Embed Size (px)

Citation preview

Refer to pages 51-52 for Important Disclosures, including Analyst's Certification. For Important Disclosures on the stocks discussed in this report, please go to http://researchglobal.bmocapitalmarkets.com/Company_Disclosure_Public.asp.

Fadi Chamoun, CFA*Transport – Rails416-359-6775

Jason Granger, CA, CFA*Transport – Trucking & Logistics416-359-4293

Sal Guatieri*Senior Economist416-359-5295

Wayne HoodRetail – Broadlines/Hardlines404-926-1590

Gerrick L. JohnsonToys & Leisure212-883-5192

Phillip Juhan, CFARestaurants404-926-1599

Jeffrey B. LogsdonGaming, Media, & Entertainment213-228-2234

Stephen MacLeod, CFA*Consumer Special Situations416-359-8069

Connie M. ManeatyHousehold & Personal Care Products212-885-4004

John MorrisRetail – Apparel & Specialty212-885-4016

Amit Sharma, CFAFood & Beverage212-885-4132

Karen ShortFood Retailing212-885-4123

Peter Sklar, CA*Auto Parts416-359-5188

Kenneth B. Zaslow, CFAFood & Ag Products212-885-4017

$5 Gas?March 21, 2012

BMO RESEARCH ROUNDTABLE

*Employee of BMO Nesbitt Burns Inc.; otherwise, employee of BMO Capital Markets Corp.

Financial GroupA member of BMO January 4, 2012

Electric Utilities BMO Capital Markets

2

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

3

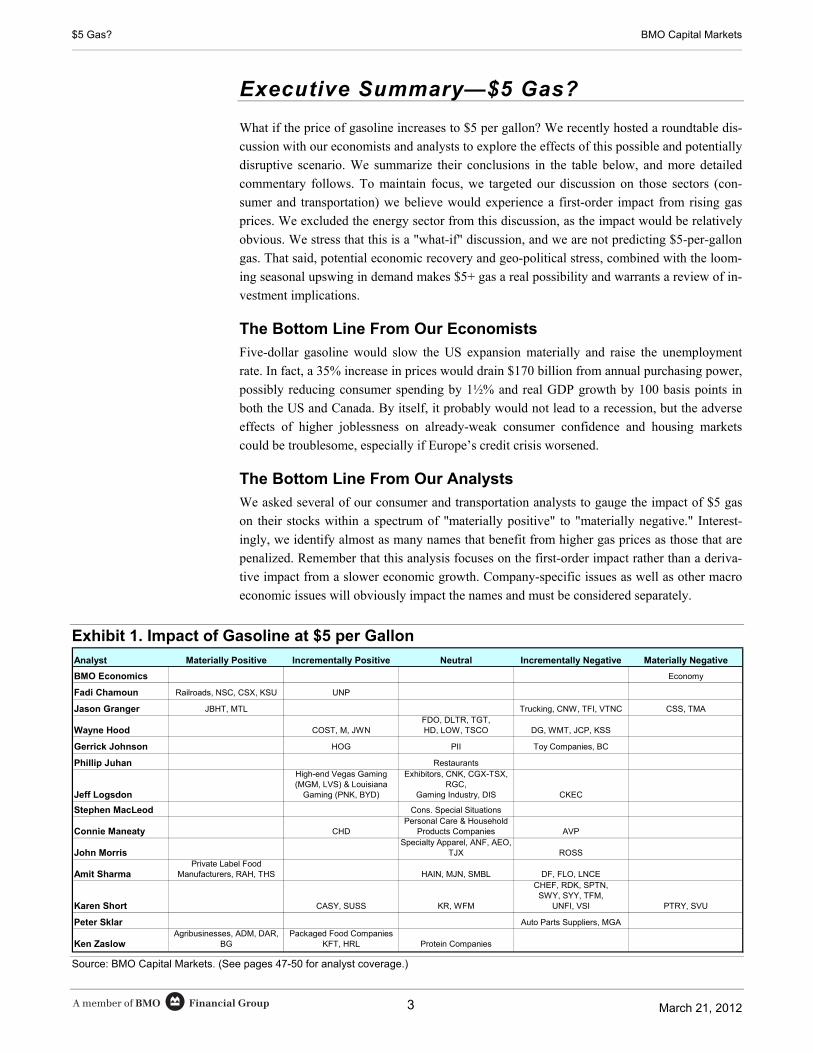

Executive Summary—$5 Gas?

What if the price of gasoline increases to $5 per gallon? We recently hosted a roundtable dis-

cussion with our economists and analysts to explore the effects of this possible and potentially

disruptive scenario. We summarize their conclusions in the table below, and more detailed

commentary follows. To maintain focus, we targeted our discussion on those sectors (con-

sumer and transportation) we believe would experience a first-order impact from rising gas

prices. We excluded the energy sector from this discussion, as the impact would be relatively

obvious. We stress that this is a "what-if" discussion, and we are not predicting $5-per-gallon

gas. That said, potential economic recovery and geo-political stress, combined with the loom-

ing seasonal upswing in demand makes $5+ gas a real possibility and warrants a review of in-

vestment implications.

The Bottom Line From Our Economists

Five-dollar gasoline would slow the US expansion materially and raise the unemployment

rate. In fact, a 35% increase in prices would drain $170 billion from annual purchasing power,

possibly reducing consumer spending by 1½% and real GDP growth by 100 basis points in

both the US and Canada. By itself, it probably would not lead to a recession, but the adverse

effects of higher joblessness on already-weak consumer confidence and housing markets

could be troublesome, especially if Europe’s credit crisis worsened.

The Bottom Line From Our Analysts

We asked several of our consumer and transportation analysts to gauge the impact of $5 gas

on their stocks within a spectrum of "materially positive" to "materially negative." Interest-

ingly, we identify almost as many names that benefit from higher gas prices as those that are

penalized. Remember that this analysis focuses on the first-order impact rather than a deriva-

tive impact from a slower economic growth. Company-specific issues as well as other macro

economic issues will obviously impact the names and must be considered separately.

Exhibit 1. Impact of Gasoline at $5 per Gallon

Analyst Materially Positive Incrementally Positive Neutral Incrementally Negative Materially Negative

BMO Economics Economy

Fadi Chamoun Railroads, NSC, CSX, KSU UNP

Jason Granger JBHT, MTL Trucking, CNW, TFI, VTNC CSS, TMA

Wayne Hood COST, M, JWNFDO, DLTR, TGT, HD, LOW, TSCO DG, WMT, JCP, KSS

Gerrick Johnson HOG PII Toy Companies, BC

Phillip Juhan Restaurants

Jeff Logsdon

High-end Vegas Gaming (MGM, LVS) & Louisiana

Gaming (PNK, BYD)

Exhibitors, CNK, CGX-TSX, RGC,

Gaming Industry, DIS CKEC

Stephen MacLeod Cons. Special Situations

Connie Maneaty CHDPersonal Care & Household

Products Companies AVP

John MorrisSpecialty Apparel, ANF, AEO,

TJX ROSS

Amit SharmaPrivate Label Food

Manufacturers, RAH, THS HAIN, MJN, SMBL DF, FLO, LNCE

Karen Short CASY, SUSS KR, WFM

CHEF, RDK, SPTN, SWY, SYY, TFM,

UNFI, VSI PTRY, SVU

Peter Sklar Auto Parts Suppliers, MGA

Ken ZaslowAgribusinesses, ADM, DAR,

BGPackaged Food Companies

KFT, HRL Protein Companies Source: BMO Capital Markets. (See pages 47-50 for analyst coverage.)

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

4

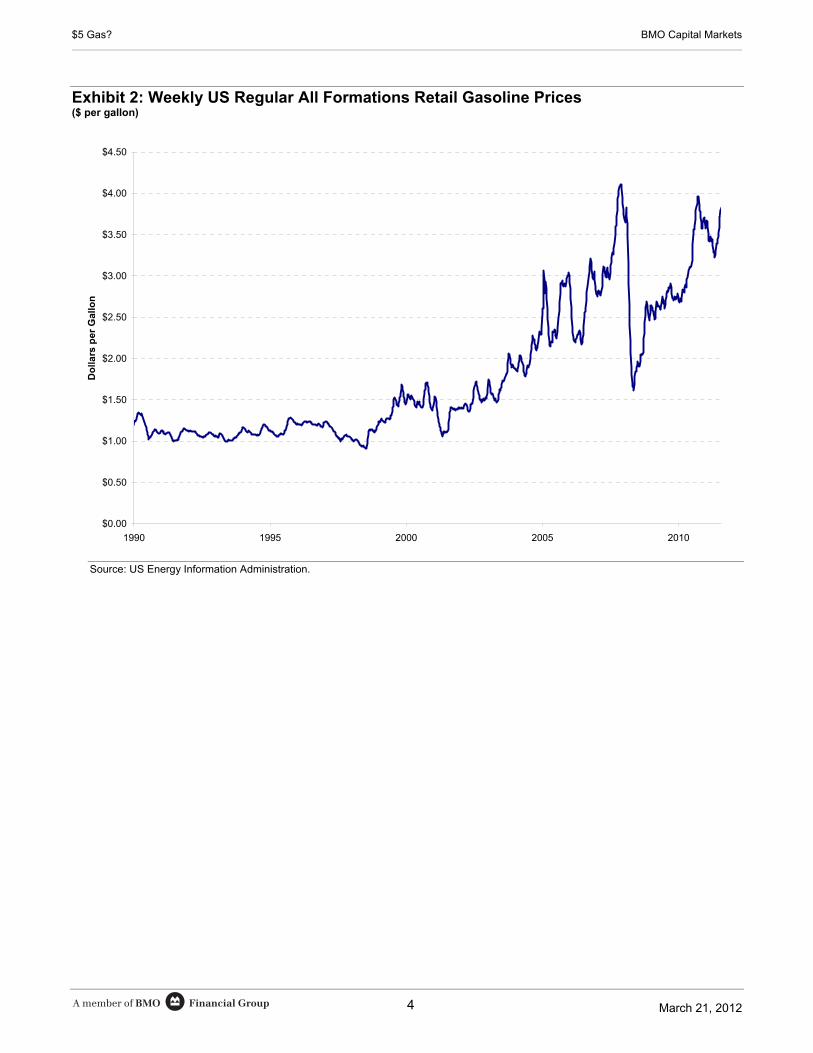

Exhibit 2: Weekly US Regular All Formations Retail Gasoline Prices ($ per gallon)

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

1990 1995 2000 2005 2010

Do

llars

per

Gal

lon

Source: US Energy Information Administration.

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

5

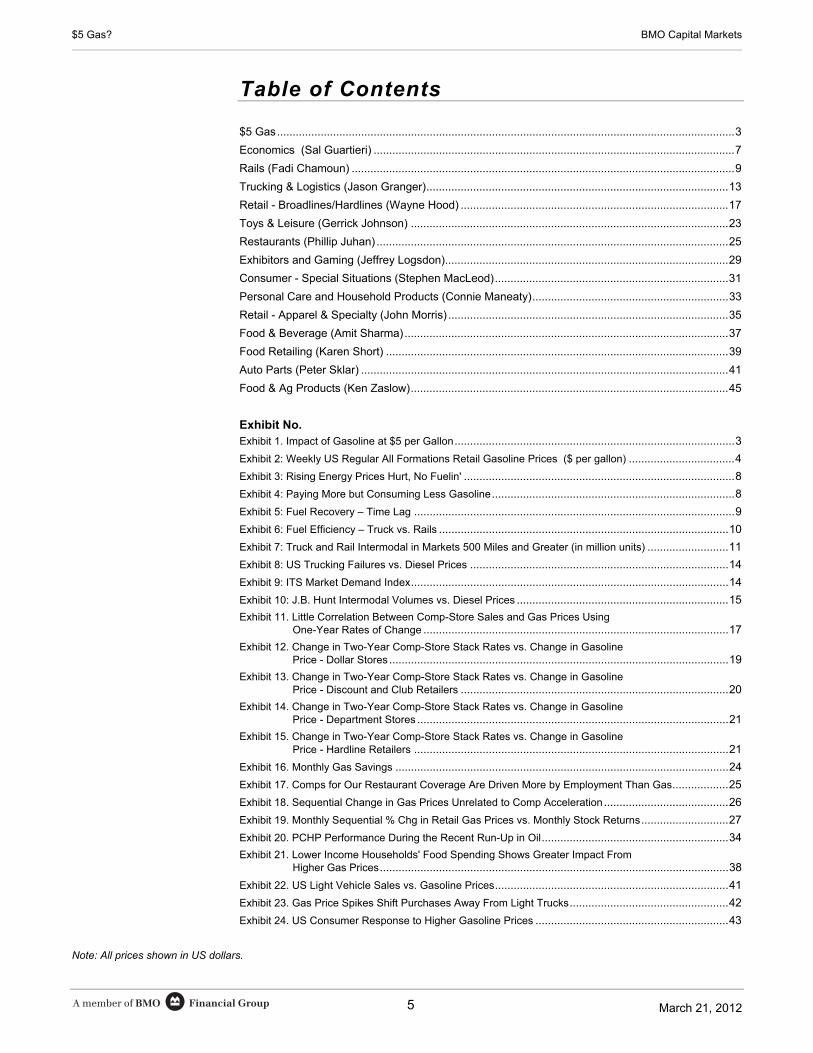

Table of Contents

$5 Gas...................................................................................................................................................3

Economics (Sal Guartieri) ....................................................................................................................7

Rails (Fadi Chamoun) ...........................................................................................................................9

Trucking & Logistics (Jason Granger).................................................................................................13

Retail - Broadlines/Hardlines (Wayne Hood) ......................................................................................17

Toys & Leisure (Gerrick Johnson) ......................................................................................................23

Restaurants (Phillip Juhan) .................................................................................................................25

Exhibitors and Gaming (Jeffrey Logsdon)...........................................................................................29

Consumer - Special Situations (Stephen MacLeod)...........................................................................31

Personal Care and Household Products (Connie Maneaty)...............................................................33

Retail - Apparel & Specialty (John Morris) ..........................................................................................35

Food & Beverage (Amit Sharma)........................................................................................................37

Food Retailing (Karen Short) ..............................................................................................................39

Auto Parts (Peter Sklar) ......................................................................................................................41

Food & Ag Products (Ken Zaslow)......................................................................................................45

Exhibit No. Exhibit 1. Impact of Gasoline at $5 per Gallon..........................................................................................3

Exhibit 2: Weekly US Regular All Formations Retail Gasoline Prices ($ per gallon) ..................................4

Exhibit 3: Rising Energy Prices Hurt, No Fuelin' .......................................................................................8

Exhibit 4: Paying More but Consuming Less Gasoline..............................................................................8

Exhibit 5: Fuel Recovery – Time Lag .......................................................................................................9

Exhibit 6: Fuel Efficiency – Truck vs. Rails .............................................................................................10

