Embed Size (px)

Citation preview

Making Indonesia 4.0 Fokus Pangan dan Energi

Oleh : Achdiat Atmawinata

Anggota Komtek Material Maju DRN

4/20/2018 1 BALITBANGBUN BOGOR 19 April 2018

Making

Indonesia 4.0

Making

Indonesia

Agenda

2

6

Next Steps

5

Economic Benefit and Job Creations

4

10 National Priorities for “Making Indonesia 4.0”

3

Five Focus Sectors for “Making Indonesia 4.0”

2

“Making Indonesia 4.0” Aspirations

1

Background

Making

Indonesia

Making

Indonesia

3

Background

Making

Indonesia

Making

Indonesia

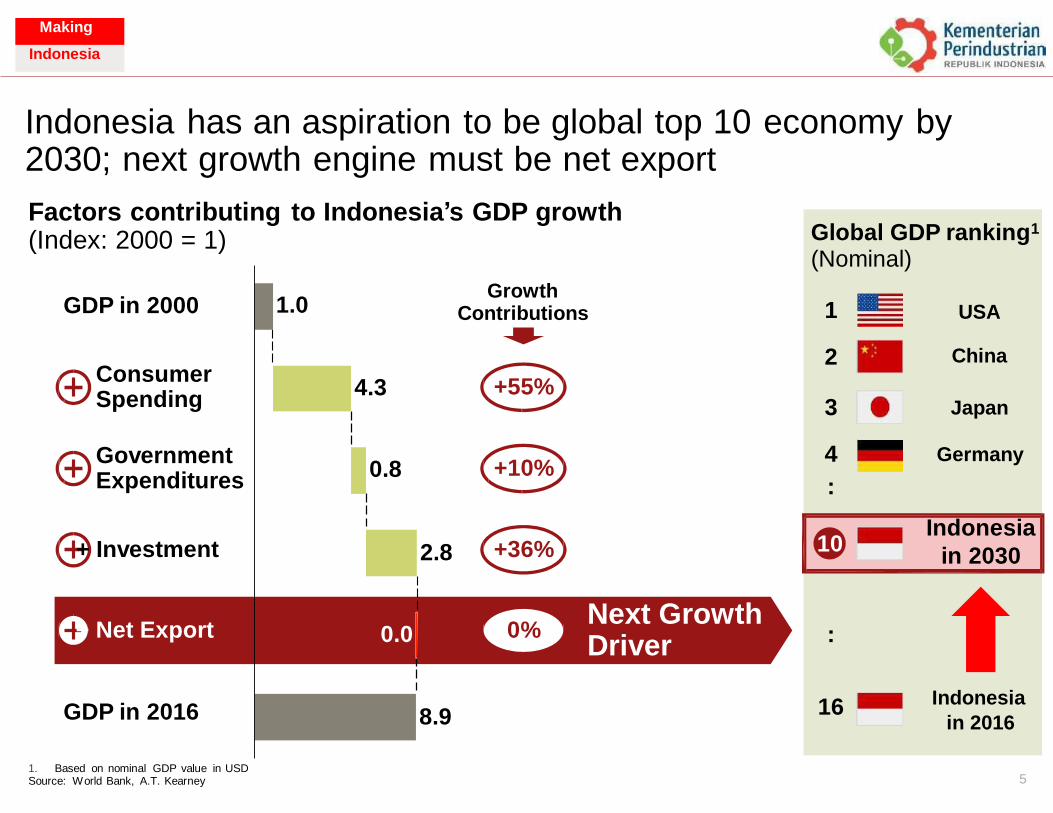

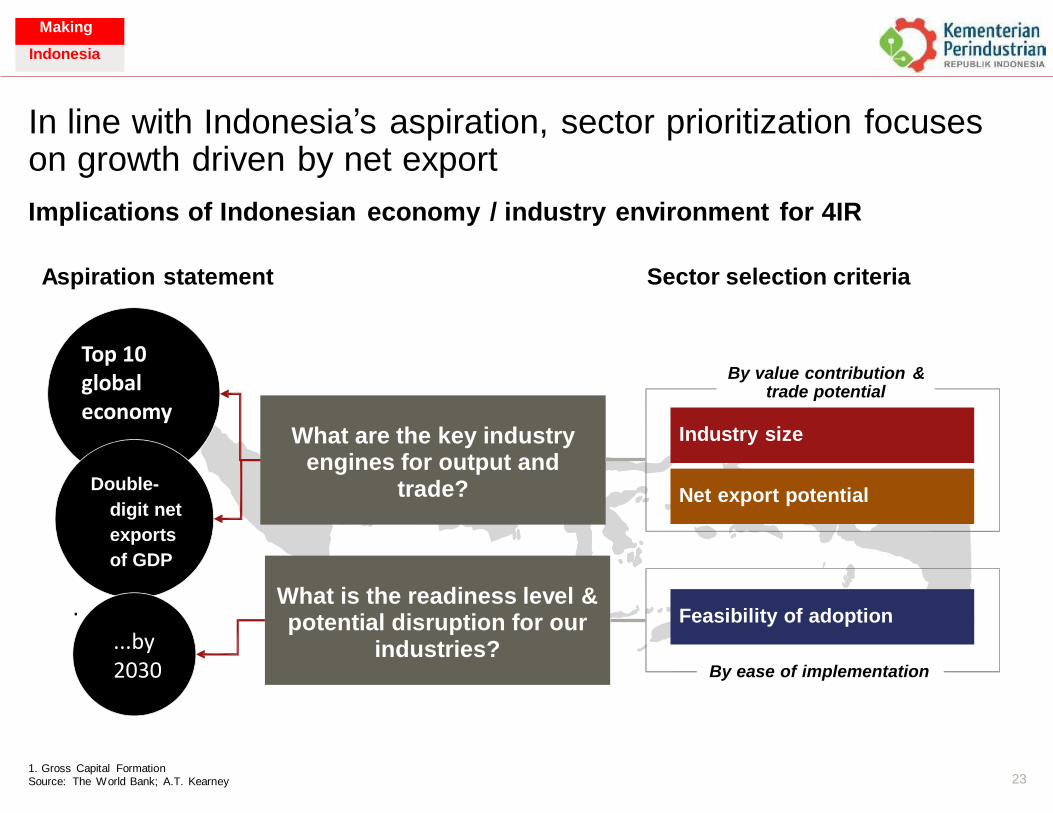

Indonesia has an aspiration to be global top 10 2030; next growth engine must be net export

economy by

Factors contributing (Index: 2000 = 1)

to Indonesia’s GDP growth

Growth Contributions GDP in 2000

Consumer Spending

+55%

Government Expenditures

+10%

+ Investment +36% 2.8

Next Growth + Net Export 0%

Driver

GDP in 2016 8.9 in 2016

1. Based on nominal GDP value in USD 5 Source: World Bank, A.T. Kearney

1.0

4.3

0.8

0.0

Global GDP ranking1 (Nominal)

1 USA

2 China

3 Japan

4 Germany

:

Indonesia 10

in 2030

:

16 Indonesia

Making

Indonesia

Making

Indonesia

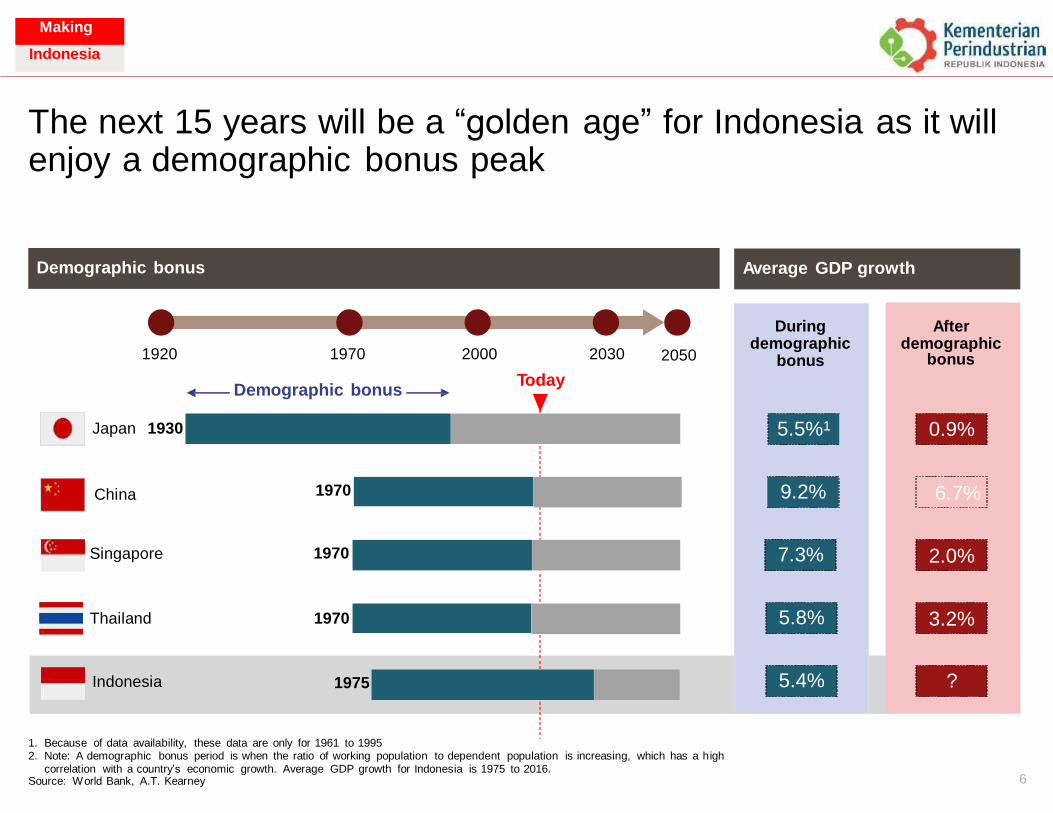

The next 15 years will be a “golden age” for Indonesia as it will enjoy a demographic bonus peak

bonus

1. Because of data availability, these data are only for 1961 to 1995 2. Note: A demographic bonus period is when the ratio of working population to dependent population is increasing, which has a h igh

correlation with a country’s economic growth. Average GDP growth for Indonesia is 1975 to 2016. Source: World Bank, A.T. Kearney 6

1920 1970 2000 2030 2050

Demographic bonus Today

Japan 1930

China 1970

Singapore 1970

Thailand 1970

During demographic

bonus

5.5%1

9.2%

7.3%

5.8%

5.4%

After demographic

0.9%

6.7%

2.0%

3.2%

Indonesia 1975

?

Average GDP growth

Demographic bonus

Making

Indonesia

Making

Indonesia

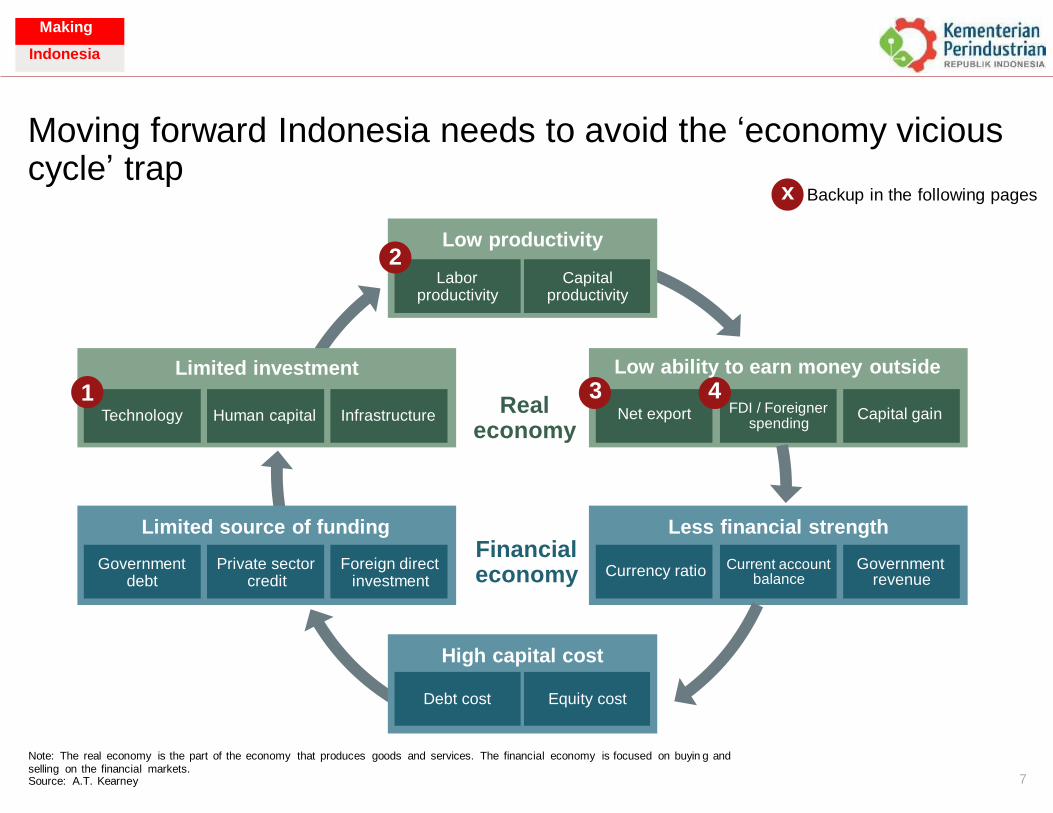

Moving forward Indonesia needs to avoid the ‘economy vicious

x cycle’ trap

Backup in the following pages

2

Real economy

Financial economy

Note: The real economy is the part of the economy that produces goods and services. The financial economy is focused on buyin g and selling on the financial markets. Source: A.T. Kearney 7

High capital cost

Debt cost Equity cost

revenue

balance

Less financial strength

Currency ratio Current account Government

Limited source of funding

Government Private sector Foreign direct debt credit investment

spending

Low ability to earn money outside

3 4 Net export FDI / Foreigner Capital gain

Limited investment

1 Technology Human capital Infrastructure

Low productivity

Labor Capital productivity productivity

Making

Indonesia

Making

Indonesia

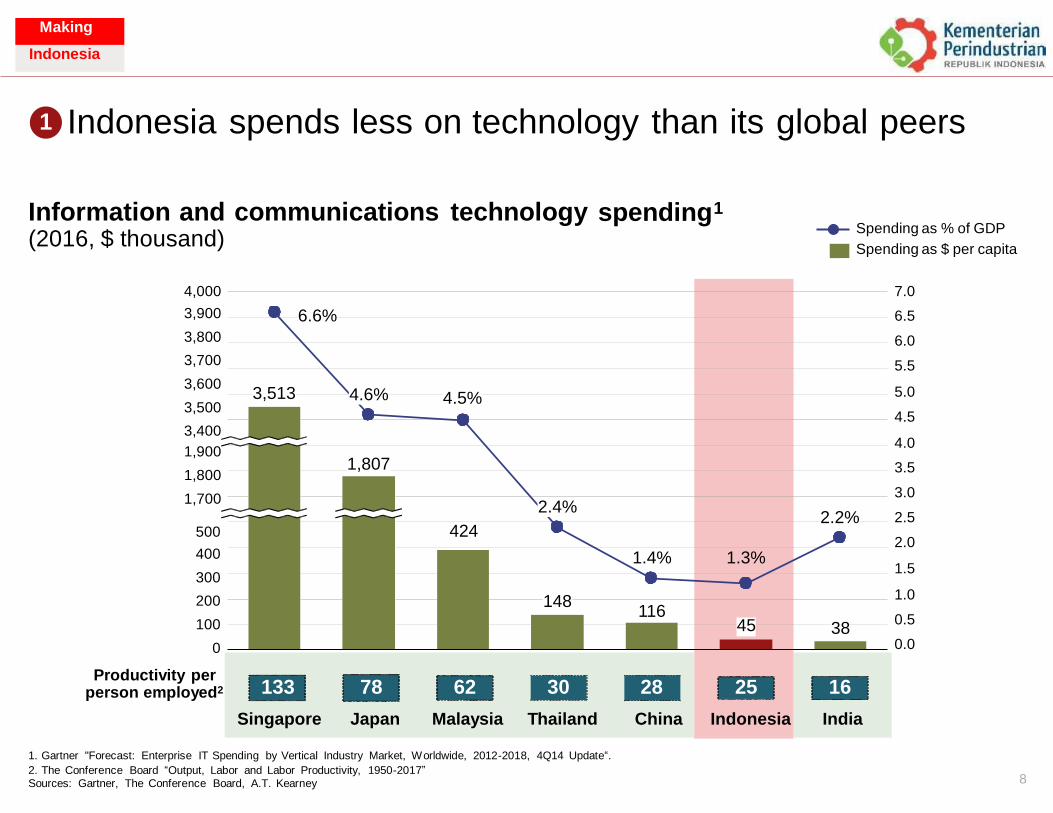

Indonesia spends less on technology than its global peers 1

spending1 Information and (2016, $ thousand)

communications technology Spending as % of GDP

Spending as $ per capita

4,000

3,900

3,800

3,700

3,600

3,500

3,400

1,900

1,800

1,700

7.0

6.5

6.0

5.5

5.0

4.5

4.0

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

500

400

300

200

100

0

Productivity per person employed2

116

1. Gartner "Forecast: Enterprise IT Spending by Vertical Industry Market, Worldwide, 2012-2018, 4Q14 Update“.

2. The Conference Board “Output, Labor and Labor Productivity, 1950-2017”

Sources: Gartner, The Conference Board, A.T. Kearney 8

6.6%

3,513 4.6% 4.5%

1,807

2.4%

2.2% 424

1.4% 1.3%

148

38 45

133 78 62 30 28

Singapore Japan Malaysia Thailand China

25

Indonesia

16

India

Making

Indonesia

Making

Indonesia

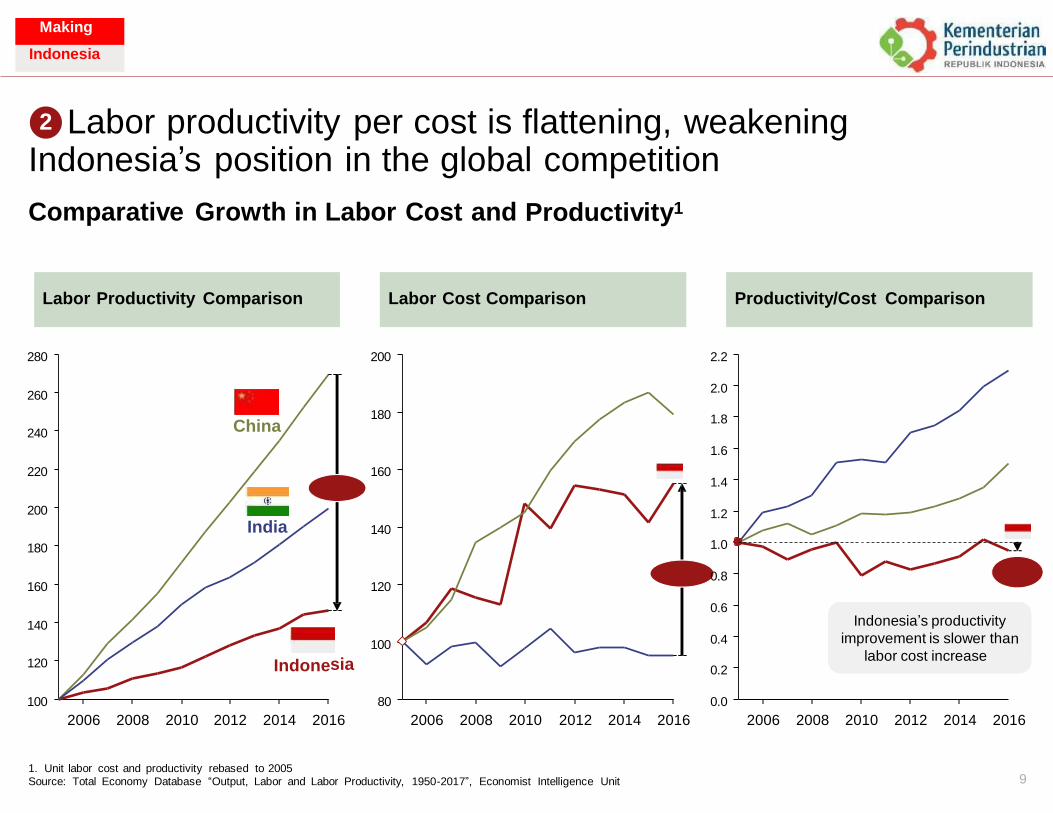

Labor productivity per cost is flattening, weakening 2

Indonesia’s position in the global competition

Productivity1 Comparative Growth in Labor Cost and

280 200 2.2

2.0 260

180 1.8 240

1.6

220 160 1.4

200 1.2

140 1.0 180

0.8 160 120

0.6

140 0.4 100

120 sia 0.2

100 80 0.0

2006 2008 2010 2012 2014 2016 2006 2008 2010 2012 2014 2016 2006 2008 2010 2012 2014 2016

1. Unit labor cost and productivity rebased to 2005

Source: Total Economy Database “Output, Labor and Labor Productivity, 1950-2017”, Economist Intelligence Unit 9

Indonesia’s productivity

improvement is slower tha

labor cost increase

n

China

India

Indone

Productivity/Cost Comparison

Labor Cost Comparison

Labor Productivity Comparison

Making

Indonesia

Making

Indonesia

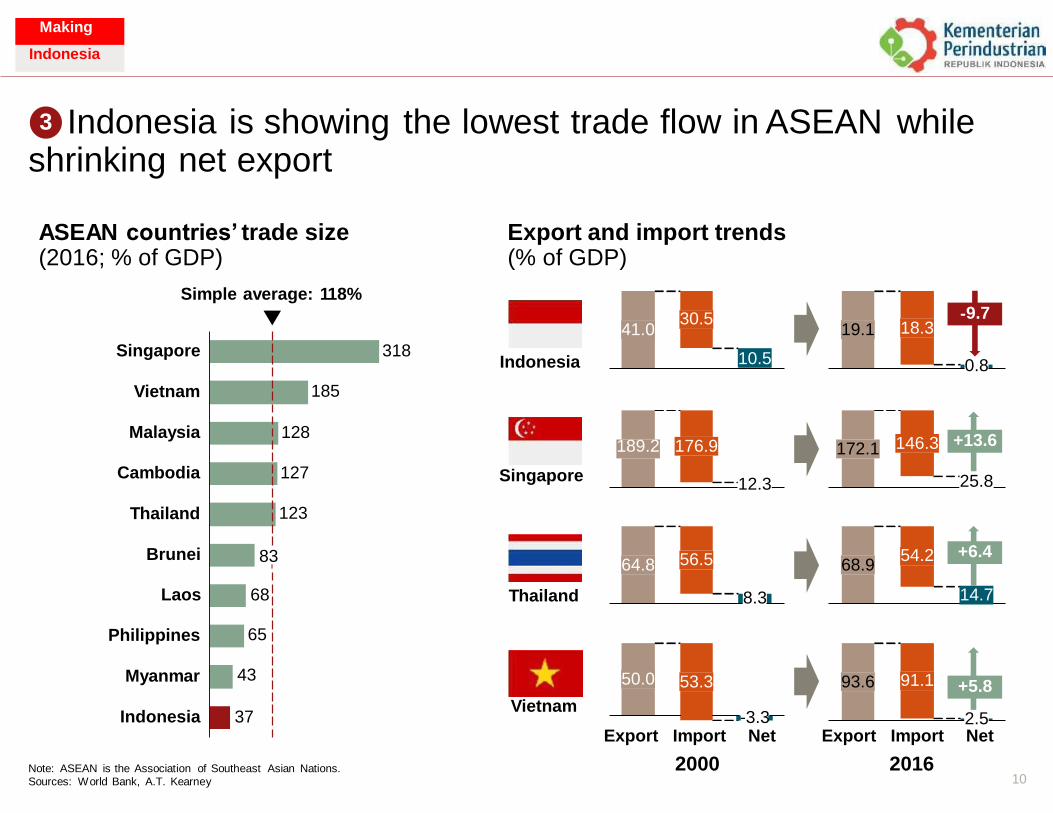

Indonesia is showing the lowest trade flow in ASEAN while 3

shrinking net export

ASEAN countries’ trade size (2016; % of GDP)

Simple average: 118%

Export and import trends (% of GDP)

Singapore 318 Indonesia 0.8

Vietnam

Malaysia

Cambodia Singapore 25.8 12.3

Thailand

Brunei

Laos Thailand 8.3

Philippines

Myanmar

Vietnam Indonesia -3.3 2.5

Export Import Net

2000

Export Import Net

2016 Note: ASEAN is the Association of Southeast Asian Nations.

Sources: World Bank, A.T. Kearney 10

+5.8

93.6

91.1

50.0

53.3

68.9

54.2

+6.4

14.7

64.8

56.5

+13.6 146.3 172.1 189.2 176.9

185

128

127

123

83

68

65

43

37

9.7

19.1

18.3

-

41.0

30.5

10.5

Making

Indonesia

Making

Indonesia

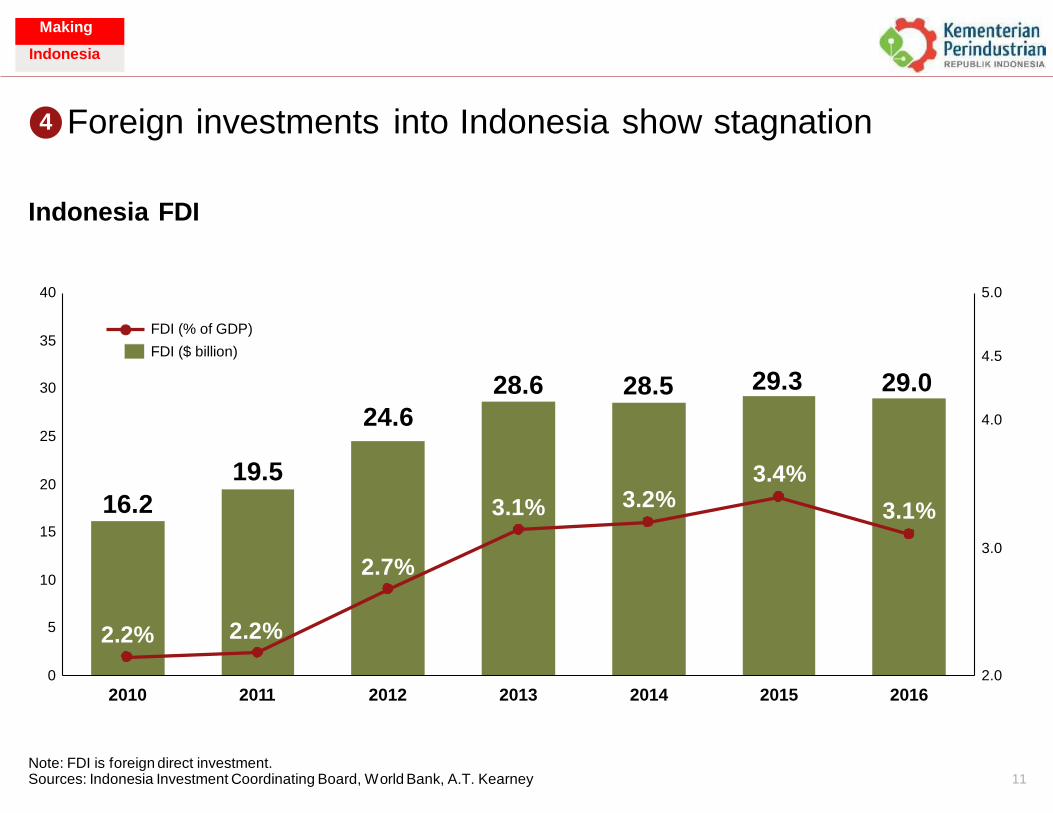

Foreign investments into Indonesia show stagnation 4

Indonesia FDI

40 5.0

35 4.5

30

4.0 25

20

15 3.0

10

5

0 2.0

2010 2011 2012 2013 2014 2015 2016

Note: FDI is foreign direct investment. Sources: Indonesia Investment Coordinating Board, World Bank, A.T. Kearney 11

FDI (% of GDP)

FDI ($ billion)

