Embed Size (px)

Citation preview

malaysian EcOnOmyFirst Quarter 2011

1st kulit warna.indd 1 5/20/11 11:45:48 PM

Highlights

❐ Global economy grew at a moderate pace

❐ The Malaysian economy continued to expand

❐ Growth spearheaded by services and manufacturing sectors

❐ Growth expected to strengthen in the coming quarters of 2011

Quarterly Updateon the Malaysian Economy – 1 Quarter 2011

International Performance

Moderate global growth…

The global economy continued to grow at a moderate pace in the first quarter of 2011. Most advanced economies registered moderate growth as domestic demand remained subdued amid elevated unemployment. Global growth was also impacted by the contraction of the Japanese economy after the March 11 earthquake. Growth in many emerging and developing economies was strong, contributed largely by robust domestic demand, and favourable export performance despite growing concerns of overheating. Unrest in the Middle East and North Africa led to sharp increases in oil prices and rising inflation worldwide.

In the United States (US), GDP grew at a slower pace of 2.3% (Q4 2010: 2.8%). Growth was mainly supported by consumption expenditure on durable goods and investment in equipment and software which rose 11.4% and 14.7% (Q4 2010: 10.9%; 16.9%), respectively. However, higher import growth and sharply lower government spending on defence led to the deceleration in overall expansion. Industrial production remained stable, increasing by 6.0% (Q4 2010: 6.0%) with marginal increase in capacity utilisation rate to 77.1%.

(Q4 2010: 76.1%). Labour market conditions improved with the unemployment rate easing to 8.9% (Q4 2010: 9.6%), following higher net job creation by the private sector. The housing sector remained depressed with housing starts, sales and building permits contracting significantly by 8.7%, 18.2% and 13.9% (Q4 2010: -5.2%; -19.3%; -8.2%), respectively. The Consumer Price Index (CPI) increased 2.1% (Q4 2010: 1.3%) due to rising food and fuel prices. Despite the build-up of inflationary pressures, the Federal Reserve continued with the accommodative monetary stance and maintained its policy rate close to zero to strengthen growth prospects.

st

2

The euro area continued to record a higher growth of 2.5% (Q4 2010: 2.0%), following favourable performance in most countries, except in Greece and Portugal. Germany, the largest economy, expanded significantly by 4.8% (Q4 2010: 3.8%), the highest pace since the German reunification in 1990. Growth was led by investment and consumer spending. In France, GDP grew strongly by 2.2% (Q4 2010: 1.4%) due to significantly higher manufacturing production and investment.

China’s economy continued to sustain a strong growth of 9.7% (Q4 2010: 9.8%) contributed mainly by domestic demand and external trade. Private consumption expanded in tandem with increases in rural and urban per capita household income of 14.3% and 7.1%, respectively. This was reflected by the steady growth in retail sales of 16.3% (Q4 2010: 22.0%). Investment in real estate increased 34.1%, of which residential buildings grew by 37.4%. Merchandise exports increased 26.5% (Q4 2010: 24.9%), while imports rose 32.6% (Q4 2010: 29.5%). The CPI rose to 5.0% (Q4 2010: 4.6%) due to higher food and property prices. To mop up excess liquidity in the banking system, the People’s Bank of China revised upward its benchmark lending and one-year deposit rates by 25 basis points to 6.06% and 3.0%, respectively in February. In addition, the reserve requirement ratio for major banks was increased three times by 50 basis points each from 18.5% to 20.0%.

Japan’s GDP contracted 1.0% (Q4 2010: 2.2%), following the earthquake disaster. Private consumption which accounts for almost 60% of Japanese economy declined 1.0% (Q4 2010: 0.6%) as consumers reduced on spending after the quake. Capital investment moderated to 2.8% (Q4 2010: 5.5%) due to lacklustre business spending on anticipation of lower corporate profits. External trade remained positive despite merchandise exports moderating to 12.9% (Q4 2010: 13.3%), following the disruption to production and

supply chains. Meanwhile, imports gained 22.7% (Q4 2010: 19.4%), mainly due to the higher cost of imports, particularly petroleum products. The CPI trended down to 0% (Q4 2010: 0.1%), mainly due to falling housing prices. The Bank of Japan kept its policy interest rate unchanged between 0.0% to 0.1% to help stimulate economic growth.

Korea’s GDP grew 4.2% (Q4 2010: 4.7%) attributed to higher exports at 18.6% (Q4 2010: 15.8%), particularly semiconductors, electronic components and automobiles. Private comsumption was stable at 3.0% (Q4 2010: 2.9%) due to sustained spending on automobiles and audio-visual products. On the supply side, manufacturing output grew 9.9% (Q4 2010: 11.1%), mainly due to increases in electrical equipment, steel and motor vehicles. The wholesale and retail trade as well as financial intermediation sectors expanded, partially offsetting the decline in recreational, cultural and sporting services. The CPI rose 4.5% in line with higher food and energy costs. To ease the impact of rising inflation, the Bank of Korea increased its policy rate for three consecutive months from 2.66% to 2.92%.

Major economies in the ASEAN region registered six consecutive quarters of positive growth since the fourth quarter of 2009. Singapore’s GDP expanded 8.3% (Q4 2010: 12.0%), mainly driven by the manufacturing and services sectors which grew 13.1% and 7.3%, respectively. Growth in the manufacturing sector was attributed to the strong performance in the electronics and precision engineering clusters, while growth in the services sector was driven primarily by financial services activities. Indonesia’s GDP continued to register strong growth at 6.5% (Q4 2010: 6.9%), largely due to a surge in exports, sustained private consumption and rising investment. Bank Indonesia raised its policy rate in February from 6.50% to 6.75% to mitigate rising inflationary pressures.

3

Private consumption expenditure grew 6.7% (Q4 2010: 6.4%), backed by favourable labour market conditions and higher disposable income, following firm commodity prices and a vibrant stock market. Robust consumer spending was ref lected by the strong performance of major consumption indicators such as sales of food, credit card spending and consumption credit disbursed. These indicators recorded a double-digit growth of 19.3%, 12.5% and 12.4% (Q4 2010: 28.5%; 14.2%; 27.2%), respectively. This was also reflected by the Consumer Sentiments Index (CSI) which remained above the 100-point threshold at 108.2 points (Q4 2010: 117.2 points). Meanwhile, public consumption grew strongly by 6.1% (Q4 2010: 0.1%), led by higher expenditure on emoluments as well as supplies and services.

Malaysian Economy

Growth remained healthy…

Malaysia’s GDP grew 4.6% in the first quarter of 2011 (Q4 2010: 4.8%) led by steady performance of the services and manufacturing sectors. The services sector expanded 5.9% (Q4 2010: 6.1%), mainly supported by the wholesale and retail trade, finance and insurance as well as real estate and business services sub-sectors. The manufacturing sector registered a positive growth of 5.4% (Q4 2010: 6.2%), despite contraction in the transport equipment and other manufactures as well as electrical and electronics (E&E)sub-sectors. The construction sector expanded 3.8% (Q4 2010: 5.6%) on account of higher activity in the residential and non-residential sub-sectors. The agriculture sector registered a smaller decline of 0.3% (Q4 2010: -3.9%) largely contributed by higher production of livestock, fishing and other agriculture sub-sectors. Meanwhile, the mining sector contracted 3.0% (Q4 2010: -1.2%), affected by lower production of crude oil.

Domestic demand strengthened further…

Domestic demand remained robust, expanding by 6.6% (Q4 2010: 5.9%) during the quarter. This was attributed to buoyant consumer spending, strong private investment as well as higher public consumption.

4

Gross Fixed Capital Formation recorded growth of 6.5% (Q4 2010: 10.0%) in tandem with strengthening domestic economic activities as well as rigorous measures undertaken by the Government to spur private investment. Strong regional demand also helped to boost private investment activities. Easy access to financing was reflected by strong loan disbursements to businesses which increased by 6.3%. Other major investment indicators such as imports of capital goods, intermediate goods and sales of commercial vehicles also recorded strong growth rates of 9.3%, 13.2% and 10.2% (Q4 2010: 10.5%; 10.5%; 16.4%), respectively. In line with this, the Business Conditions Index (BCI) rose sharply to 113.3 points (Q4 2010: 99.5 points), indicating increased business optimism.

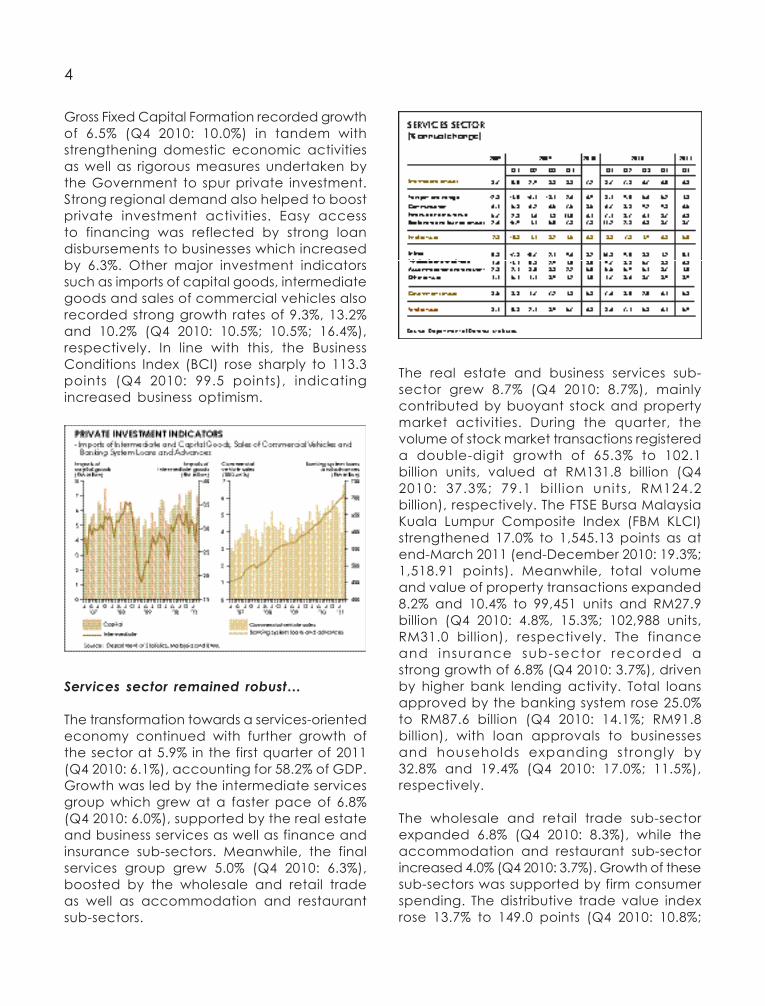

Services sector remained robust…

The transformation towards a services-oriented economy continued with further growth of the sector at 5.9% in the first quarter of 2011 (Q4 2010: 6.1%), accounting for 58.2% of GDP. Growth was led by the intermediate services group which grew at a faster pace of 6.8% (Q4 2010: 6.0%), supported by the real estate and business services as well as finance and insurance sub-sectors. Meanwhile, the final services group grew 5.0% (Q4 2010: 6.3%), boosted by the wholesale and retail trade as well as accommodation and restaurant sub-sectors.