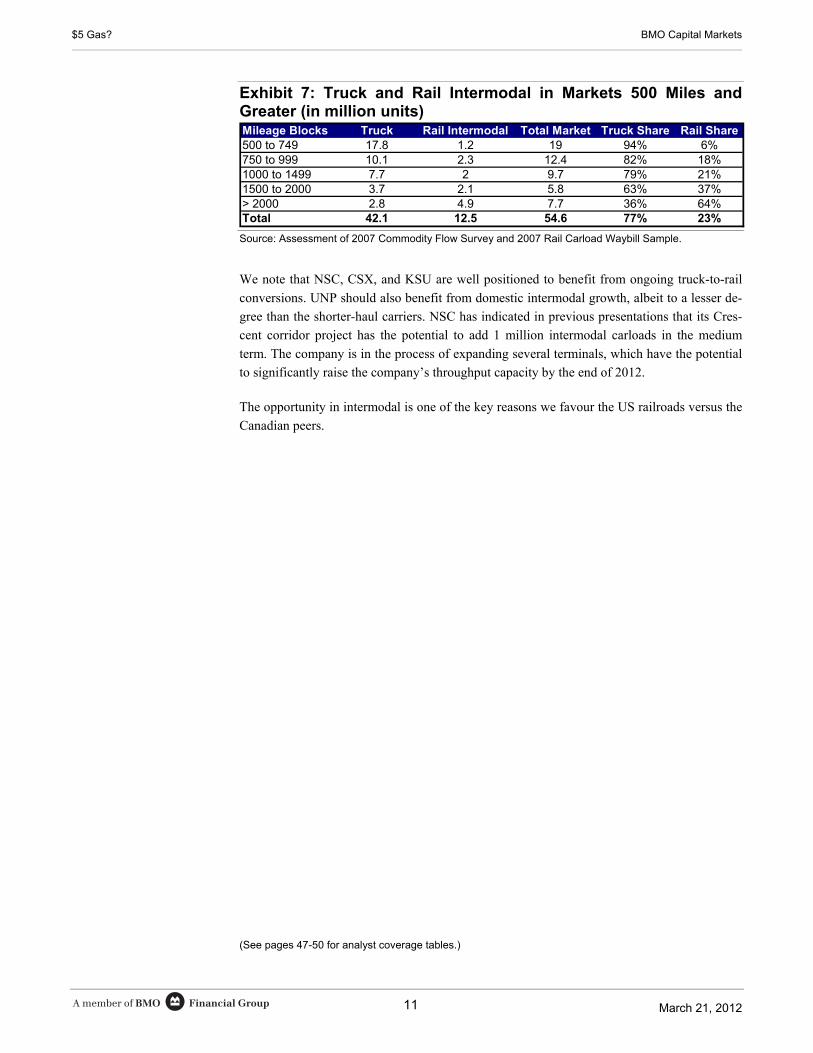

Exhibit 7: Truck and Rail Intermodal in Markets 500 Miles and Greater (in million units) ..........................11

Exhibit 8: US Trucking Failures vs. Diesel Prices ...................................................................................14

Exhibit 9: ITS Market Demand Index......................................................................................................14

Exhibit 10: J.B. Hunt Intermodal Volumes vs. Diesel Prices ....................................................................15

Exhibit 11. Little Correlation Between Comp-Store Sales and Gas Prices Using One-Year Rates of Change ..................................................................................................17

Exhibit 12. Change in Two-Year Comp-Store Stack Rates vs. Change in Gasoline Price - Dollar Stores .............................................................................................................19

Exhibit 13. Change in Two-Year Comp-Store Stack Rates vs. Change in Gasoline Price - Discount and Club Retailers ......................................................................................20

Exhibit 14. Change in Two-Year Comp-Store Stack Rates vs. Change in Gasoline Price - Department Stores ....................................................................................................21

Exhibit 15. Change in Two-Year Comp-Store Stack Rates vs. Change in Gasoline Price - Hardline Retailers .....................................................................................................21

Exhibit 16. Monthly Gas Savings ...........................................................................................................24

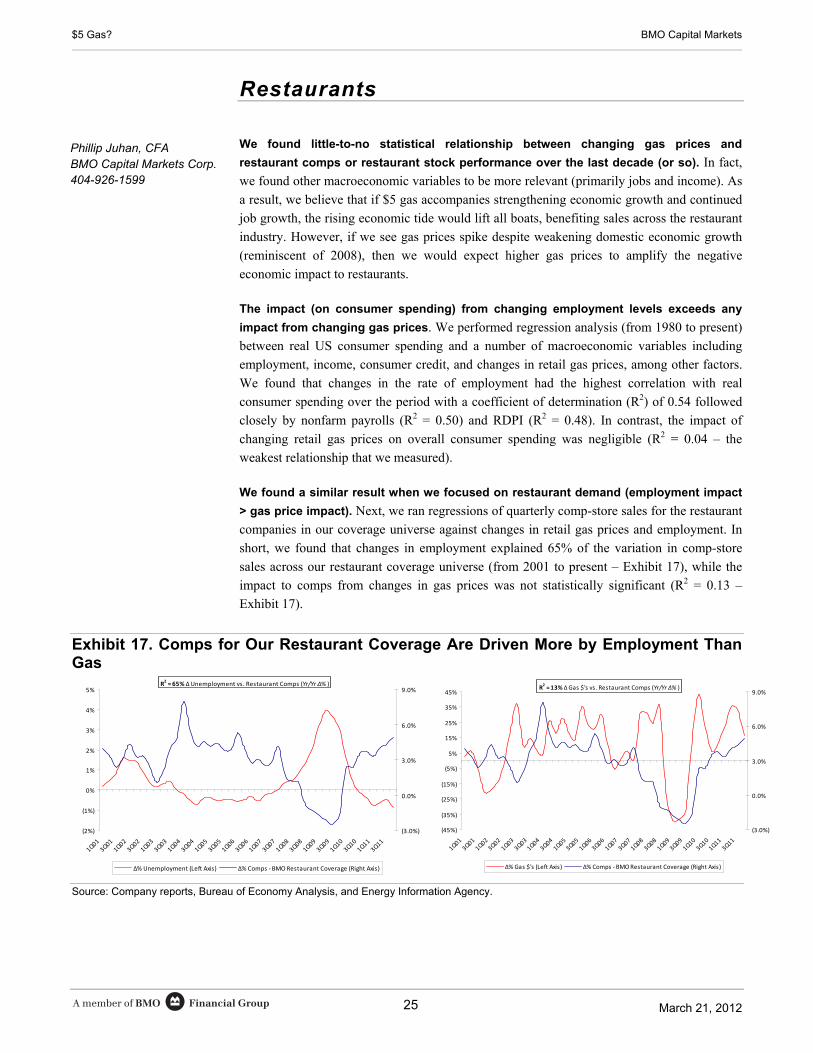

Exhibit 17. Comps for Our Restaurant Coverage Are Driven More by Employment Than Gas..................25

Exhibit 18. Sequential Change in Gas Prices Unrelated to Comp Acceleration........................................26

Exhibit 19. Monthly Sequential % Chg in Retail Gas Prices vs. Monthly Stock Returns............................27

Exhibit 20. PCHP Performance During the Recent Run-Up in Oil............................................................34

Exhibit 21. Lower Income Households' Food Spending Shows Greater Impact From Higher Gas Prices................................................................................................................38

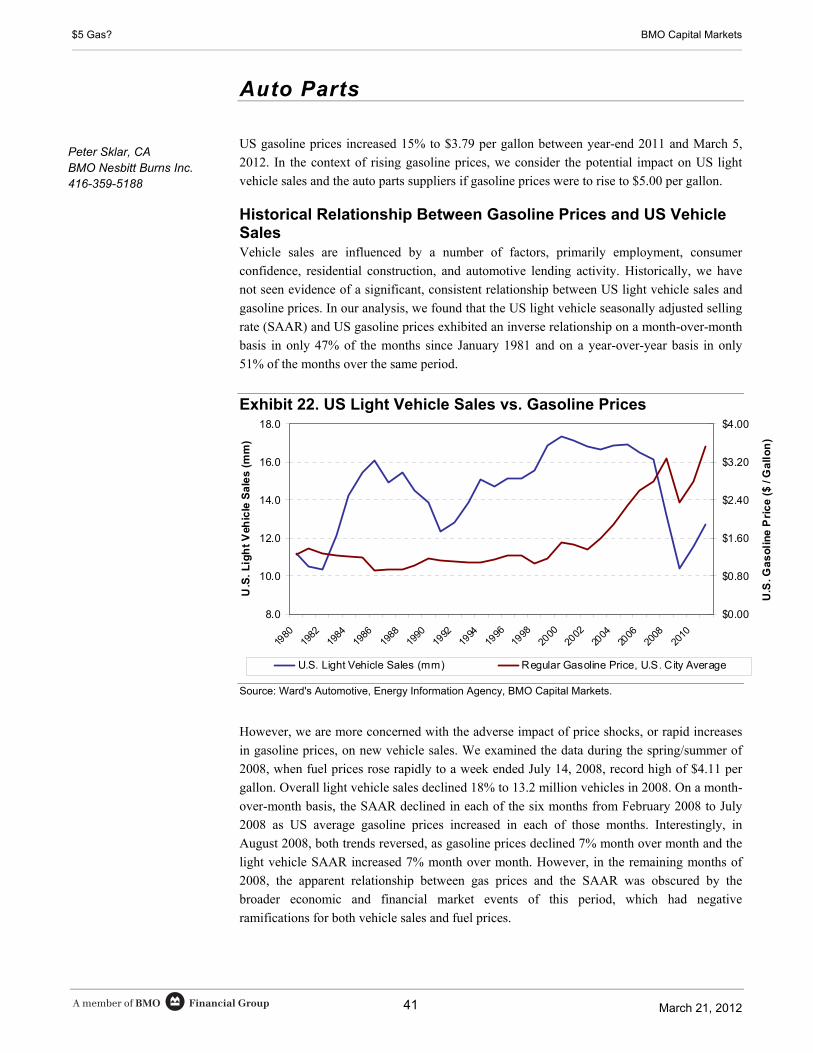

Exhibit 22. US Light Vehicle Sales vs. Gasoline Prices...........................................................................41

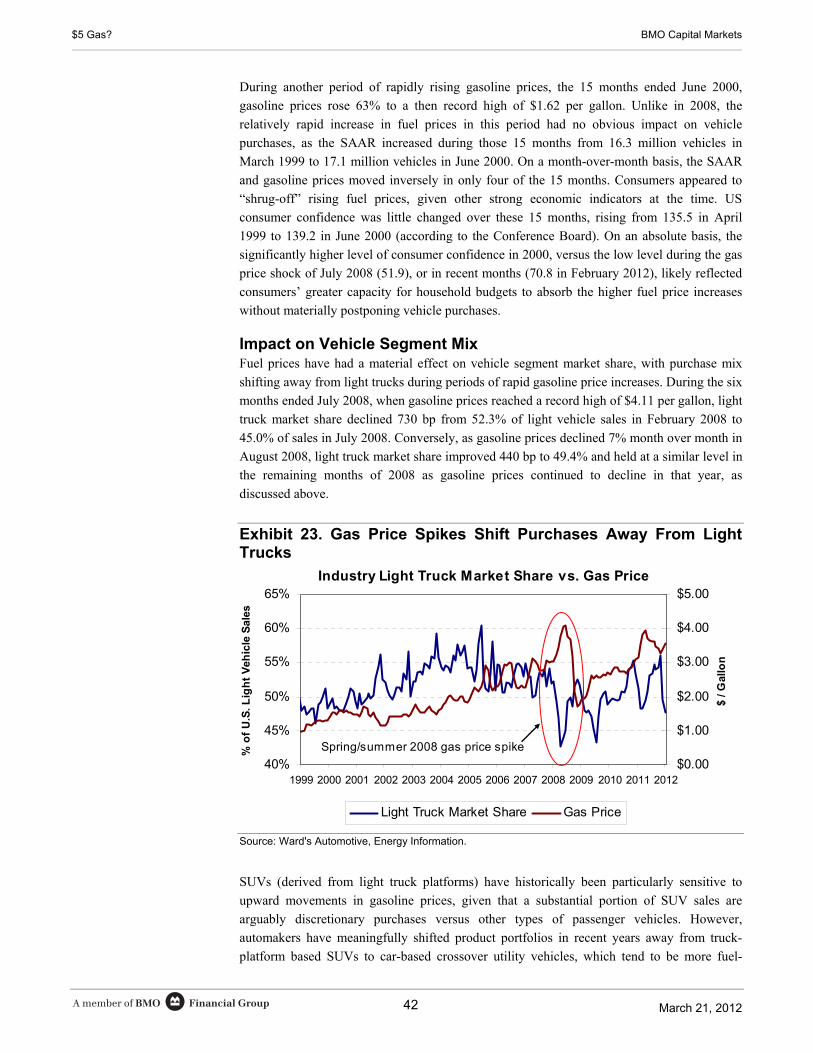

Exhibit 23. Gas Price Spikes Shift Purchases Away From Light Trucks...................................................42

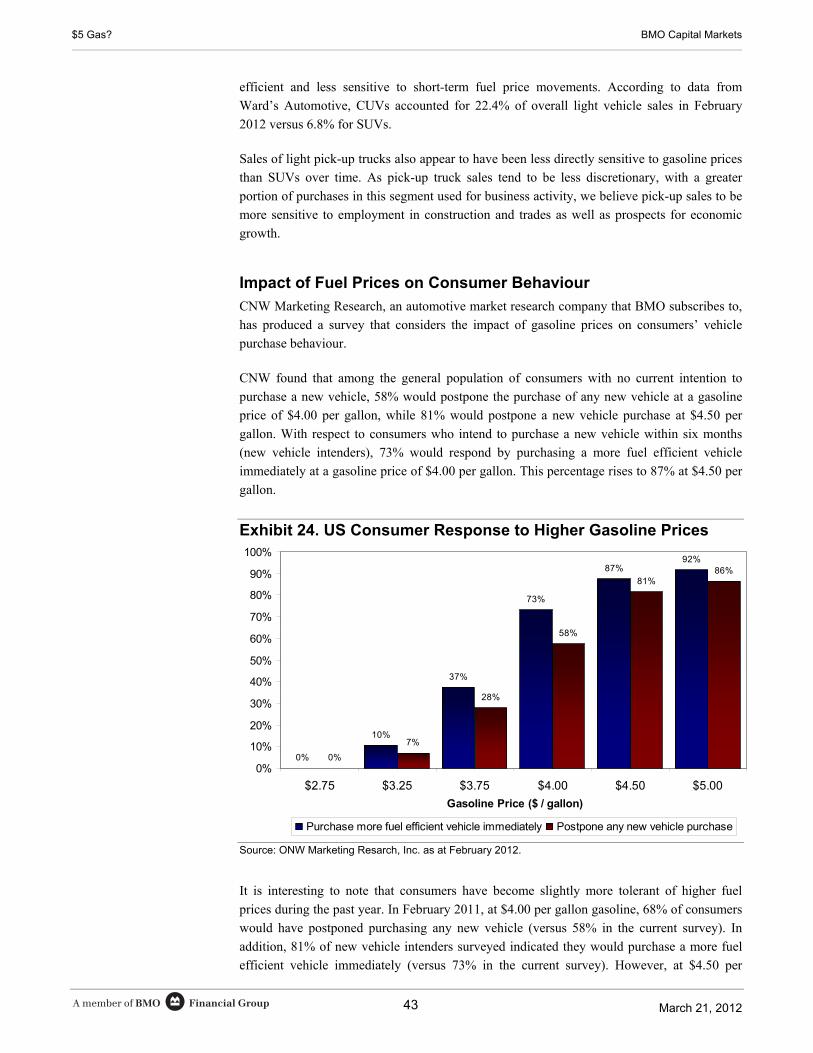

Exhibit 24. US Consumer Response to Higher Gasoline Prices ..............................................................43

Note: All prices shown in US dollars.

