Embed Size (px)

Citation preview

• Management Accounting

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting

1 Management accounting

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting

1 Management accounting or managerial accounting is concerned

with the provisions and use of accounting information to managers within organizations, to provide them

with the basis to make informed business decisions that will allow

them to be better equipped in their management and control functions.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting

1 In contrast to financial accountancy information, management accounting

information is:

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Definition

1 According to the Institute of Management Accountants (IMA):

"Management accounting is a profession that involves partnering in management decision making, devising planning and performance management systems,and providing expertise in financial reporting and control to assist management in the

formulation and implementation of an organization's strategy".

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Definition

1 The American Institute of Certified Public Accountants (AICPA) states that management accounting as practice extends to the following

three areas:

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Definition

1 Management accounting knowledge and experience can therefore be obtained from varied fields and

functions within an organization, such as information management,

treasury, efficiency auditing, marketing, valuation, pricing,

logistics, etc.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Traditional vs. innovative practices

1 Within the area of management accounting there are almost an

infinite number of tools, methods, techniques and approaches floating

around.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Traditional vs. innovative practices

1 Traditional standard costing (TSC), used in cost accounting, dates back to the 1920s and is a central method in management accounting practiced today because it is used for financial statement reporting for the valuation

of income statement and balance sheet line items such as cost of

goods sold (COGS) and inventory valuation

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Traditional vs. innovative practices

1 In the late 1980s, accounting practitioners and educators were

heavily criticized on the grounds that management accounting practices (and, even more so, the curriculum taught to accounting students) had changed little over the preceding 60 years, despite radical changes in the

business environment

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Traditional vs. innovative practices

1 RCA was derived by taking the best costing characteristics of the German

management accounting approach Grenzplankostenrechnung (GPK), and combining the use of activity-based drivers when needed, such as those

used in activity-based costing

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Role within a corporation

1 In corporations that derive much of their profits from the information economy, such as banks, publishing houses, telecommunications companies and defence contractors, IT costs

are a significant source of uncontrollable spending, which in size is often the greatest

corporate cost after total compensation costs and property related costs. A function of

management accounting in such organizations is to work closely with the IT department to

provide IT cost transparency.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Role within a corporation

1 Given the above, one widely held view of the progression of the accounting and

finance career path is that financial accounting is a stepping stone to

management accounting. Consistent with the notion of value creation,

management accountants help drive the success of the business while strict

financial accounting is more of a compliance and historical endeavor.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting An alternative view

1 Stated differently, management accounting information is the

mechanism which can be used by managers as a vehicle for the overview of the whole internal structure of the organization to facilitate their control functions

within an organization.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Resource consumption accounting (RCA)

1 Resource consumption accounting (RCA) is formally defined as a dynamic, fully integrated,

principle-based, and comprehensive management accounting approach that

provides managers with decision support information for enterprise optimization. RCA

emerged as a management accounting approach around 2000 and was subsequently

developed at CAM-I the Consortium for Advanced Manufacturing–International, in a

Cost Management Section RCA interest group in December 2001.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Transfer pricing

1 Once transfer pricing is applied and any other management accounting entries or adjustments are posted to the ledger (which are usually memo accounts and are not included in the

legal entity results), the business units are able to produce segment financial results which are used by both internal and external users to

evaluate performance.https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Resources and continuous learning

1 There are a variety of ways to keep current and continue to build one's

knowledge base in the field of management accounting. Certified

Management Accountants (CMAs) are required to achieve continuing

education hours every year, similar to a Certified Public Accountant. A company may also have research

and training materials available for use in a corporate owned library. This

is more common in "Fortune 500" companies who have the resources

to fund this type of training medium.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting Resources and continuous learning

1 There are also numerous journals, on-line articles and blogs available. The journal Cost Management (ISSN

1092-8057) and the Institute of Management Accounting (IMA) site

are sources which includes Management Accounting Quarterly and Strategic Finance publications. Indeed, management accounting is

needed in an organization.https://store.theartofservice.com/the-management-accounting-toolkit.html

Accounting - Management accounting

1 Management accounting focuses on the measurement, analysis and

reporting of information that can help managers in making decisions to

fulfil the goals of an organization. In management accounting, internal

measures and reports are based on cost-benefit analysis, and are not

required to follow GAAP.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Accounting - Management accounting

1 Management accounting produces future-oriented reports—for example the budget for 2006 is prepared in 2005—and the time span of reports

varies widely. Such reports may include both financial and

nonfinancial information, and may, for example, focus on specific

products and departments.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting in supply chains

