Embed Size (px)

Citation preview

May 2013 | Making Home Affordable

Making Home AffordableWorking Together to Help Homeowners

2May 2013 | Making Home Affordable

You will be able to print today’s presentation and listen to the Encore Replay this evening from HMPadmin.com

Learning Center =>Trusted Advisors=>Presentations=>Short Sale Workshop & Webinars

5/16: Short Sale Workshop –

Chicago, IL

Follow us on Twitter!! @MHA4Partners

3May 2013 | Making Home Affordable

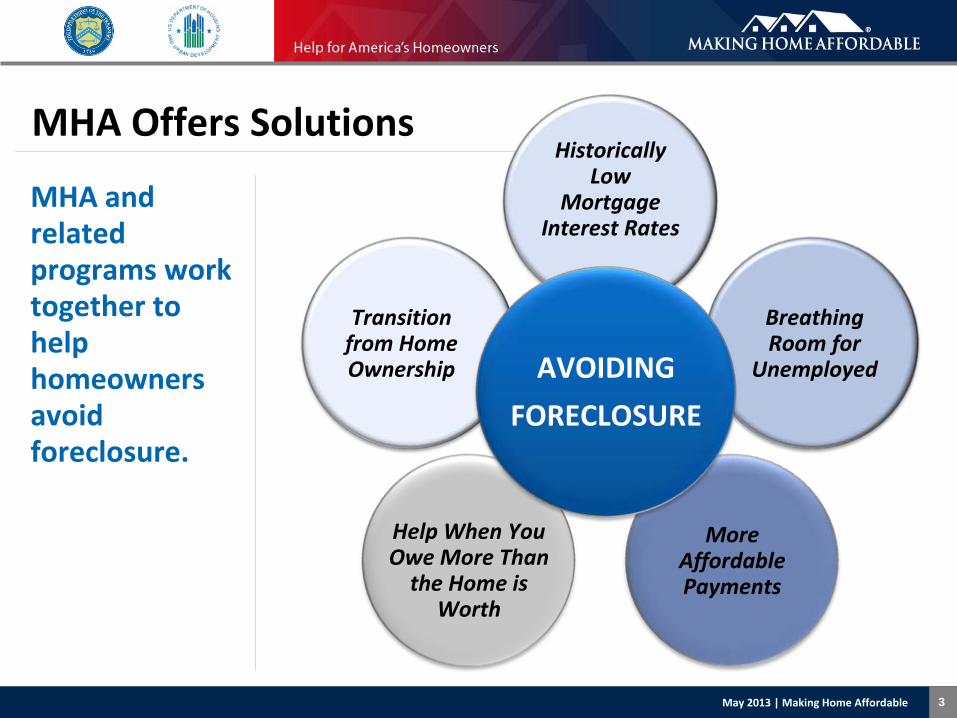

MHA and

related

programs work

together to

help

homeowners

avoid

foreclosure.

MHA Offers SolutionsHistorically

Low

Mortgage

Interest Rates

Breathing

Room for

Unemployed

More

Affordable

Payments

Help When You

Owe More Than

the Home is

Worth

Transition

from Home

Ownership AVOIDING

FORECLOSURE

4May 2013 | Making Home Affordable

Source: Making Home Affordable ProgramPerformance Report Through March 2013

MHA Provides Relief to Struggling Homeowners

MHA Foreclosure Avoidance ProgramsHomeowner

Assistance

Actions

MHA First Lien Modifications Started 1,306,119

Second Lien Modification Program (2MP) 109,313

Home Affordable Foreclosure Alternatives (HAFA) 140,434

Unemployment Program (UP) Forbearance Plans 32,154

Total 1,588,020

Nearly 1.6

million actions

taken to help

homeowners.

*Does not include 2.36 million Home Affordable Refinance Program (HARP) refinances through February 2013.

5May 2013 | Making Home Affordable

There’s Still Work to Do

While we see

signs of

recovery, many

families and

communities

continue to

struggle with

foreclosure.

Source: RealtyTrac

6May 2013 | Making Home Affordable

When the

weight of

homeownership

becomes too

great, there are

still options to

avoid

foreclosure.

HAFA Offers Transition from Homeownership

•

Home Affordable Foreclosure Alternatives

(HAFA) includes short sale and deed‐in‐lieu of

foreclosure (DIL). •

Think HAFA when:

Mortgage has become unaffordable, and

homeowner needs a way out.

Homeowner doesn’t qualify for

modification.

Modification doesn’t work out.

Homeowner has moved and needs to sell.

Path back to homeownership generally shorter from short sale than from foreclosure.

7May 2013 | Making Home Affordable

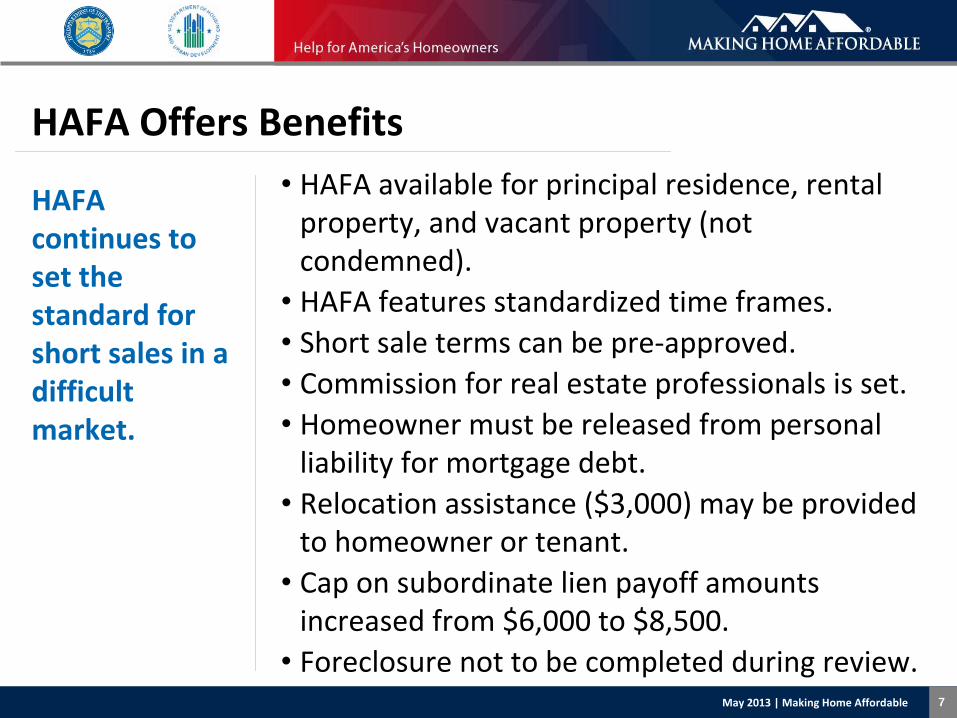

HAFA Offers Benefits

HAFA

continues to

set the

standard for

short sales in a

difficult

market.

•

HAFA available for principal residence, rental

property, and vacant property (not

condemned).•

HAFA features standardized time frames.

•

Short sale terms can be pre‐approved.•

Commission for real estate professionals is set.

•

Homeowner must be released from personal

liability for mortgage debt.•

Relocation assistance ($3,000) may be provided

to homeowner or tenant.•

Cap on subordinate lien payoff amounts

increased from $6,000 to $8,500.•

Foreclosure not to be completed during review.

8May 2013 | Making Home Affordable

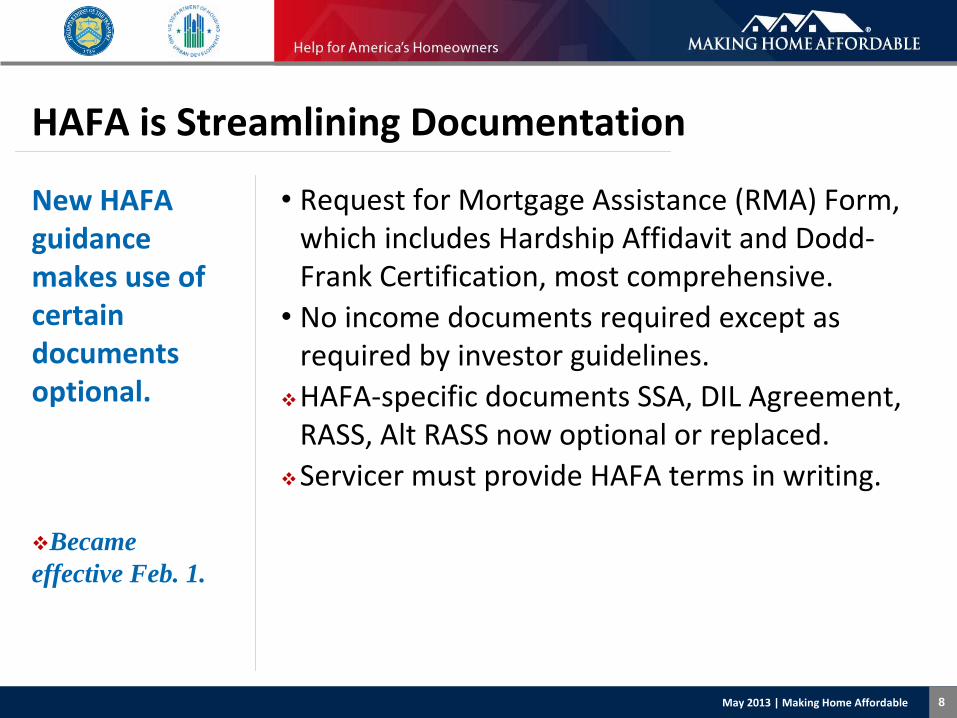

HAFA is Streamlining Documentation

New HAFA

guidance

makes use of

certain

documents

optional.

Became effective Feb. 1.

•

Request for Mortgage Assistance (RMA) Form,

which includes Hardship Affidavit and Dodd‐

Frank Certification, most comprehensive.•

No income documents required except as

required by investor guidelines.

HAFA‐specific documents SSA, DIL Agreement,

RASS, Alt RASS now optional or replaced.

Servicer must provide HAFA terms in writing.

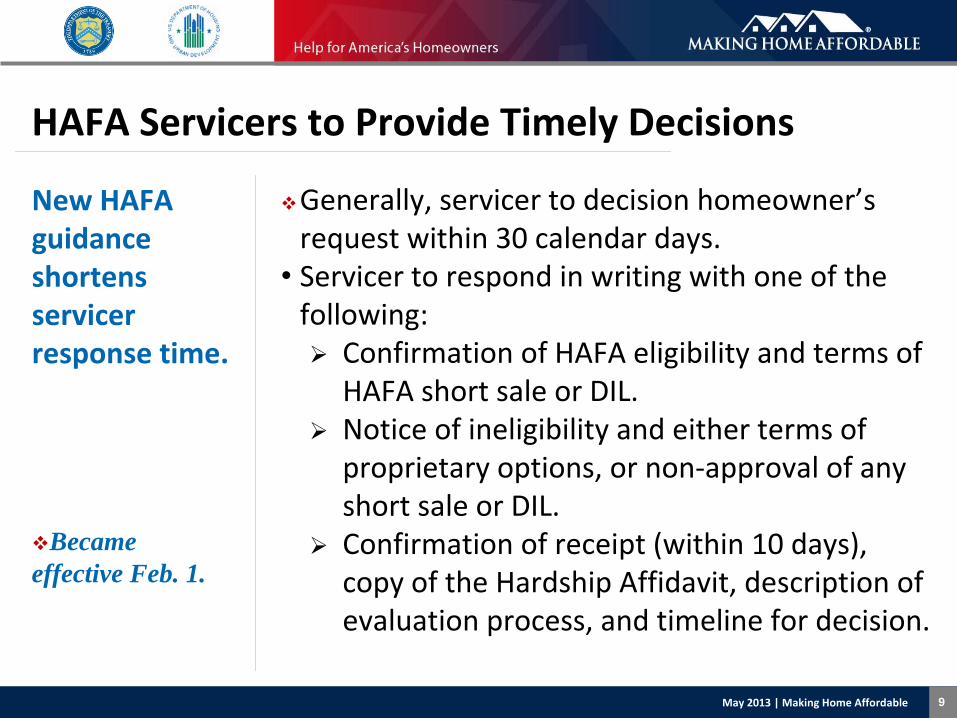

9May 2013 | Making Home Affordable

HAFA Servicers to Provide Timely Decisions

Generally, servicer to decision homeowner’s

request within 30 calendar days.•

Servicer to respond in writing with one of the

following:

Confirmation of HAFA eligibility and terms of

HAFA short sale or DIL.

Notice of ineligibility and either terms of

proprietary options, or non‐approval of any

short sale or DIL.

Confirmation of receipt (within 10 days),

copy of the Hardship Affidavit, description of

evaluation process, and timeline for decision.

New HAFA

guidance

shortens

servicer

response time.

Became effective Feb. 1.