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

6

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

7

Economics

Economic Impact of $5 Gasoline—It’s Not a Gas! Five-dollar gasoline could reduce US economic growth from a projected moderate rate of

2½% on average in 2012-2013 to 1½%, driving the unemployment rate back to 9%. Ameri-

cans consume about 130 billion gallons of gasoline each year, accounting for slightly less than

4% of total spending. As fuel costs rise, households cut back on non-essential trips and spend-

ing on other items. A 35% increase from $3.70 a gallon to $5.00 could drain $170 billion

from annual purchasing power, reducing consumer spending by 1½% and real GDP growth

by 100 basis points.

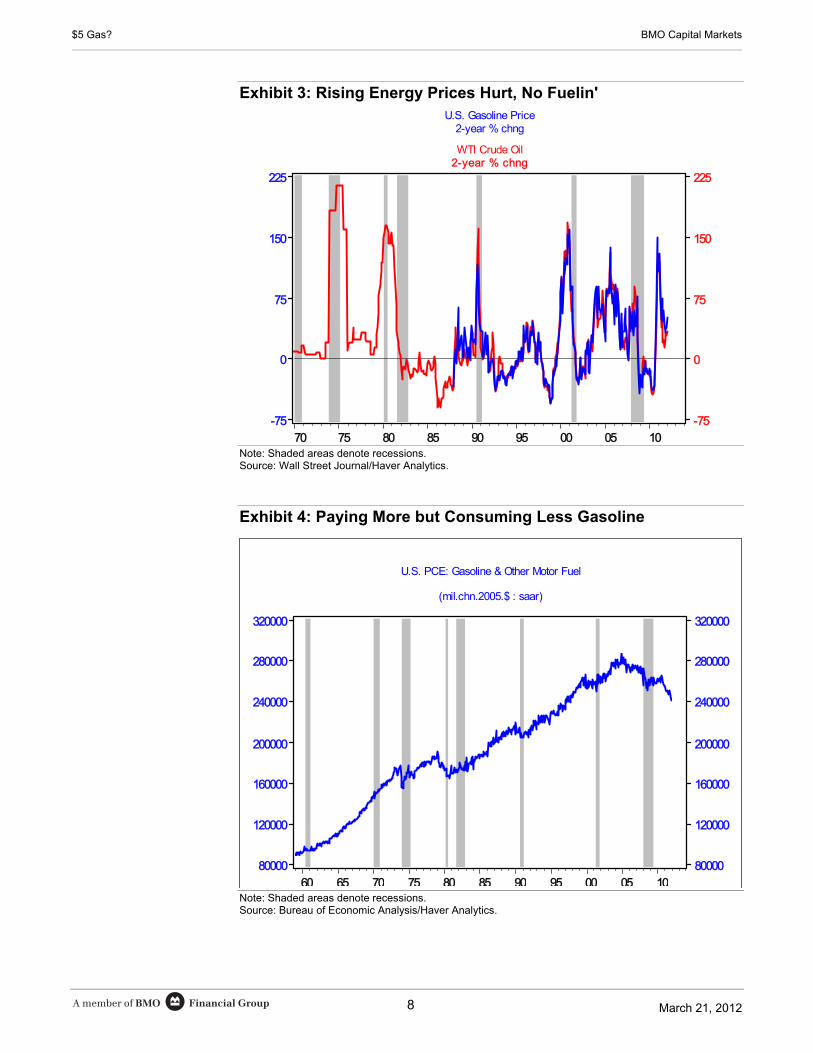

In the past, soaring energy costs have often preceded recessions (see Exhibit 3). Although

higher fuel costs were usually not the main cause of the downturn, they certainly weren’t

helpful. Today, an aggravating factor is the fragile nature of the recovery, with households

still burdened by high debt, soft house prices, and weak wage growth, and with governments

tightening their fiscal belts. Thus, the economy could be more sensitive to higher gasoline

prices than in the past. As well, with pump prices already high (double the two-decade mean),

a further sharp increase could have a disproportionate large impact on demand. In addition,

with interest rates so low, the economy has lost a major shock absorber.

Tempering these aggravating factors, the economic impact of higher energy costs has de-

clined, reflecting a reduction in fuel consumption since the mid-2000s, in part, due to more

fuel-efficient vehicles (see Exhibit 4). In addition, because of high unemployment, rising

gasoline prices are unlikely to stoke inflation, precluding an early Fed tightening. Instead, the

adverse effect of costlier fuel on the economy would likely keep the Fed on hold for longer

(possibly until 2016) and encourage a third round of quantitative easing, resulting in lower

long-term interest rates.

Canada would also suffer from costlier gasoline, which accounts for a slightly larger share

(4¼%) of personal spending than in the United States. The adverse effect would be amplified

by a weaker US economy and elevated household debt. A 35% increase in gasoline prices to

about C$1.70 a litre could reduce Canadian economic growth from about 2¼% projected in

2012-2013 to 1¼%, lifting the unemployment rate to 8%. However, if the run-up in gasoline

prices arose from higher oil prices (as opposed to refinery capacity constraints), the economic

impact could be tempered by improved terms of trade, as oil net exports are the biggest con-

tributor to Canada’s goods trade surplus. Alberta, Saskatchewan, and Newfoundland would

benefit disproportionately, while more manufacturing-based Central Canada would suffer.

Sal Guatieri

BMO Nesbitt Burns Inc.

416-359-5295

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

8

Exhibit 3: Rising Energy Prices Hurt, No Fuelin' U.S. Gasoline Price

2-year % chng

WTI Crude Oil2-year % chng

100500959085807570

225

150

75

0

-75

225

150

75

0

-75

Note: Shaded areas denote recessions. Source: Wall Street Journal/Haver Analytics.

Exhibit 4: Paying More but Consuming Less Gasoline

U.S. PCE: Gasoline & Other Motor Fuel

(mil.chn.2005.$ : saar)

1005009590858075706560

320000

280000

240000

200000

160000

120000

80000

320000

280000

240000

200000

160000

120000

80000

Note: Shaded areas denote recessions. Source: Bureau of Economic Analysis/Haver Analytics.

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

9

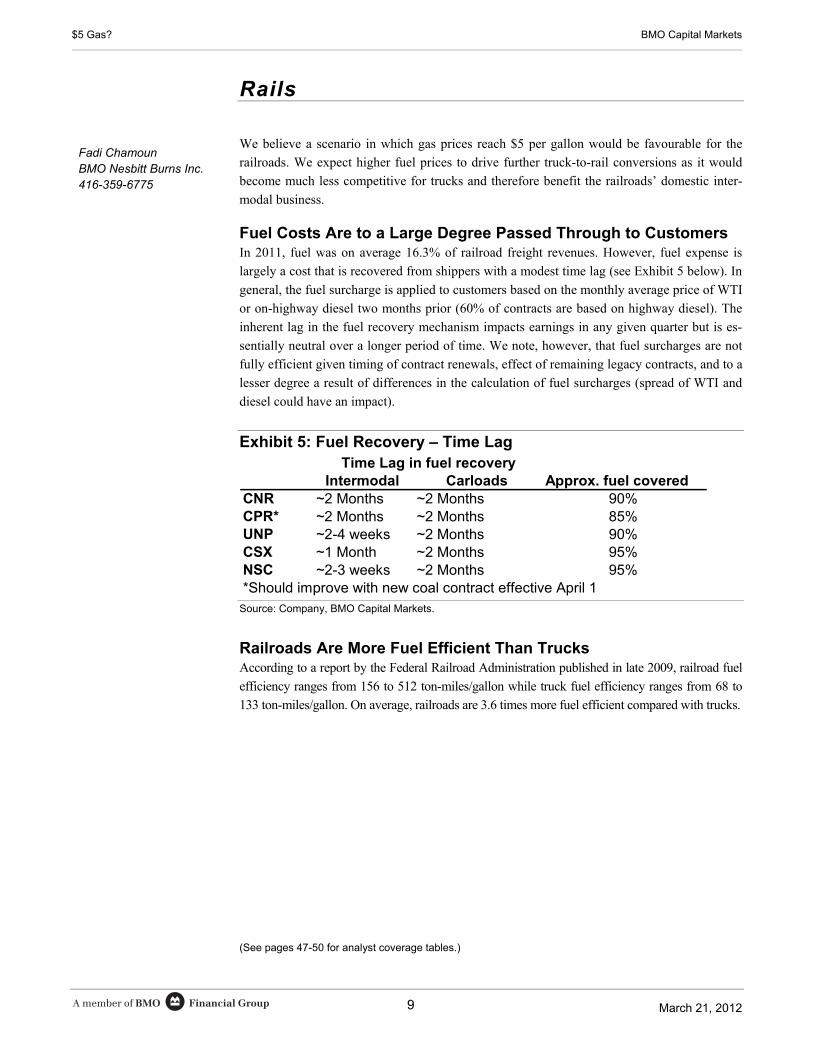

Rails

We believe a scenario in which gas prices reach $5 per gallon would be favourable for the

railroads. We expect higher fuel prices to drive further truck-to-rail conversions as it would

become much less competitive for trucks and therefore benefit the railroads’ domestic inter-

modal business.

Fuel Costs Are to a Large Degree Passed Through to Customers In 2011, fuel was on average 16.3% of railroad freight revenues. However, fuel expense is

largely a cost that is recovered from shippers with a modest time lag (see Exhibit 5 below). In

general, the fuel surcharge is applied to customers based on the monthly average price of WTI

or on-highway diesel two months prior (60% of contracts are based on highway diesel). The

inherent lag in the fuel recovery mechanism impacts earnings in any given quarter but is es-

sentially neutral over a longer period of time. We note, however, that fuel surcharges are not

fully efficient given timing of contract renewals, effect of remaining legacy contracts, and to a

lesser degree a result of differences in the calculation of fuel surcharges (spread of WTI and

diesel could have an impact).

Exhibit 5: Fuel Recovery – Time Lag

Intermodal Carloads Approx. fuel coveredCNR ~2 Months ~2 Months 90%CPR* ~2 Months ~2 Months 85%UNP ~2-4 weeks ~2 Months 90%CSX ~1 Month ~2 Months 95%NSC ~2-3 weeks ~2 Months 95%*Should improve with new coal contract effective April 1

Time Lag in fuel recovery

Source: Company, BMO Capital Markets.

Railroads Are More Fuel Efficient Than Trucks According to a report by the Federal Railroad Administration published in late 2009, railroad fuel

efficiency ranges from 156 to 512 ton-miles/gallon while truck fuel efficiency ranges from 68 to

133 ton-miles/gallon. On average, railroads are 3.6 times more fuel efficient compared with trucks.

(See pages 47-50 for analyst coverage tables.)

Fadi Chamoun BMO Nesbitt Burns Inc. 416-359-6775

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

10

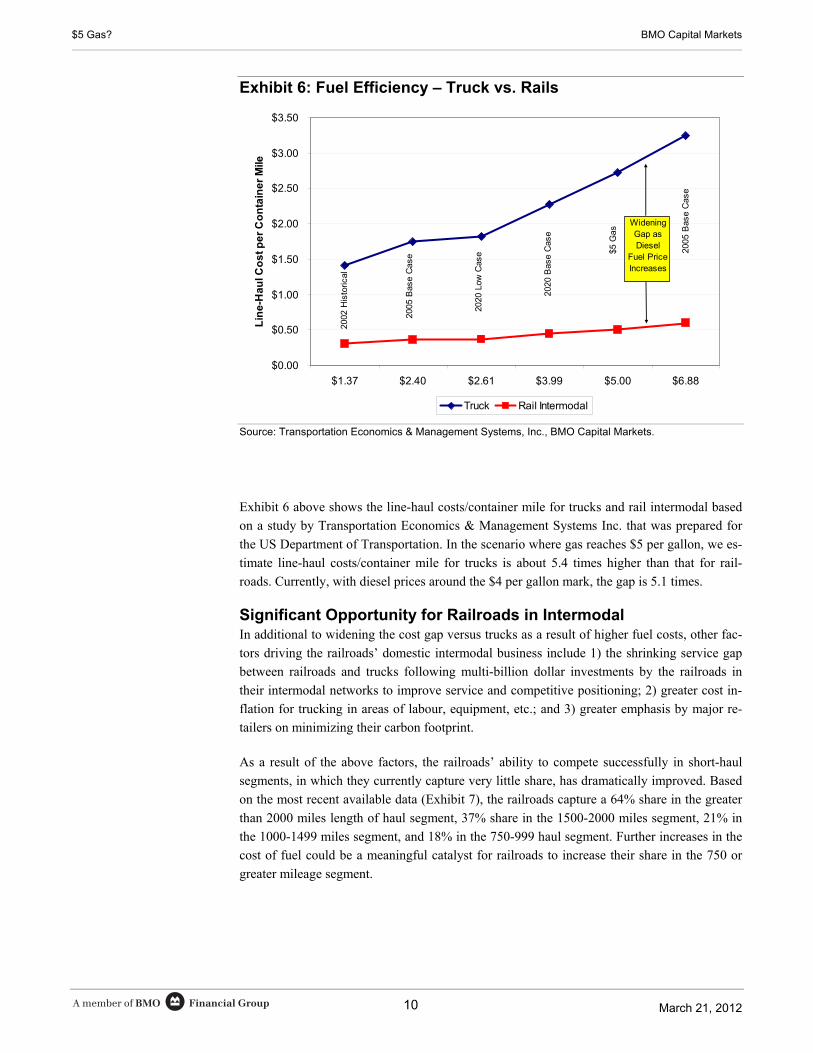

Exhibit 6: Fuel Efficiency – Truck vs. Rails

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$1.37 $2.40 $2.61 $3.99 $5.00 $6.88

Lin

e-H

aul C

os

t pe

r C

on

tain

er

Mile

Truck Rail Intermodal

2002

His

toric

al

2005

Bas

e C

ase

2020

Low

Cas

e 2005

Bas

e C

ase

2020

Bas

e C

ase

$5 G

as

WideningGap as Diesel

Fuel PriceIncreases

Source: Transportation Economics & Management Systems, Inc., BMO Capital Markets.

Exhibit 6 above shows the line-haul costs/container mile for trucks and rail intermodal based

on a study by Transportation Economics & Management Systems Inc. that was prepared for

the US Department of Transportation. In the scenario where gas reaches $5 per gallon, we es-

timate line-haul costs/container mile for trucks is about 5.4 times higher than that for rail-

roads. Currently, with diesel prices around the $4 per gallon mark, the gap is 5.1 times.

