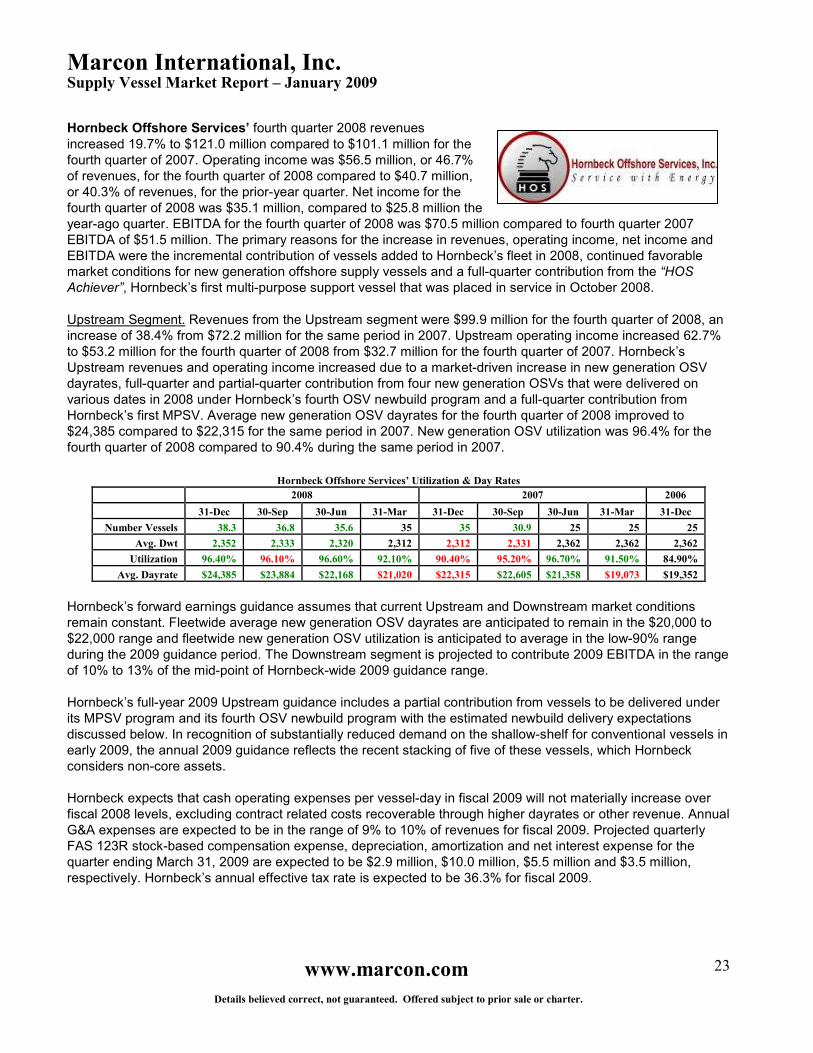

Embed Size (px)

Citation preview

Marcon International, Inc. Vessels and Barges for Sale or Charter Worldwide

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

P.O. Box 1170 9 NW Front Street, Suite 201 Coupeville, WA 98239 U.S.A. Telephone (360) 678 8880 Fax (360) 678-8890 E Mail: [email protected] http://www.marcon.com

January 2009

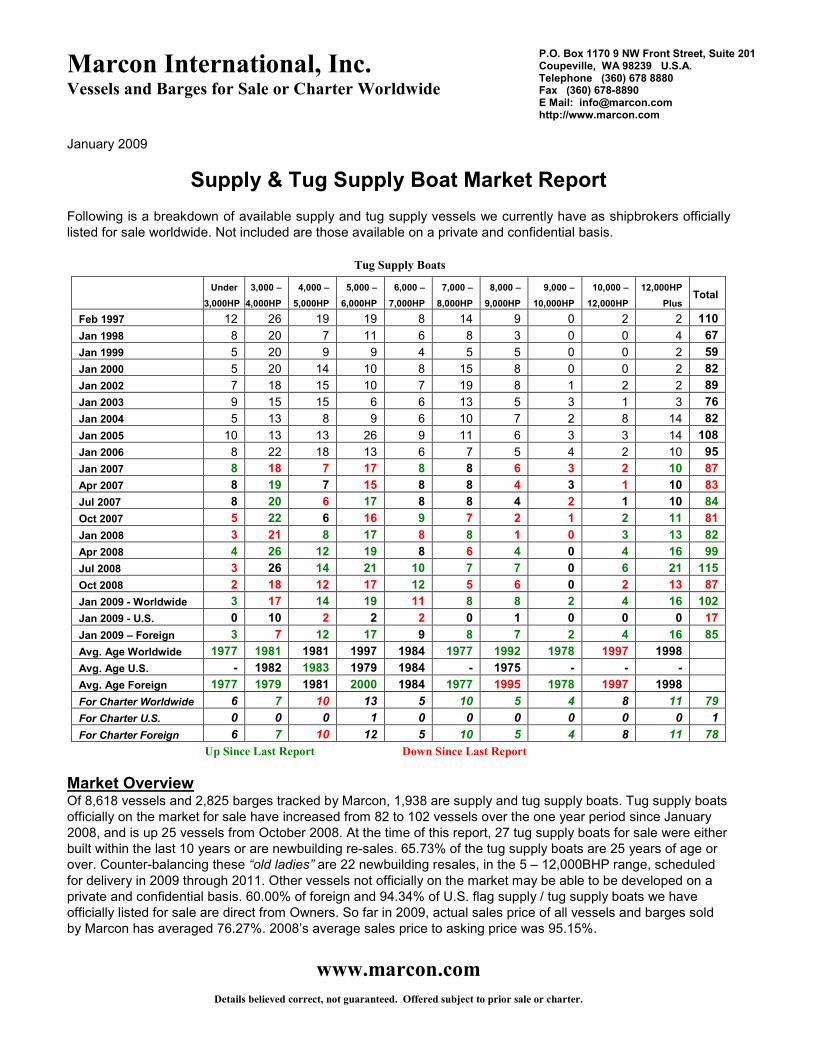

Supply & Tug Supply Boat Market Report Following is a breakdown of available supply and tug supply vessels we currently have as shipbrokers officially listed for sale worldwide. Not included are those available on a private and confidential basis.

Tug Supply Boats

Up Since Last Report Down Since Last Report

Market Overview Of 8,618 vessels and 2,825 barges tracked by Marcon, 1,938 are supply and tug supply boats. Tug supply boats officially on the market for sale have increased from 82 to 102 vessels over the one year period since January 2008, and is up 25 vessels from October 2008. At the time of this report, 27 tug supply boats for sale were either built within the last 10 years or are newbuilding re-sales. 65.73% of the tug supply boats are 25 years of age or over. Counter-balancing these “old ladies” are 22 newbuilding resales, in the 5 – 12,000BHP range, scheduled for delivery in 2009 through 2011. Other vessels not officially on the market may be able to be developed on a private and confidential basis. 60.00% of foreign and 94.34% of U.S. flag supply / tug supply boats we have officially listed for sale are direct from Owners. So far in 2009, actual sales price of all vessels and barges sold by Marcon has averaged 76.27%. 2008’s average sales price to asking price was 95.15%.

Under

3,000HP

3,000 –

4,000HP

4,000 –

5,000HP

5,000 –

6,000HP

6,000 –

7,000HP

7,000 –

8,000HP

8,000 –

9,000HP

9,000 –

10,000HP

10,000 –

12,000HP

12,000HP

Plus Total

Feb 1997 12 26 19 19 8 14 9 0 2 2 110

Jan 1998 8 20 7 11 6 8 3 0 0 4 67

Jan 1999 5 20 9 9 4 5 5 0 0 2 59

Jan 2000 5 20 14 10 8 15 8 0 0 2 82

Jan 2002 7 18 15 10 7 19 8 1 2 2 89

Jan 2003 9 15 15 6 6 13 5 3 1 3 76

Jan 2004 5 13 8 9 6 10 7 2 8 14 82

Jan 2005 10 13 13 26 9 11 6 3 3 14 108

Jan 2006 8 22 18 13 6 7 5 4 2 10 95

Jan 2007 8 18 7 17 8 8 6 3 2 10 87

Apr 2007 8 19 7 15 8 8 4 3 1 10 83

Jul 2007 8 20 6 17 8 8 4 2 1 10 84

Oct 2007 5 22 6 16 9 7 2 1 2 11 81

Jan 2008 3 21 8 17 8 8 1 0 3 13 82

Apr 2008 4 26 12 19 8 6 4 0 4 16 99

Jul 2008 3 26 14 21 10 7 7 0 6 21 115

Oct 2008 2 18 12 17 12 5 6 0 2 13 87

Jan 2009 - Worldwide 3 17 14 19 11 8 8 2 4 16 102

Jan 2009 - U.S. 0 10 2 2 2 0 1 0 0 0 17

Jan 2009 – Foreign 3 7 12 17 9 8 7 2 4 16 85

Avg. Age Worldwide 1977 1981 1981 1997 1984 1977 1992 1978 1997 1998

Avg. Age U.S. - 1982 1983 1979 1984 - 1975 - - -

Avg. Age Foreign 1977 1979 1981 2000 1984 1977 1995 1978 1997 1998

For Charter Worldwide 6 7 10 13 5 10 5 4 8 11 79

For Charter U.S. 0 0 0 1 0 0 0 0 0 0 1

For Charter Foreign 6 7 10 12 5 10 5 4 8 11 78

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

2

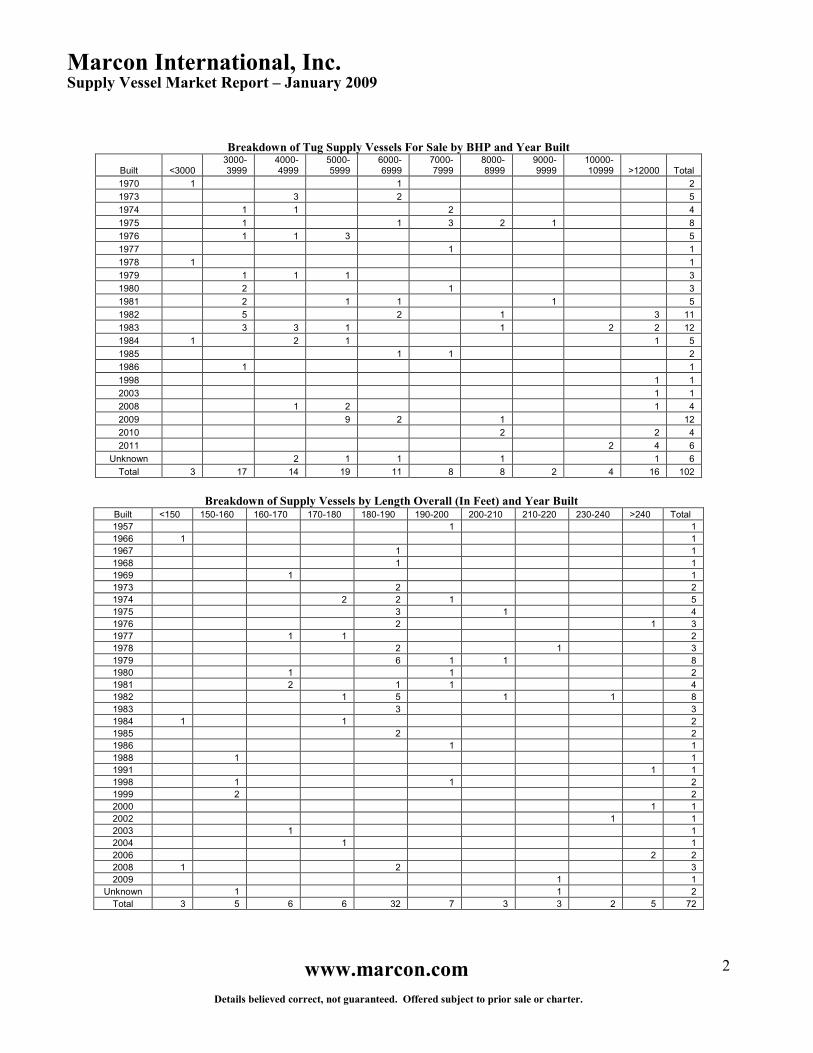

Breakdown of Tug Supply Vessels For Sale by BHP and Year Built

Built <3000 3000-3999

4000-4999

5000-5999

6000-6999

7000-7999

8000-8999

9000-9999

10000-10999 >12000 Total

1970 1 1 2

1973 3 2 5

1974 1 1 2 4

1975 1 1 3 2 1 8

1976 1 1 3 5

1977 1 1

1978 1 1

1979 1 1 1 3

1980 2 1 3

1981 2 1 1 1 5

1982 5 2 1 3 11

1983 3 3 1 1 2 2 12

1984 1 2 1 1 5

1985 1 1 2

1986 1 1

1998 1 1

2003 1 1

2008 1 2 1 4

2009 9 2 1 12

2010 2 2 4

2011 2 4 6

Unknown 2 1 1 1 1 6

Total 3 17 14 19 11 8 8 2 4 16 102

Breakdown of Supply Vessels by Length Overall (In Feet) and Year Built

Built <150 150-160 160-170 170-180 180-190 190-200 200-210 210-220 230-240 >240 Total

