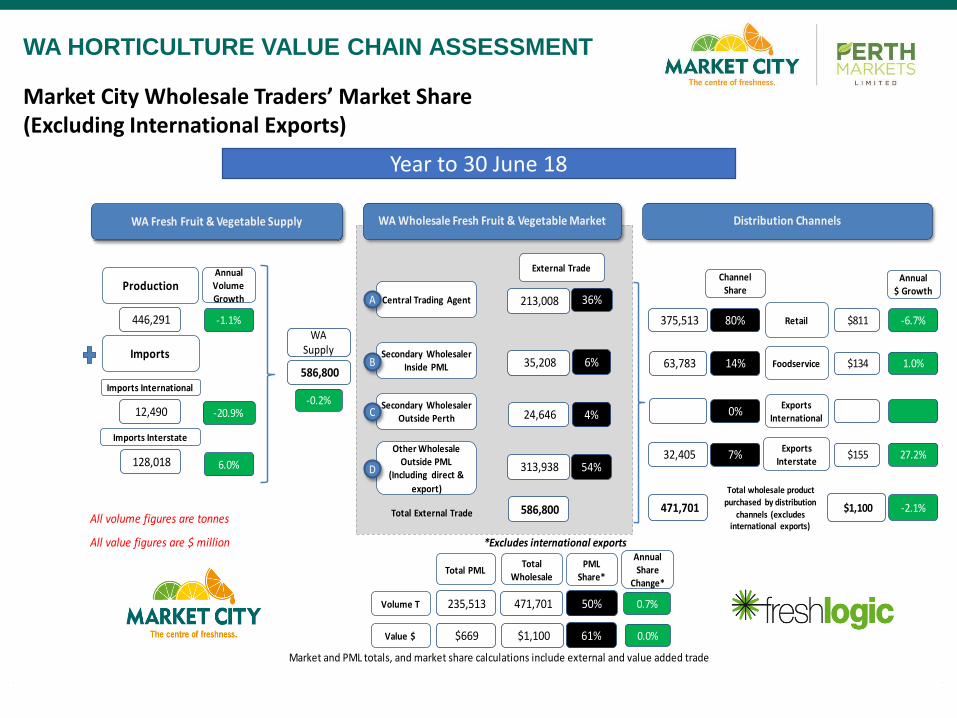

Year to 30 June 18

WA HORTICULTURE VALUE CHAIN ASSESSMENT

All volume figures are tonnes

All value figures are $ million *Excludes international exports

Market and PML totals, and market share calculations include external and value added trade

Distribution ChannelsWA Fresh Fruit & Vegetable Supply WA Wholesale Fresh Fruit & Vegetable Market

Production

Imports

Imports International

Imports Interstate

Annual Volume Growth

446,291

12,490

128,018

-1.1%

-20.9%

6.0%

586,800

WA Supply

-0.2%

Central Trading Agent

Secondary Wholesaler Inside PML

Secondary Wholesaler Outside Perth

Other Wholesale Outside PML

(Including direct &

export)

A

B

C

D

Total External Trade

213,008 36%

35,208 6%

24,646 4%

313,938 54%

External Trade

586,800

Foodservice63,783 14%

Retail

32,405

375,513 80%

Exports International

Exports Interstate

0%

7%

$811

$134

$155

-6.7%

1.0%

27.2%

Annual $ Growth

ChannelShare

471,701 $1,100

Total wholesale product

purchased by distribution channels (excludes

international exports)

-2.1%

471,701 235,513

$1,100 $669

50%

61%

Total Wholesale

Total PMLPML

Share*

Volume T

Value $

0.7%

0.0%

Annual Share

Change*

Market City Wholesale Traders’ Market Share (Excluding International Exports)

Retail competition and floor space has increased with downward price pressure on fruit and vegetable produce.

The biosecurity restrictions on movement of produce to the Eastern States caused disruption and oversupply in the WA market.

Increased Avocado production and good prices have had a material impact. Carrots remain the largest horticultural export.

General low economic growth and restrained household finances along with low population growth continue to depress price and overall consumption.

