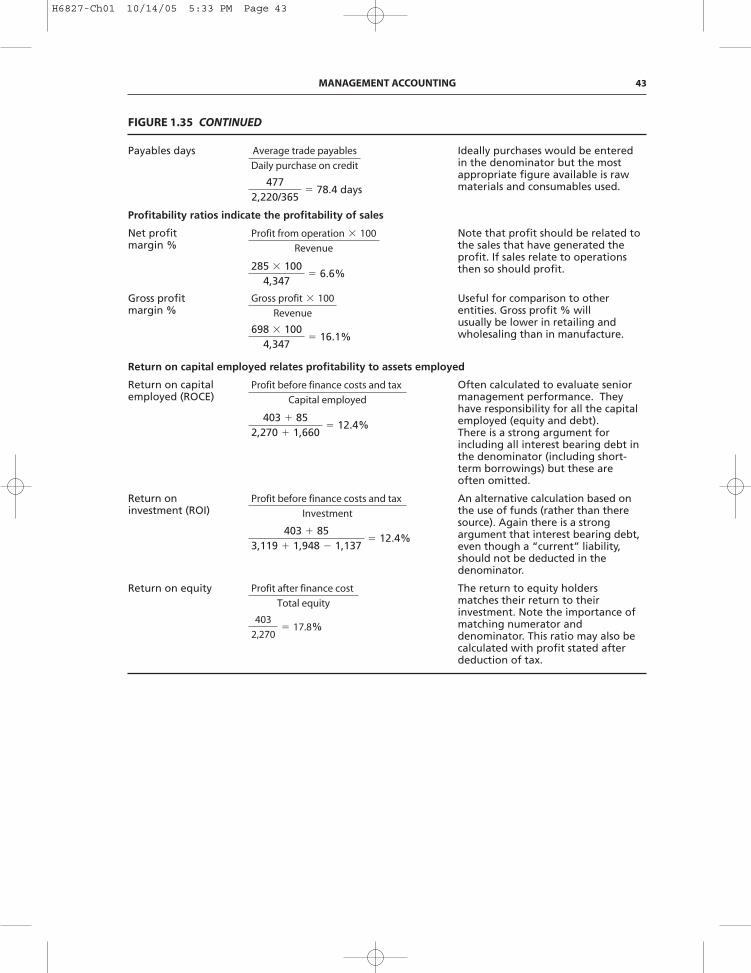

Embed Size (px)

Citation preview

Management Accounting

1

H6827-Ch01 10/14/05 5:32 PM Page 1

abnormal gain Improvement on theaccepted or normal level of loss associatedwith a production activity. It is isolated as aperiod entry rather than as an adjustmentto product cost.

abnormal loss Any loss in excess ofthe normal loss allowance. It is isolated asa period entry rather than as a componentof product cost.

absorbed overhead Overhead attachedto products or services by means of anabsorption rate, or rates.

under- or over-absorbed overhead Thedifference between overhead incurred andoverhead absorbed, using an estimatedrate, in a given period.

If overhead absorbed is less than thatincurred there is under-absorption, if

overhead absorbed is more than thatincurred there is over-absorption.Over- and under-absorptions are treated asperiod cost adjustments. See Figure 1.1.

absorption rate See overhead absorption rate.

accounting manual Collection of accountinginstructions governing the responsibilities ofpersons, and the procedures, forms andrecords relating to the preparation and useof accounting data. There can be separatemanuals for the constituent parts of theaccounting system, such as a budget manualor cost accounting manual.

accounting period Time period coveredby the accounting statements of an entity.There may be different time periods fordifferent accounting statements, forexample management accounts may be

2 CIMA OFFICIAL TERMINOLOGY

DIRECT COST $ $ $ $$ $ $

FACTORYTOTAL

MachineShop

AssemblyDepartment

EngineeringServices Stores

FactoryAdmin

QualityControl

PRODUCTION COSTCENTRES

SERVICE COST CENTRES

$ /machinehour

$ /unit$ /directlabourhour

(Absorption rates)

Productcost

per unit

Attribution of budgeted payroll cost

Indirect wages cost and salaries

Direct workers’ time not working on products

Sickness, holiday, Nl and pension costs

Indirect workers’ wages and employment costs

Supervision salaries & employment costs

Engineering salaries & employment costs

Quality control salaries & employment costs

Storekeepers’ salaries & employment costs

Other salaries

Total overhead payroll cost

Other allocated overhead

Apportioned costs, e.g. building service costs

Total budgeted production overhead

Re-apportionment of service cost centre costs

Direct material cost allocated

Direct wages cost allocated

Production overhead

– machine shop

– assembly

– quality control

Production cost per unit

X

X

X

X

X

X

X

X

X

X

X

X X

X

X

X

X

X X X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X X X X X X X

X

X

X

X

X

X

X

OV

ERH

EAD

AB

SOR

PTIO

NC

OST

APP

OR

TIO

NM

ENT

CO

STA

LLO

CA

TIO

N

FIGURE 1.1 COST ALLOCATION, APPORTIONMENT AND OVERHEAD ABSORPTION

H6827-Ch01 10/14/05 5:32 PM Page 2

for four- or five-week periods to coincidewith a thirteen-week financial accountingperiod.

accounts, integrated Set of accountingrecords that integrates both financial andcost accounts using a common input ofdata for all accounting purposes.

accounts, interlocking Set of accountingrecords where the cost and financial accountsare distinct, the two being kept continuouslyin agreement by the use of control accountsor reconciled by other means.

activities, hierarchy of Classification ofactivities by level of organisation, forexample unit, batch, product sustainingand facility sustaining.

activity, batch level Activity (such as setting-up machines) where volume varies directlywith the number of batches of output but isindependent of the number of units in abatch. See activities, hierarchy of.

activity cost pool Aggregation of all costsrelated to a specific activity.

activity driver Transaction that causes anactivity. For example, receipt of a sales ordersets in train the order processing activity.

activity driver analysis Identification andevaluation of the activity drivers used totrace the cost of activities to cost objects.

activity, facility sustaining Activityundertaken to support the organisation

as a whole, and which cannot be logicallylinked to individual units of output.Accounting is a facility sustaining activity.See activities, hierarchy of.

activity, product sustaining Activityundertaken to develop or sustain a product(or service). Product sustaining costs arelinked to the number of products orservices, not to the number of unitsproduced.

activity-based budgeting Methodof budgeting based on an activityframework and utilising cost driver datain the budget setting and variance feedbackprocesses.

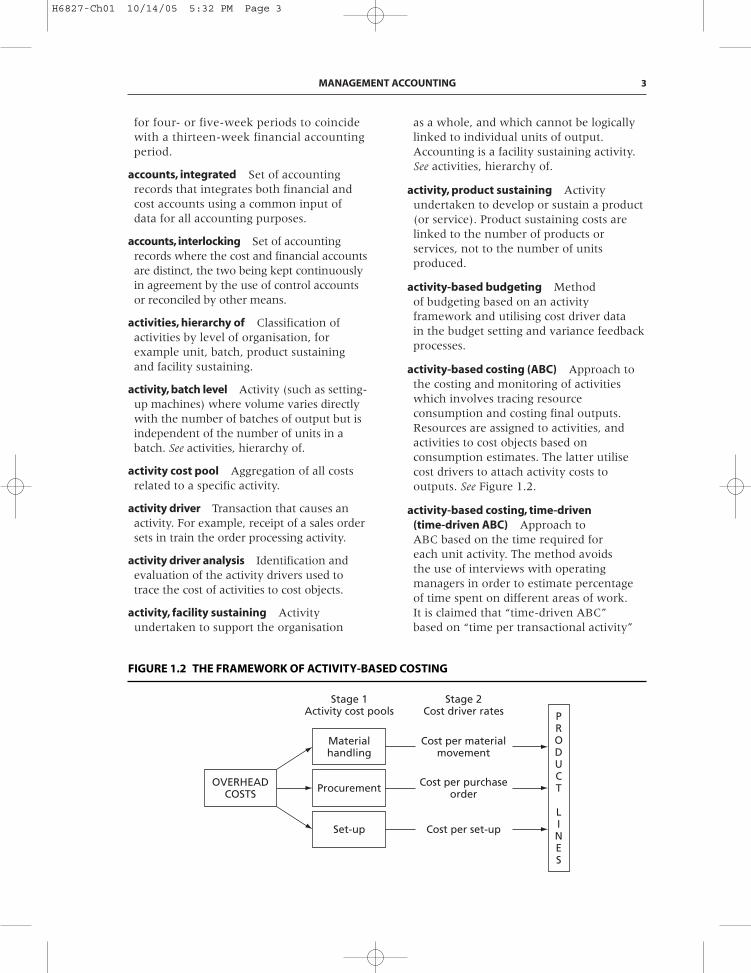

activity-based costing (ABC) Approach tothe costing and monitoring of activitieswhich involves tracing resourceconsumption and costing final outputs.Resources are assigned to activities, andactivities to cost objects based onconsumption estimates. The latter utilisecost drivers to attach activity costs tooutputs. See Figure 1.2.

activity-based costing, time-driven(time-driven ABC) Approach toABC based on the time required foreach unit activity. The method avoidsthe use of interviews with operatingmanagers in order to estimate percentageof time spent on different areas of work.It is claimed that “time-driven ABC”based on “time per transactional activity”

MANAGEMENT ACCOUNTING 3

Stage 1Activity cost pools

Stage 2Cost driver rates

Cost per materialmovement

Cost per purchaseorder

Cost per set-up

OVERHEADCOSTS

Materialhandling

Procurement

Set-up

PRODUCT

LINES

FIGURE 1.2 THE FRAMEWORK OF ACTIVITY-BASED COSTING

H6827-Ch01 10/14/05 5:32 PM Page 3

is simpler to install and update and canhighlight unused capacity.

activity-based management (ABM)operational ABM Actions, based on activitydriver analysis, that increase efficiency,lower costs and/or improve assetutilisation.

strategic ABM Actions, based on activity-based cost analysis, that aim to change thedemand for activities so as to improveprofitability.

allocate To assign a whole item of cost,or of revenue, to a single cost unit,centre, account or time period. In theUS, “allocate” does not have this precisemeaning, it is used more generally to referto the whole process of overheadapportionment, allocation and absorption.See Figure 1.1.

apportion To spread indirect revenuesor costs over two or more cost units,centres, accounts or time periods. Thismay also be referred to as “indirectallocation”.

re-apportion The re-spread of costsapportioned to service departments toproduction departments. See Figure 1.1

apportionment basis Physical orfinancial unit used to apportion costs tocost centres.

batch Group of similar units whichmaintains its identity throughout one ormore stages of production and is treated asa cost unit.

behavioural implications, accountingWays in which people affect, and areaffected by, the creation, existence anduse of accounting information. Forexample, see budgeting, behaviouralaspects and consequences.

bill of materials Detailed specification,for each product, of the subassemblies,components and materials required,distinguishing items purchasedexternally from those manufacturedin-house.

bottleneck Facility that has lower capacitythan prior or subsequent facilities and

restricts output based on current capacity.See theory of constraints, throughput.

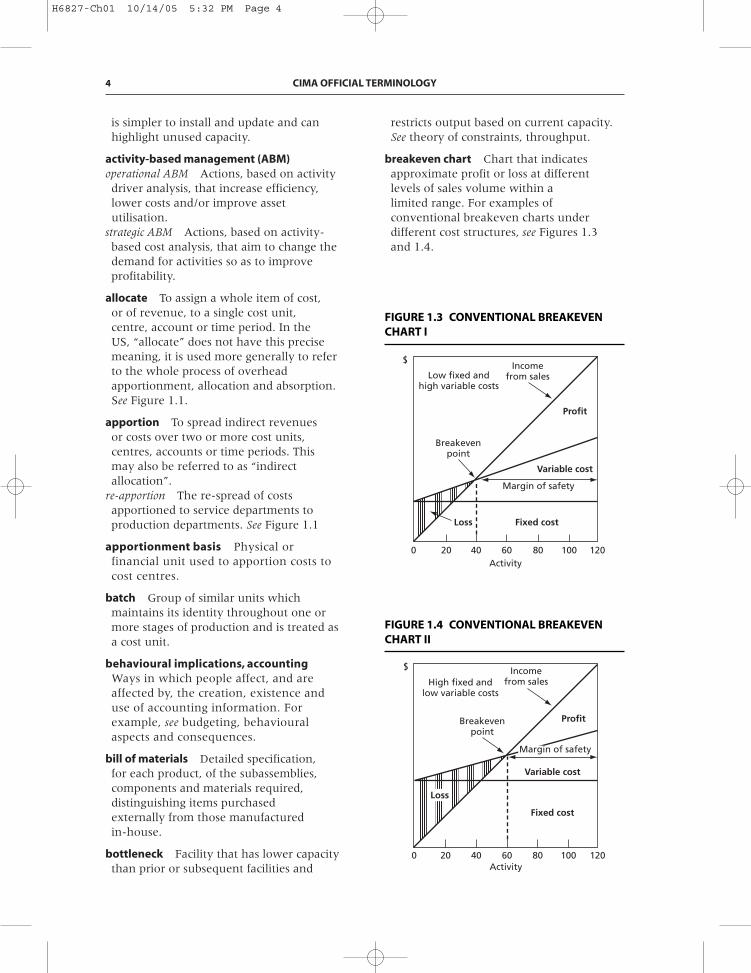

breakeven chart Chart that indicatesapproximate profit or loss at differentlevels of sales volume within alimited range. For examples ofconventional breakeven charts underdifferent cost structures, see Figures 1.3and 1.4.