The real estate and business services sub-sector grew 8.7% (Q4 2010: 8.7%), mainly contributed by buoyant stock and property market activities. During the quarter, the volume of stock market transactions registered a double-digit growth of 65.3% to 102.1 billion units, valued at RM131.8 billion (Q4 2010: 37.3%; 79.1 bi l l ion units, RM124.2 billion), respectively. The FTSE Bursa Malaysia Kuala Lumpur Composite Index (FBM KLCI) strengthened 17.0% to 1,545.13 points as at end-March 2011 (end-December 2010: 19.3%; 1,518.91 points). Meanwhile, total volume and value of property transactions expanded 8.2% and 10.4% to 99,451 units and RM27.9 billion (Q4 2010: 4.8%, 15.3%; 102,988 units, RM31.0 billion), respectively. The finance and insurance sub-sector recorded a strong growth of 6.8% (Q4 2010: 3.7%), driven by higher bank lending activity. Total loans approved by the banking system rose 25.0% to RM87.6 billion (Q4 2010: 14.1%; RM91.8 billion), with loan approvals to businesses and households expanding strongly by 32.8% and 19.4% (Q4 2010: 17.0%; 11.5%), respectively.

The wholesale and retail trade sub-sector expanded 6.8% (Q4 2010: 8.3%), while the accommodation and restaurant sub-sector increased 4.0% (Q4 2010: 3.7%). Growth of these sub-sectors was supported by firm consumer spending. The distributive trade value index rose 13.7% to 149.0 points (Q4 2010: 10.8%;

5

138.1 points), with the wholesale and retail trade value index increasing 14.5% and 8.3% (Q4 2010: 12.2%; 7.9%), respectively.

The communication sub-sector rose 6.5% (Q4 2010: 9.8%), supported by higher usage of cellular, broadband and 3G services. As at end-March 2011, the cellular phone subscriber base grew 11.9% to 34.5 million with a penetration rate of 121.0% (end-December 2010: 12.3%; 33.9 million; 119.2%). Growth was mainly driven by the non-voice segment following rising demand for data services. In addition, the performance of the 3G segment, which surged 29.6% to 9.7 million subscriptions (end-December 2010: 25.2%; 9.2 million), provided the impetus for growth in the cellular segment. Meanwhile, the broadband subscriber base expanded 68.1% to 4.9 million subscriptions to record a household penetration rate of 57.6% (end-December 2010: 80.2%; 4.7 million; 55.6%). Various initiatives to enhance broadband adoption and coverage, particularly in the rural areas and among low-income households boosted demand for broadband services. The number of wireless hotspots also increased to 14,061 locations nationwide (end-December 2010: 11,291). In contrast, the number of fixed line subscribers remained at 4.4 million, registering a household penetration rate of 42.6% (end-December 2010: 4.4 million; 42.3%).

The transport and storage sub-sector grew 4.3% (Q4 2010: 5.2%), supported by sustained travel and trade-related activities. Port activity remained upbeat attributed to favourable external trade amid continued improvements in port efficiency and productivity. Container handling at seven major ports posted a double-digit growth of 12.7% to 4.7 million TEUs (Q4 2010: 8.9%; 4.6 million TEUs). Port Klang accounted for 48.3% of total container throughput and remained the largest container port in the country, while Port of Tanjung Pelepas handled 38.3%.

6

In the land transport segment, traffic volume on tolled highways rose 7.0% to 356.1 million vehicles (Q4 2010: 6.7%; 372.1 mil l ion), especially during the school holidays and festive seasons. Total ridership on urban rail services (Ampang Line, Kelana Jaya Line, KL Monorail, Express Rail Link and KTM Komuter) expanded strongly by 10.1% to 44.1 million passengers (Q4 2010: 3.7%; 43.6 million), boosted by ongoing Government initiatives to improve public transport in the Klang Valley. KTM intercity train passenger ridership increased 7.2% to 1.1 million (Q4 2010: 11.6%; 1.2 million), while revenue rose 23.1% to RM25.9 million (Q4 2010: 24.6%; RM29.1 million), largely due to higher Electric Train Service ridership. KTMB cargo tonnage increased 7.8%, following higher volume of construction-related freight, which saw revenue rising to RM30.1 million (Q4 2010: -1.9%; RM29.9 million).

Total passenger volume at al l airports registered a double-digit growth of 11.8% to 15.4 million (Q4 2010: 6.3%; 15.9 million). Likewise, total passengers on MAS and AirAsia rose 10.3% to 7.5 million (Q4 2010: 6.6%; 7.9 million). This was spurred by increased frequency, connectivity and capacity as well as continuous promotional activities. Total air cargo handled at all airports, however, grew marginal ly by 0.1% to 215.3 million tonnes (Q4 2010: 3.0%; 235.6 million tonnes). Cargo handling by MAS and AirAsia contracted 2.3% to 121.2 million tonnes (Q4 2010: 2.9%; 138.6 million tonnes), mainly due to slower exports of E&E products.

The utilities sub-sector grew marginally by 0.4% (Q4 2010: 4.2%) in line with lower demand from the manufacturing sector. Electricity sales increased 1.2% (Q4 2010: 3.8%) with maximum demand for electricity peaking at 14,989 megawatts (MW) in March 2011 (Q4 2010: 14,916 MW in October 2010). Growth of the other services sub-sector remained at

3.9% (Q4 2010: 3.9%) attributed to sustained private education and health activities. Meanwhile, the government services sub-sector grew 5.3% (Q4 2010: 6.1%).

G r o w t h l e d b y d o m e s t i c - o r i e n t e d industries…

Value-added of the manufacturing sector expanded 5.4% (Q4 2010: 6.2%) led by stronger domestic-oriented manufacturing act iv i t ies . Th i s was ref lected by the increase in manufacturing output at 5.7% (Q4 2010: 6.6%) and sales of manufacturing products which rose s ign i f icant ly by 10.6% to RM143.7 billion (Q4 2010: 7.5%; RM139.1 billion) during the period. Meanwhile, the overall capacity utilisation rate in the sector remained high at 82.9% (Q4 2010: 82.8%).

The domestic-oriented industries grew 7.3% (Q4 2010: 8.4%) with construction-related sub-sectors continuing to drive growth. Of significance, output of fabricated metal products as well as non-metallic mineral and other related products registered strong growth of 32.8% and 21.7% (Q4 2010: 24.7%; 26.1%), respectively. Output of transport equipment contracted 4.5% (Q4 2010: 20.8%), mainly due to lower production of engines, parts

7

Production of export-oriented industries grew 4.3% (Q4 2010: 5.1%), supported by strong global demand for resource-based products, such as petroleum (26.1%) and rubber (13.5%). Likewise, output of machinery and equipment increased further by 49.3% (Q4 2010: 31.3%). However, output of E&E products contracted 10.4% (Q4 2010: -2.0%) due to lower external demand for computers and computer peripherals, as a result of changes in consumer preference for media tablets and smart phones. Consequently, output of computers and computer peripherals declined 40.4% during the quarter (Q4 2010: -31.1%).

Strong performance of agriculture food produce…

The agriculture sector improved with a smaller negative growth of 0.3% (Q4 2010: -3.9%), bolstered by the strong performance o f t h e l i v e s t o c k , f i s h i n g a n d o t h e r a g r i c u l t u r e s u b - s e c t o r s . M e a n w h i l e , value-added of the oil palm sub-sector contracted 7.9% (Q4 2010: -15.4%) due to lower crude palm oi l product ion, following unfavourable weather conditions. S imi lar ly, value-added of the forestry and logging sub-sector declined further by 12.1% (Q4 2010: -4.2%), on account of lower logging activity, particularly in Sabah and Sarawak. Despite the onset of the winter ing season, value-added of the rubber sub-sector g rew 2 .2% (Q4 2010: 6.3%), backed by increased tapping activity, fol lowing f i rm rubber p r ices which averaged RM15.44 per k i l og ra m m e ( Q 4 2 0 1 0 : RM 1 2 .8 5 p e r kilogramme). Meanwhile, the livestock sub-sector rose sharply by 9.6% (Q4 2010: 5.1%), following higher output of poultry, eggs and cattle. Value-added of the fishing sub-sector strengthened further by 7.7% (Q4 2010: 3.8%) due to higher landings of marine fish. The other agriculture sub-sector grew sharply by 9.7% (Q4 2010: 4.8%), supported by increased output of paddy (14.4%), fruits (12.4%) and vegetables (9.2%).

and accessories for motor vehicles as well as slower building and repairing of marine vessels during the first quarter of 2011.

8

Weaker crude oil production…

Value-added of the mining sector contracted further by 3.0% (Q4 2010: -1.2%), following lower production of crude oil. Crude oil and condensates production shrank 6.3% (Q4 2010: -3.3%), affected by scheduled maintenance of offshore facilities. However, production of natural gas registered a marginal increase of 0.9% (Q4 2010: 2.0%), following sustained demand of liquefied natural gas (LNG) from regional importers.

7.7% (Q4 2010: 1.0%) due to higher housing starts which increased sharply by 52.2% in the first quarter of 2011. This was due to the strong demand for housing in line with improved household income, easy financing and Government initiatives to encourage home ownership. The non-residential sub-sector grew 5.5% (Q4 2010: 18.8%), supported by the continued expansion in the construction of industrial, shop and office buildings in tandem with robust domestic economic activities. Meanwhile, the civil engineering and special trade sub-sector registered a growth of 2.2% (Q4 2010: 2.4%), partly backed by the commencement of infrastructure projects under the Tenth Malaysia Plan (10MP). In addition, construction of major ongoing civil engineering projects also contributed to the growth of the sub-sector. These include the Electrified Double Track Seremban - Gemas, East - Coast Jabur – Kuala Terengganu (Phase 2) Expressway and Bakun Hydroelectric Power Project.

Strong housing starts…

Construction activities grew 3.8% (Q4 2010: 5.6%), spurred by the robust residential and non-residential sub-sectors. Growth in the residential sub-sector expanded strongly by

Prices

Rising inflationary pressures…

Headline inflation, as measured by the annual change in the CPI, edged up to 2.8% in the first quarter of 2011 (Q4 2010: 2.0%), in line with rising global food commodity and crude oil prices. This was the fifth consecutive quarterly increase and doubled the level

9

recorded in the first quarter of 2010 (1.3%). The increase in CPI was mainly contributed by the food and non-alcoholic beverages, transport as well as housing, water, electricity, gas and other fuels groups, which together contributed 2.3 percentage points.

