Embed Size (px)

Citation preview

Annual Report and Financial Statementsfor the year ended 31 December 2015

Markel InternationalInsurance Company Limited

Registered Number 966670

Markel International Insurance Company Limited

Annual Report and Financial Statements

for the year ended 31 December 2015

Contents

Directors and administration 1

Strategic report 2

Directors' report 7

Statement of Directors' responsibilities 9

Independent Auditor's report 10

Income Statement: Technical Account 12

Income Statement: Non-Technical Account 13

Statement of Comprehensive Income 14

Statement of Changes in Equity 15

Statement of Financial Position: Assets 16

Statement of Financial Position: Liabilities 17

Notes to the Financial Statements 18

Annual Report and Financial Statements for the year ended 31 December 2015

Directors and administration

Board of Directors

Ian Marshall (Chairman)Jeremy W BrazilStephen M Carroll (Resigned 2 June 2015)Andrew J DaviesPaul H JenksNicholas J S LineHugh A J Maltby (Appointed 20 March 2015)Jeremy A Noble (Appointed 9 September 2015)Ralph C SneddenJohn W J Spencer (Appointed 1 January 2016)William D StovinAnne Whitaker

Company Secretary

Andrew J Bailey

Registered office

20 Fenchurch StreetLondonEC3M 3AZ

Investment manager

Markel Gayner Asset Management Corporation

Bankers

Bank of New YorkBarclays Bank plcCitibank N.A. Royal TrustNorthern Trust

Registered number

The Company's registered number is 966670 (England and Wales).

Registered Auditor

KPMG LLP, London

Lawyers

Norton Rose Fulbright LLP, London

1 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

Strategic reportThe Directors submit their Strategic report for Markel International Insurance Company Limited ("theCompany") for the year ended 31 December 2015.

Review of the business

The Company is a subsidiary of Markel Capital Holdings Limited (“MCH”). Its ultimate holding company isMarkel Corporation (“Markel”), which is incorporated in Virginia in the United States and its ultimate EuropeanEconomic Area (EEA) parent company is Markel International Limited ("MINT"). The Company’s principalactivity is the transaction of general insurance from its office in London and its branch operations in Spain,Sweden, the Netherlands, and Germany, in addition to overseas operations in Latin America and Dubai.

Since January 2015, the Company also has branches in Ireland and Switzerland and has established arepresentative office in Colombia. In addition, Markel (UK) Limited underwrites on behalf of the Companythrough its UK branch network.

The Company holds Surplus Lines Licences and is an accredited reinsurer in most US States. It is also able towrite general insurance in a number of other overseas territories.

On 9 March 2015, with the exception of one specific account, the Company entered into agreements with athird party to reinsure its remaining liabilities and exposures relating to business underwritten with respect to1992 and all prior underwriting years. With effect from 18 March 2015, the third party took over themanagement of claims and all future administration relating to these liabilities and exposures. It is anticipatedthat a Part VII transfer will be finalised in the latter half of 2016.

On 1 July 2015, the Company merged its business with that of Markel Europe plc, an insurance companyregistered and based in the Republic of Ireland. The companies merged under the Companies (Cross-BorderMergers) Regulations of 2007 in the UK, and similar regulations in the Republic of Ireland.

Markel Europe plc transferred all of their assets and liabilities to the Company, and was then dissolved underthe relevant legislation without going into liquidation.

Business profile and units

The Company operates eight underwriting units, namely Marine and Energy, Professional Liability, NationalMarkets, Specialty, Equine, Trade Credit, Casualty Treaty and Latin America.

Marine and Energy

The Marine and Energy unit underwrites a portfolio of coverage's for cargo, energy, hull, liability, war,terrorism, specie and ports and terminals risks. The cargo account comprises of a broad portfolio of transitand storage risks covering most industries on a global basis. The energy account includes all aspects of oiland gas activities. The hull account covers physical damage to ocean-going tonnage, yachts, building risksand mortgagee’s interest. The liability account provides coverage for a broad range of energy liabilities, aswell as traditional marine exposures including charterers, terminal operators and ship repairers. The waraccount offers coverage for marine and aviation war across all vessel types and tonnages. The terrorismaccount covers physical damage resulting from terrorism, strikes, riots, war and political violence. The specieaccount includes coverage for fine art, exhibition business and other aspects of valuable item insurance. Theports and terminals account encompasses the complete range of insurance products to fulfil the requirementsof port and terminal operators around the world.

Markel International Insurance Company Limited 2

Annual Report and Financial Statements for the year ended 31 December 2015

Professional Liability

The Professional Liability unit underwrites professional indemnity, emerging risks, management liability andfinancial institutions insurance. The professional indemnity account services most core and regulatedprofessions as well as other miscellaneous professions. The emerging risks account includes specialisms inmedia, patent and intellectual property insurance as well as information technology, telecommunications andcyber/privacy risks. The management liability account spans a wide range of industries and coverage includesdirectors' and officers' liability (D&O), employment practices liability (EPL) and limited liability partnership(LLP) cover. Financial institutions insurance can provide cover on a stand alone basis or as a blended packageto include bankers blanket bond, professional indemnity and D&O, depending on the client's requirements.The Professional Liability division writes business on a worldwide basis, limiting exposure in the United States.

National Markets

The National Markets unit offers a full range of professional liability products, including professionalindemnity, directors’ and officers’ liability and employment practices liability. In addition, coverage is providedfor small to medium-sized commercial property risks on both a stand-alone and package basis. The branchoffices provide insureds and brokers with direct access to decision-making underwriters who possessspecialised knowledge of their local markets. The unit also underwrites certain niche liability products such ascoverage's for social welfare organisations.

The National Markets unit also includes business written through Abbey Protection Group ("Abbey"), acquiredby MCH in January 2014. Abbey sells and underwrites insurance products which provide protection againstlegal expenses and other professional fees incurred by clients as a result of legal actions and HMRCinvestigations. It also provides legal, human resources and specialist tax consultancy services.

Specialty

The Specialty unit provides property treaty reinsurance on an excess of loss and proportional basis for perrisk and catastrophe exposures on a worldwide basis. The Specialty unit also offers direct coverage for anumber of specialist classes including contingency, property open market, accident and health and otherspecial risks.

Equine

The Equine unit writes equine and livestock accounts on a worldwide basis. The equine account providescoverage for risks of mortality, theft, infertility and specified perils for insureds ranging in size from largebreeding and racing operations to private horse owners. The livestock account provides coverage for farms,zoos and aquarium and animals in transit.

Trade Credit

The Trade Credit unit writes short-term trade credit coverage for commercial risks, including insolvency,protracted default and contract frustration. Political risks are covered in conjunction with commercial risks forcurrency inconvertibility, government action, import/export licence cancellation, public buyer default and war.Products include coverage's for captive reinsurance, trade receivables securitisation, vendor financing, pre-credit/work in progress, anticipatory credit, factoring and contract replacement. Policies are designed toprovide clients with certainty of cover and are underwritten with the aim of establishing a long-termpartnership with the insured.

3 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

Casualty Treaty

The Casualty Treaty unit underwrites a diversified account, including general liability, professional indemnity,directors' and officers' liability and medical malpractice. The portfolio is worldwide, excluding United Statesdomiciled business.

Latin America

The Company's operations in Latin America transact reinsurance business on a range of product linesincluding accident and health, property and surety.

Results and performance

The results of the Company for the year, as set out on pages 12 - 14 show a profit on ordinary activitiesbefore taxation of $98.2m (2014, profit of $89.0m). Shareholder's funds as at 31 December 2015 were$580.7m (2014, $706.3m).

The Company reported an underlying underwriting profit of $44.5m for the year (2014, $11.1m profit),having benefited from benign large loss and catastrophe activity during the year. This represents a combinedratio of 83.6% (2014, 96.7%).

The result included a release from prior year reserves of $100.6m (2014, $79.2m). This release is a result ofthe Markel strategy to reserve prudently, more favourable claims development than originally anticipated andthe work of our claims department in dealing with claims in an expeditious manner.

Gross written premiums of $503.4m for the year represent a decrease on prior year of 19.3%, primarily dueto the exit from UK motor business on the Casualty Treaty unit.

During the year the Company commuted internal reinsurance arrangements with Markel Bermuda Limited("MBL"), on the Spanish speaking Latin America and Marine books of business. The net cash settlement onthese commutations was $0.1m.

The investment return of $39.1m comprises income of $32.9m, net realised gains of $82.6m and unrealisedlosses of $75.8m, primarily on the equity portfolio.

The Company’s operating performance and Statement of Financial Position remains strong and this wasrecognised by both AM Best and Fitch, who maintained their ratings at A (Excellent) and A (High),respectively.

