Embed Size (px)

DESCRIPTION

Making the Most of the Economic Stimulus Act. A Webinar Presented by NPES and PIA/GATF. Welcome and Introduction. Today’s Presenters Lisbeth Lyons, VP of Govt. Affairs PIA/GATF Mark Nuzzaco, NPES Dir. of Govt. Affairs Dennis Tingey, Tax Specialist, US Dep. Of Treasury - PowerPoint PPT Presentation

Citation preview

Making the Most of the Economic Stimulus Act

A Webinar Presented by

NPES and PIA/GATF

Welcome and Introduction

Today’s PresentersLisbeth Lyons, VP of Govt. Affairs PIA/GATFMark Nuzzaco, NPES Dir. of Govt. AffairsDennis Tingey, Tax Specialist, US Dep. Of TreasuryKathleen Reed, Chief, Branch 7, Office of Associate

Chief Counsel (Income Tax and Accounting) IRSStuart Margolis, CPA, Principal, MargolisBecker

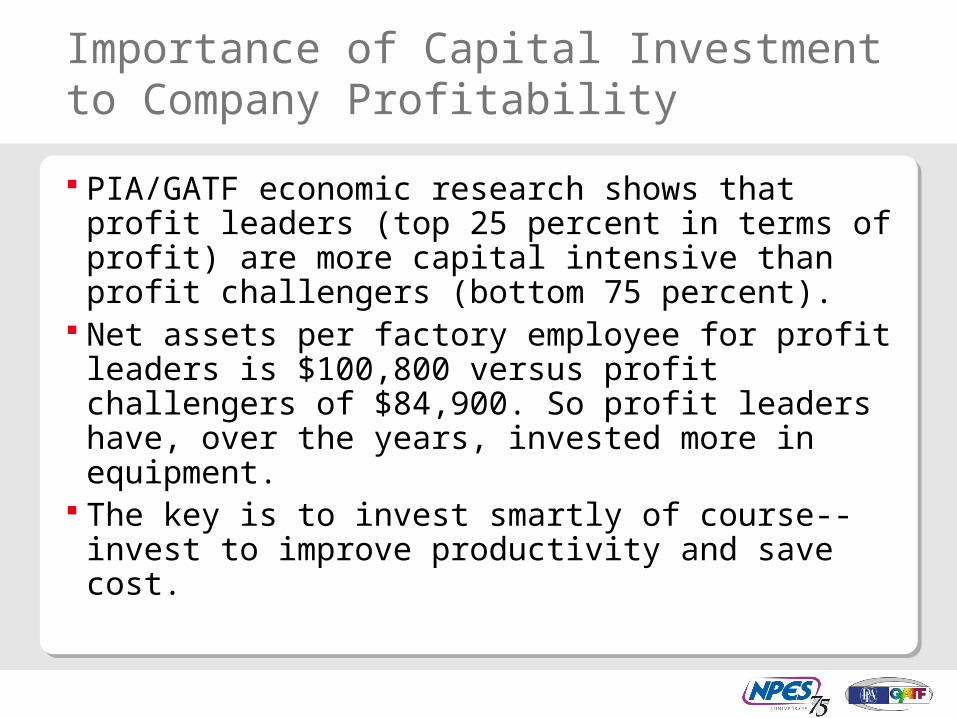

Importance of Capital Investment to Company Profitability

PIA/GATF economic research shows that profit leaders (top 25 percent in terms of profit) are more capital intensive than profit challengers (bottom 75 percent).

Net assets per factory employee for profit leaders is $100,800 versus profit challengers of $84,900. So profit leaders have, over the years, invested more in equipment.

The key is to invest smartly of course--invest to improve productivity and save cost.

