Embed Size (px)

Citation preview

MOJAKOE

March 25

2013 Dilarang memperbanyak MOJAKOE ini tanpa seijin

SPA FEUI. Download MOJAKOE dan SPA Mentoring

di : www.spa-feui.com

Akuntansi Manajemen

MOJAKOE

Question I : Cost-Volume-Profit Analysis

PT. Newstar is distributors that sells ‘Me-Pad’ a brand new type of gadget at an exhibition.

Newstar plans to sell ‘Me-Pad’ for $500 each. The company purchase Me-Pad from

manufacturer at $350 each, with the privilege of returning any unsold units for a full refund.

The exhibition offer Newstar with 2 alternatives :

1. A fixed payment of %5,000 during exhibition

2. 10% of total revenues earned during exhibition

Assume Newstar incur no other costs.

Required :

1. Calculate BEP in unit for option 1 and 2

2. At what level of unit sold will Newstar earn the same operating income under either

option? For what range of unit sales will Newstar prefer option 1 over option 2?

3. Calculate margin of safety and degree of operating leverage at sales of $100 units for

two rental option

4. Give your analysis on your answer to requirement 3

Question II : Master Budget!

PT. ABC is a local t-shirt manufacturer. In 2012 management projected that they can sell

8000 units of various types t-shirt. Data required to develop this year’s budget is as follows :

a. Finished goods inventory on January 1 is 100 units, each costing Rp15.000.

Management planned to maintain its current level of finished goods inventory at the

end of 2012.

b. Inputs include the following :

Price Quantity Inventory at Jan 1

Fabric Rp 10.000 per meter 1 meter per shirt 75 meter at Rp9.000

Dye Rp 1.000 per ounce 3 ounces per shirt 100 ounces at Rp750

Labor Rp 10.000 per DLH 0.25 DLH per shirt

c. Overhead costs for 2012 are estimated for fixed and variable components: (measured

in direct labor hour (DLH)). Overhead are allocated to finish product using direct

labor hour as the cost allocation base.

Fixed Cost Component Variable Cost Component

Supplies - Rp 500

Power - Rp 1.000

Maintenance Rp 20.000.000 -

Supervision Rp 60.000.000 -

Depreciation Rp 75.000.000 -

Other Rp 15.000.000 -

MOJAKOE

Required :

Prepare a partial annual operating budget for the year 2012 :

(1) Production Budget

(2) Direct Material Usage Budget

(3) Direct Labor Cost Budget

(4) Manufacturing Overhead Cost Budget

(5) Cost of Goods Sold Budget

Question III : Cash Budget

Champion Hardware is a hardware wholesaler. All sales are credit sales with the term of

payment 5/10, n/end of month. Information about the store’s operation follows :

December 2011 sales amounted to $500.000

Sales are budgeted at $540.000 for January 2012 and $500.000 for February 2012

Collection are expected to be 30% in the month of sale within the discount period,

30% also in month of sale but after the discount period, and 38% in the month

following the sale. Two percent of sales are expected to uncollectible. Bad debt

expense is recognized monthly.

Cost of goods sold is 75% of sales.

A total of 70% of the merchandise for resale is purchased in the month prior to the

month of the sale, and 30% is purchased in the month of the sale. Payment for

merchandise is made in the month following the purchase. The company always take

the benefit of 2% discount offered by the supplier for payment before the 10th of the

month.

Annual operating expenses for 2012 is budgeted for $1.600.000. From this amount

$1.000.000 is fixed cost which include $200.000 depreciation expense. The remaining

operating expense is considered variable. All operating expense will be paid as

incurred. The budgeted annual operating expenses is based on the expected annual

sales $6.000.000

The company’s balance sheet of December 31,2011 is as follows :

Champion Hardware Inc.

Balance Sheet

December 31, 2011

Assets

Cash $ 44.000

Account Receivable (net $75.000 allowance for uncollectible accounts) $ 190.000

Inventory $ 280.000

Property and Equipment (net of $1.180.000 accumulated depreciation) $ 1.724.000

Total Assets $ 2.238.000

MOJAKOE

Liabilities and Stockholder’s Equity

Account Payable $ 324.000

Common Stock $ 1.590.000

Retained Earning $ 324.000

Total Liabilities and Stockholder’s Equity $ 2.238.000

Required :

1. Prepare a cash budget for January 2012 in detail (show your computation) to show the

expected cash balance at the end of January 2012.

2. Suppose you are preparing a budgeted balance sheet as of January 31, 2012. Please

show the balance for the following account :

a. Cash

b. Account Receivable

c. Account Payable

3. If the company has minimum cash balance policy of $40.000, how this will affect

your answer.

Question IV : Flexible Budgets, Direct-Cost Variances, and Overhead-Cost Variances

The following information is provided to assist you in evaluating the performance of

Odysius, Inc. :

Actual Cost:

Direct Material Purchased and Used $ 188,700 (102,000 pounds)

Direct Labor $ 140,000 (10,700 hours)

Manufacturing Overhead $ 204,000 (61% is variable)

Standard Cost per Unit:

Direct Material $ 1.65x5 pounds per unit output

Direct Labor $ 14.00 per hour x 0.5 hour/unit

Variabel Overhead $ 11.90 per direct-labor hour

Production Budget:

Direct Material $ 165,000

Direct Labor $ 140,000

Manufacturing Labor $ 199,000

Variable overhead is applied on the bases of direct – labor hours. The company’s actual

production and sales was 21,000 units, which was 17,5% market share. Average selling price

MOJAKOE

was $38. The company expected to get 20% market share. The exacted market for this

product is 100.000 units. Its selling price is budgeted at $40.

