Embed Size (px)

Citation preview

Submitted to Operations Researchmanuscript OPRE-2014-03-142

Managing Inventories for Agricultural Products:The Optimal Selling Policies

Jim (Junmin) ShiDept. of Managerial Sciences, Robinson College of Business, Georgia State University, 35 Broad Street, Atlanta, GA 30303,

Yao ZhaoDept. of Supply Chain Management & Marketing Sciences, Rutgers Business School, Rutgers University, Newark, NJ 07102,

Rose B. KiwanukaAfrica Nazarene University, Nairobi, Kenya, [email protected]

The inventory control theory in the operations research and management literature is primarily concerned

about manufactured products, for which, the typical assumptions are ample external supplies and predictable

prices, and the decision is on how much to order or produce. Agricultural products, on the other hand,

are rarely studied in this literature but deserve an attention long overdue because of their unique features,

such as the limited and unpredictable supply, inelastic demand and thus highly unpredictable prices, and

a decision of how much to sell. Such features are considered in the agricultural economics literature which

provides insights and strategic guidelines but with limited structural results on the theory. Inspired by real-

life practice in the Kenya coffee industry, we consider a class of stochastic and dynamic inventory models

for storable agricultural products with random exogenous supply and price. We characterize the optimal

inventory (selling) policies for a variety of cost functions relevant in practice. In the cases of linear cost

functions, we derive closed-form expressions for the optimal policies and the optimal discounted profits. Our

theoretical advancement reveals additional insights and deepens the understanding of inventory management

for agricultural products. Applying the theory to practice, we show that making selling decisions judiciously

can significantly outperform the prevailing practice of selling-all regardless.

Key words : Agricultural products, inventory management, optimal selling policies, price fluctuation,

dynamic programming

1

Shi, Zhao and Kiwanuka: Agricultural Supply Chain2 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

1. Introduction

Many of the world’s poor still depend directly or indirectly on agricultural commodities for their

income, most of them are small-scale farmers in the third world countries. Taking coffee as an

example, an estimated 25 million small-scale farmers grow about 70% of the world’s coffee, and

about 125 million people in the world depend directly on coffee for their livelihoods (Oxfam 2001).

In the 1990s, exports by the 52 developing countries (Brazil, Vietnam, Colombia, Kenya, etc.) were

about U.S. $10-12 billion with the retail sales value, mainly in industrialized countries (the United

States, Germany, Japan, Italy, etc.) of about U.S. $30 billion (Osorio 2002). This makes coffee the

second most traded commodity in the world after petroleum.

1.1. The World Coffee Supply Chain

Coffee beans pass by many hands in various forms as they travel from farmers in the third-world

countries to consumers in the industrialized world (see Kiwanuka and Zhao 2009). Briefly, fresh

coffee cherries are harvested by farmers and then handed in, within 24 hours, to cooperatives for

the primary processing. The processed coffee beans, called the parchment coffee, are next passed to

millers for the secondary processing into green coffee beans, which have a long shelf-life (i.e., more

than ten years under proper storage conditions). The green coffee beans are then traded in the

international markets to importers, from where go to roasters before they finally reach retailers.

Coffee harvest (the supply) mainly depends on three factors: acreage of planting, weather and

farm input. The impact of acreage is not immediate as a coffee tree takes 5 to 6 years to mature.

Over the time, the world’s coffee harvest is increasing but significantly fluctuated due to unpre-

dictable weather conditions (Kiwanuka and Zhao 2009). The world’s coffee consumption, on the

other hand, grows steadily over time at an annual rate of about 0.5% (Daviron and Ponte 2006).

Generally, coffee consumption is insensitive to the price in the short term (Akiyama and Varangis

1990).

The random harvest (or supply) and the inelastic consumption of coffee have led to an extremely

fluctuated price for green coffee beans in the world commodity market; see Figure 1 for the inter-

national indicator price of coffee. For example, the sharp price spikes in 1975-77 and 1994-97 were

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 3

caused by adverse weather conditions in Brazil. Indeed, frosts and droughts in Brazil where some

30% of the world’s coffee is grown have normally led to sudden upward movements in coffee prices

(Ponte 2002). Another significant factor on the price is the collapse of the International Coffee

Agreement (ICA) in 1989. ICA regulated coffee supply by setting quotas to exporting countries to

prevent price from falling below certain levels. Following the collapse of ICA, the price has been

driven primarily by market forces, and have fallen to a 30-year low in 1999-2001 which was below

the average production cost – causing the so-called “coffee crisis”.

Figure 1 Indicator price of coffee in the international market (in U.S. cents per lb.)

Source: International Coffee Organization: Statistics on Coffee.

The collapse of ICA and the following market liberalization put small-scale farmers world-wide

at a disadvantage. Specifically, the farmers face high transaction costs (e.g., variable and fixed

selling costs) with limited technical skills and market information. They (including their represent-

ing cooperatives) are price takers because they are too small to have leverage in the international

market. Finally, they must face the price fluctuations directly but lack of inventory and risk man-

agement tools. As a result, the prevailing practice in the developing countries is to sell-all harvest

regardless. Thus, the farmers cannot take advantage of an increase in price because no inventory is

kept. When the price drops, millions of small-scale farmers are driven out of business into poverty

and hunger.

Shi, Zhao and Kiwanuka: Agricultural Supply Chain4 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

1.2. Kenya Coffee Industry

Kenya’s coffee industry exemplifies the impact of price fluctuations on small-scale farmers. Due

to its ideal geographical location and weather, Kenya produces one of the finest types of coffee

(Colombian milds) in the world. Coffee is an important crop in Kenya contributing significantly

to the country’s export earnings and creates over 100,000 jobs plus supporting 5 million people

(Nyangito 2002). Statistically, 95% of Kenya’s annual harvest is exported, and Kenya’s share of

the world’s market on Colombian milds varies from 4.8% to 14% from 1990 to 2011.

There are two types of coffee farmers in Kenya: more than 700,000 small-scale farmers utilizing

just a few hectares of land, and about 3,400 estate (large-scale) farmers. Overall, the small-scale

farmers produce the majority of Kenya’s coffee with a better quality than the estate farmers because

of a better on-farm care and input. However, the small-scale farmers have been suffering the most

from the price fluctuations.

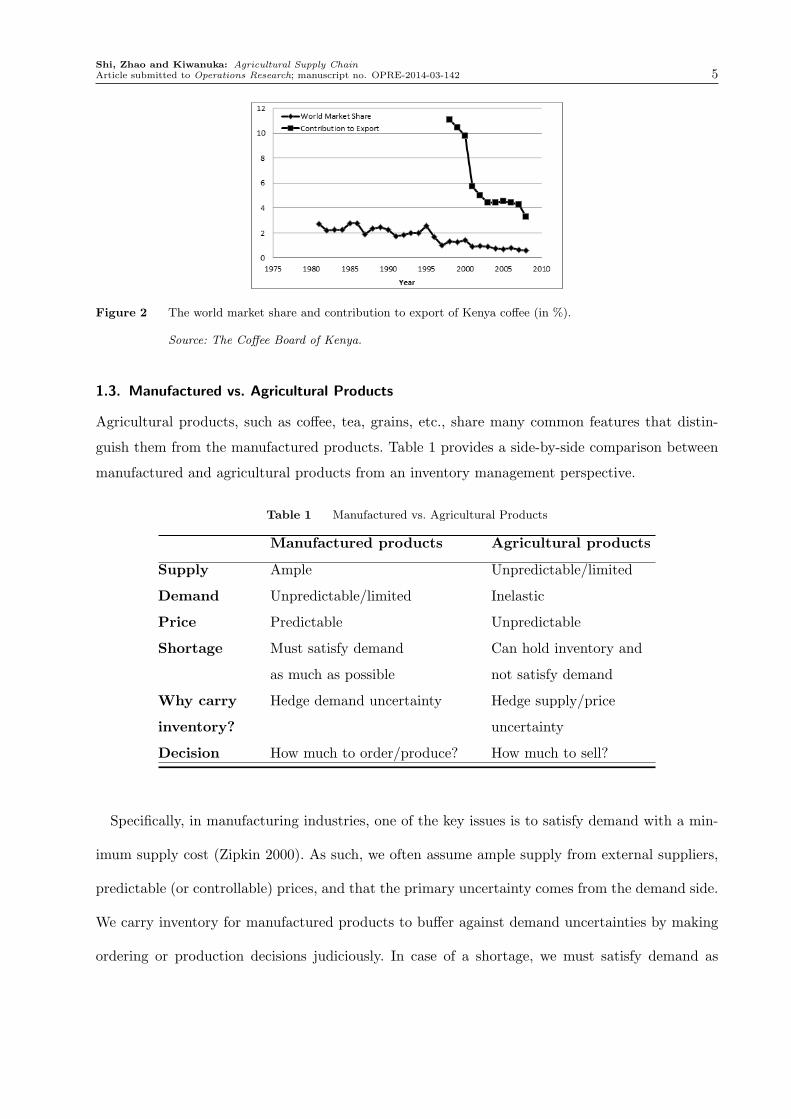

In the past two decades, Kenya’s coffee production has been largely declining (see Figure 2).

Coffee was the top foreign exchange earner in Kenya accounting for over 10% of the total export

earnings during the 1970s and the 1980s. In 1998, the sector contributed 11.07% to export earnings.

But since then, coffee production and export have been sharply declining, and in 2008, to the level

of 3.27%, making coffee the fourth in the rank of export earnings. Meanwhile, the world market

share of Kenya’s coffee has been decreasing from around 3% in the 1980s to 0.6% in 2008. The

decline of the coffee industry has a disastrous impact on the livelihood of coffee growers in Kenya as

well as the country’s economy. It is neither good for the international buyers and the consumers in

the industrialized world. To achieve the Millennium goal No. 1 of eradicating extreme hunger and

poverty, and to sustain the coffee industry in the long-run, we must improve small-scale farmers’

income. Clearly, many things can be done here, such as collective marketing to improve leverage,

and information and education to enhance visibility and productivity. In this paper, we develop

mathematical models and theory for the inventory management of agricultural products to improve

profitability.

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 5

Figure 2 The world market share and contribution to export of Kenya coffee (in %).

Source: The Coffee Board of Kenya.

1.3. Manufactured vs. Agricultural Products

Agricultural products, such as coffee, tea, grains, etc., share many common features that distin-

guish them from the manufactured products. Table 1 provides a side-by-side comparison between

manufactured and agricultural products from an inventory management perspective.

Table 1 Manufactured vs. Agricultural Products

Manufactured products Agricultural products

Supply Ample Unpredictable/limited

Demand Unpredictable/limited Inelastic

Price Predictable Unpredictable

Shortage Must satisfy demand Can hold inventory and

as much as possible not satisfy demand

Why carry Hedge demand uncertainty Hedge supply/price

inventory? uncertainty

Decision How much to order/produce? How much to sell?

Specifically, in manufacturing industries, one of the key issues is to satisfy demand with a min-

imum supply cost (Zipkin 2000). As such, we often assume ample supply from external suppliers,

predictable (or controllable) prices, and that the primary uncertainty comes from the demand side.

We carry inventory for manufactured products to buffer against demand uncertainties by making

ordering or production decisions judiciously. In case of a shortage, we must satisfy demand as

Shi, Zhao and Kiwanuka: Agricultural Supply Chain6 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

much as possible until we exhaust all available inventory. In contrast, the primary uncertainty of

an agricultural product may come from the supply side due to the unpredictable weather condi-

tions. Agricultural products satisfy the essential needs of people and thus the demand is generally

inelastic to prices. So, the price for an agricultural product is inherently random driven by unpre-

dictable and limited supplies. While it is unwise to hold inventory and shortage simultaneously

for a manufactured product, it is legitimate to do so for agricultural products if the price is not

right. Thus, we may carry inventory for agricultural products to buffer against supply and price

uncertainties by deciding, judiciously, how much to sell.

Intuitively, the selling decision must balance the following trade-off: (i) selling now, then we can

carry less inventory into the future but must accept the current price. (ii) Selling later, then we

have to carry more inventory but may get a better price in the future. Based on this intuition, a

simple strategy developed in the agricultural economics literature (e.g., Fackler and Livingstone

2002) says that “Agricultural producers with access to storage have flexibility in choosing the timing

and quantities of sales out of storage, e.g., a simple strategy considers whether the price is expected

to rise in the near future to cover the cost of storage (including the opportunity cost of capital).”

In this paper, we attempt to answer the following research questions:

1) How to manage inventories for agricultural products? Specifically, when to sell? How much to

sell? What is the impact?

2) How does the selling decision depend on transaction costs (holding, selling), price statistics, and

the planning horizon?

3) When does the simple strategy developed in the agricultural economics literature work? When

does it not work?

1.4. Results and Contributions

In this paper, we consider a class of stochastic and dynamic inventory models for agricultural

products with random exogenous supply and prices. The models are inspired and justified by an

empirical study of the real-life practice in the Kenya coffee industry. We characterize the optimal

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 7

inventory (selling) policy for a variety of cost functions, such as linear or linear plus fixed cost for

selling, concave or convex cost for carrying inventory. For convex carrying cost and linear selling

cost functions, we show that the optimal policy is a selling-down-to policy that sells a portion of

the available inventory while retains the rest. Including a fixed selling cost shall change the optimal

policy to a “selling-down-to (S, s)” policy. Interestingly, for all other combinations of the cost

functions, the optimal policy is a selling-all-or-retaining-all policy although the critical thresholds

on price or inventory may differ. For linear cost functions, we further derive closed-form recursive

equations to calculate the optimal cut-off prices and the optimal discounted profit in a finite time

horizon. For the corresponding infinite horizon problem, we prove the convergence of the optimal

cut-off prices and discounted profits, and derive closed-form expressions for the limits. Finally, we

apply the theory to the empirical data and demonstrate the potential impact of the optimal policies

in the Kenya’s coffee industry.

This paper introduces the inventory management issues of agricultural products to the operations

research and management literature. As we shall show, sophisticated OR/OM models and tools,

such as stochastic dynamic programming, can significantly advance the knowledge and insights

previously unaware in the agricultural economics literature, and can make a significant impact on

practice - improving the livelihood for millions of farmers around the world and helping to sustain

the agricultural industries in the long run.

The remainder of this paper is organized as follows: we review the related literature in §2, which

is followed by an empirical study on the price and harvest processes of Kenya coffee in §3. In §4,

we present the mathematical model and the general theory on the optimal selling policy. In §5, we

analyze an important special case where the inventory holding cost is linear and derive closed-form

expressions and managerial insights. We conduct a numerical study to quantify the potential of

the optimal selling policies based on real-life data in §6, and conclude the paper in §7.

2. Literature Review

This paper is related to two large bodies of literature: inventory control theory in the operations

research and management literature, and post-harvest inventory management in the agricultural

Shi, Zhao and Kiwanuka: Agricultural Supply Chain8 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

economics literature. We shall review the related results and point out the contributions of our

work.

2.1. Operations Research and Management Literature

From a modeling perspective, the optimal selling problem of agricultural products is related to

some classic problems studied in the operations research literature, such as the asset selling problem

and the dam control problem.

The asset selling problem (cf. Bertsekas 1976) considers the case where a person has an asset

(e.g., a piece of land) for sale and receives offers from period to period. The offers are random and

the seller needs to make a decision in each period either to take or reject the offer. In the last period,

the seller must accept the offer regardless if the asset was not sold in a previous period. For such

a problem, it has been shown that the optimal policy for revenue maximization is characterized

by a cut-off price, namely, if the offer is greater than the cut-off price, the seller will sell the

asset, otherwise will hold the asset to the next period. The optimal selling problem of agricultural

products can be regarded as a generalization of the asset selling problem to include many real-

life complexities, such as random fresh harvest every period, variable and fixed selling costs, and

convex/concave holding costs. The decision in the agricultural context also goes beyond a simple

taking or rejecting the offer to determining the amount to be sold or carried over. Interestingly,

we show that even with these complexities, the optimal selling policy can still be characterized a

cut-off price in certain (but not all) circumstances.

Another related classical problem is the water releasing problem in a dam because of the random

exogenous supply, see Prabhu (1998) for a review of the dam models. However, the dam models do

not have price as a necessary component and thus the trade-offs handled there are different from

those of selling agricultural products.

The inventory control theory in the operations management literature is primarily concerned

about manufactured products and one of the classical issues is to satisfy the demand with minimum

cost by making decisions on the supply judiciously (Zipkin 2000, Porteus 2002, Simchi-Levi and

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 9

Zhao 2011). This is consistent to the nature of manufactured products which can be cheaply and

massively produced and thus a failure to satisfy the demand often results in intolerable losses. The

optimal ordering and production policies of manufactured products are studied extensively in this

literature with many real-life complexities such as random yield or capacity (Yano and Lee 1995,

Wang and Gerchak 1996), supply disruptions (Tomlin 2006, Wang, Gilland and Tomlin 2010),

controllable price (Federgruen and Heching 1991, Chen and Simchi-Levi 2004), and releasing deci-

sions (Bhaskaran, Ramachandran and Semple 2010). This literature goes beyond order/production

decisions to analyze various sourcing strategies, innovative supply contracts, operational flexibility

and demand pooling strategies (e.g., component commonality), please see Huchzermeier and Cohen

(1996), Van Mieghem (1999, 2003, and 2007), Boyabatli and Toktay (2004), and the reference

therein.

Surprisingly, there is little work in the operations management literature on the inventory man-

agement of agricultural products thus far, to the best of our knowledge. However, one cannot simply

infer the models and results of manufactured products to agricultural products because the radical

difference of the latter (from the former) requires new models, methodologies and insights. One

of the main differences is that one can intentionally hold inventory of agricultural products from

satisfying the demand if the price is not right. That is, the selling decision is at least as important

as the planting (production) decision for the farmers and their cooperatives. For crops such as

coffee and tea, the supply is exogenous in the short term (due to the multiple years of time for

the trees to mature) driven primarily by unpredictable weather conditions. Thus, for these crops,

selling is likely the only decision relevant operationally. Another important difference lies in the

trade-off addressed by inventory control: for manufactured products, the trade-off typically centers

around inventory carrying cost vs. stockout cost; but for agricultural products, the trade-off is on

inventory carrying cost vs. a potentially higher price in the future. A comprehensive comparison

between manufactured and agricultural products can be found in Table 1.

More recently, the optimal selling policy has been studied in connection to the ordering policies

by Bhaskaran, Ramachandran and Semple (2010) in the operations management literature. This

Shi, Zhao and Kiwanuka: Agricultural Supply Chain10 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

paper considers manufactured products but assumes a convex ordering cost and the demand can

be rejected if the unit ordering cost exceeds the benefit of satisfying an additional demand. The

paper shows that the optimal ordering policy is an order-up-to policy dependent on the initial

inventory level and the optimal selling policy is to stop selling when backorders reach a critical

threshold. As typical in this literature, Bhaskaran, et al. (2010) assumes that supply is ample and

price is not a consideration. The trade-off studied in the paper is between a higher ordering cost

and losses of sales.

Despite the difference between manufactured and agricultural products, the optimal selling poli-

cies of the latter bear some resemblances to the optimal ordering policies of the former under

certain conditions. We shall explore and discuss these resemblances at length later in the paper.

The agriculture sector presents many operational challenges and is an important research area

from the perspective of social well-being, and thus has gained attentions from the operations

management literature in recent years, see, e.g., Kazaz and Webster (2011) and An, Cho and Tang

(2013). In particular, An, et al. (2013) study the impact of cooperatives and collective marketing

on producing cost, yield, brand awareness, supply chain consolidation and price uncertainty. Kazaz

and Webster (2011) study the agricultural industry under yield-dependent trading cost structure

in the presence of supply and demand uncertainty. To hedge supply uncertainty, they propose three

strategies: leasing farm space, free trading out/in materials in an open market, and pricing the

final product. It is shown that the yield-dependent unit purchasing cost has a significant impact

on the optimal decisions regarding the sale price and the production quantity. However, inventory

is not considered in these papers.

2.2. Agricultural Economics Literature

The agricultural economics literature has studied post-harvest inventory management since the

1950s when Gustafson (1958) introduces dynamic programming to problems of grain storage and

discusses the optimal stockpiling rules from a government perspective. The paper seeks the objective

of maximizing net benefit to the general public by evening out variations in year-to-year supplies.

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 11

Random price fluctuation is not considered in this class of models. We refer to Wright (2001) for

a review of related follow-up works.

Another stream in this literature takes into account the price fluctuation from the institu-

tional/governmental sellers’ perspective. For instance, Alaouze, Sturgess and Watson (1978) studies

a dynamic programming model for Australian wheat assuming that Australia is a price taker with

a limited storage capacity. They solved the model numerically based on empirical data using value

iteration. Knapp (1982) generalizes Alaouze, et al. (1978) by considering trade and borrowing

options in the presence of foreign exchange issues between countries subject to fluctuations in

domestic harvests and world grain prices. For a simple case (two harvest levels and two prices),

they provide intuitions (but without a proof) for the optimal policy. Tronstad and Taylor (1991)

studies a risk-neutral dynamic model to make grain storage decisions and futures market transac-

tions by taking nonlinear tax issues into account. However, because of the large number of factors

considered in the model, the resulting decision rule is difficult to characterize and calculate.

