Embed Size (px)

Citation preview

ManagingHealth Expense

Chapter 11

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 2

Learning Objectives

1. Identify ways that people can manage the financial burdens resulting from illness or injury.

2. Distinguish among the types of protection for direct health expenses.

3. Describe the benefits and limitations of health care plans.

4. Explain how to protect yourself from the expenses for long-term care.

5. Develop a plan to protect your income when you cannot work due to disability.

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 3

Introduction

There are three finance related health care

issues :

1. Direct medical care costs

2. Lost Income when you cannot work due to illness or injury

3. Rehabilitative and custodial care costs

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 4

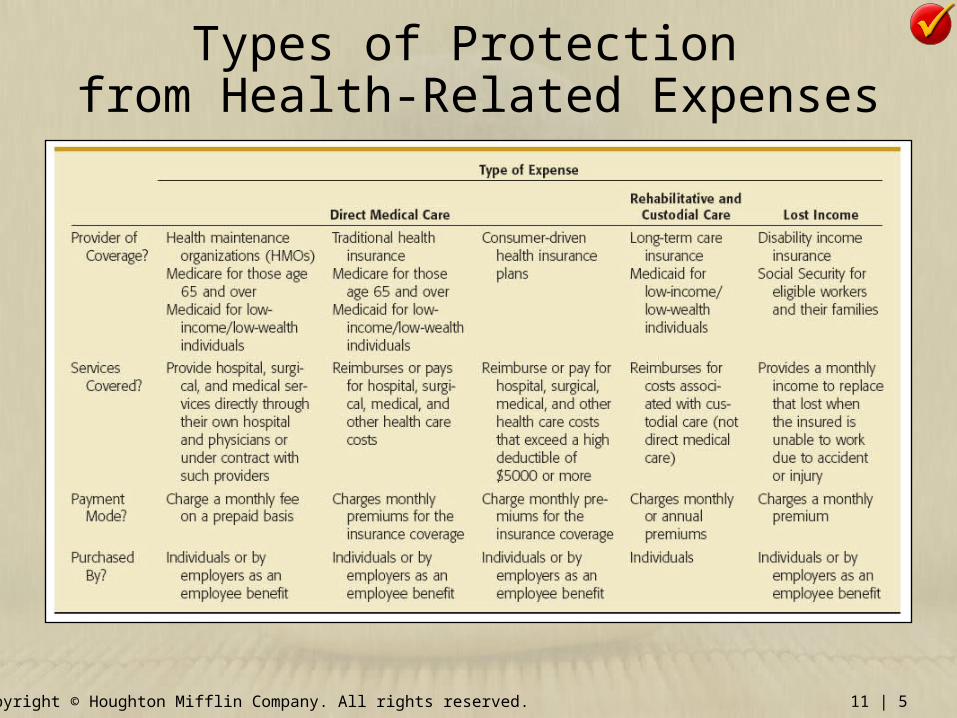

Financial Burdens of Illness or Injury• Group Health Plans:

1. Covering Your Direct Medical Care Costs

• Medicaid, Medicare – Insurance coverage funded by the government for low income or people age 65+.

– Medicare Part A – Hospital coverage with no premium

– Medicare Part B – Supplemental care for office visits with premium

– Medicare Part D – Prescription coverage with copayment

• Employer Medical – Insurance coverage partially funded by employer for employee and dependents

2. Covering Your Rehabilitative and Custodial Care Costs

• Long-term care insurance – Reimbursement for costs associated with intermediate-term and custodial care in a nursing facility or at home.

3. Covering Your Lost Income

• Social Security disability income insurance – Benefits provided by the government for individuals who cannot work for at least one year.

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 5

Types of Protection from Health-Related Expenses

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 6

Sources of Protection fromDirect Medical Care Costs

• Medical Care Plan

• Health Maintenance Organizations – Provide a broad range of health care services for a set monthly fee on a prepaid basis.

– HMOs, Managed Care Plans – Provide specific types of medical care under contract with provider at a set rate.

• Ex: Preapproval for hospital admission, restrictions on procedure and doctor selected for treatment

– Primary-Care Physician – An approved physician who is responsible for patient care and approves referrals to specialized health care providers.

– Individual Practice Organization – A group of physicians who maintain their own offices and contract with the HMO to provide patient care.

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 7

Traditional Health Insurance• Health Insurance – Provides protection against financial

losses resulting from illness and injury.

– Ex: Coverage for hospital, surgical or other medical expenses.

• Comprehensive Health Insurance – Differs from an HMO as policy is limited and reimburses rather than prepays the amount for health care coverage.

• Indemnity Plan – Compensate insured for the cost of care received up to a specified policy limit.

• Preferred Provider Organization – PPO is a group of medical care providers who contract with a health insurance company to provide services at a discount.

– Ex: Discount offered to policyholders reduces deductibles or coinsurance requirements

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 8

Consumer-Driven Health CareAssumes patients will spend their own money more carefully than they would spend funds from an employer health plan.

• High-Deductible Health Care Plan – Applies to traditional or HMO plans as a method to lower insurance premiums. Minimum deductible is $1,200 (Single) or $2,400 (Family). Maximum out-of-pocket costs is $6,050 (Single) or $12,100 (Family)

• Health Savings Account – Tax-deductible savings account where employees can deposit tax-sheltered funds to pay medical bills. Useful to offset cost of high deductible medical plans. Limit is $3,100 individual or $6,250 Family

• Health Reimbursement Account – Funds from employers provided to reimburse employees for qualified medical expenses.

• Flexible Spending Account – Employer-sponsored account that allows employee-paid expenses for medical or dependent care to be paid with pretax dollars rather than after-tax income. Allows up to $2,500 Max per year

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 9

Medical Plan Considerations• Certificate of Insurance: Paper or booklet that outlines group

health insurance benefits and coverage. Questions to ask include:– What types of Care Are Covered?