1 'Management accounting in supply chains' (or supply chain controlling, SCC) is

part of the supply chain management concept. This necessitates planning,

monitoring, management and information about logistics and manufacturing

processes throughout the value chain. The goal of management accounting in supply chains is optimizing these processes. This

strategy focuses on supporting management.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting in supply chains - Requirements

1 The requirements for management accounting in supply chains are

significantly higher than the provision of key figures, but this is a

fundamental task.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting in supply chains - Tasks and functions

1 Management accounting in supply chains has the following

features:

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting in supply chains - Aims

1 Because of different controlling directions, in management

accounting of supply chains different aims are pursued and influence each

other. Again, the challenge is the cross-company factor. Independent

companies must agree on a common strategy for the SCM and define

common aims. Two types of aims exist: direct and indirect.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting in supply chains - Indirect

1 Company-wide, generalized aims may be pursued with management

accounting in supply chains. Examples are competitiveness, expanding cooperation, growth,

market development and greater customer orientation.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting in supply chains - Instruments

1 Management accounting in supply chains draws on modified traditional instruments of

managerial accounting to accomplish cross-company objectives. There are two measuring instruments: the supply-chain mapGardner, T.;

Cooper, M. (2003): “Strategic Supply Chain Mapping Approaches”; in: Journal of Business

Logistics, Vol.24/2, 37–64. and the supply-chain operations reference (SCOR).Poluha, R. (2007): “Application of the SCOR Model in Supply Chain

Management”, Youngstown, New York 2007.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting in supply chains - Cross-company activity-based costing

1 (2000): ““Supply chain management and management accounting: a case

study of activity-based costing”, International Journal of Logistics: Research and Applications, Vol

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management accounting in supply chains - Supply-chain performance-measurement system

1 A primary task of management accounting in supply chains is performance measurement

https://store.theartofservice.com/the-management-accounting-toolkit.html

History of accounting - Financial and management accounting

1 management accounting) and external

(i.e

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles

1 'Management accounting principles (MAP)' were developed to serve the core needs of internal management

to improve decision support objectives, internal business

processes, resource application, customer value, and capacity utilization needed to achieve corporate goals in an optimal

manner. Another term often used for management accounting principles for these purposes is managerial

costing principles. The two management accounting principles

are:

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles

1 These two principles serve the management accounting community and its customers – the management of businesses. The above principles are incorporated into the Managerial

Costing Conceptual Framework (MCCF) along with concepts and constraints to help govern the

management accounting practice. The framework ends decades of

confusion surrounding management accounting approaches, tools and techniques and their capabilities.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles

1 The framework of principles, concepts, and constraints will drive the classification of management

accounting practices in the profession to enable a better understanding both inside the profession and outside, of the compromises that result from

inappropriate principles. Without foundational principles, managers and accounting professionals have no consistent footing on which to

challenge or evaluate new theories of methods for managerial costing.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles

1 The idea that separate management accounting principles exist for managerial decision support distinct from financial reporting needs is now

recognized by professional accounting bodies such as the International Federation of Accountants [http://www.ifac.org/about-ifac/professional-

accountants-business Professional Accountants In Business Committee] and the Institute of

Management Accountants [http://www.imanet.org/resources_and_publication

s/ExposureDraft.aspx Managerial Costing Conceptual Framework (MCCF) Task Force].

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Brief History of 'Principles' in Accounting

1 In contrast, management accounting principles have been overlooked from

both a conceptual and a standards point of view and, for the most part,

overshadowed by financial accounting standards. Generally accepted accounting principles

applies strictly to financial accounting because it was either the only guidance they had at the time,

or did not know what else to do.https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Brief History of 'Principles' in Accounting

1 Over the last century it is more and more evident that management

accounting principles be viewed as indispensable to the evaluation and improvement of MA methods and practices (Clinton, Van der Merwe

2012).

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Historical Timeline ― Establishing Management Accounting Principles

1 Church discussed practices that conveyed the management

accounting principles of causality and analogy but never formally

defined them

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Historical Timeline ― Establishing Management Accounting Principles

1 :'1923 – John Maurice Clark. Studies in the Economics of Overhead Costs'.