1957 1 1

1966 1 1

1967 1 1

1968 1 1

1969 1 1

1973 2 2

1974 2 2 1 5

1975 3 1 4

1976 2 1 3

1977 1 1 2

1978 2 1 3

1979 6 1 1 8

1980 1 1 2

1981 2 1 1 4

1982 1 5 1 1 8

1983 3 3

1984 1 1 2

1985 2 2

1986 1 1

1988 1 1

1991 1 1

1998 1 1 2

1999 2 2

2000 1 1

2002 1 1

2003 1 1

2004 1 1

2006 2 2

2008 1 2 3

2009 1 1

Unknown 1 1 2

Total 3 5 6 6 32 7 3 3 2 5 72

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

3

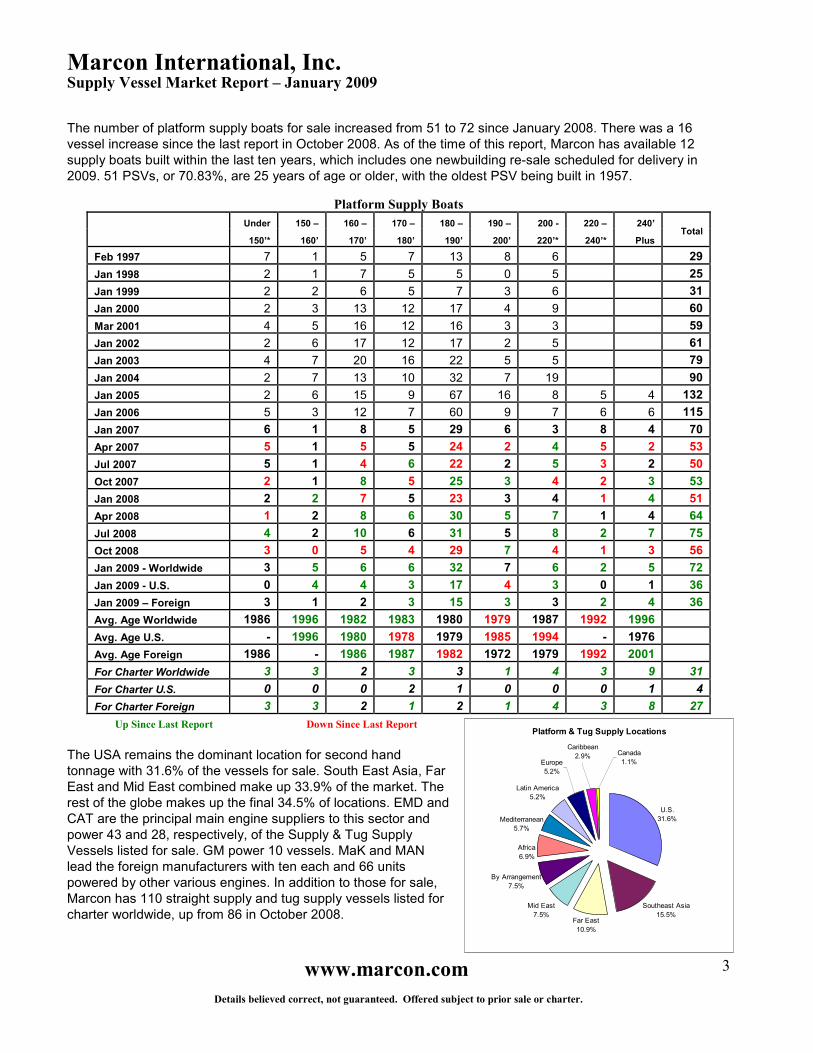

The number of platform supply boats for sale increased from 51 to 72 since January 2008. There was a 16 vessel increase since the last report in October 2008. As of the time of this report, Marcon has available 12 supply boats built within the last ten years, which includes one newbuilding re-sale scheduled for delivery in 2009. 51 PSVs, or 70.83%, are 25 years of age or older, with the oldest PSV being built in 1957.

Platform Supply Boats

Under 150 – 160 – 170 – 180 – 190 – 200 - 220 – 240’

150’* 160’ 170’ 180’ 190’ 200’ 220’* 240’* Plus Total

Feb 1997 7 1 5 7 13 8 6 29

Jan 1998 2 1 7 5 5 0 5 25

Jan 1999 2 2 6 5 7 3 6 31

Jan 2000 2 3 13 12 17 4 9 60

Mar 2001 4 5 16 12 16 3 3 59

Jan 2002 2 6 17 12 17 2 5 61

Jan 2003 4 7 20 16 22 5 5 79

Jan 2004 2 7 13 10 32 7 19 90

Jan 2005 2 6 15 9 67 16 8 5 4 132

Jan 2006 5 3 12 7 60 9 7 6 6 115

Jan 2007 6 1 8 5 29 6 3 8 4 70

Apr 2007 5 1 5 5 24 2 4 5 2 53

Jul 2007 5 1 4 6 22 2 5 3 2 50

Oct 2007 2 1 8 5 25 3 4 2 3 53

Jan 2008 2 2 7 5 23 3 4 1 4 51

Apr 2008 1 2 8 6 30 5 7 1 4 64

Jul 2008 4 2 10 6 31 5 8 2 7 75

Oct 2008 3 0 5 4 29 7 4 1 3 56

Jan 2009 - Worldwide 3 5 6 6 32 7 6 2 5 72

Jan 2009 - U.S. 0 4 4 3 17 4 3 0 1 36

Jan 2009 – Foreign 3 1 2 3 15 3 3 2 4 36

Avg. Age Worldwide 1986 1996 1982 1983 1980 1979 1987 1992 1996

Avg. Age U.S. - 1996 1980 1978 1979 1985 1994 - 1976

Avg. Age Foreign 1986 - 1986 1987 1982 1972 1979 1992 2001

For Charter Worldwide 3 3 2 3 3 1 4 3 9 31

For Charter U.S. 0 0 0 2 1 0 0 0 1 4

For Charter Foreign 3 3 2 1 2 1 4 3 8 27

Up Since Last Report Down Since Last Report

The USA remains the dominant location for second hand tonnage with 31.6% of the vessels for sale. South East Asia, Far East and Mid East combined make up 33.9% of the market. The rest of the globe makes up the final 34.5% of locations. EMD and CAT are the principal main engine suppliers to this sector and power 43 and 28, respectively, of the Supply & Tug Supply Vessels listed for sale. GM power 10 vessels. MaK and MAN lead the foreign manufacturers with ten each and 66 units powered by other various engines. In addition to those for sale, Marcon has 110 straight supply and tug supply vessels listed for charter worldwide, up from 86 in October 2008.

Platform & Tug Supply Locations

Mid East

7.5%

By Arrangement

7.5%

Africa

6.9%

Europe

5.2%

Caribbean

2.9% Canada

1.1%

Far East

10.9%

U.S.

31.6%

Southeast Asia

15.5%

Mediterranean

5.7%

Latin America

5.2%

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

4

Marcon Gulf Of Mexico Market Commentary (Note: this article was written in late December and published in the January / February 2009 edition of Offshore Support Journal.)

The Gulf of Mexico remains an enigma. Given an unprecedented 12 month ride through 2008, you could be as close to predicting the forthcoming year if one was to undertake a “Do-It-Yourself” Astrology course compared to any in-depth research or analysis. Hurricanes, credit crisis, oil prices and recession have all impacted this year and their affects will continue to be felt well into 2009 and beyond.

One article that brought sharply into focus the regional uncertainty was the recent release by Barclays Capital of The Original E&P Spending Survey, which reports that global exploration and production (E&P) expenditures will contract by 12 percent to US$400 billion in 2009. However, the United States is likely to see a much sharper decline, with 2009 levels dropping 26 percent to US$79 billion, which would end a four-year upturn in U.S. E&P spending. The decline in spending comes as spending budgets are being cut in response to the significant decline in commodity prices, constrained

cash flow, and the tight credit markets. Across the border, Mexican state oil company Petroleos Mexicanos (Pemex) is actually expected to increase spending by five percent from US$16.1 billion to US$16.9 billion with efforts more focused on reviving production in several areas. Whilst some figures reported in 2008 varied depending on market segment and others were buried in wider global accounts making it hard to generalize, most of the major players reported increases in revenues and net incomes mostly as a result of new tonnage or acquisitions coming online. Utilization figures remained steady and fairly high across the board, but there appeared to be some softening of rates throughout the year until Hurricane season. One operator reported a decline on their domestic based vessel revenues due primarily to lower utilization rates as a result of weakness in the GOM market despite increases in average day rates and to fewer vessels operating in the GOM due to the transfer of vessels to international markets. Units below 200’ were seeing rates soften with only term contracts keeping revenues at expected levels. The back-to-back Hurricanes Ike and Gustav coupled with its associated repair work is only expected to keep U.S-based vessel demand high for several months compared to the multi-year efforts of the previous Hurricanes. Most owners at the Work Boat Show reported that they are still finding work and busy with post hurricane clean up work. Repair work for Hurricanes Ivan (2004), Katrina & Rita (2005) has all but been completed. One vessel owner reported he has pending offshore wind farm work which may receive an injection with incoming the White House Administration. Looking back across the past year certain long term trends remain like the outflow of shallow water rigs to overseas markets (5% decrease from 3Q 2008 over 3Q 2007). Though this rate has slowed in recent times, the offshore rig count in the GOM remains at historically low levels. ODS Petrodata expects rig demand to rise in the GOM for 2009 on the back of stronger drillship demand, but the Jack up market (the most numerous rig type) is likely to soften further.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

5

One of the bigger stories in the region this year was the tie up between GulfMark Offshore and Rigdon Marine, which most analysts concur was a positive mesh of vessel and operating portfolios. Whether operators will have the confidence and resources to spend on mergers in the coming year is unpredictable. If conditions for some operators worsen dramatically like those of the fortunes of some Wall Street institutions back in September, either the spectre of Chapter 11 reorganization looms or perhaps some “shotgun weddings” will be hastily arranged. Globally, the (lack of) credit issue has been front, middle and center across the news. Workboat magazine highlighted in their December issue some of the measures US operators (both inland and offshore) had taken as a result of the credit seizure. For offshore operators, only Tidewater Inc was listed as postponing a $200 million share buy back program in order to “maintain maximum financial flexibility.” Hornbeck reported in their Stock Exchange filings that the financial meltdown had not had a significant impact on their financial positions. Reports on project cancellations have not been widely reported yet though one survey suggested a quarter of respondents had seen projects recently postponed or cancelled. With the expected decline in E&P next year, it’s possible this may start to become a bigger hole in fixture calendar; which could lead to vessel lay ups. One operator reported that, though wary of this whole credit issue, that they hadn’t been affected, but would likely to start seeing issues like the slowing down of the payment cycles. Another operator reported that they have only benefited so far from the slowdown with opening yard slots and cheaper newbuild prices (being more in line with yard costs, without the high premiums of recent years). Orders for newbuilds are likely to soften as per the shipping wide industry slowdown, though two GOM operators just reported newbuild orders at US yards this week. The local yard orderbook looks fairly strong for the next 12 months. Marine Log/Colton currently list 67 OSV units on order at US shipyards compared with 57 about 15 months ago. Given the “maximum mobility” of these units, players are keen to emphasize to shareholders that they are able to reposition these high specification, capital intensive units to oversea deepwater areas for lucrative contracts if the market contracts domestically. The financial backdrop heading into 2009 is not encouraging for OSV operators, 2008 did see ever increasing amounts of money that oil companies were willing to bid for acreage licenses in the US GOM especially in deepwater blocks (>800ft water depth) which maybe an indicator to the longer term health of the region once commodity prices rebound.

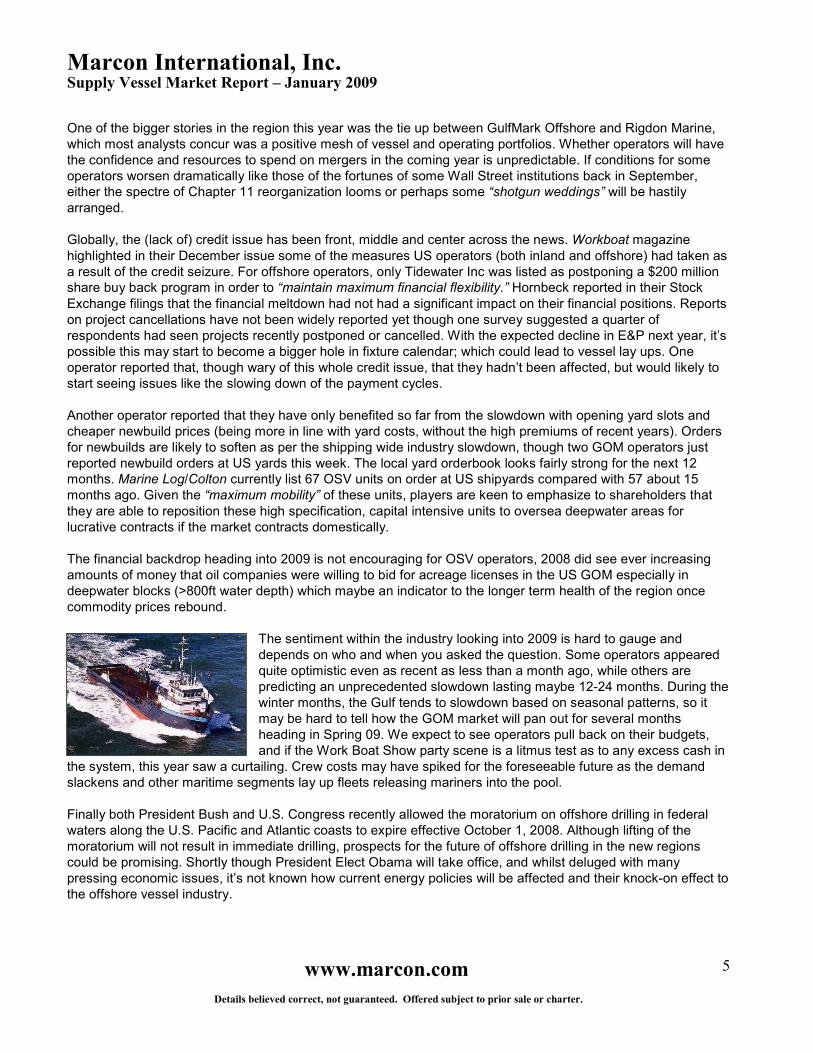

The sentiment within the industry looking into 2009 is hard to gauge and depends on who and when you asked the question. Some operators appeared quite optimistic even as recent as less than a month ago, while others are predicting an unprecedented slowdown lasting maybe 12-24 months. During the winter months, the Gulf tends to slowdown based on seasonal patterns, so it may be hard to tell how the GOM market will pan out for several months heading in Spring 09. We expect to see operators pull back on their budgets, and if the Work Boat Show party scene is a litmus test as to any excess cash in

the system, this year saw a curtailing. Crew costs may have spiked for the foreseeable future as the demand slackens and other maritime segments lay up fleets releasing mariners into the pool. Finally both President Bush and U.S. Congress recently allowed the moratorium on offshore drilling in federal waters along the U.S. Pacific and Atlantic coasts to expire effective October 1, 2008. Although lifting of the moratorium will not result in immediate drilling, prospects for the future of offshore drilling in the new regions could be promising. Shortly though President Elect Obama will take office, and whilst deluged with many pressing economic issues, it’s not known how current energy policies will be affected and their knock-on effect to the offshore vessel industry.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