4 CIMA OFFICIAL TERMINOLOGY

Low fixed andhigh variable costs

Incomefrom sales

Profit

Breakevenpoint

Variable cost

Margin of safety

Loss Fixed cost

Activity

$

0 20 40 60 80 100 120

FIGURE 1.3 CONVENTIONAL BREAKEVENCHART I

FIGURE 1.4 CONVENTIONAL BREAKEVENCHART II

High fixed andlow variable costs

Incomefrom sales

ProfitBreakevenpoint

Variable cost

Fixed cost

Activity

$

0 20 40 60 80 100 120

Loss

Margin of safety

H6827-Ch01 10/14/05 5:32 PM Page 4

$

Sales 10,000Variable costs (e.g. direct materials, direct labour) 6,000Contribution 4,000Fixed cost 2,000Profit 2,000

Number of units sold 1,000Contribution per unit $4Contribution to sales ratio

Number of units to be sold to breakeven

Sales value at breakeven point

Time to breakeven

(assuming that the period is one year, andthat the rate of sales is constant within thatperiod)

budget Quantitative expression of aplan for a defined period of time. Itmay include planned sales volumesand revenues; resource quantities, costs andexpenses; assets, liabilities and cash flows.

budget, cash Detailed budget ofestimated cash inflows and outflowsincorporating both revenue and capitalitems.

budget centre Section of an entityfor which control may be exercisedthrough prepared budgets. It isoften a responsibility centre where themanager has authority over, andresponsibility for, defined costs and(possibly) revenues.

� 6 mth

Total fixed cost � 365

Total contribution �

$2,000

$4,000� 365

� $5,000

Total fixed cost

Contribution to sales ratio �

$2,000

40%

� $500 units

Total fixed cost

Contribution per unit �

$2,000

$4

$4,000

$10,000� 100 � 40%

MANAGEMENT ACCOUNTING 5

FIGURE 1.5 CONTRIBUTION BREAKEVENCHART

Incomefrom sales

Breakevenpoint

Fixed cost

Variable cost

$

Loss

0 50% 100%Activity

Mar

gin

al c

ost

Co

ntr

ibu

tio

n

Profit

FIGURE 1.6 PROFIT–VOLUME CHART

50%Activity

Fixed costLoss

Sales

Breakevenpoint

Fixe

d c

ost

Contribution

Co

ntr

ibu

tio

n

Profit

0 100%

$

Figure 1.5 shows a contributionbreakeven chart and Figure 1.6 aprofit–volume chart.

breakeven point Level of activity atwhich there is neither profit nor loss.It can be ascertained by using abreakeven chart or by calculation.See Figures 1.3, 1.4, 1.5, 1.6 andexample:

H6827-Ch01 10/14/05 5:32 PM Page 5

budget cost allowance Calculated after anaccounting period, the cost allowancereflects the actual level of output achieved.Variable costs are flexed in proportion tovolume achieved and fixed costs are basedon the annual budget.

budget, departmental/functional Budgetof income and/or expenditure applicable toa particular function frequently includingsales budget, production cost budget (basedon budget production, efficiency andutilisation), purchasing budget, humanresources budget, marketing budget, andresearch and development budget.

budget, fixed Budget set prior to thecontrol period and not subsequentlychanged in response to changes in activity,costs or revenues. It may serve as abenchmark in performance evaluation.

budget, flexible See budget flexing.

budget flexing Flexing variable costs fromoriginal budgeted levels to the allowancespermitted for actual volume achieved whilemaintaining fixed costs at original budgetlevels.

(Variable cost allowance � Ratio ofactual volume achieved to budgetvolume � original budget variable cost)

budget lapsing Withdrawal of unspentbudget allowance due to the expiry of thebudget period.

budget, line item Traditional form of budgetlayout showing, line by line, the costs of acost centre analysed by their nature (forexample salaries, occupancy, maintenance).

budget manual Detailed set of guidelinesand information about the budget processtypically including a calendar of budgetaryevents, specimen budget forms, a statementof budgetary objectives and desired results,listing of budgetary activities and budgetassumptions regarding, for example,inflation and interest rates.

budget, master Consolidates all subsidiarybudgets and is normally comprised of thebudgeted profit and loss account, balancesheet and cash flow statement.

budget, operating Budget of the revenuesand expenses expected in a forthcomingaccounting period.

budget padding See budget slack.

budget period Period for which a budget isprepared and used, which may then besubdivided into control periods.

budget, principal factor Principal budgetfactor limits the activities of anundertaking. Identification of the principalbudget factor is often the starting point inthe budget setting process. Often theprincipal budget factor will be sales demandbut it could be production capacity ormaterial supply.

budget purposes Budgets may help inauthorising expenditure, communicatingobjectives and plans, controllingoperations, co-ordinating activities,evaluating performance, planning andrewarding performance. Often, rewardsystems involve comparison of actual withbudgeted performance.

budget, rolling/continuous Budgetcontinuously updated by adding a furtheraccounting period (month or quarter)when the earliest accounting period hasexpired. Its use is particularly beneficialwhere future costs and/or activities cannotbe forecast accurately. See rolling forecast(Chapter 2).

budget setting processesbottom-up budgeting Budgeting processwhere all budget holders have theopportunity to participate in setting theirown budgets.

imposed/top-down budgeting Budgetingprocess where budget allowances areset without permitting ultimate budgetholders the opportunity to participate in theprocess.

negotiated budget Budget in which budgetallowances are set largely on the basis ofnegotiations between budget holders andthose to whom they report.

participative budgeting See bottom-upbudgeting.

6 CIMA OFFICIAL TERMINOLOGY

H6827-Ch01 10/14/05 5:32 PM Page 6

budget slack Intentional overestimationof expenses and/or underestimation ofrevenue during budget setting. Also knownas budget padding.

budget virement Authority to apply savingunder one budget subhead to meetexcesses on others.

budgetary control Master budget,devolved to responsibility centres, allowscontinuous monitoring of actual resultsversus budget, either to secure byindividual action the budget objectives orto provide a basis for budget revision.See control, feedback and control,feedforward.

budgeting, behavioural aspects andconsequences

budget constrained style Excessive pressure toachieve budgets that can lead to job-relatedtension, recriminations, buck-passing andbudget padding.

non-accounting style Management style thatlargely ignores budgets and financialinformation.

profit conscious style Management style thattakes account of budgets together withother information and evaluatesmanagerial performance in a flexiblemanner.

target setting “Tight but achievable” levelsare recommended to motivate optimumperformance. Too loose a budget can leadto under-achievement as can too tight abudget – and this can also bede-motivating.

budgeting, beyond Idea thatcompanies need to move beyondbudgeting because of the inherentflaws in budgeting especially when usedto set incentive contracts. It is argued thata range of techniques, such as rollingforecasts and market-relatedtargets, can take the place of traditionalbudgets.

budgeting, incremental Method ofbudgeting based on the previous budget

or actual results, adjusting for knownchanges and inflation, for example.

budgeting, priority-based Method ofbudgeting whereby budget requests areaccompanied by a statement outlining thechanges expected if the prior period budgetwere increased or decreased by a certainamount or percentage. These changes areprioritised.

budgeting, zero-based Method of budgetingthat requires all costs to be specificallyjustified by the benefits expected.

burden US equivalent of “overhead”.

by-product Output of some value producedincidentally while manufacturing the mainproduct. See joint products.

capital employed Investment in an entity.In assessing managers it is usuallycalculated as total assets less currentliabilities.

equity capital employed Shareholders’ stakein the company. This is important whencalculating return to shareholders.

capital expenditure control Procedures forauthorising and subsequently monitoringcapital expenditure.

capital expenditure proposal/authorisationFormal request for authority to incur capitalexpenditure usually supported by the casefor expenditure in accordance with capitalinvestment appraisal criteria. Levels ofauthority should be clearly defined withreporting of actual expenditure to theequivalent authority levels.

centre Department, area or function towhich costs and/or revenues are charged.See Figure 1.1.

budget centre Centre for which an individualbudget is drawn up.

cost centre Production or service location,function, activity or item of equipment forwhich costs are accumulated. See Figure 1.1.

investment centre Profit centre withadditional responsibilities for capitalinvestment and possibly for financing, andwhose performance is measured by itsreturn on investment.

MANAGEMENT ACCOUNTING 7

H6827-Ch01 10/14/05 5:32 PM Page 7

profit centre Part of a business accountablefor both costs and revenues.

responsibility centre Departmental ororganisational function whose performanceis the direct responsibility of a specificmanager.

revenue centre Centre devoted to raisingrevenue with no responsibility for costs,for example a sales centre. Often usedin not-for-profit organisations.

service cost centre Cost centre providingservices to other cost centres. Whenthe output of an organisation is a service,rather than goods, an alternative nameis normally used, for example supportcost centre or utility cost centre.See Figure 1.1.

classification Arrangement of itemsin logical groups by nature, purposeor responsibility. Classification systemsallow financial information to bereported under subjective headings,by cost object or responsibility centre.See code.

code Brief, accurate referencedesigned to assist classification of itemsby facilitating entry, collation andanalysis. For example, in costing, the firstthree digits in the composite symbol211.392 might indicate the nature of theexpenditure (subjective classification), andthe last three digits might indicate thecost centre or cost unit to be charged(objective classification).

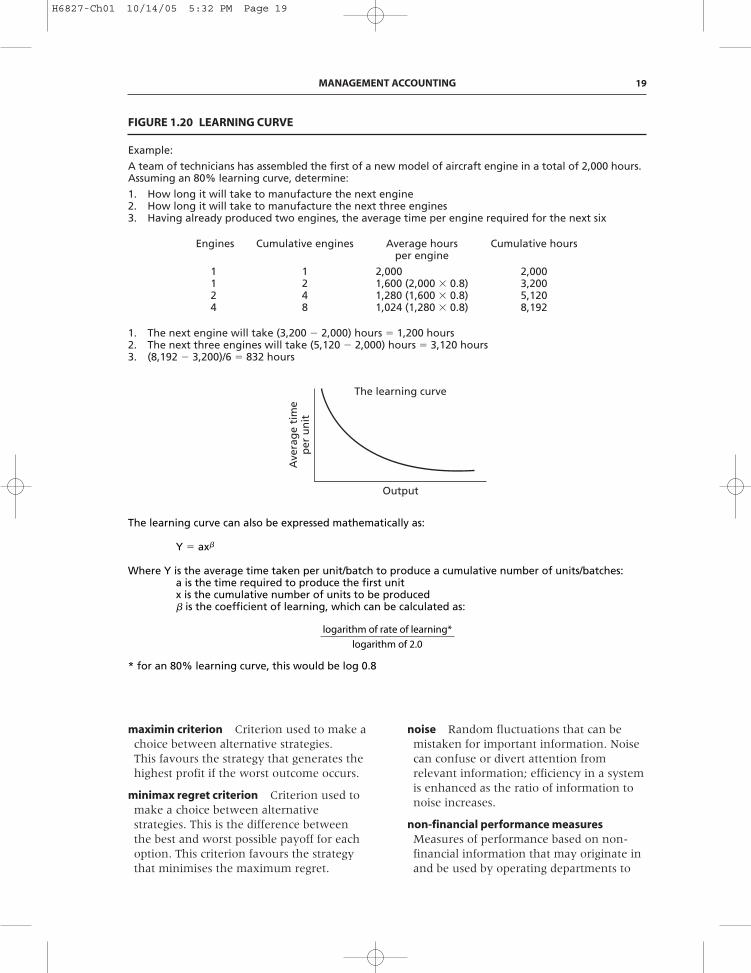

constraint Activity, resource or policythat limits the ability to achieve anobjective. See theory of constraints. Inlinear programming, constraints definethe feasible region within which asolution must lie. See linear programming.See Figure 1.19.

