Embed Size (px)

Citation preview

Macroeconomic Models and Events of the Last Half Century

By Tim Fulmer, Ph.D.

copyright 2014, Tim Fulmer, Ph.D.

Contents A. Macroeconomic Models I. Preliminary Concepts II. Neoliberal/Neoclassical Models

a. The Fama-Friedman Free & Efficient Market b. The Austrian Business Cycle

III. Keynesian Models a. Hansen: The Simplified Business Cycle Model b. Hicks: The IS-LM General Equilibrium Model c. Minsky: The Financial Crisis Model

IV. Rational Expectations Models a. The Stochastic Dynamic General Equilibrium (DSGE) Model

V. Marxist Model B. Macroeconomic Events I. 1970s Stagflation and Reaganomics II. 1987 – 2007: The Great Moderation III. The 2007 – 2009 U.S. Financial Crisis & Recession IV. The 2010 - 2014 Growth Stagnation V. Policy Summary & Evaluation C. Supplementary Materials

a. Opinions On What Caused the U.S. Financial Crisis b. Rebuttals to the Efficient Market Hypothesis (EMH) c. Rebuttals to Using Policy

D. Bibliography

copyright 2014, Tim Fulmer, Ph.D.

A. Macroeconomic Models

copyright 2014, Tim Fulmer, Ph.D.

I. Preliminary Concepts

copyright 2014, Tim Fulmer, Ph.D.

U.S. economic output (demand) consists of three basic components: Consumers, businesses, and governments

copyright 2014, Tim Fulmer, Ph.D.

All the models assume a three-component economy

Federal & Local Governments (Policy)

Business owners & Investors

Consumers (Workers)

Taxes on

Business & Investment Taxes on

Income

Government Transfer Payments

Income

Consumption Profit Savings

Surplus

copyright 2014, Tim Fulmer, Ph.D.

G

I (Y, i) C (Y-T)

Total Output = Total Income Y = C + I + G

The Policy Components of the U.S. Economy:

1) O n the domestic level

a) Federal law ( U.S. Constitution ) – serves interests of poor & workers –

the state combats political inequality (risk: big government , loss of

individual freedoms )

a. Welfare clause (combat poverty , devastation and sickness )

b. Commerce clause ( combat monopolies )

c. Due process clause ( combat workplace discrimination )

b) F ederal budget ( fiscal policy ) – serves interests of poor & wealthy – the

state combats poverty (risk: debt default)

a. Spending ( “military - industrial complex” ; “welfare state” )

b. Progressive taxation

c) C entral bank ( monetary policy ) – serves interests of wealthy & financial

sector - the state combats market crises (risk: moral hazard , excess

speculation , excess market volatility )

a. Manipulating interest rates

b. Lender of last resort ; bailouts

d) Various government agencies – promotes and funds technological

innovation – the state combats “market failure”

2) O n the international level – serve domestic political interests

a) Tariffs

b) Subsidies

c) Currency manipulation

copyright 2014, Tim Fulmer, Ph.D.

II. Neoliberal/Neoclassical Models

copyright 2014, Tim Fulmer, Ph.D.

a. The Fama-Friedman Free & Efficient Market

copyright 2014, Tim Fulmer, Ph.D.

A free market promotes political freedom

“On the one hand, freedom in economic arrangements is itself a component of freedom broadly understood, so economic freedom is an end in itself. In the second place, economic freedom is also an indispensable means toward the achievement of political freedom.”

“The kind of economic organization that provides economic freedom directly, namely, competitive capitalism, also promotes political freedom because it separates economic power from political power and in this way enables one to offset the other.”

-- Milton Friedman, Chapter I, Capitalism And Freedom (1962, 1982, 2002)

copyright 2014, Tim Fulmer, Ph.D.

In a free market, prices allocate economic resources

“The economic problem of society” is “a problem of how to secure the best use of resources known to any of the members of society, for ends whose relative importance only these individuals know. Or, to put it briefly, it is the problem of the utilization of knowledge which is not given to anyone in its totality.”

“Fundamentally, in a system in which the knowledge of the relevant facts is dispersed among many people, prices act to coordinate the separate actions of different people … “

“We must look at the price system as such a mechanism for communicating information if we want to understand its real function … The most significant fact about this system is the economy of knowledge with which it operates, or how little the individual participants need to know in order to be able to take the right action” (all italics mine).

-- Friedrich A. Hayek, “The Use of Knowledge in Society” (1945)

copyright 2014, Tim Fulmer, Ph.D.

Efficient Market Hypothesis (EMH) :

1) The d efinition: In an efficient market, an asset’s price ( i.e., “fundamental value”) always and immediately reflects the total available information on that asset. Moreover, because the availability of (new) information on an asset is basically unpredictable (i.e., a random walk), an asset’s price is also unpredictable. Therefore, the chances of accurately predicting future asset prices based on past and current in formation is vanishingly small; mispricing, when it does o ccur, represents only a statistical “anomaly.”

2) The h ypothesis: Actual markets (e.g., the U.S. equity market)

behave like an efficient market under given (all?) time and space conditions .

3) The m echanism : Aggregate investor behavior drives “rational”

price discovery over given ( all?) time and space conditions – i.e., investors on average represent “smart money”: they do not overreact ( become overly optimistic) or underreact ( become overly pessimistic) to new in formation, whether good news or bad news.

In a free market, prices reflect all available information on all assets

copyright 2014, Tim Fulmer, Ph.D.

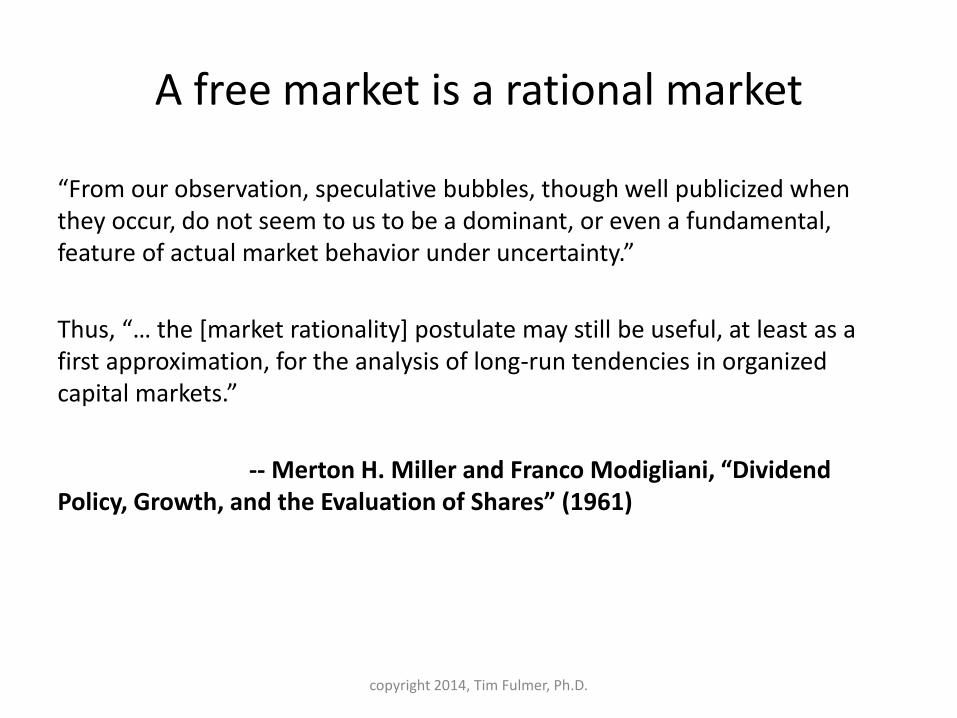

A free market is a rational market

“From our observation, speculative bubbles, though well publicized when they occur, do not seem to us to be a dominant, or even a fundamental, feature of actual market behavior under uncertainty.”

Thus, “… the [market rationality] postulate may still be useful, at least as a first approximation, for the analysis of long-run tendencies in organized capital markets.”

-- Merton H. Miller and Franco Modigliani, “Dividend Policy, Growth, and the Evaluation of Shares” (1961)

copyright 2014, Tim Fulmer, Ph.D.

b. The Austrian Business Cycle

copyright 2014, Tim Fulmer, Ph.D.

Expansions Alternate With Contractions

Low Consumption

- High Savings

Low Interest Bank Loans

Increased Long-term Production

Expansion

High Consumption

– Low Savings

High Interest Bank Loans

Decreased Long-term Production

Contraction

Say’s Law

Exogenous Initiating Factor

copyright 2014, Tim Fulmer, Ph.D.

Economic Causality Under the Neoliberal/Neoclassical View

copyright 2014, Tim Fulmer, Ph.D.