28.6 28.5 29.3 29.0

3.4%

3.1%

24.6

3.1%

3.2%

19.5

16.2

2.7%

2.2% 2.2%

Making

Indonesia

Making

Indonesia

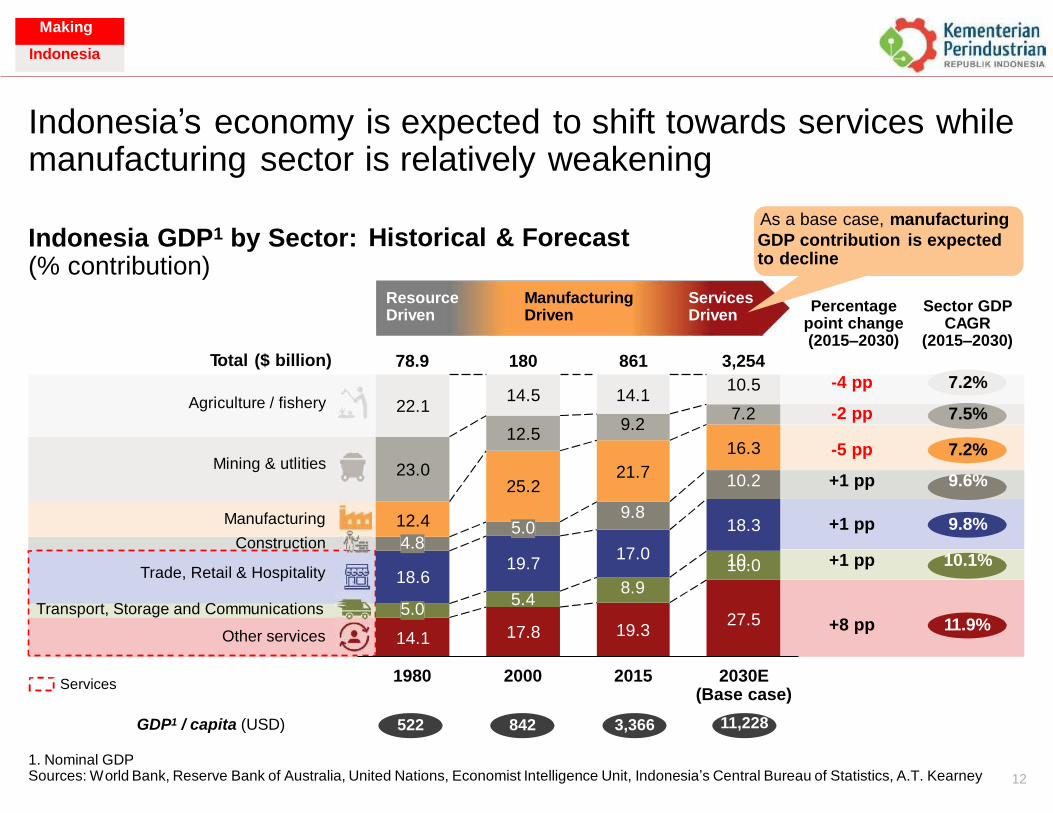

Indonesia’s economy is expected to shift towards services while manufacturing sector is relatively weakening

As a base case, manufacturing

Indonesia GDP1 by Sector: Historical & Forecast GDP contribution is expected to decline (% contribution)

Resource Driven

Manufacturing Driven

Services Driven

Percentage point change (2015–2030)

Sector GDP CAGR

(2015–2030)

Total ($ billion) 78.9 180 861 3,254

10.0

1980 2000 2015 2030E (Base case)

11,228

Services

GDP1 / capita (USD) 522 842 3,366

1. Nominal GDP Sources: World Bank, Reserve Bank of Australia, United Nations, Economist Intelligence Unit, Indonesia’s Central Bureau of Statistics, A.T. Kearney 12

Agriculture / fishery

22.1

14.5

14.1 10.5 -4 pp 7.2%

7.2 -2 pp 7.5%

12.5 9.2

16.3

-5 pp 7.2% Mining & utlities

23.0

21.7

25.2 10.2 +1 pp 9.6%

Manufacturing

12.4 9.8

18.3

+1 pp 9.8% 5.0

17.0 Construction 4.8

19.7

Trade, Retail & Hospitality

18.6 10. +1 pp 10.1%

8.9

27.5

+8 pp 11.9%

5.4 Transport, Storage and Communications 5.0

19.3

17.8

Other services

14.1

Making

Indonesia

Making

Indonesia

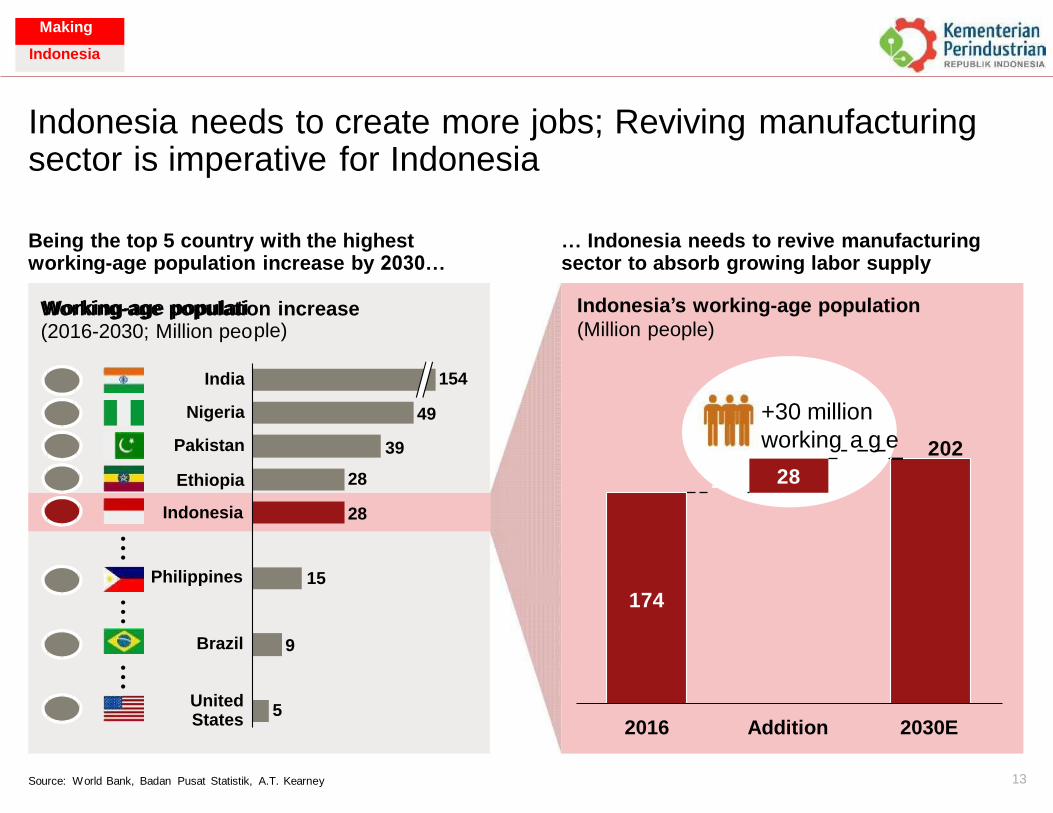

Indonesia needs to create more jobs; Reviving manufacturing sector is imperative for Indonesia

Being the top 5 country with the highest working-age population increase by 2030…

… Indonesia needs to revive manufacturing sector to absorb growing labor supply

Working-age population increase ple)

154

49

39

28

States

13 Source: World Bank, Badan Pusat Statistik, A.T. Kearney

Indonesia’s working-age population

(Million people)

+30 million

working a g e 202 28

174

2016 Addition 2030E

Working-age populati (2016-2030; Million peo

India

Nigeria

Pakistan

Ethiopia 28

Indonesia

Philippines 15

Brazil 9

United 5

Making

Indonesia

Making

Indonesia

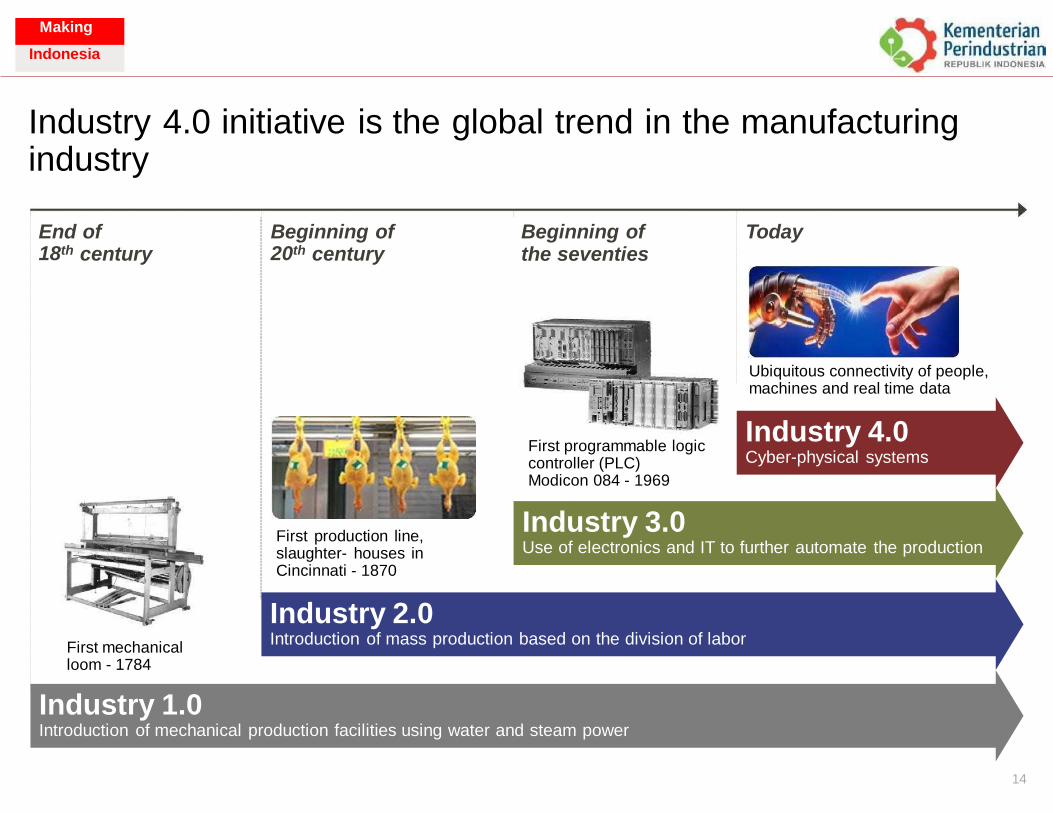

Industry industry

4.0 initiative is the global trend in the manufacturing

End of Beginning of Beginning of the seventies

Today 18th 20th century century

Ubiquitous connectivity of people, machines and real time data

Industry 4.0 Cyber-physical systems

First programmable logic controller (PLC) Modicon 084 - 1969

Industry 3.0 Use of electronics and IT to further automate the production

First production line, slaughter- houses in Cincinnati - 1870

Industry 2.0 Introduction of mass production based on the division of labor

First mechanical loom - 1784

Industry 1.0 Introduction of mechanical production facilities using water and steam power

14

Making

Indonesia

Making

Indonesia

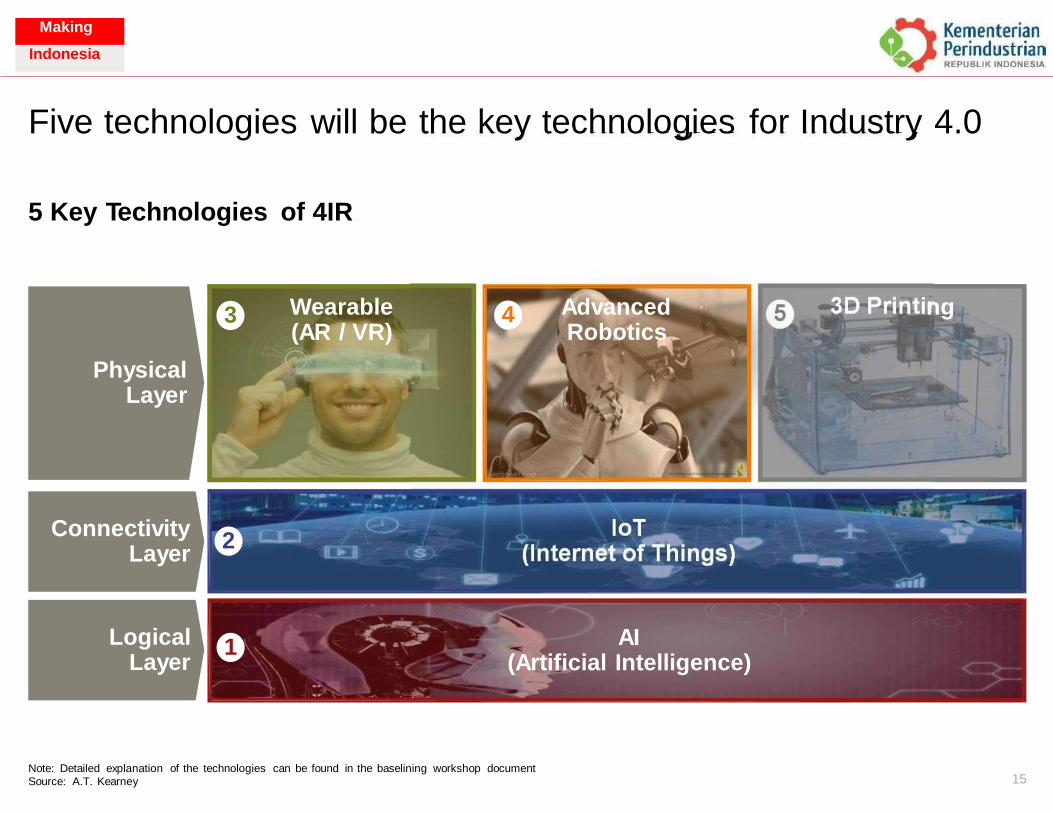

5 3D Printi

IoT (Internet of Things)

Five technologies will be the key technologies for Industry 4.0

5 Key Technologies of 4IR

Wearable Advanced Robotics

ng 3 4 (AR / VR)

Physical Layer

Connectivity Layer

2

Logical Layer

AI (Artificial Intelligence)

1

Note: Detailed explanation of the technologies can be found in the baselining workshop document

Source: A.T. Kearney 15

Making

Indonesia

Making

Indonesia

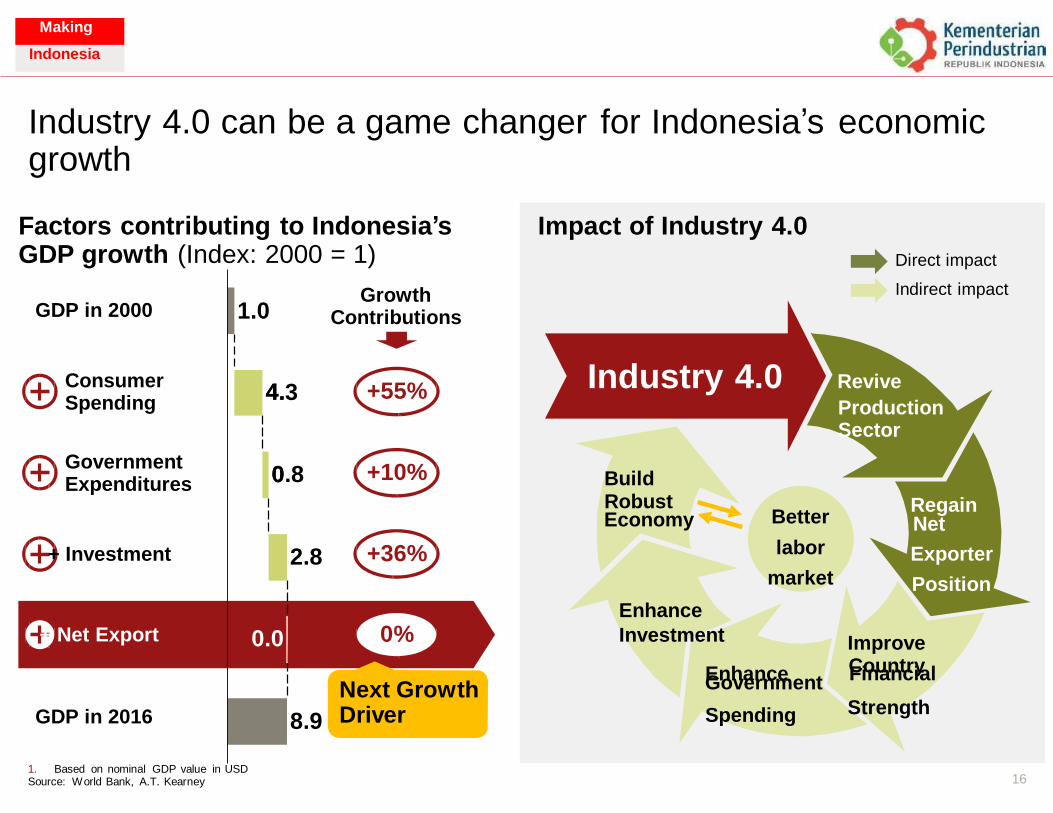

Industry 4.0 can be a game changer growth

for Indonesia’s economic

Factors contributing to Indonesia’s GDP growth (Index: 2000 = 1)

Growth Contributions GDP in 2000

Consumer Spending

+55% 4.3

Government Expenditures

+10% 0.8

Better Economy Net

+36% + Investment 2.8

0% + Net Export

Financial Government Next Growth Driver GDP in 2016 8.9

1. Based on nominal GDP value in USD 16 Source: World Bank, A.T. Kearney

1.0

4.

0

0.0

Impact of Industry 4.0

Direct impact

Indirect impact

Industry 4.0 Revive

Production Sector

Build Robust Regain

labor Exporter

market Position

Enhance

Investment Improve Enhance Country

Spending Strength

Making

Indonesia

Making

Indonesia

17

“Making Indonesia 4.0” Aspirations

Making

Indonesia

Making

Indonesia

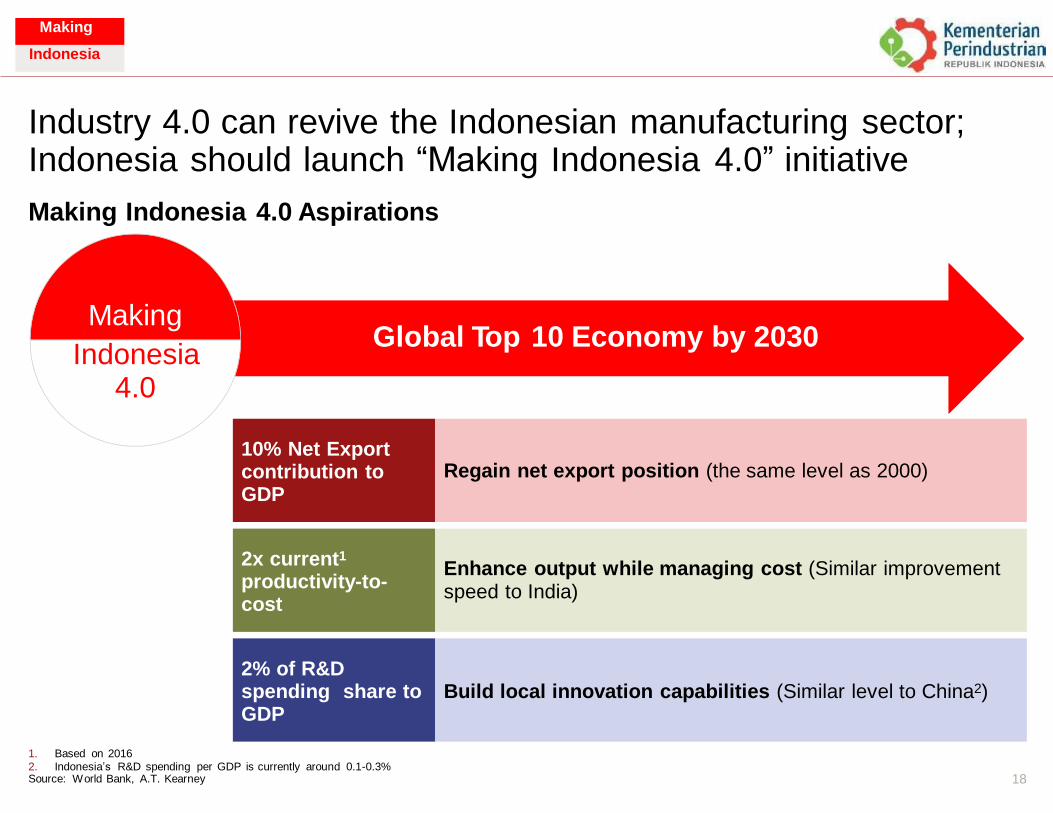

Industry 4.0 can revive the Indonesian manufacturing sector; Indonesia should launch “Making Indonesia 4.0” initiative

Making Indonesia 4.0 Aspirations

Making

Indonesia 4.0

Global Top 10 Economy by 2030

speed to India)

1. 2.

Based on 2016 Indonesia’s R&D spending per GDP is currently around 0.1-0.3%

Source: World Bank, A.T. Kearney 18

2% of R&D spending share to GDP

Build local innovation capabilities (Similar level to China2)

2x current1

productivity-to- cost

Enhance output while managing cost (Similar improvement

10% Net Export contribution to GDP

Regain net export position (the same level as 2000)

Making

Indonesia

Making

Indonesia

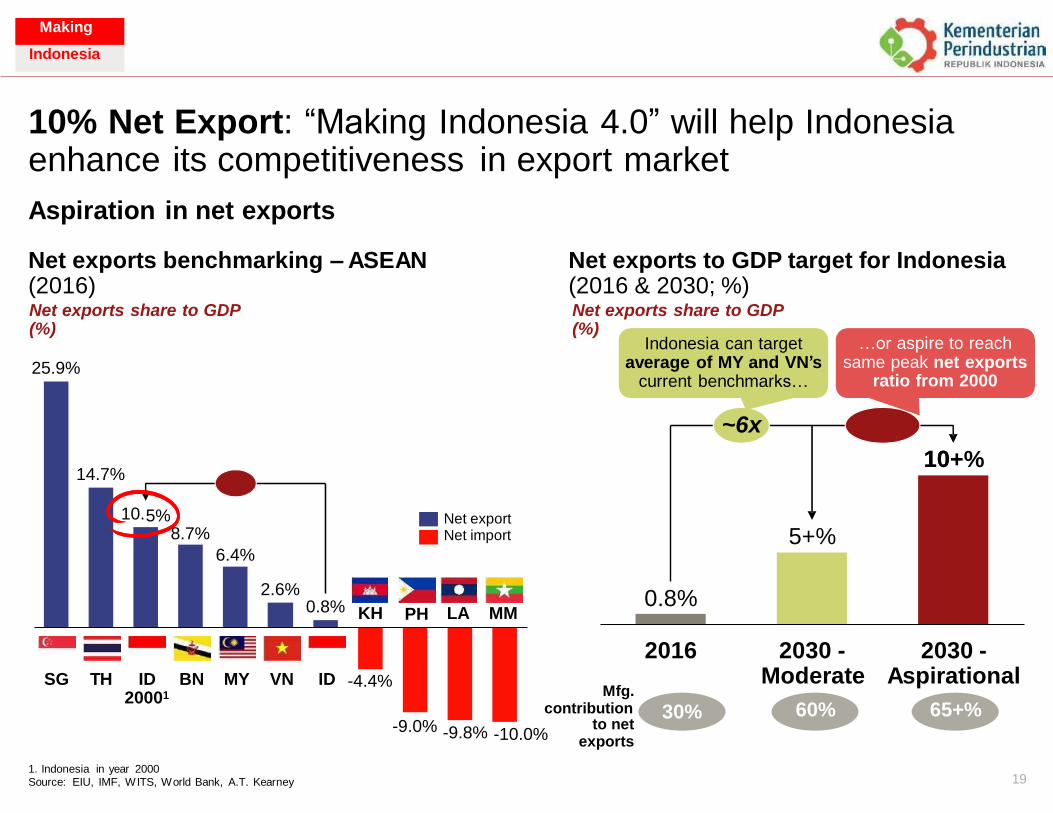

10% Net Export: “Making Indonesia 4.0” will help Indonesia enhance its competitiveness

Aspiration in net exports

in export market

Net exports benchmarking (2016) Net exports share to GDP (%)

– ASEAN Net exports to GDP target for Indonesia (2016 & 2030; %) Net exports share to GDP (%)

Indonesia can target average of MY and VN’s

current benchmarks…

…or aspire to reach same peak net exports

ratio from 2000 25.9%

~6x

10+% 14.7%

10. Net export Net import

2.6% 0.8% KH LA MM PH

2016 2030 - 2030 - Aspirational

65+%

Moderate

60%

SG TH ID 20001

BN MY VN ID -4.4% Mfg.

contribution 30% -9.0% -9.8% -10.0% to net

exports

1. Indonesia in year 2000 Source: EIU, IMF, WITS, World Bank, A.T. Kearney 19

5% 8.7%

6.4%

0.8%

10

5+%

Making

Indonesia

Making

Indonesia

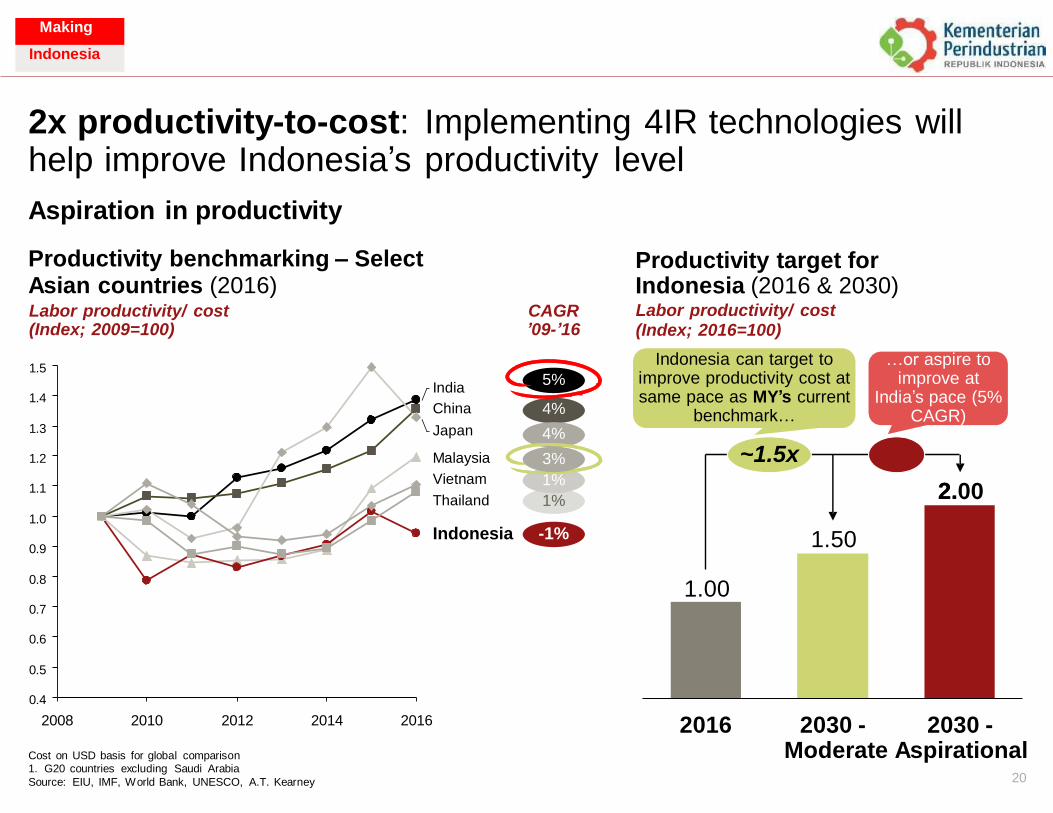

2x productivity-to-cost: Implementing 4IR technologies will help improve Indonesia’s productivity

Aspiration in productivity

Productivity benchmarking – Select Asian countries (2016)

level

Productivity target for Indonesia (2016 & 2030) Labor productivity/ cost (Index; 2016=100)

Labor productivity/ cost (Index; 2009=100)

CAGR ’09-’16

Indonesia can target to improve productivity cost at same pace as MY’s current

benchmark…

…or aspire to improve at

India’s pace (5% CAGR)

1.5 5%

4%

4%

3%

1%

1%

India

China

Japan

Malaysia

Vietnam

Thailand

1.4

1.3

~1.5x 1.2

2.00 1.1

1.0

Indonesia -1% 0.9

0.8

0.7

0.6

0.5

0.4

2008 2010 2012 2014 2016 2016 2030 - 2030 - Moderate Aspirational

20

Cost on USD basis for global comparison 1. G20 countries excluding Saudi Arabia

Source: EIU, IMF, World Bank, UNESCO, A.T. Kearney

1.00

2.