6

STOP PRESS Since this article was sent to the publishers, news reports have continued to highlight the growing pains in the offshore market. Vessel demand has softened in the GOM in line with the slackening rig count. The prospect of vessel stacking is becoming a greater reality as utilization reduces, whilst the pressure on downward rates is likely to accelerate. The Obama Administration has unveiled the strategy for its offshore energy plan. The strategy calls for extending the public comment period on a proposed 5-year plan for oil and gas development on the U.S. Outer Continental Shelf (proposed by the Bush Administration on its last day in office) by 180 days, assembling a detailed report from Interior agencies on conventional and renewable offshore energy resources, holding four regional conferences to review these findings, and expediting renewable energy rulemaking for the Outer Continental Shelf. Current sentiment indicates that “renewables” will be pushed higher up the agenda, whilst the moratorium of offshore drilling could be reinstated.

Crude Oil Prices USD May 08 Jun 08 Jul 08 Aug 08 Sep 08 Oct 08 Nov 08 Dec 08

WTI - Cushing, Oklahoma $125.40 $133.88 $133.37 $116.67 $104.11 $76.61 $57.31 $41.12

Brent - Europe $122.80 $132.32 $132.72 $113.24 $97.23 $71.58 $52.45 $39.95

Source: Energy Information Administration, Office of Oil and Gas.

Natural Gas Est. Average Wellhead Prices

May 08 Jun 08 Jul 08 Aug 08 Sep 08 Oct 08 Nov 08 Dec 08

Price ($ per Mcf) $9.81 $10.82 $10.62 $8.32 $7.27 $6.36 $5.97 $5.87

Price ($ per MMBtu) $9.53 $10.52 $10.32 $8.09 $7.07 $6.18 $5.80 $5.70

Source: Energy Information Administration, Office of Oil and Gas.

Worldwide Sale & Purchase News GulfMark Rederi A/S has sold its Platform Supply Vessel UT706L design, “North Fortune” (ex-Skandi Fortune) to Nor Supply Offshore for a price in the region of USD 19 million. Built in 1983 at Ulstein Hatlo, Norway, the vessel is powered by twin Bergen KVMB12 producing 6,120BHP and has a clear deck space of 173.8'x49.2'. The 1980 Halter Marine built utility vessel “Demas Fortune” (ex-Willy 4003) powered by twin GM 12V-149-TI engines producing 1,390BHP and the 1980 Sing Koon Heng Pte built utility vessel “Samriyah“ (ex-Al-Mojil XXII) driven by a pair Kelvin Marine diesels producing 1,040BHP; both owned by Mid Gulf Offshore of the UAE, have been sold to West African interests in an en-bloc deal on private terms. Rem Offshore has sold a new anchor handling tug supply vessel. The “Rem Viking” is being built at Norway’s Kleven Verft and will be delivered in March or April, at least three months behind its original handover date. It has no charter in place and will join the North Sea spot market. The buyer is Indian operator Varun Shipping, who bought “Rem Odin” in January for a reported 420M Norwegian Kroner (approx USD 60.1M). Rem Offshore would not disclose the price of “Rem Viking” but it is thought that it went for a similar price as the “Rem Odin”.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

7

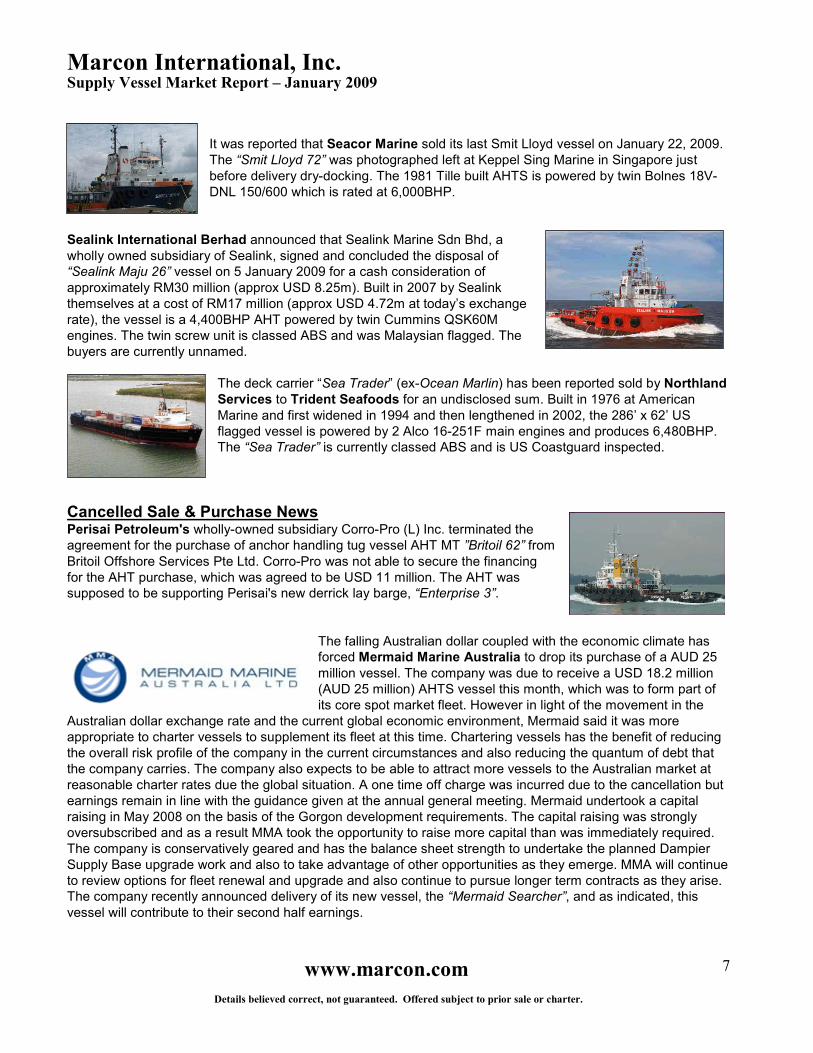

It was reported that Seacor Marine sold its last Smit Lloyd vessel on January 22, 2009. The “Smit Lloyd 72” was photographed left at Keppel Sing Marine in Singapore just before delivery dry-docking. The 1981 Tille built AHTS is powered by twin Bolnes 18V-DNL 150/600 which is rated at 6,000BHP.

Sealink International Berhad announced that Sealink Marine Sdn Bhd, a wholly owned subsidiary of Sealink, signed and concluded the disposal of “Sealink Maju 26” vessel on 5 January 2009 for a cash consideration of approximately RM30 million (approx USD 8.25m). Built in 2007 by Sealink themselves at a cost of RM17 million (approx USD 4.72m at today’s exchange rate), the vessel is a 4,400BHP AHT powered by twin Cummins QSK60M engines. The twin screw unit is classed ABS and was Malaysian flagged. The buyers are currently unnamed.

The deck carrier “Sea Trader” (ex-Ocean Marlin) has been reported sold by Northland Services to Trident Seafoods for an undisclosed sum. Built in 1976 at American Marine and first widened in 1994 and then lengthened in 2002, the 286’ x 62’ US flagged vessel is powered by 2 Alco 16-251F main engines and produces 6,480BHP. The “Sea Trader” is currently classed ABS and is US Coastguard inspected.

Cancelled Sale & Purchase News Perisai Petroleum's wholly-owned subsidiary Corro-Pro (L) Inc. terminated the agreement for the purchase of anchor handling tug vessel AHT MT ”Britoil 62” from Britoil Offshore Services Pte Ltd. Corro-Pro was not able to secure the financing for the AHT purchase, which was agreed to be USD 11 million. The AHT was supposed to be supporting Perisai's new derrick lay barge, “Enterprise 3”.

The falling Australian dollar coupled with the economic climate has forced Mermaid Marine Australia to drop its purchase of a AUD 25 million vessel. The company was due to receive a USD 18.2 million (AUD 25 million) AHTS vessel this month, which was to form part of its core spot market fleet. However in light of the movement in the

Australian dollar exchange rate and the current global economic environment, Mermaid said it was more appropriate to charter vessels to supplement its fleet at this time. Chartering vessels has the benefit of reducing the overall risk profile of the company in the current circumstances and also reducing the quantum of debt that the company carries. The company also expects to be able to attract more vessels to the Australian market at reasonable charter rates due the global situation. A one time off charge was incurred due to the cancellation but earnings remain in line with the guidance given at the annual general meeting. Mermaid undertook a capital raising in May 2008 on the basis of the Gorgon development requirements. The capital raising was strongly oversubscribed and as a result MMA took the opportunity to raise more capital than was immediately required. The company is conservatively geared and has the balance sheet strength to undertake the planned Dampier Supply Base upgrade work and also to take advantage of other opportunities as they emerge. MMA will continue to review options for fleet renewal and upgrade and also continue to pursue longer term contracts as they arise. The company recently announced delivery of its new vessel, the “Mermaid Searcher”, and as indicated, this vessel will contribute to their second half earnings.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

8

The sale to Nigerian Buyers of the Garware Offshore owned 2008-built UT755LN “Mana” failed and the vessel remains available for charter. Norwegian offshore shipping company Solstad Offshore ASA disclosed in January that its 71.7% ship-owning subsidiary Normand Skarven KS has cancelled the sale of its anchor handling tug supply vessel “Normand Skarven”. The company agreed in 2008 to sell the vessel to a foreign buyer. Although the buyer paid a 10% deposit, it did not comply with further payment obligations. The “Normand Skarven” is currently contracted to StatoilHydro.

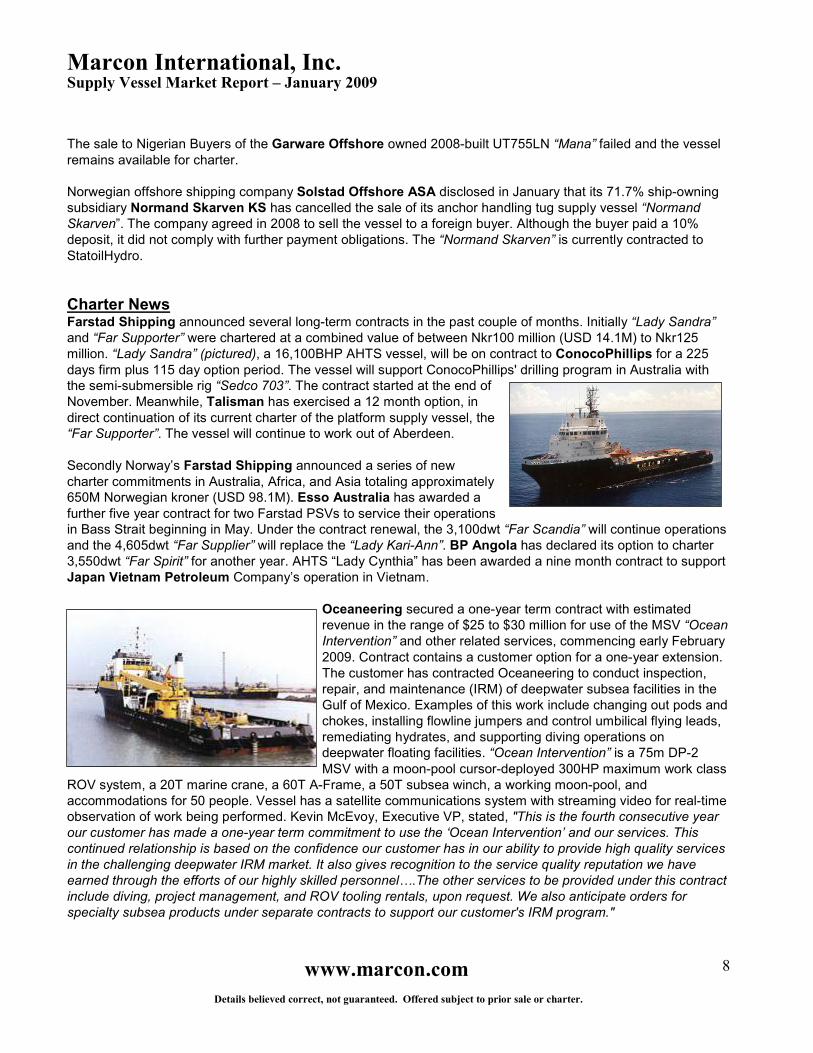

Charter News Farstad Shipping announced several long-term contracts in the past couple of months. Initially “Lady Sandra” and “Far Supporter” were chartered at a combined value of between Nkr100 million (USD 14.1M) to Nkr125 million. “Lady Sandra” (pictured), a 16,100BHP AHTS vessel, will be on contract to ConocoPhillips for a 225 days firm plus 115 day option period. The vessel will support ConocoPhillips' drilling program in Australia with the semi-submersible rig “Sedco 703”. The contract started at the end of November. Meanwhile, Talisman has exercised a 12 month option, in direct continuation of its current charter of the platform supply vessel, the “Far Supporter”. The vessel will continue to work out of Aberdeen. Secondly Norway’s Farstad Shipping announced a series of new charter commitments in Australia, Africa, and Asia totaling approximately 650M Norwegian kroner (USD 98.1M). Esso Australia has awarded a further five year contract for two Farstad PSVs to service their operations in Bass Strait beginning in May. Under the contract renewal, the 3,100dwt “Far Scandia” will continue operations and the 4,605dwt “Far Supplier” will replace the “Lady Kari-Ann”. BP Angola has declared its option to charter 3,550dwt “Far Spirit” for another year. AHTS “Lady Cynthia” has been awarded a nine month contract to support Japan Vietnam Petroleum Company’s operation in Vietnam.