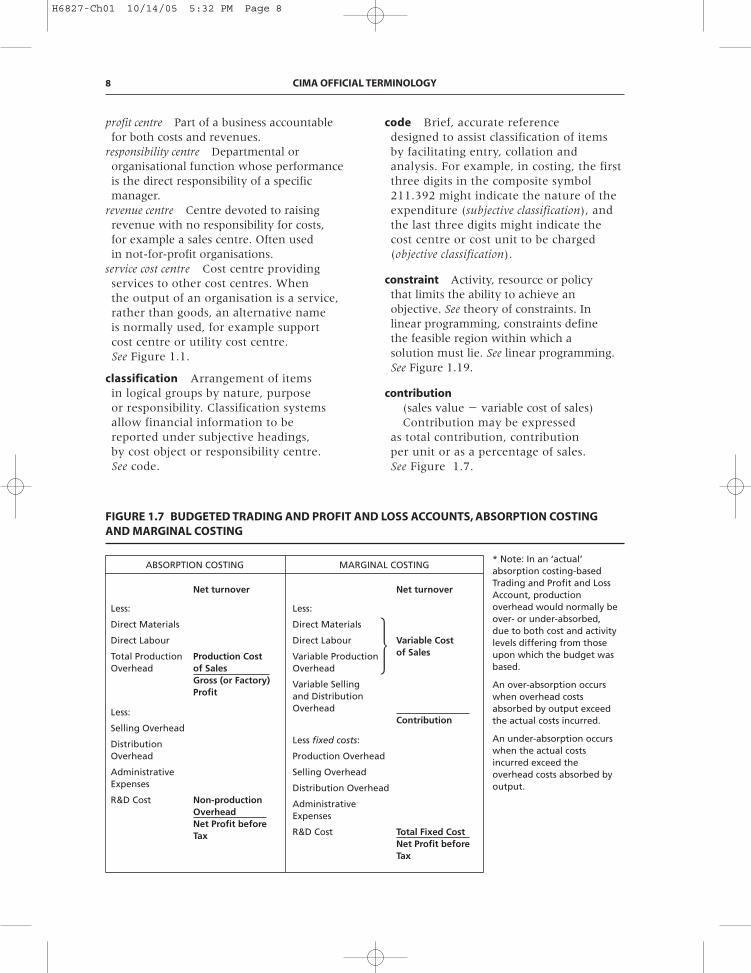

contribution(sales value � variable cost of sales)Contribution may be expressed

as total contribution, contributionper unit or as a percentage of sales.See Figure 1.7.

8 CIMA OFFICIAL TERMINOLOGY

* Note: In an ‘actual’ absorption costing-based Trading and Profit and Loss Account, production overhead would normally be over- or under-absorbed, due to both cost and activity levels differing from those upon which the budget was based.

An over-absorption occurs when overhead costs absorbed by output exceed the actual costs incurred.

An under-absorption occurs when the actual costs incurred exceed the overhead costs absorbed by output.

Net turnover

Less:

Direct Materials

Direct Labour Variable Cost

Variable Production of Sales

Overhead

Variable Sellingand Distribution Overhead

Contribution

Less fixed costs:

Production Overhead

Selling Overhead

Distribution Overhead

AdministrativeExpenses

R&D Cost Total Fixed CostNet Profit before Tax

Net turnover

Less:

Direct Materials

Direct Labour

Total Production Production CostOverhead of Sales

Gross (or Factory)Profit

Less:

Selling Overhead

DistributionOverhead

AdministrativeExpenses

R&D Cost Non-productionOverheadNet Profit beforeTax

ABSORPTION COSTING MARGINAL COSTING

FIGURE 1.7 BUDGETED TRADING AND PROFIT AND LOSS ACCOUNTS, ABSORPTION COSTINGAND MARGINAL COSTING

�

H6827-Ch01 10/14/05 5:32 PM Page 8

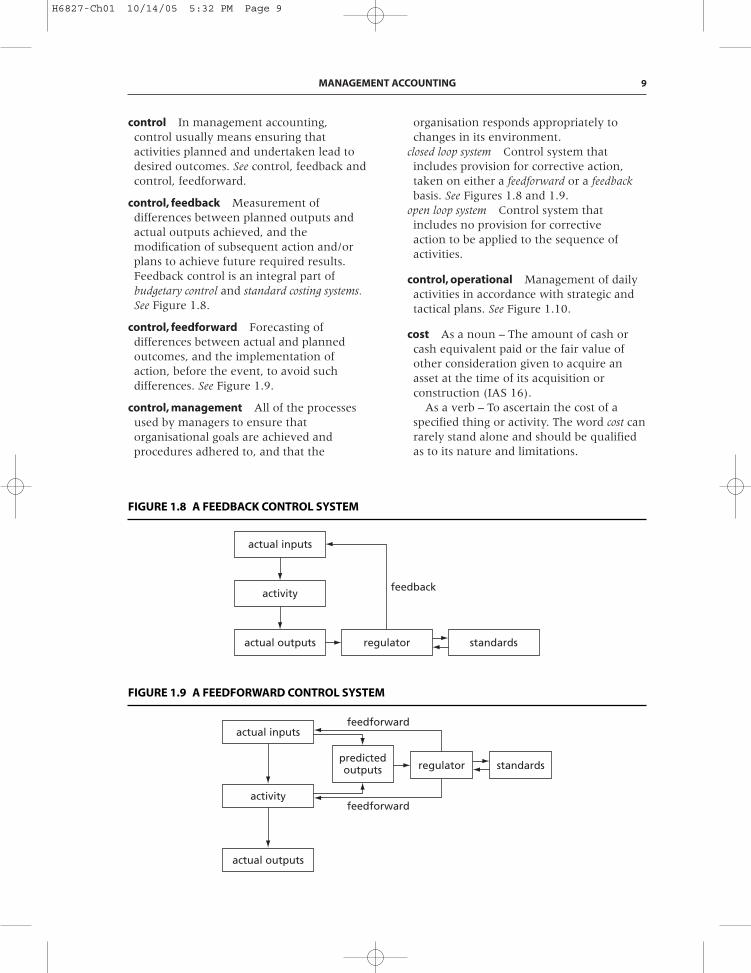

control In management accounting,control usually means ensuring thatactivities planned and undertaken lead todesired outcomes. See control, feedback andcontrol, feedforward.

control, feedback Measurement ofdifferences between planned outputs andactual outputs achieved, and themodification of subsequent action and/orplans to achieve future required results.Feedback control is an integral part ofbudgetary control and standard costing systems.See Figure 1.8.

control, feedforward Forecasting ofdifferences between actual and plannedoutcomes, and the implementation ofaction, before the event, to avoid suchdifferences. See Figure 1.9.

control, management All of the processesused by managers to ensure thatorganisational goals are achieved andprocedures adhered to, and that the

organisation responds appropriately tochanges in its environment.

closed loop system Control system thatincludes provision for corrective action,taken on either a feedforward or a feedbackbasis. See Figures 1.8 and 1.9.

open loop system Control system thatincludes no provision for correctiveaction to be applied to the sequence ofactivities.

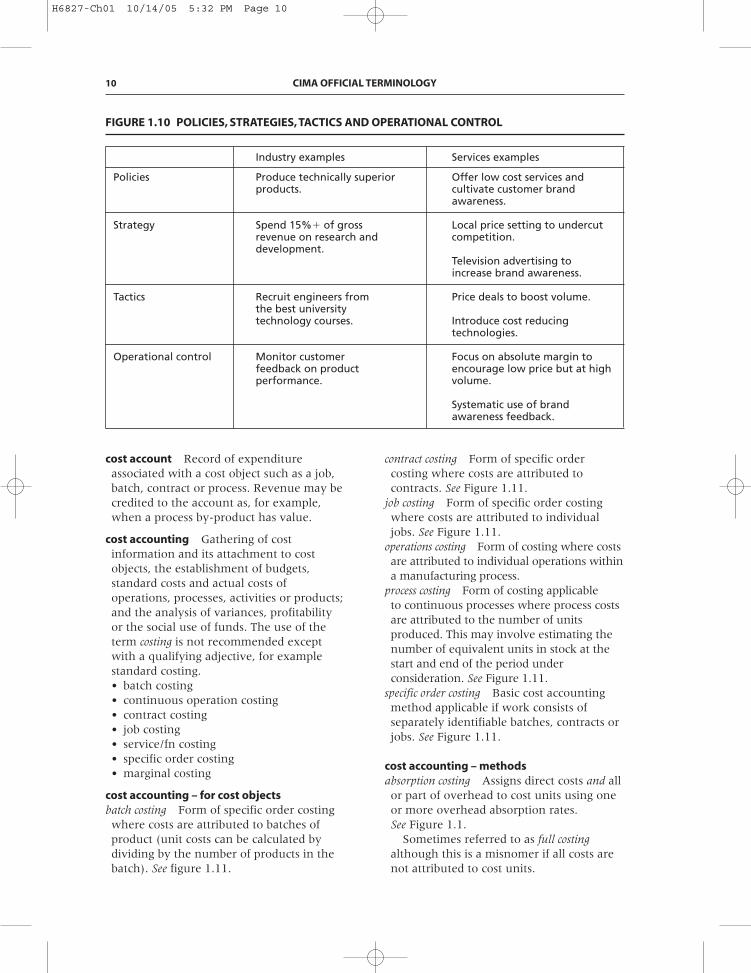

control, operational Management of dailyactivities in accordance with strategic andtactical plans. See Figure 1.10.

cost As a noun – The amount of cash orcash equivalent paid or the fair value ofother consideration given to acquire anasset at the time of its acquisition orconstruction (IAS 16).

As a verb – To ascertain the cost of aspecified thing or activity. The word cost canrarely stand alone and should be qualifiedas to its nature and limitations.

MANAGEMENT ACCOUNTING 9

actual inputs

activityfeedback

actual outputs regulator standards

FIGURE 1.8 A FEEDBACK CONTROL SYSTEM

FIGURE 1.9 A FEEDFORWARD CONTROL SYSTEM

actual inputs

activity

actual outputs

regulator standardspredictedoutputs

feedforward

feedforward

H6827-Ch01 10/14/05 5:32 PM Page 9

cost account Record of expenditureassociated with a cost object such as a job,batch, contract or process. Revenue may becredited to the account as, for example,when a process by-product has value.

cost accounting Gathering of costinformation and its attachment to costobjects, the establishment of budgets,standard costs and actual costs ofoperations, processes, activities or products;and the analysis of variances, profitabilityor the social use of funds. The use of theterm costing is not recommended exceptwith a qualifying adjective, for examplestandard costing.• batch costing• continuous operation costing• contract costing• job costing• service/fn costing• specific order costing• marginal costing

cost accounting – for cost objectsbatch costing Form of specific order costingwhere costs are attributed to batches ofproduct (unit costs can be calculated bydividing by the number of products in thebatch). See figure 1.11.

contract costing Form of specific ordercosting where costs are attributed tocontracts. See Figure 1.11.

job costing Form of specific order costingwhere costs are attributed to individualjobs. See Figure 1.11.

operations costing Form of costing where costsare attributed to individual operations withina manufacturing process.

process costing Form of costing applicableto continuous processes where process costsare attributed to the number of unitsproduced. This may involve estimating thenumber of equivalent units in stock at thestart and end of the period underconsideration. See Figure 1.11.

specific order costing Basic cost accountingmethod applicable if work consists ofseparately identifiable batches, contracts orjobs. See Figure 1.11.

cost accounting – methodsabsorption costing Assigns direct costs and allor part of overhead to cost units using oneor more overhead absorption rates. See Figure 1.1.

Sometimes referred to as full costingalthough this is a misnomer if all costs arenot attributed to cost units.

10 CIMA OFFICIAL TERMINOLOGY

FIGURE 1.10 POLICIES, STRATEGIES, TACTICS AND OPERATIONAL CONTROL

Industry examples Services examples

Policies Produce technically superior Offer low cost services and products. cultivate customer brand

awareness.

Strategy Spend 15%� of gross Local price setting to undercut revenue on research and competition.development.

Television advertising toincrease brand awareness.

Tactics Recruit engineers from Price deals to boost volume.the best universitytechnology courses. Introduce cost reducing

technologies.

Operational control Monitor customer Focus on absolute margin to feedback on product encourage low price but at high performance. volume.

Systematic use of brandawareness feedback.

H6827-Ch01 10/14/05 5:32 PM Page 10

direct costing See variable costing.full costing See absorption costing.marginal costing See variable costing.uniform costing Used by severalundertakings, usually in the same industry,of the same costing methods, principles andtechniques.

variable costing Assigns only variablecosts to cost units while fixed costs arewritten off as period costs. See Figure 1.7.Also known as marginal costing and,especially in the US, as direct costing.

cost allocation/apportionment See allocationand apportionment.

cost, avoidable Specific cost of an activityor sector of a business that would beavoided if the activity or sector did notexist.

