Embed Size (px)

Citation preview

1

11 Mar ±∆ ±%BDI 388 p 39 11.2%

BCI 176 p 12 7.3%

BPI 477 p 91 23.6%

BSI 420 p 49 13.2%

BHSI 249 p 17 7.3%

W-O-W change

Strong volatility and a general shake up in the commodities markets has been the

main description of this past week’s events and continuing on from last week’s article

it is more and more evident that most traders in the market are fairly confused at the

signs being given. Last week the commodities markets (especially in the case of most

dry bulk commodities such as iron ore and coal) noted a firm hike in prices both in the

futures and physical markets. This was largely driven by China’s National People’s

Congress which discussed the proposed changes and targets it plans to put through

for its next five year plan (pointing to the major role China still plays not only in the

physical markets of these commodities but also in the minds of most investors world-

wide). Speculation was rife, as some sought to take a more optimistic view as to what

was coming out of China. Most of these traders might have been overeager to pull the

trigger on their investment strategies, inpatient as to when the market would turn.

However it seems as though they might have miscalculated the timing, having avoided

to read some of the fine print from China’s next stimulus plan.

As such we have started off the week with the biggest two-day slide in commodity

prices, while in turn this has had knock off effects on global stocks and other financial

instruments. At the same time the recent decision by the Bank of Japan to jump off

the stimulus bandwagon hindered by the growing underlining risk of a negative inter-

est-rate strategy has left further woes for the global economy. As such, much is left in

question as to the true direction of global economic growth.

Of course, in the physical market, the actual uptick in demand (and therefore in prices)

of iron ore have been more reliant on supply, demand and inventories as always ra-

ther than mere expectations of financial markets. However, once you take a closer

look, these are more near-term in nature. Namely low inventories and the prospects

of a forced stoppage in the output of several still mills in China over the summer

months, have pushed many to scramble for ore while trying to operate at full capacity

in order to build stocks of metals so as to be ready to supply the seasonal pickup in

construction in spring. This chain has more to do with seasonality then any political

decision undertaken, however it does hold a small truth as to the state of the market.

Expectations are that new real estate constructions are slowly going to pick up, based

on the increasing level of home sales and higher prices. Home prices have risen by as

much as 50% in some of China’s most popular cities over the past year, pointing to

potential shortages in comparison to rising demand. The clarification here is that this

trend is still held within a few key cities, while the excess backlog in real estate supply

across the whole of China is still fairly big. At the same time there are some who fear

that this is more of a bubble rather than an indicator as to the state of real demand.

Efforts have been made by the central government to push demand for the housing

markets outside the main five hottest markets, yet the results have been meagre so

far.

In conclusion, after the dissipation of the initial hype, the fog has cleared to the reality

that little is clear as of yet as to the true effectiveness of China’s next growth stimu-

lus. The dry bulk market may have bolstered slightly over the past week, but it’s too

early to have been caused by any shift in fundamentals from anything decided in Bei-

jing this past week.

George Lazaridis

Head of Market Research & Asset Valuations

07th - 11th March 2016 | Week 10

Dry Bulk Freight Market

Secondhand Market

Newbuilding Market

Demolition Market

Economic Indicators

Tanker Freight Market

11 Mar ±∆ ±%BDTI 833 p 113 15.7%

BCTI 502 q -16 -3.1%

W-O-W change

Avg Price Index (main 5 regions)

11 Mar ±∆ ±%Dry 215 p 26 13.8%

Wet 237 p 30 14.5%

W-O-W change

Aggregate Price Index

11 Mar ±∆ ±%Bulkers 78 q -1 -1.5%

Cont 99 q -1 -0.7%

Tankers 99 q -2 -1.5%

Gas 99 q -1 -1.1%

M-O-M change

11 Mar ±∆ ±%Gold $ 1,265 p 153 13.8%

Oil WTI $ 39 p 8 24.6%

Oil Brent $ 40 p 6 18.1%

Iron Ore 57 p 13 28.4%

Coal 57 p 3 5.6%

M-O-M change

Aggregate Price Index

11 Mar ±∆ ±%Capesize 36 q -1 -2.5%

Panamax 33 q -1 -1.6%

Supramax 35 q 0 -1.0%

Handysize 42 q 0 -1.1%

M-O-M change

VLCC 105 q -4 -3.7%

Suezmax 93 q -6 -6.4%

Aframax 111 q -7 -6.0%

MR 120 q -3 -2.1%

2

2015 2016

07th - 11th March 2016

Capesize - Still no clear direction in sight for the large capesize segment, though

they managed to close off the week with a slight gain in the main index thanks to

slightly higher spot rates given out of Australia and South America. The market

however is still dragging its feet, unwilling to move in any clear direction quickly

and with a plethora of tonnage still lurking open in the market, it will be hard to

see a quick positive outcome to materialize over the next couple of days.

Panamax - Things quickly started to heat up in the Panamax market, as the North

Atlantic started to feel strong gains, being heavily supported by the still active

ECSA trade which has been keeping tonnage busy for more then two weeks now.

The Pacific was also quick to step up to the plate, giving another boost on that

side, also benefiting from the limited open tonnage thanks to the previous flux of

ballasters that headed westward, while the was also a good flow of fresh inquiries

to keep things hot.

Supramax - Things were almost equally active in the Supramax segment, with all

major routes showing strong gains on a week-on-week basis. The Pacific was

slightly lagging, though the gains should start to catch up there as well. A good

inflow of fresh enquiries should keep things in the green over the next couple of

days, though for now the main gains will likely hold mainly in the North Atlantic.

Handysize - A positive feel, though slightly softer then what the rest of the size

groups were noting. The market here is still not showing a clear picture as to its

strength, causing a lack of sentiment to get things going further.