Oceaneering secured a one-year term contract with estimated revenue in the range of $25 to $30 million for use of the MSV “Ocean Intervention” and other related services, commencing early February 2009. Contract contains a customer option for a one-year extension. The customer has contracted Oceaneering to conduct inspection, repair, and maintenance (IRM) of deepwater subsea facilities in the Gulf of Mexico. Examples of this work include changing out pods and chokes, installing flowline jumpers and control umbilical flying leads, remediating hydrates, and supporting diving operations on deepwater floating facilities. “Ocean Intervention” is a 75m DP-2 MSV with a moon-pool cursor-deployed 300HP maximum work class

ROV system, a 20T marine crane, a 60T A-Frame, a 50T subsea winch, a working moon-pool, and accommodations for 50 people. Vessel has a satellite communications system with streaming video for real-time observation of work being performed. Kevin McEvoy, Executive VP, stated, "This is the fourth consecutive year our customer has made a one-year term commitment to use the ‘Ocean Intervention’ and our services. This continued relationship is based on the confidence our customer has in our ability to provide high quality services in the challenging deepwater IRM market. It also gives recognition to the service quality reputation we have earned through the efforts of our highly skilled personnel….The other services to be provided under this contract include diving, project management, and ROV tooling rentals, upon request. We also anticipate orders for specialty subsea products under separate contracts to support our customer's IRM program."

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

9

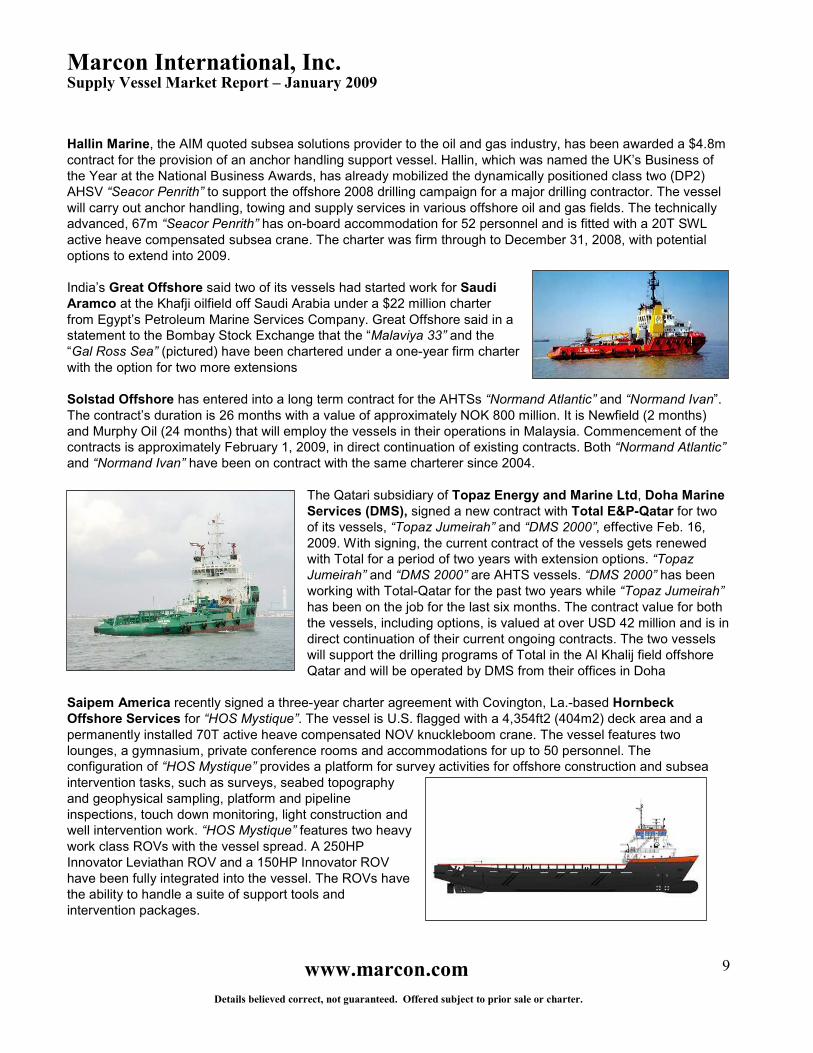

Hallin Marine, the AIM quoted subsea solutions provider to the oil and gas industry, has been awarded a $4.8m contract for the provision of an anchor handling support vessel. Hallin, which was named the UK’s Business of the Year at the National Business Awards, has already mobilized the dynamically positioned class two (DP2) AHSV “Seacor Penrith” to support the offshore 2008 drilling campaign for a major drilling contractor. The vessel will carry out anchor handling, towing and supply services in various offshore oil and gas fields. The technically advanced, 67m “Seacor Penrith” has on-board accommodation for 52 personnel and is fitted with a 20T SWL active heave compensated subsea crane. The charter was firm through to December 31, 2008, with potential options to extend into 2009. India’s Great Offshore said two of its vessels had started work for Saudi Aramco at the Khafji oilfield off Saudi Arabia under a $22 million charter from Egypt’s Petroleum Marine Services Company. Great Offshore said in a statement to the Bombay Stock Exchange that the “Malaviya 33” and the “Gal Ross Sea” (pictured) have been chartered under a one-year firm charter with the option for two more extensions Solstad Offshore has entered into a long term contract for the AHTSs “Normand Atlantic” and “Normand Ivan”. The contract’s duration is 26 months with a value of approximately NOK 800 million. It is Newfield (2 months) and Murphy Oil (24 months) that will employ the vessels in their operations in Malaysia. Commencement of the contracts is approximately February 1, 2009, in direct continuation of existing contracts. Both “Normand Atlantic” and “Normand Ivan” have been on contract with the same charterer since 2004.

The Qatari subsidiary of Topaz Energy and Marine Ltd, Doha Marine Services (DMS), signed a new contract with Total E&P-Qatar for two of its vessels, “Topaz Jumeirah” and “DMS 2000”, effective Feb. 16, 2009. With signing, the current contract of the vessels gets renewed with Total for a period of two years with extension options. “Topaz Jumeirah” and “DMS 2000” are AHTS vessels. “DMS 2000” has been working with Total-Qatar for the past two years while “Topaz Jumeirah” has been on the job for the last six months. The contract value for both the vessels, including options, is valued at over USD 42 million and is in direct continuation of their current ongoing contracts. The two vessels will support the drilling programs of Total in the Al Khalij field offshore Qatar and will be operated by DMS from their offices in Doha

Saipem America recently signed a three-year charter agreement with Covington, La.-based Hornbeck Offshore Services for “HOS Mystique”. The vessel is U.S. flagged with a 4,354ft2 (404m2) deck area and a permanently installed 70T active heave compensated NOV knuckleboom crane. The vessel features two lounges, a gymnasium, private conference rooms and accommodations for up to 50 personnel. The configuration of “HOS Mystique” provides a platform for survey activities for offshore construction and subsea intervention tasks, such as surveys, seabed topography and geophysical sampling, platform and pipeline inspections, touch down monitoring, light construction and well intervention work. “HOS Mystique” features two heavy work class ROVs with the vessel spread. A 250HP Innovator Leviathan ROV and a 150HP Innovator ROV have been fully integrated into the vessel. The ROVs have the ability to handle a suite of support tools and intervention packages.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

10

Orders

Garware Offshore Services has said it would invest about $96 million over the next 18 months to add three ships to its existing nine-vessel fleet. "We will be taking deliveries of an anchor-handling tug-cum supply vessel (AHTSV) and a platform supply vessel (PSV) at the end of February," Garware Offshore Services President Finance Sandeep Akolkar told PTI. "The AHTSV cost us about $16 million and the PSV about $25 million," he added. Besides, it will acquire a large PSV for about $55 million, the delivery for which will be in October 2010. Akolkar said the company has enough cash on its books to buy vessels. "Our fleet consists of

9 vessels now and we will be adding a construction barge and a 60-tonne anchor-handling tug (small AHT) to our fleet in July this," he said. The vessels would be bought through its wholly-owned Singapore subsidiary, Garware Offshore International Services, on a bareboat charter basis, arranged for by the NFC bank, he said. The bareboat charter will give the company an option to buy the vessel within 10 years of deployment. As of December31, 2008, Tidewater, Inc. of New Orleans had commitments to build 56 vessels at a total cost of approx. $1.1B. In addition to other vessel classes, Tidewater is committed to the construction of 21 AHTSs ranging between 6,500 to 13,600BHP. Scheduled delivery of the vessels began January 2009 with delivery of the final vessel in July 2012. As of December 31, 2008, $419m had been expended. Tidewater’s vessel construction program has been designed to replace over time the older fleet of vessels with fewer, larger and more efficient vessels, while also opportunistically revamping size and capabilities. The majority of Tidewater’s older supply and towing-supply vessels were constructed between 1976 and 1983. Since these vessels exceed 25 years of age, they could require replacement within the next several years, depending on the strength of the market during this time frame. In addition to age, market conditions also help determine when a vessel is no longer economically viable. Tidewater anticipates using future operating cash flows, existing borrowing capacity or new borrowings or lease arrangements to fund this fleet renewal and modernization program over the next several years. During the last half of 2008, worldwide demand for oil and gas dropped precipitously and energy prices sharply declined as a result of a global recession. Tidewater is assessing the possible impacts on its operations and financial condition of various scenarios, including the potential for a prolonged global recession. In particular, Tidewater continues to evaluate how a prolonged global recession might impact development plans of exploration and production companies and global demand for vessels. Among other things, Tidewater is also uncertain of the impact a prolonged global recession and the related distress in credit and capital markets will have on the ability of shipyards to meet scheduled deliveries of new vessels or the ability of the company to renew its fleet through new construction or acquisitions. Also unknown is the potential effect that the recession may have on more highly-leveraged competitors, including those companies’ abilities to continue to fund their construction commitments. At present, the financial and commodity markets are still too unstable to assess the situation with a high degree of confidence. A 285-foot supply boat is being built for an undisclosed buyer by two shipyards. VT Halter Marine is building the hull and deckhouses and Candies Shipbuilders, LLC, will perform the final outfitting. With most offshore oil vessel builders filled to capacity, sometimes shipyards with yard space to build a hull and houses will team up with another yard that can do the finish work to get a vessel delivered on time. Still, it will be January 2010 before the vessel is delivered.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

11

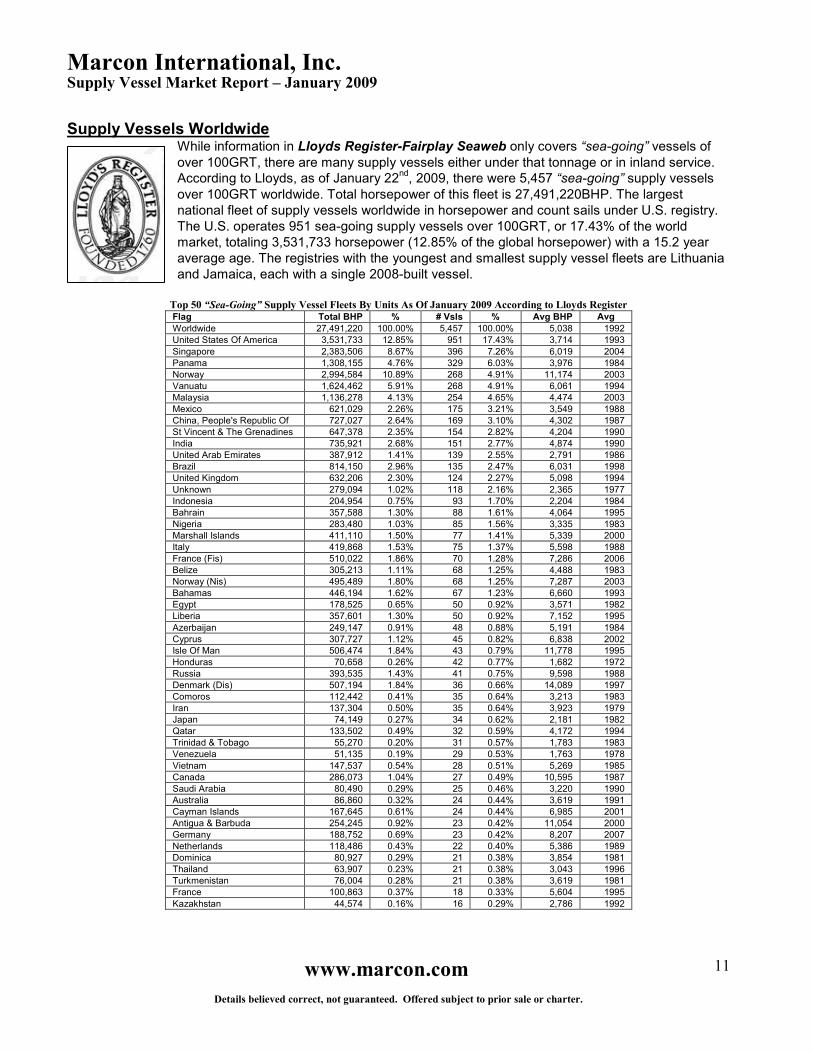

Supply Vessels Worldwide While information in Lloyds Register-Fairplay Seaweb only covers “sea-going” vessels of over 100GRT, there are many supply vessels either under that tonnage or in inland service. According to Lloyds, as of January 22

nd, 2009, there were 5,457 “sea-going” supply vessels

over 100GRT worldwide. Total horsepower of this fleet is 27,491,220BHP. The largest national fleet of supply vessels worldwide in horsepower and count sails under U.S. registry. The U.S. operates 951 sea-going supply vessels over 100GRT, or 17.43% of the world market, totaling 3,531,733 horsepower (12.85% of the global horsepower) with a 15.2 year average age. The registries with the youngest and smallest supply vessel fleets are Lithuania and Jamaica, each with a single 2008-built vessel.

