Embed Size (px)

Citation preview

Maricopa CountyEconomic and Fiscal Issues

Presentation to theGovernment Accountability Office Review Team

Maricopa County Office of Management and BudgetOctober 8, 2009

Local Economy

Arizona Employment Rank Among 50 States1980 – 2009 Growth Over Previous Year Source: Arizona State University

79

18

2 1 13

19

38

35

28

2022

5

2 2 2 2 1 2

5

8

12

42 2 2

22

47

1

6

11

16

21

26

31

36

41

46

1980 200819941982 1984 1986 1988 1990 1992 1996 1998 2000 2002 2004 2006

= YTD August = 49

Recession Periods

Provided by Elliott D. Pollack and Co.

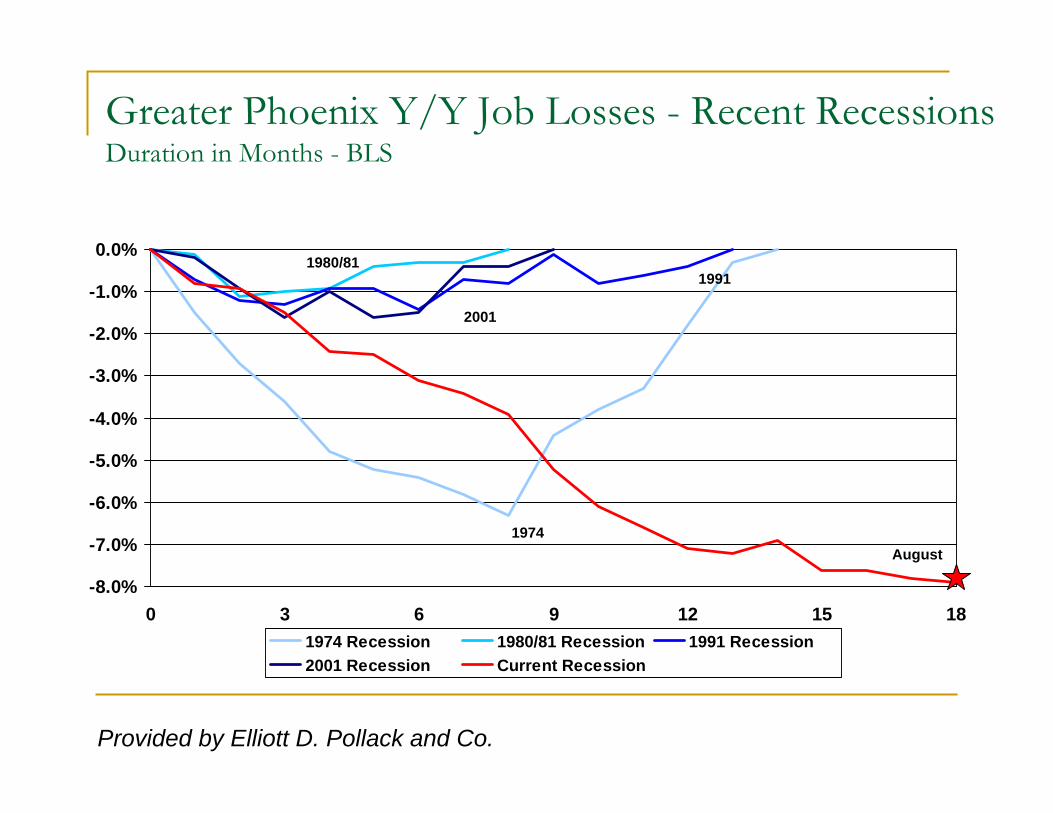

Greater Phoenix Y/Y Job Losses - Recent RecessionsDuration in Months - BLS

-8.0%

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

0 3 6 9 12 15 181974 Recession 1980/81 Recession 1991 Recession2001 Recession Current Recession

1980/81

1974

2001

1991

August

Provided by Elliott D. Pollack and Co.

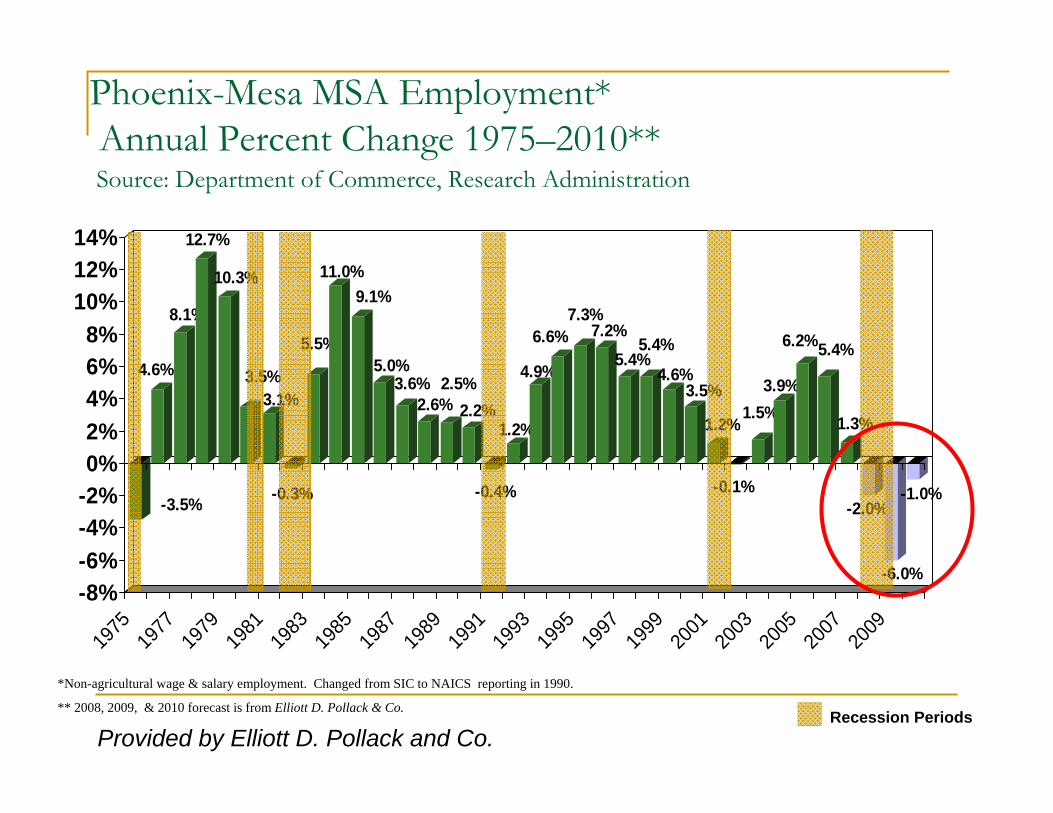

Phoenix-Mesa MSA Employment*Annual Percent Change 1975–2010**Source: Department of Commerce, Research Administration

-3.5%

4.6%

8.1%

12.7%

10.3%

3.5%3.1%

-0.3%

5.5%

11.0%9.1%

5.0%3.6%

2.6%2.5%

2.2%

-0.4%

1.2%

4.9%

6.6%7.3%

7.2%5.4%

5.4%

4.6%3.5%

1.2%

-0.1%

1.5%3.9%

6.2%5.4%

1.3%

-2.0%

-6.0%

-1.0%

-8%-6%-4%-2%0%2%4%6%8%

10%12%14%

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

*Non-agricultural wage & salary employment. Changed from SIC to NAICS reporting in 1990.

** 2008, 2009, & 2010 forecast is from Elliott D. Pollack & Co. Recession PeriodsProvided by Elliott D. Pollack and Co.

Employment Levels: Greater Phoenix back to Peak in 2014Source: ADOC

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

2,000.0

2,200.0

2,400.0

Jan-95

Jul-95

Jan-96

Jul-96

Jan-97

Jul-97

Jan-98

Jul-98

Jan-99

Jul-99

Jan-00

Jul-00

Jan-01

Jul-01

Jan-02

Jul-02

Jan-03

Jul-03

Jan-04

Jul-04

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

Jul-10

Jan-11

Jul-11

Jan-12

Jul-12

Jan-13

Jul-13

Jan-14

Jul-14

Recession Periods

Peak

Provided by Elliott D. Pollack and Co.

Phoenix-Mesa Employment Source: Arizona Department of Commerce, Research Administration

-0.7%Health Services

0.0%Educational Services

-6.5%Other Services

-9.2%Transp. & Utilities

-8.0%Manufacturing

-2.2%Leisure & hosp svcs

-5.5%Government

-11.7%Prof. & Bus. Services

-26.2%Construction

-7.4%Trade

-6.3%

-4.1%

-16.2%

Financial Activities

Information

Mining

Sectors in Decline Sectors Increasing

NONE!!!

Provided by Elliott D. Pollack and Co.

