Embed Size (px)

Citation preview

Magna India Fund – the Magna India Fund – the investment opportunityinvestment opportunity

KC ReddyKC Reddy

MannheimFebruary 2006

2Charlemagne CapitalSpecialists in Emerging Markets

IntroductionIntroduction

KC Reddy – the ManagerKC Reddy – the Manager

Kommera Chakradhar (KC) Reddy – CFA

Previously with Thames River - UK

Credit Agricole – Hong Kong

Peregrine - India

MBA, Indian Institute of Management (associated with MIT’s Sloan School)

10 years experience investing in India10 years experience investing in India

3Charlemagne CapitalSpecialists in Emerging Markets

IntroductionIntroduction

KC Reddy - historic track recordKC Reddy - historic track record

1997* 1998 1999 2000**

The Himalaya Fund

-13.50% -11.06% 110.98% 21.34%

MSCI India Index

-12.35% -22.89% 84.67% 17.59%

Source: JP Morgan Fleming country fund research

* End Oct 1997 - end Dec 1997

** End Dec 1999 – end March 2000

4Charlemagne CapitalSpecialists in Emerging Markets

Magna Umbrella Fund plc

Magna Greater China

€ 30.5m

Magna Russia

€ 61.7m

Magna Eastern

European€ 399.1m

Magna Latin

America€ 45.0m

Magna Global Emerging Markets€ 212.7m

Magna Turkey€ 69.8m

Comprehensive emerging markets offering

Source: Charlemagne Capital – end December 2005

Magna India

€ 21.1m

Introduction Introduction

The Magna fund rangeThe Magna fund range

Magna EMEA

€ 36.3m

5Charlemagne CapitalSpecialists in Emerging Markets

IndiaIndia

Convincing macroeconomic case

Diversified market: bottom-up opportunities

Our process aims to find these

Positive outlookPositive outlook

Broad market opportunitiesBroad market opportunities

6Charlemagne CapitalSpecialists in Emerging Markets

IndiaIndiaMacroeconomic summaryMacroeconomic summary

Year to March 2004 2005e 2006e

Real GDP growth % 8.6 6.9 7.1

Inflation 5.5 6.5 3.9

General govt. debt (% GDP)

65.9 57.3 55.1

Foreign debt (% GDP) 20.4 19.1 18.0

Central Bank net FX reserves ($bn)

102.0 130.6 138.1

Source: CSFB – Sept 2005

Improving economic fundamentals

7Charlemagne CapitalSpecialists in Emerging Markets

UPA election win in 2004: Manmohan Singh (Prime Minister) and P. Chidambaram (Finance Minister) both widely respected reformers

Liberalisation of key areas (telecommunications, construction, infrastructure…)

Improved relations with Pakistan

IndiaIndia

Reform-minded administrationReform-minded administration

Improved political outlook

8Charlemagne CapitalSpecialists in Emerging Markets

55%

57%

59%

61%

63%

65%

67%

69%

71%

73%

75%

Newly industrialised countries (Korea, Taiwan, HK, Singapore) South East Asia (Malaysia, Philippines, Thailand, Indonesia) China India

Working age population (% overall population)

IndiaIndia

Young population, vibrant economyYoung population, vibrant economy

Source: UBS – Nov 2005 Favourable demographic & income trendsFavourable demographic & income trends

India

Favourable demographics: 75% of population under 40

Middle income and higher to rise from 18% of total to 41% 1995-2007

9Charlemagne CapitalSpecialists in Emerging Markets

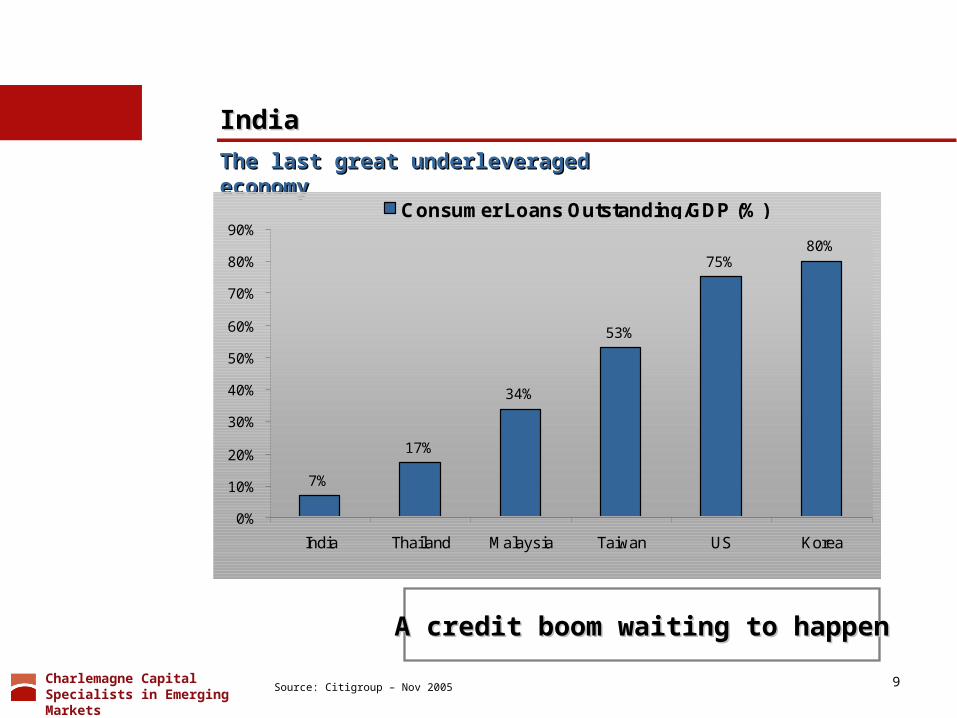

IndiaIndia

The last great underleveraged economyThe last great underleveraged economy

Source: Citigroup – Nov 2005

A credit boom waiting to happenA credit boom waiting to happen

7%

17%

34%

53%

75%80%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

India Thailand Malaysia Taiwan US Korea

Consumer Loans Outstanding/GDP (%)

10Charlemagne CapitalSpecialists in Emerging Markets

IndiaIndia

Over 5,000 listed companies

No industry group exceeds 20% of market cap

Massive improvement in corporate balance sheets

A stock picker’s paradiseA stock picker’s paradise

FY96 FY98 FY00 FY02 FY04 FY06e

Net debt to equity (%)