0

5

10

15

20

25'000 US$/day

11 Mar 04 Mar ±% 2016 2015

Baltic Dry IndexBDI 388 349 11.2% 350 711

CapesizeBCI 176 164 7.3% 232 1,009

BCI 5TC $ 2,172 $ 2,221 -2.2% $ 2,906 $ 8,001ATLANTIC RV $ 1,850 $ 2,055 -10.0% $ 3,212 $ 8,206

Cont / FEast $ 6,291 $ 6,532 -3.7% $ 8,598 $ 16,387PACIFIC RV $ 2,284 $ 2,233 2.3% $ 2,299 $ 7,394

FEast / ECSA $ 2,986 $ 2,950 1.2% $ 3,303 $ 8,353Panamax

BPI 477 386 23.6% 364 690BPI - TCA $ 3,827 $ 3,098 23.5% $ 2,913 $ 5,513

ATLANTIC RV $ 3,300 $ 2,195 50.3% $ 2,279 $ 5,925Cont / FEast $ 6,767 $ 6,138 10.2% $ 6,165 $ 10,563PACIFIC RV $ 4,762 $ 3,673 29.6% $ 2,845 $ 5,021

FEast / Cont $ 480 $ 387 24.0% $ 361 $ 542Supramax

BSI 420 371 13.2% 343 662BSI - TCA $ 4,391 $ 3,875 13.3% $ 3,589 $ 6,919

Cont / FEast $ 7,800 $ 6,533 19.4% $ 6,141 $ 9,890Med / Feast $ 6,571 $ 5,875 11.8% $ 5,720 $ 9,274PACIFIC RV $ 4,392 $ 4,142 6.0% $ 3,288 $ 5,989

FEast / Cont $ 2,000 $ 1,680 19.0% $ 1,651 $ 4,794USG / Skaw $ 6,019 $ 5,644 6.6% $ 5,767 $ 10,915Skaw / USG $ 1,950 $ 1,307 49.2% $ 1,202 $ 3,705

HandysizeBHSI 249 232 7.3% 223 364

BHSI - TCA $ 3,690 $ 3,446 7.1% $ 3,298 $ 5,354Skaw / Rio $ 2,236 $ 2,054 8.9% $ 2,046 $ 3,770

Skaw / Boston $ 2,542 $ 2,358 7.8% $ 2,103 $ 4,057Rio / Skaw $ 5,764 $ 5,344 7.9% $ 4,467 $ 8,526

USG / Skaw $ 4,818 $ 4,668 3.2% $ 4,775 $ 7,200SEAsia / Aus / Jap $ 3,036 $ 2,789 8.9% $ 2,895 $ 4,211

PACIFIC RV $ 4,043 $ 3,782 6.9% $ 3,600 $ 5,429

Spot market rates & indices Average

0

500

1,000

1,500

2,000

2,500

3,000

BDI BCI BPI BSI BHSI

0

2

4

6

8

10'000 US$/day

0

5

10

15'000 US$/day

0

3

6

9

12

15'000 US$/day

3

2015 2016

Crude Oil Carriers - Things fired up this past week in the crude oil tankers, with

the MEG showing a strong inflow of fresh inquiries boosting the late March pro-

gram and giving a strong boost on rates. Delays being noted in the Far East helped

keep tonnage lists fairly tight, while the higher interest amongst oil traders is likely

to keep things tight for both westbound and Eastbound voyages while also in-

creasing interest in the WAF as well. .

Oil Products - A mismatch of available tonnage coupled with slight softer enquir-

ies pushed for a further correction in rates this week. Things were on the low key

in the USAC and Caribs area, while the North Atlantic in general was poised for

slightly softer levels due to a diminished price arbitrage opportunity. Things were

looking more promising in the Pacific with demand from the Far East showing

signs of strengthening further. The Black Sea/Med region is also expected to pro-

vide some support over the next couple of days as things still hold firm there.

07th - 11th March 2016

11 Mar 04 Mar ±% 2016 2015

Baltic Tanker IndicesBDTI 833 720 15.7% 836 820BCTI 502 518 -3.1% 600 637

VLCCWS 46.00 28.33 62.4% 39.69 36.36

$/day $ 32,930 $ 15,141 117.5% $ 28,141 $ 31,968WS 94.32 53.32 76.9% 68.76 64.43

$/day $ 91,648 $ 50,276 82.3% $ 63,393 $ 61,629WS 92.18 51.71 78.3% 67.39 63.09

$/day $ 78,128 $ 39,570 97.4% $ 55,662 $ 68,288WS 87.50 65.00 34.6% 76.91 72.72

$/day $ 118,546 $ 85,749 38.2% $ 103,453 $ 76,589SUEZMAX

WS 72.50 65.00 11.5% 83.87 81.13$/day $ 44,245 $ 39,279 12.6% $ 54,032 $ 46,404

WS 81.14 74.86 8.4% 96.09 91.34$/day $ 25,388 $ 22,708 11.8% $ 37,291 $ 46,346

AFRAMAXWS 92.50 92.50 0.0% 103.83 111.01

$/day $ 17,214 $ 18,855 -8.7% $ 26,861 $ 37,053WS 131.89 119.72 10.2% 123.06 112.26

$/day $ 28,620 $ 26,582 7.7% $ 27,559 $ 31,406WS 135.28 138.33 -2.2% 128.20 133.63

$/day $ 27,553 $ 29,450 -6.4% $ 26,719 $ 37,962WS 70.00 72.50 -3.4% 86.58 92.57

$/day $ 19,025 $ 22,038 -13.7% $ 31,861 $ 43,406DPP

WS 122.50 130.00 -5.8% 133.92 138.77$/day $ 28,703 $ 31,641 -9.3% $ 32,803 $ 30,727

WS 92.50 100.75 -8.2% 122.14 122.73$/day $ 20,763 $ 23,983 -13.4% $ 34,187 $ 30,281

WS 138.69 119.06 16.5% 118.53 110.54$/day $ 34,976 $ 29,718 17.7% $ 29,644 $ 35,804

WS 111.56 84.28 32.4% 96.97 108.70$/day $ 24,295 $ 14,378 69.0% $ 20,195 $ 35,902