1.50

Making

Indonesia

Making

Indonesia

SG MY TH CH JP

2% of R&D spending: The by more innovation

Aspiration in R&D

R&D spending benchmarking – World Top 40 countries (2016, %) R&D share to GDP (%)

economic growth will be stimulated

R&D spending target for Indonesia (2016 & 2030, %) R&D share to GDP

ASEAN Others

…or aspire to target (%)

Indonesia can target MY’s current R&D benchmark…

China’s R&D spend and accelerate progress to Visi

2045’s R&D target xx

4.0%

Rank based on $ of R&D spending

~4x

2.0

Indonesia Singapore China Thailand S. Korea Japan Malaysia 2016 2030 - 2030 - Aspirational Moderate 1 3 20 2 28 NA 37

21 Source: Industrial Research Institute, R&D Magazine, EIU, A.T. Kearney

0.3

2

1.1

3.4%

2.6%

2.0%

1.1%

0.6% 0.3%

Making

Indonesia

Making

Indonesia

22

Electronics

Food & Beverage

Textile & Beverage

Automotive

Chemical

Five Focus Sectors for “Making Indonesia 4.0”

Food & Beverage

Textile & Beverage

Chemical

Automotive Electronics

Making

Indonesia

Making

Indonesia

What are the key industry engines for output and

trade?

What is the readiness level & potential disruption for our

industries?

.

In line with Indonesia’s aspiration, sector prioritization focuses on growth driven by net export

Implications of Indonesian economy / industry environment for 4IR

Aspiration statement Sector selection criteria

By value contribution & trade potential

Double-

digit net

exports

of GDP

By ease of implementation

1. Gross Capital Formation

Source: The World Bank; A.T. Kearney 23

Feasibility of adoption

What is the readiness level & potential disruption for our

industries?

Net export potential

Industry size

What are the key industry engines for output and

trade?

Making

Indonesia

...by 2030

Top 10 global economy

Making

Indonesia

Basic Metal

Chemical

Electronics, Optics & Elect.

Appliances

Transport Equipment –

Auto

Metal Goods

Pharmaceutical and Traditional

Medicines

Tobacco

Processing

Food & Beverage

Non-Metal

Goods

Rubber & Plastic Goods

Wood & Furniture

Industrial Machinery & Equipment

Jewelry & Valuable Goods

Paper-Related

Products

Textile, Apparel & Leather

Goods

Coal, Oil & Gas

Refinery

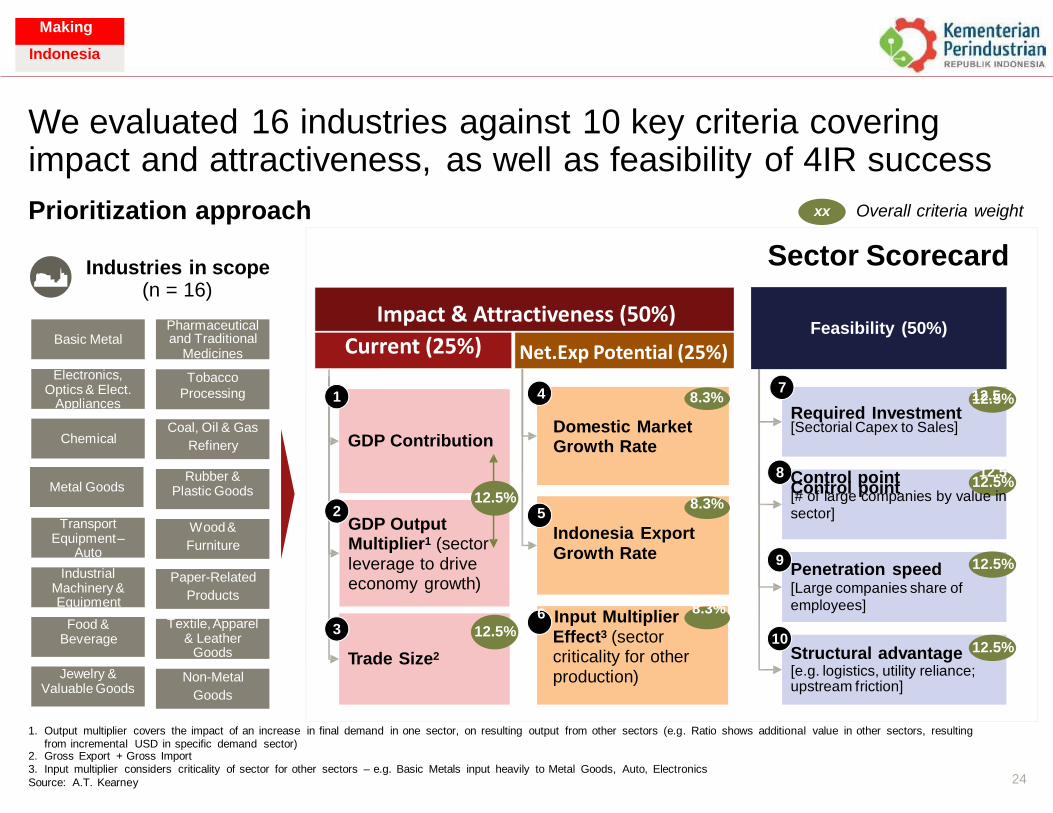

We evaluated 16 industries against 10 key criteria covering impact and attractiveness,

Prioritization approach

as well as feasibility of 4IR success

Overall criteria weight xx

Sector Scorecard Industries in scope (n = 16)

and Traditional

7 1 12.5%

Required Investment

Refinery

8 12.5% Control point

12.5% 2

GDP Output Furniture

9 12.5%

Products

3 12.5% 10

12.5%

[e.g. logistics, utility reliance;

Goods

1. Output multiplier covers the impact of an increase in final demand in one sector, on resulting output from other sectors (e.g. Ratio shows additional value in other sectors, resulting from incremental USD in specific demand sector)

2. Gross Export + Gross Import 3. Input multiplier considers criticality of sector for other sectors – e.g. Basic Metals input heavily to Metal Goods, Auto, Electronics

Source: A.T. Kearney 24

Non-Metal Jewelry & Valuable Goods

Structural advantage

upstream friction]

Textile, Apparel & Leather

Goods

Food & Beverage

Trade Size2

6 Input Multiplier 8.3%

Effect3 (sector criticality for other production)

Paper-Related Industrial Machinery & Equipment

Penetration speed [Large companies share of

employees]

Wood & Transport Equipment –

Auto

Multiplier1 (sector leverage to drive economy growth)

8.3% 5

Indonesia Export Growth Rate

Control point 12.5

[# of large companies by value in

sector]

Rubber & Plastic Goods

Metal Goods

Coal, Oil & Gas

Chemical

12.5

[Sectorial Capex to Sales]

4 8.3%

Domestic Market Growth Rate

GDP Contribution

Tobacco

Processing

Electronics, Optics & Elect.

Appliances

Basic Metal Pharmaceutical

Medicines

Feasibility (50%)

Making

Indonesia

Impact & Attractiveness (50%)

Current (25%) Net.Exp Potential (25%)

Making

Indonesia

Top 5 Sectors

5 sectors were selected for “Making Indonesia 4.0”

Sector Prioritization Matrix

High

Food & Beverage

Textile & Apparel

~60% mfg. GDP

Impact ~65% mfg.

exports Automotive

~60% mfg. workers Electronics

Plastic Goods Process.

Chemical Low

Low

Source: A.T. Kearney, World Bank, BPS

High

Feasibility 25

Food & Beverage

Chemical

Electronics, etc. Industrial

Textile, Apparel Metal Goods Machinery

Wood & Furniture Basic Metal Non-Metal Goods Indust. Trans.

Paper Industry Eqpt. (Auto)

Pharmaceutical Tobacco Rubber &

Coal, Oil & Gas

Refinery Jewelry & Valuable Goods

Top 5 Sectors

Making

Indonesia

Making

Indonesia

Improve upstream agri-sector productivities by technologies e.g. yield mgmt. (IoT/ Big Data)

Empower SME segment by funding and technology support e.g. technology bank, eCommerce

Improve supply chain efficiencies e.g. build better

cold chain network

Enhance modern packaged food productions by product innovations e.g. incentivize R&D

Scale up the industry by leveraging domestic large demand (build economies of scale)

Accelerate export and be the regional #1 F&B

production powerhouse

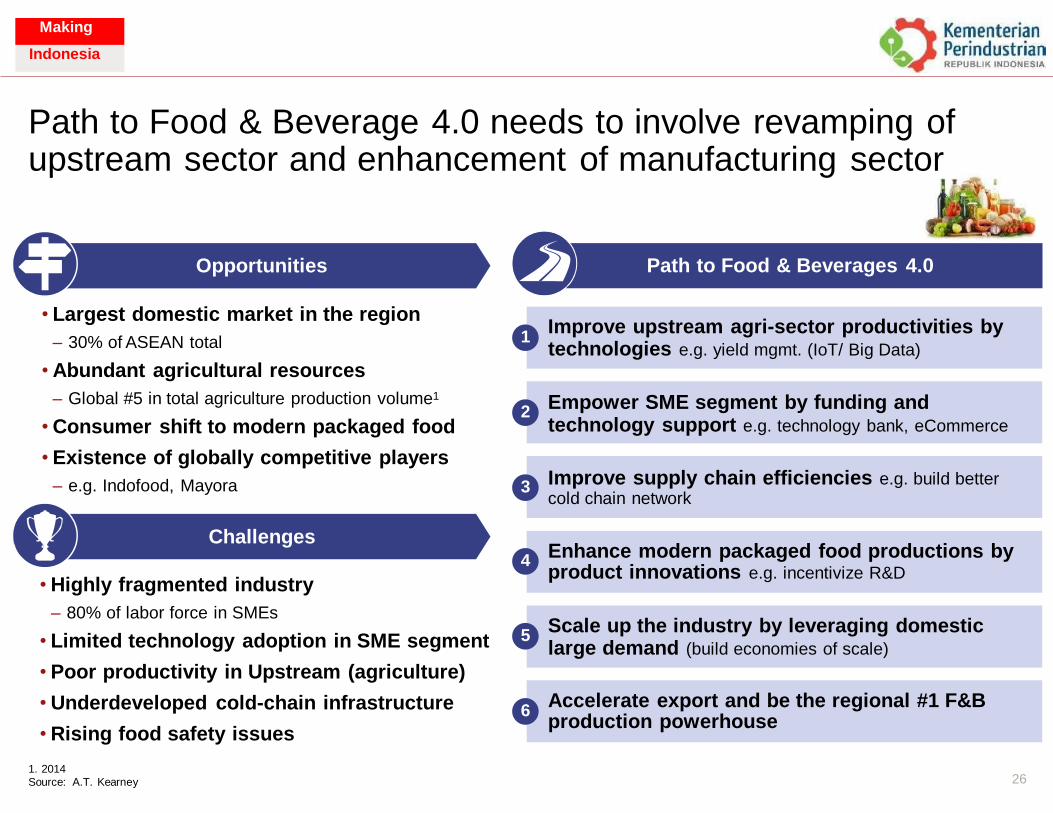

Path to Food & Beverage 4.0 needs to involve revamping of upstream sector and enhancement of manufacturing sector

Opportunities

• Largest domestic market in the region

– 30% of ASEAN total

• Abundant agricultural resources

– Global #5 in total agriculture production volume1

• Consumer shift to modern packaged food

• Existence of globally competitive players

– e.g. Indofood, Mayora

1 technologies e.g. yield mgmt. (IoT/ Big Data)

2

Improve supply chain efficiencies e.g. build better 3

Challenges Enhance modern packaged food productions by

4

• Highly fragmented industry

– 80% of labor force in SMEs

• Limited technology adoption in SME segment

• Poor productivity in Upstream (agriculture)

• Underdeveloped cold-chain infrastructure

• Rising food safety issues

1. 2014 Source: A.T. Kearney

5 large demand (build economies of scale)

Accelerate export and be the regional #1 F&B 6

26

production powerhouse

Scale up the industry by leveraging domestic

product innovations e.g. incentivize R&D

cold chain network

Empower SME segment by funding and technology support e.g. technology bank, eCommerce

Improve upstream agri-sector productivities by

Path to Food & Beverages 4.0

Making

Indonesia

Making

Indonesia

Improve upstream capabilities locally i.e. low-cost

and high-quality chemical fibers / fabrics

Enhance productivity by adopting technologies e.g. sensor-based waste control system, digital proto typing

Build functional clothing design and production capabilities

Scale up and leverage economies of scale to be competitive in the global market

Establish textile industrial clusters and promote vertical integration i.e. better industry zoning

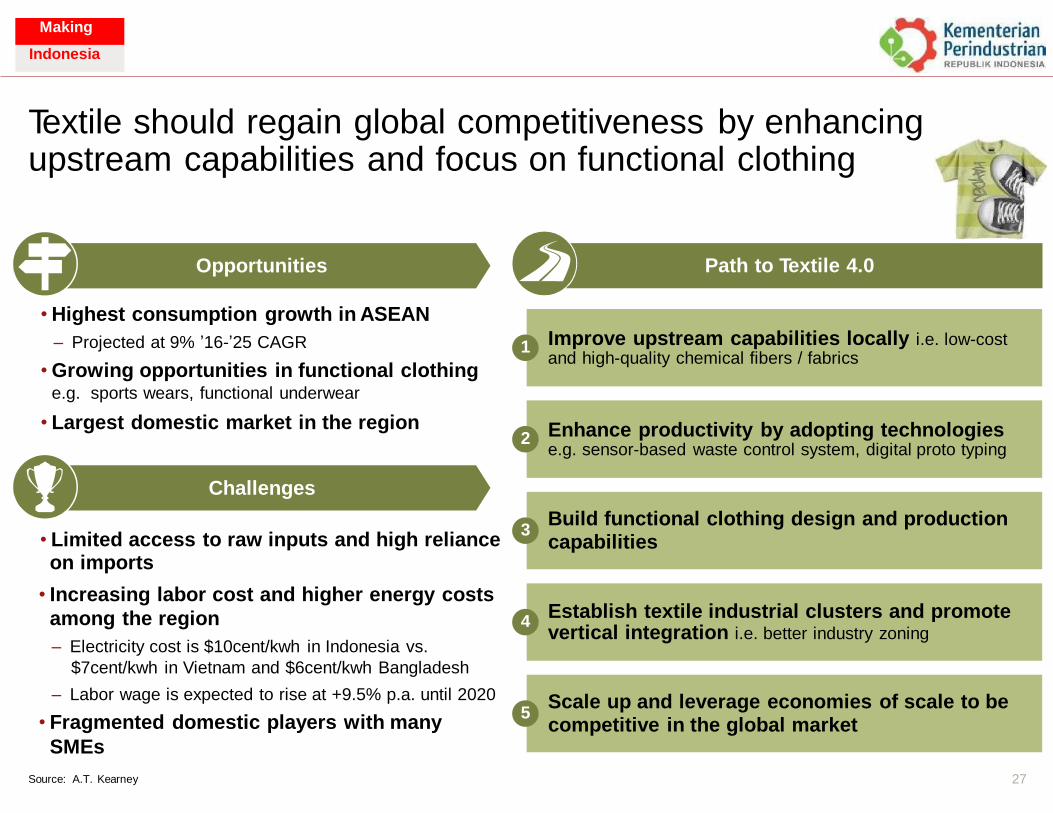

Textile should regain global competitiveness by enhancing upstream capabilities and focus on functional clothing

Opportunities

• Highest consumption growth in ASEAN

– Projected at 9% ’16-’25 CAGR

• Growing opportunities in functional clothing e.g. sports wears, functional underwear

• Largest domestic market in the region

Improve upstream capabilities locally i.e. low-cost 1

Enhance productivity by adopting technologies 2

Challenges

3 • Limited access to raw inputs and high reliance on imports

• Increasing labor cost and higher energy costs

among the region

– Electricity cost is $10cent/kwh in Indonesia vs.

$7cent/kwh in Vietnam and $6cent/kwh Bangladesh

– Labor wage is expected to rise at +9.5% p.a. until 2020

• Fragmented domestic players with many

SMEs

Source: A.T. Kearney

capabilities

Establish textile industrial clusters and promote 4

5 competitive in the global market

27

Scale up and leverage economies of scale to be

vertical integration i.e. better industry zoning

Build functional clothing design and production

e.g. sensor-based waste control system, digital proto typing

and high-quality chemical fibers / fabrics

Path to Textile 4.0

Making

Indonesia

Making

Indonesia

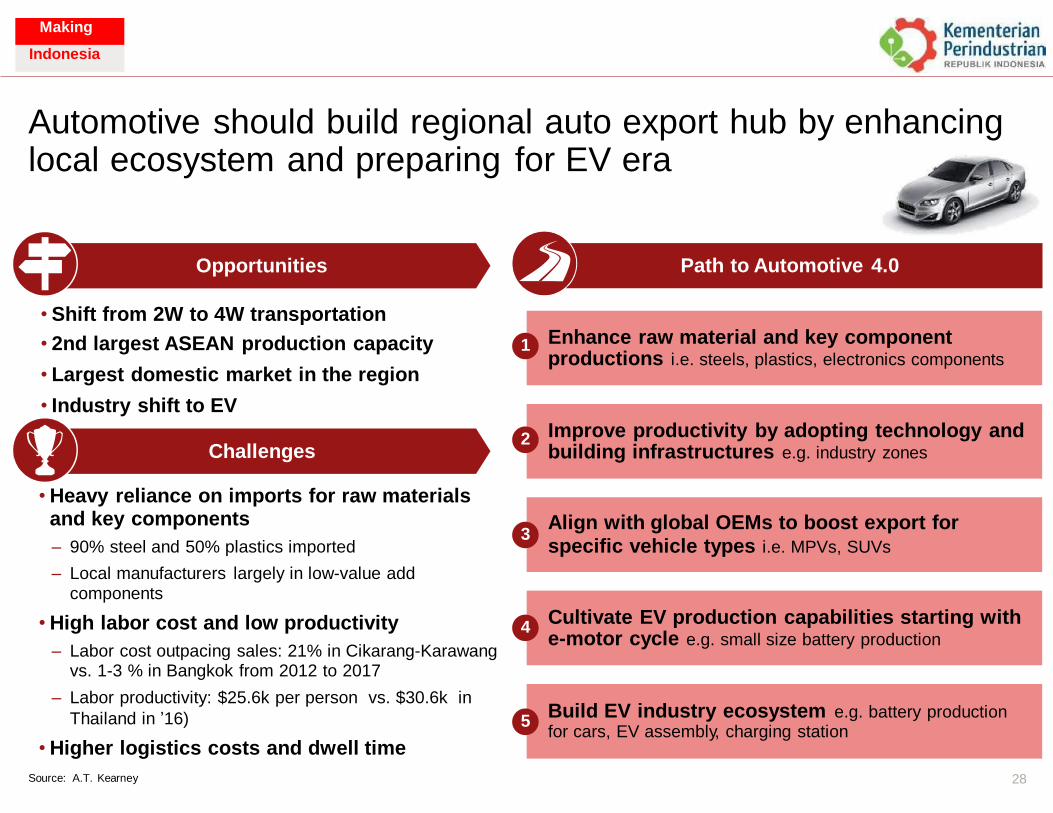

Enhance raw material and key component productions i.e. steels, plastics, electronics components

Improve productivity by adopting technology and building infrastructures e.g. industry zones

Align with global OEMs to boost export for specific vehicle types i.e. MPVs, SUVs

Cultivate EV production capabilities starting with e-motor cycle e.g. small size battery production

Build EV industry ecosystem e.g. battery production

for cars, EV assembly, charging station

Automotive should build regional auto export hub by enhancing local ecosystem and preparing for EV era

Opportunities

• Shift from 2W to 4W transportation

• 2nd largest ASEAN production capacity

• Largest domestic market in the region

• Industry shift to EV

Enhance raw material and key component 1

Improve productivity by adopting technology and 2 Challenges

• Heavy reliance on imports for raw materials and key components

– 90% steel and 50% plastics imported

– Local manufacturers largely in low-value add components

• High labor cost and low productivity

– Labor cost outpacing sales: 21% in Cikarang-Karawang vs. 1-3 % in Bangkok from 2012 to 2017

– Labor productivity: $25.6k per person vs. $30.6k in

Thailand in ’16)

• Higher logistics costs and dwell time

Source: A.T. Kearney

3 specific vehicle types i.e. MPVs, SUVs

Cultivate EV production capabilities starting with 4

5 for cars, EV assembly, charging station

28

Build EV industry ecosystem e.g. battery production

e-motor cycle e.g. small size battery production

Align with global OEMs to boost export for

building infrastructures e.g. industry zones

productions i.e. steels, plastics, electronics components

Path to Automotive 4.0

Making

Indonesia

Making

Indonesia

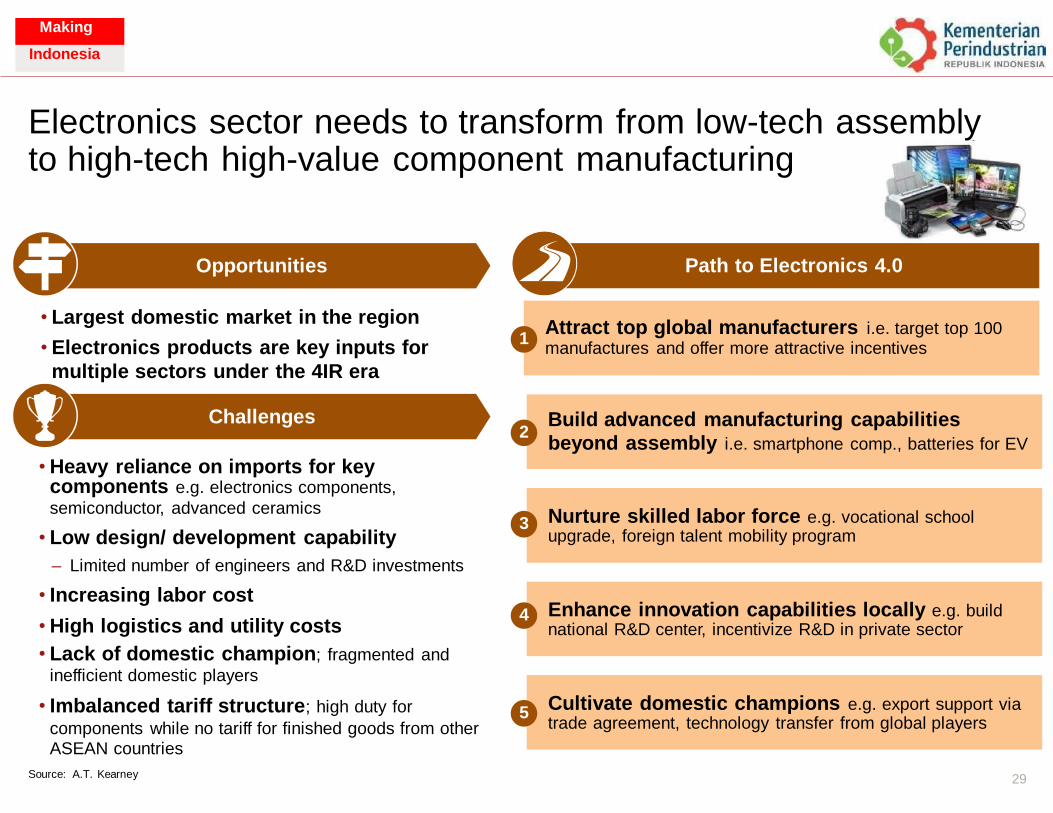

Build advanced manufacturing capabilities beyond assembly i.e. smartphone comp., batteries for EV

Attract top global manufacturers i.e. target top 100

manufactures and offer more attractive incentives

Nurture skilled labor force e.g. vocational school

upgrade, foreign talent mobility program

Cultivate domestic champions e.g. export support via

trade agreement, technology transfer from global players

Enhance innovation capabilities locally e.g. build

national R&D center, incentivize R&D in private sector

Electronics sector needs to transform from low-tech assembly to high-tech high-value component manufacturing

Opportunities

• Largest domestic market in the region

• Electronics products are key inputs for

multiple sectors under the 4IR era

1 manufactures and offer more attractive incentives

Challenges 2

beyond assembly i.e. smartphone comp., batteries for EV

• Heavy reliance on imports for key components e.g. electronics components,

semiconductor, advanced ceramics

• Low design/ development capability

– Limited number of engineers and R&D investments

• Increasing labor cost

• High logistics and utility costs

• Lack of domestic champion; fragmented and

inefficient domestic players

• Imbalanced tariff structure; high duty for

components while no tariff for finished goods from other ASEAN countries

Source: A.T. Kearney

Nurture skilled labor force e.g. vocational school 3

Enhance innovation capabilities locally e.g. build 4

Cultivate domestic champions e.g. export support via 5

29

trade agreement, technology transfer from global players

national R&D center, incentivize R&D in private sector

upgrade, foreign talent mobility program

Build advanced manufacturing capabilities

Attract top global manufacturers i.e. target top 100

Path to Electronics 4.0

Making

Indonesia

Making

Indonesia

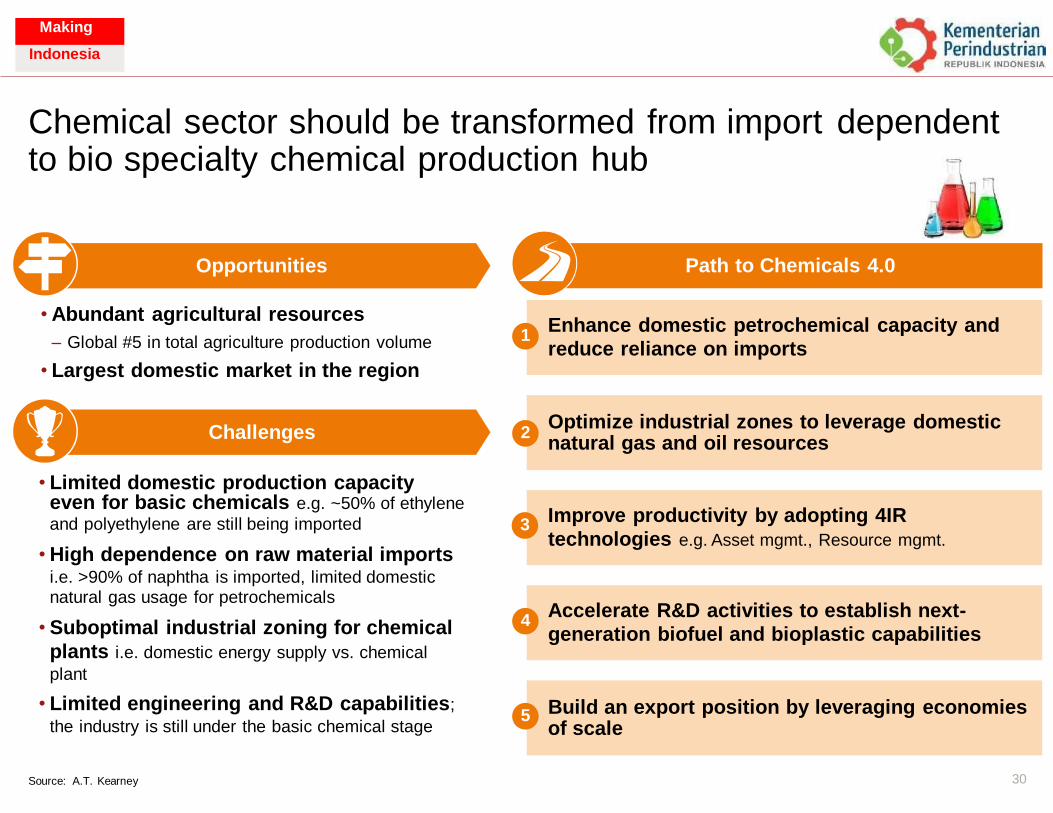

Enhance domestic petrochemical capacity and reduce reliance on imports

Optimize industrial zones to leverage domestic natural gas and oil resources

Accelerate R&D activities to establish next- generation biofuel and bioplastic capabilities

Improve productivity by adopting 4IR

technologies e.g. Asset mgmt., Resource mgmt.

