Embed Size (px)

Citation preview

Machinery insurance

Machinery insurance_e 03.11.2000 8:14 Uhr Seite u3

Machinery insurance

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 1

Contents

1 Introduction 5

2 Scope of cover 7

3 Insured items 8

4 Insured perils 10

5 General conditions 12

6 Exclusions 13

7 Sum insured 17

8 Property valuation 18

9 Premium calculation 24

10 Deductible (excess) 25

11 Risk inspection 26

12 Clauses/cover extensions 29

13 Indirect damage insurance 31

14 Rating 32

15 Claims handling 34

16 Outlook 37

Appendix: Index of terms 38

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 3

5

Machinery insurance has always been instrumen-tal in promoting the acceptance of new technolo-gies. A direct correlation between the economicclimate and the acceptance of new technologyremains. For instance, nuclear power plant facili-ties and high output thermal and hydroelectricpower plants could have never been built andoperated without the backing of adequate insur-ance protection. Even financially strong enter-prises would have hardly had the means toabsorb potential or even actual losses incurred.

Apart from surging technological progress, anadverse competitive environment also compelsindustry players to tighten production and test-ing schedules so that new machines and equip-ment are often installed onsite without priorcomprehensive testing. Insurers may also providecover for machines and equipment which, inresponse to greater commercial pressures, featurenovel designs and new, unproven materials andprocesses. Underwriters are advised to exercisecaution when providing cover for this category of risk.

This brochure is designed to assist underwritersin this challenging field of insurance by pro-viding sound fundamentals before discussingspecific technical details and typical problemareas of machinery insurance.

1 Introduction

The origin of boiler and machinery insurance isinseparably linked with harnessing and utilisingpower. Virtually nothing has changed in everydaylife as radically as power generation. The inven-tion of the steam engine in the early 19th cen-tury launched the industrial revolution, usheringin a new era with decisive, far-reaching changes.

The advent of the steam engine also creatednovel hazards and prompted the need for anentirely new range of insurance covers. Technicalcovers including boiler and pressure vessel insur-ance and machinery insurance were designed to protect equipment such as steam boilers,turbines, generators and motors which generateor utilise power. Moreover, changing socio-economic factors, which shifted the workplacefrom the home to the factory f loor, promptedthe need for employers’ liability and workmen’scompensation insurance.

Today’s ever greater power demands for produc-ing capital and consumer goods coupled withincreased urbanisation continues to spur devel-opments toward attaining higher performancemachines and installations of enhanced effi-ciency. Technological advancement has led tonew materials which must withstand more strin-gent design parameters such as higher pressures,temperatures, operating speeds, etc. This, inturn, has led to greater stresses and increasedexposure to both material and operating failures.The development of higher performancemachines targets greater capacity and efficiencyas an ongoing objective, and manufacturersvigorously vie with one other to push the limitsof technology.

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 5

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 6

7

Apart from conventional fire and extended perilscoverage, no commercial property risk manage-ment programme is complete without consider-ing mechanical and electrical equipment break-down exposure. Any device that uses, generatesor alters mechanical or electrical power is subjectto break down.

Machinery insurance provides cover against a wide range of losses from breakdown of plantproduction equipment, electrical equipment,boilers, pressure vessels, heating and coolingequipment, etc.

In addition to material damage, equipmentbreakdown frequently results in substantialconsequential loss such as business interruption,extra expenses and ancillary services interruption(eg power generation, refrigeration systems, etc).Insurance can be extended to include theseconsequential losses either as stand-alone coversor as endorsements to the direct damage cover.

The primary focus of engineering insurancecover is not the type of perils insured, sincepolicies, by and large, provide quasi all-riskcover; rather, the special features of the insureditems are the decisive criteria in this insurancecategory.

Consequently, it is evident that a broad spec-trum of items can be insured, eg power plants,printing machines, chemical installations, com-puters etc. The great diversity of insurable itemsnaturally implies an equally wide range of dif-ferent insurance requirements. All engineeringcovers in force today can be subdivided basicallyinto two main categories, ie single project coversand those annually renewable. Boiler andmachinery insurance covers constitute the largestshare of the latter category.

2 Scope of cover

Engineering insurance

Since machinery covers were first introduced, thescope of cover has changed to optimally complywith client needs and is still subject to ongoingmodification. As will be discussed, the scope of cover may vary from country to country, butthe basic elements of all policies remain thesame.

Business insurance (BI)Deterioration of stock(DOS)Extra expensesetc

Delay in startup (DSU)Force majeure (FM)Liquidated damages(LD)

Third party liabilityBodily injury

Mat

eria

lda

mag

e co

ver

Con

sequ

enti

allo

ss c

over

sC

asua

lty

Non-renewable Renewable

Boiler explosionMachinery insuranceContractors’ plantComputerLow voltage &electronic equipmentetc

EARCARDefectsLiability

Technically, a break-down is a malfunc-tion, but is insurableonly when it issudden, accidentaland involves physi-cal damage to themachine or equip-ment in whole orpart.