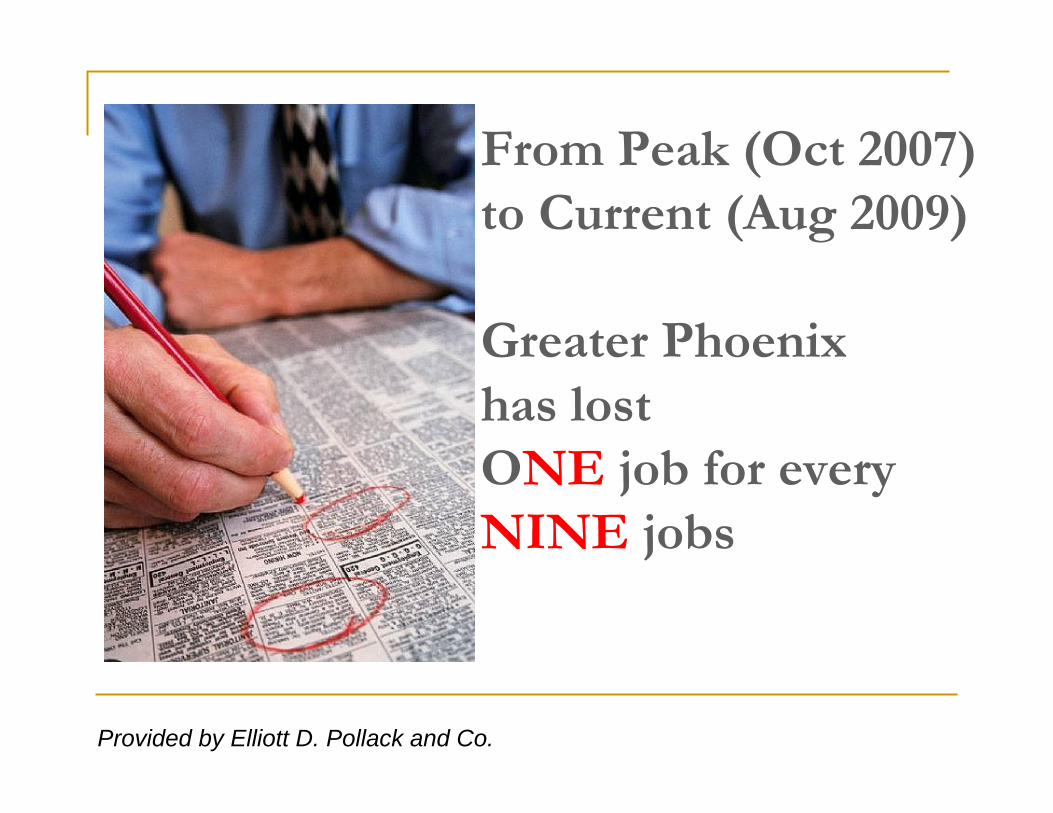

From Peak (Oct 2007) to Current (Aug 2009)

Greater Phoenix has lost ONE job for every NINE jobs

Provided by Elliott D. Pollack and Co.

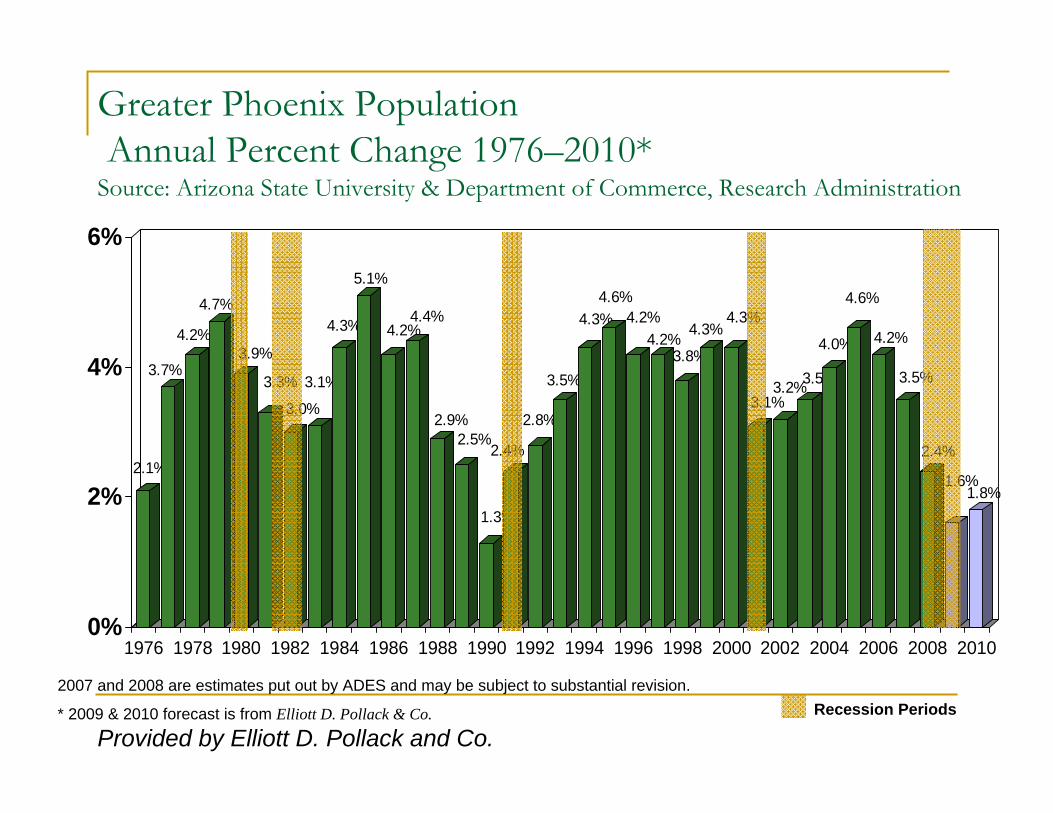

2.1%

3.7%

4.2%

4.7%

3.9%

3.3%

3.0%

3.1%

4.3%

5.1%

4.2%4.4%

2.9%2.5%

1.3%

2.4%

2.8%

3.5%

4.3%4.6%

4.2%4.2%

3.8%

4.3%4.3%

3.1%3.2%3.5%

4.0%

4.6%

4.2%

3.5%

2.4%

1.6%1.8%

0%

2%

4%

6%

1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Greater Phoenix PopulationAnnual Percent Change 1976–2010*

Source: Arizona State University & Department of Commerce, Research Administration

2007 and 2008 are estimates put out by ADES and may be subject to substantial revision.

* 2009 & 2010 forecast is from Elliott D. Pollack & Co. Recession Periods

Provided by Elliott D. Pollack and Co.

Greater Phoenix PopulationNet Change 1975–2010Source: ADOC

35.828.7

50.559.6

69.860.0

52.749.7

53.2

75.6

94.581.3

89.3

60.154.9

29.7

54.6

64.5

83.8

104.2

118.6 111.9115.6

111.0

130.4

136.3

100.5107.8

122.7

146.0

172.9164.6

142.6

103.3

69.4

79.3

020406080

100120140160180200

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

Recession Periods

*Forecasts from Elliott D. Pollack & CompanyProvided by Elliott D. Pollack and Co.

Greater Phoenix Net Migration1975–2010Source: University of Arizona

23.217.3

38.1

47.3

56.1

38.042.4

32.335.4

58.5

74.5

59.466.5

36.9

30.3

6.3

44.8

54.5

70.2

98.5

105.9

85.580.682.874.2 69.2 74.9

73.6

64.9

83.6

118.3121.3

86.0

72.4

7.4

25.7

0

20

40

60

80

100

120

140

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

Recession Periods

*Forecasts from UofAProvided by Elliott D. Pollack and Co.

Properties in the Foreclosure Process Maricopa County 2002 – 2009 Source: The Information Market

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Jan-02

Mar-02

May-02

Jul-02

Sep-02

Nov-02

Jan-03

Mar-03

May-03

Jul-03

Sep-03

Nov-03

Jan-04

Mar-04

May-04

Jul-04

Sep-04

Nov-04

Jan-05

Mar-05

May-05

Jul-05

Sep-05

Nov-05

Jan-06

Mar-06

May-06

Jul-06

Sep-06

Nov-06

Jan-07

Mar-07

May-07

Jul-07

Sep-07

Nov-07

Jan-08

Mar-08

May-08

Jul-08

Sep-08

Nov-08

Jan-09

Mar-09

May-09

*Data through May 2009.Provided by Elliott D. Pollack and Co.

Arizona Delinquency RatesPercent Change Quarter Ago1998 – 2009* Source: Mortgage Bankers Association

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%20.0%22.0%24.0%26.0%

1998

Q1

1998

Q3

1999

Q1

1999

320

00 Q

120

00 Q

320

01 Q

120

01 Q

320

02 Q

120

02 Q

320

03 Q

120

03 Q

320

04 Q

120

04 Q

320

05 Q

120

05 Q

320

06 Q

120

06 Q

320

07 Q

120

07 Q

320

08 Q

120

08 Q

320

09 Q

1

Prime Subprime * Data through 1st quarter 2009

Recession Periods

Provided by Elliott D. Pollack and Co.

Single-Family Vacancy RateGreater Phoenix 1993–2009q2Source: PMHS

2.3%2.5% 2.4%

2.1%2.0% 2.1%

2.3%2.5%

2.3%

2.8% 2.8%1.9% 2.0%

2.9%

5.0%5.6%

9.8%

0%

2%

4%

6%

8%

10%

12%

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Provided by Elliott D. Pollack and Co.