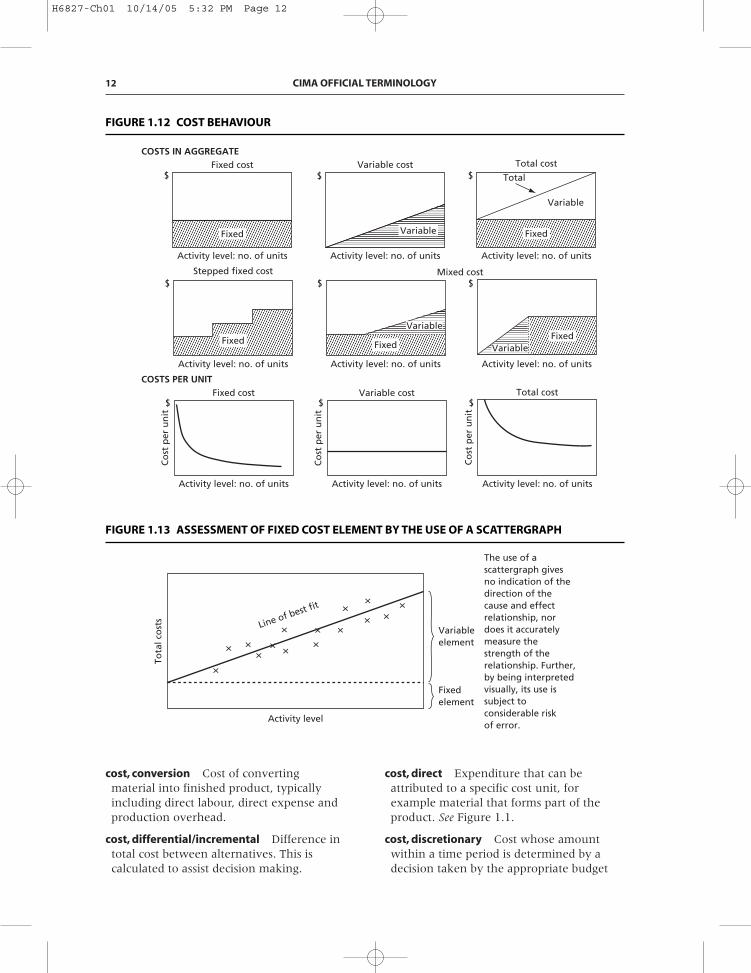

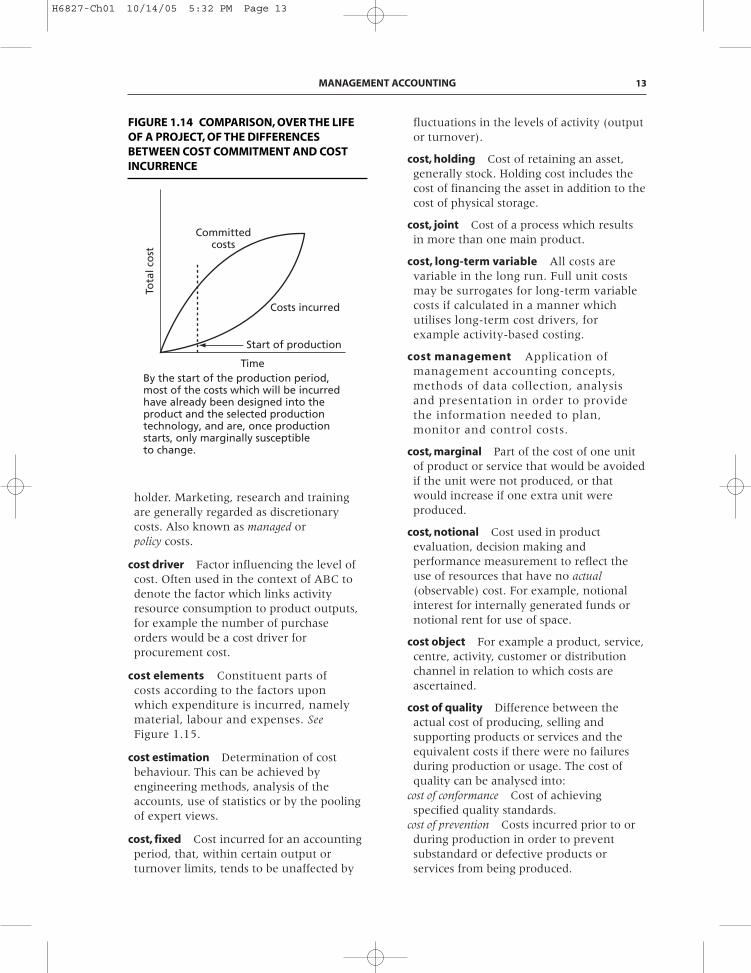

cost behaviour Variability of input costswith activity undertaken. Cost mayincrease proportionately with increasingactivity (the usual assumption for avariable cost), or it may not change withincreased activity (a fixed cost). Some costs(semi-variable) may have both variable andfixed elements. Other behaviour is possible,costs may increase more or less than indirect proportion, and there may be stepchanges in cost, for example. To a largeextent cost behaviour will be dependenton the timescale assumed. See Figures 1.12and 1.13.

cost classification Arrangement of elementsof cost into logical groups with respect totheir nature (fixed, variable, value adding),function (production, selling) or use in thebusiness of the entity.

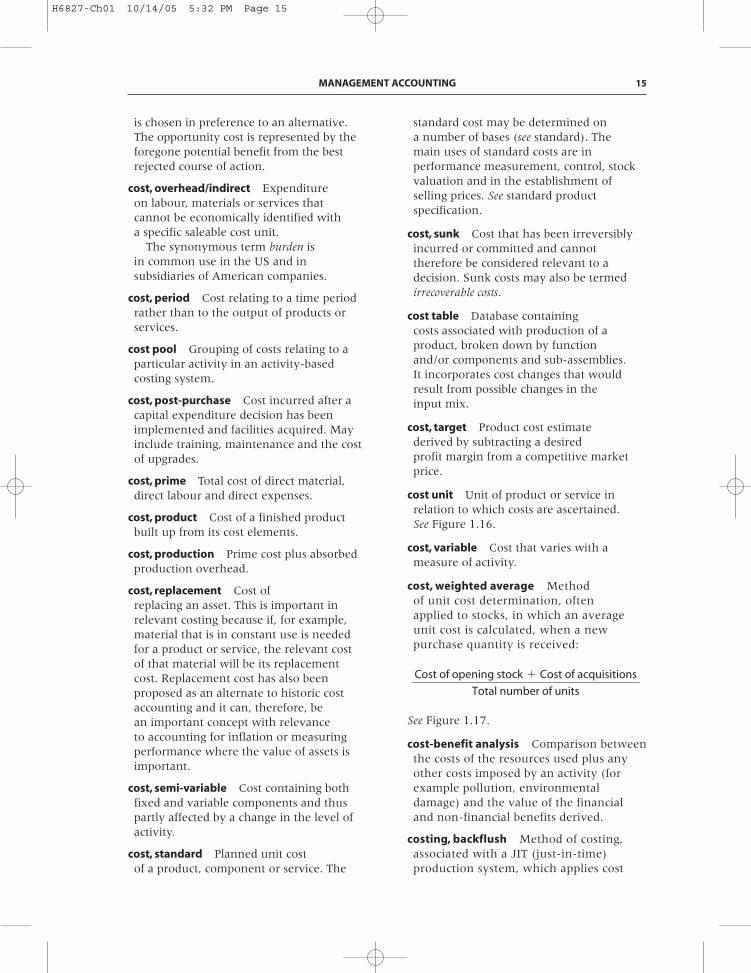

cost, committed Cost arising from priordecisions, which cannot, in the short run,be changed. Committed cost incurrenceoften stems from strategic decisionsconcerning capacity with resultingexpenditure on plant and facilities. Initialcontrol of committed costs at the decisionpoint is through investment appraisaltechniques. See commitment accounting.See Figure 1.14.

cost, common Cost relating to more thanone product or service.

cost, contract Aggregated costs of a singlecontract. This usually applies to majorlong-term contracts rather than short-term jobs.

cost control Process that ensures actionis taken if costs exceed a pre-setallowance (see control, feedback) or thataction is taken if costs are forecast toexceed expected levels (see control,feedforward).

cost, controllable Cost that can becontrolled, typically by a cost, profit orinvestment centre manager.

MANAGEMENT ACCOUNTING 11

FIGURE 1.11 ELEMENTS OF A PRODUCT COSTING SYSTEM

Overall Control System: Budgetary Control

Product costing system Specific orders Continuous operations

Costing method Job costing Batch Contract Continuous Service/costing costing operation/ function

process costingcosting

Treatment offixed production Absorption or marginaloverhead

Method of cost Standard or actualcontrol

H6827-Ch01 10/14/05 5:32 PM Page 11

cost, conversion Cost of convertingmaterial into finished product, typicallyincluding direct labour, direct expense andproduction overhead.

cost, differential/incremental Difference intotal cost between alternatives. This iscalculated to assist decision making.

cost, direct Expenditure that can beattributed to a specific cost unit, forexample material that forms part of theproduct. See Figure 1.1.

cost, discretionary Cost whose amountwithin a time period is determined by adecision taken by the appropriate budget

12 CIMA OFFICIAL TERMINOLOGY

Activity level: no. of units

Co

st p

er u

nit

$

Activity level: no. of units

Co

st p

er u

nit

$

Activity level: no. of units

Co

st p

er u

nit

$

COSTS PER UNITFixed cost Variable cost Total cost

Activity level: no. of units

Fixed

Variable

$

Activity level: no. of units

Stepped fixed cost

Fixed

$

Activity level: no. of units

Mixed cost

FixedVariable

$

COSTS IN AGGREGATEFixed cost

Activity level: no. of units

Fixed

$Variable cost

Activity level: no. of units

Variable

$Total cost

Activity level: no. of units

Fixed

$ Total

Variable

FIGURE 1.12 COST BEHAVIOUR

Activity level

Line of best fit

Tota

l co

sts

Variableelement

The use of ascattergraph givesno indication of thedirection of thecause and effectrelationship, nordoes it accuratelymeasure thestrength of therelationship. Further,by being interpretedvisually, its use issubject toconsiderable riskof error.

Fixedelement

××

×

×

××× ×

××

× ××

× ×

FIGURE 1.13 ASSESSMENT OF FIXED COST ELEMENT BY THE USE OF A SCATTERGRAPH

H6827-Ch01 10/14/05 5:32 PM Page 12

holder. Marketing, research and trainingare generally regarded as discretionarycosts. Also known as managed orpolicy costs.

cost driver Factor influencing the level ofcost. Often used in the context of ABC todenote the factor which links activityresource consumption to product outputs,for example the number of purchaseorders would be a cost driver forprocurement cost.

cost elements Constituent parts ofcosts according to the factors uponwhich expenditure is incurred, namelymaterial, labour and expenses. SeeFigure 1.15.

cost estimation Determination of costbehaviour. This can be achieved byengineering methods, analysis of theaccounts, use of statistics or by the poolingof expert views.

cost, fixed Cost incurred for an accountingperiod, that, within certain output orturnover limits, tends to be unaffected by

fluctuations in the levels of activity (outputor turnover).

cost, holding Cost of retaining an asset,generally stock. Holding cost includes thecost of financing the asset in addition to thecost of physical storage.

cost, joint Cost of a process which resultsin more than one main product.

cost, long-term variable All costs arevariable in the long run. Full unit costsmay be surrogates for long-term variablecosts if calculated in a manner whichutilises long-term cost drivers, forexample activity-based costing.

cost management Application ofmanagement accounting concepts,methods of data collection, analysisand presentation in order to providethe information needed to plan,monitor and control costs.

cost, marginal Part of the cost of one unitof product or service that would be avoidedif the unit were not produced, or thatwould increase if one extra unit wereproduced.

cost, notional Cost used in productevaluation, decision making andperformance measurement to reflect theuse of resources that have no actual(observable) cost. For example, notionalinterest for internally generated funds ornotional rent for use of space.

cost object For example a product, service,centre, activity, customer or distributionchannel in relation to which costs areascertained.

cost of quality Difference between theactual cost of producing, selling andsupporting products or services and theequivalent costs if there were no failuresduring production or usage. The cost ofquality can be analysed into:

cost of conformance Cost of achievingspecified quality standards.

cost of prevention Costs incurred prior to orduring production in order to preventsubstandard or defective products orservices from being produced.

MANAGEMENT ACCOUNTING 13

Committedcosts

Costs incurred

Start of production

TimeBy the start of the production period,most of the costs which will be incurredhave already been designed into theproduct and the selected productiontechnology, and are, once productionstarts, only marginally susceptibleto change.

Tota

l co

st

FIGURE 1.14 COMPARISON, OVER THE LIFEOF A PROJECT, OF THE DIFFERENCESBETWEEN COST COMMITMENT AND COSTINCURRENCE

H6827-Ch01 10/14/05 5:32 PM Page 13

cost of appraisal Costs incurred in order toensure that outputs produced meetrequired quality standards.

cost of non-conformance Cost of failureto deliver the required standard ofquality.

cost of internal failure Costs arising frominadequate quality which are identifiedbefore the transfer of ownership fromsupplier to purchaser.

cost of external failure Cost arising frominadequate quality discovered after the

transfer of ownership from supplier topurchaser.

Note: There is no universally accepteddefinition of quality, which may beassessed on a number of bases, such asconformance to specification, ability tosatisfy wants, inclusion of attractiveperformance/aesthetic attributes, oroffering value for money.

cost, opportunity The value of thebenefit sacrificed when one course of action

14 CIMA OFFICIAL TERMINOLOGY

Direct costs Overhead

Materials

Labour

Expenses

Materials

Labour

Expenses

Prime cost Production

Production cost

Total cost

Stock adjustment

Cost of sales Sales

PROFIT

Production overhead

Absorbedoverhead

Under/overabsorbedoverhead

MarketingAdministration R&D

Selling Distribution

Notes: 1. The above chart is based on the absorption costing principle. 2. In the case of marginal costing, the amount of production overhead absorbed would relate to the variable element only. 3. The relative sizes of the boxes are of no significance.