Top 50 “Sea-Going” Supply Vessel Fleets By Units As Of January 2009 According to Lloyds Register Flag Total BHP % # Vsls % Avg BHP Avg

Age Worldwide 27,491,220 100.00% 5,457 100.00% 5,038 1992

United States Of America 3,531,733 12.85% 951 17.43% 3,714 1993

Singapore 2,383,506 8.67% 396 7.26% 6,019 2004

Panama 1,308,155 4.76% 329 6.03% 3,976 1984

Norway 2,994,584 10.89% 268 4.91% 11,174 2003

Vanuatu 1,624,462 5.91% 268 4.91% 6,061 1994

Malaysia 1,136,278 4.13% 254 4.65% 4,474 2003

Mexico 621,029 2.26% 175 3.21% 3,549 1988

China, People's Republic Of 727,027 2.64% 169 3.10% 4,302 1987

St Vincent & The Grenadines 647,378 2.35% 154 2.82% 4,204 1990

India 735,921 2.68% 151 2.77% 4,874 1990

United Arab Emirates 387,912 1.41% 139 2.55% 2,791 1986

Brazil 814,150 2.96% 135 2.47% 6,031 1998

United Kingdom 632,206 2.30% 124 2.27% 5,098 1994

Unknown 279,094 1.02% 118 2.16% 2,365 1977

Indonesia 204,954 0.75% 93 1.70% 2,204 1984

Bahrain 357,588 1.30% 88 1.61% 4,064 1995

Nigeria 283,480 1.03% 85 1.56% 3,335 1983

Marshall Islands 411,110 1.50% 77 1.41% 5,339 2000

Italy 419,868 1.53% 75 1.37% 5,598 1988

France (Fis) 510,022 1.86% 70 1.28% 7,286 2006

Belize 305,213 1.11% 68 1.25% 4,488 1983

Norway (Nis) 495,489 1.80% 68 1.25% 7,287 2003

Bahamas 446,194 1.62% 67 1.23% 6,660 1993

Egypt 178,525 0.65% 50 0.92% 3,571 1982

Liberia 357,601 1.30% 50 0.92% 7,152 1995

Azerbaijan 249,147 0.91% 48 0.88% 5,191 1984

Cyprus 307,727 1.12% 45 0.82% 6,838 2002

Isle Of Man 506,474 1.84% 43 0.79% 11,778 1995

Honduras 70,658 0.26% 42 0.77% 1,682 1972

Russia 393,535 1.43% 41 0.75% 9,598 1988

Denmark (Dis) 507,194 1.84% 36 0.66% 14,089 1997

Comoros 112,442 0.41% 35 0.64% 3,213 1983

Iran 137,304 0.50% 35 0.64% 3,923 1979

Japan 74,149 0.27% 34 0.62% 2,181 1982

Qatar 133,502 0.49% 32 0.59% 4,172 1994

Trinidad & Tobago 55,270 0.20% 31 0.57% 1,783 1983

Venezuela 51,135 0.19% 29 0.53% 1,763 1978

Vietnam 147,537 0.54% 28 0.51% 5,269 1985

Canada 286,073 1.04% 27 0.49% 10,595 1987

Saudi Arabia 80,490 0.29% 25 0.46% 3,220 1990

Australia 86,860 0.32% 24 0.44% 3,619 1991

Cayman Islands 167,645 0.61% 24 0.44% 6,985 2001

Antigua & Barbuda 254,245 0.92% 23 0.42% 11,054 2000

Germany 188,752 0.69% 23 0.42% 8,207 2007

Netherlands 118,486 0.43% 22 0.40% 5,386 1989

Dominica 80,927 0.29% 21 0.38% 3,854 1981

Thailand 63,907 0.23% 21 0.38% 3,043 1996

Turkmenistan 76,004 0.28% 21 0.38% 3,619 1981

France 100,863 0.37% 18 0.33% 5,604 1995

Kazakhstan 44,574 0.16% 16 0.29% 2,786 1992

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

12

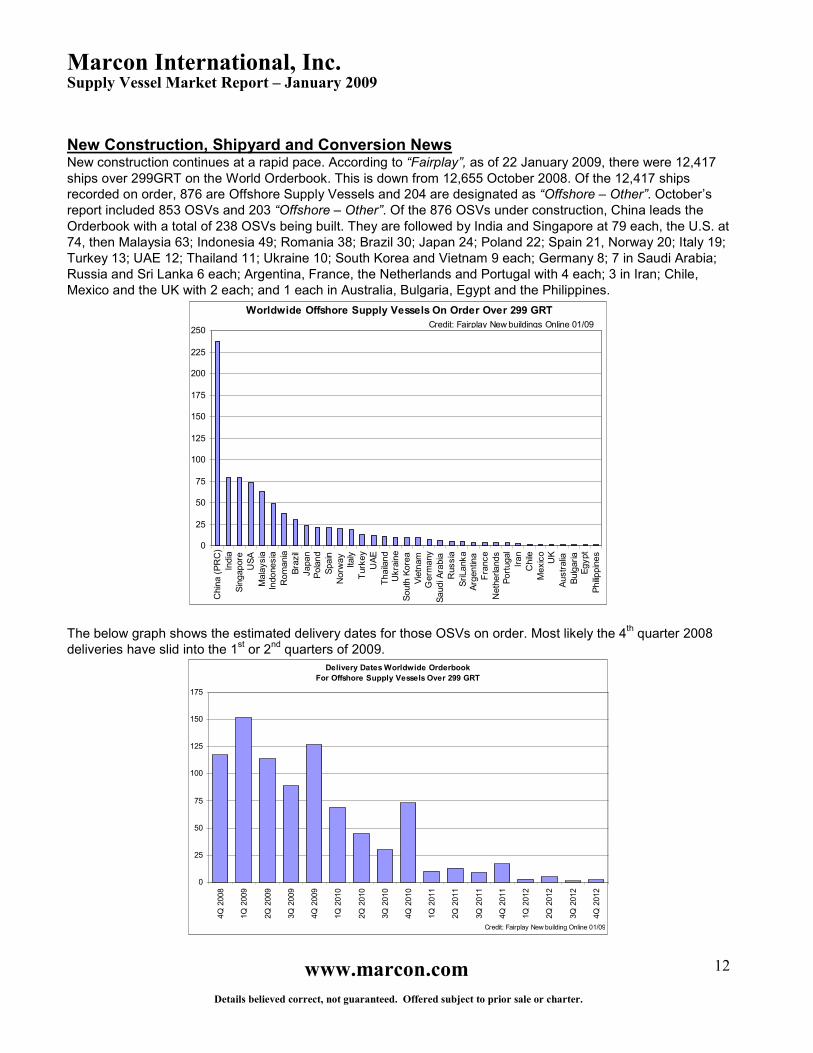

New Construction, Shipyard and Conversion News New construction continues at a rapid pace. According to “Fairplay”, as of 22 January 2009, there were 12,417 ships over 299GRT on the World Orderbook. This is down from 12,655 October 2008. Of the 12,417 ships recorded on order, 876 are Offshore Supply Vessels and 204 are designated as “Offshore – Other”. October’s report included 853 OSVs and 203 “Offshore – Other”. Of the 876 OSVs under construction, China leads the Orderbook with a total of 238 OSVs being built. They are followed by India and Singapore at 79 each, the U.S. at 74, then Malaysia 63; Indonesia 49; Romania 38; Brazil 30; Japan 24; Poland 22; Spain 21, Norway 20; Italy 19; Turkey 13; UAE 12; Thailand 11; Ukraine 10; South Korea and Vietnam 9 each; Germany 8; 7 in Saudi Arabia; Russia and Sri Lanka 6 each; Argentina, France, the Netherlands and Portugal with 4 each; 3 in Iran; Chile, Mexico and the UK with 2 each; and 1 each in Australia, Bulgaria, Egypt and the Philippines.

Worldwide Offshore Supply Vessels On Order Over 299 GRT

0

25

50

75

100

125

150

175

200

225

250

Chin

a (

PR

C)

India

Sin

gapore

US

A

Mala

ysia

Indonesia

Rom

ania

Bra

zil

Japan

Pola

nd

Spain

Norw

ay

Italy

Turk

ey

UA

E

Thaila

nd

Ukra

ine

South

Kore

a

Vie

tnam

Germ

any

Saudi A

rabia

Russia

SriLanka

Arg

entin

a

Fra

nce

Neth

erlands

Port

ugal

Iran

Chile

Mexic

oU

K

Austr

alia

Bulg

aria

Egypt

Philippin

es

Credit: Fairplay New buildings Online 01/09

The below graph shows the estimated delivery dates for those OSVs on order. Most likely the 4

th quarter 2008

deliveries have slid into the 1st or 2

nd quarters of 2009.

Delivery Dates Worldwide Orderbook

For Offshore Supply Vessels Over 299 GRT

0

25

50

75

100

125

150

175

4Q

2008

1Q

2009

2Q

2009

3Q

2009

4Q

2009

1Q

2010

2Q

2010

3Q

2010

4Q

2010

1Q

2011

2Q

2011

3Q

2011

4Q

2011

1Q

2012

2Q

2012

3Q

2012

4Q

2012

Credit: Fairplay New building Online 01/09

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

13

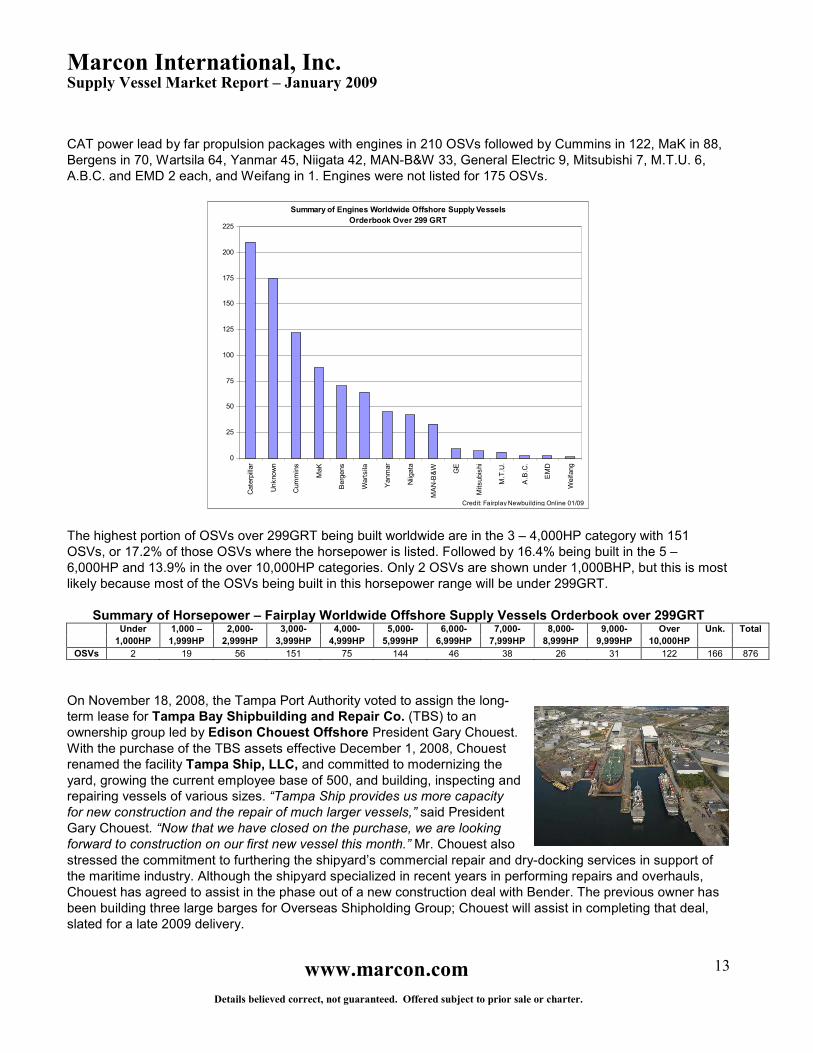

CAT power lead by far propulsion packages with engines in 210 OSVs followed by Cummins in 122, MaK in 88, Bergens in 70, Wartsila 64, Yanmar 45, Niigata 42, MAN-B&W 33, General Electric 9, Mitsubishi 7, M.T.U. 6, A.B.C. and EMD 2 each, and Weifang in 1. Engines were not listed for 175 OSVs.