Prices of food and non-alcoholic beverages rose 4.3% (Q4 2010: 2.9%) and contributed 1.3 percentage points to the CPI increase. Higher price increases were recorded in the food at home (4.8%) and food away from home (3.7%) categories. Significant price increases were also recorded in vegetables (12.4%); sugar, jam, honey, chocolate and confectionery (10.9%); milk and eggs (6.8%); fruits (6.7%); meat (5.4%) as well as fish and seafood (3.4%). This was attributed to stronger demand during the Chinese New Year festivities and school holidays as well as supply constraints, following unfavourable weather conditions.

the decline in prices of clothing and footwear as well as communication at 0.5% and 0.3% (Q4 2010: -0.9%, -0.1%), respectively. This was due to aggressive promotional activities and stiff competition.

Prices in the transport group rose at a faster pace of 4.4% (Q4 2010: 2.5%), contributing 0.7 percentage point to the increase in CPI. The increase reflected the adjustment in pump price of RON97 by 10 sen a litre on 4 January and 1 February 2011, respectively. Meanwhile, prices in the housing, water, electricity, gas and other fuels group rose 1.5% (Q4 2010: 1.4%) and contributed 0.3 percentage point. However, the increase in inflation continued to be partly mitigated by

[Headline inflation in April 2011 rose further by 3.2% (March 2011: 3.0%), mainly due to increases in the prices of food and non-alcoholic beverages by 4.9%. Transport prices also increased by 5.3%, following the adjustment in pump price of RON97 by 20 sen to RM2.70 a litre on 2 April 2011]

The Producer Price Index (PPI), a measure of changes in the prices of commodities charged by domestic producers and those paid by importers, rose sharply by 7.4% in the first quarter of 2011 (Q4 2010: 4.8%). The increase reflected higher prices of locally produced goods and imported components. The PPI for local production increased at a faster pace of 9.9% (Q4 2010: 6.6%) contributed by animal and vegetables oils and fats (45.1%); crude materials, inedible (39.1%) as well as mineral fuels and lubricants (8.5%). In contrast, the PPI for imports increased 1.8% (Q4 2010: 1.1%). This was on account of the slower price increases in the machinery and transport equipment group at 2.1%, following the appreciation of the ringgit against the US dollar.

10

Employment

Labour market cond i t ions remained stable…

Labour market conditions remained stable with the unemployment rate at 3.2% in the fourth quarter of 2010 (Q3 2010: 3.2%). During the quarter, total employment increased slightly to 11.38 million (Q3 2010: 11.23 million), while the total labour force grew to 11.75 million (Q3 2010: 11.61 million).

Monetary and Financial Developments

Monetary aggregates continued to grow…

In the first quarter of 2011, the monetary aggregates continued to expand. M1 or narrow money, which comprises currency in circulation and demand deposits grew 14.0% as at end-March 2011 (end-December 2010: 11.7%) while M3 or broad money increased 8.2% (end-December 2010: 7.0%). The growth in M3 was largely attributed to higher bank lending to the private sector and increased net foreign assets.

Vacancies registered with JobsMalaysia increased sharply to 568,717 in the first quarter of 2011 (Q4 2010: 393,408) in line with the continued expansion in economic activities. The services sector registered the highest vacancies at 233,385, followed by the manufacturing (172,875) and agriculture (95,802) sectors. The number of active jobseekers declined further to 358,270 as at end-March 2011 (end-December 2010: 368,094).

Meanwhile, total retrenchments increased to 2,621 workers (Q4 2010: 1,761). The bulk of retrenchments were from the manufacturing sector at 1,822 workers, accounting for 69.5% of total retrenchments (Q4 2010: 748; 42.4%), followed by the services sector (644 workers) and construction sector (116 workers).

Interest rates remained accommodative…

Amid rising global energy and commodity prices, the overnight policy rate (OPR) was held at 2.75% as at end-March 2011 to remain supportive of growth. However, on 11 March 2011, the statutory reserve requirement (SRR) was raised from 1.00% to 2.00% effective 1 April 2011 as a pre-emptive measure to manage l iquidity ar is ing from large capital inf lows. The average base lending rate (BLR) of commercial banks stood at 6.27% while the average lending rate (ALR) climbed marginally to 5.06% as at end-March 2011 (end-December 2010: 6 .27%; 5 .05%) . Meanwhi le , the sav ings depos i t rate

11

notched up 1 basis point (bp) to 1.01% (end-December 2010: 1.00%) while the 1-month to 12-month fixed deposit rates were in the range of 2.71% and 2.98%, respectively as at end-March 2011 (end-December 2010: 2.71% and 2.97%).

Financing remained robust…

Total gross private sector financing raised through the banking system and capital market expanded 6.4% to RM202.0 billion during the first quarter of 2011 (Q4 2010: 2.1%; RM221.0 billion). The strong growth in capital market financing was contributed by larger issuances of private debt securities (PDS) which recorded a significant growth of 174.8% to RM12.2 bi l l ion (Q4 2010: 5.9%, RM17.4 billion) while equity issuance amounted to only RM1.1 bi l l ion. Loan disbursements by the banking system remained strong at RM188.6 billion (Q4 2010: RM188.9 billion).

[On 5 May 2011, the OPR was raised 25 bps for the first time since July 2010 to 3.00% amid favourable domestic growth prospects while the SRR was increased further to 3.00% from 2.00%, effective 16 May 2011 to manage the risks of large liquidity build-up]

During the first quarter of 2011, bank lending activities remained robust with higher demand, especial ly from households. Total loan applications grew 26.8% (Q4 2010: 22.9%) as demand picked up in March after slowing down in February. Loan approvals and disbursements expanded at a faster pace of 25.0% and 8.2% (Q4 2010: 14.1%; 1.0%), respectively. Loans extended to the business and household sectors increased 10.9% and 13.2%, (end-December 2010: 9.4%; 13.4%), respectively. Meanwhile, total loans outstanding grew 13.2% to RM912.1 billion as at end-March 2011 (end-December 2010: 12.7%; RM883.3 billion).

12

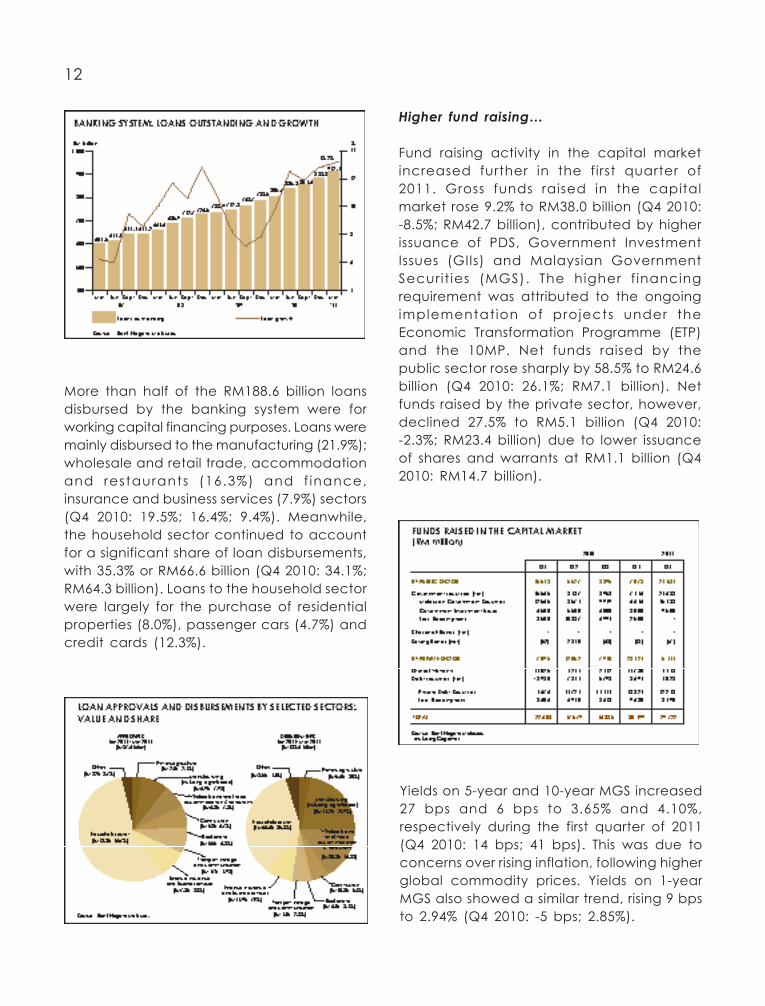

More than half of the RM188.6 billion loans disbursed by the banking system were for working capital financing purposes. Loans were mainly disbursed to the manufacturing (21.9%); wholesale and retail trade, accommodation and restaurants (16.3%) and f inance, insurance and business services (7.9%) sectors (Q4 2010: 19.5%; 16.4%; 9.4%). Meanwhile, the household sector continued to account for a significant share of loan disbursements, with 35.3% or RM66.6 billion (Q4 2010: 34.1%; RM64.3 billion). Loans to the household sector were largely for the purchase of residential properties (8.0%), passenger cars (4.7%) and credit cards (12.3%).

Higher fund raising…

Fund raising activity in the capital market increased further in the first quarter of 2011. Gross funds raised in the capital market rose 9.2% to RM38.0 billion (Q4 2010: -8.5%; RM42.7 billion), contributed by higher issuance of PDS, Government Investment Issues (GIIs) and Malaysian Government Securit ies (MGS). The higher f inancing requirement was attributed to the ongoing implementation of projects under the Economic Transformation Programme (ETP) and the 10MP. Net funds raised by the public sector rose sharply by 58.5% to RM24.6 billion (Q4 2010: 26.1%; RM7.1 billion). Net funds raised by the private sector, however, declined 27.5% to RM5.1 billion (Q4 2010: -2.3%; RM23.4 billion) due to lower issuance of shares and warrants at RM1.1 billion (Q4 2010: RM14.7 billion).

Yields on 5-year and 10-year MGS increased 27 bps and 6 bps to 3.65% and 4.10%, respectively during the first quarter of 2011 (Q4 2010: 14 bps; 41 bps). This was due to concerns over rising inflation, following higher global commodity prices. Yields on 1-year MGS also showed a similar trend, rising 9 bps to 2.94% (Q4 2010: -5 bps; 2.85%).

13

The yield movement of private bonds was more stable with yields on 5-year AAA-rated PDS increasing 4 bps (Q4 2010: 1 bps) and BBB rated bonds edging up 3 bps (Q4 2010: 0.1 bps). Overall PDS yields were in the range of 4.11% and 11.46% during the quarter (Q4 2010: 4.07% and 11.43%).