FIGURE 1.15 ELEMENTS OF AN ABSORPTION COSTING SYSTEM

H6827-Ch01 10/14/05 5:32 PM Page 14

is chosen in preference to an alternative.The opportunity cost is represented by theforegone potential benefit from the bestrejected course of action.

cost, overhead/indirect Expenditureon labour, materials or services thatcannot be economically identified witha specific saleable cost unit.

The synonymous term burden isin common use in the US and insubsidiaries of American companies.

cost, period Cost relating to a time periodrather than to the output of products orservices.

cost pool Grouping of costs relating to aparticular activity in an activity-basedcosting system.

cost, post-purchase Cost incurred after acapital expenditure decision has beenimplemented and facilities acquired. Mayinclude training, maintenance and the costof upgrades.

cost, prime Total cost of direct material,direct labour and direct expenses.

cost, product Cost of a finished productbuilt up from its cost elements.

cost, production Prime cost plus absorbedproduction overhead.

cost, replacement Cost ofreplacing an asset. This is important inrelevant costing because if, for example,material that is in constant use is neededfor a product or service, the relevant costof that material will be its replacementcost. Replacement cost has also beenproposed as an alternate to historic costaccounting and it can, therefore, bean important concept with relevanceto accounting for inflation or measuringperformance where the value of assets isimportant.

cost, semi-variable Cost containing bothfixed and variable components and thuspartly affected by a change in the level ofactivity.

cost, standard Planned unit costof a product, component or service. The

standard cost may be determined ona number of bases (see standard). Themain uses of standard costs are inperformance measurement, control, stockvaluation and in the establishment ofselling prices. See standard productspecification.

cost, sunk Cost that has been irreversiblyincurred or committed and cannottherefore be considered relevant to adecision. Sunk costs may also be termedirrecoverable costs.

cost table Database containingcosts associated with production of aproduct, broken down by functionand/or components and sub-assemblies.It incorporates cost changes that wouldresult from possible changes in theinput mix.

cost, target Product cost estimatederived by subtracting a desiredprofit margin from a competitive marketprice.

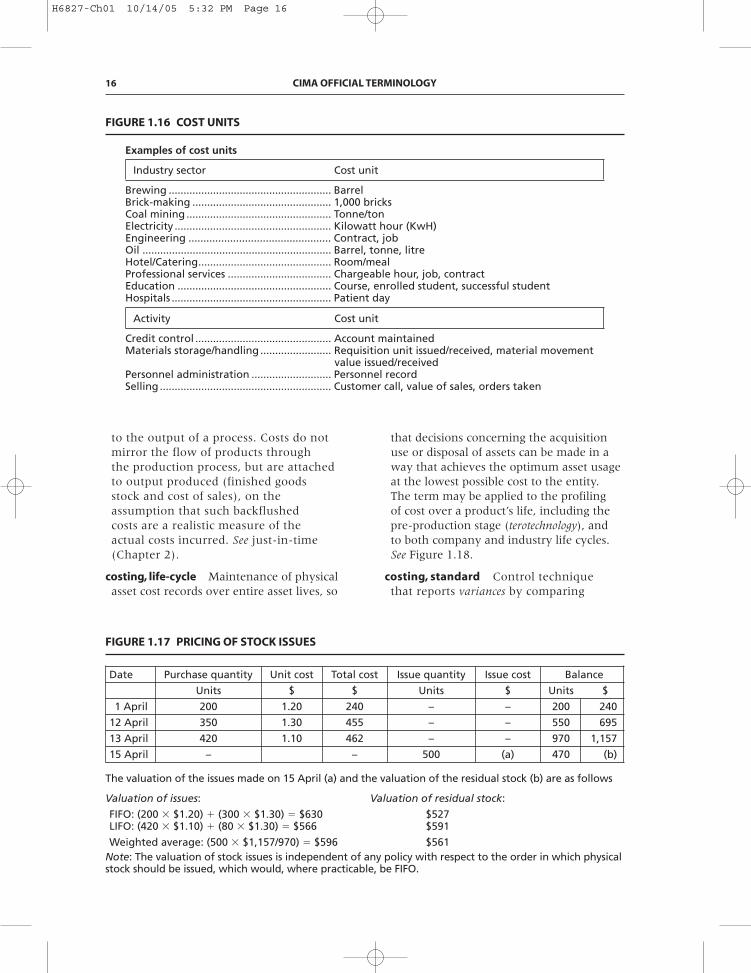

cost unit Unit of product or service inrelation to which costs are ascertained.See Figure 1.16.

cost, variable Cost that varies with ameasure of activity.

cost, weighted average Methodof unit cost determination, oftenapplied to stocks, in which an averageunit cost is calculated, when a newpurchase quantity is received:

See Figure 1.17.

cost-benefit analysis Comparison betweenthe costs of the resources used plus anyother costs imposed by an activity (forexample pollution, environmentaldamage) and the value of the financialand non-financial benefits derived.

costing, backflush Method of costing,associated with a JIT (just-in-time)production system, which applies cost

Cost of opening stock � Cost of acquisitions

Total number of units

MANAGEMENT ACCOUNTING 15

H6827-Ch01 10/14/05 5:32 PM Page 15

to the output of a process. Costs do notmirror the flow of products throughthe production process, but are attachedto output produced (finished goodsstock and cost of sales), on theassumption that such backflushedcosts are a realistic measure of theactual costs incurred. See just-in-time(Chapter 2).

costing, life-cycle Maintenance of physicalasset cost records over entire asset lives, so

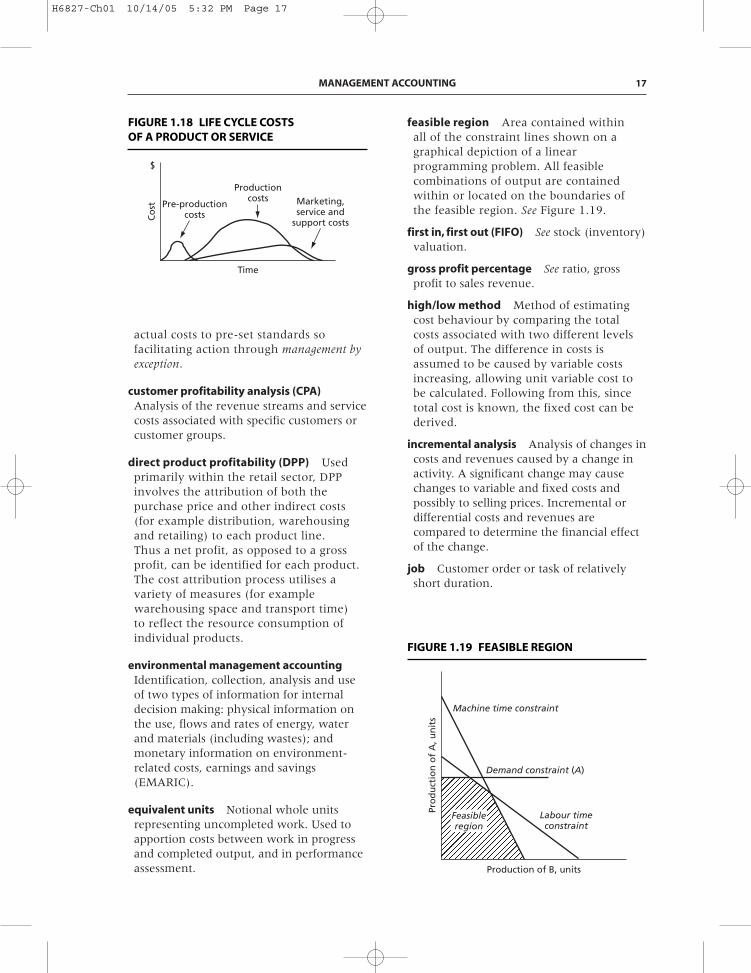

that decisions concerning the acquisitionuse or disposal of assets can be made in away that achieves the optimum asset usageat the lowest possible cost to the entity.The term may be applied to the profilingof cost over a product’s life, including thepre-production stage (terotechnology), andto both company and industry life cycles.See Figure 1.18.

costing, standard Control techniquethat reports variances by comparing

16 CIMA OFFICIAL TERMINOLOGY

Examples of cost units

Industry sector Cost unit

Brewing ....................................................... BarrelBrick-making ............................................... 1,000 bricksCoal mining ................................................. Tonne/tonElectricity ..................................................... Kilowatt hour (KwH)Engineering ................................................ Contract, jobOil ................................................................ Barrel, tonne, litreHotel/Catering............................................. Room/mealProfessional services ................................... Chargeable hour, job, contractEducation .................................................... Course, enrolled student, successful studentHospitals ...................................................... Patient day

Activity Cost unit

Credit control .............................................. Account maintainedMaterials storage/handling ........................ Requisition unit issued/received, material movement

value issued/receivedPersonnel administration ........................... Personnel recordSelling .......................................................... Customer call, value of sales, orders taken

FIGURE 1.16 COST UNITS

Date Purchase quantity Unit cost Total cost Issue quantity Issue cost Balance

Units $ $ Units $ Units $

1 April 200 1.20 240 – – 200 240

12 April 350 1.30 455 – – 550 695

13 April 420 1.10 462 – – 970 1,157

15 April – – 500 (a) 470 (b)

The valuation of the issues made on 15 April (a) and the valuation of the residual stock (b) are as follows

Valuation of issues: Valuation of residual stock:

FIFO: (200 � $1.20) � (300 � $1.30) � $630 $527LIFO: (420 � $1.10) � (80 � $1.30) � $566 $591

Weighted average: (500 � $1,157/970) � $596 $561Note: The valuation of stock issues is independent of any policy with respect to the order in which physicalstock should be issued, which would, where practicable, be FIFO.

FIGURE 1.17 PRICING OF STOCK ISSUES

H6827-Ch01 10/14/05 5:32 PM Page 16

actual costs to pre-set standards sofacilitating action through management byexception.

customer profitability analysis (CPA)Analysis of the revenue streams and servicecosts associated with specific customers orcustomer groups.

direct product profitability (DPP) Usedprimarily within the retail sector, DPPinvolves the attribution of both thepurchase price and other indirect costs(for example distribution, warehousingand retailing) to each product line.Thus a net profit, as opposed to a grossprofit, can be identified for each product.The cost attribution process utilises avariety of measures (for examplewarehousing space and transport time)to reflect the resource consumption ofindividual products.

environmental management accountingIdentification, collection, analysis and useof two types of information for internaldecision making: physical information onthe use, flows and rates of energy, waterand materials (including wastes); andmonetary information on environment-related costs, earnings and savings(EMARIC).

equivalent units Notional whole unitsrepresenting uncompleted work. Used toapportion costs between work in progressand completed output, and in performanceassessment.

feasible region Area contained withinall of the constraint lines shown on agraphical depiction of a linearprogramming problem. All feasiblecombinations of output are containedwithin or located on the boundaries ofthe feasible region. See Figure 1.19.

first in, first out (FIFO) See stock (inventory)valuation.

gross profit percentage See ratio, grossprofit to sales revenue.

high/low method Method of estimatingcost behaviour by comparing the totalcosts associated with two different levelsof output. The difference in costs isassumed to be caused by variable costsincreasing, allowing unit variable cost tobe calculated. Following from this, sincetotal cost is known, the fixed cost can bederived.

incremental analysis Analysis of changes incosts and revenues caused by a change inactivity. A significant change may causechanges to variable and fixed costs andpossibly to selling prices. Incremental ordifferential costs and revenues arecompared to determine the financial effectof the change.

job Customer order or task of relativelyshort duration.

MANAGEMENT ACCOUNTING 17

Time

Pre-productioncosts

Productioncosts Marketing,

service andsupport costsC

ost

$

FIGURE 1.18 LIFE CYCLE COSTSOF A PRODUCT OR SERVICE

Machine time constraint

Demand constraint (A)

Labour timeconstraint

Production of B, units

Pro

du

ctio

n o

f A

, un

its

Feasibleregion

FIGURE 1.19 FEASIBLE REGION

H6827-Ch01 10/14/05 5:32 PM Page 17

job cost sheet Detailed record of theamount, and cost, of the labour, materialand overhead charged to a specific job.

joint products Two or more productsproduced by the same process and separatedin processing, each having a sufficiently highsaleable value to merit recognition as a mainproduct. See by-product.

key performance indicators (KPIs)Quantitative but not necessarily financialmetrics that can indicate progress or lack ofprogress towards a strategic objective. Forexample, metrics may be devised for safety,quality, turnover of key staff. Keyperformance indicators were important tothe idea of management by objectives and areintegral to the scorecard ideas developed inthe 1990s.

knowledge management Systematicprocess of finding, selecting, organising,distilling and presenting information so asto improve comprehension of a specificarea of interest. Specific activities helpfocus the organisation on acquiring,storing and utilising knowledge for suchthings as problem solving, dynamiclearning, strategic planning and decisionmaking.

last in, first out (LIFO) See stock (inventory)valuation.

