Embed Size (px)

Citation preview

Managing Finance and Budgets

Seminar 3

Seminar Three - Preparation

Read Chapters 5 and 16 Review key concepts:

Cash Flow Statement

Working Capital Exercises 5.7 (pages 170-1) and 16.3 (page 540)

Seminar 2 - Activities

During this seminar we will: Review the key concepts and ideas from the

lecture Review Chapter 5 of the set book Examine exercise 5.7 (pages 170-1) Review Chapter 16 of the set book Examine exercise 16.3 (page 540)

Some Starting Points

Explain the difference between Cash and Profit. Explain what is meant by the following:

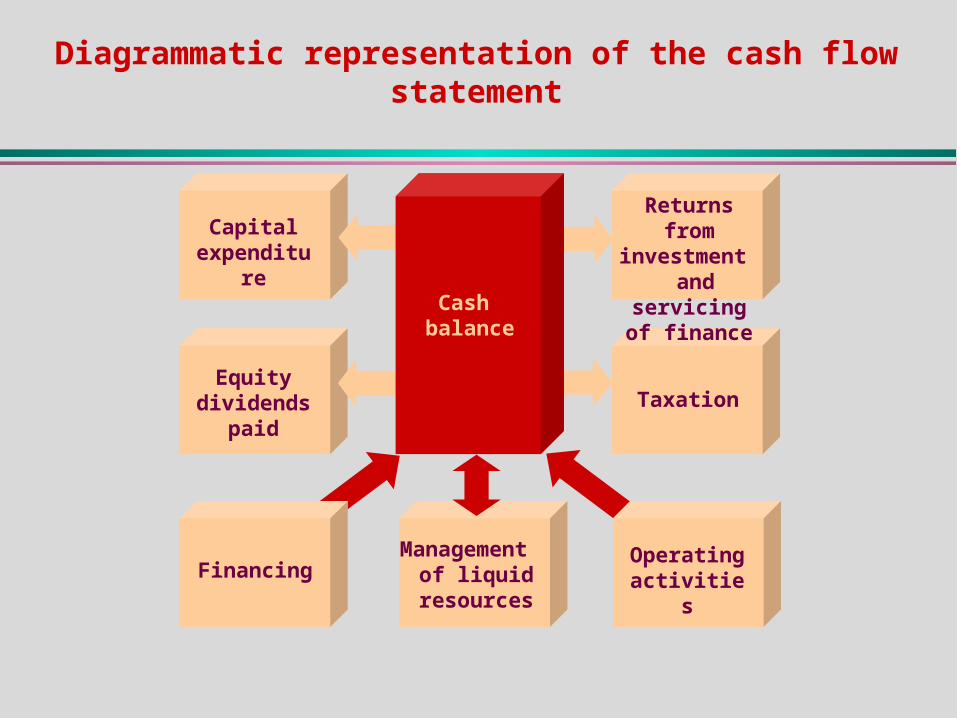

Operating Activities Returns from Investment Servicing of Finances Taxation Capital Expenditure Equity Dividends Liquid Resources

The Cash-Flow Statement 1

Describe the structure of the Cash-Flow Statement.

State what is meant by the direct and indirect methods of deducing the Net Cash-Flow from the Operating Activities, explaining briefly the difference between them.

Equity dividends

paid

Financing

Capital expenditure

Returns from investment

and servicing of finance

Taxation

Management of liquid

resources

Operating activities

Cash balance

Diagrammatic representation of the cash flow statement

plus or minus

plus or minus

plus or minus

plus or minus

equals

plus or minus

plus or minus

Increase or decrease in cash over the period

Net cash flow from operating activities

Returns from investment and servicing of

finance

Taxation

Capital expenditure

Equity dividends paid

Management of liquid resource

Financing

Standard layout of the cash flow statement

The Cash-Flow Statement 2

For the Indirect method of calculating the net cash-flow, state the list of items, taken in order, that you would need to include in your calculations.

Exercise 5.7 p 169

plus

plus or minus

equals

plus or minus

plus or minus

Net cash flow from operating activities

Net operating profit

Depreciation expense

Increase (minus) or decrease (plus) in stock

Increase (minus) or decrease (plus) in debtors

Increase (plus) or decrease (minus) in creditors

The indirect method of deducing the net cash flow from the operating activities

Summarising…

Describe the relationship(s) between:The Balance SheetThe Cash-Flow StatementThe Profit & Loss Account

Balance sheet at the start of

the accounting period

Owner’s claim

Cash

Balance sheet at the end of

the accounting period

Owner’s claim

CashCash flow statement

Profit and loss account

The relationship between the balance sheet, the profit and loss account and the cash flow statement

Managing Working Capital

Explain what is meant by “working capital”, describing some of the elements which affect it.

