Embed Size (px)

Citation preview

RESTAURANT BRANDS NEW ZEALAND LIMITED

Sydney

4 May 2017Russel Creedy Group CEO

Macquarie Investor Day Presentation

Presentation Outline

• RBD – Who Are We

• FY17 Trading Results

• Hawaiian Acquisition

• Growth Opportunities

Restaurant Brands (RBD) is a corporate franchisee based in New Zealand with operations in Hawaii and Australia

Restaurant Brands has seen a solid sales and profit performance primarily from its New Zealand business over the past 5 years

311.9 329.3 359.5 387.6

497.2

FY2013 FY2014 FY2015 FY2016 FY2017

Sales $NZm

17.7 18.922.5 24.2

30.6

FY2013 FY2014 FY2015 FY2016 FY2017

Trading NPAT $NZm

Restaurant Brands is truly an international multi-brand operator

NZ Australia NZ NZ HawaiiHawaii TotalNZ$NZm

Sales 310 130 40 25 40 100 80 725

Brand EBITDA 65 20 4 5 2 18 8 122

People 2,300 2,200 400 300 450 850 1,070 7,570

Stores 94 47 30 24 20 37 45 297

FY18 (analyst consensus)

Trading results for the 12 months ended 27 February 2017 (FY17)

Commentary (FY17 vs FY16)

• Group Revenues +28.1%

• NPAT (excluding non-trading) +26.3%

• Reported NPAT (including non-trading) +7.8%

• Brand EBITDA +$19.3m driven by KFC Australia

• Fully imputed 13.5 cps final dividend brings full year to +9.5%

• Hawaiian expansion with acquisition of Pacific Island Restaurants (post balance date)

FY15 FY16 FY17

$372.6m $404.1m $517.5m

$22.5m $24.2m $30.6m

$23.8m $24.1m $26.0m

$61.5m $66.9m $86.2m

19.0cps 21.0cps 23.0cps

- 82 stores

Restaurant Brands enjoys very strong operating cash flows

Cash Flow $m FY15 FY16 FY17

Operating cash flow 36.5 44.3 47.9

Investing cash flow (33.0) (15.3) (79.0)

Free cash flow 3.5 29.0 (31.1)

FY15 FY16 FY17Investing cash outflow (QSR) - - (63.9)

Investing cash outflow (other) (41.4) (20.8) (20.3)

Investing cash inflow 8.4 5.5 5.2

(33.0) (15.3) (79.0)

The New Zealand business grew strongly in FY17 with sales of $400m, led by KFC

265.0 282.5

296.5

7.7%6.3%

3.6%

FY15 FY16 FY17

KFC Sales

Total Sales $m Same Store Sales %

48.4 44.9 40.5

6.3% 2.6%3.6%

FY15 FY16 FY17

Pizza Hut Sales

Total Sales $m Same Store Sales %

26.1

26.8

26.7

5.1%

6.9%

4.5%

FY15 FY16 FY17

Starbucks Sales

Total Sales $m Same Store Sales %

20.1 33.4 36.3

-28%-5% -3.8%

FY15 FY16 FY17

Carl's Jr. Sales

Total Sales $m Same Store Sales %

KFC also drove New Zealand earnings growth in FY17

50.8 57.2 61.4

19.2%20.2%

20.7%

12.0%

16.0%

20.0%

FY15 FY16 FY17

KFC EBITDA

EBITDA $m EBITDA % of Sales

6.4 4.9 4.1

13.2%

10.9%10.0%

0.0%

4.0%

8.0%

12.0%

16.0%

FY15 FY16 FY17

Pizza Hut EBITDA

EBITDA $m EBITDA % of Sales

4.3 4.4

4.8

16.3% 16.4%

17.8%

12.0%

16.0%

20.0%

FY15 FY16 FY17

Starbucks EBITDA

EBITDA $m EBITDA % of Sales

0.2

0.4

1.0

0.8% 1.3%

2.7%

FY15 FY16 FY17

Carl's Jr. EBITDA

EBITDA $m EBITDA % of Sales

Dividend up 9.5% to 23.0 cents commensurate with profitability (fully imputed at 28%)

FY15 FY16 FY17

Earnings per share (excluding non-trading) cps 23.0 24.7 28.4

Total dividend cps 19.0 21.0 23.0

Payout ratio of NPAT (excluding non-trading) % 83% 85% 81%

The QSR acquisition settled on 27 April 2016. The 42 KFC stores have delivered ahead of plan