The selling decisions have been studied in this literature for small-scale farmers. Berg (1987)

considers both risk-neutral and risk-averse farmers for grain carryover problems. Assuming risk

neutrality and i.i.d. price process, the paper studies the selling-all-or-retaining-all (SARA) policies

and provides a recursive procedure to calculate the best cut-off prices. For risk-averse farmers,

the paper shows that spreading sales over the crop season can be a better policy than the SARA

policy. Blakeslee (1997) considers a risk-averse model with a negative exponential utility function

for wheat storage, and uses Taylor-series to approximate the expected utility functions. Lai, Myers

and Hanson (2003) confirms the result of Berg (1987) that the policy of spreading sales out over

the crop season outperforms the SARA policy for risk averse farmers under a more general price

distribution.

For risk-neutral models, the only result to date on the optimal selling policy is obtained by

Fackler and Livingston (2002) which considers dynamic selling decisions in a continuous-time model

with linear profits. The price process is modeled by an one-factor Ito diffusion process. The paper

Shi, Zhao and Kiwanuka: Agricultural Supply Chain12 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

shows that the optimal policy is an SARA policy where the optimal cut-off price can be found by

solving a partial differential equation. For discrete models, it is not known what policy is optimal

even for the linear cost functions, let alone real-world complexities such as convex, concave, linear

plus fixed cost functions and storage capacity constraints. Although Berg (1987) studies the SARA

policy in discrete time, it does not show whether the policy is optimal among all possible policies.

Indeed, as we shall show in this paper, the SARA policy may not be optimal for some nonlinear

cost functions relevant in practice.

This paper contributes to this literature in several ways: (1) we broaden the scope of this lit-

erature by considering much more general cost functions (i.e., concave or convex carrying cost,

fixed selling cost) and price processes (e.g., Markovian) relevant in practice. (2) We advance the

inventory theory for agricultural products by characterizing the optimal selling policies for all

aforementioned cost functions and price processes in a risk-neutral discrete-time model. Interest-

ingly, we show that the popular selling-all-or-retaining-all policy is optimal not only for linear cost

functions but also for a wide-range of nonlinear cost functions under a general Markovian price

process. However, for convex cost functions, the optimal policy has a different structure, which is

of the type of selling-down-to (resembling the optimal ordering policy of manufactured products).

(3) For the well studied case of linear cost functions and independent price process, our closed-

form expressions for the optimal cut-off price in a finite time horizon simplify those of Berg (1987)

by directly connecting the prices in different periods without calculating the cost-to-go functions.

Our closed-form results for the optimal profit functions and for the infinite time horizon case are

new. (4) The theoretical advancement allow us to develop deeper insights and tell when the simple

insight of Fackler and Livingstone (2002, see §1.3) holds true and when it does not hold.

3. An Empirical Study

In this section, we conduct an empirical study on the price, harvest and export processes for Kenya

coffee which provides a basis to formulate the mathematic model in §4.

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 13

3.1. Kenya Coffee Price Process

Kenya coffee is classified by the International Coffee Organization (ICO) as an Columbian Mild

and sold as such. We collect the monthly “Columbian Milds selling prices” published by ICO from

crop year 1991/92 to 2010/11. The price is in U.S. cents per lb. Because Kenya coffee has one

main harvest season each year, we average the monthly prices over a crop-year to obtain a series

of annual coffee prices.

A descriptive statistics shows that the price has a mean of 167.29 cents and a standard deviation

of 60.17 cents. To study the autocorrelation of the price process, we use a simple least-square

regression which yields the following model:

Pt−1 = 58.91+0.66Pt + ϵt,

where periods are backward indexed (such convention will be adopted throughout this paper), the

noise term ϵt has a mean of 0 and a standard deviation of 47.69, and the R-square is 0.405.

To further test the strength of the first-order auto-correlation, we use the Q-statistic introduced

by Box and Pierce (Pindyck and Rubinfeld 1998) to test the following:

H0: The first-order auto-correlation coefficient of the price process is zero.

H1: The first-order auto-correlation coefficient of the price process is NOT zero.

We shall reject the null hypothesis if the Q-statistic is greater than the critical 5-percent level

for a chi-square distribution. In our case, the Q-statistic is 7.41 and the critical value is 3.84, so we

reject the null hypothesis and conclude that the first-order auto-correlation coefficient of the coffee

price process is not zero at the 5-percent level of significance.

Now we estimate the probability distribution of the residuals ϵt. The descriptive statistics shows

that ϵt has a standard deviation of 47.69 cents. We further test the following:

H0: The residuals ϵt follow a normal distribution.

H1: The residuals ϵt do not follow a normal distribution.

Shi, Zhao and Kiwanuka: Agricultural Supply Chain14 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

We test these hypotheses using the Shapiro-Wilk Normality test (Ugarte, Militino and Arnholt

2008, pg 461) and the Jarque Bera test (Pindyck and Rubinfeld 1998, pg 47) at the 5-percent level

of significance. Our calculations show that the Shapiro-Wilk Normality test and Jarque Bera test

yield statistically insignificant p-values of 0.12 and 0.43 respectively. Therefore, we fail to reject

the null hypothesis at the 5-percent level of significance, and conclude that the residuals follow a

normal distribution.

3.2. Kenya Coffee Harvest Process

We collect the annual coffee harvest (production) data from the annual reports of the Coffee Board

of Kenya (CBK) for the crop years from 1991/92 to 2010/11. A descriptive statistics shows that

the annual harvest has a mean of 60,956 tons and a standard deviation of 21,567 tons. To study

the autocorrelation of the harvest data, we use a simple least-square regression which shows an

R-square of 0.221.

To further test the strength of the first-order auto-correlation in annual harvest data, we use the

Q-statistic by Box and Pierce (ibid) to test the following hypothesis.

H0: The first-order auto-correlation coefficient of annual harvest is zero.

H1: The first-order auto-correlation coefficient of annual harvest is NOT zero.

Similar to the price process, we shall reject the null hypothesis if the Q-statistic is greater than

the critical 5-percent level. In this case, the Q-statistic is 3.29 while the critical value is 3.84, so

we fail to reject the null hypothesis and conclude that the first-order auto-correlation coefficient

in the harvest process is zero. In addition to the Box and Pierce test, we use the Breusch-Pagan

and White Tests (Pindyck and Rubinfeld 1998) to test the above hypothesis. In our case, the test

statistic is 0.15 for the Breusch-Pagan and 3.60 for the White Test, each of which is less than the

critical value 3.84 at the 5 percent level. Hence, we fail to reject the null hypothesis and reach

the same conclusion. For each approach tried here, we also tested higher order auto-correlations

(e.g., the 2nd and 3rd) and obtain the same result. Based on these evidences, we can statistically

conclude that Kenya’s coffee harvests are independent across crop years.

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 15

3.3. Coffee Price vs. Export

We now study the dependence between price and export for Kenya coffee. Our calculation shows

that the correlation coefficient between the annual price process and the annual export process is

as small as 0.20. To further test the strength of the correlation, we use the following hypothesis.

H0: The correlation coefficient between price and export is zero.

H1: The correlation coefficient between price and export is NOT zero.

We test this hypothesis using the Pearson product-moment correlation coefficient (Sheskin 2000,

pg 766). The decision rule is to reject the null hypothesis if the statistic is less than the critical value

of 0.414 at the 5-percent level of significance (for our case). Our calculation shows that the statistic

is 0.88 and thus we fail to reject the null hypothesis and conclude that there isn’t a significant

correlation between prices and exports for Kenya coffee.

We also test the correlations between coffee exports and the lagged coffee prices, but find them

statistically insignificant. From the foregoing statistical evidences, we can reasonably conclude that

the price for Kenya’s coffee is independent of Kenya’s export. Intuitively, this statement makes

sense as the price is determined by the total coffee traded in the world coffee market, of which

Kenya’s share is insignificant, 1-3%. This fact renders Kenya a price taker.

4. The Mathematic Model and General Theory

In this paper, we consider risk neutral sellers (e.g., growers or their cooperatives). Based on the

empirical study in §3, we make the following assumptions.

Assumption 1 a) The seller is a price taker, that is, the price is exogenous and independent of

the selling quantities over all seasons (periods).

b) The harvest in a season (period) is independent of the harvests in previous seasons (periods).

c) The price process is a Markov process in general; specifically, it can be auto-correlated and follow

an AR(1) process (for which the i.i.d. price process is a degenerated case).

Shi, Zhao and Kiwanuka: Agricultural Supply Chain16 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

Assumption 1 implies that the price does not depend on the selling quantity. We shall point out

that such a price taker assumption is often made in the literature, see, e.g., Alaouze, et al. (1978),

Berg (1987), and Fackler and Livingston (2002). In this paper we consider storable agricultural

products, e.g., green coffee beans, which can be held in inventory for an indefinite time under

proper conditions. For inventory carried over from one season to the next, a carrying cost incurs,

which includes storage cost, capital cost and interest, among others.

Following notational convention, we consider a finite planning horizon of T + 1 periods with a

backward index t = 0,1,2, ..., T where t = 0 denotes the last period and t = T denotes the first

period. For period t, we introduce the following notation:

• Pt: unit price after deducting tax and variable transaction cost, Pt > 0;

• pt: the realization of random variable Pt;

• Qt: newly available supply/harvest for sales (a random variable) in period t, Qt > 0;

• It: total inventory available for sales in period t;

• xt: the amount of sales made in period t;

• yt: inventory carried over from period t to t− 1;

• Ht(·): holding cost function for carrying inventory over from period t to t− 1;

• Kt: the fixed cost for sales transaction in period t;

• βt: the time discounted factor in period t.

The sequence of events can be described as follows: At the beginning of season t, the initial

inventory available for sales is yt+1. Then, the newly available supply/harvest for sales in this

season, Qt, is realized as qt. The seller updates the inventory as It = yt+1 + qt. Next, the market

price is observed as pt, the sales decision, xt, is made, and the leftover inventory (if any) yt = It−xt

is carried to the next period t− 1. In the sequel, we shall take yt as the decision variable in lieu of

xt. In the last season t= 0, we assume that all inventory available must be sold regardless of the

price p0.

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 17

Let Vt(It, pt) be the optimal total discounted profit for the seller from season t to the end of

the planning horizon with an initial inventory It and a price pt observed in period t. We have the

following dynamic programming formulation:

Vt(It, pt) = pt · It + gt(It, pt); (1)

gt(It, pt) = max0≤yt≤It

{− δ(It − yt) ·Kt +Gt(yt, pt)

}; (2)

Gt(yt, pt) = −pt · yt −Ht(yt)+βt−1 ·E[Vt−1(yt +Qt−1, Pt−1)

∣∣∣∣pt], (3)

where the expectation in Eq. (3) is taken with respect to Qt−1 and Pt−1 conditioning on the

observed price pt in season t, and the function δ(x) = 1 if x > 0, δ(x) = 0 otherwise. For the last

period t= 0, V0(I0, p0) = I0 · p0 − δ(I0) ·K0.