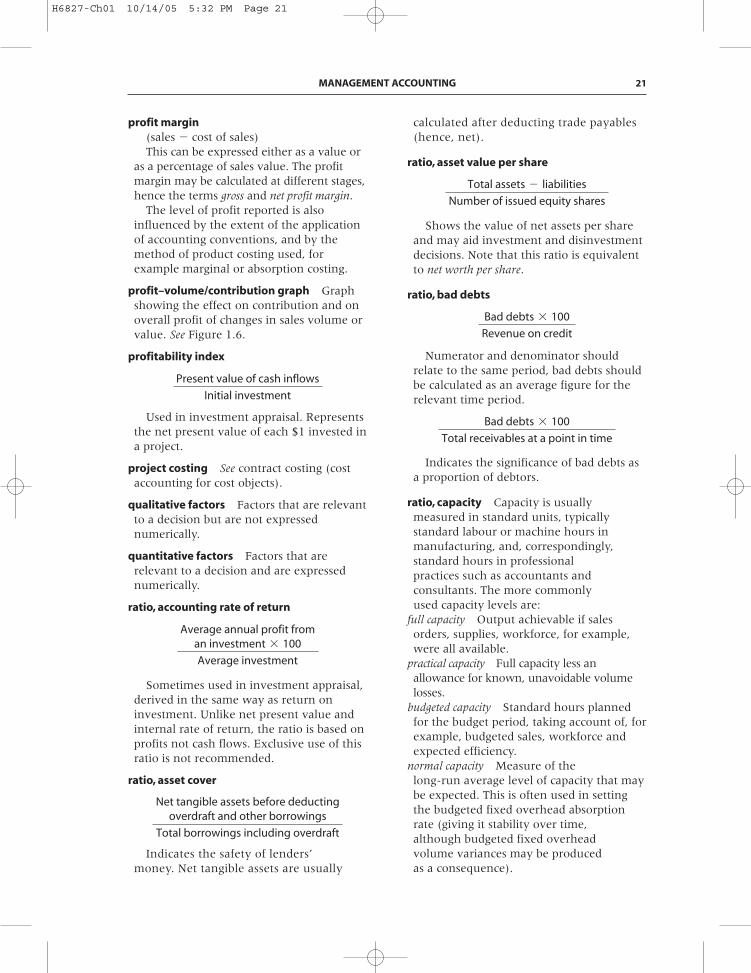

learning curve Mathematical expression ofthe commonly observed effect that, ascomplex and labour-intensive proceduresare repeated, unit labour times tend todecrease. The equation (see Figure 1.20)usually relates the average time taken perunit/batch to the cumulative number ofunits/batches produced. An alternative,little used, formulation uses the sameequation but relates the incremental (notaverage) time for the nth unit to thecumulative number of units/batchesproduced.

management accounting Managementaccounting is the application of theprinciples of accounting and financialmanagement to create, protect, preserveand increase value for the stakeholders of

for-profit and not-for-profit enterprises inthe public and private sectors.

Management accounting is an integralpart of management. It requires theidentification, generation, presentation,interpretation and use of relevantinformation to:• Inform strategic decisions and formulate

business strategy• Plan long, medium and short-run

operations• Determine capital structure and fund

that structure• Design reward strategies for executives

and shareholders• Inform operational decisions• Control operations and ensure the

efficient use of resources• Measure and report financial and non-

financial performance to managementand other stakeholders

• Safeguard tangible and intangible assets

• Implement corporate governanceprocedures, risk management andinternal controls.

management by exception Practiceof concentrating on activities thatrequire attention and ignoring thosewhich appear to be conforming toexpectations.

Typically, standard cost variances orvariances from budget are used to identifythose activities that require attention.

margin Difference between the sellingprice and cost of sales expressed either as apercentage of sales or as an absoluteamount. See mark-up.

marginal revenue Additional revenuegenerated from the sale of one additionalunit of output.

maximax criterion Criterion used to makea choice between alternative strategies. Thisfavours the strategy that might lead to thehighest possible profit, irrespective of theprobability of that profit actually beingachieved and the outcome if it is notsuccessful.

18 CIMA OFFICIAL TERMINOLOGY

H6827-Ch01 10/14/05 5:32 PM Page 18

maximin criterion Criterion used to make achoice between alternative strategies.This favours the strategy that generates thehighest profit if the worst outcome occurs.

minimax regret criterion Criterion used tomake a choice between alternativestrategies. This is the difference betweenthe best and worst possible payoff for eachoption. This criterion favours the strategythat minimises the maximum regret.

noise Random fluctuations that can bemistaken for important information. Noisecan confuse or divert attention fromrelevant information; efficiency in a systemis enhanced as the ratio of information tonoise increases.

non-financial performance measuresMeasures of performance based on non-financial information that may originate inand be used by operating departments to

MANAGEMENT ACCOUNTING 19

Example:

A team of technicians has assembled the first of a new model of aircraft engine in a total of 2,000 hours.Assuming an 80% learning curve, determine:

1. How long it will take to manufacture the next engine2. How long it will take to manufacture the next three engines3. Having already produced two engines, the average time per engine required for the next six

FIGURE 1.20 LEARNING CURVE

Engines Cumulative engines Average hours Cumulative hours per engine

1 1 2,000 2,0001 2 1,600 (2,000 � 0.8) 3,2002 4 1,280 (1,600 � 0.8) 5,1204 8 1,024 (1,280 � 0.8) 8,192

1. The next engine will take (3,200 � 2,000) hours � 1,200 hours2. The next three engines will take (5,120 � 2,000) hours � 3,120 hours3. (8,192 � 3,200)/6 � 832 hours

The learning curve

Output

Ave

rag

e ti

me

per

un

it

The learning curve can also be expressed mathematically as:

Y � ax�

Where Y is the average time taken per unit/batch to produce a cumulative number of units/batches:a is the time required to produce the first unitx is the cumulative number of units to be produced� is the coefficient of learning, which can be calculated as:

* for an 80% learning curve, this would be log 0.8

logarithm of rate of learning*

logarithm of 2.0

H6827-Ch01 10/14/05 5:32 PM Page 19

monitor and control their activities withoutany accounting input.

Non-financial performance measures maygive a more timely indication of the levelsof performance achieved than financialmeasures do, and may be less susceptible todistortion by factors such as uncontrollablevariations in the effect of market forces onoperations.

Non-financial measures are now integratedwith financial measures in systems suchas the balanced scorecard™. Examples ofnon-financial performance measures:

Area assessed Performance measure

Service quality Number of complaintsProportion of repeat

bookingsCustomer waiting timeOn-time deliveries

Production Set-up timesperformance Number of suppliers

Days’ inventory in hand

Output per employeeMaterial yield percentageSchedule adherenceProportion of output

requiring reworkManufacturing lead

times

Marketing Trend in market shareeffectiveness Sales volume growth

Customer visits per salesperson

Client contact hours per salesperson

Sales volume forecast v.actual

Number of customersCustomer survey

response information

Personnel Number of complaints received

Staff turnoverDays lost through

absenteeismDays lost through

accidents/sicknessTraining time per

employee

The values expected may varysignificantly between industries/sectors.

normal loss Expected loss, allowed for inthe budget, and normally calculated as apercentage of the good output from aprocess during a period of time. Normallosses are generally either valued at zero orat their disposal values.

operational gearing Relationship of fixedcost to total cost of an operating unit. Thegreater the proportion of total costs that arefixed (high operational gearing), thegreater is the advantage to the organisationof increasing sales volume. Conversely,should sales volumes drop, a highly gearedorganisation would find the highproportion of fixed costs to be a majorproblem, possibly causing a rapid swingfrom profitability into loss. Gearing mayalso be referred to as leverage. See ratio,gearing/leverage.

overhead absorption rate A means ofattributing overhead to a product orservice, based for example on direct labourhours, direct labour cost or machinehours.

direct labour cost percentage rate Overheadabsorption rate based on direct labourcost.

direct labour hour rate Overhead absorptionrate based on direct labour hours.

machine hour rate Overheadabsorption rate based on machine hours.See Figure 1.1.

payroll analysis Analysis of labour costsfor accounting purposes identifying, forexample: gross pay by department,operation or product; and/or gross payanalysed into direct pay or lost time.

performance measurement Process ofassessing the proficiency with which areporting entity succeeds, by the economicacquisition of resources and their efficientand effective deployment, in achieving itsobjectives. Performance measures may bebased on non-financial as well as onfinancial information. See non-financialperformance measures.

20 CIMA OFFICIAL TERMINOLOGY

H6827-Ch01 10/14/05 5:32 PM Page 20

profit margin(sales � cost of sales)This can be expressed either as a value or

as a percentage of sales value. The profitmargin may be calculated at different stages,hence the terms gross and net profit margin.

The level of profit reported is alsoinfluenced by the extent of the applicationof accounting conventions, and by themethod of product costing used, forexample marginal or absorption costing.

profit–volume/contribution graph Graphshowing the effect on contribution and onoverall profit of changes in sales volume orvalue. See Figure 1.6.

profitability index

Used in investment appraisal. Representsthe net present value of each $1 invested ina project.

project costing See contract costing (costaccounting for cost objects).

qualitative factors Factors that are relevantto a decision but are not expressednumerically.

quantitative factors Factors that arerelevant to a decision and are expressednumerically.

ratio, accounting rate of return

Sometimes used in investment appraisal,derived in the same way as return oninvestment. Unlike net present value andinternal rate of return, the ratio is based onprofits not cash flows. Exclusive use of thisratio is not recommended.

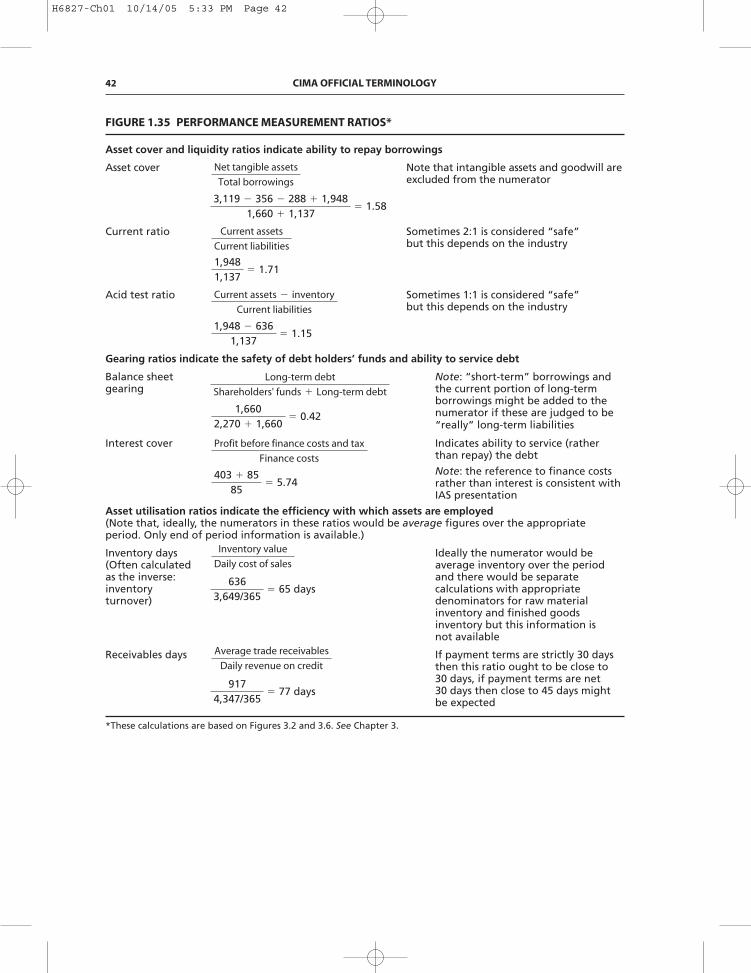

ratio, asset cover

Indicates the safety of lenders’money. Net tangible assets are usually

overdraft and other borrowingsNet tangible assets before deducting

Total borrowings including overdraft

an investment � 100Average annual profit from

Average investment

Present value of cash inflows

Initial investment

calculated after deducting trade payables(hence, net).

ratio, asset value per share

Shows the value of net assets per shareand may aid investment and disinvestmentdecisions. Note that this ratio is equivalentto net worth per share.

ratio, bad debts

Numerator and denominator shouldrelate to the same period, bad debts shouldbe calculated as an average figure for therelevant time period.

Indicates the significance of bad debts asa proportion of debtors.

ratio, capacity Capacity is usuallymeasured in standard units, typicallystandard labour or machine hours inmanufacturing, and, correspondingly,standard hours in professionalpractices such as accountants andconsultants. The more commonlyused capacity levels are:

full capacity Output achievable if salesorders, supplies, workforce, for example,were all available.

practical capacity Full capacity less anallowance for known, unavoidable volumelosses.

budgeted capacity Standard hours plannedfor the budget period, taking account of, forexample, budgeted sales, workforce andexpected efficiency.

normal capacity Measure of thelong-run average level of capacity that maybe expected. This is often used in settingthe budgeted fixed overhead absorptionrate (giving it stability over time,although budgeted fixed overheadvolume variances may be producedas a consequence).