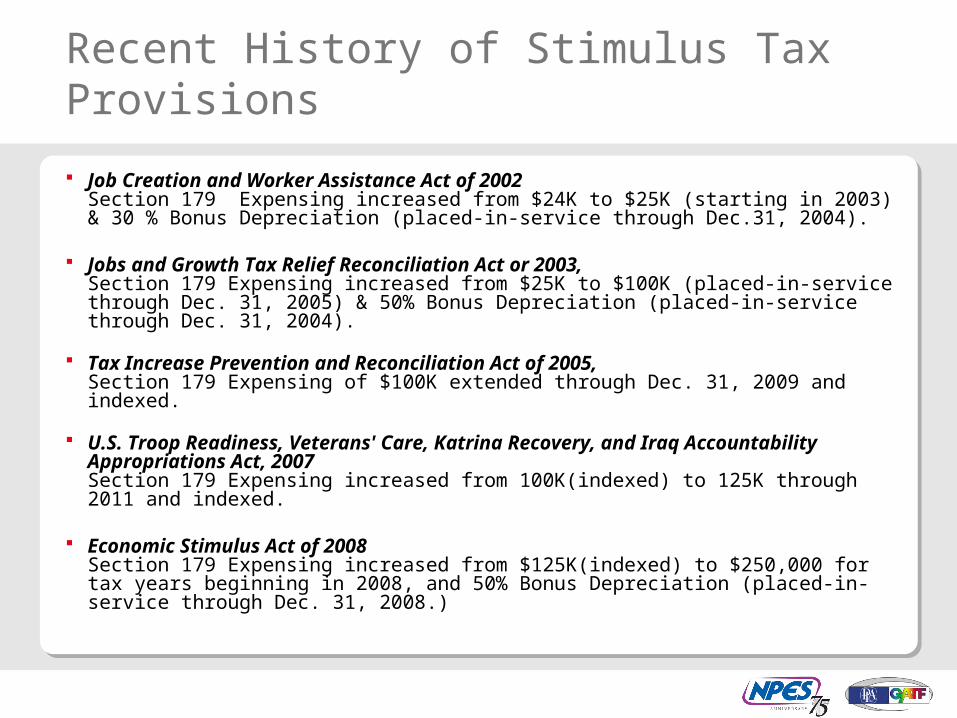

Recent History of Stimulus Tax Provisions

Job Creation and Worker Assistance Act of 2002Section 179 Expensing increased from $24K to $25K (starting in 2003)& 30 % Bonus Depreciation (placed-in-service through Dec.31, 2004).

Jobs and Growth Tax Relief Reconciliation Act or 2003, Section 179 Expensing increased from $25K to $100K (placed-in-service through Dec. 31, 2005) & 50% Bonus Depreciation (placed-in-service through Dec. 31, 2004).

Tax Increase Prevention and Reconciliation Act of 2005, Section 179 Expensing of $100K extended through Dec. 31, 2009 and indexed.

U.S. Troop Readiness, Veterans' Care, Katrina Recovery, and Iraq Accountability Appropriations Act, 2007Section 179 Expensing increased from 100K(indexed) to 125K through 2011 and indexed.

Economic Stimulus Act of 2008Section 179 Expensing increased from $125K(indexed) to $250,000 for tax years beginning in 2008, and 50% Bonus Depreciation (placed-in-service through Dec. 31, 2008.)

Enhanced Section 179 Expensing

Eligible Property Tax Years Beginning in 2008 Limits to Deduction

The Annual Dollar Limit The Annual Investment LimitThe Annual Taxable Income LimitLess Obvious Advantages of Section 179 Deduction

Enhanced Section 179 Expensing

Eligible PropertyProperty that may be deducted in the year of purchase, rather than

depreciated over the asset’s useful life, includes: Machinery and equipment, including printing, publishing and

converting technology Furniture and fixtures Most storage facilities Single-purpose agricultural or horticultural structures Of-the-shelf computer software Property only has to be “new to the purchaser”

Enhanced Section 179 Expensing

Tax Years Beginning in 2008Property may be placed-in-service after December 31, 2008 if the

taxpayer is using a fiscal “tax year” that extends into 2009 provided that it begins in 2008.

Enhanced Section 179 Expensing

Limits to DeductionThe Annual Dollar Limit refers to the amount a taxpayer can claim

under Section 179 each year. This amount has been indexed for inflation as follows:

2002 $24,000 2003 $100,000 2004 $102,000 2005 $105,000 2006 $108,000 2007 $125,000 2008 $250,000 2009 $250,000/$125,000 + Index 2010 $125,000 + Index

Enhanced Section 179 Expensing

Limits to DeductionThe Annual Investment Limit refers to the total amount of deductible

property a taxpayer can put into service in a year before the Section 179 deduction starts to phase out. This amount has also been indexed for inflation as follows:

2003, phase-out begins at $400,000 2004, phase-out begins at $410,000 2005, phase-out begins at $420,000 2006, phase-out begins at $430,000 2007, phase-out begins at $500,000 2008, phase-out begins at $800,000 2009, phase-out begins at $800,000/$500,000 + Index 2010, phase-out begins at $500,000 + Index

Enhanced Section 179 Expensing

Limits to DeductionThe Annual Taxable Income Limit refers to the fact that a taxpayer’s

annual deduction is limited to their aggregate taxable income from the active conduct of any trade or business.

The Section 179 deduction is not automatic. Taxpayers must elect to take the deduction by using IRS form 4562.