Banking system remained healthy…

The banking system remained resi l ient with ample liquidity and better quality of lending as well as higher profitability. The risk-weighted capital ratio (RWCR) registered

14.3% and the core capital ratio (CCR) 12.7% as at end-March 2011 (end-December 2010: 14.8%; 13.0%). Total deposits in the banking system rose 9.7% to RM1.17 trillion as at end-March 2011 (end-December 2010: 7.3%; RM1.14 trillion). Pre-tax profits of the banking sector for the first 3 months of 2011 increased to RM6.9 billion (Q4 2010: RM5.7 billion), supported by higher gains on t rading and invesment portfol ios. The quality of lending in the banking system improved with the ratio of net impaired loans to net total loans at 2.2% as at end-March 2011 (end-December 2010: 2.3%).

Upbeat stock market performance...

The FBM KLCI recorded an upward trend following higher capital inflows, better-than-expected corporate earnings, prospects for mergers and acquisitions as well as the strong domestic macroeconomic fundamentals. Market sentiment was also bolstered by the announcement of new investment activities under the ETP estimated at RM2.3 billion. The FBM KLCI reached a new all-time high of 1,574.49 points on 17 January 2011, and gained 17.0% year-on-year (y-o-y) to 1,545.13 points as at end-March 2011 (end-December 2010: 19.3%; 1,518.91 points).

14

Market capitalisation expanded 2.8% or RM35.7 billion to RM1,311 billion as at end-March (end-December 2010: RM1,275.3 billion). Total turnover surged 65.3% y-o-y to 102.1 billion units, valued at RM131.8 billion during the first quarter (Q4 2010: 37.3%; 79.1 billion units; RM124.2 billion).

[The FBM KLCI retreated to 1,541.27 points on 18 May 2011, fo l lowing renewed concerns over global economic prospects, rising inflation, further credit tightening in China and Europe’s debt woes]

Ringgit stronger against the greenback…

During the first quarter of 2011, the ringgit continued to strengthen against the US dollar in line with other regional currencies and recorded several new peaks against the greenback since the 1997/98 financial crisis. The ringgit reached a high of RM3.0259 per US dollar on 31 March 2011. During the quarter, the ringgit gained 1.9% against the US dollar and also appreciated 3.5% against the yen. However, the ringgit eased against the euro and the pound by 4.6% and 1.8%, respectively and traded mixed against most regional currencies.

[During the period end-March to 18 May 2011, the ringgit advanced against the US dollar and breached the RM3.00-per US dollar level. The ringgit touched a new high of RM2.9615 against the greenback on 28 April 2011. However, on 18 May, the ringgit retreated against the US dollar and other currencies in the range of 0.2% to 2.3% on investor concerns over slowing global growth and fluctuating commodity prices]

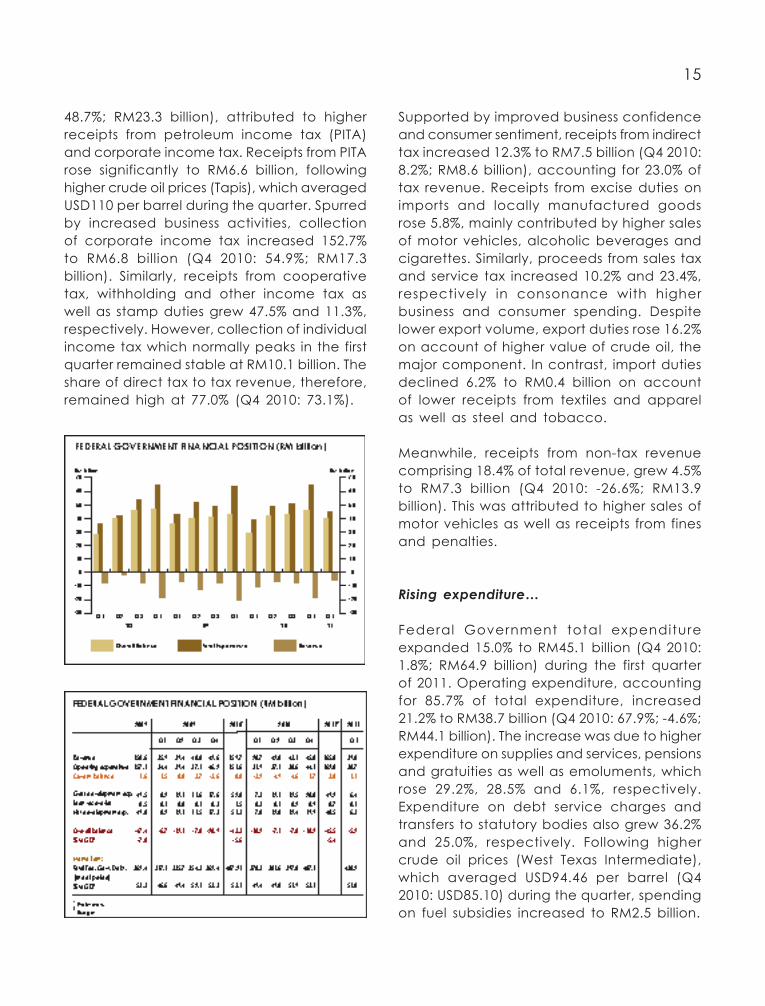

Federal Government Finance

Higher revenue collection…

Federal Government revenue posted a strong growth of 38.4% to RM39.8 billion (Q4 2010: 7.6%; RM45.8 billion) in the first quarter of 2011, following higher collection of tax and non-tax revenue.

Tax revenue, accounting for 81.6% of total revenue, rose 49.3% to RM32.4 billion (Q4 2010: 35.1%; RM31.9 billion) in tandem with robust domestic economic activities. All major components of direct and indirect taxes, with the exception of import duties, registered positive growth. Direct tax grew sharply by 65.7% to RM25.0 billion (Q4 2010:

15

48.7%; RM23.3 billion), attributed to higher receipts from petroleum income tax (PITA) and corporate income tax. Receipts from PITA rose significantly to RM6.6 billion, following higher crude oil prices (Tapis), which averaged USD110 per barrel during the quarter. Spurred by increased business activities, collection of corporate income tax increased 152.7% to RM6.8 billion (Q4 2010: 54.9%; RM17.3 billion). Similarly, receipts from cooperative tax, withholding and other income tax as well as stamp duties grew 47.5% and 11.3%, respectively. However, collection of individual income tax which normally peaks in the first quarter remained stable at RM10.1 billion. The share of direct tax to tax revenue, therefore, remained high at 77.0% (Q4 2010: 73.1%).

Supported by improved business confidence and consumer sentiment, receipts from indirect tax increased 12.3% to RM7.5 billion (Q4 2010: 8.2%; RM8.6 billion), accounting for 23.0% of tax revenue. Receipts from excise duties on imports and locally manufactured goods rose 5.8%, mainly contributed by higher sales of motor vehicles, alcoholic beverages and cigarettes. Similarly, proceeds from sales tax and service tax increased 10.2% and 23.4%, respectively in consonance with higher business and consumer spending. Despite lower export volume, export duties rose 16.2% on account of higher value of crude oil, the major component. In contrast, import duties declined 6.2% to RM0.4 billion on account of lower receipts from textiles and apparel as well as steel and tobacco.

Meanwhile, receipts from non-tax revenue comprising 18.4% of total revenue, grew 4.5% to RM7.3 billion (Q4 2010: -26.6%; RM13.9 billion). This was attributed to higher sales of motor vehicles as well as receipts from fines and penalties.

Rising expenditure…

Federal Government total expenditure expanded 15.0% to RM45.1 billion (Q4 2010: 1.8%; RM64.9 billion) during the first quarter of 2011. Operating expenditure, accounting for 85.7% of total expenditure, increased 21.2% to RM38.7 billion (Q4 2010: 67.9%; -4.6%; RM44.1 billion). The increase was due to higher expenditure on supplies and services, pensions and gratuities as well as emoluments, which rose 29.2%, 28.5% and 6.1%, respectively. Expenditure on debt service charges and transfers to statutory bodies also grew 36.2% and 25.0%, respectively. Following higher crude oil prices (West Texas Intermediate), which averaged USD94.46 per barrel (Q4 2010: USD85.10) during the quarter, spending on fuel subsidies increased to RM2.5 billion.

16

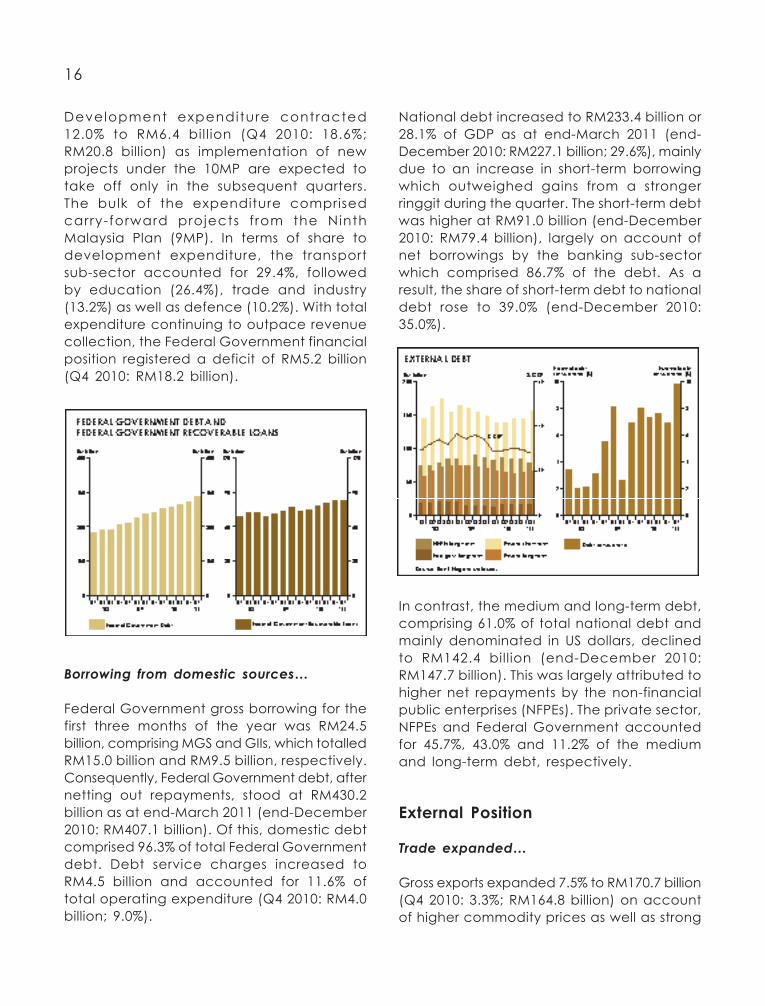

Development expenditure contracted 12.0% to RM6.4 bil l ion (Q4 2010: 18.6%; RM20.8 billion) as implementation of new projects under the 10MP are expected to take off only in the subsequent quarters. The bulk of the expenditure comprised carry-forward projects f rom the Ninth Malaysia Plan (9MP). In terms of share to development expenditure, the transport sub-sector accounted for 29.4%, followed by education (26.4%), trade and industry (13.2%) as well as defence (10.2%). With total expenditure continuing to outpace revenue collection, the Federal Government financial position registered a deficit of RM5.2 billion (Q4 2010: RM18.2 billion).