10May 2013 | Making Home Affordable

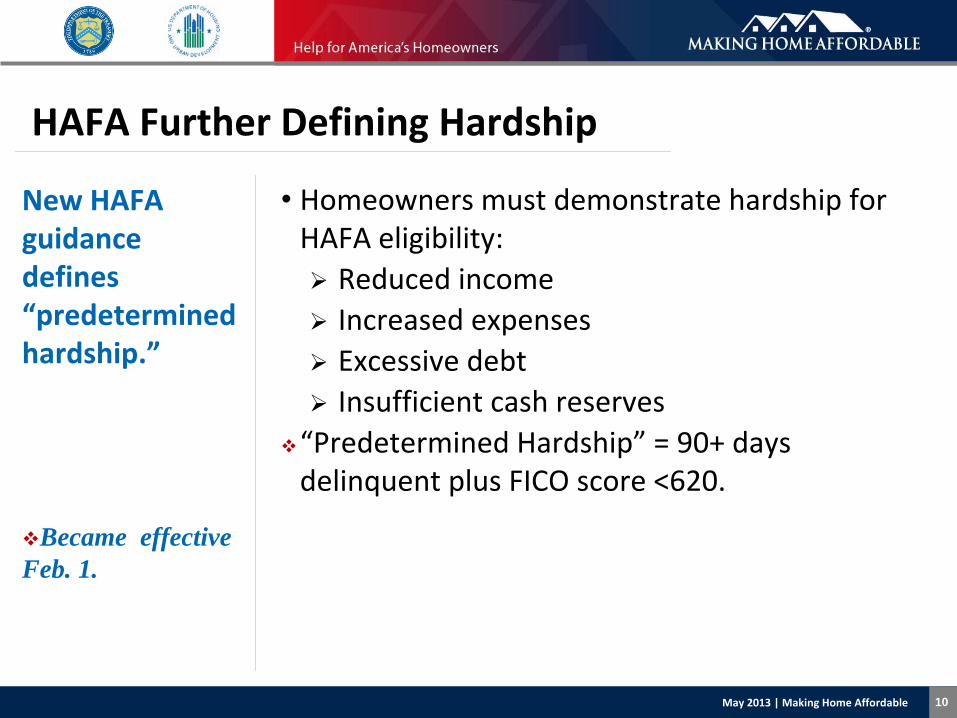

HAFA Further Defining Hardship

•

Homeowners must demonstrate hardship for

HAFA eligibility:

Reduced income

Increased expenses

Excessive debt

Insufficient cash reserves

“Predetermined Hardship”

= 90+ days

delinquent plus FICO score <620.

New HAFA

guidance

defines

“predetermined

hardship.”

Became effective Feb. 1.

11May 2013 | Making Home Affordable

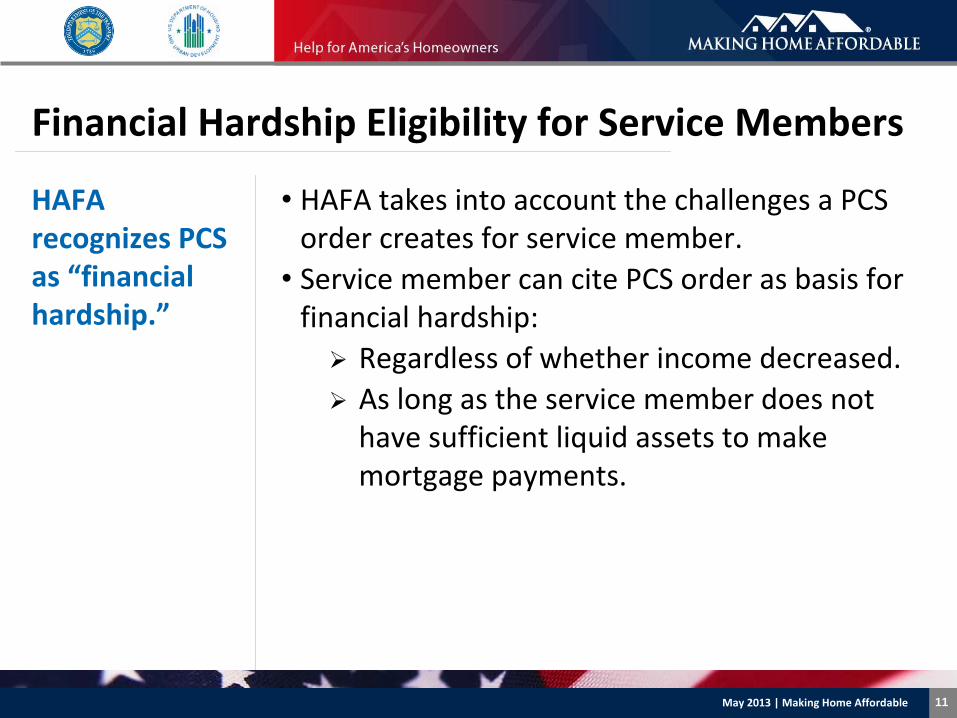

Financial Hardship Eligibility for Service Members

•

HAFA takes into account the challenges a PCS

order creates for service member.•

Service member can cite PCS order as basis for

financial hardship:

Regardless of whether income decreased.

As long as the service member does not

have sufficient liquid assets to make

mortgage payments.

HAFA

recognizes PCS

as “financial

hardship.”

12May 2013 | Making Home Affordable

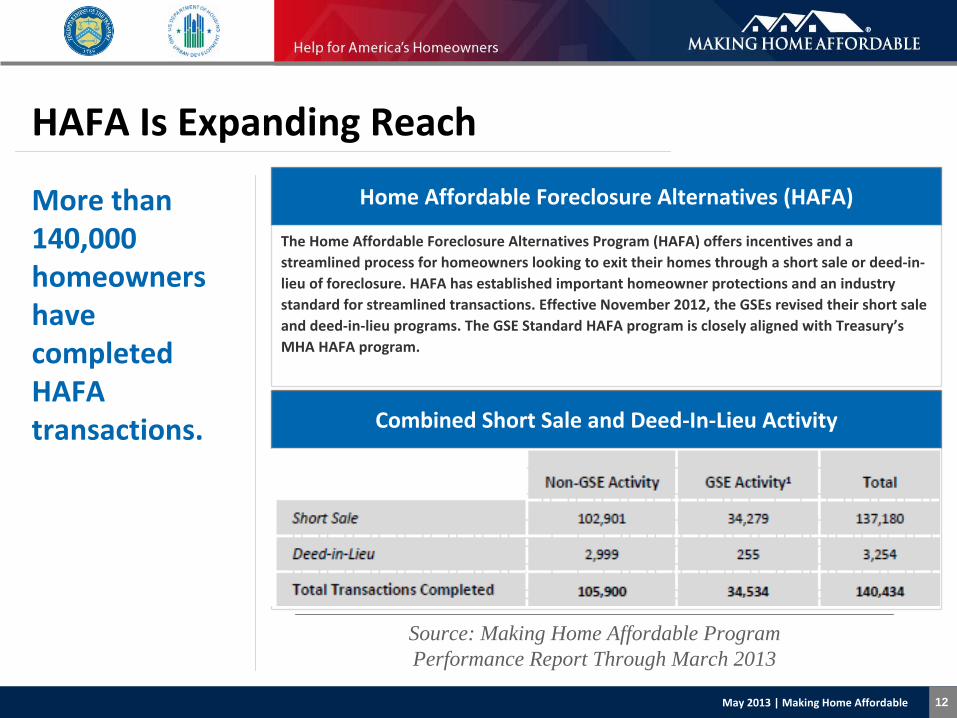

HAFA Is Expanding Reach

More than

140,000

homeowners

have

completed

HAFA

transactions.

Source: Making Home Affordable ProgramPerformance Report Through March 2013

Home Affordable Foreclosure Alternatives (HAFA)

The Home Affordable Foreclosure Alternatives Program (HAFA) offers incentives and a

streamlined process for homeowners looking to exit their homes through a short sale or deed‐in‐

lieu of foreclosure. HAFA has established important homeowner protections and an industry

standard for streamlined transactions. Effective November 2012, the GSEs

revised their short sale

and deed‐in‐lieu programs. The GSE Standard HAFA program is closely aligned with Treasury’s

MHA HAFA program.

Combined Short Sale and Deed‐In‐Lieu Activity

GSE Activity

13May 2013 | Making Home Affordable

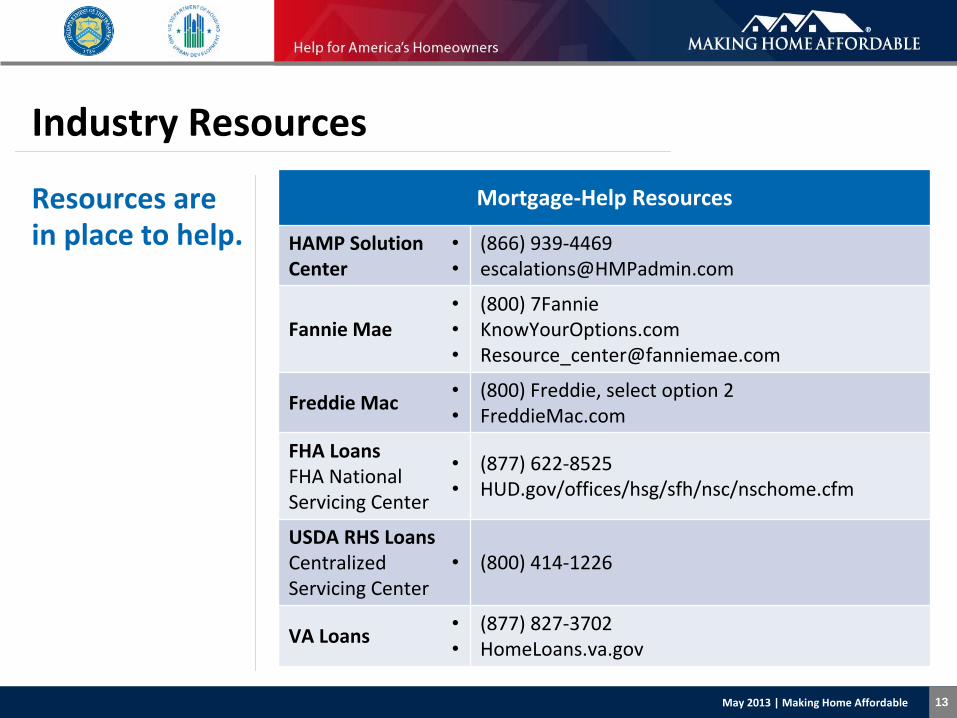

Industry Resources

Resources are

in place to help.Mortgage‐Help Resources

HAMP Solution

Center

• (866) 939‐4469• [email protected]

Fannie Mae• (800) 7Fannie• KnowYourOptions.com• [email protected]

Freddie Mac• (800) Freddie, select option 2 • FreddieMac.com

FHA LoansFHA National

Servicing Center

• (877) 622‐8525• HUD.gov/offices/hsg/sfh/nsc/nschome.cfm

USDA RHS LoansCentralized

Servicing Center

• (800) 414‐1226

VA Loans• (877) 827‐3702• HomeLoans.va.gov

14May 2013 | Making Home Affordable

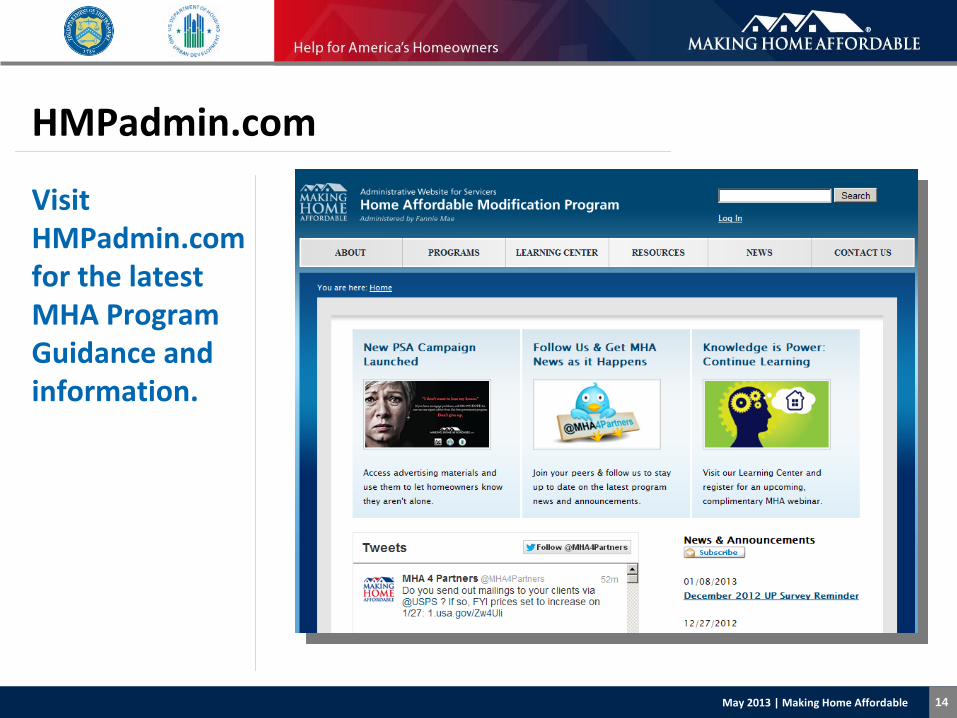

HMPadmin.com

Visit

HMPadmin.com

for the latest

MHA Program

Guidance and

information.