For more information see IRS Publication 946: How to Depreciate Property.

50 Percent Bonus Depreciation

Eligible Property Acquisition of Property Placed-in-service Date Original Use of Property

50 Percent Bonus Depreciation

Eligible PropertyProperty that may be deducted in the year of purchase, rather than

depreciated over the asset’s useful life, includes: Machinery and equipment, including printing, publishing and

converting technology Furniture and fixtures Most storage facilities Single-purpose agricultural or horticultural structures Of-the-shelf computer software Property must be new

50 Percent Bonus Depreciation

Acquisition of PropertyFor 50% Bonus Depreciation the taxpayer must acquire the property

after December 31, 2007and before January 1, 2009, but only if no binding contract was in existence before January 1, 2008.

50 Percent Bonus Depreciation

Placed-in-service DateThe property must be placed in service before January 1, 2009.

50 Percent Bonus Depreciation

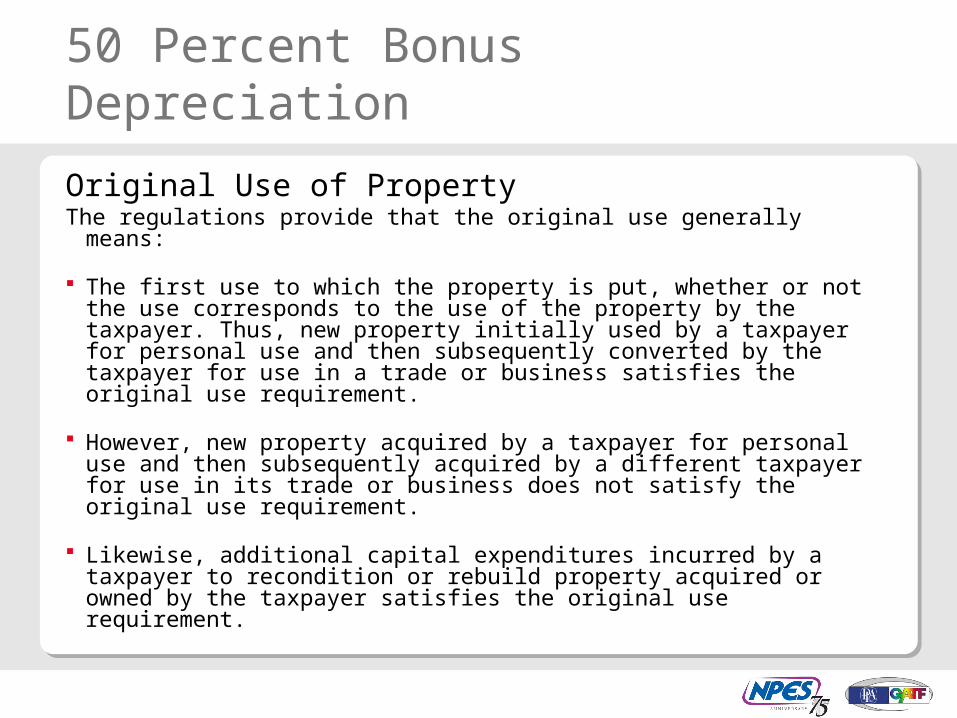

Original Use of PropertyThe regulations provide that the original use generally means:

The first use to which the property is put, whether or not the use corresponds to the use of the property by the taxpayer. Thus, new property initially used by a taxpayer for personal use and then subsequently converted by the taxpayer for use in a trade or business satisfies the original use requirement.

However, new property acquired by a taxpayer for personal use and then subsequently acquired by a different taxpayer for use in its trade or business does not satisfy the original use requirement.

Likewise, additional capital expenditures incurred by a taxpayer to recondition or rebuild property acquired or owned by the taxpayer satisfies the original use requirement.

50 Percent Bonus Depreciation

Original Use of Property cont.The regulations provide that the original use generally means:

However, the cost of reconditioned or rebuilt property acquired by the taxpayer does not satisfy the original use requirement.

The question of whether property is reconditioned or rebuilt is a question of fact.

The regulations provide a safe harbor that property containing used parts will not be treated as reconditioned or rebuilt if the cost of the used parts is not more than 20% of the total cost of the property.

50 Percent Bonus Depreciation

Original Use of Property cont.The regulations provide that the original use generally means:

The regulations provide special rules for certain sale-leaseback and syndication transactions. Concisely, if other requirements are met, an equipment purchaser in a rent-to-own transaction is eligible to claim the depreciation bonus if they purchase the machine within three months of the date on which it is first put into service, and if the machine has had only one user during that period.