National debt increased to RM233.4 billion or 28.1% of GDP as at end-March 2011 (end-December 2010: RM227.1 billion; 29.6%), mainly due to an increase in short-term borrowing which outweighed gains from a stronger ringgit during the quarter. The short-term debt was higher at RM91.0 billion (end-December 2010: RM79.4 billion), largely on account of net borrowings by the banking sub-sector which comprised 86.7% of the debt. As a result, the share of short-term debt to national debt rose to 39.0% (end-December 2010: 35.0%).

Borrowing from domestic sources…

Federal Government gross borrowing for the first three months of the year was RM24.5 billion, comprising MGS and GIIs, which totalled RM15.0 billion and RM9.5 billion, respectively. Consequently, Federal Government debt, after netting out repayments, stood at RM430.2 billion as at end-March 2011 (end-December 2010: RM407.1 billion). Of this, domestic debt comprised 96.3% of total Federal Government debt. Debt service charges increased to RM4.5 billion and accounted for 11.6% of total operating expenditure (Q4 2010: RM4.0 billion; 9.0%).

In contrast, the medium and long-term debt, comprising 61.0% of total national debt and mainly denominated in US dollars, declined to RM142.4 billion (end-December 2010: RM147.7 billion). This was largely attributed to higher net repayments by the non-financial public enterprises (NFPEs). The private sector, NFPEs and Federal Government accounted for 45.7%, 43.0% and 11.2% of the medium and long-term debt, respectively.

External Position

Trade expanded…

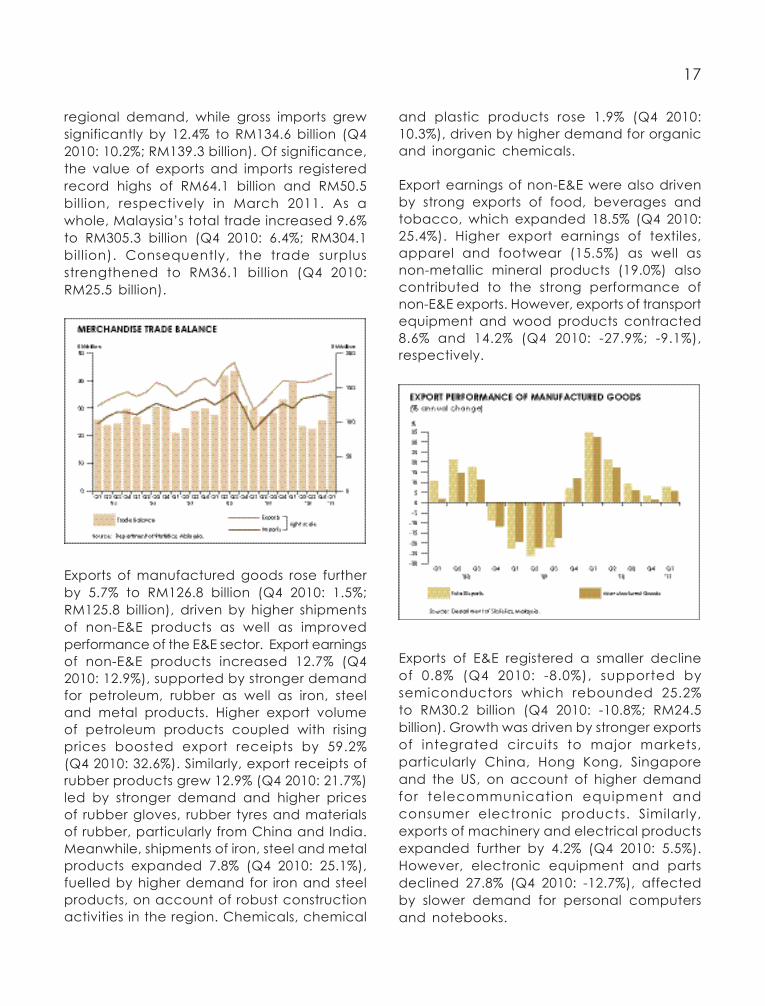

Gross exports expanded 7.5% to RM170.7 billion (Q4 2010: 3.3%; RM164.8 billion) on account of higher commodity prices as well as strong

17

and plastic products rose 1.9% (Q4 2010: 10.3%), driven by higher demand for organic and inorganic chemicals.

Export earnings of non-E&E were also driven by strong exports of food, beverages and tobacco, which expanded 18.5% (Q4 2010: 25.4%). Higher export earnings of textiles, apparel and footwear (15.5%) as well as non-metallic mineral products (19.0%) also contributed to the strong performance of non-E&E exports. However, exports of transport equipment and wood products contracted 8.6% and 14.2% (Q4 2010: -27.9%; -9.1%), respectively.

regional demand, while gross imports grew significantly by 12.4% to RM134.6 billion (Q4 2010: 10.2%; RM139.3 billion). Of significance, the value of exports and imports registered record highs of RM64.1 billion and RM50.5 billion, respectively in March 2011. As a whole, Malaysia’s total trade increased 9.6% to RM305.3 billion (Q4 2010: 6.4%; RM304.1 bill ion). Consequently, the trade surplus strengthened to RM36.1 billion (Q4 2010: RM25.5 billion).

Exports of E&E registered a smaller decline of 0.8% (Q4 2010: -8.0%), supported by semiconductors which rebounded 25.2% to RM30.2 billion (Q4 2010: -10.8%; RM24.5 billion). Growth was driven by stronger exports of integrated circuits to major markets, particularly China, Hong Kong, Singapore and the US, on account of higher demand for telecommunication equipment and consumer electronic products. Similarly, exports of machinery and electrical products expanded further by 4.2% (Q4 2010: 5.5%). However, electronic equipment and parts declined 27.8% (Q4 2010: -12.7%), affected by slower demand for personal computers and notebooks.

Exports of manufactured goods rose further by 5.7% to RM126.8 billion (Q4 2010: 1.5%; RM125.8 billion), driven by higher shipments of non-E&E products as well as improved performance of the E&E sector. Export earnings of non-E&E products increased 12.7% (Q4 2010: 12.9%), supported by stronger demand for petroleum, rubber as well as iron, steel and metal products. Higher export volume of petroleum products coupled with rising prices boosted export receipts by 59.2% (Q4 2010: 32.6%). Similarly, export receipts of rubber products grew 12.9% (Q4 2010: 21.7%) led by stronger demand and higher prices of rubber gloves, rubber tyres and materials of rubber, particularly from China and India. Meanwhile, shipments of iron, steel and metal products expanded 7.8% (Q4 2010: 25.1%), fuelled by higher demand for iron and steel products, on account of robust construction activities in the region. Chemicals, chemical

18

surged 13.2% to RM92.2 billion (Q4 2010: 10.5%; RM94.2 billion), mainly due to strong imports of industrial supplies (20.3%) in tandem with increased activities in the construction and manufacturing sectors. Following improving domestic investment activities, imports of capital goods increased 9.3% to RM17.8 billion (Q4 2010: 10.5%; RM21.6 billion). Meanwhile, imports of consumption goods expanded 5.3% to RM8.8 billion (Q4 2010: 6.9%; RM9.1 billion), spurred by higher household disposable income and a stronger ringgit.

International reserves strengthened…

The international reserves remained strong at RM344.5 billion or USD113.8 billion as at end-March 2011 (end-December 2010: RM328.6 billion; USD106.5 billion). The reserves level remained useable and unencumbered, adequate to finance 8.4 months of retained imports and is 4.3 times the short-term external debt.

[As at 13 May 2011, the international reserves strengthened further to RM401.0 billion (USD132.6 billion). This is sufficient to finance 9.4 months of retained imports and is 4.4 times the short-term external debt]

Agriculture exports increased further by 26.6% to RM19.7 billion (Q4 2010: 36.0%; RM18.5 billion), largely contributed by the higher earnings of palm oil and rubber. Palm oil exports surged 19.9% to RM13.6 billion (Q4 2010: 32.4%; RM13.2 billion) backed by a 39.2% increase in export price to average RM3,556.1 per tonne during the quarter (Q4 2010: RM2,966.0; 30.3%). However, shipments of palm oil declined 13.8% to 3.8 million tonnes (Q4 2010: 1.6%; 4.4 million tonnes) due to slower demand from major importers. Exports of rubber rose 76.0% to RM3.8 billion (Q4 2010: 69.0%; RM2.7 billion) on account of higher shipments and rising prices (RM14.75 per kg).

Export receipts of minerals rebounded 0.1% to RM19.3 billion (Q4 2010: -6.5%; RM16.1 billion), mainly supported by higher exports of natural gas. Export earnings of natural gas increased 6.9% to RM10.7 billion (Q4 2010: 12.3%; RM9.4 billion) following higher shipments as well as better prices. Meanwhile, earnings from crude petroleum declined 11.2% to RM7.9 billion (Q4 2010: -27.9%; RM6.2 billion) due to lower export volume. Shipments of crude oil shrank further, affected by lower demand from China, Thailand and Korea.

Gross imports edged higher to 12.4% (Q4 2010: 10.2%) with expansion across all major categories. Imports of intermediate goods

19

Outlook

Growth momentum to continue…

Prospects for global economic growth remain positive, in view of continued buoyant demand in emerging and developing economies and a pick-up in private sector activities in advanced countries. However, there are downside risks to the growth, especially high unemployment coupled with weak fiscal and financial positions in advanced economies; rising inflationary pressures; and large capital inflows into fast growing emerging economies. The political turmoil in the Middle East and North African region as well as the impact of the earthquake-related disasters in Japan also pose further challenges to global growth.

The Malaysian economy is expected to sustain its growth momentum in the remaining quarters of 2011. This was reflected by the

Leading Index which increased 2.1% in the first quarter of 2011. On the demand side, growth is expected to emanate from domestic consumption and investment activities. On the supply side, growth will be supported by continued expansion in the services and manufacturing sectors.