Markel International Insurance Company Limited 4

Annual Report and Financial Statements for the year ended 31 December 2015

Key Performance Indicators

Income Statement 2011

$m2012

$m2013

$m2014

$m2015

$m

Gross written premiums 267.7 286.1 342.2 623.8 503.4

Net written premiums 237.2 255.8 264.8 378.8 238.5

Retention rate 88.6% 89.4% 77.4% 60.7% 47.4%

Net earned premiums 224.6 247.2 269.2 330.6 271.9

Underlying underwriting result (1) (18.8) 41.8 40.3 11.1 44.5

Loss and LAE ratio 68.0% 40.6% 45.4% 55.0% 25.3%

Expense ratio 40.4% 42.5% 39.6% 41.7% 58.3%

Combined ratio 108.4% 83.1% 85.0% 96.7% 83.6%

Investment return (2) 40.6 68.0 109.9 84.4 39.1

Investment yield 3.5% 6.0% 9.0% 5.8% 2.6%

Operating profit (3) 26.2 108.7 142.2 89.0 98.2

Statement of Financial Position2011

$m2012

$m2013

$m2014

$m2015

$m

Financial investments (2) 1,109.3 1,168.4 1,278.2 1,638.6 1,375.1

Reinsurers' share of claims outstanding 70.5 68.9 107.5 618.8 617.6

Gross claims outstanding 785.8 764.3 797.2 1,413.7 1,346.6

Net claims outstanding 715.3 695.4 689.7 794.9 729.0

Shareholder's Equity 407.8 436.9 491.4 706.3 580.7

Individual Capital Guidance (ICG) 218.0 225.9 242.6 263.9 255.6

Shareholder's Equity / ICG 187.1% 193.4% 202.6% 267.6% 227.2%

2014 onwards shows KPIs including Markel Europe

(1) excluding movement on equalisation provision(2) excluding investments in subsidiaries(3) operating profit is equal to profit before taxation for all years.

Financial success is measured by growth in shareholders' equity over time as this reflects the impact of bothunderwriting and investment performance and is consistent with Markel’s key financial goal of buildingshareholder value. Underwriting performance is measured by underwriting profit or loss and combined ratio,whilst investment performance is measured by total investment return.

Business environment and future prospects

With disciplined underwriting and its strong financial condition the Company is in an excellent position tocapitalise on opportunities as they arise. The Company will continue to apply Markel’s underwriting disciplineof underwriting for profit rather than volume and, accordingly, will decline business where the rates are notacceptable.

5 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

The Company will continue to look to develop new lines of business and markets, within the parameters ofthe overall underwriting strategy. The Company invests in high-quality corporate, government and municipalbonds, as well as a diverse equity portfolio and plans to continue this investment strategy in 2016.

Going concern

No material uncertainties that cast doubt about the ability of the Company to continue as a going concernhave been identified by the Directors.

The Directors have a reasonable expectation that the Company has adequate resources to continue inoperational existence for the foreseeable future. Thus, the Directors continue to adopt the going concernbasis of accounting in preparing the Financial Statements.

Principal risks and uncertainties

The Company has a risk register detailing the risks to which it is exposed, which includes all businessunderwritten by the Company. Risks are grouped under the following categories:

• Underwriting Risk• Reserving Risk• Market Risk• Credit Risk• Operational Risk• Liquidity Risk• Group Risk

The management of the finance and insurance risks are disclosed in note 2 of these financial statements.There are currently 24 risks in the risk register. A formal review by the Risk Committee and the CompanyBoard occurs at least annually to ensure that the risk register identifies all the risks to which the Company isexposed. Key controls are identified to mitigate each risk and quarterly confirmation is sought from theowners of these controls that they are in place and are operating effectively.

Our Risk and Capital Committee meets quarterly to consider Key Risk Indicators and any Risk issues thathave arisen. These are summarised in the Director of Risk Management’s quarterly report to the CompanyBoard.

At least annually an Own Risk and Solvency Assessment report is produced being a forward lookingassessment of the risk profile and adequacy of the Company's capital to meet solvency needs over thebusiness planning time horizon.

The Company has received approval from the Prudential Regulation Authority ("PRA") to use an internalmodel to calculate the Solvency Capital Requirement from 1 January 2016 under Solvency II.

By order of the Board,

Andrew J Davies DirectorLondon

22 March 2016

Markel International Insurance Company Limited 6

Annual Report and Financial Statements for the year ended 31 December 2015

Directors' reportThe Directors submit the Annual Report and Financial Statements of the Company for the year ended 31December 2015.

Future developments

Likely future developments in the business of the Company are discussed in the Strategic report on page 2.

Dividends

During the year dividends of $200m were paid (2014, $Nil).

Directors

The Directors of the Company who served during 2015 and up to the date of this report were as follows:

Ian Marshall (Chairman)Jeremy W BrazilStephen M Carroll (Resigned 2 June 2015)Andrew J DaviesPaul H JenksNicholas J S LineHugh A J Maltby (Appointed 20 March 2015)Jeremy A Noble (Appointed 9 September 2015)Ralph C SneddenJohn W J Spencer (Appointed 1 January 2016)William D StovinAnne Whitaker

Markel maintains liability insurance cover on behalf of the Directors and named Officers of the Company andits subsidiaries.

Financial instruments and risk management

Information on the use of financial instruments by the Company and its management of the associatedfinancial risk is disclosed in note 2 of these Financial Statements. In particular the Company's exposures toprice risk, credit risk and liquidity risk are separately disclosed in that note. The Company's exposure to cashflow risk is addressed under the headings of 'Market risk', 'Credit risk' and 'Liquidity risk'.

Branches outside the UK

Branches outside the UK are discussed in the Strategic report on page 2.

Political donations

No political donations were made in the year (2014, Nil).

7 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

Carbon policy

As set out in the “Markel Style” the Company has a commitment to its communities which we recogniseincludes environmental responsibilities. Our goal is to minimise our environmental impact whilst still adheringto our other company principles as expressed in the Markel Style and our company profile.

Through the development of best practices in our business, the Company aims to use no more consumablesthan are necessary and recycle the maximum of those we do use. The Directors also believe that embeddingenvironmental awareness throughout the organisation will be best achieved through a continuous programmeof employee education.

Disclosure of information to the Auditor

The Directors who held office at the date of approval of this Directors' report confirm that, so far as they areeach aware, there is no relevant audit information of which the Company's Auditor is unaware; and eachDirector has taken all the steps that they ought to have taken as a Director to make themselves aware of anyrelevant audit information and to establish that the Company's Auditor is aware of that information.

Auditor

In accordance with Section 487 of the Companies Act 2006, the Auditor will be deemed to be reappointedand KPMG LLP will, therefore, continue in office.

By order of the Board,

Jeremy W Brazil DirectorLondon

22 March 2016

Markel International Insurance Company Limited 8

Annual Report and Financial Statements for the year ended 31 December 2015

Statement of Directors' responsibilities The Directors are responsible for preparing the Strategic report, the Directors’ report and the FinancialStatements in accordance with applicable law and regulations.

Company law requires the Directors to prepare Financial Statements for each financial year. Under that lawthe Directors have elected to prepare the Financial Statements in accordance with UK Accounting Standardsand applicable law (UK Generally Accepted Accounting Practice), including Financial Reporting Standard("FRS") 102 the Financial Reporting Standard applicable in the UK and Republic of Ireland and FRS 103Insurance Contracts.

Under Company law, the Directors must not approve the Financial Statements unless they are satisfied thatthey give a true and fair view of the state of affairs of the Company and of the profit or loss of the Companyfor that period.

In preparing these Financial Statements, the Directors are required to:

• select suitable accounting policies and then apply them consistently;• make judgements and estimates that are reasonable and prudent;• state whether applicable UK Accounting Standards have been followed, subject to any material departures

disclosed and explained in the Financial Statements; and• prepare the Financial Statements on the going concern basis unless it is inappropriate to presume that the

Company will continue in business.

The Directors are responsible for keeping adequate accounting records that are sufficient to show and explainthe Company’s transactions and disclose with reasonable accuracy at any time the financial position of theCompany and enable them to ensure that its Financial Statements comply with the Companies Act 2006.They have a general responsibility for taking such steps as are reasonably open to them to safeguard theassets of the Company and to prevent and detect fraud and other irregularities.

The Directors are responsible for the maintenance and integrity of the corporate and financial informationincluded in the Company’s website. Legislation in the UK governing the preparation and dissemination ofFinancial Statements may differ from legislation in other jurisdictions.

