Embed Size (px)

Citation preview

1 | P a g e

Economic Advisory Council to the Prime Minister

Manufacturing,

Emerging

Industries,

Trade,

Technology,

Services and

Skill

Development

2 | P a g e

3 | P a g e

Contents

Acknowledgements ........................................................................................................................................ 7

List of Tables and Figures ............................................................................................................................... 9

List of Members of the Working Group ........................................................................................................ 11

List of Abbreviations .................................................................................................................................... 13

Executive Summary ...................................................................................................................................... 15

Chapter 1. Blue Trade .................................................................................................................................. 21

1.1 Blue Trade in Goods: Emerging Trends ....................................................................................... 21

1.2 Issues in Blue Trade ........................................................................................................................ 21

1.3 Broad Blue Trade Sectors .............................................................................................................. 23

1.4 Trends in Global Maritime Service Trade ................................................................................... 26

1.5 Marine Service Trade in India ....................................................................................................... 28

1.6 Opportunities and Challenges in Marine Services Trade ........................................................... 29

1.7 Recommendations ........................................................................................................................... 31

Chapter 2. Blue Investment .......................................................................................................................... 33

2.1 Sectoral Relevance .......................................................................................................................... 33

2.2 Domestic Blue Initiatives ................................................................................................................ 34

2.3 Global Experience ........................................................................................................................... 37

2.4 Recommendations ........................................................................................................................... 38

Chapter 3. Blue SMEs ................................................................................................................................... 41

3.1 Emerging Sectors ............................................................................................................................ 41

3.2 Opportunities and Challenges........................................................................................................ 42

3.3 Global Strategies ............................................................................................................................. 45

3.4 Recommendations ........................................................................................................................... 45

Chapter 4. Blue Technologies ....................................................................................................................... 47

4.1 Relevance of Technology in Blue Economy .................................................................................. 47

4.2 Existing Potential and Status in Different Sectors ....................................................................... 48

4.2.1 Fishing Industry ....................................................................................................................... 48

4.2.2 Marine natural products ......................................................................................................... 48

4.2.3 Multidimensional Seaweed biorefinery design ...................................................................... 49

4.2.4 Gas Hydrate exploration ......................................................................................................... 49

4 | P a g e

4.2.5 Placer Minerals ........................................................................................................................ 50

4.3 Recommendations ........................................................................................................................... 51

Chapter 5. Marine Manufacturing ................................................................................................................ 53

5.1 Traditional Sectors .......................................................................................................................... 53

5.1.1 Fisheries .................................................................................................................................... 53

5.1.2 Shipping and Port Facilities .................................................................................................... 56

5.2 Emerging Sectors ............................................................................................................................ 58

5.2.1 Aquaculture .............................................................................................................................. 58

5.2.2 Energy ....................................................................................................................................... 58

5.2.3 Biotechnology ........................................................................................................................... 59

5.2.4 Mineral Prospecting ................................................................................................................. 60

5.3 Prospects for India .......................................................................................................................... 62

5.4 Recommendations ........................................................................................................................... 63

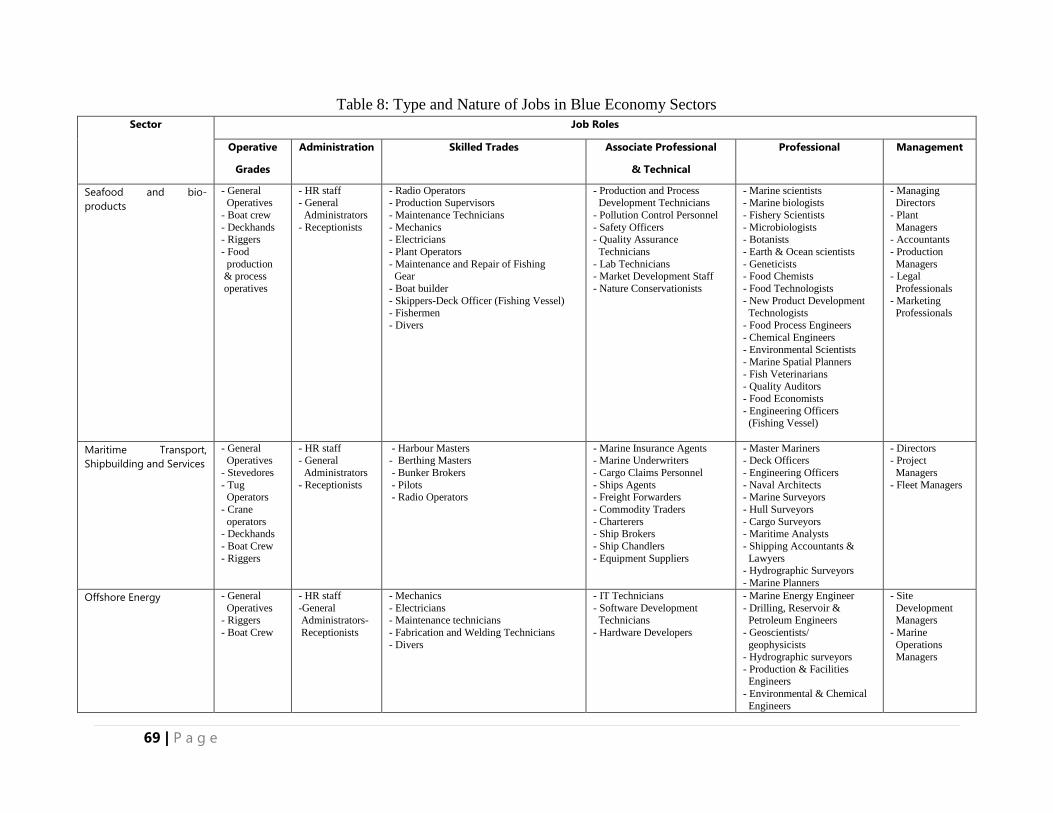

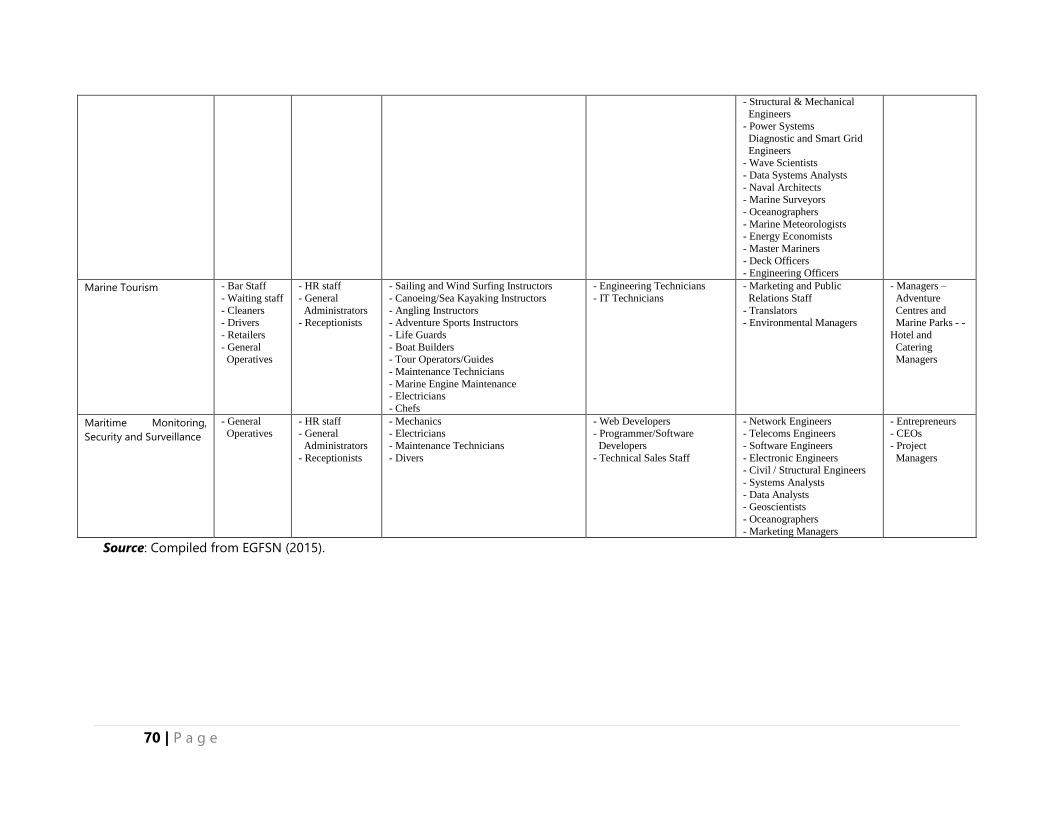

Chapter 6. Skill Development and Employment ........................................................................................... 67

6.1 Overview .......................................................................................................................................... 67

6.2 Nature and Types of Jobs in Blue Economy ................................................................................. 67

6.3 Employment in Blue Economy Sectors ......................................................................................... 72

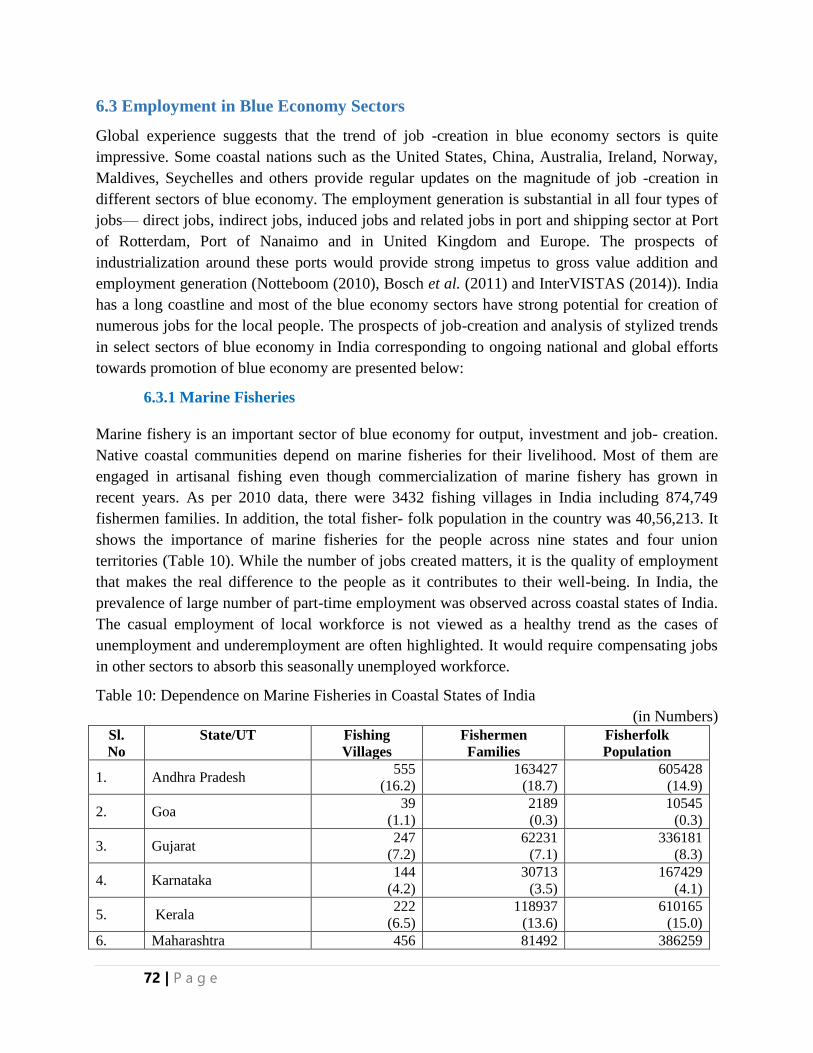

6.3.1 Marine Fisheries ....................................................................................................................... 72

6.3.2 Ports and Shipping ................................................................................................................... 74

6.3.3 Ocean Renewable Energy ........................................................................................................ 76

6.4 Recommendations ........................................................................................................................... 79

Chapter 7. Marine Services .......................................................................................................................... 81

7.1 Introduction ..................................................................................................................................... 81

7.2 Potential and Dynamics in Maritime Services Sectors ................................................................ 81

7.2.1 Ship Repair ............................................................................................................................... 82

7.2.2 Coastal Shipping ...................................................................................................................... 83

7.2.3 Port Services ............................................................................................................................. 85

7.2.4 Reception Facility ..................................................................................................................... 88

7.2.5 Seafarer Facilitation ................................................................................................................ 88

7.2.6 Pilotage ...................................................................................................................................... 88

7.2.7 Automation Traffic Control in the Maritime Sector ............................................................ 89

7.2.8 Logistics and Supply Chain Management ............................................................................. 89

5 | P a g e

7.2.9 Marine Finance and Insurance ............................................................................................... 90

7.2.10 Maritime Consultancy and Certification ............................................................................. 92

7.2.11 Maritime Personnel Services ................................................................................................. 92

7.2.12 Maritime Legal Services ........................................................................................................ 93

7.2.13 Marine Salvage Services ........................................................................................................ 94

7.2.14 Maritime Classification Services .......................................................................................... 95

7.2.15 Tourism and Recreation ........................................................................................................ 96

7.2.16 Public Administration ............................................................................................................ 96

7.3 Recommendations ........................................................................................................................... 97

References ................................................................................................................................................... 99

6 | P a g e

7 | P a g e

Acknowledgements The Economic Advisory Council to Prime Minister constituted seven working groups on

National Blue Economy and Sustainable Development Policy vide their memorandum dated 30th

August 2018. The Working Group 4 was constituted under my Chairmanship to prepare a report

on Manufacturing, Emerging Industries, Trade, technology, Services and Skill Development.