15May 2013 | Making Home Affordable

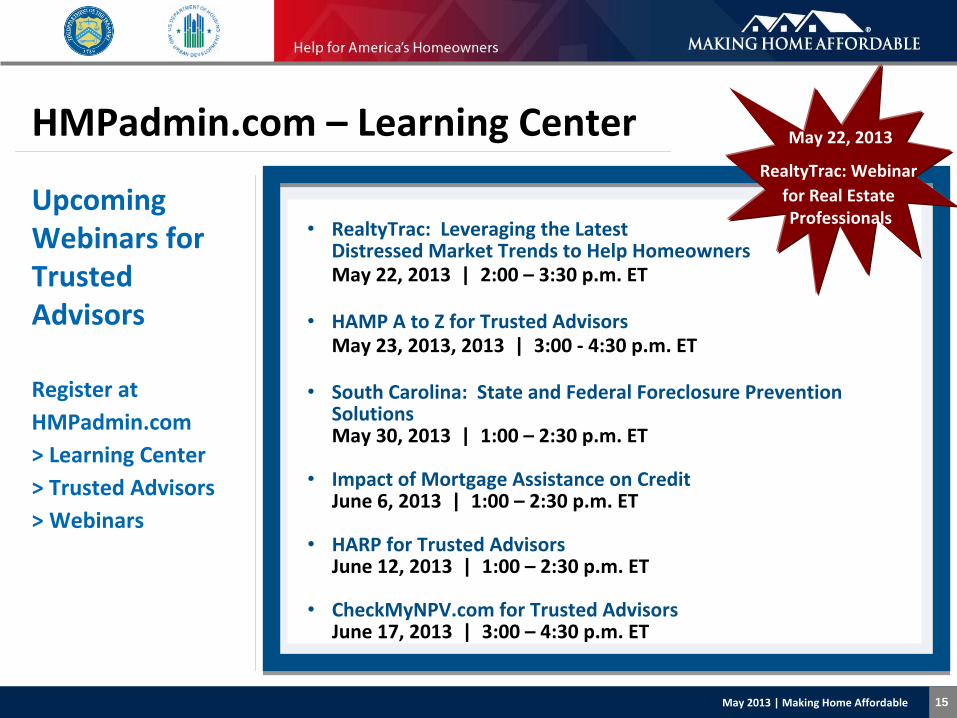

HMPadmin.com

–

Learning Center

Upcoming

Webinars for

Trusted

Advisors

Register at

HMPadmin.com

> Learning Center

> Trusted Advisors

> Webinars

•

RealtyTrac: Leveraging the Latest Distressed Market Trends to Help Homeowners May 22, 2013 | 2:00 – 3:30 p.m. ET

•

HAMP A to Z for Trusted Advisors

May 23, 2013, 2013 | 3:00 ‐

4:30 p.m. ET

•

South Carolina: State and Federal Foreclosure Prevention

Solutions

May 30, 2013 | 1:00 – 2:30 p.m. ET

•

Impact of Mortgage Assistance on Credit

June 6, 2013 | 1:00 – 2:30 p.m. ET

•

HARP for Trusted Advisors

June 12, 2013 | 1:00 – 2:30 p.m. ET

•

CheckMyNPV.com

for Trusted Advisors

June 17, 2013 | 3:00 – 4:30 p.m. ET

May 22, 2013

RealtyTrac: Webinar for Real Estate Professionals

16May 2013 | Making Home Affordable

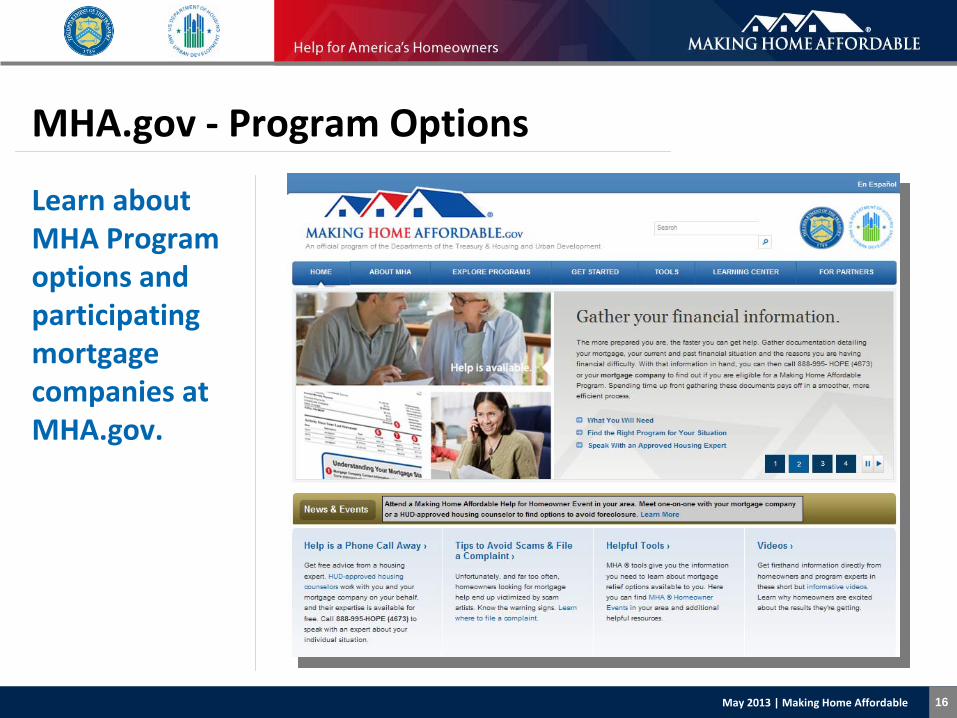

Learn about

MHA Program

options and

participating

mortgage

companies at

MHA.gov.

MHA.gov

‐

Program Options

17May 2013 | Making Home Affordable

MHAStorefront.com

Order MHA

brochures and

posters. Have

them shipped

to you at no

cost.

18May 2013 | Making Home Affordable

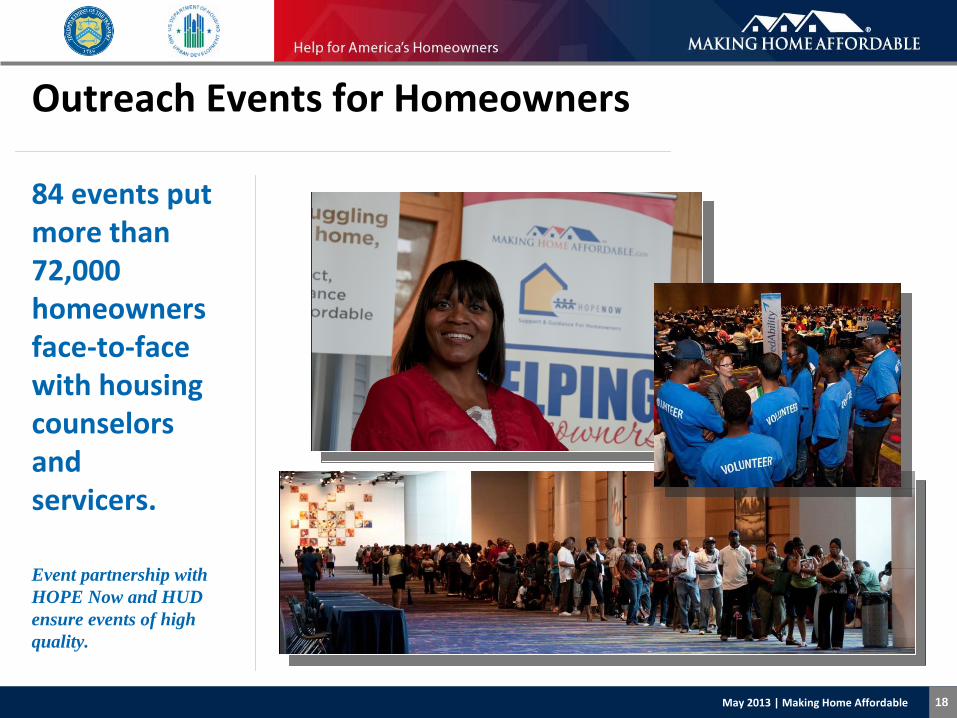

84 events put

more than

72,000

homeowners

face‐to‐face

with housing

counselors

and

servicers.

Event partnership with HOPE Now and HUD ensure events of high quality.

Outreach Events for Homeowners

19May 2013 | Making Home Affordable

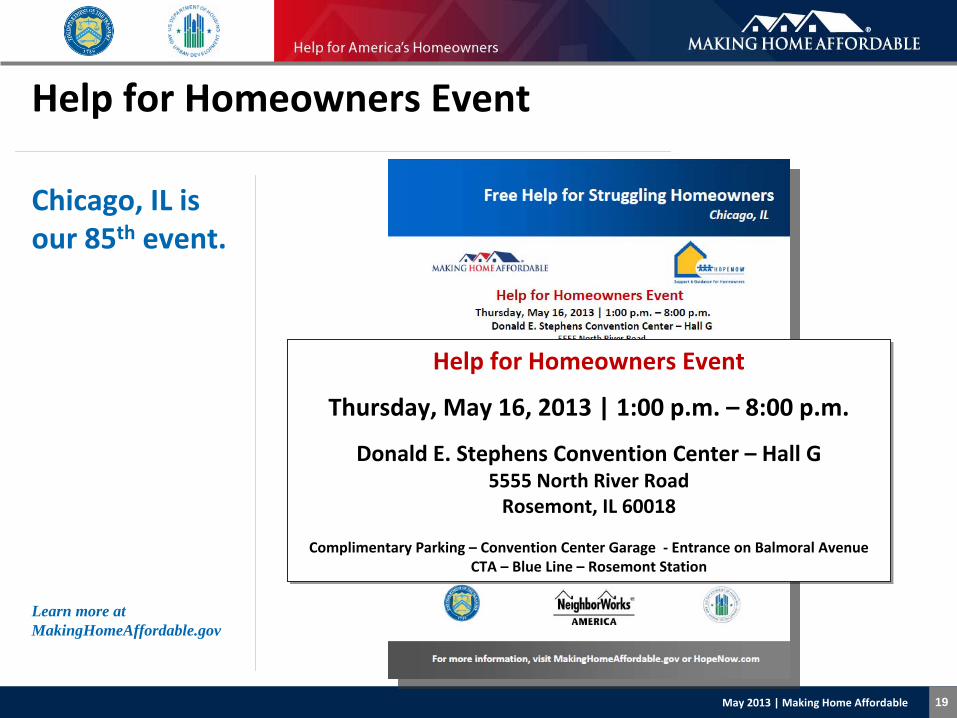

Chicago, IL is

our 85th

event.

Learn more at MakingHomeAffordable.gov

Help for Homeowners Event

Help for Homeowners Event

Thursday, May 16, 2013 | 1:00 p.m. – 8:00 p.m.

Donald E. Stephens Convention Center – Hall G5555 North River RoadRosemont, IL 60018

Complimentary Parking – Convention Center Garage ‐

Entrance on Balmoral

AvenueCTA – Blue Line – Rosemont Station

Help for Homeowners Event

Thursday, May 16, 2013 | 1:00 p.m. – 8:00 p.m.

Donald E. Stephens Convention Center – Hall G5555 North River RoadRosemont, IL 60018

Complimentary Parking – Convention Center Garage ‐

Entrance on Balmoral

AvenueCTA –

Blue Line – Rosemont Station

SHORT SALE PROGRAM

Page 21

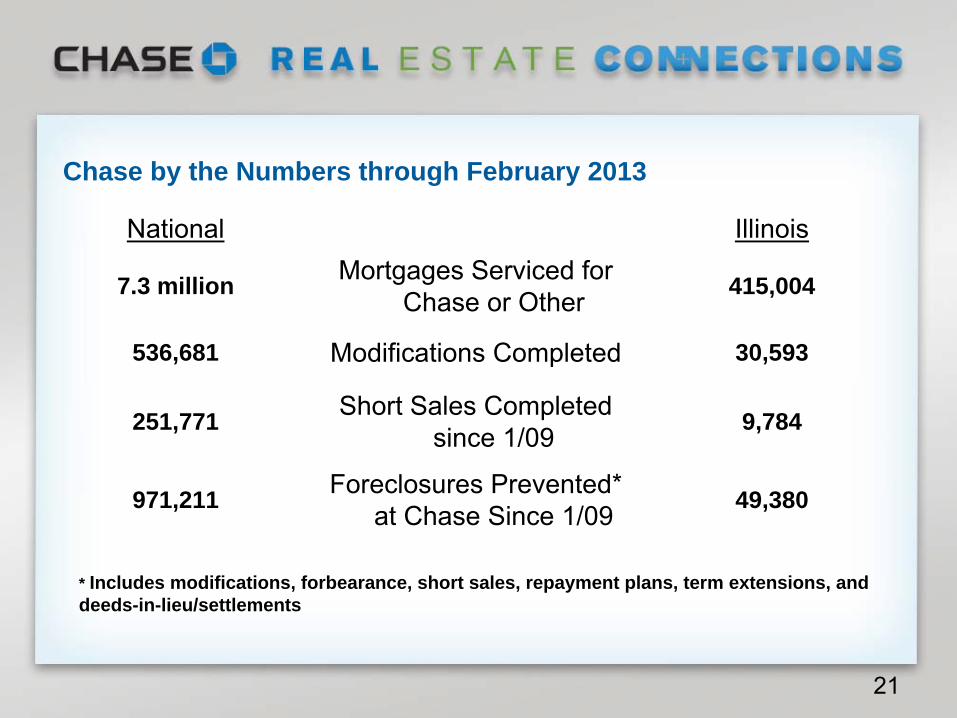

Chase by the Numbers through February 2013

* Includes modifications, forbearance, short sales, repayment plans, term extensions, and deeds-in-lieu/settlements

National Illinois

7.3 million Mortgages Serviced for Chase or Other 415,004

536,681 Modifications Completed 30,593

251,771 Short Sales Completed since 1/09 9,784

971,211 Foreclosures Prevented* at Chase Since 1/09 49,380

21

Page 22

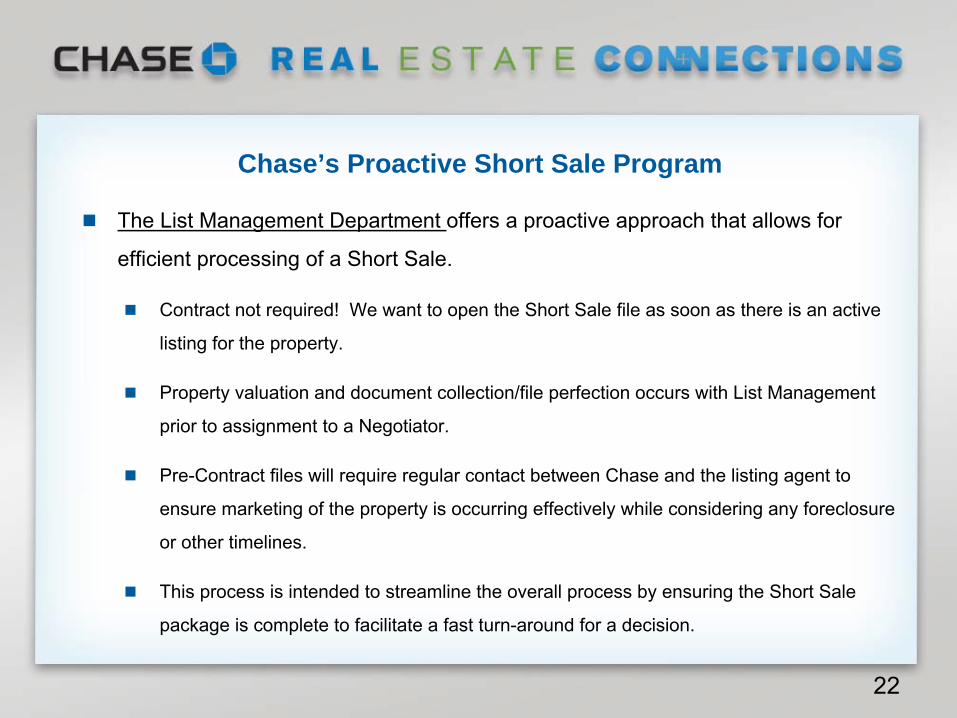

The List Management Department offers a proactive approach that allows for

efficient processing of a Short Sale.