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 7

8

3 Insured items

For insurance purposes, machine items aredescribed according to the following threecategories:

Individual listing A specific, detailed list and brief description of each item insured. The list should includespecifications such as rating, continuous workingcapacity (kW), operating speed (rpm), safetyvalue load, etc; year of manufacture, manufac-turer’s name and registration number, new replacement value.

Blanket groups Insurance covers for specific machine and equip-ment categories, eg blanket all boilers. Policies inthis category provide cover for all items of thatparticular specification (in our example, boilers).

Comprehensive formThis category includes all machines and equip-ment installed at the insured site(s).

The comprehensive form of cover is so broadthat it includes many items of low value, whichare hardly worth insuring. However, since thecost of insuring each of these items individuallywould be prohibitive, an adequate deductible ismandatory for this cover to keep insurance costwithin an economically justifiable level.

Machinery insurance covers a truly diverse spec-trum of machines and equipment in commercialand production facilities. Cover is granted onlyfor those machines and equipment items whichare cited in the policy schedule and are in use or intended for use at the site indicated in thepolicy. Therefore, the insured items must beaccurately described, particularly in cases wherecover is granted not only for stand-alonemachines but for entire plants.

Ready for use

Plant facilities and machines are considered ready foruse after successful testing and commissioning and assuch are ready for commercial operation.

Test procedures for equipment acceptance by the buyer(operator) are detailed in the works and/or supplycontract. A Provisional Acceptance Certificate (PAC) isissued after these tests have been successfully com-pleted. It cites all minor defects or deficiencies whichwill not jeopardise safe operation of the item.

The responsibility for the insured object is then trans-ferred from the builder/supplier to the buyer/operator, ie the buyer/operator now bears the responsibility for the risk of loss, except for the minor defects ordiscrepancies cited in the PAC.

The need for machinery insurance also arises at thispoint. The successful testing/commissioning of theinsured item is the sole prerequisite for machinery insur-ance eligibility, and cover is not extended for lossesencountered prior to successful testing/commissioning.The testing/commissioning phase of any item must be covered elsewhere, usually within the scope of therelevant Erection All Risk (EAR) policy (builders’ risk).

After the machines/items have been installed at theinsured location and are ready for use, they can be ini-tially insured and remain covered irrespective of whetherthey are in use, not in use, dismantled for cleaning,maintenance or overhauling or are being moved on thepremises or during the course of subsequent re-erection.Re-commissioning of machines and equipment afteroverhauling or repair is covered within the scope ofmachinery insurance. However, this cover excludes thetesting/commissioning of new machines.

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 8

9

The terms blanket and/or comprehensive aretypically found in US policies. In the Europeanmarket, it is more common to find schedulescontaining a detailed list of individual items. Thisis because, in Europe, the insured is required to complete a relevant questionnaire and furnishthe insurer with the requested informationregarding the machines and equipment to beinsured. The insured bears all responsibility forany inaccurate information.

By contrast, it is common practice in the US forthe insurer to obtain the relevant information atthe insured premises. Consequently, the insuredis obligated to permit a survey and to answer all questions correctly and in good faith suchthat the insurer is able to adequately assess theexposure at the insured premises.

The term blanket often leads to misunderstand-ing by insurers more familiar with the Europeanform. A US policy written on the blanket basis,does not – as is often erroneously assumed – lackthe full details on all the covered machines andequipment. By inspecting the plant(s), theinsurer obtains the information required to cor-rectly assess the risk and gauge the cover price.However, the insurer considers this type of infor-mation confidential and therefore does not inte-grate it in the policy or make it available topotential competitor(s), brokers or other insur-ance companies.

If the insured provides the underwriting infor-mation on the basis of a completed question-naire typical for the European form, it is custom-ary to integrate the questionnaire in the policy.

Regardless of the manner used to describe the insured machines and equipment (insureditems), certain components and parts areexcluded from coverage.

Cover excludes the following:Exchangeable tools – drills– crusher bits, etc

Non-metallic parts – foundation blocks – furnace refractories– conveyor belts

Feedstock and media, eg:– fuels, catalysts, etc.

The following types of equipment are custom-arily excluded from machinery insurance:

Office machinesData processing equipmentVehicles Mobile construction equipment

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 9

10

Machinery insurance is a quasi all risk cover and provides protection (subject to specificexclusions) against any sudden and unforeseenphysical loss or damage to the insured machinesand equipment. Emphasis is placed on the termsudden and unforeseen or, quite often, on thesynonymous term sudden and accidental which is regarded as a single concept. By itself, the termsudden is of little significance since any damagein insurance nomenclature which can no longerbe prevented would be considered suddendamage, irrespective of the time frame in whichit occurred, provided that, based on generalexperience, such an event could not have beenreasonably expected.