This Working Group consists of 11 Members and one Member Convener.

The report of this Working Group is the result of team-work and consultation with key

stakeholders.

Contributions to this report include all Members of the Working Group namely; Representatives

from Department of Science & Technology, Representatives from Department of Heavy

Industries, Representatives from Department of Commerce and Representatives from

Department of Financial Services.

The group benefitted immensely from the comments and inputs from other members of the

Working Group namely; Dr. Akhilesh Gupta, Head, SPLICE, Department of Science &

Technology, Dr. Nitya Nanda, Associate Director, The Energy & Resources Institute, Prof. Rupa

Chanda, Indian Institute of Management Ahmedabad, Dr. H. Purushotham, Chairman &

Managing Director, National Research Development Corporation, Dr. Satyaki Roy, Associate

Professor, Institute for Studies in Industrial Development (ISID), Dr. Bala Pisupati, Research and

Information System for Developing Countries (RIS), Ms. Madhura Roy, Deputy Director, Skill

Development & Women Entrepreneurship.

This Working Group extends its gratitude to Dr. S.K. Mohanty, Professor, Research and

Information System for Developing Countries (RIS) for putting together the material and

bringing out a concise, comprehensive and insightful document.

I also gracefully acknowledge the academic support of RIS for the preparation of the report. RIS

team comprises of Dr. Priyadarshi Dash, Assistant Professor, Ms. Pankhuri Gaur, Consultant and

Ms. Chandni Dawani, Research Assistant.

I especially thank Shri B.N. Satpathy, Senior Consultant, EAC to PM and Shri Suneet Mohan,

Assistant Consultant, EAC to PM for coordinating activities in bringing out this document.

My special gratitude to Shri Ratan P. Watal, Principal Adviser, NITI Aayog and Member

Secretary, EAC to PM for leading this initiative.

(Dr. Vishwapati Trivedi)

Chairman Blue Economy

Working Group- 4

8 | P a g e

9 | P a g e

List of Tables and Figures

List of Tables

Table 1: World Sea Transport Services Trade, 2013-17 ............................................................................. 27

Table 2: Sea Transport Services Trade in Coastal Economies ................................................................... 27

Table 3: Trade in Blue Economy Services, 2011-17 .................................................................................. 28

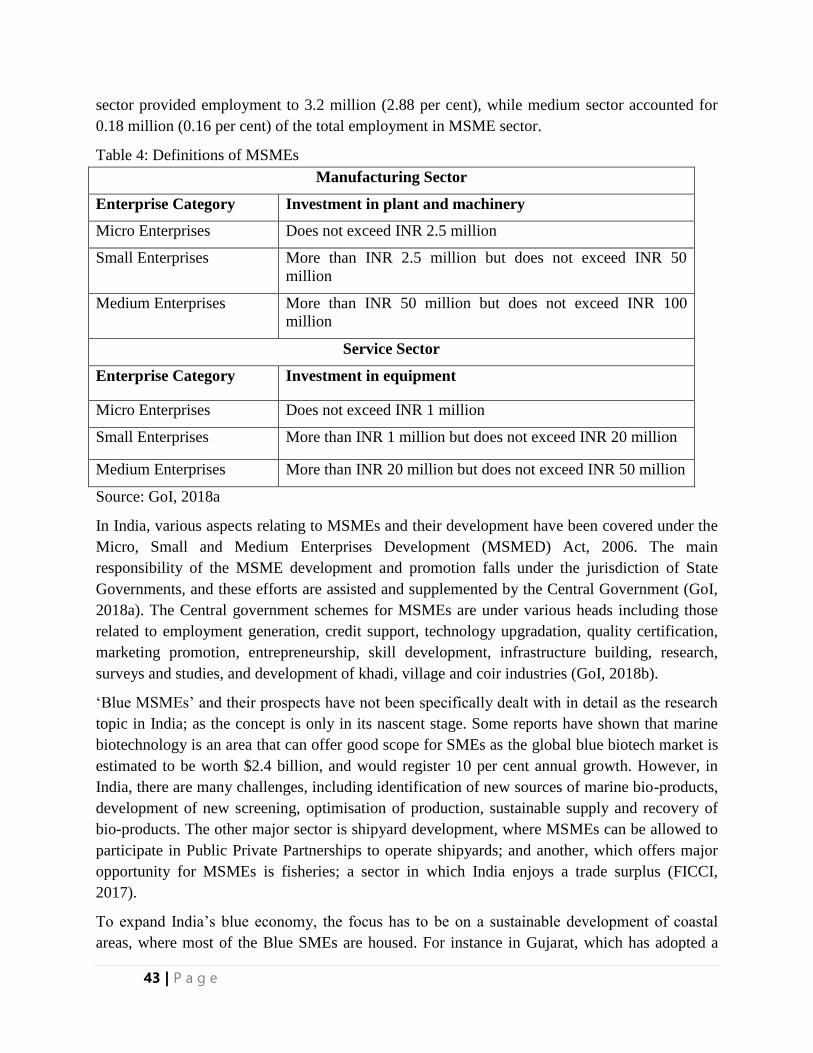

Table 4: Definitions of MSMEs .................................................................................................................. 43

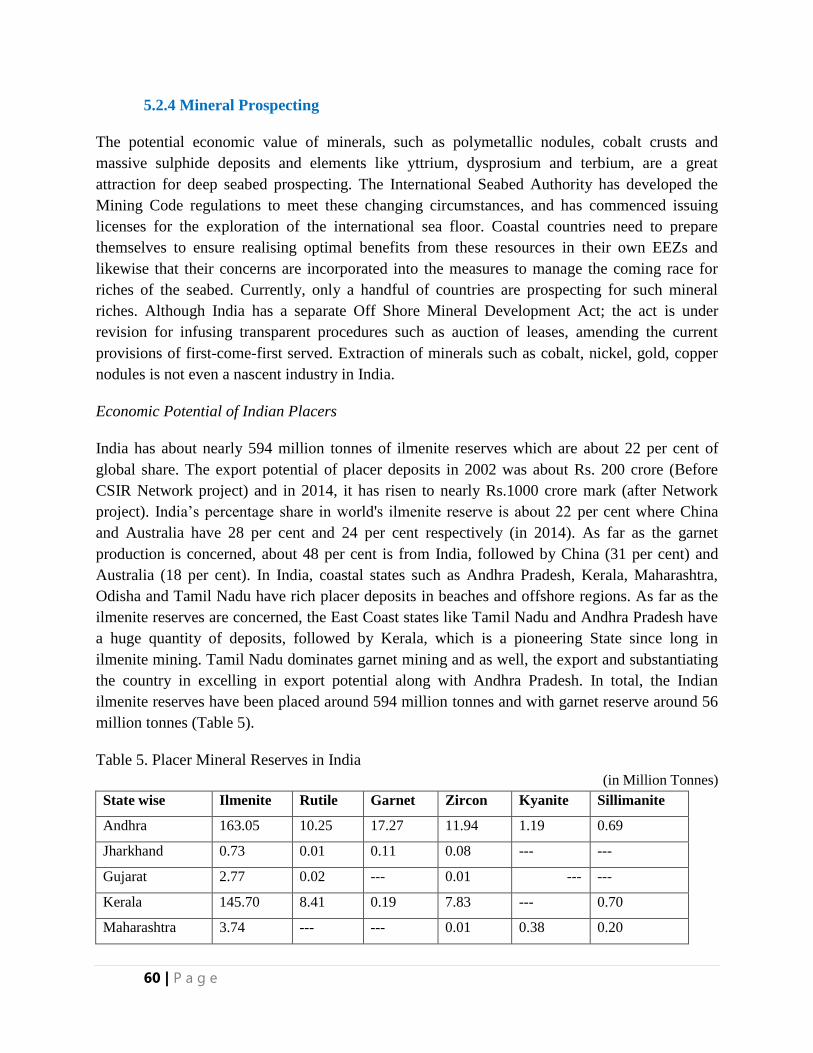

Table 5. Placer Mineral Reserves in India .................................................................................................. 60

Table 6. Placer mineral annual production and its value in global market ................................................. 61

Table 7: Blue Economy Sectors to be prioritise in India ............................................................................ 62

Table 8: Type and Nature of Jobs in Blue Economy Sectors ..................................................................... 69

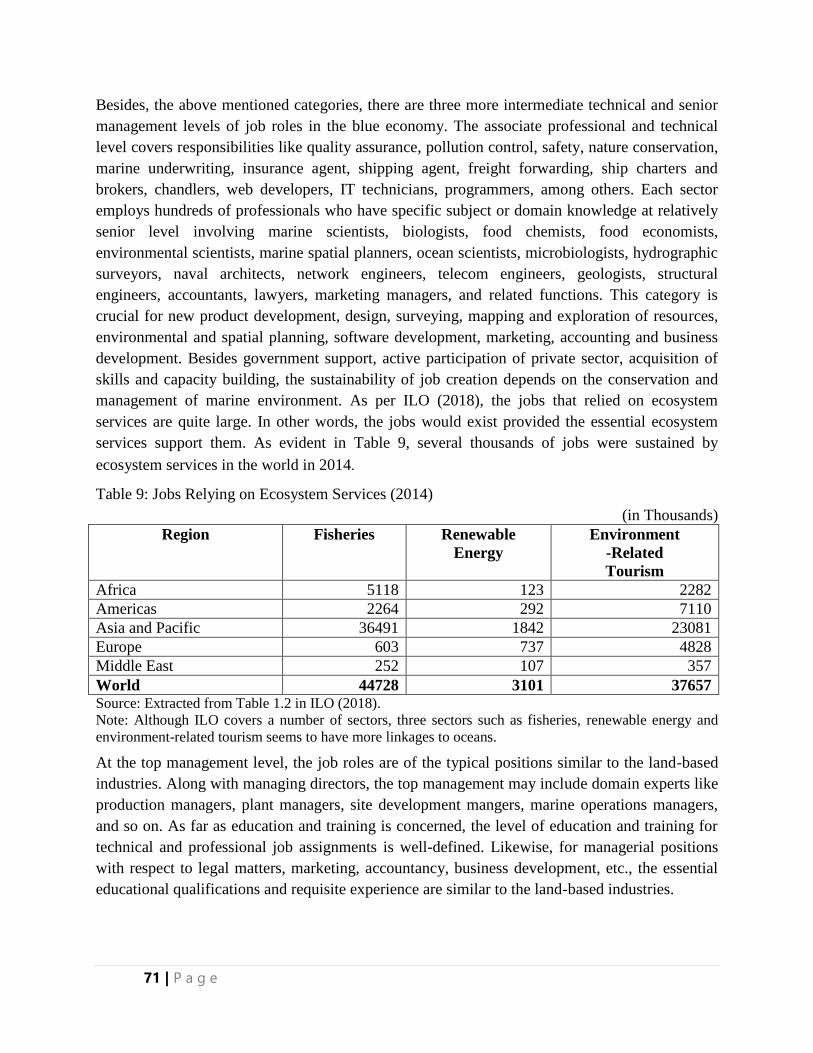

Table 9: Jobs Relying on Ecosystem Services (2014) ................................................................................ 71

