Embed Size (px)

Citation preview

1

Mark D. Abrahams, CPA

President, The Abrahams Group

May 2015

Recreation Accounting Options under Massachusetts General Laws

2

Session Description

This session discusses several accounting options for recreation activities. To operate recreation programs under(1) A municipal revolving fund under the provisions of MGL 44:53E½. (2) A recreation revolving fund under MGL 44:53D.(3) An enterprise fund under MGL 44:53F½.

3

Learning Outcomes

Participants will be able to:1. Understand the pros and cons for operating recreation programs

using a municipal revolving fund under the provisions of MGL 44:53E½

2. Understand the pros and cons for operating the recreation programs under MGL 44:53D, a Recreation Revolving fund.

3. Understand the pros and cons for operating the recreation programs under the enterprise fund statute, 44:53F½.

4

Basic Premise

• One of the most fundamental principles of municipal finance in Massachusetts is established by M.G.L. Ch. 44 Sec. 53. • It creates the basic rule that all revenues from any source are

unrestricted general revenues available for expenditure for any valid municipal purpose after appropriation by the municipality’s legislative body.

5

Basic Premise - Exceptions

• There are many exceptions that permit particular receipts to be segregated into a separate, special fund. • However, any exception to M.G.L. Ch. 44 Sec. 53 must be created by

another statute, either a general law or special act that applies to the particular city or town. • A special fund cannot be created by the selectmen, mayor, finance

director, or department head, commissioners, a vote of the legislative body, or bylaw or ordinance.

6

Funds

Fund Types• General Fund• Special Revenue Funds• Capital Projects Funds• Enterprise Funds• Trust Funds• Agency Funds

Special Revenue Funds• Revolving Funds• Receipt Reserved for

Appropriations• Grants (State, Federal, Private)• Gifts and Donations

7

Recreation Funds

General Fund

Special Revenue Funds1. Municipal revolving fund under the provisions of MGL 44:53E½.2. MGL 44:53D, a Recreation Revolving fund.

Enterprise Fund3. Enterprise fund statute, MGL 44:53F½.

8

Options/Objectives – General Fund• The city or town always has the option of funding Recreation entirely

through the General Fund with fees as local receipts. • All expenditures budgeted in the general fund.• All receipts budgeted in the general fund.• Not to be confused with the recreation revolving fund or recreation

municipal revolving fund where the recreation budget is included in the general fund, usually full time salaries, and fees are generally set to recover direct operating program costs in the revolving funds.

9

Recreation Revolving Fund, 44:53D

• A town may establish a revolving fund which will be kept separate and apart from all other monies by the treasurer and in which shall be deposited the receipts received in connection with the conduct of self-supporting recreation and park services. • The principal and interest will be expended at the direction of the town

authority, commission, board or official without further appropriation, but only with the written approval of the selectmen in towns and only for the purpose of operating self-supporting recreation and park services. • The town accountant is required to submit annually a report of the

revolving fund to the board of selectmen for their review and a copy of the report to the director of the bureau of accounts.