KEY CHANGES AND DRIVERS OF MARKET SHARE

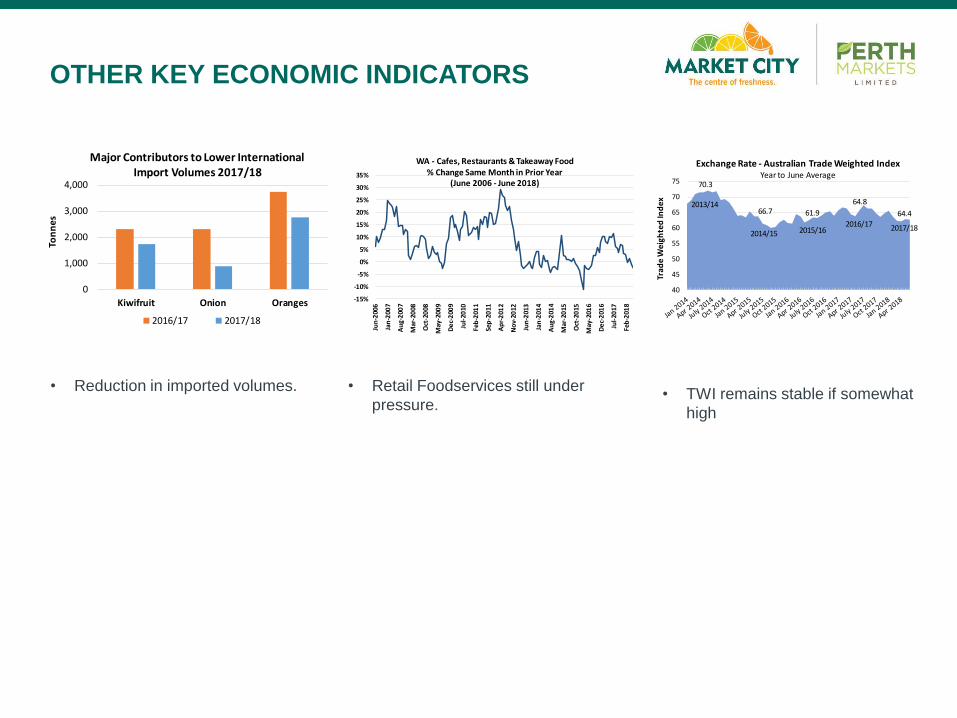

• Reduction in imported volumes. • Retail Foodservices still under

pressure.• TWI remains stable if somewhat

high

OTHER KEY ECONOMIC INDICATORS

0

1,000

2,000

3,000

4,000

Kiwifruit Onion Oranges

Ton

ne

s

Major Contributors to Lower International Import Volumes 2017/18

2016/17 2017/18

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Jun

-200

6

Jan

-200

7

Au

g-2

007

Mar

-20

08

Oct

-20

08

May

-200

9

De

c-2

009

Jul-

2010

Feb

-201

1

Sep

-20

11

Ap

r-2

012

No

v-20

12

Jun

-201

3

Jan

-201

4

Au

g-2

014

Mar

-20

15

Oct

-20

15

May

-201

6

De

c-2

016

Jul-

2017

Feb

-201

8

WA - Cafes, Restaurants & Takeaway Food % Change Same Month in Prior Year

(June 2006 - June 2018)

40

45

50

55

60

65

70

75

Tra

de

We

igh

ted

Ind

ex

Exchange Rate - Australian Trade Weighted IndexYear to June Average

70.3

66.7 64.4 61.9

64.82013/14

2014/152017/182016/17

2015/16

Perth Markets Limited (PML) is an industry based facility owner, manager, and developer.

The Market City site is a diverse cluster of businesses involved in wholesale food trading, retailing, business services, and weekend consumer markets.

The site, as a whole, not only plays a critical role as the State’s only Wholesale

Fresh Produce Market, but makes a significant contribution to the economy,

the local community, and families.

