Embed Size (px)

Citation preview

BBAV - Semester

104 52

Directorate of Distance Education

MANAGEMENT ACCOUNTING

ALAGAPPA UNIVERSITY[Accredited with ‘A+’ Grade by NAAC (CGPA:3.64) in the Third Cycle

and Graded as Category–I University by MHRD-UGC]

(A State University Established by the Government of Tamil Nadu)

KARAIKUDI – 630 003

All rights reserved. No part of this publication which is material protected by this copyright notice may be reproduced or transmitted or utilized or stored in any form or by any means now known or hereinafter invented, electronic, digital or mechanical, including photocopying, scanning, recording or by any information storage or retrieval system, without prior written permission from the Alagappa University, Karaikudi, Tamil Nadu.

Information contained in this book has been published by VIKAS® Publishing House Pvt. Ltd. and has been obtained by its Authors from sources believed to be reliable and are correct to the best of their knowledge. However, the Alagappa University, Publisher and its Authors shall in no event be liable for any errors, omissions or damages arising out of use of this information and specifically disclaim any implied warranties or merchantability or fitness for any particular use.

Vikas® is the registered trademark of Vikas® Publishing House Pvt. Ltd.

VIKAS® PUBLISHING HOUSE PVT. LTD.E-28, Sector-8, Noida - 201301 (UP)Phone: 0120-4078900 • Fax: 0120-4078999Regd. Office: A-27, 2nd Floor, Mohan Co-operative Industrial Estate, New Delhi 1100 44• Website: www.vikaspublishing.com • Email: [email protected]

Work Order No.AU/DDE/DE12-27/Preparation and Printing of Course Materials/2020 Dated 12.08.2020 Copies 600

“The copyright shall be vested with Alagappa University”

AuthorsM A Sahaf, Professor, The Business School University of Kashmir, SrinagarUnits (1-13) Dr Bhavesh M Patel, Director, Post Graduate Institute of Management and Dean, Amrut Mody School of Management Ahmedabad University, Gujarat Unit (14)

Reviewer Dr. G. Nedumaran Professor of Commerce,

Alagappa University, Karaikudi, Tamil Nadu.

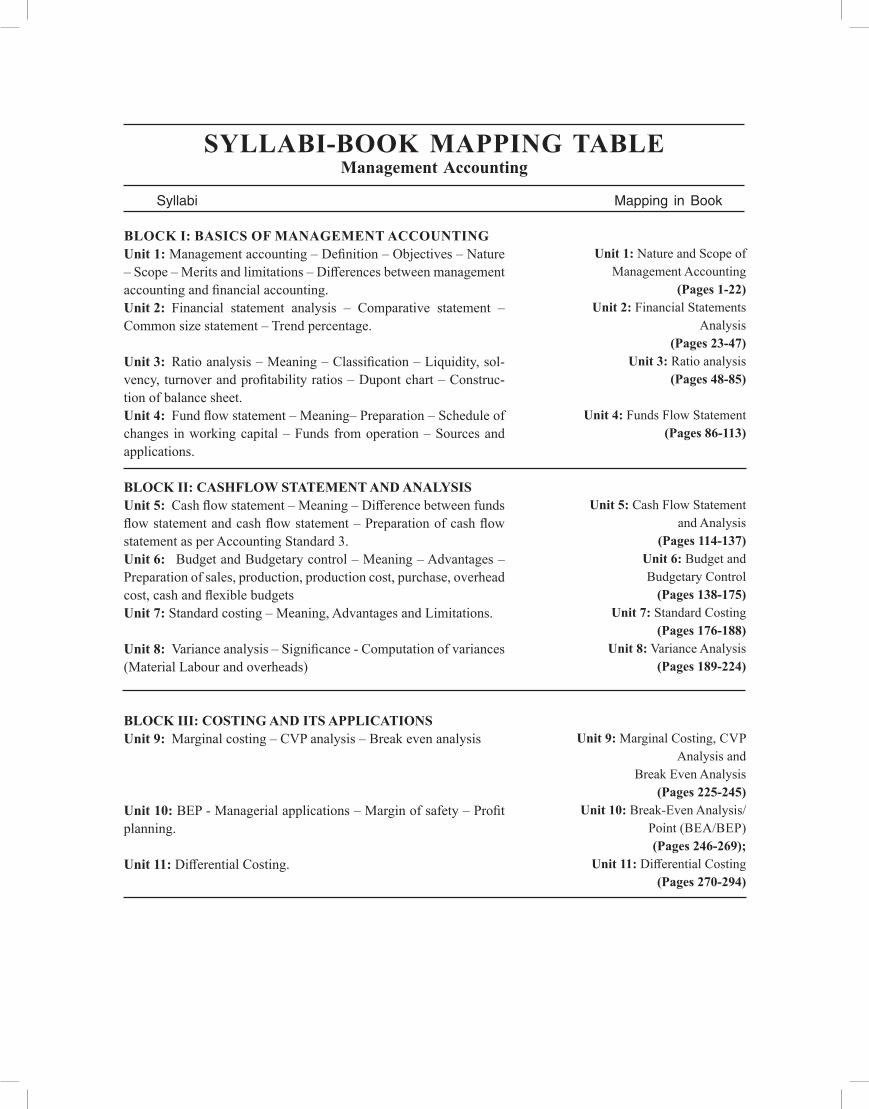

SYLLABI-BOOK MAPPING TABLE Management Accounting

BLOCK I: BASICS OF MANAGEMENT ACCOUNTINGUnit 1: Management accounting – Definition – Objectives – Nature – Scope – Merits and limitations – Differences between management accounting and financial accounting. Unit 2: Financial statement analysis – Comparative statement – Common size statement – Trend percentage.

Unit 3: Ratio analysis – Meaning – Classification – Liquidity, sol-vency, turnover and profitability ratios – Dupont chart – Construc-tion of balance sheet.Unit 4: Fund flow statement – Meaning– Preparation – Schedule of changes in working capital – Funds from operation – Sources and applications.

BLOCK II: CASHFLOW STATEMENT AND ANALYSISUnit 5: Cash flow statement – Meaning – Difference between funds flow statement and cash flow statement – Preparation of cash flow statement as per Accounting Standard 3.Unit 6: Budget and Budgetary control – Meaning – Advantages – Preparation of sales, production, production cost, purchase, overhead cost, cash and flexible budgets Unit 7: Standard costing – Meaning, Advantages and Limitations.

Unit 8: Variance analysis – Significance - Computation of variances (Material Labour and overheads)

BLOCK III: COSTING AND ITS APPLICATIONSUnit 9: Marginal costing – CVP analysis – Break even analysis

Unit 10: BEP - Managerial applications – Margin of safety – Profit planning.

Unit 11: Differential Costing.

Syllabi Mapping in Book

Unit 1: Nature and Scope of Management Accounting

(Pages 1-22)Unit 2: Financial Statements

Analysis (Pages 23-47)

Unit 3: Ratio analysis (Pages 48-85)

Unit 4: Funds Flow Statement (Pages 86-113)

Unit 5: Cash Flow Statement and Analysis

(Pages 114-137)Unit 6: Budget and Budgetary Control

(Pages 138-175)Unit 7: Standard Costing

(Pages 176-188)Unit 8: Variance Analysis

(Pages 189-224)

Unit 9: Marginal Costing, CVP

Analysis and Break Even Analysis

(Pages 225-245)Unit 10: Break-Even Analysis/

Point (BEA/BEP) (Pages 246-269);

Unit 11: Differential Costing (Pages 270-294)

BLOCK IV: METHODS OF CAPITAL BUDGETINGUnit 12: Capital Budgeting – Meaning – Importance – Appraisal methods

Unit 13: Payback period –– Accounting rate of return - Discounted cash flow – Net present value – Profitability index – Internal rate of return.Unit 14: Methods of evaluation of Alternative Capital Expenditure Programme.

Unit 12: Capital Budgeting: Meaning and Importance

(Pages 295-305);Unit 13: Appraisal Methods

(Pages 306-344);

Unit 14: Methods of Evaluation of Alternative Capital

Expenditure Programme (Pages 345-364)

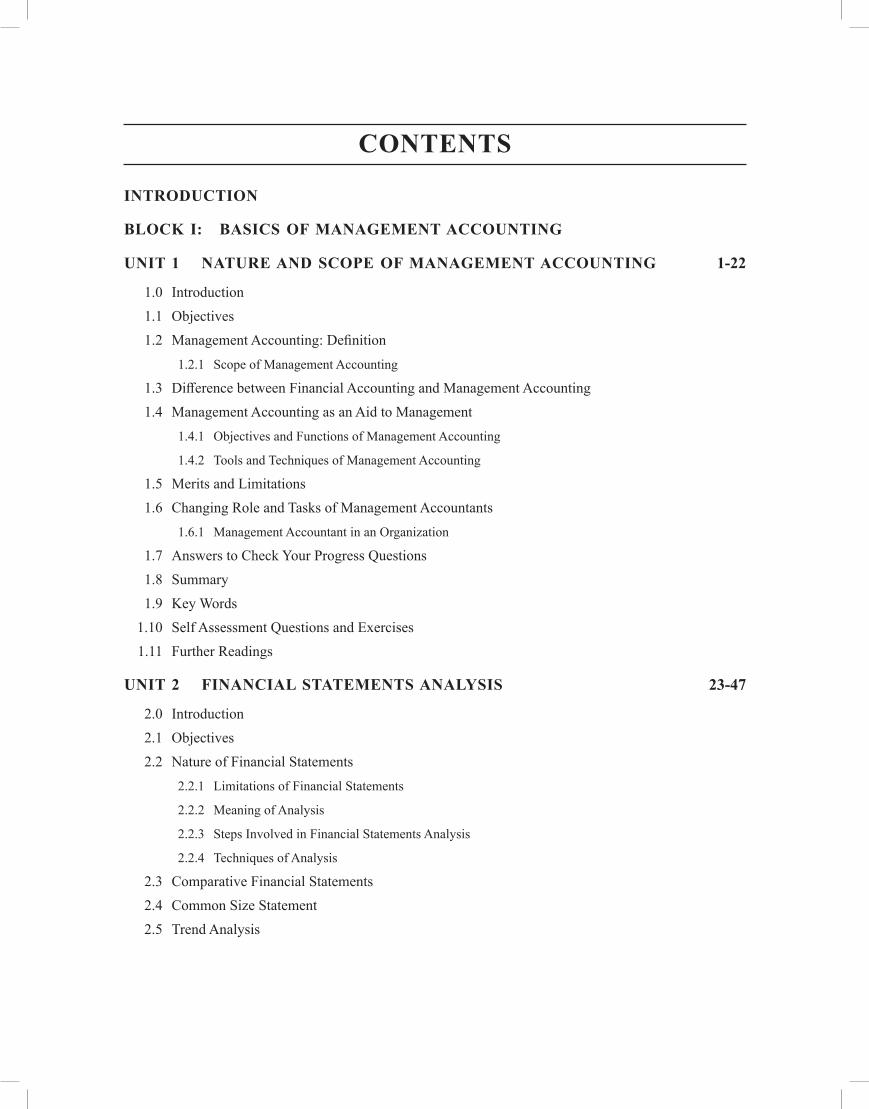

INTRODUCTION

BLOCK I: BASICS OF MANAGEMENT ACCOUNTING

UNIT 1 NATURE AND SCOPE OF MANAGEMENT ACCOUNTING 1-22

1.0 Introduction 1.1 Objectives 1.2 Management Accounting: Definition

1.2.1 Scope of Management Accounting

1.3 Difference between Financial Accounting and Management Accounting 1.4 Management Accounting as an Aid to Management

1.4.1 Objectives and Functions of Management Accounting

1.4.2 Tools and Techniques of Management Accounting

1.5 Merits and Limitations 1.6 Changing Role and Tasks of Management Accountants

1.6.1 Management Accountant in an Organization

1.7 Answers to Check Your Progress Questions 1.8 Summary 1.9 Key Words 1.10 Self Assessment Questions and Exercises 1.11 Further Readings

UNIT 2 FINANCIAL STATEMENTS ANALYSIS 23-47

2.0 Introduction 2.1 Objectives 2.2 Nature of Financial Statements

2.2.1 Limitations of Financial Statements

2.2.2 Meaning of Analysis

2.2.3 Steps Involved in Financial Statements Analysis

2.2.4 Techniques of Analysis

2.3 Comparative Financial Statements 2.4 Common Size Statement 2.5 Trend Analysis

CONTENTS

2.6 Answers to Check Your Progress Questions 2.7 Summary 2.8 Key Words 2.9 Self Assessment questions and Exercises 2.10 Further Readings