Summary of Engines Worldwide Offshore Supply Vessels

Orderbook Over 299 GRT

0

25

50

75

100

125

150

175

200

225

Cate

rpill

ar

Unknow

n

Cum

min

s

MaK

Berg

ens

Wart

sila

Yanm

ar

Niig

ata

MA

N-B

&W GE

Mitsubis

hi

M.T

.U.

A.B

.C.

EM

D

Weifang

Credit: Fairplay Newbuilding Online 01/09 The highest portion of OSVs over 299GRT being built worldwide are in the 3 – 4,000HP category with 151 OSVs, or 17.2% of those OSVs where the horsepower is listed. Followed by 16.4% being built in the 5 – 6,000HP and 13.9% in the over 10,000HP categories. Only 2 OSVs are shown under 1,000BHP, but this is most likely because most of the OSVs being built in this horsepower range will be under 299GRT.

Summary of Horsepower – Fairplay Worldwide Offshore Supply Vessels Orderbook over 299GRT Under 1,000 – 2,000- 3,000- 4,000- 5,000- 6,000- 7,000- 8,000- 9,000- Over

1,000HP 1,999HP 2,999HP 3,999HP 4,999HP 5,999HP 6,999HP 7,999HP 8,999HP 9,999HP 10,000HP

Unk. Total

OSVs 2 19 56 151 75 144 46 38 26 31 122 166 876

On November 18, 2008, the Tampa Port Authority voted to assign the long-term lease for Tampa Bay Shipbuilding and Repair Co. (TBS) to an ownership group led by Edison Chouest Offshore President Gary Chouest. With the purchase of the TBS assets effective December 1, 2008, Chouest renamed the facility Tampa Ship, LLC, and committed to modernizing the yard, growing the current employee base of 500, and building, inspecting and repairing vessels of various sizes. “Tampa Ship provides us more capacity for new construction and the repair of much larger vessels,” said President Gary Chouest. “Now that we have closed on the purchase, we are looking forward to construction on our first new vessel this month.” Mr. Chouest also stressed the commitment to furthering the shipyard’s commercial repair and dry-docking services in support of the maritime industry. Although the shipyard specialized in recent years in performing repairs and overhauls, Chouest has agreed to assist in the phase out of a new construction deal with Bender. The previous owner has been building three large barges for Overseas Shipholding Group; Chouest will assist in completing that deal, slated for a late 2009 delivery.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

14

Tampa Ship is conveniently located in the protected harbors of Tampa Bay directly accessible from the Gulf of Mexico via a 43ft (13.11m) channel, and is the largest, most complete shipyard between Pascagoula, Mississippi, and Hampton Roads, Virginia. Tampa Ship fronts Sparkman Channel. Sparkman Channel is 43ft (13.11m) in depth 500ft (152.4m) wide with a 700ft (213.36m) turning basin and is maintained by the U.S. Army Corps of Engineers. One of the very few limitations to ship size it can handle is due to the Skyway Bridge at the mouth of Tampa Bay. This bridge limits the max height out of water (H.O.W) to 175 ft (54.559m). The shipyard covers 62 acres (25.09ha) and features four graving docks with 28ft (8.53m) draft capabilities for ships up to 746ft (227.38m) in length, and 24ft (7.31m) draft for ships up to 907ft (276.44m) in length, and a covered erection building 600ft (182.88m) long x 145ft (44.20m) wide x 115ft (35.05m) high capable of 880T lifts. Year-round warm weather, skilled craftsmen, and an extensive local network of experienced subcontractors combine to create the ideal environment for ship repair, conversion, or new construction projects.

Contract News Singapore Technologies Engineering Ltd announced that its marine arm, Singapore Technologies Marine Ltd, has secured a S$30m contract to provide detailed design, construction and outfitting of a 228ft seismic survey vessel for Swire Pacific Offshore Operations (Pte) Ltd, a wholly-owned subsidiary of Swire Pacific Limited. Construction is expected to commence in May 2009 and delivery is planned for the second half of 2010. This contract is not expected to have any material impact on the consolidated net tangible assets per share and earnings per share of ST Engineering for the current financial year. This 223ft by 49ft seismic survey vessel, with medium speed diesel propulsion of 2 x 2,880kW, will be designed, constructed, completed and delivered in compliance with the rules, regulations and with all requirements of and under the survey of American Bureau of Shipping, and shall be distinguished in the registry by the symbol and annotation of ABS Class +A1, +AMS, ACCU, SPS, E, Ice Class Notation C. Seismic survey vessels are capable of driving at a selected surveying speed through the water and the hull form of the marine seismic survey vessel is arranged to produce low wake field turbulence as it is widely used in the offshore oil and gas exploration field.

Deliveries Newbuild floating production, storage and offloading vessel (FPSO) “Hai Yang Shi You 117” was scheduled to leave SMOE's shipyard (division of Sembcorp Marine Ltd) in mid-December for CNOOC's Penglai 19-3 (PL 19-3) development in China. The FPSO will be towed to location by SEMCO's AHTs “Salviceroy” and “Salviscount” and AHTS “Posh Vantage”. The three offshore support vessels will be joined by two other tugs, “Salvaliant” and “Salvigour”, upon their expected arrival on location at Penglai in the first week of January. CNOOC's engineering arm COOEC and SEMCO will jointly undertake the FPSO installation. The topsides fabrication for the FPSO and its final installation were completed at SMOE's yard. Its hull was constructed by Shanghai Waigaoqiao

Shipbuilding. FPSO “Hai Yang Shi You 117” was scheduled to start production at PL 19-3 from the end of this year and was part of the Phase II development at the oil field. PL 19-3 Phase II development also includes five wellhead platforms and a central processing facility. Production first begun at one of the four wellhead platforms last year and was supported by FPSO Bohai Ming Zhu. Bohai Ming Zhu is due to undergo a 10-month maintenance program next June.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

15

Saudi Arabia's Zamil Shipbuilding & Ship Repair launched “Zamil-54”, the third Rolls Royce UT 733-2 AHTS built at its Dammam shipyard. This vessel is the third of seven vessels of the same type to be built under license agreement from Rolls Royce Marine Norway. The vessels will all be classed by ABS. Zamil Shipyard has a full order book and will be busy with new buildings to mid 2012. Other vessels on order include four more UT AHTS, one buoy handling vessel, five tugs and one diving support vessel.

US Shipbuilder Breaux Brothers recently delivered a pair of 160-ft. fast supply vessels to Edison Chouest Offshore, including the “Fast Tender” (Hull 48) and the “Fast Track” (Hull 49) – the company’s first DP 2 fast supply vessel.

"Far Scimitar" (AHTS UT712L) was delivered in November from STX Norway Offshore AS, Brevik, to Farstad Supply AS, a wholly owned subsidiary of Farstad Shipping ASA. The vessel will trade the spot market in the North Sea. A long-term facility of NOK 260 million has been drawn with Eksportfinans ASA to finance the vessel. The loan is guaranteed by Nordea Bank Norge ASA. During November the naming ceremony for the new Eidesvik vessel “Viking Poseidon” was held in Ulsteinvik. The Sponsoring Lady, Nathalie Pinon, gave name to the vessel. The M/V “Viking Poseidon” is an Offshore Construction vessel designed by Ulstein Design AS with an Ulstein X-Bow

(R) . M/V “Viking Poseidon” will go on a

long-term contract with Veolia ES Special Services Inc. (USA). The contract is for eight years with options. The ship will work with a remote operated vehicle, to inspect and repair offshore installations in the Gulf of Mexico. Eidesvik Offshore has, through its associate Eidesvik OCV KS, taken delivery of the vessel from Ulstein Verft. It has an overall length of 130m, breadth of 25m and a large cargo deck area of 1,700m2. Up to 105 persons can be accommodated and the vessel is equipped with two moon-pools, a 250T active heave compensated offshore crane, ROV-hangar, diesel-electric machinery and helicopter deck. A long-term facility of NOK 608 million has been drawn with Eksportfinans ASA to finance the vessel. The loan is guaranteed by GIEK and Sparebank 1 SR-bank. The contract has a value for the firm period of more than a Billion NOK.

The two platform supply vessels under construction at the Cochin Shipyard for Greek company Hellespont Steamship Corporation were named recently. The first vessel BY 64 was named “Hellespont Daring’’ and the other one BY 65 was named “Hellespont Dawn’ (pictured) ’. BY 64 was named by Philippines Ambassador to Germany Delia Domingo Albert while BY 65 was named by Gloria Freifrau von Olderhausen, mother of Hellespont Steam Corporation CEO Christian von Olderhausen. The PSVs are of the

popular UT-755-LN design for offshore industry. They were designed for satisfying the specific demands of transport of materials such as deck cargo, pipes, liquid cargo, cement and barite. The ships are built and classified under Det Norske Veritas and they are designed for unmanned engine room and dynamic positioning grade I. The vessels also satisfy the `CLEAN’ notation of DNV which ensures high standards of environmental safety. Presently, the yard is constructing 20 offshore vessels for European and American clients. The order is valued at Rs 3,000 crore (approx. USD 617.7m at February 13, 2009’s exchange rate).

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

16

Malaysia's offshore vessel contractor, JRI Resources Sdn Bhd recently took deliveries of two 5,150BHP AHTSVs, “MMS Pahlawan 2” and “MMS Pahlawan 3”, from Singapore-based Jaya Shipbuilding and Engineering Pte Ltd. “MMS Pahlawan 2” was christened at a ceremony on Nov. 21 at Jaya shipyard. The vessel was planning to work the local spot market. “MMS Pahlawan 3” was delivered to JRI Resourcesin October. The AHTS is expected to continue to work at the Duyong field off Peninsular Malaysia to support J. Ray McDermott's derrick barge “DB30” until early December.

US Gulf Operators Abdon Callais Offshore have taken delivery of two new 205ft class service vessels, M/V “Aco Arthur A. Forect” and M/V “Pope Benedict XVI” from Master Boat Builders. The delivery of the vessels brings Abdon’s fleet to 41 shallow draft vessels. Each vessel has the equipment required to service drilling, production, construction, seismic and other dive support operations. Each vessel

has a maximum hull depth of 15ft and a working hull draft of 13ft and can carry 925T on a clear deck. Equipment on board both vessels includes a computerized touch screen to control bulk discharge rates and flow, a Radius Reference System that works with the Kongsbeg DP 2 system and six separate internal pneumatic tanks. Abdon Callais Offshore has options to build similar vessels with Master Boat Builders through 2011, and expects to take delivery of six additional newbuild vessels in 2009.

Master Boat Builders, Inc., also delivered the “Callais Explorer”, an offshore supply vessel to Abdon Callais Offshore LLC. The vessel’s dimensions are 145ft length by 36ft beam by 12ft depth by 10ft. It is driven by two CAT 3508B main engines total power 850HP at 1,200RPM. Varun Shipping Company has taken delivery of a fourth 2008 built 16,100BHP AHTS. This is a specialized vessel which is used for deep sea oil exploration activity going on in areas like North Sea, KG basin and Atlantic Ocean off the coasts of Nigeria, Brazil and Mexico. With this acquisition, the company owns a well diversified fleet of 20 vessels comprising of 11 LPG carriers, 3 double hull Aframax crude tankers and 6 anchor handling towing and supply vessels. The acquisition was financed partly out of company’s internal resources and partly out of long term loan availed from a banker.

Bourbon Offshore took delivery of the 10th vessel in the Bourbon Liberty series. “Bourbon Liberty 110”, is a PSV intended for operations in the Gulf of Guinea. Bourbon’s decision to invest massively in a new generation of vessels able to operate in deepwater offshore, to rapidly replace old and obsolete vessels operating in continental offshore, is a key aspect of its Horizon 2012 strategy. With this aim, Bourbon created the Bourbon Liberty concept and ordered 76 vessels: 22 oil PSVs, the Bourbon Liberty 100; and 54 platform AHTSVs, the Bourbon Liberty 200. These vessels are mass constructed in shipyards in China. The first PSV was delivered in March 2008. Ten vessels have been delivered to date. In line with the initial schedule, Bourbon Liberty deliveries will continue at regular intervals through to September 2011.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

17

The “Lamnalco Malkoha” was delivered to Lamnalco Group from ABG Shipyard in India. The 53m long 90T bollard pull ahead and 80T bollard pull astern azimuth drive propulsion AHTS is fitted with Kongesberg Dynamic positioning (DP-1) equipment to hold position in rough sea condition. The vessel is able to carry out anchor handling, towing, rescue, offshore supply, transport pipes, fresh water, diesel oil, stores, materials and equipment, move men and materials between platforms and shore, external fire fighting (FiFi-1 class) and other related duties. The vessel is to supply, support the Floating Production Offloading Storage (FPSO) vessels, offshore oil and gas field on a twenty four hour per day basis. The “Lamnalco Malkoha” is the second vessel delivered to Lamnalco in this financial year. So far Lamnalco Group accepted delivery of 10 vessels, including the present one. ABG Shipyard is building another 4 vessels for the Lamnalco Group. The Fleet strength of the group is over 90 vessels. Colombo Dockyard PLC (CDPLC) launched the fourth AHTSV built for Greatship Global Offshore Services Limited of Singapore (GGOSL). The specialty of the launching was that it marked the first vessel built by assembling units on top of a barge due to space constraints faced by the premier shipbuilding yard in Colombo. This ceremony marks the launching of the last vessel of a series of four AHTSVs that CDPLC is building for GGOSL. GGOSL is a wholly owned subsidiary of one of India's largest private sector shipping companies, the Great Eastern Shipping Company, which is in the business of providing offshore oil field services catering to the oil and gas domain. The first AHTSV “Greatship Anjali” was delivered in January 2008; “Abha” is being outfitted and is scheduled to be delivered in January 2009. This fourth AHTSV “Greatship Aditi” will immediately go in for machinery installation, piping, electrical and ship outfitting work and will join her sister vessels in April 2009. The second AHTSV “Greatship Amrita” was delivered in April 2008.