In inventory models for manufactured products, the decision is typically on the order-

ing/production quantities that are determined before demand uncertainty is resolved. In contrast,

for agricultural products, the decision here is on the selling quantity that is determined after supply

and price uncertainties are resolved.

In what follows, we shall classify the model defined in Eqs. (1)-(3) by various cost structures

(for selling and inventory holding). In practice, a selling transaction may involve a fixed cost,

Kt > 0, representing shipping, loading/unloading, sampling and testing, as well as sales, general

and administrative (SG&A) expenses. While in some cases, such costs are covered by buyers and/or

sales agents, i.e., Kt = 0 for the seller; in other cases, the seller has to pay by itself, i.e., Kt > 0.

Inventory cost often includes storage cost and capital cost/interest as its two main components.

If the storage cost dominates, then the inventory carrying cost Ht(y) is likely concave due to

economies of scale in storage. Conversely, if the capital cost dominates, then Ht(y) is likely convex

due to the dis-economies of scale in capital cost and interest. In the sequel, we shall derive the

optimal dynamic selling policy for each of the four combinations of these cost structures: (i) Kt = 0

and concave holding cost, (ii) Kt > 0 and concave holding cost, (iii) Kt = 0 and convex holding

cost, and (iv) Kt > 0 and convex holding cost. More results are developed for the special case of

linear holding cost in §5.

Shi, Zhao and Kiwanuka: Agricultural Supply Chain18 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

4.1. Zero Fixed Selling Cost and Concave Holding Cost

In this section, we consider the dynamic program model by Eqs. (1)-(3) with Kt = 0 and concave

Ht(·) for all t. Thus, for each period t, the cost function, −ptyt −Ht(yt), is convex. We have the

following theorem (all proofs are included in Appendix).

Theorem 1 If Kt = 0 and Ht(y) is concave for all t= 1,2, ..., T , then,

(i) Vt(It, pt) is increasing and convex in It for all t.

(ii) The optimal selling policy is a selling-all-or-retaining-all policy. Specifically, there exists a

threshold quantity, Rt(pt)≥ 0, such that the optimal carry-over inventory

y∗t =

It, if It ≥Rt(pt);

0, o.w.

(4)

where

Rt(pt) = sup

{y≥ 0

∣∣∣∣ Gt(y, pt)≤Gt(0, pt)

}. (5)

In particular, Rt(pt) = +∞ if Gt(y, pt)<Gt(0, pt) for all y > 0; Rt(pt) = 0 if Gt(y, pt)>Gt(0, pt)

for all y > 0.

Theorem 1 states that there exists a price-dependent threshold, and it is optimal to sell all the

inventory if the inventory level is smaller than this threshold, otherwise, it is optimal to retain

all the inventory. This statement is consistent to the economies of scale in holding inventory, as

represented by the concavity of the inventory holding cost function Ht(·).

To study the sensitivity of the optimal profit function and the threshold value Rt(pt) with respect

to the price, we make the following assumption.

Assumption 2 The price process satisfies

Pt =At · ft(pt+1)+Bt, (6)

where the random variables At and Bt are independent of pt+1, At ≥ 0, and ft(p) is differentiable

and satisfies

0≤ f ′t(p) ·E[At]< 1. (7)

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 19

Remark: The price process defined in Eq. (6) represents a general class of Markovian processes,

where the future price is stochastically increasing in the current price pt because f′t(p)> 0. However,

the price process is stable over time as f ′t(p)E[At] < 1. An example of this price process is the

AR(1) process, Pt = a · pt+1 + ϵ, where ft(p) = a · p, At = 1 and Bt = ϵ.

Proposition 1 If Kt = 0 and Ht(y) is concave all t = 1,2, ..., T , the following statements hold

under Assumption 2:

(i) Functions Vt(I, p) and Gt(y, p) satisfy

∂2Vt(I, p)

∂I · ∂p≤ 1;

∂2Gt(y, p)

∂y · ∂p≤ 0. (8)

(ii) The threshold Rt(pt) increases in pt.

Proposition 1 implies we should sell more and carry less inventory at a higher price pt, and vice

versa. This is true because the future price is more likely to drop by Assumption 2.

Proposition 2 If Kt = 0 and Ht(y) is concave for all t= 1,2, ..., T , then Vt(I, p) is increasing and

convex in p under Assumption 2 and the assumption of convex ft(p).

4.2. Positive Fixed Selling Cost and Concave Holding Cost

In this section, we assume that Kt > 0 and Ht(·) is concave for all t. Similar to §4.1, the cost

function, −ptyt −Ht(yt), is convex for all t. The following theorem characterizes the structure of

the optimal selling policy.

Theorem 2 If Kt > 0 and Ht(y) is concave for all t= 1,2, ..., T , then,

(i) Vt(It, pt) is increasing and convex in It for all t.

(ii) The optimal selling policy is an selling-all-or-retaining-all policy and there exists a pair of

thresholds 0≤ rt(pt)≤Rt(pt), such that the optimal carry-over inventory

y∗t =

0, if rt(pt)< It <Rt(pt);

It, o.w.

(9)

Shi, Zhao and Kiwanuka: Agricultural Supply Chain20 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

The two thresholds rt(pt)≤Rt(pt) are given by

rt(pt) = inf

{y≥ 0

∣∣∣∣ Gt(y, pt)≤Gt(0, pt)−Kt

}; (10)

Rt(pt) = sup

{y≥ 0

∣∣∣∣ Gt(y, pt)≤Gt(0, pt)−Kt

}, (11)

and Rt(pt) =+∞ if limy→∞

Gt(y, pt)<Gt(0, pt)−Kt.

Theorem 2 suggests to retain all inventory if It ≤ rt(pt). This is true because of the fixed selling

cost. Theorem 2 also suggests to retain all inventory if It ≥Rt(pt). This can be explained by the

economies of scale in holding inventory as in §4.1.

Similar to §4.1, we characterize the sensitivity of the thresholds as follows.

Proposition 3 If Kt > 0 and Ht(y) is concave for all t= 1,2, ..., T , then

(i) It is optimal to retain all inventory if and only if

Gt(0, pt)−miny>0

Gt(y, pt)<Kt. (12)

(ii) As Kt increases, rt(pt) increases and Rt(pt) decreases.

(iii) Under Assumption 2, rt(pt) decreases and Rt(pt) increases in pt.

Proposition 3 shows that it is less likely to sell all inventory if the fixed selling cost is greater, and

if the fixed selling cost is sufficiently large, it is optimal to retain all inventory. On the other hand,

it is more likely to sell all inventory if the observed price is higher.

4.3. Zero Fixed Selling Cost and Convex Holding Cost

In this section, we assume that Kt = 0 and Ht(·) is convex for all t. In this case, for each period t,

the cost function, −ptyt−Ht(yt), is concave. Theorem 3 provides structural results for the optimal

selling policy.

Theorem 3 If Kt = 0 and Ht(y) is convex for all t= 1,2, ..., T , then,

(i) Gt(yt, pt) is concave in yt for all t.

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 21

(ii) Vt(It, pt) is increasing and concave in It for all t.

(iii) The optimal selling policy is an selling-down-to s policy, that is, there exists a threshold,

st(pt), such that the optimal carry-over inventory

y∗t =

st(pt), if It ≥ st(pt);

It, o.w.

(13)

where

st(pt) = argmaxy≥0

{Gt(y, pt)}, (14)

and st is independent of It and Qt.

Note that Theorem 3 holds for any V0(I0, p0) that is concave in I0. Intuitively, Theorem 3 shows

that it is optimal to sell down to st(pt) if the inventory level is above it; otherwise, retain all

inventory. We should point out that the selling-down-to policy for agricultural products resembles

the optimal order-up-to policies in inventory models for manufactured products although no simple

transformation can convert one model to the other.

Similar to previous sections, we characterize the sensitivity of the threshold as follows.

Proposition 4 If Kt = 0 and Ht(y) is convex for all t= 1,2, ..., T , the following statements hold

under Assumption 2:

(i) functions Vt(I, p) and Gt(y, p) satisfy

∂2Vt(I, p)

∂I · ∂p≤ 1;

∂2Gt(y, p)

∂y · ∂p≤ 0; (15)

(ii) the threshold st(pt) decreases in pt.

Proposition 4 indicates that it is more likely to sell more if the price pt is higher, and vice versa.

4.4. Positive Fixed Selling Cost and Convex Holding Cost

In this section, we assume that Kt > 0 and Ht(·) is convex for all t. Similar to §4.3, the cost

function, −ptyt −Ht(yt), is concave for all t. Theorem 4 characterizes the structure of the optimal

selling policy.

Shi, Zhao and Kiwanuka: Agricultural Supply Chain22 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

Theorem 4 If Kt > 0 and Ht(y) is convex for all t= 1,2, ..., T , and 0< βt ·Kt ≤Kt+1, then for

any given pt,

(i) gt(yt, pt) is Kt-concave in yt.

(ii) Vt(It, pt) is increasing and Kt-concave in It.

(iii) The optimal selling policy is an selling-down-to (S, s) policy, that is, in period t > 0, there

exists a pair of thresholds, 0≤ st(pt)<St(pt), such that the optimal carry-over inventory

y∗t =

st(pt), if It ≥ St(pt),

It, o.w.

(16)

where st(pt) = argmaxy≥0

{Gt(y, pt)} and

St(pt) = sup{y∣∣y > st, Gt(y, pt) =Gt(st, pt)−Kt

}. (17)

The thresholds St(pt) and st(pt) are independent of It and Qt.

Theorem 4 states that it is optimal to sell down to st if the inventory is greater than (or equal

to) St where St > st; otherwise, it is optimal to retain all inventory. Such a selling − down − to

(S, s) policy for agricultural products is analogous to the well-known (s, S) ordering policy for

manufactured products. The key difference is that the policies operate in the opposite direction:

ordering to stock up the inventory for manufactured products versus selling to deplete the inventory

for agricultural products.

5. Special Cases with Linear Holding Cost

In this section, we consider linear holding cost, that is, Ht(yt) = ht · yt for all t, where ht ≥ 0 is the

inventory carrying cost per unit per period. The dynamic programming model given by Eq. (3)

can be written as

Gt(yt, pt) =−(pt +ht) · yt +βt−1E[Vt−1(yt +Qt−1, Pt−1)|pt], (18)

where the equations for Vt(It, pt) and gt(It, pt) remain the same. Interestingly, linear inventory cost

allows us to derive much stronger results (e.g., closed-form recursive expressions) for the optimal

policy and discounted profit with or without a fixed selling cost.

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 23

5.1. Zero Fixed Selling Cost

The following theorem provides closed-form recursive equations for the optimal selling policy and

discounted profit,

Theorem 5 If Kt = 0 and Ht(y) = ht · y for each period t, then

(i) the optimal selling policy is a selling-all-or-retaining-all policy characterized by a cut-off price,

p∗t , such that,

y∗t =

0, if pt ≥ p∗t ,

It, o.w.