Bad debts � 100

Total receivables at a point in time

Bad debts � 100

Revenue on credit

Total assets � liabilities

Number of issued equity shares

MANAGEMENT ACCOUNTING 21

H6827-Ch01 10/14/05 5:32 PM Page 21

On the following given data, the relatedratios are set out below:

Full capacity standard hours 100Practical capacity standard hours 95Budgeted capacity (budgeted

input hours, 90 at 90%efficiency) 81

Actual input hours 85Standard hours produced 68

idle capacity ratio

Indicates the budgeted shortfall incapacity as a proportion of practicalcapacity.

production volume ratio

Shows the actual output as a proportionof budgeted output.

production efficiency ratio

Measures the relationship betweenoutput produced and productive timetaken, which may be measured in eitherdirect labour or machine hours, asappropriate.

ratio, capital turnover

Expresses the number of times thatcapital is covered by sales in a year or therevenue generated by each $1 of capitalemployed. Capital employed is usuallycalculated as either:

Revenue for the year

Average capital employed in year

�68 � 100

85� 80%

Standard hours produced � 100

Actual hours

�68 � 100

81� 84%

Standard hours produced � 100

Budgeted capacity

�(95 � 81) � 100

95� 15%

(Practical capacity – budgeted capacity) � 100

Practical capacity

(a) total net assets(fixed assets � current assets – currentliabilities) or

(b) capital employed(equity � long-term debt).The two methods are equivalent.

ratio, contribution per unit of limiting factor

Used in short-term decision making tomeasure the contribution to fixedoverhead and profit generated by theuse of each unit of limiting factor. Thisis used to rank alternative uses of thelimiting factor.

ratio, contribution to sales

Of particular use in product profitplanning and as a means of rankingalternative products. Also important inbreakeven problems that assume a constantproduct mix. Note, although contributionto sales ratio can be used to rank products,it cannot be used to solve limiting factorproblems (unless the limiting factor is salesrevenue).

ratio, creditor days See ratio, payables days.

ratio, debtor days See ratio, receivablesdays.

ratio, dividend cover

Indicates the number of times the profitsattributable to the equity shareholders coverthe net dividends payable for the period.

ratio, dividend payout

Shows the proportion of earningsdistributed to ordinary shareholders asdividends. Indicates how safe the

Ordinary dividends for the year

Earnings attributable to theordinary shareholders

Earnings per share

Dividend per share

(Revenue � all variable costs) � 100

Revenue

Product/service contribution

Product/service usage of unitsof limiting factor

22 CIMA OFFICIAL TERMINOLOGY

H6827-Ch01 10/14/05 5:32 PM Page 22

dividend is (as does the dividend coverratio).

ratio, fixed asset turnover

Indicates the revenue generated byeach $1 of fixed assets, or the number oftimes fixed assets are turned over in theyear.

ratio, gearing/leverage Relates tofinancial gearing, which is therelationship between an entity’sborrowings, which includes both priorcharge capital, for example preferenceshares, and long-term debt, and its share-holders’ funds (ordinary sharecapital plus reserves). Gearing calculationscan be made in a number of ways, andmay be based on capital values or onearnings/interest relationships. Overdraftsand interest paid thereon may also beincluded.

Shows the effect of interest on theoperating profit (income gearing). See alsoratio, interest cover.

Shows the proportion of long-termfinancing which is being supplied by debt(balance sheet gearing).

A measure of the capacity to redeem debtobligations by the sale of assets.

Measures ability to redeem debt. Anentity with a high proportion of priorcharge capital to shareholders’ funds ishigh geared, and is low geared if thereverse situation applies.

of financereturns on investment and servicing

Repayments of debt due within one year

Operating cashflows � taxation paid �

Total long-term debt

Total assets

Total long-term debt

Shareholders' funds � long-term debt

Profit before interest and tax

Profit before tax

Revenue for the year

Average net book value of fixed assets

ratio, gross profit to sales revenue(gross profit margin %)

Used to gain an insight into therelationship between production/purchasingcosts and sales revenues.

ratio, interest cover

Used by lenders to determinevulnerability of interest payments to adrop in profit.

ratio(s), inventory daysnumber of days’ inventory

Number of days’ inventory at theforecast or recent usage rate. Can beapplied to finished goods, raw materialand work in progress by usingappropriate numerators anddenominators.

number of weeks’ inventoryThe efficiency of inventory utilisation is

indicated by:

These ratios are normally calculatedusing appropriate values although, incertain circumstances, quantities maybe used.

ratio, length of order book

The sales value of production may bebased on planned, current or availablecapacity production.

Sales value of orders outstanding

Sales value of production perday/week/month

Work in progress

Average weekly production

Raw material stock

Average weekly raw material usage

Finished goods stock

Average weekly despatches

Stock value

Average daily cost of sales in period

Profit before interest and tax

Interest payable

(Sales – cost of sales) � 100

Sales for the period

MANAGEMENT ACCOUNTING 23

H6827-Ch01 10/14/05 5:32 PM Page 23

ratio(s), liquidity Relate to working capitaland indicate the ability to meet liabilitiesfrom assets available. The most commonlyused are:

acid test/quick ratio

Indicates the ability to pay creditors inthe short term.

current ratio

An overall measure of liquidity.

ratio, margin of safety

Indicates the percentage by whichforecast revenue exceeds or falls short ofthat required to break even.

ratio, net profit to sales revenue(net profit margin %)

A key profitability ratio. If the numeratoris not multiplied by 100 it shows the profitgenerated by each $1 of sales.

ratio, payables days

Indicates the average time taken, incalendar days, to pay for supplies receivedon credit. Adjustment is needed if the ratiois materially distorted by value added orother taxes.

ratio, price/earnings (P/E ratio)

Shows the number of years it wouldtake to recoup an equity investment fromits share of the attributable profit. The P/Eratio values the shares of the company asa multiple of current or prospective

Market price per share

Earnings per share

Average trade payables

Average daily purchases on credit terms

Net profit before interest and tax � 100

Revenue

breakeven revenue ) � 100(Forecast revenue �

Forecast revenue

Current assets at end of period

Current liabilities at end of period

Current assets – stock at end of period

Current liabilities at end of period

earnings. The P/E ratio is the mostcommon way of reporting the relationshipbetween earnings and share prices,although its inverse, the earnings yield,is probably intuitively easier to grasp.A low P/E ratio implies a high earningsyield. A low P/E ratio might indicatethat the market perceives earnings to be“low quality”.

ratio, profit per employee

Indication of the effectiveness of theemployment of staff. When there arefull- and part-time employees, full-timeequivalents should be used. See sales peremployee.

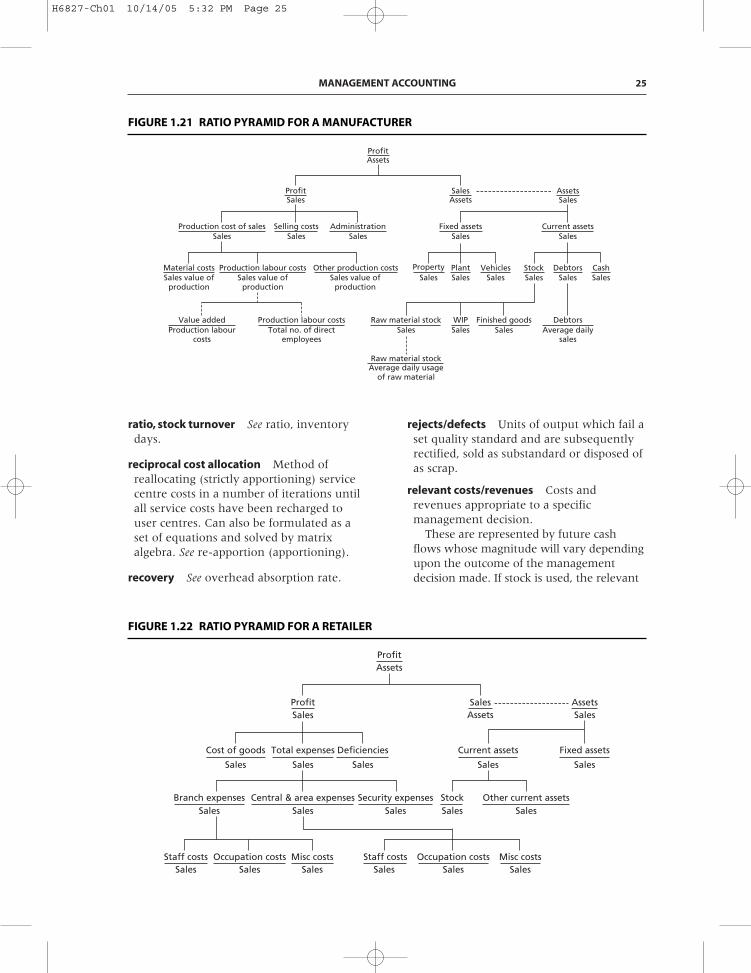

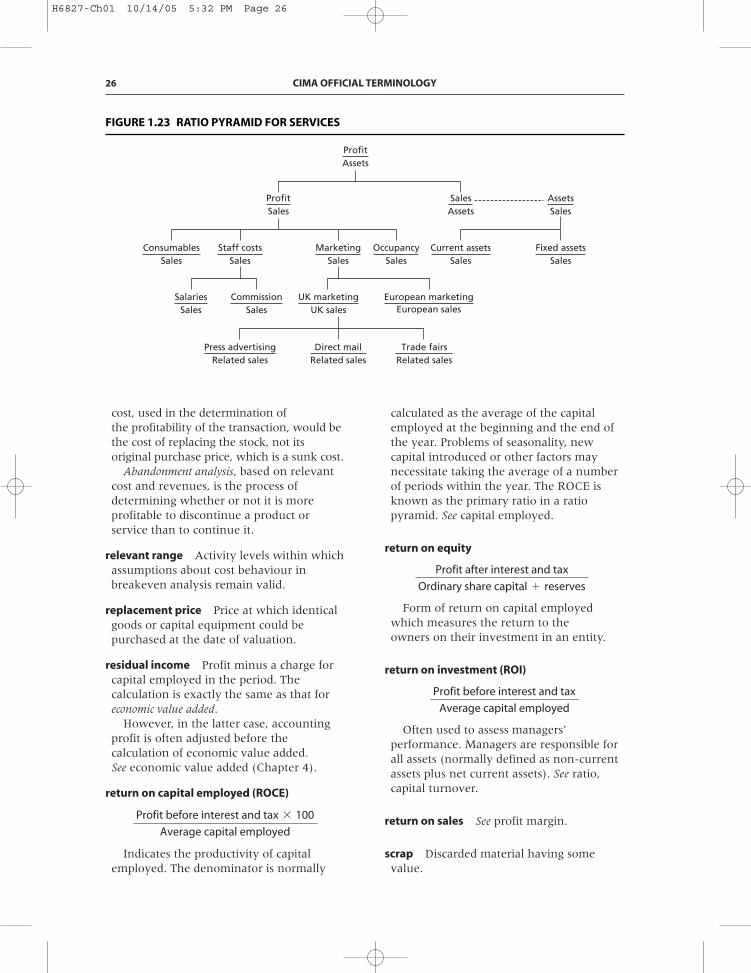

ratio pyramid The analysis of a primaryratio into mathematically linked secondaryratios. For example:

primary ratio

(a)

Secondary ratio

(b) (c)

Ratio a � b � c. Ratios b and c can beanalysed by further ratios if desired. Thepyramid continues with further analysis ofthe secondary ratios. See Figures 1.21, 1.22and 1.23.

ratio, receivables days

Indicates the average time taken, incalendar days, to receive payment fromcredit customers. Adjustment is needed ifthe ratio is materially distorted by valueadded or other taxes.

ratio, sales per employee

Indicator of labour productivity. See profitper employee.

Revenue for the year

Average number of employees

Average trade receivables

Average daily revenue on credit terms

Turnover

Capital employed

Profit

Turnover

Profit

Capital employed

Profit for the year before interest and tax

Average number of employees

24 CIMA OFFICIAL TERMINOLOGY

H6827-Ch01 10/14/05 5:32 PM Page 24

ratio, stock turnover See ratio, inventorydays.

reciprocal cost allocation Method ofreallocating (strictly apportioning) servicecentre costs in a number of iterations untilall service costs have been recharged touser centres. Can also be formulated as aset of equations and solved by matrixalgebra. See re-apportion (apportioning).

recovery See overhead absorption rate.

rejects/defects Units of output which fail aset quality standard and are subsequentlyrectified, sold as substandard or disposed ofas scrap.

relevant costs/revenues Costs andrevenues appropriate to a specificmanagement decision.