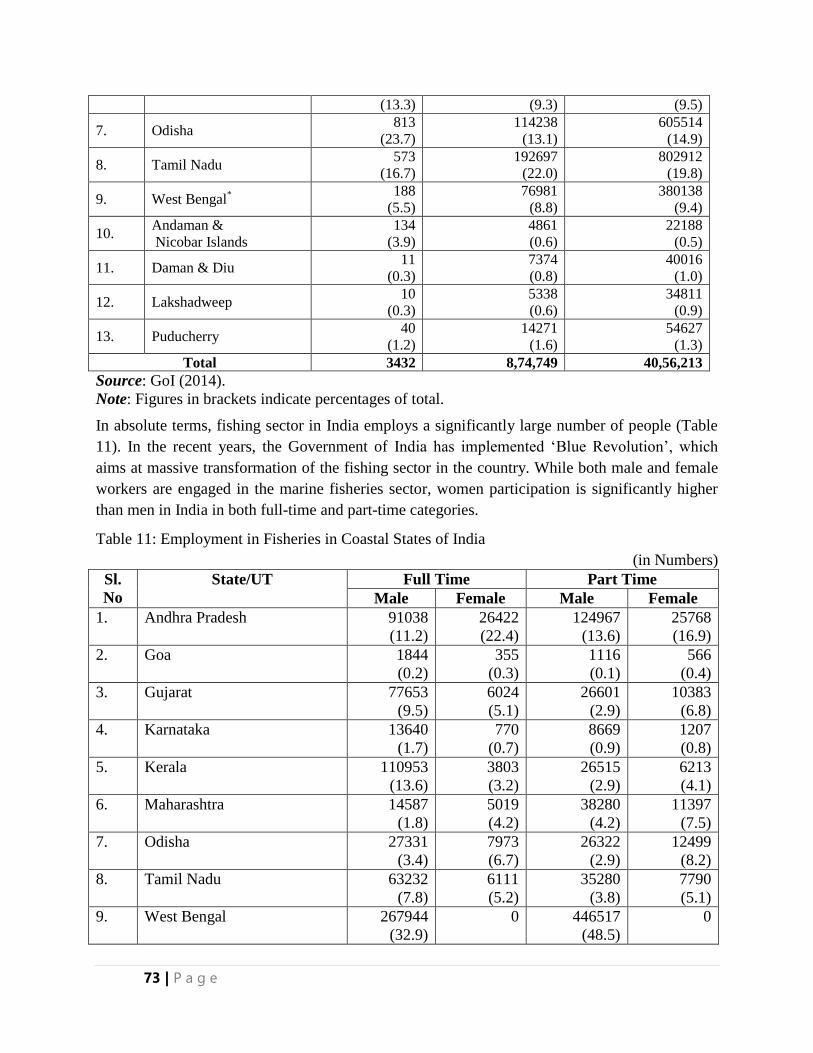

Table 10: Dependence on Marine Fisheries in Coastal States of India ....................................................... 72

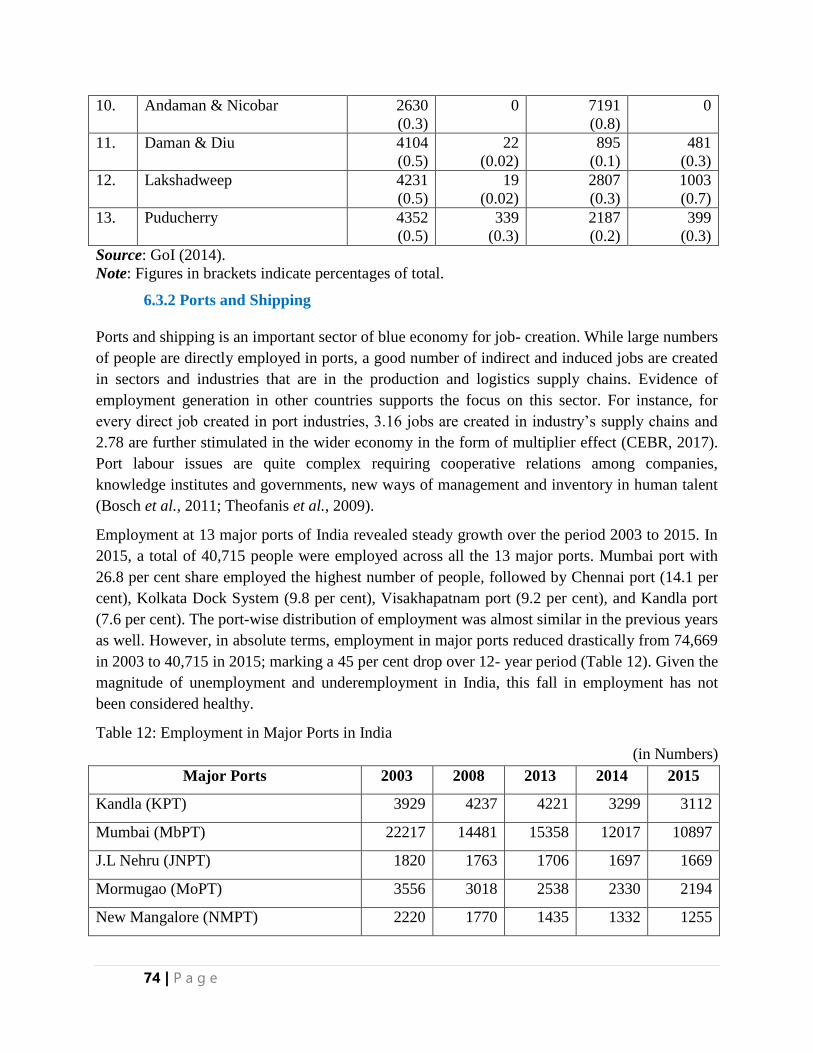

Table 11: Employment in Fisheries in Coastal States of India ................................................................... 73

Table 12: Employment in Major Ports in India .......................................................................................... 74

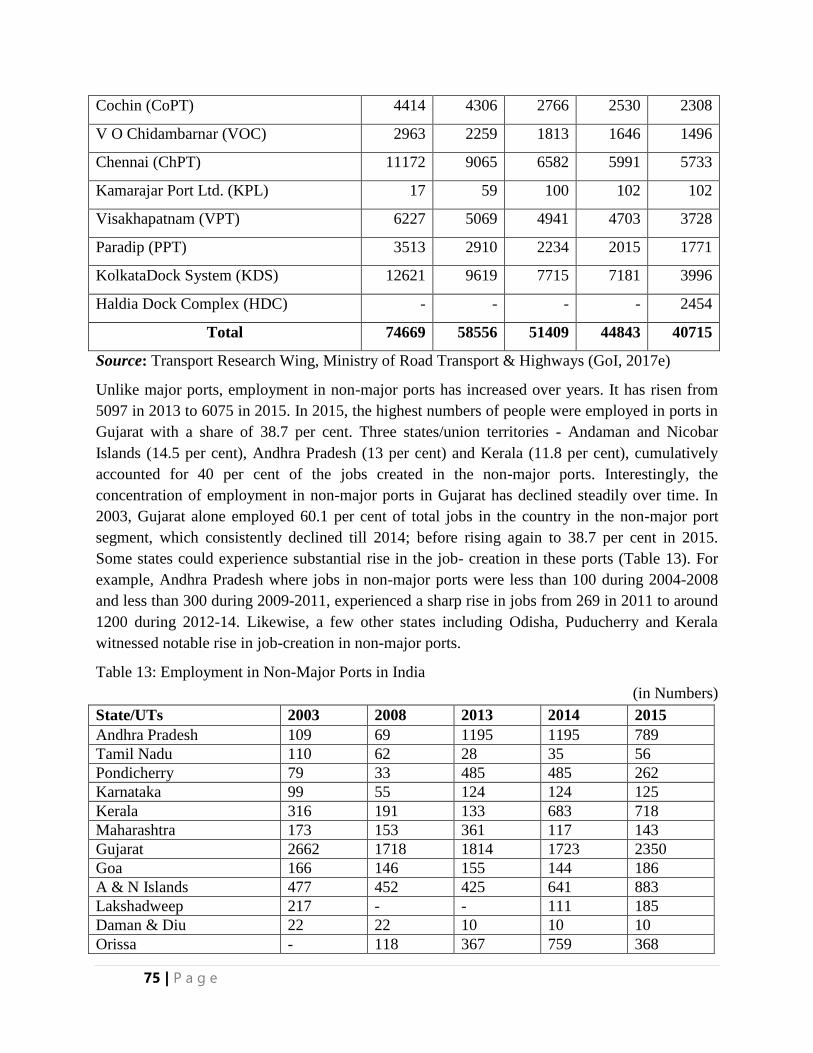

Table 13: Employment in Non-Major Ports in India .................................................................................. 75

Table 14: Port Labour Productivity (Output Per Gang Shift) (2016-17) .................................................... 78

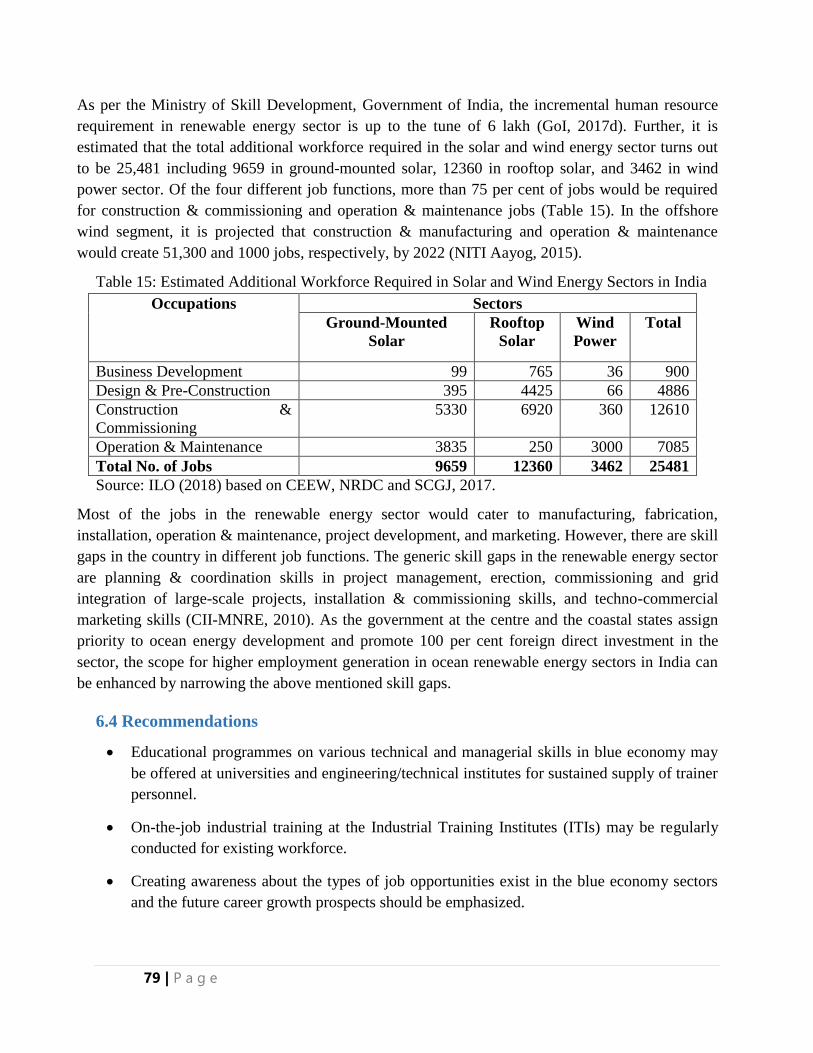

Table 15: Estimated Additional Workforce Required in Solar and Wind Energy Sectors in India ............ 79

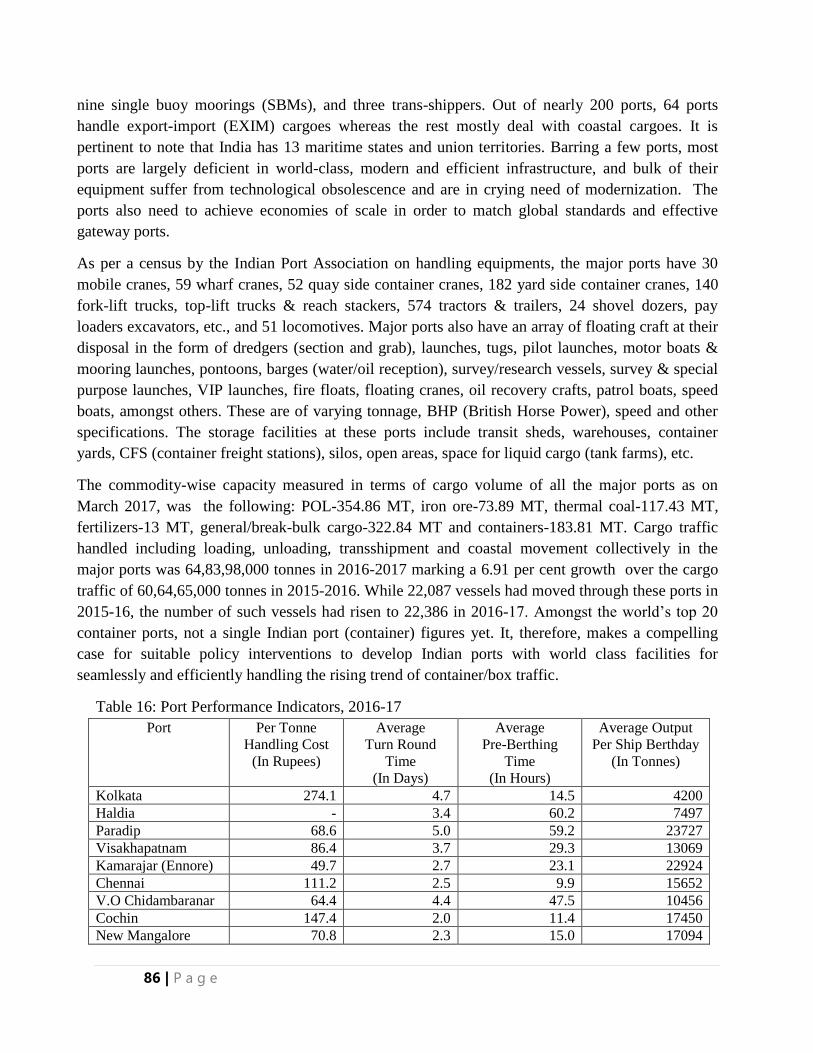

Table 16: Port Performance Indicators, 2016-17 ........................................................................................ 86