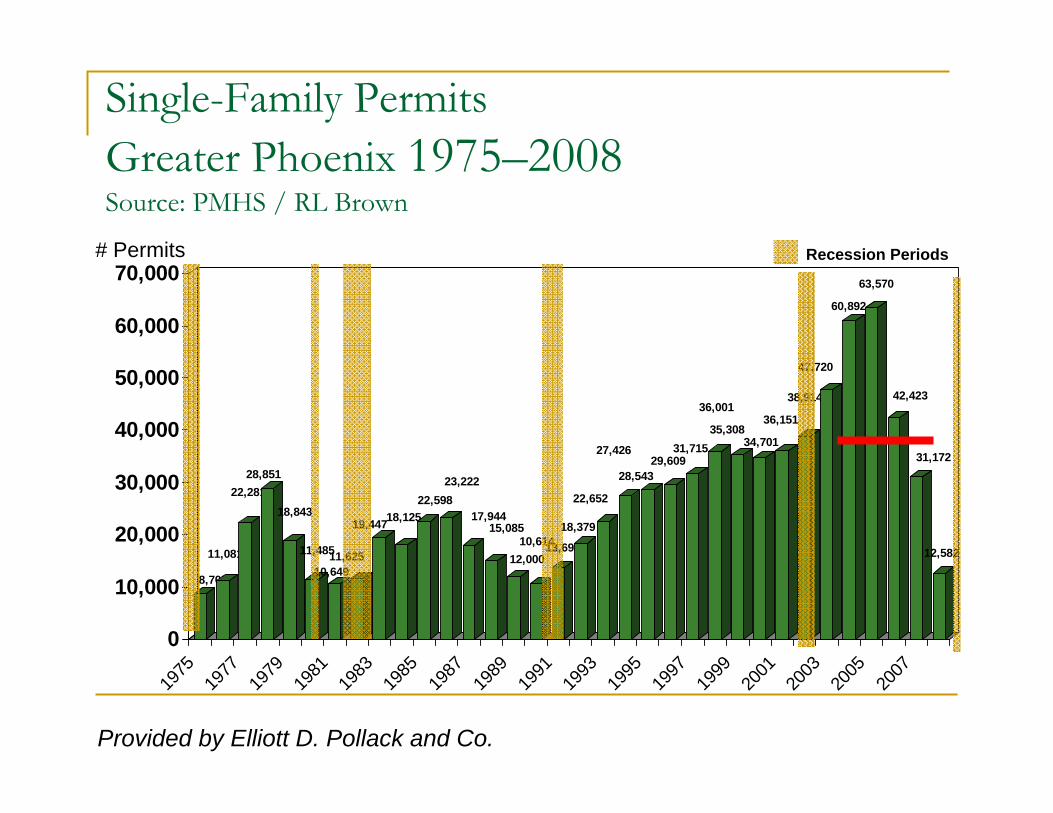

8,705

11,081

22,28128,851

18,843

11,485

10,64911,625

19,44718,12522,598

23,222

17,94415,085

12,00010,61413,698

18,379

22,652

27,426

28,54329,609

31,715

36,001

35,30834,701

36,151

38,914

47,720

60,892

63,570

42,423

31,172

12,582

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

# Permits Recession Periods

Provided by Elliott D. Pollack and Co.

Single-Family PermitsGreater Phoenix 1975–2008Source: PMHS / RL Brown

Oversupply of Housing

Greater Phoenix long-term demographics call for roughly 35,000-40,000 single family units per year (much less next two years)It appears that we overbuilt by as many as 75,000 units between 2003 and 2006 (exact figures depend on actual population flows) Even at the end of next year, given the expectation that foreclosures will continue to flood the market, excess supply could still be 40,000 to 50,000 units regardless of how we do the calculationBalance between supply and demand will not be fully achieved until about 2014, but building will still occur between now and then

Greater Phoenix S&P/Case-Schiller Home Price Index** Percent Change Year Ago1990 – 2009* Source: Macro Markets, LLC

-40%-35%-30%-25%-20%-15%-10%-5%0%5%

10%15%20%25%30%35%40%45%50%

Jan-90

Jul-9

0Jan

-91Ju

l-91

Jan-92

Jul-9

2Jan

-93Ju

l-93

Jan-94

Jul-9

4Jan

-95Ju

l-95

Jan-96

Jul-9

6Jan

-97Ju

l-97

Jan-98

Jul-9

8Jan

-99Ju

l-99

Jan-00

Jul-0

0Jan

-01Ju

l-01

Jan-02

Jul-0

2Jan

-03Ju

l-03

Jan-04

Jul-0

4Jan

-05Ju

l-05

Jan-06

Jul-0

6Jan

-07Ju

l-07

Jan-08

Jul-0

8Jan

-09

Recession Periods

*Data through June 2009**Measures changes in existing single family home prices given a constant level of quality.

Provided by Elliott D. Pollack and Co.

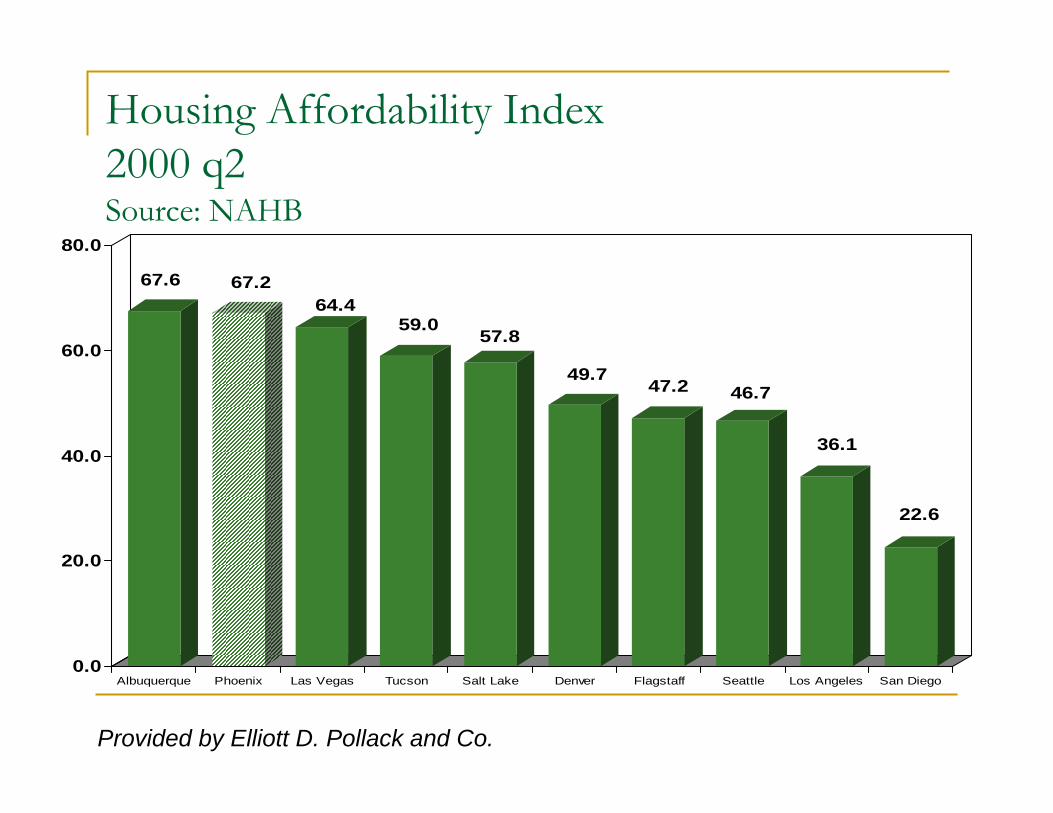

Housing Affordability Index2000 q2Source: NAHB

67.6 67.264.4

59.057.8

49.747.2 46.7

36.1

22.6

0.0

20.0

40.0

60.0

80.0

Albuquerque Phoenix Las Vegas Tucson Salt Lake Denver Flagstaff Seattle Los Angeles San Diego

Provided by Elliott D. Pollack and Co.

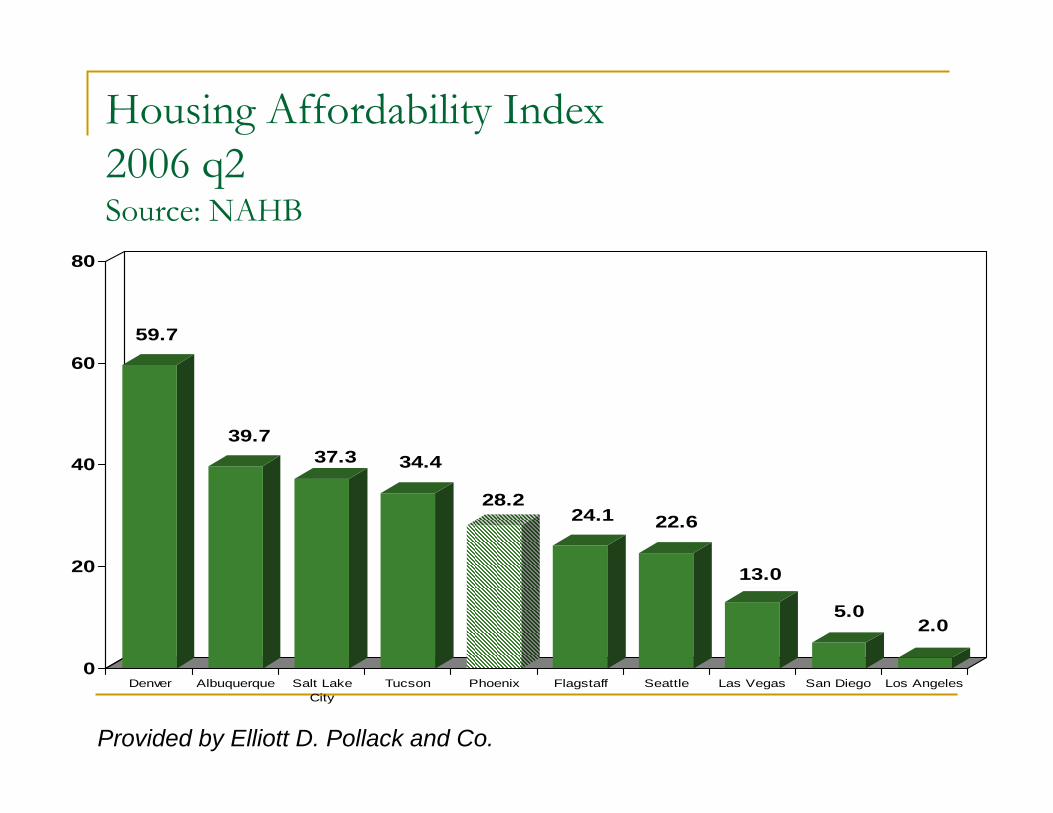

Housing Affordability Index2006 q2Source: NAHB

59.7

39.737.3 34.4

28.224.1 22.6

13.0

5.02.0

0

20

40

60

80

Denver Albuquerque Salt LakeCity

Tucson Phoenix Flagstaff Seattle Las Vegas San Diego Los Angeles

Provided by Elliott D. Pollack and Co.

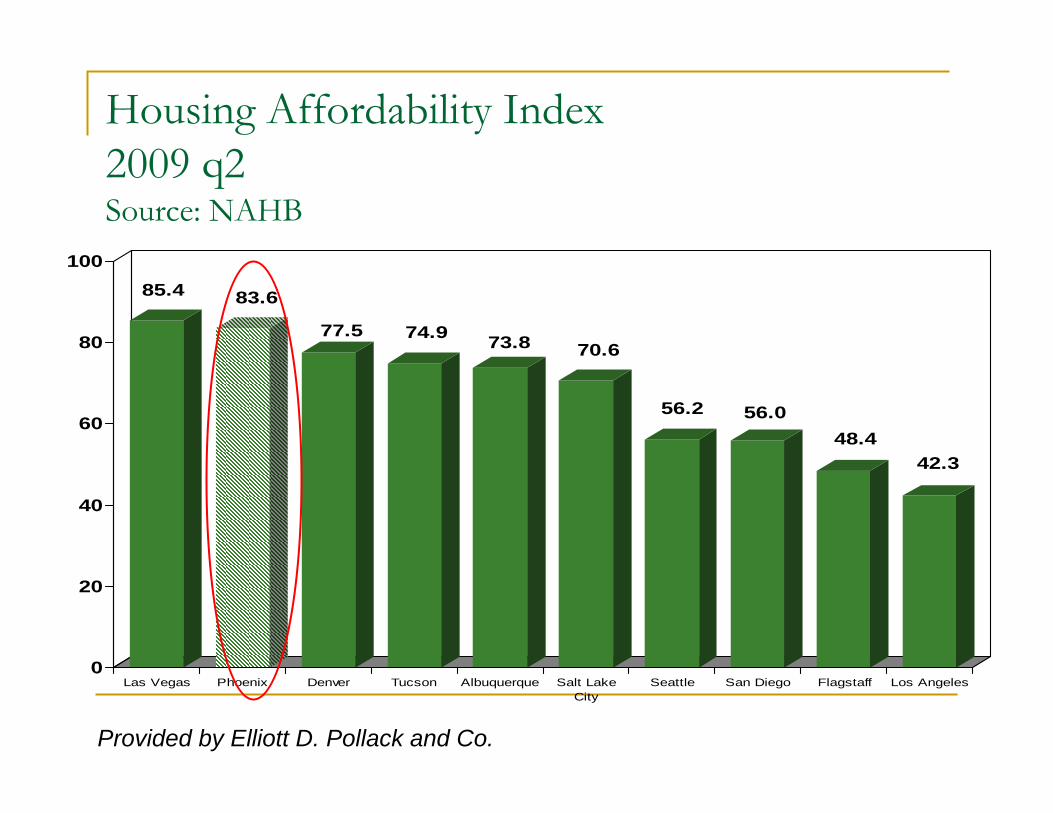

Housing Affordability Index2009 q2Source: NAHB

85.4 83.6

77.5 74.9 73.8 70.6

56.2 56.048.4

42.3

0

20

40

60

80

100

Las Vegas Phoenix Denver Tucson Albuquerque Salt LakeCity

Seattle San Diego Flagstaff Los Angeles

Provided by Elliott D. Pollack and Co.

Office Space Year-End Vacancy RatesMaricopa County 1986–2010*Source: CB Richard Ellis

26.7%

22.8%24.0%

26.7%26.4%

25.4%

22.7%

18.8%

14.8%

11.7%

9.5% 9.2%9.5%

10.0% 9.9%

16.0%

18.8%18.3%

16.4%

12.6%11.1%

13.9%

19.1%

25.3%

27.1%

0%

5%

10%

15%

20%

25%

30%

35%

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

*2009 -2010 are forecasts from CB Richard Ellis

Recession Periods

Provided by Elliott D. Pollack and Co.

No significant office building in Greater

Phoenix for next 5 years.

Provided by Elliott D. Pollack and Co.

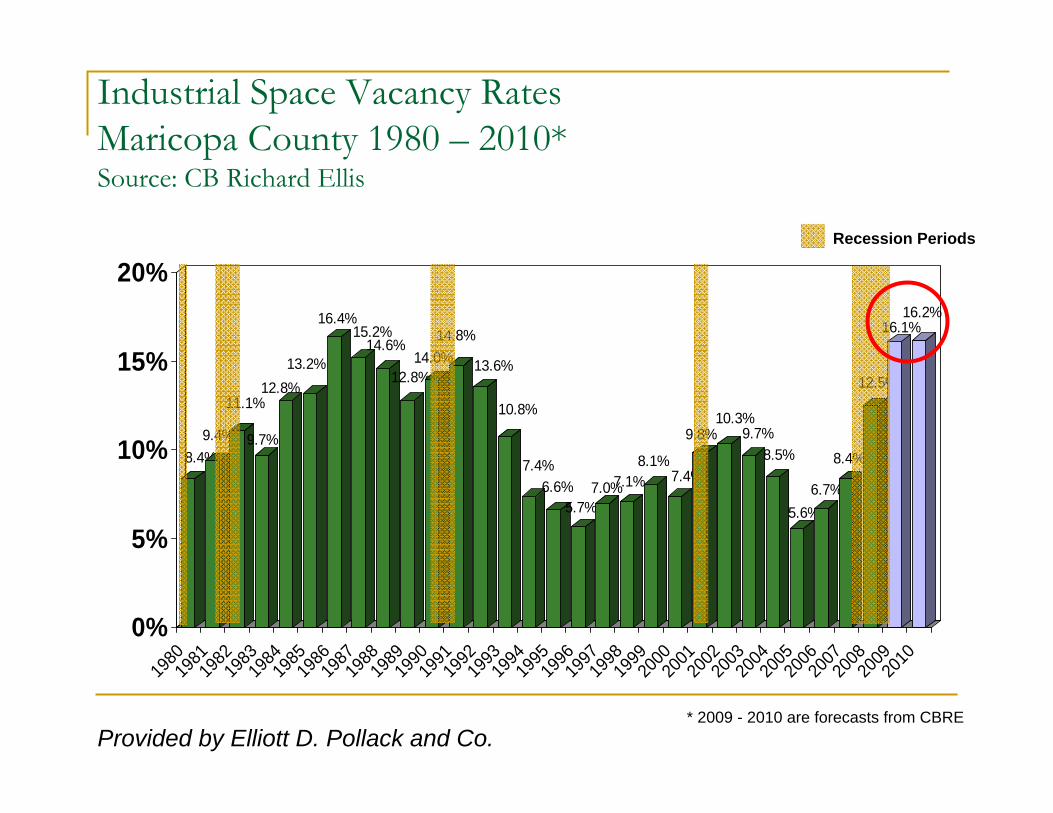

Industrial Space Vacancy RatesMaricopa County 1980 – 2010*Source: CB Richard Ellis

8.4%9.4%

11.1%

9.7%

12.8%13.2%

16.4%15.2%

14.6%

12.8%14.0%

14.8%

13.6%

10.8%

7.4%6.6%

5.7%7.0%7.1%

8.1%7.4%

9.8%10.3%

9.7%8.5%

5.6%6.7%

8.4%

12.5%

16.1%16.2%

0%

5%

10%

15%

20%

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

* 2009 - 2010 are forecasts from CBRE

Recession Periods

Provided by Elliott D. Pollack and Co.

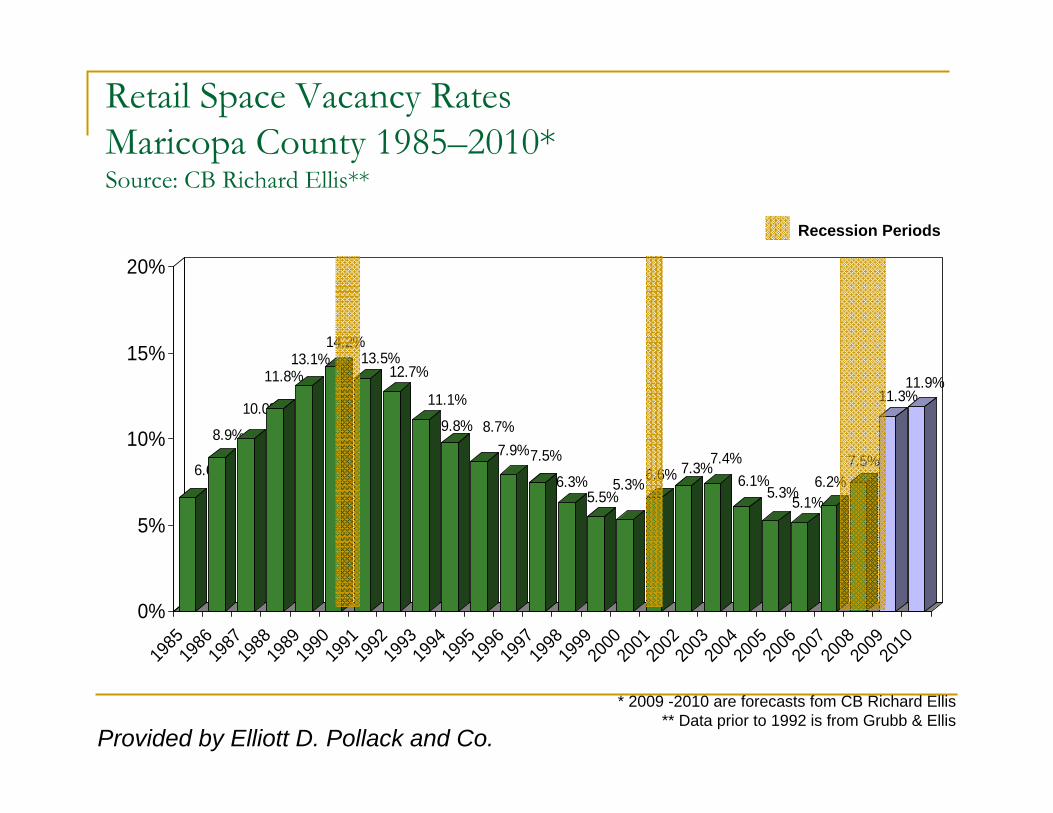

Retail Space Vacancy RatesMaricopa County 1985–2010*Source: CB Richard Ellis**

6.6%

8.9%

10.0%

11.8%13.1%

14.2%13.5%

12.7%

11.1%

9.8% 8.7%7.9%7.5%

6.3%5.5%

5.3%6.6% 7.3%7.4%6.1%

5.3%5.1%6.2%

7.5%

11.3%11.9%

0%

5%

10%

15%

20%

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

* 2009 -2010 are forecasts fom CB Richard Ellis** Data prior to 1992 is from Grubb & Ellis

Recession Periods

Provided by Elliott D. Pollack and Co.

It could take a decade before prices get back to peak levels in the commercial

markets.

Provided by Elliott D. Pollack and Co.

AZ Summary:

You are here.

Mixed News Good News

Provided by Elliott D. Pollack and Co.

Employment should be picking up by middle of next year.

Retail sales could have significant rebound because down so far . However, it is not sustainable in terms of percentage gains.

Population will lag growth in employment.

Underlying dynamics still good but changes in policy needed at State level.

Greater Phoenix Summary

Provided by Elliott D. Pollack and Co.

Greater Phoenix Forecast 2009 – 2010

Source: Elliott D. Pollack & Company, AZ Blue Chip, Department of Commerce, Research Administration

5.0%-9.0%-10.0%0.1%Retail Sales

2.5%-1.0%3.0%4.5%Personal Income

-1.0%-6.0%-2.0%1.3%Employment

1.8%1.6%2.4%3.5%Population

2010200920082007Indicator

? ? ?

Provided by Elliott D. Pollack and Co.

Maricopa County Budget

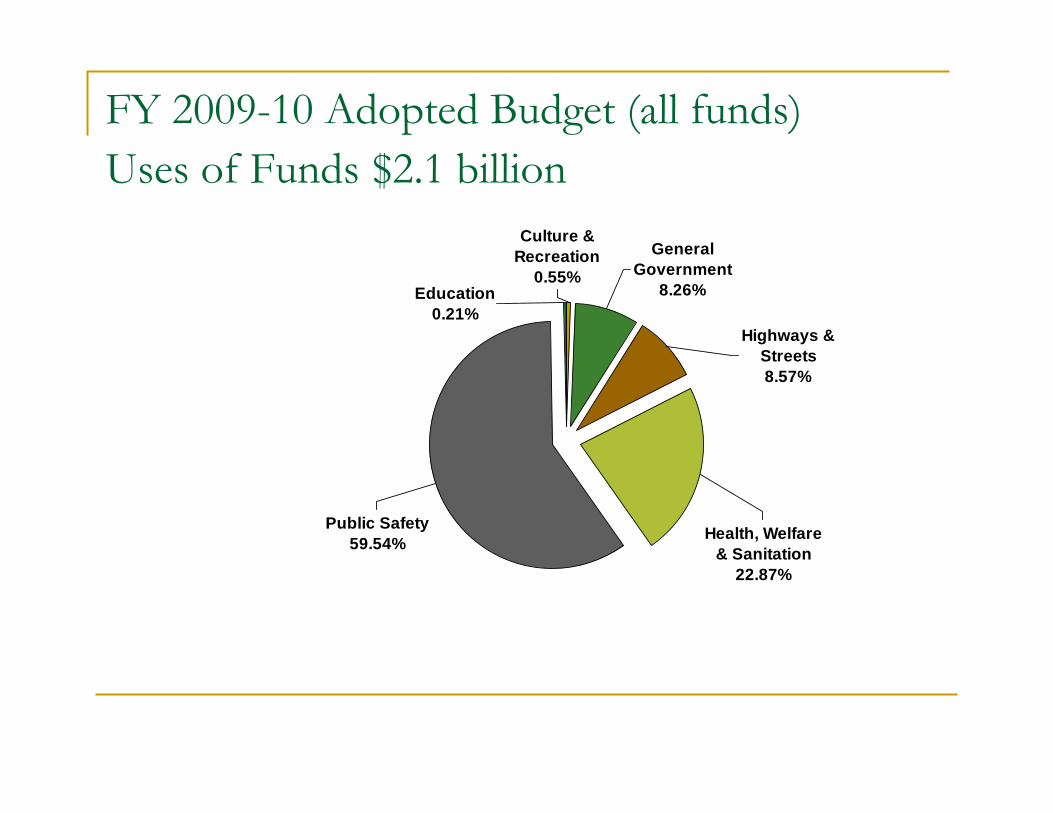

FY 2009-10 Adopted Budget (all funds)Uses of Funds $2.1 billion

Highways & Streets8.57%

Health, Welfare & Sanitation

22.87%

Public Safety59.54%

Education0.21%

General Government

8.26%

Culture & Recreation

0.55%

General Fund Operating Revenue$1.09 billion

State-Shared Sales Tax, $368.40 M,

34%

Vehicle License Tax, $118.40 M,

11%

Property Tax, $487.40

M , 44%

Other Revenues,

$115.20 M , 11%

2009-10 Net Variance overFY 2008-09 Adopted Budget

(millions)FY 2008-09 FY 2009-10

Adopted Recomm. Reduction %

Total County 2,259$ 2,136$ 122$ 5.4%

Total County Operating 1,772$ 1,712$ 60$ 3.4%

Total General Fund 1,443$ 1,273$ 170$ 11.8%

General Fund Operating 1,167$ 1,089$ 77$ 6.6%

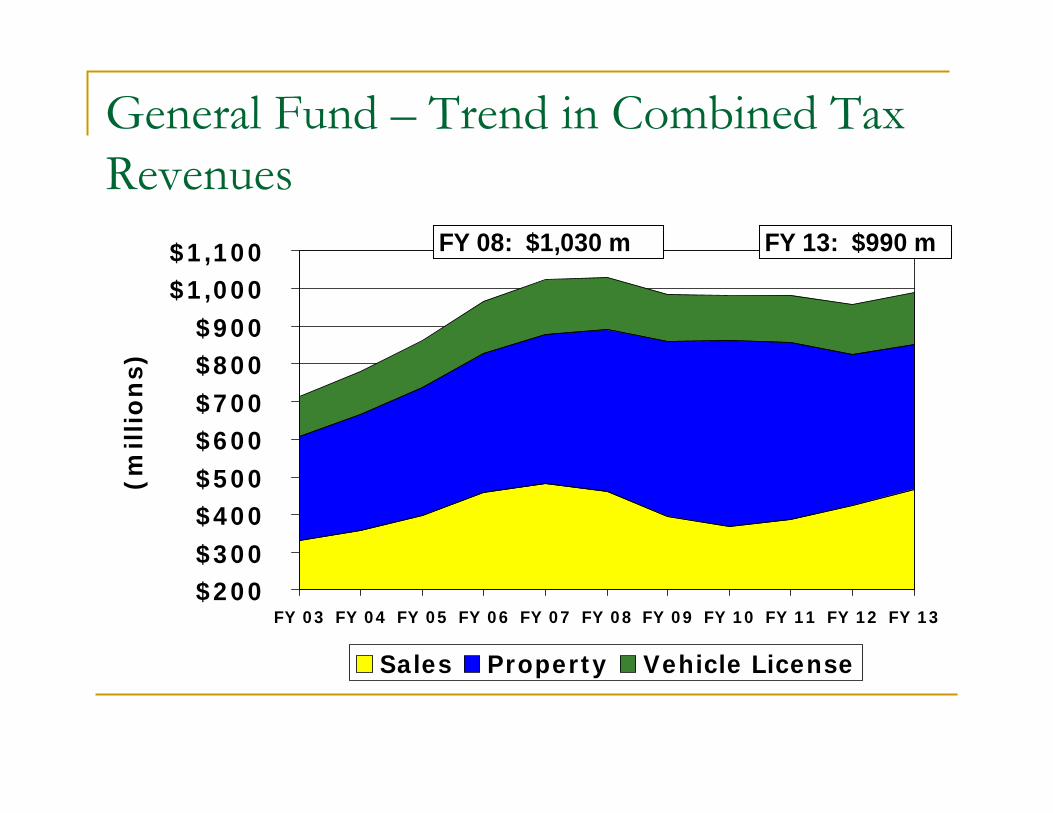

General Fund – Trend in Combined Tax Revenues

$200$300$400$500$600$700$800$900

$1,000$1,100

FY 03 FY 04 FY 05 FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13

(mil

lio

ns)

Sales Property Vehicle License

FY 08: $1,030 m FY 13: $990 m

Sales Tax Trend

$357.5$368.4

$468.1

$425.5

$386.9$394.9

$461.0

$480.4

$457.8

$397.7

$300$320$340$360$380$400$420$440$460$480$500

FY 04 FY 05 FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13

(mil

lio

ns)

Forecasts – Elliott D. Pollack pessimistic scenario, July 2009

Vehicle License Tax Trend

$104

$126

$138$143

$149

$132

$127

$120

$139

$144

$138

$123

$116

$80

$90

$100

$110

$120

$130

$140

$150

$160

FY 03 FY 04 FY 05 FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13 FY 14 FY 15

(mil

lio

ns)