Management Accounting theory developed and was embedded in his

cost allocation discussion; Clark stressed the need to consider causes

and their effects. He was also the first to delineate operational cost

concepts from decision cost concepts having introduced the concept of

avoidability.https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Historical Timeline ― Establishing Management Accounting Principles

1 His framework's stated intent was not to cater for Management

Accounting per se but it nevertheless argued for causality as a principle.)

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Historical Timeline ― Establishing Management Accounting Principles

1 :'1983 – Choudhury. [ http://www.tandfonline.com/toc/rabr2

0/current Accounting and Business Research]'. In discussing the

confusion surrounding the lack of common and meaningful

management accounting terminology says, … we are no nearer to being

provided with a coherent theory of, if you like, a conceptual framework for

management accounting. Choudhury did not; however, propose

a management accounting conceptual framework.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Historical Timeline ― Establishing Management Accounting Principles

1 # the use of financial accounting criteria to judge the quality of management accounting

systems,

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Historical Timeline ― Establishing Management Accounting Principles

1 It added a philosophical foundation by using the basic Epistemology of Deductive reasoning and Inductive

reasoning and two of the four laws of logic to show that management accounting's two principles are

causality and analogy and that they are rooted in a bedrock of truth.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Historical Timeline ― Establishing Management Accounting Principles

1 :'2009 – International Federation of Accountants, Professional

Accountants in Business Committee. [

http://www.ifac.org/sites/default/files/publications/files/evaluating-and-improving-co_0.pdf International

Good Practice Guidance: Evaluation and Improving Costing in

Organizations]'. The principles as proposed in the Management Accounting Philosophy series

(referenced above; 2007) were adopted in IFAC's International Good

Practice Guidance (IGPG).

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Historical Timeline ― Establishing Management Accounting Principles

1 The maturity model was published as supplementary to the principles-based IGPG (referenced above) to allow companies to assess where

they were on the proposed costing continuum as far as their

management accounting maturity is concerned

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Historical Timeline ― Establishing Management Accounting Principles

1 :'2011 – Institute of Management Accountants. [

http://www.imanet.org/resources_and_publications/strategic_finance_magazine.aspx Strategic Finance Journal]'. In the October 2011 issue, an article

titled Why We Need a Conceptual Framework for Managerial Costing

provides a brief overview of the reasons why management

accounting needs its own framework distinctly separate for internal

managers.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Historical Timeline ― Establishing Management Accounting Principles

1 :'2012 – Institute of Management Accountants, MCCF Task Force. [

http://www.imanet.org/PDFs/Public/Research/CFMC%20Draft%20for%20Review.pdf

Managerial Costing Conceptual Framework (MCCF)]'. An Exposure Draft was released July 2012 for public comment and is the most extensive and thorough guidance available to management accounting

practitioners and users of management accounting information.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Importance of management accounting principles and its objectives

1 There are two interrelated parts in understanding why management

accounting principles are so important and how these principles

help managers achieve their primary objective: enterprise optimization.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Importance of management accounting principles and its objectives

1 The cumulative application of both principles (causality and analogy)

achieves management accounting's objectives and fulfills the managers'

needs – the optimization of the company's operations, generally

referred to as enterprise optimization.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Importance of management accounting principles and its objectives

1 At a more granular level the consistent application of

management accounting's principles hold a number of benefits for an

organization.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Truth as the Foundation in Management Accounting Principles

1 Therefore, truth corresponds to facts and when applied to Management

Accounting it translates to resources in operation creates a factual

situation

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Truth as the Foundation in Management Accounting Principles

1 The recognition of truth as the basis for management accounting goes back a long

way.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Truth as the Foundation in Management Accounting Principles

1 But Decision science —that which management accounting supports,

with the information it provides — is a science

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Truth as the Foundation in Management Accounting Principles

1 This disconnect is clearly documented in research such as the

2003 Survey of Management Accounting by Ernst Young LLP; co-sponsored by IMA and the follow up survey 2012 Alta Via, SAP, and IMA Management Accounting Survey: A

Replication and Longitudinal Comparison

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Management Accounting Principles Are Not GAAP

1 Accountants may argue that financial accounting principles

represent true values and are more than sufficient for management

accounting purposes

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Management Accounting Principles Are Not GAAP

1 By examining two of the four financial accounting principles, it will

reveal that financial accounting principles (e.g., Historical cost, Revenue recognition, Matching

principle, and Full Disclosure) 'do not' serve the objectives of management

accounting. Let's examine the following two GAAP principles:

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Management Accounting Principles Are Not GAAP