Any loss or damage under machinery insurancecover must be sudden and unforeseen (acciden-tal) insofar as the insured is concerned. The termunforeseen (or accidental) denotes damage whichthe insured neither noticed in time nor couldhave had foreseen despite a degree of competencereasonably expected from the machine operator.In this context, the insured is understood as themanagement of the insured including the opera-tions manager. Moreover, the insured is obligedto carefully monitor machine operation forunusual noises, vibrations, output reduction, etcand to respond immediately – even interruptingoperations – to prevent or minimise possiblemachine damage.

The term sudden and unforeseen is essential todistinguish accidental loss or damage from wearand tear which is defined as a predictable operat-ing parameter within routine maintenance andservicing and therefore does not qualify as anindemnifiable event under machinery insurance.Some policy wordings introduce the term acci-dental and then set forth its scope of definition.

Policy forms, which rely solely on the termsudden and unforeseen loss or damage followed by a fairly long list of exclusions to define thecover, often led and still lead to questions ofwhat would actually be covered by the policy.This prompted insurers to list some of the pri-mary perils, eg on-the-job accidents relating tomaladjustment, loose parts, entry of foreignobjects, centrifugal force serrations, defective orfaulty design, material or manufacturing anderection faults, improper operation, lack of skill,carelessness, malicious intent of employees, etc.However, despite this listing of some of the cov-ered perils, the quasi all risk cover type is main-tained by supplementing the list with the follow-ing wording: any other accident not hereinafter

excluded.

4 Insured perils

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 10

11

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 11

12

5 General conditions

General policy conditions to be observed:• The insured shall ensure that all insured

machines and equipment are maintained ingood working order and that they are nothabitually or intentionally overloaded. Theinsured shall fully observe the manufacturers’instructions for operation, inspection andoverhaul as well as governmental, statutory,municipal and all other binding regulations inforce regarding the operation and maintenanceof the insured machines and equipment.

• Unless an endorsement is signed by theinsurer to ensure policy continuance, it will bevoid in the event of the following conditions:any material change in the original insureditem; alteration, modification or addition to an insured item; non-observance of specifiedoperating conditions resulting in increased riskof loss or damage, or changes in the insured’sstatus (such as business discontinuation andliquidation or receivership).

• The insured must immediately notify theinsurers of any occurrence which might giverise to a claim under the policy, and supply all required particulars and proof of claim.

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 12

13

6 Exclusions

The list of exclusions must be accurate and com-plete. Machinery insurance is intended to pro-vide so-called quasi all risk cover in conjunctionwith a standard fire and extended perils policy.To achieve this goal, exclusions listed in themachinery insurance must be co-ordinated withthe perils covered under the fire and extendedperils policy.

6.1 General exclusions

Apart from the more specific engineering exclu-sions dealt with subsequently, there are also so-called general exclusions, ie:• Damage arising from wilful acts, wilful negli-

gence by the insured or its management.• Nuclear risks: losses arising from ionising radi-

ation or radioactive contamination from anynuclear fuel, or from any nuclear waste fromthe combustion of nuclear fuel, as well aslosses caused by, contributed to, or arisingfrom nuclear weapons.

• Political risks such as war, civil war, civilcommotion, riots, etc.

• Consequential loss, damage or liability of any nature.

6.2 Standard fire and extended perils exclusions

The primary excluded perils are usually thosecovered by a standard fire and extended perilspolicy, eg fire, lightning, explosion, major perils,theft, burglary, etc.

The extent to which perils are covered undersuch policies varies from country to country.Machinery insurance often includes elementaryperils such as windstorm, frost (freezing), ice driftand ground settlement. However, the followingperils are always excluded: earthquake, seaquake,tsunami, rockfall, f lood, inundation, hurricane,typhoon, cyclone and volcanic eruption.

6.2.1 Distinction between fire insurance and machinery insurance

In fire insurance, fire is generally understood ashostile fire. Furnace heat damage is not regardedas fire damage. Damage due to glowing embersor heated objects not in f lame which scorch orburn holes without igniting a fire is not regardedas fire damage.

A friendly impellent fire is one which remainswithin a specific confinement area, eg thecombustion chamber of a furnace or a gasturbine. Essentially, fire is required to generateheat by means of combustible media (oil, gas orother fuel). Damage does not occur as long asthe combustion process remains under control.However, process irregularities may lead todamage such as local overheating in the combus-tion chamber. Such damage would be excludedfrom fire policies and falls within the scope ofthe machinery insurance. Any resulting firedamage, should it occur, would fall within thescope of the fire policy.