Key Datahttp://www.treasury.gov.my

23

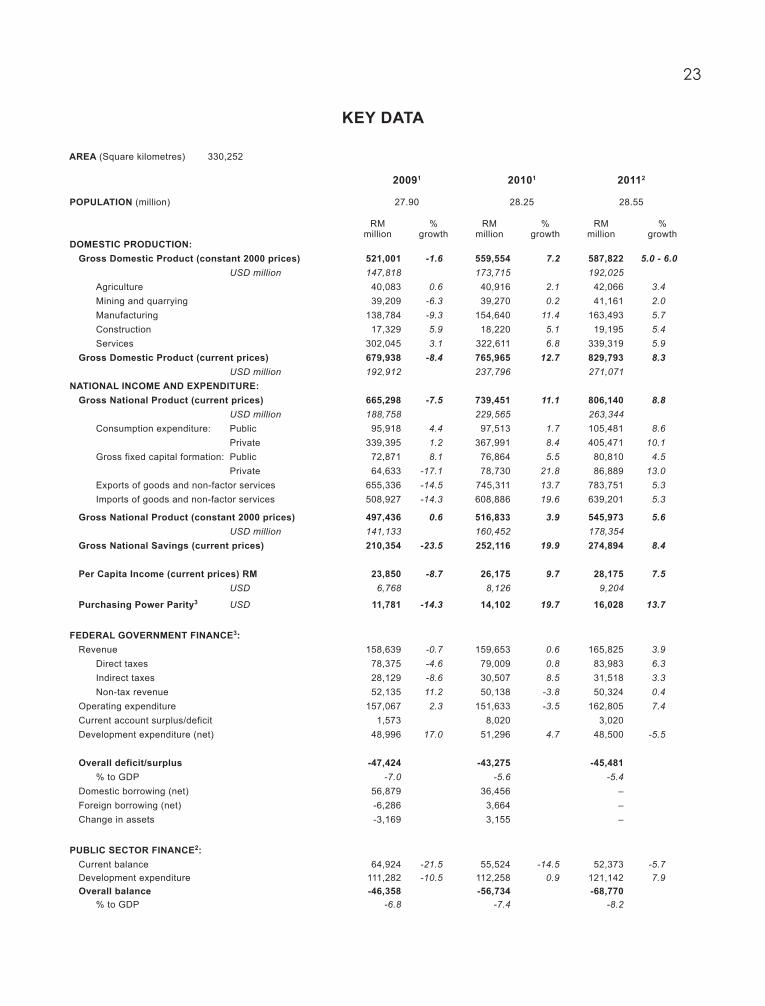

KEY DATA

AREA (Square kilometres) 330,252 20091 20101 20112

POPULATION (million) 27.90 28.25 28.55 RM % RM % RM % million growth million growth million growth DOMESTIC PRODUCTION: Gross Domestic Product (constant 2000 prices) 521,001 -1.6 559,554 7.2 587,822 5.0 - 6.0 USD million 147,818 173,715 192,025 Agriculture 40,083 0.6 40,916 2.1 42,066 3.4 Mining and quarrying 39,209 -6.3 39,270 0.2 41,161 2.0 Manufacturing 138,784 -9.3 154,640 11.4 163,493 5.7 Construction 17,329 5.9 18,220 5.1 19,195 5.4 Services 302,045 3.1 322,611 6.8 339,319 5.9 Gross Domestic Product (current prices) 679,938 -8.4 765,965 12.7 829,793 8.3 USD million 192,912 237,796 271,071 NATIONAL INCOME AND EXPENDITURE: Gross National Product (current prices) 665,298 -7.5 739,451 11.1 806,140 8.8 USD million 188,758 229,565 263,344 Consumption expenditure: Public 95,918 4.4 97,513 1.7 105,481 8.6 Private 339,395 1.2 367,991 8.4 405,471 10.1 Gross fixed capital formation: Public 72,871 8.1 76,864 5.5 80,810 4.5 Private 64,633 -17.1 78,730 21.8 86,889 13.0 Exports of goods and non-factor services 655,336 -14.5 745,311 13.7 783,751 5.3 Imports of goods and non-factor services 508,927 -14.3 608,886 19.6 639,201 5.3

Gross National Product (constant 2000 prices) 497,436 0.6 516,833 3.9 545,973 5.6 USD million 141,133 160,452 178,354 Gross National Savings (current prices) 210,354 -23.5 252,116 19.9 274,894 8.4 Per Capita Income (current prices) RM 23,850 -8.7 26,175 9.7 28,175 7.5 USD 6,768 8,126 9,204

Purchasing Power Parity3 USD 11,781 -14.3 14,102 19.7 16,028 13.7

FEDERAL GOVERNMENT FINANCE3: Revenue 158,639 -0.7 159,653 0.6 165,825 3.9 Direct taxes 78,375 -4.6 79,009 0.8 83,983 6.3 Indirect taxes 28,129 -8.6 30,507 8.5 31,518 3.3 Non-tax revenue 52,135 11.2 50,138 -3.8 50,324 0.4 Operating expenditure 157,067 2.3 151,633 -3.5 162,805 7.4 Current account surplus/deficit 1,573 8,020 3,020 Development expenditure (net) 48,996 17.0 51,296 4.7 48,500 -5.5

Overall deficit/surplus -47,424 -43,275 -45,481 % to GDP -7.0 -5.6 -5.4 Domestic borrowing (net) 56,879 36,456 – Foreign borrowing (net) -6,286 3,664 – Change in assets -3,169 3,155 –

PUBLIC SECTOR FINANCE2: Current balance 64,924 -21.5 55,524 -14.5 52,373 -5.7 Development expenditure 111,282 -10.5 112,258 0.9 121,142 7.9 Overall balance -46,358 -56,734 -68,770 % to GDP -6.8 -7.4 -8.2

24

KEY DATA 20091 20101 20112

RM % RM % RM % million growth million growth million growth National debt2 232,717 -1.5 227,107 -2.4 _ _ USD million 67,324 72,828 _ Medium and long-term debt 155,328 -0.8 147,660 -4.9 _ _ Federal Government 13,787 -32.1 16,745 21.5 _ _ NFPEs 71,600 13.4 66,589 -7.0 _ _ Private sector 69,941 -4.4 64,325 -8.0 _ _ Short-term debt 77,390 -2.9 79,447 2.7 _ _

Debt to GDP (%) 34.2 29.6 _

Debt service ratio (%) 6.9 6.9 _

RM million RM million RM million BALANCE OF PAYMENTS: Current Account 112,139 90,511 100,697 USD million 31,815 27,634 30,743 Goods 141,745 136,575 144,321 Services 4,664 863 230 Income -14,639 -25,249 -23,653 Transfers -19,631 -21,677 -20,200 Financial account -80,208 -21,918 _ Overall balance 13,831 -2,721 _

RM % % RM % % RM % % million growth share million growth share million growth share EXTERNAL TRADE: Total Exports (f.o.b.) 552,518 -16.7 639,428 15.7 170,6674 7.5 USD million 156,760 198,512 55,752 Manufactured goods 432,244 -12.6 78.1 487,974 12.9 76.3 126,796 5.7 74.3 Palm oil (crude and processed) 36,795 -21.8 6.7 45,998 25.0 7.2 13,621 19.9 8.0 Crude petroleum 25,360 -41.8 4.6 30,765 21.3 4.8 7,872 -11.2 4.6 Liquefied natural gas 31,195 -24.8 5.6 38,099 22.1 6.0 10,723 6.9 6.3

Total Imports (c.i.f.) 434,670 -16.4 529,195 21.7 134,5934 12.4 USD million 123,325 164,290 43,968 Intermediate goods 297,465 -21.5 68.4 363,153 22.1 68.6 92,247 13.2 68.5 Capital goods 65,195 -5.0 15.0 76,435 17.2 17.2 17,807 9.3 13.2 Consumption goods 31,492 -2.2 7.2 34,591 9.8 9.8 8,779 5.3 6.5

Balance of Trade 117,848 110,234 36,074

Gross international reserves 331,301 328,577 401,0415

USD million 96,695 106,498 132,622 Months of retained imports 9.8 8.5 9.45

Multiples of short term debt 4.1 4.1 4.45

Trading Partners: (% to total trade) ASEAN 25.5 26.2 26.34

European Union 11.2 10.5 10.14

USA 11.1 10.0 9.34

Japan 11.0 11.4 11.44

China 24.5 12.6 12.44

Others 16.7 29.3 30.54

Index % growth Index % growth Index % growth Consumer Price Index (2010=100) 98.3 0.6 100.0 1.7 102.24 2.8 Producer Price Index (2005=100) 111.1 -7.3 117.3 5.6 125.04 7.4 Thousands % growth Thousands % growth Thousands % growth LABOUR: Labour force8 12,061.1 0.8 12,216.8 1.3 12,506.3 2.4 Unemployment8 (% of labour force) 440.6 3.7 443.5 3.6 437.8 3.5

25

KEY DATA 2009 2010 2011 End-March End-March End-March RM % RM % RM % million growth million growth million growth MONEY AND BANKING: Money Supply (M1) 179,679.4 3.5 201,162.3 12.0 229,361.3 14.0 (M2) 921,831.5 9.3 1,002,708.2 8.8 1,088,616.4 8.6 (M3) 949,445.1 7.4 1,031,851.4 8.7 1,116,288.5 8.2

Banking system: Deposits 985,855.3 8.0 1,068,733.8 8.4 1,172,874.9 9.7 Loans 733,873.5 10.9 805,690.4 9.8 912,096.1 13.2

End-March (%) End-March (%) End-March(%) Loan-deposit ratio9 (end of period) 73.7 79.1 82.0

End-March (%) End-March (%) End-March (%) Interest rates (average rates at end of period): 3-month interbank 2.08 2.50 3.00 Commercial banks: Fixed deposits: 3-month 2.04 2.28 2.74 12-month 2.52 2.67 2.98 Savings deposit 0.95 0.86 1.01 Base lending rate (BLR) 5.53 5.76 6.27 Treasury bill (3-month) 1.94 2.14 2.83 Malaysian Government securities (1-year) 1.99 2.58 2.94 Malaysian Government securities (5-year) 3.49 3.75 3.65

End-April End-April End-AprilMovement of Ringgit (end-period)10: RM per SDR; % change 5.3354 -3.8 4.8122 10.9 4.8159 -0.1 RM per USD; % change 3.5610 -11.3 3.1905 11.6 2.9735 7.3 RM per Euro; % change 4.7404 3.8 4.2284 12.1 4.4100 -4.1 RM per 100 Yen; % change 3.6570 -17.0 3.3951 7.7 3.6462 -6.9

End-April End-April End-AprilBursa Malaysia (end-period): KLCI / FBM KLCI 990.74 1,346.38 1,534.95 Market capitalisation (RM billion) 754.20 1,079.66 1,310.79

SOCIAL INDICATORS: Life expectancy at birth1 : Male (years) 71.7 71.7 n.a. Female (years) 76.5 76.6 n.a. Infant mortality1 (per ‘000 live births) 6.5 6.3 n.a. Literacy rate1 92.7 n.a. n.a. Water coverage:total hour/units with piped water8 (%) 96.6 n.a. n.a. Electricity coverage:rural housing units8 (% of population) 92.2 n.a. n.a. Fixed line telephone subscribers11 (per 100 households) 44.0 42.3 42.66

Cellular phone subscribers11 (per 100 population) 105.4 119.2 121.06

Broadband subscribers11 (per 100 households) 31.7 55.6 57.66

Tourist arrivals (million) 23.6 24.6 1.97

1 Department of Statistics, Malaysia. 2 BNM Annual Report 2010. 3 Economic Report 2010/2011. 4 For the period of January- March 2011. 5 As at 13 May 2011. 6 As at End-March 2011. 7 For the period of January 2011. 8 Economic Planning Unit. 9 Excludes transactions by financial institutions. 10 Annual rate of appreciation (+) or depreciation (-).