Employment/ Income

Consumption/ Output

Prices determined by an efficient free market

Adaptive expectations of future prices

Purchasing Behavior

Observational Data Sustained Economic Growth & Full Employment

Supply/Demand Decisions Rational Psychology

III. Keynesian Models

copyright 2014, Tim Fulmer, Ph.D.

Investment Uncertainty Destabilizes Capitalism

“The peculiar circularity of a capitalist economy” is that “sufficient investment to assure the economy does well now will be forthcoming only as it is believed that sufficient investment to assure the economy does well will be forthcoming in the future.”

-- Hyman Minsky, Chapter 10, Stabilizing an Unstable Economy (2008)

copyright 2014, Tim Fulmer, Ph.D.

Investment Uncertainty Drives Fluctuations in Employment

“… Given the psychology of the public, the level of output and employment as a whole depends on the amount of investment. … More comprehensively, aggregate output depends on the propensity to hoard, on the policy of the monetary authority …, on the state of confidence concerning the prospective yield of capital-assets, on the propensity to spend and on the social factors which influence the level of the money wage. But of those several factors, it is those which determine the rate of investment which are most unreliable, since it is they which are influenced by our views of the future about which we know so little” (my italics).

“This that I offer is, therefore, a theory of why output and employment are so liable to fluctuation.”

-- J. M. Keynes, “The General Theory of Employment” (1937)

copyright 2014, Tim Fulmer, Ph.D.

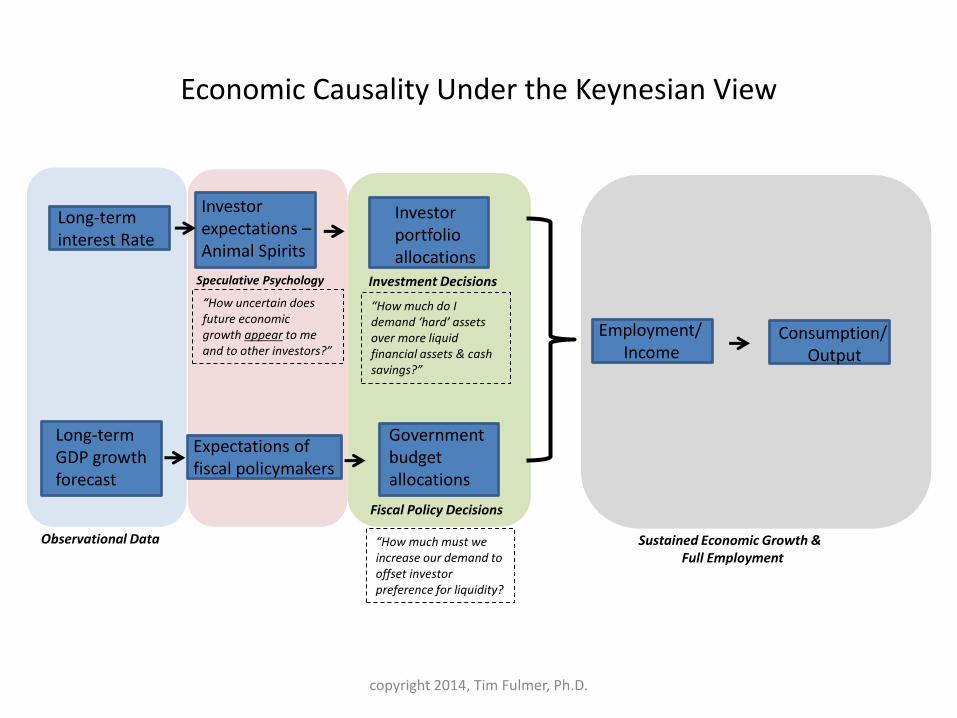

Economic Causality Under the Keynesian View

copyright 2014, Tim Fulmer, Ph.D.

Long-term interest Rate

Investor expectations – Animal Spirits

Investor portfolio allocations

Long-term GDP growth forecast

Expectations of fiscal policymakers

Government budget allocations

Employment/ Income

Consumption/ Output

Observational Data

Speculative Psychology Investment Decisions

Sustained Economic Growth & Full Employment

“How uncertain does future economic growth appear to me and to other investors?”

“How much do I demand ‘hard’ assets over more liquid financial assets & cash savings?”

Fiscal Policy Decisions

“How much must we increase our demand to offset investor preference for liquidity?

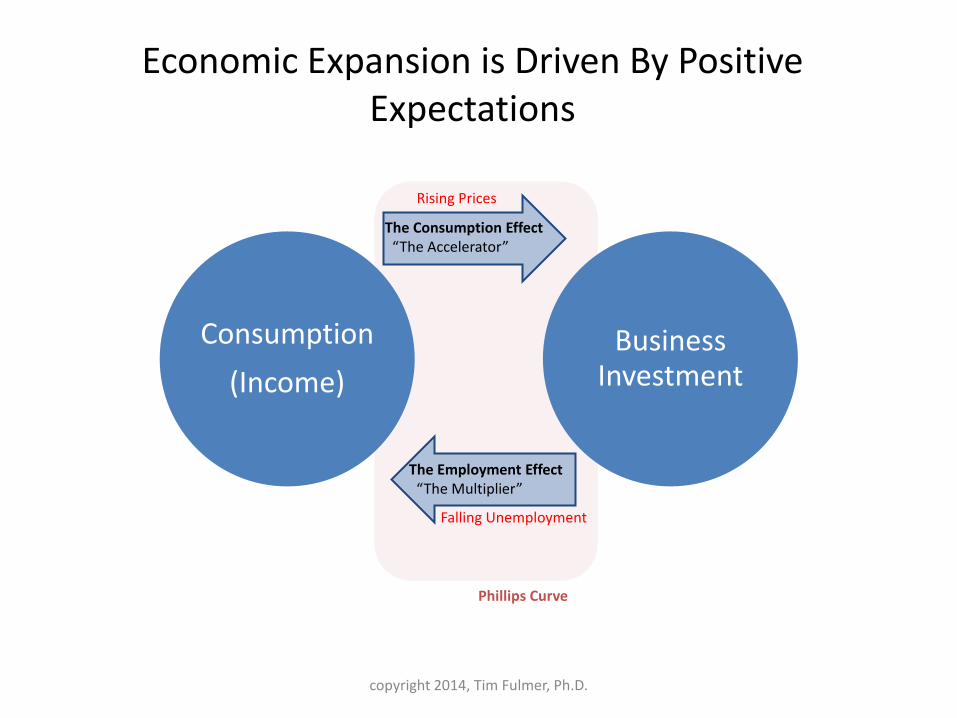

a. Hansen: The Simplified Business Cycle Model

copyright 2014, Tim Fulmer, Ph.D.

Consumption

(Income)

Business Investment

Economic Expansion is Driven By Positive Expectations

The Consumption Effect “The Accelerator”

The Employment Effect “The Multiplier”

Rising Prices

Falling Unemployment

Phillips Curve

copyright 2014, Tim Fulmer, Ph.D.

Expansion ends when*:

• Full employment is reached

• Consumers increasingly favor saving over spending (for whatever reason)

And/or

• Investors increasingly favor saving over investing because of increasingly lower rates of return on new investments

*For a “classical” view, see, for example, chapter 11, “The Multiplier and the Acceleration Coefficient,” in Alvin H. Hansen’s Business Cycles and National Income (1951; 1964); for a more “modern” treatment that takes credit markets into account, see, for example, “The Financial Accelerator and the Flight to Quality” by Ben Bernanke, Mark Gertler, and Simon Gilchrist (1996).

copyright 2014, Tim Fulmer, Ph.D.

Economic Contraction is Driven By Negative Expectations

Consumption

(Income)

Business Investment

The Consumption Effect

The Employment Effect

Deflation

Rising Unemployment

Savings Savings & Financial Investments

Uncertainty Uncertainty

copyright 2014, Tim Fulmer, Ph.D.

Uncertainty Alters Investment Priorities

Portfolio Composition

Financing Conditions

Level of Uncertainty

Savings & Financial Investments

Cash

Asset Values – “Financial Markets”

Productive Assets – “Real Economy”

Liquidity preference increasing with uncertainty

copyright 2014, Tim Fulmer, Ph.D.

Keynes’ Liquidity Preference

“The possession of actual money lulls our disquietude; and the premium which we require to make us part with money is the measure of the degree of our disquietude. … And changes in the propensity to hoard, or in the of state of liquidity-preference as I have called it, primarily affect, not prices, but the rate of interest; any effect on prices being produced by repercussion as an ultimate consequence of a change in the rate of interest.”

-- J. M. Keynes, “Mr. Keynes on the Causes of Unemployment” (1936)

copyright 2014, Tim Fulmer, Ph.D.