CPPWS 97.22 87.72 10.8% 112.25 105.50

$/day $ 18,422 $ 17,068 7.9% $ 23,830 $ 28,796WS 97.05 113.41 -14.4% 125.15 134.68

$/day $ 8,321 $ 11,801 -29.5% $ 14,261 $ 18,755WS 130.00 175.00 -25.7% 140.15 134.05

$/day $ 23,281 $ 34,812 -33.1% $ 26,119 $ 22,099WS 90.00 112.50 -20.0% 100.01 96.47

$/day $ 7,607 $ 12,041 -36.8% $ 10,304 $ 12,481

MED-MED

CONT-USAC

USG-CONT

MEG-USG

MEG-SPORE

WAF-USG

BSEA-MED

MEG-SPORE

MEG-JAPAN

WAF-USAC

NSEA-CONT

CARIBS-USG

CARIBS-USAC

SEASIA-AUS

MEG-JAPAN

CARIBS-USAC

BALTIC-UKC

ARA-USG

Spot market rates & indices Average

250

450

650

850

1,050

1,250

BDTI BCTI

-101030507090

110'000 US$/day

-25

0

25

50

75

100'000 US$/day

0

20

40

60

80

100'000 US$/day

5101520253035

'000 US$/day

4

last 5 years

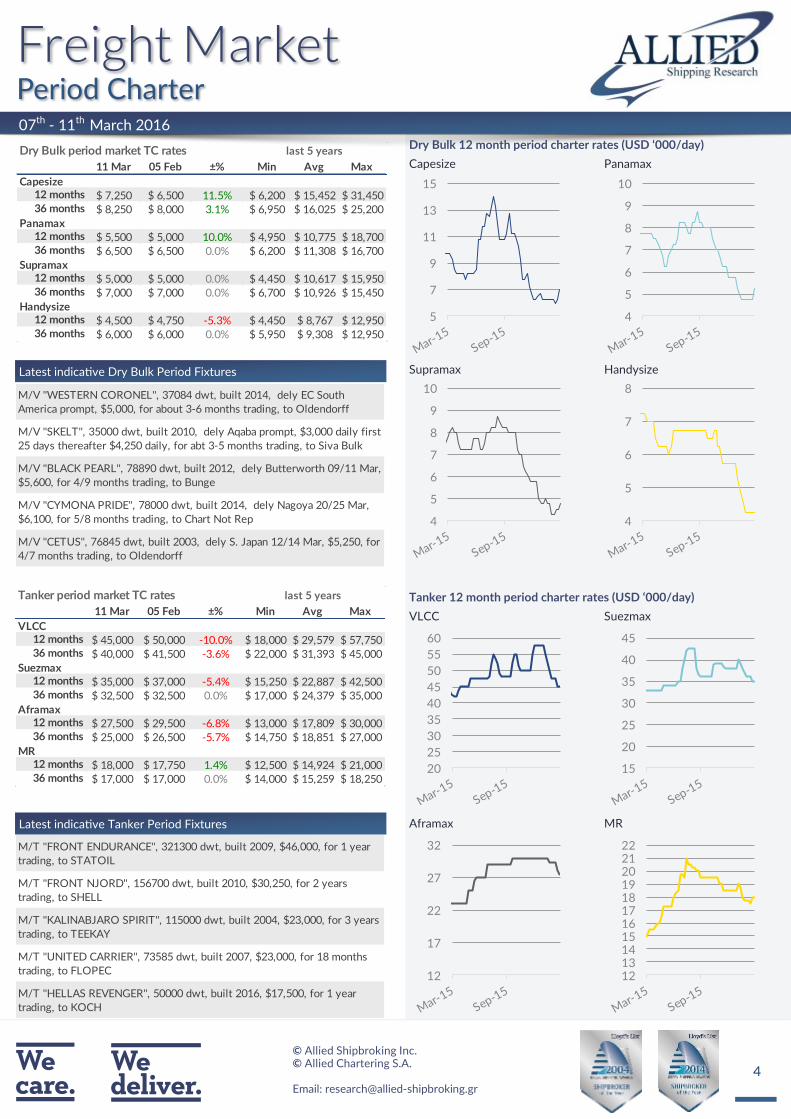

11 Mar 05 Feb ±% Min Avg Max

VLCC

$ 45,000 $ 50,000 -10.0% $ 18,000 $ 29,579 $ 57,750

$ 40,000 $ 41,500 -3.6% $ 22,000 $ 31,393 $ 45,000

Suezmax

$ 35,000 $ 37,000 -5.4% $ 15,250 $ 22,887 $ 42,500

$ 32,500 $ 32,500 0.0% $ 17,000 $ 24,379 $ 35,000

Aframax

$ 27,500 $ 29,500 -6.8% $ 13,000 $ 17,809 $ 30,000

$ 25,000 $ 26,500 -5.7% $ 14,750 $ 18,851 $ 27,000

MR

$ 18,000 $ 17,750 1.4% $ 12,500 $ 14,924 $ 21,000

$ 17,000 $ 17,000 0.0% $ 14,000 $ 15,259 $ 18,250

12 months

36 months

12 months

36 months

Tanker period market TC rates

12 months

36 months

12 months

36 months

last 5 years

11 Mar 05 Feb ±% Min Avg Max

Capesize

$ 7,250 $ 6,500 11.5% $ 6,200 $ 15,452 $ 31,450

$ 8,250 $ 8,000 3.1% $ 6,950 $ 16,025 $ 25,200

Panamax

$ 5,500 $ 5,000 10.0% $ 4,950 $ 10,775 $ 18,700

$ 6,500 $ 6,500 0.0% $ 6,200 $ 11,308 $ 16,700

Supramax

$ 5,000 $ 5,000 0.0% $ 4,450 $ 10,617 $ 15,950

$ 7,000 $ 7,000 0.0% $ 6,700 $ 10,926 $ 15,450

Handysize

$ 4,500 $ 4,750 -5.3% $ 4,450 $ 8,767 $ 12,950

$ 6,000 $ 6,000 0.0% $ 5,950 $ 9,308 $ 12,950

12 months

Dry Bulk period market TC rates

12 months

36 months

36 months

12 months

36 months

12 months

36 months

07th - 11th March 2016

Latest indicative Dry Bulk Period Fixtures

Latest indicative Tanker Period Fixtures

5

7

9

11

13

15

4

5

6

7

8

9

10

4

5

6

7

8

9

10

4

5

6

7

8

20

25

30

35

40

45

50

55

60

15

20

25

30

35

40

45

12

17

22

27

32

1213141516171819202122M/T ''FRONT ENDURANCE'', 321300 dwt, built 2009, $46,000, for 1 year