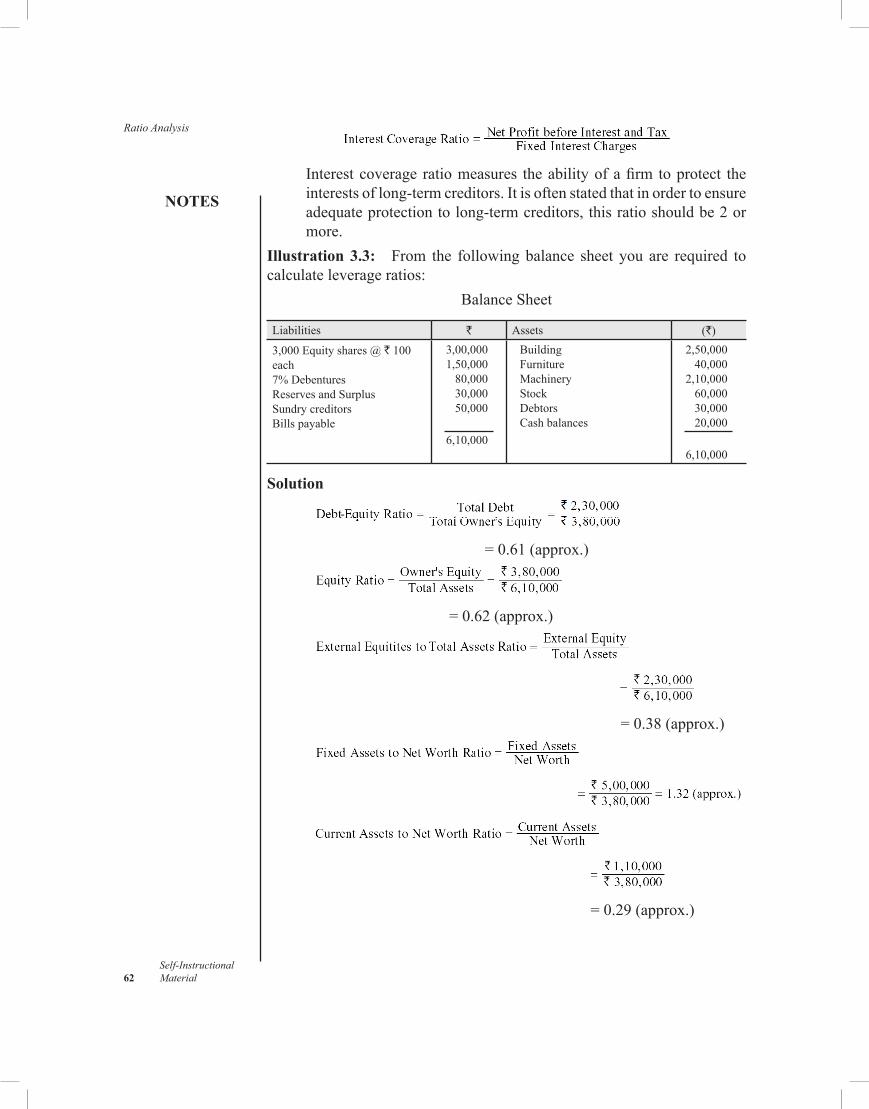

UNIT 3 RATIO ANALYSIS 48-85

3.0 Introduction 3.1 Objectives 3.2 Ratio Analysis: Meaning 3.3 Classification of Ratios

3.3.1 Liquidity Ratios

3.3.2 Leverage or Solvency Ratios

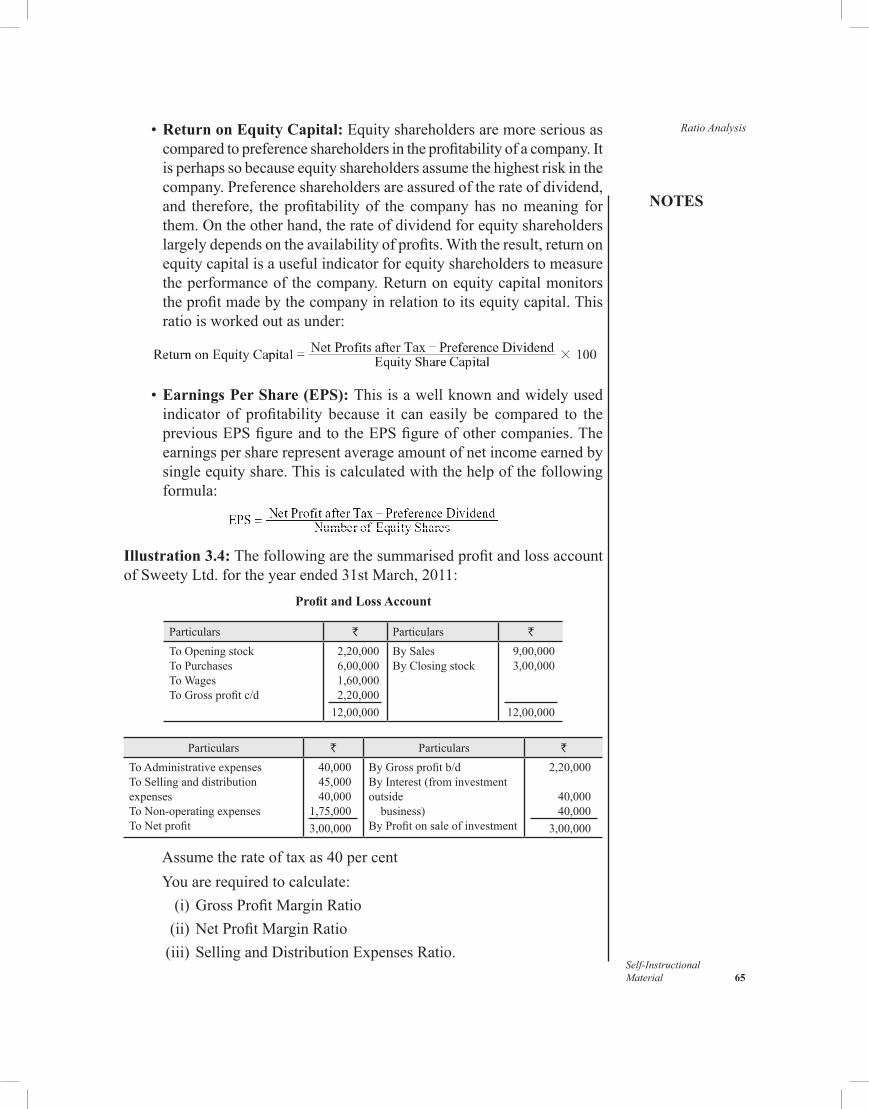

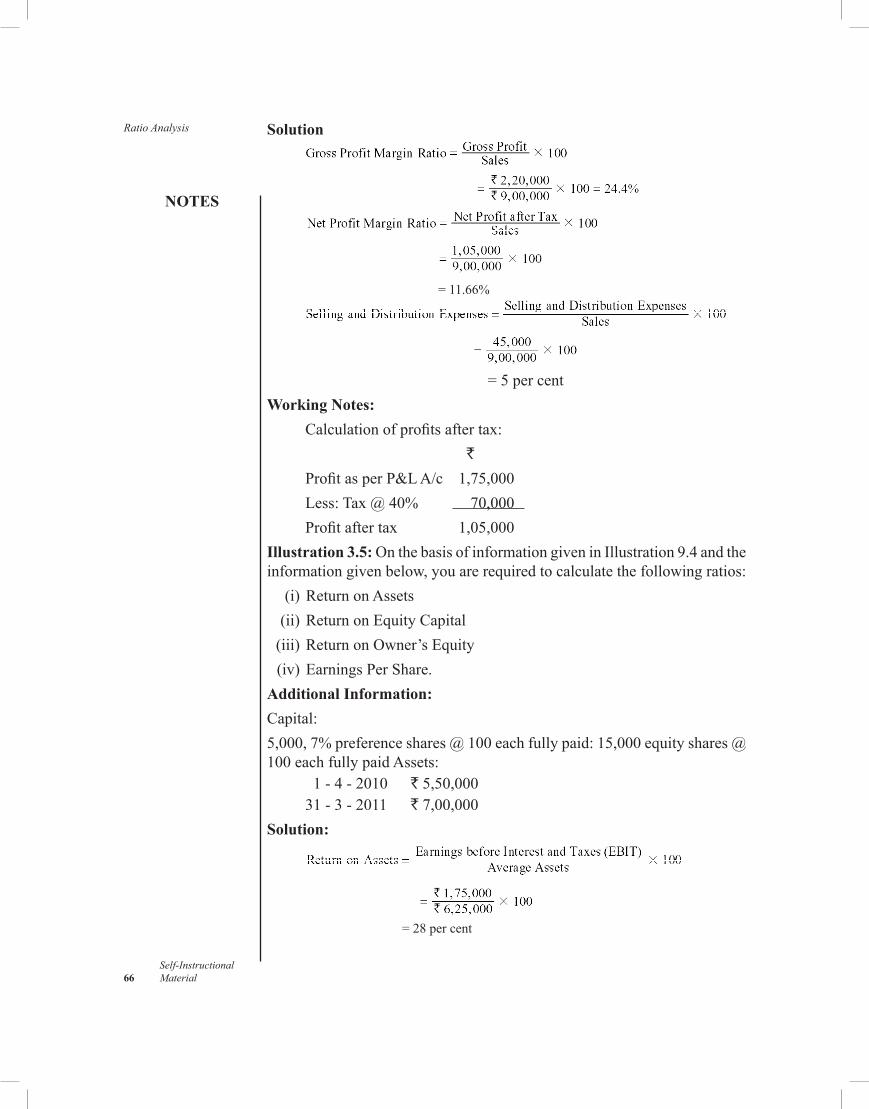

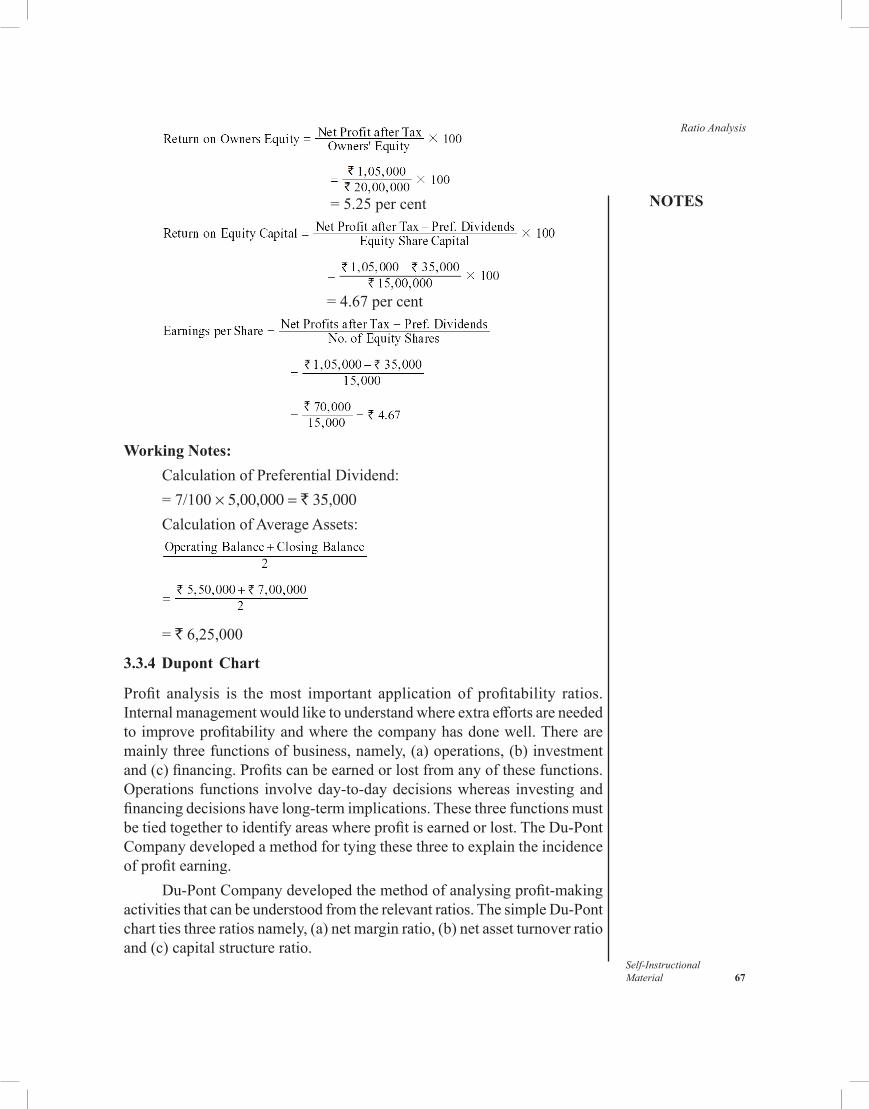

3.3.3 Profitability Ratios

3.3.4 Dupont Chart

3.3.5 Activity or Turnover Ratios

3.4 Construction of Balance Sheet 3.5 Answers to Check Your Progress Questions 3.6 Summary 3.7 Key words 3.8 Self Assessment Questions and Exercises 3.9 Further Readings