Build an export position by leveraging economies of scale

Chemical sector should be transformed from import to bio specialty chemical production hub

dependent

Opportunities

• Abundant agricultural resources

– Global #5 in total agriculture production volume

• Largest domestic market in the region

1 reduce reliance on imports

Optimize industrial zones to leverage domestic Challenges 2

• Limited domestic production capacity even for basic chemicals e.g. ~50% of ethylene

and polyethylene are still being imported

• High dependence on raw material imports i.e. >90% of naphtha is imported, limited domestic natural gas usage for petrochemicals

• Suboptimal industrial zoning for chemical

plants i.e. domestic energy supply vs. chemical

plant

• Limited engineering and R&D capabilities;

the industry is still under the basic chemical stage

3 technologies e.g. Asset mgmt., Resource mgmt.

4 generation biofuel and bioplastic capabilities

Build an export position by leveraging economies 5

30 Source: A.T. Kearney

of scale

Accelerate R&D activities to establish next-

Improve productivity by adopting 4IR

natural gas and oil resources

Enhance domestic petrochemical capacity and

Path to Chemicals 4.0

Making

Indonesia

Making

Indonesia

31

10 NationalPriorities for Indon

Making esia 4.0”

Making

Indonesia

Making

Indonesia

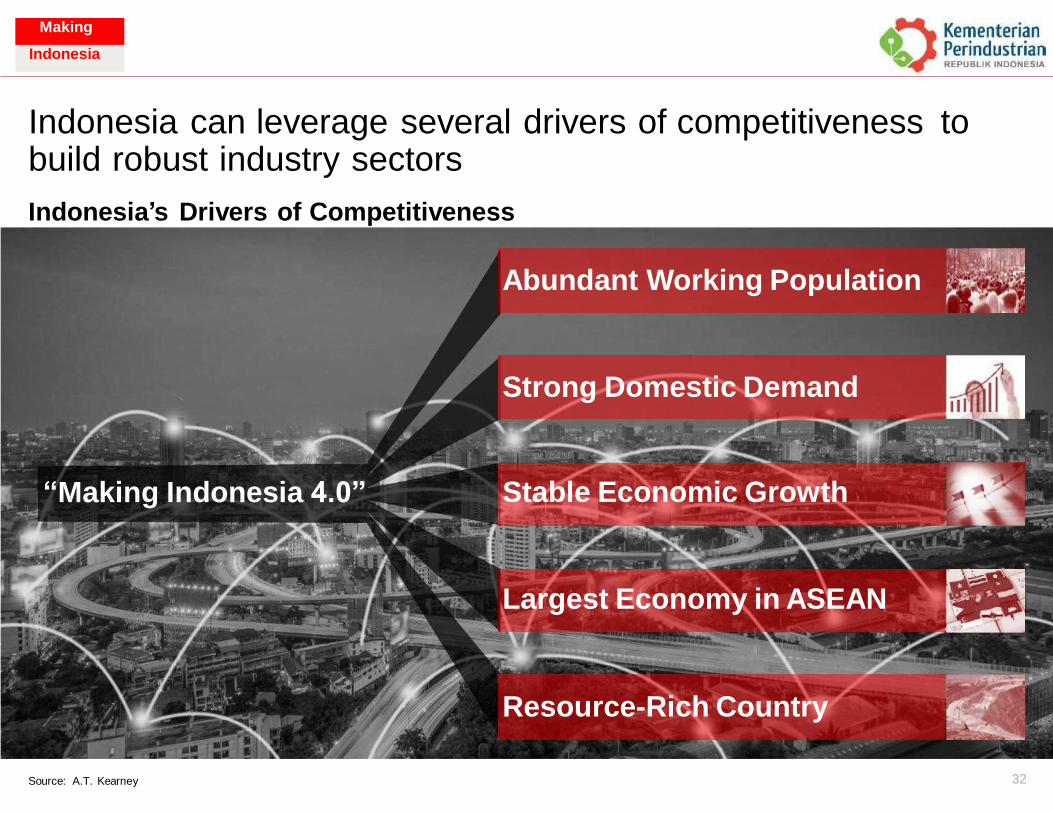

Indonesia can leverage several drivers of competitiveness build robust industry sectors

to

Indonesia’s Drivers of Competitiveness

Abundant Working Population

Strong Domestic Demand

“Making Indonesia 4.0” Stable Economic Growth

Largest Economy in ASEAN

Resource-Rich Country

32 Source: A.T. Kearney

Making

Indonesia

Making

Indonesia

All industry sectors in Indonesia are facing 10 common issues

10 Key Challenges Across the Industries (1/2)

– >50% of petrochemicals, 74% of basic metals

oil gas vs. petrochemicals • Underdeveloped and underutilized economic zones

developed economies

– Exports need to meet requirements e.g. EUROx

micro enterprises with low productivities

– Mobile: currently adopting 4G (not ready for 5G)

33 Source: IHS Markit, BPS, Desk Research, A.T. Kearney

• 62% of workers in Indonesia are working at small or

• Sustainability trends are no longer only for

– Shift to business opportunities e.g. solar, biomaterials

• Absence of comprehensive industry zoning plan e.g.

e.g. Batam, Karawang, Bekasi and Central Java

Underdeveloped • Raw materials and critical parts are highly import

Up-midstream Industry

1 dependent e.g.

– All the critical parts for electronics and automotive

Underleveraged Geographical Potential

2

Inevitable Global Sustainability Trends

3

Left-Behind SMEs

4

Must-Have Digital Infrastructure

5 • Digital platforms are still underdeveloped

– Fiber: average speed is <10Mbps (not 1Gbps)

– Cloud: limited cloud infrastructures

Making

Indonesia

Making

Indonesia

All industry sectors in Indonesia are facing 10 common issues

10 Key Challenges Across the Industries (2/2)

growth during ’13-’16) although Indonesia is suffering

technologies

7

% of GDP

8

9

by multiple organizations; e.g. upstream by MOE, midstream by MOI and trade by MOT, central

34 Source: BKPM, Desk Research, A.T. Kearney

• Currently no comprehensive incentives for 4th

Industrial Revolution technology adoption e.g. tax exemptions, subsidies, funding support etc.

• Very limited R&D spending as a country; only 0.1-0.3

• No strong government led R&D/innovation centers

as well as private sector ’s

• Indonesia has 4th largest working population in the world, however, very limited trained talents; e.g. government education spending is only $114 per capita

Limitation of • Recently, FDI inflow to Indonesia is flattening (0%

Domestic Funding and Technologies

6

from limited source of funding and access to new

Abundant but under trained people

Absence of Innovation Centers

Inertia to stay in status quo

Regulation & Policy

10 • Overcomplicated regulations and policies, handled

Roadblocks

government vs. local government

Making

Indonesia

Making

Indonesia

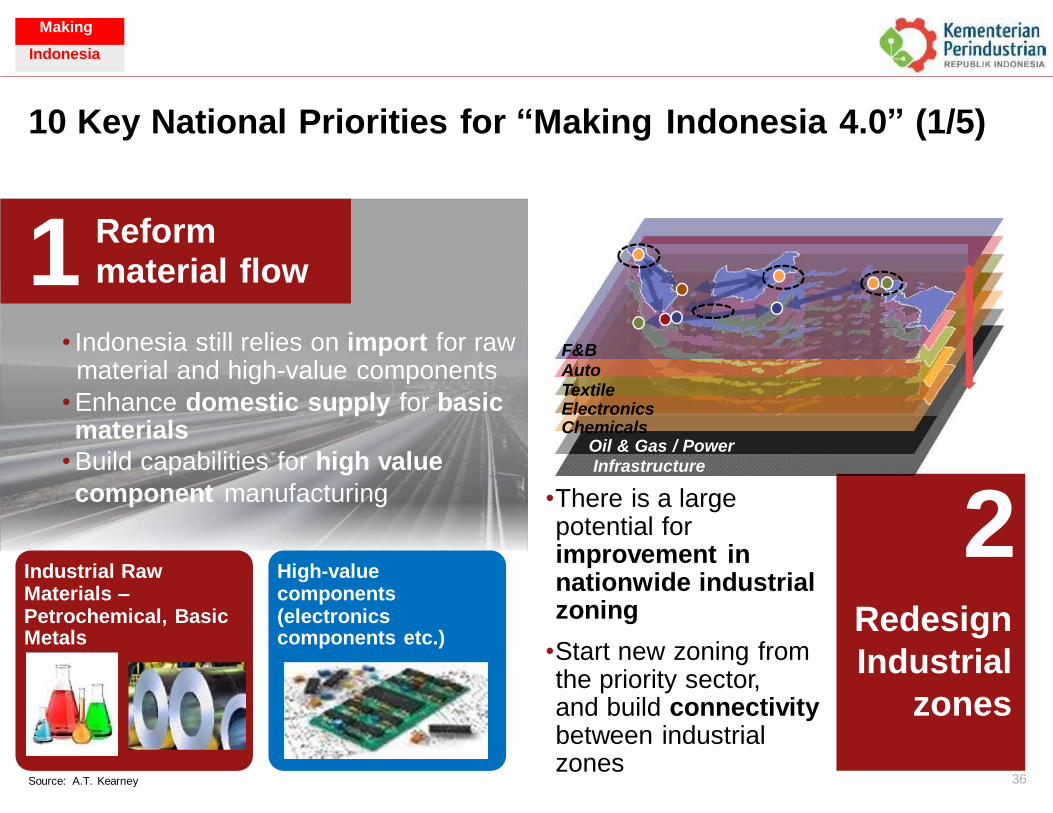

Reform Material Flow

Redesign Industrial Zones

Embrace sustainability

Empower SMEs

Build Nationwide Digital Infrastructure

Attract Foreign Investments

Upgrade Human Capital

Establish Innovation Ecosystem

Incentivize Technology Investment

Reoptimize Regulations & Policies

Indonesia has set 10 National Priorities for “Making Indonesia 4.0”

10 National Priorities

• Enhance domestic upstream material production; e.g. 50% of petrochemical is imported

• Engage top global manufacturers with attractive offer and accelerate technology transfer

•

•

Redesign education curriculum under 4IR era

Create professional talent mobility program • Build a single nationwide industry zoning

roadmap; resolve zoning inconsistency challenges

• Grab opportunities under global sustainability trend; e.g. EV, biofuel, renewables

• Enhance R&D centers by government, private sector and universities

Empower 3.7 million SMEs1 by technologies; e.g. build SME e-commerce, technology bank

• • Introduce tax exemption/subsidies for technology adoption and support funding

• Advance network and digital platform; e.g. 4G to 5G, Fiber speed 1Gbps, Data center and Cloud

• Build more coherent policies/regulations by cross-ministry collaborations

1. Including micro enterprises 35 Source: Ministry of Industry, A.T. Kearney

5 Build Nationwide Digital Infrastructure 10 Reoptimize Regulations & Policies

4 Empower SMEs 9 Incentivize Technology Investment

3 Embrace sustainability 8 Establish Innovation Ecosystem

2 Redesign Industrial Zones 7 Upgrade Human Capital

1 Reform Material Flow 6 Attract Foreign Investments

Making

Indonesia

Making

Indonesia

10 Key National Priorities for “Making Indonesia 4.0” (1/5)

1 Reform material flow

• Indonesia still relies on import for raw material and high-value components

• Enhance domestic supply for basic materials

• Build capabilities for high value

F&B Auto Textile Electronics Chemicals

Oil & Gas / Power Infrastructure

•There is a large potential for improvement in nationwide industrial zoning

•Start new zoning from the priority sector, and build connectivity between industrial zones

component manufacturing

Industrial Raw Materials – Petrochemical, Basic Metals

High-value components (electronics components etc.)

36 Source: A.T. Kearney

2 Redesign

Industrial

zones

Making

Indonesia

Making

Indonesia

Low Carbon Emission Vehicle

EV and their components

Electric and fuel cell motorcycles

Biofuel- and gas-powered vehicles

Encourage bioplastic uses

Increase min. biofuel content in gasoline

10 Key National Priorities for “Making Indonesia 4.0” (2/5)

3 Accommodate

2017 2035

Sustainability Plan Low Carbon Emission Vehicle

Electric and fuel cell motorcycles • There is sustainability challenge through the improvement in Euro emission standard and recent palm oil ban

• Identify green growth opportunities

EV and their components

Biofuel- and gas-powered vehicles

Increase min. biofuel content in gasoline

and promote conducive environment Encourage bioplastic uses for green investment

Micro

4 Empower SMEs

Nearly 70% of Indonesian

labor force works for micro, small

and medium

Large

Build nationwide e- commerce platform, build technology banks, develop local small business foundations

32%

46%

6% Medium enterprises in 2015 Small

37 Source: A.T. Kearney

5%

Making

Indonesia

Making

Indonesia

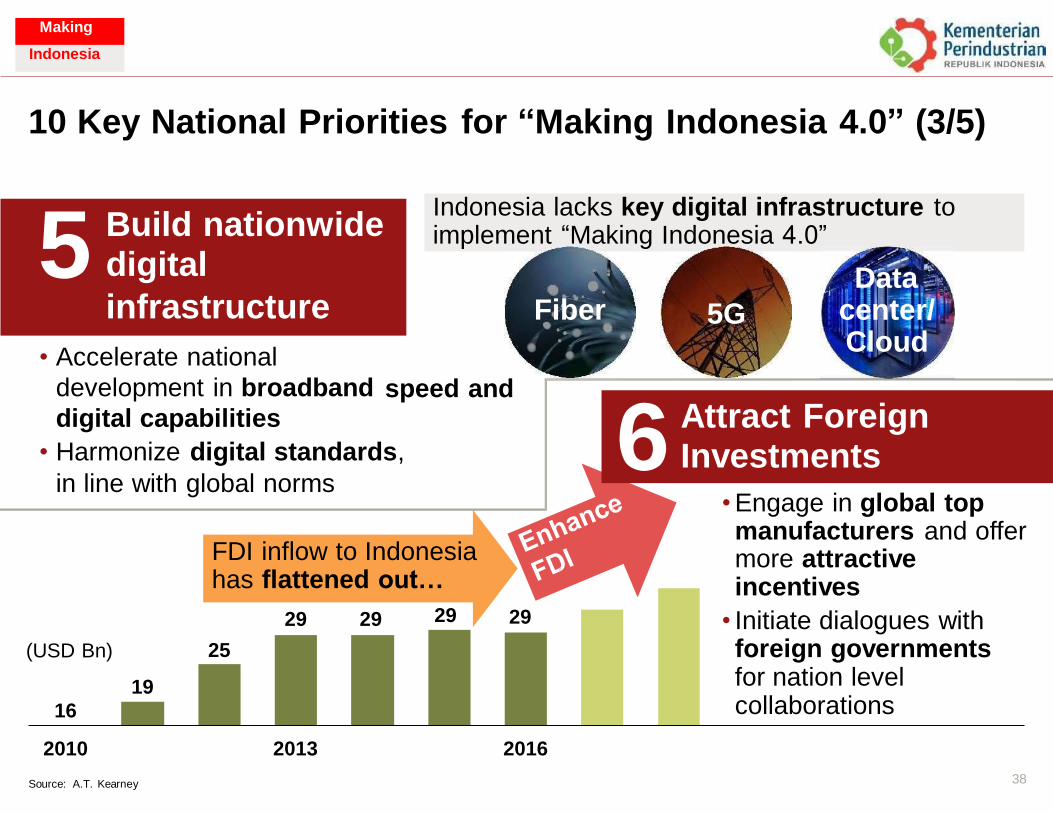

Indonesia lacks key digital infrastructure to implement “Making Indonesia 4.0”

10 Key National Priorities for “Making Indonesia 4.0” (3/5)

5 Build nationwide digital

infrastructure Data

center/ Cloud

Fiber 5G

• Accelerate national

development in broadband

digital capabilities speed and

6 Attract Foreign Investments • Harmonize digital standards,

in line with global norms • Engage in global top manufacturers and offer more attractive incentives

FDI has

inflow to Indonesia flattened out…

(USD Bn) 25

2010

Source: A.T. Kearney

2013 2016

38

• Initiate dialogues with foreign governments for nation level collaborations

29 29 29 29

19

16

Indonesia lacks key digital infrastructure to implement “Making Indonesia 4.0”

Making

Indonesia

Making

Indonesia

Indonesia is facing talent

development challenges

Indonesia lacks strong gov./private

R&D/innovation centers &D/innovation centers

10 Key National Priorities for “Making Indonesia 4.0” (4/5)

8 Establish innovation ecosystem

Tertiary school enrollment

78%

27% 24% 11%

2015 1990 2000 2005 2015 Optimize regulations

Develop a national

innovation

center

blueprint

7 Upgrade human

Govern- ment

Develop capital center Industries Indonesian

R&D ecosystem

• Reform education curriculums adopting STEAM (Science,

by

Technology, Engineering, Art Math) education

and Univer- sities

Accelerate cross-sector

collaborations Initiate a pilot project

• Upgrade vocational schools

• Leverage foreign talents

39 Source: A.T. Kearney

37%

7

Indonesia lacks strong gov./private

Indonesia is facing talent

development challenges

Making

Indonesia

Making

Indonesia

Goods from Indonesia

Goods produced in ASEAN

10 Key National Priorities for “Making Indonesia 4.0” (5/5)

9 innovation Incentivize

High costs (energy, labor, parts tariffs, …)

locally produced product losing

competitiveness

Indonesian market Countries are aggressively incentivizing technology adoption

• €400Mn funding for in cyber-physical systems, IoT, and other 4IR tech research

• Government subsidies for select industries, esp. robotics and New Energy Vehicles

• Government commitment of SGD 3.2 Bn

over 2016-2020

No tariff for finished goods

Indonesia needs to simplify Need tighter coordination policies by coordinating

across ministries

10 Indonesia will need to commit to

Reoptimize incentives

Tax

across industries

Funding Subsidies

incentives

• Tax holiday

• (Import) Tax reduction

support

• Guarantees

• Capital injection

• Govt. assistance

• Grants

40 Source: A.T. Kearney

Industry

Regulations

&

Policies

Goods produced in ASEAN

Goods from Indonesia

Making

Indonesia

Making

Indonesia

ions

41

Economic Benefit and Job Creat

Making

Indonesia

Making

Indonesia

GDP Growth

Job Creation Manufacturing GDP

Contribution

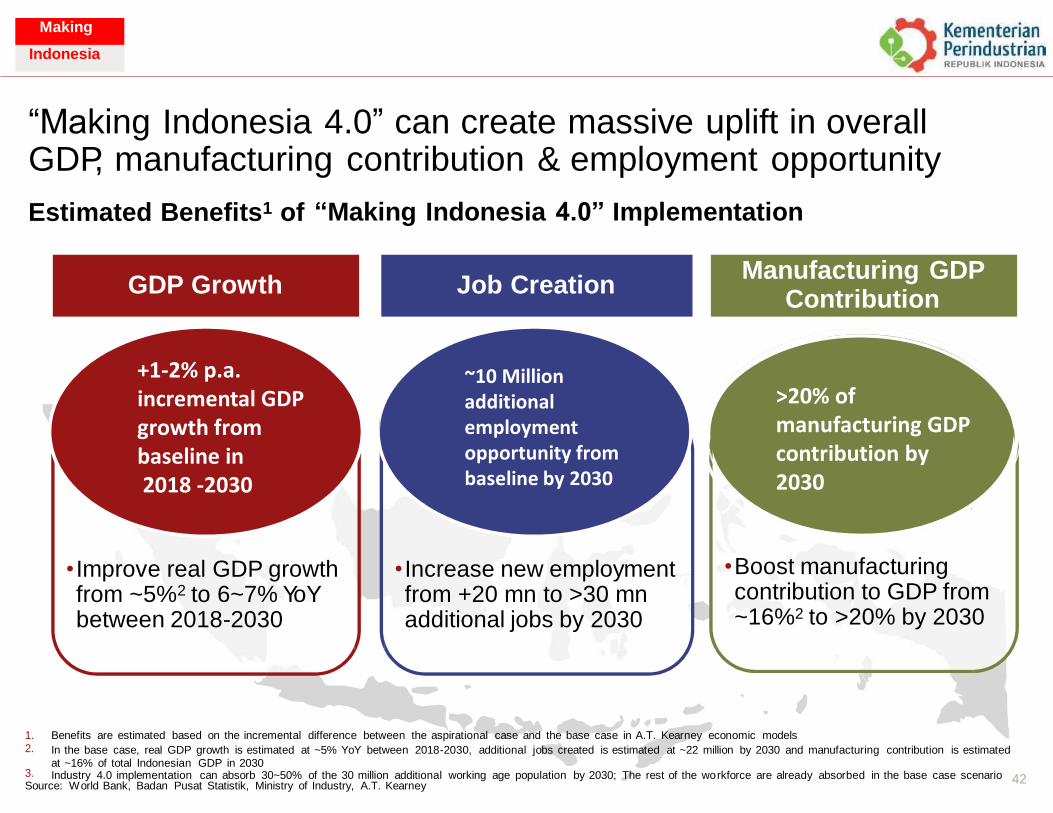

“Making Indonesia 4.0” can create massive uplift in overall GDP, manufacturing contribution & employment opportunity

Estimated Benefits1 of “Making Indonesia 4.0” Implementation

Contribution

• Boost manufacturing contribution to GDP from ~16%2 to >20% by 2030

• Improve real GDP growth from ~5%2 to 6~7% YoY between 2018-2030

• Increase new employment from +20 mn to >30 mn additional jobs by 2030

1. 2.

Benefits are estimated based on the incremental difference between the aspirational case and the base case in A.T. Kearney economic models

In the base case, real GDP growth is estimated at ~5% YoY between 2018-2030, additional jobs created is estimated at ~22 million by 2030 and manufacturing contribution is estimated at ~16% of total Indonesian GDP in 2030 Industry 4.0 implementation can absorb 30~50% of the 30 million additional working age population by 2030; The rest of the wo rkforce are already absorbed in the base case scenario 3.

42 Source: World Bank, Badan Pusat Statistik, Ministry of Industry, A.T. Kearney

GDP Growth

Job Creation Manufacturing GDP

Making

Indonesia

+1-2% p.a. incremental GDP growth from baseline in 2018 -2030

~10 Million additional employment opportunity from baseline by 2030

>20% of manufacturing GDP contribution by 2030

Making

Indonesia

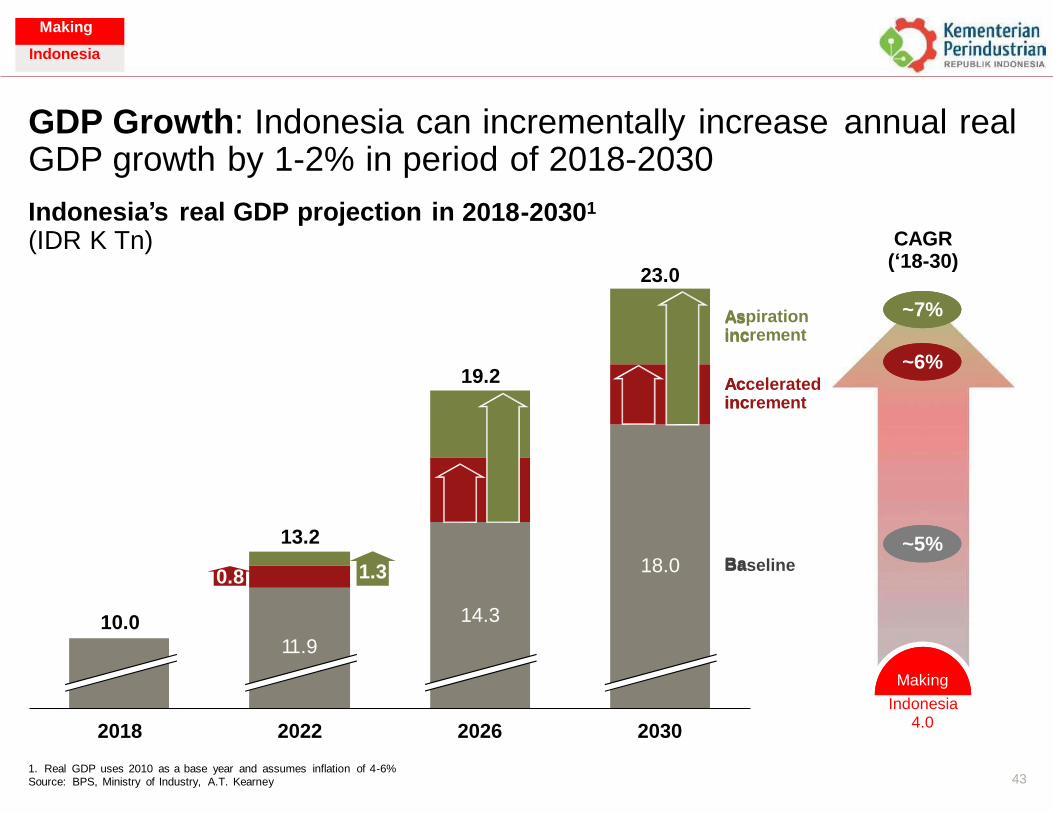

GDP Growth: Indonesia can incrementally increase GDP growth by 1-2% in period of 2018-2030

annual real

2018-20301 Indonesia’s real GDP projection in (IDR K Tn) CAGR

(‘18-30) 23.0

~7% Aspiration increment

~6% Accelerated increment

~5% Baseline

Making

Indonesia 4.0

2018 2022 2026 2030

1. Real GDP uses 2010 as a base year and assumes inflation of 4-6%

Source: BPS, Ministry of Industry, A.T. Kearney 43

19.2

As inc

Ac inc

Ba

13.2

18.0

14.3

0.8

10.0

1.3

11.9

Making

Indonesia

Making

Indonesia

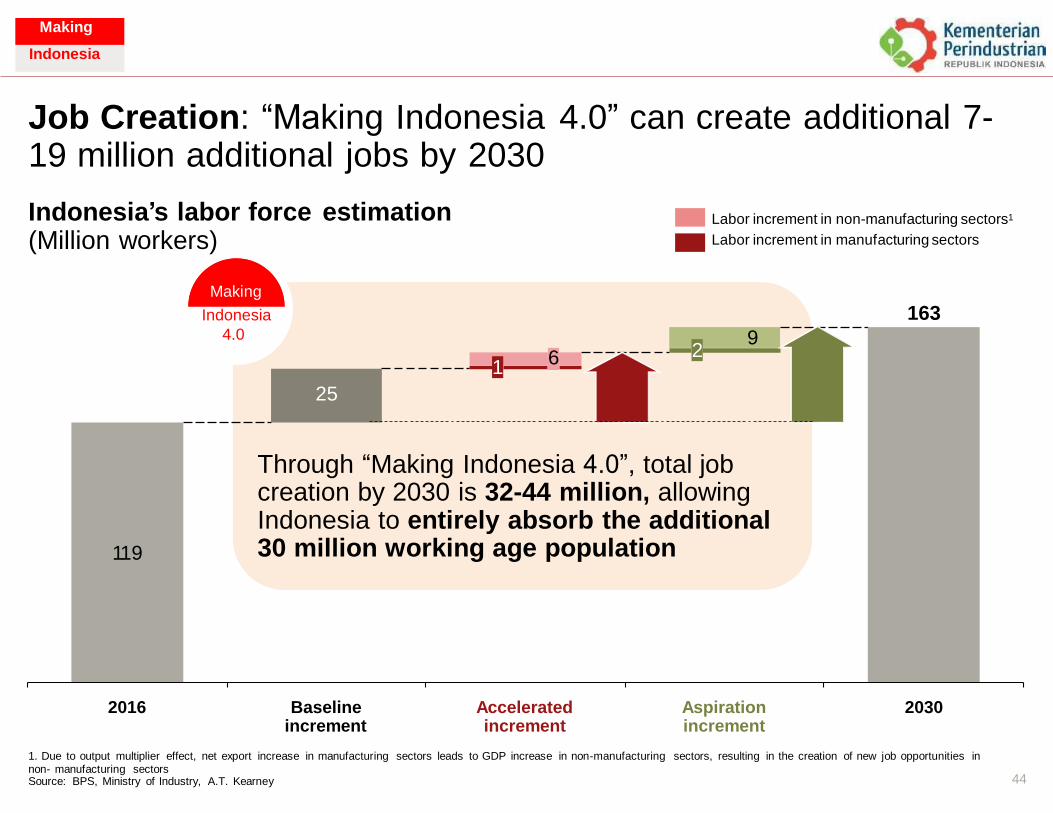

Job Creation: “Making Indonesia 4.0” can create additional 7- 19 million additional jobs by 2030