Significant Opportunity for Railroads in Intermodal In additional to widening the cost gap versus trucks as a result of higher fuel costs, other fac-

tors driving the railroads’ domestic intermodal business include 1) the shrinking service gap

between railroads and trucks following multi-billion dollar investments by the railroads in

their intermodal networks to improve service and competitive positioning; 2) greater cost in-

flation for trucking in areas of labour, equipment, etc.; and 3) greater emphasis by major re-

tailers on minimizing their carbon footprint.

As a result of the above factors, the railroads’ ability to compete successfully in short-haul

segments, in which they currently capture very little share, has dramatically improved. Based

on the most recent available data (Exhibit 7), the railroads capture a 64% share in the greater

than 2000 miles length of haul segment, 37% share in the 1500-2000 miles segment, 21% in

the 1000-1499 miles segment, and 18% in the 750-999 haul segment. Further increases in the

cost of fuel could be a meaningful catalyst for railroads to increase their share in the 750 or

greater mileage segment.

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

11

Exhibit 7: Truck and Rail Intermodal in Markets 500 Miles and Greater (in million units) Mileage Blocks Truck Rail Intermodal Total Market Truck Share Rail Share500 to 749 17.8 1.2 19 94% 6%750 to 999 10.1 2.3 12.4 82% 18%1000 to 1499 7.7 2 9.7 79% 21%1500 to 2000 3.7 2.1 5.8 63% 37%> 2000 2.8 4.9 7.7 36% 64%Total 42.1 12.5 54.6 77% 23% Source: Assessment of 2007 Commodity Flow Survey and 2007 Rail Carload Waybill Sample.

We note that NSC, CSX, and KSU are well positioned to benefit from ongoing truck-to-rail

conversions. UNP should also benefit from domestic intermodal growth, albeit to a lesser de-

gree than the shorter-haul carriers. NSC has indicated in previous presentations that its Cres-

cent corridor project has the potential to add 1 million intermodal carloads in the medium

term. The company is in the process of expanding several terminals, which have the potential

to significantly raise the company’s throughput capacity by the end of 2012.

The opportunity in intermodal is one of the key reasons we favour the US railroads versus the

Canadian peers.

(See pages 47-50 for analyst coverage tables.)

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

12

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

13

Trucking & Logistics

Near-Term Headwind; Pressure Eases as Surcharges Catch Up

We believe a rapid rise in fuel prices would be a near-term headwind for earnings because

fuel surcharges in the trucking sector generally lag the change in the price of fuel by one week

to one month. However, once the fuel prices settle at a higher level, the pressure eases as the

fuel surcharges catch up. Some shippers have negotiated caps on fuel surcharges, whereby

they avoid paying the additional cost once diesel fuel exceeds a certain price. Ultimately, a

carrier’s ability to pass on the full amount of fuel surcharges depends on industry conditions

and pricing power. We note that industry conditions in the US and Canada have become more

balanced as capacity exited the system during the most recent downturn. As such, we would

expect the surcharge mechanisms to be reasonably effective and the earnings pressure to sub-

side once the cost of diesel fuel stabilizes.

Truckload More Sensitive Than Less-Than-Truckload

The impact of rising fuel prices is generally more pronounced in the truckload sector than the

less-than-truckload space. Long-haul truckload carriers typically have a higher percentage of

empty miles where the carrier is not hauling revenue-generating freight and cannot levy fuel

surcharges.

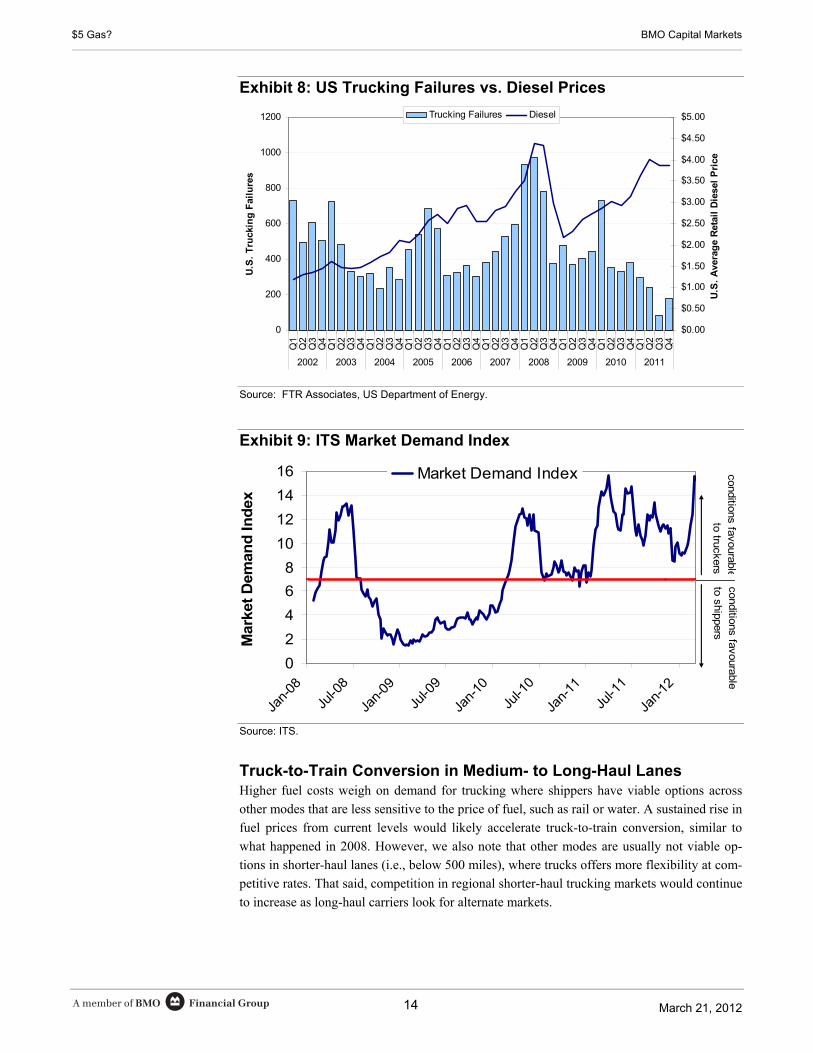

Upturn in Bankruptcies Likely but Not to Same Extent as in 2008

In H1/08, coinciding with the abrupt spike in fuel prices, there was a significant surge in busi-

ness failures (up 130% y/y) among trucking companies as some struggled to fully offset

higher fuel costs with rate increases. An indirect benefit from the acceleration in bankruptcies

was a reduction in industry capacity. However, we do not expect the same dynamic as we saw

in 2008 if there were a rapid rise in the price of gas to $5.00 per gallon. This scenario would

translate into a more moderate fuel cost increase of roughly 20% compared with the spike of

almost 60% that was realized from Q2/07 to Q2/08. Moreover, industry conditions are in a

better position today in light of capacity that has exited the system and flat-to-rising demand

(ITS Market Demand Index below shows relative strength of US truckload industry condi-

tions). This should allow trucking companies to pass through rate increases more easily, as-

suming volumes hold relatively steady. We would expect some upturn in bankruptcies but not

to the same extent as in 2008.

Jason Granger BMO Nesbitt Burns Inc. 416-359-4293

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

14

Exhibit 8: US Trucking Failures vs. Diesel Prices

0

200

400

600

800

1000

1200

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

U.S

. T

ruck

ing

Fai

lure

s

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

U.S

. A

vera

ge

Ret

ail

Die

sel

Pri

ce

Trucking Failures Diesel

Source: FTR Associates, US Department of Energy.

Exhibit 9: ITS Market Demand Index

0

2

4

6

8

10

12

14

16

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Mar

ket

Dem

and

In

dex

Market Demand Index

conditions favourable to shippers

conditions favourableto truckers

Source: ITS.

Truck-to-Train Conversion in Medium- to Long-Haul Lanes Higher fuel costs weigh on demand for trucking where shippers have viable options across

other modes that are less sensitive to the price of fuel, such as rail or water. A sustained rise in

fuel prices from current levels would likely accelerate truck-to-train conversion, similar to

what happened in 2008. However, we also note that other modes are usually not viable op-

tions in shorter-haul lanes (i.e., below 500 miles), where trucks offers more flexibility at com-

petitive rates. That said, competition in regional shorter-haul trucking markets would continue

to increase as long-haul carriers look for alternate markets.

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

15

J.B. Hunt – Intermodal Leaves Company Well Positioned

In 2011, J.B. Hunt’s intermodal business accounted for about 68% of consolidated operating

income. As fuel prices rise, shippers become more willing to consider intermodal opportuni-

ties to combat higher freight costs. We estimate that at current diesel prices ($4.15 per gallon),

the cost advantage of intermodal over trucking is about 40% for JB Hunt’s book of business.

If diesel were to spike to $5 per gallon, we estimate the cost advantage would increase to

50%. There is a substantial market opportunity in the eastern portion of the US (where the

adoption of intermodal is at an earlier stage) because of the denser population base and shorter

average length of haul compared to the western US. CSX has estimated that a market poten-

tial of up to 9.3 million loads (>550 miles) could be converted to intermodal in the Eastern

US. By comparison, JB Hunt shipped 1.25 million intermodal loads across its entire business

in 2011. The company has been generating impressive volume growth as it benefits from on-

going truck-to-train conversion and penetration of new markets. In 2011, J.B. Hunt’s inter-

modal loads were up 16%, including a 32% surge in the eastern network and a 10% increase

in transcontinental loads (western/central network).

Exhibit 10: J.B. Hunt Intermodal Volumes vs. Diesel Prices

100

150

200

250

300

350

Q1 Q2Q3 Q4 Q1 Q2Q3 Q4 Q1 Q2Q3 Q4 Q1 Q2Q3 Q4 Q1 Q2Q3 Q4 Q1 Q2Q3 Q4 Q1 Q2Q3 Q4

2005 2006 2007 2008 2009 2010 2011

JBH

T I

nte

rmo

dal

Lo

ads

(tho

usan

ds)

$1.80

$2.20

$2.60

$3.00

$3.40

$3.80

$4.20

$4.60

US

Ret

ail

On

-Hig

hw

ay D

iese

l P

rice

s

Intermodal Loads Diesel Qtrly Avg

Source: US Department of Energy (DOE), Company reports, BMO Capital Markets.

Mullen Group – Oilfield Services Business Expected to More Than Offset Headwind in Trucking In the event of a surge in fuel prices, we believe the headwinds faced by Mullen’s trucking

operations would be more than offset by stronger demand and pricing for its oilfield services

operations (70% of operating income). Higher oil prices should be positive for activity in the

oil patch. This should benefit Mullen’s business units exposed to oilfield production (i.e.,

hauling crude oil from well sites to processing facilities), oil sands and infrastructure (hauling

heavy over-sized equipment), and drilling activity (i.e., rig moving, hauling/warehousing

drilling mud). However, we note that labour constraints in western Canada would be expected

to hold back some of this momentum.

(See pages 47-50 for analyst coverage tables.)

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

16

TransForce – Impact Should Be Muted Due to Non-Traditional Trucking and Increased Emphasis on Asset Light Trucking While higher fuel prices are expected to present headwinds for truckload and less-than-

truckload carriers, the overall impact to TransForce should be only modestly negative. Trans-

Force generates roughly two-thirds of its earnings from non-traditional trucking services (i.e.,

courier, oilfield services), the majority of which are less sensitive to higher fuel prices. More-

over, the company has been growing in a less asset intensive manner by using more owner

operators, who would likely absorb some of the higher fuel costs.

Trimac – Most Negative Exposure to Fuel Price Surge Given Higher Percentage of Empty Miles Within our coverage universe, we believe Trimac would face the most pressure under the sce-

nario of higher fuel costs. The company hauls certain bulk commodities that require special-

ized rolling-stock equipment, which limits backhaul opportunities. As a result, Trimac has a

higher percentage of empty miles and would have more difficulty offsetting fuel cost in-

creases with rate hikes.

(See pages 47-50 for analyst coverage tables.)