List of Figures

Figure 1: Proposed Solar Power Generation Capacity by 2020 ................................................................ 366

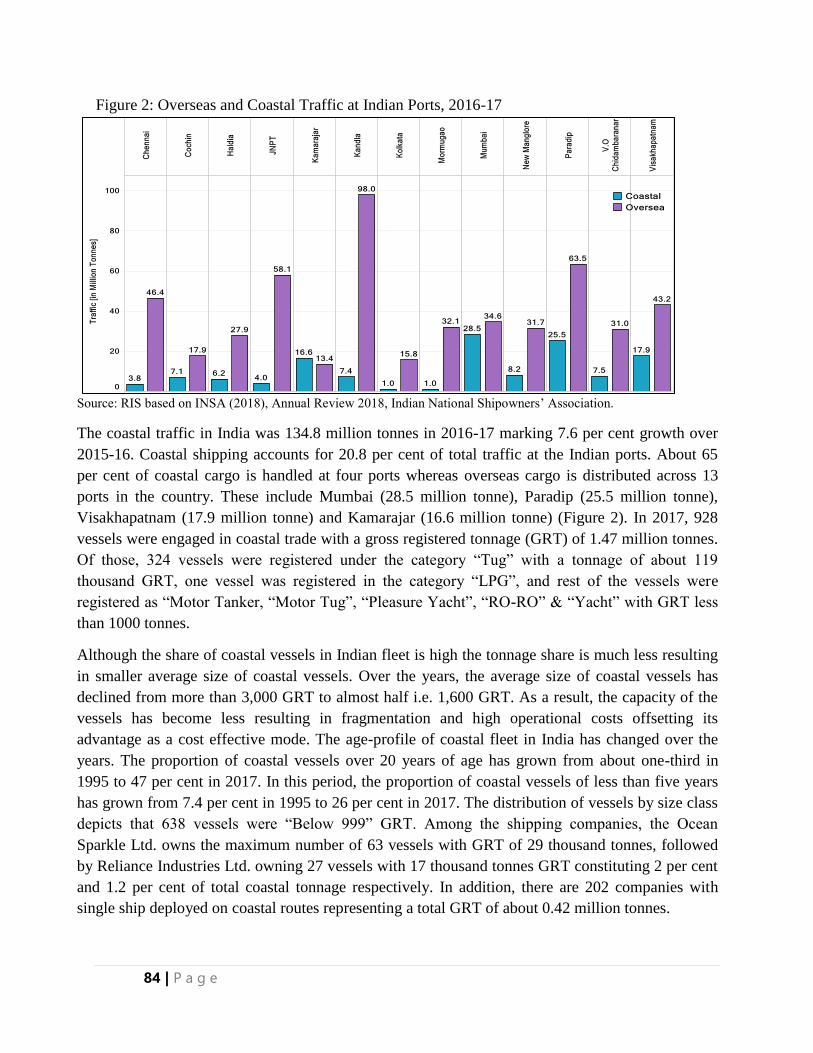

Figure 2: Overseas and Coastal Traffic at Indian Ports, 2016-17 ............. Error! Bookmark not defined.4

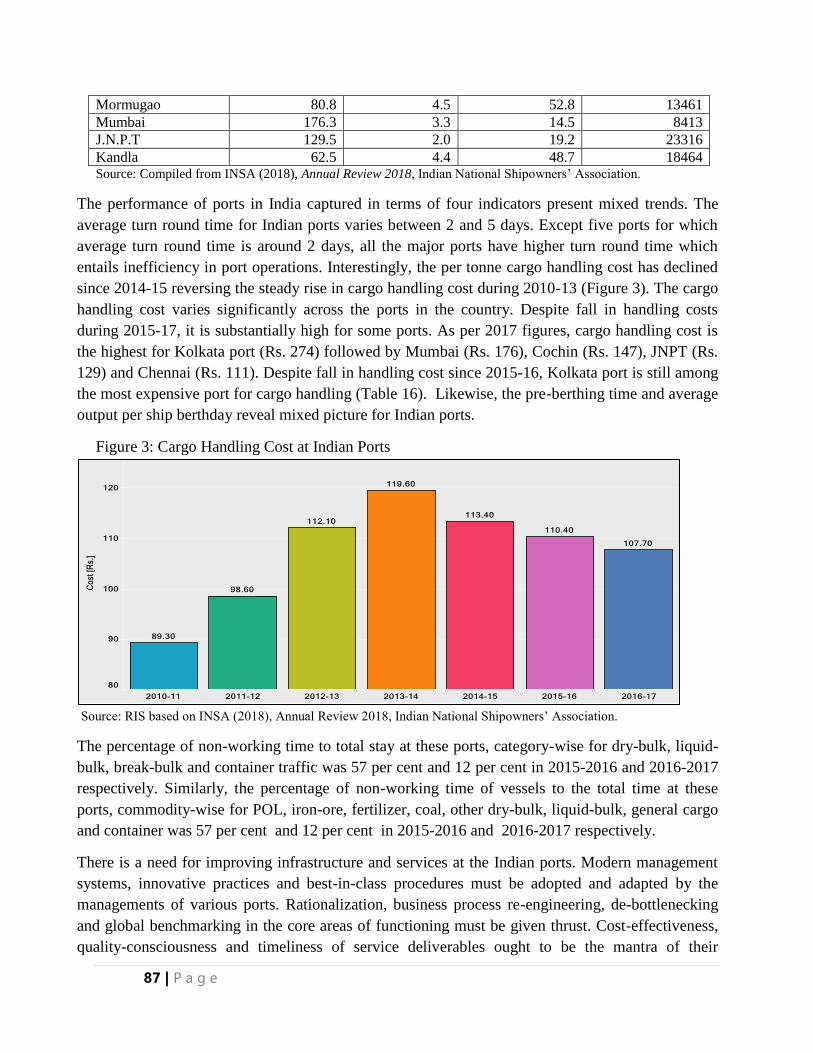

Figure 3: Cargo Handling Cost at Indian Ports ......................................... Error! Bookmark not defined.7

10 | P a g e

11 | P a g e

List of Members of the Working Group

1. Dr. Vishwapati Trivedi, Former Secretary to Govt of India… Chairman

2. Secretary, Department of Science & Technology, Ministry of Science and Technology

3. Secretary (HI), Department of Heavy Industries, Ministry of Heavy Industries and Public

Enterprises

4. Commerce Secretary, Department of Commerce, Ministry of Commerce and Industry

5. Secretary (FS), Department of Financial Services, Ministry of Finance

6. Dr. Nitya Nanda, Associate Director, The Energy and Resources Institute

7. Prof. S.K Mohanty, Research and Information System for Developing Countries (RIS)

8. Prof. Rupa Chanda, Economics & Social Sciences, Indian Institute of Management

9. Dr. H. Purushotham, Chairman & Managing Director, National Research Development

Corporation

10. Dr. Satyaki Roy, Associate Professor, Institute for Studies in Industrial Development

(ISID)

11. Dr. Bala Pisupati, Research and Information System for Developing Countries (RIS)

12. Ms. Madhura Roy, Deputy Director, Ministry of Skill Development

13. Shri B.N. Satpathy, Sr. Consultant (EAC-PM) … Nodal Officer

1

12 | P a g e

13 | P a g e

List of Abbreviations

ALDFG Abandoned, Lost or otherwise Discarded Fishing Gear

ATC Automatic Traffic Control

BICA Bio-Marine International Clusters Association

CAGR Compound Annual Growth Rate

CEZs Coastal Economic Zones

CEZs Coastal Economic Zones

CFS Container Freight Stations

CFSs Container Freight Stations

CHAs Custom House Agents

COSME Competitiveness of Enterprises and Small and Medium-sized Enterprises

DGH Directorate General of Hydrocarbons

DPD Direct Port Delivery

EEZ Exclusive Economic Zone

EMFF European Maritime and Fisheries Fund

ETVs Emergency Towing Vessels

FDI Foreign Direct Investment

GDP Gross Domestic Product

GOOS Global Ocean Observing System

GRT Gross Registered Tonnage

GVA Gross Value Added

GVO Gross Value of Output

IACS International Association of Classification Societies

ICDs Inland Container Depots

ICG Indian Coast Guard

ICT Information and Communication Technology

ILO International Labor Organization

IMF International Monetary Fund

IMO International Maritime Organization

INCOIS Indian National Centre for Ocean Information Services

INSA Indian National Shipowners’ Association

IORA Indian Ocean Rim Association

IoT Internet of Things

IRS Indian Register of Shipping

ISPS International Ship and Port Facility Security

ITIs Industrial Training Institutes

IUU Illegal Unreported and Unregulated

IWAI Inland Waterways Authority of India

IWT Inland Waterways Transport

14 | P a g e

JNPT Jawaharlal Nehru Port Trust

MARIBE Marine Investment for Blue Economy

MIS Maritime India Summit

MLC Maritime Labour Convention

MMLPs Multi-Modal Logistics Parks

MMTPA Million Metric Tonnes per Annum

MP&IAI Maritime Protection & Indemnity Association of India

MSME Micro, Small and Medium Enterprises

MSMED Micro, Small and Medium Enterprises Development

NCCR National Centre of Coastal Research

NIMPIS National System for the Prevention and Management of Marine Pest Incursions

NIO National Institute of Oceanography

NVOCC Non Vessel Operating Common Carrier

NWs National Waterways

OSROs Oil Spill Response Organizations

OTEC Ocean Thermal Energy Conversion

PFZ Potential Fishery Zone

PPP Public Private Partnership

SDG Sustainable Development Goals

SIDS Small Island Developing States

SST Sea-surface Temperature

STCW Standards of Training, Certification & Watch-keeping

THC Terminal Handling Charges

UNCLOS United Nation Convention on the Law of the Seas

UNDESA United Nations Department of Economic and Social Affairs

UNECA United Nations Economic Commission for Africa

VTMS Vessel Tracking Management Service

WWF World Wide Fund for Nature

15 | P a g e

Executive Summary

The Blue Economy is an inter-disciplinary concept emerging as an alternative development

paradigm. And there is yet to be a universally agreed definition of Blue Economy. It is also

important that each country defines Blue Economy and its specific relevant aspects in its own

context. A working definition of the Blue Economy as relevant for India can be as follows.

“The Blue Economy refers to exploring and optimizing the potential of the oceans

and seas which are under India’s legal jurisdiction for socio-economic development

while preserving the health of the oceans. The Blue Economy links production and

consumption to capacity and envisages an integrated approach to economic

development and environmental sustainability. It covers both the marine that is

offshore resources as well as the coastal that is onshore resources and involves:-

(i) A framework for proper measurement of Blue Economy activities and their

contribution to the national income;

(ii) Spatially oriented planning along with scientific assessment of resources and their

replenishment;

(iii) Investment in financial capital, physical capital, natural capital and human capital

to harness the potential of the Blue Economy;

(iv) Innovation to ensure zero waste, low carbon technologies that yield economic

dividend for large sections of the population.”

The current report highlights potential of the Blue Economy sector in Indian Economy while

using the above definition. It underlines that a well-integrated policy to develop Blue Economy

in India would have a very promising future. The governments at the central and at the state level

have embarked upon with many programmes to leverage the untapped potential of the sector.

Sagarmala Project of the Ministry of Shipping is one such a gigantic effort in this direction.

Marine and offshore mineral resources are considered as new sources of economic growth in the

country. Blue Economy encompasses multiple sectors and all types of economic activities—

primary, secondary and tertiary with varying levels of technological applications, capital

requirements, skill development, trade prospects, and so on. Investments and explorations in the

state-of-the-art technologies in Blue Economy and in marine resource management can broaden

frontiers of marine manufacturing sector and would boost trade in marine goods, minerals and

services.

India’s participation in global trade of marine goods and services has improved considerably

regardless of the annual fluctuations in export proceeds and trade balance. Global trade in marine

services, particularly, sea transport services rebounded in 2017 after registering a steady decline

during 2014-16; in this, exports of sea transport services had declined sharper than imports.