1 Where Management accounting's objectives exist is to inform internal managers of the correct choices for

long term economic success.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Principles

1 Principle of Analogy governs the user of management accounting

information's ability to apply the knowledge or insights gained from the causal relationships modeled (e.g., in planning, control, what-if

analysis) using inductive and deductive reasoning about past and

future outcomes for continuous optimization efforts.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Management Accounting Principles - Constraints

1 The following 'constraints' have been identified for management

accounting. The quantitative and qualitative characteristics of these constraints are meant to serve as controls or checks and balances

when constructing a cost model or when using management accounting

information.

https://store.theartofservice.com/the-management-accounting-toolkit.html

Historical cost - Management accounting techniques

1 In management accounting there are a number of techniques used as

alternatives to historical cost accounting including:-

https://store.theartofservice.com/the-management-accounting-toolkit.html

Managerial accounting - Differences between financial accountancy and management accounting

1 Management accounting information differs from financial accountancy information in

several ways:

https://store.theartofservice.com/the-management-accounting-toolkit.html

Managerial accounting - Differences between financial accountancy and management accounting

1 * while shareholders, creditors, and public regulators use publicly

reported financial accountancy information, only managers within the organization use the normally

confidential management accounting information;

https://store.theartofservice.com/the-management-accounting-toolkit.html

Managerial accounting - Differences between financial accountancy and management accounting

1 * while financial accountancy information is historical,

management accounting information is primarily forward-looking;

https://store.theartofservice.com/the-management-accounting-toolkit.html

Managerial accounting - Differences between financial accountancy and management accounting

1 * while financial accountancy information is case-based,

management accounting information is model-based with a degree of abstraction in order to support

generic decision making;

https://store.theartofservice.com/the-management-accounting-toolkit.html

Managerial accounting - Differences between financial accountancy and management accounting

1 * while financial accountancy information is computed by reference

to general financial accounting standards, management accounting

information is computed by reference to the needs of managers, often using management information

systems.

https://store.theartofservice.com/the-management-accounting-toolkit.html

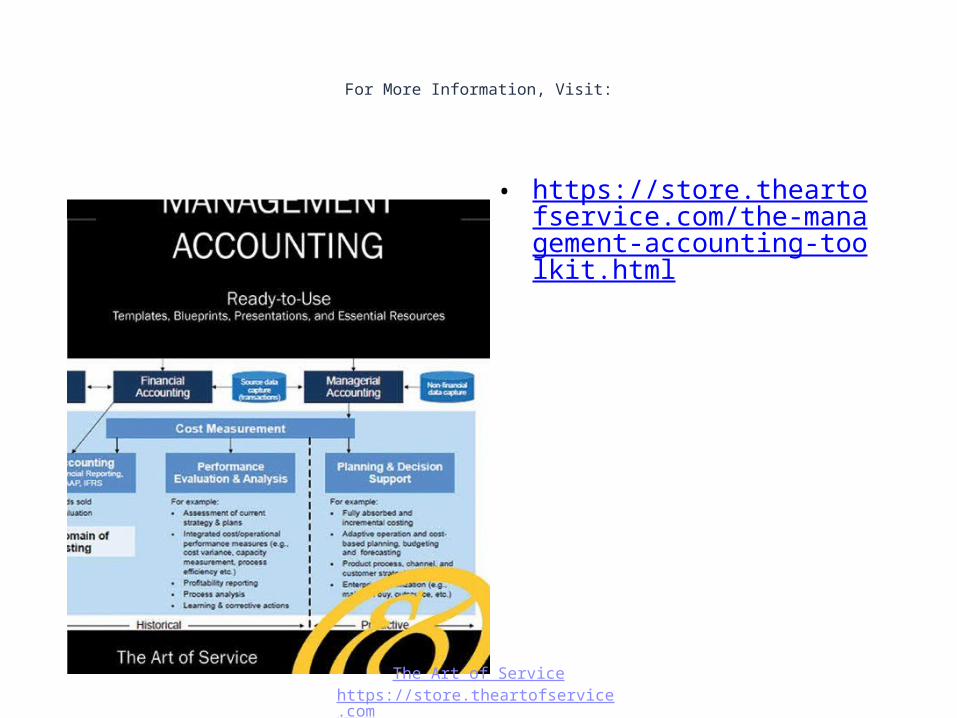

For More Information, Visit:

• https://store.theartofservice.com/the-management-accounting-toolkit.html

The Art of Servicehttps://store.theartofservice.com