Loss or damage to machines and equipment is frequently caused by electrical phenomena. A short circuit can often result in fire and,conversely, a fire can cause a short circuit.

The fire policy excludes loss or damage tomachines, equipment, electrical conductorsresulting from the direct effect of electricalpower itself, eg overvoltage, surge voltages,increasing temperatures due to overloading as well as loss or damage to protective devices(safety gear, fuses, etc) occurring during thenormal operation of such devices.

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 13

14

Loss or damage due to lightning, however, iscovered within the scope of the fire policy. Insome countries, machinery policies also coverfire losses of electrical equipment arising fromsudden and unforeseen electrical phenomena inthe equipment itself. Any resulting fire, loss or damage to other machines or equipment,however, falls within the scope of the fire policy.Loss or damage caused by explosion is coveredby the fire policy.

Explosion is understood as an instantaneous manifes-tation of fire, triggered by expanding gases or vapours.With respect to pressure vessels (eg steam boilers,cylinders, or vessels for vapour, gas or liquid, or boilingunits, steam pipes), explosion damage is deemed tohave occurred only if the walls of the receptacle aredamaged to such extent that the pressures inside andoutside the receptacle are instantaneously equalised.

In fire insurance, however, explosion peril doesnot include distortion, whether or not accom-panied by the rupture of any part of the pressureplant caused by crushing stress through forcesrelated to steam or other f luid pressure (apartfrom the pressure associated with ignited f luegases). Furthermore, it does not encompass the destruction of rotating machines caused bycentrifugal forces nor loss or damage caused by implosion (instantaneous deformation of avacuum receptacle caused by external overpres-sure). Consequently, this loss or damage is notconsidered to be an explosion in the sense of fire insurance and thus falls within the scope of the machinery insurance.

Machinery insurance also provides cover for loss or damage in the case of sudden and violentbursting of pressure plants by internal steamforce or other f luid pressure (except pressure ofchemical action or of f lue gas ignition) causingstructural physical displacement of any part ofthe pressure plant together with forcible ejectionof its contents. Damage caused by fire precedingor following such events, however, is excludedfrom machinery cover.

6.3 Machinery-specific exclusions

The following four exclusions are typical to machinery insurance:

The events listed above often give rise to claimsdisputes, particularly regarding the exposuredefined as corrosion.

Modern science classifies the various types of corrosion as follows:

A Corrosion in the absence of mechanical stresses:Uniform corrosionShallow pit formationPitting corrosionCrevice corrosionGalvanic corrosionCorrosion by differential aerationDeposit attackSelective corrosion– Intergranular– TransgranularDew point corrosionCorrosion by condensed waterIdle corrosionMicrobiological corrosionScaling (high temperature oxidation)Accelerated oxidationSubsurface corrosion

B Corrosion types under additional mechanical stresses:Stress corrosion cracking (SCC)*Corrosion fatigue (low cycle corrosion fatigue)Strain-induced corrosionCorrosion – erosionCavitation corrosionFretting corrosion

*SCC is defined as the failure of metals under thecombined effect of tensile stress and a corrosiveenvironment.

1. Foreseeable events, eg consequences of normaloperation, any continual mechanical, thermal,chemical or electrical effects, wear and tear, corro-sion, erosion, undue deposits, mud, boiler scale, etc.

6 Exclusions

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 14

15

Loss or damage caused by any of these corrosiontypes has the following common characteristics: – Develops gradually– Results in machines and equipment from

ongoing exposure (operation and standstill) – Can be detected through modern materials

testing methods and is therefore not under-stood as sudden and unforeseen.

The interpretation as to what degree of loss ordamage caused by the above-mentioned foresee-able events is indemnifiable varies considerablyfrom country to country.

– Short-term overstressing cannot be avoidedwhile inspecting the operational integrity ofsafety gear under excessive conditions whichmay occur during any operational phase.However, the following events are expresslycovered:– Disconnecting a turboset under full load

conditions;– Short-circuit testing of a transformer; and – Emergency brake testing for a cableway.

– The testing exclusion rules out experimentssuch as setting the minimum pressure or loadon a boiler safety valve in excess of the designvalue or increasing the trip rate of an over-speed guard, etc.

3. Breakdown caused by testing or experiments in which normal operating stresses are willinglyexceeded.

2. Any faults or defects existing at the time of policyinception which were known or should have beenknown to the insured or its management.

– This exclusion does not, however, apply to theextent that manufacturers, suppliers, contrac-tors or other parties are unable to dischargetheir liability, and the insured is able to pro-vide evidence of this fact.

Furthermore, this exclusion applies only dur-ing the manufacturer’s warranty period whichis usually between 12 and 24 months after theservice period commences. Notwithstandingthe material damage, business interruptioncover, if provided, would be triggered despitethis exclusion.