97.2

116.6 106.4

FY17 (10 monthsactual)

FY17 (annualised) Year 1 Target

$NZm

QSR – Sales above Target

15.0

18.0 16.0

FY17 (10 monthsactual)

FY17 (annualised) Year 1 Target

$NZm

EBITDA up on target

Material growth opportunities are already being exploited in Australia

Expand restaurant networkA number of locations have been identified which represent ideal and profitable opportunities to increase the restaurant portfolio footprint in existing trade area

Acquire other franchises/portfoliosPotential scope to expand the QSR KFC portfolio footprint in NSW and other states, either through building restaurants in new locations or the acquisition of other franchise portfolios in the KFC network

Potential acquisition of Yum restaurantsYum owns approximately 150 KFC restaurants in Australia and has just put 100 of them on the market

• Two new stores under construction • Five independent store acquired (settled after balance date)

• RBD is actively evaluating the possible purchase of some of these stores

Restaurant Brands Hawaii – Progress to date

• Agreement to purchase 100% of shares in Pacific Island Restaurants Inc. (PIR) for $US105 million signed 26 October 2016

• PIR is the sole Taco Bell and Pizza Hut franchisee in Hawaii, Guam and Saipan

• Successful capital raising in November 2016 through Accelerated Renounceable Entitlement Offer (AREO) raised $NZ94 million from mainly existing shareholders

• Transaction was finally settled on 7 March 2017

• Acquired business is expected to deliver $NZ180 million in sales and store EBITDA of $27 million; on target to deliver this to date

Transaction highlights

PIR is a well-established, profitable business with potential for improved profitability from a targeted re-investment programme, and provides a beachhead for other potential opportunities

1. Established in 1971, PIR is the sole Taco Bell and Pizza Hut franchisee in Hawaii, Guam and Saipan, has been consistently profitable in recent years and has a stable, experienced management team (average tenure of 25 years)

2. Taco Bell and Pizza Hut are both iconic Yum! brands and have leading positions in their respective markets with attractive and stable margins

3. There is an opportunity to execute an investment programme (which has been substantially agreed with Yum!) to progressively refresh PIR’s stores, which Restaurant Brands believes will improve PIR’s profitability, reflecting RBNZ’s experience over the last ten years in New Zealand

4. PIR provides the next stage of RBNZ’s growth platform and an entry point into the Hawaii market and platform for other potential bolt-on acquisitions

5. Hawaii has a stable legal and economic framework, with sound forecast GDP growth of approximately 4% p.a. from 2015 forecast through to 20192

6. PIR’s primary exposure is to the domestic Hawaiian market, and provides an opportunity to service a portion of the 8.9 million visitor arrivals to Hawaii each year

• Store network

Hawaii Guam Saipan

30

38

7

6 1

• Leading market share in branded QSR pizza and Mexican food in Hawaii1

Pizza Hut43%

Domino's21%

Papa John's16%

Little Caesars12%

Boston's7%

Harpo's1%

Taco Bell91%

Taco Del Mar9%

• 1. Market share data as at March 2016 based on Oahu, Hawaii customer visits per Ward Research Inc, extrapolated to account for PIR presence in neighbouring islands; 2. State Hawaii, Department of Business, Economic Development and Tourism, Outlook for the Economy Q3 2016.