Among sub-sectors, sea-transport freight registered the sharpest decline in both exports and

16 | P a g e

imports. Barring the Philippines and Bangladesh, India is one of the leading trading nations in

global trade in blue services. While it seems that India’s payments are apparently higher than

receipts on different blue services, still the overall balance of payment position on account of

blue services cannot be conclusively assessed owing to insufficient data.

Among services sectors, ship repair, marine finance and insurance, marine ICT, coastal tourism

and port services can unleash a huge potential for investments and job-creation under an

integrated policy to develop and harness potential of Blue Economy. As an example to be more

specific, with a robust infrastructure and timely supply of parts and components, the ship repair

sector in India can be improved to be beneficial. With India’s strategic location in the Indian

Ocean, an efficient well-geared ship repair facility closer to the international shipping routes can

attract foreign ships and vessel calling on the Indian ports as well as those passing through the

vicinity of the Indian waters. With the progressive implementation of the policies and the

initiatives on the Blue Economy, demand for the world-class port services can be developed. For

global competitiveness, there is a need for creating competition among ports and building in port

specialization.

With a fast pick-up in awareness about business and investment opportunities in the country,

there would be demand for loans and other financial services for marine and other related

sectors. A strong and a deep market for supporting and satiating demand for finance and

financial services is the need of the hour. In addition to the traditional financial products, the

opportunity for financing new technology development projects for harnessing ocean energy

sources and deep-sea exploration may require substantial funding and commercialization support

from traditional sources of finance and venture capitalists. Applications of artificial intelligence,

internet of things, big data analytics, block-chain and related technologies may trigger growth of

marine ICT in India.

Investment is the crucial determinant of the future of Blue Economy in India. Blue investments

are primarily needed in the form of R&D and technology development, manufacturing, and for

the development of necessary infrastructure. For living resources, there are immense investment

opportunities for seafood production, aquaculture, trade in fish products, fishing-net and gear-

making, ice production and supply, boat construction and maintenance, fish-processing

equipment, packaging, marketing and distribution. Investments in marine living resources can be

aptly used in production of pharmaceutical products and for chemical applications. Likewise,

desalination, extraction of minerals and oil and gas, renewable energy sources (wind, wave, and

tidal energy), transport and trade (shipping, ship building and breaking, maritime transport, port

infrastructure and related services), tourism and recreation (tourism and coastal

development/urbanisation) are green-field areas for investments in non-living resources.

The major sectors with strong investment prospects are shipping, including capacity expansion

of vessels, ship-building, repairing and breaking, coastal shipping, ship chartering and ship

brokerage services, warehousing, freight forwarding, bunkering and storage facilities, developing

dedicated coastal shipping, and dedicated coastal berths management. But, investments in Blue

17 | P a g e

Economy sectors involve many unknown risks as more than 80 per cent of the oceans stay

unmapped, unobserved and unexplored. This sector also requires comprehensive assessment of

the associated environmental, social and governance risks and adoption of suitable risk-

management strategies. Dedicated regulation and enforcement regimes across the exclusive

economic zones (EEZs) and innovative financing models, e.g. blue bonds, would be desirable for

providing congenial environment for the growth of the Blue Economy.

The Government of India has set out a vision for promotion of Blue Economy. Some of the

major initiatives in this endeavour include the Sagarmala project, SAGAR, Blue Revolution and

Development of Coastal Economic Zones (CEZs). Sagarmala aims at port-led industrialization

and development with massive investment plans for port modernization, development of

industrial corridors and strengthening of regional value- chains. Likewise, SAGAR envisages a

secure maritime space for achieving sustainable development in the country. The 13 identified

Coastal Economic Zones can be a game changer for synergistic growth of Blue Economy.

Foreign Direct Investment (FDI) through the automatic route has been permitted in Blue

Economy-related sectors such as mining and petroleum and natural gas, industrial parks, duty-

free shops and railway infrastructure. Smart Industrial Port Cities, Dedicated Freight Corridor

(Eastern and Western), construction of inland ports and inland water transport projects are other

sunrise sectors for investment.

At the regional level, IORA and ASEAN are two important regional organizations for fostering

international cooperation. ASEAN would facilitate maritime transport, promotion of coastal

shipping services, investment in marine ICT, research and innovation in marine biotechnology,

greater access to sea-bed resources, proper integration of coastal tourism and other services,

renewable energy, coastal management and marine resource conservation. African countries

have also prioritized Blue Economy as a prospective sector of economic diversification and

employment generation in the Agenda 2063. In Europe, the European Commission has funded

MARIBE (Marine Investment for Blue Economy) to explore cooperation opportunities for

companies to invest in blue biotechnology, aquaculture, seabed mining, ocean energy and coastal

tourism. Further, the European Maritime and Fisheries’ Fund has boosted EC’s maritime

priorities, and has helped pilot the Blue Growth strategy.

The Micro, Small and Medium Enterprises (MSME) in Blue Economy sectors offer immense

potential for industrial growth in the country. Countries and international blocs are making

efforts to rope MSMEs into the Blue Economy ecosystem. The Nairobi Statement of Intent on

Advancing the Global Sustainable Blue Economy 2018 supports growth of SMEs for building a

sustainable Blue Economy. In 2015, the IORA Jakarta Declaration on Blue Economy reiterated

importance of promoting entrepreneurship, innovation and SMEs with a special focus on

promoting youth and women’s engagement in the sustainable development of Blue Economy. To

promote MSME sector, the initiatives like Innovation Union, provision of funds through the

European Maritime and Fisheries Fund (EMFF), Competitiveness of Enterprises and Small and

18 | P a g e

Medium-sized Enterprises (COSME) programme, Horizon 2020 and the SME Instrument would

be important catalysts.

Marine manufacturing is a relatively untapped field of Blue Economy. It covers a range of

activities such as ship building, development of marine compounds and drugs, manufacturing of

equipment and instrumentation, exploration equipments for deep-sea mining, net making, boat

making, and fish processing and aquaculture equipments. While marine manufacturing industries

are potentially high-growth sectors, they would inflict several environmental challenges.

For expanding Blue Economy, India needs to focus on the sustainable development of the coastal

areas where most of the blue MSMEs are localized. However, MSME sector faces some of the

following challenges — poor access to finance, technology and skills. Lack of information and

knowledge about Blue Economy is also a core reason behind negligence of this sector in overall

economy. In the marine products segments, MSMEs grapple with problems of identification of

new sources of marine bio-products, development of new screening, optimization of production,

sustainable supply and recovery of bio-products. Public private partnerships (PPPs) in Blue

Economy sectors, like shipyard development and fisheries, definitely offer major opportunities

for the growth of MSMEs.

The success of Blue Economy is organically linked to technology and innovation. Proper

scientific knowledge and mapping of marine resources and development of technologies for

commercialization of industrial applications of those resources would determine contribution of

the Blue Economy to national income. Along with the technologies for efficient economic use of

marine resources, the capacity to curb greenhouse gas emissions by the environment-friendly

technologies would play a crucial role in monitoring and conserving ocean resources. For the

measurement of the ocean asset-base, the techniques like Acoustics, Optics and Radar are used

for bathymetry to get data and potential of different sources from the oceans. Other technologies

like Remotely Operated Underwater Vehicles, Satellite Oceanography, GIS, SONAR and

Animal Telemetry would help in mapping ocean resources. Desalination technology and Ocean

Thermal Energy Conversion (OTEC) would benefit in harnessing simultaneously energy and

freshwater production. Digitisation in marine sector by enhancing efficiency of transit with

technologies, like blockchain, Internet of Things (IoT) is vital. Marine-based products, gas

hydrate-based technology for various applications, including gas recovery, sequestration, water

purification etc., are under R&D worldwide. With huge deposits of placer minerals, India has

ventured into a systematic approach in exploring with new deposits and improved mining

procedures. In line with many years of technical advancements, India has developed appropriate

capability to technologically support Indian Ocean Rim Countries for such offshore mineral

exploration and exploitation in an eco-friendly and economically feasible framework. In India,

coastal states such as Andhra Pradesh, Kerala, Maharashtra, Odisha and Tamil Nadu have rich

placer deposits in beaches and offshore regions.

Employment generation in Blue Economy is the most attractive public policy attraction for

countries like India with abundant young workforce. Some of the potential high-employment

19 | P a g e

sectors in the sector are fisheries, port and shipping, marine biotechnology, renewable ocean

energy, deep-sea mining, coastal tourism and marine services. Along with the domestic

expansion of Blue Economy, the greater market access for exports and scope for value addition

would contribute indirectly to the competition-induced catch- up of local labour force to global

standards. In absolute terms, the fishing sector in India employs significantly larger number of

people; and female-labour participation in fishing-related activities is much more than the male-

labour participation.

In summing up, a well-coordinated and focused ‘Blue Revolution’ programme can transform not

just the traditional sectors such as fishing, but also can open up several new sub-sectors with the

use of technology and frontline financial innovative methodologies.. This would also have a

higher employment and income multiplier effect on both the coastal areas and the hinterland.

20 | P a g e

21 | P a g e

Chapter 1. Blue Trade

1.1 Blue Trade in Goods: Emerging Trends

Blue Economy is becoming the main stay of many littoral countries, and Blue Trade is likely to

be the growth driver for many of them. Norway and others countries have large exports, mostly

steaming from marine sector. Blue trade has not been that intensely discussed as the accounting

framework issues of Blue Economy in the literature. Several studies have indicated sectoral

performance of blue trade, such as fishery, transport, coastal tourism, hotels and restaurants,

shipping, etc. which are part of the Blue Economy sector. There is hardly any study that has

examined the entire spectrum of Blue Trade in a stylised framework of Blue Economy. In

Denmark (Danish Government, 2006; 2010), there are certain estimates of Blue Trade sectors,

covering direct and indirect exports of the country. Still, the study covers only those trade sectors

which are considered established trade sectors of Blue Economy. But this report presents a

framework for Blue Trade in India.

1.2 Issues in Blue Trade

Blue Trade is unevenly spread in the entire range of tradable sectors. Since trade sector is more

disaggregated than economic activity sectors, identification of products (Based on HS) in Blue

Trade is somewhat more convenient than identification of industries under economic activity

sectors (ISIC). International comparison of Blue Trade is more tenable than Blue Economy

sectors as HS codes are more disaggregated than ISIC industries.

Expansion of economic activity and trade codes favours the latter since it is more thinly sliced

than the other. Despite having relatively easy solution to identify Blue Trade product codes over

activities, there is very little work done globally in this sector. In Blue Economy, certain sectors

are linked traditionally to ocean, and such sectors are often identified in the literature as fishery,

transport, coastal tourism, etc. These established sectors have been operating since last several

centuries, but sustainability and growth dynamism are the main issues (EU, 2018). There are

several emerging sectors, which are gradually coming up with considerable growth prospects and

also confirming with environmental sustainability issues.

The Blue Trade is different from the normal trade because of the geographical factor and other

intricacies. Blue Trade may loosely be expressed as one which is directly or indirectly liked with

incoming/outgoing resources or activities from/to ocean or water -bodies. Thus Blue Trade

covers both trade in goods and services together. Like the System of National Accounts (SNA),

UN, normal trade follows same pattern where trade in goods and trade in services (TIS) is

presented separately to show contribution of the external sector to the GDP of the country. In the

literature, Blue Economy has its own classification of sectors such as living, non-living sectors,

etc. among others, which are somewhat unconventional than other classifications like production,

22 | P a g e

trade, end-use, etc. Moreover, in each of the defined sector of the Blue Economy, all activities

within the sector, including goods and services, are taken together.

Activity and location of the occurrence are necessary and sufficient conditions to designate an

activity as part of the Blue Economy in the literature. It is not just customary to emphasize on

linkage of the products directly to oceans, which is necessary to be labelled as part of the Blue

Economy, but it also cover those products which are indirectly associated with oceans. While

choosing products under the Blue Trade, the land-based and ocean-based industries are

categorically discussed. The reason is that the nature of production function would differ

significantly for land and water for a given ocean-cased industry. This would lead to variations in

cost prices of the product originating from two production bases. Production function of

hydrocarbon from land and ocean would differ significantly. Moreover, possibility of the spread

of environmental pollution can be more acute in water than on land, and therefore, environmental

regulations would need to be more stringent in water than land-based operations. In a way,

coverage of products in Blue Trade would have- some linkages with the ocean or waterbodies.

Many sectors conventionally part of the Blue Trade are fisheries, coastal minerals, shipping,

port, coastal tourism, etc. and hence, products falling within them are part of the Blue Trade.