42.2 40.7 34.6 26.4 14.8 1.9

Source: Citigroup – Nov 2005

Broad market, good fundamentalsBroad market, good fundamentals

11Charlemagne CapitalSpecialists in Emerging Markets

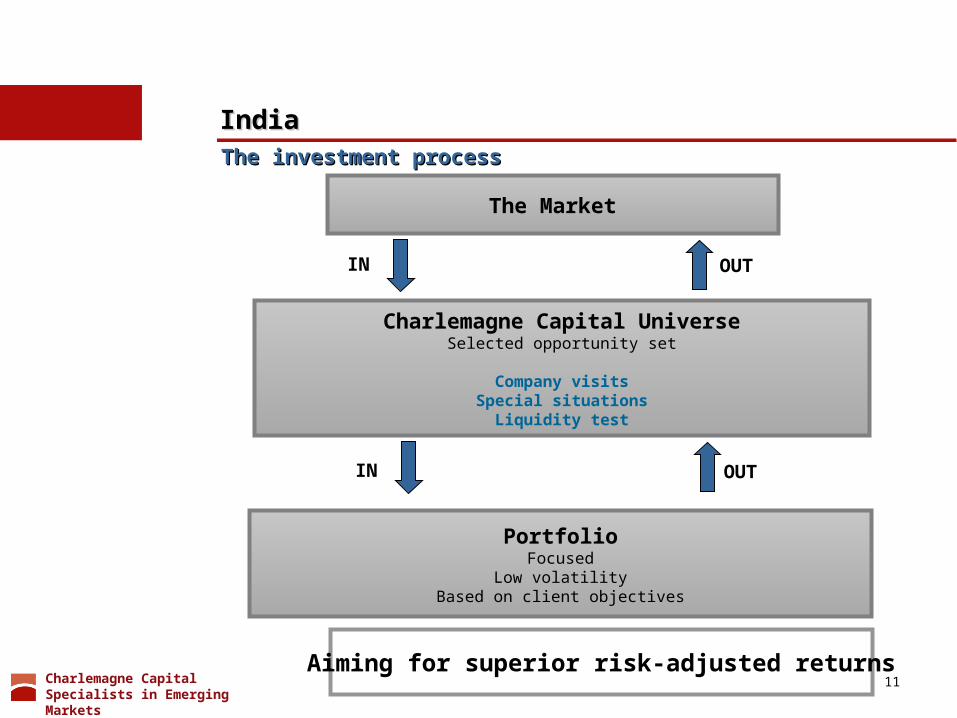

The Market

Charlemagne Capital UniverseSelected opportunity set

Company visitsSpecial situations

Liquidity test

PortfolioFocused

Low volatilityBased on client objectives

IN OUT

IN OUT

Aiming for superior risk-adjusted returns

IndiaIndiaThe investment processThe investment process

12Charlemagne CapitalSpecialists in Emerging Markets

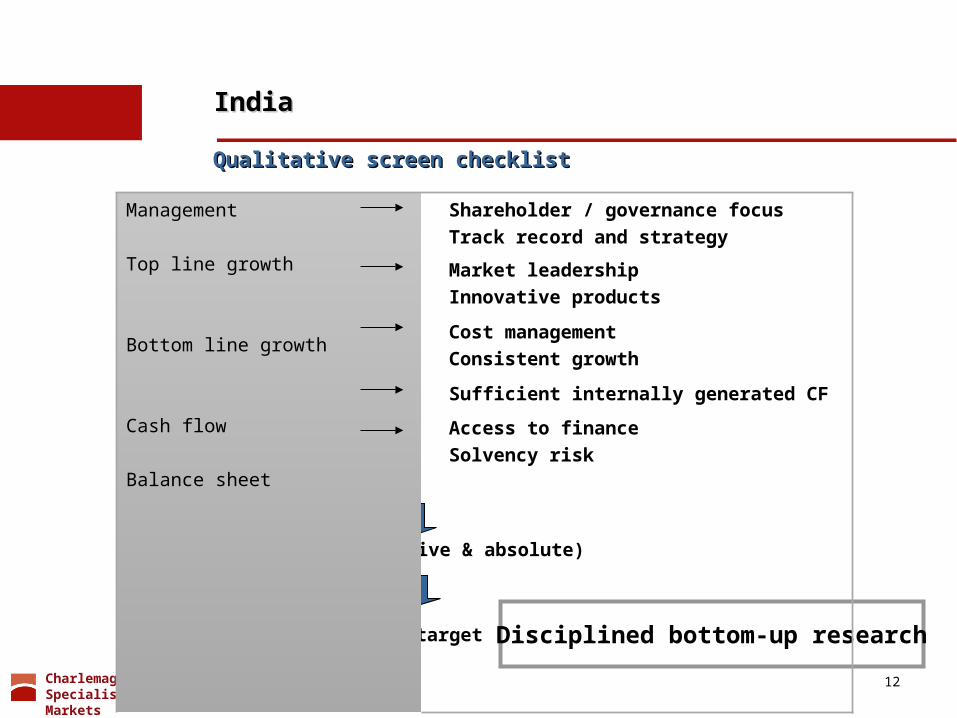

Disciplined bottom-up research

Valuation (relative & absolute)