Contract not required! We want to open the Short Sale file as soon as there is an active

listing for the property.

Property valuation and document collection/file perfection occurs with List Management

prior to assignment to a Negotiator.

Pre-Contract files will require regular contact between Chase and the listing agent to

ensure marketing of the property is occurring effectively while considering any foreclosure

or other timelines.

This process is intended to streamline the overall process by ensuring the Short Sale

package is complete to facilitate a fast turn-around for a decision.

22

Chase’s Proactive Short Sale Program

Page 23

Short Sale – Financing and Timing

It is essential to initiate the buyer’s loan approval process early for non-cash

transactions to avoid delays in closing

Once the short sale is approved, it may take up to 90 days to close if a buyer does

not have a strong pre-approval and an early start with financing

A primary cause for approved short sales not completing is failure of the buyer to

secure financing

If the transaction does not complete, the file will remain active with our List

Management Department while listed on the MLS.

Having well-qualified, pre-approved back-up buyers is essential!

23

Page 24

What Can You Do to Help With a Short Sale?

Use Equator. Chase began roll-out on October 5.

All files are in Equator as of 12/15/12.

Full capability for customers and real estate agents to upload:

•

Third party authorizations

•

Listing agreements and agreements of sale

•

HUD-1 settlement statements

•

Financial documentation•

Obtain transaction status updates and communicate directly with negotiators through the portal, minimizing phone traffic and outside email

24

Page 25

What Can You Do to Help With a Short Sale?

Set reasonable

expectations regarding timelines and valuations.

Know your seller. Properly pre-approve

your buyer!

Submit complete

short sale request prior to receiving a contract or at time of listing -

do not wait for a buyer! Start the process!

Maintain regular contact with Chase and return required documents promptly (within

3 days of request).

Escalate when necessary.

Ensure proposed transaction is “at arm’s length”

and there is no potential conflict of

interest.

Partnership with your Mortgage Banker is critical!

25

Page 26

Chase Short Sale Resources

Short Sale Hotline: 866-233-5320

chase.com/avoidforeclosure

Chase Homeownership Centers:

●

Locate Chase Homeownership Centers at chase.com/MyHome

26

Page 27

Disclosures

This material is intended for home lending professionals or nonprofit, HUD-approved, housing counselors and not for distribution to consumers. This document is not an advertisement for consumer credit as defined in 12 CFR 1026.2(a)(2).

All home lending products are subject to credit and property approval. Rates, program terms and conditions are subject to change without notice. Not all products are available in all states or for all dollar amounts. Other restrictions and limitations apply.

Information presented is for informational purposes only. It is believed to be reliable, but Chase does not warrant its completeness, timeliness or accuracy.

Home lending and deposit products offered by JPMorgan Chase Bank

N.A. Member FDIC.

©

2012 JPMorgan Chase & Co.

27

“All About Short Sales” A guide to working with Wells Fargo

Pierre Gelinas

Short Sale Manager

Live Workshop and Webinar for Real Estate

Professionals

May 16th, 2013 Chicago, IL

Wells Fargo’s objectives

Wells Fargo’s primary concern and obligation is to our customers and investors.

Our real estate agents’ expertise helps us to:

Deliver timely solutions to assist customers

Minimize losses to investors

Help to rebuild and stabilize our communities

It is critical that we work together to help in the recovery of a strong housing market.

29

303030

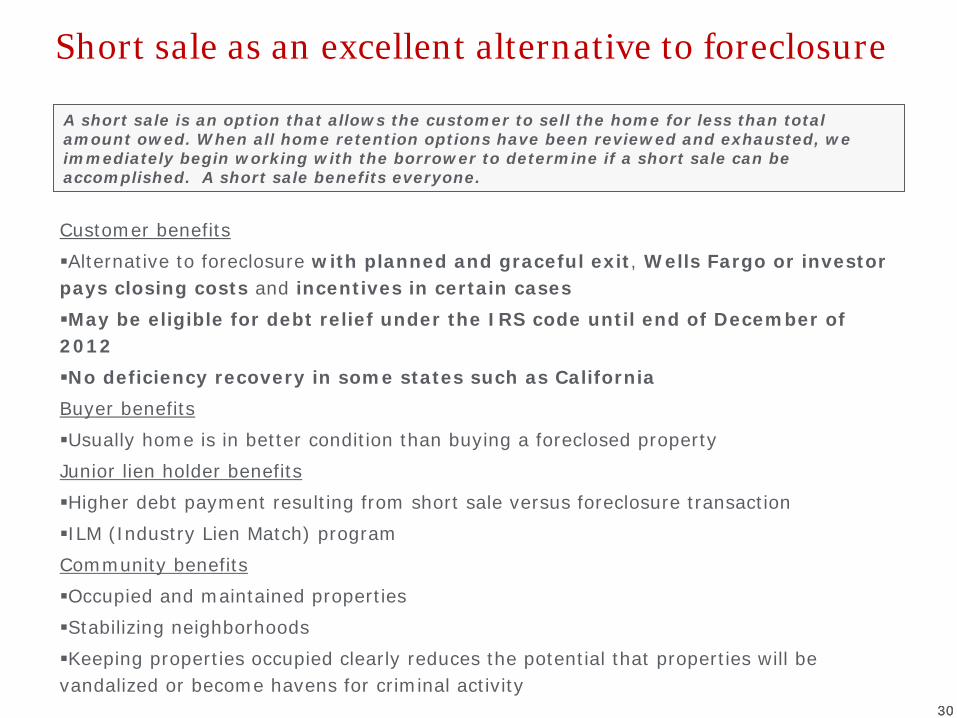

Short sale as an excellent alternative to foreclosure

Customer benefits

Alternative to foreclosure with planned and graceful exit, Wells Fargo or investor pays closing costs and incentives in certain cases

May be eligible for debt relief under the IRS code until end of December of 2012

No deficiency recovery in some states such as California

Buyer benefits

Usually home is in better condition than buying a foreclosed property

Junior lien holder benefits

Higher debt payment resulting from short sale versus foreclosure transaction

ILM (Industry Lien Match) program

Community benefits

Occupied and maintained properties

Stabilizing neighborhoods

Keeping properties occupied clearly reduces the potential that properties will be vandalized or become havens for criminal activity

A short sale is an option that allows the customer to sell the home for less than total amount owed. When all home retention options have been reviewed and exhausted, we immediately begin working with the borrower to determine if a short sale can be accomplished. A short sale benefits everyone.

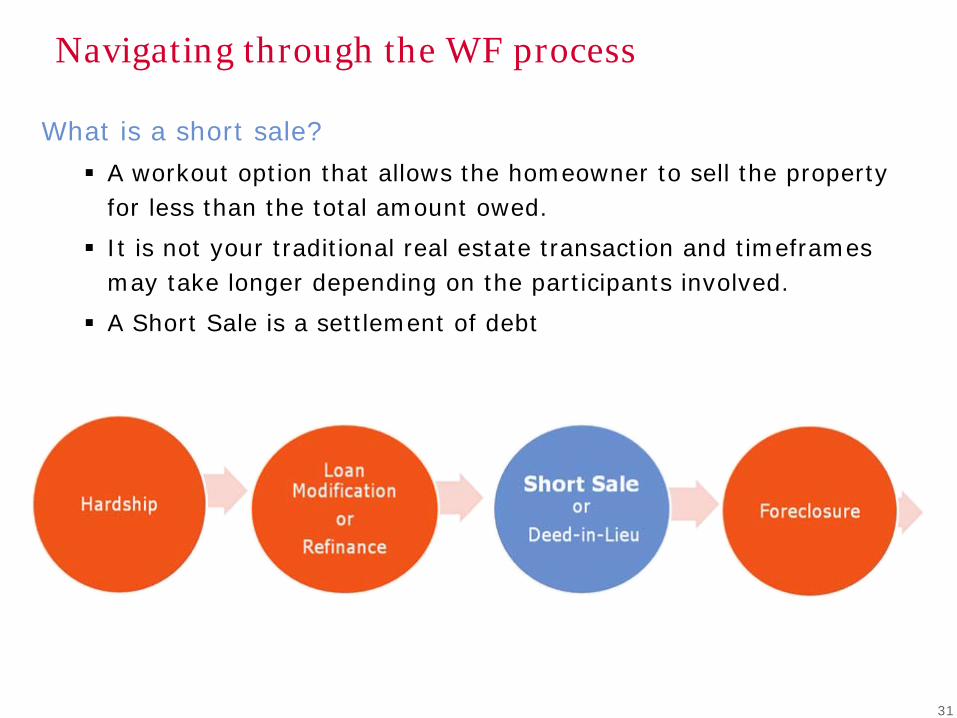

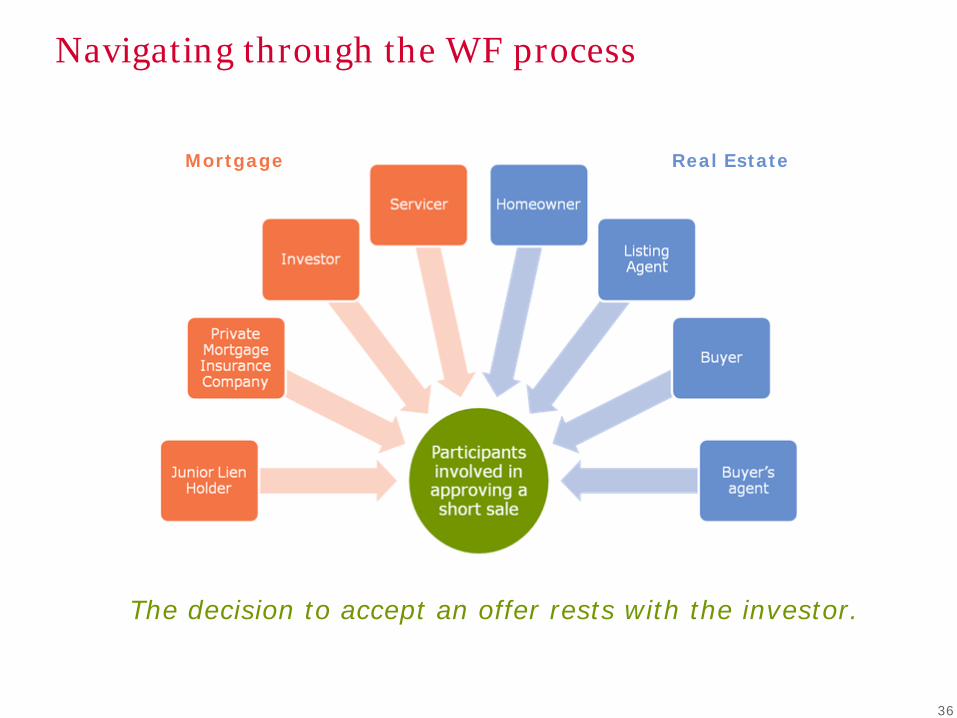

Navigating through the WF process

31

What is a short sale?

A workout option that allows the homeowner to sell the property for less than the total amount owed.

It is not your traditional real estate transaction and timeframes may take longer depending on the participants involved.

A Short Sale is a settlement of debt

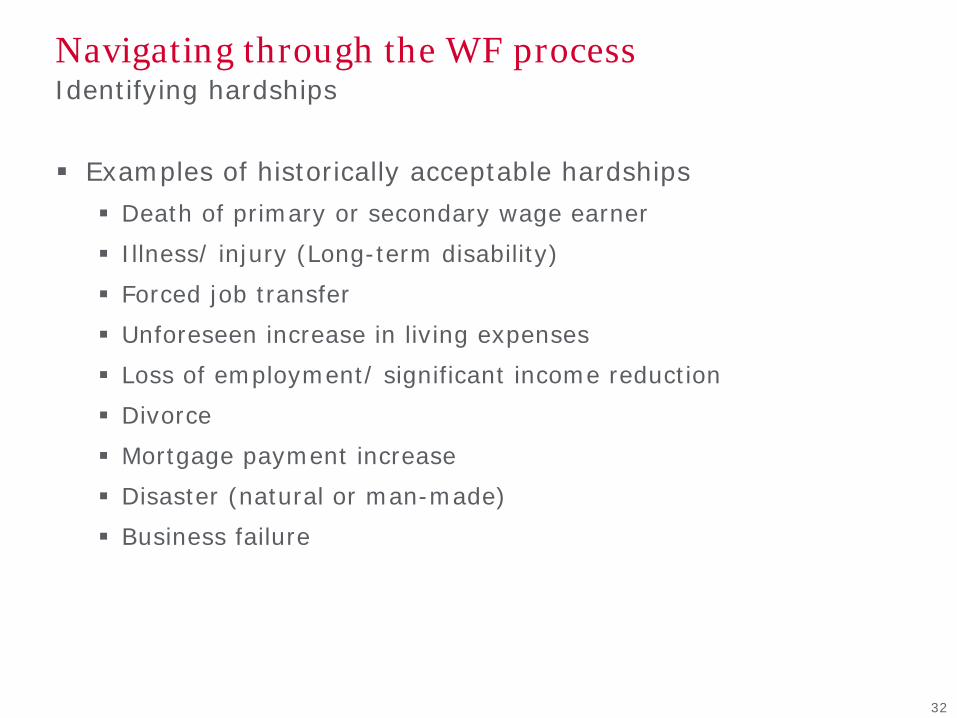

Navigating through the WF process Identifying hardships

Examples of historically acceptable hardships

Death of primary or secondary wage earner

Illness/ injury (Long-term disability)