Required :

Prepare a complete various report and analysis consists of :

a. Direct-material price and quantity variances

b. Direct-labor rate&efficiency variances

c. Variable-overhead spending&efficiency variances

d. Fixed-overhead spending & production volume variances

e. Sales price variance

f. Sales volume variance

g. Sales quantity variance

h. Market Share and Market Size Variance

i. The flexible budget variance

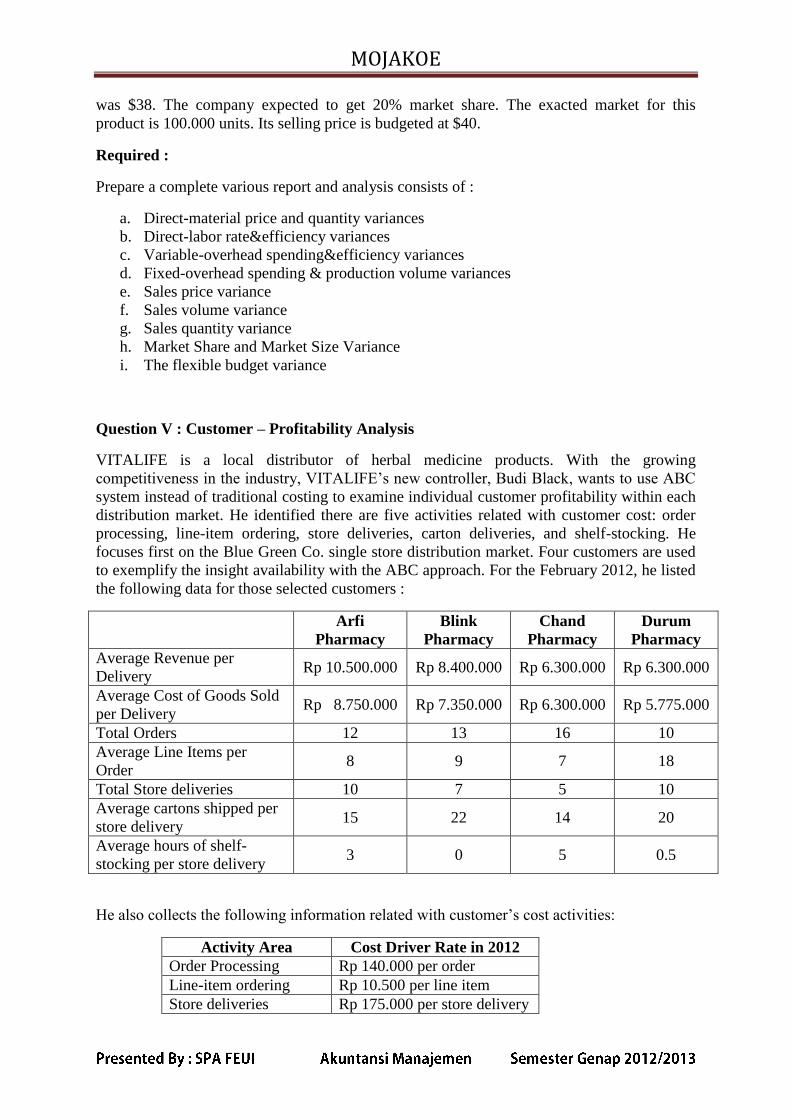

Question V : Customer – Profitability Analysis

VITALIFE is a local distributor of herbal medicine products. With the growing

competitiveness in the industry, VITALIFE’s new controller, Budi Black, wants to use ABC

system instead of traditional costing to examine individual customer profitability within each

distribution market. He identified there are five activities related with customer cost: order

processing, line-item ordering, store deliveries, carton deliveries, and shelf-stocking. He

focuses first on the Blue Green Co. single store distribution market. Four customers are used

to exemplify the insight availability with the ABC approach. For the February 2012, he listed

the following data for those selected customers :

Arfi

Pharmacy

Blink

Pharmacy

Chand

Pharmacy

Durum

Pharmacy

Average Revenue per

Delivery Rp 10.500.000 Rp 8.400.000 Rp 6.300.000 Rp 6.300.000

Average Cost of Goods Sold

per Delivery Rp 8.750.000 Rp 7.350.000 Rp 6.300.000 Rp 5.775.000

Total Orders 12 13 16 10

Average Line Items per

Order 8 9 7 18

Total Store deliveries 10 7 5 10

Average cartons shipped per

store delivery 15 22 14 20

Average hours of shelf-

stocking per store delivery 3 0 5 0.5

He also collects the following information related with customer’s cost activities:

Activity Area Cost Driver Rate in 2012

Order Processing Rp 140.000 per order

Line-item ordering Rp 10.500 per line item

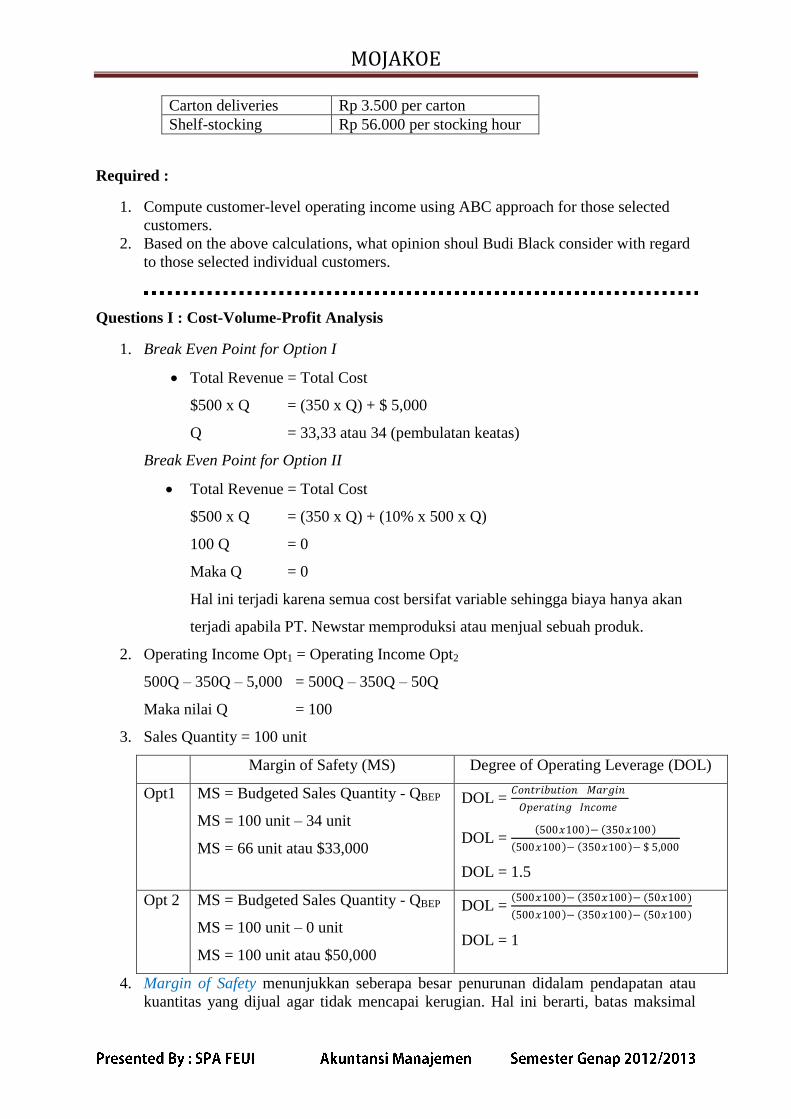

Store deliveries Rp 175.000 per store delivery

MOJAKOE

Carton deliveries Rp 3.500 per carton

Shelf-stocking Rp 56.000 per stocking hour

Required :

1. Compute customer-level operating income using ABC approach for those selected

customers.

2. Based on the above calculations, what opinion shoul Budi Black consider with regard

to those selected individual customers.

Questions I : Cost-Volume-Profit Analysis

1. Break Even Point for Option I

Total Revenue = Total Cost

$500 x Q = (350 x Q) + $ 5,000

Q = 33,33 atau 34 (pembulatan keatas)

Break Even Point for Option II

Total Revenue = Total Cost

$500 x Q = (350 x Q) + (10% x 500 x Q)

100 Q = 0

Maka Q = 0

Hal ini terjadi karena semua cost bersifat variable sehingga biaya hanya akan

terjadi apabila PT. Newstar memproduksi atau menjual sebuah produk.

2. Operating Income Opt1 = Operating Income Opt2

500Q – 350Q – 5,000 = 500Q – 350Q – 50Q

Maka nilai Q = 100

3. Sales Quantity = 100 unit

Margin of Safety (MS) Degree of Operating Leverage (DOL)

Opt1 MS = Budgeted Sales Quantity - QBEP

MS = 100 unit – 34 unit

MS = 66 unit atau $33,000

DOL = 𝐶𝑜𝑛𝑡𝑟𝑖𝑏𝑢𝑡𝑖𝑜𝑛 𝑀𝑎𝑟𝑔𝑖𝑛

𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝐼𝑛𝑐𝑜𝑚𝑒

DOL = 500𝑥100 − 350𝑥100

500𝑥100 − 350𝑥100 − $ 5,000

DOL = 1.5

Opt 2 MS = Budgeted Sales Quantity - QBEP

MS = 100 unit – 0 unit

MS = 100 unit atau $50,000

DOL = 500𝑥100 − 350𝑥100 − (50𝑥100)

500𝑥100 − 350𝑥100 − (50𝑥100)