Indonesia’s labor force estimation Labor increment in non-manufacturing sectors1

Labor increment in manufacturing sectors (Million workers)

Making

Indonesia 163

9 2

1

2016 Baseline increment

Accelerated increment

Aspiration increment

2030

1. Due to output multiplier effect, net export increase in manufacturing sectors leads to GDP increase in non-manufacturing sectors, resulting in the creation of new job opportunities in non- manufacturing sectors Source: BPS, Ministry of Industry, A.T. Kearney 44

4.0

6

25

119

Through “Making Indonesia 4.0”, total job creation by 2030 is 32-44 million, allowing Indonesia to entirely absorb the additional 30 million working age population

Making

Indonesia

Making

Indonesia

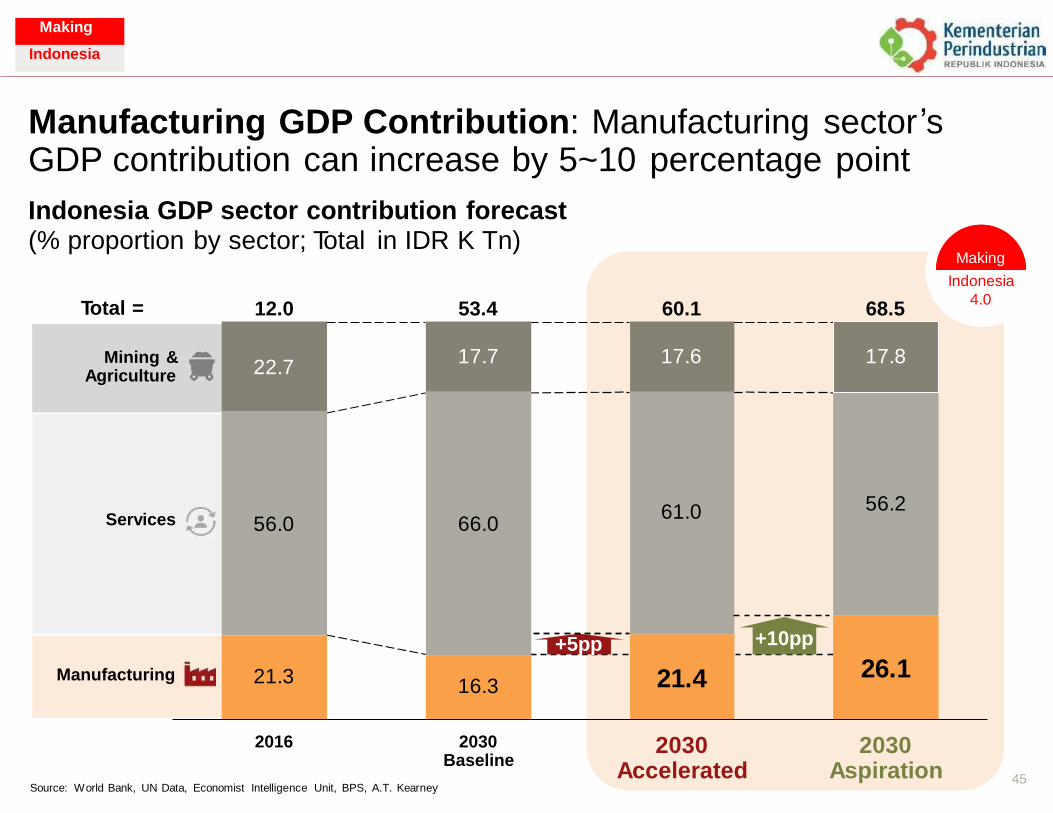

Manufacturing GDP Contribution: Manufacturing sector ’s GDP contribution can increase by 5~10

Indonesia GDP sector contribution forecast

percentage point

(% proportion by sector; Total in IDR K Tn) Making

Indonesia

4.0 Total = 12.0 53.4 60.1 68.5

2016 2030 Baseline

2030 Accelerated

2030 Aspiration 45

Source: World Bank, UN Data, Economist Intelligence Unit, BPS, A.T. Kearney

Mining & Agriculture

22.7

17.7

17.6

17.8

66.0

61.0

56.2

Services

56.0

+10pp

26.1

Manufacturing

21.3

+5pp

21.4

16.3

Making

Indonesia

Making

Indonesia

46

Next Steps

Making

Indonesia

Making

Indonesia

Overall

Vertical initiatives

Horizontal initiatives

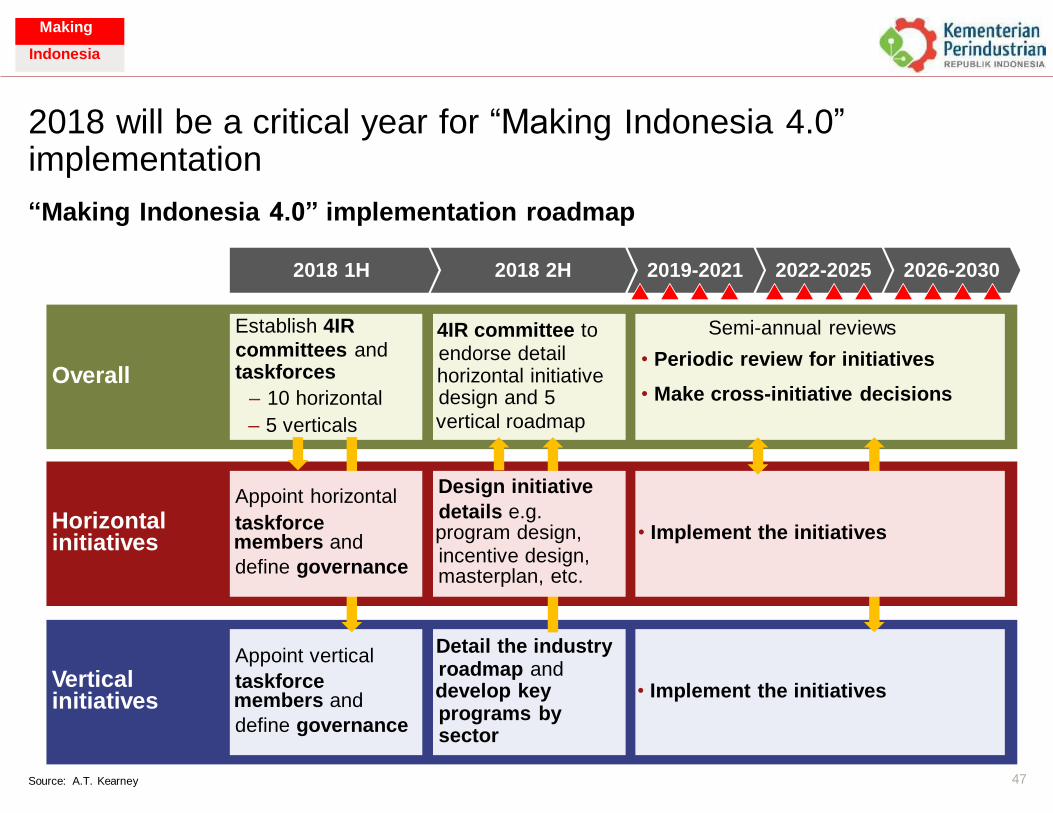

2018 will be a critical year for “Making Indonesia 4.0” implementation

“Making Indonesia 4.0” implementation roadmap

2018 1H 2018 2H 2019-2021 2022-2025 2026-2030

Horizontal

Vertical

47 Source: A.T. Kearney

roadmap and

programs by

taskforce

define governance

Appoint vertical Detail the industry

initiatives members and develop key • Implement the initiatives

sector

details e.g.

incentive design,

taskforce

define governance

Appoint horizontal Design initiative

initiatives members and program design, • Implement the initiatives

masterplan, etc.

• Periodic review for initiatives

• Make cross-initiative decisions

endorse detail

design and 5

committees and

– 10 horizontal

Establish 4IR 4IR committee to Semi-annual reviews

Overall taskforces horizontal initiative

– 5 verticals vertical roadmap

Making

Indonesia

Making

Indonesia

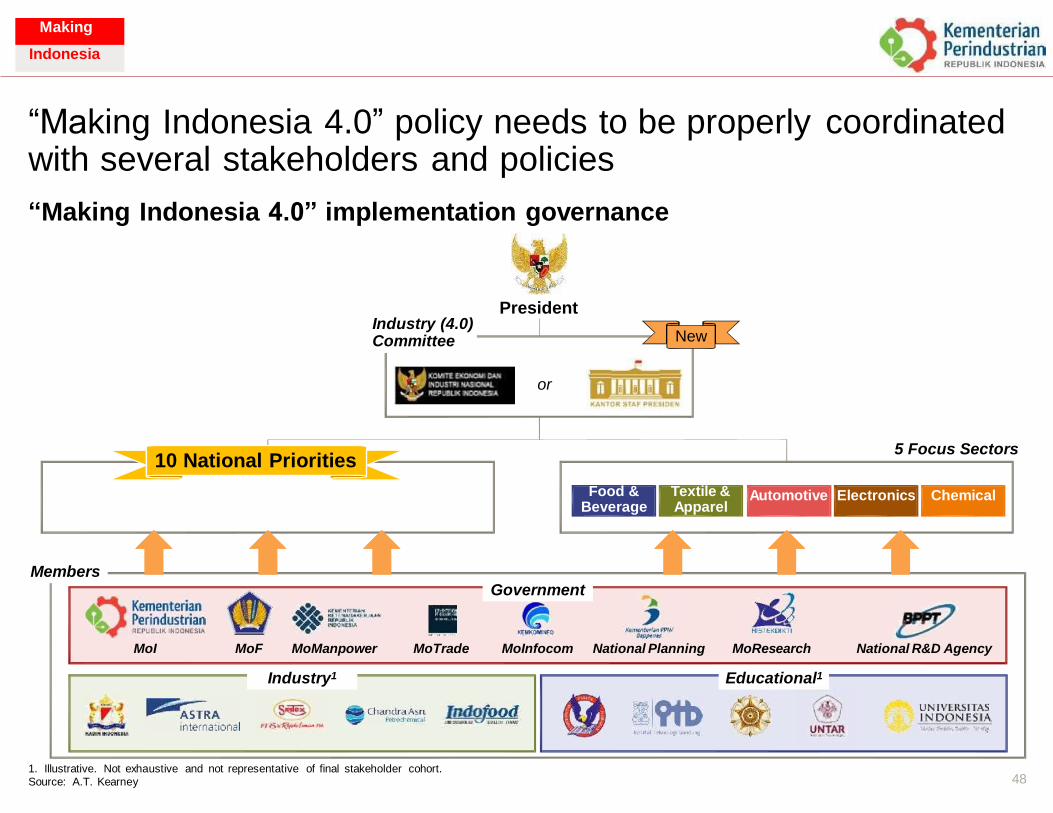

“Making Indonesia 4.0” policy needs to be properly with several stakeholders and policies

coordinated

“Making Indonesia 4.0” implementation governance

President Industry (4.0) Committee New

or

5 Focus Sectors 10 National Priorities

1 2 3 4 5 6 7 8 9 10

Members

1. Illustrative. Not exhaustive and not representative of final stakeholder cohort.

Source: A.T. Kearney 48

Industry1 Educational1

Government

MoI MoF MoManpower MoTrade MoInfocom National Planning MoResearch National R&D Agency

Food & Beverage

Textile & Apparel

Automotive Electronics Chemical

Making

Indonesia

Making

Indonesia

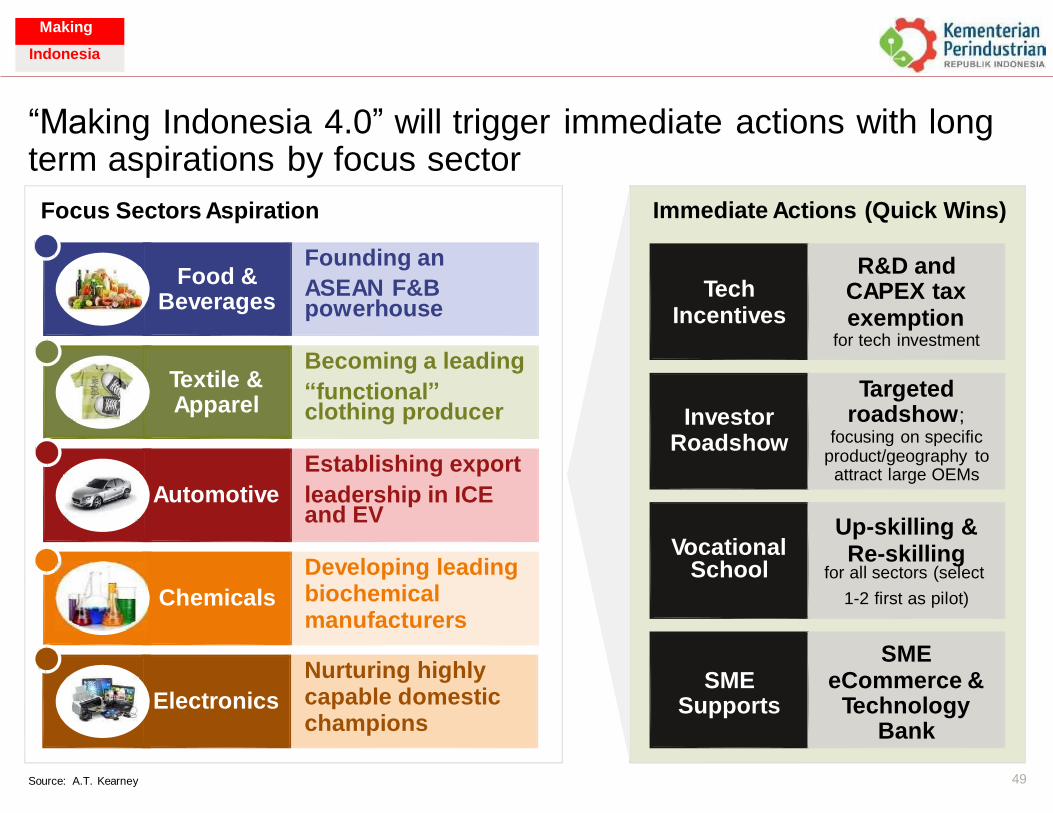

“Making Indonesia 4.0” will trigger term aspirations by focus sector

immediate actions with long

Focus Sectors Aspiration

ASEAN F&B

“functional”

leadership in ICE

49 Source: A.T. Kearney

Electronics

Nurturing highly capable domestic champions

Chemicals

Developing leading biochemical manufacturers

Vocational

Re-skilling

Automotive

Establishing export

and EV

Roadshow

focusing on specific

Textile & Apparel

Becoming a leading

clothing producer

Food & Beverages

Founding an

powerhouse

Immediate Actions (Quick Wins)

R&D and Tech CAPEX tax

Incentives exemption for tech investment

Targeted

Investor roadshow;

product/geography to attract large OEMs

Up-skilling &

School for all sectors (select

1-2 first as pilot)

SME SME eCommerce &

Supports Technology Bank

Making

Indonesia

Making

Indonesia

APPENDIX

50

Making

Indonesia

Making

Indonesia

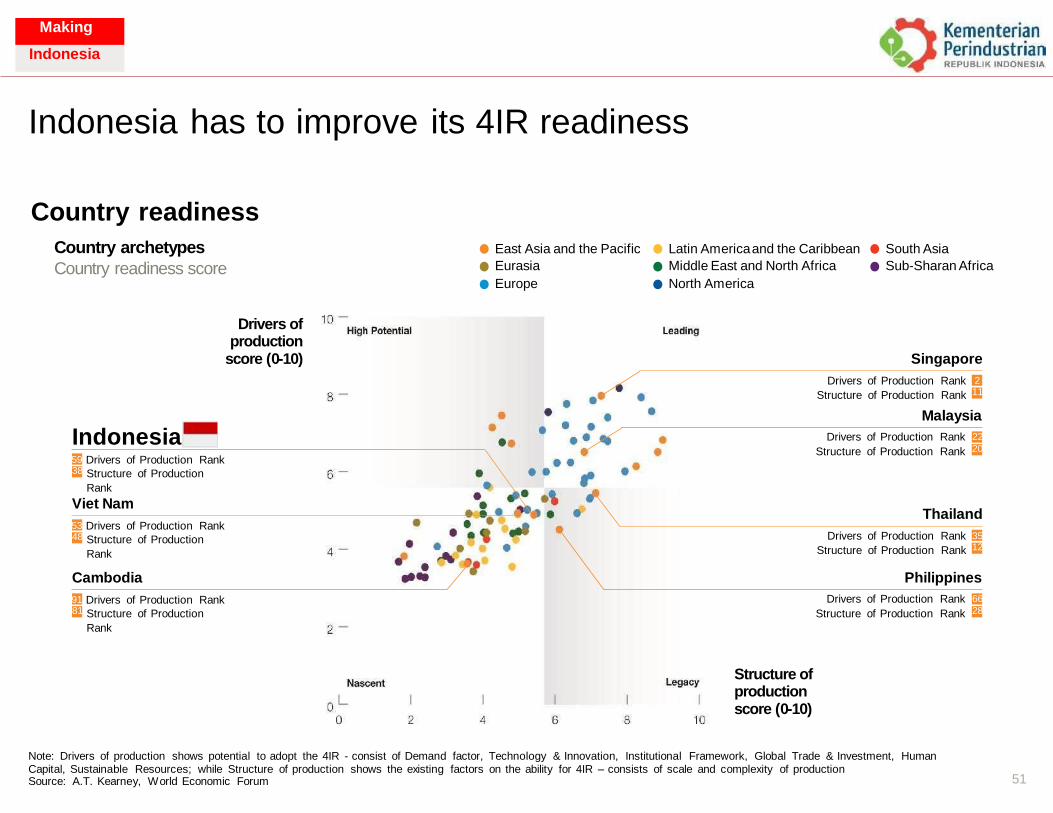

Indonesia has to improve its 4IR readiness

Country readiness

Country archetypes

Country readiness score

East Asia and the Pacific

Eurasia

Europe

Latin America and the Caribbean

Middle East and North Africa

North America

South Asia

Sub-Sharan Africa

Drivers of production

score (0-10) Singapore

Drivers of Production Rank

Structure of Production Rank

2

Malaysia

Indonesia Drivers of Production Rank 22 Structure of Production Rank

59 Drivers of Production Rank

Structure of Production

Rank

Viet Nam Thailand

53 Drivers of Production Rank Drivers of Production Rank

Structure of Production Rank Structure of Production

Rank

Cambodia Philippines

91 Drivers of Production Rank Drivers of Production Rank 66 Structure of Production

Rank

Structure of Production Rank

Structure of production score (0-10)

Note: Drivers of production shows potential to adopt the 4IR - consist of Demand factor, Technology & Innovation, Institutional Framework, Global Trade & Investment, Human Capital, Sustainable Resources; while Structure of production shows the existing factors on the ability for 4IR – consists of scale and complexity of production Source: A.T. Kearney, World Economic Forum 51

28 81

35 12

48

38

20

11

Making

Indonesia

Making

Indonesia

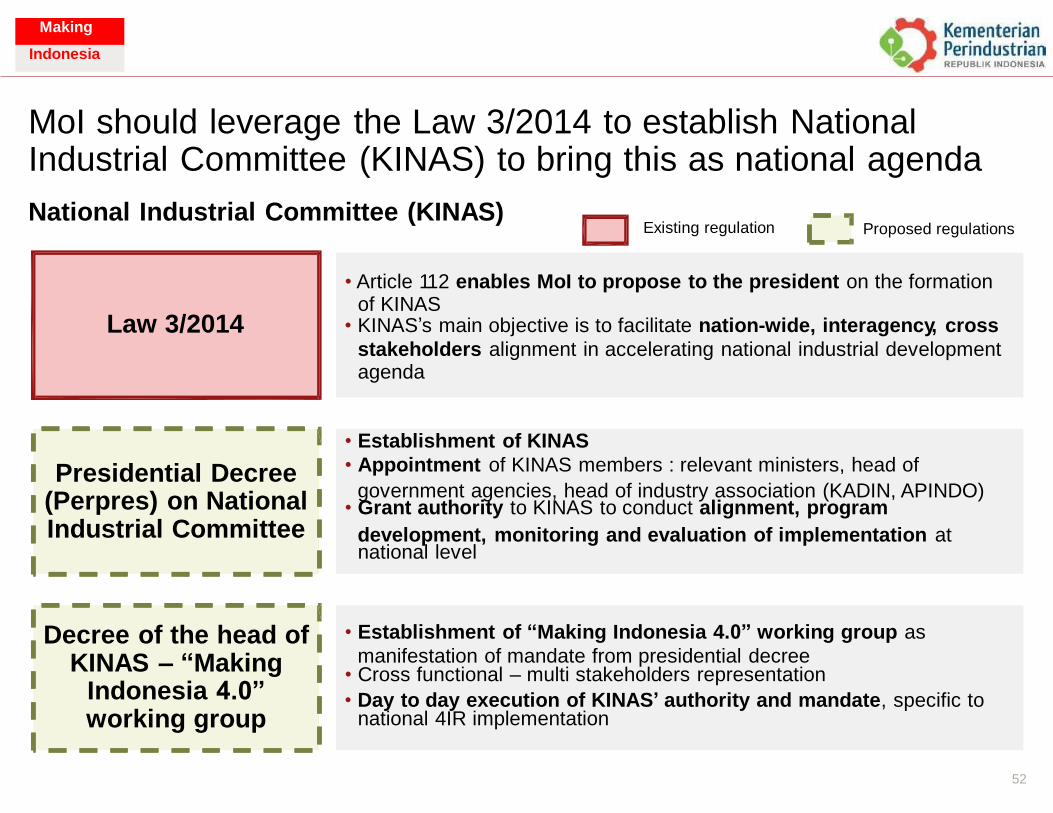

MoI should leverage the Law 3/2014 to establish National Industrial Committee (KINAS) to bring this as national agenda

National Industrial Committee (KINAS) Existing regulation Proposed regulations

• KINAS’s main objective is to facilitate nation-wide, interagency, cross

government agencies, head of industry association (KADIN, APINDO)

development, monitoring and evaluation of implementation at

manifestation of mandate from presidential decree

• Day to day execution of KINAS’ authority and mandate, specific to

52

• Establishment of “Making Indonesia 4.0” working group as

• Cross functional – multi stakeholders representation

national 4IR implementation

Decree of the head of KINAS – “Making

Indonesia 4.0” working group

• Establishment of KINAS

• Appointment of KINAS members : relevant ministers, head of

• Grant authority to KINAS to conduct alignment, program

national level

Presidential Decree (Perpres) on National Industrial Committee

Law 3/2014

• Article 112 enables MoI to propose to the president on the formation of KINAS

stakeholders alignment in accelerating national industrial development agenda

Making

Indonesia

Making

Indonesia

4IR Working Group

4IR Working Group

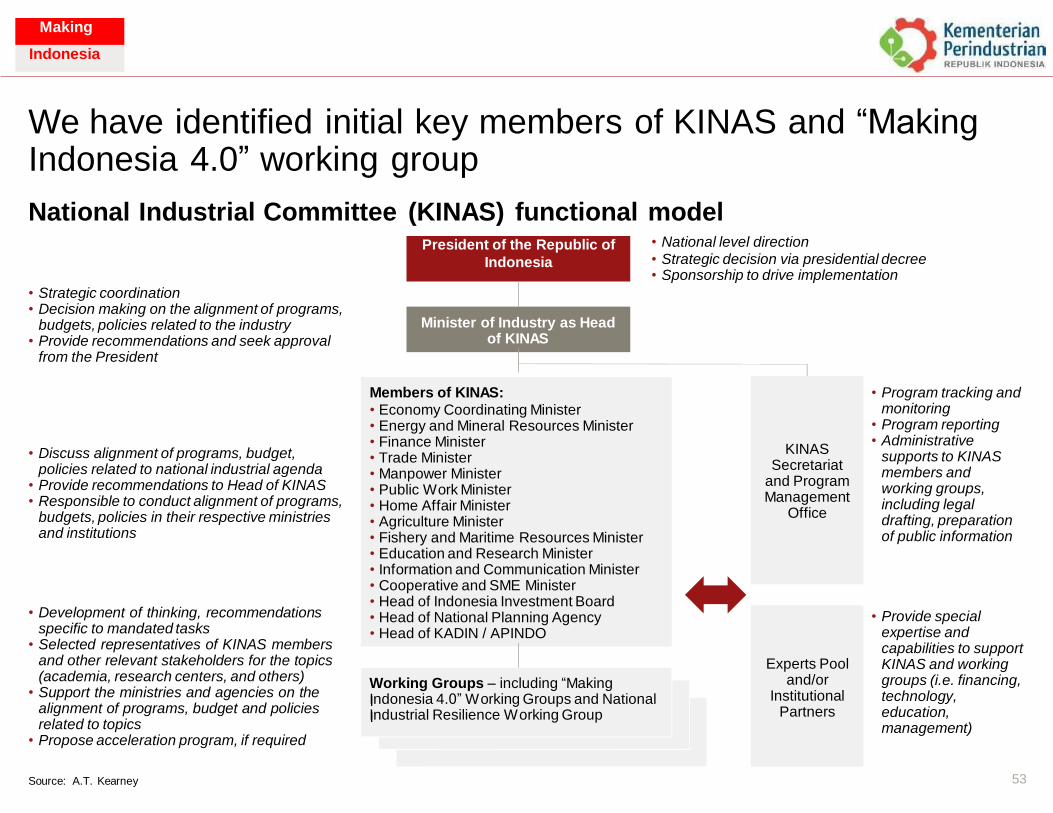

We have identified initial key members of KINAS and “Making Indonesia 4.0” working group

National Industrial Committee (KINAS) functional model • National level direction

• Strategic decision via presidential decree • Sponsorship to drive implementation

• Strategic coordination • Decision making on the alignment of programs,

budgets, policies related to the industry • Provide recommendations and seek approval

from the President

• Program tracking and monitoring

• Program reporting • Administrative

supports to KINAS members and working groups, including legal drafting, preparation of public information

• Discuss alignment of programs, budget, policies related to national industrial agenda

• Provide recommendations to Head of KINAS • Responsible to conduct alignment of programs,

budgets, policies in their respective ministries and institutions

• Development of thinking, recommendations specific to mandated tasks

• Selected representatives of KINAS members and other relevant stakeholders for the topics (academia, research centers, and others)

• Support the ministries and agencies on the alignment of programs, budget and policies related to topics

• Propose acceleration program, if required

• Provide special expertise and capabilities to support KINAS and working groups (i.e. financing, technology, education, management)

Working Groups – including “Making Indonesia 4.0” Working Groups and National Industrial Resilience Working Group

53 Source: A.T. Kearney

Experts Pool and/or

Institutional Partners

KINAS Secretariat

and Program Management

Office

Members of KINAS:

• Economy Coordinating Minister • Energy and Mineral Resources Minister • Finance Minister • Trade Minister • Manpower Minister • Public Work Minister • Home Affair Minister • Agriculture Minister • Fishery and Maritime Resources Minister • Education and Research Minister • Information and Communication Minister • Cooperative and SME Minister • Head of Indonesia Investment Board • Head of National Planning Agency • Head of KADIN / APINDO

