Embed Size (px)

Citation preview

Actes du GERPISA n° 33 7

MANAGING INFORMATION FLOWS IN SUPPLIER-CUSTOMER RELATIONSHIPS :

ISSUES, METHODS AND EMERGING PROBLEMS

Giuseppe VolpatoAndrea Stocchetti

TOWARDS A NEW SUPPLY CHAINSTRUCTURE : FROM PRODUCTIONRATIONALIZATION TO STRATEGICRATIONALIZATION

The new competitive pressuresThe analysis of the recent evolution of the

automobile supply chain shows that anextraordinary reorganization in the whole industrystructure has begun1. This reorganization mainlystems from the effort carried on by OEMs todevelop a new relationship with end customers,based upon a make-and-deliver-to-order approach,as opposed to the previous one, based upon thestock order approach. This implies a radicaltransformation in the internal organization ofautomobile firms, but it also requires a profoundreorganization in the component supply chain. As amatter of fact, the component supply chain hasbeen under pressure for about a decade, towardshigher efficiency levels, but until now this pressure

1 On most recent analysis of the reorganization of the

supply chain see : Camuffo e Volpato [1997], Sako and Helper[1999], de Banville and Chanaron [1999], Clark and Veloso[2000].

mainly related to forms of internal firmorganization (OEMs and Suppliers), and to theirwork methods. The new feature of the emergingprogram of supply chain reorganization lies in thestrategic dimension of the whole stream, mainly inthe forms of interaction between different subjectsin the chain: customers, manufacturers andsuppliers. This transformation can be seen as amove from a “production” rationalization of thecomponent supply chain to a “strategic”rationalization, where by production rationalizationwe mean a rationalization mainly (although notexclusively) based upon innovations applied oncomponent manufacturing processes, while bystrategic rationalization we mean a much widerprocess, which can influence the forms ofcomponent manufacturing, but which involves thecompetitive structure of automobile firms, and inparticular their way of interacting : from design ofwhole vehicle to manufacturing and distribution ofthe final product to drivers. What we want tounderline is that while the first thrust towardsrationalization mainly applied within individualfirms in the automobile supply chain, the secondmainly applies to the way of interaction among

Actes du GERPISA n° 338

firms in the chain, as elements of a more and morearticulated and complex system.

The scope and the radical nature of thetransformation in progress cannot be immediatelygrasped in its amplitude, since the objectives ofautomobile firms have not changed. They still aimat the supply of innovative components, capable ofensuring higher standards to the final product, withlower costs. But this objective cannot be pursuedfurther in an effective and efficient way with thepresent structure of the manufacturing chain. Aboutone decade ago, when competition triggered afurther rationalization process, known as leanproduction1, this has translated into a internalreorganization of supplier firms (as well as somereorganization within automobile firms), throughthe definition of higher quality standards : inproducts, in manufacturing processes, and inservicing. This led to a stage of great managerialand technological effort which has generatedconsiderable results2. Now, however, after thisstage of intense innovation, the process ofproduction internationalization3 on a worldwidescale and the new stage of mergers & acquisitions4,rapidly accelerating after May 1998, with themerger between Daimler and Chrysler, has led to awider competitive confrontation, which requiresbroader and more complex initiatives than theprevious ones, which were mainly aimed at higherinternal efficiency within individual supplier firms.This previous line of action will continue further,but with less and less relevant results.

1 On these aspects see Womack, Jones, Roos [1990] and

Womack, Jones [1996].2 On the specific aspects of strategic trajectories applied by

individual car manufacturers see contributions in Freyssenet etal. [1998].

3 In this paper the concept of internationalization meansthe geographic expansion of the activities (purchasing, design,manufacturing, selling) carried on by a firm.

4 The most significant stages in merger & acquisition afterthe establishment of Daimler-Chrysler in May 1998 are theacquisition of Rolls Royce and Bentley by Volkswagen in June1998, the acquisition of Dacia by Renault in July 1998, theacquisition of Bugatti by Volkswagen and GM purchasing10% of Suzuki’s capital in September 1998, the purchase ofKia and Asia Motor by Hyundai in October 1998, the purchaseof Volvo Car by Ford in January 1999, the purchase of 49% ofIsuzu by GM and of 36.8% Of Nissan and of 22.5% of NissanDiesel by Renault in March 1999, the purchase by GM of 20%of Fuji Heavy Industries which controls the Subaru brand inDecember 1999, the growth of GM’s control to 100% inJanuary 2000 and, finally, the cross-participation between GMand Fiat Auto and the acquisition by Daimler-Chrysler of 34%of Mitsubishi in March 2000.

From the organizational model of the leanorganization the greatest share of the potential forimprovement has been extracted. In order toachieve additional important efficiencies ofstructural nature, and not based upon a continuousimprovement process (kaizen), significant butmarginal, a new and more advanced organizationalmodel must be adopted, where the whole structureof the component supply chain is under scrutiny.The transformations in the last ten years haveturned out to be undoubtedly effective, and haveled to leaps both in innovation and in costreduction, but margins of future improvement havebecome gradually thinner. If one wishes tomaintain the trend of improvement expressed overthe last decade, one must shift to a neworganizational model which encompasses not justthe internal structure of individual componentmanufacturers, but the whole structure of theinternational automobile supply chain.

The objectives of the reorganizationAs it is known, the pressure towards this

profound transformation stems from the quest ofautomobile manufacturers for higher profitabilitylevels, which during recent years have decreased,along with the growing financial needs generatedby production expansion in emerging markets. The“hunt” for higher profitability levels, made moreimportant also by the inter-industry competition incapital acquisition brought by the new economy,lies in a set of dimensions, but it can besummarized as a hunt for larger scale and scopeeconomies, accomplished through forms ofmergers & acquisitions, and the focus by carmanufacturers on strategic activities which arebelieved to be capable of providing higher addedvalue. On the whole, the key fact is to externalizeall activities which a supplier can perform at alower cost compared to an integrated production,allowing to reduce total capital investment andincrease the net profit of both kinds of firm :suppliers and OEMs. The effective development ofthis scheme would lead to a higher ROE, thus tothe possibility to fairly compensate allstakeholders, which represents a necessarycondition in order to gain the substantial financialmeans required by the internationalization of themanufacturing structure and by the merger &acquisition operations.

Actes du GERPISA n° 33 9

This strategy of externalization of investmentsand costs, but not of rates of return which shouldrather increase, moves through a reorganization ofthe supply chain to an extent which would haveappeared unthinkable just a few years ago1, andwhose key points are :Ø the growth in outsourcing,Ø the concentration in the number of first-tier

suppliers,Ø the design of shared platforms;Ø the integration of systems and modularization;Ø the global sourcing.

All these initiatives, which must be movedfurther in parallel to the process of geographicexpansion in all consolidated automobile markets(USA, W. Europe, and Japan), and more recently inall emerging markets, must then be linked to ascheme of integrated management which can bereferred to as globalization2.

The growth in outsourcing,The most evident measure of the diffusion of

outsourcing lies in the gradual reduction inemployment levels of car manufacturers, linked toa marked increase in the production volume. Aclear example of this trend is General Motors.Total employment for this manufacturer decreasedfrom 761,000 units in 1990 to 388,000 units in1999, though marking in the same period a growthin car & truck production from 7.45 million to 8.78million units 3. As it is known, a considerable shareof this change has been accomplished through thede-merging of internal component manufacturingactivities which led to the establishment of Delphi,but undoubtedly the growth in outsourcingextended far beyond this de-merging operation,which has been anticipated or followed by manyother manufacturers such as Daimler-Chrysler,

1 Another relevant aspect linked to this reorganization, but

which cannot be dealt with in this paper, lies in the futureevolution of the forms of public regulation, both on vehicleemissions and on future forms of distribution. On the impact ofcommunity regulation on the European supply chain seeVolpato [2000].

2 In this paper globalization means: to implement adecision-making system able to integrate the managerialoperations of an internationalized firm in all the most relevantaspects and functions (procurement, design manufacturing,distribution and so on. See Porter [1986]. On the Fiat Auto’sglobalization project see: Volpato [1999].

3 Fiat Auto in the same period has reduced employmentworldwide from 133,431 to 82,450 units (-38.2%) maintainingthe same production level.

Ford, Fiat and Renault, which were previouslymore highly vertically integrated. The outcome ofthis policy has generated also a great increase inthe size of the component supply market, whichpresently is estimated at about $ 1,000 billion, forcars alone.

The concentration in the number of first-tier suppliers

As it has been said the effectiveness of theproduction decentralization is based upon thehypothesis that the supply system can take theplace of direct production by OEMs, with reductionin component costs. Car manufacturers try tofavour this objective through supply concentrationand the more frequent adoption of relationshipsbased upon single suppliers. This led to atransformation of the supply system from a flatstructure, where each supplier, even of small size,had direct relationships with the car manufacturer,to a highly hierarchical structure, where only first-tier suppliers have direct contacts with the OEM,and are in charge of setting up in turn a hierarchicalsystem of specialist sub-suppliers. The newdivision of labor between automobile firms andsuppliers has in turn generated new opportunitiesof merger & acquisitions with a dramatic reductionin firms specialized in production dedicated to theautomobile industry. According to estimates by theEconomist Intelligence Unit the number ofsuppliers has declined dramatically over ten years,from approximately 30,000 in 1988 to less than8,000 in 1999.

But this is just one side of the picture, althoughone of the most important in the transformationcycle triggered, given that individual suppliers arealso redefining their respective areas oftechnological competency. In the previous “flat”supply scheme each supplier tried to maximize therange of products offered, as this tended to simplifythe procedures of buyer evaluation and selection bycar manufacturers. Now in the hierarchicalstructure this aspect does not represent anadvantage, but rather a weakness since a broadproduct catalog implies too large investments anddifficulties in sustaining an adequate level ofinnovation on the whole range of products offered.Hence the supply chain is experimenting a processwhere first-tier suppliers are focusing on anarrower and more homogeneous range ofproducts, obtained through sale of activities where

Actes du GERPISA n° 3310

one is less competitive, and purchase from othersuppliers of those where one already has a strongspecialization.

Furthermore, the firms’ concentration stemsfrom specific technical needs. As suppliers must beactivated with short lead times, if one wants tomake them capable of supplying an effectivedevelopment on parts to be inserted in new models,it is necessary to carry out a process of stronginformation exchange with manufacturer designers,and the establishment of a true culture sustainingco-design1.