THE MARKET CITY COMPLEX

THE MARKET CITY SITE

Established in Canning Vale in 1989

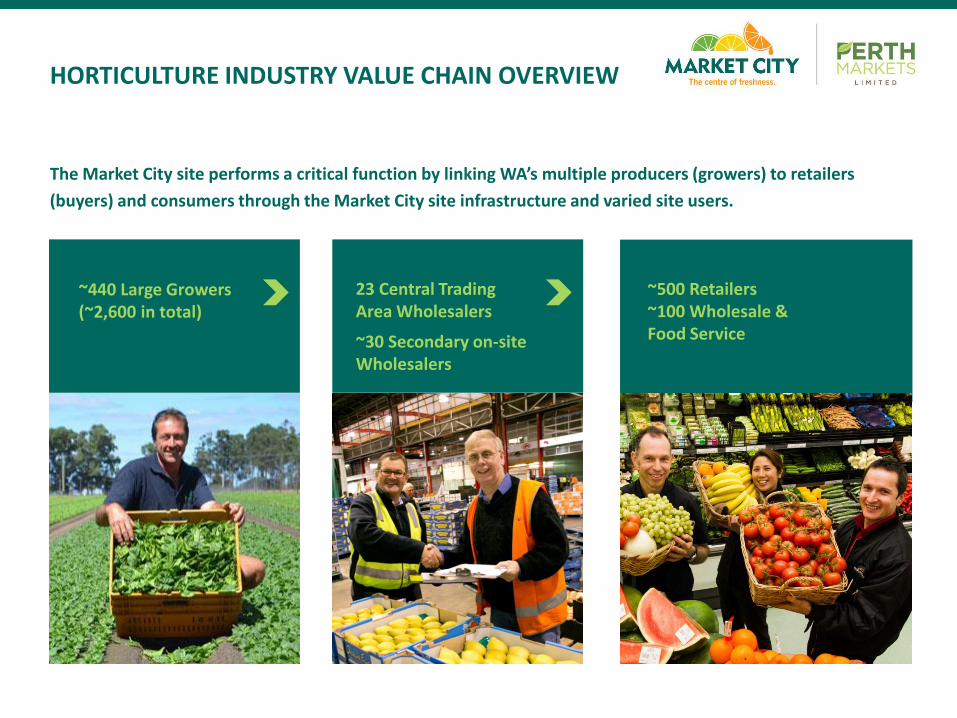

HORTICULTURE INDUSTRY VALUE CHAIN OVERVIEW

23 Central Trading Area Wholesalers

~30 Secondary on-site Wholesalers

The Market City site performs a critical function by linking WA’s multiple producers (growers) to retailers

(buyers) and consumers through the Market City site infrastructure and varied site users.

~440 Large Growers (~2,600 in total)

~500 Retailers~100 Wholesale & Food Service

THE MARKET CITY SITE

Existing Land Use

KEY SITE FACTS

• 51ha complex (≈15ha to be developed)

• Site activities include Wholesale F&V

Market, Fresh Fish Market, related

businesses, Retail, Professional Services

• 86,819m2 GLA building area

• 170 leases and licenses

• 99+% occupancy over last 8 years

• The Market City site operates 24/7/364

• Over 100 business located on site with

≈ 2,000 direct employees

• ≈ 4,500 daily site vehicle movements

• ≈ 4,100 site users (access cards)

• ≈ 355 registered forklifts

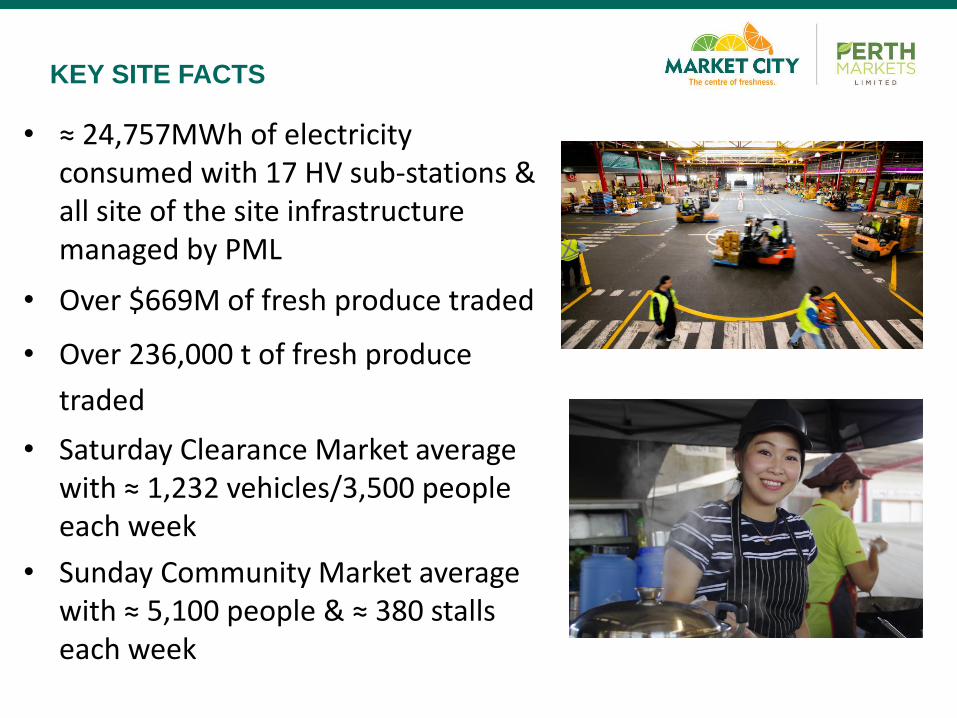

KEY SITE FACTS

• ≈ 24,757MWh of electricity consumed with 17 HV sub-stations & all site of the site infrastructure managed by PML

• Over $669M of fresh produce traded

• Over 236,000 t of fresh produce

traded

• Saturday Clearance Market average with ≈ 1,232 vehicles/3,500 people each week

• Sunday Community Market average with ≈ 5,100 people & ≈ 380 stalls each week

• Market City was owned and operated by the PMA, a Statutory State Government Agency.

• The site and the “going concern business” was put up for sale by tender as part of the Government’s Asset Sales Program run by the State Treasury.

• The successful buyer was Perth Markets Limited (PML), with a broad industry supported and funded offer.

• The transaction was settled as at 31/3/2016.

BRIEF CORPORATE HISTORY

Impact of Privatisation

on

Market Operations

1

In simple terms

No Change

To general site operations

IMPACT OF PRIVATISATION

• The Market has continued to operate as normal with a “Business as Usual” management approach taken.

• The Site Operation Rules have proven effective in maintaining operations following By-Law removal.

• Some internal staffing and process issues were encountered given most staff did not transition but these were expected give it was effectively a start up.

• Some cost increases for tenants (statutory charges, insurance) partly offset by reduced electricity costs.

• All site usage metrics have remained stable

IMPACT OF PRIVATISATION

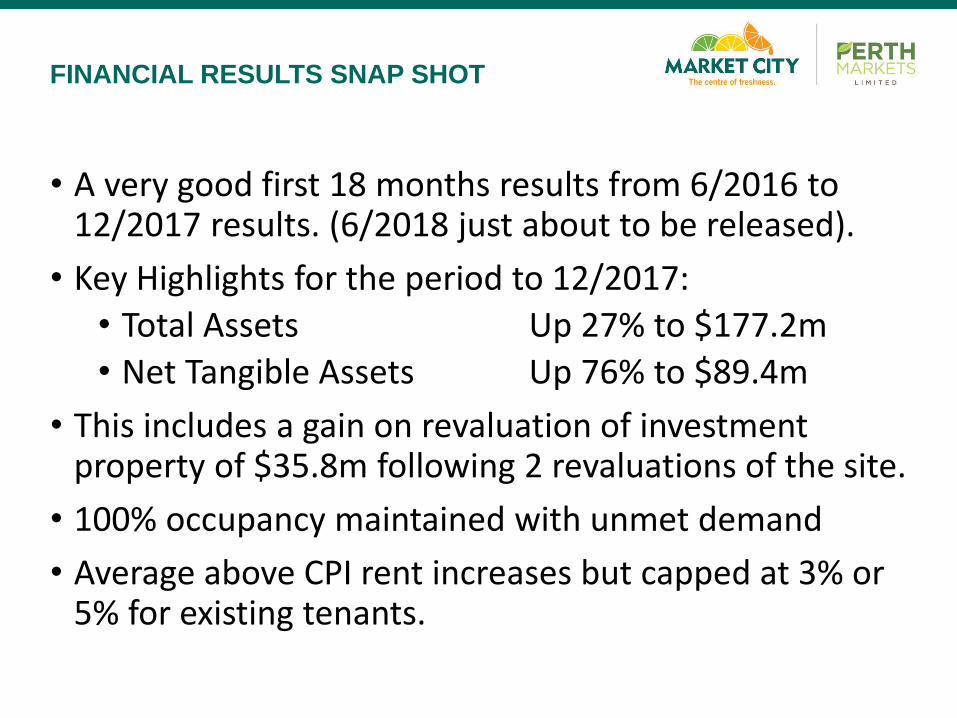

• A very good first 18 months results from 6/2016 to 12/2017 results. (6/2018 just about to be released).

• Key Highlights for the period to 12/2017:

• Total Assets Up 27% to $177.2m

• Net Tangible Assets Up 76% to $89.4m

• This includes a gain on revaluation of investment property of $35.8m following 2 revaluations of the site.

• 100% occupancy maintained with unmet demand

• Average above CPI rent increases but capped at 3% or 5% for existing tenants.

FINANCIAL RESULTS SNAP SHOT

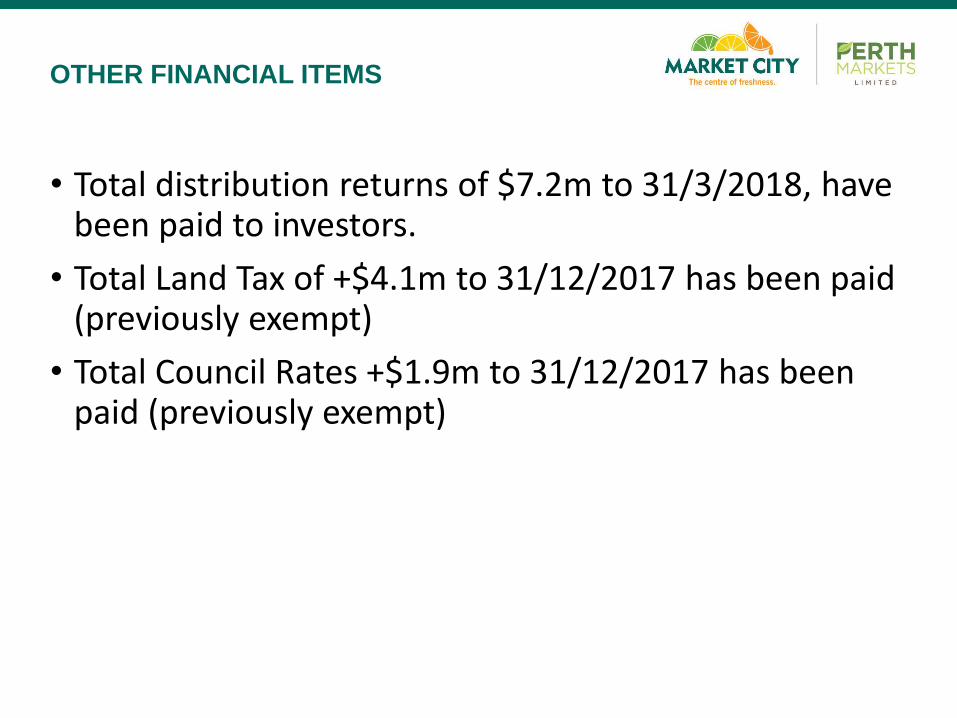

• Total distribution returns of $7.2m to 31/3/2018, have been paid to investors.

• Total Land Tax of +$4.1m to 31/12/2017 has been paid (previously exempt)

• Total Council Rates +$1.9m to 31/12/2017 has been paid (previously exempt)

OTHER FINANCIAL ITEMS

• Master Plan review completed

• SE Development Triangle identified as the priority

• Possible commercial/residential development mid term with Metronet being the catalyst.

SITE DEVELOPMENT ACTIVITY

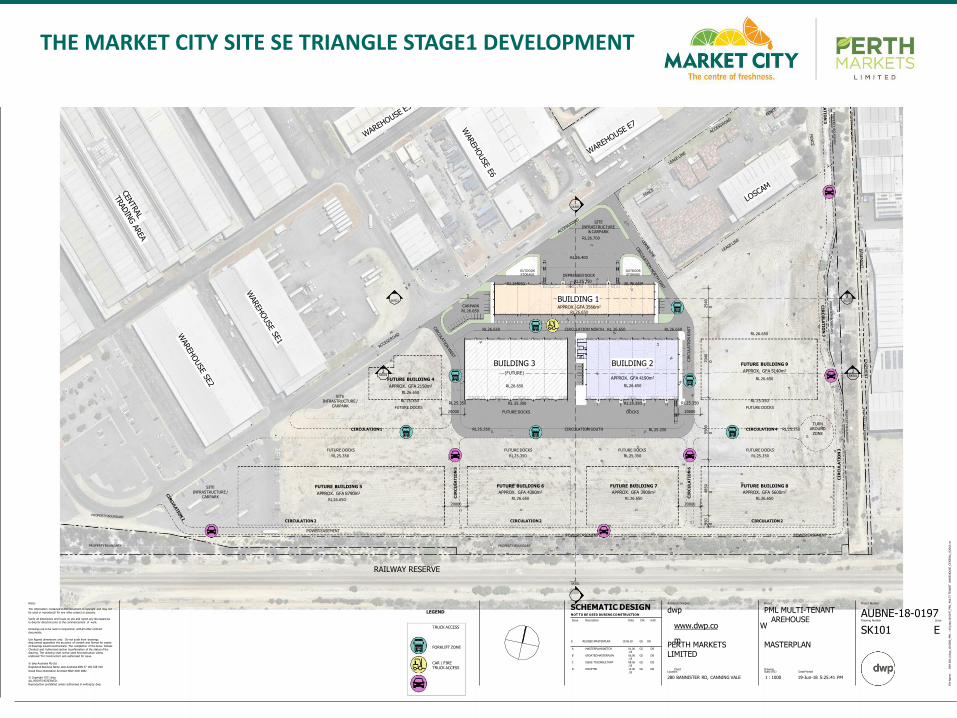

THE MARKET CITY SITE METRO NET CONSIDERATIONS

Indicative Long Term Options – Retaining Full Market Function

• EOI process confirms significant demand for new Cool Chain buildings on the development site

• Full Design Team appointed, with preliminary works underway

• Development Approval (DA) about to be submitted.

SITE DEVELOPMENT ACTIVITY

1SK501

2SK501

3SK501

RAILWAY RESERVE

PROPERTY BOUNDARYPROPERTY BOUNDARY

POWEREASEMENTPOWEREASEMENT POWEREASEMENT

BUILDING 1

BUILDING 2

2540

07040

05500

04850

0950

0

BUILDING 3(FUTURE)