DOL = 1

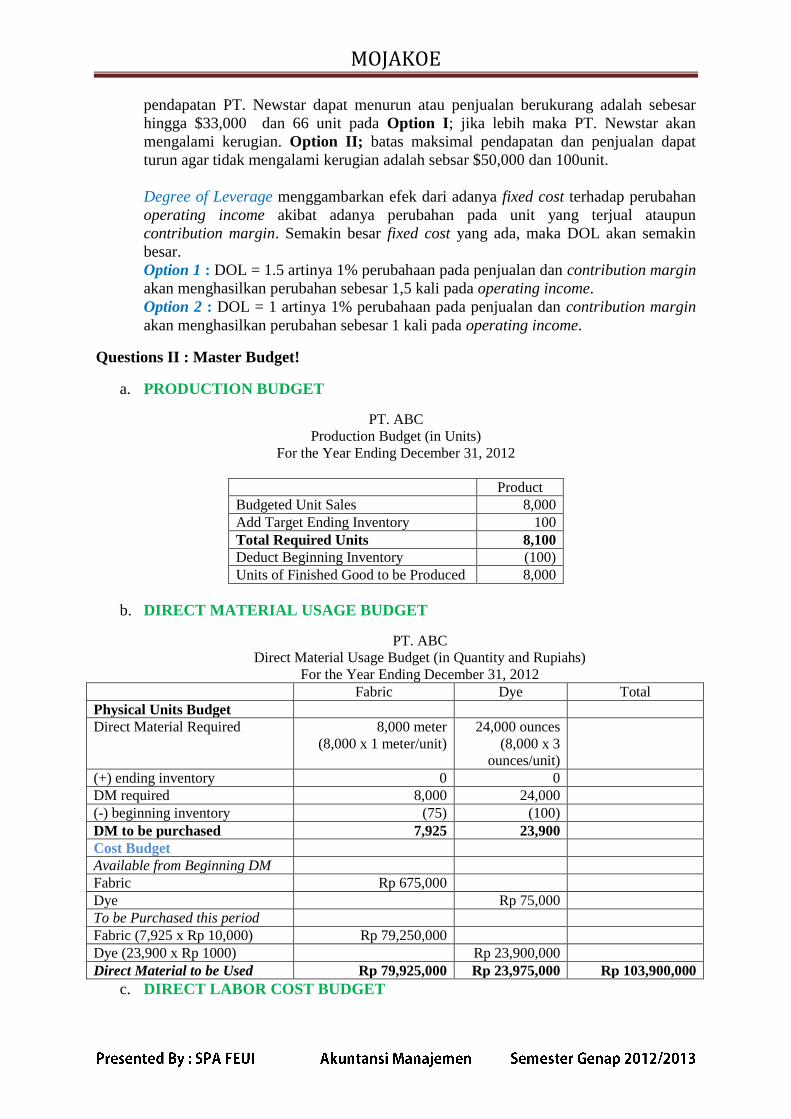

4. Margin of Safety menunjukkan seberapa besar penurunan didalam pendapatan atau

kuantitas yang dijual agar tidak mencapai kerugian. Hal ini berarti, batas maksimal

MOJAKOE

pendapatan PT. Newstar dapat menurun atau penjualan berukurang adalah sebesar

hingga $33,000 dan 66 unit pada Option I; jika lebih maka PT. Newstar akan

mengalami kerugian. Option II; batas maksimal pendapatan dan penjualan dapat

turun agar tidak mengalami kerugian adalah sebsar $50,000 dan 100unit.

Degree of Leverage menggambarkan efek dari adanya fixed cost terhadap perubahan

operating income akibat adanya perubahan pada unit yang terjual ataupun

contribution margin. Semakin besar fixed cost yang ada, maka DOL akan semakin

besar.

Option 1 : DOL = 1.5 artinya 1% perubahaan pada penjualan dan contribution margin

akan menghasilkan perubahan sebesar 1,5 kali pada operating income.

Option 2 : DOL = 1 artinya 1% perubahaan pada penjualan dan contribution margin

akan menghasilkan perubahan sebesar 1 kali pada operating income.

Questions II : Master Budget!

a. PRODUCTION BUDGET

PT. ABC

Production Budget (in Units)

For the Year Ending December 31, 2012

Product

Budgeted Unit Sales 8,000

Add Target Ending Inventory 100

Total Required Units 8,100

Deduct Beginning Inventory (100)

Units of Finished Good to be Produced 8,000

b. DIRECT MATERIAL USAGE BUDGET

PT. ABC

Direct Material Usage Budget (in Quantity and Rupiahs)

For the Year Ending December 31, 2012

Fabric Dye Total

Physical Units Budget

Direct Material Required 8,000 meter

(8,000 x 1 meter/unit)

24,000 ounces

(8,000 x 3

ounces/unit)

(+) ending inventory 0 0

DM required 8,000 24,000

(-) beginning inventory (75) (100)