The design of shared platformsThe suppliers’ move towards scale and scope

economies can be adequately enriched only withforms of further standardization of products by carmanufacturers. However it is now clear that“simple” forms of standardization based upon theoffer world cars have proved to be a failure. Thishas already emerged from the difficultiesencountered in the transfer of products in moreadvanced markets of the triad (USA, WesternEurope and Japan), but the inadequatestandardization of models is going to worsen asemerging markets will consolidate (EasternEurope, Latin America, China, India and so on).

As a consequence car manufacturers areexperimenting new forms of standardization, whichare more refined and complex, but partial sincethey aim at sharing parts without standardizingmodels as they must maintain margins ofcustomization in different national markets andwith respect to the needs of the individual endcustomer2 as well. This process moves through thedesign of “common platforms” capable of using aconsiderable number of common sub-systems, butleaving room to develop the body and otherelements which can be perceived by the consumeraccording to exigencies of different markets. It is acrucial step which no car manufacturer can claimto have satisfactorily accomplished so far, buttowards which all manufacturers, with noexception, are striving, aware that it is the only wayto solve the contradiction between market varietyand manufacturing standardization.

1 See Lecler and al. [1999].2 For an analysis of the evolution of variety strategies

developed over time by car manufacturers see the essays inLung et al. [1999]. On the issue of world car and commonplatforms see Camuffo and Volpato [1997], Volpato [1998].

System integration and modularizationAnother key element of the strategic

reorganization of the automobile supply chain liesin designing a vehicle as a sum of integratedsystems and in assembly’s modularization. Theseare different things which are worth distinguishing,although they evidently share common aspects.Vehicle design by integrated systems stems fromthe fact that the vehicle can be described as a set offunctional elements, each in charge to carry outspecific tasks: production of moving energy and itstransmission to wheels (engine and powertrain), thebraking system, the steering system, the exhaustsystem. In the past these systems had a low degreeof internal integration from the design point ofview, as they were made of individual mechanicelements which could be drawn and formed withlimited forms of interdependence. Presently allthese functional systems feature a very high degreeof internal integration due to the fact that theiroperation is managed by electronic devices. Insubstance each functional system is not themechanical sum of many different parts, but itrepresents an integrated complex which can bedesigned in an optimal way only through an unitarylead, managed by a supplier acting as systemintegrator3.

On the other hand the aspect of modularizationdoes not refer to the design of individual parts in afunctional system, but focuses on its assembly andtesting activities to be carried out in the stageimmediately preceding its transfer onto the vehiclefinal assembly line. The module is then a macro-component, made with many parts which it ispossible and economically convenient to assembleand test outside the vehicle final assembly line, inorder to increase simplicity and speed. In somecases it can happen that a functional systemcoincides with a module, as in the case ofpowertrain and exhaust system, but in other casesthis does not happen. For example, the vehiclelighting system or the steering system clearlyrepresent functional systems, but their complexityand their extension over a variety of vehicle partsprevents their pre-assembly as modules4.

3 The key feature of a system integrator is that it assumes

responsibility for the execution of the most relevant technicaltasks in the product/system chain and the co-ordination of thechain’s technical and operational performance over time.

4 For an analysis of the different aspects involved bymodule production see : Sako and Warburton [1999].

Actes du GERPISA n° 33 11

Global sourcingLast, but not least, comes Global Sourcing (a

buying system based upon a worldwide monitoringand selection of most convenient suppliers). A firmhas a global sourcing system in place when it cansource parts through a choice which comparessupplier offers on a worldwide scale. The systemrequires a specific organizational structure whichallows not just to monitor a large number ofpotential suppliers scattered around manycontinents, but also a system of evaluation andconstant control for supplier performance (actualand potential), whose costs can be borne only bymajor car manufacturers. As it is known “integral”applications of this form of globalization do notpresently exist, but scholars and practitioners agreein expecting this form of buying strategy to beenhanced.

According to some, this system would allow theselection of suppliers with the best quality/priceratio. The “would” relates to the fact that on theone hand this principle of globalization clasheswith other forms of globalization and, on the otherhand, the fact that it is systematically moreconvenient has yet to be demonstrated. Withrespect to the first aspect, it is clear that a globalsourcing supply clashes with criteria of just-in-timeservice which privileges near suppliers. If the jitsupply should be carried out by a supplier just for afew years, to be then replaced by a supplier capableof offering a higher cost reduction, it comesstraightforward that the system could not work.Hence global sourcing represents an organizationalform which can be applied effectively only tospecific types of components such as highlystandardized parts with commodity nature, or partsin manufacturer catalogs which, although oftechnological and sophisticated nature, do notrequire specific customization to the needs ofdifferent vehicle models (e.g. tires, alternators,batteries, brake pads, etc.).

However by considering this process of first-level supplier concentration and the growing usageof common platforms the share of parts negotiatedthrough global sourcing procedures is likely toexpand further1.

1 On the global sourcing experience of Fiat Auto see

Camuffo and Volpato [1999].

THE QUEST FOR NEW INTEGRATIONTOOLS

The need for more qualified informationWe could therefore agree that over the last

decade the shift from a “production rationalization”to a “strategic rationalization” has resulted from adouble action : competitive push and technologypull. These two forces shaped the actualautomobile industry giving birth, about one decadeago, to new needs and opportunities at the sametime.

On the market side, the increasing competitionand the multiplying customers’ requirementsplayed a major role, pushing car manufacturers toinvest both looking for new sources of productioneconomies and for continuous productimprovement. On the technology side, the fastgrowing complexity of products and manufacturingprocesses increased the amount of know-howrequired for process operations. Moreover, thedevelopments in Information and CommunicationTechnologies (from now on ICT) createopportunities never experienced before.

Thus, from the early 1990s car manufacturerswere urged to re-arrange the supply chain maps andtheir own operations; the reorganizationencompassed both internal operations (trendstowards lean production) and relationships withsuppliers. Here the focus lies on the second issue:very shortly, the major steps in the process ofsupply chain re-organization could be summarizedas follows :Ø to reduce the number of direct suppliers;Ø to re-arrange the supply chain in order to

establish a sort of hierarchy which dividessuppliers in tiers;

Ø to outsource functions and operationspreviously considered as strategic, such asquality control, complex part design, design,assembly and test;

Ø to extend strategic control through the supplychain – as far as their speficic business isconcerned – through the management of inter-organizational relations in a way which isgenerally known as “network”.

Clearly the ongoing process of supply chainreorganization has several consequences. Amongthese, the reshaping of information flows amongsupply chain contractors : relevant changes are

Actes du GERPISA n° 3312

taking place in the way supply chain agents have tomanage information flows, not only with respect tothe management of technical issues, but withrespect to organizational consequences. In thispicture, the most peculiar aspect of this move fromproduction rationalization to strategicrationalization of the automobile supply chain isrepresented by a marked growth in integrationneeds. As a consequence the new supply chainstructure is based upon operations which require :Ø downwards, a tighter link of production with

automobile demand like the elements of make-and-delivery-to-order previously quoted,increase in product range and shortening oflife-cycles of individual models, obtainedthrough the compression of the time-to-market;

Ø upwards, a stronger cooperation betweenoperators such as co-design between first-tiersuppliers and OEMs and co-makershipbetween the system integrator and 2nd and 3rd

tier supplier.

Then the success of this great transformation islinked to the capabilities of the actors to carry outsystem of information and organizationalintegration, with higher levels of quality andcomplexity compared to those reached so far.

The control of the system implies the capabilityto exchange information with a degree ofcompleteness, speed and precision which is largelysuperior to the one which is presently available.The qualitative aspect of the new informationrequired must be underlined and qualified, sincethis dimension appears much more relevant thanthe mere quantitative development of exchangedinformation. The move from an operations chaingoverned by a push logic to a pull logic, pulled bya demand which is differentiated and variableovertime, implies a different management ofinformation. In the push logic the wholecoordination of the supply chain relies upon the exante planning activities, carried out by carmanufacturers and transmitted through a cascade-like approach on the whole supply chain. In thisscheme the chain slacks represent an efficiencyloss which is considered as inevitable, and whichcan be partly recovered through an anticipation oftimes associated with initial operations (if onewants to arrive earlier must leave earlier).

On the contrary in a pull logic, where thestarting point for operations is not governed by car

manufacturers, but results from the composition ofa large number of individual decisions byconsumers, it must be taken as a given (without anypossibility to be changed), and any reduction in thechain slack represents not just a cost reduction, butalso (and most important) a strategic capability toanticipate the competitor in design, manufacturingand delivery of vehicles which are bettersynchronized with the evolution of the market. Sofar the difference between push and pullorganization was applied only to manufacturingstages, but with the strategic reorganization of thesupply chain the difference must be looked atwithin a wider context, which encompasses also thedesign and development stages both of new modelsand of components associated to them. In otherwords the system should evolve towards a supplychain which does not require only ex-antecoordination of decisions, which in turn is basedupon information managed by planning activities,but also a simultaneous coordination of operations,based upon execution information.

From hierarchical links to network links inthe whole supply chain

If we look at the relationship between a carmanufacturer and its suppliers from the standpointof information flow management, we could say thatuntil the 1980s such relationship was quite simple.To make a long story short, the OEM was the onewho led the whole project; parts and componentswere mainly designed and engineered by the carmanufacturer, while suppliers were asked tomanufacture them. In an oversimplifieddescription, one could say that such as relationshipconsisted in a few key elements :Ø The decision making process related to product

development – concept, design, engineering,product tests, changes – took place almostexclusively within the car manufacturer’sorganization; suppliers were more or less askedto manufacture some parts at some cost. Noneor very little interaction took place between thecar manufacturer and its supplier with respectto product development issues. Consequently,key decisions were mainly taken in an intra-firm process, that is: if it was necessary to takea difficult decision (e.g. to choose amongdifferent and/or incompatible solutions) theproblem could have been simply shifted to thehigher hierarchical level in the organization,

Actes du GERPISA n° 33 13

until someone took a decision. This is a formof coordination based upon ex ante planning,which has a key requirement : exclusively thefinal assembler must be fully aware of thewhole supply chain operations.

Ø In such condition the relationship with thesupplier is a “market-hierarchical relationship”in its proper sense: the car manufacturerspurchases a product (part or component) at aset price. Its overwhelming bargaining power isthe main element which causes the agreementson price of the supply to take place almost inthe form of a spot market auction; forsuppliers, profitability comes from theircapability to make the process as efficient aspossible;

Ø Consequently, the information involved in suchas customer-supplier relationship mainlyconsisted in one-way flows of technical details,prices, quantities, billing, terms of payment,etc.