10

Recreation Revolving Fund, 44:53D

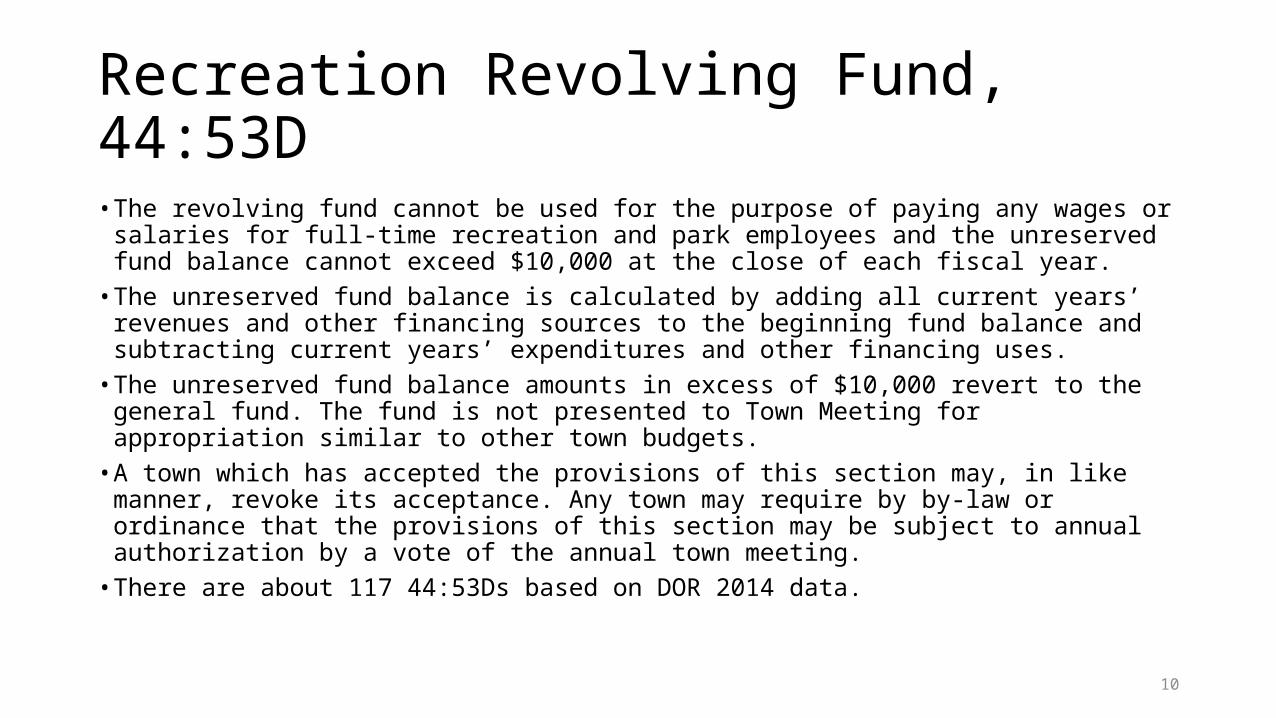

• The revolving fund cannot be used for the purpose of paying any wages or salaries for full-time recreation and park employees and the unreserved fund balance cannot exceed $10,000 at the close of each fiscal year.

• The unreserved fund balance is calculated by adding all current years’ revenues and other financing sources to the beginning fund balance and subtracting current years’ expenditures and other financing uses.

• The unreserved fund balance amounts in excess of $10,000 revert to the general fund. The fund is not presented to Town Meeting for appropriation similar to other town budgets.

• A town which has accepted the provisions of this section may, in like manner, revoke its acceptance. Any town may require by by-law or ordinance that the provisions of this section may be subject to annual authorization by a vote of the annual town meeting.

• There are about 117 44:53Ds based on DOR 2014 data.

11

MGL 44:53E1/2 - Municipal Revolving Fund • A departmental revolving fund is a place to set aside revenue

received, through fees and charges, for providing a specific service or program. • The revenue pool is, in turn, a source of funds available to use by a

department without further appropriation to support the particular service or program.

12

MGL 44:53E1/2 - Municipal Revolving Fund • Most frequently, cities and towns create general departmental revolving

funds under M.G.L. Ch. 44 Sec. 53E½. • The fund is created with an initial town meeting authorization that

identifies which department’s receipts are to be credited to the revolving fund and specifies the program or purposes for which money may be spent. • It designates the department, board or official with authority to expend the

funds and places a limit on the total amount of the annual expenditure. To continue the revolving fund in subsequent years, annual approval of a similar article is necessary. Thus a rescission vote is not necessary per se.• Managers are also required, each year, to report on the fund and program

activities. However a detailed budget is not presented to Town Meeting.

13

MGL 44:53E1/2 - Municipal Revolving Fund • Under Sec. 53E½, any expenditure from a revolving fund is restricted

to the then current fund balance or to the authorized spending limit, which cannot exceed one percent of the most recent tax levy. • The combined authorized expenditures for all revolving funds cannot

exceed ten percent of the levy.

14

MGL 44:53E1/2 - Municipal Revolving Fund • If a revolving fund balance remains after total spending has reached

the authorized limit, the balance carries over to the next fiscal year. Interest that accrues on a revolving fund balance under Sec. 53E½ reverts to the general fund. • However, if the revolving fund is not reauthorized, any remaining

balance closes to free cash, unless it is transferred by town meeting to another revolving fund. • Including Ch. 53E½, Massachusetts General Laws allow revolving

funds for about a dozen specific, non-school related purposes. Another 13 apply to schools, but are not discussed here.

15

Enterprise Funds, 44:53F1/2

• Increasingly, communities are establishing enterprise funds for their business type services for:• Public Utilities• Health Care• Recreation• Transportation

• Common enterprise activities are water, sewer, trash disposal, ambulance services, skating rinks, pools, golf courses, airports, dock and wharf facilities. • By vote of the city council with the approval of the mayor or by town

meeting, an enterprise is adopted.

16

Enterprise Funds, 44:53F1/2

• Enterprise accounting allows a community to demonstrate to the public the total cost of providing a service. • With all the direct and indirect costs (e.g., interdepartmental support,

health and insurance costs), debt service and capital expenditures associated with providing the service in a consolidated fund, the community will be able to readily identify the true cost of the service.• To support the service, a community may choose to recover total

costs through user charges (rates), through a partial subsidy from the tax levy or from other available funds.

17

Enterprise Funds, 44:53F1/2

• At year-end, the performance of an enterprise fund is measured in terms of positive (surplus) and negative (deficit) operations. • An operating surplus is the result of revenue collected in excess of

estimates and appropriation turnbacks, and translates into retained earnings that are maintained in the fund rather than closing to the general fund. • Retained earnings of an enterprise fund are certified by the Director

of Accounts as an available fund after the submission of a June 30th balance sheet to DLS.

18

Enterprise Funds, 44:53F1/2

• Once certified, retained earnings may be appropriated only for expenditures relating to the enterprise fund. • Conversely, if during the year, the enterprise fund incurs an operating

loss, the loss must be raised in the subsequent year’s budget. • With the consolidation of all related revenues and costs of the service

and information on the operating performance (positive or negative) of the fund, the community will have useful information to make decisions on user charges and other budgetary items.