Forecasts – Elliott D. Pollack pessimistic scenario, July 2009

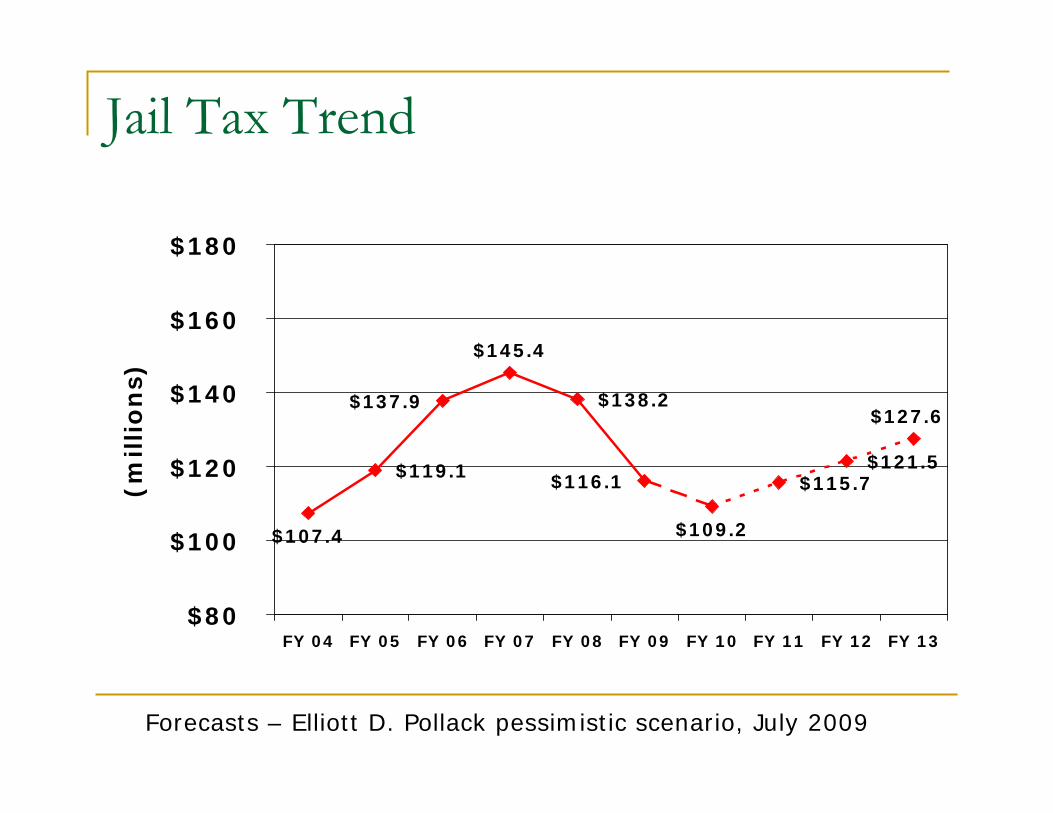

Jail Tax Trend

$107.4 $109.2

$119.1

$137.9

$145.4

$138.2

$116.1 $115.7$121.5

$127.6

$80

$100

$120

$140

$160

$180

FY 04 FY 05 FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13

(millio

ns)

Forecasts – Elliott D. Pollack pessimistic scenario, July 2009

State Shared Highway User Revenues

$86.6

$80.1

$90.6

$97.0

$107.6

$102.8

$87.8 $93.4$96.2

$99.1

$60

$70

$80

$90

$100

$110

$120

FY 04 FY 05 FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13

(millions)

Forecasts – Elliott D. Pollack pessimistic scenario, July 2009

Total Net Assessed Value

Primary

Secondary

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

(billio

ns)

Forecasts – Elliott D. Pollack pessimistic scenario, July 2009

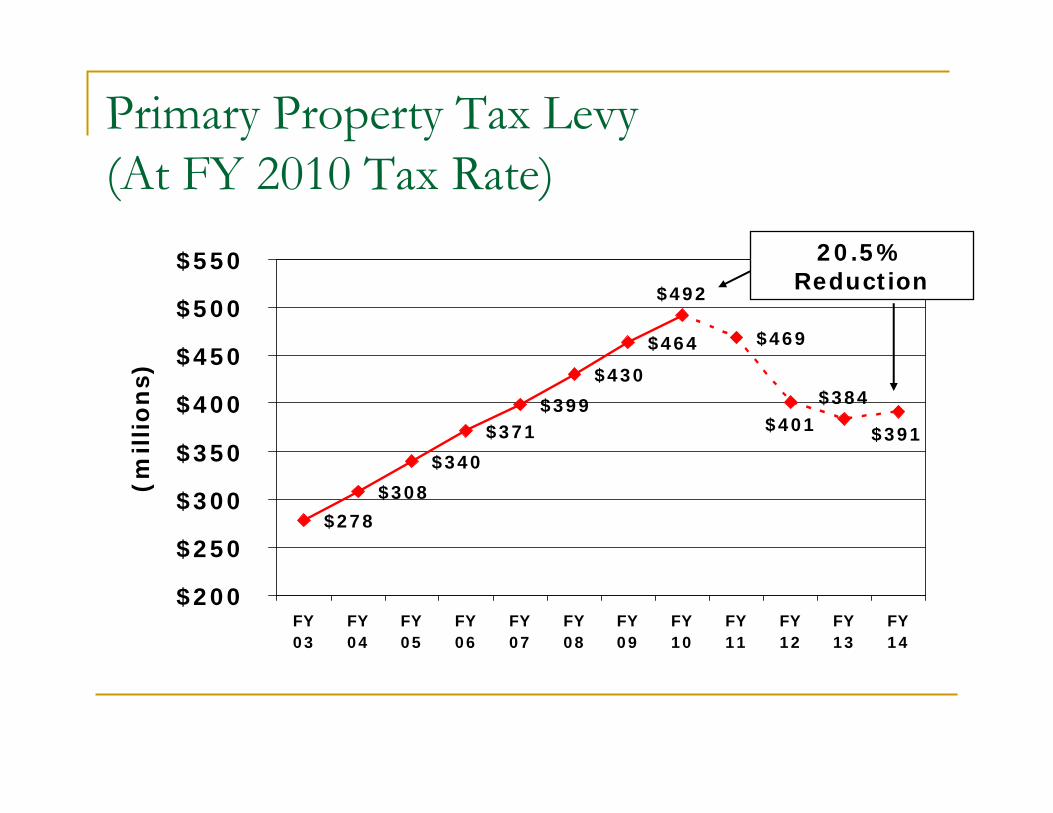

Primary Property Tax Levy(At FY 2010 Tax Rate)

$278

$464

$384

$391$401

$469

$492

$430

$399$371

$340

$308

$200

$250

$300

$350

$400

$450

$500

$550

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

(millio

ns)

20.5% Reduction

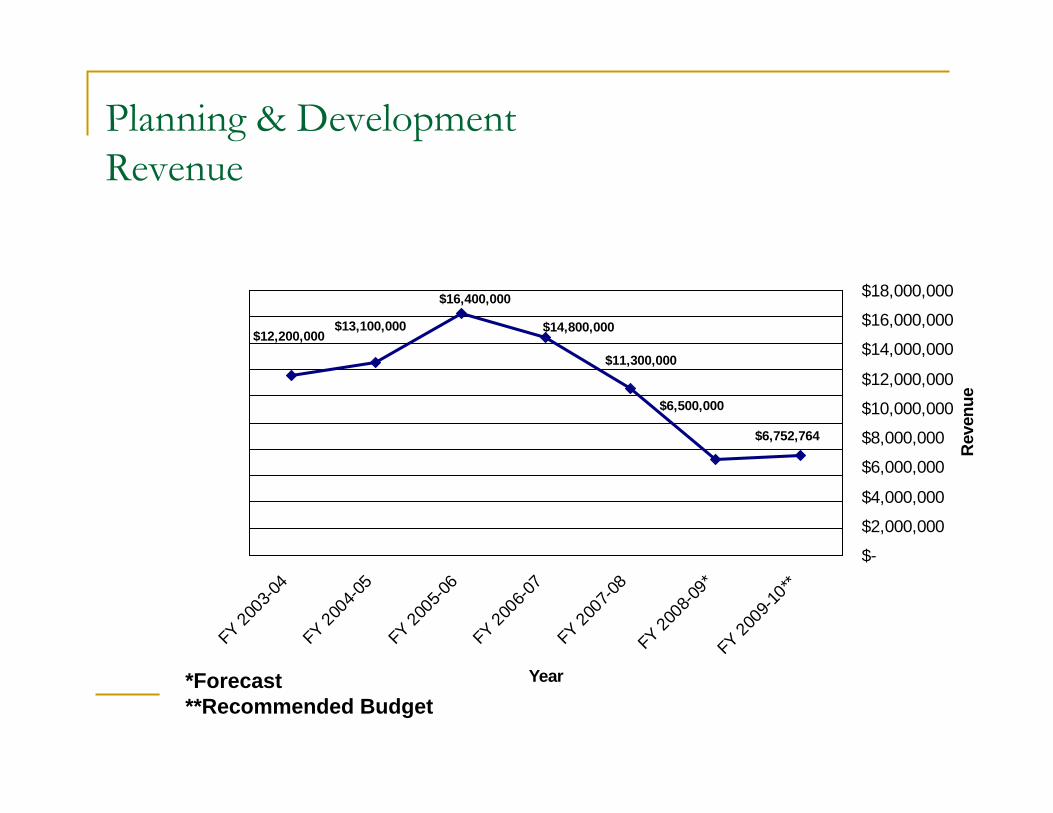

Planning & DevelopmentRevenue

$6,752,764

$6,500,000

$11,300,000

$14,800,000

$16,400,000

$13,100,000$12,200,000

$-$0$0$0$0$1$1$1$1$1$1

FY 20

03-04

FY 2004-0

5

FY 20

05-06

FY 20

06-07

FY 200

7-08

FY 20

08-09

*FY

2009

-10**

Year

$-

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

$16,000,000

$18,000,000

Rev

enue

*Forecast**Recommended Budget

State ImpactsCounty Contribution – budgeted at $24.1 m, but was included in budget reconciliation bill vetoed by the Governor; expected to come backHURF Diversion to DPS – estimated impact nearly $6 million per yearOutcome of FMAP savings not entirely clear

$45 million reduction in FY 10 County contribution to long term care (not enacted until after County budget adoption)Refunds expected for FY 09 long term care and FY 09 and FY 10 acute care, but no notification of specific amountsCounty has to treat any FMAP savings as a one-time source

Maricopa County ALTCS Contribution Growth, FY 2002-2010 (excludes FMAP)