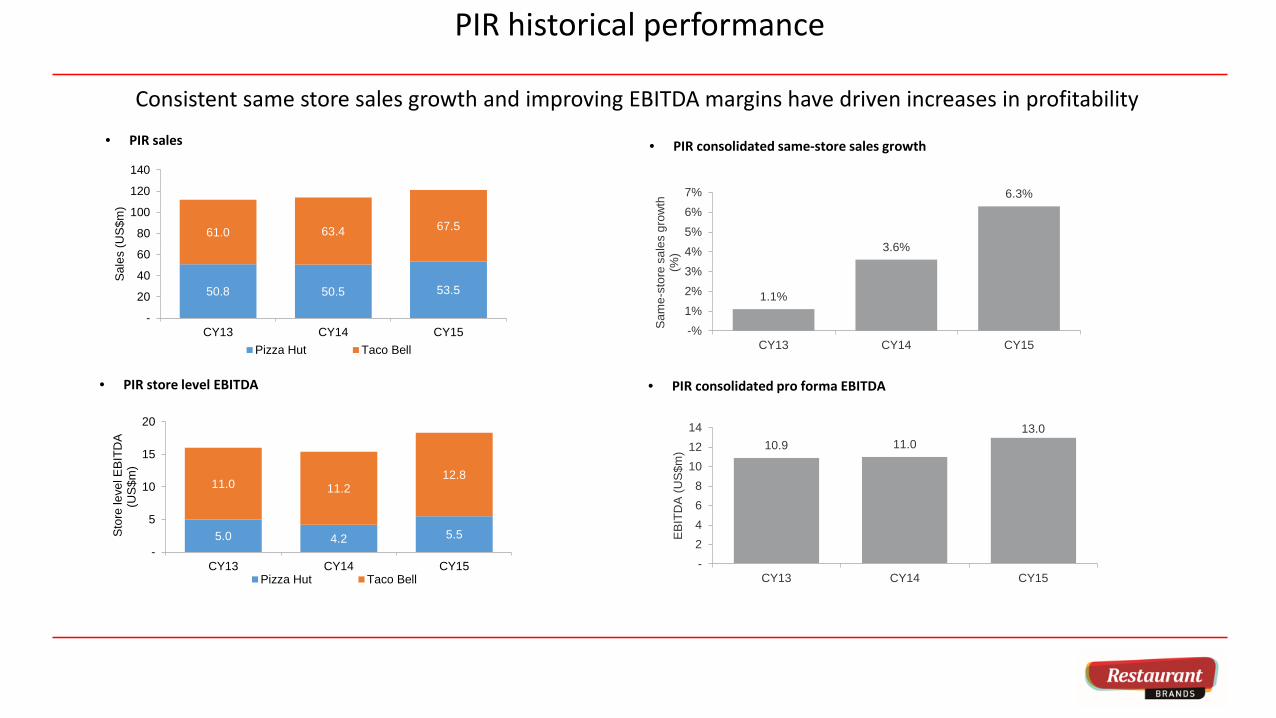

PIR historical performance

Consistent same store sales growth and improving EBITDA margins have driven increases in profitability

• PIR consolidated same-store sales growth

• PIR store level EBITDA • PIR consolidated pro forma EBITDA

• PIR sales

1.1%

3.6%

6.3%

-%1%2%3%4%5%6%7%

CY13 CY14 CY15

Sam

e-st

ore

sale

s gr

owth

(%

)

50.8 50.5 53.5

61.0 63.4 67.5

-

20

40

60

80

100

120

140

CY13 CY14 CY15

Sal

es (U

S$m

)

Pizza Hut Taco Bell

5.0 4.2 5.5

11.0 11.212.8

-

5

10

15

20

CY13 CY14 CY15

Sto

re le

vel E

BIT

DA

(U

S$m

)

Pizza Hut Taco Bell

10.9 11.013.0

-2468

101214

CY13 CY14 CY15

EB

ITD

A (U

S$m

)

Taco Bell

Taco Bell is a strongly performing QSR with a loyal customer base and strong margins

Key facts Hawaiian market leader in Mexican QSR1

10.2 11.0 11.212.8

-

5

10

15

CY12 CY13 CY14 CY15

Sto

re le

vel E

BIT

DA

(U

S$m

)

1. Market share data as at March 2016 based on Oahu, Hawaii customer visits per Ward Research Inc, extrapolated to account for PIR presence in neighbouring islands.

• 37 stores, 30 in Hawaii and seven in Guam

• Contributed 70% of PIR’s CY15 store level EBITDA

• Leading Mexican QSR in the local market; key competitors include:

• McDonald’s, Burger King, Jack in the Box, Wendy’s, Zippy’sand Taco Del Mar

• Taco Bell store formats cover drive-thru, dine-in and takeaway

• Higher margins driven in part by an all day menu which includes breakfast and late night options

• Staged upgrade of “mission style” buildings by 2025

Unique product offering supported by continued innovation

EBITDA growth driven by a combination of sales growth and margin improvement (US$m and % sales)