UNIT 4 FUNDS FLOW STATEMENT 86-113

4.0 Introduction 4.1 Objectives 4.2 Funds Flow Statement : Meaning 4.3 Preparation of Funds Flow Statement

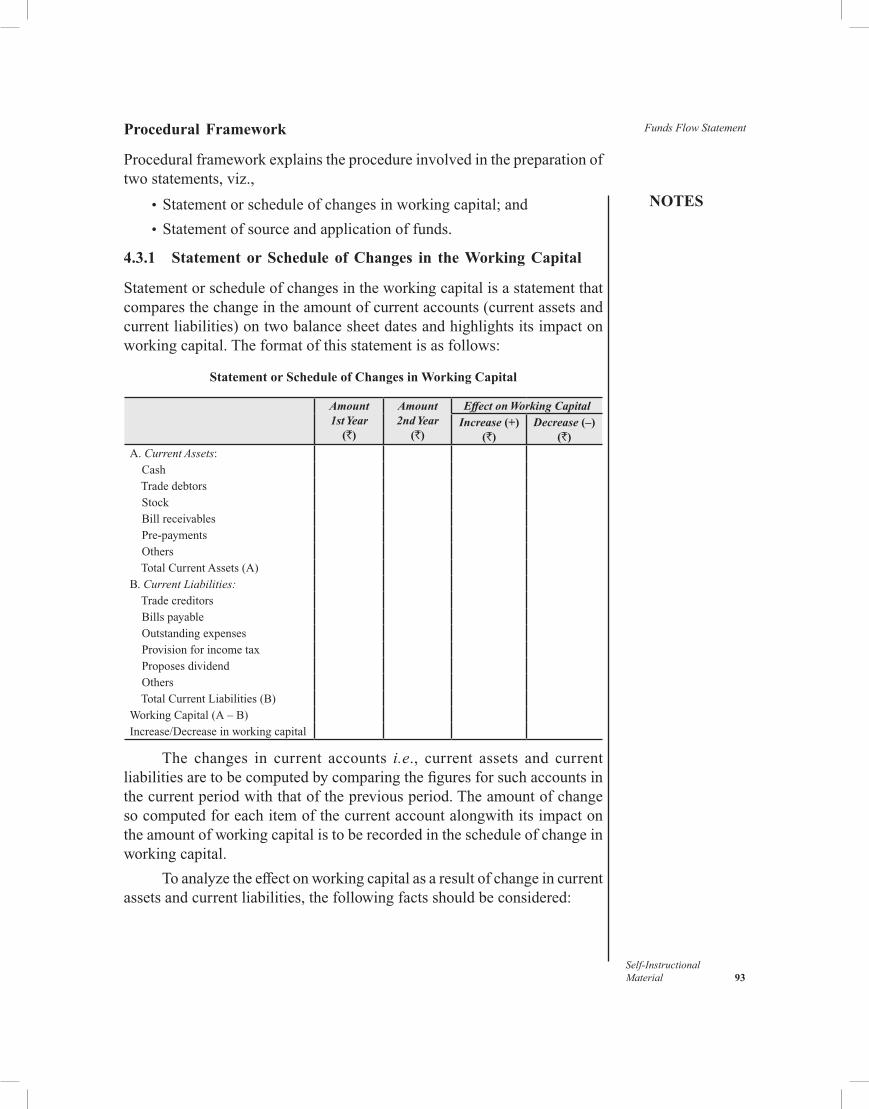

4.3.1 Statement or Schedule of Changes in the Working Capital

4.3.2 Statement of Sources and Applications of Funds

4.3.3 Funds from Operation/Operational Profit

4.3.4 Adjustment of Typical Items

4.3.5 Preparation of Working Accounts and Notes (Hidden Transaction)

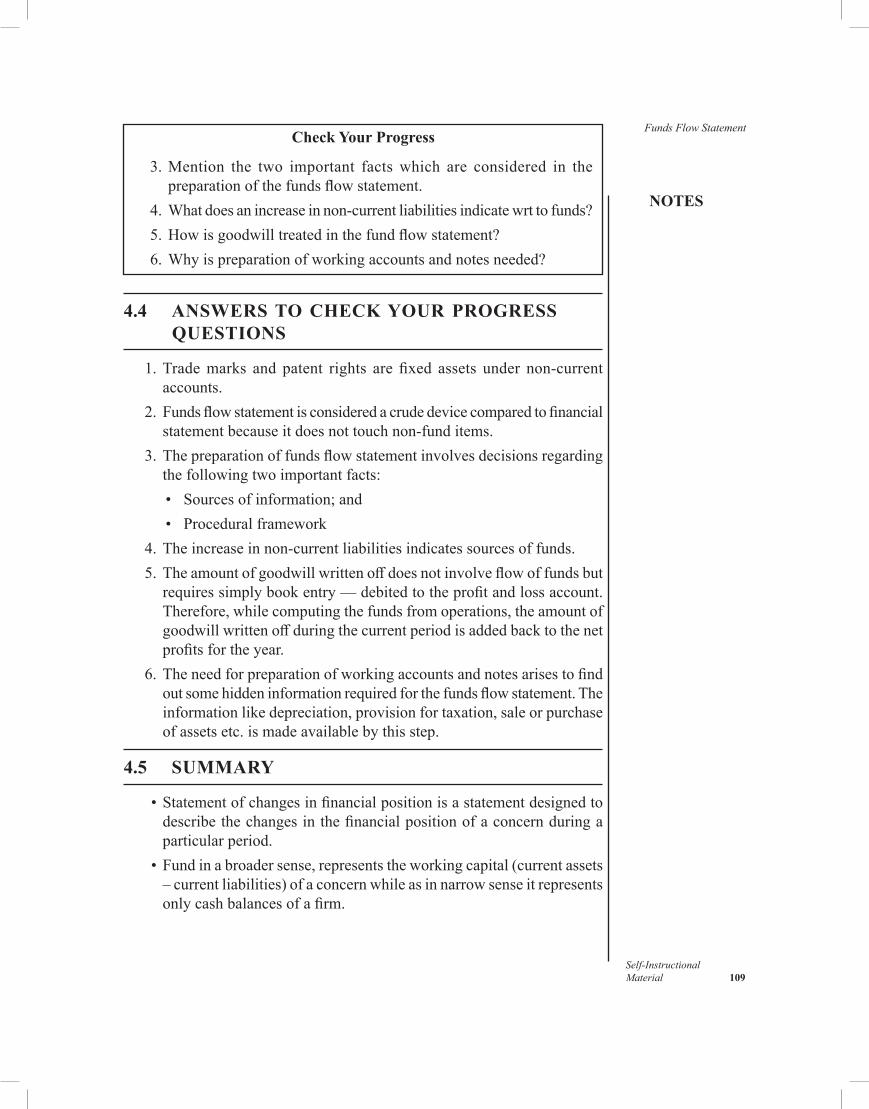

4.4 Answers to Check Your Progress Questions 4.5 Summary 4.6 Key Words

4.7 Self Assessment Question and Exercises 4.8 Further Readings

BLOCK II: CASH FLOW STATEMENT AND ANALYSIS

UNIT 5 CASH FLOW STATEMENT AND ANALYSIS 114-137

5.0 Introduction 5.1 Objectives 5.2 Meaning Of Cash Flow Statement

5.2.1 Difference between Cash Flow Statement and Fund Flow Statement

5.2.2 Concept of Cash Flow

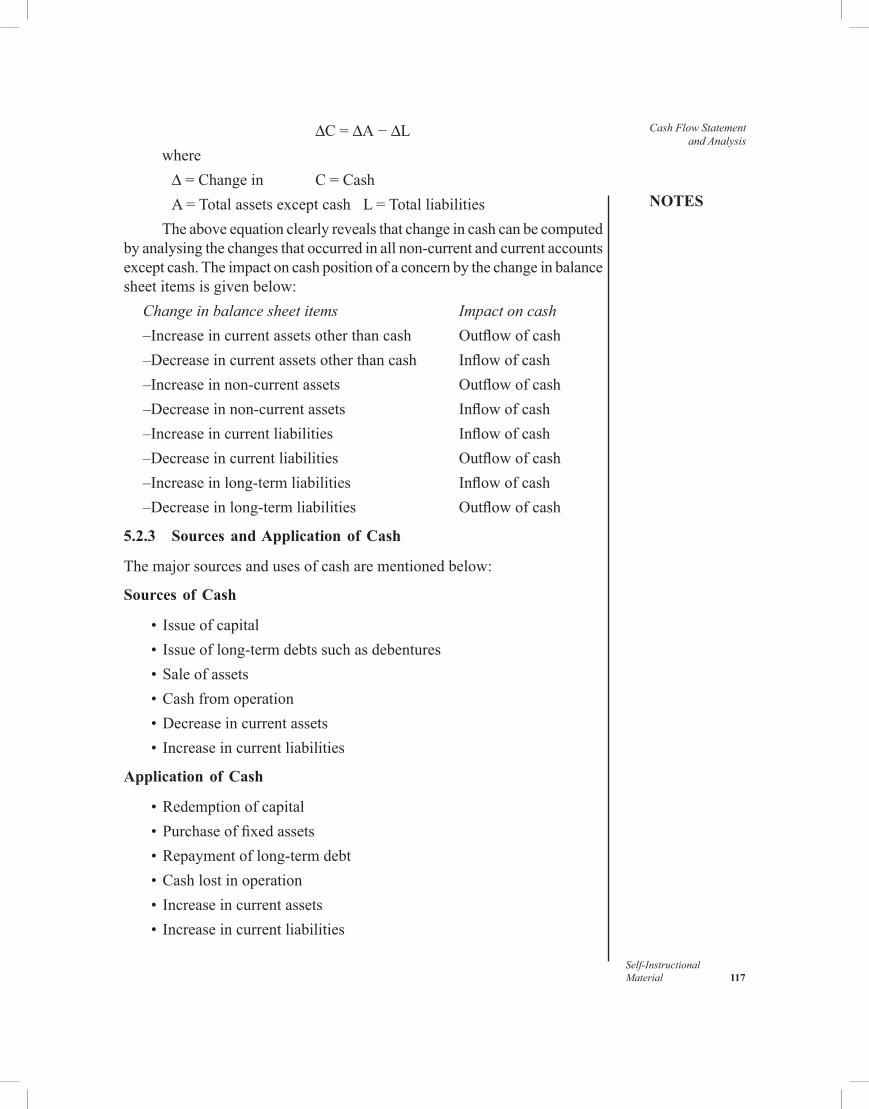

5.2.3 Sources and Application of Cash

5.2.4 Calculation of Cash From Operations

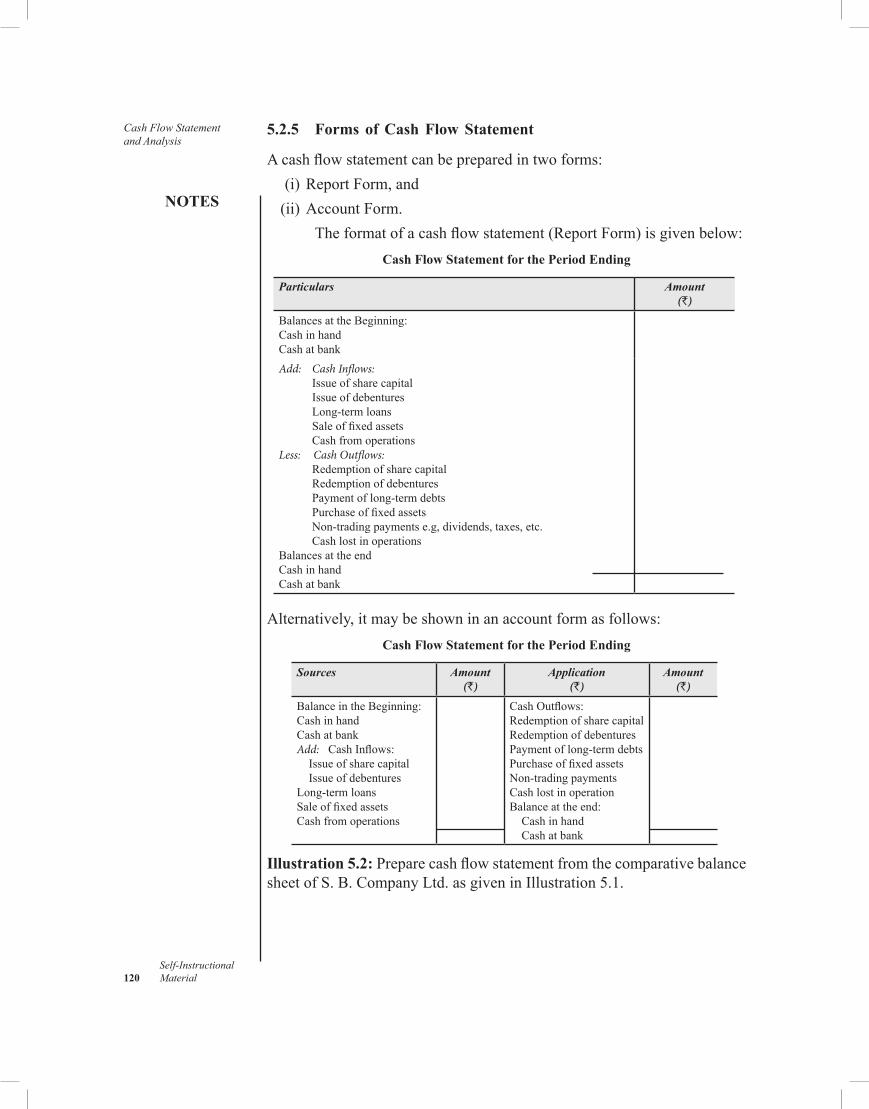

5.2.5 Forms of Cash Flow Statement

5.3 Preparation Of Cash Flow Statement as per AS 3 5.4 Answers to Check Your Progress Questions 5.5 Summary 5.6 Key Words 5.7 Self Assessment Questions and Exercises 5.8 Further Readings

UNIT 6 BUDGET AND BUDGETARY CONTROL 138-175

6.0 Introduction 6.1 Objectives 6.2 Budget and Budgetary Control: Meaning

6.2.1 Advantages and Limitations of Budgetary Control

6.2.2 Essential Characteristics of a Good Budgetary Control

6.3 Classification and Preparation of Budgets 6.3.1 Sales Budget

6.3.2 Production Budget

6.3.3 Production Cost Purchase and Overheads Budget

6.3.4 Cash Budget

6.4 Answers to Check Your Progress Questions 6.5 Summary 6.6 Key Words

6.7 Self Assessment Questions and Exercises 6.8 Further Readings

UNIT 7 STANDARD COSTING 176-188

7.0 Introduction 7.1 Objectives 7.2 Meaning of Standard Costing

7.2.1 Advantages and Limitations of Standard Costing

7.3 The Standard Costing System 7.4 Answers to Check Your Progress Questions 7.5 Summary 7.6 Key Words 7.7 Self Assessment Questions and Exercises 7.8 Further Readings

UNIT 8 VARIANCE ANALYSIS 189-224

8.0 Introduction 8.1 Objectives 8.2 Variances Analysis : Meaning, Significance and Types 8.3 Direct Material Variance 8.4 Labour Variances 8.5 Overhead Variance 8.6 Practical Problems 8.7 Answers to Check Your Progress Questions 8.8 Summary 8.9 Key Words 8.10 Self Assessment questions and Exercise 8.11 Further Readings

BLOCK III: COSTING AND ITS APPLICATIONS

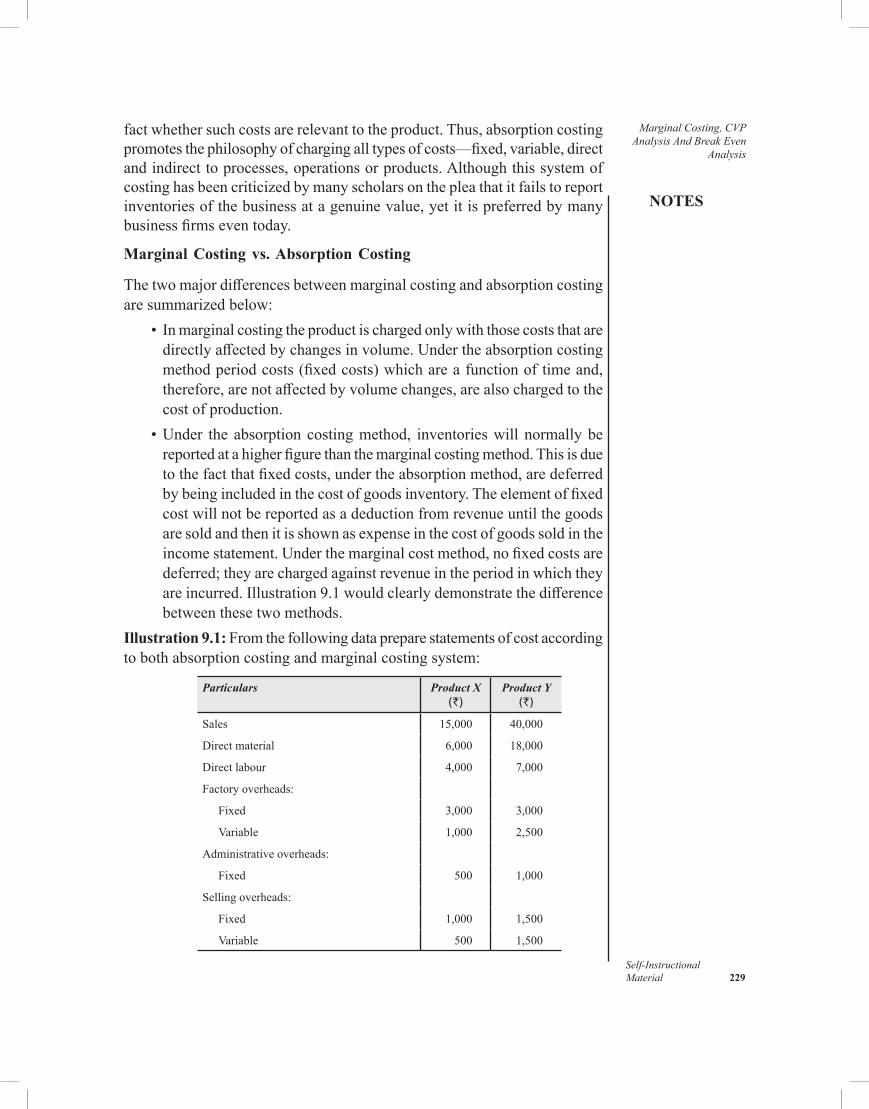

UNIT 9 MARGINAL COSTING, CVP ANALYSIS AND BREAK EVEN ANALYSIS 225-245

9.0 Introduction 9.1 Objectives 9.2 Concept of Marginal Costing

9.2.1 Advantages and Disadvantages of Marginal Costing

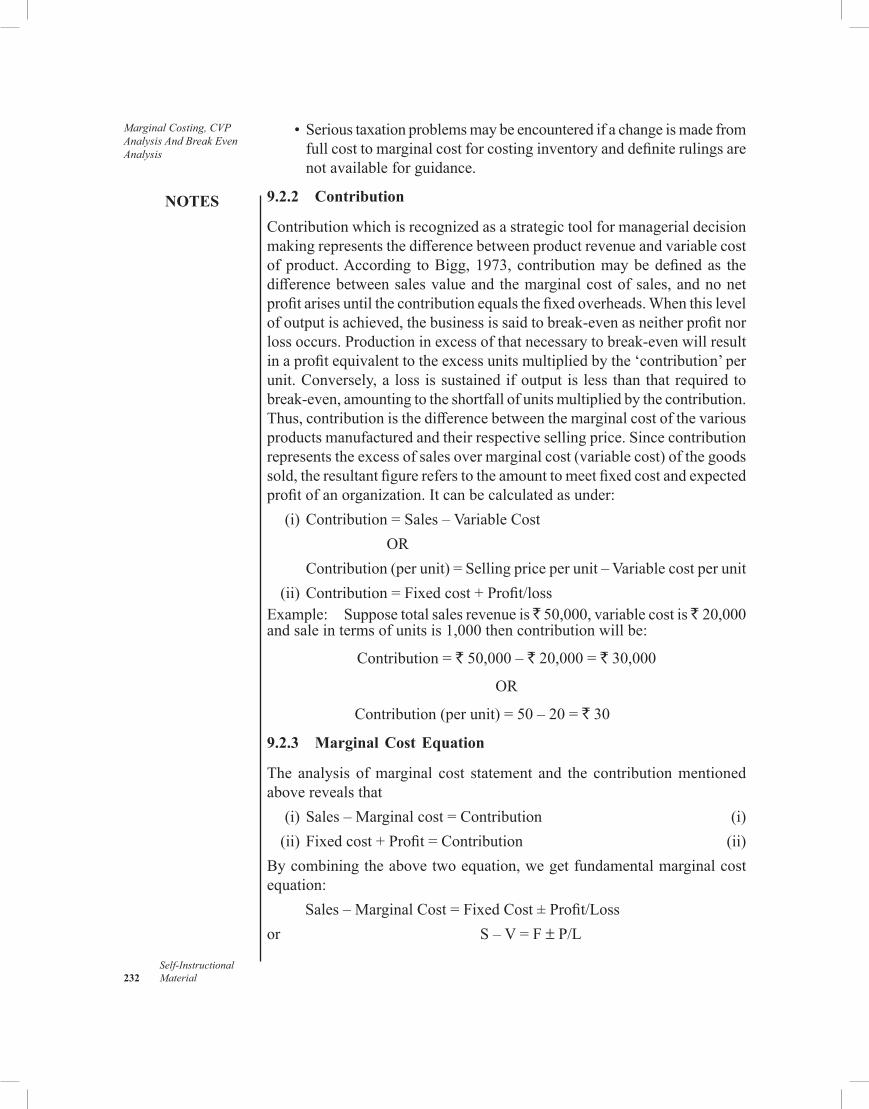

9.2.2 Contribution

9.2.3 Marginal Cost Equation

9.2.4 Profit/Volume Ratio (P/V Ratio)

9.3 Managerial Application of Marginal Costing 9.4 CVP Analysis And Break Even Analysis 9.5 Answers to Check Your Progress Questions 9.6 Summary 9.7 Key Words 9.8 Self Assessment Questions and Exercises 9.9 Further Readings

UNIT 10 BREAK-EVEN ANALYSIS/POINT (BEA/BEP) 246-269

10.0 Introduction 10.1 objectives 10.2 Concept of Break-Even Point/Analysis

10.2.1 Managerial Applications and Profit Planning

10.2.2 Assumptions, Advantages and Limitations

10.2.3 Margin of Safety

10.2.4 Angle of Incidence

10.2.5 Profit-Volume Graph

10.3 Answers to Check Your Progress 10.4 Summary 10.5 Key Words 10.6 Self Assessment Questions and Exercises 10.7 Further Readings

UNIT 11 DIFFERENTIAL COSTING 270-294

11.0 Introduction 11.1 Objectives 11.2 Nature and Scope of Differential Costing 11.3 Decision Making Process 11.4 Application of Differential Costing 11.5 Answers to Check Your Progress 11.6 Summary 11.7 Key Words

11.8 Self Assessment Questions and Exercises 11.9 Further Readings

BLOCK IV: METHODS OF CAPITAL BUDGETING

UNIT 12 CAPITAL BUDGETING: MEANING AND IMPORTANCE 295-305

12.0 Introduction 12.1 Objectives 12.2 Capital Budgeting: Meaning

12.2.1 Importance

12.2.2 Steps in Capital Budgeting Process

12.2.3 Objectives of Capital Budgeting Programmes

12.2.4 Kinds of Proposals

12.2.5 Appraisal Methods

12.3 Answers To Check Your Progress 12.4 Summary 12.5 Key Words 12.6 Self Assessment Questions and Exercises 12.7 Further Readings

UNIT 13 APPRAISAL METHODS 306-344

13.0 Introduction 13.1 Objectives 13.2 Methods of Evaluation or Appraisal 13.3 Non-discounted Cash Flow Method

13.3.1 Payback and Payback Reciprocal Method

13.3.2 Accounting Rate of Return

13.4 Discounted Cash Flow (Time-adjusted) Method 13.4.1 The Net Present Value Method

13.4.2 Internal Rate of Return (IRR) Method

13.4.3 Profitability Index

13.5 Practical Problems 13.6 Answers to Check Your Progress Questions 13.7 Summary 13.8 Key Words

13.9 Self Assesment Questions and Exercises 13.10 Further Readings

UNIT 14 METHODS OF EVALUATION OF ALTERNATIVE CAPITAL EXPENDITURE PROGRAMME 345-364

14.0 Introduction 14.1 Objectives 14.2 Economic Rate of Return (ERR): Economic Cost-Benefit Analysis 14.3 Social Rate of Return (SRR): Social Cost-Benefit Analysis 14.4 Capital Amortization Schedule (CAS) 14.5 Risk Adjusted Discount Rate (RADR)

14.5.1 Intuitive Approach

14.5.2 Constant Share Price Approach

14.5.3 CAPM Aapproach

14.5.4 Adjusted WACC approach

14.6 Answers to Check Your Progress Questions 14.7 Summary 14.8 Key Words 14.9 Self Assessment Questions and Exercises 14.10 Further Readings

Introduction

NOTES

Self-Instructional 12 Material

INTRODUCTION

Management accounting is a vast subject and encompasses all that accounting information which helps management in planning, controlling, decision making and performance measurement of business operations. CIMA has observed that management accounting combines accounting with finance and management with the leading edge techniques needed to drive successful business.

Management accountant plays a very important role in an organization. He analyses and interprets accounting information and meets the informational needs of management at different levels. In an organization, a management accountant generally performs a staff function, i.e., advisory role. But if he is permitted to participate in planning and decision-making, he is a part of the management team and thus becomes a part of the line function. It is very important that status of the management accountant in the organization is clearly defined so that the scope of his work and responsibilities are accordingly determined.

This book, Management Accounting, is written with the distance learning student in mind. It is presented in a user-friendly format using a clear, lucid language. Each unit contains an Introduction and a list of Objectives to prepare the student for what to expect in the text. At the end of each unit are a Summary and a list of Key Words, to aid in recollection of concepts learnt. All units contain Self-Assessment Questions and Exercises, and strategically placed Check Your Progress questions so the student can keep track of what has been discussed.

NOTES

Self-InstructionalMaterial 1

Nature and Scope of Management AccountingBLOCK - I

BASICS OF MANAGEMENT ACCOUNTING

UNIT 1 NATURE AND SCOPE OF MANAGEMENT ACCOUNTING

Structure 1.0 Introduction 1.1 Objectives 1.2 ManagementAccounting:Definition

1.2.1 Scope of Management Accounting 1.3 DifferencebetweenFinancialAccountingandManagementAccounting 1.4 Management Accounting as an Aid to Management

1.4.1 ObjectivesandFunctionsofManagementAccounting 1.4.2 ToolsandTechniquesofManagementAccounting

1.5 Merits and Limitations 1.6 ChangingRoleandTasksofManagementAccountants

1.6.1 Management Accountant in an Organization 1.7 AnswerstoCheckYourProgressQuestions 1.8 Summary 1.9 Key Words 1.10 SelfAssessmentQuestionsandExercises 1.11 FurtherReadings

1.0 INTRODUCTION

Accountingplaysacrucialroleinthefunctioningofanorganization.Itnotonlyhelpsinenhancingdecisionmakingcapabilities,butalsofacilitatestheefficientutilizationofresources.Organizationsacrosstheglobeoperateinahighlydynamicandcomplexbusinessenvironment,inwhichmanagersneedrelevantandcurrentinformationtoaidthemindecisionmaking.Accountingmust respond to the changing needs of the decision-makers in order tojustifyitsrelevanceincontemporarybusiness.Infact,thesignificanceoffinancialinformationhasalwaysbeenrecognized,butinthepresentbusinessscenario,suchinformationhasbecomearesourceparallelinimportancetofactorsofproduction.Consequently,accounting information isbecomingincreasinglycriticaltothecontinuingsuccessofanorganization.Withthegrowingimportanceofinformationasaresource,organizationshavefelttheneedforasystemthatiscapableofmanagingthisresourceefficiently.Thisis,perhaps,thebasicreasonforbusinessstudentstostudytheanatomyandoperationoftheaccountingsystem,whichprovidesinformationtomanagersfordecisionmaking.

Nature and Scope of Management Accounting

NOTES

Self-Instructional 2 Material

Modernaccountingasadynamicandgrowingfield isemergingasa strategicweapon that is helping to shape the direction and growth oforganizationsinthechangingbusinessenvironment.However,toexploreandutilizethefinancialinformationgeneratedbytheaccountingsystemofanorganizationforcompetitiveadvantage,managersmusthaveafairknowledgeofthetoolsandtechniquesthattheycanuseforanalyzingandinterpretingthe available information. Both the prerequisites of effective decisionmaking—financialinformationandanalyticaltechniques—arecoveredunderManagement Accounting, whichinvolvesthestudyofaccountinginformationandtechniquesthatmanagersuseinanalysingsuchinformation.

In this unit, youwill be introduced to the concept ofmanagementaccounting.

1.1 OBJECTIVES

Aftergoingthroughthisunit,youwillbeableto: •Discussthedefinition,objectives,natureandscopeofmanagement

accounting •Explainthedifferencesbetweenmanagementaccountingandfinancial

accounting •Describethemeritsandlimitationsofmanagementaccounting

1.2 MANAGEMENT ACCOUNTING: DEFINITION

Managementaccountingisasegmentofaccountingthatdealsspecificallywith the analysis and reportingof information tomanagement about theoperationsoftheorganizationwithanobjectivetofacilitatedecisionmaking.Ontheonehand,managementaccountingaimstoprovideadequatefinancialinformationtomanagersfordecisionmakingandontheother,itisorientedtowardsmanagerialcontrol.Managementfrequentlyrequirestimelyfinancialinformationconcerningdifferentaspectsoftheorganization,rangingfromspecialpurposereportofaspecificdepartment’soperatingperformancetothepreparationofannualbudgetsandforecasts,whichencompasstheentirebusiness.

Theterm‘managementaccounting’wasfirstformallymentionedin1950inareportentitled‘Management Accounting’,publishedbytheAnglo-AmericanCouncilofProductivityManagementAccountingTeamafteritsvisit totheUnitedStatesinthesameyear.Theteaminitsreportdefinedmanagement accounting as the presentation of accounting information in such a way as to assist management in the creation of policy and in the day-to-day operation of an undertaking.

NOTES

Self-InstructionalMaterial 3

Nature and Scope of Management Accounting

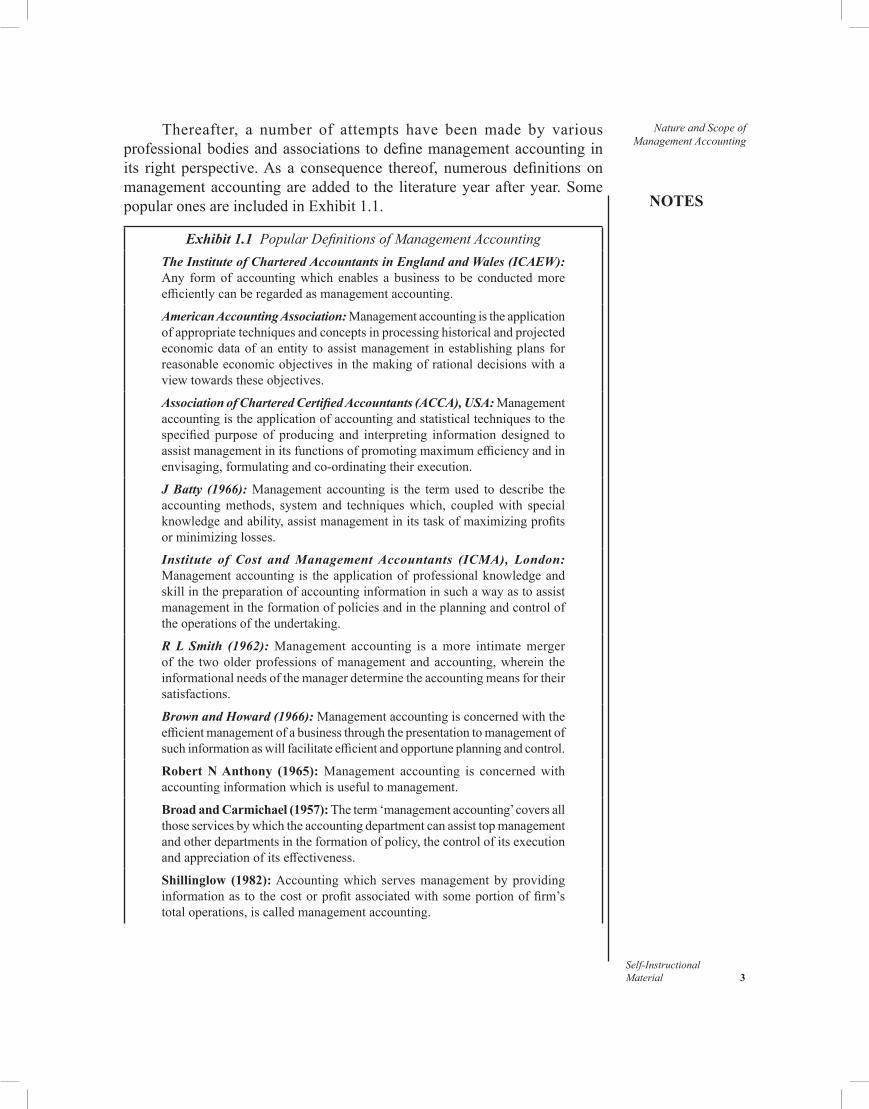

Thereafter, a number of attempts have beenmade by variousprofessionalbodiesandassociations todefinemanagementaccountinginits right perspective.As a consequence thereof, numerous definitions onmanagementaccountingareadded to the literatureyearafteryear.SomepopularonesareincludedinExhibit1.1.

Exhibit 1.1 Popular Definitions of Management AccountingThe Institute of Chartered Accountants in England and Wales (ICAEW): Any formof accountingwhich enables a business to be conductedmoreefficientlycanberegardedasmanagementaccounting.

American Accounting Association: Managementaccountingistheapplicationofappropriatetechniquesandconceptsinprocessinghistoricalandprojectedeconomicdataofanentity toassistmanagement inestablishingplansforreasonableeconomicobjectivesinthemakingofrationaldecisionswithaviewtowardstheseobjectives.

Association of Chartered Certified Accountants (ACCA), USA: Management accountingistheapplicationofaccountingandstatisticaltechniquestothespecified purpose of producing and interpreting information designed toassistmanagementinitsfunctionsofpromotingmaximumefficiencyandinenvisaging,formulatingandco-ordinatingtheirexecution.

J Batty (1966): Management accounting is the termused to describe theaccountingmethods, system and techniqueswhich, coupledwith specialknowledgeandability,assistmanagementinitstaskofmaximizingprofitsorminimizinglosses.

Institute of Cost and Management Accountants (ICMA), London: Managementaccounting is theapplicationofprofessionalknowledgeandskillinthepreparationofaccountinginformationinsuchawayastoassistmanagementintheformationofpoliciesandintheplanningandcontroloftheoperationsoftheundertaking.

R L Smith (1962): Management accounting is a more intimate merger of the twoolderprofessionsofmanagement andaccounting,wherein theinformationalneedsofthemanagerdeterminetheaccountingmeansfortheirsatisfactions.

Brown and Howard (1966): Managementaccountingisconcernedwiththeefficientmanagementofabusinessthroughthepresentationtomanagementofsuchinformationaswillfacilitateefficientandopportuneplanningandcontrol.

Robert N Anthony (1965):Management accounting is concernedwithaccountinginformationwhichisusefultomanagement.

Broad and Carmichael (1957):Theterm‘managementaccounting’coversallthoseservicesbywhichtheaccountingdepartmentcanassisttopmanagementandotherdepartmentsintheformationofpolicy,thecontrolofitsexecutionandappreciationofitseffectiveness.

Shillinglow (1982):Accountingwhich servesmanagement by providinginformationas to thecostorprofitassociatedwithsomeportionoffirm’stotaloperations,iscalledmanagementaccounting.

Nature and Scope of Management Accounting

NOTES

Self-Instructional 4 Material

T G Rose, (1957):Managementaccountingistheadaptationandanalysisofaccountinginformationanditsdiagnosisandexplanationinsuchawayasto assist management.

R H Garrison (1982):Managementaccountingisconcernedwithprovidinginformationtomanagers;thatis,tothosewhoareinsideanorganizationandwhoarechargedwithdirectingandcontrollingitsoperations.

All thesedefinitionsplace emphasis on the informationprocessinganddecisionmakingaspectsofaccounting.Theanalysisofthedefinitionsfurtherrevealsthatthesystemofmanagementaccountingisnotdesignedto appraise andmonitor the past performanceof individuals andgroupsbuttoassistmanagerialdecisionsaffectingthefuture.Thus,managementaccountingisasystemforgathering,summarizing,reportingandinterpretingaccountingdataandotherfinancial informationprimarilyfor the internalneedsofmanagement.Thus, management accounting is a system capable of generating accounting information that assists internal management in the efficient formulation, execution and appraisal of business plans that help the organizations to achieve their strategic objectives.

Thus,management accounting in addition to helpingmanagersin the decisionmaking process, facilitates them in intra-firm resourceallocations,fixationofresponsibilitiesandtheevaluationoffuturepoliciesandstrategies.Allthisbringstolightanimportantfact—thatmanagementaccountinghastoperformtwoseparate,distinctfunctionsoffinancialandmanagementreportingandthatthedataneedsforeachareoftendifferent.Fewintelligentfinancialandeconomicdecisionscanbemadeintheabsenceofthatinformationreservoir.Involvementwithbothtimedimensions,pastandfuture,placestheexecutivenearthecentreofthecontrolanddecisionmakingprocessesinanyorganization.

1.2.1 Scope of Management Accounting

Traditionally,thesubjectmatterofmanagementaccountingmainlyconsistedoffinancialstatementanalysisandcostingtheory.Asorganizationsbegantooperate in a highlydynamic and complexbusiness environment, theyrealized that the existing subjectmatter ofmanagement accountingwasinsufficienttomeetthechallengesofthechangingenvironment.Toaddressthe emerging challenges,management accounting enhanced its scopebyincluding in its ambitmany frameworks, tools and techniques borrowedfromotherdisciplinessuchaseconomics,finance,mathematics,statisticsandoperationsresearch.Thecontemporarysubjectmatterofmanagementaccountingissummarizedbelow:

Financial Accounting: Financialaccountingisaprerequisiteforanydiscussiononthesubjectofmanagementaccounting.Financialstatementsasgeneratedbyfinancialaccountingcontainenoughdatathatisconverted

NOTES

Self-InstructionalMaterial 5

Nature and Scope of Management Accounting

intoinformationbyorganizationsandusedintheirdecisionmaking.Infact,managementaccountingprovidesonlytoolsandtechniquesforinterpretationandanalysisandthemanagementaccountantsgetthedataforthepurposemainlyfromfinancialaccounting.Thus,managementaccountingcannotexistwithoutefficientfinancialaccountingsystem.

Cost Accounting: Althoughmanagers generally use financialinformationindecisionmaking,theyoftensupplementtheirdecisionswithcostinformationastheyhaverealizedthatanyactivityofanorganizationcanbedescribedbyitscost.Theymakeuseofvariouscostdatainmanagingorganizationseffectively.Infact,costaccountingisconsideredthebackboneofmanagementaccountingasitprovidestheanalyticaltoolssuchasbudgetarycontrol, standard costing,marginal costing, inventory control, operatingcosting,etc.,whichareusedbymanagementtodischargeitsresponsibilitiesefficiently.

Financial Statement Analysis: Managersfrequentlyuseinformationbasedonthedatacollectedfromfinancialstatements.Thisinformationcanbeobtainedeitherbyselectingindividualnumbersfromthestatementsorbydevelopingcertaintrendsandratios.Anyattemptinthisdirectionisreferredtoasfinancialstatementanalysis.Theanalysisandinterpretationofthedatacontainedinfinancialstatementscanprovideareadermeaningfulinsightsandconclusionsabouttheorganization.Overthepastfewdecades,numeroustechniqueshavebeendevelopedwhichareusefulfortheproperinterpretationandanalysisoffinancialstatements.

Budgeting: Budgeting, which lies at the heart ofmanagementaccounting,referstoasystematicplanfortheutilizationoforganizationalresources.Asamanagementtool,budgetingaimstocoordinateandintegratetheeffortsandactivitiesofvariousdepartmentswiththecooperationofthosewhoseektoachieveacommongoal.Infact,theorganizationsexercisetheiroperationalcontrolthroughthebudgetspreparedinadvanceforeverymajoractivityofthebusiness.

Inflation Accounting: Inflationaccountingattemptstoidentifycertaincharacteristicsofaccountingthattendtodistort thereportingoffinancialresultsduringperiodsofrapidlychangingprices.Itdevisesandimplementsappropriatemethodstoanalyseandinterprettheimpactofinflationonthebusiness transactions.

Management Reporting: Clear,informativeandtimelyreportshavealwaysbeenrecognizedasmanagerialtoolsinreachingdecisionsthatnotonlyhelptheorganizationstoimprovetheirperformancebutalsomakethebestuseoftheirresources.Thus,oneofthebasicresponsibilitiesofmanagementaccountingistokeepthemanagementwellinformedabouttheoperationsof the business.To discharge this responsibility efficiently,management

Nature and Scope of Management Accounting

NOTES

Self-Instructional 6 Material

accountingneedstopreparequarterly,half-yearlyandotherinterimreportsandsubmitthesametothemanagement.

Quantitative Techniques: Manymanagersrecognizethatthefinancialandeconomicdataavailableformanagerialdecisionscanbemoreusefulifanalysedwithhighlysophisticatedtechniquesofanalysisandevaluation.Suchtechniquesasthesubjectmatterofquantitativeanalysisallowmanagerstocreate information from theirfinancialdatabase that isnot,otherwise,available.Inadditiontothetechniquesliketimeseries,regressionanalysisandsamplingtechniques,themanagersalsomakeuseoflinearprogramming,gametheoryandqueuingtheoryforthispurpose.

Tax Accounting: Since taxation plays an important role in theprofitabilityofacommercialorganization,itisessentialforamanagementaccountanttohaveacompleteknowledgeofbusinesstaxation.Thebusinessprofitandthetaxthereonaretobeascertainedaspertheprovisionoftaxation.Thefilingoftaxreturnsandthepaymentoftaxinduetimeistheexclusiveresponsibilityofthemanagementaccountant.

Internal Audit: Internalauditasadisciplineofmanagementaccountingmakesarrangementsforperformanceappraisaloftheorganization’svariousdepartments.Thus,amanagementaccountantmustpossessknowledgeaboutthefixationofresponsibilitiesandmeasurementofresults.

Office Services: To discharge the responsibilities efficiently, amanagementaccountanthas todealwithdataprocessing,filing,copyingandduplicating.His area of responsibilities also included the evaluationandreportingabouttheutilityofdifferentofficeproceduresandmachines.

1.3 DIFFERENCE BETWEEN FINANCIAL ACCOUNTING AND MANAGEMENT ACCOUNTING

The compartmentalizationof accounting into various branches generallysoundssomewhatartificialandmisleadingasallthesebranchesareusuallydrawn from a commonpool of financial data used in preparing reportsforgroupswhoareoften involved inmakingavarietyof interdependentdecisions.Butacloseexaminationofthetwosystemsshowsthattheydifferinseveralwaysfromeachother.SomemajordifferencesbetweenthesetwoaccountingsystemsaresummarizedinExhibit1.2:

NOTES

Self-InstructionalMaterial 7

Nature and Scope of Management Accounting

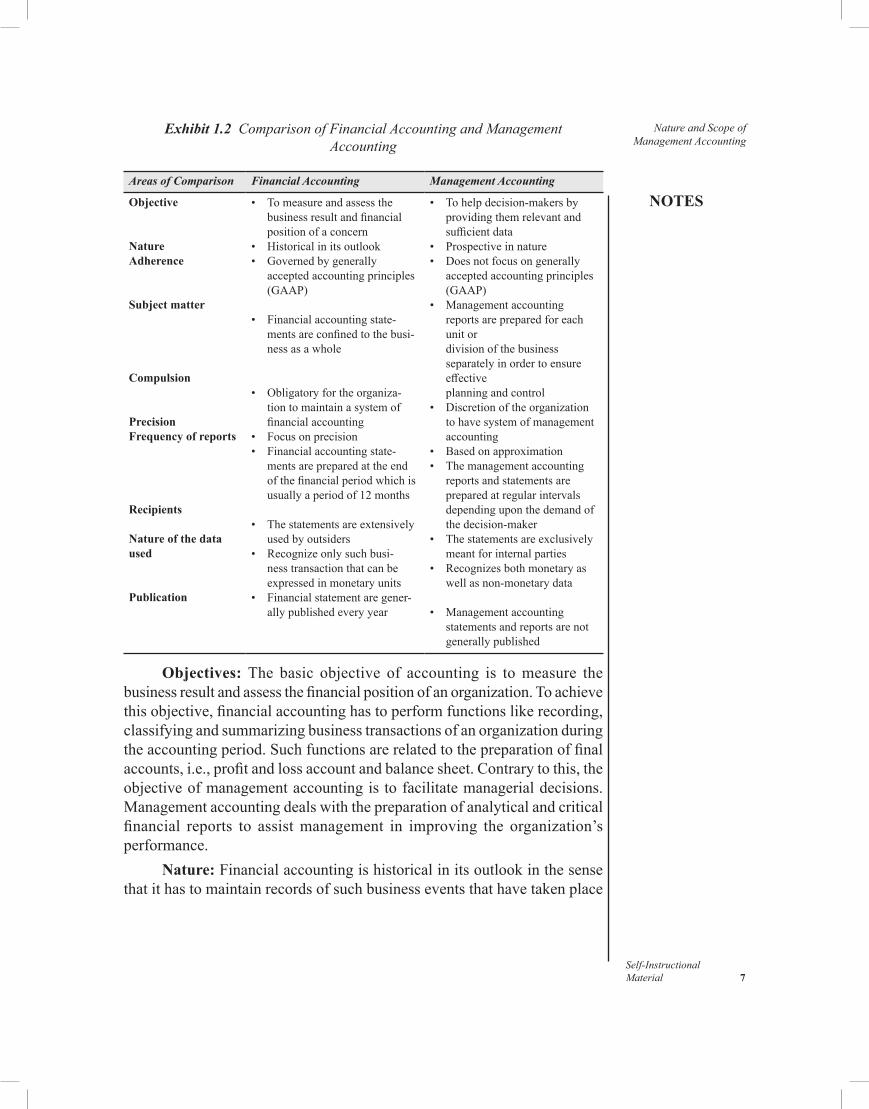

Exhibit 1.2 Comparison of Financial Accounting and Management Accounting

Areas of Comparison Financial Accounting Management Accounting

Objective

NatureAdherence

Subject matter

Compulsion

PrecisionFrequency of reports

Recipients

Nature of the data used

Publication

• Tomeasureandassessthe businessresultandfinancial position of a concern

• Historicalinitsoutlook• Governedbygenerally

acceptedaccountingprinciples(GAAP)

• Financialaccountingstate-mentsareconfinedtothebusi-nessasawhole

• Obligatoryfortheorganiza-tion to maintain a system of financialaccounting

• Focusonprecision• Financialaccountingstate-

mentsarepreparedattheendofthefinancialperiodwhichisusuallyaperiodof12months

• Thestatementsareextensivelyused by outsiders

• Recognizeonlysuchbusi-nesstransactionthatcanbeexpressedinmonetaryunits

• Financialstatementaregener-allypublishedeveryyear

• Tohelpdecision-makersby providingthemrelevantand sufficientdata

• Prospectiveinnature• Doesnotfocusongenerally

acceptedaccountingprinciples(GAAP)

• Managementaccountingreportsarepreparedforeachunit or divisionofthebusinessseparatelyinordertoensureeffective planningandcontrol

• Discretionoftheorganizationtohavesystemofmanagementaccounting

• Basedonapproximation• Themanagementaccounting

reports and statements are preparedatregularintervalsdependinguponthedemandofthedecision-maker

• Thestatementsareexclusivelymeantforinternalparties

• Recognizesbothmonetaryaswellasnon-monetarydata

• Managementaccounting statements and reports are not generallypublished

Objectives: The basic objective of accounting is tomeasure thebusinessresultandassessthefinancialpositionofanorganization.Toachievethisobjective,financialaccountinghastoperformfunctionslikerecording,classifyingandsummarizingbusinesstransactionsofanorganizationduringtheaccountingperiod.Suchfunctionsarerelatedtothepreparationoffinalaccounts,i.e.,profitandlossaccountandbalancesheet.Contrarytothis,theobjectiveofmanagementaccountingistofacilitatemanagerialdecisions.Managementaccountingdealswiththepreparationofanalyticalandcriticalfinancial reports to assistmanagement in improving the organization’sperformance.

Nature: Financialaccountingishistoricalinitsoutlookinthesensethatithastomaintainrecordsofsuchbusinesseventsthathavetakenplace

Nature and Scope of Management Accounting

NOTES

Self-Instructional 8 Material

duringtheaccountingperiod.Underfinancialaccountingsystematransactionisrecordedasandwhenittakesplace.Therefore,prospectivetransactionsarenotconsideredbeforetheirmaturityundersuchsystemofaccounting.Ontheotherhand,managementaccountingsystemisdevisedtohelpmanagersinshapingfutureoperationsofthebusiness.Itdealswithprojectionofdatatobeusedforplanninganddecisionmakingforthefuture.Thus,managementaccountinghasprospectivecharacter.

Adherence to Accounting Principles: Financialaccountingsystemisbasedonsomeaccountingprinciplesandconventionswhichafinancialaccountant has to strictly followwhile preparingfinancial accounts andstatements.Thefinancial accounting system can be result-oriented onlywhentheaccountingprinciplesandconventionshavebeenproperlyfollowedandapplied.Butmanagementaccountingisnotboundbytheconstraintsofgenerallyacceptedaccountingprinciplesandconventions.Thepreparationofreportsandstatementsundermanagementaccountingaregovernedbytherequirementsofthemanagement.Managementcanframeitsowngroundrulesandprinciplesregardingtheformandcontentofinformationrequiredforinternaluse.

Subject Matter: Financialaccountingconsidersthebusinessasoneentityandaccordinglyfinancialaccountingreportshavebeenconfinedtothebusinessoperationsasawhole.Suchstatementspresentthepositionandtheperformanceoftheentirebusiness.Whereasundermanagementaccountingsystemeachunit/department/division/costcentreofthebusinessistreatedasaseparateentityinordertoensureeffectiveplanningandcontrol.Therefore,profitabilityandperformancereportsarepreparedforeachunitordivisionofthebusinessseparately.

Compulsion: TheIndianCompaniesActhasmadeitobligatoryforthecompaniestomaintainasystemoffinancialaccounting.Atthesametime,thebenefitsasofferedbyafinancialaccountingsystemhavemadeitmoreorlesscompulsoryforthenon-companyorganization.Ontheotherhand,thesettingupofmanagementaccountingsystemisatthediscretionofthemanagement.

Precision: Financialaccountingpaysmoreemphasisonprecisionandconsidersonlyactualfiguresinthepreparationofitsstatements.Thereisnoscopeforapproximatefiguresinfinancialaccounting.Butthereportsandstatements as prepared under management accounting system contain more approximatefiguresthantheactualfigures.Thus,managementaccountingislesspreciseascomparedtofinancialaccounting.

Frequency of Reports: Thefinancial statements, the outcome offinancialaccounting,arepreparedattheendofthefinancialperiodwhichis

NOTES

Self-InstructionalMaterial 9

Nature and Scope of Management Accounting

usuallyaperiodof12months.Butthemanagementaccountingreportsandstatementsarepreparedatregularintervalssothatmanagementmaynotfaceanydifficultyindecisionmaking.Managementisconstantlyinformedaboutthebusinessperformancethroughthesereportsandstatements.Thus, thereportingfrequencyofmanagementaccountingismuchhigherascomparedtoreportingoffinancialaccounting.

Recipients: Financialstatementssuchasprofitandlossandbalancesheet, are extensively used by outsiders i.e., shareholders, creditors, taxauthorities, etc.On the other hand,management accounting reports areexclusivelymeantformanagement.Suchreportsarenoteasilyavailabletooutsiders.

Nature of Data Used: Thefinancial statements as preparedunderfinancial accounting contain only such transactions that are expressed inmonetaryterms.Thenon-monetaryeventssuchasnatureofcompetition,businessreputation,changeinfashion,arenotatallconsideredbyfinancialaccounting.Butmanagement accounting uses bothmonetary and non-monetary data.

Publication: Financialaccountingstatementsarepublishedbyalmosteverybusinessorganizationfortheinformationofthegeneralpublic.TheIndianCompaniesActhasmadeitcompulsoryforeverycompanytopublishitsfinalaccountsi.e.,profitandlossaccountandbalancesheet.Bycontrast,the publication ofmanagement accounting reports and statements is notmandatory.

Check Your Progress

1.Whatisinflationaccounting? 2.Statethefrequencyofreportstobepreparedunderfinancialand

management accounting.

1.4 MANAGEMENT ACCOUNTING AS AN AID TO MANAGEMENT

Theprimaryobjectiveofamanagementaccountingsystem is toprovideaccurateandrelevantinformationtointernaluserswiththeaimofhelpingthemanagementtoattainefficiencyandeffectivenessintheorganization.Toachievethisgoal,managementaccountinghelpsanorganizationintheprocessofmanagementwhichgenerallyconsistsofactivitieslikeplanning,organizing,evaluating,andcommunicating(Figure1.1).

Nature and Scope of Management Accounting

NOTES

Self-Instructional 10 Material

Fig. 1.1 Management Accounting as an Aid to the Management Process

Planning: Planning is an activity ofmanagement that requires theapplicationofnotonlyascientificapproachbutalsoasystemicapproachtodecisionmaking.Allorganizationsirrespectiveoftheirnatureofbusiness,needtoplanbothatstrategicandoperationallevelstoremaincompetitiveinthemarket.Sincethemostcrucialdimensionofplanningthatthemanagementofanorganizationmustfocusuponisstrategicinnature,oneofthebasicfunctionsofthemanagementaccountantistohelpmanagementnotonlyintheselectionofthecompany’sgoalsandformulationofpoliciesandstrategiesbutalsointheallocationofresourcestoachievethesegoals.Differentaccountingtechniquesareusedbythemanagementtodischargethefunctionofplanningefficiently. Important among themare cost-volume-profit analysis, directcosting,capitalbudgetingandcashbudgeting.

Organizing: Organizing,which basically involves grouping ofactivities,definingtheresponsibilityandgrantingauthoritytoemployees,aimstodevelopstructuralrelationshipamongpeopleandphysicalresourcestocarryoutplansandaccomplishtheorganization’sstatedobjectives.Sinceorganizing is prerequisite for the success of anyorganization, therefore,thisfunctionnotonlycallsforundividedattentionfromthemanagementofanorganizationbutalsocontinuousmonitoringandaudit toensure itseffectivenessandrelevanceinadynamicbusinessenvironment.Toattainthisobjective,managementaccountingassiststhemanagementofanorganizationinorganizingbyestablishingcostand/orcostcentres.

Evaluating: Evaluating,commonlyknownascontrolling,istheprocessofdeterminingwhethertheorganizationalperformanceisconsistentwiththeplans.Thisfunctionofmanagement,infact,involvesthecomparisonofactualperformancewiththestandardstoidentifythedeviationifanyforthepurposeofinitiatingandimplementingmeasurestoadjustorganizationalactivitiestowardgoalattainment.Managementaccountinghelpsthemanagementofanorganization tomonitorprogressandmakeappropriateadjustmentbygeneratingvarious feedback/performance reports.Aneffectiveevaluation

NOTES

Self-InstructionalMaterial 11

Nature and Scope of Management Accounting

systemcontributestotheefficiencyoforganizationwhichinturnincreasestheprofitabilityoftheconcern.

Communication:Communication,which involves transmissionofinformationtothestakeholders,hasbeenrecognizedasanessentialfunctionofmanagementaccounting.Infact,themanagementaccountantspendsthemaximumtimeincommunicatingwithvariouspartiesthatareinterestedintheaffairsofthebusiness.Inadditiontothepublicationofcompany’sannualreport,whichisconsideredthebasictaskofamanagementaccountant,itbecomesequallyimportantforhimtopreparevarioussupplementaryreportsrequiredbythemanagementtoaddressvariousproblemsandchallengesthatemergeduetochangingandcompetitivebusinessenvironment.

1.4.1 Objectives and Functions of Management Accounting

Thebasicroleofmanagementaccountingistoprovideaccurateandrelevantinformationtotheinternalpartiesofanorganizationfordecisionmaking.To discharge this responsibility effectively,management accounting hastoundertakecollection,processing,analysingandinterpretingofdata,aswellascommunicationoftheresultinginformationtosuchinternalpartieswhointendtousethesameintheirdecisionmakingprocess.Infact, thesaidactivitiescanberecognizedasthebasestoidentifyandexaminethefunctionsofmanagementaccountingandaccordinglythemajorfunctionsaresummarizedbelow:

Data Collection: Thefirst function ofmanagement accounting isto collect the requisite data from all possible resources. Since the datawas traditionally restricted only to economic andfinancial items/factors,managementaccountantswouldmakeuseofthefinancialstatementslikeprofit&lossaccountandbalancesheetforthepurpose.Overthepastfewyears,theactivitiesofmanagementaccountinghavecrossedalltraditionalboundariesbyconsideringnotonlymonetaryitemsandfactorsinitsstudiesbutalsonon-monetaryfactorslike.Suchparadigmshiftintheapproachofthemanagementaccountinghasmadeitsscopemuchwider.Tomeetthegrowingdemandsofthewiderscope,managementaccountingisboundtoutilizebothinternalaswellasexternalsourcesofdatacollection.

Data Processing: The data so collected and stored needs to beconvertedintoinformationthroughprocessing.Dataprocessingreferstotheseriesofactivitiesconsistingofcompilation,classification,tabulationandsummarizationthataimstomakedatainformation.

Analysis and Interpretation:Thedatacollectedfromvariousinternalaswellasexternalsourcesdoesnothaveinherentmeaningandinfact,itsmeaningisgenerally influencedbythenatureandscopeof the toolsandtechniquesusedforitsanalysis.Further,thedataassuchisnotofmuchuseforthemanagementbutitbecomessoonceitisanalysedandinterpretedin

Nature and Scope of Management Accounting

NOTES

Self-Instructional 12 Material

thecontextofthenatureofthedecisions.Thus,theprocessofanalysisandinterpretationmakesthedatasosignificantforthesuccessoftheorganizationthatitisbeingrecognizedasastrategicassetforthecompanyinacompetitivemarket.However,themanagementaccountanthastochoosetherelevantandmostappropriatetechniqueforproperinterpretationofthedataaftertakingintoconsiderationthenatureoftheconcernedproblem.

Communication as a crucial function ofmanagement calls for thetransmissionofinformationtotheconcernedpartiesforuse.Managementaccountingplaysaspecialroleinmanagingtheaffairsofthebusinessbyprovidingnotonly theconventional reports to thedecisionmakersofanorganizationsbutalso in takingnecessarymeasures toensure the supplyofadequateinformationatrighttimetoenablethedecision-makersoftheorganizationtoaddressthechallengesofthechangingenvironment.

Inadditiontobasicfunctionsdiscussedabove,managementaccountingisalsoresponsibletocarryoutsomesecondaryfunctionsthataresummarizedbelow:

Coordinating: Management accounting isoftenentrustedwith theresponsibilitytocoordinatethevariousactivitiesofabusiness.Organizationsgenerallyusetechniquessuchasbudgetingandfinancialreportingforthepurpose.

Special Studies: Contemporary business is operating in a dynamic environmentwhereevenaminorchangeinanyof itselementscanhaveasignificantimpactonthebusinessoutcomes.Therefore,managementisalwaysinterestedtoknowtheareasofbusinesswhichcancontributetothestabilityandprofitabilityoftheconcern.Tomeetthisobjective,managementaccountingcarriesoutvariousspecialstudiessuchassalesanalysis,economicforecasts,pricespreadanalysis,etc.

Tax Administration: In themodern business organizations, taxadministrationisbeingrecognizedasasignificantareaofstudythatfallswithin thescopeofmanagementaccounting.Taxadministrationinvolvestasks like the submission of necessary documents and return to the taxauthorities,includingthesupervisionofallmattersrelatingtotax.

1.4.2 Tools and Techniques of Management Accounting

Management accounting is an information system designed to communicate meaningfuleconomicandfinancialinformationtomanagers,sothattheymaydischargetheirfunctionsefficiently.Itmakesextensiveuseofanumberoftoolsandtechniquestomeettheincreasingneedsofbusiness.Importantamongthemare:

Financial Planning: Planning is necessary not only for betterorganizationalperformanceandprogress,butalso forefficientutilization

NOTES

Self-InstructionalMaterial 13

Nature and Scope of Management Accounting

ofavailableresources.Infact,itisrecognizedasaprerequisiteforfinancialfunctionswhereinfinanceplaysadecidingroleinexecutingthemeffectively.Financial planning is the process of deciding in advance the financialobjectives,policiesandprocedures.Anorganizationcanachievelong-term,aswellasshort-term,financialobjectivesbyemployingfinancialplanning.Intheshortterm,itcanhelpaconcerninmeetingitsobligationsbybalancingtheflowoffunds.Atthesametime,itsproperapplicationcanensureefficientutilizationofavailablefinancialresourcesinthelongterm.

Analysis of Financial Statement: Financialstatementanalysisisagrowingandeverchangingsetofsystemsandproceduresdesignedtoprovidedecisionmakerswith relevant informationderived frombasic sourcesofdata such as companyfinancial statements andgovernment and industrypublications.Overtheyears,anumberoftechniqueshavebeendevisedtoanalysefinancialstatementse.g.,comparativefinancialstatements,common-sizestatements,ratioanalysis,trendanalysisandfundflowstatement.

Cost Accounting: Costaccountingisavitalpartof theaccountingsystem.Itincludesrecording,classifying,analysisandreportingofallcostfacetsinacompany’sperformance.Costaccountingprocedureshavetobedesignedcarefullyaftertakingintoconsiderationthenatureandrequirementsofthebusinessandthedatarequiredatthedifferentlevelsofmanagementforeffectivecostcontrolandcostreduction.

Standard Costing: Anothermajor technique commonly used bythe organizations for exercising control is standard costing.Under thisarrangementstandardcostsareusedtocontrol themajoractivitiesof thebusiness.Standardcostsarepredeterminedtargetsagainstwhichactualresultsareevaluated.Thisisthebasisforasystemofmanagementcontrolforwhichthepropermonitoringofperformanceisakeyfactor.Thevariancesbetweenstandardandactualcostsarecomputedandreportedtomanagement.

Marginal Costing: Marginalcostingisamanagerialtechniquethatconsiders only variable cost in the decisions concerningwith additionaloutput.Itisareportingsystemthatvaluesinventoryandcostofsalesatitsmanufacturingvariablecost.Itisfrequentlyusedaninternalmanagementreporting system.

Budgetary Control: Budgetarycontrolreferstoasystemofbusinesscontrol that usesbudgets to control themajor activitiesofbusiness.Thebudgetsforallmajoractivitiesofthebusinessarepreparedinadvanceandtheactualoperationsarecarriedoutinaccordancewiththebudgetestimates.Generallythebudgetsarepreparedbyupdatingthepreviousyear’sfiguresinthelightofsomeforwardprojections.

Funds Flow Analysis: Fundsflowanalysisattemptstohighlightthecausesofchangeinthefinancialpositionofabusinessenterprisebetween

Nature and Scope of Management Accounting

NOTES

Self-Instructional 14 Material

twobalancesheetdates.Anystatementpreparedforthispurposereferstoasfundsflowstatement.Afundsflowstatementhelpsmanagersintheefficientmanagement of funds.

Management Reporting: Management reporting is considered as an essentialcomponentofawelldesignedplanningandcontrolsystem.Decisionmakersfrequentlyrequireinformationonvariousaspectsofbusiness.Thus,itistheresponsibilityofthemanagementaccountanttocommunicatetherequiredinformationtomanagementattherighttimeandinarightmanner.

Statistical Analysis: Accountantsfrequentlyconfrontmassesofdatafromwhichtheyhavetodrawsystematicandlogicalconclusions.Statisticalanalysisingeneralandsamplingtheoryinparticularprovidesthemascientificmethodtodrawreliableandvalidconclusionsaboutthepropertiesofanentirepopulationbystudyingonlyachosensampleofthepopulation.

1.5 MERITS AND LIMITATIONS

In this section, let’s discuss themerits and limitations ofmanagementaccounting.

Merits of Management Accounting

Managementaccountingoffersthefollowingbenefitstotheorganizations: • Itincreasestheefficiencyinbusinessactivities. • Itensuresefficientregulationofbusinessactivitiesbyestablishingan

efficientsystemofplanningandbudgeting. • Itmakespossibletheefficientutilizationoftheavailableresourcesand

therebyincreasethereturnoncapitalemployed. • It ensures effective control by comparing actual resultswith the

standards. • Ithelpsmaintaingoodrelationswiththepublicbyprovidingquality

servicetothecustomers. • Itprovidesthemeanstomotivatetheemployees. • It keepsmanagers informed about the ongoingoperations, thereby

enablingthemtosuggestremedialmeasuresincaseofdeviations. • It helps in evaluating the efficiency and effectiveness of the

organization’sbusinesspoliciesbyincorporatingmanagementaudit.

Limitations of Management Accounting

Despitethebenefitsmentionedabove,managementaccountingsuffersfromseveraldrawbacks: •Managementaccountingusesdata thatareavailable fromfinancial

statements.Thus,thevalidityofthedecisionslargelydependsonthe

NOTES

Self-InstructionalMaterial 15

Nature and Scope of Management Accounting

reliabilityofthehistoricaldataasobtainedfromconventionalfinancialstatements.Anydrawbackinsuchstatementsisboundtoaffecttheeffectivenessofthedecision.

•Theapplicationofmanagementaccountingtoolsandtechniquesrequiresknowledgeaboutvarioussubjectslikeaccounting,costing,economics,taxation,statisticsandmathematics,engineeringandmanagement.Tofindamanagerintheorganizationwithacomprehensiveknowledgeofallthesesubjectsisalmostimpossible.

•Thoughmanagementaccountingattemptstoanalysebothqualitativeandquantitativefactorsthatinfluenceadecision,theelementofintuitioninmanagerialdecisionhasnotbeencompletelyeliminated.Thereisatendencyamongbusinessexecutivestouseashort-cutapproachtomanagerialproblemsratherthanthelengthyprocessasrequiredbythescientificanalysisprescribedbymanagementaccounting.

•The installationofmanagementaccountingsystemrequiresahugeinvestmentbothintermsofmoneyandmanpower.Therefore,smallerconcernsmaynotbeabletoaffordit.

•Managementaccountingisintheprocessofevolutionandassuchitstillhastogothroughmanydevelopmentalprocessesbeforereachingafinalstage.Consequently,thetechniquesofmanagementaccountinglackthesharpnessandfluiditythatisrequiredofanefficientsystem.Eventheanalysisandinterpretationconsiderablydifferfromorganizationto organization.

•Themanagementsystemcannotbereplacedbyasystemofmanagementaccounting,asthelattersystemsimplyprovidesthenecessarydataforadecisionandnotthedecisionitself.

•Theprincipleofobjectivityisnotalwaysfollowedinitsrealspiritinmanagementaccountingasthecollectionandanalysisareconsiderablyinfluencedbythepersonalbiasofthemanagementaccountant.

1.6 CHANGING ROLE AND TASKS OF MANAGEMENT ACCOUNTANTS

Traditionally,theroleofthemanagementaccountanthasbeenofafacilitatorresponsibleforprovidingsufficientaccountinginformationtothedecision-makers in an organization.Therefore, themanagement accountantwasresponsible fordevisingandoperatinganaccounting informationsystemthatwascapableofcollecting,processing,interpretingandcommunicatingtheaccountinginformationforusewithintheorganizationwiththeaimofattaining organizational efficiency and effectiveness.Thus, traditionally,thejobofthemanagementaccountantinanorganizationasadvocatedby Williamson(2003),hasrevolvedaroundthefollowingmajoractivities:

Nature and Scope of Management Accounting

NOTES

Self-Instructional 16 Material

•Accountingforproductvaluationandpricing •Policyformulationandplanning •Decisionmaking •Costcontrol

Recent developments in information technology, accompanied bytheemergenceofknowledgemanagement,arapidlychangingcompetitiveenvironment and increasingglobalization of business have led corporatehouses to introduce strategic orientation in their planning process.Thechangeinorientationisboundtobringadrasticchangenotonlyinthenatureandscopeofmanagementaccountingbutalsointhetaskandroleof themanagementaccountantinbusinessorganizations.Realizingtheneedtobringchangesintheroleofmanagementaccountants,SiegelandSorensenstatethattheroleofaccountantsshouldcontinuallyevolvetoremainrelevantinthechangingbusinessenvironment.Thetraditionalroleofthemanagementaccountant,which has been restricted to the supplier of operational andfinancialinformationwithintheorganization,isnolongersufficienttomeetthegrowingdemandsofachangingbusinessenvironment.Therefore,themanagement accountnt needs to grow into a high-level decision supportspecialistwhowould help a company in strategicmanagement efforts.Thus,theemergingroleofamanagerialaccountantwillbequitedifferentfromhistraditionalroleinthesensethathehastobeanactiveparticipantinthedecisionmakingprocess,alongwiththefunctionalmanagersinanorganization.Suchparticipationwillnotonlymakehimamemberofafirm’sfunctional teamthat is responsibleforvaluecreationbutalsochange thenatureofhisjobfroma‘staff’toa‘businesspartner’.

Thenewroleofthemanagementaccountant,whichcallsforachangenotonlyinthetaskbutalsoinhisstatuswithinanorganization,hasbeencapturedbymanyscholarsas:

Management accountantswill get a number of opportunities to initiateand execute specific actions to address the changes in the global economicenvironment.The traditional roleofprovidingaccurate, timelyand relevantinformation of amanagement accountantwill be replaced by awider andvibrantrolewherehewillbeanactiveparticipantinthestrategicprocessofan organization.

Thebelow-mentionedcommentsofSiegelandKuleszaaboutthenewroleofmanagementaccountantarenotdifferentfromtheabove-mentionedviews:

Managementaccountantsarebusinesspartnerswiththeircustomers(managersinoperatingorserviceunits),internalconsultantsandorganizationaleducators.

These views are also supplemented by the remarks of Siegel andSorensen,whosaidthatthecharacterizationofmanagementaccountantsinleading-edgecompanieshasgonefrom‘beancounter’and‘corporatecop’on

NOTES

Self-InstructionalMaterial 17

Nature and Scope of Management Accounting

theperipheryofbusinessdecisionmaking,to‘businesspartner’and‘valuedteammember’attheverycentreofstrategicactivity.

Thus,theemergingroleofmanagerialaccountantwillbequitedifferentfromhistraditionalroleinthesensethathewillbeactiveparticipantinthedecisionmakingprocessalongwithfunctionalmanagersinanorganization.Suchparticipationwillnotonlymakehimamemberofafirm’sfunctionalteamthatisresponsibleforvaluecreationbutalsochangethenatureofhisjobfroma‘staff’ toa‘businesspartner’.Thechangeintheroleofmanagementaccountantontheonehandwillwidenthehorizonofhisjobandontheotherhandwillmakehisjobmoredemandingintermsofpotentialandskills.Thenewrole,infact,willprovidethemanagementaccountantmoreopportunitiestoexplorehispotentialinmeetingtheexpectationsofthestakeholdersinanorganization.However,toaddresstheemergingchallengesofthenewrole,themanagementaccountantmustbeadaptablewithsufficientknowledgeofarangeofrelevantdisciplinessoastobeabletoprovidetherightinformationattherighttime.

Tocompeteandgrowinahighlycompetitiveandcomplexbusinessenvironment of the future, organizations need to develop capacity andcompetence to create and deliver superior delivered value to customersanduse the same as a sustainable competitive advantage.Consequently,managementaccountantsareboundtohelptheirorganizationsnotonlyinmeasuringthecostofoperationaccuratelybutalsoinidentifyinganddevisingthemeansforeliminatingnon-valueaddedcostswhichtheywillbeabletodoonlyiftheypossessadequateknowledgeofthevalue-creatingprocessoftheirrespectiveorganizations.Whilecommentingontheopportunitiesofenhancingthevalueofafirm’soutput,Cooperstatesthatcostmanagement,likequality,hastobecomeadisciplinepractisedbyvirtuallyeverypersoninthefirm.Sincetheeffectiveuseofcostmanagementtechniquescallsfortheapplicationoftoolsandtechniquesnotonlyfrommanagementaccountingbutalsofromengineeringandotherfunctionalareasofmanagement, thetaskofmanagementaccountantshasbecomemultifaceted,whichdemandsknowledge of projectmanagement andmanufacturing processes.Thus,managementaccountantsneedtopossesssufficientknowledgeofthelatestcosting tools and techniques like target costing, activity-based costing,throughputcosting,strategiccostmanagement,kaizencostingandbalancedscorecard.

1.6.1 Management Accountant in an Organization

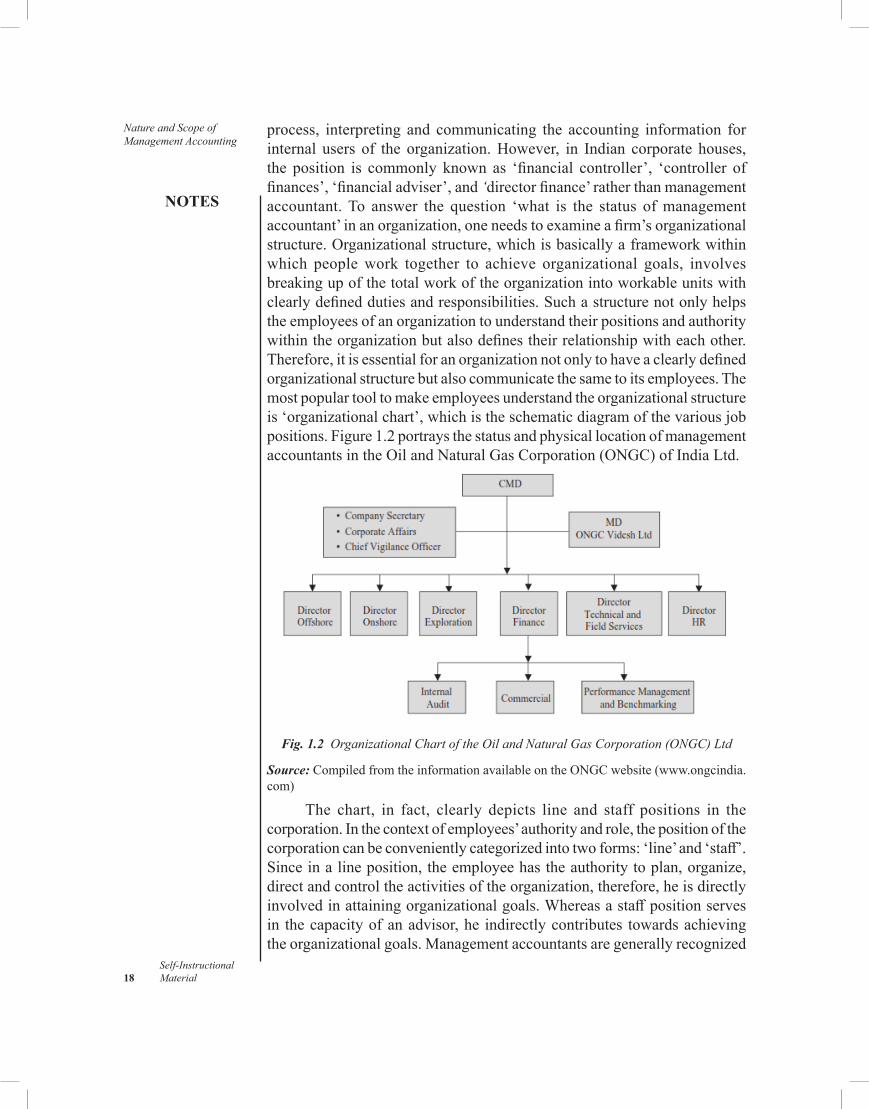

Thequestions that generally strike themindof a studentwhile studyingmanagementaccountingare(i)whoisamanagementaccountant?and(ii)whatishisstatusintheorganization?Amanagementaccountantoccupiesapivotalposition in theorganizationand is responsible fordevisingandoperatinganaccounting informationsystemthat iscapableofcollecting,

Nature and Scope of Management Accounting

NOTES

Self-Instructional 18 Material

process, interpreting and communicating the accounting information forinternal users of the organization.However, in Indian corporate houses,the position is commonly known as ‘financial controller’, ‘controller offinances’,‘financialadviser’,and‘directorfinance’ratherthanmanagementaccountant.To answer the question ‘what is the status ofmanagementaccountant’inanorganization,oneneedstoexamineafirm’sorganizationalstructure.Organizationalstructure,whichisbasicallyaframeworkwithinwhich peoplework together to achieve organizational goals, involvesbreakingupofthetotalworkoftheorganizationintoworkableunitswithclearlydefineddutiesandresponsibilities.Suchastructurenotonlyhelpstheemployeesofanorganizationtounderstandtheirpositionsandauthoritywithintheorganizationbutalsodefinestheirrelationshipwitheachother.Therefore,itisessentialforanorganizationnotonlytohaveaclearlydefinedorganizationalstructurebutalsocommunicatethesametoitsemployees.Themostpopulartooltomakeemployeesunderstandtheorganizationalstructureis‘organizationalchart’,whichistheschematicdiagramofthevariousjobpositions.Figure1.2portraysthestatusandphysicallocationofmanagementaccountantsintheOilandNaturalGasCorporation(ONGC)ofIndiaLtd.

Fig. 1.2 Organizational Chart of the Oil and Natural Gas Corporation (ONGC) Ltd

Source: CompiledfromtheinformationavailableontheONGCwebsite(www.ongcindia.com)

The chart, in fact, clearly depicts line and staff positions in thecorporation.Inthecontextofemployees’authorityandrole,thepositionofthecorporationcanbeconvenientlycategorizedintotwoforms:‘line’and‘staff’.Sinceinalineposition,theemployeehastheauthoritytoplan,organize,directandcontroltheactivitiesoftheorganization,therefore,heisdirectlyinvolvedinattainingorganizationalgoals.Whereasastaffpositionservesin thecapacityofanadvisor,he indirectlycontributes towardsachievingtheorganizationalgoals.Managementaccountantsaregenerallyrecognized

NOTES

Self-InstructionalMaterial 19

Nature and Scope of Management Accounting

asstaffpositionsthataredevoidoftheformalrighttomakedecisionsandas suchhavenodirect responsibility for accomplishing theobjectivesofan organization.Therefore,management accountants aremeant to assistfunctionalmanagersincarryingoutthetasksthatarenecessaryforattainingthegoalsoftheorganization.However,theaccountantspossesstheauthorityovertheirstaffdeployedintheirrespectiveunits.

Itmust be understood thatmanagement accountants in India aregenerallymembersofstrategicteamsinlargeorganizations.Infact, theyhavetheresponsibilityofprovidingrelevantandtimelydatatotheteaminorderhelpitinplanningandcontrollingactivitiesoftheorganization.

Check Your Progress

3.What is the special role played bymanagement accounting inmanagingtheaffairsofthebusiness?

4.Howdoestheelementofintuitionaffectmanagementaccounting? 5.Mention the activities around which the traditional job of

managementaccountingrevolvedasperWilliamson.

1.7 ANSWERS TO CHECK YOUR PROGRESS QUESTIONS

1. Inflation accounting attempts to identify certain characteristics ofaccountingthattendtodistortthereportingoffinancialresultsduringperiodsofrapidlychangingprices.

2.Financialaccountingstatementsarepreparedattheendofthefinancialperiodwhichisusuallyaperiodof12monthswhereasmanagementaccounting reports and statements are prepared at regular intervalsdependinguponthedemandofthedecision-maker.

3.Managementaccountingplaysaspecialroleinmanagingtheaffairsof the business by providing not only the conventional reports tothedecisionmakersofanorganizationbutalsointakingnecessarymeasurestoensurethesupplyofadequateinformationatrighttimetoenablethedecision-makersoftheorganizationtoaddressthechallengesofthechangingenvironment.

4.Theelementofintuitionismanagerialdecisionhasnotbeencompletelyeliminated.Thereisatendencyamongbusinessexecutivestouseashort-cut approach tomanagerial problems rather than the lengthyprocessasrequiredbythescientificanalysisprescribedbymanagementaccounting.

Nature and Scope of Management Accounting

NOTES

Self-Instructional 20 Material

5.Traditionally,thejobofmanagementaccountantinanorganizationasadvocatedbyWilliamson(2003),hasevolvedaroundthefollowingmajor activities:• Accountingforproductvaluationandpricing• Policyformulationandplanning• Decisionmaking• Costcontrol

1.8 SUMMARY

•Management accounting is a segment of accounting that dealsspecificallywith the accounting and reporting of information tomanagementregardingthedetailedoperationsofthecompanyinorderfordecisionstobetakeninvariousareasofbusiness.

•Apersoncangainmeaningfulinsightsandconclusionsaboutthefirmwiththehelpofanalysisandinterpretationoftheinformationcontainedinfinancialstatements.

•Budgetingisameansofcoordinatingactivitieswiththeco-operationofthosewhoseektoachieveacommongoal.

• Inflation accounting attempts to identify certain characteristics ofaccountingthattendtodistortthereportingoffinancialresultsduringperiodsofrapidlychangingprices.

•Clear,informative,timelyreportsareessentialmanagementtoolsinreachingdecisionsthatmakethebestuseofacompany’sresources.

•Quantitativeanalysismethodsallowmanagerstodevelopinformationfromtheirfinancialdatabasethatisnot,otherwise,available.

•Taxationplaysanimportantroleintheprofitabilityofacommercialconcern.

• Internal audit as a discipline ofmanagement accountingmakesarrangements for performance appraisal of the company’s variousdepartments.

•Todischargetheresponsibilityeffectively,managementaccounting,therefore, has to carry out not only the activities like collection,processing,analysingandinterpretingofthedatabutalsocommunicatingtheresultinginformationtosuchinternalpartieswhointendtousethesameintheirdecisionmakingprocess.

•Management accounting helps an organization in the process ofmanagement,which generally consists of activities like planning,organizing,evaluatingandcommunicating.

NOTES

Self-InstructionalMaterial 21

Nature and Scope of Management Accounting

• Financialplanningistheprocessofdecidinginadvancethefinancialobjectives,policiesandprocedures.

•Financial statement analysis is a growing and ever changing setof systems and procedures designed to provide decisions-makerswith relevant information derived from the basic sources of datasuchascompanyfinancialstatementsandgovernmentandindustrypublications.

•Standardcostsarepredeterminedtargetsagainstwhichactualresultsareevaluated.

•Marginalcostingisamanagerialtechniquethatconsidersonlyvariablecostintheadditionaloutputdecisions.

•Budgetary control refers to a systemof business control that usesbudgetstocontrolthemajoractivitiesofbusiness.

•Fundsflowanalysisattemptstohighlightthecausesofchangeinthefinancialconditionofabusinessenterprisebetweentwodates.

•Managementreportingisconsideredanessentialcomponentofawell-designedplanningandcontrolsystem.

• In his new role, themanagement accountantwill providemoreopportunitiestoexplorehispotentialinmeetingtheexpectationsofthestakeholdersinanorganization.

•Amanagementaccountantisresponsiblefordevisingandoperatinganaccountinginformationsystemthatiscapableofcollecting,processing,interpretingandcommunicatingaccountinginformationforinternalusersoftheorganization.

1.9 KEY WORDS

•Management accounting: It is a segment of accounting thatdeals specificallywith the analysis and reportingof information tomanagementabouttheoperationsoftheorganizationwithanobjectivetofacilitatedecisionmaking.

•Financial accounting:Itisagrowingdisciplinewhichhelpstoregulateasystemthatiscapableofrecording,classifyingandsummarizingthemercantiletransactionsoccurringinanorganization.

•Budgeting: It refers to a systematic plan for the utilization oforganizationalresources.

•Data processing: It refers to the series of activities consisting ofcompilation,classification,tabulationandsummarizationthataimstomakedatainformation.

Nature and Scope of Management Accounting

NOTES

Self-Instructional 22 Material

1.10 SELF ASSESSMENT QUESTIONS AND EXERCISES

Short-Answer Questions

1.Whatismanagementaccounting?Howisitdifferentfromfinancialaccounting?

2.Brieflydiscussthescopeofmanagementaccounting. 3.Statetheobjectivesandlimitationsofmanagementaccounting.

Long-Answer Questions

1. ‘Managementaccountingisthepresentationofaccountinginformationin such away as to assist themanagement in decisionmaking.’Comment.

2.Discussindetailthefunctionsofmanagementaccounting. 3.Explainthetoolsofmanagementaccounting. 4. ‘Management accounting can be viewed asmanagement oriented

accounting.’Comment. 5. Identifyandexaminethechangingroleofthemanagementaccountant

in contemporary business.

1.11 FURTHER READINGS

Sahaf,M.A.2013.Management Accounting: Principles and Practice,3rdedition.NewDelhi:VikasPublishingHouse.

Arora,M.N.2012.A textbook of Cost and Management Accounting,10thedition.NewDelhi:VikasPublishingHouse.

Maheshwari,S.N.,SuneelK.andSharadK.2018.A Textbook of Accounting for Management,4thedition.NewDelhi:VikasPublishingHouse.

NOTES

Self-InstructionalMaterial 23

Financial Statements AnalysisUNIT 2 FINANCIAL STATEMENTS

ANALYSISStructure 2.0 Introduction 2.1 Objectives 2.2 NatureofFinancialStatements

2.2.1 LimitationsofFinancialStatements 2.2.2 MeaningofAnalysis 2.2.3 StepsInvolvedinFinancialStatementsAnalysis 2.2.4 TechniquesofAnalysis

2.3 ComparativeFinancialStatements 2.4 Common Size Statement 2.5 TrendAnalysis 2.6 AnswerstoCheckYourProgressQuestions 2.7 Summary 2.8 Key Words 2.9 SelfAssessmentquestionsandExercises 2.10 FurtherReadings

2.0 INTRODUCTION

Thefundamental,clearanddefiniteunderstandingoffinancialstatementsisrecognizedasaprerequisiteforanaccurate,completeandrelevantfinancialdecision.However,thisdoesnotmeanthatdecisionmakerslikeabusinessexecutive,commercialorinvestmentbanker,orinvestor,speculator,businesscounsellor, mercantile creditman, or financial analyst need tomasterthemselvesinthepreparationofthesestatements.Infact,qualifiedfinancialaccountants capable of preparing such statements are available almosteverywhere in theworld.But the unchallenged ability to interpret thesefinancialstatementsintelligentlyandaccuratelyareessentialtounderstandthefinancialstatusandperformanceofabusiness.

Inthisunit,youwilllearnaboutsometoolsoffinancialstatementanalysis.

2.1 OBJECTIVES

Aftergoingthroughthisunit,youwillbeableto: •Describethemeaning,limitations,stepsandtechniquesoffinancial

statementanalysis •Explaintheconceptofcomparativestatement •Discussthepreparationofcommonsizestatement •Examinethemethodoftrendpercentageasatooloffinancialstatement

analysis

Financial Statements Analysis

NOTES

Self-Instructional 24 Material

2.2 NATURE OF FINANCIAL STATEMENTS

Financialstatementsenableareadernotonlytomeasurebusinessresultsof an organization but also to assess its financial position; hence, theyare generally predictive by nature. Such statements contain not onlysufficientbutalsovaluableinformationabouttheorganizationthatwouldhelpmanagersindecisionmaking.ThenatureoffinancialstatementswasadmirablysummarizedontraditionalgroundsanumberofyearsagobytheAmericanInstituteofCertifiedPublicAccountants,1936 inthefollowinglines:Financial statements are prepared for the purposes of presenting a periodical review or report by the management and deal with the status of the investment in the business and the results achieved during the period under review.

Thus,financial statements are reporting instruments that provide asummaryoftheaccountingdataofanorganization’sbusinesspertainingtoaspecificaccountingperiod.Theobjectivesofsuchstatementsaresummarizedbelow:

• Tomeasureanorganization’sbusinessresultsandassessitsfinancialposition;

• Topresenttrueandfairviewofthebusiness;• Torevealimplicationsofoperatingprofitonthefinancialposition

of a concern;• Toprovidesufficientandrelevantfinancialinformationtovarious

partiesinterestedinfinancialstatementanalysis;and• Toserveasthebasisforfutureplanningandstrategy.Generally,financialstatementsrefertoatleasttwostatementswhichan

organizationpreparesattheendofagivenperiodoftime.Thesestatementsare:

• Profitandlossaccounts;and• BalancesheetInaddition to theabove-mentionedstatements,manyorganizations

prepare the following twofinancial statements inorder to strengthen theaccounting information system:

• Profit and Loss Appropriation Account: Anaccountthatshowsthedistributionofprofitisknownasprofitandlossappropriationaccount.Generallythisaccounthasthesameformat,i.e.,‘T’form,asisfollowedincaseofprofitandlossaccount.Thecurrentprofitof thebusiness(that is transferredfromprofitandlossaccount)alongwiththebalanceofprofit,ifany,ofthepreviousyearappear

NOTES

Self-InstructionalMaterial 25

Financial Statements Analysis

on the credit sideof the account.Thedebit sideof the accountshowsappropriationtransactionslikedividend,incometax,generalreserve,etc.Aspecimenofthisaccountisgivenbelow:

Profit and Loss Appropriation Account

` `

Proposeddividend xxx Balanceat…… xxxProvisionforincome-tax xxx Profit(TransferredfromP&LA/c) xxxGeneralreserve xxxBalancec/d xxx

xxxx xxxx

• Statement ofChanges inFinancial Position The statement ofchanges infinancial position, often referred to as ‘FundsFlowStatement’,providesinformationabouttheflowoffund(workingcapital)duringaparticularperiod.Italsoprovidesinformationaboutthefinancialandinvestingactivitiesofabusinessenterprise.Suchastatementexplainsthecauseofchangeinthefinancialposition(balancesheet)fromthebeginningoftheperiodtotheendoftheperiod.

Since thestudentsneed topossessknowledgeabout thenatureandstructureofprofitandlossaccountandbalancesheetbeforetheyanalysesuchstatementsforagivenpurpose,inthesubsequentsectionsofthischapteranattempthasbeenmadeinthisdirection.

Profit and Loss Account

Profit and loss account reports the results of business activities for anaccountingperiod.Suchanaccountnotonlyrevealsthedetailsoftheincomeandexpenditureofabusinessorganizationoveraperiodoftimebutalsocomparethemwitheachotherwithanobjectivetofindthedeviationwhichrepresents theamountofprofitor loss for theperiod. If incomeexceedsexpenditurethedifferenceiscallednetprofitandincaseexpenditureexceedsincome,thedifferenceiscallednetloss.Dataconcerningsales,costofgoodssold,returnsandallowances,sellinganddistributionexpensesandnetincomearenormallypresentedin theprofitandlossaccount.Theprofitandlossaccountsometimesiscalledincomestatementortheoperatingstatement.

There isnospecificproformafor thepreparationofprofitand lossaccount.However, the proformagivenbelow is commonlyused for thispurpose:

Financial Statements Analysis

NOTES

Self-Instructional 26 Material

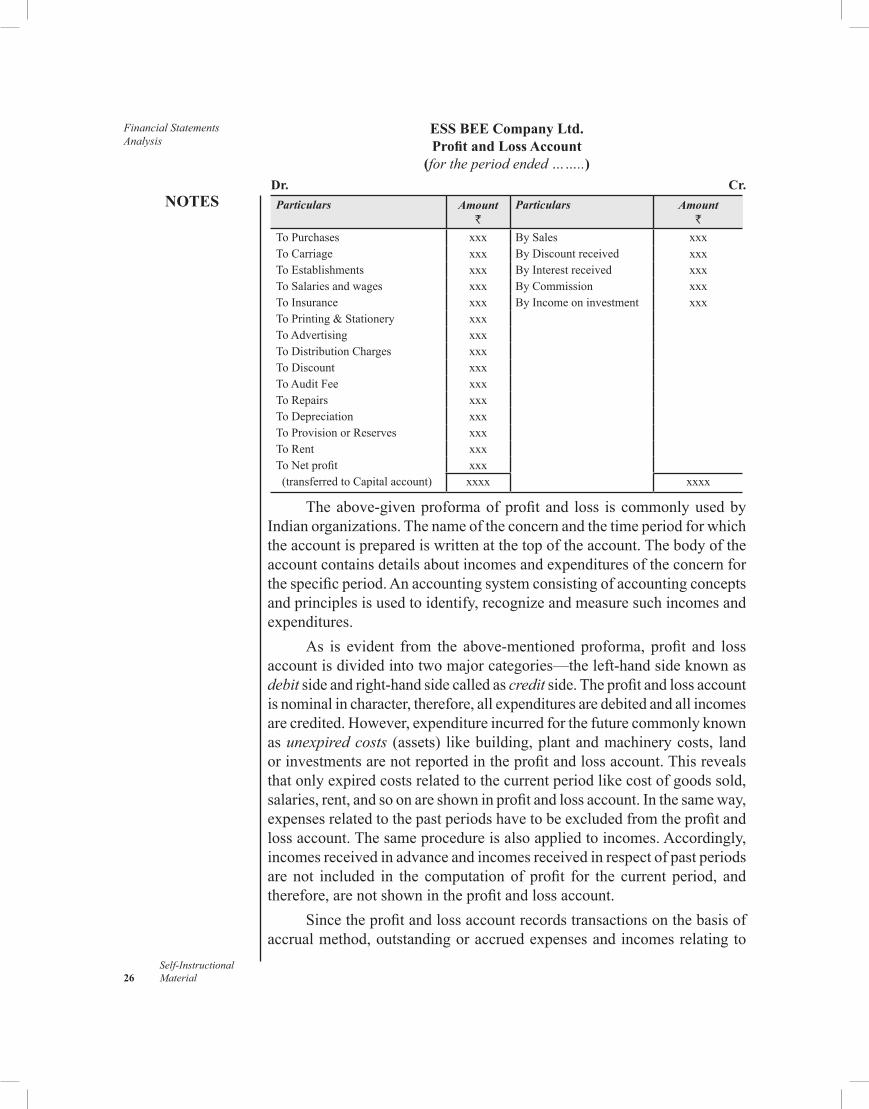

ESS BEE Company Ltd. Profit and Loss Account

(for the period ended ……..) Dr. Cr.

Particulars Amount`

Particulars Amount`

ToPurchases xxx BySales xxxTo Carriage xxx ByDiscountreceived xxxToEstablishments xxx ByInterestreceived xxxToSalariesandwages xxx ByCommission xxxTo Insurance xxx ByIncomeoninvestment xxxToPrinting&Stationery xxxTo Advertising xxxToDistributionCharges xxxTo Discount xxxToAuditFee xxxToRepairs xxxTo Depreciation xxxToProvisionorReserves xxxToRent xxxToNetprofit xxx (transferredtoCapitalaccount) xxxx xxxx

Theabove-givenproformaofprofitand loss iscommonlyusedbyIndianorganizations.Thenameoftheconcernandthetimeperiodforwhichtheaccountispreparediswrittenatthetopoftheaccount.Thebodyoftheaccountcontainsdetailsaboutincomesandexpendituresoftheconcernforthespecificperiod.Anaccountingsystemconsistingofaccountingconceptsandprinciplesisusedtoidentify,recognizeandmeasuresuchincomesandexpenditures.

As is evident from the above-mentionedproforma, profit and lossaccountisdividedintotwomajorcategories—theleft-handsideknownasdebit sideandright-handsidecalledascredit side.Theprofitandlossaccountisnominalincharacter,therefore,allexpendituresaredebitedandallincomesarecredited.However,expenditureincurredforthefuturecommonlyknownas unexpired costs (assets) likebuilding,plantandmachinerycosts, landorinvestmentsarenotreportedintheprofitandlossaccount.Thisrevealsthatonlyexpiredcostsrelatedtothecurrentperiodlikecostofgoodssold,salaries,rent,andsoonareshowninprofitandlossaccount.Inthesameway,expensesrelatedtothepastperiodshavetobeexcludedfromtheprofitandlossaccount.Thesameprocedureisalsoappliedtoincomes.Accordingly,incomes received in advance and incomes received in respect of past periods are not included in the computationof profit for the current period, andtherefore,arenotshownintheprofitandlossaccount.

Sincetheprofitandlossaccountrecordstransactionsonthebasisofaccrualmethod,outstandingoraccruedexpensesandincomesrelatingto

NOTES

Self-InstructionalMaterial 27

Financial Statements Analysis

thecurrentperiodbutnotyetpaidorreceivedaretobereportedinprofitandlossaccount.