I I

President of the Republic of

Indonesia

Minister of Industry as Head of KINAS

Making

Indonesia

Making

Indonesia

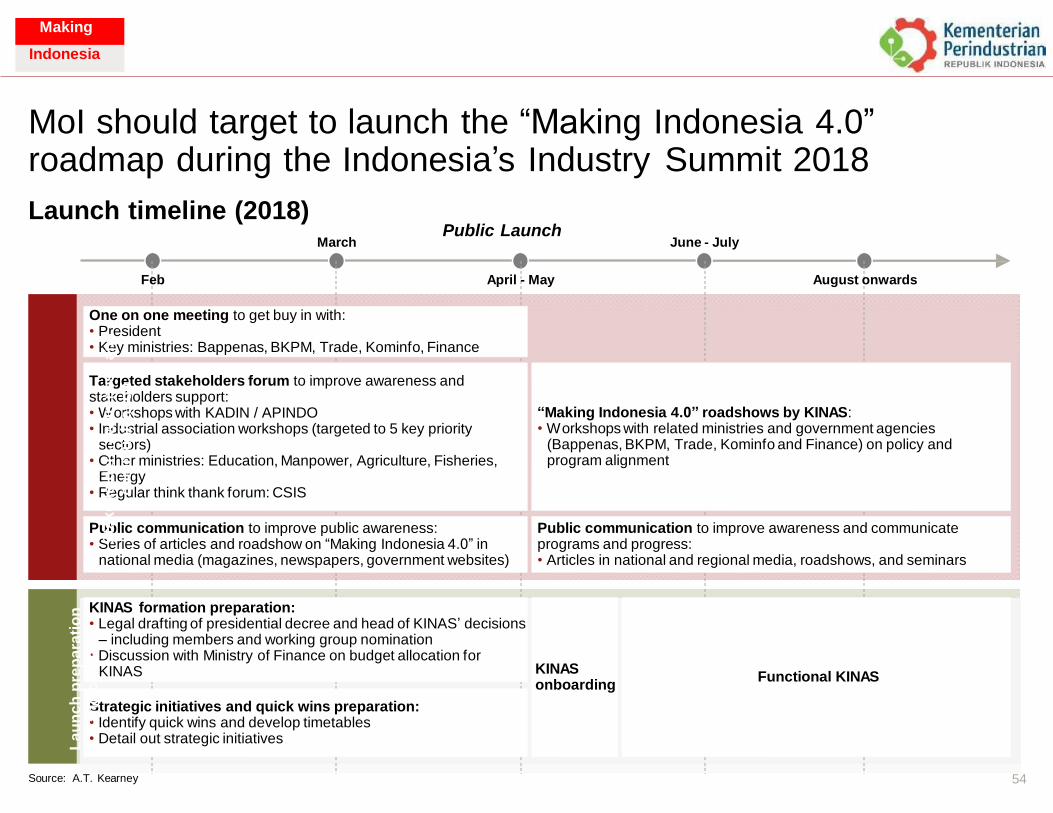

MoI should target to launch the “Making Indonesia 4.0” roadmap during the Indonesia’s Industry

Launch timeline (2018)

Summit 2018

Public Launch March June - July

Feb April - May August onwards

One on one meeting to get buy in with: • President • Key ministries: Bappenas, BKPM, Trade, Kominfo, Finance

Targeted stakeholders forum to improve awareness and stakeholders support: • Workshops with KADIN / APINDO • Industrial association workshops (targeted to 5 key priority

sectors) • Other ministries: Education, Manpower, Agriculture, Fisheries,

Energy • Regular think thank forum: CSIS

“Making Indonesia 4.0” roadshows by KINAS: • Workshops with related ministries and government agencies

(Bappenas, BKPM, Trade, Kominfo and Finance) on policy and program alignment

Public communication to improve public awareness: • Series of articles and roadshow on “Making Indonesia 4.0” in

national media (magazines, newspapers, government websites)

Public communication to improve awareness and communicate programs and progress: • Articles in national and regional media, roadshows, and seminars

KINAS formation preparation: • Legal drafting of presidential decree and head of KINAS’ decisions

– including members and working group nomination • Discussion with Ministry of Finance on budget allocation for

KINAS KINAS onboarding

Functional KINAS

Strategic initiatives and quick wins preparation: • Identify quick wins and develop timetables • Detail out strategic initiatives

Source: A.T. Kearney 54

La

un

ch

pre

pa

rati

on

a

nd

co

nte

nt

Sta

ke

ho

lde

rs a

wa

ren

es

s a

nd

c

om

mu

nic

ati

on

Making

Indonesia

Making

Indonesia

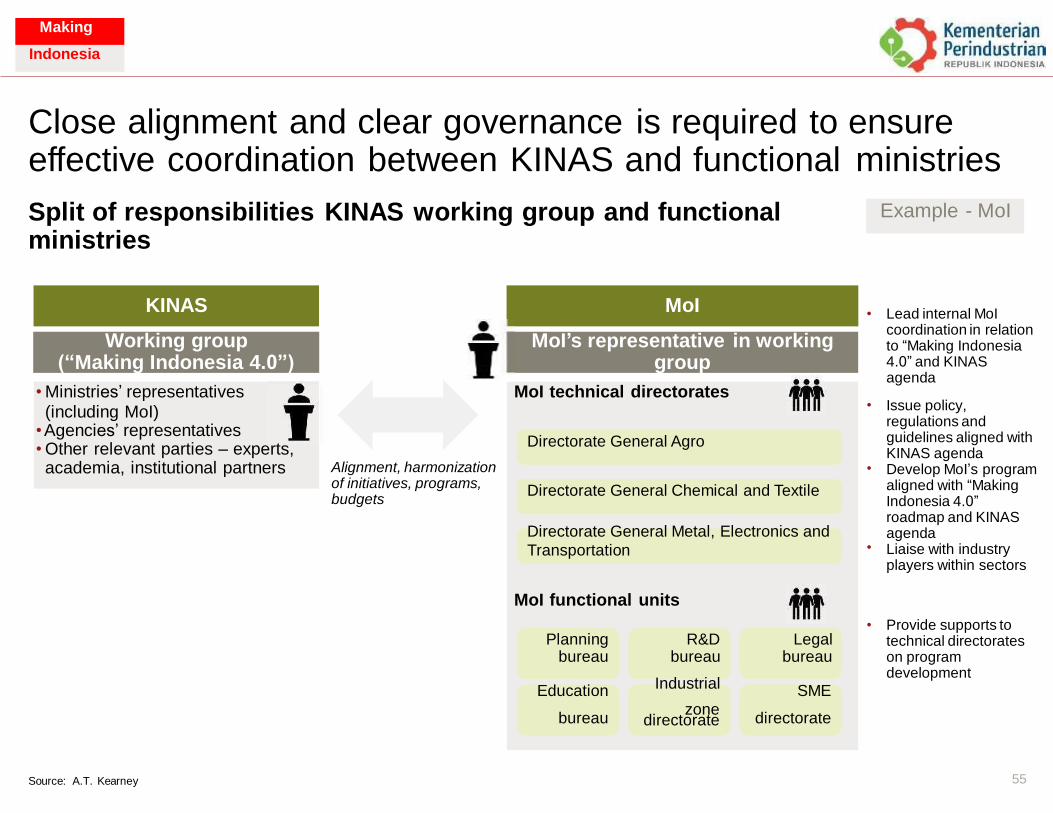

Close alignment and clear governance is required to ensure effective coordination between KINAS and functional ministries

Split of responsibilities ministries

KINAS working group and functional

• Lead internal MoI coordination in relation to “Making Indonesia 4.0” and KINAS agenda

Issue policy, regulations and guidelines aligned with KINAS agenda Develop MoI’s program aligned with “Making Indonesia 4.0” roadmap and KINAS agenda Liaise with industry players within sectors

•

Alignment, harmonization of initiatives, programs, budgets

•

•

• Provide supports to technical directorates on program development

zone bureau directorate

55 Source: A.T. Kearney

MoI technical directorates

Directorate General Agro

Directorate General Chemical and Textile

Directorate General Metal, Electronics and

Transportation

MoI functional units

Planning R&D Legal bureau bureau bureau

Education Industrial SME

directorate

• Ministries’ representatives (including MoI)

• Agencies’ representatives • Other relevant parties – experts, academia, institutional partners

MoI’s representative in working group

Working group (“Making Indonesia 4.0”)

MoI

KINAS

Example - MoI

Making

Indonesia

Lampiran Pangan dan Energi

Sectoral deep dive

Table of Contents

■ Priority Sector Strategies

–

–

–

–

Textile/Apparel

Automotive

Electronics

Chemicals

– Food & Beverages

4/20/2018 57

Sectoral deep dive

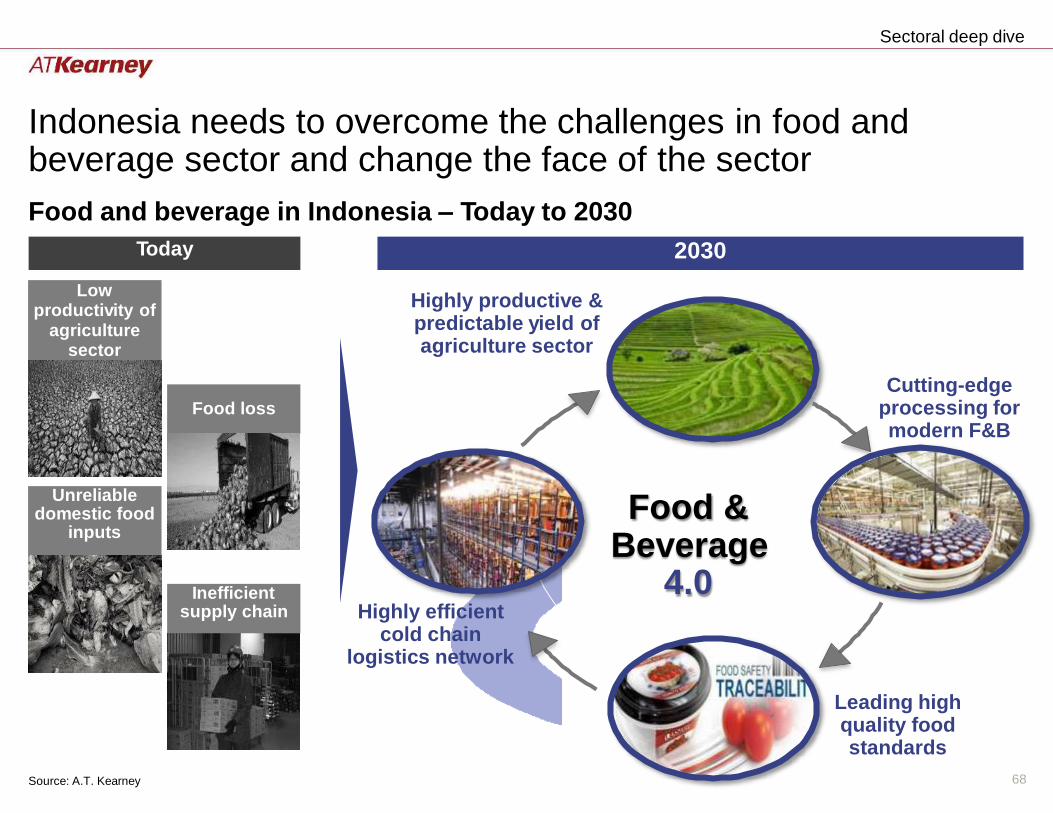

Indonesia needs to overcome the challenges in food and beverage sector and change the face of the sector

Food and beverage in Indonesia – Today to 2030

Highly productive & predictable yield of agriculture sector

Cutting-edge processing for modern F&B

Food & Beverage

4.0 Highly efficient

cold chain logistics network

Leading high quality food standards

68 Source: A.T. Kearney

Inefficient supply chain

Unreliable domestic food

inputs

Food loss

Low productivity of

agriculture sector

2030 Today

Sectoral deep dive

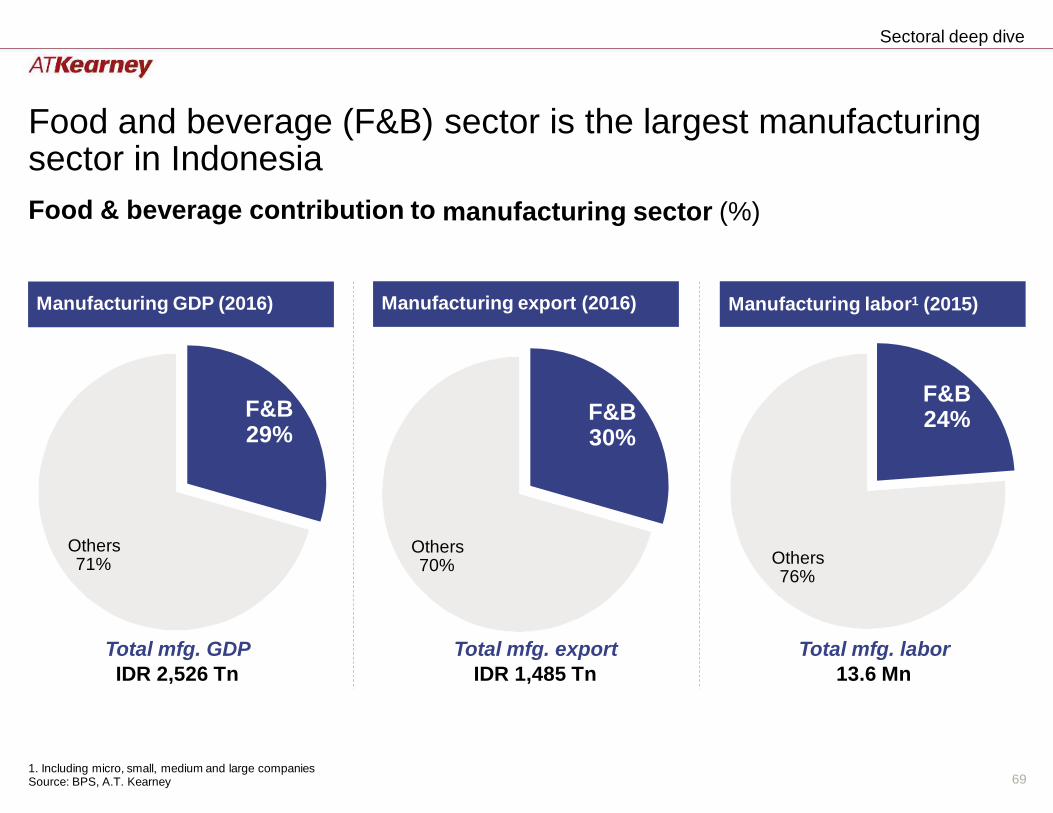

Food and beverage (F&B) sector in Indonesia

Food & beverage contribution to

sector is the largest manufacturing

manufacturing sector (%)

F&B 24% F&B

29% F&B 30%

Others 71%

Others 70% Others

76%

Total mfg. GDP

IDR 2,526 Tn

Total mfg. export

IDR 1,485 Tn

Total mfg. labor

13.6 Mn

1. Including micro, small, medium and large companies Source: BPS, A.T. Kearney 69

Manufacturing labor1 (2015)

Manufacturing export (2016)

Manufacturing GDP (2016)

Sectoral deep dive

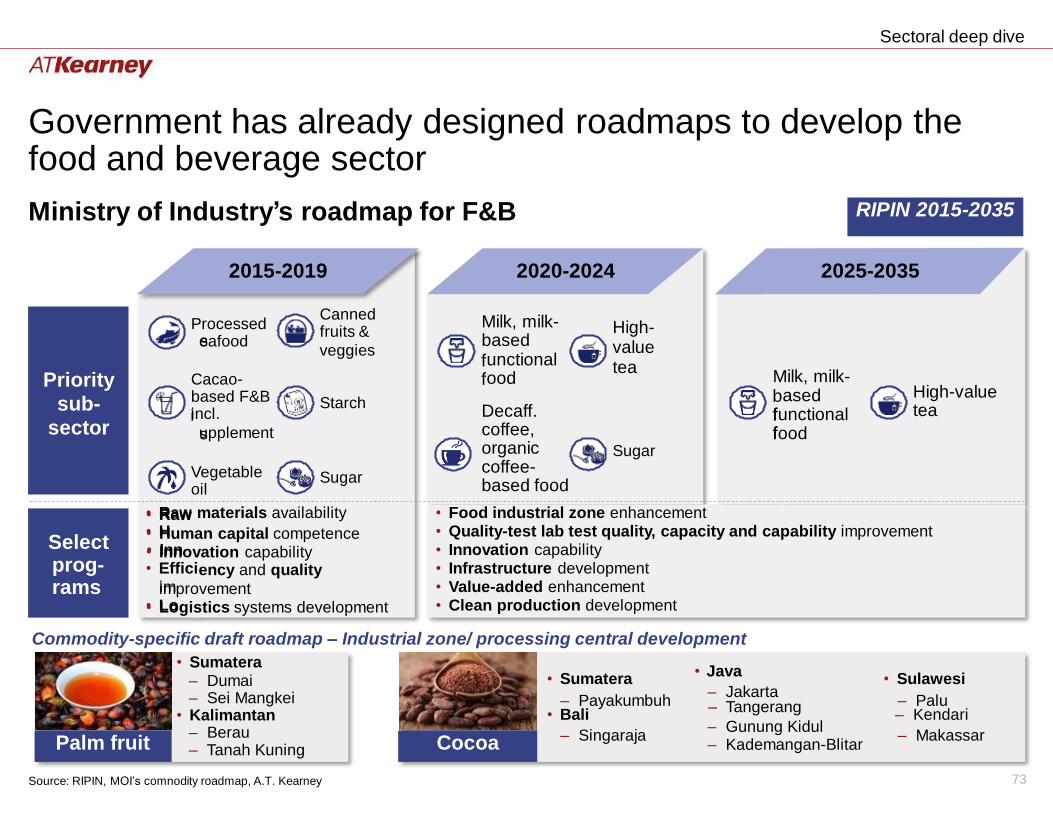

Government has already designed food and beverage sector

roadmaps to develop the

Ministry of Industry’s roadmap for F&B

Canned fruits &

Milk, milk- based

Processed High- value tea

eafood

unctional ood Milk, milk- Cacao-

based F&B incl.

High-value tea

ased Starch Decaff. coffee, organic coffee- based food

functional upplement food

Sugar

Vegetable oil

Sugar

• • •

Raw

Human capital competence Innovation capability

improvement Logistics systems development •

Commodity-specific draft roadmap – Industrial zone/ processing central development

– Jakarta – Payakumbuh – Palu

– Gunung Kidul – Singaraja – Makassar

73 Source: RIPIN, MOI’s comnodity roadmap, A.T. Kearney

• Sumatera • Java

• Sulawesi

• Bali – Tangerang

– Kendari

– Kademangan-Blitar Cocoa

• Sumatera – Dumai – Sei Mangkei

• Kalimantan – Berau – Tanah Kuning Palm fruit

2015-2019

veggies

2020-2024

2025-2035

Priority sub-

sector

s

i s

f f

b f f

Select prog- rams

• Raw • H • Inn • Effici

im • Lo

materials availability

ency and quality

• Food industrial zone enhancement • Quality-test lab test quality, capacity and capability improvement • Innovation capability • Infrastructure development • Value-added enhancement • Clean production development

RIPIN 2015-2035

Sectoral deep dive

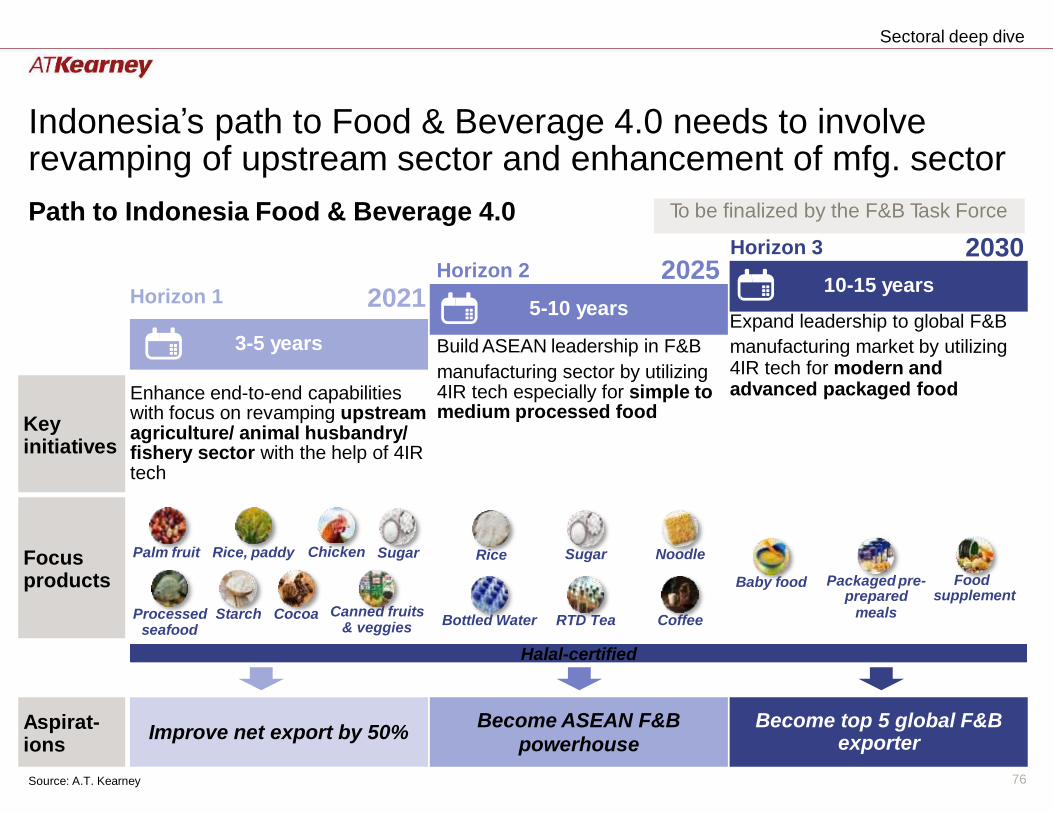

Indonesia’s path to Food & Beverage 4.0 needs to involve revamping of upstream sector and enhancement of mfg. sector

Path to Indonesia Food & Beverage 4.0

2030 Horizon 3

manufacturing market by utilizing 4IR tech for modern and advanced packaged food

manufacturing sector by utilizing 4IR tech especially for simple to medium processed food

Enhance end-to-end capabilities with focus on revamping upstream agriculture/ animal husbandry/ fishery sector with the help of 4IR tech

Palm fruit Rice, paddy Chicken Sugar Sugar Noodle Rice

Packaged pre- Food prepared supplement

meals

Baby food

Canned fruits & veggies

Processed Starch Cocoa seafood

Bottled Water RTD Tea Coffee

Halal-certified

exporter

76 Source: A.T. Kearney

Aspirat- ions

Improve net export by 50%

Become ASEAN F&B powerhouse

Become top 5 global F&B

Focus products

Key initiatives

Horizon 2 2025

10-15 years Horizon 1 2021 5-10 years

Expand leadership to global F&B

3-5 years Build ASEAN leadership in F&B

To be finalized by the F&B Task Force

(

p produced commodit

Market size/ ID’s scale

Sectoral deep dive

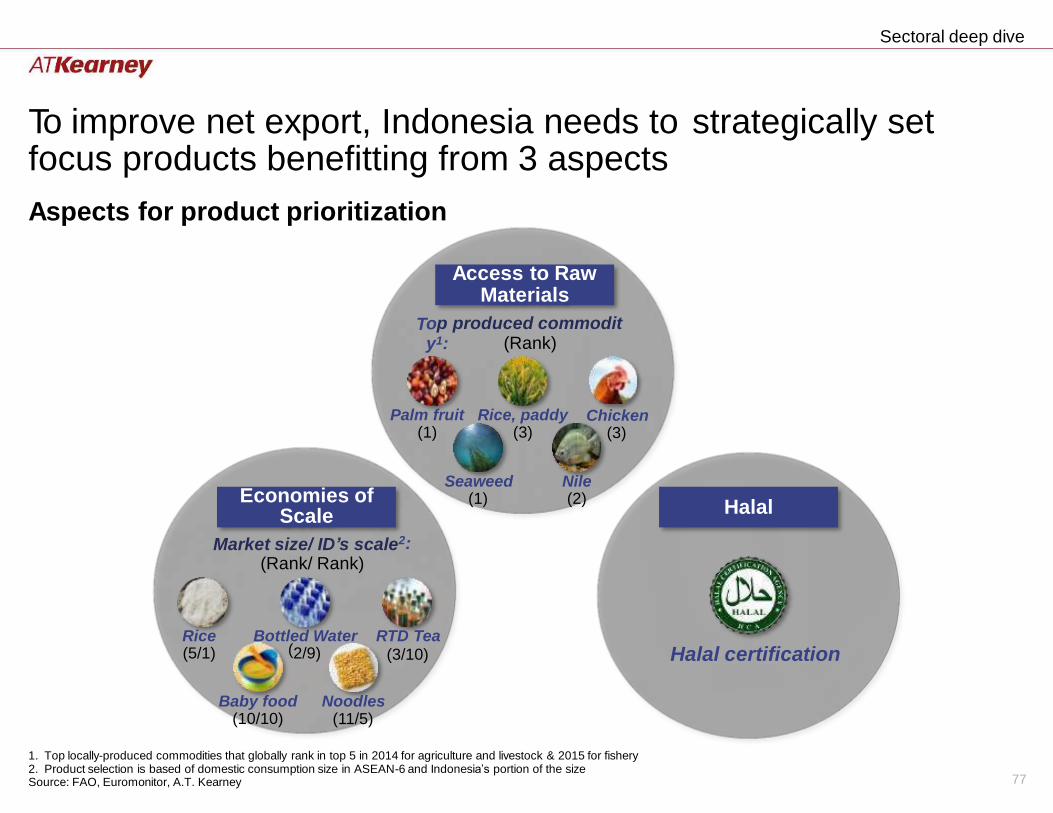

To improve net export, Indonesia needs to focus products benefitting from 3 aspects

strategically set

Aspects for product prioritization

o y1:

T (Rank)

Palm fruit Rice, paddy Chicken (3) (1) (3)

Seaweed (1)

Nile (2)

2: (Rank/ Rank)

Rice (5/1)

Bottled Water 2/9)

RTD Tea (3/10) Halal certification

Baby food Noodles (10/10) (11/5)

1. Top locally-produced commodities that globally rank in top 5 in 2014 for agriculture and livestock & 2015 for fishery 2. Product selection is based of domestic consumption size in ASEAN-6 and Indonesia’s portion of the size Source: FAO, Euromonitor, A.T. Kearney 77

Halal Economies of

Scale

Access to Raw Materials

Sectoral deep dive

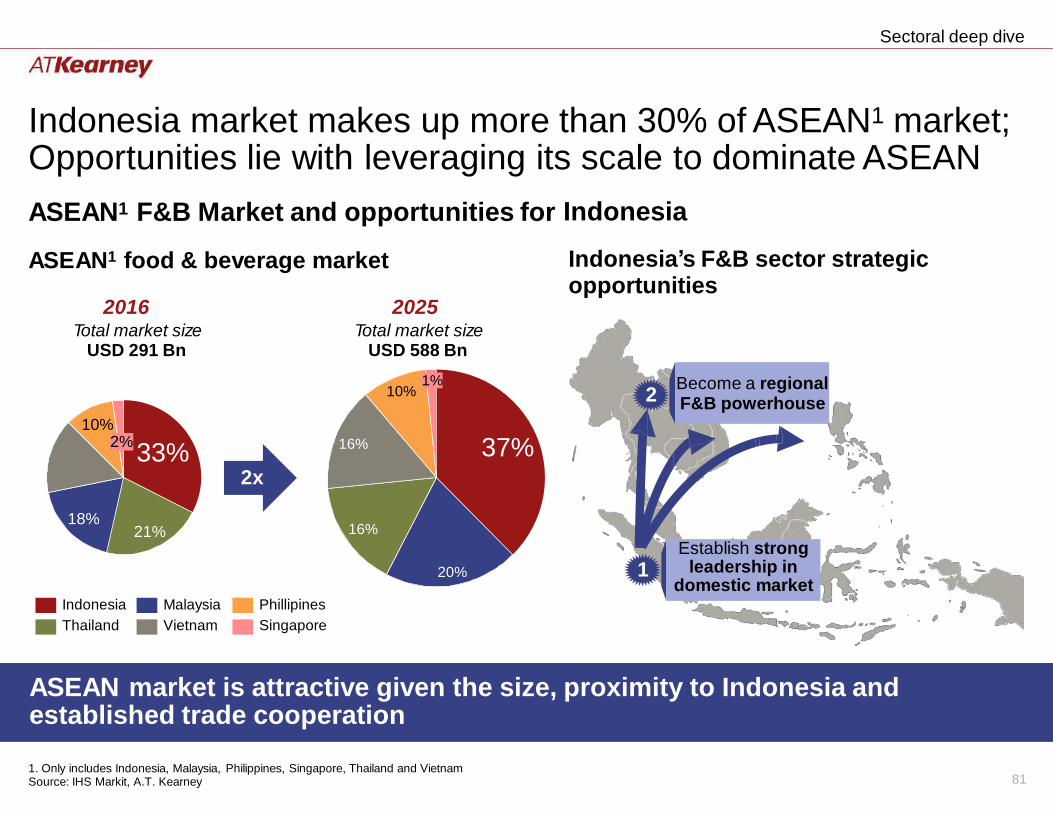

Indonesia market makes up more than 30% of ASEAN1 market; Opportunities lie with leveraging its scale to dominate ASEAN

ASEAN1 F&B Market and opportunities for

ASEAN1 food & beverage market

Indonesia

Indonesia’s F&B sector strategic opportunities

2016 Total market size

USD 291 Bn

2025 Total market size

USD 588 Bn

10% 2

10%

37% 16% 33%

2x

18% 16% 21%

1 20%

Indonesia

Thailand

Malaysia

Vietnam

Phillipines

Singapore

ASEAN market is attractive given the size, established trade cooperation

proximity to Indonesia and

1. Only includes Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam Source: IHS Markit, A.T. Kearney 81

Establish strong leadership in

domestic market

2%

1%

Become a regional F&B powerhouse

Sectoral deep dive

Table of Contents

■ Priority Sector Strategies

–

–

–

–

Food & Beverages

Textile/Apparel

Automotive

Electronics

– Chemicals

4/20/2018 64

Sectoral deep dive

Indonesia needs to overcome the and change the face of the sector

challenges in chemical sector

Chemical in Indonesia – Today to 2030

Enhanced basic

chemical production

with predictive

maintenance & yield

mgmt.