9 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

Independent Auditor's report

to the Members of Markel International Insurance CompanyLimited

We have audited the Financial Statements of Markel International Insurance Company Limited for the yearended 31 December 2015, set out on pages 12 to 46. The financial reporting framework that has beenapplied in their preparation is applicable law and UK Accounting Standards (UK Generally AcceptedAccounting Practice), including FRS 102 the Financial Reporting Standard applicable in the UK and Republic ofIreland and FRS 103 Insurance Contracts, having regard to the statutory requirement for insurancecompanies to maintain equalisation provisions. The nature of equalisation provisions, the amounts set asideat 31 December, and the effect of movement in those provisions during the year on shareholders' funds, thebalance on the general business technical account and profit before tax, are disclosed in note 21.

This report is made solely to the Company's members, as a body, in accordance with Chapter 3 of Part 16 ofthe Companies Act 2006. Our audit work has been undertaken so that we might state to the Company'smembers those matters we are required to state to them in an auditor's report and for no other purpose. Tothe fullest extent permitted by law, we do not accept or assume responsibility to anyone other than theCompany and the Company's members, as a body, for our audit work, for this report, or for the opinions wehave formed.

Respective responsibilities of Directors and Auditor

As explained more fully in the Statement of Directors’ responsibilities set out on page 9, the Directors areresponsible for the preparation of the Financial Statements and for being satisfied that they give a true andfair view. Our responsibility is to audit, and express an opinion on, the Financial Statements in accordancewith applicable law and International Standards on Auditing (UK and Ireland). Those Standards require us tocomply with the Auditing Practices Board’s Ethical Standards for Auditors.

Scope of the audit of the Financial Statements

A description of the scope of an audit of Financial Statements is provided on the Financial Reporting Council’swebsite at www.frc.org.uk/auditscopeukprivate.

Opinion on Financial Statements

In our opinion the Financial Statements:

• give a true and fair view of the Company’s affairs as at 31 December 2015 and of its profit for the year thenended;

• have been properly prepared in accordance with UK Generally Accepted Accounting Practice; and • have been prepared in accordance with the requirements of the Companies Act 2006.

Opinion on other matter prescribed by the Companies Act 2006

In our opinion the information given in the Strategic report and the Directors' report for the financial year forwhich the Financial Statements are prepared is consistent with the Financial Statements.

Markel International Insurance Company Limited 10

Annual Report and Financial Statements for the year ended 31 December 2015

Based solely on the work required to be undertaken in the course of the audit of the Financial Statementsand from reading the Strategic report and Directors' report:

• we have not identified material misstatements in those reports; and • in our opinion, those reports have been prepared in accordance with the Companies Act 2006.

Matters on which we are required to report by exception

We have nothing to report in respect of the following matters where the Companies Act 2006 requires us toreport to you if, in our opinion:

• adequate accounting records have not been kept, or returns adequate for our audit have not been received from branches not visited by us; or

• the Financial Statements are not in agreement with the accounting records and returns; or• certain disclosures of Directors’ remuneration specified by law are not made; or• we have not received all the information and explanations we require for our audit.

Ben Priestley (Senior Statutory Auditor)for and on behalf of KPMG LLP, Statutory AuditorChartered Accountants15 Canada SquareLondonE14 5GL

22 March 2016

11 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

Income Statement: Technical Account

2015 2014

Notes $'000 $'000 $'000 $'000

Earned premiums, net of reinsurance

Gross written premiums 3 503,446 623,799

Outward reinsurance premiums (264,958) (245,001)

Net written premiums 238,488 378,798

Change in the gross provision for unearned premiums 47,943 (39,870)Change in the provision for unearned premiumsreinsurers' share (14,483) (8,287)

33,460 (48,157)

Net Earned Premiums 271,948 330,641

Claims incurred, net of reinsurance

Claims paid

Gross amount (236,069) (244,164)

Reinsurers' share 87,048 118,459

Net paid claims (149,021) (125,705)

Change in the provision for claims

Gross amount 15,059 (111,508)

Reinsurers' share 65,046 55,395

Net change in provision 80,105 (56,113)

Net claims incurred (68,916) (181,818)

Net operating expenses 5 (158,568) (137,772)

Change in the equalisation provision 21 12,424 (5,594)

Balance on the technical account 56,888 5,457

The notes on pages 18 to 46 form part of these Financial Statements.

Markel International Insurance Company Limited 12

Annual Report and Financial Statements for the year ended 31 December 2015

Income Statement: Non-Technical Account

Notes 2015$'000

2014$'000

Balance on the technical account 56,888 5,457

Investment income 6 126,991 54,016

Investment expenses and charges 7 (11,469) (7,700)

Unrealised (losses)/gains on investments 8 (76,428) 38,043

Net foreign exchange gains/(losses) 2,169 (798)

Profit on ordinary activities before taxation 9 98,151 89,018

Taxation on profit on ordinary activities 11 (24,634) (15,532)

Profit for the year 73,517 73,486

The notes on pages 18 to 46 form part of these Financial Statements.

13 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

Statement of Comprehensive Income

Notes 2015$'000

2014$'000

Profit for the year 73,517 73,486

Profit/(loss) recognised in pension schemes 25 1,691 (13,980)

Movement on deferred tax relating to pension scheme 25 159 3,084

Movement on pension asset recognition limit 25 (1,037) 8,469

Total Comprehensive Income for the year 74,330 71,059

The notes on pages 18 to 46 form part of these Financial Statements.

Markel International Insurance Company Limited 14

Annual Report and Financial Statements for the year ended 31 December 2015

Statement of Changes in Equity

2015

Called-upShare

Capital$'000

SharePremium

$'000

OtherReserves

$'000

ComprehensiveIncome

$'000Total $'000

At beginning of year 267,202 199,765 (37,565) 276,946 706,348

Total comprehensive income for the year - - - 74,330 74,330

Dividends paid - - - (200,000) (200,000)

At end of year 267,202 199,765 (37,565) 151,276 580,678

2014

Called-upShare

Capital$'000

SharePremium

$'000

OtherReserves

$'000

ComprehensiveIncome

$'000Total $'000

At beginning of year 226,876 98,313 - 166,259 491,448

Merger of Markel Europe plc 40,326 101,452 (37,565) 39,628 143,841

Total comprehensive income for the year - - - 71,059 71,059

At end of year 267,202 199,765 (37,565) 276,946 706,348

15 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

Statement of Financial Position: Assets

as at 31 December 2015

Notes2015$'000

2014$'000

Investments

Investments in group undertakings and participating interests 15 5,922 6,459

Other financial investments 15 1,375,102 1,638,587

Deposits with ceding undertakings 1,762 471

1,382,786 1,645,517

Reinsurers' share of technical provisions

Provisions for unearned premiums 21 47,523 127,689

Claims outstanding 21 617,641 618,763

665,164 746,452

Debtors

Debtors arising out of direct insurance operations 16 67,782 205,064

Debtors arising out of reinsurance operations 16 159,409 31,485

Deferred taxation asset 17 364 321

Other debtors 18 3,392 15,446

230,947 252,316

Tangible Assets

Tangible assets 19 99 990

99 990

Prepayments and accrued income

Accrued interest 10,805 11,438

Deferred acquisition costs 21 40,450 21,046

Other prepayments - 896

51,255 33,380

Total Assets 2,330,251 2,678,655

The notes on pages 18 to 46 form part of these Financial Statements.

Markel International Insurance Company Limited 16

Annual Report and Financial Statements for the year ended 31 December 2015

Statement of Financial Position: Liabilities

as at 31 December 2015

Notes2015$'000

2014$'000

Capital and reserves

Called up share capital 20 267,202 267,202

Share premium account 199,765 199,765

Other reserve (37,565) (37,565)

Comprehensive Income 151,276 276,946

Shareholder's funds attributable to equity interests 580,678 706,348

Technical provisions

Provisions for unearned premiums 21 218,165 282,192

Claims outstanding 21 1,346,600 1,413,718

Equalisation provision 21 10,954 23,378

1,575,719 1,719,288

Provisions for other risks and charges 22 804 1,377

Creditors

Creditors arising out of direct insurance operations 23 1,909 161,958

Creditors arising out of reinsurance operations 23 110,067 63,837

Other creditors including taxation and social security 24 61,074 20,472

173,050 246,267

Accruals and deferred income - 5,375

Net liabilities excluding pension liability 2,330,251 2,678,655

Pension liability 25 - -

Total Liabilities and Shareholder's Funds 2,330,251 2,678,655

Approved by the Board of Directors on 22 March 2016 and signed on behalf of the Company by AndrewDavies, Company Director.

Andrew J Davies DirectorLondon,

22 March 2016

The notes on pages 18 to 46 form part of these Financial Statements.