While certain other products, which are contributing to Blue Trade sectors, should be taken

partly in estimating contribution of the product to Blue Trade. Therefore, product weights may

be used to account for partial contribution of the product to Blue Trade. For example, beach

placer is part of the Blue Trade but not desert placers. Hydrocarbon coming from offshore can be

part of Blue Trade, but not from the land. Similarly, several sectors and products exist in Indian

economy where part of these products can be part of the Blue Trade. Apportioning of a product

has to be undertaken on the basis of its contribution to Blue Trade by assigning appropriate

weights to products. Therefore, difficulty arises while assigning weight to tradable products,

which are partly linked to Blue Trade.

Experiences of countries indicate that Blue Economy is the fastest growing segment of a littoral

country (Mohanty, Dash, Gupta and Gaur, 2015). During the last 40 years, international trade has

grown much faster than the global output (Dean and Sebastia-Barriel, 2004; Mohanty and Saha,

2019). In a similar vein, Blue Trade is likely to dominate the global trade scene in future, if not

so far. Contrary to the conventional view, Blue Trade exists in almost all trade sectors and sub-

sectors, including goods and services. Since the global economy has not concluded in mapping

the coverage of ocean-related economic activities, estimation of Blue Trade would continue to

remain underestimated. There are several industries contributing directly or indirectly to trade

activities, which are yet to be in the framework of Blue Trade. However, known sources of trade

activities in the sector are many, and several spotty evidences linked to Blue Trade have been

discussed in the literature. Some sectors are rather better known than others, and reorganisation

of such evidences can form a framework for estimating contribution of Blue Trade in India.

23 | P a g e

1.3 Broad Blue Trade Sectors

For a large number of products, place of production and place of consumption are linked through

trade. The worth of marine products is growing faster as the local market for these products is

gradually expanding to the global market through trade. In the absence of international trade,

several countries of the world would have been deprived of products in the form of consumption.

The trade holds the key for setting the stage for economic growth for new product innovation for

trade, generation of a modern entrepreneurial class, export diversification, employment

generation and fresh investment.

One of the most important sectors under the Blue Trade is aquatic animals and plants which are

in the agricultural sector. Fishery sector is the most dominant segment of the global food trade.

Growth rate of fishery trade is very high and intra-regional trade in finfish and shellfish has been

very strong in Asia, including India (Mohanty, Dash and Gaur, 2019). In the fishery sector,

robust trade has been shown by seafood, but trade in aquatic products and seaweeds is gaining

momentum (Ferdouse et al., 2018). India has been a major player in the global production and

trade in fisheries. Rising demand for fishery products, particularly processed fish, is due to

enhanced demand for such products across the developing and the developed countries, growing

preference for consumption of fish on health grounds, shortage of wild fish as the result of

depletion of species, freezing technology, fish preparation, improved control in harvesting

process and transportation break-through, etc. among many factors (UNCTAD, 2014).

Fishery trade is emerging as one of the most valuable non-hydrocarbon sector traded globally

(Potts et al., 2014). Since trade in wild fish is declining owing to slowing down of catch, it is

being increasingly replaced by fish from aquaculture (Asche and Khatun, 2006; Asche and

Smith, 2010; Hughes et al., 2016). As Aquaculture is the largest contributor to global supply of

seafood, it is likely to bridge protein gap by 2020 (Bush et al., 2013). Global demand for fish

consumption is specific to certain species, and only countries specialised in the production and

export of those products, would benefit from global trade. It is empirically examined that as

many as 1471 fishery species are traded globally, but ten top species account for 36 per cent of

the global trade in this sector (Wabnitz et al., 2003). Global trade in fishery sector is picking up

in the processed food sector where specialisation in body parts, refrigeration system, quality of

preparation and packaging and species type matter in accessing global fish market (Mohanty,

Dash and Gaur, 2019). Fishery has a large number of sectors where several products are traded,

and some of them are – fishery catch, aquatic products, seafood, hatcheries, retail and wholesale

trade of seafood, etc. Living resources sector covers both goods and services in the Blue Trade.

Imprints of Blue Trade are very much felt in the mining sector. In the context of Blue Economy,

placer minerals are important for both domestic consumption and for foreign trade. Placers are

found from deposits of sand or gravel in the river bed, streams, lake and sea coast, and they are

valuable minerals. It is observed that stream and beach placers are important sources of placer

deposits in India. In the coastal region, sea wave plays an important role in shifting materials

through shore currents; and thus heavy metals get concentrated at the shore. India is a leading

24 | P a g e

country in the production and trade in placer and placer-related products along with a few others,

including Australia, Brazil, the US, etc. India is presently exporting and importing several placer

metals and placer-related products.

Minerals are sub-divided into metals and non-metals. Metals are further classified into

radioactive and non-radioactive products. Some metals are radioactive (i.e., uranium, thorium,

Ilmenite, Rutile, Monazite, etc.) and others are non-radioactive (Hematite, Magnetite, Tin,

Platinum, gold, etc.). Among non-metal marine minerals, some of them are linked to marine

chemicals and some are non-chemicals, like sand and gravels. Moreover, marine minerals can be

classified into several groups on the basis of unique properties such as electronic, optical and

magnetic characteristics of these metals.

Placer minerals have a large market in India, and its potential is of about INR 900 billion lately.

Such materials are exceptionally useful for enhancing manufacturing base in India, particularly

becoming important in the context of Make in India Initiative and Industry 4.0. India had

initiated significant liberalisation in the mineral sector in 1998, but the reform process was

reversed in 2006. Mining of such minerals in India is undertaken primarily with two public

sector companies— Indian Rare Earth (IRE) and Kerala Minerals and Metal Limited (KMML),

operating under Department of Atomic Energy. Extraction of radioactive-placer is a capital-

intensive venture. The sector in India can absorb a capital investment of INR 1,200 billion and

has export potential of INR 500 billion in a year. Since China has the largest holding of rare

earth minerals compared to India, the latter needs to focus more on creation of value -added

products using placer metals for exports. As the basic raw material is markedly available within

the country compared to many other countries in the world, India has a strategic advantage in the

area of coastal placer.

India has evolved advance technology in desalination of water from sea. Ministry of Earth

Sciences, National Research Development Corporation (NRDC) and several public and private

sector companies have developed a low- cost technology in the sector. This has been effective in

dealing with water scarcity in coastal regions and small islands. Many such technologies are

experimented in Lakshadweep and have been found successful and also cost -effective. This

sector has large potential for Blue exports.

Demand for offshore renewable trade is growing fast because of depleting reserves of fossil fuel

in the world. Among known offshore energy sources of production, wind energy is leading,

expanding almost at the rate of 40 per cent per annum (UNCTAD, 2014). At present, commercial

production of alternative source of offshore energy is low, and is focused mostly on algae biofuel

(Halvorson et al., 2001). In 2013, annual production of algae biofuel was 3 million gallon and

this expected to reach 61 million gallon per annum by 2020. In terms of value such biodiesel

from algae would be $1.3 billion (UNCTAD, 2014). Among many other characteristics of

biodiesel, it has the capacity to reduce CO2 emission. There is a large potential of trade in new

products in areas like high-valued bio-products in medicine, food and in the cosmetic industry,

using microalgae (Commonwealth, 2016).

25 | P a g e

Marine manufacturing covers wide range of industries classified into established and emerging

industries, producing a large number of products. These products directly or indirectly are

associated with ocean-related manufacturing activities. As experiments with the ocean and its

resources are relatively recent phenomenon, several new industries and activities are coming up.

In some of the existing cases, proper mapping of industries and their marine-linked products

have not been properly identified. Gradually many such actives have unveiled and therefore, they

are being consistently added to the inventory of Blue Trade. Because of this trend, Blue Trade

would continue to be underestimated, until all activities under this sector are identified fully and

accounted for estimation.

A designate taskforce may be formed to examine the sectors and activities under Blue Trade,

including the manufacturing sector. Manufacturing sector is a major contributor to Blue Trade.

Deep-sea capture fishing, hatchery, aquaria products, and processed fish products are part of the

manufacturing Blue Trade. Biotechnology products from biopharma, food additives, cosmetics

and bio-fuel, are included in the manufacturing sector. Offshore petroleum and gas from shallow

water and services for maintaining production site are also important. Building of merchant and

military ships, boats, dredging equipments, fishing ships/boast, trawler, spare parts and repair

services are associated with ocean, and domestic waterways are also covered under the sector.

Activities involved in shipbreaking industry is also fragment of the sector. Sea cabling and its

servicing have merged as import for the trade sector. Ice-making, rope, net, gear, marine

equipments, etc. are also traded internationally. There are other products which can be part of

blue trade.

Various sectors under Blue Trade require special treatment because they are different from the

normal trade. For example, fishery sector is a growing sector in global food trade. Fishery sector

is outside the purview of WTO agricultural trade negotiation. Most of the countries have adopted

protected trade regime for the fish sector. The sector faces stringent Non-Tariff Barriers (NTBs),

mostly in the form of SPS and TBT measures. Fishery sector is subject to subsidy reduction for

conservation and sustainable fisheries. It has not only implications for fishery trade but also on

industrial fishing as well as production/trade of fishing vessels.

Similarly species trade in biodiversity is often restricted taking into account conservation

measures. In many cases, entire plants or animals are not traded; they are rather done partially.

Trade in this sector is limited to leaves, roots, steams, bark, seeds, flower, and body parts of

plants as well as animals. While undertaking trade, exporters have to pass through stringent

regulatory processes. In many cases, trade is allowed for specific purposes only. Certain

medicinal varieties of rice, wheat, fish, etc. are allowed to be exported for edible purpose and not

for research. Several biodiversity species like sponge, coral, algae, fish, cereals, etc. fall in this

category. From the point of trade, several products under Blue Trade are subject to more

stringent regulations than the normal trade.

The multilateral trade regime is mostly opposed to use of subsidy in trade. The practice of

providing subsidy brings distortion to global trade, and contrary to the principle of laissez faire.

26 | P a g e

Restriction on subsidy to the agricultural sector is regulated by special Article on Agreement on

Agriculture (AoA). Similarly, fishery subsidy is a major issue in WTO, falling under Non-

Agriculture Market Access (NAMA). Such provisions on the use of subsidy are also applicable

to manufacturing sector. However, this principle is not uniformly applied to all tradable sectors.

Shipbuilding sector is not subject to subsidy commitments under the WTO. Domestic

governments can give production subsidy to the sector without any capping. For this reason, the

sector is thriving in China, Japan and South Korea, and only because of patronage by the state

through subsidy, even when the sector is passing through the phase of global recession.

Blue Trade is likely to be the most dynamic sector in the overall trade sector of the littoral

economies. In India, some attempts have been made to discuss about the framework of

estimating contribution of Blue Economy to GDP, but more discussions are required to create a

framework for Blue Trade (Mohanty, 2018). However, the sector has huge trade prospects as

complete potential of the sector is yet to be tapped. Global trade barriers are too much stringent

for products of Blue Trade. To overcome the constraints related to market access for Blue Trade

products, technology related solutions are to be evolved. Innovations, technology, product

development and quality of products would pave the way for rapid expansion in Blue Trade.

Trade in Services has a great potential in India, particularly in the Blue Trade sector.

1.4 Trends in Global Maritime Service Trade

Like marine goods, trade in marine services can help expand the frontiers of activity in blue

economy. Currently, little knowledge exists on exports and imports in marine services globally

except some coastal nations for which some statistics for certain sectors are available. For India,

there is no such systematic account of exports and imports in marine services even though data

for a few sectors are presented separately by concerned ministries or departments. While all

sectors of marine services are not tradable, a number of sectors including coastal tourism, sea

transport, marine finance and insurance, shipping services including freight operations, ship

repair and other port services may unleash huge prospects for trade expansion. Moreover, as the

contribution of services to gross domestic product in India is growing, the demand for marine

services would also get a boost along with overall spurt in blue economy activities.

Given data limitations, it is difficult to properly assess the trends in global exports and imports of

marine services. Based on standard Global Database on trade in marine services (IMF), it is clear

that data on trade are available for only four services (including both broad and sub-sectors).

This includes sea transport and three of its sub-sectors such as sea transport freight, sea transport

passenger, and sea transport other. Global exports and imports of all the four marine services

have registered steady decline during 2014-16; more specifically in 2015 and 2016. In particular,

sea transport exports dropped by around 11.5 per cent in these two years whereas imports of sea

transport services decreased by around 9 per cent. Among the sub-sectors, both exports and

imports of sea transport freight registered the sharpest decline. However, this trend was reversed

in 2017 with modest rise in exports and imports of all the four services (Table 1).