(19)

where the cut-off price is recursively given by

p∗t ≡ p∗t (pt) = βt−1 ·E[max{Pt−1, p

∗t−1(Pt−1)}

∣∣∣∣pt]−ht, (20)

with p∗0 = 0.

(ii) The optimal discounted profit is explicitly given by

Vt(It, pt) =max{pt, p∗t} · It +t∑

s=1

βt,s ·(E[p∗s|pt] +hs

)·E[Qs−1] (21)

where for 0≤ s < t, βt,s = βt−1 ·βt−2 · · ·βs is the cumulative discount factor from period s to period

t (backward indexed).

Theorem 5 is consistent to Theorems 1 and 3. Specifically, for a linear Ht(·), we can show that,

depending on price pt, either Rt = 0 or Rt =+∞ in Theorem 1; either st = 0 or st =+∞ in Theorem

3. More precisely, st is determined by,

st =

0, if pt ≥ p∗t ,

+∞, o.w.

(22)

Theorem 5 provides rich insights on how to sell inventory for agricultural products. Let’s first

look at the 2nd last period. By Eq. (20) and the fact that p∗0 = 0, i.e., we sell all inventory in the

last period,

p∗1 = β0E[P0|p1]−h1. (23)

Shi, Zhao and Kiwanuka: Agricultural Supply Chain24 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

Thus it is optimal to sell all inventory in the 2nd last period if the price p1 is greater than or equal

to p∗1 which is the discounted expected price for the period 0 subtracting the inventory holding

cost. Furthermore, the cut-off price, p∗1, does not depend on the available inventory or the harvest.

This insight is nearly identical to the observation made by Fackler and Livingstone(2002), a simple

strategy considers whether the price is expected to rise in the near future to cover the cost of storage.

For periods prior to the 2nd last period, Eq. (20) indicates that the optimal cut-off price of one

period depends on the cut-off price of the next period. Hence, the simple observation of Fackler

and Livingstone(2002) does not work because we do not sell all inventory regardless of the price in

the next period, but only when the next periods cut-off price is met. Thus we must take the next

periods cut-off price into account in determining this period’s cut-off price.

Steady-State Analysis for I.I.D. Price Process. If prices in all periods are i.i.d. random

variables, i.e., Pt equals to P in distribution for all t, and the system parameters are stationary,

that is, ht = h, βt = β, ∀t, then we can obtain closed-form expressions for the optimal cut-off price

and the optimal discounted profit in steady state.

Proposition 5 If Pt = P in distribution, ht = h, βt = β for all t, then

(i) the cut-off prices satisfy

β ·E[P ]−h= p∗1 ≤ . . .≤ p∗t ≤ p∗t+1 → p∗,

where p∗ is uniquely determined by

p∗ = β ·E[max{P,p∗}]−h. (24)

(ii) If {Qt} are i.i.d. random variables, i.e., Qt =Q in distribution for all t, then

limt→∞

Vt(I, p) =max{p, p∗} · I +(p∗ +h)E[Q]/(1−β). (25)

Proposition 5 part (i) shows that p∗ depends only on β, h and the price distribution but not on

the distribution of supply Qt. The monotonicity of {p∗t} has an important practical implication:

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 25

with more seasons in the future to sell, the higher the cut-off price should be because one has a

better chance of getting a good price in the future.

Optimal Selling Policy vs. Selling-All. With the closed-form expression of the optimal dis-

counted profit, we can make an explicit comparison between the performance of the optimal selling

policy and that of the benchmark strategy of selling-all.

Proposition 6 If the initial inventory is zero, then the optimal selling policy improves the selling-

all strategy in expected profit by

T−1∑t=0

βtE[max{PT−t, p

∗T−t(PT−t)}−PT−t

∣∣∣∣PT

]E[QT−t]≥ 0.

For stationary parameters, we can derive an even simpler expression for the gap between the

optimal selling policy and the “selling-all” strategy in steady-state. In view of Proposition 6, the

improvement can be simplified as(E[max{P,p∗}]−E[P ]

)·E[Q]/(1−β).

Storage Capacity Constraints. Storage capacity imposes a restriction on the maximum inven-

tory level and thus changes the structure of the optimal selling policy. Under a fixed storage capacity

constraint, Ct, the dynamic programming model can be written as,

Vt(It, pt) = pt · It + max0≤yt≤min{It,Ct}

{− (pt +ht) · yt +βt−1E[Vt−1(yt +Qt−1, pt−1)|pt]

}, (26)

where V0(I0, p0) = p0 · I0.

Theorem 6 If Kt = 0, Ht(y) = ht · y, and the constant Ct > 0 is the storage capacity for period t,

then Vt(It, pt) is concave in It for all t≥ 0 and the optimal selling policy is a selling-down-to policy.

Theorem 6 implies that with a storage capacity constraint, the optimal policy is a selling-down-

to policy which suggests to sell a portion of the available inventory (if any) down to the threshold

level and retain the rest.

Shi, Zhao and Kiwanuka: Agricultural Supply Chain26 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

5.2. Positive Fixed Selling Cost

With a fixed selling cost Kt > 0 and a linear inventory holding cost, Theorem 2 shows that the

optimal selling policy is a selling-all-or-retaining-all policy. To see the impact of the fixed selling

cost, we take the 2nd last period (t = 1) as an example and derive the optimal policy and the

optimal discounted profit. Following a similar procedure as in the proof of Theorem 5, we obtain

V1(I1, p1) = max{p1 · I1 −K1, p∗1 · I1

}+β0 ·E[P0] ·E[Q0]−β0 ·K0, (27)

where p∗1 is defined in Eq. (23), and the optimal policy is

y∗1 =

0 if (p1 − p∗1) · I1 ≥K1,

I1 o.w.

We can see here that to sell all, it requires not only p1 > p∗1 as in Eq. (19) for a zero fixed cost,

but also p1 to be sufficiently greater than p∗1 so as to cover the fixed selling cost K1. Note that the

cut-off price here is p∗1 +K1/I1 which depends on the available inventory I1.

The following theorem provides closed-form recursive equations for the optimal selling policy

and discounted profit of any period.

Theorem 7 For any period t, if Ht(y) = hty and Kt > 0, then Vt(It, pt) has the following expression

Vt(It, pt) = pt · It −Kt +

[(p∗t − pt) · It +Kt +βt−1 · [Tt−1(It)−Tt−1(0)]

]+

+At, (28)

where p∗t is recursively given by Eq. (20) and for t > 0

At =t−1∑i=0

βi

[E[Pi] ·E[Qi]−Ki +Tt−1(0)

], (29)

Tt(y) = E[(p∗t −Pt)(y+Qt)+Kt +βt−1 · [Tt−1(y+Qt)−Tt−1(0)]

]+

, (30)

and A0 = 0, T0(y) = 0 for any y≥ 0, βi = β0 ·β1 · · ·βi.

Furthermore, the optimal decision is to sell all if and only if

(p∗t − pt) · It +Kt +βt−1 · [Tt−1(It)−Tt−1(0)]> 0; (31)

otherwise to retain all.

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 27

6. Numerical Study: Kenya Cooperative Coffee Exporters

In this section, we conduct a numerical study based on the real-life data of a grower organization

in Kenya, Kenya Cooperative Coffee Exporters (KCCE). Our objective is to quantify the optimal

selling policies and their potential impact on practice. We shall also illustrate the sensitivity of the

optimal policy and its performance with respect to various parameters, such as holding cost, time

horizon, and discounted rate, as well as the price process.

KCCE was founded in 2009 by small-scale grower cooperatives in Kenya to market their coffee.

KCCE conducts secondary processing, storage, marketing and distribution for its own brand of

coffee named KEN CAFE. Not only does KCCE consolidate the supply chain but also unite the

ownership and control of the coffee in one entity. With the ownership of the coffee, KCCE can

control the amount of coffee sold in each season and retain the rest to future seasons for a potentially

better price. KCCE sells weekly at Nairobi coffee auction year around (not every week, depending

on the crop seasons).

We retrieve the weekly harvest (and export) and selling price data of KCCE at the Nairobi Coffee

Exchange (auction) from 11/16/2010 to 2/22/2011. Consistent to the empirical study in §3.3, a

statistical study shows that the exports of KCCE are independent of KCCE’s selling prices, the har-

vests (in 50kg bags) follow an i.i.d. process with a marginal distribution of Normal(173.32,148.74),

and the price process of KCCE (in US$ per 50kg bag) follows an AR(1) process as

Pt−1 = 165.4+0.6886Pt + ϵt, ϵt ∼Normal(0,46.5). (32)

We set other parameters for the numerical study in the following way: we follow Sengupta and

Wang (1991) and Berg (1987) to set the inventory holding cost to be $0, $2, $4, · · · , $40 (per 50kg

bag per week). The discounted rate is obtained from the interest rate of the treasury bill issued

by the Kenya government, about 3% a year (Central Bank of Kenya, 8/2010); which leads to a

weekly discounted rate of β = 99.84%. To study the impact of the discounted rate, we also vary β

over β = 80%, 85%, 90% and 95%. The transaction costs of selling are obtained from Coffee Board

of Kenya which are bundled into a variable cost and subtracted from the price. Hence, the model

with zero fixed selling cost and linear holding cost applies here. As a benchmark, we compute the

discounted profit for the prevailing selling-all policy (“SA”) for every instance and compare it to

that of the optimal policy (the selling-all-retaining-all policy – “SARA”). All numerical studies

are conducted on the observed sample path of the actual harvest of KCCE. Finally, to study the

impact of the price process, we shall consider both i.i.d. and AR(1) price processes.

Shi, Zhao and Kiwanuka: Agricultural Supply Chain28 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

6.1. I.I.D. Price Process

In this section, we ignore the autocorrelation among prices in consecutive periods (as specified

in Eq. 32), and model the price process as a series of i.i.d. random variables but with the same

marginal distribution. In particular, according to Eq. (32), we calculate the marginal distribution of

the price to be P ∼Normal(530.8, 149.2) (in US$ per 50kg bag), which is used as the distribution

for the price in each period. Our objective is to develop insights on the optimal selling policy for

i.i.d. price processes and also to use the results as a benchmark for comparison with those of AR(1)

price process.

We compute the optimal cut-off prices for various inventory holding costs, time horizons and

discounted rates. Figures 3-4 summarize the results and reveal the following insights:

�������

�������

�������

�������

�������

�������

�������

�������

� � �� �� � � � � �� �� ��

�������

���

��� ���������� �����

������������ ������������������ �����

����� ��� ��������������

����

����

�����

p*=$795.53

p*=$731.41

p*=$688.72

Figure 3 Asymptotic Analysis of Cut-off Price

��������

��������

��������

��������

��������

��������

��������

�� ��� ��� ��� ���� ���� ���� ���� ����

������������

� ������� ������

Cut-off Price vs Holding Cost (with Selected Discount Rates)

���

���

���

���

Figure 4 Cut-off Price vs. Holding Cost

• The optimal cut-off price increases in the number of periods (weeks) left in the planning

horizon and exponentially converges to the steady-state value p∗ as the number of periods goes to

infinity, confirming our analysis in §5.1.