Forced job transfer

Unforeseen increase in living expenses

Loss of employment/ significant income reduction

Divorce

Mortgage payment increase

Disaster (natural or man-made)

Business failure

32

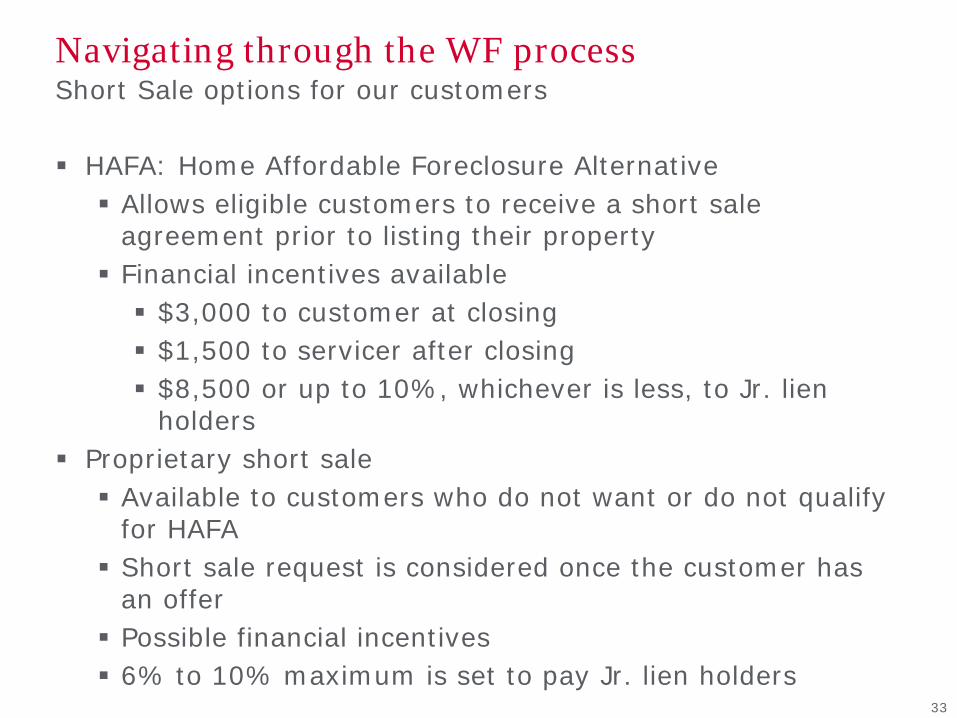

Navigating through the WF process Short Sale options for our customers

HAFA: Home Affordable Foreclosure Alternative

Allows eligible customers to receive a short sale agreement prior to listing their property

Financial incentives available

$3,000 to customer at closing

$1,500 to servicer after closing

$8,500 or up to 10%, whichever is less, to Jr. lien holders

Proprietary short sale

Available to customers who do not want or do not qualify for HAFA

Short sale request is considered once the customer has an offer

Possible financial incentives

6% to 10% maximum is set to pay Jr. lien holders33

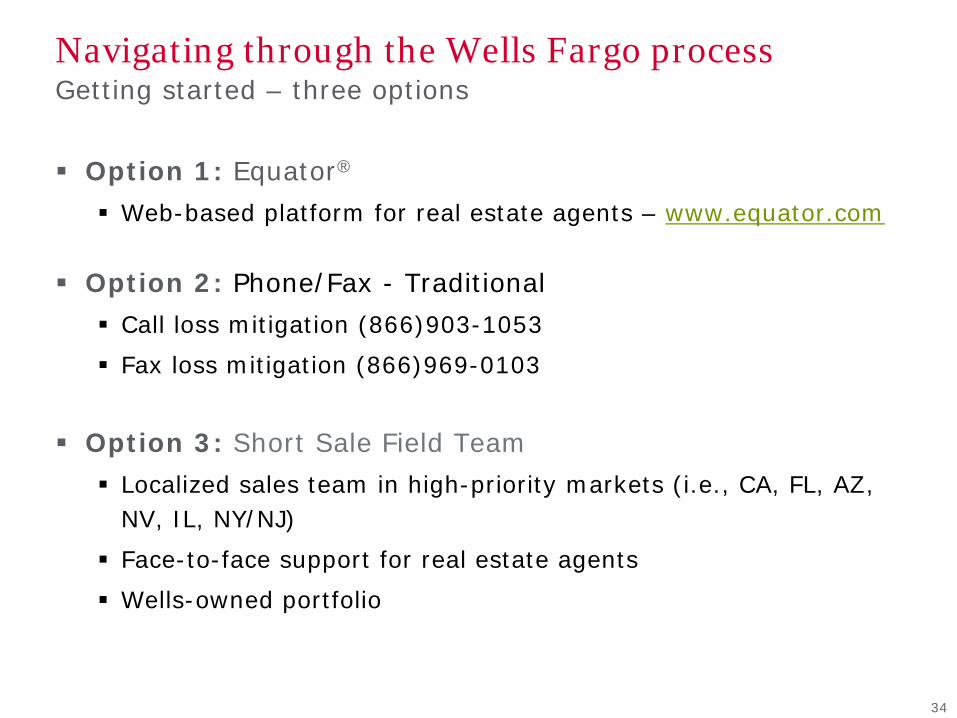

Navigating through the Wells Fargo process Getting started – three options

Option 1: Equator®

Web-based platform for real estate agents – www.equator.com

Option 2: Phone/Fax - Traditional

Call loss mitigation (866)903-1053

Fax loss mitigation (866)969-0103

Option 3: Short Sale Field Team

Localized sales team in high-priority markets (i.e., CA, FL, AZ, NV, IL, NY/NJ)

Face-to-face support for real estate agents

Wells-owned portfolio

34

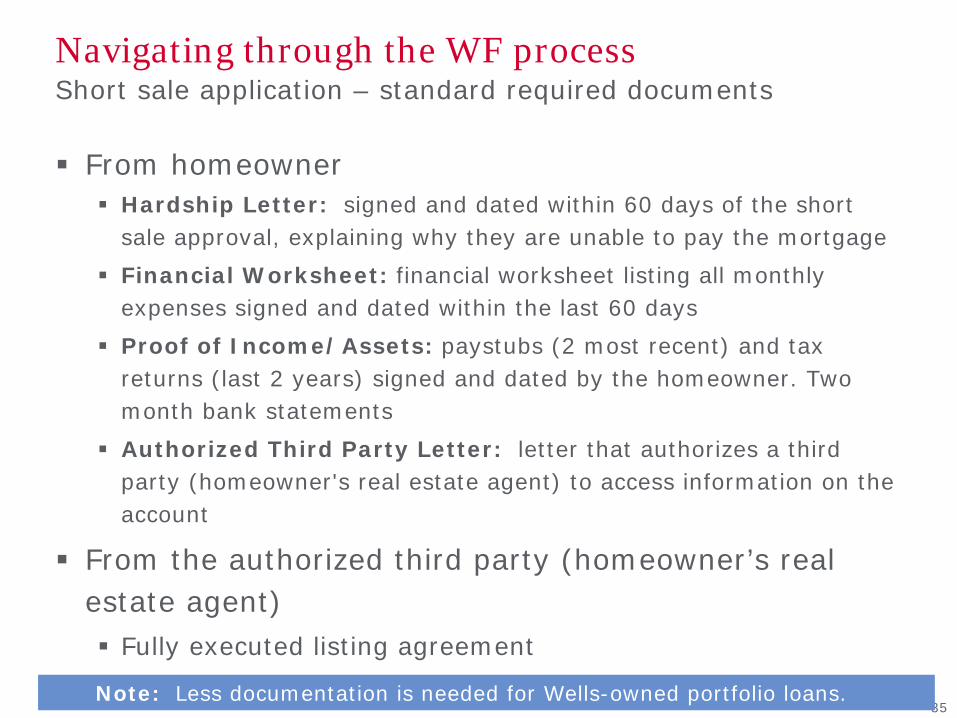

Navigating through the WF process Short sale application – standard required documents

From homeowner

Hardship Letter: signed and dated within 60 days of the short sale approval, explaining why they are unable to pay the mortgage

Financial Worksheet: financial worksheet listing all monthly expenses signed and dated within the last 60 days

Proof of Income/Assets: paystubs (2 most recent) and tax returns (last 2 years) signed and dated by the homeowner. Two month bank statements

Authorized Third Party Letter: letter that authorizes a third party (homeowner's real estate agent) to access information on the account

From the authorized third party (homeowner’s real estate agent)

Fully executed listing agreement

Estimated HUD-135

Note: Less documentation is needed for Wells-owned portfolio loans.

Navigating through the WF process

36

The decision to accept an offer rests with the investor.

Mortgage Real Estate

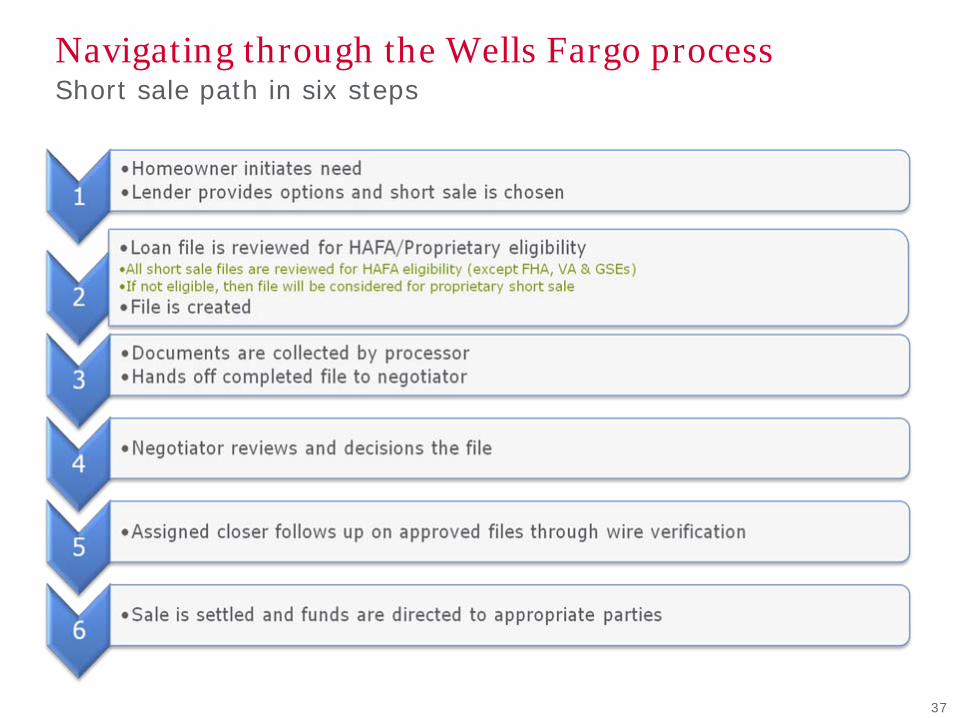

Navigating through the Wells Fargo process Short sale path in six steps

37

Wells Fargo Online Agent Resource Center

38

New robust online agent content launched September 14th

Provides short sale educational materials, downloadable information and other resources www.wellsfargo.com/shortsaleagent

39

Agent resources

Short Sale Manager – FHA and Portfolio specialist

Pierre Gelinas, 312-909-6584, [email protected]