27 | P a g e

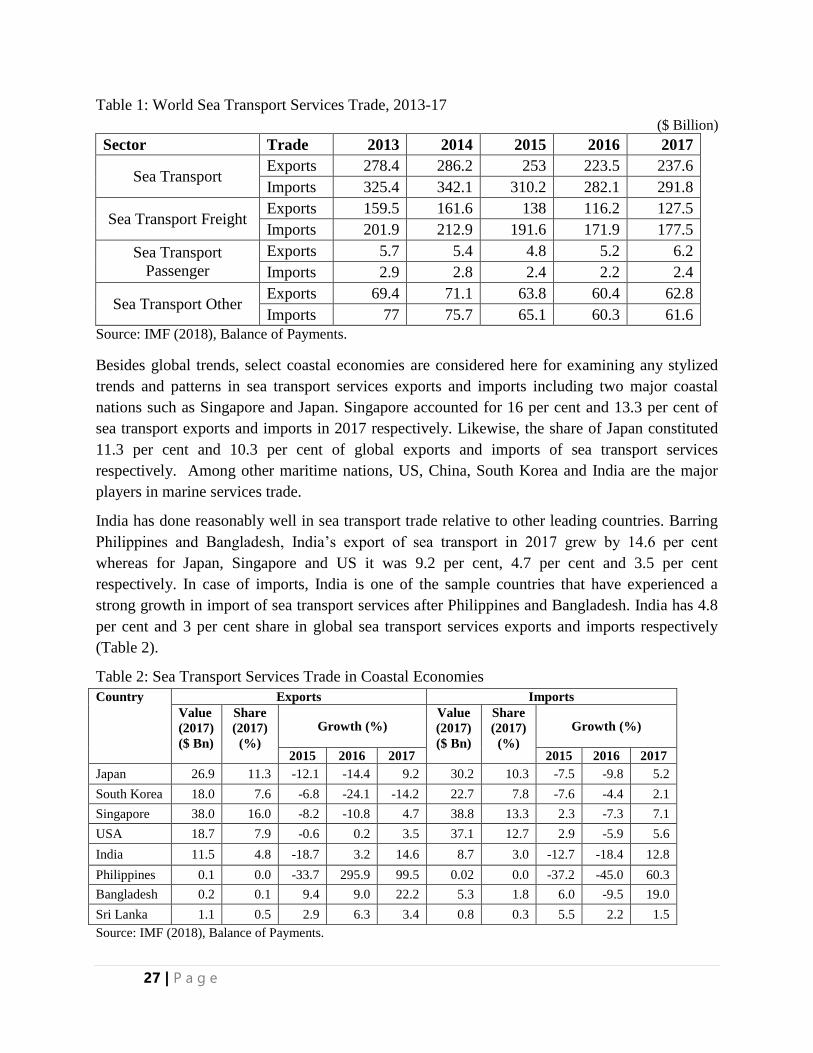

Table 1: World Sea Transport Services Trade, 2013-17

($ Billion)

Sector Trade 2013 2014 2015 2016 2017

Sea Transport Exports 278.4 286.2 253 223.5 237.6

Imports 325.4 342.1 310.2 282.1 291.8

Sea Transport Freight Exports 159.5 161.6 138 116.2 127.5

Imports 201.9 212.9 191.6 171.9 177.5

Sea Transport

Passenger

Exports 5.7 5.4 4.8 5.2 6.2

Imports 2.9 2.8 2.4 2.2 2.4

Sea Transport Other Exports 69.4 71.1 63.8 60.4 62.8

Imports 77 75.7 65.1 60.3 61.6

Source: IMF (2018), Balance of Payments.

Besides global trends, select coastal economies are considered here for examining any stylized

trends and patterns in sea transport services exports and imports including two major coastal

nations such as Singapore and Japan. Singapore accounted for 16 per cent and 13.3 per cent of

sea transport exports and imports in 2017 respectively. Likewise, the share of Japan constituted

11.3 per cent and 10.3 per cent of global exports and imports of sea transport services

respectively. Among other maritime nations, US, China, South Korea and India are the major

players in marine services trade.

India has done reasonably well in sea transport trade relative to other leading countries. Barring

Philippines and Bangladesh, India’s export of sea transport in 2017 grew by 14.6 per cent

whereas for Japan, Singapore and US it was 9.2 per cent, 4.7 per cent and 3.5 per cent

respectively. In case of imports, India is one of the sample countries that have experienced a

strong growth in import of sea transport services after Philippines and Bangladesh. India has 4.8

per cent and 3 per cent share in global sea transport services exports and imports respectively

(Table 2).

Table 2: Sea Transport Services Trade in Coastal Economies

Country Exports Imports

Value

(2017)

($ Bn)

Share

(2017)

(%)

Growth (%) Value

(2017)

($ Bn)

Share

(2017)

(%)

Growth (%)

2015 2016 2017 2015 2016 2017

Japan 26.9 11.3 -12.1 -14.4 9.2 30.2 10.3 -7.5 -9.8 5.2

South Korea 18.0 7.6 -6.8 -24.1 -14.2 22.7 7.8 -7.6 -4.4 2.1

Singapore 38.0 16.0 -8.2 -10.8 4.7 38.8 13.3 2.3 -7.3 7.1

USA 18.7 7.9 -0.6 0.2 3.5 37.1 12.7 2.9 -5.9 5.6

India 11.5 4.8 -18.7 3.2 14.6 8.7 3.0 -12.7 -18.4 12.8

Philippines 0.1 0.0 -33.7 295.9 99.5 0.02 0.0 -37.2 -45.0 60.3

Bangladesh 0.2 0.1 9.4 9.0 22.2 5.3 1.8 6.0 -9.5 19.0

Sri Lanka 1.1 0.5 2.9 6.3 3.4 0.8 0.3 5.5 2.2 1.5

Source: IMF (2018), Balance of Payments.

28 | P a g e

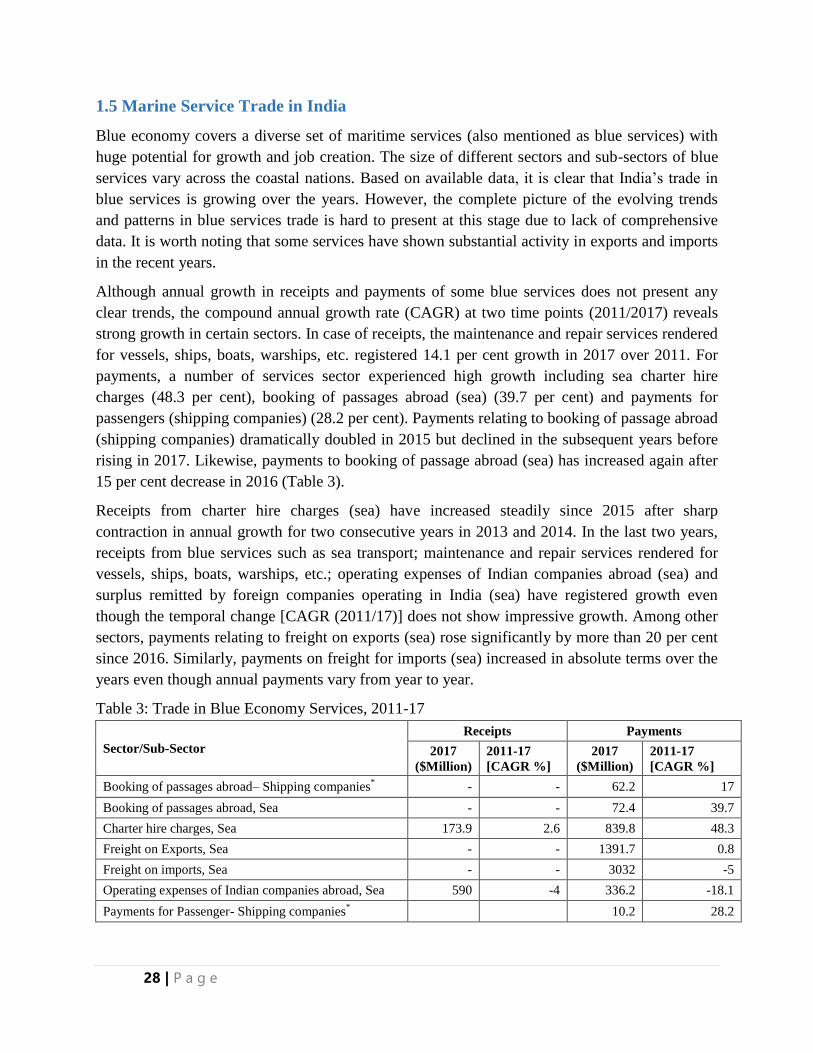

1.5 Marine Service Trade in India

Blue economy covers a diverse set of maritime services (also mentioned as blue services) with

huge potential for growth and job creation. The size of different sectors and sub-sectors of blue

services vary across the coastal nations. Based on available data, it is clear that India’s trade in

blue services is growing over the years. However, the complete picture of the evolving trends

and patterns in blue services trade is hard to present at this stage due to lack of comprehensive

data. It is worth noting that some services have shown substantial activity in exports and imports

in the recent years.

Although annual growth in receipts and payments of some blue services does not present any

clear trends, the compound annual growth rate (CAGR) at two time points (2011/2017) reveals

strong growth in certain sectors. In case of receipts, the maintenance and repair services rendered

for vessels, ships, boats, warships, etc. registered 14.1 per cent growth in 2017 over 2011. For

payments, a number of services sector experienced high growth including sea charter hire

charges (48.3 per cent), booking of passages abroad (sea) (39.7 per cent) and payments for

passengers (shipping companies) (28.2 per cent). Payments relating to booking of passage abroad

(shipping companies) dramatically doubled in 2015 but declined in the subsequent years before

rising in 2017. Likewise, payments to booking of passage abroad (sea) has increased again after

15 per cent decrease in 2016 (Table 3).

Receipts from charter hire charges (sea) have increased steadily since 2015 after sharp

contraction in annual growth for two consecutive years in 2013 and 2014. In the last two years,

receipts from blue services such as sea transport; maintenance and repair services rendered for

vessels, ships, boats, warships, etc.; operating expenses of Indian companies abroad (sea) and

surplus remitted by foreign companies operating in India (sea) have registered growth even

though the temporal change [CAGR (2011/17)] does not show impressive growth. Among other

sectors, payments relating to freight on exports (sea) rose significantly by more than 20 per cent

since 2016. Similarly, payments on freight for imports (sea) increased in absolute terms over the

years even though annual payments vary from year to year.

Table 3: Trade in Blue Economy Services, 2011-17

Sector/Sub-Sector

Receipts Payments

2017

($Million)

2011-17

[CAGR %]

2017

($Million)

2011-17

[CAGR %]

Booking of passages abroad– Shipping companies* - - 62.2 17

Booking of passages abroad, Sea - - 72.4 39.7

Charter hire charges, Sea 173.9 2.6 839.8 48.3

Freight on Exports, Sea - - 1391.7 0.8

Freight on imports, Sea - - 3032 -5

Operating expenses of Indian companies abroad, Sea 590 -4 336.2 -18.1

Payments for Passenger- Shipping companies* 10.2 28.2

29 | P a g e

Receipts on account of maintenance and repair services

rendered for Vessels, Ships, Boats, Warships, etc.®

176.5 14.1 42.5 -22.6

Sea Transport 1419.6 -2.3 8197.8 -3

Surplus remitted by Foreign companies operating in

India, Sea 655.7 -1.8 2525.8 -3.7

Source: RBI (Various Issues).

Note: ‘*’ & ‘®’ denote 2013-17 and 2012-17 respectively.

On payments front, two services that have registered large and steady decline are receipts on

account of maintenance and repair services rendered for vessels, ships, boats, warships, etc. and

operating expenses of Indian companies abroad (sea). In general, receipts from blue services are

either thin or has shrunk over time. While it appears that India’s payments are apparently higher

than receipts on various blue services, the overall balance of payments position on account of

blue services cannot be assessed due to insufficiency of data.

1.6 Opportunities and Challenges in Marine Services Trade

As reiterated above, blue economy is yet to assume separate space in national economic policies,

statistics and human consciousness in coastal nations including India. It applies equally to marine

goods and services. Moreover, it is difficult to conjecture the future prospects of trade in marine

services based on fragmented and piecemeal information about exports and imports. While sea

transport is a major sector of marine services, there are number of other sectors whose potential

is yet to be understood. As activities in most marine services sectors are implicitly included in

the common sectors, the assessment of future growth path of those sectors at this stage can be

based on global experience and economic environment factors. Besides sectoral dynamics there

could be some environmental factors which would determine the activity in the marine sectors.

This section attempts to decipher the emerging pattern of trade in select focus sectors and

identifies certain factors shaping activities in those sectors.

Ship Repair

Ship repair services offer huge opportunity for India as the country is embarking upon a number

of flagship programmes linked to oceans. Sagarmala and SAGAR are two ocean-centric

programmes of the central government. Sagarmala, in particular, aims for port modernization,

new port development and port-led industrialization. This would boost activity in shipping

sector, thereby demand for ship repair services. It would not be exaggeration to point out that the

market for ship repair services is not tapped yet. As India is strategically located in the Indian

Ocean which is the busiest maritime trade route in the world, robust ship repair facility may

attract foreign ships calling on Indian water for repair services. At present, ships plying in Indian

Ocean mostly choose Colombo or Singapore for these services. Modern and well-equipped ship

yards with timely supply of parts and components may help India emerge as a ship repair hub.