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

17

Retail - Broadlines/Hardlines

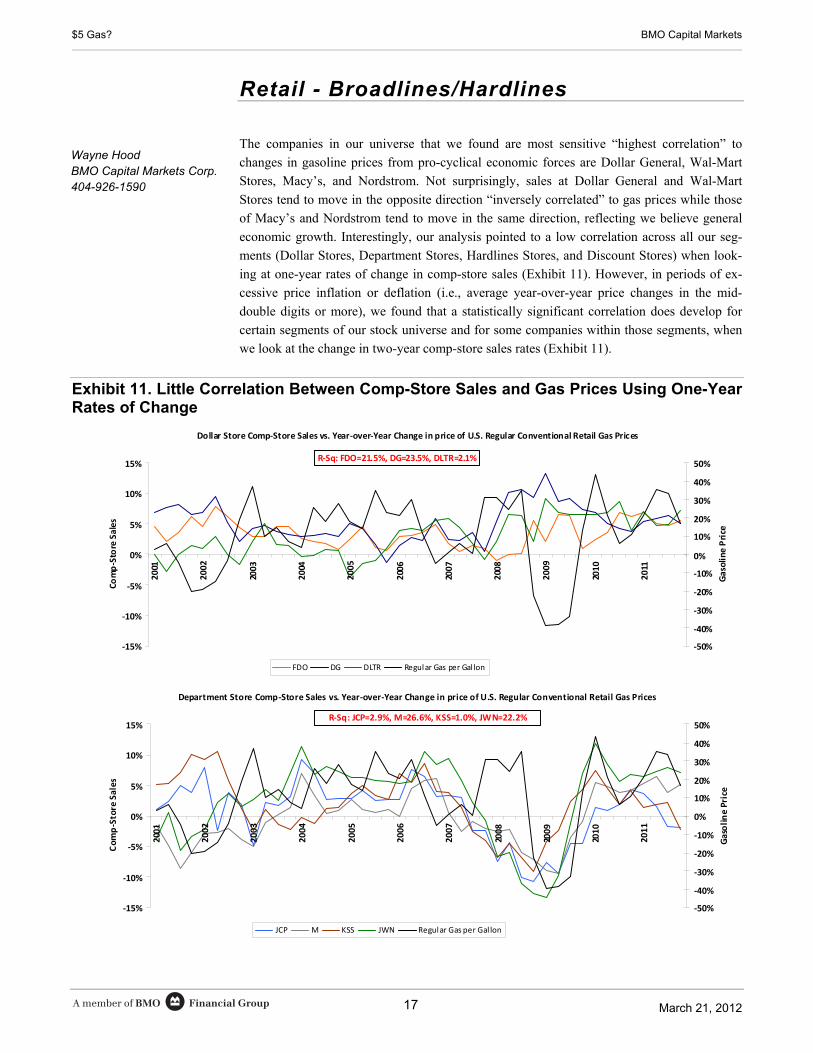

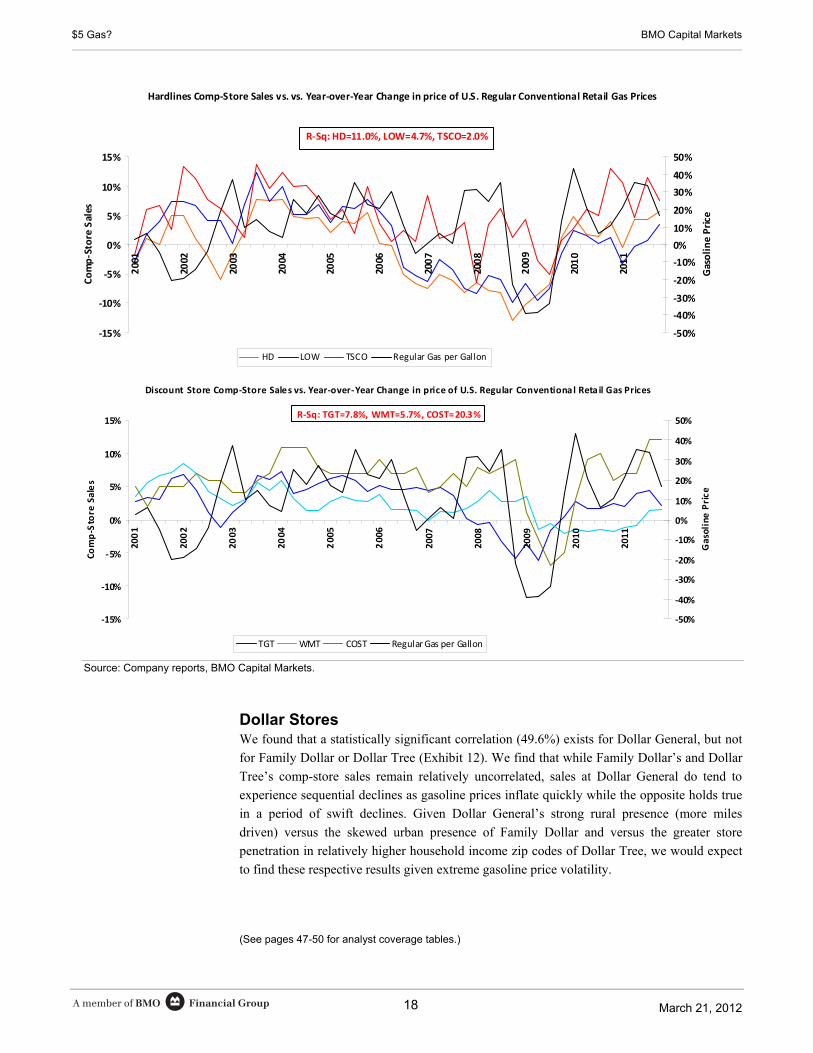

The companies in our universe that we found are most sensitive “highest correlation” to

changes in gasoline prices from pro-cyclical economic forces are Dollar General, Wal-Mart

Stores, Macy’s, and Nordstrom. Not surprisingly, sales at Dollar General and Wal-Mart

Stores tend to move in the opposite direction “inversely correlated” to gas prices while those

of Macy’s and Nordstrom tend to move in the same direction, reflecting we believe general

economic growth. Interestingly, our analysis pointed to a low correlation across all our seg-

ments (Dollar Stores, Department Stores, Hardlines Stores, and Discount Stores) when look-

ing at one-year rates of change in comp-store sales (Exhibit 11). However, in periods of ex-

cessive price inflation or deflation (i.e., average year-over-year price changes in the mid-

double digits or more), we found that a statistically significant correlation does develop for

certain segments of our stock universe and for some companies within those segments, when

we look at the change in two-year comp-store sales rates (Exhibit 11).

Exhibit 11. Little Correlation Between Comp-Store Sales and Gas Prices Using One-Year Rates of Change

Dollar Store Comp‐Store Sales vs. Year‐over‐Year Change in price of U.S. Regular Conventional Retail Gas Prices

‐15%

‐10%

‐5%

0%

5%

10%

15%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Comp‐Store Sales

‐50%

‐40%

‐30%

‐20%

‐10%

0%

10%

20%

30%

40%

50%

Gasoline

Price

FDO DG DLTR Regular Gas per Gal lon

R‐Sq: FDO=21.5%, DG=23.5%, DLTR=2.1%

Department Store Comp‐Store Sales vs. Year‐over‐Year Change in price of U.S. Regular Conventional Retail Gas Prices

‐15%

‐10%

‐5%

0%

5%

10%

15%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Comp‐Store Sales

‐50%

‐40%

‐30%

‐20%

‐10%

0%

10%

20%

30%

40%

50%Gasoline Price

JCP M KSS JWN Regular Gas per Gal lon

R‐Sq: JCP=2.9%, M=26.6%, KSS=1.0%, JWN=22.2%

Wayne Hood BMO Capital Markets Corp. 404-926-1590

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

18

Hardlines Comp‐Store Sales vs. vs. Year‐over‐Year Change in price of U.S. Regular Conventional Retail Gas Prices

‐15%

‐10%

‐5%

0%

5%

10%

15%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Comp‐Store Sales

‐50%

‐40%

‐30%

‐20%

‐10%

0%

10%

20%

30%

40%

50%

Gasoline Price

HD LOW TSCO Regular Gas per Gallon

R‐Sq: HD=11.0%, LOW=4.7%, TSCO=2.0%

Discount Store Comp‐Store Sales vs. Year‐over‐Year Change in price of U.S. Regular Conventional Reta il Gas Prices

‐15%

‐10%

‐5%

0%

5%

10%

15%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Comp‐Store Sales

‐50%

‐40%

‐30%

‐20%

‐10%

0%

10%

20%

30%

40%

50%

Gasoline

Price

TGT WMT COST Regular Gas per Gallon

R‐Sq: TGT=7.8%, WMT=5.7%, COST=20.3%

Source: Company reports, BMO Capital Markets.

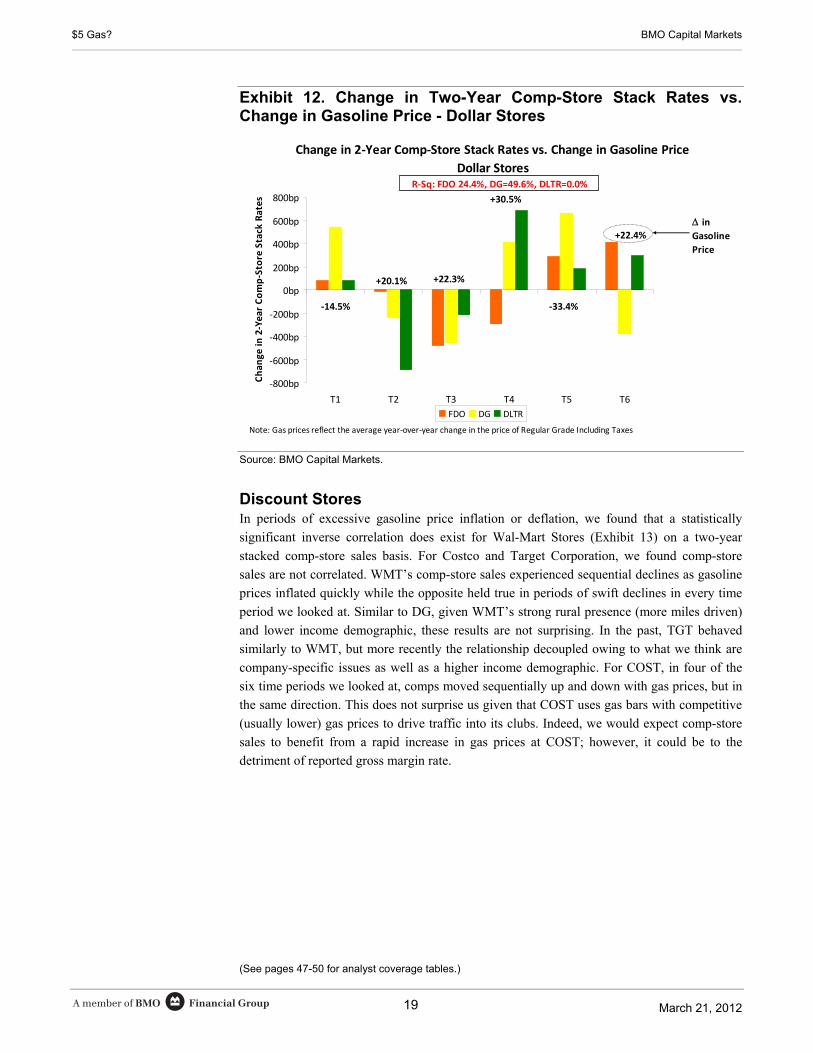

Dollar Stores We found that a statistically significant correlation (49.6%) exists for Dollar General, but not

for Family Dollar or Dollar Tree (Exhibit 12). We find that while Family Dollar’s and Dollar

Tree’s comp-store sales remain relatively uncorrelated, sales at Dollar General do tend to

experience sequential declines as gasoline prices inflate quickly while the opposite holds true

in a period of swift declines. Given Dollar General’s strong rural presence (more miles

driven) versus the skewed urban presence of Family Dollar and versus the greater store

penetration in relatively higher household income zip codes of Dollar Tree, we would expect

to find these respective results given extreme gasoline price volatility.

(See pages 47-50 for analyst coverage tables.)

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

19

Exhibit 12. Change in Two-Year Comp-Store Stack Rates vs. Change in Gasoline Price - Dollar Stores

Change in 2‐Year Comp‐Store Stack Rates vs. Change in Gasoline Price

Dollar Stores

‐800bp

‐600bp

‐400bp

‐200bp

0bp

200bp

400bp

600bp

800bp

T1 T2 T3 T4 T5 T6

Chan

ge in 2‐Year Comp‐Store Stack Rates

FDO DG DLTR

in Gasoline

Price

+22.4%

‐14.5%

+20.1% +22.3%

+30.5%

‐33.4%

Note: Gas prices reflect the average year‐over‐year change in the price of Regular Grade Including Taxes

R‐Sq: FDO 24.4%, DG=49.6%, DLTR=0.0%

Source: BMO Capital Markets.

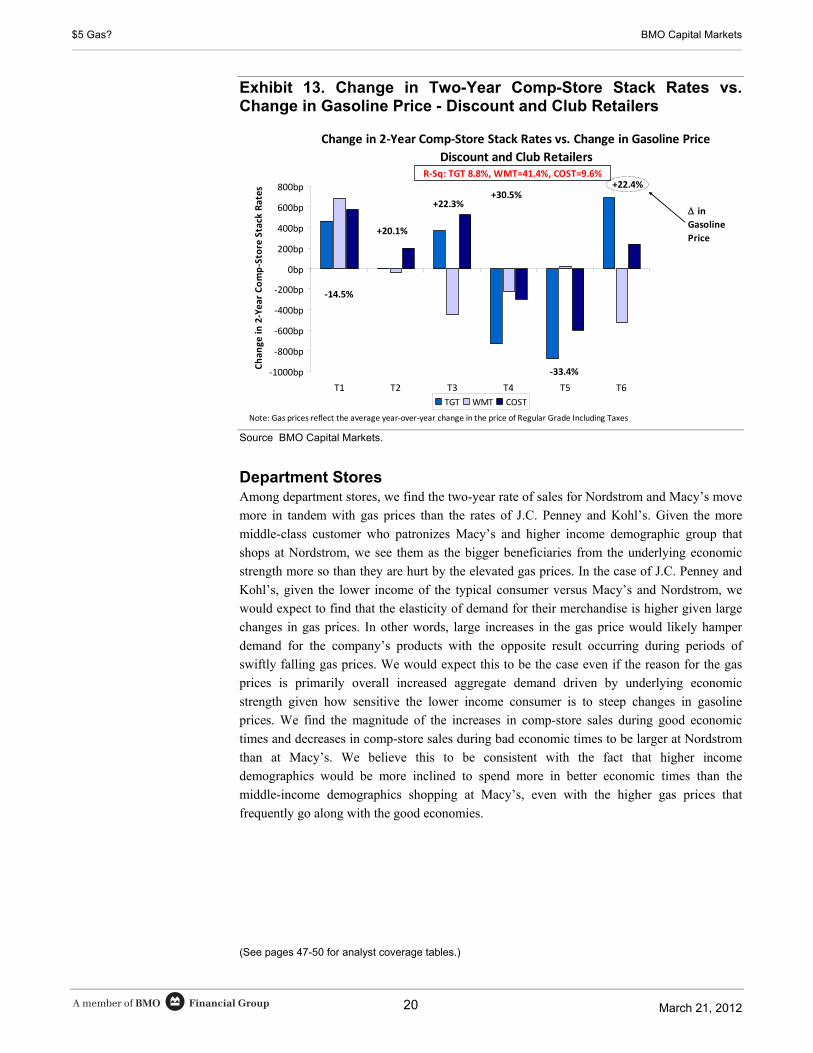

Discount Stores In periods of excessive gasoline price inflation or deflation, we found that a statistically

significant inverse correlation does exist for Wal-Mart Stores (Exhibit 13) on a two-year

stacked comp-store sales basis. For Costco and Target Corporation, we found comp-store

sales are not correlated. WMT’s comp-store sales experienced sequential declines as gasoline

prices inflated quickly while the opposite held true in periods of swift declines in every time

period we looked at. Similar to DG, given WMT’s strong rural presence (more miles driven)

and lower income demographic, these results are not surprising. In the past, TGT behaved

similarly to WMT, but more recently the relationship decoupled owing to what we think are

company-specific issues as well as a higher income demographic. For COST, in four of the

six time periods we looked at, comps moved sequentially up and down with gas prices, but in

the same direction. This does not surprise us given that COST uses gas bars with competitive

(usually lower) gas prices to drive traffic into its clubs. Indeed, we would expect comp-store

sales to benefit from a rapid increase in gas prices at COST; however, it could be to the

detriment of reported gross margin rate.

(See pages 47-50 for analyst coverage tables.)

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

20

Exhibit 13. Change in Two-Year Comp-Store Stack Rates vs. Change in Gasoline Price - Discount and Club Retailers

Change in 2‐Year Comp‐Store Stack Rates vs. Change in Gasoline Price

Discount and Club Retailers

‐1000bp

‐800bp

‐600bp

‐400bp

‐200bp

0bp

200bp

400bp

600bp

800bp

T1 T2 T3 T4 T5 T6

Change

in 2‐Year Comp‐Store Stack Rates

TGT WMT COST

in Gasoline

Price

+22.4%

‐14.5%

+20.1%

+22.3%+30.5%

‐33.4%

Note: Gas prices reflect the average year‐over‐year change in the price of Regular Grade Including Taxes

R‐Sq: TGT 8.8%, WMT=41.4%, COST=9.6%

Source BMO Capital Markets.

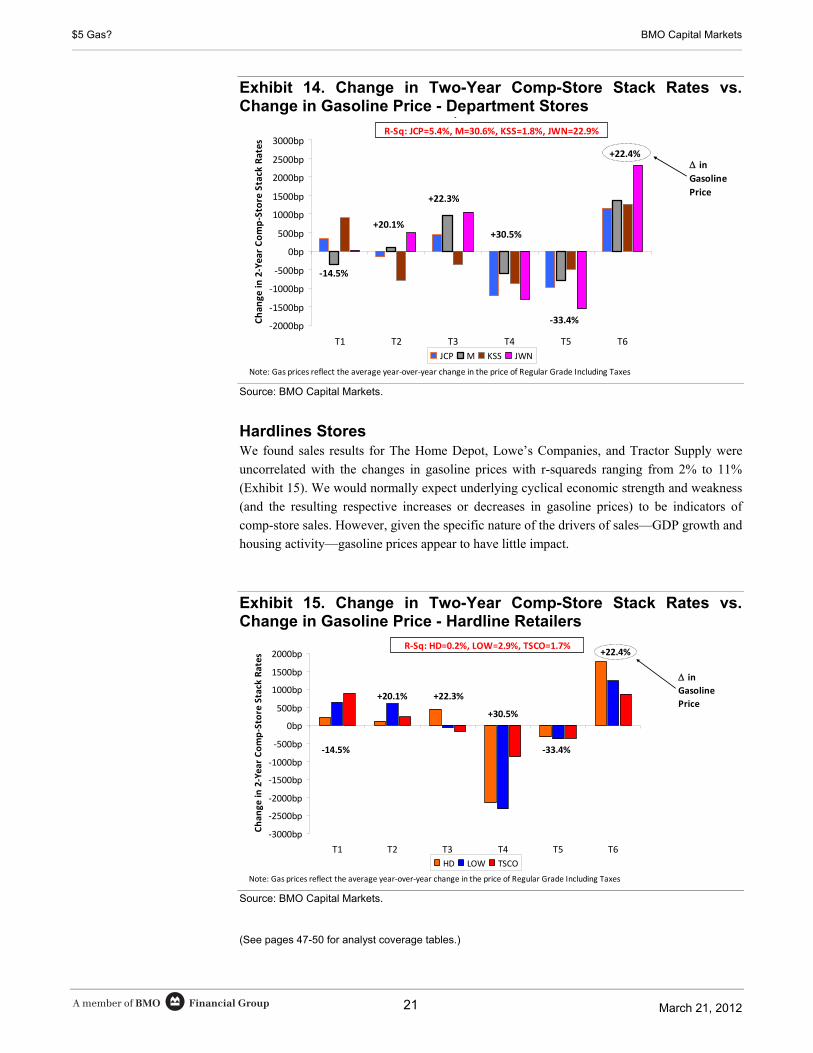

Department Stores Among department stores, we find the two-year rate of sales for Nordstrom and Macy’s move

more in tandem with gas prices than the rates of J.C. Penney and Kohl’s. Given the more

middle-class customer who patronizes Macy’s and higher income demographic group that

shops at Nordstrom, we see them as the bigger beneficiaries from the underlying economic

strength more so than they are hurt by the elevated gas prices. In the case of J.C. Penney and

Kohl’s, given the lower income of the typical consumer versus Macy’s and Nordstrom, we

would expect to find that the elasticity of demand for their merchandise is higher given large

changes in gas prices. In other words, large increases in the gas price would likely hamper

demand for the company’s products with the opposite result occurring during periods of

swiftly falling gas prices. We would expect this to be the case even if the reason for the gas

prices is primarily overall increased aggregate demand driven by underlying economic

strength given how sensitive the lower income consumer is to steep changes in gasoline

prices. We find the magnitude of the increases in comp-store sales during good economic

times and decreases in comp-store sales during bad economic times to be larger at Nordstrom

than at Macy’s. We believe this to be consistent with the fact that higher income

demographics would be more inclined to spend more in better economic times than the

middle-income demographics shopping at Macy’s, even with the higher gas prices that

frequently go along with the good economies.

(See pages 47-50 for analyst coverage tables.)

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

21

Exhibit 14. Change in Two-Year Comp-Store Stack Rates vs. Change in Gasoline Price - Department Stores p

‐2000bp

‐1500bp

‐1000bp

‐500bp

0bp

500bp

1000bp

1500bp

2000bp

2500bp

3000bp

T1 T2 T3 T4 T5 T6

Chan

ge in

2‐Year Comp‐Store Stack Rates

JCP M KSS JWN

in Gasoline

Price

+22.4%

‐14.5%

+20.1%

+22.3%

+30.5%

‐33.4%

Note: Gas prices reflect the average year‐over‐year change in the price of Regular Grade Including Taxes

R‐Sq: JCP=5.4%, M=30.6%, KSS=1.8%, JWN=22.9%

Source: BMO Capital Markets.

Hardlines Stores We found sales results for The Home Depot, Lowe’s Companies, and Tractor Supply were

uncorrelated with the changes in gasoline prices with r-squareds ranging from 2% to 11%

(Exhibit 15). We would normally expect underlying cyclical economic strength and weakness

(and the resulting respective increases or decreases in gasoline prices) to be indicators of

comp-store sales. However, given the specific nature of the drivers of sales—GDP growth and

housing activity—gasoline prices appear to have little impact.

Exhibit 15. Change in Two-Year Comp-Store Stack Rates vs. Change in Gasoline Price - Hardline Retailers

‐3000bp

‐2500bp

‐2000bp

‐1500bp

‐1000bp

‐500bp

0bp

500bp

1000bp

1500bp

2000bp

T1 T2 T3 T4 T5 T6

Change

in 2‐Year Comp‐Store Stack Rates

HD LOW TSCO

in Gasoline

Price

+22.4%

‐14.5%

+20.1% +22.3%

+30.5%

‐33.4%

Note: Gas prices reflect the average year‐over‐year change in the price of Regular Grade Including Taxes

R‐Sq: HD=0.2%, LOW=2.9%, TSCO=1.7%

Source: BMO Capital Markets.

(See pages 47-50 for analyst coverage tables.)

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

22

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

23

Toys & Leisure

Higher gas prices will have the most obvious effect on the powersports sector of the leisure

industry, as these companies sell products whose cost of use is directly related to the price of

gasoline.

The company to have the biggest negative impact is Brunswick (BC), the world’s largest boat

and boat engine manufacturer. 75% of BC’s sales are related to the boating industry. We

believe it is well known that boats get very poor gas mileage. Smaller fiberglass boats

generally get 2-4 miles per gallon, while larger inboard/sterndrive sport-yachts are lucky if

they get up to 1 mile per gallon. Thus, higher gas prices can significantly increase the cost of

boating.

What is also impactful, but perhaps not as obvious, is the fact that a rising price of gasoline

will also increase the cost of getting a boat to the water, or getting to a boat that is moored or

docked on the water. According to the NMMA, boat owners spent more on gas in 2010 to get

to their boat or get their boat to water ($3.7 billion) than they actually did in the operation of

their boat ($2.4 billion). We estimate that about 60% of all boats are trailered, about 25% are

stored at a marina, while just 15% are on the water at the owners’ residence. Therefore, 85%

of all boaters are required to travel in some way to use their boat, while 60% actually have to

haul their boat. Hauling a boat on a trailer will reduce a vehicle’s mileage by about 20%-35%,

depending on the weight of the boat.

Polaris (PII) is the world leader in off-road vehicles, with most sales coming from ATVs,

side-by-sides, and snowmobiles. All of PII’s products consume gasoline, and all would be

negatively impacted by a significant increase in the price of gasoline. However, we think the

use of these vehicles would be much less affected than boats.

First, in the off-road vehicle segment (ATV and side-by-side), which generates 80% of PII’s

sales, we estimate that about half of its sales are to farmers, ranchers, landscapers, and the

government, all of which tend to use the vehicles for work-related purposes. We believe the

use of these vehicles will see no impact from higher gas prices.

The balance of PII’s product portfolio is used for recreational purposes. But even in this

segment, we see minimal impact from higher gas prices. PII’s customers generally take their

ATVs, side-by-sides, or snowmobiles out on weekends and perhaps ride 100 miles on them

during each outing. Gas mileage on off-road vehicles averages 12-15 mpg, so if gas prices rise

from a current $3.75 to $5.00 per gallon, that adds about $10 to the cost of their day of fun.

We doubt these powersports enthusiasts would give up riding for a day because it costs an

extra $10.

For Harley-Davidson (HOG), owing to the superior gas mileage of motorcycles, we think the

impact of higher gas prices would be mostly positive. In the face of rising gas prices, we think

people are looking to motorcycles as a less expensive form of transportation. The appeal of

high-mileage motorcycle could be especially strong for a commuter who is consistently

putting extensive miles on his/her car.

(See pages 47-50 for analyst coverage tables.)

Gerrick Johnson BMO Capital Markets Corp. 212-883-5192

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

24

The Harley-Davidson Forty-Eight, a small sportster, gets 57 miles per gallon on the highway.

The larger Electra Glide Ultra touring bike gets 54 mpg. In comparison, a Toyota Camry gets

33 mpg on the highway, while a Ford F150 pickup truck gets 23 mpg. If gas prices spike to $5

per gallon, we estimate that a commuter making a 20-mile round trip commute, five days a

week, would save anywhere from $35 to $65 per month by switching over to a Harley

sportster from a car or truck. This savings is based on mpg from new vehicles, so should a

consumer be switching over to a Harley from a gas-guzzling clunker, the savings could be

significantly higher.

Feedback we have received from dealers indicates a strong interest in Sportsters (883-1200cc)

as younger customers look to the gas mileage they provide as a way to save money on gas.

This is positive for the long term, as sportsters are “gateway bikes,” which tend to lead to

purchases of larger, more expensive, and more customizable bikes.

Exhibit 16. Monthly Gas Savings Per-Month Commuter Savings Gained by Switching to a Harley-Davidson Sportster.*

Car ModelFord F150 (23 mpg) $64Honda CRV (28 mpg) $44Ford Fusion (29 mpg) $40Chevy Equinox (32 mpg) $36Toyota Camry (33 mpg) $36

Car ModelFord F150 (23 mpg) $128Honda CRV (28 mpg) $88Ford Fusion (29 mpg) $81Chevy Equinox (32 mpg) $71Toyota Camry (33 mpg) $71

Round Trip

Round Trip20 mile

40 mile

*Based on a 5 day workweek. Car model mpg is a city/highway mix based on a new car purchase. Source: fueleconomy.gov, Harley-Davidson, BMO Capital Markets.

Toys The stocks that could get impacted the most from higher gasoline prices, and where the effect

may not be initially recognized by investors, is in the toy stocks we cover: Mattel (MAT),

Hasbro (HAS), LeapFrog (LF), JAKKS Pacific (JAKK), Mega Brands (MB-T), and Build-A-

Bear Workshop (BBW).

We think gas prices will be most impactful to people who have a regular routine and stick

tight to a budget. If a family has a set budget for necessities, including rent/mortgage, food,

clothing, toys for the kids, then rising gasoline prices will disrupt this budget, forcing

consumers to cut back in other areas. This is supported by the strongly negative correlation

between the spending on “other” categories and gas for households with annual income of

less than $70,000. Simply put, the incremental or impulse toy purchase is an easy one to do

without when it costs an extra $10 or $20 to fill the family car’s gas tank.

The toy industry is not coming out of a period of strength either, with 2011 US toy retail sales

declining 2%. We think sales were down 3%-4% in the important fourth quarter. Normally parents

do not scrimp on the kids. This likely still holds true, but with higher costs to fill the tank, and as

illustrated in holiday 2011, parents will forgo the extra toy purchase if they feel they have to.

(See pages 43-46 for analyst coverage tables.)

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

25

Restaurants

We found little-to-no statistical relationship between changing gas prices and

restaurant comps or restaurant stock performance over the last decade (or so). In fact,

we found other macroeconomic variables to be more relevant (primarily jobs and income). As

a result, we believe that if $5 gas accompanies strengthening economic growth and continued

job growth, the rising economic tide would lift all boats, benefiting sales across the restaurant

industry. However, if we see gas prices spike despite weakening domestic economic growth

(reminiscent of 2008), then we would expect higher gas prices to amplify the negative

economic impact to restaurants.

The impact (on consumer spending) from changing employment levels exceeds any

impact from changing gas prices. We performed regression analysis (from 1980 to present)

between real US consumer spending and a number of macroeconomic variables including

employment, income, consumer credit, and changes in retail gas prices, among other factors.

We found that changes in the rate of employment had the highest correlation with real

consumer spending over the period with a coefficient of determination (R2) of 0.54 followed

closely by nonfarm payrolls (R2 = 0.50) and RDPI (R2 = 0.48). In contrast, the impact of

changing retail gas prices on overall consumer spending was negligible (R2 = 0.04 – the

weakest relationship that we measured).

We found a similar result when we focused on restaurant demand (employment impact

> gas price impact). Next, we ran regressions of quarterly comp-store sales for the restaurant

companies in our coverage universe against changes in retail gas prices and employment. In

short, we found that changes in employment explained 65% of the variation in comp-store

sales across our restaurant coverage universe (from 2001 to present – Exhibit 17), while the

impact to comps from changes in gas prices was not statistically significant (R2 = 0.13 –

Exhibit 17).

Exhibit 17. Comps for Our Restaurant Coverage Are Driven More by Employment Than Gas

(2%)

(1%)

0%

1%

2%

3%

4%

5%

1Q01

3Q01

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

(3.0%)

0.0%

3.0%

6.0%

9.0%

∆% Unemployment (Left Axis) ∆% Comps ‐ BMO Restaurant Coverage (Right Axis)

R2 = 65% ∆ Unemployment vs. Restaurant Comps (Yr/Yr ∆% )

Source: Company reports, Bureau of Economy Analysis, and Energy Information Agency.