trading, to STATOIL

M/T ''FRONT NJORD'', 156700 dwt, built 2010, $30,250, for 2 years

trading, to SHELL

M/T ''KALINABJARO SPIRIT'', 115000 dwt, built 2004, $23,000, for 3 years

trading, to TEEKAY

M/T ''UNITED CARRIER'', 73585 dwt, built 2007, $23,000, for 18 months

trading, to FLOPEC

M/T ''HELLAS REVENGER'', 50000 dwt, built 2016, $17,500, for 1 year

trading, to KOCH

M/V ''WESTERN CORONEL'', 37084 dwt, built 2014, dely EC South

America prompt, $5,000, for about 3-6 months trading, to Oldendorff

M/V ''SKELT'', 35000 dwt, built 2010, dely Aqaba prompt, $3,000 daily first

25 days thereafter $4,250 daily, for abt 3-5 months trading, to Siva Bulk

M/V ''BLACK PEARL'', 78890 dwt, built 2012, dely Butterworth 09/11 Mar,

$5,600, for 4/9 months trading, to Bunge

M/V ''CYMONA PRIDE'', 78000 dwt, built 2014, dely Nagoya 20/25 Mar,

$6,100, for 5/8 months trading, to Chart Not Rep

M/V ''CETUS'', 76845 dwt, built 2003, dely S. Japan 12/14 Mar, $5,250, for

4/7 months trading, to Oldendorff

5

Reported Transactions

Despite the fact that on face value it looks as though the newbuild-

ing market was suddenly given new life, the reported activity holds a

slight misdirection as to the given position of the market right now.

There was a strong order placed in the very large dry bulkers this

week, supported by Brazil’s Vale and the Chinese government, both

of whom for their separate reasons have made a move in contrary to

what the market fundamentals dictate. Through the determination to

minimize its freight costs and increase its competitiveness, the major

Brazilian iron ore producer has found a close ally within the Chinese

government how have eagerly taken up this opportunity to prop up

their national orderbook and support their shipbuilders. Beyond this

order the rest have been for considerably smaller sized orders (both

in number of units and the size of the vessels in question), while the

focus is still on the more specialized vessels which are harder to be

sourced from within the secondhand market. As such it looks as

though things are still subdued in terms of real interest in newbuild-

ing orders and government support is still playing a major role in

keeping some shipbuilders afloat.

07th - 11th March 2016

10

20

30

40

50

60

Capesize Panamax Supramax Handysize

US$ million

30

50

70

90

110VLCC Suezmax Aframax LR1 MR

US$ million

Indicative Dry NB Prices (US$ million) last 5 years

11 Mar 05 Feb ±% Min Avg Max

Dry Bulkers

Capesize (180,000dwt) 45.5 46.0 -1.1% 45.5 50.4 58.0

Kamsarmax (82,000dwt) 26.0 26.3 -1.0% 26.0 29.1 36.5

Panamax (77,000dwt) 25.3 25.8 -1.9% 25.3 28.2 34.5

Ultramax (64,000dwt) 24.0 24.3 -1.0% 24.0 26.4 31.0

Handysize (37,000dwt) 20.0 20.5 -2.4% 20.0 22.4 26.5

Container

Post Panamax (9,000teu) 87.0 88.0 -1.1% 76.5 86.6 94.5

Panamax (5,200teu) 55.0 56.0 -1.8% 48.6 57.2 65.6

Sub Panamax (2,500teu) 29.5 29.5 0.0% 29.5 33.1 41.0

Feeder (1,700teu) 20.5 20.5 0.0% 20.5 24.5 29.4

Indicative Wet NB Prices (US$ million) last 5 years

11 Mar 05 Feb ±% Min Avg Max

Tankers

VLCC (300,000dwt) 92.5 93.5 -1.1% 89.5 96.3 104.0

Suezmax (160,000dwt) 61.5 62.5 -1.6% 55.8 61.5 66.0

Aframax (115,000dwt) 50.5 51.5 -1.9% 47.0 51.9 56.0

LR1 (75,000dwt) 45.0 45.8 -1.6% 40.5 44.0 47.0

MR (56,000dwt) 35.0 35.5 -1.4% 33.5 35.3 37.3

Gas

LNG 160k cbm 199.0 199.0 0.0% 198.0 200.1 203.0

LPG LGC 80k cbm 76.5 77.0 -0.6% 70.0 74.2 80.0

LPG MGC 55k cbm 66.5 67.5 -1.5% 62.0 64.6 68.5

LPG SGC 25k cbm 44.0 45.0 -2.2% 41.0 44.1 46.5

Type Units Size Shipbuilder Price Buyer Delivery Comments

BULK 10 400,000 dwt SWS, China N/ACHINA COSCO SHIPPING -

China2018

BULK 6 400,000 dwt YANGZIJIANG, China N/A ICBC LEASING - China 2018

BULK 7 400,000 dwt BEIHAI, China N/A ICBC LEASING - China 2018

BULK 4 34,500 dwt OSHIMA SHIPBUILDING, Japan N/A FEDNAV - Canada 2018

TANKER 1 49,800 dwt ONOMICHI, Japan N/AFAIRFIELD CHEMICAL

CARRIERS - U. S. A.2019 Declared option

TANKER 2 7,000 dwt CHENGXI SHIPYARD, China N/A WINNING INT, - Singapore 2016/2017