Chemicals 4.0

Highly reliable

chemical

logistics via

advanced

inventory

monitoring in-

transit

Advanced

processing of

biomass to

biochemicals

Refined bio-plastics technology hub 131 Source: A.T. Kearney

Basic supply chain

Lacks R&D capabilities

Low technology adoption

Inefficient plants

2030 Today

Sectoral deep dive

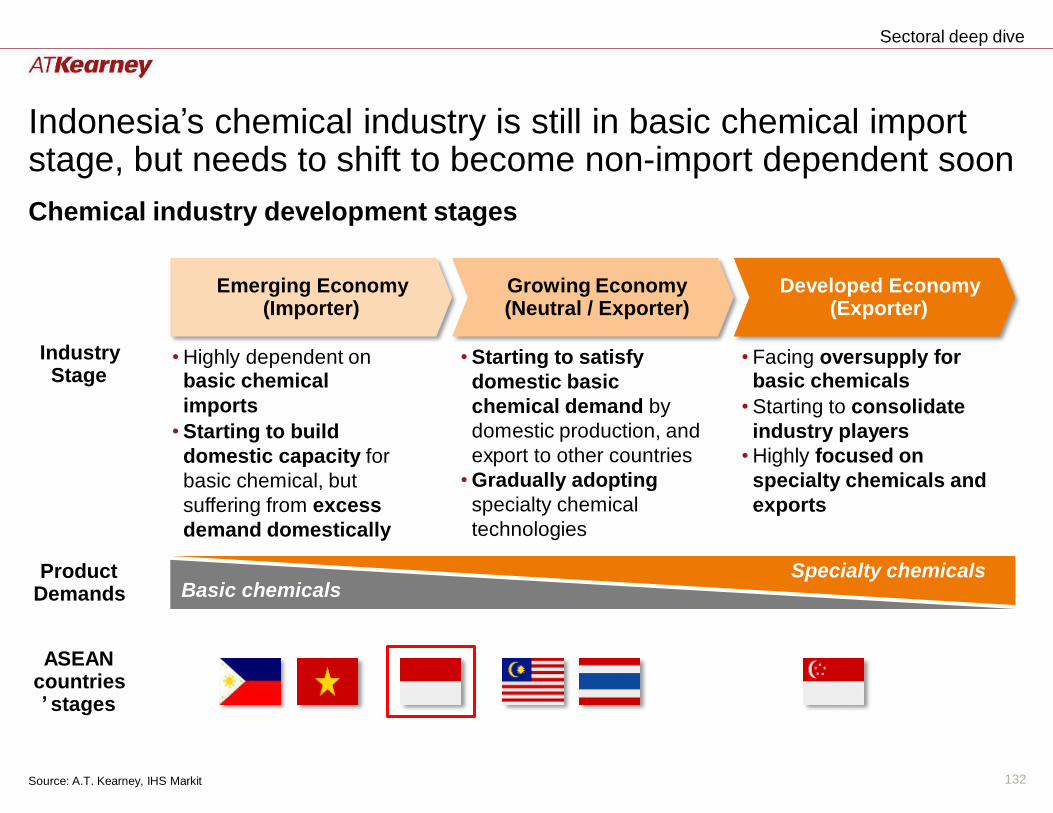

Indonesia’s chemical industry is still in basic chemical import stage, but needs to shift to become non-import dependent soon

Chemical industry development stages

Emerging Economy (Importer)

Growing Economy (Neutral / Exporter)

Developed Economy (Exporter)

Industry Stage

• Highly dependent on basic chemical

imports

• Starting to build

domestic capacity for

basic chemical, but

suffering from excess

demand domestically

• Starting to satisfy

domestic basic

chemical demand by

domestic production, and

export to other countries

• Gradually adopting

specialty chemical

technologies

• Facing oversupply for basic chemicals

• Starting to consolidate

industry players

• Highly focused on

specialty chemicals and

exports

Specialty chemicals Product Demands Basic chemicals

ASEAN countries ’ stages

132 Source: A.T. Kearney, IHS Markit

Sectoral deep dive

Indonesia’s chemical sector is largely dependent on petrochemical…

Indonesia’s chemical industry sales & consumption breakdown by product

$39.3Bn (77%) $2.1Bn (4%)

$5.0Bn

Basic chemicals $6.2Bn (12%)

Synthetic fibers

1. Sales from local production Source: A.T. Kearney, IHS Markit 133

Consumption (2016; US$ Bn)

Others Petrochemical basis

Soap & cosmetics $3.9Bn (8%)

Agrochemical $0.9Bn (2%)

Fertilizers

(10%)

Synthetic resins

$32.8Bn (64%)

$0.3Bn (1%)

Total Chemical Consumption: US$51.2Bn

Sales1 (2016; US$ Bn) Petrochemical basis

Others $32.2Bn (72%) $2.9Bn (6%)

Soap & cosmetics $4.9Bn (11%)

Agrochemical

$0.8Bn (2%)

Fertilizers

$4.0Bn (9%)

Basic chemicals Synthetic resins $29.7Bn (66%)

$2.1Bn (5%)

Synthetic fibers

$0.4Bn (1%)

Total Chemical Sales: US$44.8Bn

Sectoral deep dive

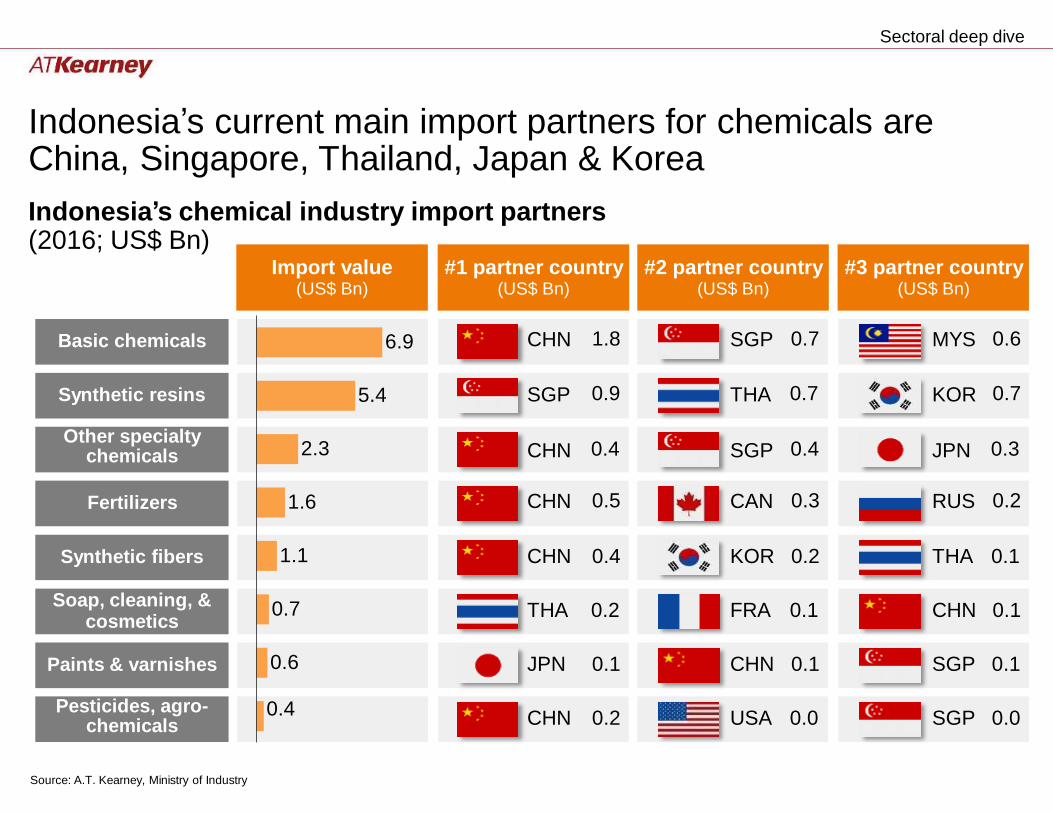

Indonesia’s current main import partners for China, Singapore, Thailand, Japan & Korea

chemicals are

Indonesia’s chemical industry import partners (2016; US$ Bn)

6.9

5.4

2.3

1.6

1.1

0.7

0.6

Source: A.T. Kearney, Ministry of Industry

CHN 0.2

USA 0.0

SGP 0.0 Pesticides, agro-

chemicals

JPN 0.1

CHN 0.1

SGP 0.1

Paints & varnishes

THA 0.2

FRA 0.1

CHN 0.1 Soap, cleaning, &

cosmetics

CHN 0.4

KOR 0.2

THA 0.1

Synthetic fibers

CHN 0.5

CAN 0.3

RUS 0.2

Fertilizers

CHN 0.4

SGP 0.4

JPN 0.3 Other specialty

chemicals

SGP 0.9

THA 0.7

KOR 0.7

Synthetic resins

CHN 1.8

SGP 0.7

MYS 0.6

0.4

Basic chemicals

Import value (US$ Bn)

#1 partner country (US$ Bn)

#2 partner country (US$ Bn)

#3 partner country (US$ Bn)

Sectoral deep dive

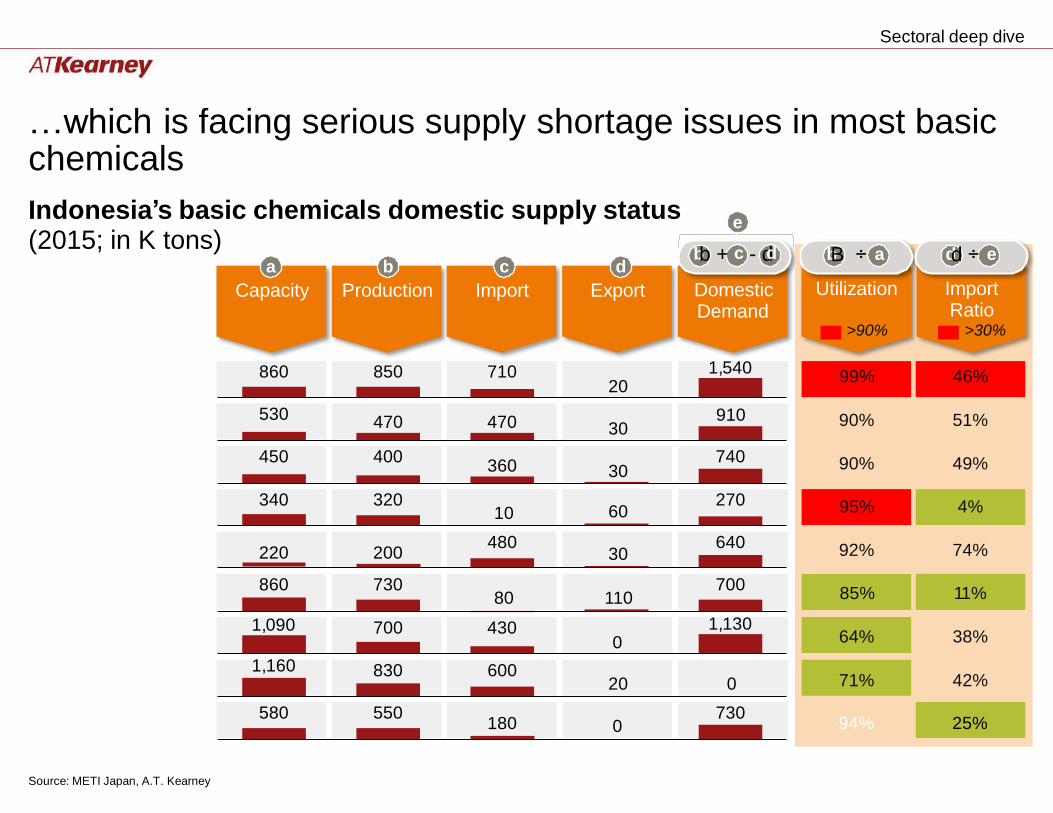

…which is facing serious supply shortage issues chemicals

Indonesia’s basic chemicals domestic supply status

in most basic

e

bb + c - dd

Domestic Demand

(2015; in K tons) a

Capacity

b

Production

c

Import

d

Export

1,540 Ethylene

910 Low Density

High Density

Styrene Monomer

Ethylene Glycol

PVC

1,130 Propylene

Polypropylene

Benzene

Source: METI Japan, A.T. Kearney

580 550

180

0 730

1,160 830 600

20

0

1,090 700 430

0

860 730

80

110 700

220

200 480

30 640

340 320

10

60 270

450 400

360

30 740

530

470

470

30

860 850 710

20

bB ÷ a dd ÷ e

Utilization Import Ratio

>90% >30%

99% 46%

90% 51%

90% 49%

95% 4%

92% 74%

85% 11%

64% 38%

71% 42%

94% 25%

Sectoral deep dive

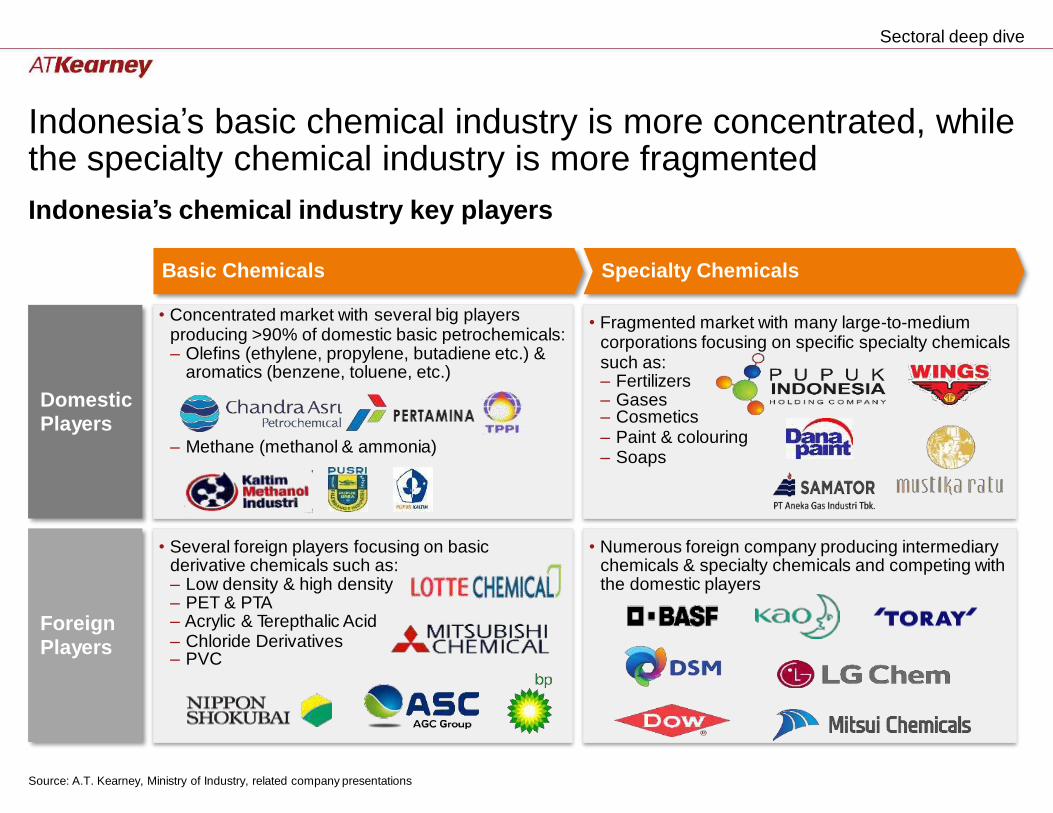

Indonesia’s basic chemical industry is more concentrated, the specialty chemical industry is more fragmented

Indonesia’s chemical industry key players

while

Basic Chemicals Specialty Chemicals

– Cosmetics

– Chloride Derivatives

Source: A.T. Kearney, Ministry of Industry, related company presentations

• Several foreign players focusing on basic derivative chemicals such as: – Low density & high density – PET & PTA – Acrylic & Terepthalic Acid

– PVC

• Numerous foreign company producing intermediary chemicals & specialty chemicals and competing with the domestic players

Foreign Players

• Concentrated market with several big players producing >90% of domestic basic petrochemicals: – Olefins (ethylene, propylene, butadiene etc.) &

aromatics (benzene, toluene, etc.)

– Methane (methanol & ammonia)

• Fragmented market with many large-to-medium corporations focusing on specific specialty chemicals such as: – Fertilizers – Gases

– Paint & colouring – Soaps

Domestic Players

Sectoral deep dive

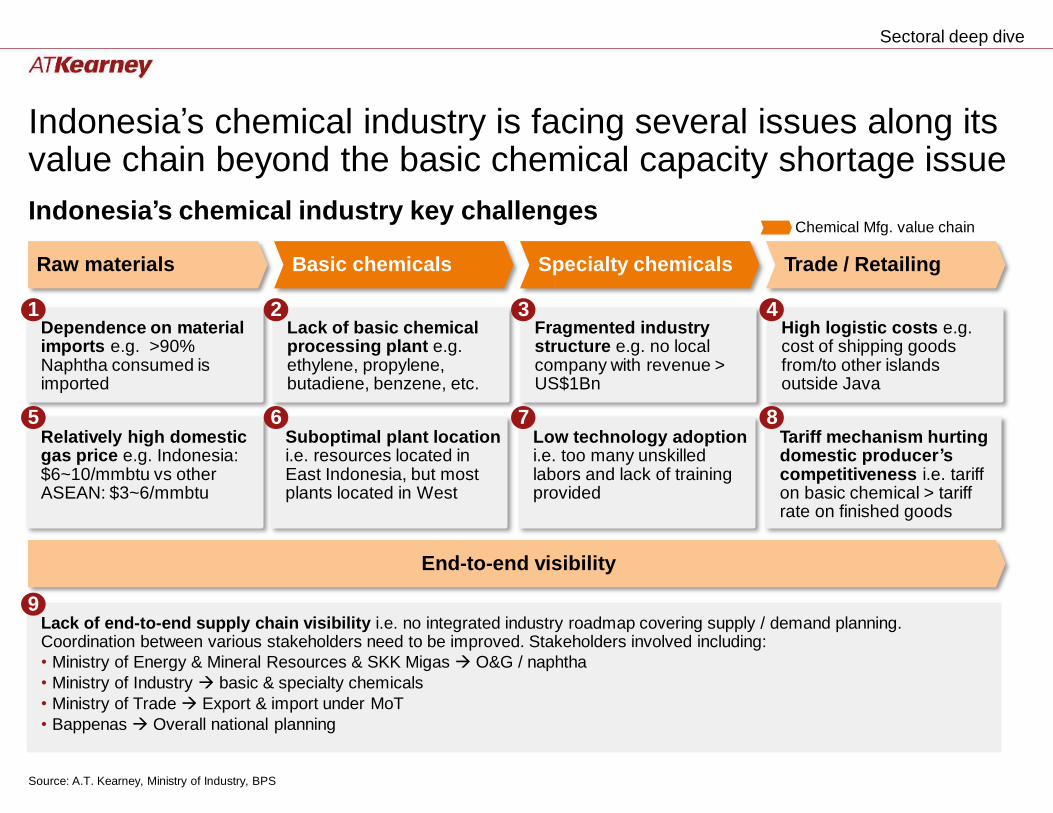

Indonesia’s chemical industry is facing several issues along its value chain beyond the basic chemical capacity

Indonesia’s chemical industry key challenges

shortage issue

Chemical Mfg. value chain

Raw materials Basic chemicals Specialty chemicals Trade / Retailing

1 2 3 4

5 6 7 8

End-to-end visibility

9

Source: A.T. Kearney, Ministry of Industry, BPS

Lack of end-to-end supply chain visibility i.e. no integrated industry roadmap covering supply / demand planning. Coordination between various stakeholders need to be improved. Stakeholders involved including:

• Ministry of Energy & Mineral Resources & SKK Migas O&G / naphtha

• Ministry of Industry basic & specialty chemicals

• Ministry of Trade Export & import under MoT

• Bappenas Overall national planning

Relatively high domestic gas price e.g. Indonesia: $6~10/mmbtu vs other ASEAN: $3~6/mmbtu

Suboptimal plant location i.e. resources located in East Indonesia, but most plants located in West

Low technology adoption i.e. too many unskilled labors and lack of training provided

Tariff mechanism hurting domestic producer’s competitiveness i.e. tariff on basic chemical > tariff rate on finished goods

Dependence on material imports e.g. >90% Naphtha consumed is imported

Lack of basic chemical processing plant e.g. ethylene, propylene, butadiene, benzene, etc.

Fragmented industry structure e.g. no local company with revenue > US$1Bn

High logistic costs e.g. cost of shipping goods from/to other islands outside Java

Sectoral deep dive

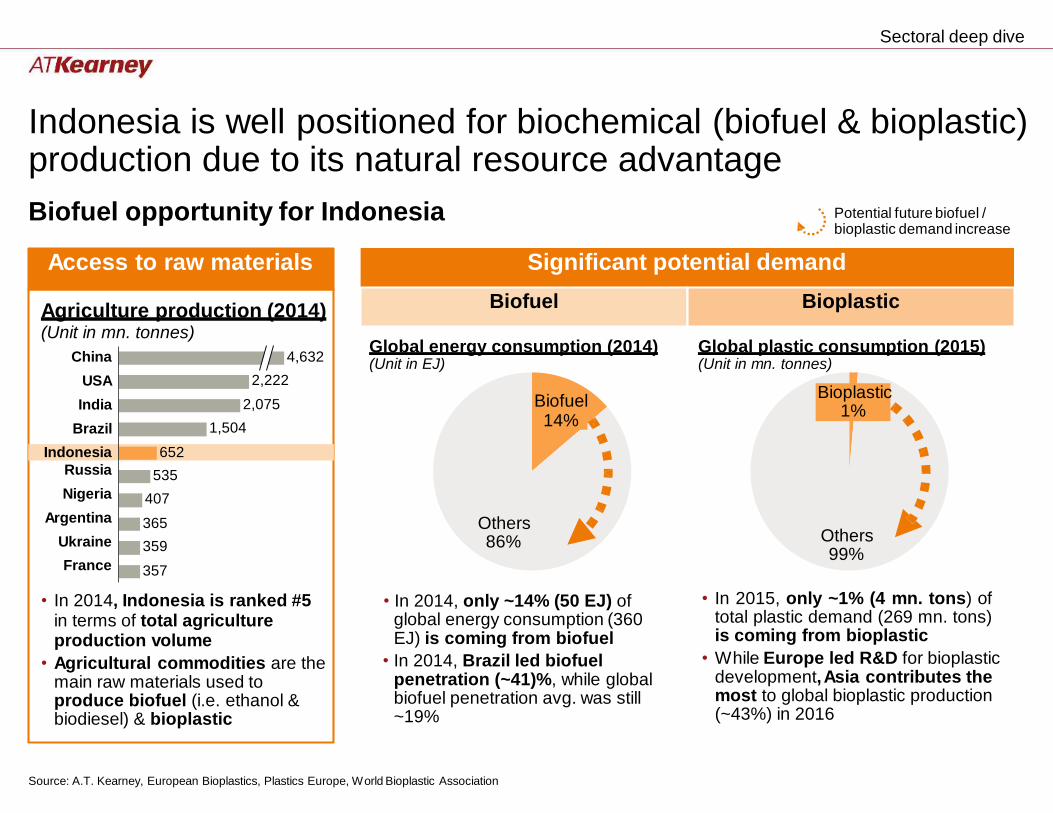

Indonesia is well positioned for biochemical (biofuel & bioplastic) production due to its natural resource advantage

Biofuel opportunity for Indonesia Potential future biofuel / bioplastic demand increase

Global energy consumption (2014) Global plastic consumption (2015) (Unit in EJ) (Unit in mn. tonnes)

14%

Others 86% Others

99%

• In 2015, only ~1% (4 mn. tons) of total plastic demand (269 mn. tons) is coming from bioplastic

• While Europe led R&D for bioplastic development, Asia contributes the most to global bioplastic production (~43%) in 2016

• In 2014, only ~14% (50 EJ) of global energy consumption (360 EJ) is coming from biofuel

• In 2014, Brazil led biofuel penetration (~41)%, while global biofuel penetration avg. was still ~19%

Source: A.T. Kearney, European Bioplastics, Plastics Europe, World Bioplastic Association

Biofuel Bioplastic

1%

Significant potential demand

Biofuel Bioplastic

Access to raw materials

Agriculture production (2014) (Unit in mn. tonnes)

China

USA

India

Brazil

4,632

2,222

2,075

1,504

Indonesia 652

Russia

Nigeria

Argentina

Ukraine

France

535

407

365 359

357

• In 2014, Indonesia is ranked #5 in terms of total agriculture production volume

• Agricultural commodities are the main raw materials used to produce biofuel (i.e. ethanol & biodiesel) & bioplastic