In the 4th quarter of 2008, US operator Trico Marine Services, Inc. took

delivery from Bender Shipbuilding and Repair Co. Inc, the 210’ x 54’ Guido Perla designed GPA 640, “Trico Moon”. It is ABS classed and rated DP 2. The vessel was chartered to Mexico on a two year basis.

Alam Maritim Resources Bhd’s associate under Alam-PE JV Co has successfully commissioned an anchor handling tug supply vessel, MV “Setia Hebat”, with its maiden voyage to Kuantan Port for immediate charter. In a statement, the group said that “Setia Hebat” had 5,000BHP and DP-1 capacity. Alam Maritim has entered into a joint venture with CIMB Private Equity (CIMB-PE) to acquire five vessels amounting to USD 70m. The joint venture company would be able to leverage off CIMB-PE’s experience and knowledge of the financial industry to secure itself financially, Alam Maritim said. “Setia Hebat” has been awarded the contract for the provision of straight supply vessel by an oil major for domestic drilling operations and the contract has a primary duration of three years with a one-year extension option. The delivery of the “Setia Hebat” has increased the group’s fleet to 28 units. Its fleet under management and operation will increase to 38 units by end of 2010.

On December 15th, in yard number 79 at Bergen Yard's Fosen shipyard, “Boa Thalassa”, was named and delivered to Norwegian operator Boa Offshore. The ship is the first ship in the world purpose-built for the electromagnetic seismic surveys of the type developed by EMGS for so-called “seabed logging”.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

18

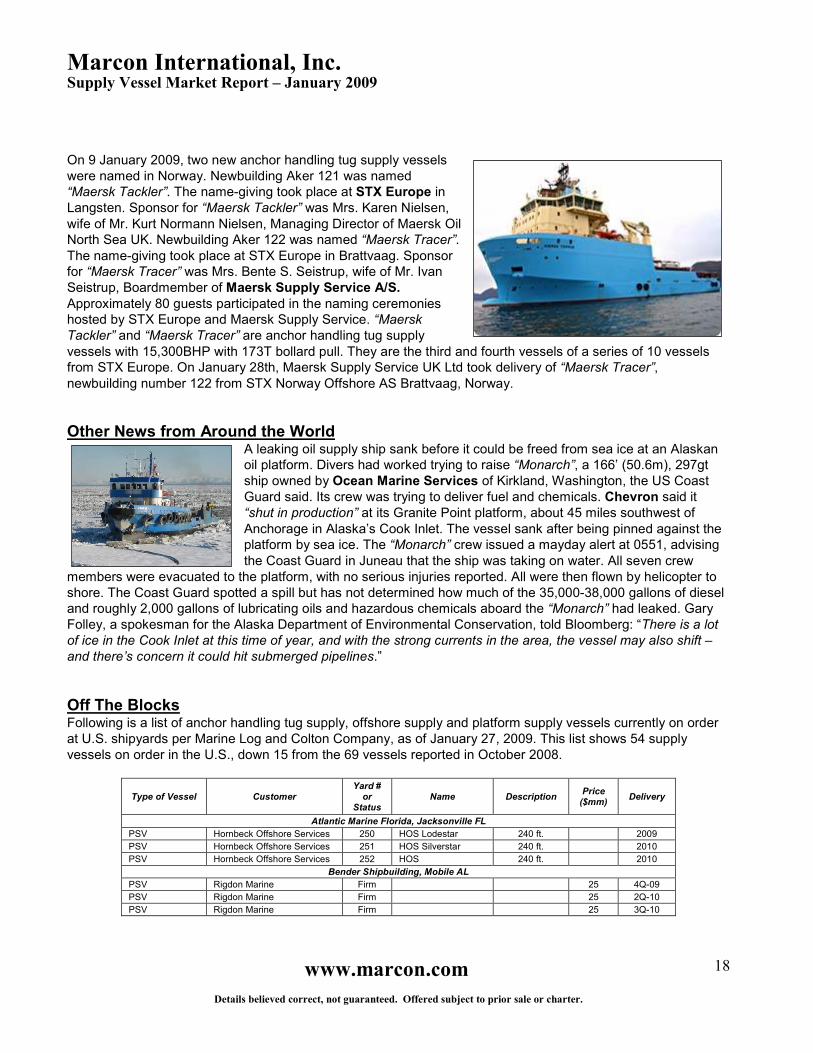

On 9 January 2009, two new anchor handling tug supply vessels were named in Norway. Newbuilding Aker 121 was named “Maersk Tackler”. The name-giving took place at STX Europe in Langsten. Sponsor for “Maersk Tackler” was Mrs. Karen Nielsen, wife of Mr. Kurt Normann Nielsen, Managing Director of Maersk Oil North Sea UK. Newbuilding Aker 122 was named “Maersk Tracer”. The name-giving took place at STX Europe in Brattvaag. Sponsor for “Maersk Tracer” was Mrs. Bente S. Seistrup, wife of Mr. Ivan Seistrup, Boardmember of Maersk Supply Service A/S. Approximately 80 guests participated in the naming ceremonies hosted by STX Europe and Maersk Supply Service. “Maersk Tackler” and “Maersk Tracer” are anchor handling tug supply vessels with 15,300BHP with 173T bollard pull. They are the third and fourth vessels of a series of 10 vessels from STX Europe. On January 28th, Maersk Supply Service UK Ltd took delivery of “Maersk Tracer”, newbuilding number 122 from STX Norway Offshore AS Brattvaag, Norway.

Other News from Around the World A leaking oil supply ship sank before it could be freed from sea ice at an Alaskan oil platform. Divers had worked trying to raise “Monarch”, a 166’ (50.6m), 297gt ship owned by Ocean Marine Services of Kirkland, Washington, the US Coast Guard said. Its crew was trying to deliver fuel and chemicals. Chevron said it “shut in production” at its Granite Point platform, about 45 miles southwest of Anchorage in Alaska’s Cook Inlet. The vessel sank after being pinned against the platform by sea ice. The “Monarch” crew issued a mayday alert at 0551, advising the Coast Guard in Juneau that the ship was taking on water. All seven crew

members were evacuated to the platform, with no serious injuries reported. All were then flown by helicopter to shore. The Coast Guard spotted a spill but has not determined how much of the 35,000-38,000 gallons of diesel and roughly 2,000 gallons of lubricating oils and hazardous chemicals aboard the “Monarch” had leaked. Gary Folley, a spokesman for the Alaska Department of Environmental Conservation, told Bloomberg: “There is a lot of ice in the Cook Inlet at this time of year, and with the strong currents in the area, the vessel may also shift – and there’s concern it could hit submerged pipelines.”

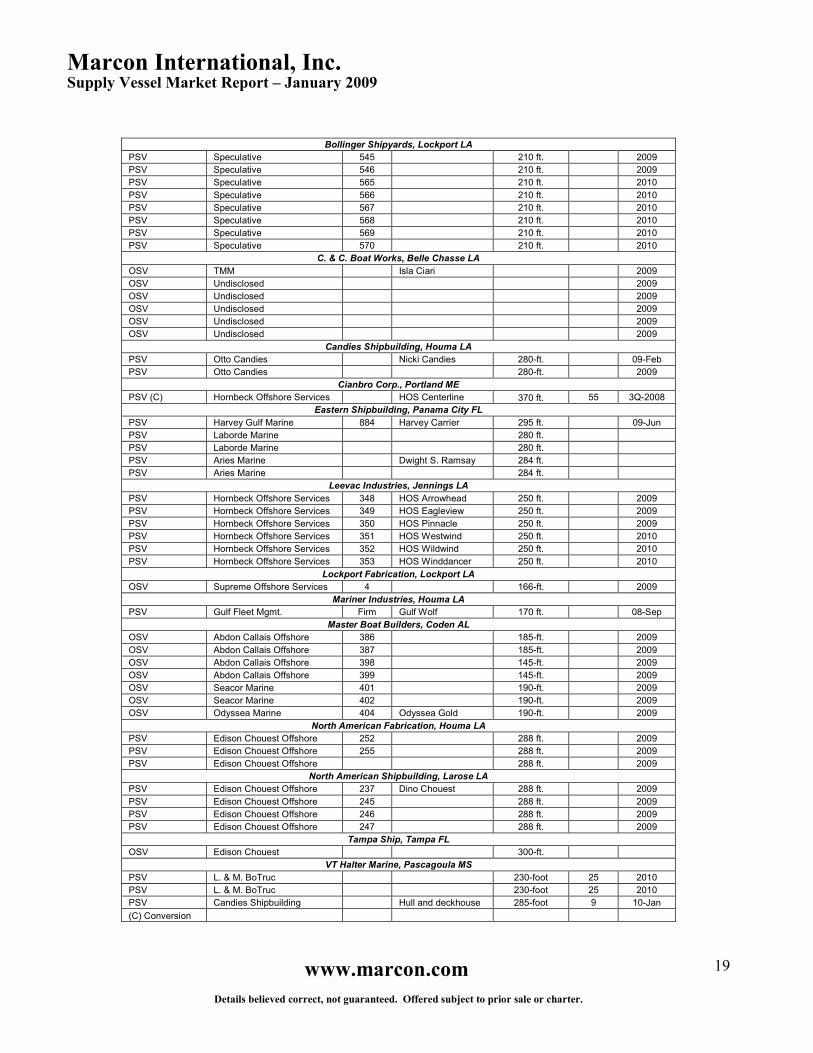

Off The Blocks Following is a list of anchor handling tug supply, offshore supply and platform supply vessels currently on order at U.S. shipyards per Marine Log and Colton Company, as of January 27, 2009. This list shows 54 supply vessels on order in the U.S., down 15 from the 69 vessels reported in October 2008.

Type of Vessel Customer Yard # or

Status Name Description

Price ($mm)

Delivery

Atlantic Marine Florida, Jacksonville FL

PSV Hornbeck Offshore Services 250 HOS Lodestar 240 ft. 2009

PSV Hornbeck Offshore Services 251 HOS Silverstar 240 ft. 2010

PSV Hornbeck Offshore Services 252 HOS 240 ft. 2010

Bender Shipbuilding, Mobile AL

PSV Rigdon Marine Firm 25 4Q-09

PSV Rigdon Marine Firm 25 2Q-10

PSV Rigdon Marine Firm 25 3Q-10

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

19

Bollinger Shipyards, Lockport LA

PSV Speculative 545 210 ft. 2009

PSV Speculative 546 210 ft. 2009

PSV Speculative 565 210 ft. 2010

PSV Speculative 566 210 ft. 2010

PSV Speculative 567 210 ft. 2010

PSV Speculative 568 210 ft. 2010

PSV Speculative 569 210 ft. 2010

PSV Speculative 570 210 ft. 2010

C. & C. Boat Works, Belle Chasse LA

OSV TMM Isla Ciari 2009

OSV Undisclosed 2009

OSV Undisclosed 2009

OSV Undisclosed 2009

OSV Undisclosed 2009

OSV Undisclosed 2009

Candies Shipbuilding, Houma LA

PSV Otto Candies Nicki Candies 280-ft. 09-Feb

PSV Otto Candies 280-ft. 2009

Cianbro Corp., Portland ME

PSV (C) Hornbeck Offshore Services HOS Centerline 370 ft. 55 3Q-2008

Eastern Shipbuilding, Panama City FL

PSV Harvey Gulf Marine 884 Harvey Carrier 295 ft. 09-Jun

PSV Laborde Marine 280 ft.

PSV Laborde Marine 280 ft.

PSV Aries Marine Dwight S. Ramsay 284 ft.

PSV Aries Marine 284 ft.

Leevac Industries, Jennings LA

PSV Hornbeck Offshore Services 348 HOS Arrowhead 250 ft. 2009

PSV Hornbeck Offshore Services 349 HOS Eagleview 250 ft. 2009

PSV Hornbeck Offshore Services 350 HOS Pinnacle 250 ft. 2009

PSV Hornbeck Offshore Services 351 HOS Westwind 250 ft. 2010

PSV Hornbeck Offshore Services 352 HOS Wildwind 250 ft. 2010

PSV Hornbeck Offshore Services 353 HOS Winddancer 250 ft. 2010

Lockport Fabrication, Lockport LA

OSV Supreme Offshore Services 4 166-ft. 2009

Mariner Industries, Houma LA

PSV Gulf Fleet Mgmt. Firm Gulf Wolf 170 ft. 08-Sep

Master Boat Builders, Coden AL

OSV Abdon Callais Offshore 386 185-ft. 2009

OSV Abdon Callais Offshore 387 185-ft. 2009

OSV Abdon Callais Offshore 398 145-ft. 2009

OSV Abdon Callais Offshore 399 145-ft. 2009

OSV Seacor Marine 401 190-ft. 2009

OSV Seacor Marine 402 190-ft. 2009

OSV Odyssea Marine 404 Odyssea Gold 190-ft. 2009

North American Fabrication, Houma LA

PSV Edison Chouest Offshore 252 288 ft. 2009

PSV Edison Chouest Offshore 255 288 ft. 2009

PSV Edison Chouest Offshore 288 ft. 2009

North American Shipbuilding, Larose LA

PSV Edison Chouest Offshore 237 Dino Chouest 288 ft. 2009

PSV Edison Chouest Offshore 245 288 ft. 2009

PSV Edison Chouest Offshore 246 288 ft. 2009

PSV Edison Chouest Offshore 247 288 ft. 2009

Tampa Ship, Tampa FL

OSV Edison Chouest 300-ft.