Let’s now look at the actual supply chain as faras the customer-supplier relationship is concerned :as previously said, it is based upon an ex anteplanning mechanism, thus some interestingasymmetry takes place with respect to the elementsspecified above. First, the fundamental aspect ofcoordination based upon ex ante planning is thatany individual operator does not need informationon the whole chain of operations. Any chainoperator must know only start and end date for agiven activity, and must be concerned aboutprecisely meeting its specific deadline. Thisimplies a hierarchical management of information.But forms of simultaneous coordination on thewhole of operations, aimed at compressing chainslacks require on line access to the whole sequenceof operations, in order to carry out adaptations anytime in which downwards demand triggers a waveof change which involves the whole upwardoperation chain. In other words, this implies formsof network connections among operators.

The decision making processes related toproduct development involve both the carmanufacturer and first tier suppliers. According tothe continuous improvement both in product andprocess technology, nowadays the competenciesthat are necessary in order to manufacture acompetitive car encompass a wide range of fieldsof expertise. As a result, critical decisions might

often take place in an inter-firm process and thusan agreement among peers could be required.

For instance, managers of both the carmanufacturer and the supplier might be asked toshare a strategic belief as, for instance, an idea ofwhat will be positively evaluated from the market,or an opinion of what will be the technologicaltrend, and so on.

In such a condition it is absolutely notadvantageous to base the relationship with the first-tier supplier upon a mere spot-market agreement.Since the part supplied consists in a complexmodule which the first tier supplier develops forthat specific customer, the idiosyncrasy of therelationship increases in a significant way. Theprice-fixing process shifts from a bargainingpower-based process to a long-term / partnership-based one.

Since the car manufacturer needs a complexmodule to be developed and integrated in itsvehicle, the amount of information exchanged withthe first tier supplier is huge. The vehiclearchitecture definition is clearly still the coreactivity of the car manufacturer, but design andengineering of parts and modules deeply involvefirst tier suppliers. Consequently, the relationshipwill not only include the usual commercial terms(prices, quantities, billing, terms of payment), butwill become a mutual exchange of designs,projects, suggestions, changes and technical details.

If one considers that here the activities to besynchronized and integrated more closely are notjust those of the manufacturing process (where thetime frame of reference does not exceed a fewweeks, and individual events can be forecastedrather effectively), but those related to the wholedesign, production and delivery process, where thetime frame of reference amounts at least to a fewyears, and the variability game can apply to alargely more differentiated and complex level, it iseasy to understand that the information exchange tobe achieved in the move from the hierarchicalinformation scheme to the network informationscheme appears much more sophisticated than theone obtainable through the traditional informationtools. For example, if one considers a variation inthe levels of an information chain which is rigidlyhierarchical, according to the coordination modebased upon planning, the addition of new operatorsimplies the establishment of further stages, butfrom the information viewpoint complexity grows

Actes du GERPISA n° 3314

by an additional factor. If on the other hand newelements are added to a definite number of subjectswho are linked in a network, informationcomplexity due to the increase in the number ofpotential subjects involved grows by a multiplyingfactor. Here we are facing a transformation whichrequires mechanisms of information integrationwhich are largely more advanced and flexible.

Two steps are therefore needed in order toimplement such evolution.

First : a shift from the classic tools of datatransmission (sheets of paper, phone calls and soon) towards electronic communication tools andstandard protocols is needed, that is the adoption ofElectronic Data Interchange (EDI) systems, in theirbroad sense (standard protocols of data sending andreceiving). The first step is a move towardsinformation flow integration.

Second : the whole supply chain might gain inefficiency if the internal processes of each firm areplanned and scheduled on real-time requests.Significant shortening of cycle times might beobtained through the adoption of EnterpriseResource Planning (ERP) systems, intended as asystem (based on software packages) which issupposed to synchronize the resources required tooptimize manufacturing and delivery of products,considering constraints such as lack of materials orcapacity limits. This second step is a move towardsproduction process integration.

Integration is not just a technological eventThe fast development in Information and

Communication Technology (ICT) tools (e.g. EDI,ERP, communication networks as the internet, etc.)might give the idea that the integration processwhich car manufacturers aim at accomplishing caneasily rely upon technological means withextraordinary power, capable of generating in arelatively short time the transformations whichhave been pointed out. This would be misleading.As a matter of fact, the evolution of relationshipsamong car manufacturers and first tier suppliers isprimarily an answer to a change in the competitiveenvironment, although the trajectory of thereorganization has been deeply shaped by theopportunities offered by ICT.

No one could deny that the advantages derivingfrom the actual organization of automobile supplychains would not have been possible without thecontribution of ICT. Nonetheless, the impact of

ICT goes far beyond being just technical tollsmaking it easier, faster and cheaper the exchangeof information. Here we claim that the chance tofully exploit the opportunities introduced by ICT ismuch more an organizational problem than atechnological one. A vast and complexreorganization such as the one here mentioned cannever be accomplished through the mere adoptionof innovative tools, even though powerful andflexible. In fact, if one remembers the old saying“information is power”, then it comesstraightforward that the re-design of the supplychain, as based upon a different distribution ofinformation compared to the past, implies also arestructuring in bargaining power among thesubjects in the supply chain, and therefore in theircapacity to gain portions of the added valuegenerated by efficiency gains in the system. Notransformation can take place leaving previouspower relations unchanged, hence notransformation will then be accomplished if anydecisional center expects no gains from the change,and believes to have the strength to stay away fromthe transformation.

As a consequence, the process of developmentof ICT systems is not determined by their intrinsicprocess of technological innovation, but rather bythe evolution of the degree of convergence /divergence of interests borne by the participants ofthe chain. Only the understanding of new powerequilibria emerging in the chain show the actualforms of application and diffusion of newinformation1 tools.

THE FIELD RESEARCH

Questions and methodologyThe aim of the field study was to highlight

important issues related to supplier-customerrelationships whose transactions and productionprocess gets highly integrated through advancedICT systems. In our opinion, although there is acommon view on how ICT can improveproductivity and competitiveness through a closerconnection among contractors, little has been done

1 The manufacturing industry has already met a similar

occurrence with the introduction of flexible automation, whenit has been widely recognized that technology in itself does notcreate major efficiency or effectiveness if it is not linked to theorganizational and strategic design. See, for instance,Parthasarthy (1992), Boer and Krabbendam (1994).

Actes du GERPISA n° 33 15

to investigate some important issues that lie at thebasis of this study. In other words, the applicationsof technological opportunities are largelyunexplored. Main questions might be summarizedas follows.

First : the advantage which a single firm canobtain from such integration is to some extentinfluenced by the specific kind of relationshipsestablished among firms in the supply chain; on theother hand, ICT integration will probably affectexisting relations and the competitive position ofsupply chain contractors. The question is : howdoes ICT-based integration affect customer-supplier relationships? Is the relation changing in asignificant way? Which trajectory should weexpect?

Second: we have seen that the closer integrationof supply chain's contractors is a key trend. But it isarguable that such a process might take placewithout disadvantages for one or both contractors,so : which kinds of obstacles and problems occurin the ICT integration process?

In our view the answer to those questions mustbe sought with respect to the various kinds ofrelationships that are likely to take place among

supplier and customers; then focussing on thedifferent kind of possible information flows. Insuch view, the research steps have been thefollowing :Ø to identify a specific kind of relation to focus

the empirical analysis on;Ø to carry out a field study trying to provide an

answer to the above specified questions.Ø The empirical analysis included :Ø in-depth interviews devoted to paradigmatic

cases,Ø a questionnaire-based survey on a sample of

firms to attempt to shed light on the actualdegree of diffusion of ICT-based customersupplier relationships.

Background no. 1 : ICT relevance in smalland big problems

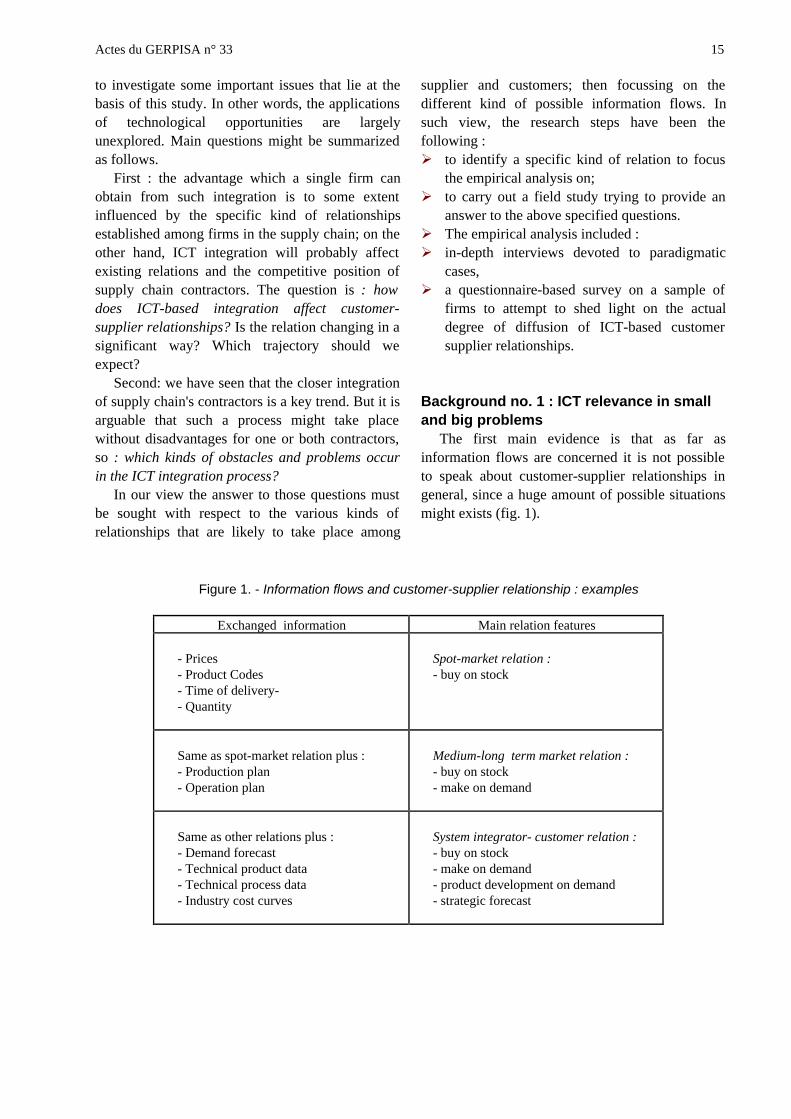

The first main evidence is that as far asinformation flows are concerned it is not possibleto speak about customer-supplier relationships ingeneral, since a huge amount of possible situationsmight exists (fig. 1).