30 | P a g e

Port Services

Port services are backbones of a port as it determines the attractiveness of a port for cargo and

related businesses. The major ports of the world such as Rotterdam, Singapore, Colombo and

others have emerged as hub ports for maritime trade because of the efficient port services even

though location of the ports in global maritime space does matter for concentration of cargo.

Indian ports have experienced notable progress in operations and services. However, there are

many areas that need improvement. As blue economy is being viewed as prospective sectors for

investment and growth in India, the demand for world-class port services is likely to pick up.

Moreover, the resurgence of the seaborne trade would accelerate activity in the port and shipping

sector which would also require more port services. As port services involve highly-technical

and semi-skilled jobs the priority to ship repair services in India is timely and consistent with the

current government policy. Since the demand for port services is derived, the central and state

governments can push activity in blue economy sectors so as to activate ports as the centre of

economic activity. Another dimension to transform port and port services for trade is the relative

attraction of Indian ports vis-à-vis other nearby foreign ports. From experience of other countries

it is observed that port service issues were mostly around price not on quality. In that light, there

is a need for injecting competition among ports and encourage port specialization.

Marine Finance and Insurance

Marine finance and insurance is a virgin segment of the financial sector in India. In sync with

overall financial development in the country, marine finance may offer tremendous opportunities

for investment, trade and job creation. Given the difficulty faced by the shipping companies, it is

natural to expect that the financing needs of the shipping sector and other marine sectors would

grow in the near future. Since awareness about business and investment opportunities are

spreading fast in the country, there would be demand for loans and other financial services. In

addition to traditional financial products, the opportunity for developing sector-specific financial

products particularly in emerging high-technology sectors like marine biotechnology, ocean

energy, deep-sea mining, marine construction, and so on may be unleashed over the years. Along

with lending, insurance sector is very much likely as certain risks are unique to the marine

sectors. For instance, ship accidents, breakdown, sinking, piracy, armed robbery, etc. could result

in significant losses to the shipping companies. Likewise, new compound development in marine

pharmaceuticals requires long-term investment with better packaging of known and unknown

risks. Financing of new technology development projects for harnessing ocean energy sources

and deep sea exploration may require substantial funding and commercialization support.

Similarly, other sectors of blue economy may gradually open up new areas of lending and

financing.

Marine ICT

With development of artificial intelligence, internet of things, big data analytics, blockchain and

related technologies, the information and communication technology (ICT) sector is undergoing

massive transformation. The implications of this new technologies and technological platforms

31 | P a g e

are profound on every sector of the economy including the bleu economy. Blue economy has

potential for a wide range of ICT applications in almost all areas such as port operations,

shipping, biotechnology, marine finance, among others. The pace of digitization in marine

sectors is growing worldwide which could unleash huge market for IT software services. India

being a leading exporter of software services can tap this market for marine ICT applications. In

order to capitalize on the ‘first-mover’ advantage, India should identify all possible fields of ICT

applications in different sectors of blue economy and encourage firms to explore business

opportunities in those fields.

1.7 Recommendations

Include separate chapters on Blue Industry in the industrial policies of Government of

India and State Governments. The Coastal states may be the first ones to formulate such a

policy.

Introduce a separate chapter on Blue Trade in the export-import policy which is due for

revision in 2020. The list of exports-imports items falling under the group of 160

identified industries can be recorded in the document.

Improve India’s rank in Ease of Doing Business in the parameter relating to trading

across borders from 80 to 40 by 2022. Ease of Doing Business at district level will

benefit coastal districts in attracting FDI in blue sectors.

Double FDI for sea transport and ports by 2022.

Expand exports of Blue Trade using sea transport for which an adaptive port ecosystem

emphasizing on port competition, robust infrastructure and efficient port services should

be developed.

Adopt sector approach marine services strength

Focused sector approach should be followed for promoting trade in marine services. To

begin with, the sectors like ship repair, port services, marine finance & insurance, and

marine ICT may be considered.

Develop a statistical reporting system for all the ministries relating to blue economy

sectors for record of exports and imports information. The database would be the

repository for both Blue Trade in goods and trade in marine services.

Put digitisation on high priority to empower Blue Economy sectors. India’s talent pool in

software services can be deployed to tap the market for applications of blockchain, big

data, artificial intelligence, internet of things and cloud computing.

32 | P a g e

33 | P a g e

Chapter 2. Blue Investment

2.1 Sectoral Relevance

There are huge investment opportunities in a host of blue- economy segments. Some of these are

in living resources —pertaining to seafood involving primary fish production, aquaculture, trade

of edible and non-edible seafood items, fisheries-related activities, such as processing, net- and

gear- making, ice production and supply, boat construction and maintenance, manufacturing of

fish processing equipment, packaging, marketing and distribution, as well as use of marine-

living resources for pharmaceutical products and chemical applications. Other sectors with major

potential include non-living resources (freshwater generation through desalination as well as

extraction of minerals and oil and gas), renewable energy sources (wind, wave, and tidal energy),

transport and trade (shipping, ship building and breaking, maritime transport, port infrastructure

and related services), tourism and recreation (tourism and coastal development/urbanisation).

And indirect sectors with good prospects for investments are: coastal protection, carbon

sequestration, waste disposal for land-based industry as well as conservation of species and

habitat (World Bank and UNDESA, 2017).

The global market for just one of the emerging blue economy sectors, marine biotechnology,

alone would touch USD 5.9 billion by 2022due to growing demand for natural marine

ingredients for the production of cosmetics, pharmaceuticals, new foods and bio energy. This is

thus leading to huge investments into marine biotechnology research (UNECA, 2016).

It is much easier to invest in land-based sectors than in ocean economy as many of the risks

regarding the former are known ones. However, since oceans are under-explored and not-so-

well-developed, investments in the ocean economy are fraught with several unknown risks. More

than 80 per cent of the oceans stay unmapped, unobserved, and unexplored (NOAA, 2018). Even

an estimate of 91 per cent of ocean species have not yet been classified (Mora, et al, 2011).

Therefore, prior to making blue investments, it is important, to comprehensively assess

associated environmental, social and governance risks and firm up with risk-management

strategies as well as make appropriate allocations to improve ocean health. The policy -makers,

on their part, need to roll out dedicated regulation and enforcement regimes across the exclusive

economic zones (EEZs) to save the investors from the trouble of inconsistent standards. Besides

it is important to push innovative financing models including bringing in export credit agencies

and development banks to manage risks, especially at the initial stages of projects as well as in

promoting instruments such as blue bonds (Economist Intelligence Unit, 2015). Blue bonds are

defined as debt instruments issued by governments, development banks or others to raise money

from impact investors to fund marine and ocean-based projects that would have positive

environmental, economic and climate benefits. Incidentally, Seychelles has already come out

with a sovereign blue bond with the help of the World Bank and the Global Environment Facility

(World Bank, 2018).

34 | P a g e

2.2 Domestic Blue Initiatives

With a 7,516 kilo metre-long coastline and 14,500 km of waterways, India aims to be a global

maritime hub and a blue economy giant. Towards this objective, the government of India has

rolled out a port-led development initiative, called ‘Sagarmala’, and has marked out more than

600 projects, which would attract investments to the tune of USD120 billion (around Rs 8 lakh

crore) by the year 2020. One of the main objectives is to generate around 10 million new jobs.

Also, the Sagarmala initiative is expected to help India save on USD six billion per year through

the costs related to logistics. It is projected that the programme would enhance country’s port

capacity from 800 Million Metric Tonnes per Annum (MMTPA) to an overall 3500 MMTPA.

It also envisages in the development of 13 Coastal Economic Zones (CEZs), each entailing an

investment worth USD 150 million. These would house not only townships but also several

industries, which would contribute to global trade; through sea links. In addition, investment of

more than USD one billion is proposed for setting-up skilling centres and bringing out skill

development programmes across several coastal districts of the country. There is also a plan to

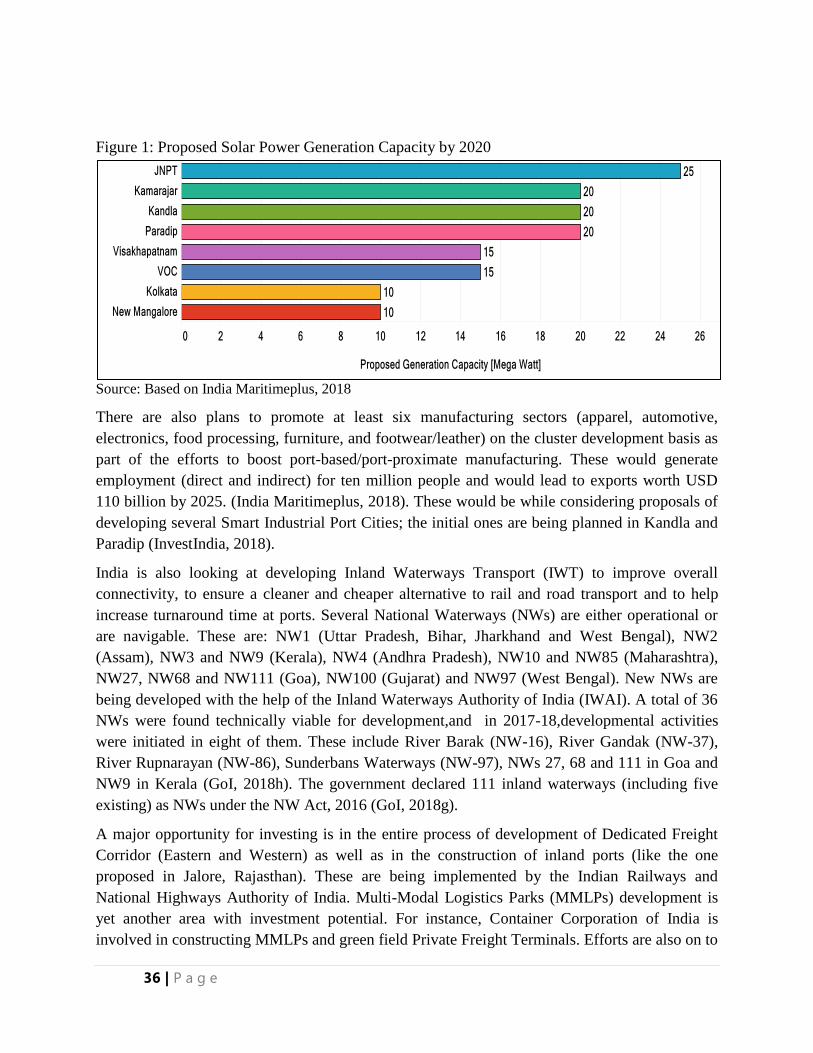

green blue economy initiatives through following projects — 31 MW of captive solar power

generation at various ports; setting -up of oil- spill response facilities and proposals for waste

water reuse at ports (GoI, 2018e). In order to develop India’s maritime ecosystem, the

government is prioritizing sectors, such as CEZ, ports, shipping, shipbuilding, cruise and

lighthouse tourism, Container Freight Stations/Inland Container Depots, road, rail and coastal

connectivity, investments, advisory, technology and training (GoI, 2017a).

Under the Foreign Direct Investment Policy, 100 per cent FDI allowed through the automatic

route (without government approval) is permitted in the shipping sector for port and harbour

construction and maintenance. The government has also incentivised port and inland waterways

development through a 10-year tax holiday to firms developing, maintaining and operating ports,

inland waterways and inland ports. In order to make port-projects more attractive to investors,

the government is considering revision of the Model Concession Agreement. To improve

operations of major ports, project UNNATI has been flagged off, which aims at boosting the

shipping sector, by permitting the foreign flagged ships to carry containers for transhipment

(IBEF, 2018).

Similarly, 100 per cent FDI allowed through the automatic route is permitted in blue economy-

related sectors such as mining and petroleum and natural gas, industrial parks, duty- free shops

and railway infrastructure (GoI, 2017b). In India, between April 2000 and June 2018, sea-

transport sector received FDI inflows of $3.82 billion, while ports sector got FDI worth $1.63

billion (GoI, 2018f). To highlight investment opportunities in the maritime sector, the Ministry

of Shipping organised a Maritime India Summit (MIS) in April 2016 in Mumbai for the first

time. Of the 141 business agreements with proposed investments to the tune of INR 83,000 crore

were inked during the Summit; out of which 49 MoUs, entailing investments worth around INR

35,539.79 crore, could be completed by July 2017 (IPA, 2017). Some of the major global

investors in India’s ports and shipping sector include Maersk, DP World, Jan De Nul Group,

35 | P a g e