DM to be purchased 7,925 23,900

Cost Budget

Available from Beginning DM

Fabric Rp 675,000

Dye Rp 75,000

To be Purchased this period

Fabric (7,925 x Rp 10,000) Rp 79,250,000

Dye (23,900 x Rp 1000) Rp 23,900,000

Direct Material to be Used Rp 79,925,000 Rp 23,975,000 Rp 103,900,000

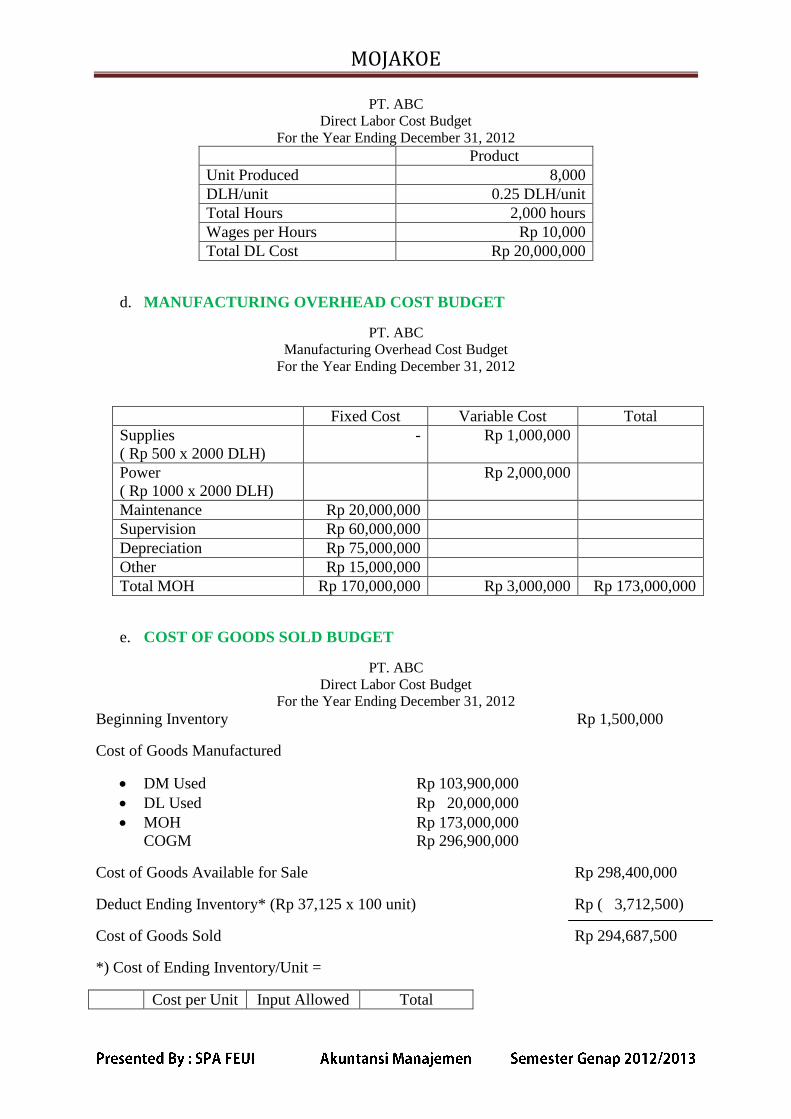

c. DIRECT LABOR COST BUDGET

MOJAKOE

PT. ABC

Direct Labor Cost Budget

For the Year Ending December 31, 2012

Product

Unit Produced 8,000

DLH/unit 0.25 DLH/unit

Total Hours 2,000 hours

Wages per Hours Rp 10,000

Total DL Cost Rp 20,000,000

d. MANUFACTURING OVERHEAD COST BUDGET

PT. ABC

Manufacturing Overhead Cost Budget

For the Year Ending December 31, 2012

Fixed Cost Variable Cost Total

Supplies

( Rp 500 x 2000 DLH)

- Rp 1,000,000

Power

( Rp 1000 x 2000 DLH)

Rp 2,000,000

Maintenance Rp 20,000,000

Supervision Rp 60,000,000

Depreciation Rp 75,000,000

Other Rp 15,000,000

Total MOH Rp 170,000,000 Rp 3,000,000 Rp 173,000,000

e. COST OF GOODS SOLD BUDGET

PT. ABC

Direct Labor Cost Budget

For the Year Ending December 31, 2012

Beginning Inventory Rp 1,500,000

Cost of Goods Manufactured

DM Used Rp 103,900,000

DL Used Rp 20,000,000

MOH Rp 173,000,000

COGM Rp 296,900,000

Cost of Goods Available for Sale Rp 298,400,000

Deduct Ending Inventory* (Rp 37,125 x 100 unit) Rp ( 3,712,500)

Cost of Goods Sold Rp 294,687,500

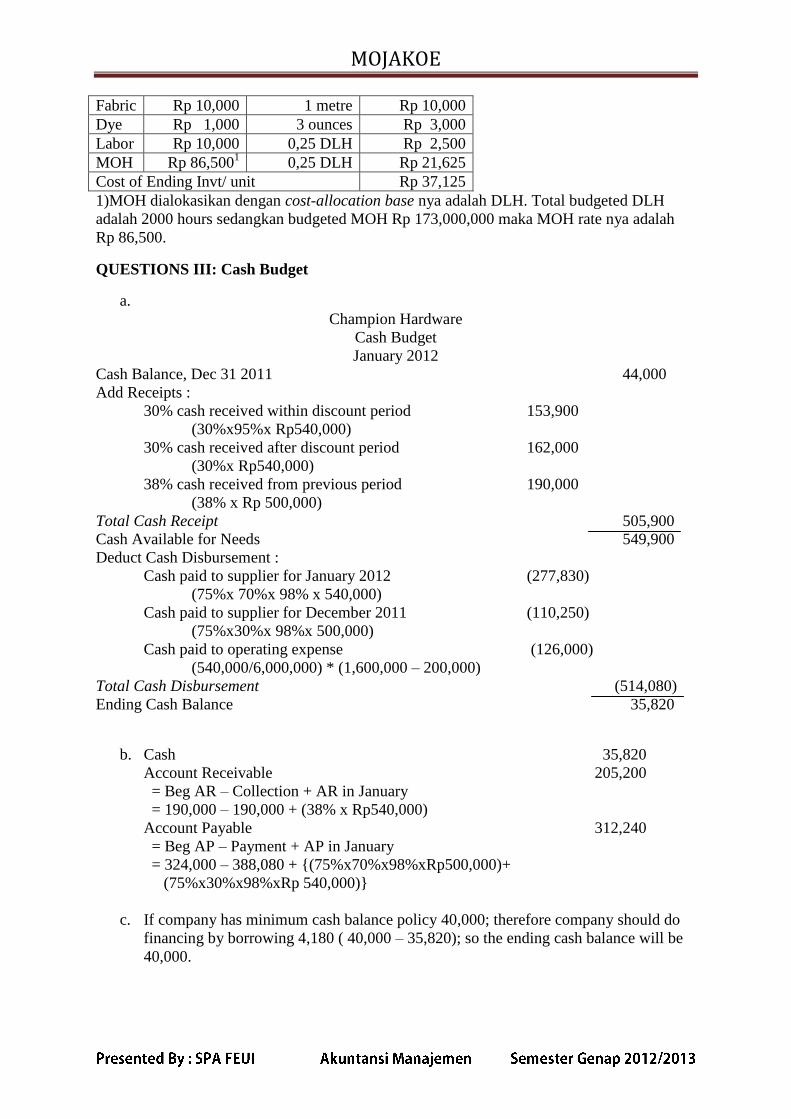

*) Cost of Ending Inventory/Unit =

Cost per Unit Input Allowed Total

MOJAKOE

Fabric Rp 10,000 1 metre Rp 10,000

Dye Rp 1,000 3 ounces Rp 3,000

Labor Rp 10,000 0,25 DLH Rp 2,500

MOH Rp 86,5001 0,25 DLH Rp 21,625

Cost of Ending Invt/ unit Rp 37,125

1)MOH dialokasikan dengan cost-allocation base nya adalah DLH. Total budgeted DLH

adalah 2000 hours sedangkan budgeted MOH Rp 173,000,000 maka MOH rate nya adalah

Rp 86,500.

QUESTIONS III: Cash Budget

a.