Figure 1. - Information flows and customer-supplier relationship : examples

Exchanged information Main relation features

- Prices- Product Codes- Time of delivery-- Quantity

Spot-market relation :- buy on stock

Same as spot-market relation plus :- Production plan- Operation plan

Medium-long term market relation :- buy on stock- make on demand

Same as other relations plus :- Demand forecast- Technical product data- Technical process data- Industry cost curves

System integrator- customer relation :- buy on stock- make on demand- product development on demand- strategic forecast

Actes du GERPISA n° 3316

For this reason a 360-degree oriented researchwould require a vast synthesis effort to evaluateevery single possible situation. In this research wedecided to focus on the specific relationshipstaking place among a system-integrator supplierand its customer; such relationship is at the sametime the more complex and the one where thehigher integration is required, since it implies adeep sharing of information. Such a decision camefrom the obvious opinion that the more intense theobserved information flow would have been themore interesting situations we would meet.

Actually, this revealed to be only partially true;academic studies normally look at complexity (inits broad sense) as one of the problems that arebetter solved from ICT systems integration.Nevertheless, the interviews gave as a result thatthe obvious advantages regarding repetitive tasks(seemingly less important in the mind of a scholar)are evaluated with major attention by apractitioner’s mind.

An element that emerged during the in-depthinterview, as totally unexpected, is that one of thegreater sources of efficiency gains comes from therole of "error-killer" played by electronic datatransfer tools. For instance, in a traditional system asingle document (e.g.: a bill, an order and so on)requires to copy a series of codes from a piece ofpaper to another piece of paper; then it is sent byfax to another firm where it has to be copied again.The probability of an error might be high or low,depending on the kind of information exchanged,but it is quite common that if an error occurs then alot of time is wasted in trying to fix it. Thereforefirms give great importance to the capability ofEDI and other ICT technologies to eliminate errorsattributable to manual transfer and keying of data.

We then asked ourselves why such an importantelement is not given its legitimate importance;maybe the answer lies in the fact that frequently thecomparison among ICT and traditional technologyassumes an error-free environment. In other words,both traditional technology for supplier-customerinformation exchange and the ICT-based one areconsidered at their best. On the contrary, as far aspossible faults are concerned, they both featurepeculiar aspects. ICT will probably suffer from itsown possible faults, but for sure traditionaltechnologies rely upon human activity for datatransfer (and this causes problems) while ICT do

not. In an EDI integrated system data aretransferred without manual keying but with asimple "forward" input. In conclusion, the range ofpossible information exchange situations is broad :there might be structured circumstances as well asde-structured ones, complex and simple ones, andso on. We tried to investigate the more relevantquestions and therefore we have chosen to focus onthe relationship among first tier and/or system-integrator and assembler, but this does not meanthat more common situations have to be lessinteresting.

Background no. 2: ICT advantagesLeaving apart the unexpected relevance of

rudimentary ICT benefits, there is a shared viewabout the potential advantages deriving from theintegration of production processes through ICT.

Here we talk about Information andCommunication Technologies as including allthose tools (hardware and software) which arebased on electronic devices and which allow totransmit and process information such as data,sound, images, movies and so on. The "physical"elements include hardware, software andcommunication networks. Fields of application ofICT in supplier-customer relationship potentiallyfind no limits; just to give some examples :Ø Exchange of information and dataØ Sending and processing of messagesØ Preparing support to allow the diffusion of

informationØ Collecting informationØ Exchanging documentsØ Preparing supports to control and evaluate

firms activitiesØ Preparing supports to collect past informationØ Search for new business opportunities

Since customer/supplier relationships require agreat amount of work in several activities involvingseveral actors, ICT aims at providing a set of toolsthat help in each of these activities throughautomation of routinary/repetitive procedures andthrough easier and faster access to information.

Specifically, the main sources of benefits mightbe summarized as follows :

Actes du GERPISA n° 33 17

Ø Automation of procedures connected with in-bound and out-bound information flows.Electronic Data Interchange (EDI) shouldeliminate the manual handling of informationand forms concerning, for instance, deliverycalls, dispatch advice, invoice, confirmation ofreceipt and so on;

Ø Automation of procedures connected with theinner information flows related to orderfulfilment. The recent developments of the socalled Enterprise Resource Planning Systems(ERP) should give the opportunity of co-ordinating the information flows coming fromthe outside with the internal production system.For instance, the whole planning of orderfulfilment - from purchasing of parts andmaterial to delivering the order - might bemanaged, in theory, through an advanced ERPsystem, within the time constraints applying tothat specific order1.

Ø Electronic communication of data of variouskind : from draft and technical notes to vocalcomments. GroupWare allows teamwork atdistance, significantly improving the chance toimplement practices as co-design and co-engineering among contractors withoutincreasing transactional costs.

The potential improvement brought by suchpractices in supplier-customer relationships is oftentaken for granted. Actually, if it would be possibleto integrate at its best the available ICT, we couldobserve an immediate effect on the competitivenessof both contractors, due to :Ø Shortened time-to-market, due to faster and

safer exchange of data and its effect on workphases, like design, engineering, prototypingand development.

Ø Faster planning and production scheduling,Ø Work-in-progress reduction,Ø Reduction in idle times.Ø In reality, ICT advantages stands in the

overcoming of spatial distances and in thesubstitution of manual operations withautomated ones; for instance:

Ø Videoconferencing substitutes meetingsØ EDI substitutes manual keying of orders,

billings and so on

1 The CEO of one of the company analyzed in our research

calculates in 56 hour of one-man work each week the totalamount of time-saving related to the use of EDI interfacedwith ERP supply management.

Ø ERP substitutes manual operational planningØ MRP substitutes manual calculation of needs,

re-ordering, scheduling and so on.Ø CAD substitutes manual design and

calculations of componentsØ etc.

First results from the interviewsSix supplier firms have been selected for in-

depth visits and interviews :Ø Two OEM first-tier auto-industry supplier;Ø One auto-industry first tier supplier;Ø One producer of ERP systems;Ø One OEM first-tier mechanical firm producing

components for agriculture;Ø One firm LAN-WAN administrator and

software producer.

All the manufacturing companies interviewedhave adopted EDI and MRP and/or ERP systems.Except in the case of the ERP producer and of theagricultural-machine producer, the subjectsinterviewed were the CEO together with anotherexecutive and with personnel both frommanufacturing and from the technical staff. In thecase of the ERP producer the person interviewedwas the product-manager responsible for specificsoftware, while for the agriculture industry firm theinterviewed was a production engineer responsiblefor inventory management.

The interviews have been carried out betweenJune 1999 and March 2000.

The main results can be summarized in just afew words : problems are not related to technicalissues but to the management of productionprocesses and to the management of relations withcustomers.

ICT-based integration and firm organization

According to almost all the subjects interviewedICT improves profitability but advantages areanyway connected to the internal organization ofproduction. ICT improves but does not overcomethe problem connected to the upward design of theproduction flow.

For instance, the implementation of advancedsystems like ERP systems requires responsibilityand decision processes within the firm to be welldefined and efficient. In other words, it must beclear:

Actes du GERPISA n° 3318

Ø who is responsible for each activity within eachprocess,

Ø which procedure has to be activated for eachsituation.

Actually we cannot agree with the commonstatement that "ERP systems allow the re-designand improvement of organizational structure of afirm" [Cerruti, 1999]. On the contrary, a re-designis likely to be needed for an ERP system to workproperly. According to the product manager of theERP producer interviewed, when the managementof a medium-sized firm decides to invest inadvanced planning systems and ICT integration,they roughly know what they are buying. Veryoften it is up to the ERP seller to suggest theintroduction of workflow management systemstogether with a re-design of tasks andresponsibilities.

One of the OEM suppliers declared that thehuge problems encountered in adopting SAP-R3derived from difficulties in interfacing personneldedicated to managing the information system andthe rest of the firm organization. Just consideringthe bare money implications, it resulted that thestarting proposal of investment was about Euro 2.5million, but the period of set-up has been longerthan expected and total investment increased up toEuro 15 million over six years1.ICT and relationships among firms

In one of the two carmaker's OEM suppliersinterviewed (working mainly on batch productions)the whole process of order fulfillment is managedthrough an EDI-MRP system; the implementationof ICT tools has been required by carmanufacturers with whom the firm is operating.

Thanks to the EDI connection the firm’scustomers (carmakers) can send their orders almostcontinuously2. Together with one of its customers,individually, the supplier has developed a systemthat allows the carmaker to “see” the inventory of

1 In our view there is a significant difference between this

case and other (even worse) cases that Davenport calls "horrorstories about failed or out-of-control projects" [Davenport,1998]. A certain amount of problems and failures might beconsidered physiological among first-adopters, but theinterviewed company started to adopt advanced planningsystems after several years of experience in the field.

2 Company CEO said that they were just testing duringthose days a 24-hours connection for continuos ordering.

the firm and to set the orders and the productionschedule according to what is in stock.3.

All other carmakers do not know, in fact, thelevel of inventory for the specific item they need,nor if and how the production capacity of thesupplier is allocated at that time. Since allcarmakers ask the supplier to fulfil just in timedelivery with intense scheduling (from 1 to 5deliveries a week), as a result the company has toface a trade-off between :Ø keeping a slack of production capacity to be

sure that it can fulfil the order on time;Ø keeping a higher level of inventory than it

would be necessary.

Anyway, such a solution has been implementedunder the condition of a long-term, almostpartenarial, relation among the supplier and thecustomer.

On the other hand, out of such assumption the“viewable inventory” has been labeled as“dangerous” from another executive interviewed.According to the engineer from the OEMagricultural machine producer (batch production),to let the customers know the internal plan ofproduction and operational scheduling might createthe conditions for renegotiations of terms (pricesand times) for each batch. Such a situation exist, inhis opinion, since very often in that specificindustry the customer has a bargaining powertowards first-tier suppliers which is greater than inthe car industry. As a consequence, finalassemblers seldom seek a long-term partnershipagreement and an opportunistic attitude is thereforecommon from both parts. For instance, a problemtakes place whenever parts or components in stockare not enough to fulfil DELJIT-request from twodifferent customers4; in this case it is necessary toestablish a priority or, possibly, to find out acompromise to displease none of the customers.

3 This might be a nice example of those kind of benefits

from ICT integration that make Dudenhöffer [2000] predictthat the carmaker in the future will have online access up totier 7 supplier with systems to systems data exchange.