Balance Sheet

Theprofitandlossaccountdiscussedabovedepictstheincomeandexpenditurefor a specificaccountingperiod,but it fails to indicate thepositionof theorganizationintermsofitsassetsandliabilities.Topresentsuchaninformation,anaccountingframeworkisrequiredwhichisknownasthebalance sheet. Thebalancesheetisastatementofthefinancialpositionofanenterpriseasatagivendatewhichexhibitsitsassets,liabilities,capital,reservesandotheraccountbalancesattheirrespectivebookvalues(ICAI,1983).

Thus,balancesheetisastatementwhichdisclosesthefinancialstatusofanorganizationconsistingofthevaluesassignedtoitsassets,liabilities,andowner’sequity,ataspecifictime.Itcontainstwosides,viz.,liabilitiesandassets.

Liabilities denote the amountwhich a business owes to others ondifferentaccounts.Itrepresentsclaimsofcreditorsandequityoftheowners.Theliabilitiesareusuallydividedintothreemajorcategories:

• Currentliabilitiesrepresentshort-termfinancialobligationswhichare expected to be paidwithin the coming year or the normaloperatingcycle.Sundrycreditors,billspayableandoutstandingexpensesarethebestexamplesofsuchliabilities.

• Long-termliabilitiesareliabilitiesthatarenotexpectedtoberepaidwithinthecomingyearbutareof thelong-termnature.Thus, itincludesdebtsnotfallingdueuntilmorethanayearfromthebalancesheetdate.

• Owner’sequityrepresentstheamountofliabilitiesforwhichownersofabusinesshaveclaim.Itincludessharecapitalandaccumulatedresources.

Assets arethematerialthingsorpossessionsorpropertiesofbusinessincludingtheamountduetoitfromothers.Assetsareusuallyclassifiedintothreemajorcategories:

• Currentassetsrepresentcashplusthoseassets thatareexpectedtobeconvertedintocashorconsumedduringtheyearornormaloperatingcycle,e.g.,stock,sundrydebtors,billsreceivable,etc.

• Fixed asssets are those assetswhich are to be used in businessoperationover a relatively longperiodof time.Such assets areincidental to production such as land and building, plant andmachinery,furnitureandfittings,etc.

• Intangibleassetsalsoknownasfictitiousassetsarenotrepresentedbyanytangiblepossessionorproperty.Theyaredebitbalancesofcertainaccountswhicharenotyetwrittenoffsuchaspreliminaryexpenses,patents,goodwill,etc.

Financial Statements Analysis

NOTES

Self-Instructional 28 Material

Thus,theliabilitiessideshowsourceswherefromfundswereobtainedwhileassetssidedescribesthewayinwhichthefundswereutilized.

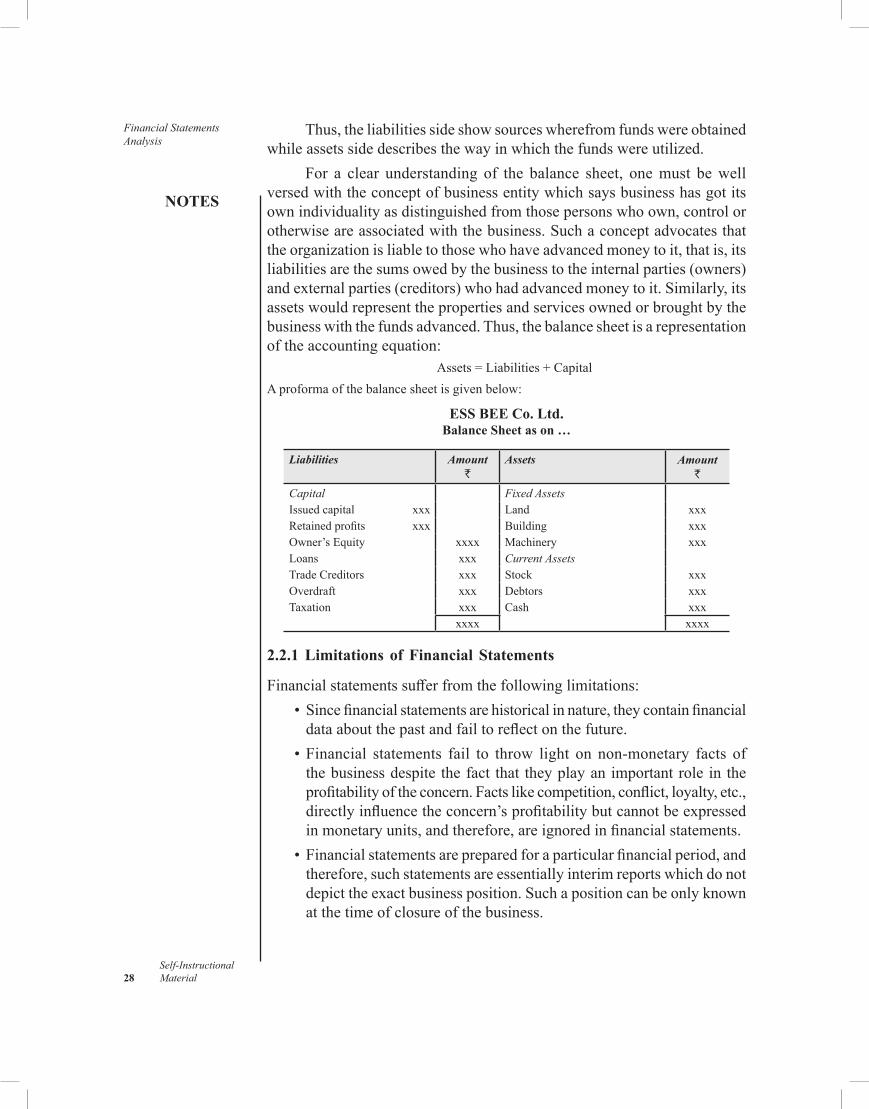

For a clear understanding of the balance sheet, onemust bewellversedwiththeconceptofbusinessentitywhichsaysbusinesshasgotitsownindividualityasdistinguishedfromthosepersonswhoown,controlorotherwiseareassociatedwiththebusiness.Suchaconceptadvocatesthattheorganizationisliabletothosewhohaveadvancedmoneytoit,thatis,itsliabilitiesarethesumsowedbythebusinesstotheinternalparties(owners)andexternalparties(creditors)whohadadvancedmoneytoit.Similarly,itsassetswouldrepresentthepropertiesandservicesownedorbroughtbythebusinesswiththefundsadvanced.Thus,thebalancesheetisarepresentationoftheaccountingequation:

Assets=Liabilities+CapitalAproformaofthebalancesheetisgivenbelow:

ESS BEE Co. Ltd.Balance Sheet as on …

Liabilities Amount`

Assets Amount`

Capital Fixed AssetsIssuedcapital xxx Land xxxRetainedprofits xxx Building xxxOwner’sEquity xxxx Machinery xxxLoans xxx Current AssetsTrade Creditors xxx Stock xxxOverdraft xxx Debtors xxxTaxation xxx Cash xxx

xxxx xxxx

2.2.1 Limitations of Financial Statements

Financialstatementssufferfromthefollowinglimitations: •Sincefinancialstatementsarehistoricalinnature,theycontainfinancial

dataaboutthepastandfailtoreflectonthefuture. •Financial statements fail to throw light on non-monetary facts of

thebusinessdespite thefact that theyplayanimportantrole in theprofitabilityoftheconcern.Factslikecompetition,conflict,loyalty,etc.,directlyinfluencetheconcern’sprofitabilitybutcannotbeexpressedinmonetaryunits,andtherefore,areignoredinfinancialstatements.

•Financialstatementsarepreparedforaparticularfinancialperiod,andtherefore,suchstatementsareessentiallyinterimreportswhichdonotdepicttheexactbusinessposition.Suchapositioncanbeonlyknownatthetimeofclosureofthebusiness.

NOTES

Self-InstructionalMaterial 29

Financial Statements Analysis

•Afinancialstatementisasnearlyastheaccountantcanmakeitso.Therefore,suchstatementsareinfluencedbyhispersonaljudgementswhichdefinitelyaffectthequalityandutilityofthestatements.

•Financialstatementsfailstoreflectthetrueandfairviewofthebusinessasthepreparationofthestatementsisgovernedbyvariousaccountingconcepts and conventionswhich suffer frommanydrawbacks. Forexample,assetsaretoberecordedatcostratherthantheirrealisablevaluewhichdefinitelyhidestherealpositionsoftheconcern.

2.2.2 Meaning of Analysis

Like lines in thepalmorhoroscope,financial statementscanbe studied,puzzledover,andscrutinized(Woelfel,1980).Theanalysisofsuchstatementsprovidevaluableinformationformanagerialdecisions.Financialstatementis—asnearlyasthefinancialexecutivecanmakeitso—simplyareportoffacts.Theutilityofthestatementdoesnotlieintheamountofinformationitcontainsbut intheexpertiseandtheskillof theanalyst toanalyseandinterprettheinformationinthestatementinordertogetthestorybehindthe facts—to readbetween the lines.Financial statement does not speakanythinginandof itself. Itmerelycontainsfinancialdataaboutbusinessevents.Theusergainsmeaningfulinsightsandconclusionsaboutthefirmonlythroughhisownanalysisandinterpretationoftheinformationinthestatements(Woelfel,1908).

Financial statement analysis involves a systematic and carefulexaminationoftheinformationcontainedinthefinancialstatementswithadefinitepurpose.Itisadetailedinquiryintofinancialdatatoevaluateanorganization’sperformance,futurerisksandpotential.Itattemptstodeterminethe significance andmeaningof thebusiness information as depictedbyfinancial statements so that prospects for future earnings, ability to payinterestanddebtmaturities(bothcurrentandlong-term)andprofitabilityofasounddividendpolicymaybeforecast.AccordingtoMyer,1969Financialstatement analysis is largelya study of relationships among the various financial factors in a business, as disclosed by a single set of statements and study of these factors as shown in a series of statements.

Thus,financialstatementanalysisisaprocessofanalysingthefinancialdatainordertojudgetheprofitabilityandfinancialpositionofanorganization.Itistheevaluationoftheeconomicandfinancialdatapresentedinthefinancialstatementsformakingdecisionsandmaintainingcontrol.

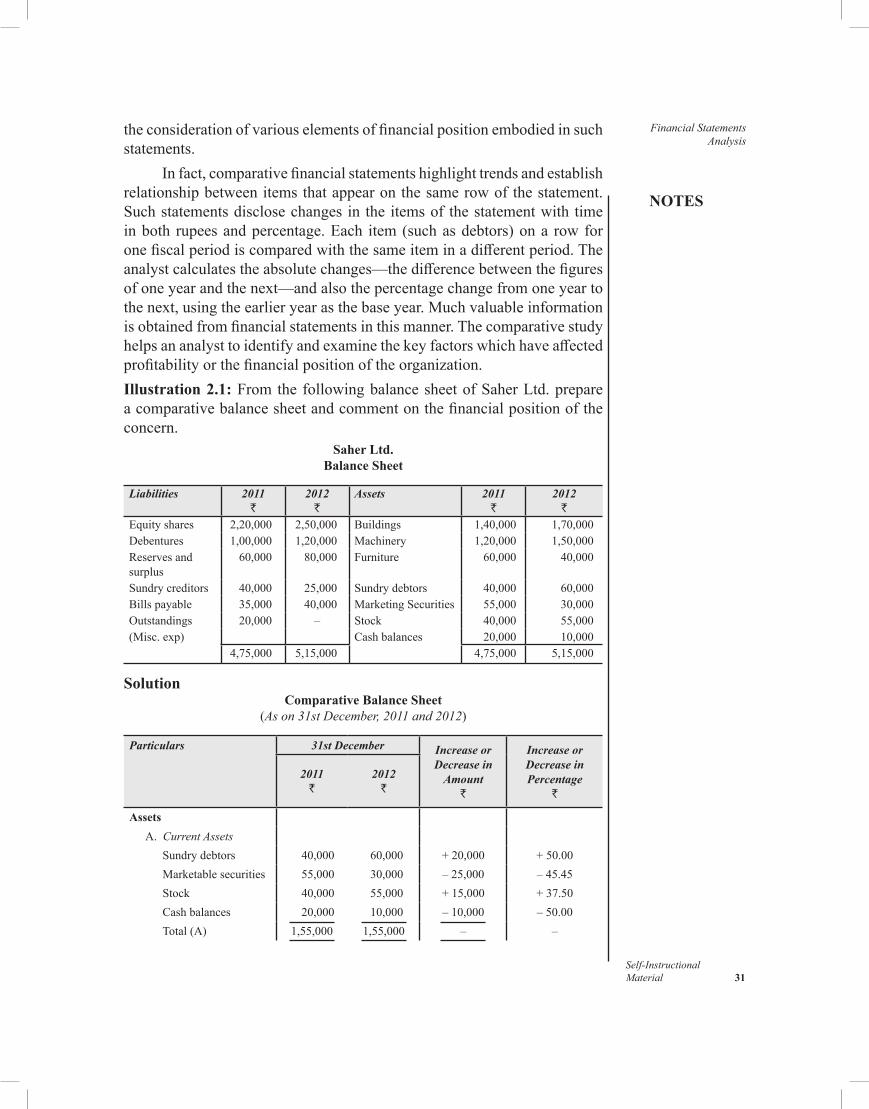

2.2.3 Steps Involved in Financial Statements Analysis

Theprocessoffinancialstatementanalysisconsistsofthefollowingsixsteps: • determinationofscopeandobjectivesofanalysis; • studyoffinancialstatements;

Financial Statements Analysis

NOTES

Self-Instructional 30 Material

• collectionofrelevantinformation; • rearrangementofthedata; • analysisofdatabyanalyticaltechniques;and • interpretation,presentationandpreparationofreports.

2.2.4 Techniques of Analysis

Overthepastfewdecadesanumberoftechniqueshavebeendevelopedfortheanalysisoffinancialstatements.Theselectionofappropriateanalyticaltechnique generally depends upon the purpose of the analysis.Usuallyanalystsprefertousesuchtechniquesincombinationtoensurebetterresults.Thecommonlyusedtechniquesare: • comparativefinancialstatement; • common-sizestatement; • trendanalysis; • ratioanalysis; • fundflowstatements;and • cashflowstatementsInthesubsequentsectionsofthisunit,anattemptismadetodiscussindetailthefirstthreetechniquesi.e.,comparativefinancialstatement,common-sizestatement,andtrendanalysis.However,thelastthreetechniquesi.e.,ratioanalysis,fundflowstatementandcashflowstatementhavebeendiscussedindetailinthesubsequentunits.

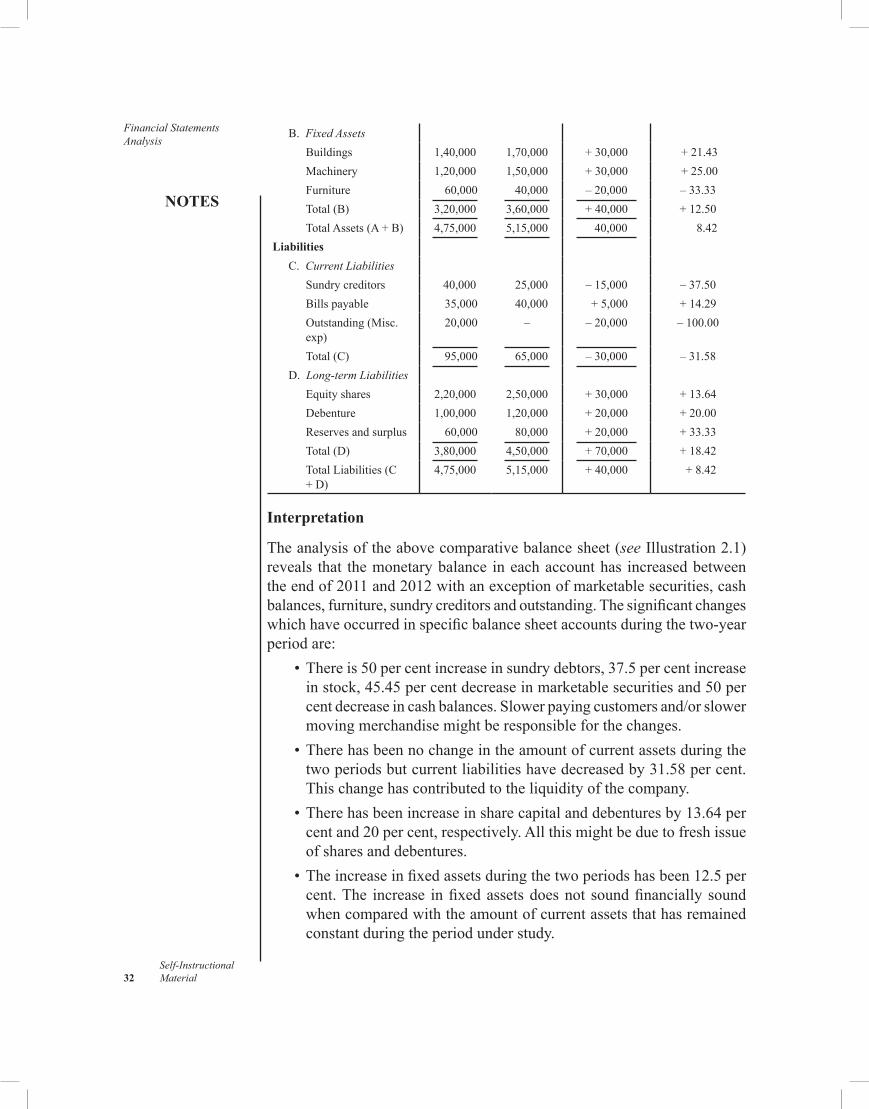

Check Your Progress