Champion Hardware

Cash Budget

January 2012

Cash Balance, Dec 31 2011 44,000

Add Receipts :

30% cash received within discount period 153,900

(30%x95%x Rp540,000)

30% cash received after discount period 162,000

(30%x Rp540,000)

38% cash received from previous period 190,000

(38% x Rp 500,000)

Total Cash Receipt 505,900

Cash Available for Needs 549,900

Deduct Cash Disbursement :

Cash paid to supplier for January 2012 (277,830)

(75%x 70%x 98% x 540,000)

Cash paid to supplier for December 2011 (110,250)

(75%x30%x 98%x 500,000)

Cash paid to operating expense (126,000)

(540,000/6,000,000) * (1,600,000 – 200,000)

Total Cash Disbursement (514,080)

Ending Cash Balance 35,820

b. Cash 35,820

Account Receivable 205,200

= Beg AR – Collection + AR in January

= 190,000 – 190,000 + (38% x Rp540,000)

Account Payable 312,240

= Beg AP – Payment + AP in January

= 324,000 – 388,080 + {(75%x70%x98%xRp500,000)+

(75%x30%x98%xRp 540,000)}

c. If company has minimum cash balance policy 40,000; therefore company should do

financing by borrowing 4,180 ( 40,000 – 35,820); so the ending cash balance will be

40,000.

