Embed Size (px)

DESCRIPTION

MANAGEMENT OF ACCOUNTS RECEIVABLES AND PROFITABILITY OF SMALL SCALE ENTREPRISES

Citation preview

MANAGEMENT OF ACCOUNTS RECEIVABLES AND PROFITABILITY OF

SMALL SCALE ENTREPRISES

CASE STUDY: IKONGO ENTERPRISES

BY

MR. BWAMBALE JOSEPH

REG. NO. 07/U/7654/EXT

SUPERVISOR

MR. NZIBONERA ERIC

A RESEARCH REPORT SUBMITTED IN PARTIAL FULFILMENT OF THE

REQUIREMENTS FOR THE AWARD OF THE DEGREE OF BACHELOR

OF COMMERCE OF MAKERERE UNIVERSITY

MAY 2011

i

ii

DECLARATION

I, Bwambale Joseph, declare that this work is an original of my own effort and has never

been represented by any academic institution for any a ward.

Signature…………………………………….

BWAMBALE JOSEPH

Date………………………………

This report has been submitted for examination with my approval as a university

supervisor.

Signature……………………………………….

MR. NZIBONERA ERIC

Date………………………………………………………..

iii

DEDICATION

I dedicate this work to my family and particularly my parents Mr. Kolera Dirian and Mrs.

Kolera Agness whose lives were the answers to my academic struggle and who might

have foregone some of the basic needs during the time of my struggle.

iv

ACKNOWLEDGEMENT

I take this as an opportunity to put in writing my appreciation to my brother Baluku Julius

Kolera whose contribution has been profoundly felt from the nascent stages of my

academic struggle up to the end. On the same note, I extend my appreciations to the

family of Mr. Masereka Paul without whose assistance I would be constrained along my

way.

I further appreciate my relatives; Muhindo David, Kolera Stephen, Kolera Tomas, Kolera

Jimy, Kolera Juliet and Kolera Janet, Cosmus, and Grace. I feel indebted to all of you for

the unsecured support, guidance and comfort given to me during the time of my academic

struggle.

In a special way, I wish to acknowledge my supervisor Mr. Nzibonera Eric who guided

me in an effort to make this work reflect the required academic standards of Makerere

University.

Special thanks go to my friends Mr. Rumanzi Collins, Ms. Nakagwa Doreen and Mr.

Gule Swadik whose contribution to my struggle can not be under estimated

I also acknowledge my friend Tsongo Andrew and Mukamba Samuel with whom I felt

the importance of friendship.

Thank you. To you, I owe my support.

v

TABLE OF CONTENTS

DECLARATION..................................................................................................................i

DEDICATION.....................................................................................................................ii

ACKNOWLEDGEMENT..................................................................................................iii

TABLE OF CONTENTS...................................................................................................iv

LIST OF TABLES.............................................................................................................vii

ABSTRACT.......................................................................................................................ix

CHAPTER ONE..................................................................................................................1

1.0 Introduction....................................................................................................................1

1.1 Back ground of the study...............................................................................................1

1.2 statement of the problem................................................................................................3

1.3 Purpose of the study.......................................................................................................3

1.4. Objectives of the study..................................................................................................3

1.5 Research questions.........................................................................................................4

1.6 Scope of the study..........................................................................................................4

1.7. Significance of the study...............................................................................................4

CHAPTER TWO.................................................................................................................6

2.0 LITERATURE REVIEW..............................................................................................6

2.1 Introduction....................................................................................................................6

2.2 Accounts receivables.....................................................................................................6

2.3 Justification for investment in account receivables.......................................................7

2.4.0 Account receivables management policy....................................................................8

2.3.1 Credit policy................................................................................................................8

2.4.2 Credit standards..........................................................................................................9

2.4.3 Credit terms...............................................................................................................10

2.4.4 Collection procedures...............................................................................................10

2.5 Profitability..................................................................................................................10

2.6 Relationship between accounts receivables management and profitability.................11

2.7 Conclusion..................................................................................................................12

CHAPTER THREE...........................................................................................................13

vi

3.0 Methodology................................................................................................................13

3.1 Introduction..................................................................................................................13

3.2 Research design...........................................................................................................13

3.3 Study population..........................................................................................................13

3.4 Sample size and sample procedure..............................................................................13

3.5 Sources of data.............................................................................................................14

3.6 Data collection methods and techniques......................................................................14

3.7 Data presentation and analysis.....................................................................................14

3.8 Limitations of the study...............................................................................................14

CHAPTER FOUR..............................................................................................................16

4.0 Presentation, interpretation and discussion of findings...............................................16

4.1 Introduction..................................................................................................................16

4.2.0 Characteristics of respondents..................................................................................16

4.2.1 Classification according to gender............................................................................16

4.2.2 Classification according to age.................................................................................17

4.2.3 Classification according to education level..............................................................17

4.2.4 Classification according to the time respondents have been in dealings with Ikongo

enterprise............................................................................................................................18

4.3.0 Finding on accounts receivables management..........................................................18

4.4.0 Findings on profitability...........................................................................................24

4.5.0 Finding on the relationship between accounts receivables management and

profitability........................................................................................................................26

CHAPTER FIVE...............................................................................................................30

5.0 Introduction..................................................................................................................30

5.2.0 Summary of findings.................................................................................................30

5.2.1 Accounts receivables management...........................................................................30

5.2.2 Profitability...............................................................................................................30

5.2.3 Relationship between accounts receivables management and profitability..............30

5.3.0 Conclusion................................................................................................................31

5.4 Recommendations........................................................................................................31

5.5 Suggested areas for further researchers.......................................................................31

vii

REFERENCES..................................................................................................................32

APPENDICES...................................................................................................................33

APPENDIX I: questionnaire to the management and employees of Ikongo enterprise....33

APPENDIX II Questionnaire to the customers of Ikongo enterprise................................36

APPENDIX III Introductory Letter...................................................................................39

viii

LIST OF TABLES

Table 1: Showing composition of respondents by gender.................................................16

Table 2: Showing composition of respondents by age......................................................17

Table 3: Showing respondents’ level of education............................................................17

Table 4: Showing time respondents have been dealing with Ikongo enterprise................18

Table 5: Showing respondents’ response on the use of receivable management policy at

Ikongo enterpise.................................................................................................................19

Table 6: Showing responses whether Ikongo enterprise extends credit to customers.......19

Table 7: Showing responses on the effectiveness of accounts recievables collection in

Ikongo enterprise...............................................................................................................20

Table 8: Showing responses of respondents on whether the prevailing economic and

social political factors might affect customers ability to pay............................................21

Table 9: Showing responses on bad debt losses................................................................21

Table 10: Showing responses on cash discounts for early payment of credit...................22

Table 11: Showing responses on collateral security..........................................................23

Table 12: Showing responses on default of payments.......................................................24

Table 13: Showing responses on the growth of profitability at Ikongo enterprise between

2005 and 2010....................................................................................................................25

Table 14: Showing the ratio of bad debts to profitability (net profit)................................26

Table 15: Showing calculation of the relationship between accounts recievables

management and profitability using Pearson’s product moment correlation coefficient. .27

ix

x

ABSTRACT

The study was meant to establish the influence accounts receivables management on

profitability of small scale enterprises in reference to Ikongo enterprise. Ikongo enterprise

operates a diversity of business operations in and around Kasese District. The study

covered the period between 2005-2010.

The objectives of the study were; to examine the receivables management policy applied

by Ikongo enterprise, to determine the profitability of Ikongo enterprise and to determine

the relationship between receivables management and profitability at Ikongo enterprise.

Both simple random and stratified sampling were used. Data was collected by use of

questionnaires. Data was processed by editing, summarized, presented in tables and was

manually analyzed.

In the findings, most of the respondents strongly agreed or agreed to the fact that

receivable management influences profitability which was found to be a positive strong

correlation coefficient of 0.97.

It was also established that Ikongo enterprise applies a stringent receivables management

policy that ensures effectiveness in the collection of receivables and thus reduction in bad

debt losses hence improving the profitability of the enterprise.

From the finding, the researcher recommended that; accounts receivables constitute a

significant portion of the current assets of a firm and thus all efforts should be

coordinated to ensure optimal investment in them, the credit control department should

be adequately staffed to make fast the collection process, enterprise should adopt a

receivables management policy that maximizes the expected profits and is compatible

with other policy decisions.

xi

CHAPTER ONE

1.0 Introduction

This chapter shows the background of the study, statement of the problem, purpose of the

study objectives, research questions, scope and significance of the study.

1.1 Back ground of the study

According to Kakuru julius (2000), when a firm sells its products or services and does not

receive cash for it, the firm is said to have granted trade credit to customers. Trade credit

thus creates receivables which the firm is expected to collect in the near future. The

would be cash payment for goods and services by the buyer are made in a future period

and customers from which receivables are collected in future period are called debtors.

Business enterprises today use trade credit as a prominent strategy in the area of

marketing and financial management. Thus, credit is necessary in the growth of the

business.

Accounts receivables occurs if a company gets an order from a customer with payment

terms agreed upon in advance. In most firms accounts receivables are executed by

generating an invoice which is delivered to the customer, who in turn must pay with in

the agreed terms, for instance it can be net30 meaning payment is due at the end of

30days.

Brealey and Meyers (1988), defined receivables as money due from another business or

individual in payment for the performance of services or sale of goods on credit.

Receivables constitute a substantial portion of the current assets of several firms. In most

firms, trade debtors, after inventories, are the major components of current assets.

xii

Trade credit is very important to a firm because it helps to protect its sales from being

eroded by competitors and also attract potential customers to buy at favorable terms. As

long as there is competition is an industry, selling, on credit becomes inevitable.

A business will loose its customers to competitors if it does not allow credit to them.

Thus investment in recievables may not be a matter of choice but a matter of survival

(Kakuru Julius, 2001).

Given that investment in receivables has both benefits and costs; it becomes important to

have such a level of investment in receivables at the same time observing the twin

objectives of liquidity and profitability.

To ensure optimal investment in receivables, a firm required an appropriate credit policy.

Credit policy is designed to minimize costs associated with credit while maximizing the

benefits from it. Credit policy is either lenient or stringent. A lenient credit policy tends

to give credit to customers on very liberal terms and standards such that credit is granted

for longer periods even to those whose credit worthiness is not fully known. A stringent

credit policy allows credit only to those whose credit worthiness has been ascertained and

is financially strong.

Profitability is the excess of income and expenditure that can be expressed by the ratios

like gross profit margin and return on equity (ACCA Financial reporting paper F7 2009).

Profitability is an indicator of an organization’s competitive position in the market place

and reflects the quality of the organization’s management (MC Naughton and Dietz,

1996). Firm should generate more profits in order to sustain day to day operations, more

funds for reinvestment and to provide income to share holders through dividends.

Higher level of investment in receivables enhance the liquidity position of the firm at the

expense of profitability due to costs associated while lower levels of investment in

receivables leads to loss of liquidity though enhances profitability (ACCA, Financial

management, paper F9, 2009)

xiii

To remain profitable, the firm must ensure proper management of its receivables (Foulks,

2005). The management of receivables is a practical problem. Firm can find their

liquidity under considerable strain if the level of their accounts receivables is not properly

regulated (Samuels and walkers, 1993). Thus management of accounts receivables is

important, for without it; receivables will build up to excess levels leading to declining

cash flows. Poor management of receivables will definitely result into dad debts which

lower the firm’s profitability levels.

1.2 statement of the problem

Organizations establish receivables management policy in order to ensure optimal

investment in receivables so as to achieve sound financial position and profitable

operations (Kakuru Julius, 2000). Despite the efforts by Ikongo enterprise to achieve

sound receivables management and profitable operations, the enterprise has continued to

register accumulated debt balances and bad debt write offs, which lower down its profits

(Debtors valuations records, 2008). This put into question the relationship between

receivables management policy and the profit levels of Ikongo enterprise.

1.3 Purpose of the study.

The purpose of the study was to determine the relationship between management of

accounts receivables and profitability levels of small scale enterprises.

1.4. Objectives of the study

i. To examine receivables management policy applied by small scale enterprises

ii. To determine the profitability levels of small scale enterprises

iii. To determine the relationship between receivables management and profitability

of small scale enterprises.

xiv

1.5 Research questions.

i. What receivable management policy is applied by small scale enterprises?

ii. What are the profitability levels of small scale enterprises?

iii. What is the relationship between receivables management and profitability of

small scale enterprises?

1.6 Scope of the study

i. Subject scope. The study focused on the relationship between management of

accounts receivables and the profitability levels of Ikongo enterprise.

ii. Geographical scope. The research was carried out from the trading premises of

Ikongo enterprise in Bwera branch and its branches in Hima, Kagando,Katwe and

Kasese municipality.

iii. Time scope. The study covered the operations of Ikongo enterprise for the period

from 2005 to 2010

1.7. Significance of the study

i. The study findings will enable the management of Ikongo enterprise to identify

the weakness in the instituted receivable management policy. If the management

of Ikongo enterprise accepts this report, it will provide a good guide for the

improvements in the enterprise receivables management.

ii. The study will provide literature review to the subsequent researchers or scholars

who will conduct research in the same field of study.

xv

iii. The study will improve the researcher’s knowledge on reporting aspects, data

collection and analysis.

iv. The study will enable the researchers to qualify for the award of bachelor of

commerce degree.

xvi

CHAPTER TWO

2.0 LITERATURE REVIEW

2.1 Introduction.

This chapter carries out a review of the literature on the relationship between

management of accounts receivables and profitability levels. It covers receivables,

justification for investment in receivables, receivables management policy, profitability,

the relationship between receivables management and profit levels and the conclusion.

2.2 Accounts receivables.

According BPP Publishers, Financial management (2009), accounts receivables represent

the firm’s claim on the assets of customers. Receivables constitute a substantial

proportion of the current assets of several organizations, thus represent investment.

Kakuru (2000) defines receivables as book debts which the firm is expected to collect in

the near future and those receivables is money owed to the business for a short period of

time.

Eskew (1989) noted that receivables are investments and should neither be too many nor

too few but rather the test should be whether the level of return the firm is able to earn

from receivables equals or exceeds the potential gain from other commitments.

Dickerson (1995), also commented that if it is possible to sell on credit, then selling on

credit becomes more profitable, for it leads to increased sales as well as profits. And

helps to maintain and retain customers. Thus companies should sell on credit than on

cash.

xvii

However, firm’s potential to earn a favorable return on investment in receivables is

dependent on the volume of credit sales, collection period and credit policy applied.

2.3 Justification for investment in account receivables.

Trade credit is important to a firm because it helps to protect its sales from being eroded

by its competitors and also attract potential customers to buy at favorable terms. In most

economies, including Uganda, trade credit is significant source of working capital

(Pandey, 1996).

Kakuru (2000), noted that different business firms depending on their size, the nature of

the business dealt in and type of industry give various justifications for investment in

receivables;

Firm use trade credit as marketing tool. When a firm has just launched its products,

credit can be used to expand sales. In declining market, it can be used to maintain the

market share. Credit is also extended so as to build long term relationships with the

customer or as a reward for their loyalty i.e. building customer good will.

Depending on the status of the buyer, credit is granted. Because of bulk purchases and

higher bargaining power, large scale buyers demand easy credit terms. Some companies

may not grant credit to small scale retailers since it becomes hard to collect receivable

from them. By extending large amounts of credit to big firms, the company extending

credit will be at an advantage as it will collect the money in lump sums.

Trade credit enhances a company’s bargaining power. If a company’s bargaining power

is low, it will grant more credit so as to build and enhance its bargaining power unlike a

company with a high bargaining power.

xviii

Granting credit to customers may be a practice with in a given industry. Thus new

entrants in the industry are left with no option but find it inevitable to offer credit. This is

done so as to win customers from competitors and later on maintain them using the same

incentive. Therefore, if any firm is to survive in any competitive industry, granting credit

becomes inevitable.

2.4.0 Account receivables management policy.

To ensure optimal investment in receivables, a firm requires an appropriate credit policy.

Kakuru (2000) define credit policy as a set of policy actions designed to minimize costs

associated with credit while maximizing benefits from it. It is aimed at having optimal

investment in receivables. Optimal investment is that level of investment where there is a

trade off between the costs and the benefits associated with a particular investment. A

firm’s credit policy should maximize the firm’s value. The firm’s value is maximized

When incremental rate of return is equal to incremental costs of funds used to finance the

investment (ACCA Financial management, paper F9, 2009).

2.3.1 Credit policy.

This refers to guidelines that are followed in managing credit in a business. Credit policy

includes credit standards, credit terms and collection procedures. Credit sales are a

function of total sales; total sales depend on such factors as the economic conditions e.t.c

credit sales are also influenced by the nature of the business and industrial norms. All

these factors are to a very large extent uncontrolled by a financial manger. The only way

credit sales can be controlled is by making alterations in the firm’s credit policy. A firm

therefore requires credit policy in its operations since a proportionately large amount of

sales are made on credit and credit policy variables are the ones in the control of the

manger (Kakuru, 2001).

Credit policy is designed to minimize costs associated with credit while maximizing the

benefits from it. Credit policy is either lenient or stringent.

xix

Lenient credit policy

This policy tends to give credit to customers on very liberal terms and standards. Credit

is granted for period of time even to those customers whose credit worthiness is not fully

known or whose financial position is doubtful. Credit is granted at high discount rates.

Stringent credit policy.

A stringent credit policy gives credit on highly selective basis only to customers whose

credit worthiness has been ascertained and is financially strong. Credit periods are shorter

and discounts are lower. It involves low costs but may be detrimental to sales returns. A

firm needs to formulate a credit policy which is optimum.

Credit policy involves three variables. i.e. credit standards, credit terms and collection

procedures (Kakuru, 2000)

2.4.2 Credit standards.

These focus on the person who wants credit and thus determines who qualifies for the

credit. Credit standards are the criteria, which the firm follows in selection of customers

for credit extension. In order to analyze customers and set credit standards, the firm

should consider the average collection period (ACP) and the default rate. Average

collection period is the period in which the debts remain outstanding. On the other hand,

default rate is the rate of uncollected receivables to total receivables. From the default

ratio, the firm is able to determine that the customer will not meet his credit obligation.

To estimate the probability of default, a financial manager should consider the 5c’s of

credit i.e. character, capacity, condition, capital and collateral.

i. Character. This is the willingness of a customer to settle his credit obligations.

The financial manager should ascertain whether the customer would make honest

efforts to honor his debt obligation.

xx

ii. Capacity. This is the ability of a customer to pay the credit advanced to them.

The manager should look at financial statements, previous experience with the

client, trade references, bank references, amount and the purpose of credit.

iii. Condition. It involves assessment of the prevailing economic and other factors

like social, political which may affect the customers’ ability to pay. e.g.; it is

undesirable to grant credit during inflationary conditions.

iv. Capital. This is the contribution or interest of the customer in his business. It is

undesirable to grant credit to customers who have little capital in their business.

v. Collateral. This is security against failure to pay. The person seeking credit

should offer security before credit is granted. The security should easily be

marketable.

2.4.3 Credit terms.

These are stipulations under which a firm grants credit to customers. Credit terms should

be more attractive to act as an incentive to clients without incurring high level of bad debt

losses. Thus the terms offered should confirm to the average industrial terms.

2.4.4 Collection procedures.

These are effort applied in order to accelerate collections from slow paying customers

and to reduce bad debt losses. Collection procedures include sending reminders, use of

litigation, insuring debtors, e.t.c.

2.5 Profitability.

Profitability is the difference between the cost of providing goods or services and the

revenue derived from the sale (Mutenyo, 2007).

xxi

The scholars noted that accountants define profits as the difference between costs and

revenues. They further noted that in business, profit was put by the sandilands

committee; “ is the maximum value which the company can distribute during the year

and still expect to be as well off at the end of the year as it was at the beginning”.

According to traditional economist, profit maximization is taken as the objective of a

business. Profit is the end result of an organization and a reward to entrepreneurs for

undertaking risks (Mutenyo, 2007)

Pandey (1996) further noted that a company should earn profits to survive and grow over

a long period of time. Sufficient profits should be earned to sustain the operations of the

business and to contribute towards the social overheads for the welfare of the society.

Stoner (1996) defines profitability as the excess of income and expenditure that can be

expressed by the rations like gross profit margin, net margin and return on equity.

Besides the management of the company, creditors and shareholders are also interested in

the profitability of the firm; creditors want to earn interest on repayment of the principal

amount while shareholders want to get a reasonable return on their investment. This can

only be possible when the firm earns profits.

2.6 Relationship between accounts receivables management and profitability.

For effective management of accounts receivables, a firm must put in place an

appropriate credit policy. Credit policy influences the level of book debts. A firm should

be discretionary in giving debts to customers depending on the trust in them and should

be prompt in collecting them (Kakuru, 2000). However with other current assets, the

financial manager can vary the level of receivables in keeping with the trade off between

profitability and liquidity. Lowering credit standards increases the level of sales leading

to an increase in profits. But also there is an additional cost corresponding to an increase

in receivables as well as greater risk of bad debt losses.

xxii

Brockington (1993), argues that there is an opportunity cost of additional receivables

resulting from increased sales and the slower average collection period and that, if new

customers are attracted by the liberal credit standards, collections from these customers

are likely to be slower than collection from existing customers. Thus a liberal extension

of credit may cause certain customers to be relaxed in the payment of debt obligations on

time.

Kakuru (2000), notes that a liberal credit policy may be undesirable because the firm may

not attain its benefit at the least possible cost and hence a danger of higher costs. On the

other hand a stringent credit policy may be advantageous in the low costs are involved.

But this may slow down sales returns.

2.7 Conclusion.

With regards to the literature used in this research, it has been observed that there is wide

data about the variables under study and that it is not easy to establish a perfect system of

receivables management that will guarantee maximum profitability. This is because of

the conflicting interests of the firm i.e promoting profitability while maintaining a certain

level of liquidity. That to achieve one, there is an opportunity cost of loosing another.

Thus it becomes necessary to strike a balance where investment in receivables is at

optimum. The need to achieve optimal investment in receivables calls for a firm to

institute a credit policy.

xxiii

CHAPTER THREE

3.0 Methodology

3.1 Introduction

This chapter explains the methods that were used to conduct the research in the collection

of data and a plan of how the study was conducted. It presents research design, sampling

design, study population, sample size, source of data, data collection methods and

techniques, data presentation and analysis, then limitations of the study.

3.2 Research design

The study was both descriptive and explanatory and based on both quantitative and

qualitative data.

3.3 Study population

The study population was made up of the management, staff and the customers of Ikongo

enterprise. There are 9 management staff and 50 employees with a quite number of

customers.

3.4 Sample size and sample procedure

The researcher purposively selected 5 management staff and 18 employees

Both stratified and simple random sampling was used to select 17 customers. The sample

population was divided into strata from which the researcher used simple random in

selection of customers so as minimize bias.

xxiv

3.5 Sources of data

Data was obtained from both primary and secondary sources.

i. Primary data. This provided first hand information through questionnaires.

ii. Secondary data. The researcher used information from management meeting

minutes; company recorded e.g. debtor’s valuations records and information from

previous research reports.

3.6 Data collection methods and techniques.

Questionnaires. Closed end questions were designed and distributed to all respondents for

answering.

3.7 Data presentation and analysis.

The data collected was edited, coded to ensure reliability and completeness. It was the

presented using frequency tables and percentages.

3.8 Limitations of the study

i. With the economic of scarcity of resources, the researcher did not exhaust all the

data. Several costs were involved e.g typing and printing, transport and telephone

calls among others.

ii. Withholding information. Some of the respondents were not willing to disclose

the Information; some were not in the moods of discussions.

xxv

iii. Time limit. Given other academic demands like course works, test and final

exams, the researcher did not have enough time to enable him exhaust all the

study variables. However, he apportioned time so as to arrive at valid conclusions.

xxvi

CHAPTER FOUR

4.0 Presentation, interpretation and discussion of findings.

4.1 Introduction.

On obtaining the data from both primary and secondary sources, the findings were coded,

edited, presented inform of tables, frequencies and percentages from which discussions

and findings were based.

4.2.0 Characteristics of respondents.

The respondents were classified according to sex, age, education level so as to get a fair

representation of the study population.

4.2.1 Classification according to gender.

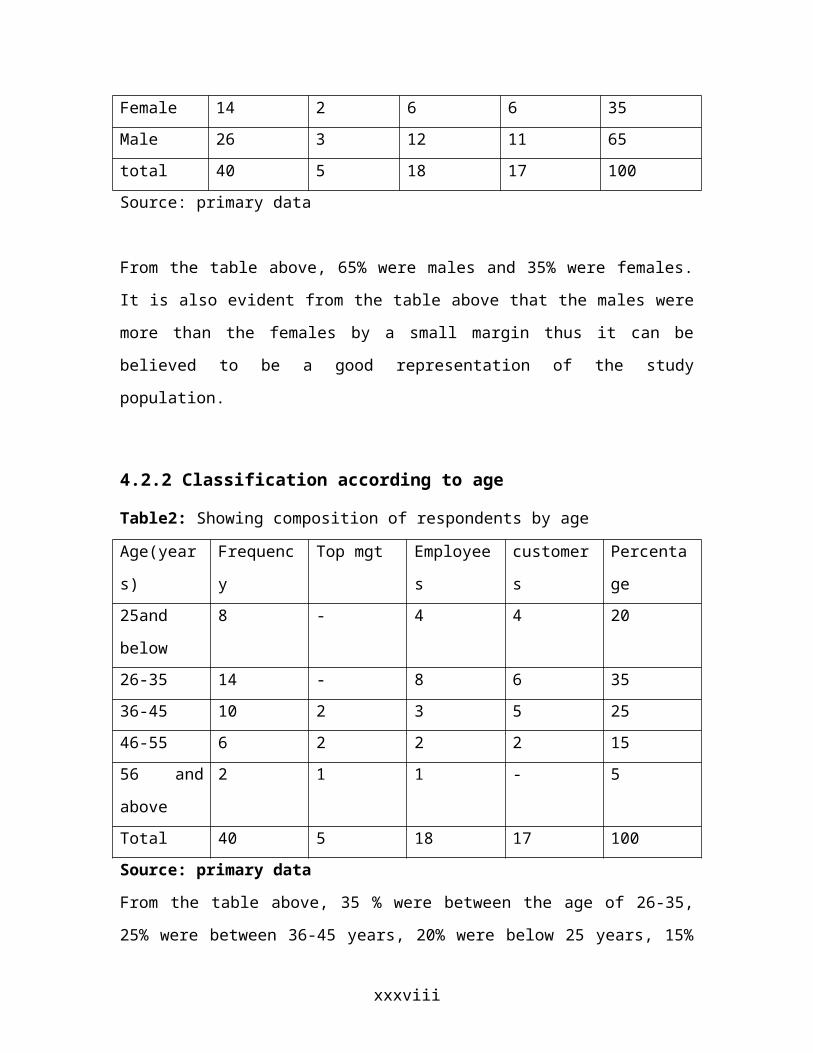

Table 1: showing composition of respondents by gender.

sex frequency Top mgt employees customers percentage

Female 14 2 6 6 35

Male 26 3 12 11 65

total 40 5 18 17 100

Source: primary data

From the table above, 65% were males and 35% were females. It is also evident from the

table above that the males were more than the females by a small margin thus it can be

believed to be a good representation of the study population.

xxvii

4.2.2 Classification according to age

Table2: Showing composition of respondents by age

Age(years) Frequency Top mgt Employees customers Percentage

25and below 8 - 4 4 20

26-35 14 - 8 6 35

36-45 10 2 3 5 25

46-55 6 2 2 2 15

56 and

above

2 1 1 - 5

Total 40 5 18 17 100

Source: primary data

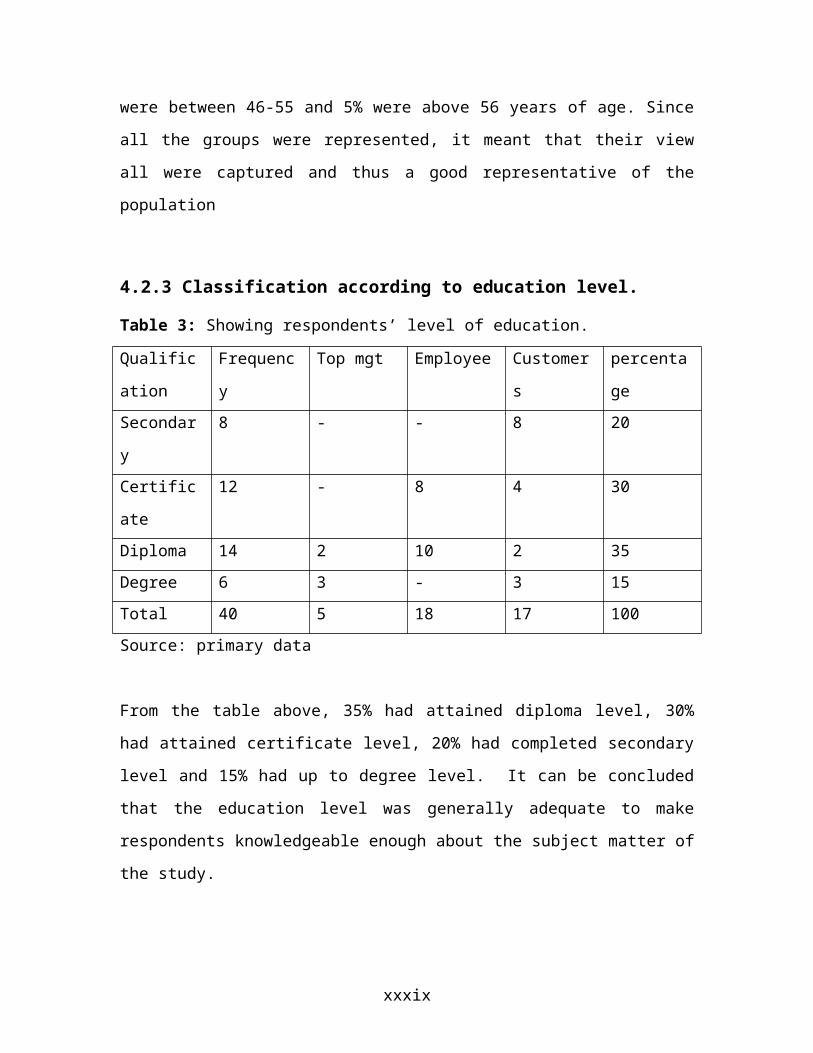

From the table above, 35 % were between the age of 26-35, 25% were between 36-45

years, 20% were below 25 years, 15% were between 46-55 and 5% were above 56 years

of age. Since all the groups were represented, it meant that their view all were captured

and thus a good representative of the population

4.2.3 Classification according to education level.

Table 3: Showing respondents’ level of education.

Qualification Frequency Top mgt Employee Customers percentage

Secondary 8 - - 8 20

Certificate 12 - 8 4 30

Diploma 14 2 10 2 35

Degree 6 3 - 3 15

Total 40 5 18 17 100

Source: primary data

From the table above, 35% had attained diploma level, 30% had attained certificate level,

20% had completed secondary level and 15% had up to degree level. It can be concluded

that the education level was generally adequate to make respondents knowledgeable

enough about the subject matter of the study.

xxviii

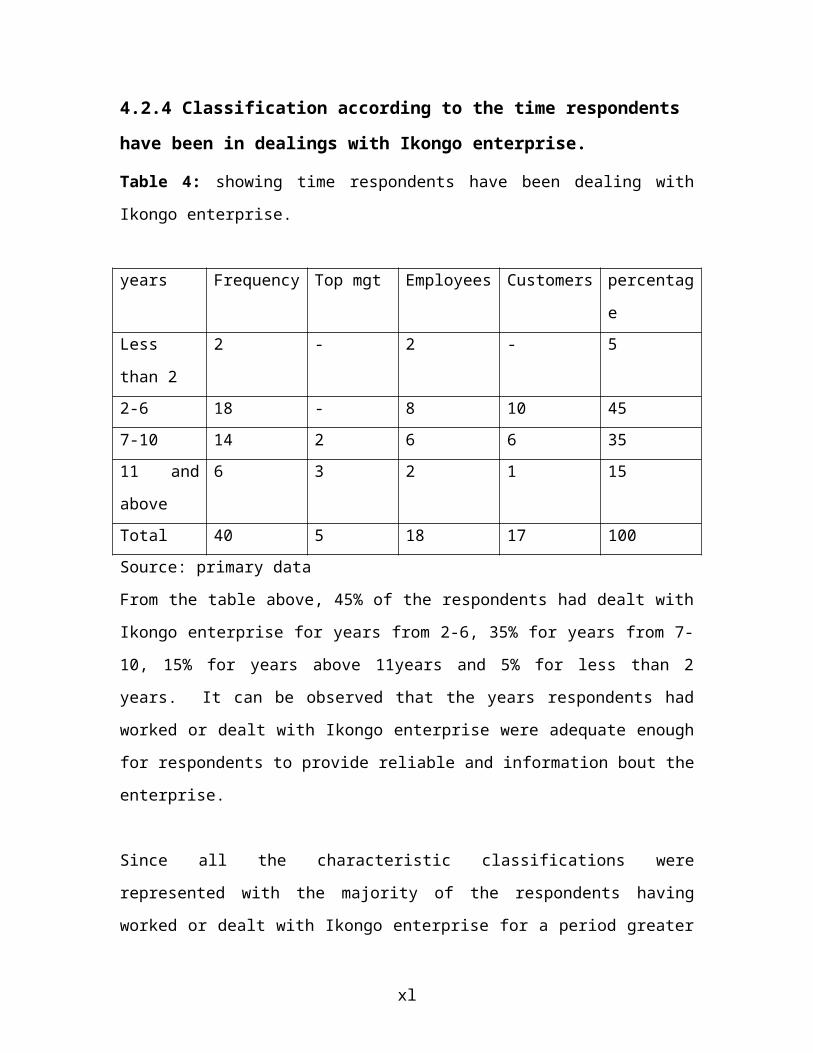

4.2.4 Classification according to the time respondents have been in dealings

with Ikongo enterprise.

Table 4: showing time respondents have been dealing with Ikongo enterprise.

years Frequency Top mgt Employees Customers percentage

Less than 2 2 - 2 - 5

2-6 18 - 8 10 45

7-10 14 2 6 6 35

11 and

above

6 3 2 1 15

Total 40 5 18 17 100

Source: primary data

From the table above, 45% of the respondents had dealt with Ikongo enterprise for years

from 2-6, 35% for years from 7-10, 15% for years above 11years and 5% for less than 2

years. It can be observed that the years respondents had worked or dealt with Ikongo

enterprise were adequate enough for respondents to provide reliable and information bout

the enterprise.

Since all the characteristic classifications were represented with the majority of the

respondents having worked or dealt with Ikongo enterprise for a period greater than 2

years the information obtained was believed to be reliable.

4.3.0 Finding on accounts receivables management.

The study sought to establish whether the enterprise had receivables management policy

and the following were the findings.

xxix

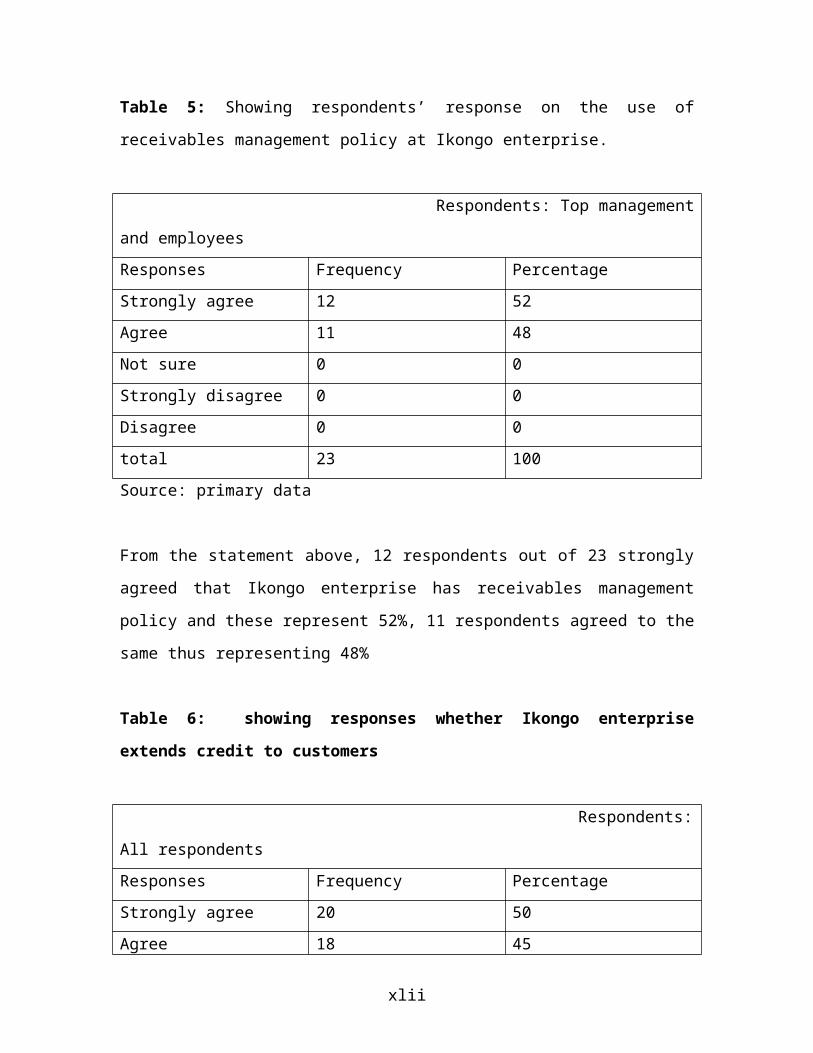

Table 5: Showing respondents’ response on the use of receivables management policy at

Ikongo enterprise.

Respondents: Top management and employees

Responses Frequency Percentage

Strongly agree 12 52

Agree 11 48

Not sure 0 0

Strongly disagree 0 0

Disagree 0 0

total 23 100

Source: primary data

From the statement above, 12 respondents out of 23 strongly agreed that Ikongo

enterprise has receivables management policy and these represent 52%, 11 respondents

agreed to the same thus representing 48%

Table 6: showing responses whether Ikongo enterprise extends credit to customers

Respondents: All respondents

Responses Frequency Percentage

Strongly agree 20 50

Agree 18 45

Not sure 2 5

Strongly disagree 0 0

Disagree 0 0

total 40 100

Source: primary data

From table above, 50% were in strong agreement to the fact that Ikongo enterprise gives

credit to customers, 45% agreed to the same and 5% were not sure if the enterprise gives

xxx

credit to customers. It could be true that those who strongly agreed or agreed might have

got or not got credit from the enterprise but they are aware of credit extension in Ikongo

enterprise. Also it could be concluded that the 5% had not got any credit from the

enterprise and therefore are not sure whether or not the enterprise gives credit.

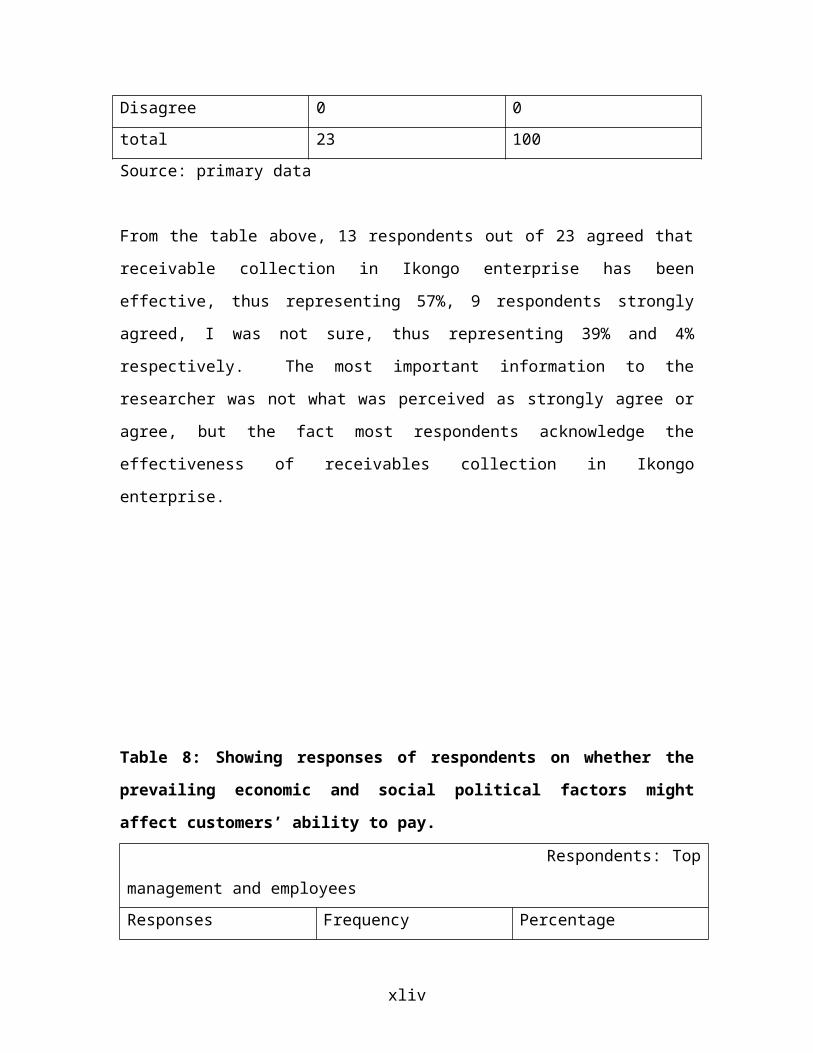

Table 7: Showing response on the effectiveness of accounts receivables collection in

Ikongo enterprise.

Respondents: Top management and employees

Responses Frequency Percentage

Strongly agree 9 39

Agree 13 57

Not sure 1 4

Strongly disagree 0 0

Disagree 0 0

total 23 100

Source: primary data

From the table above, 13 respondents out of 23 agreed that receivable collection in

Ikongo enterprise has been effective, thus representing 57%, 9 respondents strongly

agreed, I was not sure, thus representing 39% and 4% respectively. The most important

information to the researcher was not what was perceived as strongly agree or agree, but

the fact most respondents acknowledge the effectiveness of receivables collection in

Ikongo enterprise.

xxxi

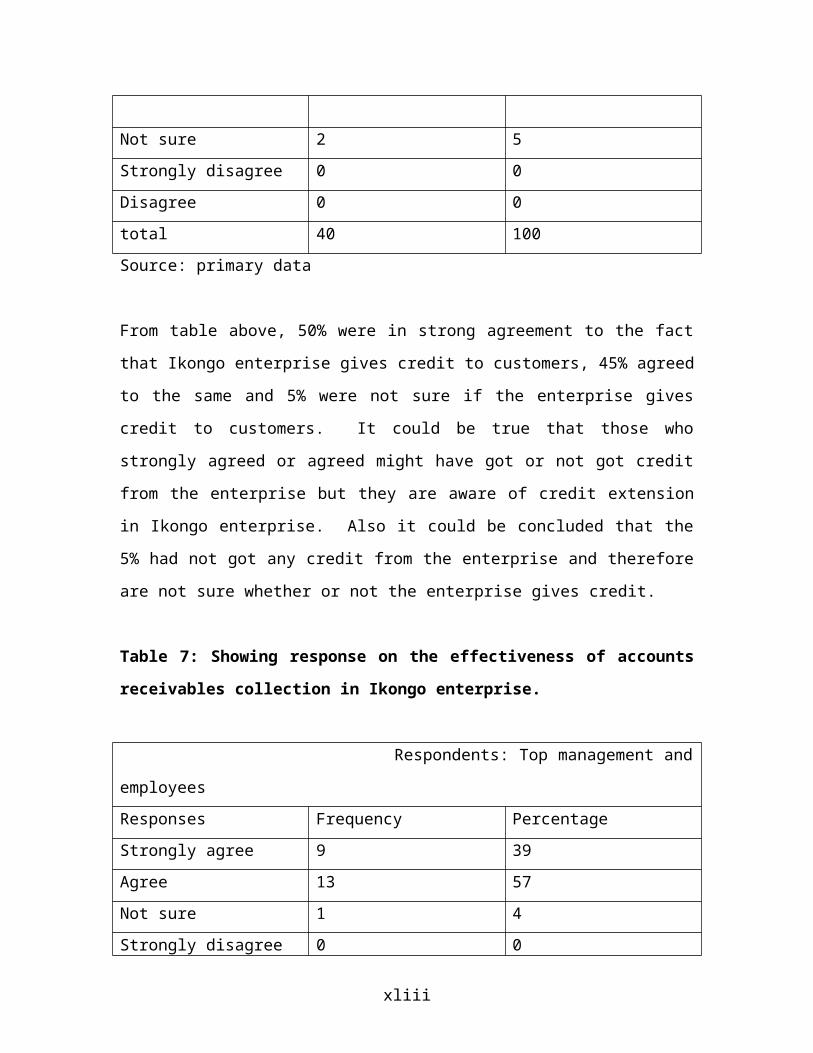

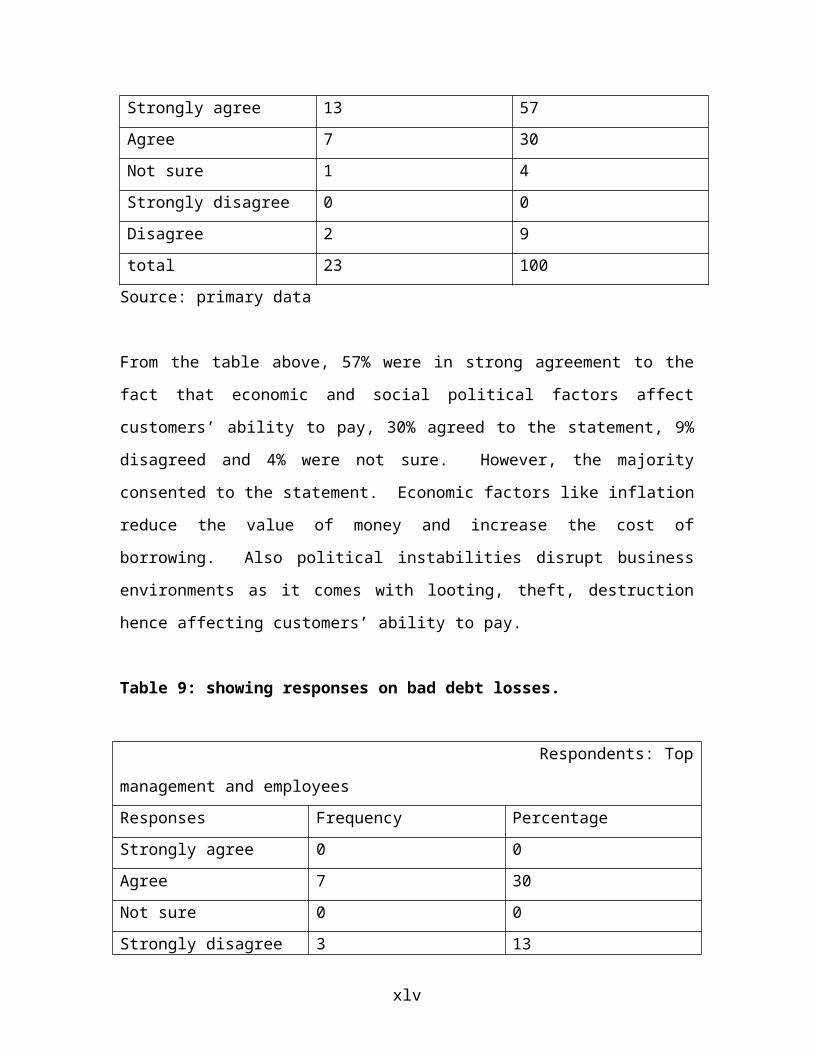

Table 8: Showing responses of respondents on whether the prevailing economic and

social political factors might affect customers’ ability to pay.

Respondents: Top management and employees

Responses Frequency Percentage

Strongly agree 13 57

Agree 7 30

Not sure 1 4

Strongly disagree 0 0

Disagree 2 9

total 23 100

Source: primary data

From the table above, 57% were in strong agreement to the fact that economic and social

political factors affect customers’ ability to pay, 30% agreed to the statement, 9%

disagreed and 4% were not sure. However, the majority consented to the statement.

Economic factors like inflation reduce the value of money and increase the cost of

borrowing. Also political instabilities disrupt business environments as it comes with

looting, theft, destruction hence affecting customers’ ability to pay.

Table 9: showing responses on bad debt losses.

Respondents: Top management and employees

Responses Frequency Percentage

Strongly agree 0 0

Agree 7 30

Not sure 0 0

Strongly disagree 3 13

Disagree 13 57

total 23 100

Source: primary data

xxxii

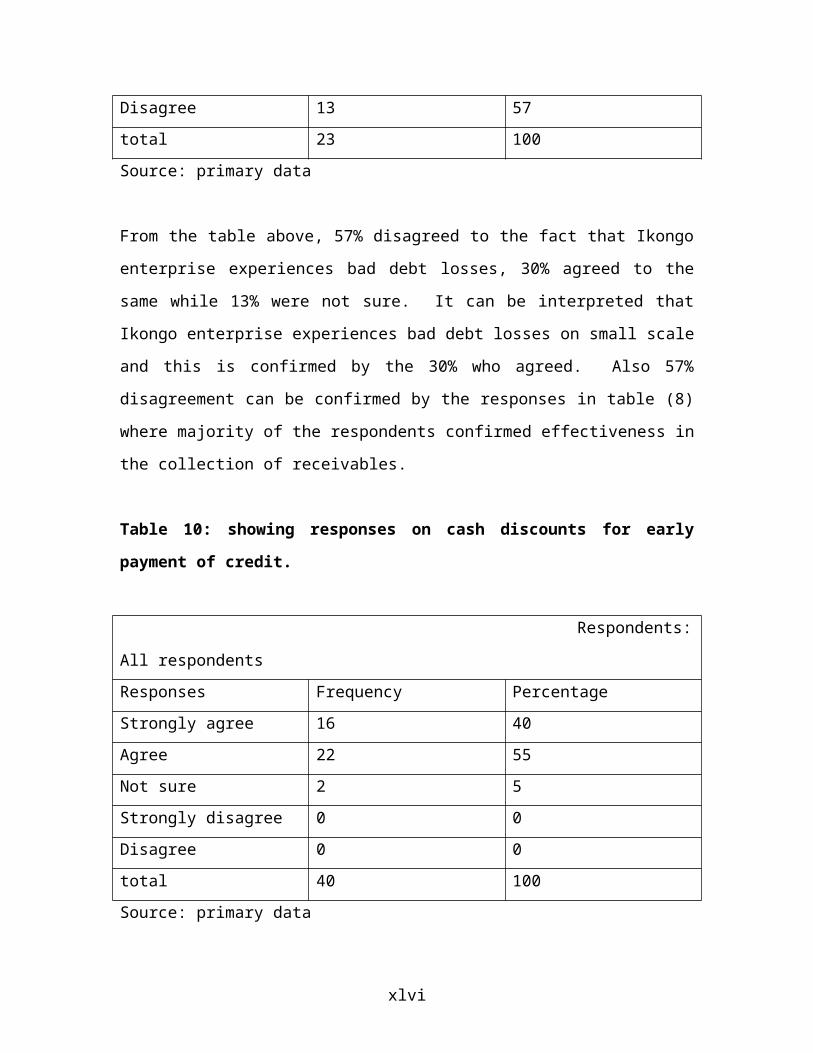

From the table above, 57% disagreed to the fact that Ikongo enterprise experiences bad

debt losses, 30% agreed to the same while 13% were not sure. It can be interpreted that

Ikongo enterprise experiences bad debt losses on small scale and this is confirmed by the

30% who agreed. Also 57% disagreement can be confirmed by the responses in table (8)

where majority of the respondents confirmed effectiveness in the collection of

receivables.

Table 10: showing responses on cash discounts for early payment of credit.

Respondents: All respondents

Responses Frequency Percentage

Strongly agree 16 40

Agree 22 55

Not sure 2 5

Strongly disagree 0 0

Disagree 0 0

total 40 100

Source: primary data

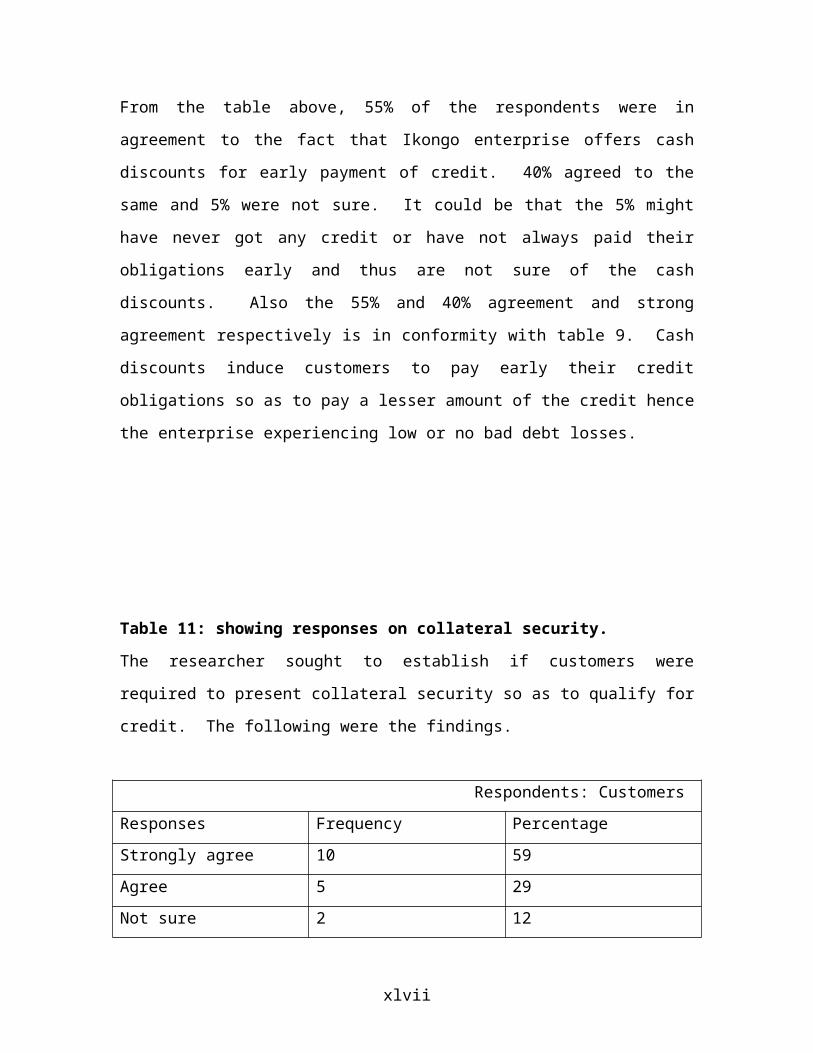

From the table above, 55% of the respondents were in agreement to the fact that Ikongo

enterprise offers cash discounts for early payment of credit. 40% agreed to the same and

5% were not sure. It could be that the 5% might have never got any credit or have not

always paid their obligations early and thus are not sure of the cash discounts. Also the

55% and 40% agreement and strong agreement respectively is in conformity with table 9.

Cash discounts induce customers to pay early their credit obligations so as to pay a lesser

amount of the credit hence the enterprise experiencing low or no bad debt losses.

xxxiii

Table 11: showing responses on collateral security.

The researcher sought to establish if customers were required to present collateral

security so as to qualify for credit. The following were the findings.

Respondents: Customers

Responses Frequency Percentage

Strongly agree 10 59

Agree 5 29

Not sure 2 12

Strongly disagree 0 0

Disagree 0 0

total 17 100

Source: primary data

From the table above, 59% were in strong agreement to the statement that Ikongo

enterprise requires collateral security before credit is extended, 29% agreed and 12%

were not sure. It can be said that the 12% who were not sure might have never got any

credit from the enterprise

xxxiv

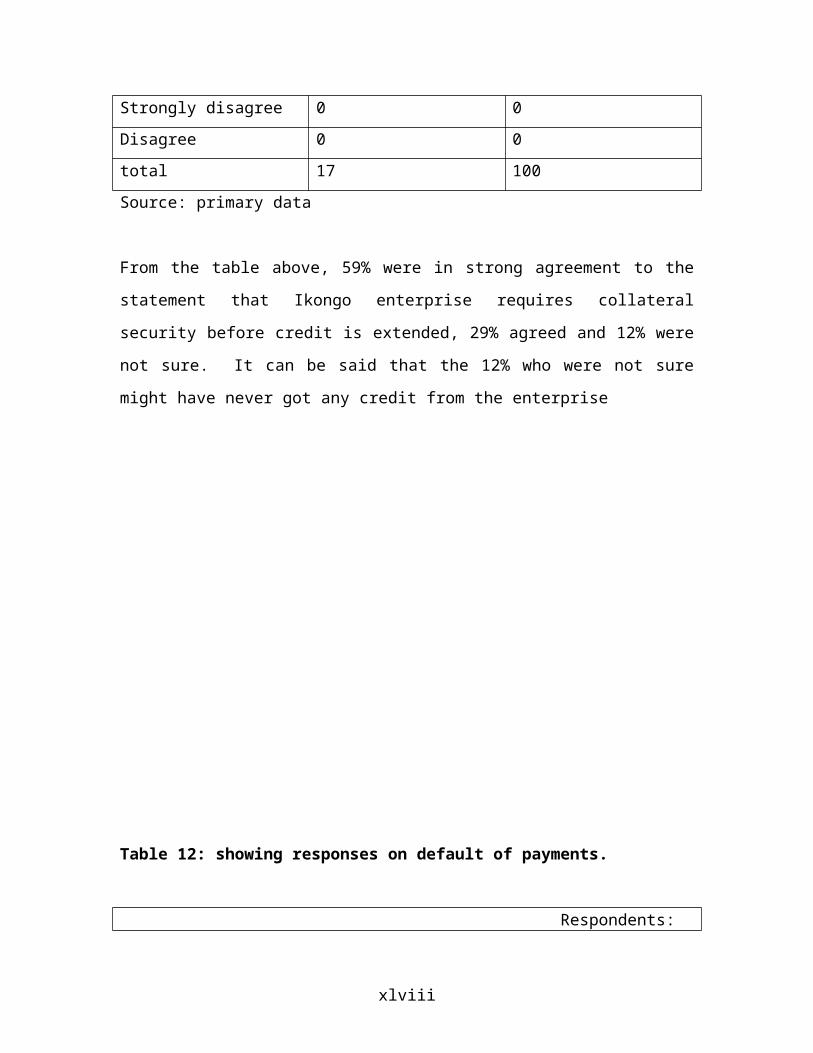

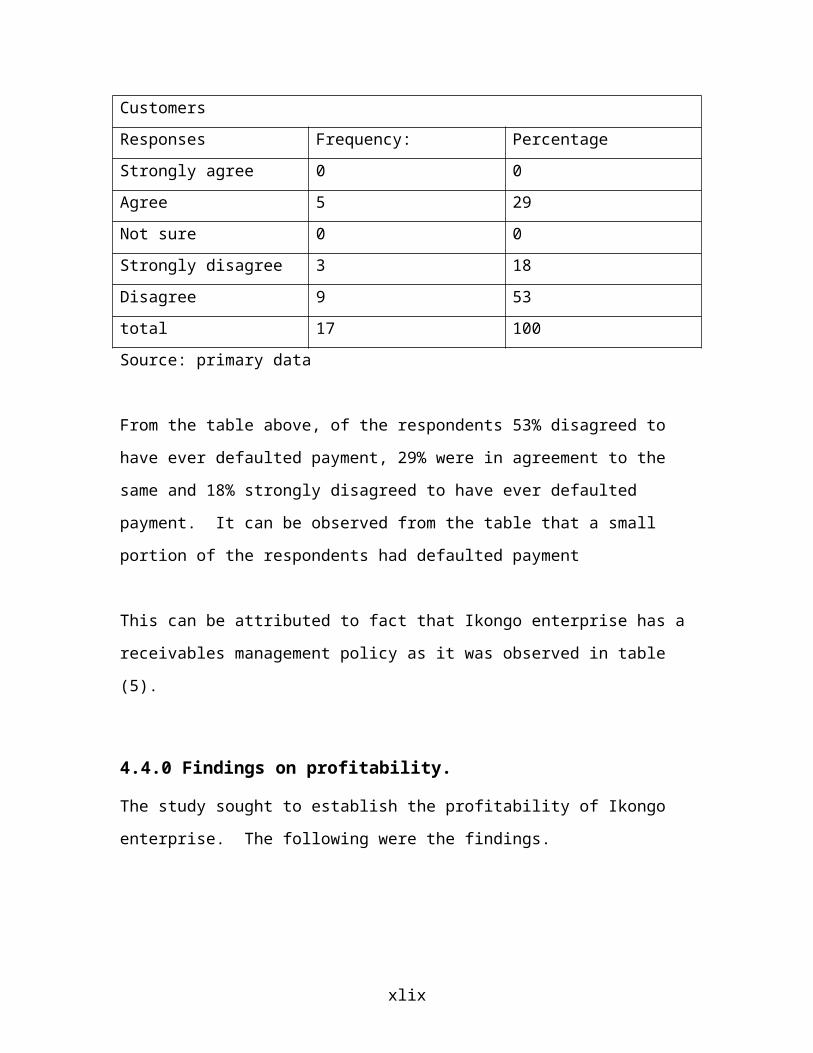

Table 12: showing responses on default of payments.

Respondents: Customers

Responses Frequency: Percentage

Strongly agree 0 0

Agree 5 29

Not sure 0 0

Strongly disagree 3 18

Disagree 9 53

total 17 100

Source: primary data

From the table above, of the respondents 53% disagreed to have ever defaulted payment,

29% were in agreement to the same and 18% strongly disagreed to have ever defaulted

payment. It can be observed from the table that a small portion of the respondents had

defaulted payment

This can be attributed to fact that Ikongo enterprise has a receivables management policy

as it was observed in table (5).

4.4.0 Findings on profitability.

The study sought to establish the profitability of Ikongo enterprise. The following were

the findings.

xxxv

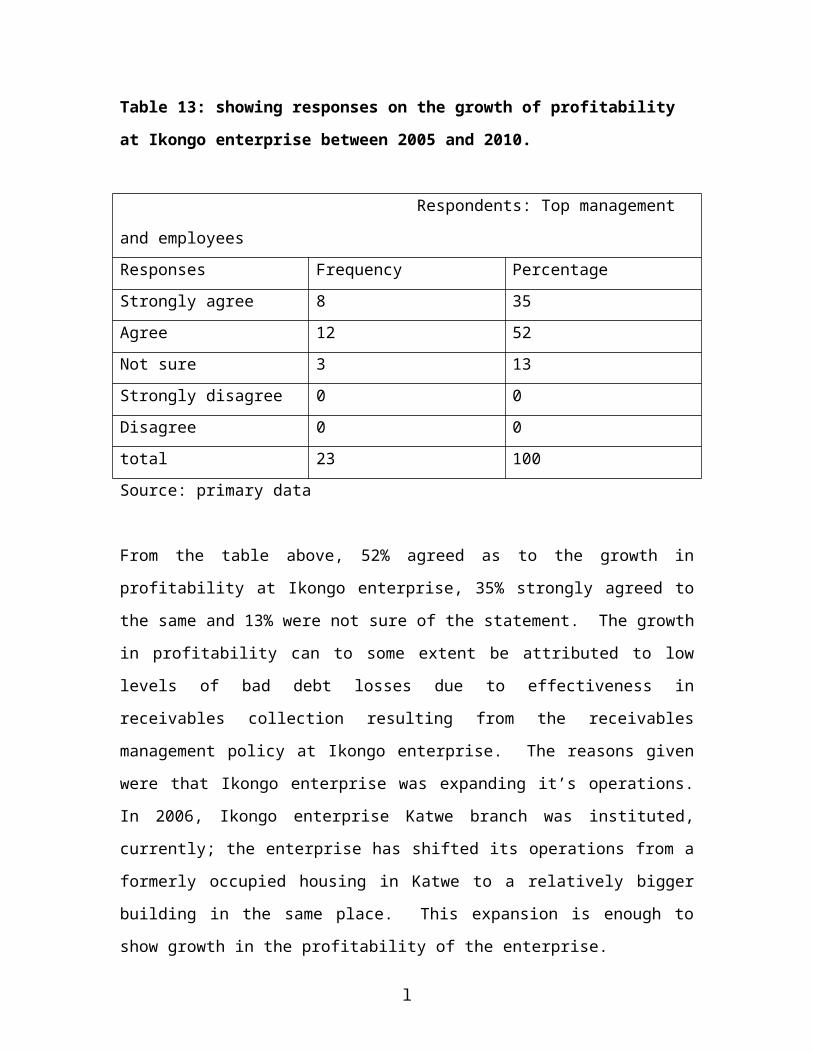

Table 13: showing responses on the growth of profitability at Ikongo enterprise

between 2005 and 2010.

Respondents: Top management and employees

Responses Frequency Percentage

Strongly agree 8 35

Agree 12 52

Not sure 3 13

Strongly disagree 0 0

Disagree 0 0

total 23 100

Source: primary data

From the table above, 52% agreed as to the growth in profitability at Ikongo enterprise,

35% strongly agreed to the same and 13% were not sure of the statement. The growth in

profitability can to some extent be attributed to low levels of bad debt losses due to

effectiveness in receivables collection resulting from the receivables management policy

at Ikongo enterprise. The reasons given were that Ikongo enterprise was expanding it’s

operations. In 2006, Ikongo enterprise Katwe branch was instituted, currently; the

enterprise has shifted its operations from a formerly occupied housing in Katwe to a

relatively bigger building in the same place. This expansion is enough to show growth in

the profitability of the enterprise.

xxxvi

Table 14: showing the ratio of bad debts to profitability (Net profit).

Year Profitability

(Shs000)

Bad debts

(Shs000)

percentage

2005 90,869 80,60 8.9

2006 94,200 78,49 8.3

2007 96,540 75,50 7.8

2008 99,800 75,20 7.5

2009 104,860 70,58 6.7

2010 116,496 68,26 5.8

Source: Secondary data

From the table above, it is observed that there is growth of profitability and reduction in

bad debts every year. The growth in profitability can be attributed to the reduction in

bad debt losses coupled with other factors like increase in market share, reduction in

operational costs, economic of expansion (economies of large scale operations), and

e.t.c. The reduction in bad debts can also be attributed to the receivables management

policy at Ikongo enterprise. Every year that goes, the enterprise gain experience and

revises the management of its accounts receivables, improves collection methods, and

introduces new ways to improving credit recovery. It could be true that in the early

years, the enterprise had no a receivables management policy that could guarantee

effective recovery of receivables leading to a reduction in bad debts like in the later years.

The optimal receivables management policy ensures that credit is extended for lesser

periods such that money that would be used for expansion and investment in productive

activities is not tied up in credit.

4.5.0 Finding on the relationship between accounts receivables management

and profitability.

The study sought to establish if there was any relationship between receivables

management and profitability.

From the findings, it was established that a flexible or lenient receivables management

policy leads to increase in the level of credit extended; increase in credit involves

xxxvii

additional costs and increased bad debt losses thus limiting profitability. Also a stringent

receivables management policy means that credit is extended to customers whose credit

worthiness has been ascertained thus reduces bad debt losses hence increasing the

profitability levels of the firm. Therefore the profitability levels of any firm will vary

depending on the receivables management policy adopted by that particular firm.

Table 15: Calculation of the relationship between accounts receivables management

and profitability using Pearson product moment correlation coefficient

Respondents: Top management and employees

Response Receivables

Management

(x)

Profitability

(y)

X2 Y2 xy

Strongly

agree 8 16 9 12

Agree 11 12 256 225 240

Not sure 0 3 9 4 6

Strongly

agree

0 0 0 0 0

Disagree 0 0 0 9 0

Total 23 23 281 247 258

Source: primary data

xxxviii

The relationship between accounts receivables management and profitability using

product moment correlation coefficient ® is given by;

r = ∩ ε x y - ε x ε y

√ [∩ε x2 – (ε x) 2] [ε y2 – (ε x) 2]

Where;

r = Pearson’s product moment correlation coefficient

ε = Summation

∩ = Number of observations

x = number of respondents (independent variable i.e receivables management)

y = number of respondents (dependent variable i,e profitability)

√ = Square root

r = (23 x 228) - ( 23 x 23)

√ [(23 x 265) – (23)2] [(23x 208) – (23)2]

r = 5244 - 529

√ [(6095 - 529)] [(4784 - 529)]

r = 4715

√ [5566] [4255]

r = 4715

xxxix

√ 2368330

r = 4715

4866.55

r = 0.968 ~ 0.97

xl

CHAPTER FIVE

5.0 Introduction.

This chapter presents the summary of finding, conclusion and recommendations derived

from the findings.

5.2.0 Summary of findings

5.2.1 Accounts receivables management

It was established that Ikongo enterprise has a receivables management policy. Most of

the respondents strongly agreed or agreed to the same. This is true as it is in conformity

with the previous studies carried out on the same topic.

5.2.2 Profitability

It was further established that between 2005 and 2010, the enterprise’s profitability was

improving. The indicators of improvement in profitability were expansion of operations

renovations of the existing facilities e.g. extension of Katwe branch. Improvement in

profitability was to some extent attributed to the use of receivables management policy

which ensures optimal investment in accounts receivables and thus minimizing bad debt

losses.

5.2.3 Relationship between accounts receivables management and

profitability

It was found out that the relationship between receivables management and profitability

was very strong with a correlation coefficient (r) of 0.97. Thus the profitability of a firm

will vary depending on the receivables management policy adopted by the particular

firm.

xli

5.3.0 Conclusion

From the finding it can be concluded that Ikongo enterprise uses a stringent receivables

management policy. The way receivables are managed profoundly affects profitability.

The researcher emphasizes that receivables constitute a significant portion of the firm’s

current assets and thus should be managed properly.

5.4 Recommendations

After analyzing the findings and found out the relationship between receivables

management and profitability, the researcher made the following findings.

In the management of receivables, credit worthiness of customers should be assessed.

The costs and risks of maintaining any credit customer should be matched with the

returns from such a customer.

Credit rating should be emphasized and adopted, such that if the probability of a

particular customer to default is high, the customer can be denied credit. Rational

decisions should be whether to or not to trade with a customer to who credit risk has been

attached.

There should be adequate work force in the credit control department so as to make fast

the process of credit collections.

The enterprise should adopt a credit policy that is compatible with other policy decisions

e.g dividend policy, investment decisions and at the same time maximizes the expected

profits.

5.5 Suggested areas for further researchers.

Further researcher should be conducted in the following areas

i. Receivables management and customer retention.

ii. Customer turnover and profitability.

iii. Receivables management and liquidity position.

xlii

REFERENCES

1. ACCA,(2009), ), Financial Management, BPP learning media

2. ACCA,(2009), Financial Reporting, BPP learning media

3. Brealey, Richard (1988), principles of corporate finance, New York: Mcgraw-hill

4. Brockington, Raymond (1993), Financial Management. London DP

PUBLICATION.

5. Dickerson (1995), 4th edition, Harcourt Brace college publisher’s.

6. Foulks lynch (2005). Financial management and control, the official professional

text, FTC fouls lynch publications, London.

7. Kakuru Julius (2000). Financial Decisions and the business(1st edition). The

business publishing group Kampala

8. Kakuru Julius (2001). Financial Decisions and the business (2nd edition). The

business publishing group Kampala

9. MC. Naughton, D (1996). Banking institutions in developing markets, building a

strong management and responding to change. Vol.1. world Bank.

10. Mutenyo,(2007), Introduction to micro economics (1st edition). The New vision

printing and publishing company Ltd

11. Pandey 1 . M (2003) Financial management (7th Edition) Aima Vikas publishing

house, pvt ltd London

12. Pandey 1.M (2003) Financial management (8th edition) Aim Vikas publishing

house (pvt) Ltd London.

13. Samuels, J.m (1993), Management of company finance, London: New York,

Chapman and hall.

14. Stoner, James A.F (1996), Management. New Delhi: Prentice hall of India

xliii

APPENDICES

APPENDIX I: questionnaire to the management and employees of Ikongo

enterprise

Dear respondent,

The researcher is a bachelor of commerce student of Makerere University, conducting an

academic study under the topic “Management of accounts receivables and profitability”.

The research is not meant for any other reason other than for academic purposes i.e for

the fulfillment of the awards of bachelor of commerce degree. It is only through your

participation that the study can be completed.

You are therefore requested to allocate little time to answer the following questions. Be

assured that each individual response will be treated with due confidentiality.

Thank you.

PERSONAL BACKGROUND INFORMATION

Tick where applicable or fill the space below.

General information.

1a) sex

i) Female ii) Male

b) Age

i) 25 years and below ii) 26 -35 years

iii) 36 – 45 years ii) 46 – 55years v) Above 56 years

c) Education level

i) Certificate ii) Diploma iii) Degree iv) Post graduate

d) Years worked in Ikongo enterprise

i) Less than 2 years ii) 2-6 years iii) 7- 10year

iv) 11years and above

xliv

2. Receivable management (Please tick where appropriate)

Strongly

agree

Agree Not sure Strongly

disagree

Disagree

Ikongo enterprise

gives credit to

customers

The enterprise has

receivables

management policy

that is used to select

customers

The enterprise

experiences bad debt

losses

The prevailing

economic and social-

political factors may

affect customer ability

to pay.

Receivables collection

in Ikongo enterprise

has been effective

The credit control

department

xlv

Collects and receives

payments.

The enterprise offers

cash discounts for

early payment of

credit.

3. Profitability ( Please tick where appropriate)

Strongly

Agree

Agree Not sure Strongly

disagree

Disagree

Profitability of

Ikongo enterprise

has been growing

between 2005 and

2010

Receivables

management policy

has an effect on

profitability

A customer failure

to pay back their

credit effects

profitability

Ikongo enterprise

usually faces

liquidity problems.

xlvi

APPENDIX II Questionnaire to the customers of Ikongo enterprise.

Dear respondent,

The researcher is a bachelor of commerce student of Makerere University conducting an

academic study under the topic “ Management of accounts receivables and profitability”.

The research is not meant for you other reasons other than for academic purpose i.e. for

the fulfillment of the award of the award of the degree of Bachelor of commerce. It is

only through your participation that the research study can be completed.

You are therefore requested to allocate a little of your time to answer the following

questions. Be assured that all responses will be treated with utmost confidentiality.

Thank you.

Personal background information.

Tick where applicable

1. What is your sex?

i) Male ii) Female

2. What is your marital status?

i) Single ii) Married

3.What is your age?

i) 25 years and below ii) 26 -35 years

iii) 36 – 45 years ii) 46 – 55years v) Above 56 years

4. What are your academic qualifications?

i) Secondary level ii) Certificate iii) Diploma v) Degree

Others

5a) Are you in business?

i) Yes ii) No

xlvii

b) If yes how long have been in business?

6. How long have you been dealing with Ikongo enterprise

i) Less than 2 years ii) 2 -6 years iii) 7years and above

7.

Strongly

agree

Agree Not sure Strongly

disagree

Disagree

You ask for

credit from

Ikongo

enterprise.

You present

collateral to

qualify for

credit

You have

ever

defaulted

payment of

your credit

obligation.

Credit

extension in

xlviii

Ikongo

enterprise. Is

rigorous/

stringent.

Discounts for

prompt

payment

improve

credit

collection.

xlix

l