These are represented by future cashflows whose magnitude will vary dependingupon the outcome of the managementdecision made. If stock is used, the relevant

MANAGEMENT ACCOUNTING 25

DebtorsAverage daily

sales

Raw material stockAverage daily usage

of raw material

Raw material stockSales

Finished goodsSales

WIPSales

CashSales

DebtorsSales

StockSales

VehiclesSales

PlantSales

PropertySales

Production labour costsTotal no. of direct

employees

Value addedProduction labour

costs

Other production costsSales value of

production

Production labour costsSales value of

production

Material costsSales value of

production

Current assetsSales

Fixed assetsSales

AdministrationSales

Selling costsSales

Production cost of salesSales

AssetsSales

SalesAssets

ProfitSales

ProfitAssets

FIGURE 1.21 RATIO PYRAMID FOR A MANUFACTURER

ProfitAssets

ProfitSales Assets

Sales AssetsSales

Sales

Cost of goods

Sales

Total expenses

Sales

Deficiencies

Sales

Current assets

Sales

Fixed assets

SalesOther current assets

SalesStock

SalesSecurity expenses

SalesCentral & area expenses

SalesBranch expenses

SalesStaff costs

SalesStaff costs

SalesOccupation costs

SalesOccupation costs

SalesMisc costs

SalesMisc costs

FIGURE 1.22 RATIO PYRAMID FOR A RETAILER

H6827-Ch01 10/14/05 5:32 PM Page 25

cost, used in the determination ofthe profitability of the transaction, would bethe cost of replacing the stock, not itsoriginal purchase price, which is a sunk cost.

Abandonment analysis, based on relevantcost and revenues, is the process ofdetermining whether or not it is moreprofitable to discontinue a product orservice than to continue it.

relevant range Activity levels within whichassumptions about cost behaviour inbreakeven analysis remain valid.

replacement price Price at which identicalgoods or capital equipment could bepurchased at the date of valuation.

residual income Profit minus a charge forcapital employed in the period. Thecalculation is exactly the same as that foreconomic value added.

However, in the latter case, accountingprofit is often adjusted before thecalculation of economic value added.See economic value added (Chapter 4).

return on capital employed (ROCE)

Indicates the productivity of capitalemployed. The denominator is normally

Profit before interest and tax � 100

Average capital employed

calculated as the average of the capitalemployed at the beginning and the end ofthe year. Problems of seasonality, newcapital introduced or other factors maynecessitate taking the average of a numberof periods within the year. The ROCE isknown as the primary ratio in a ratiopyramid. See capital employed.

return on equity

Form of return on capital employedwhich measures the return to theowners on their investment in an entity.

return on investment (ROI)

Often used to assess managers’performance. Managers are responsible forall assets (normally defined as non-currentassets plus net current assets). See ratio,capital turnover.

return on sales See profit margin.

scrap Discarded material having somevalue.

Profit before interest and tax

Average capital employed

Profit after interest and tax

Ordinary share capital � reserves

26 CIMA OFFICIAL TERMINOLOGY

ProfitAssets

ProfitSales Assets

Sales AssetsSales

SalesConsumables

SalesStaff costs

SalesMarketing

SalesOccupancy

SalesCurrent assets

SalesFixed assets

SalesCommission

SalesSalaries

Related salesTrade fairs

Related salesDirect mail

Related salesPress advertising

UK salesUK marketing

European salesEuropean marketing

FIGURE 1.23 RATIO PYRAMID FOR SERVICES

H6827-Ch01 10/14/05 5:32 PM Page 26

standard Benchmark measurement ofresource usage or revenue or profitgeneration, set in defined conditions.Standards can be set on a number of bases:(a) on an ex ante estimate of expected

performance;(b) on an ex post estimate of attainable

performance;(c) on a prior period level of performance

by the same organisation;(d) on the level of performance achieved

by comparable organisations; or(e) on the level of performance required

to meet organisational objectives.Standards may also be set at attainable

levels that assume efficient levels ofoperation, but that include allowance fornormal loss, waste and machine downtime, or at ideal levels that make noallowance for the above losses, and areonly attainable under the most favourableconditions. The effect of different levels onstaff motivation will be an importantinfluence on the type of standards that areused. See standard, ex ante, and standard,ex post.

standard cost card/standard productspecification Document or digital recorddetailing for each individual product, thestandard inputs required for production aswell as the standard selling price. Inputs arenormally divided into labour, material andoverhead categories, and both price andquantity information is shown for each.

standard direct labour cost Planned cost ofdirect labour.

(standard direct labour time for one unitof product � standard labour rate)

There are separate calculations fordifferent processes and/or grades of labour.

standard, ex ante Before the event. An exante budget or standard is set before aperiod of activity commences.

standard, ex post After the event. An expost budget, or standard, is set afterthe end of a period of activity, when itcan represent the optimum achievablelevel of performance in the conditionswhich were experienced. Thus thebudget can be flexed, and standards can

reflect factors such as unanticipatedchanges in technology and in pricelevels. This approach may be used inconjunction with sophisticated cost andrevenue modelling to determine how farboth the plan and the achieved resultsdiffered from the performance thatwould have been expected in thecircumstances which were experienced.

standard hour or minute Amount of workachievable, at standard efficiency levels, inan hour or minute.

standard performance – labour Level ofefficiency which appropriately trained,motivated and resourced employees canachieve in the long-run.

stock (inventory) valuationaverage cost Used to price issues of goods ormaterials at the weighted average cost of allunits held.

first-in, first-out (FIFO) Used to price issuesof goods or materials based on the cost ofthe oldest units held, irrespective of thesequence in which the actual issue of unitsheld takes place. Closing stock is, therefore,valued at the cost of the oldest purchases.

last-in, first-out (LIFO) Used to price issuesof goods or materials based on the cost ofthe most recently received units. Cost ofsales in the income statement is, therefore,valued at the cost of the most recentpurchases. LIFO is permitted under USGAAP but is not permitted by IAS 2 (orSSAP 9 in the UK).

standard cost All units held as stock arevalued at a standard cost so that unitsissued and closing stock are valued atstandard cost, with any variance betweenactual costs incurred and standard costreported in the income statement in theperiod in which it is incurred. All the abovemethods value stock at cost, but IAS 2requires all stocks to be valued at the lowerof cost and net realisable value. See fairvalue less costs to sell (Chapter 3).

strategic business unit Section, usually adivision, within a larger organisation that hasa significant degree of autonomy, typicallybeing responsible for developing andmarketing its own products and services.

MANAGEMENT ACCOUNTING 27

H6827-Ch01 10/14/05 5:32 PM Page 27

super variable costing See throughputaccounting.

theory, agency Hypothesis that attempts toexplain elements of organisationalbehaviour through an understanding of therelationships between principals (such asshareholders) and agents (such as entitymanagers and accountants). A conflict mayexist between the actions undertaken byagents in furtherance of their own self-interest, and those required to promote theinterests of the principals. Within thehierarchy of entities, the same goalincongruence may arise when divisionalmanagers promote their own self-interestover those of other divisions and of theentity generally.

theory, contingency Theory relatingto the design of accounting systemsthat presupposes that systems canbe effectively designed to suit thecircumstances of the firm including itstechnology, entity structure and itscompetitive environment. For example,it is argued that mechanistic (hierarchical,bureaucratic) systems can be effective instable environments. Organic (typicallyflatter, task-related) systems are said tobe more appropriate in more turbulent,competitive environments.

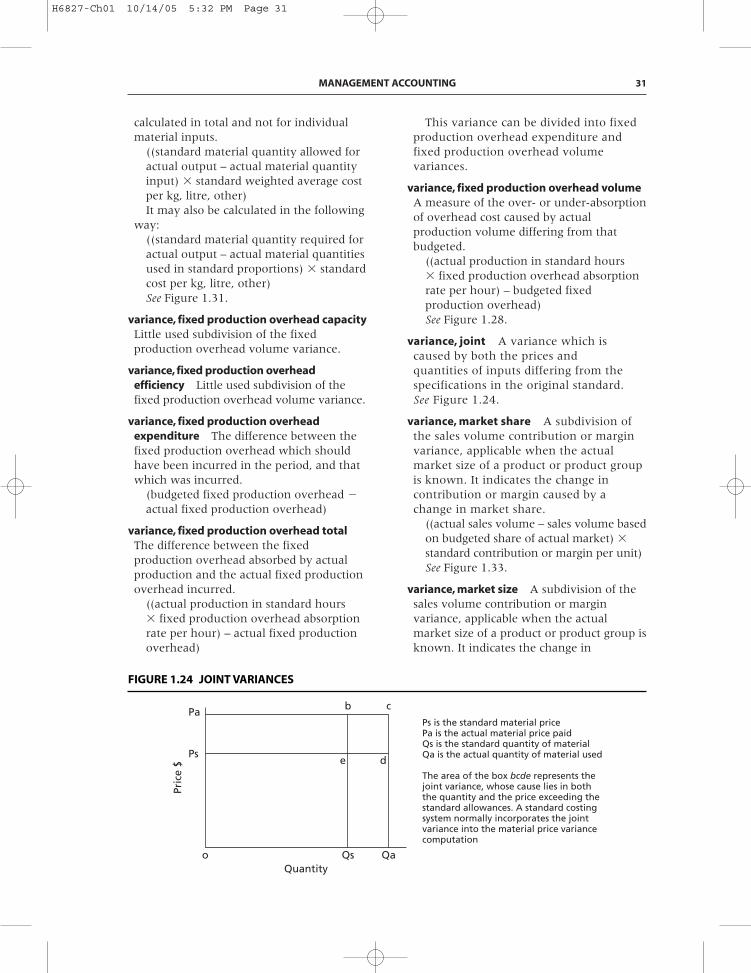

theory of constraints (TOC) Procedure basedon identifying bottlenecks (constraints),maximising their use, subordinating otherfacilities to the demands of the bottleneckfacilities, alleviating bottlenecks andre-evaluating the whole system.(Goldratt created this concept).

throughput Term defined, in work byGoldratt, as sales minus material andcomponent costs. Similar to contributionexcept material is considered the onlyvariable cost. Goldratt argues that labourcosts should be treated as fixed. InGoldratt’s analysis operating expense is allnon-material costs and inventory cost isdefined as the cost of assets employed.

throughput accounting (TA) Variable costaccounting presentation based on thedefinition of throughput (sales minus

material and component costs). Sometimesreferred to as super variable costing becauseonly material costs are treated as variable.

throughput per bottleneck minute Methodof ranking products that share the same(bottleneck) facility. Very similar to the useof contribution per unit of limiting factor.

throughput ratios Several ratios weredefined by Galloway and Waldron basedon the definition of throughput. The TA(throughput accounting) ratio is:

Note: Galloway and Waldron define factorycost in the same way that Goldratt definesoperating expense. See throughput.

If the TA ratio is greater than 1 theproduct in question is “profitable” because,if all capacity were devoted to that product,the throughput generated would exceed thetotal factory cost. If there was a bottleneckproducts could be ranked by a variant ofthe TA ratio (although the ranking isthe same as that derived by the use ofthroughput per bottleneck minute). Otherperformance ratios suggested include:

and

transfer price Price at which goods orservices are transferred between differentunits in the same company. May be set ona number of bases, such as marginal cost,full cost, market price or negotiation. Forthe transfer of goods between units indifferent countries, tax implications meanthat the respective governments have toaccept the method used. They are likely toinsist on arm’s-length transfer prices.

uniform accounting System by whichdifferent entities in the same industry adoptcommon concepts, principles andassumptions in order to generateaccounting information that facilitatesinter-entity comparison or a system of

throughput

material cost

throughput

labour cost

Throughput per bottleneck minute

Factory cost per bottleneck minute

28 CIMA OFFICIAL TERMINOLOGY

H6827-Ch01 10/14/05 5:32 PM Page 28

classifying financial accounts in a similarmanner within defined business sectors of anational economy to ensure comparability.

value added Traditionally the differencebetween sales revenue and the cost ofmaterials and bought-out services.Alternatively, it might be calculated as thesum of profit, interest and all conversioncosts. Recently, more commonly usedin the context of economic value added.See economic value added, Chapter 4.

value analysis Systematic interdisciplinaryexamination of factors affecting the cost ofa product or service, in order to devisemeans of achieving the specified purposemost economically at the required standardof quality and reliability (BS 3138)1.

value driver Activity or organisationalfocus which enhances the perceived valueof a product or service in the perceptionof the consumer, and which thereforecreates value for the producer. Advancedtechnology, reliability or reputation forcustomer care may be value drivers.

value engineering Redesign of an activity,product or service so that value to thecustomer is enhanced while costs arereduced (or, at least, increase by less thanthe resulting price increase).

variance Difference between a planned,budgeted or standard cost and the actualcost incurred. The same comparisons maybe made for revenues.

variance, administrative cost Measurementof the extent of any over- or underspendon administrative costs.

(budgeted cost of administration � actualcost)

variance analysis Evaluation of performanceby means of variances, whose timelyreporting should maximise the opportunityfor managerial action. See Figure 1.34.

variance, budget Difference, for each costor revenue element in a budget, betweenthe budgeted amount and the actual cost orrevenue. Where flexible budgeting isemployed, it is the difference between theflexed budget and the actual value.