– Who is Covered?

– When does Coverage Begin and End?

– How much Do I Pay Out of Pocket?

• Dental expense insurance – May be optional in some plans. Typically has higher deductible, copayment and coverage limits. Ex: $1,500/Yr. max coverage

• Vision care insurance – Reimbursement or discount for eye examinations, contact lenses, glasses

• Preexisting conditions – A medical condition diagnosed within a certain period of time before the plan effective date. Insurance companies are banned (beginning in 2014) from excluding coverage for preexisting conditions - Patient Protection and Affordable Care Act of 2010

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 10

Who Is Covered• When does coverage begin and end?

– Optionally renewable policies – may be canceled or changed by the policy provider only at expiration or renewal with 30 days notice.

– Ex: Short Term Medical Coverage

– Guaranteed renewable policies – Continuous coverage provided as long as policyholder pays monthly premium which may change as a group for coverage.

– Ex: Kidney Dialysis Treatment

– Noncancelable policies – Policy continues and premium may not change up to age 65 as long as premium is paid by participant.

– Ex: Disability income insurance protection.

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 11

How Much Must Your PayOut of Your Own Pocket?

• Deductibles – A requirement to pay an initial portion of medical expenses annually before receiving reimbursement

• Copayments – A requirement to pay a specific amount each time a covered expense item is used.

• Coinsurance – Payment for a proportion of any loss suffered. Ex: 80/20

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 12

Policy Limits• Item limits – Specify a limit or max payment for a given

medical cost. Goal is to contain medical costs by limiting total reimbursement paid. Ex: $75 limit for X-Ray expenses.

• Daily limits – Maximum payment of amount per day of services provided such as hospitalization expenses. Ex: $1,000 per day.

• Episode limits – Maximum payment for health care expenses per event such as $50K each event.

• Annual limits – Payment amount for coverage defined by time period which is typically a calendar year. Ex: $100K Limit/Year

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 13

Coordination of Benefits

• Maintain your medical care plan between jobs.

– COBRA rights – Federal Law which allows employee to pay the employer premium rate for a period of 18 months after termination and receive insurance coverage.

– Portability option – Allows employee to convert group insurance coverage to individual coverage within 180 days before COBRA ends. Benefit of waiving any pre-existing condition or waiting period

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 14

Planning for Long-Term Care1. The degree of impairment required for benefits to begin:

– Activities of Daily Living (ADLs) – criteria for deciding when the insured becomes eligible for long term care benefits. Policy coverage is begins when 2 or 3 ADL’s cannot be performed such as bathing, dressing, eating without assistance, etc.

2. The level of care covered:

– Skilled nursing care – Designed for people who need 24 hr. supervision and treatment by a nurse.

– Intermediate care – People who cannot live independently but do not require 24 hr. supervision.

– Custodial care – Individuals who require supervision but do not require skilled nursing care.

• Long Term Care plans are written to provide specific dollar benefits per day of care.

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 15

Planning for Long-Term Care

3. The person’s age determines the premium paid with a younger person paying a lower premium.

4. The benefit amount in the policy prescribes a specific amount per day of care such as $150

5. The benefit period determines cost and can be expensive for lifetime coverage vs. shorter time periods.

6. The waiting period for care can reduce premiums for 30 or 90 days vs. first day coverage from eligibility.

7. Inflation protection is needed for the younger policyholder (less than 60 yrs.) to ensure adequate coverage later when needed. Ex: Daily benefit increase of 4%-5% per year.

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 16

Protecting YourIncome During Disability

• Disability income insurance – Private insurance that replaces a portion of the income lost when you cannot work because of illness or injury. Ex: Aflac, Mutual of Omaha, State Farm, MassMutual

– Short Term vs. Long Term Coverage

– Supplemental plans offer flexibility

• Social Security disability insurance – Government program designed to replace a portion of the lost income of eligible disabled workers.

– Benefits begin after a 5 month waiting period

– Must be qualified as unable to work by medical professional

– Disability to last at least one year

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 17

Income Protection OptionsDuring Disability

• Level of need – most policies limit coverage to 60%-80% of after tax earnings.

• Important disability income insurance policy provisions:

– Waiting period (or elimination period) between onset of disability and period when benefits begin.

– Benefit period – Max period when benefits are paid

– Degree of disability

• Split-definition policies – provide income benefit for a limited time period such as during rehabilitation or therapy.

• Residual clause of disability income policy – Allows for a reduced level of disability income benefit when only a partial disability occurs.

– Social Security rider – Optional addition to insurance coverage which protects insured in case application for social security benefits is denied. (70% of all applications are rejected)

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 18

The Top 3 Financial ChallengesIn Managing Health Expenses

People experience difficulty when they do the following:

1. Go unprotected for health care when changing jobs.

2. Duplicate employer-provided health care protection with your spouses.

3. Ignoring the need for protection of income during a period of disability.

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 19

Good Money Habits inManaging Health Expenses

• Always maintain coverage for direct health care expenses. http://www.ehealthinsurance.com/

• When changing employers, consider continuing your medical care plan coverage using rights established through the COBRA law.

• Employees should sign up for an employer-sponsored health plan, health savings account (HSA) or a flexible spending account (FSA) for health care spending when available, to save money on taxes.

• If you are a frequent user of health care, reduce spending on deductibles and coinsurance by choosing an HMO or PPO.

• If available, take advantage of employer-sponsored long-term disability income insurance or consider purchasing protection individually.

• Regularly reevaluate your need for long-term care insurance against your resources for providing such care on your own.

Copyright © Houghton Mifflin Company. All rights reserved. 11 | 20

Questions?