GAS 1 7,500 cbm MURAKAMI, Japan N/AWISDOM MARINE LINES -

Taiwan2017

6

Indicative Dry Bulk Values (US$ million)

11 Mar 05 Feb ±% Min Avg Max

Capesize180k dwt Resale 35.0 36.0 -2.8% 35.0 49.0 65.0170k dwt 5 year old 23.0 23.0 0.0% 23.0 37.8 53.0170k dwt 10 year old 12.0 13.0 -7.7% 12.0 26.0 39.0150k dwt 15 year old 6.5 6.5 0.0% 6.5 15.7 25.0Panamax82k dwt Resale 23.0 23.0 0.0% 23.0 31.1 43.076k dwt 5 year old 11.5 11.5 0.0% 11.5 22.6 36.876k dwt 10 year old 7.3 7.3 0.0% 7.3 16.8 29.374k dwt 15 year old 3.5 4.0 -12.5% 3.5 11.1 22.0Supramax62k dwt Resale 19.5 20.0 -2.5% 19.5 29.0 36.858k dwt 5 year old 11.0 11.0 0.0% 11.0 21.7 30.552k dwt 10 year old 6.0 6.0 0.0% 6.0 15.8 24.352k dwt 15 year old 3.5 3.5 0.0% 3.5 10.6 19.0Handysize37k dwt Resale 17.5 18.0 -2.8% 17.5 23.4 30.032k dwt 5 year old 9.0 9.0 0.0% 9.0 17.8 25.532k dwt 10 year old 6.0 6.0 0.0% 6.0 13.3 19.528k dwt 15 year old 3.5 3.5 0.0% 3.5 9.0 14.5

last 5 years

07th - 11th March 2016

On the dry bulk side, activity had picked up slightly, though prices

have started to show an ability to hold at their current levels, given

both the improvement from within the freight market as well as the

strong hike in scrap steel prices. Although both of these factors may

well be temporary and are still at weaker levels compared to where

they were a couple of months back, they might still be the initial

stages of a support level that has been growing on behalf of the

sellers side and could well prove to cause difficulties in allowing any

significant further price drops to be noted over the coming weeks.

On the tanker side, activity was fairly subdued, while the drop in

prices has been in part the cause for a noticeable withdrawal of sales

candidates. Being that the freight market still lacks a clear direction

for the long-term, a sort of mismatch gap between sellers and buyers

has grown in size, and keeping activity subdued.

+0%

-12%

-34%

-30%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

1 month diff 3 months diff6 months diff 12 months diff

+0% +0%

-36%-32%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

1 month diff 3 months diff6 months diff 12 months diff

+0% +0%

-29%

-33%-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

1 month diff 3 months diff6 months diff 12 months diff

+0% +0%

-31%

-38%-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

1 month diff 3 months diff6 months diff 12 months diff

-5% -5%

-8%

-6%

-9%

-8%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1 month diff 3 months diff6 months diff 12 months diff

-8%

-9%

-11%

-6%

-12%

-10%

-8%

-6%

-4%

-2%

0%

1 month diff 3 months diff6 months diff 12 months diff

-11%

-13%

-11% -11%

-14%

-13%

-13%

-12%

-12%

-11%

-11%

-10%

1 month diff 3 months diff6 months diff 12 months diff

-2%

-5%

-4%

+2%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

1 month diff 3 months diff6 months diff 12 months diff

Indicative Tanker Values (US$ million)

11 Mar 05 Feb ±% Min Avg Max

VLCC310k dwt Resale 96.0 98.0 -2.0% 80.0 95.3 108.5310k dwt 5 year old 76.0 80.0 -5.0% 55.0 70.2 87.0250k dwt 10 year old 56.0 57.0 -1.8% 33.8 46.2 62.0250k dwt 15 year old 36.0 38.0 -5.3% 16.9 27.4 41.0Suezmax160k dwt Resale 66.0 69.0 -4.3% 53.0 64.0 73.0150k dwt 5 year old 54.5 59.0 -7.6% 38.0 50.0 62.0150k dwt 10 year old 40.0 44.0 -9.1% 24.0 33.8 44.5150k dwt 15 year old 22.0 23.0 -4.3% 14.0 18.7 23.3Aframax110k dwt Resale 55.0 55.0 0.0% 39.0 48.6 57.0110k dwt 5 year old 40.0 45.0 -11.1% 27.0 36.9 47.5105k dwt 10 year old 27.0 30.0 -10.0% 16.0 24.0 33.0105k dwt 15 year old 16.5 17.0 -2.9% 8.0 13.1 18.5MR52k dwt Resale 36.0 37.0 -2.7% 32.0 36.9 39.352k dwt 5 year old 27.5 28.0 -1.8% 22.0 26.9 31.045k dwt 10 year old 20.0 20.0 0.0% 14.0 17.9 21.045k dwt 15 year old 12.5 13.0 -3.8% 9.0 11.0 13.5