(45%)

(35%)

(25%)

(15%)

(5%)

5%

15%

25%

35%

45%

1Q01

3Q01

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

(3.0%)

0.0%

3.0%

6.0%

9.0%

∆% Gas $'s (Left Axis) ∆% Comps ‐ BMO Restaurant Coverage (Right Axis)

R2 = 13% ∆ Gas $'s vs. Restaurant Comps (Yr/Yr ∆% )

Phillip Juhan, CFA BMO Capital Markets Corp. 404-926-1599

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

26

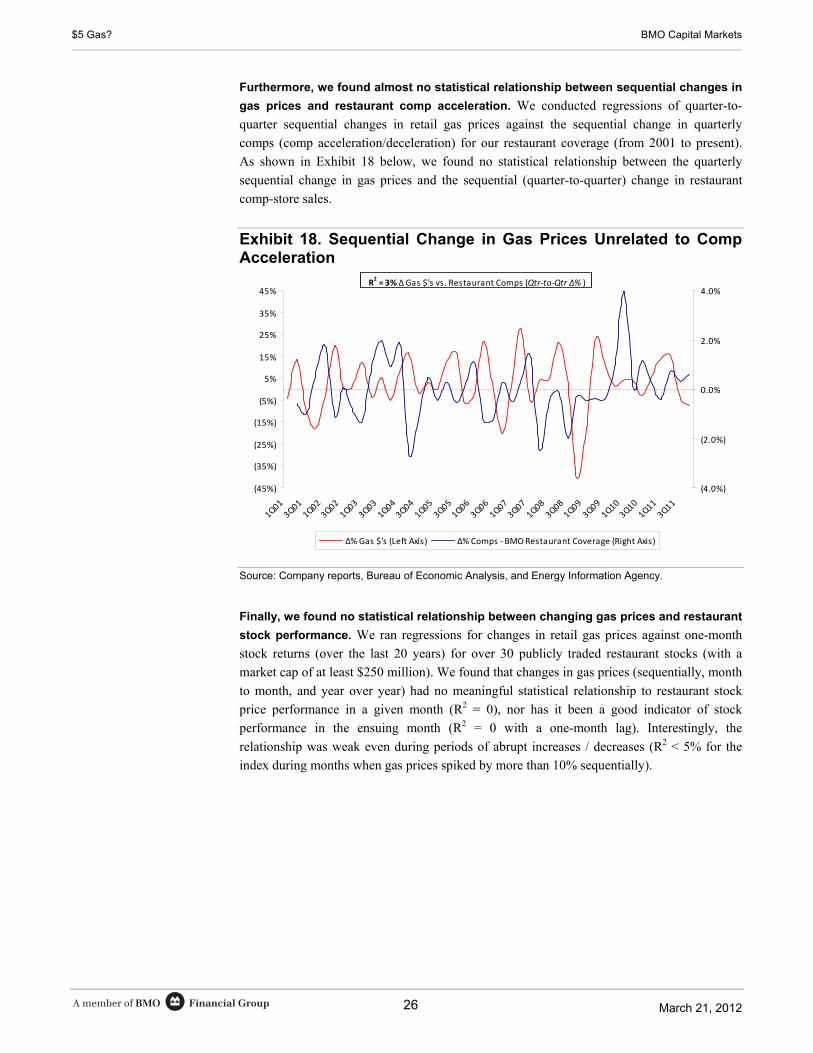

Furthermore, we found almost no statistical relationship between sequential changes in

gas prices and restaurant comp acceleration. We conducted regressions of quarter-to-

quarter sequential changes in retail gas prices against the sequential change in quarterly

comps (comp acceleration/deceleration) for our restaurant coverage (from 2001 to present).

As shown in Exhibit 18 below, we found no statistical relationship between the quarterly

sequential change in gas prices and the sequential (quarter-to-quarter) change in restaurant

comp-store sales.

Exhibit 18. Sequential Change in Gas Prices Unrelated to Comp Acceleration

(45%)

(35%)

(25%)

(15%)

(5%)

5%

15%

25%

35%

45%

1Q01

3Q01

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

(4.0%)

(2.0%)

0.0%

2.0%

4.0%

∆% Gas $'s (Left Axis) ∆% Comps ‐ BMO Restaurant Coverage (Right Axis)

R2= 3% ∆ Gas $'s vs. Restaurant Comps (Qtr‐to‐Qtr ∆% )

Source: Company reports, Bureau of Economic Analysis, and Energy Information Agency.

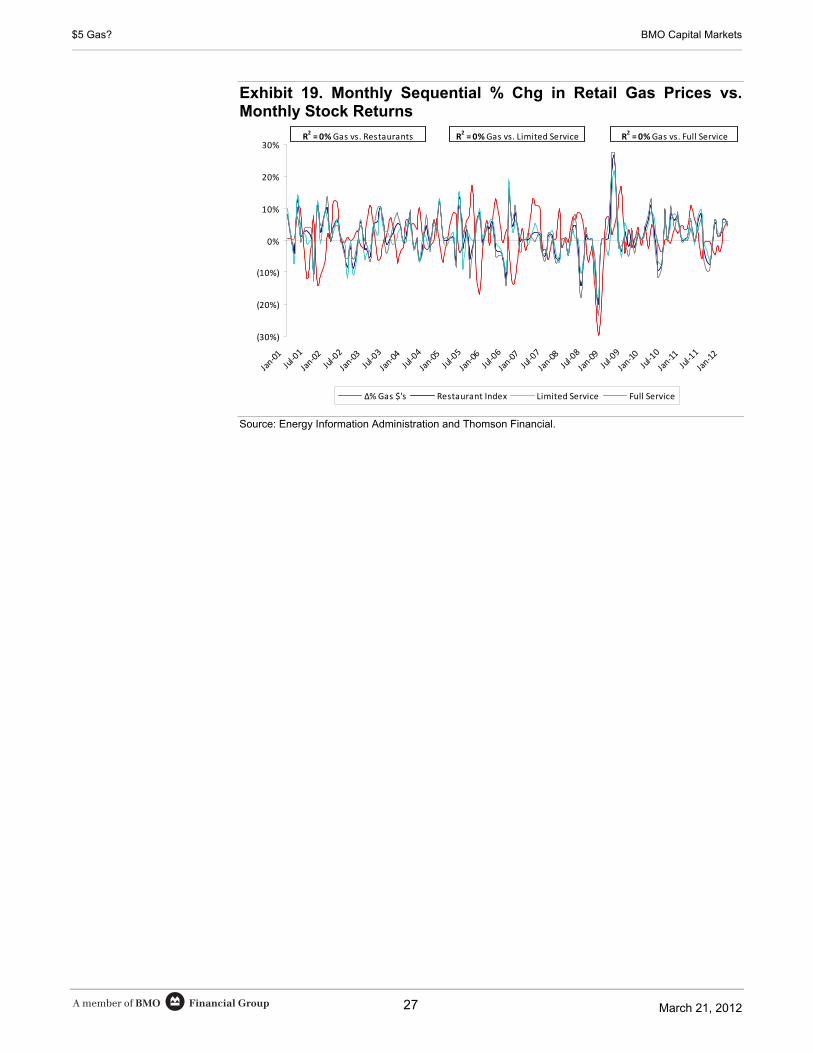

Finally, we found no statistical relationship between changing gas prices and restaurant

stock performance. We ran regressions for changes in retail gas prices against one-month

stock returns (over the last 20 years) for over 30 publicly traded restaurant stocks (with a

market cap of at least $250 million). We found that changes in gas prices (sequentially, month

to month, and year over year) had no meaningful statistical relationship to restaurant stock

price performance in a given month (R2 = 0), nor has it been a good indicator of stock

performance in the ensuing month (R2 = 0 with a one-month lag). Interestingly, the

relationship was weak even during periods of abrupt increases / decreases (R2 < 5% for the

index during months when gas prices spiked by more than 10% sequentially).

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

27

Exhibit 19. Monthly Sequential % Chg in Retail Gas Prices vs. Monthly Stock Returns

(30%)

(20%)

(10%)

0%

10%

20%

30%

Jan‐01

Jul‐01

Jan‐02

Jul‐02

Jan‐03

Jul‐03

Jan‐04

Jul‐04

Jan‐05

Jul‐05

Jan‐06

Jul‐06

Jan‐07

Jul‐07

Jan‐08

Jul‐08

Jan‐09

Jul‐09

Jan‐10

Jul‐10

Jan‐11

Jul‐11

Jan‐12

∆% Gas $'s Restaurant Index Limited Service Full Service

R2 = 0%Gas vs. Restaurants R

2 = 0% Gas vs. Full ServiceR

2= 0%Gas vs. Limited Service

Source: Energy Information Administration and Thomson Financial.

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

28

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

29

Exhibitors and Gaming

Exhibition Industry In general, the exhibition industry has been largely immune to the economic swings that have

occurred over the past two decades, including the recent spikes (2005/2008) in gasoline, which

took prices up $1 per gallon or more than previous trend lines. In fact, at the height of the

economic fears in 2009, the exhibitors saw a roughly 10% increase in revenue driven in large part

by higher attendance.

Whereas some consumer discretionary/leisure spending categories may experience some

slowdown, this has not been the case for the major exhibitors such as AMC, Cinemark (CNK,

Outperform, $29 target), Cineplex (CGX.TO, Outperform, $30 target), or Regal (RGC,

Outperform, $19 target) in the last decade, when we have gone through two major gasoline price

spikes. Whether it is the social experience, value proposition versus other out of home

entertainment options, or the attraction of high-priced comfort food (popcorn and Coke!),

eliminating the movie-going option does not appear to be the one most consumers choose to

economize when higher gas prices arrive.

Although the one major theater circuit that does seem to feel the impact of higher gas prices is

Carmike Cinemas (CKEC, Market Perform, $10 target). Historically, it seems to experience more

of an unfavorable attendance impact from the higher gas prices than the other exhibitors. The

company’s geographic footprint is largely centered in the Southeast portion of the US, and it tends

to operate in more rural settings, which perhaps explains its vulnerability when we see major

upward moves in gas prices.

We see a neutral impact to most exhibitor stocks if gas prices were to rise to $5 per gallon.

Gaming Industry The domestic gaming market can be, in simplistic terms, broken down into two broad geographical

categories: the regional casinos and the destination resorts (Las Vegas). It is estimated by the

American Gaming Association (AGA) that over 80% of the American population lives within a

two-hour drive to a casino and that close to 40% of US households gamble at least once per year.

The last two gasoline price spikes have spawned frequent chatter that rising gas prices would keep

people from driving or gambling due to the higher personal or gaming trip expense quotient. Any

brief examination of the variables would likely conclude that the individual whose gaming behavior

is impacted by higher gas prices is the marginal customer at best and represents a negligible amount

of revenue for casinos anyway. The incremental $5 or $10 cost to drive 100 miles to visit a regional

riverboat or Native American casino probably is not going to stop his entertainment routine at a local

casino, even if the overall gasoline bill were to rise $50 or $100 per month.

With about half the visitors to Las Vegas arriving by automobile, it might seem logical to presume

a measureable portion of the drive-in customers would defer or cancel a drive to Las Vegas. Using

an average of 20 miles per gallon for the 280-mile one-way commute to Las Vegas from Los

Angeles (the largest feeder market for drive-in traffic) and assuming an incremental $1 per gallon

increase in the price of gasoline, the price of the trip increases $28.

(See pages 47-50 for analyst coverage tables.)

Jeffrey Logsdon BMO Capital Markets Corp. 213-228-2234

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

30

If the average Las Vegas stay is three days and average gaming budget for the free and

independent traveler (FIT) segment is around $600, we do not think there is a lot of risk to

casino companies posed by higher gas prices and an incremental $28 trip cost. During the last

two spikes, some casinos in Las Vegas even used a free tank of gas as a promotional tool to

lure customers.

On the more positive side of the equation are the benefits of $105-$120 per barrel oil. It is

exceptionally good for Latin American gamblers as well as those most levered to oil in Texas,

Louisiana, and Oklahoma (owners and workers), many of whom have a high propensity for

gambling. Those who might be the greatest beneficiaries are the high-end casinos in Las

Vegas (MGM, LVS, WYNN) and those in Louisiana (PNK, BYD, and CZR).

Disney Disney’s domestic theme parks in Florida and California generate about 35% and 65%,

respectively, of their admissions from the “locals” market, which is broadly defined as visitors

who live within a two-hour drive to the park. Some observers may postulate that Disney could

feel some decline in attendance because of the overall expense pressure on consumers who

are having to pay higher gasoline prices or are hesitant to spend the extra dollars to get there.

Jet fuel prices rise similarly if not more than gasoline prices. However, we point out that a

significant portion of the non-commuters are booking packages 3-6 months ahead for Walt

Disney World, when the incremental cost of higher jet fuel prices on a $2,000-$10,000

vacation is not going to be that noticeable (less than a 5% package cost price increase).

Historically, periods of high gas prices have not had any measurable impact on admissions;

Park attendance was up 5% in each of 2005 and 2006 and up 2% in 2008.

Disney parks and resorts tend to be destination resorts or high priority excursions that

certainly transcend gas prices for most park and resort visitors. A $10 incremental expense for

gas for locals does not rationally seem sufficient when a family of four is likely to spend more

than $500 for a one-day visit. Locals obviously have time-shifting capabilities, but we are

skeptical that anything more than a 1%-2% reduction in spending for a very small percentage

of Disney parks’ annual visitors would occur. Indeed, per cap spending actually rose 5% in

2005, and 3% in each of 2006 and 2008, the three periods of gas price spikes mentioned

above. We believe the impact to Disney of $5 gas prices is, at the very least, neutral.

(See pages 47-50 for analyst coverage tables.)

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

31

Consumer - Special Situations

For the group of Canadian furniture retailers in our coverage universe (LNF, BRK, GBT.a,

CWA, EH), while we believe that rising gas prices takes a further bite out of consumers’

discretionary spending and general feeling of wealth, furniture, appliance, and electronics

sales (both at the retail level and wholesale level to builders) tend to correlate most highly

with housing activity. As such, the level of housing activity trumps movement in gas prices.

Consumers tend to buy household furniture and appliances when they move into a new home,

with homebuyers tending to spend more than non-moving homeowners. Typically,

homebuyer spending on furniture continues in the three years following a move, with the

majority of spending occurring in the first two years; after this, spending declines annually

until their spending is equivalent to a non-moving homeowner. In addition, a strong housing

market (higher transaction activity accompanied by rising home prices) contributes to a

consumer’s feeling of wealth, compounded by strong employment and higher consumer

confidence, which can lead to higher discretionary spending.

For North West Company, fuel prices impact the company’s operating costs to a much larger

degree, through both freight (given higher distribution costs across the breadth of its store

network – northern Canada, Alaska, Caribbean, South Pacific) and fuel-related utility costs

(powering and heating a store in a cold northern winter). Given the company’s strong

competitive position across more than 60% of its store network (namely, Alaska and northern

Canada), the company generally is able to recover a high proportion of rising fuel costs

through retail pricing. While this is less the case in its more competitive Giant Tiger and Cost-

U-Less markets, we believe that on a net basis, North West is well positioned to recover, over

time, short-term fuel-related cost pressures.

(See pages 47-50 for analyst coverage tables.)

Stephen MacLeod BMO Nesbitt Burns Inc. 416-359-8069

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

32

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

33

Personal Care and Household Products

From the standpoint of consumer behavior: Spikes in gasoline prices historically have had a

modest impact on sales volumes as people in developed markets cut back little on necessities.

However, the total dollar sales in some categories can come under pressure as consumers, as

they have in the past, trade down to more affordable value brands and private label.

In this environment of rising gas prices:

CHD appears best positioned as its portfolio of 60% premium products and 40% value

covers a wide range of price points and should capture much of the migration within its

categories. Its Arm & Hammer (at the upper end of value pricing) and Xtra (at opening

price points) detergents, about 20% of total sales, gained share during the most recent US

recession. We think they will continue to do well if high gas prices crimp consumer

spending. Most recently, Arm & Hammer and Xtra’s share gained 40 bp to 12.7 % in the

12-week IRI data ended February 19.

At the opposite end, Avon’s business may be negatively affected as there is less incentive

for its representatives, most of whom make a modest income, to drive long distances to

make sales to consumers whose income is at least temporarily under pressure. This

impact is felt greatest in North America (19% of sales and 8% of operating profit), where

representatives generally drive more and live further away from their customers than in

other countries.

From the standpoint of the personal care and househould products (PCHP) stock

behavior: While consumer behavior shifts a bit as a result of spikes in gas, the correlation

between gas and oil prices seems to have a bigger impact on the profits and stock prices of

PCHP companies. High gas prices normally follow high oil prices, and high oil prices

typically correlate with underperformance for this group. We analyzed the impact of rising oil

and gas prices in periods of geopolitically induced increases (the 1973 OPEC oil embargo, the

1979 Iranian Revolution, the 1990 Gulf War, the December 2010-April 2011 Arab Spring,

and most recently (Exhibit 20) since mid-December, the escalated tension with Iran). In

addition, we evaluated one extended period of demand-driven price increases between

January 2002 and July 2008.

