Embed Size (px)

Citation preview

Making a RRIF last for life – Case Study

issued by Sun Life Assurance Company of Canadamanaged by CI Investments Inc.

Making a RRIF last for life – Case Study Tom: The situationTom, age 71, has just retired. He has saved $200,000 in his Registered Retirement Income Fund and must start withdrawing income next year. He realizes that his retirement savings are not large, but they will have to provide for both him and his wife, Joan, also age 71.*

While Tom has other money, he still needs his RRIF to provide him with a predictable income during retirement. He is uncertain about how to get the most income from his RRIF. Currently, he is invested in low-yielding GICs, but is not happy because the interest they pay barely keeps up with inflation. He is worried about depleting his assets too quickly, which could happen if he stays in GICs and interest rates remain low. He is also concerned about being dependent on fluctuating interest rates for his retirement income.

The challengeTo find an investment solution for Tom’s RRIF that will appeal to his conservative nature, but still provide him with a predictable, sustainable income that is guaranteed for his life and Joan’s.

Tom needs an income solution that can:

y guarantee him a predictable, sustainable income for life and provide for his wife upon his death

y meet the legal requirements of a RRIFy have the potential for income growth to help

keep pace with inflation.

RRIF Minimum Annual Payment Schedule (MAP)As required by the federal government, this is the minimum amount that must be withdrawn at each age. The withdrawal is based on the market value of assets on January 1 each year.

Age % Age %below 70 <5% 82 9.27%

71 7.38% 83 9.58%72 7.48% 84 9.93%73 7.59% 85 10.33%74 7.71% 86 10.79%75 7.85% 87 11.33%76 7.99% 88 11.96%77 8.15% 89 12.71%78 8.33% 90 13.62%79 8.53% 91 14.73%80 8.75% 92 16.12%81 8.99% 93 17.92%

Source: Canada Revenue Agency

The strategyTom places his $200,000 RRIF in SunWise Essential Series Income Class. He selects the Two-Life Income Stream option, which will provide him with a guaranteed annual income for life and ensure that if he dies first, Joan will continue to receive the same annual income. Tom also has to be concerned about the RRIF minimum annual payment, or MAP. When an RRSP is converted to a RRIF, the government requires that a minimum amount be withdrawn every year (starting the calendar year after the year of purchase), based on the market value of the account. Income Class offers Tom the flexibility to withdraw the RRIF minimum annual payment, without affecting his future guaranteed income. With Income Class, he will always receive the higher amount. In years when his MAP is above the guaranteed income, he receives MAP; in years when MAP is below, he receives the guaranteed income.

Tom is comfortable investing in equities, instead of GICs, because his income is insulated from market risk. He invests in an asset mix of 70% equities and 30% income. This allows him to take advantage of the growth potential of equities and makes it more likely he will benefit from automatic market resets. Resets can lock in investment gains and increase his guaranteed income, helping him keep ahead of inflation.

* If you hold units in your contract in addition to Income Class only, a prorated portion of the RRIF MAP can be taken from the Income Class units (the LWA RRIF MAP) without adversely affecting your future income stream.

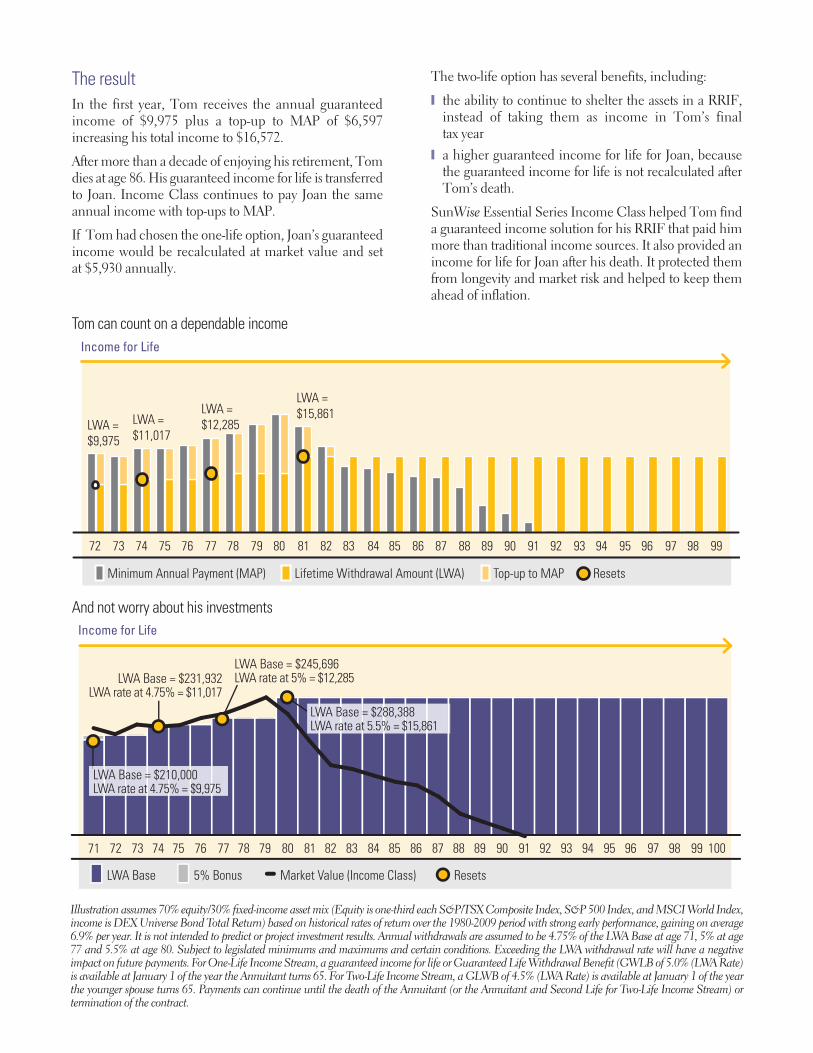

Income for Life

Minimum Annual Payment (MAP) Lifetime Withdrawal Amount (LWA) Top-up to MAP Resets