MOJAKOE

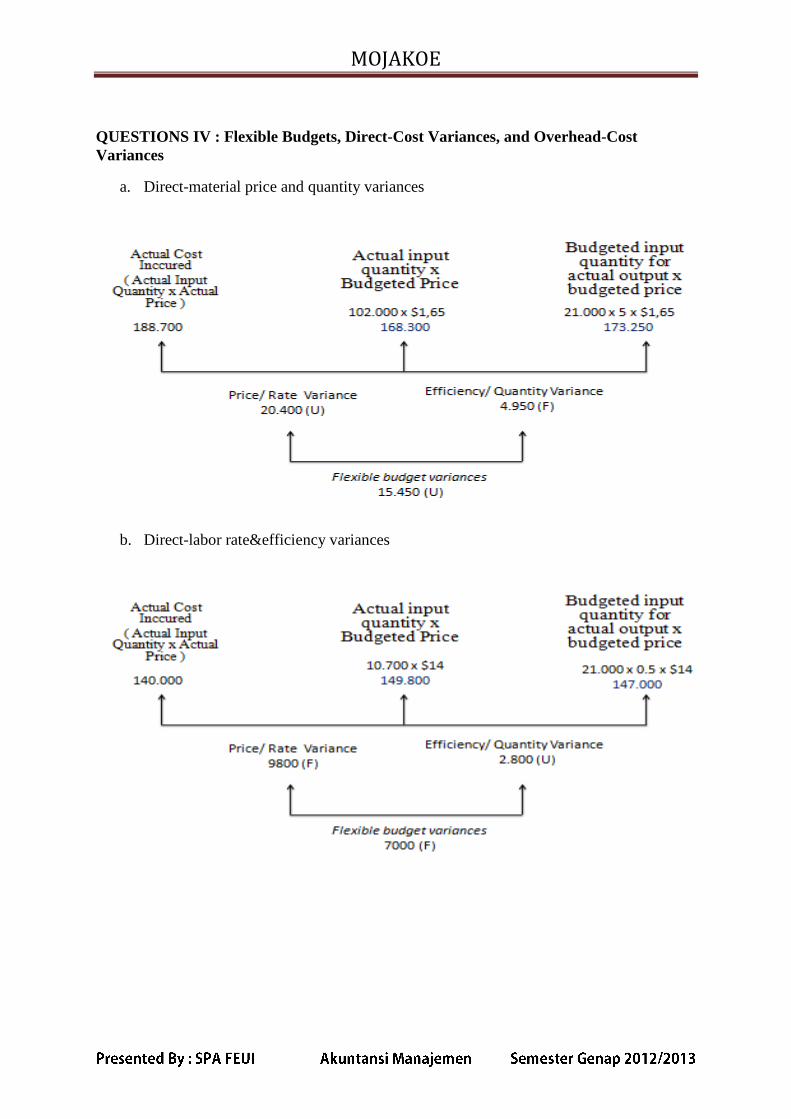

QUESTIONS IV : Flexible Budgets, Direct-Cost Variances, and Overhead-Cost

Variances

a. Direct-material price and quantity variances

b. Direct-labor rate&efficiency variances

MOJAKOE

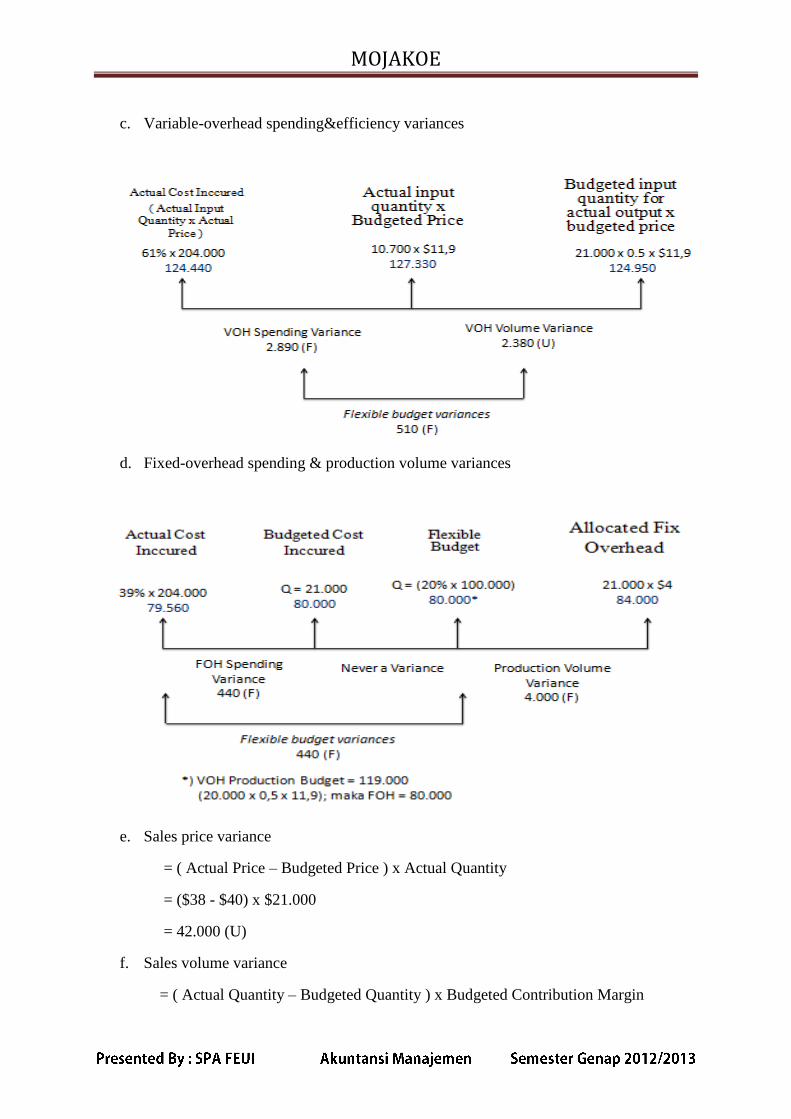

c. Variable-overhead spending&efficiency variances

d. Fixed-overhead spending & production volume variances

e. Sales price variance

= ( Actual Price – Budgeted Price ) x Actual Quantity

= ($38 - $40) x $21.000

= 42.000 (U)

f. Sales volume variance

= ( Actual Quantity – Budgeted Quantity ) x Budgeted Contribution Margin

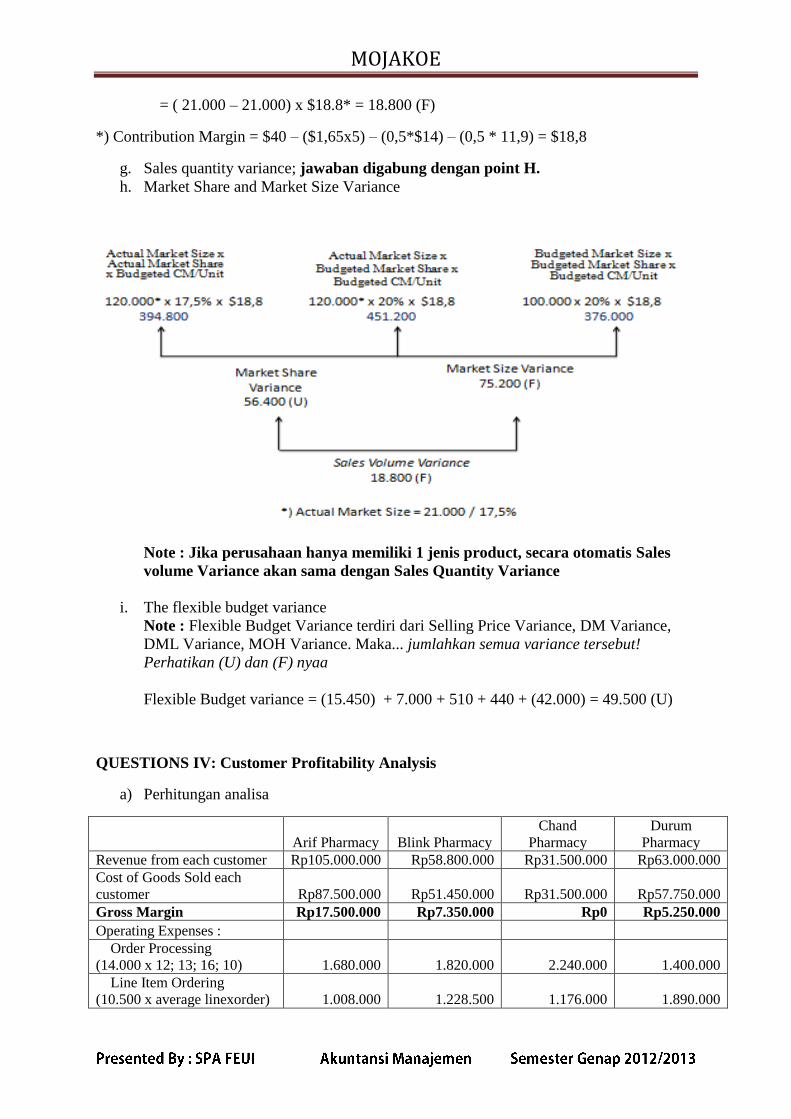

MOJAKOE

= ( 21.000 – 21.000) x $18.8* = 18.800 (F)

*) Contribution Margin = $40 – ($1,65x5) – (0,5*$14) – (0,5 * 11,9) = $18,8

g. Sales quantity variance; jawaban digabung dengan point H.

h. Market Share and Market Size Variance

Note : Jika perusahaan hanya memiliki 1 jenis product, secara otomatis Sales

volume Variance akan sama dengan Sales Quantity Variance

i. The flexible budget variance

Note : Flexible Budget Variance terdiri dari Selling Price Variance, DM Variance,

DML Variance, MOH Variance. Maka... jumlahkan semua variance tersebut!