VT Halter Marine, Pascagoula MS

PSV L. & M. BoTruc 230-foot 25 2010

PSV L. & M. BoTruc 230-foot 25 2010

PSV Candies Shipbuilding Hull and deckhouse 285-foot 9 10-Jan

(C) Conversion

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

20

Corporate News Tidewater Inc. of New Orleans third quarter net earnings for the period ended December 31, 2008, were $117 million on revenues of $362.3 million. For the same quarter last year, net earnings were $89.4 million on revenues of $314.2 million. The immediately preceding quarter ended September 30, 2008, had net earnings of $95.4 million on revenues of $346.8 million. During Summer 2008, vessel day rates trended higher as the supply/demand fundamentals in the GOM offshore vessel market tightened due to an increase in drilling activity resulting from high natural gas prices, which reached the $13.00 per Mcf range in July 2008 and which have since deflated to the $5.00 to $6.00 per Mcf range. In September 2008, Hurricanes Gustav and Ike hit the Louisiana and Texas coasts. The U.S. Minerals Management Service reported that damage caused by the two storms to the energy industry infrastructure in the U.S. Gulf and along the coast was not as extensive as the damage caused by Hurricanes Katrina and Rita in calendar year ‘05 and that the damage that was sustained would take several months to repair. The market for offshore support vessels was tight prior to the two storms, and drilling operators discovered shortages in available-for-work offshore vessels operating in the U.S. Gulf. Prior to the storms, all of Tidewater’s available-for-work U.S.-based vessels were working at relatively full utilization and, since the storms, two of the stacked vessels underwent a drydock and recertification in order to meet increased post-hurricane market demand. Demand for vessels was brisk for the majority of the quarter ended December 31, 2008, but demand has waned in the last weeks of the quarter due to normal winter slowdowns and the winding down of repair work. The deepwater offshore energy market is a growing segment of the energy market. Worldwide rig construction escalated in the past few years as rig owners capitalized on the high worldwide demand for drilling. Approximately 700 new-build vessels (PSVs and AHTSs only) are under construction and expected to be delivered worldwide over the next four years as reported by ODS-Petrodata. The current worldwide fleet of these classes of vessels approximates 2,000 vessels. An increase in vessel capacity could have the effect of lowering charter rates. However, the worldwide offshore marine vessel industry has a large number of aging vessels nearing or exceeding estimated economic lives. These older vessels could potentially retire from the market if the cost of extending the vessels’ lives is not economically justifiable. Although the future attrition rate of these aging vessels cannot be accurately predicted, Tidewater believes that the retirement of a portion of these aging vessels would likely mitigate the potential effects of new-build vessels being delivered. However, it is unknown at this time how the global recession will influence the utilization of equipment currently in existence and ultimate delivery of new drilling rigs, floating production units and vessels currently under construction. Commodity prices, and particularly the price of crude oil and natural gas, are critical factors in E&P companies’ decisions to retain drilling rigs in the Gulf of Mexico market or mobilize rigs to more profitable international markets. Prices for crude oil and natural gas have fallen dramatically from their respective peaks achieved in calendar year 2008 due to the global recession that resulted in a marked decline in worldwide demand for oil and gas. Inventory levels for natural gas rose higher than expected over the summer and were near full capacity at the end of the season as was the case during calendar years ‘06 and ‘07. Production shut-ins in the offshore drilling market caused by Hurricanes Gustav and Ike eased some of the production growth in natural gas but were insufficient to offset strong land-based natural gas drilling. Analysts estimate that inventory levels for natural gas will remain high even during the winter drawdown season due to the strong supply growth and declining demand resulting from the economic recession. High inventory levels for natural gas and low demand do not bode well for future increases in natural gas pricing. Given the historical strong correlation between commodity prices, drilling and exploration activity and demand for vessels, if gas prices remain weak during calendar year 2009, Tidewater expects that its ability to maintain the utilization rates and day rates for its vessels in that market will be under stress. However, because gas pricing and gas demand have been extremely volatile, as evidenced by the sharp increases and declines experienced during calendar year 2008, management is unable to predict with confidence what the actual experience will be in calendar year 2009.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

21

Oil and gas industry analysts reporting in 2009 E&P expenditures (both land-based & offshore) surveys that global capital expenditures budgets for E&P are forecast to decrease by approx. 12% over calendar year 2008 levels. Surveys forecast that international capital spending budgets will decline a modest 6% while North American capital spending budgets are forecast to decrease approx. 26% due to the uncertainty in commodity pricing, tight credit markets and the global recession. These budgets were based on an approx. $58 average price per barrel of oil and an approx. $6.35 per mcf average natural gas price for calendar 2009. Additionally, the International Energy Agency announced in January 2009 that it decreased its forecast of oil demand by 11.7% from its October 2008 forecast. U.S.-based vessel revenues for the quarter ended December 31, 2008, increased a modest 1% compared to the same period in fiscal year 2008, due to higher utilization rates on all vessel classes operating in the U.S. market and to higher total average day rates resulting from a stronger Gulf of Mexico market during the comparative periods despite fewer vessels operating due to transfer of vessels to international markets. Average day rates on the U.S-based towing supply/supply vessels increased approx. 34% during the quarter ended December31, 2008 compared to the same period in fiscal 2008. Utilization rates on this same class of vessel increased approx. 3% during the quarter. Average day rates for Tidewater’s international towing supply/supply class of vessels increased approx. 22% for the quarter ended December 31, 2008 while utilization rates decreased approx. 3%.

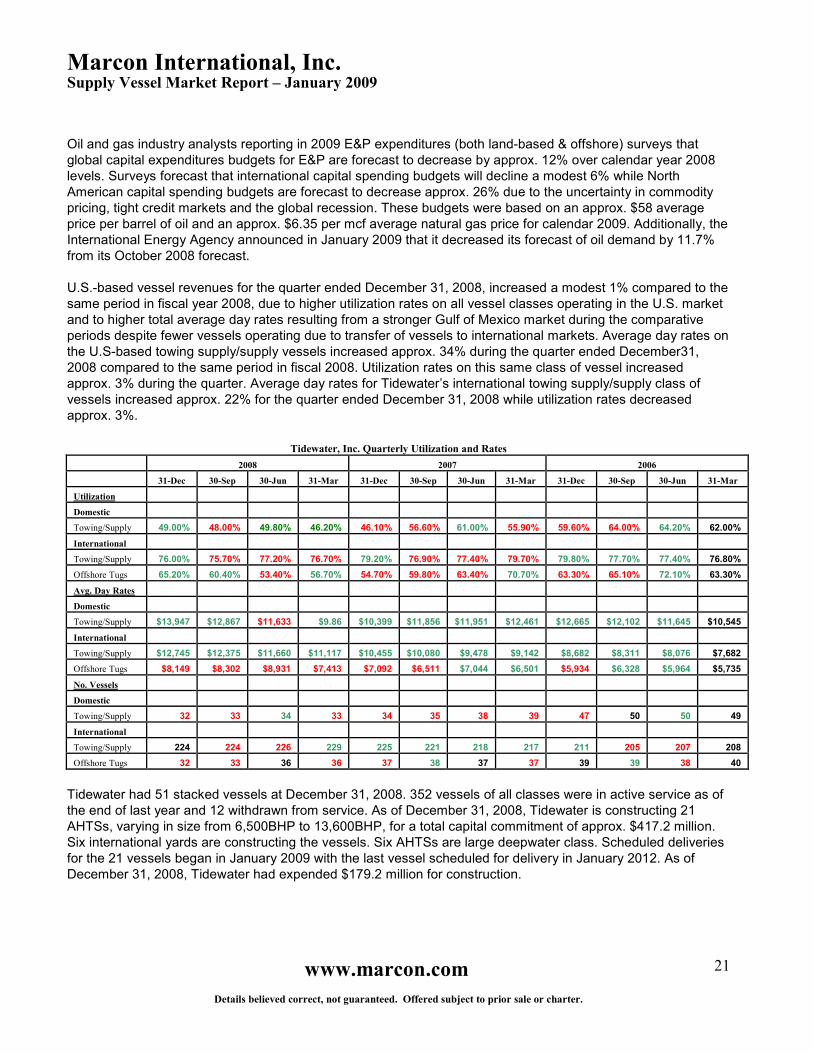

Tidewater, Inc. Quarterly Utilization and Rates

2008 2007 2006

31-Dec 30-Sep 30-Jun 31-Mar 31-Dec 30-Sep 30-Jun 31-Mar 31-Dec 30-Sep 30-Jun 31-Mar

Utilization

Domestic

Towing/Supply 49.00% 48.00% 49.80% 46.20% 46.10% 56.60% 61.00% 55.90% 59.60% 64.00% 64.20% 62.00%

International

Towing/Supply 76.00% 75.70% 77.20% 76.70% 79.20% 76.90% 77.40% 79.70% 79.80% 77.70% 77.40% 76.80%

Offshore Tugs 65.20% 60.40% 53.40% 56.70% 54.70% 59.80% 63.40% 70.70% 63.30% 65.10% 72.10% 63.30%

Avg. Day Rates

Domestic

Towing/Supply $13,947 $12,867 $11,633 $9.86 $10,399 $11,856 $11,951 $12,461 $12,665 $12,102 $11,645 $10,545

International

Towing/Supply $12,745 $12,375 $11,660 $11,117 $10,455 $10,080 $9,478 $9,142 $8,682 $8,311 $8,076 $7,682

Offshore Tugs $8,149 $8,302 $8,931 $7,413 $7,092 $6,511 $7,044 $6,501 $5,934 $6,328 $5,964 $5,735

No. Vessels

Domestic

Towing/Supply 32 33 34 33 34 35 38 39 47 50 50 49

International

Towing/Supply 224 224 226 229 225 221 218 217 211 205 207 208

Offshore Tugs 32 33 36 36 37 38 37 37 39 39 38 40

Tidewater had 51 stacked vessels at December 31, 2008. 352 vessels of all classes were in active service as of the end of last year and 12 withdrawn from service. As of December 31, 2008, Tidewater is constructing 21 AHTSs, varying in size from 6,500BHP to 13,600BHP, for a total capital commitment of approx. $417.2 million. Six international yards are constructing the vessels. Six AHTSs are large deepwater class. Scheduled deliveries for the 21 vessels began in January 2009 with the last vessel scheduled for delivery in January 2012. As of December 31, 2008, Tidewater had expended $179.2 million for construction.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

22

Day-to-day operating costs are generally affected by inflation. However, because the industry requires specialized goods and services, general economic inflationary trends may not affect operating costs. The major impact on operating costs is the level of offshore exploration, development and production spending by energy E&P companies. As spending increases, prices of goods and services used by the energy industry and energy services industry will increase. Due to an increase in business activity resulting from strong global oil & gas fundamentals in the past few years, the competitive market for experienced crew exerted upward pressure on wages, increasing operating expenses. In addition, strong fundamentals also increased activity at shipyards worldwide, which led to increased pricing for repair work and new construction. Also, the price of steel increased dramatically due to increased worldwide demand. The price of steel is high by historical standards, although prices moderated some since calendar year 2005. If the price of steel continues to rise, the cost of new vessels will result in higher capital expenditures and depreciation expenses which will reduce future operating profits, unless day rates increase. However, the financial crisis and resulting global recession dramatically reduced global demand for all commodities, including steel, which resulted in lower commodity prices. Steel market participants have already announced a reduction in steel output during 2009 which could stabilize the price of steel, although that will depend upon many factors that relate to worldwide demand.

Seacor Holdings Inc. announced net income for the fourth quarter ended December 31, 2008 of $71.8 million on operating revenues of $454.9 million. Net income for the preceding quarter ended September 30, 2008

was $75.6 million on operating revenues of $437.6 million. For the quarter ended December 31, 2007, net income was $67.9 million on operating revenues of $363.1 million. Offshore Marine Services Operating income in the fourth quarter was $97.2 million on operating revenues of $186.0 million compared with operating income of $84.5 million on operating revenues of $196.9 million in the preceding quarter. Fourth quarter results included $34.2 million in gains on asset dispositions compared with $13.5 million in gains in the preceding quarter. Excluding the impact of gains on asset dispositions, operating income in the fourth quarter was $7.9 million lower than in the preceding quarter. The decrease was primarily due to lower time charter revenues, principally in the U.S. Gulf of Mexico where Seacor’s AHTS vessels undertook fewer rig moves. Operating revenues were also lower due to net fleet dispositions and a decline in the value of the pound sterling. In the fourth quarter, $3.1 million of vessel charter hire billed to two customers was deferred due to uncertainty regarding the collection of the amounts in question. SEACOR will recognize the amounts as operating revenues as cash is collected. Overall operating expenses were lower primarily as a result of lower wage expense and lower charter-in expense. Administrative and general expenses were higher primarily due to a $1.1 million increase in the provision for doubtful accounts for receivables due from the two customers noted above. The number of days available for charter in the fourth quarter decreased by 263, or 1.7%, primarily as a result of a net reduction in fleet count. Overall utilization decreased from 87.7% to 87.5% and overall average day rates were lower at $12,402 per day compared with $13,161 per day in the preceding quarter. As of December 31, 2008, Seacor owned 20 AHTS, 16 mini-supply, 29 standby-safety and 41 supply/towing supply vessels. Seacor’s unfunded capital commitments as of December 31, 2008, consisted primarily of offshore marine vessels, helicopters, inland river barges and inland river towboats and totaled $157.4 million, of which $113.3 million is payable during 2009 and the balance payable through 2010. Of the total unfunded capital commitments, $22.6 million may be terminated without further liability other than the payment of liquidated damages of $1.8 million in the aggregate. As of December 31, 2008, SEACOR held balances of cash, cash equivalents, restricted cash, marketable securities, construction reserve funds and title XI reserve funds totaling $655.8 million.

Marcon International, Inc. Supply Vessel Market Report – January 2009

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale or charter.

23