4 DELJIT is an EDI-ODETTE acronym standing forDelivery Just In Time; it indicates the request ofimplementation of a previous confirmed order. It can be of atwofold kind: 1. pure Just in Time, which allows the supplierto adjust the delivery normally within 24 or 48 hours; 2. Pick-Up-Sheet, not adjustable, announce that the carrier is alreadyon the way to pick up the items. The situation described aboveis related to the first kind of order.

Actes du GERPISA n° 33 19

So, it should be clear that such problems asthose described above do not come from ICT, ofcourse, but from the balancing of bargaining powerbetween the supplier and its customers, togetherwith the intent of both contractors to exploit ICTadvantages. This bring to a twofold consideration :Ø From the supplier's point of view ICT have

created a situation in which the performancerequired to the supplier is much higher1. Forinstance, the OEM supplier shifted from onedelivery every 15 days to one to five deliveriesa week. At the moment of the interview thelead time was supposed to decrease from 16days down to 48 hours (make and delivery) and24 hours (just delivery).

Ø From both the carmakers’ and supplier’s pointof view, relationships became much moreidiosyncratic, since sunk costs take placeaccording to: a) the nature of ICT tools andproduction capacity2, b) high importance ofsupply for the car manufacturer and the lack ofpossibility of replacing it in short times.Therefore, if it is reasonable to think thatadvantages of ICT-based integration areconnected to the stability of relationships in thesupply chain, a question is : might such a deepintegration (paradoxically) drive towards a lessflexible relationship?

First results from the questionnaire surveyThe other part of the empirical research aimed

at evaluating the actual diffusion of ICT system insupplier-customer relations. A certain number offirms have been chosen for a questionnaire survey;selected firms were first-tier manufacturersuppliers. The survey is still going on and at themoment 31 questionnaires have been collected.

The questionnaire is made of 70 questions andtherefore it requires a considerable amount of timeto be filled. It is also evident that a great amount ofdifferent information is given; anyway, since theresearch is still ongoing here will be presented onlya first brief evaluation of what we considered to be

1 The bargaining power is, of course, one of the main

determinants on carmakers relation strategies towards supplier,together with the criticality of purchased items. See, forinstance, Kraljic [1983].

2 As we'll see in the next paragraph, the questionnairesurvey show that almost 50% of firms decide for their ICTinvestments considering ICT equipment of their customer and70% considering customer's ICT equipment.

the most relevant signals. The questionnaire isdivided into five sections :Ø Section 1 and 2 aim at collecting general

company information. Firms are anywaynameless; we decided to allow firms to remainanonymous, since we think that this wouldincrease the redemption level.

Ø Section 3 is devoted to ICT availability andinvestments.

Ø Section 4 regards the relationships with firm'ssuppliers, that in fact are sub-suppliers sincethe sample is itself made of first-tier suppliers.

Ø Section 5 regards relationships with customers;these could be final assemblers but also othersuppliers.

In table 1 the main features of the sample arepresented; later on, the main results concerningsection from three to five will be shown.

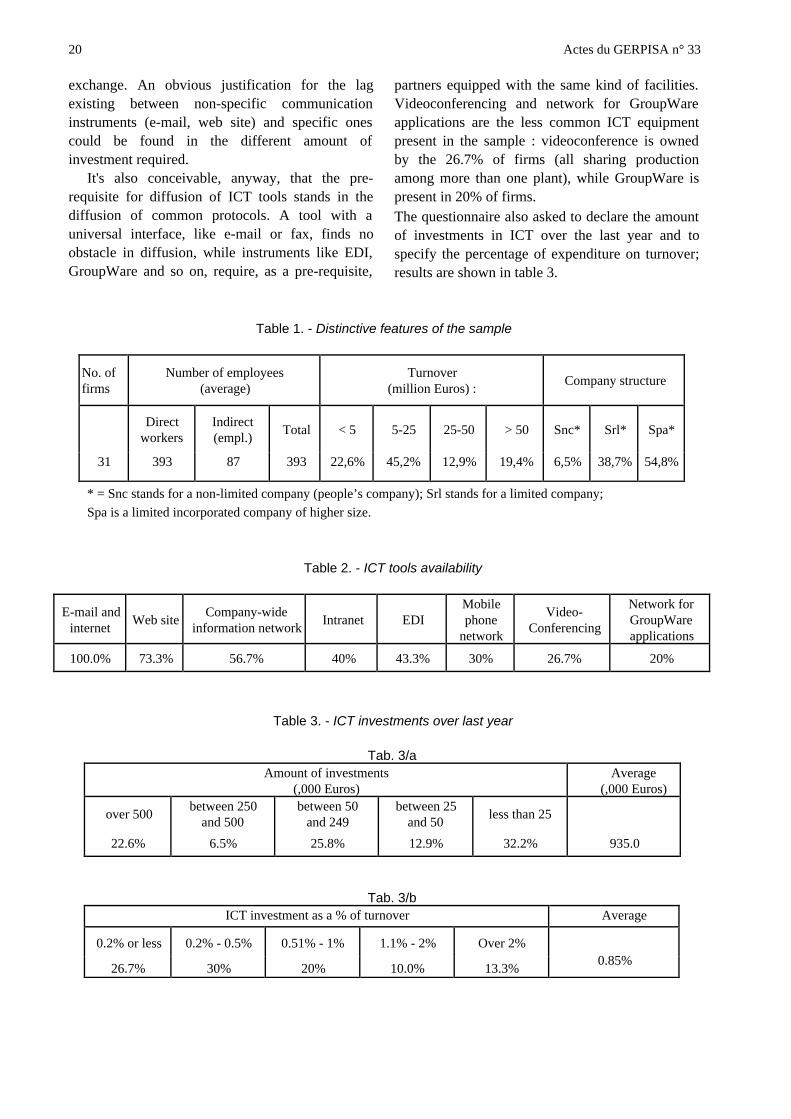

As a whole the sample is mainly made of smallsized firms3: the average number of employees is393 and less than 20% of the sample has a turnoverwhich overcome 50 million Euros. Almost 13% ofthe sample (that is: four firms out of thirty-one)have more than 500 employees; for these firmsturnover is greater than 100 million Euros. On theother hand, 45.1% of the sample has less than 100employees.

ICT Investments

The third section of the questionnaire lookedupon investments in ICT.

As a first we asked them to check boxesaccording to the ICT facility possessed. Firstresults evidence a widespread use of ICT as ageneric communication tool, but a much lesscommon use of ICT tools devoted to specific firm-network relations. As one can see (table 2) all theinterviewed firms own e-mail and internetconnection4 and more than 70% own a web site.On the other hand, only 57% of firms own acompany-network, that is an instrumentpresumably devoted to internal operationsmanagement. Moreover, only 40% of the sampleuse EDI and 43% use intranet connections, bothICT tools specifically fit for inter-firm information

3 Accordingly with EU commonly used classifications, a

firm is small-sized when has less than 500 employees.4 In the questionnaire e-mail and internet have been

presented with different boxes, although nowadays providersalways offers both internet and e-mail together.

Actes du GERPISA n° 3320

exchange. An obvious justification for the lagexisting between non-specific communicationinstruments (e-mail, web site) and specific onescould be found in the different amount ofinvestment required.

It's also conceivable, anyway, that the pre-requisite for diffusion of ICT tools stands in thediffusion of common protocols. A tool with auniversal interface, like e-mail or fax, finds noobstacle in diffusion, while instruments like EDI,GroupWare and so on, require, as a pre-requisite,

partners equipped with the same kind of facilities.Videoconferencing and network for GroupWareapplications are the less common ICT equipmentpresent in the sample : videoconference is ownedby the 26.7% of firms (all sharing productionamong more than one plant), while GroupWare ispresent in 20% of firms.The questionnaire also asked to declare the amountof investments in ICT over the last year and tospecify the percentage of expenditure on turnover;results are shown in table 3.

Table 1. - Distinctive features of the sample

No. offirms

Number of employees(average)

Turnover(million Euros) :

Company structure

Directworkers

Indirect(empl.)

Total < 5 5-25 25-50 > 50 Snc* Srl* Spa*

31 393 87 393 22,6% 45,2% 12,9% 19,4% 6,5% 38,7% 54,8%

* = Snc stands for a non-limited company (people’s company); Srl stands for a limited company;

Spa is a limited incorporated company of higher size.

Table 2. - ICT tools availability

E-mail andinternet

Web siteCompany-wide

information networkIntranet EDI

Mobilephone

network

Video-Conferencing

Network forGroupWareapplications

100.0% 73.3% 56.7% 40% 43.3% 30% 26.7% 20%

Table 3. - ICT investments over last year

Tab. 3/aAmount of investments

(,000 Euros)Average

(,000 Euros)

over 500between 250

and 500between 50

and 249between 25

and 50less than 25

22.6% 6.5% 25.8% 12.9% 32.2% 935.0

Tab. 3/bICT investment as a % of turnover Average

0.2% or less 0.2% - 0.5% 0.51% - 1% 1.1% - 2% Over 2%

26.7% 30% 20% 10.0% 13.3%0.85%

Actes du GERPISA n° 33 21

Table 4. - ICT investments expected within the next 6 months

ManufacturingManagement andAdministration

Internet Network Connections

Hardware software hardware softwareinternetpresence

updating /developing

existing ones

Development ofnew ones

61.3% 51.6% 48.4% 41.9% 58.1% 45.2% 29%

The high value of the average investment(935,000 Euros) comes from relatively few bigfirms that declared to have heavily invested on ICTover last years. In fact, the greater 13% ICT-investor of the sample account for the 83.7% of thetotal investment; this means that the first fourinvestors (out of thirty-one) have spent 25 millionEuros on a total investment of 29 million Euros.Anyway, about 55% of the firms in our samplehave spent more than the considerable amount of50,000 Euros in ICT (tab 3/a). The effort towardsimprovement is also testified from the weight ofinvestments on turnover: on an average ICTabsorbs 0.85% of turnover. Moreover, almost onequarter of the sample (23.3%) has invested morethan 1% of turnover in ICT and the 13.3% haveinvested more than 2%. (tab 3/b)