last 5 years

7

07th - 11th March 2016

Size Name Dwt Built Shipbuilder M/E Coating Price Buyers Comments

AFRA TRIDENT STAR 105,996 2005 NAMURA IMARI,

JapanMAN-B&W $ 26.0m Thai - Nathalin

buyer subs untill end

March

AFRA RATNA PUJA 104,635 2006

SHANGHAI

WAIGAOQIAO,

China

MAN-B&W $ 22.5m Greek - Eurotankers on subs

PROD/

CHEMDEVA MARIA 13,921 1990

SHIN KURUSHIMA

AKITSU, JapanB&W St St $ 2.5m undisclosed

Size Name Dwt Built Shipbuilder M/E Gear Price Buyers Comments

KMAX TENSHIN MARU 82,687 2008 TSUNEISHI

ZHOUSHAN, ChinaMAN-B&W $ 8.0m Greek

PMAX ZEYNEP K 80,669 2010 STX OFFSHORE &

SHBLDG, S. KoreaMAN-B&W $ 10.3m

PMAX SADAN K 80,306 2010 STX OFFSHORE &

SHBLDG, S. KoreaMAN-B&W $ 10.3m

PMAX JI MAY 75,900 2001 TSUNEISHI, Japan B&W $ 3.7m Chinese just passed SS/DD

PMAX CORAL SEAS 74,476 2006

HUDONG-

ZHONGHUA

SHIPBU, China

MAN-B&W N/A

PMAX GOLDEN SEAS 74,475 2006

HUDONG-

ZHONGHUA

SHIPBU, China

MAN-B&W N/A

HANDY PROSPEROUS SEAS 37,294 2012 ZHEJIANG OUHUA

SHBLDG, ChinaWartsila

4 X 30t

CRANESN/A

HANDY PROUD SEAS 37,227 2014 ZHEJIANG OUHUA

SHBLDG, ChinaWartsila

4 X 30t

CRANESN/A

HANDY PRECIOUS SEAS 37,205 2012 ZHEJIANG OUHUA

SHBLDG, ChinaWartsila

4 X 30t

CRANESN/A

HANDY PRICELESS SEAS 37,202 2013 ZHEJIANG OUHUA

SHBLDG, ChinaWartsila

4 X 30t

CRANESN/A

PMAXWASHINGTON

TRADER74,228 2000

SASEBO SASEBO,

JapanB&W $ 2.7m Chinese

PMAX IOANNIS F K 74,190 2001 NAMURA IMARI,

JapanB&W $ 3.2m Chinese

SMAX CALYPSO COLOSSUS 55,429 2009

KAWASAKI

SHIPBUILDING,

Japan

MAN-B&W4 X 30,5t

CRANES$ 8.3m

Bangladeshi - SR

Shipping

SMAX SECRET 55,395 2013 HYUNDAI

VINASHIN, VietnamMAN-B&W

4 X 35t

CRANES$ 8.3m

SMAX CAPITAL 55,340 2013 HYUNDAI

VINASHIN, VietnamMAN-B&W

4 X 30t

CRANES$ 8.5m

SMAX GLOBAL ISLAND 53,556 2004 IWAGI, Japan MAN-B&W4 X 30,5t

CRANES$ 4.5m Greek - L.A Maritime

HMAX AURORA SAPPHIRE 48,893 2000 IHI - TOKYO, Japan Sulzer4 X 30t

CRANES$ 3.0m Bangladeshi

HANDY AEC ENDURANCE 37,500 2016 SHIMANAMI, Japan MAN-B&W4 X 30,5t

CRANES$ 15.0m Japanese incl. 1yr TC Back

Tankers

Bulk Carriers

undisclosed bank controlled deal

via auction, pending

deposit South African

Greek

8

07th - 11th March 2016

Type Name Dwt Built Shipbuilder M/E Gear Price Buyers Comments

General

CargoADDI L 4,557 1995 SLIP, Russia Deutz $ 1.5m undisclosed

General

CargoFAABORG 3,469 2004

SLOVENSKE,

SlovakiaMaK

2 X 35t

CRANES$ 2.95m undisclosed

General

CargoHERTFORDSHIRE 2,489 1995

SLOVENSKE,

SlovakiaDeutz $ 1.0m undisclosed

Size Name TEU Built Shipbuilder M/E Gear Price Buyers Comments

PMAX PRETORIA 4,389 2002

HANJIN HI &

CONST - BU, S.

Korea

MAN-B&W N/A Chinese

PMAX NORDIC WISMAR 3,421 2011

RONGCHENG

SHENFEI SHIP,

China

Wartsila

3 X 45t

CRANES,

1 X 35t

CRANES

$ 20.0mNorwegian - Ness

Risan

Gen. Cargo

Containers

9

The market was struck by a sudden shift in global fundamentals in

regards to steel, causing a speculative fever to hit some of the

shipbreakers across the Indian Sub-Continent as well. Most of the

drive seems to have been building off the spike in iron ore prices that

emerged early on Monday, while the fact that some owners of over-

aged dry bulkers took a “wait and see” stance this past week also

kept demo candidates on the wain. For the moment it looks as

though the spike in offered demo prices is more based on the opti-

mistic feeling circulating the market for the moment rather then from

an actual demand spike. To what extent this may hold will heavily

depend on the effectiveness of China’s new 5 year plan and the ex-

tent of the cash they will push towards new construction and other

investment projects. It is however to early to call and as such these

price levels may well wane given that their rise might have been too

quick for the market to support just yet.

07th - 11th March 2016

Reported Transactions

100150200250300350400450500

Bangladesh India Pakistan China Turkey

US$/ldt

100150200250300350400450500

Bangladesh India Pakistan China Turkey

US$/ldt

Indicative Wet Prices ($/ldt) last 5 years

11 Mar 04 Mar ±% Min Avg Max

Indian Sub Continent

Bangladesh 285 250 14.0% 245 429 540

India 285 255 11.8% 250 438 550

Pakistan 285 255 11.8% 245 434 525

Far East Asia

China 150 120 25.0% 120 332 485

Mediterranean

Turkey 180 155 16.1% 150 273 355

Indicative Dry Prices ($/ldt) last 5 years

11 Mar 04 Mar ±% Min Avg Max

Indian Sub Continent

Bangladesh 255 225 13.3% 220 408 515

India 255 230 10.9% 225 415 525

Pakistan 255 230 10.9% 220 411 510

Far East Asia

China 140 110 27.3% 110 315 455

Mediterranean

Turkey 170 150 13.3% 145 263 355

Type Vessel's Name Dwt Built Country Built Ldt US$/ldt Buyer Sale Comments

Bulker CAPE CENTURY 172,683 2001 Japan 21,104 $ 247/Ldt Pakistani bss 'as is' S'pore, incl. 250tns ROB

Bulker CAPE VENUS 172,612 1996 Japan 21,165 $ 239/Ldt Indian Green recycling - incl. 600tns ROB

Bulker POS AMBITION 149,330 1992 S. Korea 17,077 $ 245/Ldt Bangladeshi sunb-con options