Real estate agent hotline for loan servicing default liquidation escalations

1-877-841-5301

7AM – 10PM CST Mon – Fri

May 2013

Kamara McMullen–

AVP Short Sales

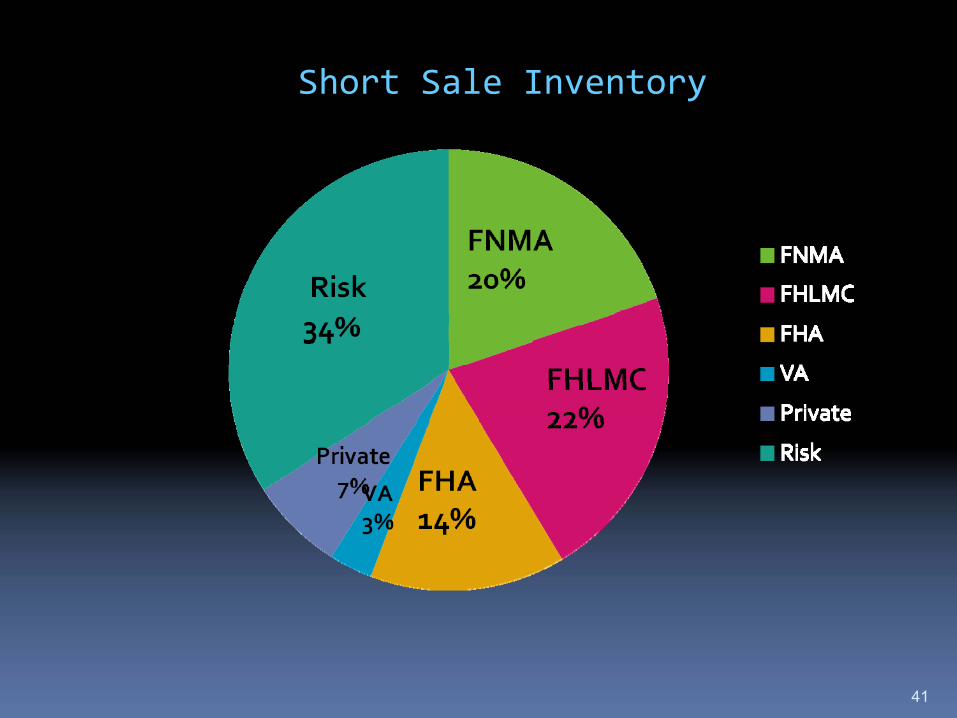

Short Sale Inventory

41

Key Items For Citi

2013

Streamline Programs

Specialized Teams

Expanded Comprehensive Short Sale Training

Current Eligibility

Pre‐approved Short Sale

42

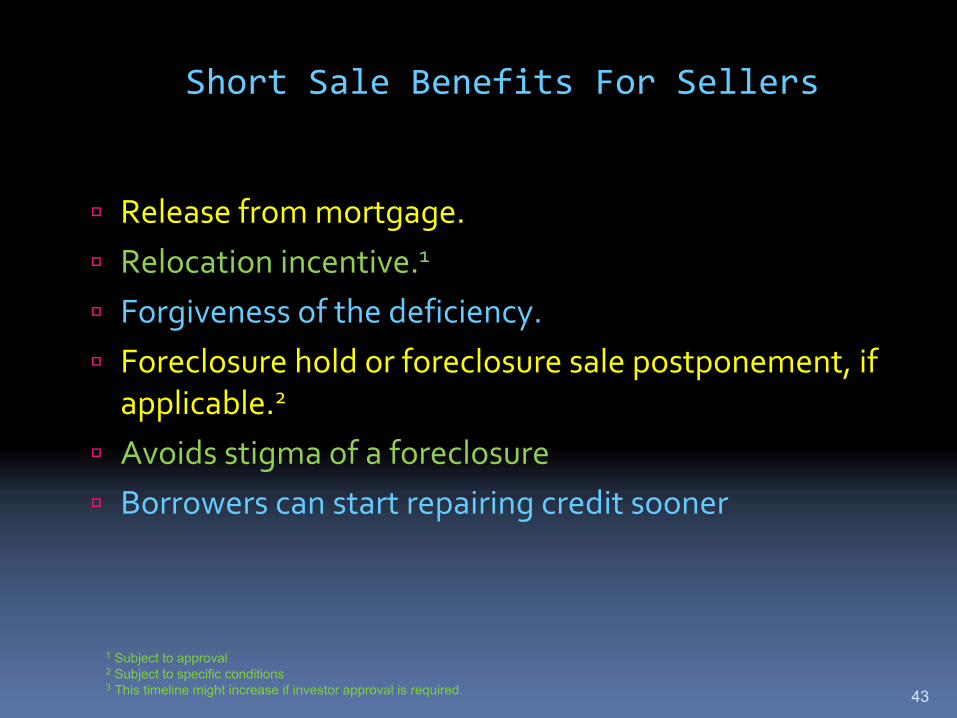

Short Sale Benefits For Sellers

Release from mortgage.

Relocation incentive.1

Forgiveness of the deficiency.

Foreclosure hold or foreclosure sale postponement, if

applicable.2

Avoids stigma of a foreclosure

Borrowers can start repairing credit sooner

43

1

Subject to approval2

Subject to specific conditions3

This timeline might increase if investor approval is required.

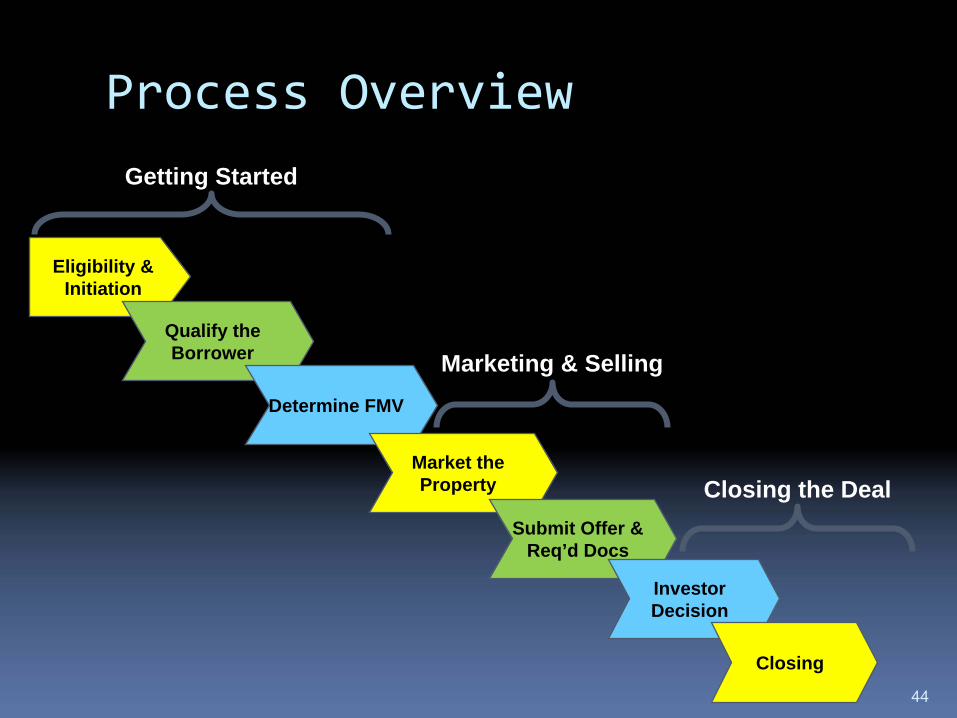

Process Overview

44

Eligibility & Initiation

Qualify the Borrower

Determine FMV

Market the Property

Submit Offer & Req’d Docs

Investor Decision

Closing

Getting Started

Marketing & Selling

Closing the Deal

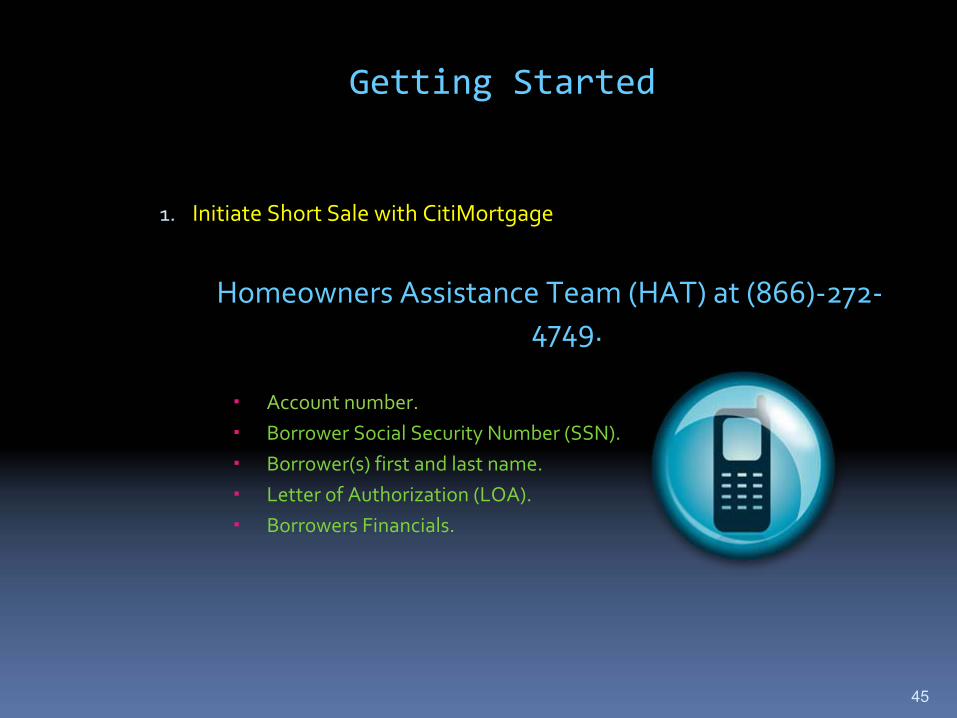

Getting Started

1.

Initiate Short Sale with CitiMortgage

Homeowners Assistance Team (HAT) at (866)‐272‐

4749.

Account number.

Borrower Social Security Number (SSN).

Borrower(s) first and last name.

Letter of Authorization (LOA).

Borrowers Financials.

45

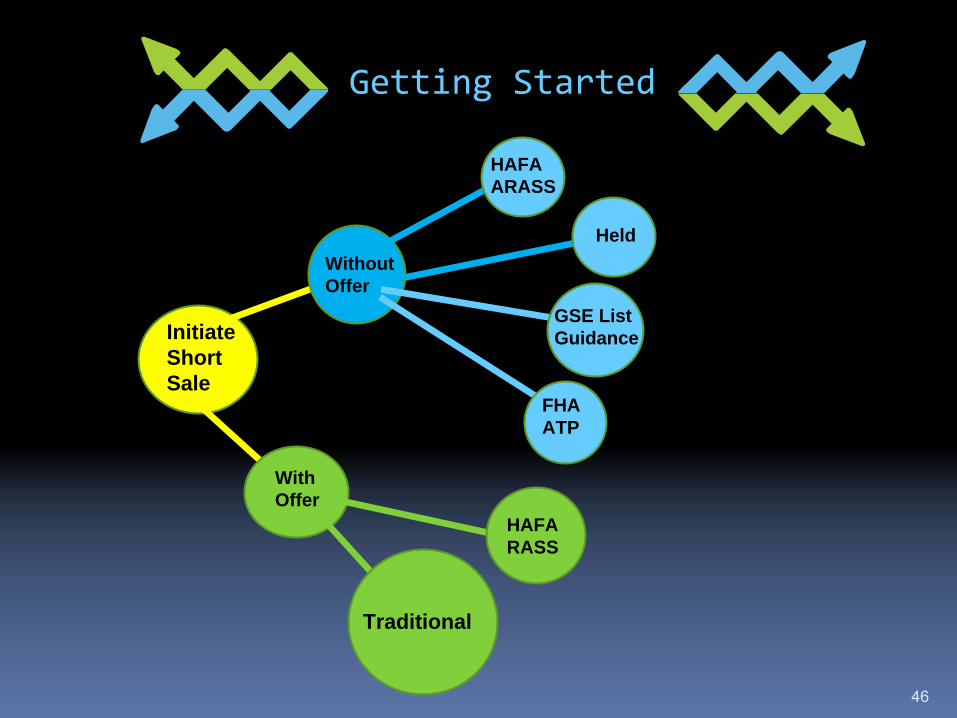

Getting Started

46

Initiate Short Sale

Without Offer

With Offer

HAFA ARASS

Held

FHA ATP

HAFA RASS

Traditional

GSE List Guidance

Getting Started

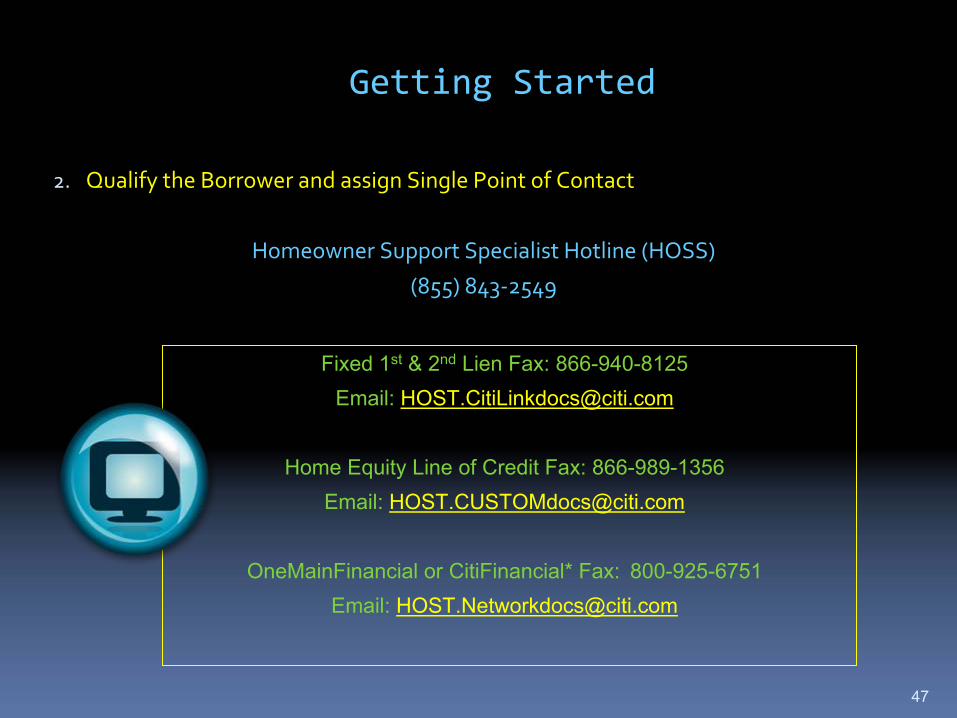

2.

Qualify the Borrower and assign Single Point of Contact

Homeowner Support Specialist Hotline (HOSS) (855) 843‐2549

47

Fixed 1st

& 2nd

Lien Fax: 866-940-8125Email: [email protected]

Home Equity Line of Credit Fax: 866-989-1356Email: [email protected]

OneMainFinancial

or CitiFinancial* Fax:

800-925-6751Email: [email protected]

Getting Started

3.