4. Machinery insurance does not cover loss or dam-age for which manufacturers, suppliers or othersare liable by law or under contractual obligations.

Machinery insurance_e 03.11.2000 8:14 Uhr Seite 15

16

Machinery insurance_e 03.11.2000 8:15 Uhr Seite 16

17

7 Sum insured

The sum insured (SI) is an amount mutuallyagreed upon between insurer and insured andserves as the basis for determining specific obli-gations, described in greater detail in the insur-ance policies. The sum insured is a policyparameter used to establish the indemnifiableamount in case of loss and to calculate thepremium for the insured risk.

With respect to material damage covers such asfire insurance and machinery insurance, it iscustomary to gear the sum insured to the totalvalue of the insured property.

The sums insured for various lines of businesscan be classified as follows:

For some policies (particularly in the US or US-dominated markets), the sum insured is oftenreplaced by an indemnity limit per loss event.

Line of business SI

Property (material New Replacement Value damage) (NRV)Business interruption Gross profit/additional costSpecial covers First loss amount

Machinery insurance_e 03.11.2000 8:15 Uhr Seite 17

18

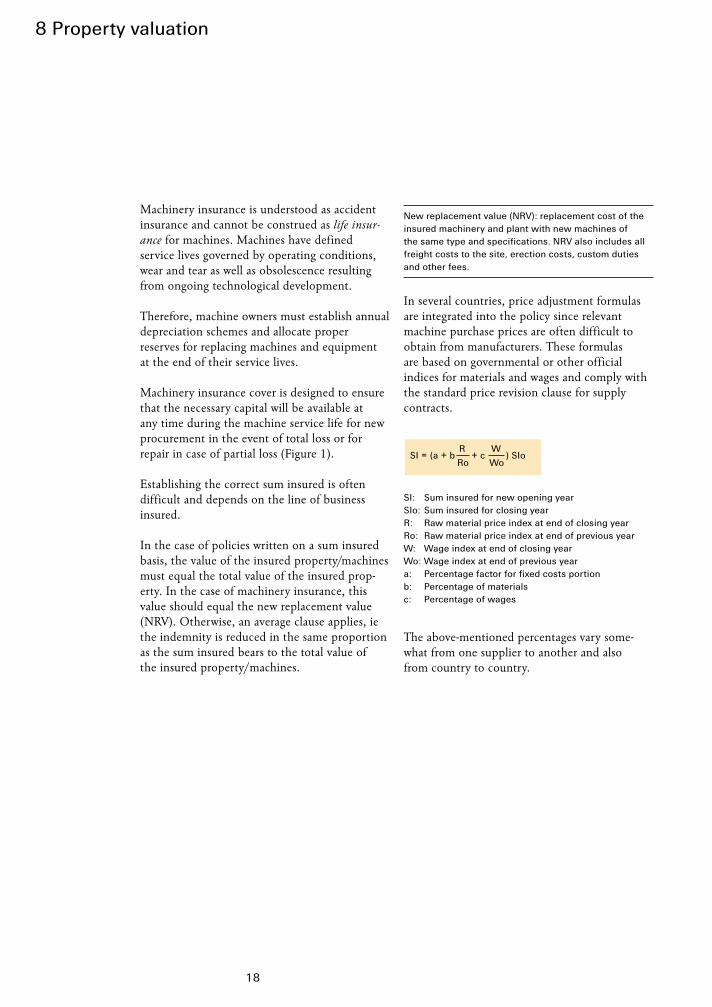

8 Property valuation

Machinery insurance is understood as accidentinsurance and cannot be construed as life insur-

ance for machines. Machines have definedservice lives governed by operating conditions,wear and tear as well as obsolescence resultingfrom ongoing technological development.

Therefore, machine owners must establish annualdepreciation schemes and allocate properreserves for replacing machines and equipmentat the end of their service lives.

Machinery insurance cover is designed to ensurethat the necessary capital will be available at any time during the machine service life for newprocurement in the event of total loss or forrepair in case of partial loss (Figure 1).

Establishing the correct sum insured is oftendifficult and depends on the line of businessinsured.

In the case of policies written on a sum insuredbasis, the value of the insured property/machinesmust equal the total value of the insured prop-erty. In the case of machinery insurance, thisvalue should equal the new replacement value(NRV). Otherwise, an average clause applies, iethe indemnity is reduced in the same proportionas the sum insured bears to the total value of the insured property/machines.

New replacement value (NRV): replacement cost of theinsured machinery and plant with new machines of the same type and specifications. NRV also includes allfreight costs to the site, erection costs, custom dutiesand other fees.

In several countries, price adjustment formulasare integrated into the policy since relevantmachine purchase prices are often difficult toobtain from manufacturers. These formulas are based on governmental or other officialindices for materials and wages and comply with the standard price revision clause for supplycontracts.

SI: Sum insured for new opening yearSIo: Sum insured for closing yearR: Raw material price index at end of closing yearRo: Raw material price index at end of previous yearW: Wage index at end of closing yearWo: Wage index at end of previous yeara: Percentage factor for fixed costs portionb: Percentage of materialsc: Percentage of wages

The above-mentioned percentages vary some-what from one supplier to another and also from country to country.

R WSI = (a + b + c ) SIo

Ro Wo

Machinery insurance_e 03.11.2000 8:15 Uhr Seite 18

19

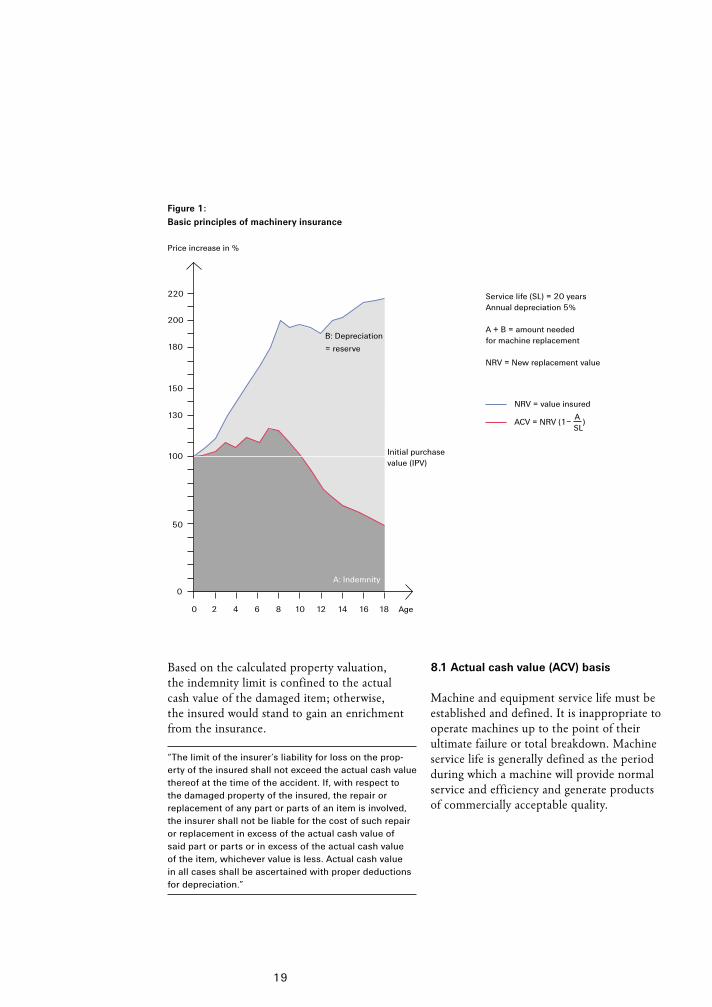

Based on the calculated property valuation, the indemnity limit is confined to the actual cash value of the damaged item; otherwise, the insured would stand to gain an enrichment from the insurance.

“The limit of the insurer’s liability for loss on the prop-erty of the insured shall not exceed the actual cash valuethereof at the time of the accident. If, with respect to the damaged property of the insured, the repair orreplacement of any part or parts of an item is involved,the insurer shall not be liable for the cost of such repairor replacement in excess of the actual cash value of said part or parts or in excess of the actual cash value of the item, whichever value is less. Actual cash value in all cases shall be ascertained with proper deductionsfor depreciation.”

8.1 Actual cash value (ACV) basis

Machine and equipment service life must beestablished and defined. It is inappropriate tooperate machines up to the point of theirultimate failure or total breakdown. Machineservice life is generally defined as the periodduring which a machine will provide normalservice and efficiency and generate products of commercially acceptable quality.

Figure 1: Basic principles of machinery insurance

200

180

150

130

100

50

Age

Price increase in %

0 2 4 6 8 10 12 14 16 18

0

220

B: Depreciation

= reserve

A: Indemnity

Service life (SL) = 20 yearsAnnual depreciation 5%

A + B = amount neededfor machine replacement

NRV = New replacement value

Initial purchasevalue (IPV)

NRV = value insured

ACV = NRV (1– A

)

SL

Machinery insurance_e 03.11.2000 8:15 Uhr Seite 19

20

8 Property valuation

Machine availability is a key factor for determin-ing its degree of economic efficiency. For thisreason, overhauls are performed at predeter-mined intervals to replace critical componentsand effectively prevent unplanned downtime.Useful service life is based on the followingcriteria: experience with similar machines, oper-ating history, non-destructive tests on parts andcomponents, theoretical service life calculation,long-term materials behaviour.

The outcome of these studies is summarised and forms the basis for manufacturers’ recom-mendations regarding parts replacement atspecified intervals during a given operatingperiod.

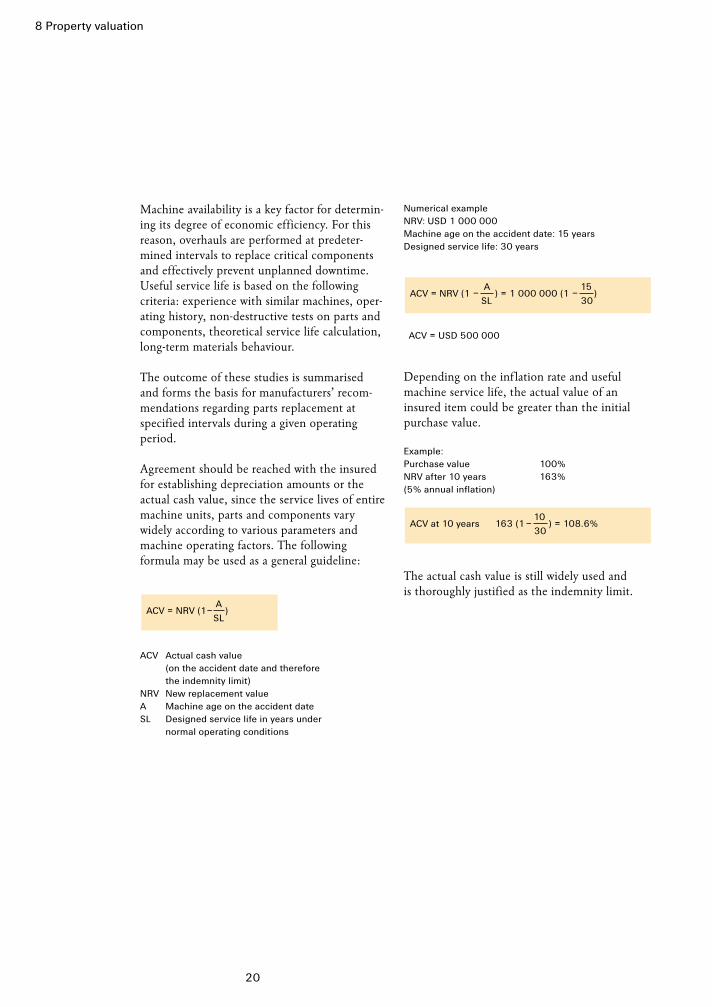

Agreement should be reached with the insuredfor establishing depreciation amounts or theactual cash value, since the service lives of entiremachine units, parts and components varywidely according to various parameters andmachine operating factors. The followingformula may be used as a general guideline:

ACV Actual cash value(on the accident date and therefore the indemnity limit)

NRV New replacement valueA Machine age on the accident date SL Designed service life in years under

normal operating conditions

AACV = NRV (1– )

SL

Numerical exampleNRV: USD 1 000 000Machine age on the accident date: 15 yearsDesigned service life: 30 years

ACV = USD 500 000

Depending on the inf lation rate and usefulmachine service life, the actual value of aninsured item could be greater than the initialpurchase value.

Example:Purchase value 100%NRV after 10 years 163%(5% annual inflation)

The actual cash value is still widely used and is thoroughly justified as the indemnity limit.

10 ACV at 10 years 163 (1– ) = 108.6%

30

A 15 ACV = NRV (1 – ) = 1 000 000 (1 – )

SL 30

Machinery insurance_e 03.11.2000 8:15 Uhr Seite 20

21

8.2 Repair or replacement basis

For many years, US insurers offered a repair or replacement cover, subject to additionalpremium, as an option to the actual cash valuebasis. In the US market, it is now known as thestandard cover and is erroneously often referredto as new for old. The insurer agrees that materialdamage (of the insured) as specified in the policyis understood as the amount actually paid by theinsured to repair or replace the property insured,subject to the following provisions:

“The damaged property shall be repaired or replacedwithin twelve months from the accident date unlesssuch period is extended by written consent of theinsurer.

The insurer’s liability for any repair or replacement shallbe limited to the smaller of the following: (1) the cost at the time of the accident to repair said property, or (2)the cost at the time of the accident to replace said prop-erty on the same site with property of like kind, capacity,size and quality; provided that if replacement is in theform of property of an improved kind or quality or oflarger capacity or size, the liability of the insurer shallnot exceed the amount that would be paid if the replace-ment had been made by property of like kind, capacity,size and quality.

The insurer shall not be liable for (1) any increase in the cost of repair or replacement necessitated by anyordinance or law regulating or restricting repair, con-struction or installation, (2) loss or damage to propertyobsolete to the insured, or (3) the cost of repairing orreplacing any part or parts of an item which is in excessof the cost of repairing or replacing the entire item.