17 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

Notes to the Financial Statements

1 Accounting policies The Financial Statements have been prepared in compliance with Financial Reporting Standard("FRS") 102, being the Financial Reporting Standard applicable in the UK and Republic of Ireland asissued in August 2014, and FRS 103 Insurance Contracts as issued in March 2014.

The Company is exempt by virtue of s401 of the Companies Act 2006 from the requirement toprepare consolidated Financial Statements on the grounds that the consolidated Financial Statementsof its ultimate parent, Markel, for the year ended 31 December 2015 are publicly available andinclude the Company in the consolidation. These Financial Statements present information about theCompany as an individual undertaking and not about its group.

In these Financial Statements, the Company is considered to be a qualifying entity for the purposesof this FRS and has applied the exemptions available under FRS 102 in respect of the followingdisclosures:- Cash Flow Statement and related notes;- Reconciliation of the number of shares outstanding from the beginning to the end of the period; - Key Management and Personnel compensation;- The disclosures required by FRS 102.11 Basic Financial Instruments and FRS 102.12 Other FinancialInstrument Issues in respect of financial instruments not falling within the fair value accountingrules.

These Financial Statements have been prepared in accordance with the historical cost conventionmodified by the revaluation of certain assets as required by the Regulations. A summary of the moreimportant accounting policies that have been applied consistently is set out below.

The Company transitioned from previously extant UK GAAP to FRS 102 and FRS 103 as at 1 January2015. An explanation of how transition to FRS 102 and FRS 103 has affected the reported financialposition and financial performance is given in note 30.

a) Use of judgements and estimates

In preparing these Financial Statements, the Directors of the Company have made judgements,estimates and assumptions that affect the application of the Company’s accounting policies and thereported amounts of assets, liabilities, income and expenses.

Actual results may differ from these estimates. Estimates and underlying assumptions are reviewedon an ongoing basis. Revisions to estimates are recognised prospectively.

Further detail on the use of judgements and estimates is detailed in the underwriting result policy.

b) Underwriting result

The underwriting result is determined using an annual basis of accounting, whereby the incurred costof claims, commission and expenses are charged against the earned proportion of premiums, net ofreinsurance, as follows:

i) Written premiums relate to business incepted during the year, together with any differencebetween booked premiums for prior years and those previously accrued, and include estimates ofpremiums not yet due or notified to the Company. Premiums are shown gross of brokeragepayable and excludes taxes and duties levied on them.

ii) Unearned premiums represent the proportion of premiums written in the year that relates tounexpired terms of policies in force at the reporting date, calculated on the basis of established

Markel International Insurance Company Limited 18

Annual Report and Financial Statements for the year ended 31 December 2015

earnings patterns or time apportionment as appropriate. In the opinion of the Directors, theresulting provision is not materially different from one based on the pattern of incidence of risk.

iii) Outwards reinsurance premiums are accounted for in the same accounting period as thepremiums for the related direct or inwards reinsurance business being reinsured.

iv) Acquisition costs, which represent commission and other expenses related to the production ofbusiness, are deferred and amortised over the period in which the related premiums are earned.

v) Provision for unexpired risks is made where claims and related expenses likely to arise after theend of the financial year in respect of contracts concluded before that date are expected toexceed the unearned premiums receivable, less the related deferred acquisition costs, under thesecontracts. Provision for unexpired risks is calculated separately by class and includes an allowancefor investment return. Unexpired risk surpluses and deficits are offset where in the opinion of theDirectors the business classes concerned are managed together and in such cases a provision forunexpired risks is made only where there is an aggregate deficit.

vi) Claims incurred comprise claims and claims handling expenses paid in the year and the change inprovisions for outstanding claims, including provisions for claims incurred but not reported andclaims handling expenses. The adequacy of the outstanding claims provisions is assessed byreference to projections of the ultimate development of claims in respect of each underwritingyear. Management continually attempts to improve its loss estimation process by refining itsability to analyse loss development patterns, claims payments and other information, but manyreasons remain for potential adverse development of estimated ultimate liabilities. The process ofestimating loss reserves is a difficult and complex exercise involving many variables and subjectivejudgements. As part of the reserving process, the Company reviews historical data and considersthe impact of various factors such as trends in claim frequency and severity, changes inoperations, emerging economic and social trends, inflation and changes in regulatory andlitigation environments. Significant delays occur in notifying certain claims and a large measure ofexperience and judgement is involved in assessing outstanding liabilities, the ultimate cost ofwhich cannot be known with certainty at the reporting date. The reserve for unpaid losses andloss adjustment expenses is determined on the basis of information currently available. However,it is inherent in the nature of the business written that the ultimate liabilities may vary as a resultof subsequent development.

The two most critical assumptions as regards these claims provisions are that the past is areasonable predictor of the likely level of claims development and that the models used forcurrent business are fair reflections of the likely level of ultimate claims to be incurred. However,the Company believes the process of evaluating past experience, adjusted for the effects ofcurrent developments and anticipated trends, is an appropriate basis for predicting future events.Management currently believes the Company’s gross and net reserves, including the reserves forenvironmental and asbestos exposures, are adequate. There is no precise method, however, forevaluating the impact of any significant factor on the adequacy of reserves, and actual results arelikely to differ from original estimates.

Management has considered environmental and latent injury claims and claims expenses inestablishing the Company’s reserve for unpaid losses and loss adjustment expenses. TheCompany continues to be advised of claims asserting injuries from hazardous materials andalleged damages to cover various clean-up costs affecting policies written in prior years.Coverage and claim settlement issues, such as determining that coverage exists and defining anoccurrence, may cause the actual loss development to show more variation than the rest of theCompany’s book of business. Traditional reserving techniques cannot be used to estimateasbestos-related and environmental pollution claims and so the uncertainty about the ultimatecost of these types of claims is greater than the uncertainty relating to standard lines of business.The Company believes it has made reasonable provisions for claims, although the ultimate liability

19 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

may be more or less than held reserves. The Company believes that future losses associated withthese claims will not have a material adverse effect on its financial position. Still, there is noassurance that such losses will not materially affect the Company’s results of operations for anyperiod. Management is not able to estimate the additional loss, or range of loss, that is reasonablypossible.

vii) Equalisation provisions are established in accordance with the requirements of INSPRU 1.4. Thisprovision, which is in addition to the provisions required to meet the anticipated ultimate cost ofsettlement of claims outstanding as at the reporting date, is required by Schedule 3 toSI2008/410 to be included within technical provisions within the Statement of Financial Positionnotwithstanding that it did not represent liabilities as at the reporting date.

viii) Underwriting acquisition costs, general overheads and other expenses are charged as incurred tothe Income Statement: Technical Account, net of the change in deferred acquisition costs.

c) Financial assets and liabilities

Debt and other fixed income securities are measured at amortised cost in accordance with Chapter11 of FRS 102. For all other financial assets and liabilities, the Company has chosen to apply therecognition and measurement provisions of International Accounting Standard ("IAS") 39 FinancialInstruments: Recognition and Measurement (as adopted for use in the EU).

ClassificationThe accounting classification of financial assets and liabilities determines the way in which they aremeasured and changes in those values are presented in the Income Statement. Financial assets andliabilities are classified on their initial recognition. Subsequent reclassifications are permitted only inrestricted circumstances.

Financial assets and financial liabilities at fair value through profit and loss comprise financial assetsand financial liabilities held for trading and those designated as such on initial recognition.Investments in shares and other variable yield securities, and debt and other fixed income securitiesare designated as at fair value through profit or loss on initial recognition, as they are managed on afair value basis in accordance with the Company’s investment strategy.

RecognitionFinancial instruments are recognised when the Company becomes a party to the contractualprovisions of the instrument. Financial assets are derecognised if the Company‘s contractual rights tothe cash flows from the financial assets expire or if the Company transfers the financial asset toanother party without retaining control of substantially all risks and rewards of the asset. A financialliability is derecognised when its contractual obligations are discharged, cancelled, or expire.

Regular way purchases and sales of financial assets are recognised and derecognised, as applicable,on the trade date, i.e. the date that the Company commits itself to purchase or sell the asset.

MeasurementA financial asset or financial liability is measured initially at fair value plus, for a financial asset orfinancial liability not at fair value through profit and loss, transaction costs that are directlyattributable to its acquisition or issue.

Investment income and expenses

Investment income comprises interest and dividends receivable for the year gross of investmentexpenses. Dividends receivable are stated after adding back any withholding taxation deducted atsource. Investment expenses are charged to the Income Statement: Non-Technical Account on anincurred basis and include the amortisation change in respect of investments carried at amortisedcost.