11 Malaysian Communications and Multimedia Commission.

Key Economic Indicators

29In

dica

tor /

Mon

th20

1020

11

Jan

Feb

Mar

Apr

May

June

Jul

Aug

Sept

Oct

Nov

Dec

Jan

Feb

Mar

Sale

s of

new

pas

seng

er c

ars

(uni

ts)

45,9

7336

,551

50,5

3343

,661

46,2

5948

,926

48,1

4449

,642

38,7

6146

,439

39,3

7549

,330

49,5

8936

,457

56,4

83

Prod

uctio

n of

veh

icle

s (u

nits

)39

,996

38,2

4254

,949

55,3

8347

,199

49,3

4155

,875

48,2

1438

,086

38,7

6641

,065

40,1

4947

,547

42,6

2943

,300

Sale

s of

mot

orcy

cles

(uni

ts)

38,8

6031

,619

41,1

6541

,250

35,5

2735

,324

42,7

5344

,544

34,5

6945

,068

32,0

7745

,419

39,2

4935

,329

48,2

28

Prod

uctio

n of

mot

orcy

cles

(u

nits

) 36

,096

28,8

4142

,490

40,4

9839

,547

36,8

5044

,341

42,9

7334

,931

45,5

4137

,005

38,8

2840

,494

33,7

7448

,563

Impo

rts o

f con

sum

ptio

n go

ods

(RM

mill

ion)

2,83

42,

409

3,09

42,

831

2,74

93,

042

3,10

32,

807

2,63

62,

813

2,95

13,

322

3,06

12,

379

3,33

9

Burs

a M

alay

sia

(end

-per

iod)

FBM

KLC

I1,

259.

161,

270.

781,

320.

571,

346.

381,

285.

011,

314.

021,

360.

921,

422.

491,

463.

501,

505.

661,

485.

231,

518.

911,

519.

941,

491.

251,

545.

13

Mar

ket c

apita

lisat

ion

(R

M b

illion

)1,

001.

731,

015.

711,

061.

061,

079.

661,

027.

921,

044.

351,

092.

291,

122.

111,

150.

121,

204.

341,

237.

371,

275.

281,

283.

981,

256.

711,

310.

99

Pric

es -

Annu

al c

hang

e (%

)

Cons

umer

Pric

e In

dex

1.4

1.2

1.4

1.6

1.6

1.6

1.8

2.0

1.8

1.9

1.9

2.1

2.4

2.9

3.0

Prod

ucer

Pric

e In

dex

- D

omes

tic4.

25.

99.

07.

45.

95.

25.

64.

84.

94.

44.

65.

56.

97.

27.

9

Labo

ur M

arke

t

R

etre

nchm

ent (

no.)

952

204

558

1,12

029

244

746

029

899

377

543

255

41,

090

227

1,30

4

V

acan

cies

(no.

)13

9,19

611

5,37

219

5,47

418

0,35

118

3,46

717

8,17

517

1,31

215

8,79

671

,670

146,

093

112,

251

135,

064

163,

350

134,

280

270,

907

I. C

ON

SUM

PTIO

N IN

DIC

ATO

RS

30In

dica

tor /

Mon

th20

1020

11

Jan

Feb

Mar

Apr

May

June

Jul

Aug

Sept

Oct

Nov

Dec

Jan

Feb

Mar

Sale

s of

new

com

mer

cial

veh

icle

s (u

nits

) 4

,649

4

,103

5

,606

5

,151

4,

624

5,0

79

5,33

95,

566

4,68

25,

858

5,47

05,

435

5,10

73,

930

6,78

2

Impo

rts (R

M m

illio

n)Ca

pita

l goo

ds 5

,319

5

,049

5

,919

6

,138

6

,374

6

,417

7,

128

6,08

36,

362

7,04

87,

235

7,36

45,

602

5,15

97,

046

Inte

rmed

iate

goo

ds 2

7,26

0 2

3,52

1 3

0,74

4 2

9,27

7 3

0,73

4 3

2,62

832

,977

31,2

6130

,555

33,4

9428

,934

31,7

6930

,897

27,1

3634

,213

Man

ufac

turin

g pr

ojec

tsM

ITI A

ppro

vals

(RM

milli

on)

2,16

01,

906

1,5

54

1,18

44,

134

4,17

54,

270

2,64

01,

876

5,04

83,

896

14,3

354,

772

2,04

05,

357

Ne

w in

vest

men

t 3

67

1,2

99

552

53

13,

575

3,13

62,

044

867

496

4,15

71,

975

4,89

61,

353

1,59

63,

482

Re

-inve

stm

ent

1,7

93

607

1

,003

65

355

81,

039

2,22

61,

773

1,38

189

11,

921

9,43

93,

419

444

1,87

5

Base

lend

ing

rate

(%)1

5.5

1 5

.51

5.7

6 5

.76

6.0

2 6

.02

6.27

6.27

6.27

6.27

6.27

6.27

6.27

6.27

6.27

Mon

ey s

uppl

y (A

nnua

l % c

hang

e)M

1 1

0.8

15.

3 1

2.0

8.9

1

2.1

12.

6 10

.713

.911

.611

.69.

911

.717

.913

.214

.0M

3 7

.9

8.2

8

.7

8.1

9

.3

8.8

8.

18.

28.

58.

48.

27.

08.

87.

98.

2

Risk

-Wei

ghte

d Ca

pita

l Rat

io (R

WCR

), %

15.

1 1

5.1

15.

0 1

5.1

15.

1 1

5.4

15.3

15.1

14.8

14.5

14.4

14.8

14.3

14.4

14.3

Ratio

of n

et im

paire

d lo

ans

to n

et to

tal

loan

s (%

)2 2

.0

2.0

1

.9

2.2

2

.2

2.1

2.

42.

32.

42.

32.

32.

32.

32.

32.

2

Bank

ing

Syst

em :

Loan

s Ap

prov

ed b

y Pu

rpos

e an

d Se

ctor

s (R

M m

illio

n) 2

3,36

4 1

9,81

5 2

6,92

7 2

9,03

1 2

7,99

8 3

3,33

930

,701

31,4

4829

,021

30,3

7730

,183

31,1

9627

,472

21,2

1438

,962

Prim

ary

agric

ultu

re 2

36

479

8

00

446

4

93

640

92

090

445

655

369

458

360

069

377

1M

inin

g an

d qu

arry

ing

71

791

1

74

71

162

5

01

258

109

563

9817

672

5715

550

3M

anuf

actu

ring

(inclu

ding

agr

o-ba

sed)

1,1

67

836

1

,549

1

,678

1

,627

2

,959

2,09

12,

841

1,86

91,

494

1,91

82,

005

1,88

81,

836

3,18

4Se

rvice

s 4

,061

4,4

54

5,1

01

7,1

37

6,5

14

8,3

126,

528

7,74

95,

910

7,18

65,

626

8,54

54,

638

3,28

38,

843

Cons

truct

ion

1,6

02

1,1

20

1,7

94

1,6

43

1,4

92

2,2

88

2,39

12,

165

3,09

42,

287

3,35

62,

293

1,86

71,

421

2,55

2Re

al E

stat

e 1

,196

6

22

1,4

26

1,7

09

1,5

87

1,9

061,

800

1,49

81,

645

1,62

01,

866

1,63

31,

472

794

3,27

1Ho

useh

old

sect

or3

14,

406

11,

165

15,

265

16,

054

15,

388

16,

033

16,2

3016

,013

15,2

2316

,540

16,5

1315

,260

16,6

0012

,654

19,5

23O

ther

sec

tor n

.e.c

. 6

24

347

8

20

293

7

36

699

483

168

261

599

193

205

352

379

315

Loan

s Di

sbur

sed

by P

urpo

se a

nd S

ecto

rs

(RM

mill

ion)

56,

681

55,

873

61,

785

60,

964

59,

149

65,

140

59,5

5356

,654

59,8

9761

,100

64,3

8563

,405

65,9

7350

,154

72,5

05

Prim

ary

agric

ultu

re 2

,809

3

,241

3

,143

1

,565

1

,929

1

,889

1,43

81,

594

1,74

91,

740

1,72

21,

809

1,57

01,

535

2,48

4

Min

ing

and

quar

ryin

g 1

91

223

3

44

246

1

52 2

25

165

257

437

528

387

329

319

382

396

Man

ufac

turin

g (in

cludi

ng a

gro-

base

d) 1

1,10

3 1

0,14

0 1

2,14

8 1

2,83

8 1

1,22

9 1

3,55

2 12

,464

11,5

7812

,103

11,9

6912

,205

12,6

6114

,418

10,8

2016

,013

Serv

ices

16,

988

18,

154

16,

549

21,

436

19,

131

21,

844

18,4

5316

,121

18,0

4720

,206

20,9

6017

,339

18,0

4814

,140

21,4

82

Cons

truct

ion

3,0

19

2,9

23

3,2

20

3,3

79 3

,316

3

,760

3,35

53,

840

4,11

93,

515

4,00

24,

368

4,18

72,

445

3,63

5

Real

Est

ate

1,6

23

1,8

09

1,7

54

1,1

10

1,4

15

1,5

96

2,14

92,

342

2,36

21,

691

2,29

43,

540

2,36

71,

354

2,64

9

Hous

ehol

d se

ctor

3 1

9,45

6 1

7,30

4 2

0,42

4 1

9,37

8 1

9,94

5 2

0,98

0 20

,385

20,0

3619

,144

20,5

7221

,713

22,0

4123

,839

18,4

5624

,275

Oth

er s

ecto

r n.e

.c.

1,4

93

2,0

79

4,2

03

1,0

13

2,0

33

1,2

94

1,14

588

41,

936

878

1,10

31,

319

1,22

41,

024

1,57

1

Regi

stra

tion

of n

ew lo

cal c

ompa

nies

(no.

)3,

834

2,64

75,

611

3,68

93,

333

3,55

53,

520

3,42

83,

072

3,78

23,

505

4,17

23,

452

2,62

84,

481

Liqu

idat

ion

of c

ompa

nies

(no.