Determine Fair

Market Value

48

Marketing & Selling

4. Market the

property

49

Marketing & Selling

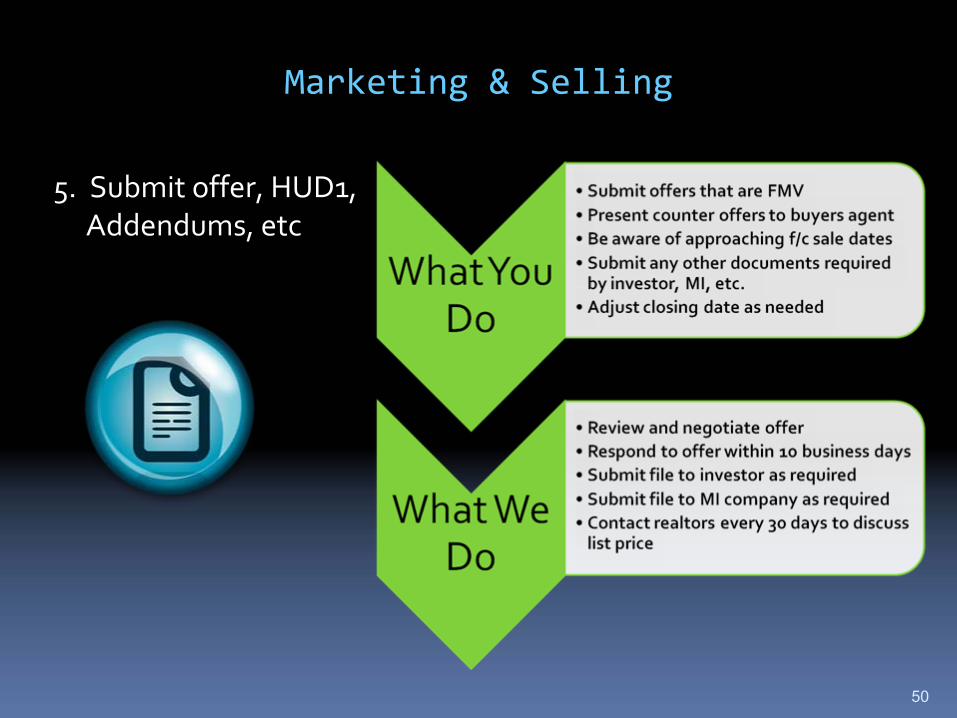

5. Submit offer, HUD1,

Addendums, etc

50

Closing the Deal

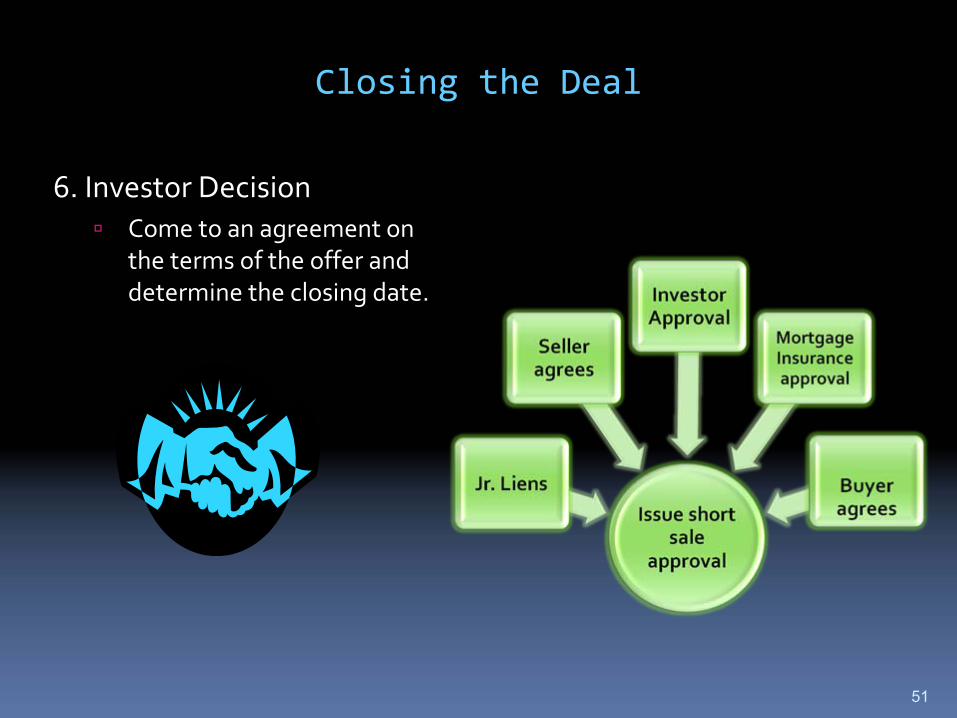

6. Investor Decision

Come to an agreement on

the terms of the offer and

determine the closing date.

51

Closing the Deal

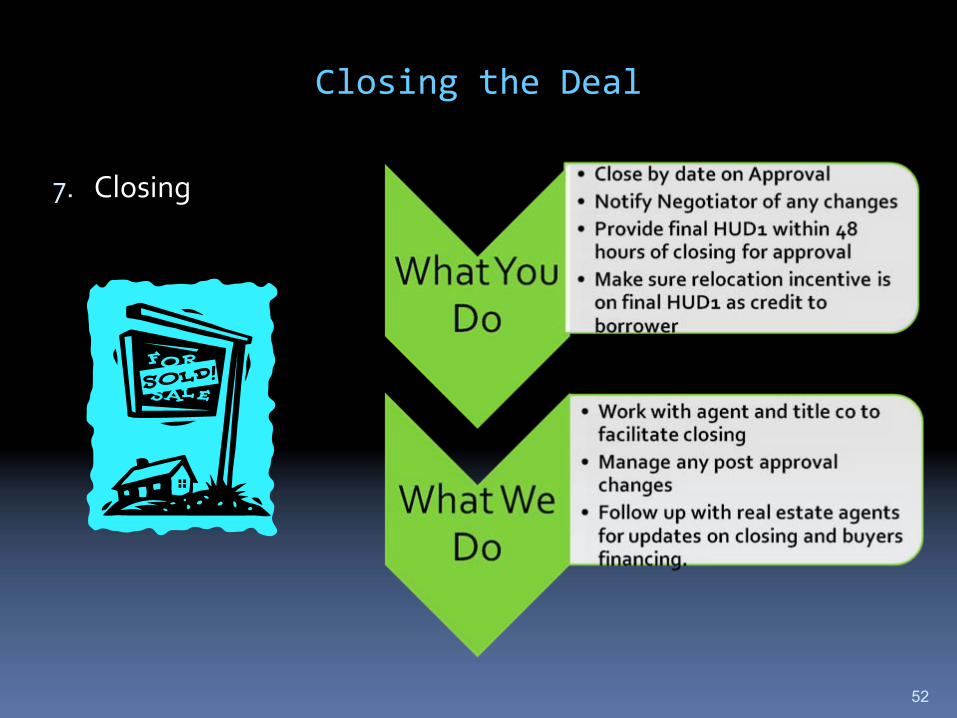

7.

Closing

52

Key Numbers

RECOVERY: (800) 824‐9907

INITIATE: Homeowners Assistance Team (HAT) at (866)‐272‐

4749

SPOC: Homeowner Support Specialist Hotline (HOSS)

(855) 843‐2549

ESCALATE: Short Sale Hotline 1‐866‐520‐5499

Information to Help You and Your Clients in the Short Sale Process

May 2013

Understanding Short Sales

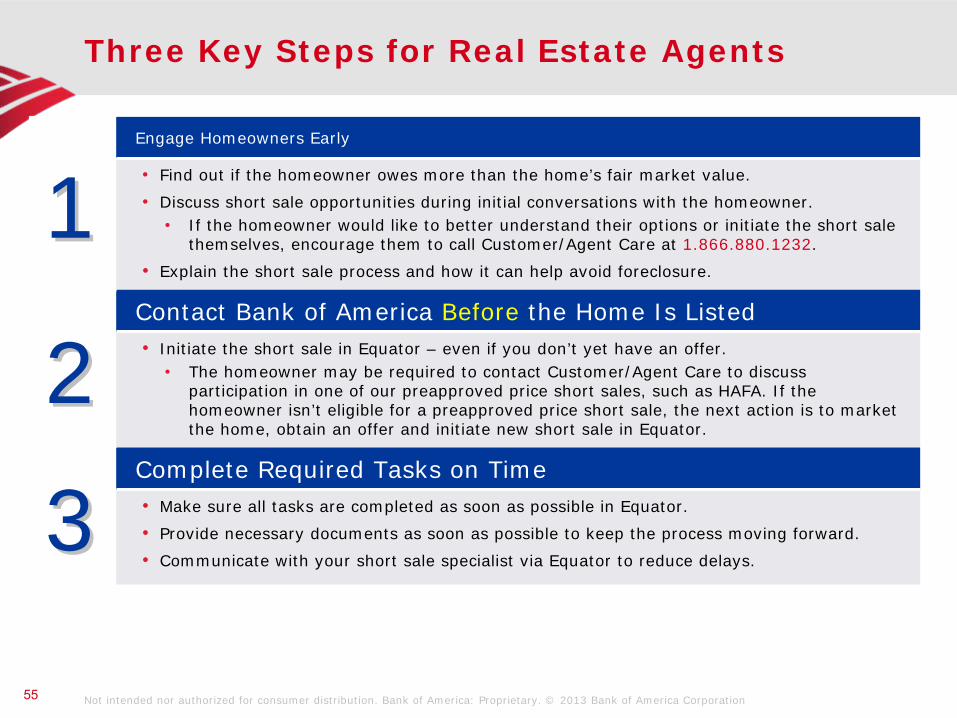

Three Key Steps for Real Estate Agents

11Engage Homeowners Early

• Find out if the homeowner owes more than the home’s fair market value.

• Discuss short sale opportunities during initial conversations with the homeowner.• If the homeowner would like to better understand their options or initiate the short sale

themselves, encourage them to call Customer/Agent Care at 1.866.880.1232.

• Explain the short sale process and how it can help avoid foreclosure.

22Contact Bank of America Before the Home Is Listed• Initiate the short sale in Equator – even if you don’t yet have an offer.

• The homeowner may be required to contact Customer/Agent Care to discuss participation in one of our preapproved price short sales, such as HAFA. If the homeowner isn’t eligible for a preapproved price short sale, the next action is to market the home, obtain an offer and initiate new short sale in Equator.

33Complete Required Tasks on Time• Make sure all tasks are completed as soon as possible in Equator.

• Provide necessary documents as soon as possible to keep the process moving forward.

• Communicate with your short sale specialist via Equator to reduce delays.

55 Not intended nor authorized for consumer distribution. Bank of America: Proprietary. © 2013 Bank of America Corporation

56 Not intended nor authorized for consumer distribution. Bank of America: Proprietary. © 2013 Bank of America Corporation

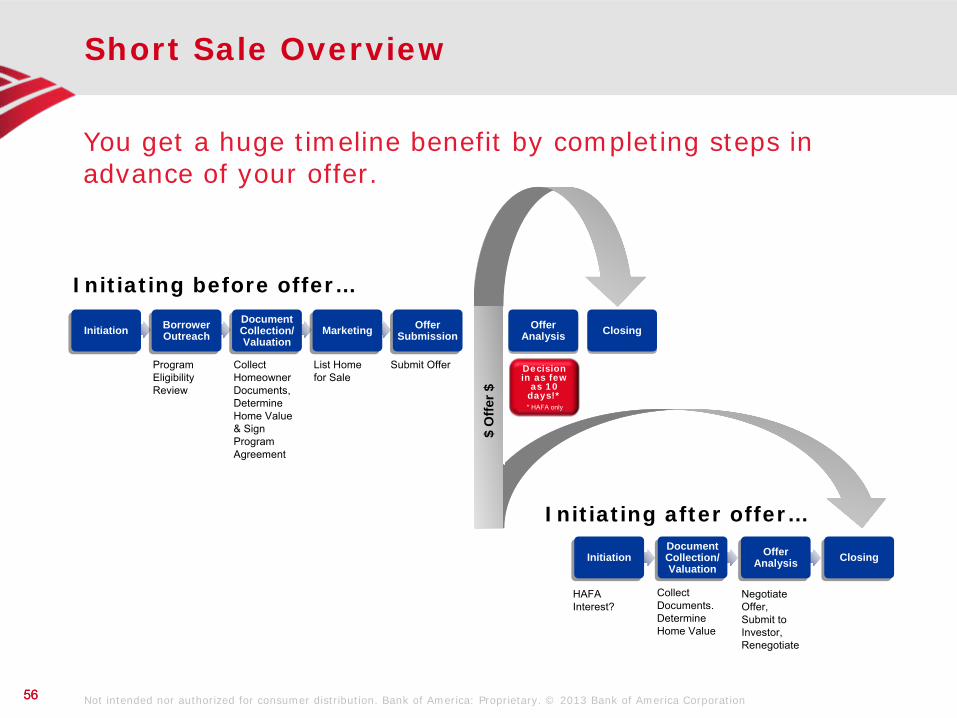

Short Sale Overview

56

Initiating before offer…

Initiating after offer…

InitiationInitiation Borrower Outreach Borrower Outreach

Document Collection/ Valuation

Document Collection/ Valuation

MarketingMarketing Offer Submission

Offer Submission

Offer Analysis

Offer Analysis ClosingClosing

Decision in as few

as 10 days!** HAFA only

Program EligibilityReview

Collect Homeowner Documents, Determine Home Value & Sign Program Agreement

List Home for Sale

InitiationInitiationDocument Collection/ Valuation

Document Collection/ Valuation

Offer Analysis

Offer Analysis ClosingClosing

Negotiate Offer, Submit to Investor,Renegotiate

HAFA Interest?

Collect Documents. Determine Home Value

Submit Offer

$ O

ffer $

You get a huge timeline benefit by completing steps in advance of your offer.

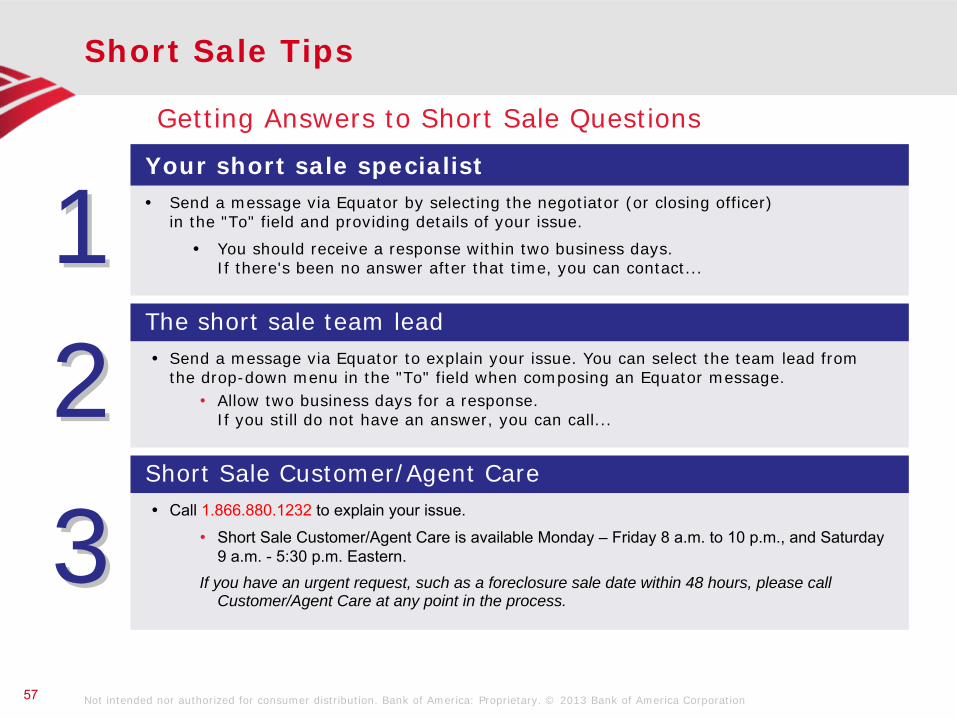

Short Sale Tips

57

Getting Answers to Short Sale Questions

11Your short sale specialist• Send a message via Equator by selecting the negotiator (or closing officer)

in the "To" field and providing details of your issue.

• You should receive a response within two business days. If there's been no answer after that time, you can contact...

22The short sale team lead• Send a message via Equator to explain your issue. You can select the team lead from

the drop-down menu in the "To" field when composing an Equator message. • Allow two business days for a response.

If you still do not have an answer, you can call...

33Short Sale Customer/Agent Care• Call 1.866.880.1232 to explain your issue.

• Short Sale Customer/Agent Care is available Monday –

Friday 8 a.m. to 10 p.m., and Saturday 9 a.m. -

5:30 p.m. Eastern.If you have an urgent request, such as a foreclosure sale date within 48 hours, please call

Customer/Agent Care at any point in the process.

Not intended nor authorized for consumer distribution. Bank of America: Proprietary. © 2013 Bank of America Corporation

How can I learn more about short sales?

58

• Important news and updates about the short sale process and enhancements

• Online subscriptions to keep you informed via email updates

• Free webinar replays• Education library of important

documents, including tips to a successful short sale

• Events • Important links • Contact information

Short Sale Agent Resource Center bankofamerica.com/shortsaleagent

Not intended nor authorized for consumer distribution. Bank of America: Proprietary. © 2013 Bank of America Corporation

59

Screenshots are the exclusive property of Equator, LLC and used herein under limited license for Bank of America training purposes only. Any distribution, reproduction, derivative, description or account of the screenshots is expressly prohibited without the express written consent of Equator, LLC. © 2013 Equator,

LLC. All rights reserved. Not intended or authorized for consumer distribution. Bank of America, N.A., Member FDIC. Equal Housing Lender. © 2013 Bank of America Corporation.

OcwenOcwen Financial Corp Financial Corp Proprietary and ConfidentialProprietary and Confidential

©1996-2012 Ocwen Financial Corporation. All rights reserved. Ocwen Financial Corporation, Ocwen and the Ocwen logo are registered trademarks of Ocwen Financial Corporation

Short Sale Program

May 2013

OcwenOcwen Financial Corp Financial Corp Proprietary and ConfidentialProprietary and Confidential

• Requesting a Short Sale Package—Legacy Ocweno Ocwen Website WWW.OCWENCUSTOMERS.COM.Homeowners or Authorized Parties can download a

package from our website by browsing to Home Page > Customer Service > Short Sale Package.

o Contact Ocwen’s Customer Care Center: Dial Toll Free 800-746-2936 and speak to a representative to request a short sale package to be sent to FAX/Email/mailing address.

• Requesting a Short Sale Package—Former GMACo Website WWW.OCWEN.MORTGAGEBANKSITE.COM. Homeowners or Authorized Parties can download

a package from our website by browsing to Home Page > Help for Homeowners > Get Help Now > Download Form.

o Contact Ocwen’s Customer Care Center: Dial Toll Free 866-725-0782 and speak to a representative to request a short sale package.

• Short Sale Reviewo Legacy Ocwen currently requires a fully executed purchase agreement prior to applying for a Short Sale except

for the loans eligible under DOJ Cooperative Short Sale Option. Soon the program will expand to the entire portfolio.

o A fully executed purchase agreement is not required for former GMAC customers to initiate a short sale review. A fully executed valid listing agreement is acceptable.

61

Short Sale: Getting Started

OcwenOcwen Financial Corp Financial Corp Proprietary and ConfidentialProprietary and Confidential

62

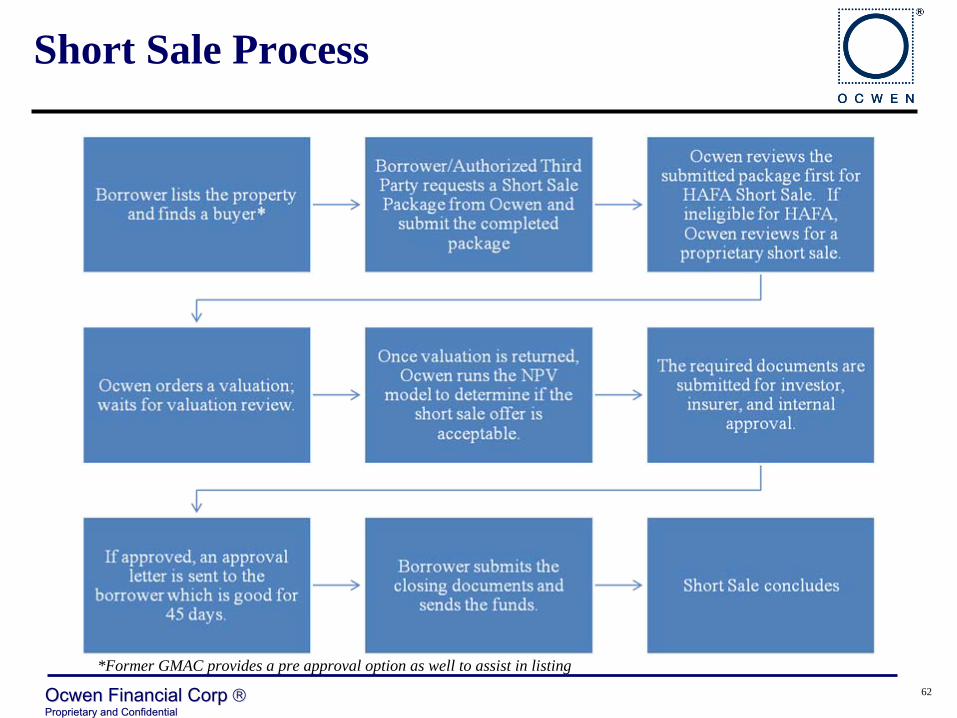

Short Sale Process

*Former GMAC provides a pre approval option as well to assist in listing

OcwenOcwen Financial Corp Financial Corp Proprietary and ConfidentialProprietary and Confidential

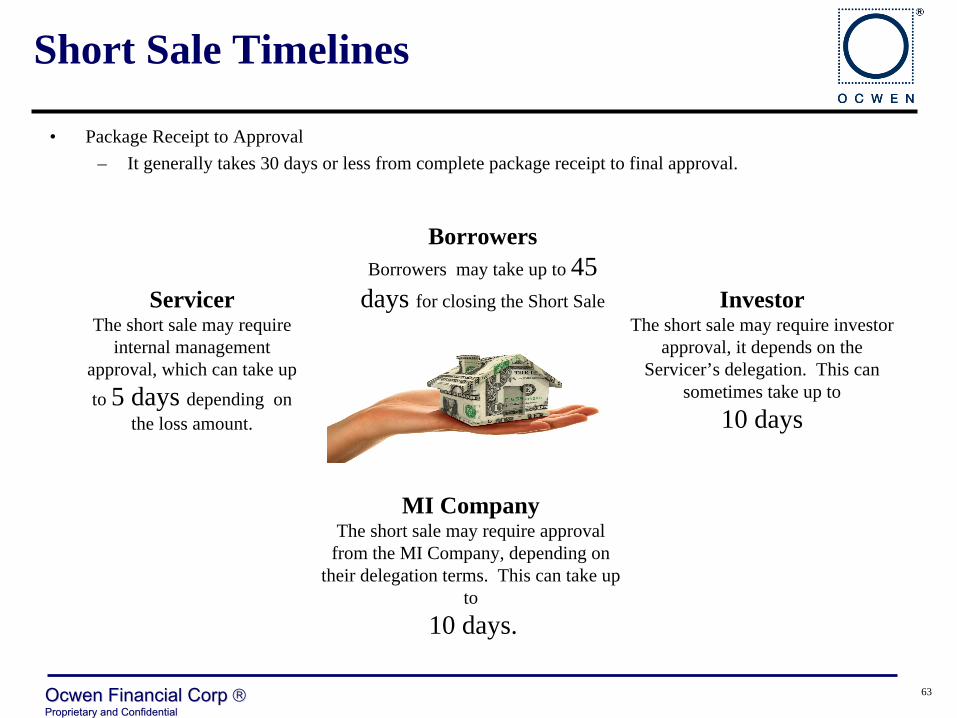

• Package Receipt to Approval– It generally takes 30 days or less from complete package receipt to final approval.

63

Short Sale Timelines

ServicerThe short sale may require

internal management approval, which can take up to 5 days depending on

the loss amount.

MI CompanyThe short sale may require approval

from the MI Company, depending on their delegation terms. This can take up

to10 days.

InvestorThe short sale may require investor

approval, it depends on the Servicer’s delegation. This can

sometimes take up to10 days

BorrowersBorrowers may take up to 45

days for closing the Short Sale

OcwenOcwen Financial Corp Financial Corp Proprietary and ConfidentialProprietary and Confidential 6464

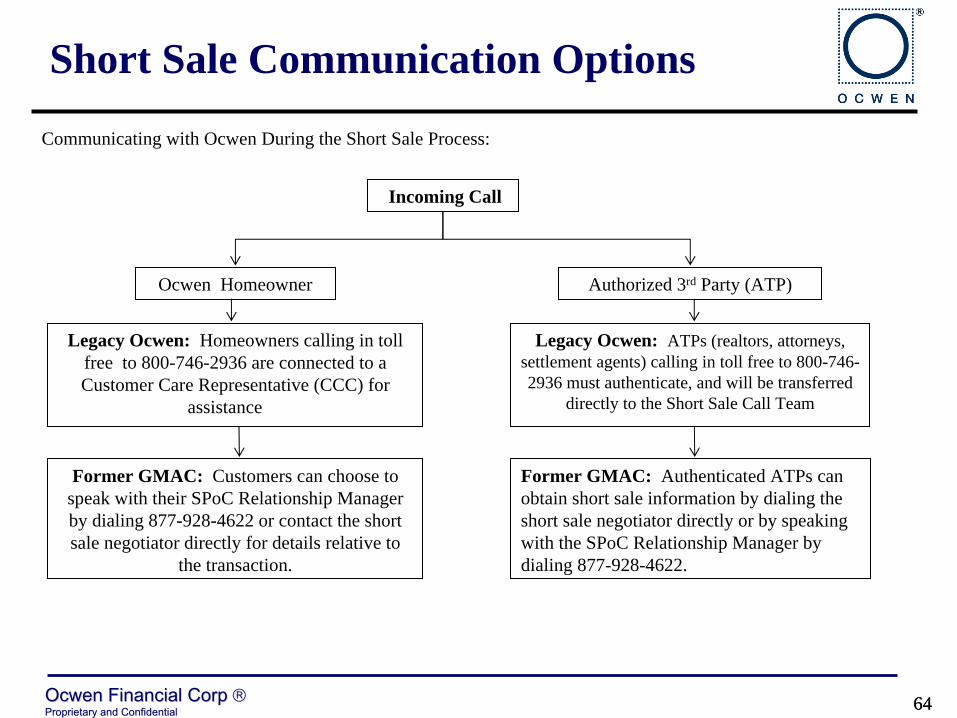

Communicating with Ocwen During the Short Sale Process:

Short Sale Communication Options

Incoming Call

Ocwen Homeowner

Former GMAC: Customers can choose to speak with their SPoC Relationship Manager by dialing 877-928-4622 or contact the short sale negotiator directly for details relative to

the transaction.

Legacy Ocwen: ATPs (realtors, attorneys, settlement agents) calling in toll free to 800-746- 2936 must authenticate, and will be transferred

directly to the Short Sale Call Team

Former GMAC: Authenticated ATPs can obtain short sale information by dialing the short sale negotiator directly or by speaking with the SPoC Relationship Manager by dialing 877-928-4622.

Authorized 3rd Party (ATP)

Legacy Ocwen: Homeowners calling in toll free to 800-746-2936 are connected to a Customer Care Representative (CCC) for

assistance

OcwenOcwen Financial Corp Financial Corp Proprietary and ConfidentialProprietary and Confidential

• Servicing Transfers to Ocweno Ocwen will honor all non-expired short sale approval letters issued by the prior servicer. An

approval letter reflecting the originally approved terms will be re-issued on Ocwen letterhead when the loan is transferred .

o Short sales in process but not approved by the prior servicer will require an Ocwen short sale package to initiate a new request .

o All Authorized Third Party information provided by the prior servicer will be uploaded as part of the loan transfer process, so as to minimize disruption to the communication process.

• Recently announced acquisitions by Ocweno Homeward Residential, Inc. loans were boarded to Ocwen systems between February and April

2013.o The former GMAC loans are now being serviced under the Ocwen name. These loans will

continue to be serviced using their existing platform, mailing addresses, etc.

65

Short Sale: Servicing Transfers to Ocwen

OcwenOcwen Financial Corp Financial Corp Proprietary and ConfidentialProprietary and Confidential

THANK YOU

66

67May 2013 | Making Home Affordable

Discussion/Questions

U.S. Department of the Treasury

Homeownership Preservation Office