19

Enterprise Funds, 44:53F1/2

• The community will be able to analyze how much the user fees and charges support the service and to what extent if any the tax levy or other available revenues are needed to subsidize the enterprise fund. • The community will also be able to include the fixed assets and

infrastructure of the enterprise as assets in the financial statements and recognize the annual depreciation of these assets. • Establishing an enterprise does not create a separate or autonomous

entity from the municipal government operation. Like every other department, a budget is prepared that is reviewed and analyzed by the finance committee.

20

Enterprise Funds, 44:53F1/2

• There are about 586 enterprise funds in Massachusetts (FY14 data), and increase of 80 since FY10.• Predominantly water (159) and sewer (154).• Recreation 23 (FY14), an increase of 7 since FY10.

21

Enterprise Funds, 44:53F1/2

The following presents the major highlights with an enterprise fund:• Interest is retained in the fund.• A balanced revenue and expenditure budget is to be presented to the Town Administrator

within 120 days of the start of a fiscal year. This budget must identify • (1) all direct enterprise fund costs• (2) indirect costs incurred in the general fund and allocated to the enterprise fund for funding • (3) any subsidy provided by the general fund

• Indirect costs are to be calculated in a fair and reasonable manner and are to be documented.• Balances are retained in the enterprise fund. Retained earnings are certified by the

Department of Revenue. Monies can be spent from retained earnings for any legal purpose only after certification by DOR.

• The enterprise fund is not required to recover its costs with enterprise generated revenues.

22

Enterprise Funds, 44:53F1/2

• The major difference with an enterprise fund for the Recreation Department is that this will require the Department to budget its program expenditures and corresponding revenues in January as part of the town budget process for the next fiscal year. • This would present challenges to the way Recreation Departments

currently budget.

23

To Accept

• To see if the town will accept the provisions of Chapter 44, § 53D of the Massachusetts General Laws establishing recreation as an revolving fund effective fiscal year 2016.• To see if the town will accept the provisions of Chapter 44, § 53E1/2 of

the Massachusetts General Laws establishing recreation as a department revolving fund effective fiscal year 2016.• To see if the town will accept the provisions of Chapter 44, § 53E1/2 of

the Massachusetts General Laws establishing recreation as an enterprise fund effective fiscal year 2016.• Any fund balance of one fund must be transferred by town meeting to

the new fund or else the fund balance reverts to the general fund.

24

Options/Objectives – Enterprise Funds• If it is the Town’s objective to have a full presentation of the revenues and expenditures

of the Recreation Department including indirect costs, potential offsets, and any subsidies, then the enterprise fund structure makes the most sense. This option would present the full Recreation budget annually to Town Meeting.

• Given the nature of Recreation programs, the Recreation Department may request additional appropriations at the spring town meeting for the then current budget year based on increased revenues and programming decisions. If there is no spring town meeting, the Recreation Commission would not be in a position to adjust its budget through a town meeting vote.

• The issue of whether recreation should be self-sustaining is a separate issue. The Town may have a Recreation enterprise fund that has a subsidy from the general fund.

• The enterprise fund option would identify the general fund subsidy. The other options do not. Additional analyses would be needed to determine the subsidy.

25

Options/Objectives – Recreation Revolving Funds• If it is the Town’s objective to keep full time salaries in the general

fund, account for program revenues and expenditures in the revolving fund and not account for indirect costs, then the 44:53D structure makes the most sense. • This option would present the general fund full time salaries to Town

Meeting for appropriation, not the full Recreation budget. This option would not include indirect costs and would require any unreserved fund balance greater than $10,000 to revert to the general fund.• Interest remains with the fund.

26

Options/Objectives – Recreation Municipal Revolving Funds• If it is the Town’s objective to keep full time salaries in the general

fund, account for program revenues and expenditures in the revolving fund and not account for indirect costs, then the 44:53E1/2 structure makes the most sense. • This option would present the general fund full time salaries to Town

Meeting for appropriation, not the full Recreation budget. This option would not include indirect costs and would limit the fund to 1% of the previous years’ tax levy.• Interest remains in with the fund.

27

Options/Objectives – Recreation Municipal Revolving Fund – 44:53F1/2

• The municipal revolving fund is a viable option• However, the 1% ceiling limits the ability to operate a municipal

revolving fund under Chapter 44 Section 53E½. • For the 44:53E½to be viable, the cap may need to be increased by

special legislation. The Town of Brookline raised its 44:53E½ to 2.5% of its levy through a special act, a process that took four years to complete.

28

Summary

• General Fund• Recreation Municipal Revolving Fund – 44:53F1/2• Recreation Revolving Fund – 44:53D• Recreation Enterprise Fund – 44:53F1/2

29

For Further Information

Mark D. Abrahams, CPAPresident, The Abrahams Group52 Flanagan Drive Framingham, MA 01701Office 508 788-9172Cell 617 803-8529Fax 508 788-617Email [email protected] www.theabrahamsgroup.com