$165

$162

$153$145

$130

$126

$102

$115

$110

$90

$110

$130

$150

$170

FY 02 FY 03 FY 04 FY 05 FY 06 FY 07 FY 08 FY 09 FY10

Mill

ions

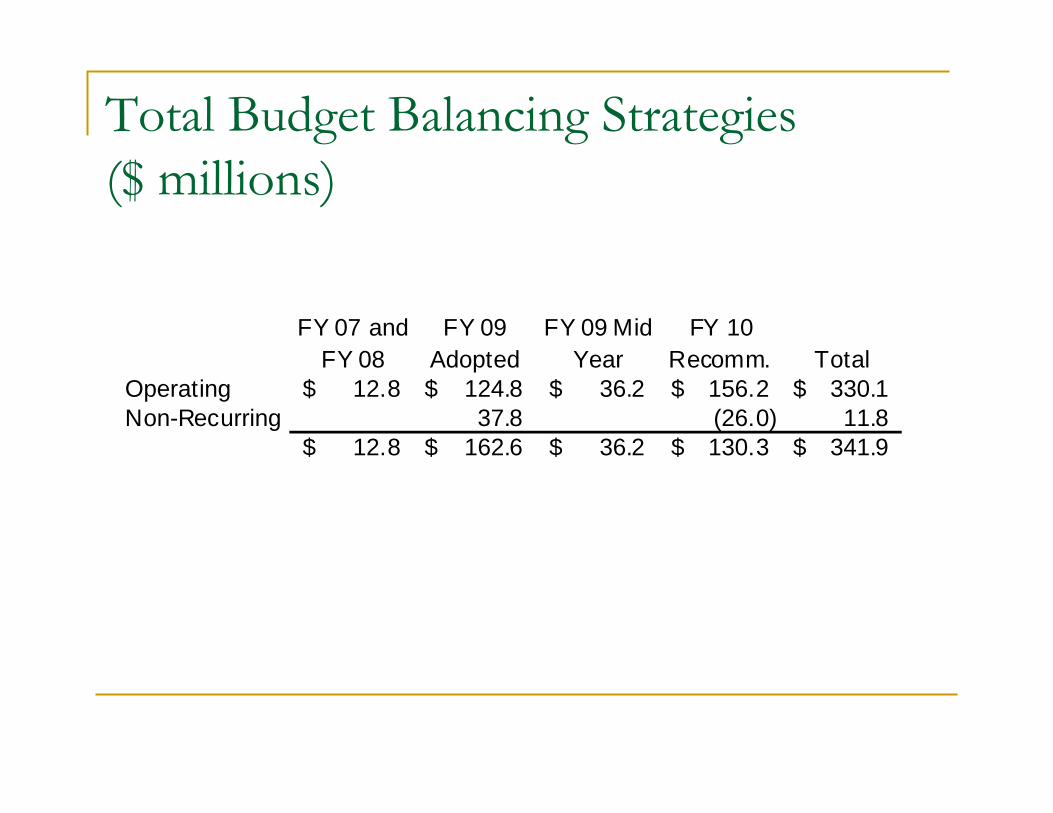

Total Budget Balancing Strategies ($ millions)

FY 07 and FY 08

FY 09 Adopted

FY 09 Mid Year

FY 10 Recomm. Total

Operating 12.8$ 124.8$ 36.2$ 156.2$ 330.1$ Non-Recurring 37.8 (26.0) 11.8

12.8$ 162.6$ 36.2$ 130.3$ 341.9$

Structurally Balanced Budget

Definition: Ongoing revenues meet or exceed ongoing

expenditures

History of Budget BalancingFY 2006-07

Lowered revenue projections and cut spending mid-year

FY 2007-08 Budget PreparationRevenue budgets for State-shared Sales, Jail Excise and Vehicle License Taxes prepared with little or no revenue growthBudget reductions in personnel budgets, court security, overtime, supplies, services

History of Budget Balancing

FY 2007-08 Mid-YearReduced all administrative budgets by 5%Froze hiring and capital expendituresFroze contingency fundsReduced overtime

FY 2008-09 Budget PreparationReduced operating budgets by an average of 5.6%

History of Budget Balancing

FY 2008-09 Mid-YearContinued hiring and capital freezesContinued contingency freezeUsed contingency funds and funds reserved for salary increases to offset $58.4 deficit

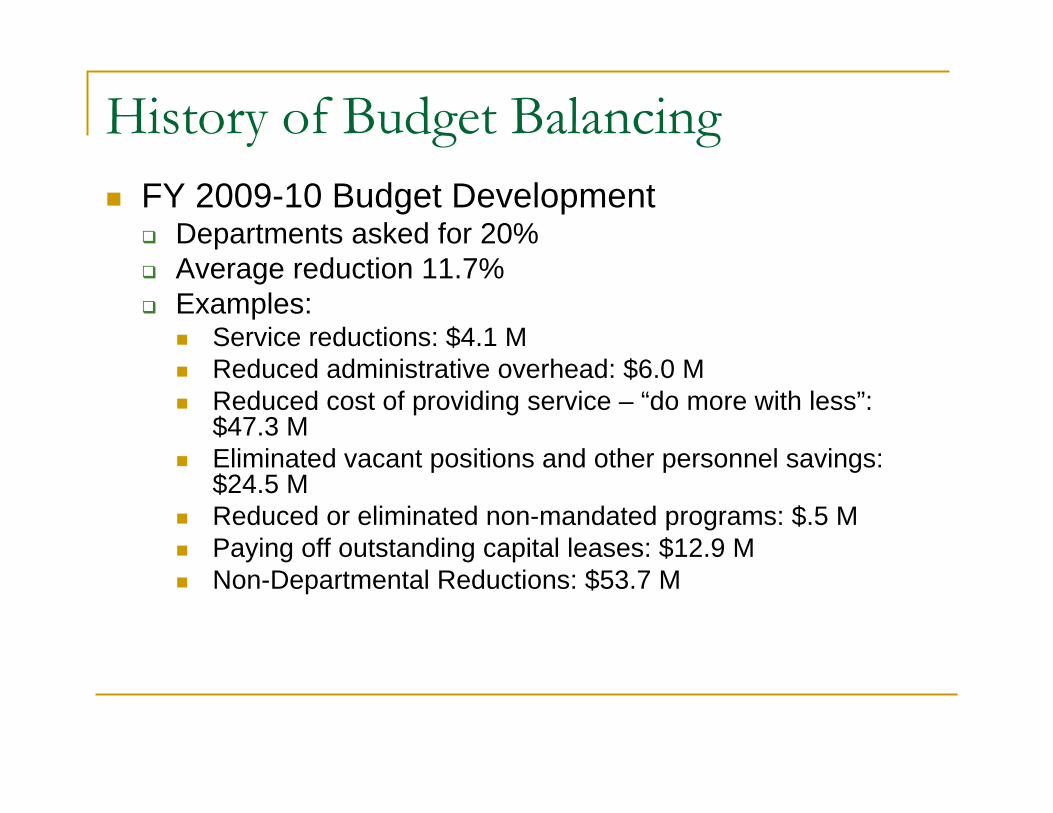

History of Budget BalancingFY 2009-10 Budget Development

Departments asked for 20%Average reduction 11.7%Examples:

Service reductions: $4.1 MReduced administrative overhead: $6.0 MReduced cost of providing service – “do more with less”: $47.3 MEliminated vacant positions and other personnel savings: $24.5 MReduced or eliminated non-mandated programs: $.5 MPaying off outstanding capital leases: $12.9 MNon-Departmental Reductions: $53.7 M

General Fund Expenditure Departmental Reductions (by category)

Public Safety, $ (38.52), 61%

Culture & Recreation, $ (0.73), 1% Education, $ (0.28), 0%

General Government, $ (21.27), 33%

Health, Welfare, & Sanitation, $ (3.36), 5%

FY 2009-10 General Fund Expenditure Departmental Reductions (by type)

Fund Shifts, $(2.75), 4%

Non-Mandated, $(0.27), 0%

Vacancies, $(18.63), 25%

Service Reductions, $(2.36), 3%

Other, $4.53 , 6% Administrative, $(5.41), 7%

Capital Lease, $(5.22), 7%

Efficiencies, $(34.12), 48%

Amounts shown in millions

General Fund Departmental Two YearBudget Reduction Summary

Average Reduction: 13.2%$74.6 million in departmental reductions

Average Appointed Reduction: 13.7%Average Elected Reduction: 13.7%Average Judicial Reduction: 12.1%