• The optimal cut-off price could be either above or below the average price, and it decreases in

h and increases in β.

To assess the potential impact of the SARA policy, we compare SARA and SA policies on

their Expected NPV, that is, the expected net present value of the profits over the periods from

11/16/2010 to 2/22/2011. Specifically, we randomly generate weekly prices (according to the i.i.d.

price process assumed above) for 106 replications (or sample paths). For each sample path (repli-

cation) of the prices, we apply the optimal SARA policy and the SA policy, and compute their

NPVs respectively. Finally, we take the average of the NPVs over all replications under each policy

to obtain the expected NPV.

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 29

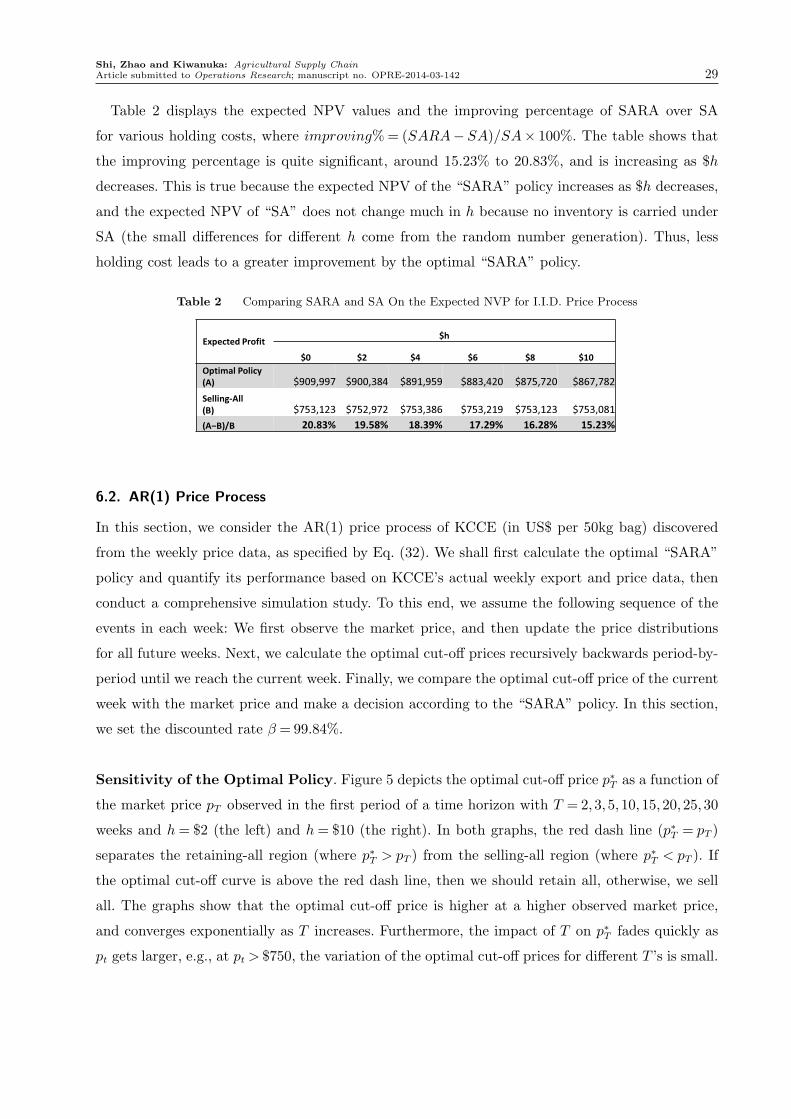

Table 2 displays the expected NPV values and the improving percentage of SARA over SA

for various holding costs, where improving%= (SARA− SA)/SA× 100%. The table shows that

the improving percentage is quite significant, around 15.23% to 20.83%, and is increasing as $h

decreases. This is true because the expected NPV of the “SARA” policy increases as $h decreases,

and the expected NPV of “SA” does not change much in h because no inventory is carried under

SA (the small differences for different h come from the random number generation). Thus, less

holding cost leads to a greater improvement by the optimal “SARA” policy.

Table 2 Comparing SARA and SA On the Expected NVP for I.I.D. Price Process

����������� ���

������ �� �� �� �� ���

��� ������ ���

���� �������� �������� ������ �������� ������� ��������

���� � !�������

�"� ������ ������� ������� ������ ������ ������

��#"�$" ������ ����� ������ ����� ������ �����

6.2. AR(1) Price Process

In this section, we consider the AR(1) price process of KCCE (in US$ per 50kg bag) discovered

from the weekly price data, as specified by Eq. (32). We shall first calculate the optimal “SARA”

policy and quantify its performance based on KCCE’s actual weekly export and price data, then

conduct a comprehensive simulation study. To this end, we assume the following sequence of the

events in each week: We first observe the market price, and then update the price distributions

for all future weeks. Next, we calculate the optimal cut-off prices recursively backwards period-by-

period until we reach the current week. Finally, we compare the optimal cut-off price of the current

week with the market price and make a decision according to the “SARA” policy. In this section,

we set the discounted rate β = 99.84%.

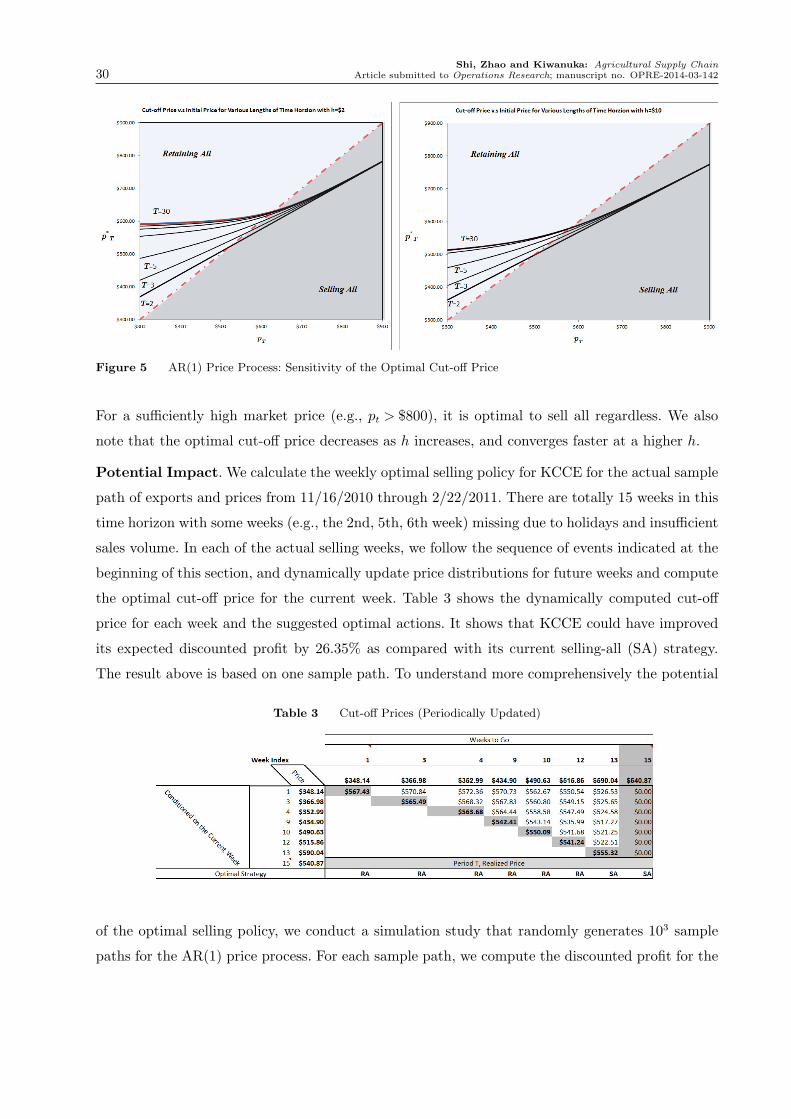

Sensitivity of the Optimal Policy. Figure 5 depicts the optimal cut-off price p∗T as a function of

the market price pT observed in the first period of a time horizon with T = 2,3,5,10,15,20,25,30

weeks and h= $2 (the left) and h= $10 (the right). In both graphs, the red dash line (p∗T = pT )

separates the retaining-all region (where p∗T > pT ) from the selling-all region (where p∗T < pT ). If

the optimal cut-off curve is above the red dash line, then we should retain all, otherwise, we sell

all. The graphs show that the optimal cut-off price is higher at a higher observed market price,

and converges exponentially as T increases. Furthermore, the impact of T on p∗T fades quickly as

pt gets larger, e.g., at pt > $750, the variation of the optimal cut-off prices for different T ’s is small.

Shi, Zhao and Kiwanuka: Agricultural Supply Chain30 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

Figure 5 AR(1) Price Process: Sensitivity of the Optimal Cut-off Price

For a sufficiently high market price (e.g., pt > $800), it is optimal to sell all regardless. We also

note that the optimal cut-off price decreases as h increases, and converges faster at a higher h.

Potential Impact. We calculate the weekly optimal selling policy for KCCE for the actual sample

path of exports and prices from 11/16/2010 through 2/22/2011. There are totally 15 weeks in this

time horizon with some weeks (e.g., the 2nd, 5th, 6th week) missing due to holidays and insufficient

sales volume. In each of the actual selling weeks, we follow the sequence of events indicated at the

beginning of this section, and dynamically update price distributions for future weeks and compute

the optimal cut-off price for the current week. Table 3 shows the dynamically computed cut-off

price for each week and the suggested optimal actions. It shows that KCCE could have improved

its expected discounted profit by 26.35% as compared with its current selling-all (SA) strategy.