Describe the ‘working capital’ cycle.

The nature and purpose of working capital

Major elements Major element

Stocks

Trade debtors

Cash (in hand and at bank)

Trade creditors

lessequals

Current liabilitiesWorking capital Current assets

The working capital cycle

Cash sales

Trade creditors

Trade debtors

Finished goods

Cash/bank overdraft

Work-in-progress

Raw materials

Managing Working Capital

Describe three financial ratios which can help a manager to monitor the flow of working capital, in relation to: stock levels, debtors and creditors.

Exercise 16.3

Managing Stocks

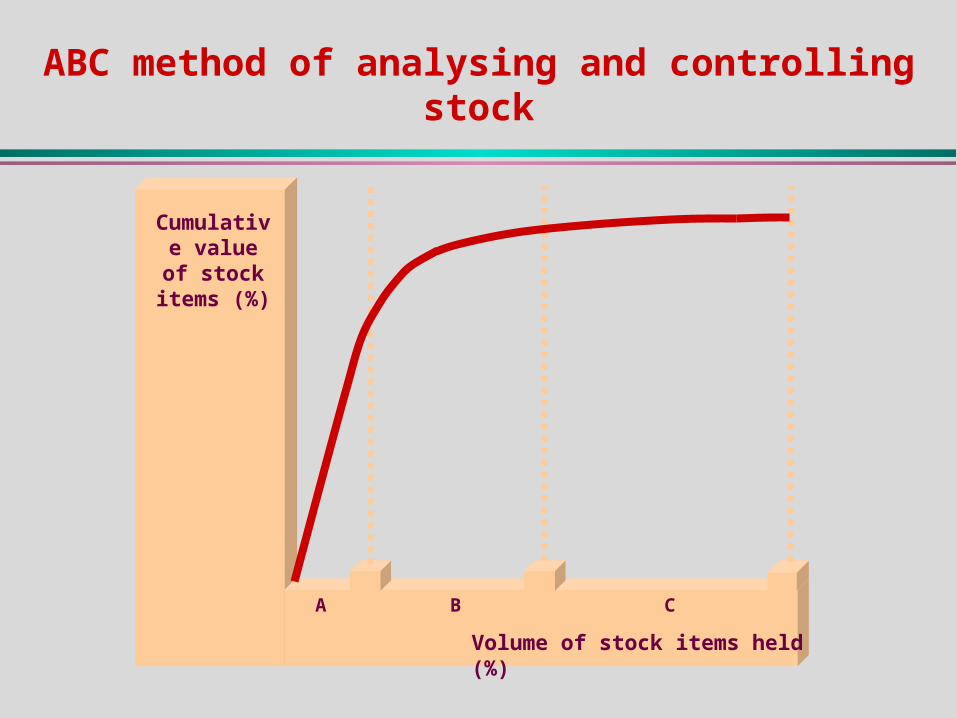

Describe the following methods of stock management: ABC system, economic order quantity, materials requirement planning, just-in-time method.

The management of stocks

Procedures and techniques

Forecasts of future demand

Financial ratios

Recording and reordering systems

Levels of control

Stock management models

Materials requirements planning (MRP) systems

Just-in-time (JIT) stock management

ABC method of analysing and controlling stock

Cumulative value of

stock items (%)

Volume of stock items held (%)