How Much Your Company Can Save

Six-color, 56 Inch Wide Sheetfed Press with CoaterExample Price: Without Tax Cut: $3.5 MillionNew 50% Bonus First-year Depreciation = $1.75 MillionPlus Regular Depreciation = $250,000Total First-year Depreciation = $2 Million (57% of new asset)Tax Savings = $800,000 (assuming 40% effective tax rate)New Effective Price With Tax Cut = $2.7 Million – a 23% Savings!

Eight-color, 40 Inch Wide Heatset Web Press Example Price: Without Tax Cut: $ 8 MillionNew 50% Bonus First-year Depreciation = $4 MillionPlus Regular Depreciation = $570,000Total First-year Depreciation = $4.57 Million (57% of new asset)Tax Savings = $1.8 Million (assuming 40% effective tax rate)New Effective Price With Tax Cut = $6.2 Million – a 23% Savings!

Good Reasons to Buy New Technology Now

These examples illustrate the powerful affect of the new investment incentives. Prices used fall into a range for the types of machines used in these examples, but could vary depending upon factors of the sale, such as features of the machine and terms and conditions of the transaction; seek counsel from your tax advisor regarding specific circumstances and transactions..

Pre-press Equipment

GOOD REASON # 1 (Total 2008 purchases do not exceed $800,000) Color Scanner Example Price - Without Tax Cut: $100,000 Enhanced Sec. 179 Small Business Expensing Provision = $250,000/year

(up $800,000 of investment) Total First-year Depreciation = $100,000 (100% of new asset) Tax Savings = $40,000 (assuming 40% effective tax rate) New Effective Price - With Tax Cut = $60,000 - a 40% Savings!

Good Reasons to Buy New Technology Now

GOOD REASON # 2 (Total 2008 purchases exceed $1,050,000) RIPs (Raster Image Processor) Example Price - Without Tax Cut: $400,000 New 50% Bonus First-year Depreciation = $200,000 Plus Regular Depreciation = $28,000 Total First-year Depreciation = $228,000 (57% of new asset) Tax Savings = $91,200 (assuming 40% effective tax rate) New Effective Price – With Tax Cut = $308,800 – a 23% Savings!

Good Reasons to Buy New Technology Now

Press Equipment

GOOD REASON # 3 (Total 2008 purchases exceed $1,050,000) Two-color, Small Sheetfed Press Example Price – Without Tax Cut: $100,000 New 50% Bonus First-year Depreciation = $50,000 Plus Regular Depreciation = $7,000 Total First-year Depreciation = $57,000 (57% of new asset) Tax Savings = $22,800 (assuming 40% effective tax rate) New Effective Price - With Tax Cut = $77,200 - a 23% Savings!

Good Reasons to Buy New Technology Now

GOOD REASON # 4 Six-color, 56 Inch Wide Sheetfed Press with Coater Example Price – Without Tax Cut: $3.5 Million New 50% Bonus First-year Depreciation = $1.75 Million Plus Regular Depreciation = $250,000 Total First-year Depreciation = $2 Million (57% of new asset) Tax Savings = $800,000 (assuming 40% effective tax rate) New Effective Price – With Tax Cut = $2.7 Million – a 23% Savings!

Good Reasons to Buy New Technology Now

GOOD REASON # 5 Eight-color, 40 Inch Wide Heatset Web Press Example Price – Without Tax Cut: $ 8 Million New 50% Bonus First-year Depreciation = $4 Million Plus Regular Depreciation = $570,000 Total First-year Depreciation = $4.57 Million (57% of new asset) Tax Savings = $1.8 Million (assuming 40% effective tax rate) New Effective Price – With Tax Cut = $6.2 Million – a 23% Savings!

Good Reasons to Buy New Technology Now

Finishing & Converting Equipment

GOOD REASON # 6 (Total 2008 purchases do not exceed $800,000) Paper Cutter Example Price – Without Tax Cut: $50,000 Enhanced Sec. 179 Small Business Expensing Provision = $250,000/year

(up $800,000 of investment) Total First-year Depreciation = $50,000 (100% of new asset) Tax Savings = $20,000 (assuming 40% effective tax rate) New Effective Price - With Tax Cut = $30,000 - a 40% Savings!

Good Reasons to Buy New Technology Now

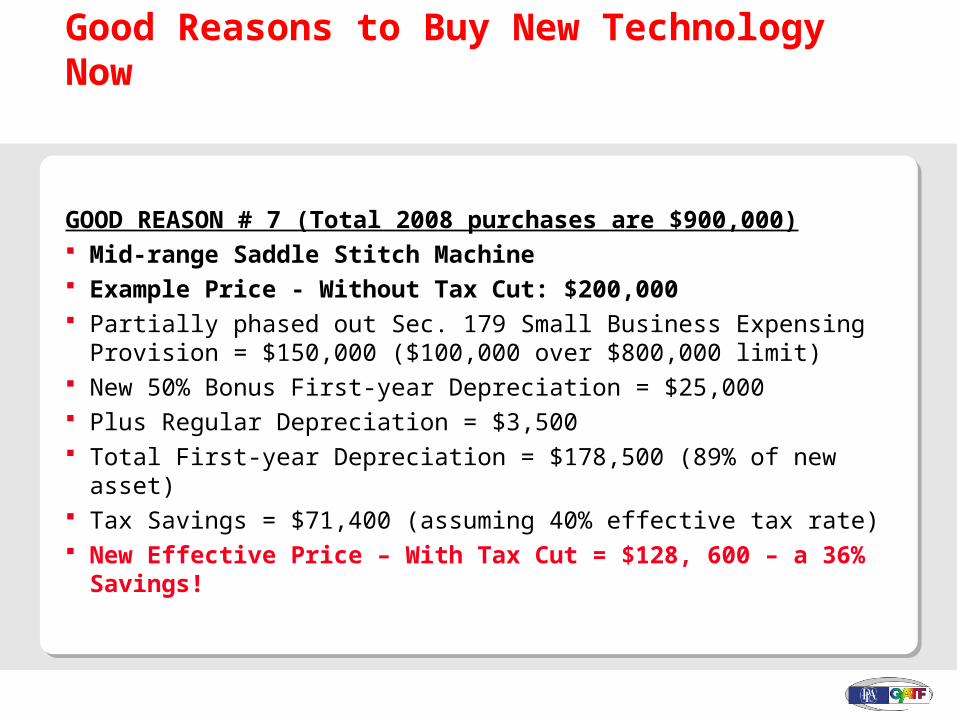

GOOD REASON # 7 (Total 2008 purchases are $900,000) Mid-range Saddle Stitch Machine Example Price - Without Tax Cut: $200,000 Partially phased out Sec. 179 Small Business Expensing Provision =

$150,000 ($100,000 over $800,000 limit) New 50% Bonus First-year Depreciation = $25,000 Plus Regular Depreciation = $3,500 Total First-year Depreciation = $178,500 (89% of new asset) Tax Savings = $71,400 (assuming 40% effective tax rate) New Effective Price – With Tax Cut = $128, 600 – a 36% Savings!

Good Reasons to Buy New Technology Now

GOOD REASON # 8 (Total 2008 purchases do not exceed $800,000) Laser Digital Converting System (die-cutter) Example Price - Without Tax Cut: $500,000 Enhanced Sec. 179 Small Business Expensing Provision = $250,000/year

(up $800,000 of investment) Plus New 50% Bonus First-year Depreciation = $125,000 Plus Regular Depreciation = $17,500 Total First-year Depreciation = $392,500 (79% of new asset) Tax Savings = $157,000 (assuming 40% effective tax rate) New Effective Price – With Tax Cut = $343,000 – a 31% Savings!

THE POWER OF 50% BONUS FIRST-YEAR DEPRECIATION

If you need new equipment and are ready to invest, waiting until 2009 will cost you time and a lot of money!

The following examples tell the story!

The following examples assume that the purchasing company’s total capital equipment investment in the year has exceeded the maximum amount allowable for Section 179 Expensing.

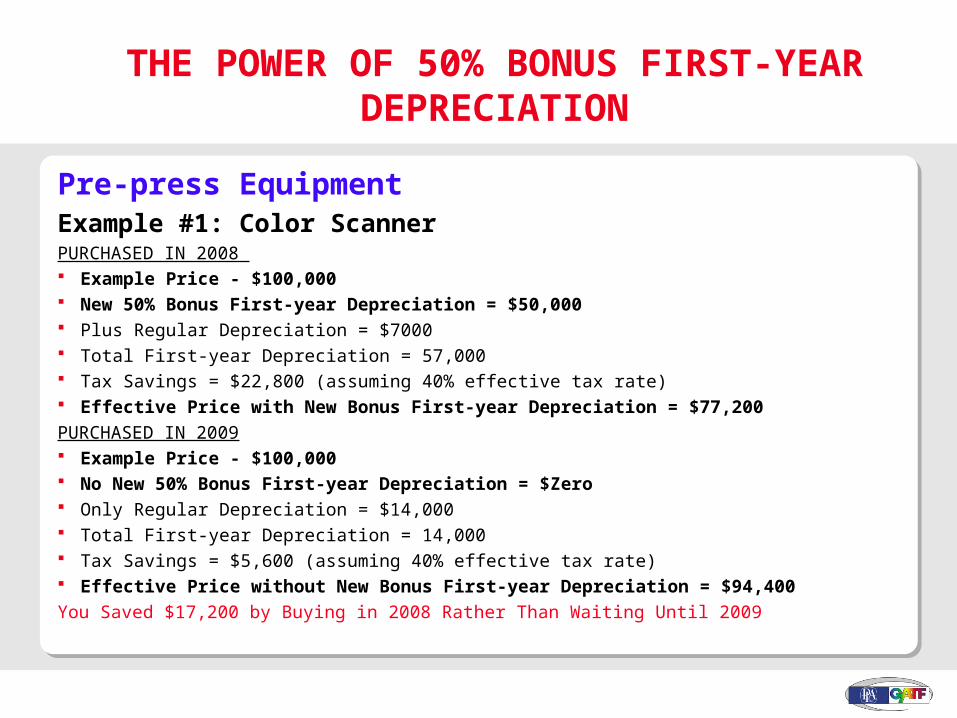

THE POWER OF 50% BONUS FIRST-YEAR DEPRECIATION

Pre-press Equipment Example #1: Color Scanner PURCHASED IN 2008 Example Price - $100,000 New 50% Bonus First-year Depreciation = $50,000 Plus Regular Depreciation = $7000 Total First-year Depreciation = 57,000 Tax Savings = $22,800 (assuming 40% effective tax rate) Effective Price with New Bonus First-year Depreciation = $77,200

PURCHASED IN 2009 Example Price - $100,000 No New 50% Bonus First-year Depreciation = $Zero Only Regular Depreciation = $14,000 Total First-year Depreciation = 14,000 Tax Savings = $5,600 (assuming 40% effective tax rate) Effective Price without New Bonus First-year Depreciation = $94,400

You Saved $17,200 by Buying in 2008 Rather Than Waiting Until 2009

THE POWER OF 50% BONUS FIRST-YEAR DEPRECIATION

EXAMPLE #2: RIPs (Raster Image Processor) PURCHASED IN 2008 Example Price - $400,000 New 50% Bonus First-year Depreciation = $200,000 Plus Regular Depreciation = $28,000 Total First-year Depreciation = $228,000 Tax Savings = $91,200 (assuming 40% effective tax rate) Effective Price with First-year Bonus Depreciation = $308,800

PURCHASED IN 2009 Example Price - $400,000 No New 50% Bonus First-year Depreciation = $Zero Only Regular Depreciation = $56,000 Total First-year Depreciation = $56,000 Tax Savings = $22,400 (assuming 40% effective tax rate) Effective Price without First-year Bonus Depreciation = $377,600

You Saved $68,600 by Buying in 2008 Rather Than Waiting Until 2009

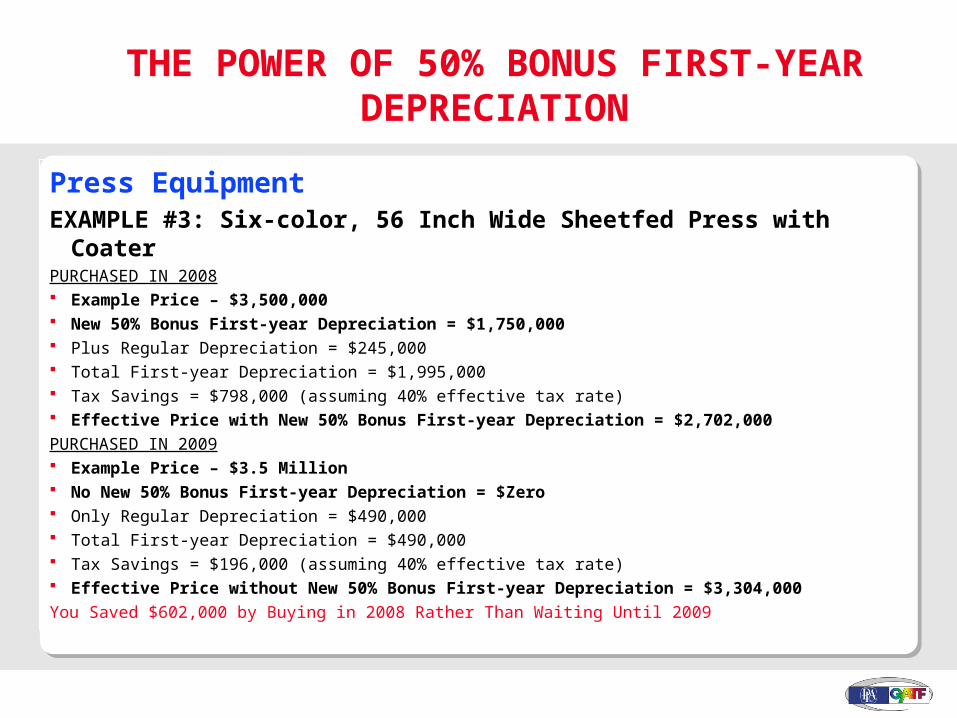

THE POWER OF 50% BONUS FIRST-YEAR DEPRECIATION

Press EquipmentEXAMPLE #3: Six-color, 56 Inch Wide Sheetfed Press with CoaterPURCHASED IN 2008 Example Price – $3,500,000 New 50% Bonus First-year Depreciation = $1,750,000 Plus Regular Depreciation = $245,000 Total First-year Depreciation = $1,995,000 Tax Savings = $798,000 (assuming 40% effective tax rate) Effective Price with New 50% Bonus First-year Depreciation = $2,702,000

PURCHASED IN 2009 Example Price – $3.5 Million No New 50% Bonus First-year Depreciation = $Zero Only Regular Depreciation = $490,000 Total First-year Depreciation = $490,000 Tax Savings = $196,000 (assuming 40% effective tax rate) Effective Price without New 50% Bonus First-year Depreciation = $3,304,000

You Saved $602,000 by Buying in 2008 Rather Than Waiting Until 2009

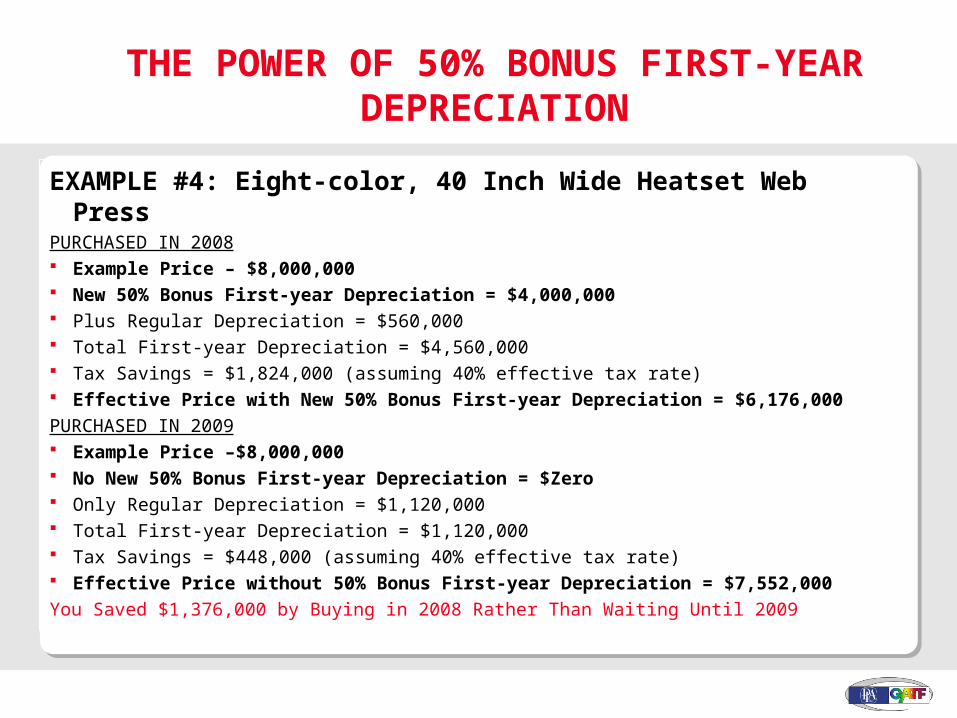

THE POWER OF 50% BONUS FIRST-YEAR DEPRECIATION

EXAMPLE #4: Eight-color, 40 Inch Wide Heatset Web Press PURCHASED IN 2008 Example Price – $8,000,000 New 50% Bonus First-year Depreciation = $4,000,000 Plus Regular Depreciation = $560,000 Total First-year Depreciation = $4,560,000 Tax Savings = $1,824,000 (assuming 40% effective tax rate) Effective Price with New 50% Bonus First-year Depreciation = $6,176,000

PURCHASED IN 2009 Example Price –$8,000,000 No New 50% Bonus First-year Depreciation = $Zero Only Regular Depreciation = $1,120,000 Total First-year Depreciation = $1,120,000 Tax Savings = $448,000 (assuming 40% effective tax rate) Effective Price without 50% Bonus First-year Depreciation = $7,552,000