Performance in the personal care and household products stocks was mixed. In the past,

companies with significant exposure to oil and its derivatives—particularly KMB and PG—

generated modest returns and underperformed the market and other sectors. A surprise finding

(and tied to the factors noted above) was how poorly AVP fared. It underperformed in 7 of 12

periods, including during the first three periods of Middle East turmoil, where it declined an

average of 36%, far worse than the 9% decrease of the S&P 500, and during the most recent

one, where its 14% increase was one of the best of the group but was still below the market’s

24% gain. There is no example of consistent outperformance when oil and gas prices are high.

Most recently, all PCHP stocks have underperformed the 25% increase in the S&P 500 since

mid-December. NWL 22% increase is the closest, but we think this has more to do with the

arrival of a new CEO and the adjustment of earnings expectations during an investment phase

than with anything else.

(See pages 47-50 for analyst coverage tables.)

Connie Maneaty BMO Capital Markets Corp. 212-885-4004

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

34

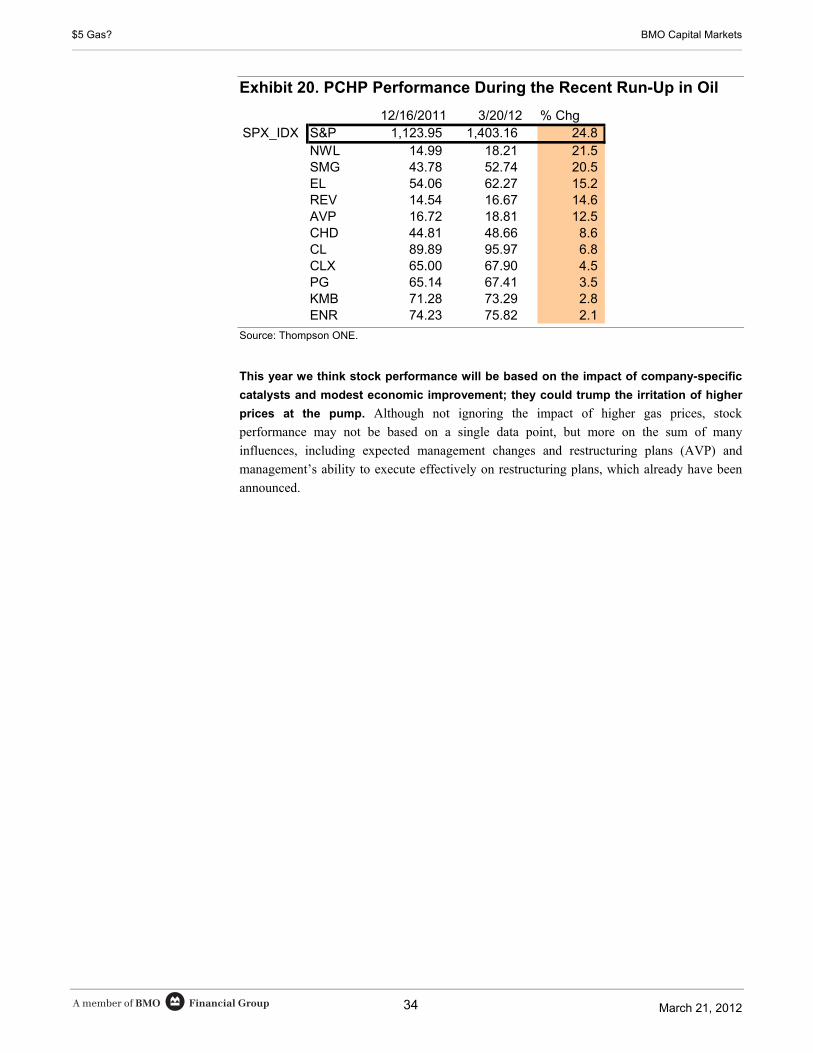

Exhibit 20. PCHP Performance During the Recent Run-Up in Oil

12/16/2011 3/20/12 % ChgSPX_IDX S&P 1,123.95 1,403.16 24.8

NWL 14.99 18.21 21.5SMG 43.78 52.74 20.5EL 54.06 62.27 15.2REV 14.54 16.67 14.6AVP 16.72 18.81 12.5CHD 44.81 48.66 8.6CL 89.89 95.97 6.8CLX 65.00 67.90 4.5PG 65.14 67.41 3.5KMB 71.28 73.29 2.8ENR 74.23 75.82 2.1

Source: Thompson ONE.

This year we think stock performance will be based on the impact of company-specific

catalysts and modest economic improvement; they could trump the irritation of higher

prices at the pump. Although not ignoring the impact of higher gas prices, stock

performance may not be based on a single data point, but more on the sum of many

influences, including expected management changes and restructuring plans (AVP) and

management’s ability to execute effectively on restructuring plans, which already have been

announced.

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

35

Retail - Apparel & Specialty

As it relates to specialty retail, so far we have not seen any noticeable impact on consumer behavior

as gas prices have increased. We would argue that consumers are likely to remain somewhat

immune—even to $5 per gallon gas—because 1) the employment outlook is brighter, 2) compelling

new spring fashions and warm weather are fueling early demand, 3) consumer sentiment is stronger,

and 4) natural gas prices have declined meaningfully, which has enabled lower heating bills to offset

higher prices at the pump. Our bottom line view is that, barring any significant and unexpected

economic shock, higher gas prices alone will have little negative effect on our companies in the

aggregate, especially as specialty apparel skews to an upper-middle income consumer.

Still, most retailers consider $4 gas prices as the tipping point where consumers begin to pull back

on their discretionary spending. So the real possibility that we could eclipse this figure and hit

$5 per gallon is causing concern in a recovering, yet still fragile, economic environment. While

exorbitant energy prices could weigh negatively on our sector outlook, we must acknowledge that

the impact of higher gasoline prices likely wouldn’t be immediate in the current environment,

where consumer bevior seems somewhat more optimistic. Unless it were a sharp and rapid price

hike (think back to Hurricane Katrina) or meaningful deterioration in other macro components

(like unemployment or overall inflation), our view is that the consumers will continue to grin and

bear it. If gas prices were to climb to $5 per gallon and remain there for three to four months, we

could start to see some changes/reductions in spending habits at the lower end, but otherwise, our

view is that it would take a material price shock to derail spending overall.

Taking a step back, the reality is that consumers have lived with high gas prices for some time now

and sales generally continue to grow across specialty apparel. To the degree consumers make one

or two less trips to the mall is not of major concern, as the trips they do make would likely be more

targeted and productive, particularly given that we are in a strong trend cycle and demand is higher

than it has been in a few years. The bigger issue, and the one which would garner investor

attention, is that performance across different companies would likely be uneven. Typically, it’s

the lower-income consumer who feels the pinch most when energy costs rise. For example, you

might see more resistance in the off-price sector, given the middle-income consumer’s higher

sensitivity to macro conditions (gas represents a higher percentage of their household budget). We

believe TJX would be less impacted than Ross Stores, because of the more diversified base of

retail concepts at the former. On the other hand, in the teen sector, looking good and being on trend

outweighs concerns about gas prices or interest rates, and therefore a rise in gas prices to $5 per

gallon would likely have less impact on the Abercrombies and American Eagles of the world.

High prices at the pump don’t tend to change the spending habits of higher income households—at

least not in the early stages of the upswing. If prices spike significantly and quickly, we

acknowledge that there could be broader spillover to other areas of the economy, which in turn

could weigh on stock prices and have a lagging effect on the high-end shopper.

The beginning of June 2008 was the first time gas prices rose above $4 per gallon and energy-

related spending hit 6% of total US consumer outlays. Retail comps in the subsequent months did

indeed turn negative. However, we caution that there was a unique set of economic circumstances

in 2008 and that extrapolating same outcome to today, especially in light of more favorable data

points, would not really be applicable.

(See pages 47-50 for analyst coverage tables.)

John Morris BMO Capital Markets Corp. 212-359-4016

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

36

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

37

Food & Beverage

Higher gas prices would create a favorable operating environment for private label consumer

packaged goods (CPG) companies, particularly private label food manufacturers. Higher

household spending on gas (in terms of both absolute dollar amount and as a percent of total

household spending) would force consumers, particularly in the lower income cohort, to

reduce other expenses, including those on food. We believe that private label food

manufacturers, with their well-established appeal to value-conscious consumers, are well

positioned to benefit from likely changes in consumer behavior, leading to continued unit and

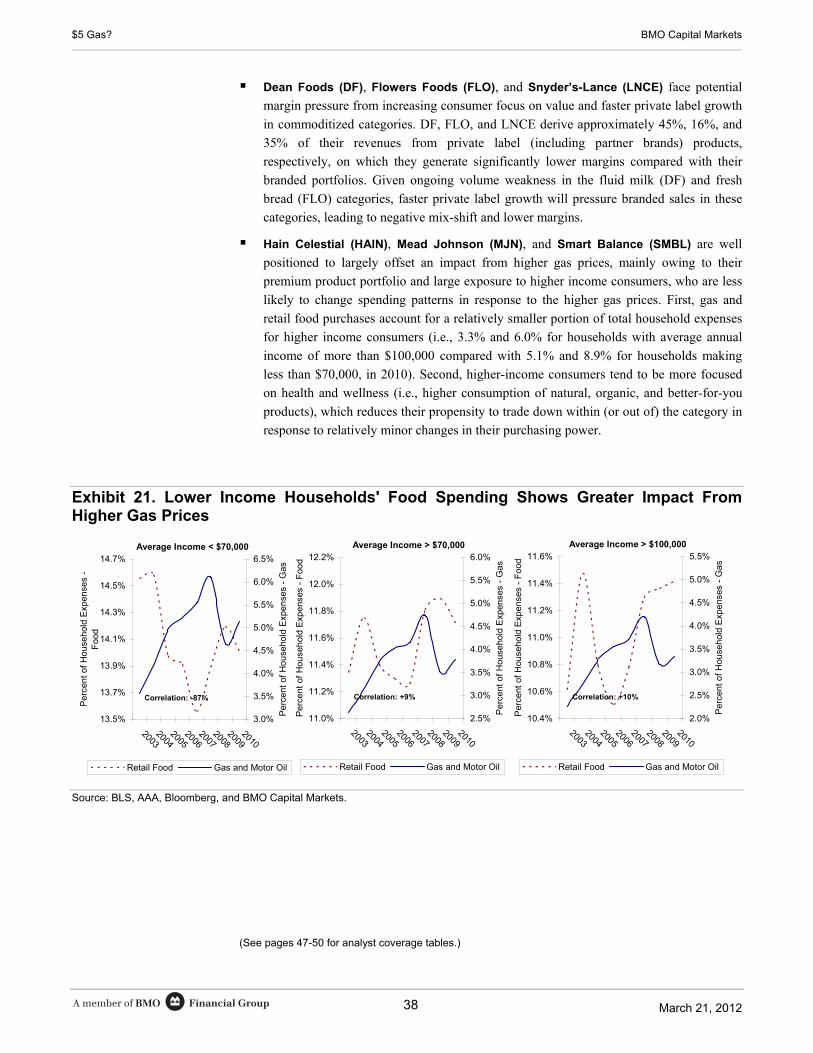

dollar share gains in the US packaged food segment. In fact, we estimate a negative 87%

correlation between household spending on food and gas (both expressed as percent of total

household spending) for households with annual income of less than $70,000 (see Exhibit 21).

On the other hand, food-related expenses for higher income households showed very little

impact from changes in gas prices as we estimate correlations of +9% and +10% for

households with average annual income of more than $70,000 and more than $100,000,

respectively, based on our analysis of household spending patterns over the last eight years.

The divergent consumer reaction, based on relative prosperity level, clearly signals that higher

gas prices would have a greater impact on food purchasing power and patterns of lower and

lower-middle income consumers, likely strengthening the ongoing trend of stronger private

label growth among value-oriented consumers and accelerating the shift to private label for

consumers on the fence.

Our investment conclusions are as follows:

We expect Ralcorp (RAH) and Treehouse Foods (THS), pure play private label

packaged food manufacturers, to continue to outgrow branded competitors in their key

categories, with 6%-8% organic top-line growth in 2012, including low-single-digit

volume growth. While private label performance varies across categories, our analysis of

75 of the top packaged food categories reveals the following trends, which support our

conclusion:

o Private label volumes have outperformed branded volumes in each of the past six

quad-weeks periods with an average decline of 0.6% compared with an average

decline of 5.9% for the top three brands in these categories;

o Price gaps between private label and top branded competitors have remained largely

stable at approximately 24%, which indicates that recent volume share gains are

sustainable (i.e., not driven by temporary widening of price gaps); and

o Private label share gains appear to be more pronounced in commoditized categories,

in which the consumer is more likely to focus on lower prices (i.e., relative to

value-added categories).

(See pages 47-50 for analyst coverage tables.)

Amit Sharma, CFA BMO Capital Markets Corp. 212-885-4132

Financial GroupA member of BMO March 21, 2012

$5 Gas? BMO Capital Markets

38

Dean Foods (DF), Flowers Foods (FLO), and Snyder’s-Lance (LNCE) face potential

margin pressure from increasing consumer focus on value and faster private label growth

in commoditized categories. DF, FLO, and LNCE derive approximately 45%, 16%, and

35% of their revenues from private label (including partner brands) products,

respectively, on which they generate significantly lower margins compared with their

branded portfolios. Given ongoing volume weakness in the fluid milk (DF) and fresh

bread (FLO) categories, faster private label growth will pressure branded sales in these

categories, leading to negative mix-shift and lower margins.

Hain Celestial (HAIN), Mead Johnson (MJN), and Smart Balance (SMBL) are well

positioned to largely offset an impact from higher gas prices, mainly owing to their

premium product portfolio and large exposure to higher income consumers, who are less

likely to change spending patterns in response to the higher gas prices. First, gas and

retail food purchases account for a relatively smaller portion of total household expenses

for higher income consumers (i.e., 3.3% and 6.0% for households with average annual

income of more than $100,000 compared with 5.1% and 8.9% for households making

less than $70,000, in 2010). Second, higher-income consumers tend to be more focused

on health and wellness (i.e., higher consumption of natural, organic, and better-for-you

products), which reduces their propensity to trade down within (or out of) the category in

response to relatively minor changes in their purchasing power.

Exhibit 21. Lower Income Households' Food Spending Shows Greater Impact From Higher Gas Prices

Average Income < $70,000

13.5%

13.7%

13.9%

14.1%

14.3%

14.5%

14.7%

20032004

20052006

20072008

20092010

Per

cent

of

Hou

seho

ld E

xpen

ses

- F

ood

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

Per

cent

of

Hou

seho

ld E

xpen

ses

- G

as

Retail Food Gas and Motor Oil

Correlation: -87%

Average Income > $70,000

11.0%

11.2%

11.4%

11.6%

11.8%

12.0%

12.2%

20032004

20052006

20072008

20092010

Per