The result above is based on one sample path. To understand more comprehensively the potential

Table 3 Cut-off Prices (Periodically Updated)

of the optimal selling policy, we conduct a simulation study that randomly generates 103 sample

paths for the AR(1) price process. For each sample path, we compute the discounted profit for the

Shi, Zhao and Kiwanuka: Agricultural Supply ChainArticle submitted to Operations Research; manuscript no. OPRE-2014-03-142 31

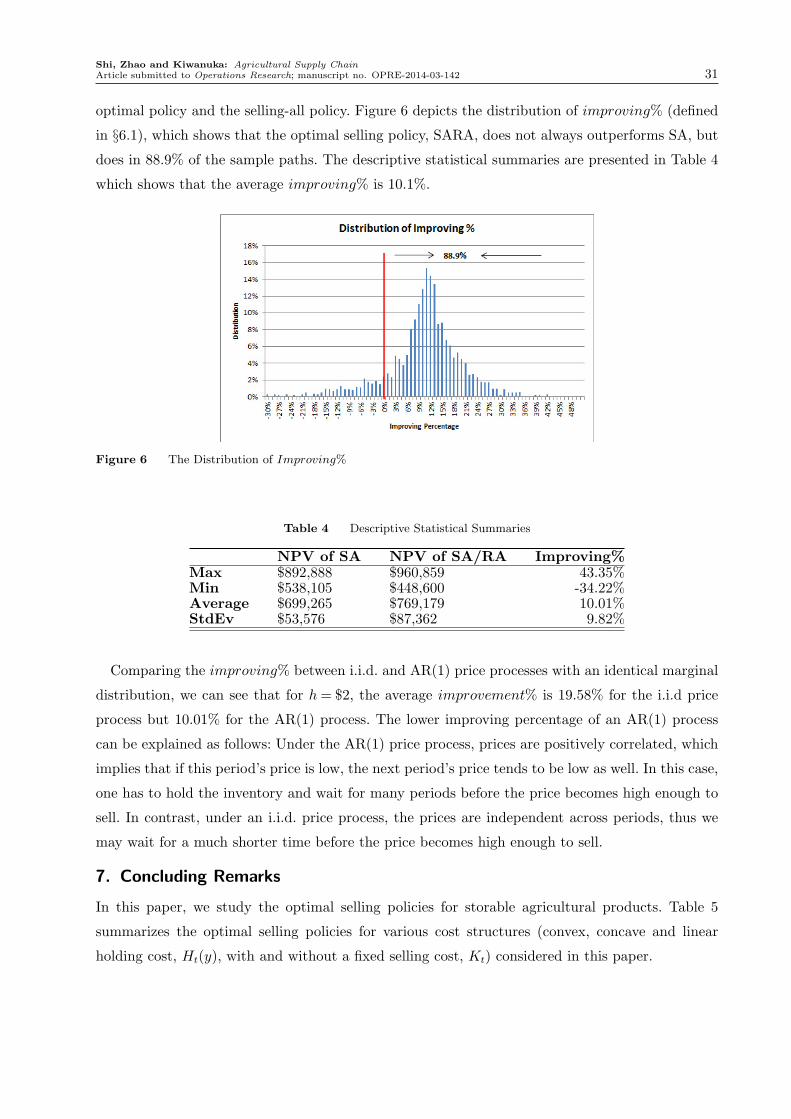

optimal policy and the selling-all policy. Figure 6 depicts the distribution of improving% (defined

in §6.1), which shows that the optimal selling policy, SARA, does not always outperforms SA, but

does in 88.9% of the sample paths. The descriptive statistical summaries are presented in Table 4

which shows that the average improving% is 10.1%.

Figure 6 The Distribution of Improving%

Table 4 Descriptive Statistical Summaries

NPV of SA NPV of SA/RA Improving%Max $892,888 $960,859 43.35%Min $538,105 $448,600 -34.22%Average $699,265 $769,179 10.01%StdEv $53,576 $87,362 9.82%

Comparing the improving% between i.i.d. and AR(1) price processes with an identical marginal

distribution, we can see that for h= $2, the average improvement% is 19.58% for the i.i.d price

process but 10.01% for the AR(1) process. The lower improving percentage of an AR(1) process

can be explained as follows: Under the AR(1) price process, prices are positively correlated, which

implies that if this period’s price is low, the next period’s price tends to be low as well. In this case,

one has to hold the inventory and wait for many periods before the price becomes high enough to

sell. In contrast, under an i.i.d. price process, the prices are independent across periods, thus we

may wait for a much shorter time before the price becomes high enough to sell.

7. Concluding Remarks

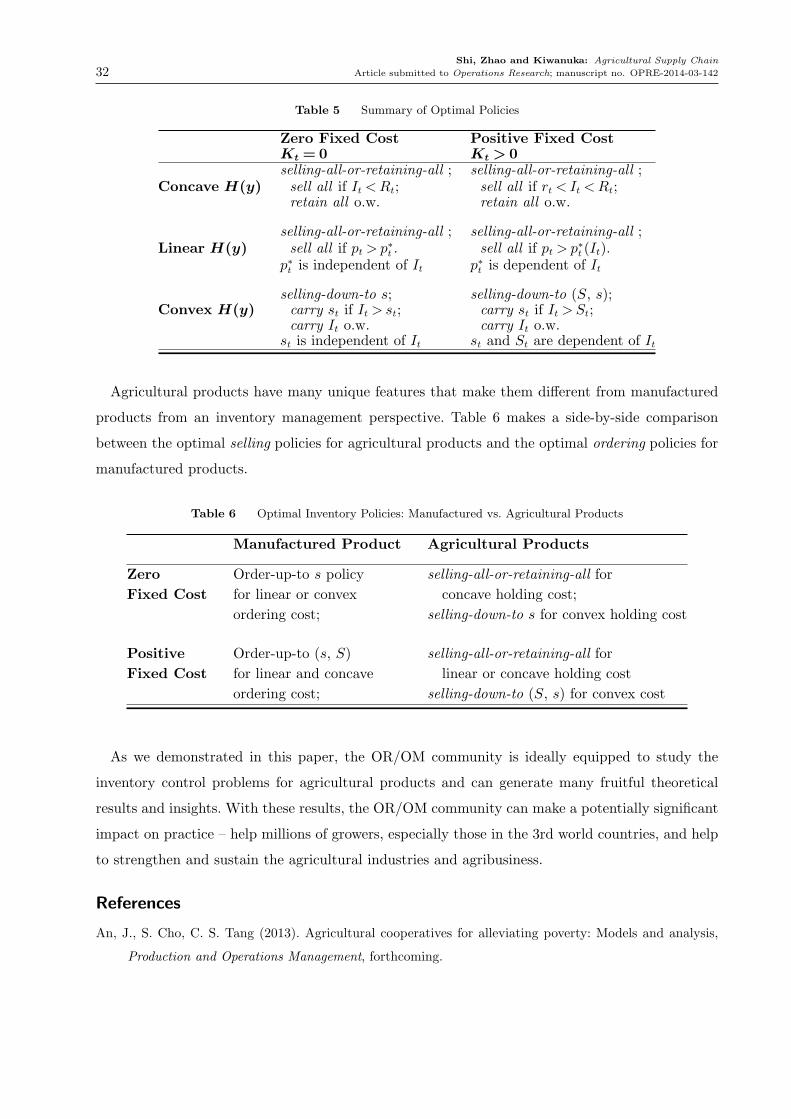

In this paper, we study the optimal selling policies for storable agricultural products. Table 5

summarizes the optimal selling policies for various cost structures (convex, concave and linear

holding cost, Ht(y), with and without a fixed selling cost, Kt) considered in this paper.

Shi, Zhao and Kiwanuka: Agricultural Supply Chain

32 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

Table 5 Summary of Optimal Policies

Zero Fixed Cost Positive Fixed CostKt = 0 Kt > 0selling-all-or-retaining-all ; selling-all-or-retaining-all ;

Concave H(y) sell all if It <Rt; sell all if rt < It <Rt;retain all o.w. retain all o.w.

selling-all-or-retaining-all ; selling-all-or-retaining-all ;Linear H(y) sell all if pt > p∗t . sell all if pt > p∗t (It).

p∗t is independent of It p∗t is dependent of It

selling-down-to s; selling-down-to (S, s);Convex H(y) carry st if It > st; carry st if It >St;

carry It o.w. carry It o.w.st is independent of It st and St are dependent of It

Agricultural products have many unique features that make them different from manufactured

products from an inventory management perspective. Table 6 makes a side-by-side comparison

between the optimal selling policies for agricultural products and the optimal ordering policies for

manufactured products.

Table 6 Optimal Inventory Policies: Manufactured vs. Agricultural Products

Manufactured Product Agricultural Products

Zero Order-up-to s policy selling-all-or-retaining-all for

Fixed Cost for linear or convex concave holding cost;

ordering cost; selling-down-to s for convex holding cost

Positive Order-up-to (s, S) selling-all-or-retaining-all for

Fixed Cost for linear and concave linear or concave holding cost

ordering cost; selling-down-to (S, s) for convex cost

As we demonstrated in this paper, the OR/OM community is ideally equipped to study the

inventory control problems for agricultural products and can generate many fruitful theoretical

results and insights. With these results, the OR/OM community can make a potentially significant

impact on practice – help millions of growers, especially those in the 3rd world countries, and help

to strengthen and sustain the agricultural industries and agribusiness.

References

An, J., S. Cho, C. S. Tang (2013). Agricultural cooperatives for alleviating poverty: Models and analysis,

Production and Operations Management, forthcoming.

Shi, Zhao and Kiwanuka: Agricultural Supply Chain

Article submitted to Operations Research; manuscript no. OPRE-2014-03-142 33

Akiyama, T., P. N. Varangis, (1990). The impact of the International Coffee Agreement on producing coun-

tries, World Bank Economic Review, 4(1): 157-173.

Alaouze, C. M., N. H. Sturgess, A.S. Watson, (1978). Australian wheat storage: A dynamic programming

approach, Australian Journal of Agricultural Economics, 22(3).

Berg, E. (1987). A sequential decision model to determine optimal farm-level grain marketing policies,

European Review of Agricultural Economics, 14: 091-116.

Bertsekas, D. P. (1976). Dynamic programming and stochastic control. Mathematics in Science and Engi-

neering, Vol. 123.

Bhaskaran, S., K. Ramachandran, J. Semple, (2010). A dynamic inventory model with the right of refusal.

Management Science, 56(12), 2265-2281.

Blakeslee, L. (1997). Optimal sequential grain marketing decisions under risk aversion and price uncertainty,

American Journal of Agricultural Economics, 79(4): 1140-1152.

Boyabatli, O., L. B. Toktay, (2004). Operational hedging: A review with discussion. Tech. rep.

Chen, X., D. Simchi-Levi, (2004). Coordinating inventory control and pricing strategies with random demand

and fixed ordering cost: The finite horizon case. Operations Research, 52(6), 887-896.

Daviron, B., S. Ponte (2006). The Coffee Paradox: Global Markets, Commodity Trade and the Elusive Promise

of Development. Zed Books Ltd, London, UK.

Dugundji, J., A. Granas (2010). Fixed Point Theory. Springer, New York.

Fackler, P. L., M. J. Livingston (2002). Optimal storage by crop producers, American Journal of Agriculture

Economics, 84(3): 645-659.

Federgruen, A., A. Heching, (1999). Combined pricing and inventory control under uncertainty. Operations

research, 47(3), 454-475.

Gustafson, R. L. (1958). Carryover levels for grain: A method for determining amounts that are optimal

under specified conditions, USDA Tech. Bull No. 1178, Washington, D.C.

Huchzermeier, A., M. A. Cohen, (1996). Valuing operational flexibility under exchange rate risk. Operations

research, 44(1), 100-113.

Kawanuka, R. K., Y. Zhao (2009). From farm to cup: The coffee supply chain in Kenya, Case Study – Rutgers

Business School-Newark and New Brunswick.

Kazaz, B., S. Webster, (2011). The impact of yield-dependent trading costs on pricing and production

planning under supply uncertainty. Manufacturing & Service Operations Management, 13(3), 404-417.

Knapp, K. C. (1982). Optimal grain carryovers in open economies: A graphical analysis, American Journal

of Agricultural Economics, 64(2): 197.

Lai, J. Y., R. J. Myers, S. D. Hanson (2003). Optimal on-farm grain storage by risk-averse farmers, Journal

of Agricultural and Resource Economics, 28(3): 558-579.

Shi, Zhao and Kiwanuka: Agricultural Supply Chain

34 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

Nyangito, H. O. (2002). Policy and legal framework for the coffee subsector and the impact of liberalization in

Kenya, KIPPRA Policy Paper No. 2., Kenya Institute of Public Policy Research and Analysis, Nairobi.

Osorio, N. (2002). Technological developments on coffee: Constraints encountered by producing countries.

International Coffee Organisation.

Oxfam International Commodity Research (2001). The coffee market: a background study,

http://www.maketradefair.com/en/assets/english/BackgroundStudyCoffeeMarket.pdf.

Pindyck, R. S., D. L. Rubinfeld (1998). Econometric Models and Economic Forecasts, 4th Ed. Irwin/McGraw-

Hill International Editions.

Ponte, S. (2002). The latte revolution? regulation, markets and consumption in the global coffee chain, World

Development, 30: 1099-1122.

Porteus, E. L. (2002). Foundations of Stochastic Inventory Theory. Stanford University Press. CA

Prabhu, N. U. (1998). Stochastic Storage Processes: Queues, Insurance Risk, Dams, and Data Communica-

tion, 2nd edition. Springer, New York.

Sengupta, J. K., E. C. Wang, (1991). Market structure implications of instability in the world coffee market,

Economic Modeling, 8(1): 102-115.

Sheskin, D. (2000). Handbook of parametric and nonparametric statistical procedures; Second Ed. Chapman

and Hall/CRC, New York.

Simchi-Levi, D., J. Bramel, X. Chen, (2005). The Logic of Logistics: Theory, Algorithms, and Applications

for Logistics and Supply Chain management. Springer.

Simchi-Levi, D., Y. Zhao, (2011). Performance evaluation of stochastic multi-echelon inventory systems: A

survey. Advances in Operations Research, Volume 2012.

Tomlin, B. (2006). On the value of mitigation and contingency strategies for managing supply chain disruption

risks. Management Science, 52(5), 639-657.

Tomlin, B., Y. Wang (2005). On the value of mix flexibility and dual sourcing in unreliable Newsvendor

networks. Manufacturing & Service Operations Management, 7(1), 37-57.

Topkis, D. M. (1998), Supermodularity and Complementarity, Princeton University Press.

Tronstad, R., C. R. Taylor (1991). Dynamically optimal after-tax grain storage, cash grain sale, and hedging

strategies, American Journal of Agricultural Economics, 73(1): 75-88.

Ugarte, M. D., A. F. Militino, A. T. Arnholt (2008). Probability and Statistics with R. Taylor and Francis

Group, LLC.

Van Mieghem, J. A. (1999). Coordinating investment, production, and subcontracting. Management Science,

45(7), 954-971.

Van Mieghem, J. A. (2003). Capacity management,investment, and hedging:Review and recent developments,

Manufacturing & Service Operations Management, 5(4), 269-302.

Shi, Zhao and Kiwanuka: Agricultural Supply Chain

Article submitted to Operations Research; manuscript no. OPRE-2014-03-142 35

Van Mieghem, J. A. (2007). Risk mitigation in Newsvendor networks: resource diversification, flexibility,

sharing, and hedging. Management Science, 53(8), 1269-1288.

Wang, Y., Y. Gerchak, (1996). Periodic review production models with variable capacity, random yield, and

uncertain demand. Management science, 42(1), 130-137.

Wang, Y., W. Gilland, B. Tomlin, (2010). Mitigating supply risk: Dual sourcing or process improvement?.

Manufacturing & Service Operations Management, 12(3), 489-510.

Wright, B. (2001). Storage and price stabilization. Chapter 14 in Handbook of agricultural economics (Ed.)

Bruce L. Gardner and Gordon C. Rausser, 817-861. Elsevier.

Yano, C. A., H. L. Lee, (1995). Lot sizing with random yields: A review. Operations Research, 43(2), 311-334.

Zipkin, P. (2000). Foundations of Inventory Management. McGraw Hill, Boston.

Shi, Zhao and Kiwanuka: Agricultural Supply Chain

36 Article submitted to Operations Research; manuscript no. OPRE-2014-03-142

8. Appendix

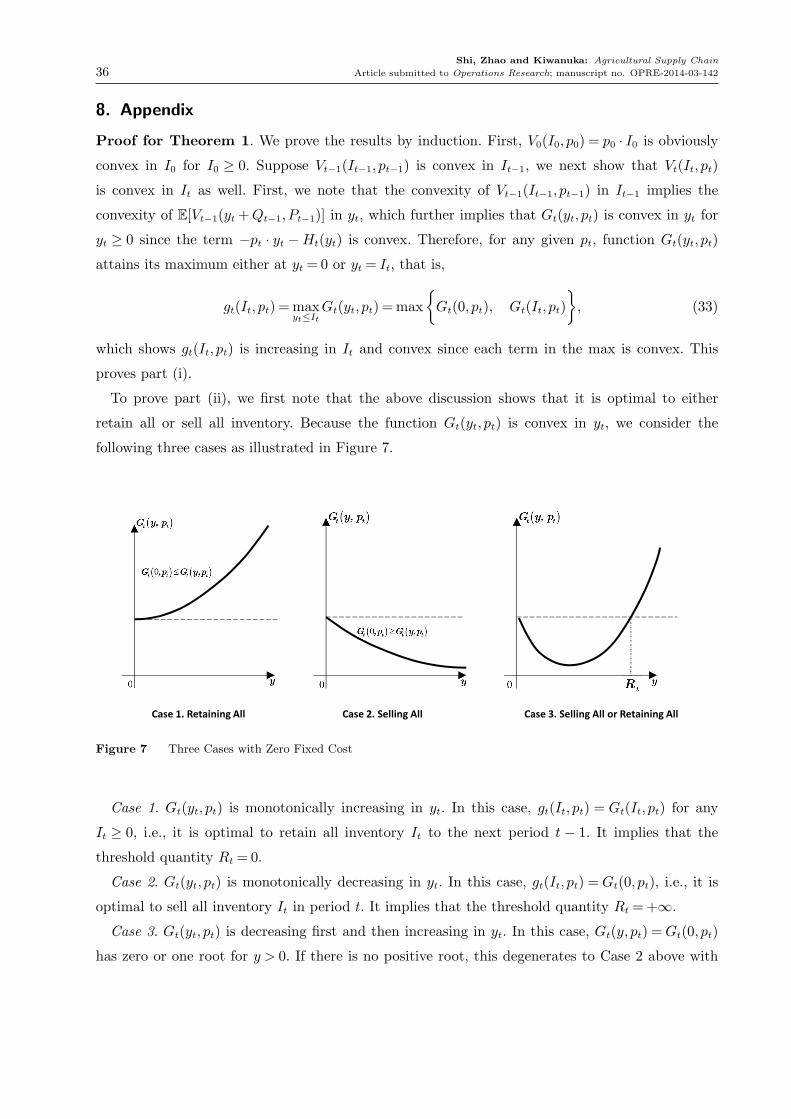

Proof for Theorem 1. We prove the results by induction. First, V0(I0, p0) = p0 · I0 is obviously

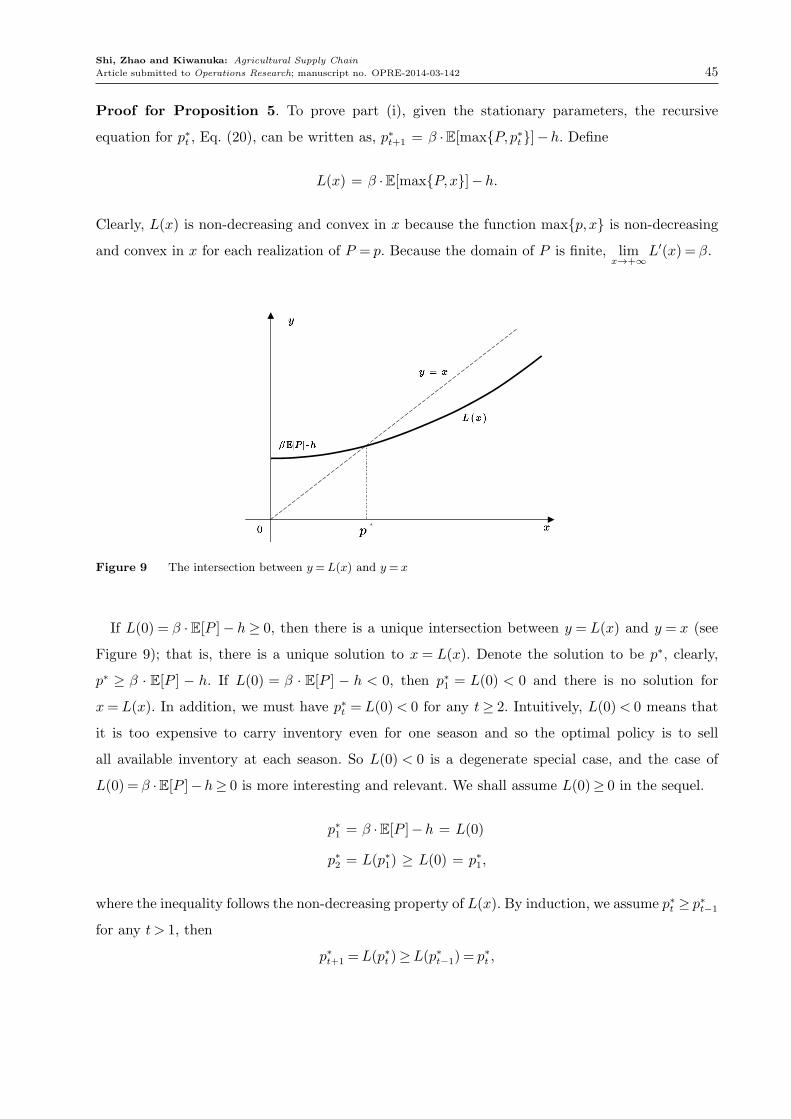

convex in I0 for I0 ≥ 0. Suppose Vt−1(It−1, pt−1) is convex in It−1, we next show that Vt(It, pt)