)1,

489

850

1,84

73,

076

2,08

22,

272

3,76

32,

619

1,17

11,

298

1,41

91,

811

1,03

71,

603

1,43

4

Prop

erty

Ove

rhan

g (e

nd p

erio

d)4

Tota

l (un

its)

28,6

8728

,043

29,5

7530

,859

31,2

66

% C

hang

e (p

rece

edin

g)-0

.23.

412

.28.

39.

0To

tal (

RM m

illion

)5,

649

5,50

46,

071

6,79

47,

145

%

Cha

nge

(pre

ceed

ing)

2.4

4.4

14.1

16.5

26.5

II. IN

VEST

MEN

T IN

DIC

ATO

RS

Not

e:

1 Com

mer

cial

ban

k ra

te.

2 B

egin

ning

fina

ncia

l yea

r 201

0, b

anki

ng in

stitu

tions

are

requ

ired

to re

port

impa

ired

loan

s in

acc

orda

nce

with

the

Gui

delin

e on

the

Cla

ssifi

catio

n an

d Im

pairm

ent P

rovi

sion

s fo

r Loa

ns/F

inan

cing

. Th

e re

porti

ng o

f non

-per

form

ing

loan

s ha

s si

nce

been

dis

cont

inue

d.

3 Hou

seho

ld s

ecto

r = to

tal l

oans

by

purp

ose

to h

ouse

hold

s.

4 Qua

rterly

dat

a.

n.

e.c

- not

els

ewhe

re c

lass

ified

.

3131In

dica

tor /

Mon

th20

1020

11Ja

nFe

bM

arAp

rM

ayJu

neJu

lAu

gSe

ptO

ctNo

vDe

cJa

nFe

bM

ar

Agric

ultu

re S

ecto

rPa

lm O

il ('0

00 to

nnes

)1,

321

1,15

71,

387

1,30

61,

385

1,42

01,

519

1,60

71,

563

1,63

71,

459

1,23

31,

058

1,09

41,

416

Price

(RM

/ to

nne)

2,51

52,

549

2,62

42,

538

2,52

92,

453

2,54

22,

718

2,71

92,

853

3,25

13,

620

3,76

93,

811

3,49

8Ru

bber

('00

0 to

nnes

)10

981

7055

6571

81

8175

9473

8510

992

65Pr

ice (s

en /

kg)

994

1,01

01,

038

1,04

692

093

3 91

595

51,

034

1,15

61,

284

1,41

61,

580

1,67

31,

429

Coco

a, e

xpor

t uni

t val

ue (R

M /

tonn

e)12

,832

12,4

9511

,979

10,9

8111

,243

10,4

8911

,324

12,4

8011

,435

9,25

210

,154

11,9

7710

,926

10,2

3211

,002

Fish

land

ing

('000

tonn

es)

104

101

120

128

124

126

129

128

129

135

110

105

103

107

121

Live

stoc

k1 :

Chi

cken

s ('0

00)

10,3

179,

542

10,7

6610

,194

9,87

6 9,

968

10,8

069,

800

10,0

5310

,344

10,4

5313

,915

9,99

68,

598

10,0

91

Cat

tle

1,48

81,

730

2,08

52,

058

2,15

82,

412

2,37

63,

164

3,32

21,

841

2,00

72,

090

1,65

51,

670

1,71

8

Goa

ts43

862

061

177

090

583

694

291

91,

282

708

1,66

11,

461

555

492

571

Cons

truct

ion

Sect

orNo

. of h

ouse

s ap

prov

ed6,

924

5,75

712

,349

9,18

311

,766

9,00

58,

258

10,9

1210

,037

9,86

513

,679

12,9

3512

,455

8,76

611

,781

New

adve

rtisin

g &

sale

s pe

rmits

(no.

)76

6194

9989

8997

8385

9610

495

107

7510

7

Tran

spor

t Sec

tor

High

way

(milli

on /

vehi

cles)

11

310

311

711

511

711

812

411

912

112

512

011

912

410

612

7Ra

il (RM

milli

on)

K

TMB

Com

mut

er re

venu

e7.

06.

06.

86.

76.

76.

66.

86.

96.

97.

26.

88.

37.

46.

26.

8

KTM

B Ca

rgo

reve

nue

9.8

9.0

10.1

9.2

9.3

9.8

10.2

9.7

9.0

10.1

9.4

10.4

9.9

9.2

11.0

K

LIA

Expr

ess

and

Tran

sit re

venu

e5.

95.

66.

66.

56.

26.

36.

66.

56.

06.

96.

26.

36.

25.

87.

0Ai

r (M

AS):

N

o.of

pas

seng

ers

('000

)1,

006

1,00

71,

102

1,05

51,

051

1,13

31,

169

1,04

81,

097

1,08

81,

103

1,25

21,

067

991

1,12

8

D

omes

tic34

438

842

639

338

243

642

434

339

136

439

246

033

331

838

5

In

tern

atio

nal

662

619

676

662

669

697

745

705

706

724

712

792

734

673

743

Carg

o (m

illion

kg)

35.0

33.8

43.0

39.5

42.5

39.6

40.6

40.0

35.6

43.1

39.5

39.8

34.6

28.7

38.8

Air (

Air A

sia):

No. o

f pas

seng

ers

('000

)1,

248

1,15

51,

282

1,21

71,

310

1,36

6 1,

375

1,25

41,

407

1,42

31,

396

1,62

21,

440

1,36

01,

519

Carg

o ('0

00 k

g)3.

73.

75.

04.

7 4.

8 4.

7 5.

65.

65.

16.

33.

96.

16.

75.

17.

3Po

rt - C

onta

iner

TEU

s (‘0

00)2

1,42

21,

274

1,45

51,

504

1,54

71,

515

1,60

81,

567

1,45

31,

555

1,51

81,

537

1,59

51,

401

1,68

2

Tour

ism

Sec

tor

Tour

ist a

rriva

ls ('0

00)

1,89

71,

832

2,02

31,

878

1,99

2 2

,246

2,

214

2,09

92,

053

2,13

82,

081

2,12

31,

919

--

Com

mun

icat

ion

Sect

or (s

ubsc

iber

s ‘0

00)3

Fixe

d Li

ne

4,32

84,

395

4,39

14,

406

4,42

6Ce

llula

r 30

,794

31,4

5632

,413

33,1

0634

,456

3G7,

459

7,86

08,

381

8,60

29,

668

Broa

dban

d (in

clude

s wi

rele

ss L

AN)

2,92

23,

232

4,28

54,

722

4,91

3

Indu

stria

l Pro

duct

ion

Inde

x- A

nnua

l cha

nge

(%)

13.2

4.4

13.7

11.4

12.4

9.1

3.4

3.9

5.7

3.0

4.8

4.5

0.5

5.2

2.4

Min

ing

Sect

orPr

oduc

tion

Inde

x - A

nnua

l cha

nge

(%)

2.5

-2

.8-1

.9-0

.30.

10.

7-5

.8-2

.61.

8-1

.3-0

.4-3

.4-6

.7-0

.7-4

.0Cr

ude

Oil &

Con

dens

ates

('00

0 ba

rrels)

20,9

7818

,332

20,0

9119

,062

20,1

6218

,729

18,5

4118

,901

19,5

6319

,493

18,8

5519

,394

19,2

5117

,472

18,8

72Cr

ude

Oil &

Con

dens

ates

('00

0 bp

d)4

677

655

648

636

651

624

598

610

653

629

628

627

621

624

612

T

apis

Blen

d (U

SD/b

arre

l)80

.777

.682

.886

.979

.178

.179

.981

.382

.389

.991

.695

.210

1.2

107.

711

8.7

D

ated

Bre

nt (U

SD/b

arre

l)76

.474

.379

.385

.076

.374

.874

.776

.777

.882

.985

.791

.896

.310

4.0

114.

4

III. P

RO

DU

CTI

ON

IND

ICAT

OR

S

Natu

ral G

as (m

msc

fd)5

6,63

75,

962

6,31

26,

297

5,80

15,

831

6,14

75,

390

6,27

16,

020

6,09

46,

014

6,40

66,

457

6,27

0Ti

n (to

nnes

)19

318

819

320

922

320

823

324

124

022

324

224

9-

--

Elec

trici

ty S

ecto

rPr

oduc

tion

Inde

x - A

nnua

l cha

nge

(%)

19.8

11.4

24.9

12.2

11.5

5.2

4.4

4.9

3.1

5.2

4.9

2.4

0.3

0.7

-0.7

Max

imum

dem

and

(MW

)14

,165

14,4

4614

,890

14,9

8315

,072

14,5

9714

,361

14,7

5814

,339

14,9

1614

,380

14,2

5114

,342

14,6

4014

,989

Sale

s (G

W h

our)

7,43

17,

331

6,96

67,

929

7,79

67,

902

7,55

87,

764

7,77

97,

136

7,91

17,

267

7,57

17,

473

6,95

0

Man

ufac

turin

g Se

ctor

Prod

uctio

n In

dex

- Ann

ual c

hang

e (%

)18

.27.

120

.516

.818

.413

.17.

46.

67.

64.

77.

08.

23.

88.

25.

3Sa

les

- Ann

ual c

hang

e (%

)29

.317

.026

.620

.120

.314

.38.

88.

96.

93.

28.

711

.97.

610

.014

.1

Note

:

1 Tot

al s

laug

hter

ed.

2 C

over

s on

ly Kl

ang,

Pen

ang,

Joh

or, K

uant

an, T

anju

ng P

elep

as, B

intu

lu a

nd K

uchi

ng (

TEUs

: Twe

nty-

foot

equ

ivale

nt u

nits

).

3 End

of p

erio

d.

4 Bar

rels

per d

ay.

5 M

illion

sta

ndar

d cu

bic

foot

per

day

.

32

Indi

cato

r / M

onth

2010

2011

Jan

Feb

Mar

Apr

May

June

Jul

Aug

Sept

Oct

Nov

Dec

Jan

Feb

Mar

RM

(mill

ion)

Gro

ss e

xpor

ts52

,447

46,8

4059

,443

52,0

2752

,297

52,8

2955

,426

52,8

5250

,474

54,9

7852

,699

57,1

6554

,039

52,6

4664

,058

Gro

ss im

ports

39,5

1635

,169

45,0

9342

,804

44,1

5346

,786

48,4

1444

,532

43,4

6748

,126

43,7

0147

,478

44,8

4739

,212

50,5

35

Trad

e ba

lanc

e 1

2,93

1 1

1,67

1 1

4,35

0 9

,223

8

,144

6

,043

7,01

28,

320

7,00

76,

852

8,99

89,

687

9,19

213

,434

13,5

23

Tota

l tra

de

91,

963

82,

009

104,

536

94,

831

96,

450

99,

616

103,

840

97,3

8493

,942

103,

104

96,4

0010

4,64

398

,886

91,8

5811

4,59

2

USD

(mill

ion)

Gro

ss e

xpor

ts15

,539

13,7

1317

,875