72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99

LWA = $9,975

LWA = $11,017

LWA = $12,285

LWA = $15,861

The resultIn the first year, Tom receives the annual guaranteed income of $9,975 plus a top-up to MAP of $6,597 increasing his total income to $16,572.

After more than a decade of enjoying his retirement, Tom dies at age 86. His guaranteed income for life is transferred to Joan. Income Class continues to pay Joan the same annual income with top-ups to MAP.

If Tom had chosen the one-life option, Joan’s guaranteed income would be recalculated at market value and set at $5,930 annually.

The two-life option has several benefits, including:

y the ability to continue to shelter the assets in a RRIF, instead of taking them as income in Tom’s final tax year

y a higher guaranteed income for life for Joan, because the guaranteed income for life is not recalculated after Tom’s death.

SunWise Essential Series Income Class helped Tom find a guaranteed income solution for his RRIF that paid him more than traditional income sources. It also provided an income for life for Joan after his death. It protected them from longevity and market risk and helped to keep them ahead of inflation.

Tom can count on a dependable income

LWA Base 5% Bonus Market Value (Income Class) Resets

72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96

Income for Life

71 97 98 99 100

LWA Base = $231,932LWA rate at 4.75% = $11,017

LWA Base = $210,000LWA rate at 4.75% = $9,975

LWA Base = $245,696LWA rate at 5% = $12,285

LWA Base = $288,388LWA rate at 5.5% = $15,861

And not worry about his investments

Illustration assumes 70% equity/30% fixed-income asset mix (Equity is one-third each S&P/TSX Composite Index, S&P 500 Index, and MSCI World Index, income is DEX Universe Bond Total Return) based on historical rates of return over the 1980-2009 period with strong early performance, gaining on average 6.9% per year. It is not intended to predict or project investment results. Annual withdrawals are assumed to be 4.75% of the LWA Base at age 71, 5% at age 77 and 5.5% at age 80. Subject to legislated minimums and maximums and certain conditions. Exceeding the LWA withdrawal rate will have a negative impact on future payments. For One-Life Income Stream, a guaranteed income for life or Guaranteed Life Withdrawal Benefit (GWLB of 5.0% (LWA Rate) is available at January 1 of the year the Annuitant turns 65. For Two-Life Income Stream, a GLWB of 4.5% (LWA Rate) is available at January 1 of the year the younger spouse turns 65. Payments can continue until the death of the Annuitant (or the Annuitant and Second Life for Two-Life Income Stream) or termination of the contract.

Sun Life Assurance Company of Canada

227 King Street SouthP.O. Box 1601 STN WaterlooWaterloo, Ontario N2J 4C5

03827_E (09/10)

2 Queen Street East, Twentieth Floor, Toronto, Ontario M5C 3G7 I www.ci.comHead Office / Toronto416-364-1145 1-800-268-9374

Calgary 403-205-43961-800-776-9027

Montreal 514-875-0090 1-800-268-1602

Vancouver 604-681-3346 1-800-665-6994

Client Services English: 1-800-563-5181 French: 1-800-668-3528

For more information about the innovative features

and benefits of SunWise Essential Series,

please visit www.sunwiseessentialseries.com.

All charts and illustrations in this guide are for illustrative purposes only. They are not intended to predict or project investment results. To the extent of any inconsistencies between this guide and the September 2010 SunWise Essential Series Information Folder and Individual Variable Annuity Contract, the terms of the Information Folder and Contract prevail. For full product details and disclosure, refer to the Information Folder and Contract.

Sun Life Assurance Company of Canada, a member of the Sun Life Financial group of companies, is the sole issuer of the individual variable annuity contract providing for investment in SunWise Essential Series segregated funds. A description of the key features of the applicable individual variable annuity contract is contained in the Information Folder. ANY AMOUNT THAT IS ALLOCATED TO A SEGREGATED FUND IS INVESTED AT THE RISK OF THE CONTRACT HOLDER AND MAY INCREASE OR DECREASE IN VALUE. ®CI Investments, the CI Investments design, Synergy Mutual Funds, Harbour Advisors, Harbour Funds, and Signature Global Advisors are registered trademarks of CI Investments Inc. ™Cambridge, Portfolio Series and Signature Funds are trademarks of CI Investments Inc. ®SunWise is a registered trademark of Sun Life Assurance Company of Canada. ®Fidelity Investments and the Fidelity design are registered trademarks of FMR Corp. ®RBC Asset Management is a registered trademark of Royal Bank of Canada. ™TD Asset Management is a trademark of The Toronto-Dominion Bank, used under licence. Franklin Templeton Investments, Franklin Templeton Investments Quotential Program and/or Franklin Templeton Investments and design are registered trademarks of Franklin Templeton Investment Corp. Dynamic Funds™ is a division of Goodman & Company, Investment Counsel Ltd. (“GCICL”). GCICL does not warrant or make any representations regarding the use or the results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise.