Embed Size (px)

Citation preview

Making Investment DecisionsA2 Business Studies

Aims and ObjectivesAim: • To understand the payback investment appraisal

techniqueObjectives:• Define investment and investment appraisal• Describe the uses of investment appraisal• Calculate payback period.• Analyse payback period.

Starter

• In pairs define:– Investment appraisal

• In pairs decide on why investment appraisal may be important.

LO1:Define investment and investment appraisal.

Investment Appraisal

Definition Investment:• Decision to spend an amount of money on

something that will benefit the business in long run. E.g. fixed asset, stakes in another business

Definition Investment Appraisal:• The process of analysing the financial benefits

of a possible future investment.

Investment Appraisal

Importance of Investment Appraisal:• Investment is important, as it may help

achieve objectives, particularly a growth strategy.

• Appraisal is important to judge the benefits of an investment decision and to judge the investment decisions of managers.

Making Investment Decisions

Two major considerations for managers when making investment decisions:

1. Total profits earned by the investment over the foreseeable future.

2. How quickly will the investment recover it’s cost?

Investment Appraisal Techniques

Payback

Average Rate of Return

Net Present Value

Investment Appraisal Techniques

• Financial figures must be considered alongside qualitative factors.

QuantitativeResults

• Non-financial factors must be considered

Qualitative Factors

Payback Method

Definition:• Calculates how long it will take to recoup (get back)

the initial investment.

Note:Before calculating any investment appraisals, tables must be drawn up to show net cash flow for each option.

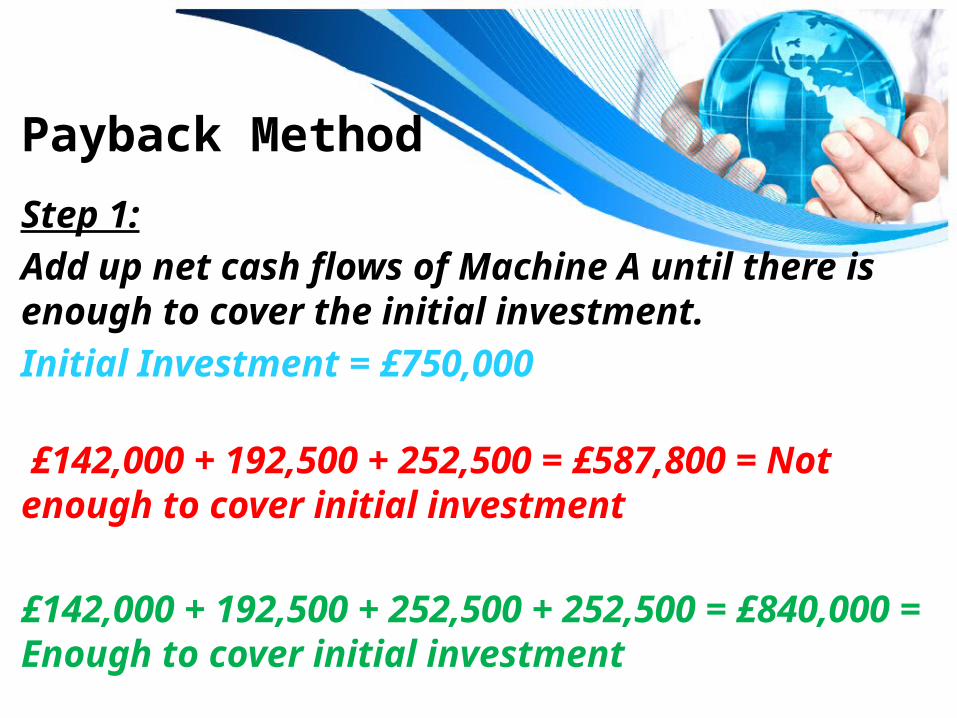

Payback Method

Step 1:Add up net cash flows of Machine A until there is enough to cover the initial investment.Initial Investment = £750,000

£142,000 + 192,500 + 252,500 = £587,800 = Not enough to cover initial investment

£142,000 + 192,500 + 252,500 + 252,500 = £840,000 = Enough to cover initial investment

Payback Method

£142,000 + 192,500 + 252,500 + 252,500 = £840,000 = £840,000 recouped after 4 years, but we want to know when £750,000 is paid back….Therefore:• By year 4 enough money has come in from the new

machine to cover the initial investment of £750,000.• However this is not accurate in terms of calculating

months. £840,000 - £750,000 = £90,000 over• Payback is therefore 3 years and ‘x’ months.

Payback Method

Step 2:Add up net cash flows of Machine A until end of year 3.

(we know the payback period falls between year 3 and year 4, but not in which month)

£142,000 + 192,500 + 252,500 = £587,800 = Year 3 Total Net Cash Flow

Payback Method

Step 2:Initial Investment minus Year 3 total cash flow.

£750,000 – £587,800 = £162,200 = Remaining cash needed to pay back the investment in year 3.

Remaining Cash x12

Net Cash Flow In Year Calculated in Step 1

Payback Method

Step 3:Calculate the month in which investment can be paid back.

£162,200x12

£252,500 = 7.7 months, rounded up to 8 months

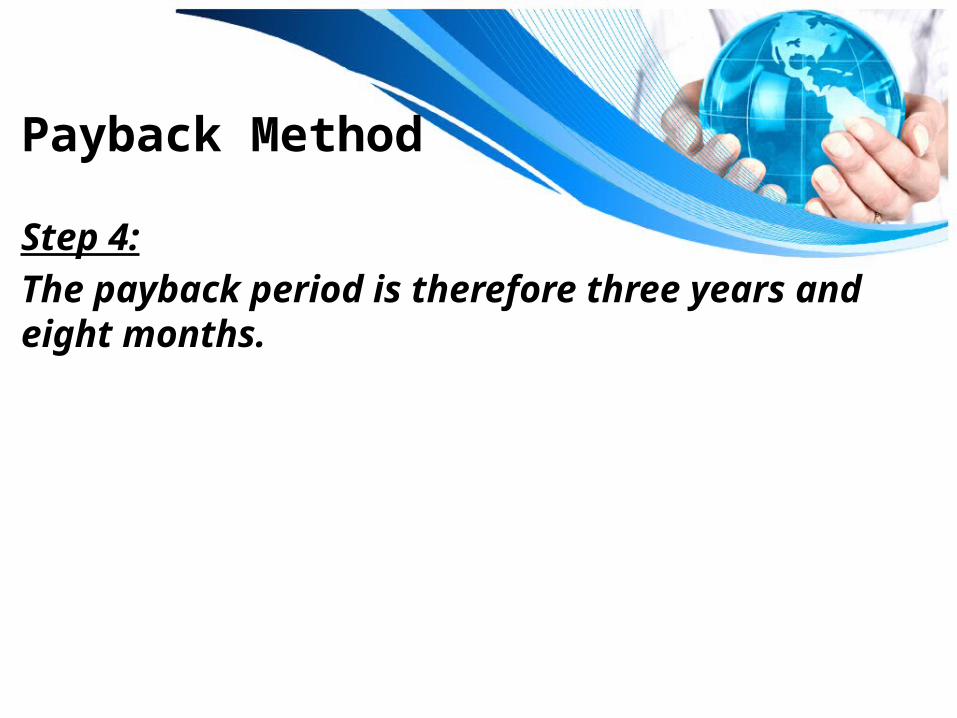

Payback Method

Step 4:The payback period is therefore three years and eight months.

Payback Method

Task:

Calculate the payback period for Machine B.

Analyse which option as managers of Walkers you should chose and why.

Payback Period AnalysedBenefits of Payback Method

• Shorter the payback period the less risky the investment, the quicker it can generate profits from its’ investment.

• Good to use if business has cash flow problems, or if investment is in assets which outdate quickly.

• Important to use if investment funded by external finance.

Payback Period AnalysedDrawback of Payback Period

• Fails to look at cash flows after the payback period, ignoring overall profitability of the investment.

• Assumes that in the year of payback the inflow of cash is steady across the year, which may not be true.

• Especially for seasonal businesses!