Markel International Insurance Company Limited 20

Annual Report and Financial Statements for the year ended 31 December 2015

Realised gains or losses represent the difference between net sales proceeds and purchase price, orin the case of investments carried at amortised cost, the latest carrying value. Realised losses mayalso include losses recognised on impairment of securities. Unrealised gains and losses oninvestments represent the difference between the current value of investments at the reporting dateand their purchase price. The movement in unrealised investment gains/losses includes anadjustment for previously recognised unrealised gains/losses on investments disposed of in theaccounting period. In the event that an unrealised investment loss is deemed more permanent innature, the loss is recognised as a realised loss and unrealised losses are adjusted accordingly.

Cash and cash equivalentsCash and cash equivalents comprise cash balances and call deposits with maturities of three monthsor less from the acquisition date that are subject to an insignificant risk of changes in fair value, andare used by the Company in the management of its short-term commitments.

Cash and cash equivalents are carried at amortised cost in the Statement of Financial position.

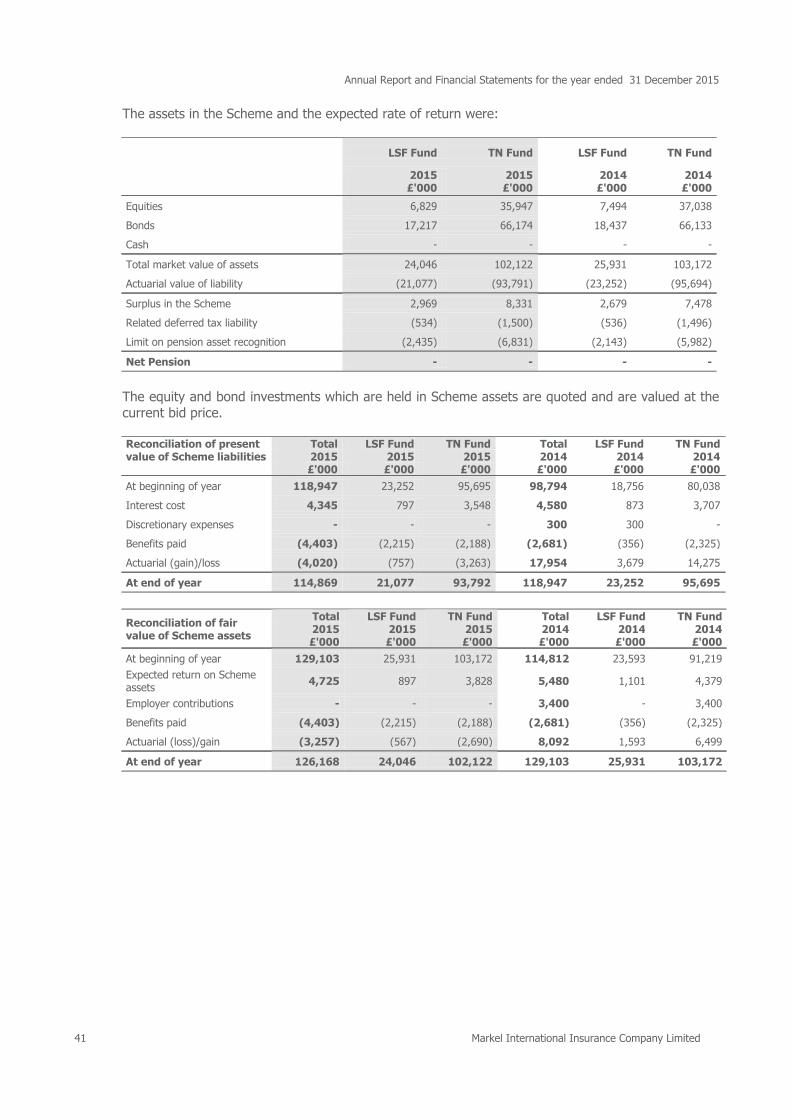

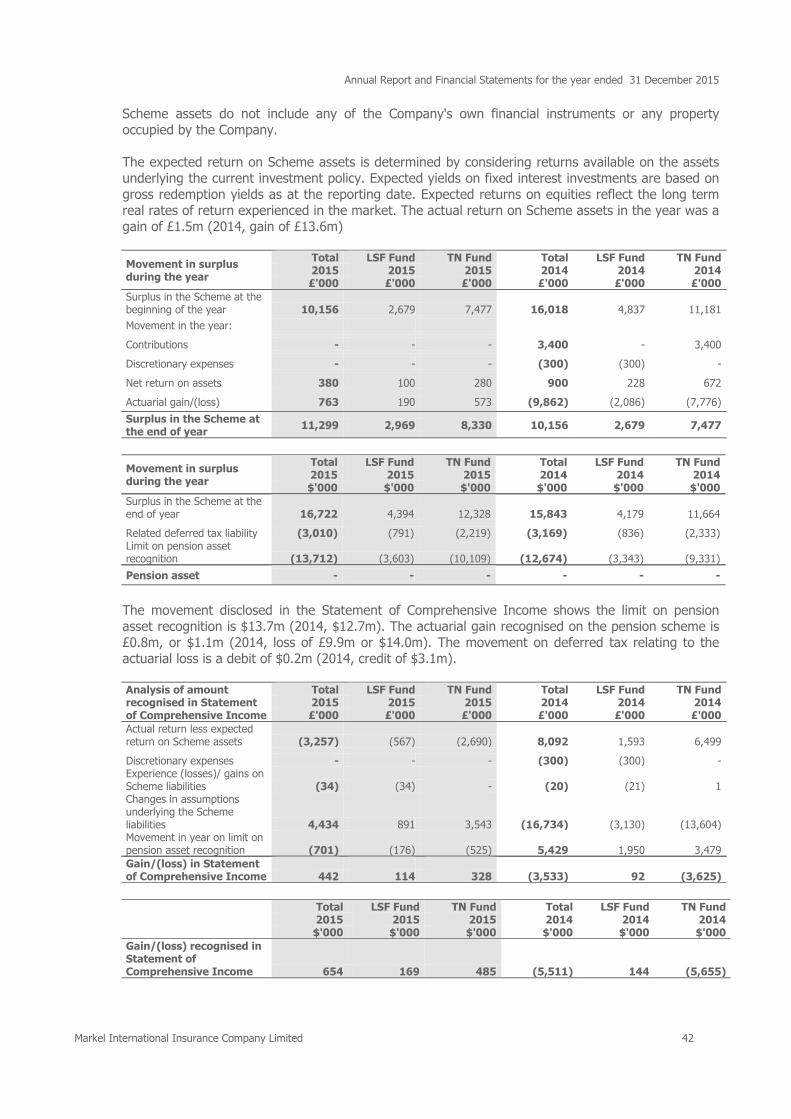

d) Pension costs

The Company operates a pension scheme providing benefits based on final pensionable pay. Theassets of the Scheme are held separately from those of the Company.

Pension scheme assets are measured using current values. Pension scheme liabilities are measuredusing a projected unit method and are discounted at the current rate of return on a high qualitycorporate bond of equivalent term and currency to the liability. The Pension Scheme deficit isrecognised in full, but any surplus is not recognised. The movement in the Scheme is split betweenservice costs and returns recognised in the profit and loss account, and contributions, actuarial gainsand losses and asset recognition limits recognised in the Statement of Comprehensive Income.

e) Financial Investments

Debt and other fixed income securities are measured at amortised cost. All other investments arestated at market value based on bid price and deposits with credit institutions are stated at cost.Financial investments recorded at market value will fall into one of the three levels in the fair valuehierarchy as follows:

i) Included in the level 1 category are financial assets that are measured by reference to publishedquotes in an active market. A financial instrument is regarded as quoted in an active market if quotedprices are readily and regularly available from an exchange, dealer, broker, industry group, pricingservice or regulatory agency and those prices represent actual and regularly occurring markettransactions on an arm’s length basis.

ii) Included in the level 2 category are financial assets measured using a valuation technique basedon assumptions that are supported by prices from observable current market transactions. Forexample, assets for which pricing is obtained via pricing services but where prices have not beendetermined in an active market, financial assets with fair values based on broker quotes, investmentsin private equity funds with fair values obtained via fund managers and assets that are valued usingthe Company’s own models whereby the significant inputs into the assumptions are marketobservable.

iii) Included in the level 3 category, are financial assets measured using a valuation technique(model) based on assumptions that are neither supported by prices from observable current markettransactions in the same instrument nor are they based on available market data. Therefore,significant unobservable inputs reflect the Company's own assumptions about the assumptions thatmarket participants would use in pricing the asset or liability (including assumptions about risk).These inputs are developed based on the best information available, which might include theCompany’s own data.