Hoarding and the Paradox of Thrift

“Suppose we were to stop spending our incomes altogether, and were to save the lot. Why, everyone would be out of work. And before long we should have no incomes to spend. No one would be a penny the richer, and the end would be that we should all starve to death.”

“…Therefore, oh patriotic housewives, sally out tomorrow early into the streets and go to the wonderful sales … And have the added joy that you are increasing employment, adding to the wealth of the country.”

-- J. M. Keynes, 1931, British radio broadcast

copyright 2014, Tim Fulmer, Ph.D.

A “Modern” Version of the Paradox of Thrift: Austerity

“We tend to forget that someone has to spend for someone else to save; otherwise the saver would have no income from which to save. … We cannot all be austere at once. All that does is shrink the economy for everyone.”

“[In the same manner], we cannot all cut our way to growth, just as we cannot all export without any concern for who is importing. This fallacy of composition problem rather completely undermines the idea of austerity as growth enhancing.”

-- Mark Blyth, Introduction, Austerity: The History of a Dangerous Idea (2013)

copyright 2014, Tim Fulmer, Ph.D.

Thrift and Austerity Are Deflationary

“… As Irving Fisher pointed out, [austerity] is an inherently deflationary act. The more one pays down debt, the less one spends. The less one spends, the less real economic demand there is for goods and services – which translates to less investment, employment, and production. In turn, that means less personal income and tax revenue – which creates bigger holes in government and household budgets and a greater need for additional borrowing.”

--Daniel Alpert, Chapter 6, The Age of Oversupply: Overcoming the Greatest Challenge of the Global Economy (2013)

copyright 2014, Tim Fulmer, Ph.D.

Policy Attempts To Thwart Negative Expectations

Consumption

(Income)

Business Investment

The Consumption Effect

The Employment Effect “The Fiscal Multiplier”

Rising Prices

Falling Unemployment

Savings Savings & Financial Investments

Less Uncertainty Less Uncertainty

Tax Cuts

Government Programs

Tax Cuts

copyright 2014, Tim Fulmer, Ph.D.

Government Spending

Keynes’ Fiscal Multiplier

If government spending “is additional and not merely in substitution for other expenditure, the increase of employment does not stop there. The additional wages and other incomes paid out are spent on additional purchases, which in turn lead to further employment.”

“… The newly employed who supply the increased purchases of those employed on the new capital works will, in their turn, spend more, thus adding to the employment of others; and so on.”

-- J. M. Keynes, The Means to Prosperity (1932)

copyright 2014, Tim Fulmer, Ph.D.

b. Hicks: The IS-LM General Equilibrium Model

copyright 2014, Tim Fulmer, Ph.D.

An Equilibrium Interpretation of Keynes The ISLM model explicitly allows for the fact that a macroeconomic disturbance may arise equally in the productive “goods” market and in the paper “asset” market and, moreover, a disturbance originating in one market will likely propagate its effects to the other.

In contrast, pre-Keynesian neoclassical models typically limited their analysis to either the goods market (the income-expenditure model) or the asset market (the quantity theory of money), replacing the other market with an oversimplified aggregate and thus potentially oversimplifying their analysis.

Nonetheless, the ILSM model shares with the neoclassical models the key assumption of an equilibrium point where markets clear (“Walras Law”). For that reason, the ISLM model is often offered as an example of the Keynesian “neoclassical synthesis.”*

*For the original formulation of the IS-LM model, see J. R. Hicks’ “Mr. Keynes and the ‘Classics’: A Suggested

Interpretation” (1937).

copyright 2014, Tim Fulmer, Ph.D.

The Investment-Saving (IS) Curve: Equilibrium in the Goods Markets

copyright 2014, Tim Fulmer, Ph.D.

Exogenous Variables: • C, Consumption • T, Taxes • I, Investment • G, Government Endogenous Variables: • Y, Output or Income • i, the Interest Rate Policymakers control T and G.

Total Output (Income) Y = C(Y-T) + I (Y, i) + G or Y = [1/(1-c1)](c0 – c1T + I + G)

Multiplier Spending

a.

b. At equilibrium, Income Y = Demand Z. Thus: Total Demand Z = (c0 - c1T + I + G) + c1Y

The Liquidity-Money (LM) Curve: Equilibrium in the Asset Markets

copyright 2014, Tim Fulmer, Ph.D.

a.

b. At equilibrium, Money Supply Ms = Money Demand Md. Thus:

Money Demand (M/P)D = Y(L, i)

Exogenous Variables: • Ms, Money Supply • P, Price Level • Md, Demand for Money Endogenous Variables: • Y, Output or Income • i, Interest Rate Policymakers control Ms.

(M/P)s = YL(i)

Interpreting the Curves

The IS Curve: Adjustments in the interest rate ensure that the aggregate quantity of goods supplied equals the aggregate quantity of goods demanded at equilibrium, thus clearing the goods market.

The LM Curve: Adjustments in the interest rate ensure that the aggregate quantities of money supplied equals the aggregate quantity of money demanded at equilibrium, thus clearing the asset market.

copyright 2014, Tim Fulmer, Ph.D.

The IS-LM General Equilibrium

copyright 2014, Tim Fulmer, Ph.D.

i

Y

IS

LM

i*

Y*

Equilibrium Full Employment (FE) Output

Equilibrium Interest Rate

FE

Limitations of the IS-LM Model

• A price level does not enter the model; therefore all adjustments to changes in demand must be in the form of changes in output, not in the form of price changes.

• The model does not incorporate inflation, which creates a difference between real and nominal interest rates and thus directly influences short-term investment decisions.

• The model cannot directly address non-equilibrium economic processes and events like financial crises.

copyright 2014, Tim Fulmer, Ph.D.

c. Minsky: The Financial Crisis Model

copyright 2014, Tim Fulmer, Ph.D.

When the Speculator Prevails over the Entrepreneur …

“With the separation between ownership and management which prevails today and with the development of organized investment markets, a new factor of great importance has entered in, which sometimes facilitates investment, but sometimes adds greatly to the instability of the system. … Thus, certain classes of investment are governed by the average expectations of those who deal on the Stock Exchange as revealed in the prices of shares, rather than by the genuine expectations of the professional entrepreneur.”

“Speculators may do no harm as bubbles on a steady stream of enterprise. But the position is serious when enterprise becomes the bubble on a whirlpool of speculation. When the capital development of a country becomes a byproduct of the activities of a casino, the job is likely to be ill-done” (italics mine).

-- J. M. Keynes, The General Theory of Employment, Interest, and Money (1936)

copyright 2014, Tim Fulmer, Ph.D.

… Self-Interest Destabilizes the Capitalist Economy

“In a world with capitalist finance, it is simply not true that [the self-interest of the free market] will lead an economy to equilibrium. The self-interest of bankers, levered investors, and investment producers can lead the economy to inflationary expansions and unemployment-creating contractions.”

-- Hyman Minsky, Chapter 10, Stabilizing an Unstable Economy (2008)

copyright 2014, Tim Fulmer, Ph.D.

Minsky’s Instability Hypothesis

“The major flaw of our type of [capitalist] economy is that it is unstable. The instability is not due to external shocks or to the incompetence or ignorance of policy makers. Instability is due to the internal processes of our type of economy. … But … institutions and policy can contain the thrust to instability. We can, so to speak, stabilize instability.”

-- Hyman Minsky, Chapter 1, Stabilizing an Unstable Economy (2008)

“Once the determinants of investment are understood, a full statement of the financial instability theory is possible. Investment is the essential determinant of the path of a capitalist economy: the government budget, the behavior of consumption, and the path of money wages are secondary.”

“Instability emerges as a period of relative tranquil growth is transformed into a speculative boom” (italics mine).

-- Chapter 8 (2008)

copyright 2014, Tim Fulmer, Ph.D.

A Boom Features High Levels of External Financing (Debt-Financing)

“… A marked increase in the fragility of an economy occurs as an externally financed investment boom takes place. The financing relations assure that an investment boom will lead to an environment with increased speculative financing positions, which in turn will lead to conditions conducive to a crisis. That is, a financial structure in which a debt deflation can occur and events that trigger the start of a debt deflation are normal results of the financing relations that lead into and take place during an investment boom.”

“A break in the boom occurs whenever short- and long-term interest rates rise enough so that attenuations and reversals in present-value relations take place. … Whether the break in the boom leads to a financial crisis, debt deflation, and deep depression or to a non-traumatic recession depends upon the overall liquidity of the economy, the relative size of the government sector, and the extent of lender-of-last-resort action by the Federal Reserve.”

-- Hyman Minsky, Chapter 9, Stabilizing an Unstable Economy (2008)

copyright 2014, Tim Fulmer, Ph.D.