Perhatikan (U) dan (F) nyaa

Flexible Budget variance = (15.450) + 7.000 + 510 + 440 + (42.000) = 49.500 (U)

QUESTIONS IV: Customer Profitability Analysis

a) Perhitungan analisa

Arif Pharmacy Blink Pharmacy Chand

Pharmacy Durum

Pharmacy Revenue from each customer Rp105.000.000 Rp58.800.000 Rp31.500.000 Rp63.000.000 Cost of Goods Sold each

customer Rp87.500.000 Rp51.450.000 Rp31.500.000 Rp57.750.000 Gross Margin Rp17.500.000 Rp7.350.000 Rp0 Rp5.250.000

Operating Expenses : Order Processing

(14.000 x 12; 13; 16; 10)

1.680.000

1.820.000

2.240.000

1.400.000 Line Item Ordering

(10.500 x average linexorder)

1.008.000

1.228.500

1.176.000

1.890.000

MOJAKOE

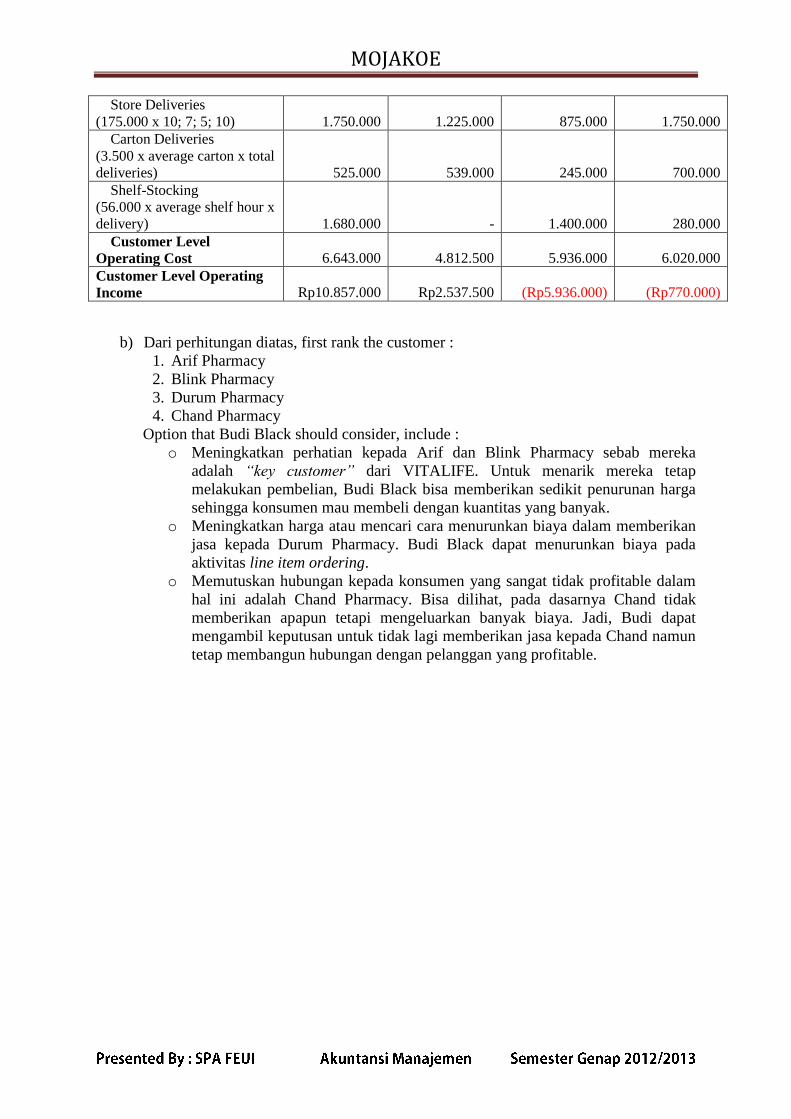

Store Deliveries

(175.000 x 10; 7; 5; 10)

1.750.000

1.225.000

875.000

1.750.000 Carton Deliveries

(3.500 x average carton x total

deliveries)

525.000

539.000

245.000

700.000 Shelf-Stocking

(56.000 x average shelf hour x

delivery)

1.680.000

-

1.400.000

280.000 Customer Level

Operating Cost

6.643.000

4.812.500

5.936.000

6.020.000 Customer Level Operating

Income Rp10.857.000 Rp2.537.500 (Rp5.936.000) (Rp770.000)

b) Dari perhitungan diatas, first rank the customer :

1. Arif Pharmacy

2. Blink Pharmacy

3. Durum Pharmacy

4. Chand Pharmacy

Option that Budi Black should consider, include :

o Meningkatkan perhatian kepada Arif dan Blink Pharmacy sebab mereka

adalah “key customer” dari VITALIFE. Untuk menarik mereka tetap

melakukan pembelian, Budi Black bisa memberikan sedikit penurunan harga

sehingga konsumen mau membeli dengan kuantitas yang banyak.

o Meningkatkan harga atau mencari cara menurunkan biaya dalam memberikan

jasa kepada Durum Pharmacy. Budi Black dapat menurunkan biaya pada

aktivitas line item ordering.

o Memutuskan hubungan kepada konsumen yang sangat tidak profitable dalam

hal ini adalah Chand Pharmacy. Bisa dilihat, pada dasarnya Chand tidak

memberikan apapun tetapi mengeluarkan banyak biaya. Jadi, Budi dapat

mengambil keputusan untuk tidak lagi memberikan jasa kepada Chand namun

tetap membangun hubungan dengan pelanggan yang profitable.

![TAX% Calculation Example - canon-ebm.com.hk · SAKLAR PEMBULATAN – Digunakan untuk pembulatan [5/4], atau pembulatan ke bawah [ ] terhadap digit desimal yang telah dipilih sebelumnya](https://img.pdfslide.us/doc/110x75/5d574d3988c9934f278bd1b0/tax-calculation-example-canon-ebmcomhk-saklar-pembulatan-digunakan.jpg)

![P23-DTSC DECIMAL POINT SELECTOR SWITCH … (ASA)… · DECIMAL POINT SELECTOR SWITCH – Used for round-up [ ] , round-off [5/4], ... pembulatan ke bawah [ ] terhadap digit desimal](https://img.pdfslide.us/doc/110x75/5b0a8b487f8b9a0b0f8bd986/p23-dtsc-decimal-point-selector-switch-asadecimal-point-selector-switch-used.jpg)