21 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

f) Investments in subsidiaries

Investments in subsidiaries are stated at the lower of cost and net realisable value.

g) Operating leases

Annual rentals relating to operating leases are charged to net operating expenses on a straight linebasis over the lease term.

h) Foreign currency translation

The Company’s functional currency and presentational currency is US Dollars. Transactionsdenominated in currencies other than the functional currency are recorded in the functional currencyat the exchange rate ruling at the date of the transactions.

Monetary assets and liabilities denominated in foreign currencies are retranslated into the functionalcurrency at the exchange rate ruling on the reporting date.

Non-monetary assets and liabilities denominated in a foreign currency, measured at fair value, aretranslated into the functional currency at the date when the fair value was determined.

Exchange differences are recorded in the Income Statement.

i) Taxation

Taxation is charged by reference to the taxable income included in the Income Statement: Non-Technical Account.

j) Deferred taxation

Full provision is made for deferred taxation assets and liabilities arising from timing differencesbetween the recognition of gains and losses in the Financial Statements and their treatment fortaxation purposes on an undiscounted basis. Deferred taxation assets are recognised to the extentthat it is more likely than not that there will be suitable taxable profits from which the future reversalof the underlying timing differences can be deducted.

k) Tangible assets

Tangible assets are stated at cost less accumulated depreciation. Depreciation is calculated to writeoff the original cost of tangible assets over their expected lives at the following rates:

- Leasehold improvements, Dublin office 11 years- Leasehold improvements, Colombian office 5 years- IT equipment, Colombian office 3 years

The Company assesses at each reporting date whether tangible assets are impaired.

l) Merger accounting

Business combinations are accounted for using the merger accounting method, which treats themerged entities as if they had been combined throughout the current and comparative accountingperiods. Merger accounting principles for these combinations are recorded in the 'other reserve’ inthe Statement of Changes in Equity, being the difference between the nominal value of new sharesissued by the Company for the acquisition of the shares of the merged entity and the merged entity'sown share capital and share premium account.

Markel International Insurance Company Limited 22

Annual Report and Financial Statements for the year ended 31 December 2015

2 Management of financial and insurance risk

Financial and insurance risk management objectivesThe Company is exposed to financial and insurance risks primarily through its financial assets,reinsurance assets and policyholder liabilities. The Company's risk management process is controlledvia the use of a risk register. Solvency II principles are used to manage the Company's capitalrequirements and to ensure that it has the financial strength to support the growth of the businessand meet the requirements of policyholders, regulators and rating agencies. The key financial andinsurance risks assessed are underwriting risk, reserving risk, market risk, credit risk and liquidity risk.

a) Underwriting risk

Underwriting Risk is the risk of loss arising from the inherent uncertainties as to the occurrence,amount and timing of insurance liabilities, focusing on risks that arise from the acceptance ofbusiness.

All underwriting at the Company is governed by high level “underwriting principles” that set outimperatives for underwriting. The first of these is related to underwriting profitable business and is“price business at a level which would enable the Company to achieve the agreed target combinedratios under US GAAP”. The Company's fundamental objective is to underwrite profitably on a grossbasis and to achieve target combined ratios. A combined ratio is the ultimate loss ratio plus expenseratio. This measure of underwriting performance excludes any benefit from investment return andfocuses attention on premium charged, coverage granted, commissions and other deductions and alldirect and indirect expenses.

The Company's underwriters and units are assigned combined ratio targets and underwriting bonusesare based on the achievement of these targets. Bonuses are readjusted, and payments made over anumber of years in line with management’s assessment of how the claims are developing on thatparticular year’s underwriting. The readjustment ensures that rewards are based on a continuingprofitability of an underwriting year over its historical development and the phasing of paymentsassists in the retention of key underwriting staff.

The Company sets prudent maximum linesizes. All underwriters have written underwritingauthorities and there are peer reviews/review processes in place to ensure that businessunderwritten does not exceed authority or is outside our business plan. Risks exceeding 18 monthsare not permitted to be written without the prior, written approval of the Director of Underwriting,although certain general exceptions are made. For example, in respect of Marine Construction riskswhere matching reinsurance exists and this has been agreed in advance as part of the Company'sunderwriting strategy. Compliance with linesize and policy duration is monitored by the Company'sLegal and Regulatory department.

Technical pricing has been developed for many classes, and rate movements have been monitoredsince 2002.

An independent reviewer performs a qualitative review of underwriting.

For natural catastrophe risk a key method of monitoring the Company's aggregate exposures is theproduction of a quarterly “Aggregations pack” which sets out the Company's exposures, both grossand net, to each material region or peril it is exposed to. This is reviewed at a quarterly"Aggregations" meeting by executives and other senior management along with the catastrophemodelling team and representatives from relevant units. Units are given aggregate limits forcatastrophe business in each zone and adherence to these is monitored within the pack. Naturalcatastrophe exposures form part of Risk Management’s quarterly assessment of risk to the Risk andCapital Committee and to the Board.

23 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

b) Reserving risk

Reserving risk is the risk of loss arising from the inherent uncertainties as to the occurrence, amountand timing of insurance liabilities, focusing on risks that arise from the quantification of thoseliabilities.

Claims handling guidelines set out the Company's approach to claims, including:

• Claims diaries – claims adjusters must ensure that they diarise relevant dates when necessaryand/or stipulated in the relevant divisional claims handling protocols. There are protocols regardingwhich types of claims are subject to diary management, and targets set are monitored on amonthly basis.

• Panel of third party advisors – a panel of approved third party advisors (Attorneys and Adjusters)has been established. Third party advisors can only be appointed with sign off from a claimsmanager.

• Claims peer review audits – each underwriting unit is subject to a periodic claims audit of selectedclaims files for identifying strengths and weaknesses in the handling of claims. Senior independentclaims personnel are responsible for the qualitative review of the handling of files.

• Static outstanding's – reports on claims that have not been reviewed for 12 months are discussedby management.

A full Actuarial reserving exercise occurs quarterly. This involves internal review within the Actuarialdepartment and discussions with relevant underwriters and claims staff. IBNR packs are producedwhich contain gross and net projections for all classes of business written at MINT. The IBNR packsare discussed in detail at quarterly “Combined Ratio Meetings”, which are attended by members ofthe Board, each unit and the reserving Actuaries.

A full reserving process document is maintained and control owners confirm quarterly that keycontrols are in place and are operating effectively.

c) Market risk

Market risk is the risk that the Company suffers loss from volatility or over-concentration in itsinvestment portfolio or due to currency mismatch between assets and liabilities.

Risk appetites are agreed annually by the Board to limit investment concentration. Adherence tothese is monitored at the Market Risk Committee and also at the Risk and Capital Committee throughKey Risk Indicators. Any exceptions to risk appetite are reported to the Board.

The Company's investment manager, Markel Gayner Asset Management Corporation ("MGAM")produces a quarterly Investment Report and in conjunction with the Company, produces a Boardreport to explain movements in the investment mix, performance against benchmark indices and anychanges in investment strategy. The principal market risks and how exposure to these risks ismanaged are as follows:

• Interest rate risk: The Company works to manage the impact of interest rate fluctuations on thefixed maturity portfolio. The effective duration of the fixed maturity profile is managed withconsideration given to the estimated duration of policyholder liabilities.

Markel International Insurance Company Limited 24

Annual Report and Financial Statements for the year ended 31 December 2015

As the Company's debt and other fixed income securities are measured at amortised cost the impactof interest rate movements on this portfolio is negligible. The table below sets out the Company'ssensitivity to stock market price movements.

2015$'000

Price risk

Impact on result of 5% increase in stock market prices 7,972

Impact on result of 5% decrease in stock market prices (7,972)

Impact on net assets of 5% increase in stock market prices 6,378

Impact on net assets of 5% decrease in stock market prices (6,378)

• Foreign exchange risk: Foreign exchange risk is managed primarily by matching assets and liabilitiesin each foreign currency as closely as possible. To assist in the matching of assets and liabilities inforeign currencies the Company may purchase foreign exchange forward contracts or buy and sellforeign currencies in the open market. No foreign exchange forward contracts have been enteredinto during the year.

The table below details the matching of material currencies on the Statement of Financial Position.The currencies are reported in converted US dollars.