A Boom Features High Levels of Financial Innovation

“Over an expansion, new financial instruments and new ways of financing [investment] activity develop. …”

“Typically, defects of the new ways and the new institutions are revealed when the crunch comes. The authorities [i.e., the central bank] intervene to prevent localized weakness from leading to a broad decline in asset values. … Since the intervention by the authorities tends to validate the new ways, the central bank sets the stage for a broader acceptance and use of the new financial instruments in subsequent expansions.”

“If the authorities constrain banks and are aware of the activities of fringe banks and other financial institutions, they are in a better position to attenuate the disruptive expansionary tendencies of our economy.”

-- Hyman Minsky, Chapter 10, Stabilizing an Unstable Economy (2008)

copyright 2014, Tim Fulmer, Ph.D.

“Tranquil” Prosperity

Investors Seek New

Profit Outlets

Financial Innovation

& Debt Financing

Investment Boom

Asset Price Inflation

Minskian “Virtuous” Cycle – The Roots of Instability

Robust economy “Productive Assets Favored”

Unstable economy “Asset Values Favored”

copyright 2014, Tim Fulmer, Ph.D.

Asset Value Bubble Bursts

Banks Holding Assets Fail to

Make Positions

Defaults and Bankruptcies

Increase

Loss of Confidence

Systemic Credit Freeze

Banks Resort to Fire Sales to

Make Positions

Minskian Vicious Cycle – Instability Triggers a Crisis

Financial Sector Significantly

Devalued

Negative Investment

Expectations

Decreased Productivity

Increased Unemployment

Decreased Consumption

Collapse of Asset Values Collapse of Productive Economy

copyright 2014, Tim Fulmer, Ph.D.

A Boom Features Other Forms of Instability

• Increasing complexity and interconnectedness of the markets – contributes to systemic volatility

• Increasing reliance on highly leveraged bank operations (“shadow banking system”) – contributes to liquidity uncertainty

• Herding behavior and investor “group-think” – contributes to systemic volatility (“asset bubbles”)

copyright 2014, Tim Fulmer, Ph.D.

Instability May Make Crises Unavoidable

“If all the eventualities cannot be anticipated (which is the case for complex [financial] systems) and if there is no time to rework the process before the problem is propagated down the line (which is the implication of tight coupling [in financial markets]), then when things go wrong a crisis will be unavoidable. Things will go bad, and when they do, they will move quickly from bad to worse before the cascade can be stopped.”

-- Richard Bookstaber, Chapter 8, A Demon of Our Own Design: Markets, Hedge Funds, and the Perils of Financial Innovation (2007)

copyright 2014, Tim Fulmer, Ph.D.

Regulation & Oversight May Not Avoid Crises

“The natural reaction to market breakdown is to add layers of protection and regulation. But trying to regulate a market entangled by complexity can lead to unintended consequences, compounding crises rather than extinguishing them because the safeguards add even more complexity … A better approach for regulation is to reduce the complexity in the first place, rather than try to control it after the fact” (italics mine).

-- Richard Bookstaber, Chapter 8, A Demon of Our Own Design: Markets, Hedge Funds, and the Perils of Financial Innovation (2007)

“The paradox is that to understand and anticipate market crises, we must know [investor] positions, but knowing and acting on positions will itself generate a feedback into the market. This feedback often will reduce liquidity, making our observations less valuable and possibly contributing to a market crisis. Or, in rare instances, the observer/feedback loop could be manipulated to amass fortunes.”

-- Richard Bookstaber, Chapter 10 (2007)

copyright 2014, Tim Fulmer, Ph.D.

IV. Rational Expectations Models

copyright 2014, Tim Fulmer, Ph.D.

Rational Expectations Underlie All Economic Behavior

“... I should like to suggest that expectations, since they are informed predictions of future events, are essentially the same as the predictions of the relevant economic theory. … We call such expectations ‘rational.’ …” This hypothesis is based on the view that “dynamic economic models do not assume enough rationality.”

“… The expectations of firms … tend to be distributed, for the same information set, about the prediction of the theory….”

-- John Muth, “Rational Expectations and the Theory of Price Movements” (1961)

copyright 2014, Tim Fulmer, Ph.D.

Rational Expectations Confound Policy Forecasting: The Lucas Critique

The critique “implies that comparisons of the effects of alternative policy rules using current macroeconometric models are invalid regardless of the performance of these models over the sample period or in ex ante short-term forecasting.”

“… The ability to forecast the consequences of ‘arbitrary,’ unannounced sequences of policy decisions … appears to be beyond the capability not only of the current-generation [Keynesian] models, but of conceivable future models as well.”

“On the other hand, … conditional forecasting under the alternative structure [of a stochastic model founded on John Muth’s rational expectations hypothesis], is, while scientifically more demanding, entirely operational.”

-- Robert Lucas, “Econometric Policy Valuation: A Critique” (1976)

copyright 2014, Tim Fulmer, Ph.D.

The Dynamic Stochastic General Equilibrium (DSGE) Model

• DSGE models start from the microeconomic principles of constrained decision-making (i.e., they are based on “microfoundations”). The decision-makers (“agents”) include households, businesses, governments, and central banks.

• DSGE models reflect how an economy evolves over time (i.e., they are dynamic) and take into account random exogenous shocks (i.e., they are stochastic).

• Three general types of input are included in DSGE models: – Preferences: agents’ economic goals

– Technology: agents’ productive capacity

– Institutional Framework

copyright 2014, Tim Fulmer, Ph.D.

V. Marxist Model

copyright 2014, Tim Fulmer, Ph.D.

Marxist/ Socialist Economic Development

Class Inequality

Class Struggle

Establishment of Socialism

Workers

Capitalists Commodity Markets

Labor Markets

Surplus Value

Immiserization/ Alienation of Workers

Worker Education on Alternatives to Capitalism

Socialized Ownership of Production

Overthrow of Capitalists

Cooperative (Not Competitive) Production

Formation of Worker Party

+ Satisfaction of Workers’ Needs & Goals

copyright 2014, Tim Fulmer, Ph.D.

B. Macroeconomic Events

copyright 2014, Tim Fulmer, Ph.D.

I. 1970s Stagflation & Reaganomics

copyright 2014, Tim Fulmer, Ph.D.

1970s Stagflation “Refutes” Keynes*

Guns & Butter Deficit Spending

Progressive Taxation

Expansionary Monetary Policy

Inflationary Expectations

High Prices

Reduced Investment

Unemployment

*Based on Chapter 6, Blyth (2002)

“Stagflation” - Phillips Curve Breaks Down

Arab Oil Embargo

copyright 2014, Tim Fulmer, Ph.D.

Reaganomics*

Cut Business & Income Taxes “Laffer Curve”

Tighten Monetary Policy “Volcker Squeeze”

Eliminate Inflationary Expectations

Lower Prices

Increase private Investment

Boost Employment & GDP Growth

Reduce Government Spending

*Based on Chapter 6, Blyth (2002)

Supply-Side Economics Monetarism Fiscal Restraint

copyright 2014, Tim Fulmer, Ph.D.

1965 – 1985: Paul Volcker Stamps Out Inflation

Fed Chairman Paul Volcker Institutes Contractionary Monetary Policy

Aug. 1971 Nixon Closes Gold Window, Institutes Price Controls

Carter Takes Office Jan. 1977

Price Controls End April 1974

Arab Oil Embargo Oct. – Nov. 1973

LBJ’s Guns & Butter

Nixon Takes Office, Inflation Highest Since Korean War Jan. 1969

9% Unemployment May 1975

Second Oil Shock March 1979

6% Unemployment Summer 1971

Reagan Takes Office Jan. 1981

copyright 2014, Tim Fulmer, Ph.D.

… And Growth Remains Strong

1984 Q1 Real GDP: 8.5%

1966 Q1 Real GDP: 8.5%

1973 Q1 Real GDP: 7.5%

copyright 2014, Tim Fulmer, Ph.D.

… But At What Cost? – Rising Federal Deficits

Reagan Takes Office Jan. 1981

Carter Takes Office Jan. 1977

Nixon Takes Office Jan. 1969

copyright 2014, Tim Fulmer, Ph.D.

Reaganomics Undone By Defense Spending & Tax Cuts

“A riotous expansion of the warfare state was foremost among the policy errors of the Reagan Revolution. Within days of Reagan taking office, the White House made a historically devastating mistake by signing over to the Pentagon a blank check known as the ‘7 percent real growth top line.’ This massive injection of fiscal firepower nearly tripled the annual defense budget from $140 million to $370 million in just six years.” -- David Stockman, Chapter 5, The Great Deformation: The Corruption of Capitalism in America (2013) “… The 1981 Reagan legislative program had been a fiscal disaster. The huge tax reduction without a matched book of spending cuts caused the structural deficit to literally explode to the then unimaginable level of 6 percent GDP. … The old-time taboo against chronic deficit finance in peacetime had been jettisoned by the Republican Party. … In fact, the average federal deficit during this twelve-year period [of the Reagan and Bush presidencies] was 4.3 percent of GDP, a level never even imagined by the most aggressive liberal Keynesians before 1980.” -- Chapter 6 (2013)

copyright 2014, Tim Fulmer, Ph.D.