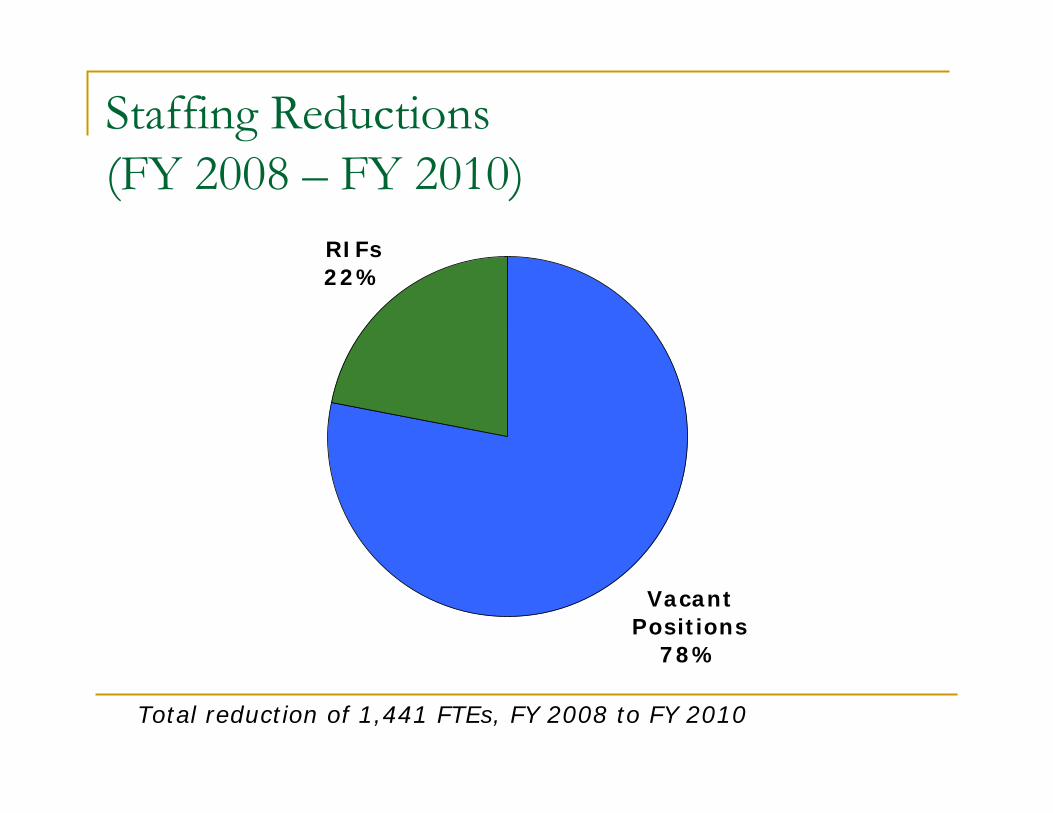

Reductions in Staffing

Total Full Time Equivalent Positions Eliminated

FY 08 FY 09 FY 09 FY 10 Total(Mid-Year) Adopted (Mid-Year) To Date (to date)

Filled (43.0) (11.0) (54.0) (209.7) (317.7) Vacant (34.0) (164.2) (91.1) (834.0) (1,123.3) Total (77.0) (175.2) (145.1) (1,043.7) (1,441.0)

Terminations and H ires (FY 08 and FY 09 to date):

Terminations: 3,427 Hires: 1,004 Net Vacancies: 2,423

Does not reflect positions added through ARRA funding.

Staffing Reductions (FY 2008 – FY 2010)

Vacant Positions

78%

RIFs22%

Total reduction of 1,441 FTEs, FY 2008 to FY 2010

Trend in General Fund Operating Revenues and Budgeted Expenditures

$1.09$1.09

$1.15$1.16

$1.09

$1.17$1.18

$1.20

$1.00

$1.05

$1.10

$1.15

$1.20

$1.25

FY 2007 FY 2008 FY 2009 FY 2010*

(billio

ns)

Actual Operating RevenuesBudgeted Operating Expenditures

*FY 2010 Budget

Structural imbalance adjusted

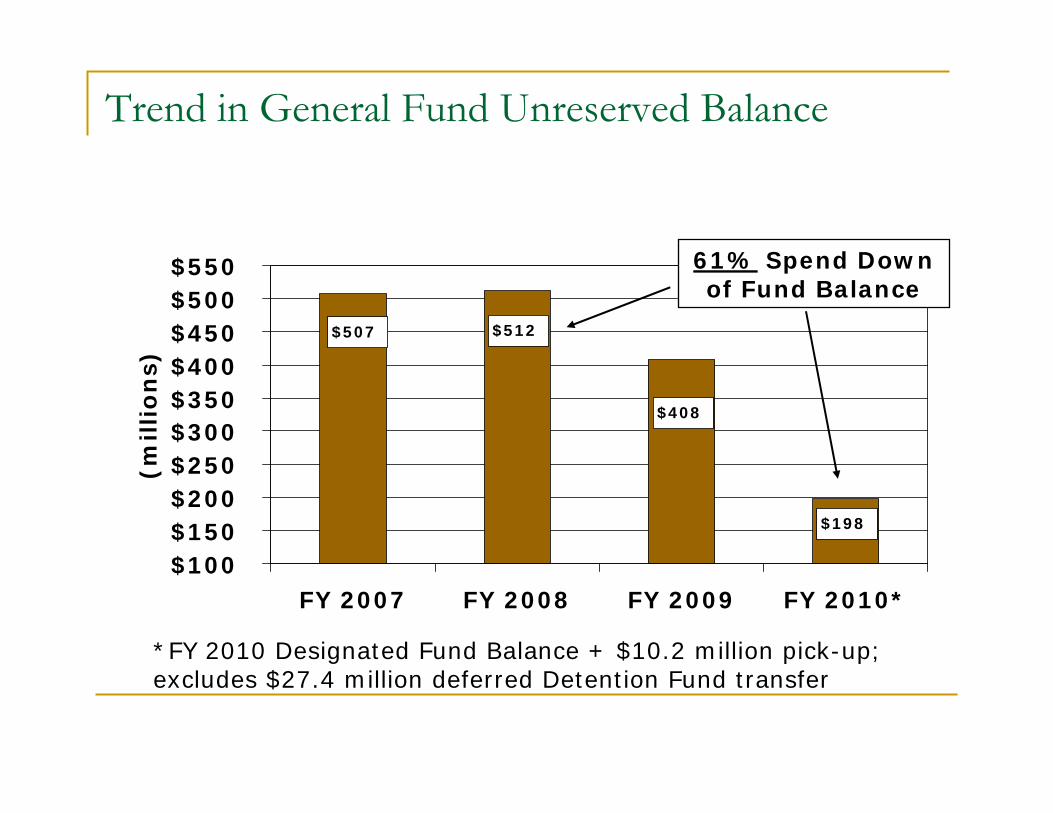

Trend in General Fund Unreserved Balance

$198

$408

$512$507

$100$150$200$250$300$350$400$450$500$550

FY 2007 FY 2008 FY 2009 FY 2010*

(millio

ns)

*FY 2010 Designated Fund Balance + $10.2 million pick-up; excludes $27.4 million deferred Detention Fund transfer

61% Spend Down of Fund Balance

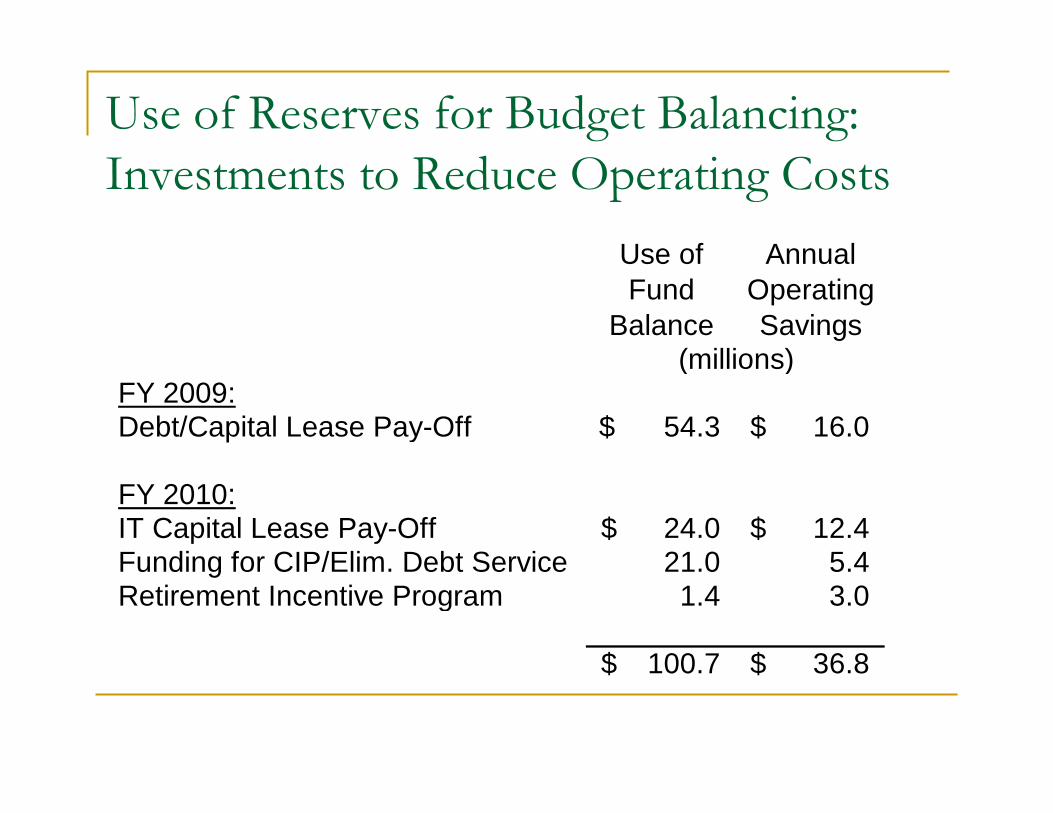

Use of Reserves for Budget Balancing:Investments to Reduce Operating Costs

Use of Fund

Balance

Annual Operating Savings

(millions)FY 2009:Debt/Capital Lease Pay-Off 54.3$ 16.0$

FY 2010:IT Capital Lease Pay-Off 24.0$ 12.4$ Funding for CIP/Elim. Debt Service 21.0 5.4 Retirement Incentive Program 1.4 3.0

100.7$ 36.8$

Moving Forward

Stabilize – continue to use fund balance responsiblySlim down services if revenue declines continueForecast continuously – adjust course as necessary to maintain structural balance

Impact of the ARRA on Budget Process

Globally, Maricopa County did not approach potential ARRA as a budget-balancing strategyOur budget was not balanced on ARRA funding, so we do not need an “exit strategy”County budget reductions focused more on efficiencies rather than service reductions or eliminationsARRA funding is allowing the County to expand services to our residents (particularly in areas where demand is heightened by the recession) and project investments

![Fiscal Issues of Statewide Significance - Washingtonleap.leg.wa.gov/leap/budget/lbns/1993-95partii.pdf · 2008. 3. 17. · Fiscal Issues of Statewide Significance ]HEALTH CARE REFORM](https://img.pdfslide.us/doc/110x75/60d0815c91e68516265617f0/fiscal-issues-of-statewide-significance-2008-3-17-fiscal-issues-of-statewide.jpg)