Cont ZAMBIA 82,171 1998 Japan 28,544 $ 290/Ldt Bangladeshi incl. 80tns propeller & extra bunkers

Bulker AQUARIA 73,236 1994 S. Korea 10,481 $ 240/Ldt Indian

Bulker SUERTE 72,516 1995 S. Korea 11,343 $ 262/Ldt Indian bss 'as is' S'pore

Bulker ORIENT RICH 70,119 1995 Japan 9,284 $ 260/Ldt Indian

Bulker MIGHTY PLEIADES 68,962 1997 Japan 9,543 $ 230/Ldt Indian

Bulker MP PANAMAX 6 68,541 1995 Japan 10,306 $ 256/Ldt undisclosed bss 'as is' Colombo, incl. 200tns ROB

Bulker THE CREATOR 68,519 1995 Japan 9,861 $ 260/Ldt undisclosed sunb-con options

Cont MOL INTEGRITY 66,559 2001 Japan 24,572 $ 258/Ldt undisclosed net price - bss 'as is' S'pore; incl. 300tns ROB

Cont NORTHERN DIVINITY 45,117 1997 S. Korea 14,446 $ 257/Ldt Indian bss 'as is' S'pore incl/ 200tns ROB

Tanker KAMPOS 41,465 1991 Japan 8,223 $ 240/Ldt Pakistani bss 'as is' S'pore

ContCAPT. STEVEN L.

BENNETT41,151 1984 S. Korea 13,147 $ 293/Ldt Indian incl. 600tns ROB

Cont ARNOLD SCHULTE 41,000 2002 S. Korea 13,900 $ 273/Ldt Indian bss 'as is' S'pore

10

350

400

450

500

550

600

650

07th - 11th March 2016

US Dollar per Euro Yen per US Dollar

Iron Ore (TSI) Coal Price Index

Yuan per US Dollar US Dollar INDEX

Oil WTI $ Palm Oil

Korean owner Hanjin Shipping is reportedly looking to find KRW 1.2

trillion ($1bn) through asset sales and savings to refinance its debt.

The Korea Economic Daily, citing government and creditor officials,

said the company will take a number of approaches to boost its financ-

es. More old vessels will be sold or jobs cut to save KRW 500bn to the

end of 2020, while it will seek to raise KRW 500bn in 2016 alone

through asset sales.

The company also wants to lower its debt ratio from 600% to 400%

on borrowings of KRW 6 trillion. It has already been reported that

Hanjin is considering a sale of 30-year bonds worth KRW 220bn, at

interest of more than 9.5%. The container line and bulker player is also

mulling the disposal of US and European trademark rights to invest-

ment company Hanjin Kal for KRW 111.3bn. It may also sell treasury

stock worth KRW 37bn and an office building in London. Hanjin is

facing $406m of maturing debts in the first six months of 2016.

The company said its net profit was $6m last year, compared to a defi-

cit of $396m in the previous 12 months. Revenue fell to $6.86bn,

down 15.3% due to lower freight rates, but its operating profit rose to

$41m, from $26m, its second year in the black. Source: Tradewinds

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

110.00

112.00

114.00

116.00

118.00

120.00

122.00

124.00

126.00

6.00

6.10

6.20

6.30

6.40

6.50

6.60

6.70

84.00

89.00

94.00

99.00

104.00

109.00

30.00

40.00

50.00

60.00

70.00

80.00

45.00

50.00

55.00

60.00

65.00

70.00

25.00

30.00

35.00

40.00

45.00

50.00

55.00

60.00

65.00

11 Mar 05 Feb ±% Min Avg Max

Markets

10year US Bond 1.98 1.85 7.0% 1.64 2.13 2.48

S&P 500 2,022.2 1,880.1 7.6% 1,829 2,036 2,131

Nasdaq 4,748.5 4,363.1 8.8% 4,267 4,903 5,219

Dow Jones 17,213.3 16,205.0 6.2% 15,660 17,338 18,312

FTSE 100 6,139.8 5,848.1 5.0% 5,537 6,431 7,104

FTSE All-Share UK 3,367.5 3,215.1 4.7% 3,047 3,517 3,834

CAC40 4,492.8 4,200.7 7.0% 3,897 4,764 5,269

Xetra Dax 9,831.1 9,286.2 5.9% 8,753 10,752 12,375

Nikkei 16,938.9 16,819.6 0.7% 14,953 18,991 20,868

Hang Seng 20,199.6 19,288.2 4.7% 18,320 23,401 28,443

DJ US Maritime 197.7 170.6 15.8% 150.2 221.6 275.4

Currencies

$ per € 1.11 1.12 -0.7% 1.06 1.10 1.16

$ per ₤ 1.43 1.45 -1.2% 1.39 1.51 1.59

₤ per € 0.77 0.77 0.5% 0.70 0.73 0.79

¥ per $ 113.6 116.8 -2.8% 111.8 120.5 125.1

$ per Au$ 0.75 0.71 5.5% 0.69 0.74 0.81

$ per NoK 0.12 0.12 1.2% 0.11 0.12 0.14

$ per SFr 0.98 0.99 -0.7% 0.91 0.97 1.03

Yuan per $ 6.50 6.57 -1.1% 6.16 6.33 6.60

Won per $ 1,194.4 1,199.2 -0.4% 1,069.2 1,153.8 1,237.8

$ INDEX 102.6 104.2 -1.5% 99.5 103.9 107.4

Commoditites

Gold $ 1,264.8 1,111.8 13.8% 1,049.4 1,146.3 1,277.5

Oil WTI $ 38.5 30.9 24.6% 26.9 45.6 61.4

Oil Brent $ 40.3 34.1 18.1% 28.2 49.6 68.3

Palm Oil 562.0 562.0 0.0% 437.5 561.8 630.5

Iron Ore 57.4 44.7 28.4% 37.0 51.6 65.4

Coal Price Index 57.0 54.0 5.6% 47.3 55.6 68.5

White Sugar 427.3 380.0 12.4% 333.6 377.5 428.8

last 12 months

11

ALLIED SHIPBROKING INC. 48, Aigialeias Street, 4th Floor, Maroussi 151 25, Greece Tel: +30 210 45 24 500 Fax: +30 210 45 25 017/ 019 E-mail: [email protected]