II. 1987 – 2007: The Great Moderation

copyright 2014, Tim Fulmer, Ph.D.

20 Years of … Falling Interest Rates,

LTCM Crisis Sept. 1998

WTC Attacks Sept. 2001

Deflation “Scare” Summer 2003

NASDAQ All-Time High March 2000

Housing Market Peaks Summer 2006

Stock Market Bottom March 2009

Bear Stearns Rescue March 2008

SPY Pre-Crash All-Time High Oct. 2007

Stock Market Crash Oct. 1987

“The Greenspan Put”

copyright 2014, Tim Fulmer, Ph.D.

… Low Inflation, Low Unemployment,

Peak Unemployment: 7.8% June 1992 Trough Unemployment: 3.8%

April 2000

copyright 2014, Tim Fulmer, Ph.D.

… And Moderate Growth

The Great Moderation 1987 - 2007

copyright 2014, Tim Fulmer, Ph.D.

… But At What Cost? – Rising Debt

The Great Moderation 1987 - 2007

copyright 2014, Tim Fulmer, Ph.D.

… And Falling Wages

The Great Moderation 1987 - 2007

copyright 2014, Tim Fulmer, Ph.D.

III. The 2007 – 2009 U.S. Financial Crisis & Recession

copyright 2014, Tim Fulmer, Ph.D.

Home values drop; foreclosures skyrocket

Value of asset-backed securities (ABS/MBS) drops; mark-to-market accounting

Value of banks drops; bankruptcies & bailouts

Value of bank collateral supporting daily operations drops; repo lines freeze

2H2006 2007 - 2008 2007 - 2008 2008

Valuation Crisis

2007 - 2008 Feb. 2007 – ABX begins collapsing

July – S&P lowers rating on 612 classes of residential mortgage bonds made 2005-2006: $12B debt

Oct. – Moody’s downgrades $33B mortgage-backed securities

Oct. – early 2008 – Moody’s downgrades 86% of all AAA 2006 mortgages and all BBB-rated securities

Dec. – Ratings dropped on $153B CDO slices

End of 2007– Bear Stearns writes down $2.6B in mortgage losses: 89% net income loss YOY

Sept. 30 2008 – SEC & FASB announce they will not suspend mark-to-market accounting

Banking Collapse

2008 - 2007 July – Bear Stearns closes two hedge funds Aug. 2007 – Repo haircuts begin [run on investment banks] Aug. 10 - Fed injects $38B liquidity into system Sept. 2007 – Fed starts cutting interest rates

March 12 – 18 2008: Bear Stearns stock falls 90%

March 16 – JPM/Fed rescue Bear Sterns

Sept. 7 – FHFA take Fannie & Freddie into conservatorship

Sept. 14 – Merrill Lynch sold to BOA

Sept. 15 – Lehmann Bros. bankruptcy

Sept. 16 – AIG bailout by Fed

Housing Collapse 2006 - 2007 June 2006 – real estate market peaks (average home prices will soon fall by 33% in the top 10 U.S. metro areas) Feb. 7 2007 – New Century reports a loss for 4Q06 April 2 – New Century files for bankruptcy

Timeline of the U.S. Financial Crisis*

*Sources: Chincarini (2012), Gorton (2012)

Recession

2008 - 2009 Sept. 6 -10 2008 – Dow falls 18% in one week

Dec. – CPI drops 0.7%

4Q2008 – Industrial output falls 11.5%

copyright 2014, Tim Fulmer, Ph.D.

Finding Blame for the U.S. Financial Crisis

Income and Wealth Inequality

“Easy Money” Fiscal And Monetary Policies

Bloated, Debt-Laden, Complacent Financial Sector

Financial Crisis and Recession (2007-2009)

Favored By Marxists

Favored By Neoliberals

Favored By Keynesians

Long-Term Declining GDP growth

copyright 2014, Tim Fulmer, Ph.D.

Data Supporting the Blame From 1969-2006, income inequality increased steadily (mainly owing to gains in IT/finance incomes)

From 06-2000 to 02-2004, Fed cut rate from 6.53% to 1% in response to internet bubble collapse , 9-11, & deflation scare

Financial Crisis and Recession (2007-2009)

In 2000-2011, GDP growth rate was 63% below 1960s levels

3

1,2

From the mid-80s, securitization of household debt increased sharply

4

From the mid-80s, outstanding mortgage-related securities increased dramatically

5

Since 2000, origination of sub- prime mortgages by GSEs and others increased sharply

6 7,8

Sources 1. Galbraith (2012), Figures 2.5, 6.1, 6.8 2. Bartels (2008), Figures 1.1, 1.2 3. Foster & McChesney (2012), Chart I.1 4. Gorton (2012), Figures 5.3, 5.4, 9.3 5. Gorton (2012), Figure 5.6 6. Chincarini (2012), Figure 10.3 7. Chincarini (2012), Figure 10.7 8. Allison (2013), Figure 3-1 9. Alpert (2013), Chapter 4 10. Stockman (2013), Chapter 4

From 1979 -2007, the incomes of the top 1% grew by 275%

9

From 1982-2008, household debt as a percentage of GDP rose from 47% to 97%

9

From 1982-2012, inflation-adjusted household income rose annually by 0.3%

10

copyright 2014, Tim Fulmer, Ph.D.

Our Macroeconomic Models Failed Us

“Most of the time, including during recessions, serious financial stability is not an issue. The standard [macroeconomic] models were designed for these non-crisis periods, and they have proven quite useful in that context. Notably, they were part of the intellectual framework that helped deliver low inflation and macroeconomic stability in most industrial countries during the two decades that began in the mid-1980s.”

-- Ben Bernanke, “On the Implications of the Financial Crisis for Economics” (Sept. 24, 2010, Princeton, New Jersey)

copyright 2014, Tim Fulmer, Ph.D.

Putting the Crisis in a Minskian Framework

“With the financial world in turmoil, Minsky’s work has become required reading. It is getting the recognition it richly deserves. The dramatic events of the past year and a half are a classic case of the kind of systemic breakdown that he – and relatively few others – envisioned.”

-- Janet Yellen, “A Minsky Meltdown: Lessons for Central Bankers” (April 16, 2009, New York City)

copyright 2014, Tim Fulmer, Ph.D.

Investors Seek New

Profit Outlets

Financial Innovation: Derivatives

Increased Debt

Financing

Investment Boom

Rapidly Rising Asset

Values

Minskian “Virtuous” Cycle – The Bubble Forms 1987 - 2007

Greenspan Put

Dollar Safe Haven

Low Interest Rates

Bush Tax Cuts

“Wall of Money”

“Tranquil” Prosperity

copyright 2014, Tim Fulmer, Ph.D.

Derivatives Bubble Bursts

Banks Holding Derivatives

Fail to Make Positions

Defaults and Bankruptcies

Increase

Loss of Confidence

Bank Repo Freezes

Banks Resort to Fire Sales to

Make Positions

Minskian Vicious Cycle – The Bubble Pops 2007 - 2009

Collapse of Investment Banks, AIG,

Fannie/Freddie

Negative Investment

Expectations

Decreased Productivity

Increased Unemployment

Decreased Consumption

Recession

Financial Crisis 2007 - 2008 Recession 2008 - 2009

copyright 2014, Tim Fulmer, Ph.D.

Avoiding the U.S. Financial Crisis

• Government policy seemed to have caused and solved the 2007 – 2009 financial collapse: a point in favor of neoliberal models

• Implied Counterfactual:

If an easy-money policy had not been in place to begin with, the financial sector would not have collapsed and there would have been no need for bailouts.

• Financial assets seemed to have been inefficiently priced/valued leading to a boom/bust scenario: a point in favor of Keynesian models

• Implied Counterfactual:

If we had not relied on unrealistic (overly optimistic) valuation models, we would not have overvalued our assets to begin with and there would have been no financial collapse.

copyright 2014, Tim Fulmer, Ph.D.

Avoiding the Crisis Cont’d

• Income and wealth inequality may have led to the easy-money policies that favored the 2007 – 2009 financial collapse: a point in favor of Marxist (and some Keynesian) models

• Implied Counterfactual:

If income and wealth had not been so unequally distributed across society, there would have been no need for easy-money

policies to drive growth in the first place.

copyright 2014, Tim Fulmer, Ph.D.

IV. The 2009-2014 Growth Stagnation

copyright 2014, Tim Fulmer, Ph.D.

Near-Zero Interest Rates …

In the wake of the 2007 – 2009 financial crisis, “the advanced economies all find themselves with short-term interest rates that are, as a practical matter, as close to zero as possible and therefore in a ‘liquidity trap’ in which additional liquidity has no further stimulative effect on growth in the affected economies. In short, with money moving at slow velocity through the real economy, excess liquidity merely piles up.”

“After repeated rounds of massive monetary stimulus we not only have anemic levels of start/stop growth, but we also have no meaningful inflation. In fact, in between rounds of monetary stimulus, we actually lapse into periods of disinflation and near-deflation!”

--Daniel Alpert, Chapter 5, The Age of Oversupply: Overcoming the Greatest Challenge of the Global Economy (2013)

copyright 2014, Tim Fulmer, Ph.D.

And Low Growth – Yet Asset Values Rise

“Since the start of this century, annual growth in U.S. domestic product has averaged less than 1.8 percent. The economy is now operating nearly 10 percent, or more than $1.6 trillion, below what the Congressional Budget Office judged to be its potential path as recently as 2007. And all this in the face of negative real interest rates for more than five years and extraordinarily easy money policies. … More troubling, even with the high degree of slack in the economy and with wage and price inflation slowing, there are signs of eroding credit standards and inflated asset values.”

--Lawrence Summers, “Strategies For Sustainable Growth,” The Washington Post (January 5, 2014)

copyright 2014, Tim Fulmer, Ph.D.

GDP under 3%, Inflation under 2%, …

copyright 2014, Tim Fulmer, Ph.D.

…And “Slow” Money…

copyright 2014, Tim Fulmer, Ph.D.

Despite 1-2% Interest Rates Worldwide …

copyright 2014, Tim Fulmer, Ph.D.

And A Bloated Fed Balance Sheet

copyright 2014, Tim Fulmer, Ph.D.

Meanwhile, Personal Income Inequality Grows, …

copyright 2014, Tim Fulmer, Ph.D.

Source of tables: Hungerford, 2012

Personal Wealth Inequality Grows, …

copyright 2014, Tim Fulmer, Ph.D.

And Corporate Profits Skyrocket

copyright 2014, Tim Fulmer, Ph.D.

Ratio of wages to corporate profits

Is This Secular Stagnation?

“There is a case for believing that the problem of maintaining adequate aggregate demand is going to be very persistent – that we may face something like the ‘secular stagnation’ many economists feared after World War II.”

“The stability of prices and output [from 1985 – 2007] masked an underlying unsustainable growth in leverage: It was a Minsky moment waiting to happen, and happen it did. When the Minsky moment came, there was a rush to deleverage; this drove down overall demand for any given interest rate … pushing us into a liquidity trap. … This meant that monetary policy could no longer do the job of stabilizing the economy: Central banks found themselves up against the zero lower bound. … And here’s the worrisome thing: what if it turns out that we need ever-growing debt to stay out of a liquidity trap?”

--Paul Krugman, “Bubbles, Regulation, and Secular Stagnation,” The New York Times (Sept. 25, 2013)

copyright 2014, Tim Fulmer, Ph.D.

… A Balance-Sheet Recession? Or…?

“When a debt-financed bubble bursts, asset prices collapse while liabilities remain, leaving millions of private sector balance sheets underwater. In order to regain their financial health and credit ratings, households and businesses are forced to repair their balance sheets by increasing savings or paying down debt. This act of deleveraging reduces aggregate demand and throws the economy into a [balance-sheet recession].”

“Flow of funds data for the U.S. show a massive shift away from borrowing to savings by the private sector since the housing bubble burst in 2007. The shift for the private sector as a whole represents 9 percent of U.S. GDP at a time of zero interest rates. Moreover, this increase in private sector savings exceeds the increase in government borrowings (5.8 percent GDP), which suggests that the government is not doing enough to offset private sector deleveraging.”

-- Richard Koo, “The world in balance sheet recession: causes, cure and politics” (2011)

copyright 2014, Tim Fulmer, Ph.D.

Decreased Aggregate Demand

Low Productivity, High Unemployment

Secular Stagnation/ Recession

Keynesian Vicious Cycle

High Levels of Risky Debt-Financing

Collapse of Financial Sector

Recession/ Depression

Minskian Vicious Cycle

High Income Managers

High consumption & High savings/investment

Low Income Workers

Low consumption & Low savings/investment

Low household debt & high financial market debt

High household debt

Income Inequality Wealth Inequality Systemic Debt Overload

Hypothesis: Secular stagnation arises from wealth inequality

Interest Rates at ZLB: “Liquidity Trap”

copyright 2014, Tim Fulmer, Ph.D.

Income Inequality Wealth Inequality Debt Overload

Decreased Aggregate Demand

Keynesian Scenario

Increased Risk of Financial Crisis

Minskian Scenario

Fiscal Policy

Monetary Policy

Both fiscal and monetary policy attempt to address the stagnation

Government Consumption & Confidence

Recession/ Stagnation

Recession/ Stagnation

copyright 2014, Tim Fulmer, Ph.D.

Income Inequality

Employment, Subsidies, Tax Breaks

Keynesian Scenario

Financial System Insurance

Minskian Scenario

Fiscal Policy

Monetary Policy

The policies, in theory, help both the wealthy & poor

• Welfare programs • Progressive Taxation

GDP Growth

• Bank bailouts • Deposit insurance

GDP Growth

The Wealthy

Low income/ Unemployed Population

“Give us income” “Protect our assets”

Federal Debt

copyright 2014, Tim Fulmer, Ph.D.

V. Policy Summary & Evaluation

copyright 2014, Tim Fulmer, Ph.D.

Policy Imperatives: 1985 - present

Policy Imperative

Benefit Risk Example Did it Work?

Sustained GDP Growth

Economy avoids the business

cycle

Irrational Exuberance;

Speculative Boom

Greenspan Put (1987 – 2007)

Yes

Prevention of “bust”

Economy avoids the business

cycle

GDP growth unnecessarily

curtailed

?? N/A

Support following

“bust”

Economy has a “floor”

Banking Moral Hazard

Fed direct lending to banks; TARP;

ARRA (2008-2009)

Yes

Renewed GDP Growth Post-

Support

Economic recovery despite

household “austerity”

Unsustainable levels of

government debt

Bernanke’s Quantitative Easing (QE) (2008-2012)

No (Not yet?)

copyright 2014, Tim Fulmer, Ph.D.

C. Supplementary Materials

copyright 2014, Tim Fulmer, Ph.D.

a. Opinions on What Caused the U.S. Financial Crisis

copyright 2014, Tim Fulmer, Ph.D.

Structured Finance Caused It

“I focus on four elements that I believe you cannot remove counterfactually and still explain the crisis. These are the bare essentials that made it possible. … They are … [1] the structure of collateral deals in US repo markets, [2] the structure of mortgage-backed derivatives and their role in repo transactions, [3] the role played by correlation and tail risk … , and [4] the damage done by a set of economic ideas that blinded [bankers and regulators] to [systemic risk]. … I stress that these are quintessentially private-sector phenomena” (italics mine).

-- Mark Blyth, Chapter 2, Austerity: The History of a Dangerous Idea (2013)

copyright 2014, Tim Fulmer, Ph.D.

A Run on Investment Banks Caused It

“The cause of financial crises is the vulnerability of transactions media, the privately created debt of financial institutions … A financial crisis in its pure form is an exit from bank debt. Such an exit can cause a massive deleveraging of the financial system.” “Whatever the form of bank money, financial crises are en masse demands by holders of bank debt for cash -- panics. The financial crisis of 2007 – 2008 was also a bank run, but it was not people who ran to their banks but firms running on investment banks.” -- Gary B. Gorton, Introduction, Misunderstanding Financial Crises: Why We Don’t See Them Coming (2012) “An important misunderstanding revealed by the [2007 – 2008] crisis is that regulators and economists did not know what firms were banks, or what debt was ‘money.’ … They did not realize that repo and asset-backed commercial paper (ABCP) are also money, indeed, the two most important money market instruments …”

-- Chapter 4 (2012)

copyright 2014, Tim Fulmer, Ph.D.

The Real Estate Bubble Caused It

“The 2008 crisis had its roots in real estate exposure, which was the common link between banking institutions, including regular banks, investment banks, hedge funds, insurance companies, and government-sponsored enterprises. When real estate values dropped, this immediately generated a string of losses throughout the economic system, then led to further economic problems.”

-- Ludwig B. Chincarini, Chapter 16, The Crisis of Crowding: Quant Copycats, Ugly Models, and the New Crash Normal (2012)

copyright 2014, Tim Fulmer, Ph.D.

Government Housing Policy Caused It

“Not only did government policy create the financial environment for a significant economic correction, but government policy makers unnecessarily turned a challenging economic environment into a crisis.” -- John A. Allison, Chapter 1, The Financial Crisis and the Free Market Cure: Why Pure Capitalism is the World’s Only Hope (2013) “The primary cause of the Great Recession was a massive mis-investment in residential real estate. … The primary sources of the massive misallocations of resources are: 1. The Federal Reserve, 2. The Federal Deposit Insurance Corporation (FDIC), 3. Government housing policy, primarily carried out by Fannie Mae and Freddie Mac, the giant government-sponsored enterprises, 4. The Securities and Exchange Commission (SEC). -- Chapter 2, (2013) “In a simple (but fundamental) sense, the only way there could have been a bubble … was if the Federal Reserve created too much money. … The ‘success’ of the Fed’s efforts to prevent significant market corrections from the early 1990s to 2007, which was achieved at the expense of a massive misallocation of capital (especially to the housing market), laid the groundwork for the [financial crisis and recession].” -- Chapter 3 (2013)

copyright 2014, Tim Fulmer, Ph.D.

Monetarism Caused It

“It is the monetary system itself, a system that enjoys wide bipartisan support, that is breaking down, and it is the federal government’s intervention into this aspect of our lives, far more than its push for subprime mortgages, that threatens our well-being and accounts for what happened” [during the financial crisis].

“While a handful of government programs and agencies helped direct our made-up money and credit to certain sectors, the hot air that filled the bubble was generated by the Fed.”

-- Thomas E. Woods Jr., Chapter 7, Meltdown: A Free-Market Look at Why the Stock Market Collapsed, the Economy Tanked, and Government Bailouts Will Make Things Worse (2009)

copyright 2014, Tim Fulmer, Ph.D.

Government Fiscal and Monetary Policy Caused It

The financial crisis “grew out of decades during which Washington defied the rules, corrupting the nation’s financial condition with unfinanced wars, tax cuts, and welfare state expansion, permitting rampant special interest plunder of the public purse and conducting a financial casino out of the Fed’s headquarters in Washington.”

“[Free markets and prosperity] have become the tools of a vicious form of crony capitalism and money politics and are in thrall to a statist policy ideology common to all three branches of today’s Washington economics: Keynesianism, monetarism, and supply-side-ism.”

-- David Stockman, Introduction, The Great Deformation: The Corruption of Capitalism in America (2013)

“The September 2008 meltdown was a financial cyclone which struck mainly within the vertical canyons of Wall Street, and would have burned out there in short order. This truth exposes the crony capitalist putsch that occurred in Washington during the fall of 2008 … There was never any evidence of Bernanke’s Great Depression bugaboo …”

-- Chapter 3 (2013)

copyright 2014, Tim Fulmer, Ph.D.

Income Inequality Caused It

“Persistent wage repression … poses the problem of lack of demand for the expanding output of capitalist corporations … The gap between what labor was earning and what it could spend was covered by the rise of the credit card industry and increasing indebtedness.”

“The growth of debt since the 1970s relates to a key underlying problem which I call ‘the capital surplus absorption problem.’ The turn to financialisation since 1973 was one born of necessity. It offered a way of dealing with the surplus absorption problem.”

“Banking became more indebted than any other sector of the economy. But when a couple of banks got into trouble, trust between banks eroded and fictitious leveraged liquidity disappeared. Deleveraging began, sparking the massive losses …”

“Government policies have exacerbated rather than assuaged the problem” (All italics mine).

-- David Harvey, Chapter 1, The Enigma of Capital and the Crises of Capitalism (2010)

copyright 2014, Tim Fulmer, Ph.D.

Wealth Inequality Caused It

“… In a deep sense, inequality was the heart of the [2007 – 2009] financial crisis. The crisis was about the terms of credit between the wealthy and everyone else, as mediated by mortgage companies, banks, ratings agencies, investment banks, government-sponsored enterprises, and the derivatives markets. Those terms of credit were what they were, because of the intrinsic instabilities involved in lending to those who cannot pay.”

-- James K. Galbraith, Chapter 1, Inequality and Instability: A Study of the World Economy Just Before the Great Crisis (2012)

“Very plainly, [rising income inequality based on the finance and IT sectors] means that since the 1980s the American business cycle has been based on financial and credit bubbles , and therefore on the enrichment, through the capital markets, of a very small number of people in a very few places. Truly we have become a “trickle-down” economy – as we were not before.”

-- Chapter 6 (2012)

copyright 2014, Tim Fulmer, Ph.D.

GDP Growth Stagnation Caused It

“Long-term economic slowdown … preceded the [2007 – 2009] financial crisis. … It was this underlying stagnation tendency … which was the reason the economy became so dependent on financialization – or a decades-long series of ever-larger speculative financial bubbles. In fact, a dangerous feedback loop between stagnation and financial bubbles has now emerged.”

“In the face of … vanishing profitable investment opportunities in the ‘real economy,’ capital formation or real investment gave way before the increased speculative use of the economic surplus of society in pursuit of capital gains through asset inflation.”

-- John Bellamy Foster & Robert W. McChesney, Introduction, The Endless Crisis: How Monopoly-Finance Capital Produces Stagnation and Upheaval from the U.S.A. to China (2012)

“Financial institutions, on their part, found new, innovative ways to accommodate this vast inflow of money capital and to leverage the financial superstructure of the economy up to ever greater heights with added borrowing… Financial expansion has become the main ‘fix’ for the system, yet is incapable of overcoming the underlying structural weakness of the economy.”

-- Chapter 1 (2012)

copyright 2014, Tim Fulmer, Ph.D.

b. Rebuttals to the Efficient Market Hypothesis (EMH)

copyright 2014, Tim Fulmer, Ph.D.

The EMH Fails To Address the Social and Historical Aspects of the Market

“Once the proposition that economic policy can shape the course of events is accepted, then answers to ‘Who will benefit?’ and ‘What production processes will be fostered?’ by policy come to the fore … we must also face the effects of institutional arrangements on social results … An appeal to an abstract market mechanism as the determinant of ‘for whom and ‘what kind’ is not permissible; what exists are specific, historical market mechanisms” (my italics).

-- Hyman Minsky, Chapter 1, Stabilizing an Unstable Economy (2008)

copyright 2014, Tim Fulmer, Ph.D.

Bubbles and Busts Cast Doubt on the EMH

“… That is where the perfect market vision starts to break down: Not only does the demand for liquidity move prices, but it – and not information – is also the primary driver of prices. … It is the primary driver of crashes and bubbles as well.”

--Richard Bookstaber, Chapter 10, A Demon of Our Own Design: Markets, Hedge Funds, and the Perils of Financial Innovation (2007)

“Financial models and investment philosophies must account for crowds and interconnected markets, both of which affect market prices regardless of inherent valuations. Bubbles sometimes form and capital allocation can become inefficient when crowds chase the same assets.”

--Ludwig Chincarini, Chapter 16, The Crisis of Crowding: Quant Copycats, Ugly Models, and the New Crash Normal (2012)

copyright 2014, Tim Fulmer, Ph.D.

Daily Market Fluctuations Cast Doubt on the EMH

“The core vulnerability of both EMH and REH [Rational Expectations Hypothesis] is the assertion that price as set in the equity markets equals fundamental value, as defined as the net present value of expected cash flows to be generated by the physical asset that underlies the financial asset. Explaining swings in asset prices not associated with any evident change in the fundamentals has challenged theorists for a long generation” (my italics).

-- William H. Janeway, Chapter 8, Doing Capitalism in the Innovation Economy: Markets, Speculation and the State (2012)

“Most of these items [that reflect company fundamentals], and the values attached to them, will hardly fluctuate as fast and far as the stock prices do. It is … a subterfuge … to say that market price will always oscillate around the true (equilibrium) price. But since no methods are developed to separate the oscillations from the basis, this is not an empirically testable assertion and it can be disregarded.”

-- Clive W.J. Granger and Oskar Morgenstern, Introduction, Predictability of Stock Market Prices (1970)

copyright 2014, Tim Fulmer, Ph.D.

The Success of the Financial Industry May Cast Doubt on the EMH

“Full adherence to the efficient market hypothesis leaves much of the financial industry in a paradoxical position. It is precisely the activity of the many people trying to track down information to make profitable trades that leads the markets to be efficient. But in the aggregate this leaves investors and traders unable to extract profits for all their trouble. … They are needed to make the markets efficient, but because they do so, they cannot profit from it.”