CrunchwrapSupreme

Nacho Cheese Doritos Locos

taco

QuesalupaBreakfast Crunchwrap

Taco Bell91%

Taco Del Mar9%

Pizza Hut

• 45 stores, 38 in Hawaii, six in Guam and one in Saipan

• Contributed 30% of PIR’s CY15 store level EBITDA

• Pizza Hut has a higher Hawaiian market share than its next two largest competitors combined1

• Named Hawaii’s Best Pizza by the Honolulu Star-Advertiser in 2016

• Stable store level EBITDA margin of ~10%

• Store upgrade plan commenced in 2015, with the majority of stores still to be upgraded

Pizza Hut is the Hawaiian market leader in Pizza QSR1Key facts

Consistent EBITDA (US$m and % sales)2

PIR has a strong network of Pizza Hut stores, which operate on similar margins to Pizza Hut New Zealand

Pizza Hut43%

Domino's21%

Papa John's16%

Little Caesars12%

Boston's7%

Harpo's1%

1 of 13 Red Roof stores, the other 32 stores are Delco (Delivery / Pickup) or Food Court stores

Strong store network

38

14 14 116

1

Pizza hut Domino's Papa Johns LittleCaesars

Boston's Harpo'sHarpo’s

4.9 5.04.2

5.5

-123456

CY12 CY13 CY14 CY15

Sto

re le

vel E

BIT

DA

(U

S$m

)

1. Market share data as at March 2016 based on Oahu, Hawaii customer visits per Ward Research Inc, extrapolated to account for PIR presence in neighbouring islands; 2. CY14 margins impacted by high commodity prices, particularly cheese

Store refresh strategy

• PIR has recently agreed a ten year investment programme with Yum! for Taco Bell and is in advanced discussions for Pizza Hut

• The investment programmes are expected to be funded out of PIR’s operating cash flows and PIR debt facility

• RBNZ’s own experience in New Zealand has been that store refresh expenditure typically results in increased store sales and profitability and generates an attractive return on capital

• In New Zealand, RBNZ has been able to achieve sustainable sales growth and an uplift in profitability across its whole store portfolio from its refresh programme

• In light of this RBNZ may spend in excess of the investment programme where management identifies attractive opportunities

New Zealand KFC Transformation ProgrammeOverview

KFC New Zealand sales growth following store transformation programme

-1

4

9

14

19

24

140

160

180

200

220

240

260

1996 1997 1998 1999 2000 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Transformation Spend ($m's) (Right Axis) Sales Revenue ($m's) (Left Axis)

Befo

re

tran

sfor

mat

ion

Afte

r tr

ansf

orm

atio

n

Restaurant Brands’ experience in New Zealand indicates that a targeted store refresh programme could further improve PIR’s profitibility

Growth Opportunities

GROWTH PATH

TRANSFORMATION & STORE REINVESTMENT

(Existing brand and geography)

Running the business better• Strong Operations• Compelling Marketing

ASSET INVESTMENT

Build profitable network growth through asset build or acquisition

BUILD NEW STORES(Existing brand and geography)

ACQUIRE INDIVIDUAL STORES(Existing geography and brand)

ACQUIRE LARGE NUMBERS OF STORES

(Existing brand and geography)

BUILD/ACQUIRE NEW BRAND

• KFC New Zealand• Taco Bell Hawaii• Pizza Hut Hawaii

• INFILL• GREENFIELD

• Pizza Hut New Zealand• KFC New Zealand• Taco Bell Hawaii• KFC Australia

• KFC New Zealand• KFC Australia • KFC Australia • Taco Bell New Zealand

• KFC Hawaii• Taco Bell Australia

ORGANIC

“To build RBD to a $1 billion company in sales and market capitalisation by growing both top and bottom line”

Strategic plans have identified expansion potential in Australia and the US, utilising strong expertise with franchise brands

New Zealand Australia Hawaii US

x x

x x x

x x

x

Presentx

identified growth opportunitiesno current expansion plans

![PM 2014 investor day 2014-06-26-CEO Investor Day Slides [FINAL]](https://img.pdfslide.us/doc/110x75/577cbc651a28aba7118da313/pm-2014-investor-day-2014-06-26-ceo-investor-day-slides-final.jpg)

![PM 2014 investor day 2014-06-26-Operations Investor Day Slides [FINAL]](https://img.pdfslide.us/doc/110x75/577cbc651a28aba7118da314/pm-2014-investor-day-2014-06-26-operations-investor-day-slides-final.jpg)