SITE INFRASTRUCTURE /

CARPARK

CIRCULATION1 CIRCULATION SOUTH

CIRCULATION2CIRCULATION2CIRCULATION2

CIR

CU

LA

TIO

N3

CIR

CU

LA

TIO

N6

CIR

CU

LA

TIO

N5

20000 20000

TURN AROUND

ZONE

SITE INFRASTRUCTURE /

CARPARK

DEPRESSEDDOCK

RL25.350

RL26.400

RL26.650

RL 25.350

FUTURE DOCKS

RL25.250 RL25.250

RL 25.350

DOCKS

CIRCULATION NORTH RL 26.650

1SK501

SITE INFRASTRUCTURE

& CARPARK

RL26.700

3SK501

CARPARK

RL26.650

RL26.650 RL26.650

RL26.650

RL25.350

20000

RL25.350

20000

APPROX. GFA 3566m2

RL26.650

APPROX. GFA 4190m2

RL26.650RL26.650

FUTURE BUILDING 9

APPROX. GFA 5140m2

RL26.650

FUTURE BUILDING 8

APPROX. GFA 5600m2

RL26.650

FUTURE BUILDING 7

APPROX. GFA 3900m2

RL26.650

FUTURE BUILDING 6

APPROX. GFA 4380m2

RL26.650

FUTURE BUILDING 5

APPROX. GFA 8790m2

RL26.650

2SK501

FUTURE BUILDING 4

APPROX. GFA 2150m2

RL26.650

CIR

CU

LATIO

NEAST

RL 25.350

FUTURE DOCKS

FUTURE DOCKS

RL25.350

FUTURE DOCKS

RL25.350

FUTURE DOCKS

RL25.350

FUTURE DOCKS

RL25.350

RL 25.350

FUTURE DOCKS

CIRCULATION 4 RL 25.250

RL26.650

OUTDOOR

STORAGE

OUTDOOR

STORAGE

TRUCK ACCESS

FORKLIFT ZONE

CAR / FIRE TRUCK ACCESS

LEGENDSCHEMATIC DESIGNNOT TO BE USED DURING CONSTRUCTION

Notes

The information contained in this document is copyright and may not

be used or reproduced for any other project or purpose.

Verify all dimensions and levels on site and report any discrepancies

to dwp for direction prior to the commencement of work.

Drawings are to be read in conjunction with all other contract

documents.

Use figured dimensions only. Do not scale from drawings.dwp cannot guarantee the accuracy of content and format for copies

of drawings issued electronically. The completion of the Issue Details

Checked and Authorised section isconfirmation of the status of the

drawing. The drawing shall not be used forconstruction unless

endorsed 'For Construction' and authorised for issue.

Architect/Designer

dwp

© dwp Australia Pty Ltd

Registered Business Name dwp Australia ABN 37 169 328 018

David Rose Nominated Architect NSW ARB 4882

© Copyright 2011 dwp.

ALL RIGHTS RESERVED.

Reproduction prohibited unless authorised in writing by dwp. File

Nam

e:

BIM

360:/

/dw

p_18-0

000_PM

L-

All

jobs/

18-0

197_PM

L_M

ULT

I-TEN

AN

TW

AR

EH

OU

SE_CEN

TR

AL_

R2018.r

vt

Scale (A1)

1 : 1000

DatePrinted

19-Jun-18 5:25:41 PM

MASTERPLAN

Drawing Number Issue

SK101 E

Project Number

AUBNE-18-0197

PERTH MARKETS LIMITED

Project

PML MULTI-TENANT AREHOUSE

Location

280 BANNISTER RD, CANNING VALE

Issue Description Date Chk Auth

www.dwp.co

m

W

A MASTERPLANSKETCH 01.06.18

GS DB

B UPDATEDMASTERPLAN 06.06.18

GS DB

C ISSUE TOCONSULTANT 08.06.18

GS DB

D DRAFTSD 13.06.18

GS DB Client Drawing

E REVISEDMASTERPLAN 19.06.18 GS DB

THE MARKET CITY SITE SE TRIANGLE STAGE1 DEVELOPMENT

The information provided by the Perth Markets

Limited (PML) is given in good faith on an "as is"

basis for general information purposes only and

is not intended to constitute or substitute other

professional advice. You must make your own

assessment of the information and rely on it

wholly at your own risk as the PML makes no

representations about the suitability, reliability,

timeliness, comprehensiveness and accuracy of

the information provided.

PML GROUP - LEGAL NOTICE

The PML shall not be liable directly or indirectly

in contract, tort, negligence, equity or otherwise

for any damage whatsoever in connection with

any information provided, including any direct,

indirect, special, incidental or consequential

damage (including but not limited to loss of

profits, interest, data, business revenue,

anticipated savings, business or goodwill). The

recipient of any information from the PML agrees

to indemnify the PML from any loss, damages or

other cost whatsoever arising out of or in

connection with any claim commenced against

the PML arising out of it in connection with

reliance upon the subject matter of, or any part

of, any information provided by the PML.

Perth Markets Limited

280 Bannister Road

Canning Vale, WA 6155

www.perthmarket.com.au

Thank you