--Richard Bookstaber, Chapter 10, A Demon of Our Own Design: Markets, Hedge Funds, and the Perils of Financial Innovation (2007)

“Hedge funds and other investors make money in spite of a world with full information because people do not act based on full information. … Our coarse behavior literally leaves money for the taking.”

--Bookstaber, Chapter 10 (2007)

copyright 2014, Tim Fulmer, Ph.D.

c. Rebuttals to Using Policy

copyright 2014, Tim Fulmer, Ph.D.

We Do Not Know Enough to Ensure Policy Won’t Disturb the Economy

“In fiscal policy as in monetary policy, all political considerations aside, we simply do not know enough to be able to use deliberate changes in taxation or expenditures as a sensitive stabilizing mechanism. In the process of trying to do so, we almost surely make matters worse. … We make matters worse by introducing a largely random disturbance that is simply added to other disturbances.”

-- Milton Friedman, Chapter V, Capitalism And Freedom (1962, 1982, 2002)

copyright 2014, Tim Fulmer, Ph.D.

Rational Decision-Making Nullifies Keynesian Policy

The argument runs as follows*:

1) A Keynesian model typically assumes that economic agents have “adaptive expectations,” i.e., the agents expect the future to be a continuation or “average” of the past. Consequently, a Keynesian model has no way of formulating expectations for a future that is substantially different from the past.

2) Yet we know from experience that a new economic policy may, in fact, signal a significant change from the past and thus lead economic agents to behave “rationally” by adopting substantially altered expectations of the future.

3) Thus, based on experience, we can assert that economic agents make decisions based on “rational expectations,” not on adaptive expectations.

4) But if that’s the case, the assumption of adaptive expectations underlying Keynesian models is wrong or, at best, correct only under unrealistic circumstances that require economic agents to behave irrationally.

5) Consequently, the accuracy and utility of the models themselves are thrown into doubt as are any policy forecasts based on those models.

*Based on Mark H. Willes’ “’Rational Expectations’ as a Counterrevolution,” published in The Crisis in Economic Theory (1981).

copyright 2014, Tim Fulmer, Ph.D.

Keynesian Policies May Encourage Excessive Government Spending

“When the economy is weak, the right course is for the government to spend as much money as possible. Doing so will not only restore prosperity by stimulating aggregate demand but will alleviate the suffering and economic security that accompany business downturns. When the economy is strong, however, the right course is … well, then it’s also for the government to spend as much money as possible. Doing so is necessary to redress the imbalance between private splendor and public squalor … With all this wealth we can afford to try … anything. Everything.”

“The precise economic conditions that call for reducing or merely stabilizing government spending remain unspecified …”

--William Voegeli, Chapter 4, Never Enough: America’s Limitless Welfare State (2012)

copyright 2014, Tim Fulmer, Ph.D.

Policy Leads To Artificial Booms & Busts

“A free market is in constant correction. … When the Federal Reserve steps in and uses monetary policy to stop the downside correction process, all it achieves is to defer problems to the future and make them worse. Its action delays and distorts the natural market correction process, thereby reducing the long-term productivity of the economic system by encouraging a misuse of capital and labor.”

[Individual market participants in a free market] “often make counterbalancing mistakes, unless ‘Big Brother,’ in this case the Federal Reserve, drives almost all market participants in the same wrong direction.”

-- John A. Allison, Chapter 3, The Financial Crisis and the Free Market Cure: Why Pure Capitalism is the World’s Only Hope (2013)

copyright 2014, Tim Fulmer, Ph.D.

The Business Cycle “Disturbed” by Government Policy

Pro-cyclical Policies

Counter-cyclical Policies

“Boom” Overheated Economy

“Bust” Recession

Low Interest Rates; Deficit Spending

High interest rates

Low Consumption - High Savings

Artificially Low interest Rate

Loans

Excess Long-term

Investment

Mal-Investment

Excess Consumption

Artificially High Interest Rate

Loans

Long-term Investment

Unsustainable

High

Unemployment

copyright 2014, Tim Fulmer, Ph.D.

D. Bibliography

Allison, John A. 2013. The Financial Crisis and the Free Market Cure: Why Pure Capitalism is the World’s Only Hope Alpert, Daniel. 2013. The Age of Oversupply: Overcoming the Greatest Challenge to the Global Economy Bartels, Larry M. 2008. Unequal Democracy: The Political Economy of the New Gilded Age Bell, Daniel and Kristol, Iriving, Eds. 1981. The Crisis In Economic Theory

Bernanke, Ben. 2013. “Long-Term Interest Rates: http://www.federalreserve.gov/newsevents/speech/bernanke20130301a.htm Bernanke, Ben. 2010. “On the Implications of the Financial Crisis for Economics”: http://www.federalreserve.gov/newsevents/speech/bernanke20100924a.pdf Bernanke, Ben, Gertler, Mark, and Gilchrist, Simon. 1996 “The Financial Accelerator and the Flight to Quality,” The Review of Economics and Statistics, Vol. 78. Blyth, Mark. 2013. Austerity: The History of a Dangerous Idea Blyth, Mark. 2002. Great Transformations: Economic Ideas And Institutional Change in the Twentieth Century Bookstaber, Richard. 2007. A Demon of Our Own Design: Markets, Hedge Funds, and the Perils of Financial Innovation Chincarini, Ludwig B. 2012. The Crisis of Crowding: Quant Copycats, Ugly Models, and the New Crash Normal Foster, John Bellamy & McChesney, Robert W. 2012. The Endless Crisis: How Monopoly-Finance Capital Produces Stagnation and Upheaval from the U.S.A. to China Friedman, Milton. 1962; 1982; 2002. Capitalism And Freedom Galbraith, James K. 2012. Inequality and Instability: A Study of the World Economy Just Before the Great Crisis Gorton, Gary B. 2012. Misunderstanding Financial Crises: Why We Don’t See Them Coming Granger, Clive W.J. and Morgenstern, Oskar. 1970. Predictability of Stock Market Prices Hansen, Alvin H. 1951; 1964. Business Cycles and National Income Harvey, David. 2010. The Enigma of Capital and the Crises of Capitalism Hayek, Friedrich A. 1945. “The Use of Knowledge in Society”

copyright 2014, Tim Fulmer, Ph.D.

D. Bibliography Cont’d Hicks, J. R. 1937. “Mr. Keynes and the ‘Classics’: A Suggested Interpretation,” Econometrica, Vol. 5 Hungerford, T. L. 2012. “Taxes and the Economy: An Economic Analysis of the Top Tax Rates Since 1945,” a CRS report Janeway, William H. 2012. Doing Capitalism in the Innovation Economy: Markets, Speculation and the State Keynes, John Maynard. 1936. The General Theory of Employment, Interest, and Money Keynes, John Maynard. 1937. “The General Theory of Employment,” The Quarterly Journal of Economics, Vol. 51 Keynes, John Maynard. 1932. The Means To Prosperity Richard Koo. 2011. “The world in balance sheet recession: causes, cure and politics,” Real-World Economics Review, No. 58 Krugman, Paul. 2013, Sept. 25. “Bubbles, Regulation, and Secular Stagnation,” The New York Times Lucas, Robert. 1976. “Econometric Policy Valuation: A Critique,” Carnegie-Rochester Conference Series on Public Policy, Vol. 1 Michael, N. and Moore, S. 2014. “Quantitative Easing, the Fed’s Balance Sheet, and Central Bank Insolvency,” a Heritage Foundation Backgrounder Miller, Merton H. and Modigliani, Franco. 1961. “Dividend Policy, Growth, and the Evaluation of Shares,” The Journal of Business, Vol. 34 Minsky, Hyman. 2008; 1975. John Maynard Keynes Minsky, Hyman. 2008; 1986. Stabilizing an Unstable Economy Muth, John. 1961. “Rational Expectations and the Theory of Price Movements,” Econometrica, Vol. 29. Stockman, David. 2013. The Great Deformation: The Corruption of Capitalism in America Summers, Lawrence. 2014, Jan. 5. “Strategies For Sustainable Growth,” The Washington Post Viner, J. 1936. “Mr. Keynes on the Causes of Unemployment,” The Quarterly Journal of Economics, Vol. 51. Voegeli, William. 2010, 2012. Never Enough: America’s Limitless Welfare State Woods, Thomas E., Jr. 2009. Meltdown: A Free-Market Look at Why the Stock Market Collapsed, the Economy Tanked, and Government Bailouts Will Make Things Worse Yellen, Janet . 2009. “A Minsky Meltdown: Lessons for Central Bankers”: http://www.frbsf.org/economic-research/publications/economic-letter/2009/may/minsky-central-bank-asset-price-bubbles/

copyright 2014, Tim Fulmer, Ph.D.