Price target

Management

Top line growth

Bottom line growth

Cash flow

Balance sheet

Shareholder / governance focus

Track record and strategy

Market leadership

Innovative products

Cost management

Consistent growth

Sufficient internally generated CF

Access to finance

Solvency risk

IndiaIndia

Qualitative screen checklistQualitative screen checklist

13Charlemagne CapitalSpecialists in Emerging Markets

* MSCI India Index

Source: Charlemagne Capital / MSCI – 30 Dec 05

Large loads = active managementLarge loads = active management

Stock name Model weighting Index weighting* Load

Infosys Technologies 0.00% 13.80% -13.80%

Satyam Computers 9.69% 3.80% +5.89%

Tata Motors 7.86% 2.78% +5.08%

Tanla Solutions 5.00% 0.00% +5.00%

Housing Dev. Finance 0.00% 4.75% -4.75%

IndiaIndia

Magna India Fund: our top ideasMagna India Fund: our top ideas

14Charlemagne CapitalSpecialists in Emerging Markets

* MSCI India Index

Source: Charlemagne Capital / MSCI – 30 December 2005

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Energy Materials Industrials Consumer HealthCare

Financials Technology Others

Fund Wgt Index Wgt

Sector Allocation 30 December 2005

IndiaIndia

e.g. property

Large loads = active managementLarge loads = active management

Magna India Fund: active managementMagna India Fund: active management

15Charlemagne CapitalSpecialists in Emerging Markets

IndiaIndia

SummarySummary

India – a market for stock pickers

Our process seeks these opportunities

Magna India Fund – our best ideas

Good outlook for this changing marketGood outlook for this changing market

16Charlemagne CapitalSpecialists in Emerging Markets

The DisclaimerThe Disclaimer

This document is issued by Charlemagne Capital (UK) Limited which is authorised and regulated by the Financial Services Authority (“FSA”). Magna Umbrella Fund plc is an open ended investment company authorised by the Financial Regulator as a UCITS, recognised by the FSA under section 264 of the Financial Services and Markets Act 2000 for marketing to persons in the UK, registered for public distribution in Germany and Luxembourg, authorised for public distribution in Austria, registered by the Autoriteit Financiële Markten in The Netherlands and authorised for public offering and solicitation in and from Switzerland by the Swiss Federal Banking Commission (the Fund is not subject to supervisions by the Swiss Federal Banking Commission or other Swiss public authority). This document must not be relied on for the purposes of making any investment decisions. Before investing in any fund(s) recipients who are not professional investors should contact their independent financial adviser and should read all documents relating to the particular fund(s) such as any report and accounts and offering memorandum/prospectus, which specifies the particular risks associated with the fund(s), together with any specific restrictions applying and the basis of dealing. The value of any investments and any income generated may go down as well as up and is not guaranteed. Past performance will not necessarily be repeated. Changes in rates of exchange may have an adverse effect on the value, price or income of an investment. There are additional risks associated with investments (made directly or through investment vehicles which invest) in emerging or developing markets. The information in this document does not constitute investment, tax, legal or other advice and is not a recommendation or an offer to sell nor a solicitation of an offer to buy shares in the fund(s), which may only be made on the basis of the fund’s prospectus/ offering memorandum which can be obtained from the address below. An investor in the United Kingdom who enters into an investment agreement to acquire an interest in the fund will not have the right to cancel the agreement under any cancellation rules made by the FSA. Charlemagne Capital (UK) Limited reasonably believes that the information contained herein is accurate as at the date of publication but no warranty or guarantee (express or implied) is given as to accuracy or completeness. The information and any opinions expressed herein may change at any time. This document and shares in the fund shall not be distributed, offered or sold in any jurisdiction in which such distribution, offer or sale would be unlawful and until the requirements of such jurisdiction have been satisfied. The purchase of shares in the fund constitutes a high risk investment and investors may lose a substantial portion or even all of the money they invest in the fund.

Issued by Charlemagne Capital (UK) Limited - Authorised and Regulated by the FSA.

Charlemagne Capital (UK) Limited

39 St. James‘s Street

London SW1A 1JD

United Kingdom

Tel: + 44 (0)20 7518 2100

Fax: + 44 (0)20 7518 2198/9

www.charlemagnecapital.com