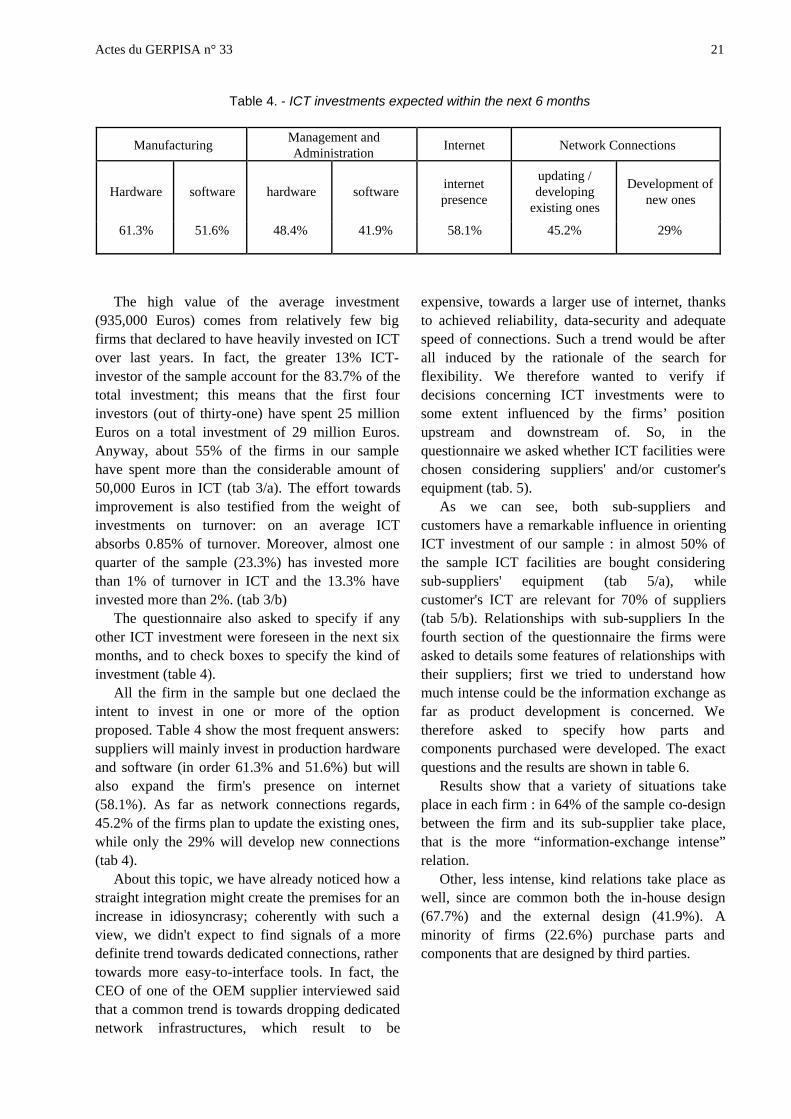

The questionnaire also asked to specify if anyother ICT investment were foreseen in the next sixmonths, and to check boxes to specify the kind ofinvestment (table 4).

All the firm in the sample but one declaed theintent to invest in one or more of the optionproposed. Table 4 show the most frequent answers:suppliers will mainly invest in production hardwareand software (in order 61.3% and 51.6%) but willalso expand the firm's presence on internet(58.1%). As far as network connections regards,45.2% of the firms plan to update the existing ones,while only the 29% will develop new connections(tab 4).

About this topic, we have already noticed how astraight integration might create the premises for anincrease in idiosyncrasy; coherently with such aview, we didn't expect to find signals of a moredefinite trend towards dedicated connections, rathertowards more easy-to-interface tools. In fact, theCEO of one of the OEM supplier interviewed saidthat a common trend is towards dropping dedicatednetwork infrastructures, which result to be

expensive, towards a larger use of internet, thanksto achieved reliability, data-security and adequatespeed of connections. Such a trend would be afterall induced by the rationale of the search forflexibility. We therefore wanted to verify ifdecisions concerning ICT investments were tosome extent influenced by the firms’ positionupstream and downstream of. So, in thequestionnaire we asked whether ICT facilities werechosen considering suppliers' and/or customer'sequipment (tab. 5).

As we can see, both sub-suppliers andcustomers have a remarkable influence in orientingICT investment of our sample : in almost 50% ofthe sample ICT facilities are bought consideringsub-suppliers' equipment (tab 5/a), whilecustomer's ICT are relevant for 70% of suppliers(tab 5/b). Relationships with sub-suppliers In thefourth section of the questionnaire the firms wereasked to details some features of relationships withtheir suppliers; first we tried to understand howmuch intense could be the information exchange asfar as product development is concerned. Wetherefore asked to specify how parts andcomponents purchased were developed. The exactquestions and the results are shown in table 6.

Results show that a variety of situations takeplace in each firm : in 64% of the sample co-designbetween the firm and its sub-supplier take place,that is the more “information-exchange intense”relation.

Other, less intense, kind relations take place aswell, since are common both the in-house design(67.7%) and the external design (41.9%). Aminority of firms (22.6%) purchase parts andcomponents that are designed by third parties.

Actes du GERPISA n° 3322

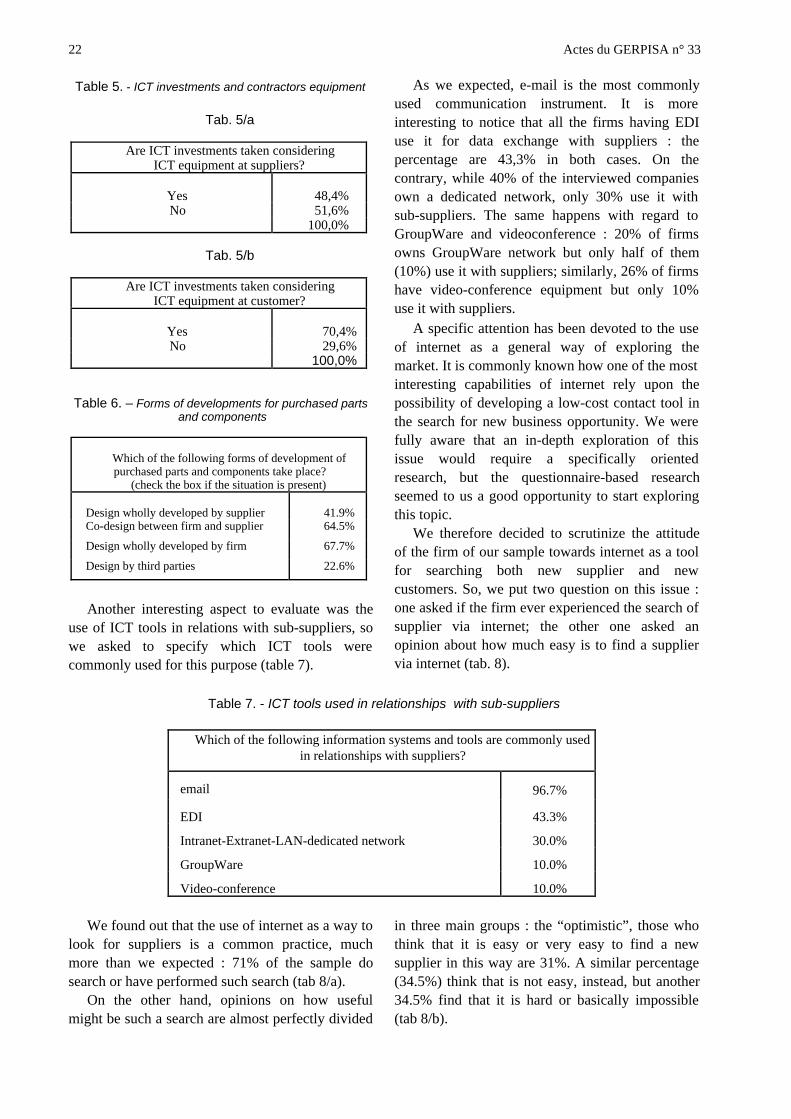

Table 5. - ICT investments and contractors equipment

Tab. 5/a

Are ICT investments taken consideringICT equipment at suppliers?

Yes 48,4%No 51,6%

100,0%

Tab. 5/b

Are ICT investments taken consideringICT equipment at customer?

Yes 70,4%No 29,6%

100,0%

Table 6. – Forms of developments for purchased parts and components

Which of the following forms of development ofpurchased parts and components take place?

(check the box if the situation is present)

Design wholly developed by supplier 41.9%Co-design between firm and supplier 64.5%

Design wholly developed by firm 67.7%

Design by third parties 22.6%

Another interesting aspect to evaluate was theuse of ICT tools in relations with sub-suppliers, sowe asked to specify which ICT tools werecommonly used for this purpose (table 7).

As we expected, e-mail is the most commonlyused communication instrument. It is moreinteresting to notice that all the firms having EDIuse it for data exchange with suppliers : thepercentage are 43,3% in both cases. On thecontrary, while 40% of the interviewed companiesown a dedicated network, only 30% use it withsub-suppliers. The same happens with regard toGroupWare and videoconference : 20% of firmsowns GroupWare network but only half of them(10%) use it with suppliers; similarly, 26% of firmshave video-conference equipment but only 10%use it with suppliers.

A specific attention has been devoted to the useof internet as a general way of exploring themarket. It is commonly known how one of the mostinteresting capabilities of internet rely upon thepossibility of developing a low-cost contact tool inthe search for new business opportunity. We werefully aware that an in-depth exploration of thisissue would require a specifically orientedresearch, but the questionnaire-based researchseemed to us a good opportunity to start exploringthis topic.

We therefore decided to scrutinize the attitudeof the firm of our sample towards internet as a toolfor searching both new supplier and newcustomers. So, we put two question on this issue :one asked if the firm ever experienced the search ofsupplier via internet; the other one asked anopinion about how much easy is to find a suppliervia internet (tab. 8).

Table 7. - ICT tools used in relationships with sub-suppliers

Which of the following information systems and tools are commonly usedin relationships with suppliers?

email 96.7%

EDI 43.3%

Intranet-Extranet-LAN-dedicated network 30.0%

GroupWare 10.0%

Video-conference 10.0%

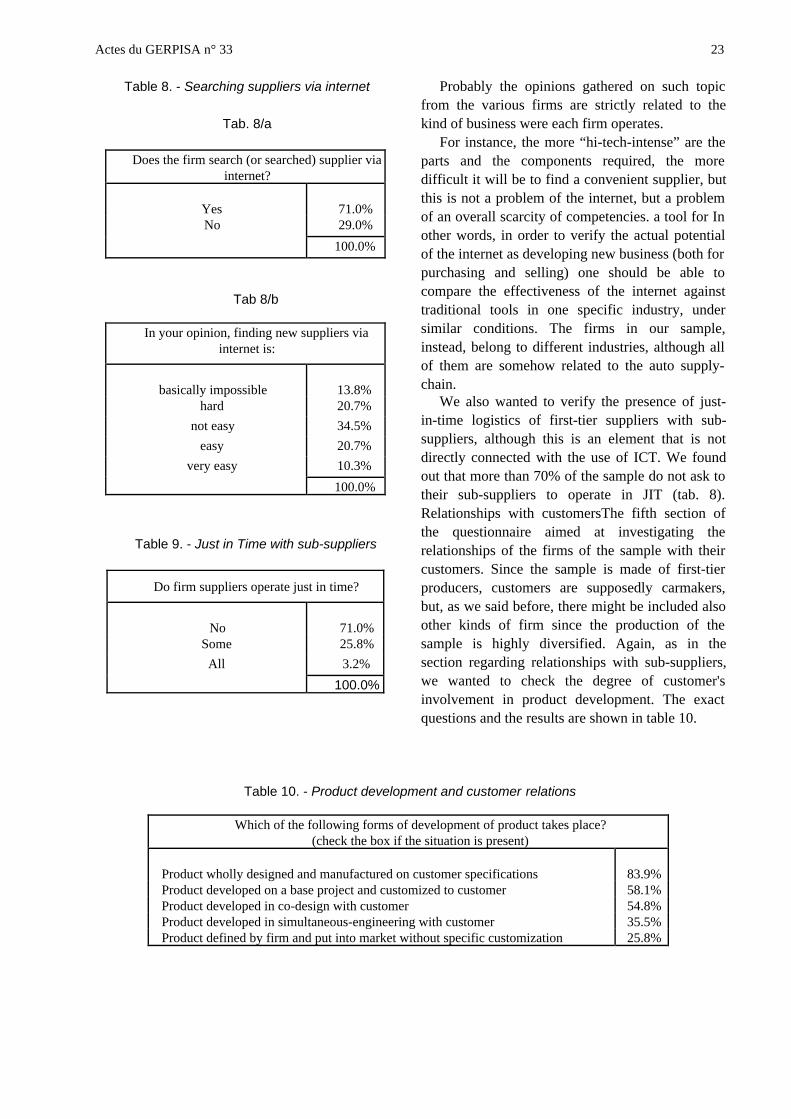

We found out that the use of internet as a way tolook for suppliers is a common practice, muchmore than we expected : 71% of the sample dosearch or have performed such search (tab 8/a).

On the other hand, opinions on how usefulmight be such a search are almost perfectly divided

in three main groups : the “optimistic”, those whothink that it is easy or very easy to find a newsupplier in this way are 31%. A similar percentage(34.5%) think that is not easy, instead, but another34.5% find that it is hard or basically impossible(tab 8/b).

Actes du GERPISA n° 33 23

Table 8. - Searching suppliers via internet

Tab. 8/a

Does the firm search (or searched) supplier viainternet?

Yes 71.0%No 29.0%

100.0%

Tab 8/b

In your opinion, finding new suppliers viainternet is:

basically impossible 13.8%hard 20.7%

not easy 34.5%

easy 20.7%

very easy 10.3%

100.0%

Table 9. - Just in Time with sub-suppliers

Do firm suppliers operate just in time?

No 71.0%Some 25.8%

All 3.2%

100.0%

Probably the opinions gathered on such topicfrom the various firms are strictly related to thekind of business were each firm operates.

For instance, the more “hi-tech-intense” are theparts and the components required, the moredifficult it will be to find a convenient supplier, butthis is not a problem of the internet, but a problemof an overall scarcity of competencies. a tool for Inother words, in order to verify the actual potentialof the internet as developing new business (both forpurchasing and selling) one should be able tocompare the effectiveness of the internet againsttraditional tools in one specific industry, undersimilar conditions. The firms in our sample,instead, belong to different industries, although allof them are somehow related to the auto supply-chain.

We also wanted to verify the presence of just-in-time logistics of first-tier suppliers with sub-suppliers, although this is an element that is notdirectly connected with the use of ICT. We foundout that more than 70% of the sample do not ask totheir sub-suppliers to operate in JIT (tab. 8).Relationships with customersThe fifth section ofthe questionnaire aimed at investigating therelationships of the firms of the sample with theircustomers. Since the sample is made of first-tierproducers, customers are supposedly carmakers,but, as we said before, there might be included alsoother kinds of firm since the production of thesample is highly diversified. Again, as in thesection regarding relationships with sub-suppliers,we wanted to check the degree of customer'sinvolvement in product development. The exactquestions and the results are shown in table 10.

Table 10. - Product development and customer relations

Which of the following forms of development of product takes place?(check the box if the situation is present)

Product wholly designed and manufactured on customer specifications 83.9%Product developed on a base project and customized to customer 58.1%Product developed in co-design with customer 54.8%Product developed in simultaneous-engineering with customer 35.5%Product defined by firm and put into market without specific customization 25.8%

Actes du GERPISA n° 3324

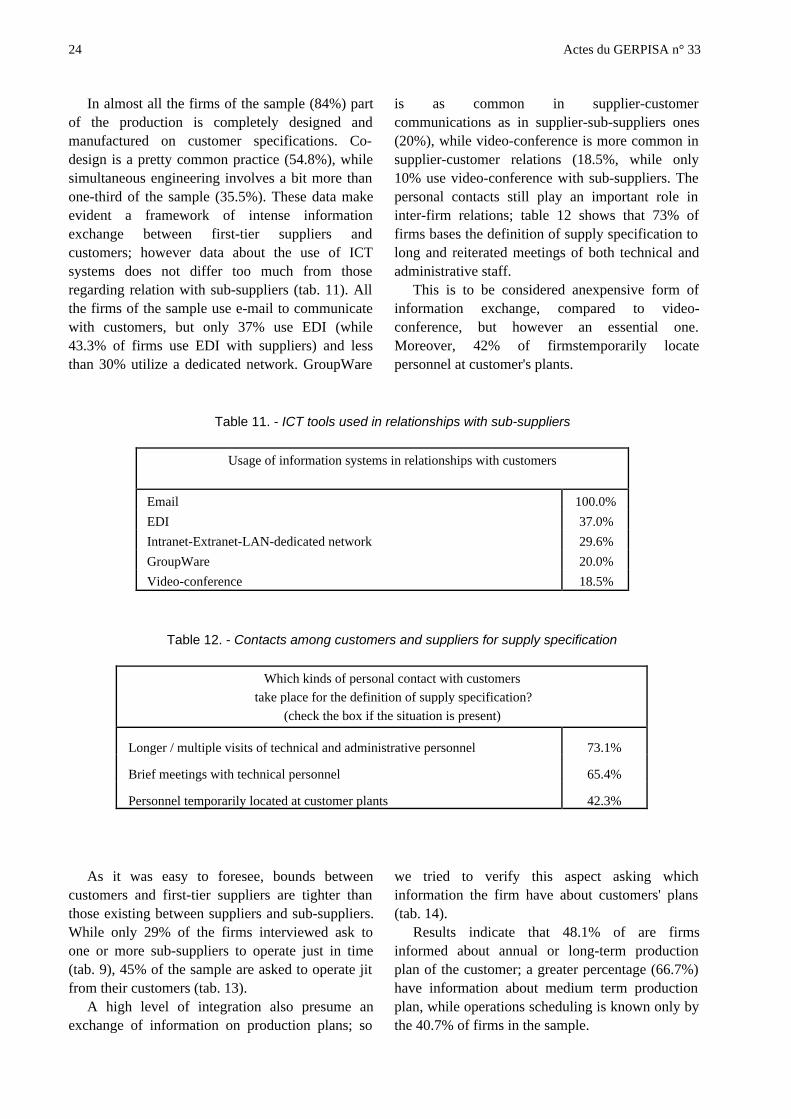

In almost all the firms of the sample (84%) partof the production is completely designed andmanufactured on customer specifications. Co-design is a pretty common practice (54.8%), whilesimultaneous engineering involves a bit more thanone-third of the sample (35.5%). These data makeevident a framework of intense informationexchange between first-tier suppliers andcustomers; however data about the use of ICTsystems does not differ too much from thoseregarding relation with sub-suppliers (tab. 11). Allthe firms of the sample use e-mail to communicatewith customers, but only 37% use EDI (while43.3% of firms use EDI with suppliers) and lessthan 30% utilize a dedicated network. GroupWare

is as common in supplier-customercommunications as in supplier-sub-suppliers ones(20%), while video-conference is more common insupplier-customer relations (18.5%, while only10% use video-conference with sub-suppliers. Thepersonal contacts still play an important role ininter-firm relations; table 12 shows that 73% offirms bases the definition of supply specification tolong and reiterated meetings of both technical andadministrative staff.

This is to be considered anexpensive form ofinformation exchange, compared to video-conference, but however an essential one.Moreover, 42% of firmstemporarily locatepersonnel at customer's plants.

Table 11. - ICT tools used in relationships with sub-suppliers

Usage of information systems in relationships with customers

Email 100.0%

EDI 37.0%

Intranet-Extranet-LAN-dedicated network 29.6%

GroupWare 20.0%

Video-conference 18.5%

Table 12. - Contacts among customers and suppliers for supply specification

Which kinds of personal contact with customers

take place for the definition of supply specification?