ALLIED CHARTERING S.A. 48, Aigialeias Street, 4th Floor, Maroussi 151 25, Greece Tel : +30 210 42 88 100 Fax: +30 210 45 24 201

E-mail: [email protected]

E-mail: [email protected]

07th - 11th March 2016 | Week 10

AERAKIS GEORGEMOBILE: +30 6946 04 57 37

BOLIS ILIASMOBILE: +30 6937 02 65 00

DASKALAKIS GEORGEMOBILE: +30 6932 24 80 07

DRAKOGIANNOPOULOS STAVROSMOBILE: +30 6932 20 15 65

DRAKOGIANNOPOULOS SAKISMOBILE: +30 6944 88 58 08

HATZIGEORGIOU NASSOSMOBILE: +30 6944 73 33 93

KARADIMAS COSTASMOBILE: +30 6932 20 15 64

KLONIZAKIS JOHNMOBILE: +30 6948 50 55 81

KOSTOYANNIS JOHNMOBILE: +30 6932 43 39 99

MANOLAS NIKOLASMOBILE: +30 6940 63 22 56

MOISSOGLOU THEODOROSMOBILE: +30 6932 45 52 41

PAPOUIS THASSOSMOBILE: +30 6944 29 49 89

PRACHALIAS ARGIRISMOBILE: +30 6947 62 82 62

STASSINAKIS JOHNMOBILE: +30 6972 60 92 09

TSALPATOUROS COSTISMOBILE: +30 6932 20 15 63

VARVAROS PLUTONMOBILE: +30 6937 25 15 15

LAZARIDIS GEORGE MOBILE: +30 6946 95 69 40

Maritime Research & Valuations

Sale & PurchaseALEXOPOULOS PANOS

MOBILE: +30 6944 34 66 15

DAOULAS SPYROS MOBILE: +30 6932 27 88 40

KAILAS VAGGELISMOBILE: +30 6942 48 05 69

KANELLOS DIMITRIS MOBILE: +30 6945 07 47 85

KAPPA ANGELIKI MOBILE: +30 6975 85 60 84

KARAMANIS COSTASMOBILE: +30 6941 54 14 65

KARAMANI NATALIA MOBILE: +30 6984 58 82 99

MANOLOPOULOS VASSILISMOBILE: +30 6988 88 13 05

MAVRIKOU GEORGINA MOBILE: +30 6974 18 07 84

PATELIS DIMITRIS MOBILE: +30 6944 04 43 61

THEODOTOS ARISTOFANIS MOBILE: +30 6951 79 82 89

TSALPATOUROU MARGARITA MOBILE: +30 6934 74 22 16

FLOURIS JOHN MOBILE: +30 6955 80 15 03

FOUROULI STELLA MOBILE: +30 6947 35 68 48

PAPANTONOPOULOS NICOLAS MOBILE: +30 6945 23 21 88

Dry Cargo Chartering

Tanker Chartering

12

Disclaimer

The information contained within this report has been provided by Allied Shipbroking Inc. and Allied Chartering S.A. for general information

purposes.

All the information is compiled through Allied Shipbroking Inc. and Allied Chartering S.A. databases, as well as from other market sources. De-

spite having taken reasonable care in the gathering, filtering and auditing of this information and believing that the information is accurate and

correct, it may still contain errors, as a lot of the views regarding market levels are partially derived from estimates and/or subject judgments

while the reported transaction activity is gathered from several sources and rumors, some of which are sometimes hard to validate in full their

accuracy and truthfulness. As such we advise that the information be taken cautiously, while advising that this information does not obviate the

need to also make further enquiries and seek further information in order to obtain a more accurate outlook. As we make no warranties of any

kind, both expressed or implied, as to the completeness, accuracy, reliability or completeness of the information herein, Allied Shipbroking Inc.

and its connected persons shall not be held liable to any loss or damage of any kind, including direct, indirect and/or consequential damages

caused by negligence of any kind on our part.

Any choice to rely on this information provided is strictly at the recipient’s own risk.

This report and its information is confidential and solely for the internal use of its recipients, while any re-production or re-distribution of the

report and its material is strictly prohibited without prior permission from Allied Shipbroking Inc.

If you wish to subscribe to this or any other report we produce, please contact us directly.

Appendix

Aggregate Price Index quoted on the first page for both Newbuilding and Secondhand relates to the current average prices levels compared to

where they stood at 1st January 2010 (i.e. index 100 = 01/01/2010)

Demolition market average price index refers to the combination of the average prices currently offered in the Indian Sub-Continent, Far East

and Mediterranean.

Period rates currently relate to Capesize of 180,000dwt, Panamax of 76,000dwt, Supramax of 56,000dwt and Handysize of 33,000dwt on the

Dry Bulk side and VLCC of 250,000dwt, Suezmax of 150,000dwt, Aframax of 115,000dwt and MR of 52,000dwt on the Tankers side respec-

tively.

In terms of Secondhand Asset Prices their levels are quoted based on following description:

All vessels built to European specifications

by top Japanese shipbuilders, with dwt size

based on the below table.

07th - 11th March 2016 | Week 10

Resale 5 year old 10 year old 15 year old

Capesize 180,000dwt 170,000dwt 170,000dwt 150,000dwt

Panamax 82,000dwt 76,000dwt 76,000dwt 74,000dwt

Supramax 62,0000dwt 58,000dwt 52,000dwt 52,000dwt

Handysize 37,000dwt 32,000dwt 32,000dwt 28,000dwt

VLCC 310,000dwt 310,000dwt 250,000dwt 250,000dwt

Suezmax 160,000dwt 150,000dwt 150,000dwt 150,000dwt

Aframax 110,000dwt 110,000dwt 105,000dwt 95,000dwt

MR 52,000dwt 45,000dwt 45,000dwt 45,000dwt