Sectoral deep dive

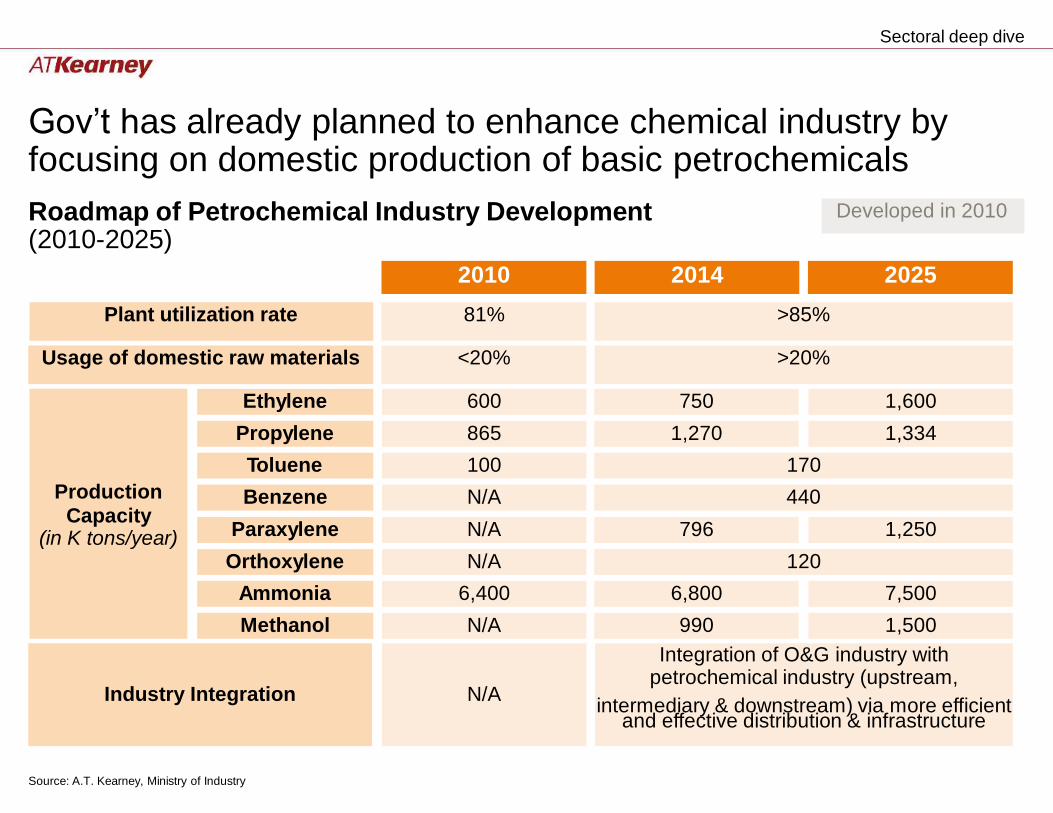

Gov’t has already planned to enhance chemical industry by focusing on domestic production of basic petrochemicals

Roadmap of (2010-2025)

Petrochemical Industry Development

intermediary & downstream) via more efficient

Source: A.T. Kearney, Ministry of Industry

Industry Integration

N/A

Integration of O&G industry with petrochemical industry (upstream,

and effective distribution & infrastructure

Methanol N/A 990 1,500

Ammonia 6,400 6,800 7,500

Orthoxylene N/A 120

Paraxylene N/A 796 1,250

Benzene N/A 440

Toluene 100 170

Propylene 865 1,270 1,334

Ethylene 600 750 1,600

Production

Capacity (in K tons/year)

Usage of domestic raw materials <20% >20%

Plant utilization rate 81% >85%

2010 2014 2025

Developed in 2010

Sectoral deep dive

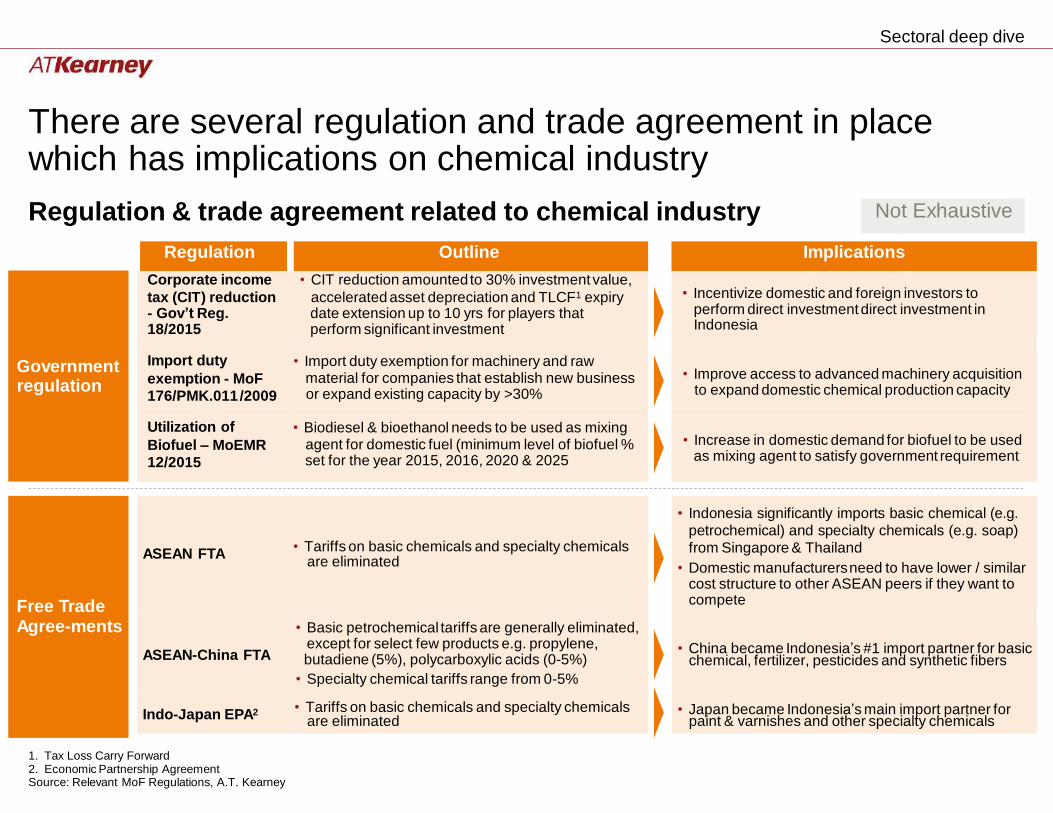

There are several regulation and trade agreement in place which has implications on chemical industry

Regulation & trade agreement related to chemical industry

perform direct investment direct investment in

regulation

as mixing agent to satisfy government requirement

are eliminated

chemical, fertilizer, pesticides and synthetic fibers

are eliminated paint & varnishes and other specialty chemicals

1. Tax Loss Carry Forward 2. Economic Partnership Agreement Source: Relevant MoF Regulations, A.T. Kearney

ASEAN FTA • Tariffs on basic chemicals and specialty chemicals

• Basic petrochemical tariffs are generally eliminated, except for select few products e.g. propylene,

ASEAN-China FTA butadiene (5%), polycarboxylic acids (0-5%)

• Specialty chemical tariffs range from 0-5%

Indo-Japan EPA2 • Tariffs on basic chemicals and specialty chemicals

• Indonesia significantly imports basic chemical (e.g.

petrochemical) and specialty chemicals (e.g. soap)

from Singapore & Thailand

• Domestic manufacturers need to have lower / similar cost structure to other ASEAN peers if they want to compete

• China became Indonesia’s #1 import partner for basic

• Japan became Indonesia’s main import partner for

Free Trade Agree-ments

Government

Implications

• Incentivize domestic and foreign investors to

Indonesia

• Improve access to advanced machinery acquisition to expand domestic chemical production capacity

• Increase in domestic demand for biofuel to be used

Regulation Outline

Corporate income • CIT reduction amounted to 30% investment value,

tax (CIT) reduction accelerated asset depreciation and TLCF1 expiry - Gov’t Reg. date extension up to 10 yrs for players that 18/2015 perform significant investment

Import duty • Import duty exemption for machinery and raw

exemption - MoF material for companies that establish new business 176/PMK.011 /2009 or expand existing capacity by >30%

Utilization of • Biodiesel & bioethanol needs to be used as mixing

Biofuel – MoEMR agent for domestic fuel (minimum level of biofuel % 12/2015 set for the year 2015, 2016, 2020 & 2025

Not Exhaustive

Sectoral deep dive

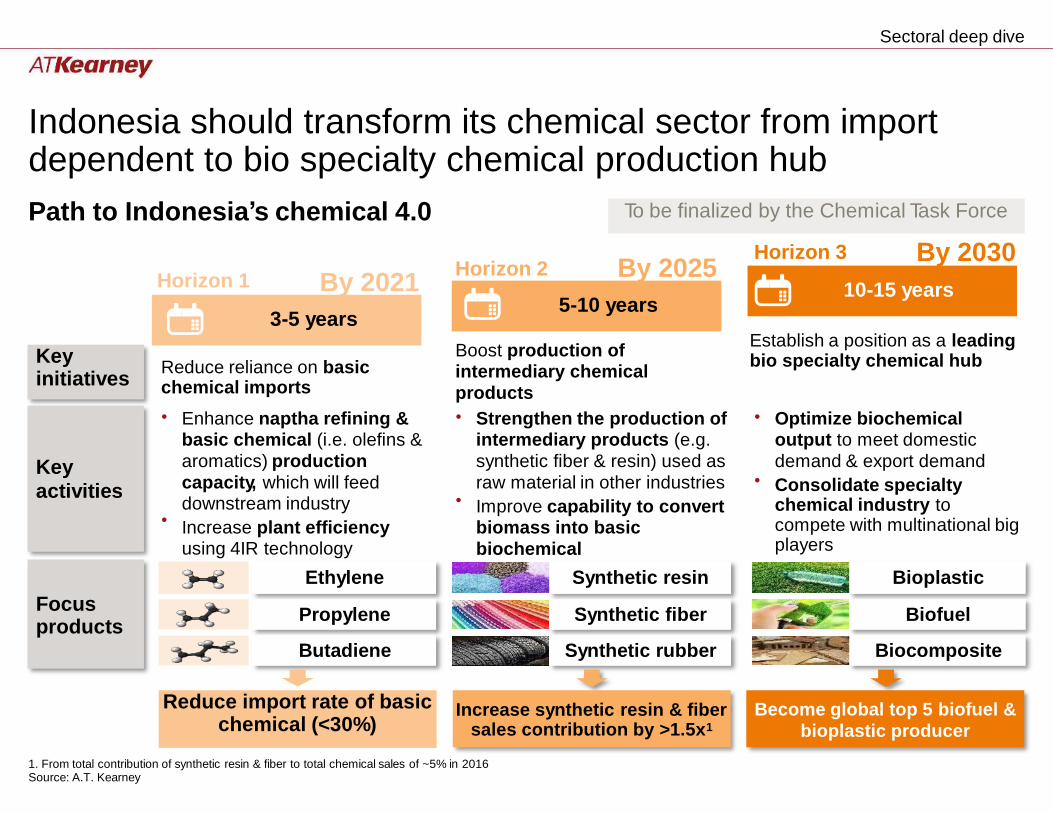

Indonesia should transform its chemical sector from import dependent to bio specialty chemical production hub

Path to Indonesia’s chemical 4.0

By 2030 Horizon 3 By 2025 Horizon 2

Horizon 1 By 2021

Establish a position as a leading bio specialty chemical hub

Boost production of intermediary chemical

products

Reduce reliance on basic chemical imports

• Enhance naptha refining & basic chemical (i.e. olefins &

aromatics) production

capacity, which will feed downstream industry

Increase plant efficiency using 4IR technology

• Strengthen the production of intermediary products (e.g.

synthetic fiber & resin) used as

raw material in other industries

Improve capability to convert biomass into basic

biochemical

• Optimize biochemical output to meet domestic

demand & export demand

Consolidate specialty chemical industry to compete with multinational big players

• •

•

Ethylene Synthetic resin Bioplastic

Propylene Synthetic fiber Biofuel

Butadiene Synthetic rubber Biocomposite

1. From total contribution of synthetic resin & fiber to total chemical sales of ~5% in 2016 Source: A.T. Kearney

Increase synthetic resin & fiber sales contribution by >1.5x1

Become global top 5 biofuel &

bioplastic producer

Reduce import rate of basic chemical (<30%)

Focus products

Key activities

Key initiatives

3-5 years

5-10 years

10-15 years

To be finalized by the Chemical Task Force

Sectoral deep dive

Indonesia’s chemical industry should introduce technologies for process improvement

advanced

Chemical industry technology adoption

flows, PH, Enable labor to inspect /

pressure level, viscosity, etc.

equipment e.g. power lines, chemical tanks, pipelines

• AI Perform data mining & modelling to

Train staffs virtually to energy consumption and create the most

situations minimize cost

chemical reaction process during delivery

Source: IBM, Libelium, Deloitte, A.T. Kearney

Plants utilization optimization

• IoT Feed data

collected from critical equipment (turbines,

compressors, extruders, etc.)

• AI Predict and diagnose potential

breakdowns and based on that, create maintenance schedule and parts procurement plan to minimize

maintenance spends & maximize outputs

Energy cost management Safety risk management

• IoT Monitor • Advanced robotics

temperature, hazardous plants location pressure level, equipment e.g. power line

Employee training

develop dynamic target values for plant’s • VR wearables

efficient energy management strategy to handle various on site

Supply chain management

Demand forecasting

• AI Create forecasting

model by considering factors e.g. seasonal effects, macro data at

domestic/regional level, regulatory changes & company strategy

Product development Product delivery visibility

• 3D Printing • IoT Monitor chemical

Allow companies to condition during delivery digitally custom process &generate alerts design a reactor when chemical conditions

which can control / become suboptimal cater to specific • AI Perform automatic troubleshooting

Asset Management

Resources Management

Labor Management

on

-

on

-

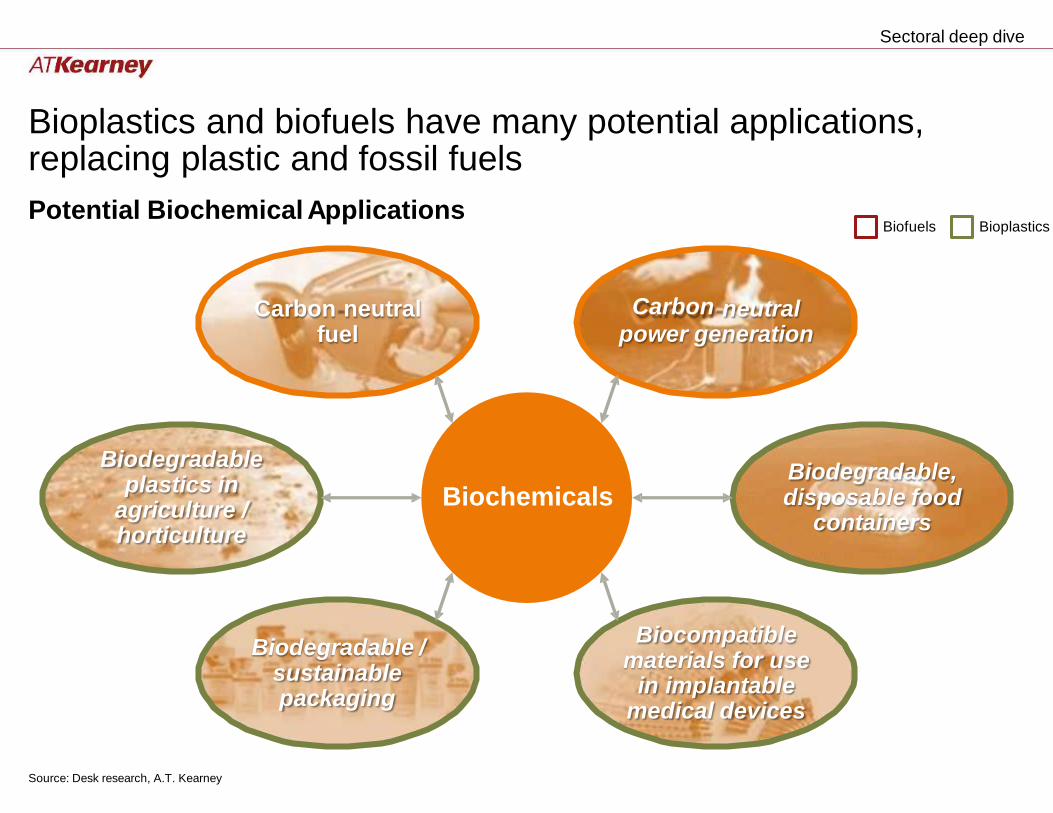

Sectoral deep dive

Bioplastics and biofuels have many replacing plastic and fossil fuels

Potential Biochemical Applications

potential applications,

Biofuels Bioplastics

Carbon neutral fuel

Carbon neutral power generation

Biodegradable plastics in

agriculture / horticulture

Biodegradable, disposable food

containers Biochemicals

Biocompatible materials for use

in implantable medical devices

Biodegradable / sustainable packaging

Source: Desk research, A.T. Kearney

Lampiran Energi/Kelistrikan

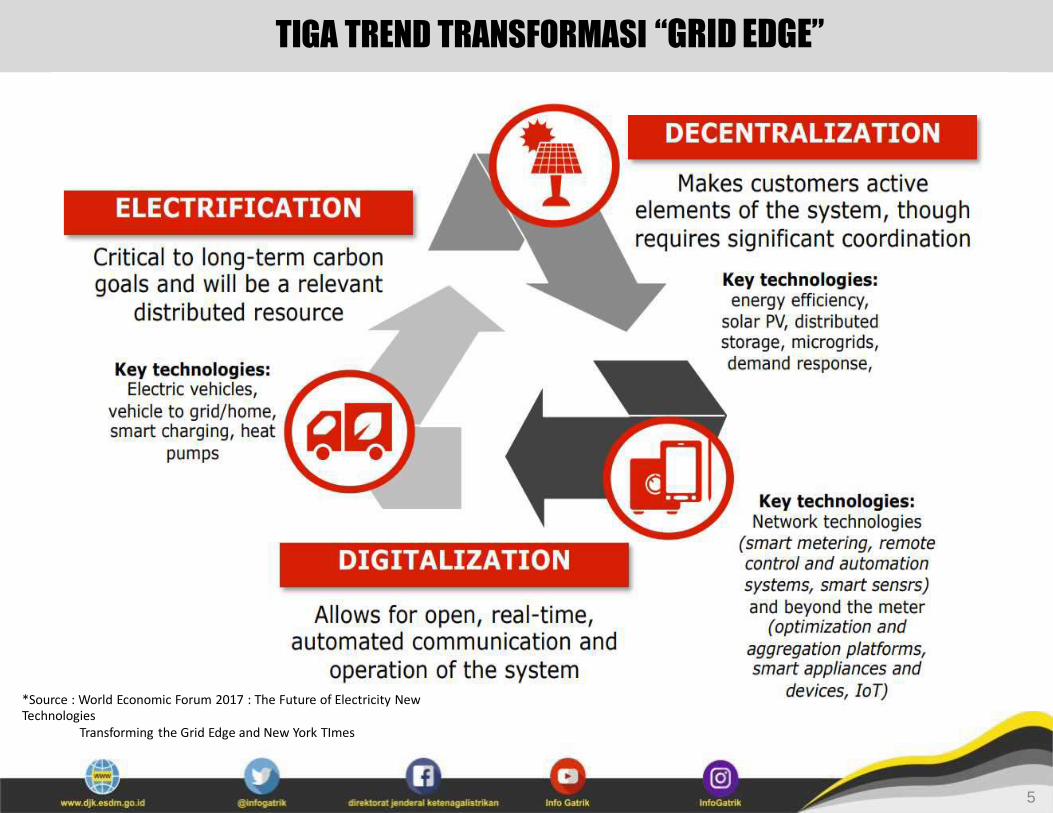

TIGA TREND TRANSFORMASI “GRID EDGE”

*Source : World Economic Forum 2017 : The Future of Electricity New Technologies

Transforming the Grid Edge and New York TImes

5

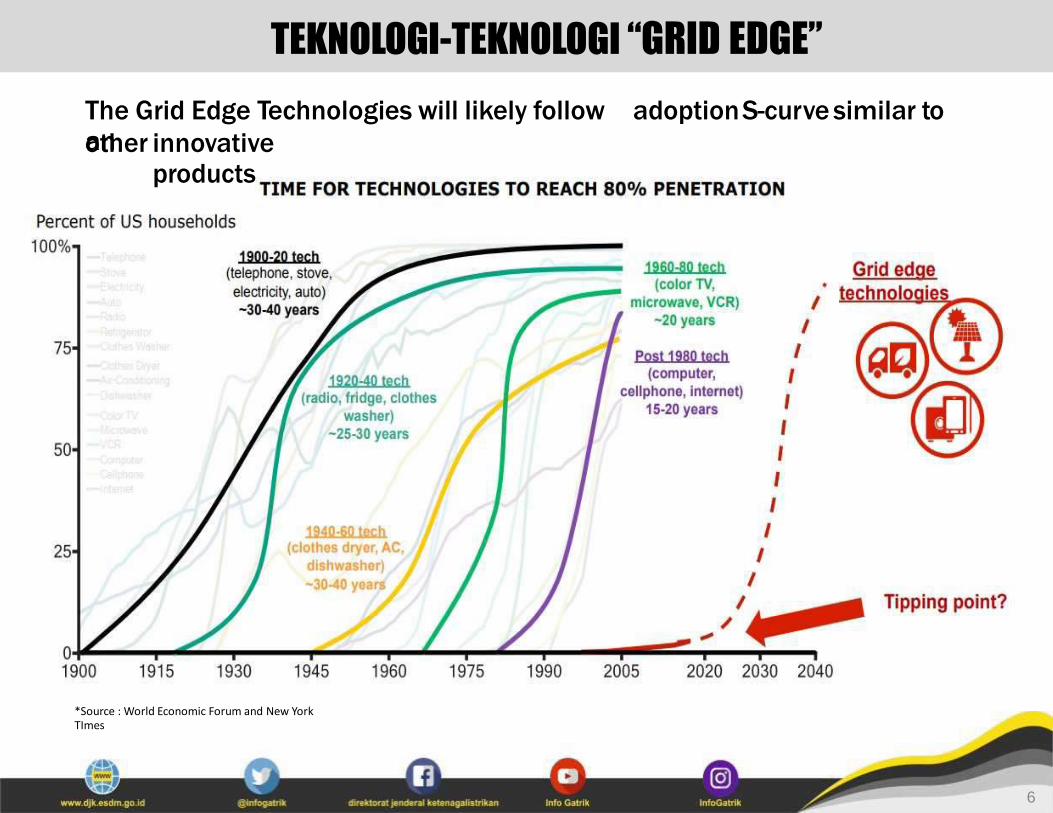

TEKNOLOGI-TEKNOLOGI “GRID EDGE”

The Grid Edge Technologies will likely follow an

adoption S-curve similar to

other innovative products

*Source : World Economic Forum and New York TImes

6

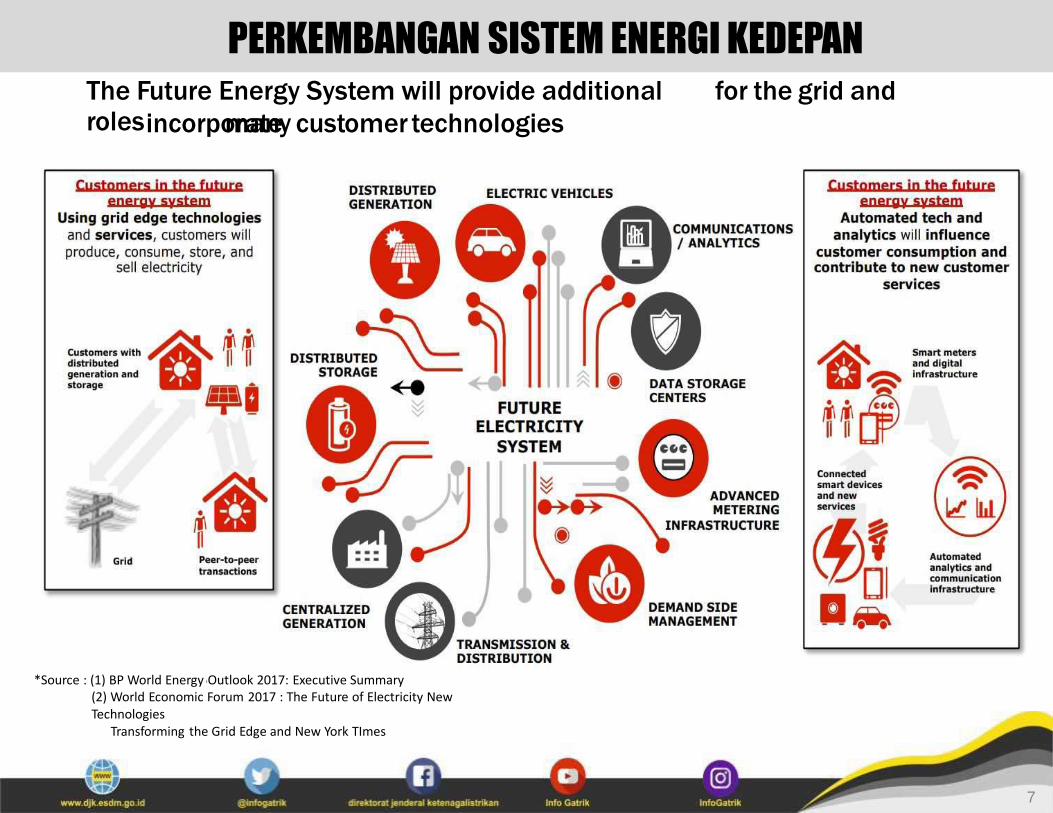

PERKEMBANGAN SISTEM ENERGI KEDEPAN

The Future Energy System will provide additional roles

for the grid and

incorporate many customer technologies

*Source : (1) BP World Energy Outlook 2017: Executive Summary (2) World Economic Forum 2017 : The Future of Electricity New Technologies

Transforming the Grid Edge and New York TImes

7

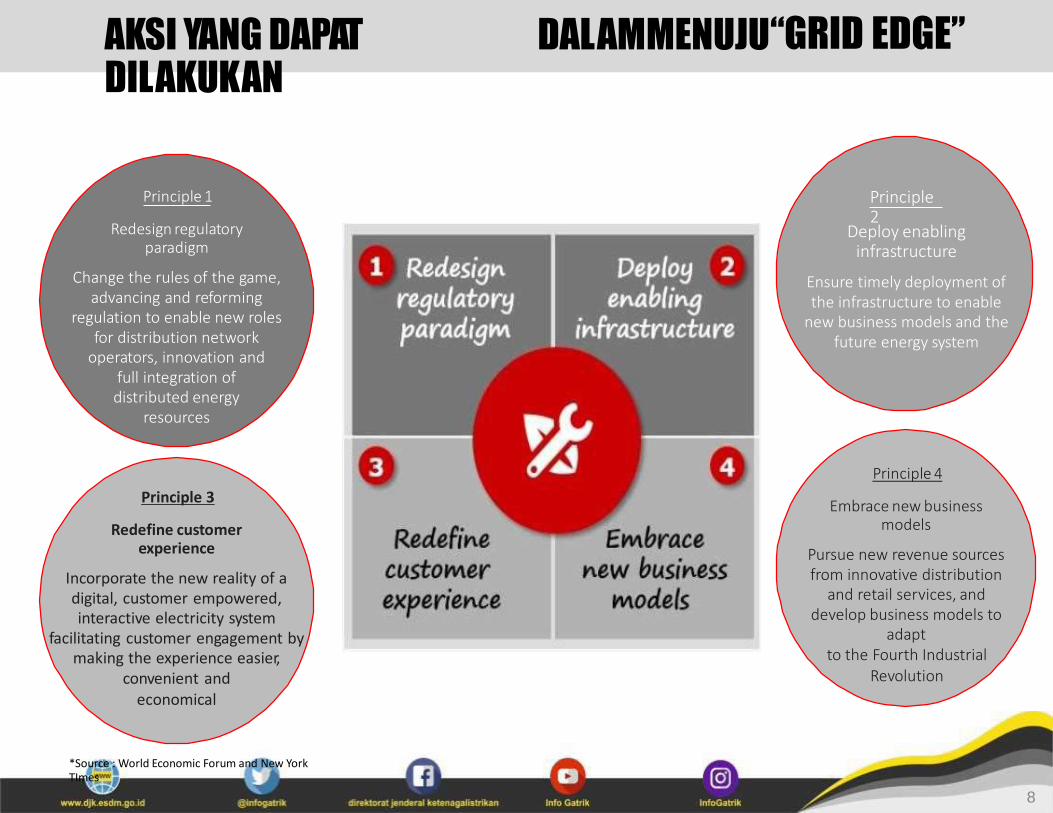

“GRID EDGE” AKSI YANG DAPAT DILAKUKAN

DALAM MENUJU

Principle 1 Principle 2

Redesign regulatory paradigm

Change the rules of the game, advancing and reforming

regulation to enable new roles for distribution network

operators, innovation and full integration of distributed energy

resources

Deploy enabling infrastructure

Ensure timely deployment of the infrastructure to enable

new business models and the future energy system

Principle 4 Principle 3 Embrace new business

models Pursue new revenue sources from innovative distribution

and retail services, and develop business models to

adapt to the Fourth Industrial