2015Currency Code GBP'000 USD'000 EUR'000 CAD'000 AUD'000 JPY'000 Other'000 Total'000

Financialinvestments 343,455 870,275 100,954 1,806 6,013 19,732 40,551 1,382,786

Reinsurers' share oftechnical provisions 104,076 479,780 46,993 3,902 3,789 951 25,673 665,164

Insurance andreinsurancereceivables 59,800 140,209 6,598 (267) 1,563 4,153 15,135 227,191

Other assets 24,581 17,669 3,271 - (171) 607 9,153 55,110

Total assets 531,912 1,507,933 157,816 5,441 11,194 25,443 90,512 2,330,251

Technical provisions525,811 777,365 157,464 4,741 6,526 17,717 86,095 1,575,719

Insurance andreinsurancepayables 1,523 95,334 6,003 1,858 1,039 766 5,454 111,977

Other creditors 23,993 42,817 (4,303) (645) (670) 215 470 61,877

Total liabilities 551,327 915,516 159,164 5,954 6,895 18,698 92,019 1,749,573

• Equity price risk: The Company sets limits on the amount of equities that can be held with any oneissuer. The overall equity portfolio is also monitored to ensure that equity risk does not exceed theCompany’s risk appetite.

d) Credit risk

Credit Risk is the risk that a counterparty will be unable to pay amounts in full when they fall due.Key areas where the Company is exposed to credit risk are:

• Amounts recoverable from reinsurers• Amounts due from insurance intermediaries and insurance contract holders• Amounts due from bond issuers

25 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

The Company’s fixed income securities portfolio is monitored to ensure credit risk does not exceedthe Company’s risk appetite. In addition, the Company places limits on exposures to a singlecounterparty or concentrations of exposures to a specific counterparty. At least 90% of theCompany's fixed income securities portfolio is rated 'A' or better.

The Board sets risk appetites for the amount of exposure it is prepared to accept in respect ofreinsurers brokers. These are monitored through reports to Risk and Capital Committee and anyexceptions are reported to the board.

The Company takes a proactive approach to the collection of reinsurance recoveries, including thepursuit of commutations. New reinsurers may be required to post collateral depending on their size,rating and potential debt to the Company. If a reinsurer is not willing to post collateral then their linesize is reduced to an acceptable level in accordance with their applicable rating and capital level.

The table below provides details of the credit rating by asset class.

2015AAA

$'000AA

$'000A

$'000BBB

$'000BB or less

$'000Not rated

$'000Total

$'000

Shares and other variable yieldsecurities and unit trusts - - - - - 159,448 159,448

Debt securities 610,506 241,429 75,415 20,791 - - 948,141

Short term investments 45,598 - - - - - 45,598

Money market funds 17,769 174 52,087 - - - 70,030

Deposits with credit institutions - 53,783 98,102 - - - 151,885

Reinsurers share of claimsoutstanding

4,462 75,625 537,390 - - 164 617,641

Reinsurance debtors 1,151 19,518 138,698 - - 42 159,409

Total credit risk 679,486 390,529 901,692 20,791 - 159,654 2,152,152

Assets not contained in the above table include: debtors arising out of direct insurance operations,deferred acquisition costs and other debtors. These assets have been excluded from the table ascredit ratings are not readily ascertainable.

e) Liquidity risk

Liquidity risk is the risk that cash may not be available to pay obligations when due at a reasonablecost, primarily claims to policyholders. The Company monitors the projected settlement of liabilitiesand, in conjunction with MGAM, sets guidelines on the composition of the portfolio in order tomanage this risk.

The average duration of liabilities is 4 years. The duration of the Company's investment portfolio ismanaged to match the expected cash outflows on liabilities.

Each year liquidity stress tests are undertaken to consider possible liquidity pressures which couldarise following a significant natural catastrophe, including trust fund requirements. These tests areconsidered by the Risk & Capital Committee in order to determine that liquidity risk has beenmitigated to a satisfactory level.

f) Group risk

Group Risk is the risk that actions or events within one part of Markel adversely affect an entity, or allentities, within MINT.

Markel International Insurance Company Limited 26

Annual Report and Financial Statements for the year ended 31 December 2015

It is considered that being part of a larger, experienced insurance group, with considerable financialresources and sound reputation to be a strength. The Company has a number of controls, such asthe internal committees that consider the interests of MINT’s legal entities, and endeavours tocommunicate the MINT perspective to Markel, with whom the Company enjoy an excellentrelationship.

The risk of the Company being part of MINT is also considered. The policy is always to consider theinterests of each legal entity, and the Company's single risk strategy, risk management approach,operational procedures and standards are effective in ensuring that each entity is treated equitably.

g) Capital management

The Company is subject to capital requirements imposed by the PRA. Throughout the year theCompany has complied with both the PRA’s risk based ICA methodology and Solvency I, which isused to calculate the Company’s capital requirement.

3 Analysis of underwriting resulta) Analysis of business by class

2015 Gross

Written

Premiums

$'000

Gross

Earned

Premiums

$'000

Gross

Claims

Incurred

$'000

Gross

Operating

Expenses

$'000

Reinsurance

Balance

$'000

Total

$'000

Direct Insurance

Marine, aviation andtransport

40,754 43,517 (13,198) (15,255) (8,301) 6,763

Fire and other damage toproperty

10,702 23,913 (4,254) (8,382) (4,543) 6,734

Third party liability 223,250 221,811 (120,531) (77,754) (35,307) (11,781)

Miscellaneous 91,642 90,780 (41,082) (31,822) (14,694) 3,182

Total Direct 366,348 380,021 (179,065) (133,213) (62,845) 4,898

Reinsurance 137,098 171,368 (41,945) (60,072) (29,785) 39,566

Total 503,446 551,389 (221,010) (193,285) (92,630) 44,464

2014 Gross

Written

Premiums

$'000

Gross

Earned

Premiums

$'000

Gross

Claims

Incurred

$'000

Gross

Operating

Expenses

$'000

Reinsurance

Balance

$'000

Total

$'000

Direct Insurance

Marine, aviation andtransport

42,832 45,989 (12,276) (20,751) (572) 12,390

Fire and other damage toproperty

41,643 40,428 (42,692) (10,963) 9,028 (4,199)

Third party liability 223,541 226,876 (169,633) (71,245) 8,682 (5,320)

Miscellaneous 89,872 61,551 (36,129) (21,868) (3,600) (46)

Total Direct 397,888 374,844 (260,730) (124,827) 13,538 2,825

Reinsurance 225,911 209,085 (94,942) (75,761) (30,156) 8,226

Total 623,799 583,929 (355,672) (200,588) (16,618) 11,051

27 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

b) Analysis of premium by geographic areaby origin:

Gross Written Premiums Profit /(Loss)

Before Taxation2015$'000

2014$'000

2015$'000

2014$'000

United Kingdom

Direct 271,255 250,339 18,323 12,683

United States

Direct (7) 3,248 (148) (517)

Rest of World

Direct 580 - (10) 1

Europe (excluding UK)

Direct 94,520 144,301 (13,267) (9,342)

366,348 397,888 4,898 2,825

Reinsurance 39,566 8,226

Change in the equalisation provision 12,424 (5,594)

Investment return 39,094 84,359

Foreign exchange gains/(losses) 2,169 (798)

Profit on ordinary activities before taxation 98,151 89,018

Direct insurance written in the United States comprises Excess and Surplus Lines business written inthose states where the Company is an authorised insurer.

by destination:

Gross Written Premiums

2015$'000

2014$'000

United States 61,795 76,187

United Kingdom 229,643 289,822

Europe (excluding UK) 88,193 113,378

Rest of the world 123,597 144,241

Canada 218 171

Total 503,446 623,799

4 Movement in prior year's provision for claims outstanding

The Company experienced a net favourable loss development in the year of $100.6m (2014,$79.2m). This comprised the following developments by class:

2015$'000

2014$'000

Marine, aviation & transport 34,860 20,042

Fire and other damage to property 6,672 630

Third party liability 39,176 42,036

Miscellaneous 8,615 3,500

Reinsurance 11,247 12,986

Total 100,570 79,194

Markel International Insurance Company Limited 28

Annual Report and Financial Statements for the year ended 31 December 2015

5 Net operating expenses

2015$'000

2014$'000

Acquisition costs 107,056 119,644

Change in deferred acquisition costs (212) (13,284)

Administrative expenses 86,441 94,228

Gross operating expenses 193,285 200,588

Reinsurance commissions and profit participation (34,717) (62,816)

Net operating expenses 158,568 137,772

Total commissions for direct insurance accounted for during the year amounted to $76.3m (2014,$74.3m).