You Saved $1,376,000 by Buying in 2008 Rather Than Waiting Until 2009

THE POWER OF 50% BONUS FIRST-YEAR DEPRECIATION

Finishing & Converting EquipmentEXAMPLE #5:Mid-range Saddle Stitch Machine PURCHASED IN 2008 Example Price - $200,000 New 50% Bonus First-year Depreciation = $100,000 Plus Regular Depreciation = $14,000 Total First-year Depreciation = $114,000 Tax Savings = $45,600 (assuming 40% effective tax rate) Effective Price with New 50% Bonus First-year Depreciation = $154,400

PURCHASD IN 2009 Example Price - $200,000 No New 50% Bonus First-year Depreciation = $Zero Only Regular Depreciation = $28,000 Total First-year Depreciation = $28,000 Tax Savings = $11,200 (assuming 40% effective tax rate) Effective Price without New 50% Bonus First-year Depreciation = $188,800

You Saved $34,400 by Buying in 2008 Rather Than Waiting Until 2009

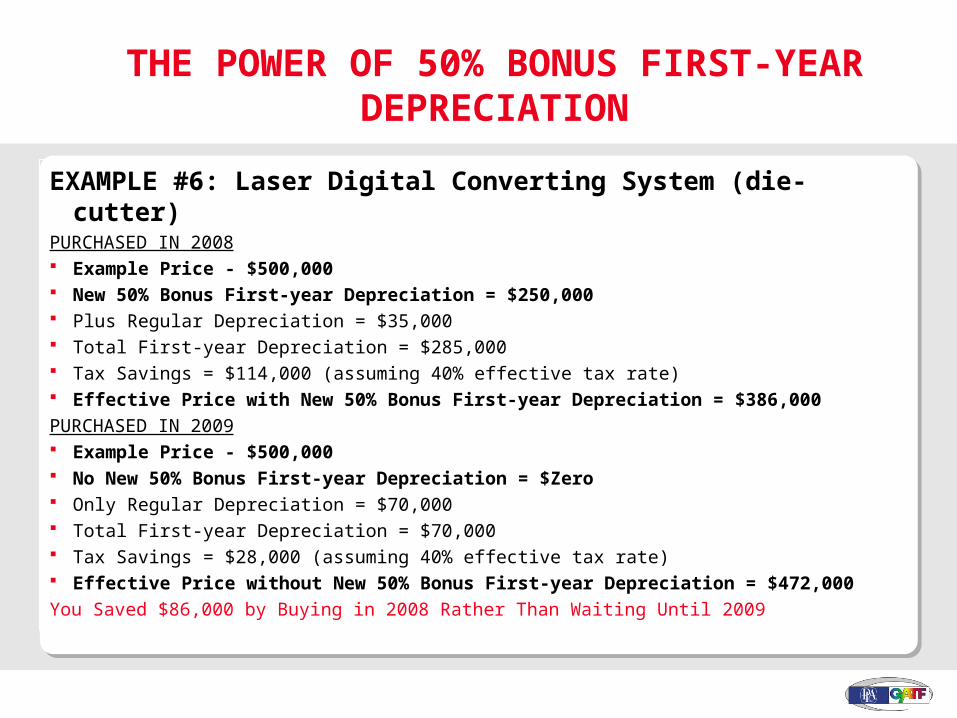

THE POWER OF 50% BONUS FIRST-YEAR DEPRECIATION

EXAMPLE #6: Laser Digital Converting System (die-cutter) PURCHASED IN 2008 Example Price - $500,000 New 50% Bonus First-year Depreciation = $250,000 Plus Regular Depreciation = $35,000 Total First-year Depreciation = $285,000 Tax Savings = $114,000 (assuming 40% effective tax rate) Effective Price with New 50% Bonus First-year Depreciation = $386,000

PURCHASED IN 2009 Example Price - $500,000 No New 50% Bonus First-year Depreciation = $Zero Only Regular Depreciation = $70,000 Total First-year Depreciation = $70,000 Tax Savings = $28,000 (assuming 40% effective tax rate) Effective Price without New 50% Bonus First-year Depreciation = $472,000

You Saved $86,000 by Buying in 2008 Rather Than Waiting Until 2009

SO WHAT ARE YOU WAITING FOR?!?!?!?!?!

For more information contact: NPES Government Affairs Director Mark J. Nuzzaco at

703-264-7235, or e-mail: [email protected]

THE POWER OF 50% BONUS FIRST-YEAR DEPRECIATION

Good Reasons to Buy New Technology Now