A B C

Stock level

Time

Patterns of stock movements over time

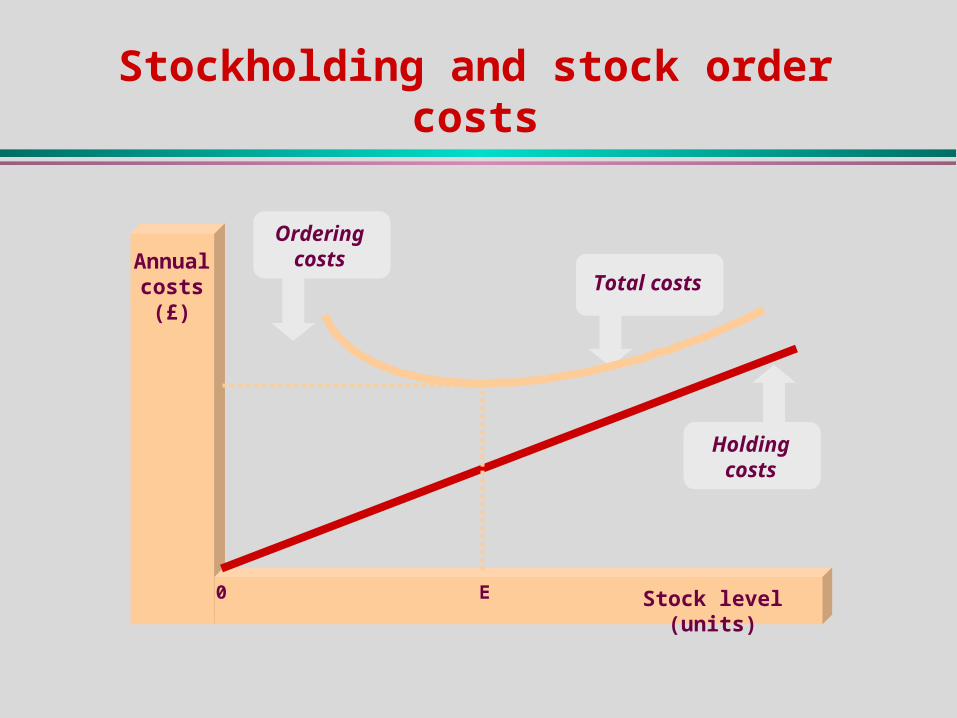

Stockholding and stock order costs

Annual costs

(£)

Stock level (units)E

Total costs

Holding costs

0

Ordering costs

Managing Working Capital

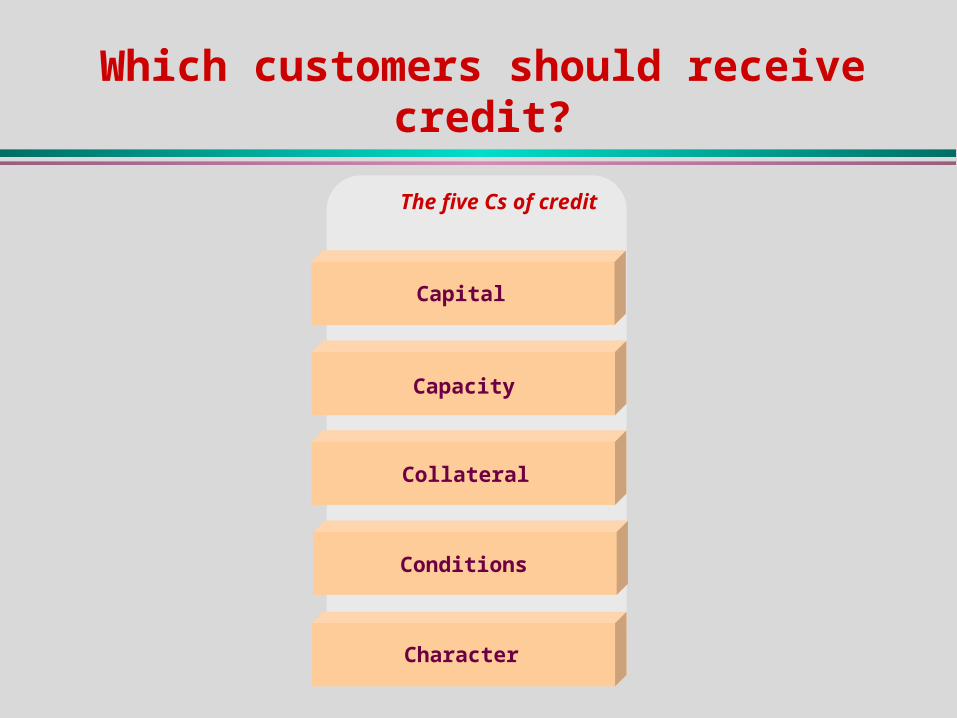

State and describe criteria which can be used to help decide which customers should receive credit.

The five Cs of credit

Capital

Capacity

Collateral

Conditions

Character

Which customers should receive credit?

%

Time

10

20

30

40

June

0

July August September

Actual

Budgeted

Comparison of actual and budgeted receipts over time for Example 16.3

The Operating Cash Cycle

Explain what is meant by the Operating Cash cycle, and discuss some methods a manager can use to control it.

Purchase of goods on credit

Payment for goods

Sale of goods on

credit

Cash received

from debtors

Stockholding period

Operating cash cycle

The operating cash cycle

equals

minus

Operating cash cycle

Average payment period for creditors

Average settlement period for debtors

plus

Average stockholding period

Calculating the operating cash cycle

Inner limit

Outer limit

Target cash balance

Inner limitCash

balance (£)

Outer limit

Time (days)

2 864 9531 7 11 12100

Controlling the cash balance