6 Investment income

2015$'000

2014$'000

Income from investments 43,520 46,310

Gains on the realisation of investments 83,471 7,706

Total 126,991 54,016

7 Investment expenses and charges

2015$'000

2014$'000

Investment management expenses, including interest 7,015 4,963

Amortisation of fixed interest securities 3,589 2,495

Losses on the realisation of investments 865 242

Total 11,469 7,700

8 Investment return

2015$'000

2014$'000

Investment income 126,991 54,016

Investment expenses and charges (11,469) (7,700)

Unrealised (losses)/gains on investments (75,831) 38,965

Impairment losses on subsidiary (597) (922)

Actual return on investments 39,094 84,359

29 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

9 Profit on ordinary activities before taxation 2015$'000

2014$'000

Profit on ordinary activities before taxation is stated after charging:

Rentals under operating leases - land and buildings 1,814 1,206

Depreciation 891 188

10 Rates of exchangeThe rates of exchange used for the principal foreign currency translations are as follows:

Year-EndRate 2015

AverageRate 2015

Year-EndRate 2014

AverageRate 2014

Sterling 0.68 0.65 0.64 0.61

Canadian dollar 1.39 1.28 1.16 1.10

Euro 0.92 0.90 0.82 0.75

Australian dollar 1.37 1.33 1.22 1.11

11 Taxation a) Analysis of charge for the year

Total taxation charge in the Statement of Comprehensive Income.

2015$'000

2014$'000

Current Taxation

Current tax on profit for the period 20,418 16,920

Adjustment in respect of prior periods 4,259 (2,768)

Total current tax charge 24,677 14,152

Deferred Taxation

Origination and reversal of timing differences (43) 1,682

Total deferred tax (credit)/charge (43) 1,682

Adjustment relating to changes in accounting policy - (302)

Taxation charge on profit on ordinary activities 24,634 15,532

Analysis of current tax recognised in the Statement of Comprehensive Income

2015$'000

2014$'000

UK corporation tax (24,677) (13,850)

Total current tax recognised in the Statement of Comprehensive Income(24,677) (13,850)

Markel International Insurance Company Limited 30

Annual Report and Financial Statements for the year ended 31 December 2015

b) Factors affecting the taxation charge for the year

The taxation charge assessed for the year is higher (2014, lower) than the standard rate ofcorporation taxation in the UK of 20.25% (2014, 21.5%). The differences are explained below:

2015$'000

2014$'000

Profit on ordinary activities before taxation 98,151 89,018

Profit on ordinary activities multiplied by standard effective rate of corporation taxation in theUK of 20.25% (2014, 21.50%)

19,876 19,139

Effects of

Dividend income not taxable (882) (966)

Loss on revaluation of investments in subsidiaries 109 198

Other permanent differences 1,507 (1,141)

Prior year adjustment 4,259 (2,768)

Payments in respect of group relief claims - 2,474

Recovery due from HMRC - (2,458)

Tax charge relating to change in accounting policy - (302)

Effect of tax rates in foreign jurisdictions - (297)

Recognition of trading losses carried forward (269) -

Other 34 1,653

Total tax charge for the year 24,634 15,532

12 Directors' remunerationThe disclosed remunerations are paid by Markel International Services Limited ("MISL") to Directorsfor their services to the Company. The remunerations are disclosed here in full as this is theCompany to which the largest proportion of their remuneration relate.

2015£

2014£

Aggregate remuneration 5,576,444 4,771,621

Company pension contributions to money purchase schemes 110,000 102,292

Retirement benefits are accruing to four Directors under defined contribution pension schemes (2014,four) and to two Directors under a defined benefit scheme (2014, two).

In February 2016, 1,160 Markel shares were awarded to seven Directors vesting on 31 December2018 based on continuous employment to that date.

Highest paid Director

2015£

2014£

Aggregate remuneration and benefits under long term incentives (excluding gains onexercise of share options and value of shares received)

1,131,715 1,006,811

The highest paid Director did not participate in the defined benefit scheme.

In February 2016, 287 Markel shares were awarded to the highest paid Director vesting on 31December 2018 based on continuous employment to that date.

31 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

13 Staff numbers and costsThe majority of staff are employed by MISL. For a full breakdown of employment costs, please referto the Annual Report and Financial Statements of MISL. The staff based in Columbia are employed byMIICL. A breakdown of their employment costs is provided below.

Staff costs 2015$'000

2014$'000

Wages and salaries 2,243 1,786

Social security costs 340 128

Other pension costs 128 61

2,711 1,975

The average number of employees of the Company during the year were as follows:

2015 2014

Administration and finance 9 4

Sales, marketing and underwriting 6 6

15 10

14 Auditor's remuneration

2015$

2014$

Audit of the Financial Statements 239,700 251,100

Other services pursuant to legislation 240,500 120,600

Total 480,200 371,700

Auditor's remuneration is included as part of the administrative expenses in note 5 to the financialstatements.

15 Investments

Investments in subsidiaries and participating interests

Carrying Value Cost

2015$'000

2014$'000

2015$'000

2014$'000

Shares in subsidiaries at beginning of year 6,459 7,381 8,538 8,538

Impairment loss on subsidiary (537) (922) - -

Shares in subsidiaries at end of year 5,922 6,459 8,538 8,538

Markel International Insurance Company Limited 32

Annual Report and Financial Statements for the year ended 31 December 2015

Set out below are the Company's subsidiaries as at 31 December 2015.

Name of Company Country of Registration Holding Nature of Business

Markel Syndicate Management Limited England and Wales 100% Ordinary Shares Underwriting Agent

Markel International Services Limited England and Wales 100% Ordinary Shares* Expense Services

Markel Europe Limited England and Wales 100% Ordinary Shares*Insurance Agent ServiceCompany

*held by Markel Syndicate Management Limited

Other financial investments

Carrying Value Cost

2015$'000

2014$'000

2015$'000

2014$'000

Shares and other variable yield securities and units in unittrusts

159,448 337,379 54,984 157,024

Debt securities and other fixed income securities 948,141 971,243 953,251 980,480

Short term investments (debt securities and commercialpaper)

45,598 45,616 45,598 45,616

Money market funds 70,030 99,012 70,030 99,012

Deposits with credit institutions 151,885 185,337 151,885 185,337

Total 1,375,102 1,638,587 1,275,748 1,467,469

2015Level 1

$'000Level 2

$'000Level 3

$'000Total

$'000

Shares and other variable yield securities and units in unittrusts

159,448 - - 159,448

Short term investments (debt securities and commercialpaper)

45,598 - - 45,598

Money market funds 70,030 - - 70,030

Deposits with credit institutions 151,885 - - 151,885

Total 426,961 - - 426,961

2014Level 1

$'000Level 2

$'000Level 3

$'000Total

$'000

Shares and other variable yield securities and units in unittrusts

336,597 782 - 337,379

Short term investments (debt securities and commercialpaper)

45,616 - - 45,616

Money market funds 99,012 - - 99,012

Deposits with credit institutions 185,337 - - 185,337

Total 666,562 782 - 667,344

33 Markel International Insurance Company Limited

Annual Report and Financial Statements for the year ended 31 December 2015

The debt and other fixed income securities which are shown at amortised cost are analysed below:

2015$'000

2014$'000

Cost 953,251 980,480

Cumulative amortisation (5,110) (9,237)

Amortised cost 948,141 971,243

Market Value 996,850 1,039,524

The redemption value of investments held at the year end was $35.3m higher (2014, $13.3m lower)than the amortised cost.

16 Debtors arising out of direct insurance operations and reinsurance operations

Direct InsuranceOperations

Reinsurance Operations

2015$'000

2014$'000

2015$'000

2014$'000

Amounts owed by fellow subsidiaries 280 776 36,634 -

Amounts owed by intermediaries 67,502 204,288 122,775 31,485

Total 67,782 205,064 159,409 31,485

17 Deferred taxation The provision for deferred taxation has been made on a full provision basis. The deferred taxationasset comprises amounts arising on:

2015$'000

2014$'000

Difference between accumulated depreciation and capital allowances 95 129

Other timing differences - 192

Recognition of trading losses carried forward 269 -

Total asset 364 321

The movement in the deferred taxation asset/(liability) during the year is as follows:

DeferredTax

Asset

PensionTax

Liability Total Total

2015$'000

2015$'000

2015$'000

2014$'000

At beginning of year 321 (3,169) (2,848) (3,282)

Income Statement charge - current 43 - 43 (2,650)

Movement in Statement of Comprehensive Income - 159 159 3,084

At end of year 364 (3,010) (2,646) (2,848)

Deferred taxation is calculated at the anticipated standard rate of UK corporation tax effective from 1April 2015 of 18.0% (2014, 20.0%). No deferred tax is recognised in respect of the pension asset.

Deferred tax in respect of timing differences expected to reverse in 2016 and subsequent years has

Markel International Insurance Company Limited 34

Annual Report and Financial Statements for the year ended 31 December 2015