(check the box if the situation is present)

Longer / multiple visits of technical and administrative personnel 73.1%

Brief meetings with technical personnel 65.4%

Personnel temporarily located at customer plants 42.3%

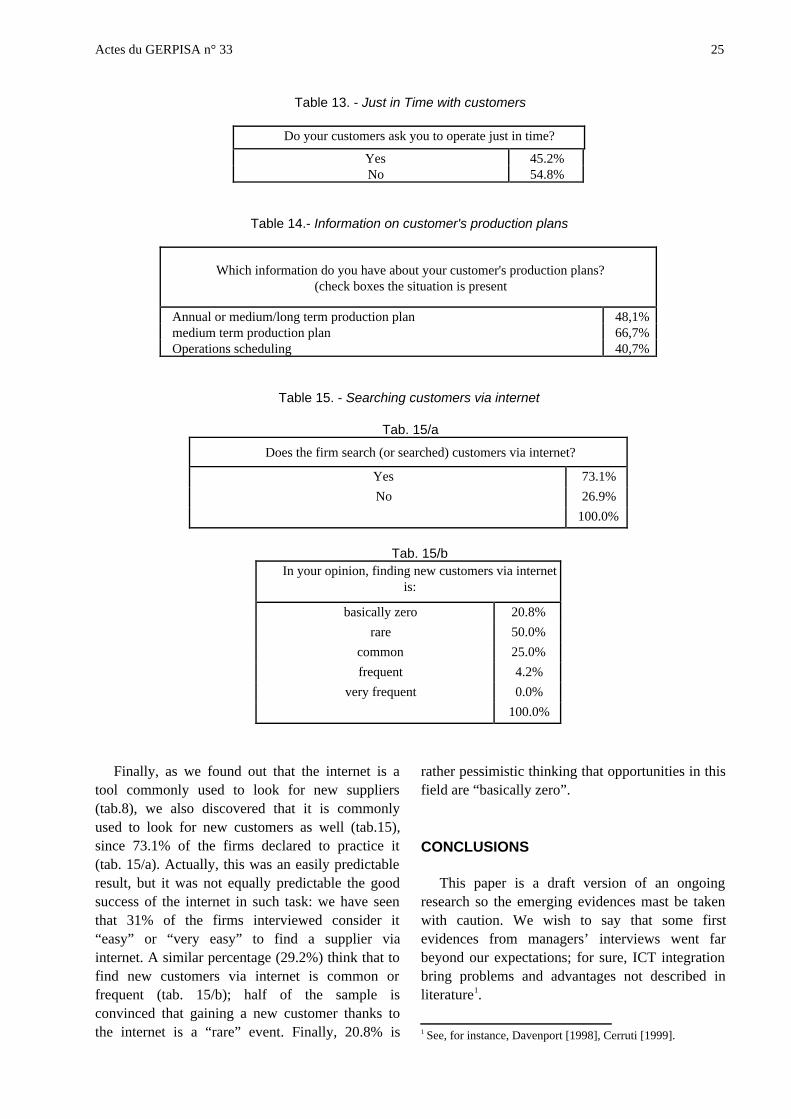

As it was easy to foresee, bounds betweencustomers and first-tier suppliers are tighter thanthose existing between suppliers and sub-suppliers.While only 29% of the firms interviewed ask toone or more sub-suppliers to operate just in time(tab. 9), 45% of the sample are asked to operate jitfrom their customers (tab. 13).

A high level of integration also presume anexchange of information on production plans; so

we tried to verify this aspect asking whichinformation the firm have about customers' plans(tab. 14).

Results indicate that 48.1% of are firmsinformed about annual or long-term productionplan of the customer; a greater percentage (66.7%)have information about medium term productionplan, while operations scheduling is known only bythe 40.7% of firms in the sample.

Actes du GERPISA n° 33 25

Table 13. - Just in Time with customers

Do your customers ask you to operate just in time?

Yes 45.2%No 54.8%

Table 14.- Information on customer's production plans

Which information do you have about your customer's production plans?(check boxes the situation is present

Annual or medium/long term production plan 48,1%medium term production plan 66,7%Operations scheduling 40,7%

Table 15. - Searching customers via internet

Tab. 15/a

Does the firm search (or searched) customers via internet?

Yes 73.1%

No 26.9%

100.0%

Tab. 15/bIn your opinion, finding new customers via internet

is:

basically zero 20.8%

rare 50.0%

common 25.0%

frequent 4.2%

very frequent 0.0%

100.0%

Finally, as we found out that the internet is atool commonly used to look for new suppliers(tab.8), we also discovered that it is commonlyused to look for new customers as well (tab.15),since 73.1% of the firms declared to practice it(tab. 15/a). Actually, this was an easily predictableresult, but it was not equally predictable the goodsuccess of the internet in such task: we have seenthat 31% of the firms interviewed consider it“easy” or “very easy” to find a supplier viainternet. A similar percentage (29.2%) think that tofind new customers via internet is common orfrequent (tab. 15/b); half of the sample isconvinced that gaining a new customer thanks tothe internet is a “rare” event. Finally, 20.8% is

rather pessimistic thinking that opportunities in thisfield are “basically zero”.

CONCLUSIONS

This paper is a draft version of an ongoingresearch so the emerging evidences mast be takenwith caution. We wish to say that some firstevidences from managers’ interviews went farbeyond our expectations; for sure, ICT integrationbring problems and advantages not described inliterature1.

1 See, for instance, Davenport [1998], Cerruti [1999].

Actes du GERPISA n° 3326

Making a long story short, we think that threemain aspects have emerged.Ø The possibility to reduce the number of errors

in routinary operations is one of the ICTbenefit executives seem to appreciate more. Onthe one hand it is an objective that could beeasily reached thanks to a relatively simpletechnology, but on the other hand it suggests aconstraint to be kept in mind when thinkingabout developing ICT solutions : does it reduceerrors or can it cause new ones? Does itsimplify work-life (reduce number ofoperations to be carried out, make decisionseasier) or does it make it more complicate?

Ø It might be useful to recall the experience thatthe car industry has undergone when flexibleautomation was first introduced1. Although thegreat benefits of automation were definitivelyvisible, obtaining those benefits was not soinstantaneous as it was first believed. Thetechnological questions which emerged causedconcern on organizational problems related tothe production process as a whole. In short, thelesson was that to insert in a complex process amachine that use and manipulate information ishardly a “neutral” or “technological”improvement as it could be to use an electric-power screwdriver instead than a manual one.

Ø ICT integration goes even beyond, presentingproblems which are much more complex thanthose introduced at that time by flexibleautomation, since it involves both the internalorganizational processes and the relations withother firms.

Ø It's necessary not to underestimate theproblems connected to the existingorganizational process. An example : if anirregularity occurs in a purchase order comingfrom EDI into ERP, the system automaticallyaddresses a message to a pre-definedorganizational position responsible for thatspecific task. Some little irregularitiesfrequently occur in day-to-day activities of thefirm. Problems might be due, for instance, to alittle deviation from contractually pre-definedterms (e.g.: that specific customer by contractis supposed to have paid the last batch beforeordering a new one, but he has made a neworder although he didn't pay last one yet). In a

1 In Italy an explanatory case is the Cassino experience[Volpato, 1996].

traditional planning process the person whoreceives that order will look for someone whotakes the responsibility to say “go ahead”, orrather “let me check the situation with Mr. X”.An ERP can do the same thing in a faster andmore effective way : using the internal net, theERP can automatically inform the responsiblevia computer, sending him a message andletting him retrieving all the documents relatedto the situation (contracts, addresses, telephonenumbers and so on). The problem is that it isnecessary a pre-defined hierarchy of positionsresponsible for each situation that mighthappen. In a traditional organization thishappen informally (a secretary goes aroundsearching for the boss); in a ERP-basedorganization one must be sure that someonewill guard that position. In short, a completeworkflow of internal processes must bedefined; this might not be an easy task.

Ø It might be necessary to drop severalestablished notions about the firm’scompetitiveness and to shift towards a visionregarding integrated-process competitiveness.In our opinion a single firm would hardly gethigher competitiveness merely from ICT tools,since ICT-based process innovation in a firmtakes place mainly in the form of externalpurchase of instruments (hardware andsoftware), while competitive advantages aresupposed to be distinct and enduring. Neitherof such features seems to apply to ICT tools inthemselves; the true source of competitiveadvantage stands in the net of internal andexternal relationships that are improved byICT. For this reason, we should expect a striveof both carmakers and first-tier supplierstowards the fastening of reciprocal relations.

Ø In a sentence, we could say that increasingintegration seems to originate increasingidiosyncrasy, mainly because in order the fullyexploited, the quite evident benefits ofinterconnections among their own productionprocesses need a relatively stable environmentand the absence of opportunistic behavior fromboth sides.

Giuseppe Volpato - Andrea Stocchetti

Universita Ca’ Foscari

Venezia – Italie

Actes du GERPISA n° 33 27

BIBLIOGRAPHY

Boer H, Krabbendam K [1992], Organizing for

manufacturing Innovation : The Case of Flexible

Manufacturing Systems, in International Journal of

Operations & Production Management, (12), 7/8, 41-

56.

Camuffo A., Volpato G. [1997], Nuove forme di

integrazione operativa : il caso della componentistica

automobilistica, F.Angeli, Milano.

Camuffo A., Volpato G. [1999], Project 178 in the Form

of an International Double Network : Internal

Exchange and Global Sourcing, IMVP Annual

Forum, MIT, Boston, 6-7 October.

Cerruti C. [1999] L'introduzione di sistemi informativi

avanzati nella media impresa : prime evidenze su

potenzialità e limiti dei sistemi ERP (The

introduction of advanced ICT systems in medium-

sized enterprise: first indications on ERP value and

limits), AIDEA Workshop 1999 - Parma (Italy) 29-

30 Oct.

Clark J.P., Veloso F. [2000], The Vertical Integration of

Component Supplier Chains and Its Impact on Multi-

tier Supplier Relations, Draft thematic document

prepared for the international workshop: The

Automotive Industry: Component Suppliers; current

and Prospective Regulatory Approaches, Porto,

Portugal, 4-5 May 2000.

de Banville E., Chanaron J-J. [1999], Inter-firm

Relationships and Industrial Models, in Lung Y.,

Chanaron J-J., Fujimoto T., Raff D. (eds.), Coping

with Variety, Ashgate, Aldershot.

Davenport T [1998] Putting the Enterprise into the

Enterprise System, in Harvard business Review, jul-

aug.

Dudenhöffer F. [2000] E-Commerce and Component

Supplier, Preparatory thematic document at the EU

Automotive Industry Workshop "The automotive

industry : component suppliers; current and

prospective regulatory approaches"- April 2000,

Lisbon

Freyssenet M., Mair A., Shimizu K., Volpato G. (eds.),

[1998], One Best Way? – Trajectories and Industrial

Models of the World’s Automobile Producers,

Oxford University Press, Oxford.

Kraljic P. [1983], Purchasing Must Become Supply

Management, in Harvard Business Review, sep.-oct.,

109-117.

Lecler Y., Perrin J., Villeval M-C. [1999], Concurrent

Engineering and Institutional Learning : A

Comparison of French and Japanese Component

Suppliers, in Lung Y., Chanaron J-J., Fujimoto T.,

Raff D. (eds.), Coping with Variety, Ashgate,

Aldershot.

Parthasarthy R. [1992], The Impact of Flexible

Automation on Business Strategy and Organizational

Structure, in Academy of Management Review, (17),

1, 86-111.

Porter M. [1986], Competition in Global Industries,

Harvard Business School Press, 1986)

Sako M., Helper S. [1999], Supplier Relations and

Performance in Europe, Japan and the US : the

Effect of the Voice/Exit Choice, in Lung Y.,

Chanaron J-J., Fujimoto T., Raff D. (eds.), Coping