If any damaged property is not repaired or replaced, theinsurer’s liability regarding such property shall be limitedto the actual cash value.”

The repair or replacement cover arose primarilydue to the second-hand machine market in the USA, which offers a wide spectrum of usedmachines and equipment. Since most claims arepartial losses, repair can be made at costs belowthe actual cash value.

The trend of including machinery insurance inProperty All Risk covers resulted in the repair or replacement basis gaining momentum in theinternational market.

Second-hand machine markets are virtually non-existent outside the US, and this form of covermay result in insurers having to pay for newmachines or equipment. This in turn leads to theexpression new for old which is not the intentionof this cover type.

8.3 Comparing valuation methods

The primary difference between the actual cashvalue basis and the repair or replacement basiscan be summarised as follows:

Machinery insurance_e 03.11.2000 8:15 Uhr Seite 21

22

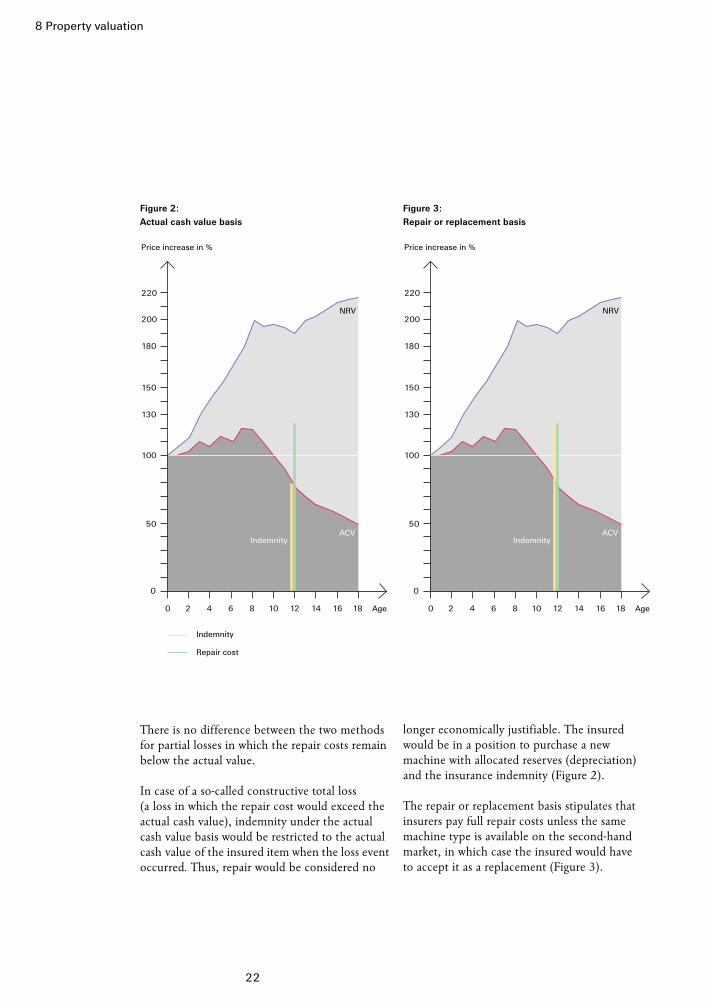

There is no difference between the two methodsfor partial losses in which the repair costs remainbelow the actual value.

In case of a so-called constructive total loss (a loss in which the repair cost would exceed theactual cash value), indemnity under the actualcash value basis would be restricted to the actualcash value of the insured item when the loss eventoccurred. Thus, repair would be considered no

200

180

150

130

100

50

Age

Price increase in %

0 2 4 6 8 10 12 14 16 18

0

220

NRV

ACV

Indemnity

Repair cost

Indemnity

longer economically justifiable. The insuredwould be in a position to purchase a newmachine with allocated reserves (depreciation)and the insurance indemnity (Figure 2).

The repair or replacement basis stipulates thatinsurers pay full repair costs unless the samemachine type is available on the second-handmarket, in which case the insured would have to accept it as a replacement (Figure 3).

200

180

150

130

100

50

Age

Price increase in %

0 2 4 6 8 10 12 14 16 18

0

220

NRV

ACVIndemnity

8 Property valuation

Figure 2:Actual cash value basis

Figure 3:Repair or replacement basis

Machinery insurance_e 03.11.2000 8:15 Uhr Seite 22

23

Machinery insurance_e 03.11.2000 8:15 Uhr Seite 23

24

The risk premium for an insured item (Rp) is afunction of loss frequency (q) in a given (annual)period, the claims amount (c) plus a surcharge(z) to compensate for specific perils and adminis-trative costs.

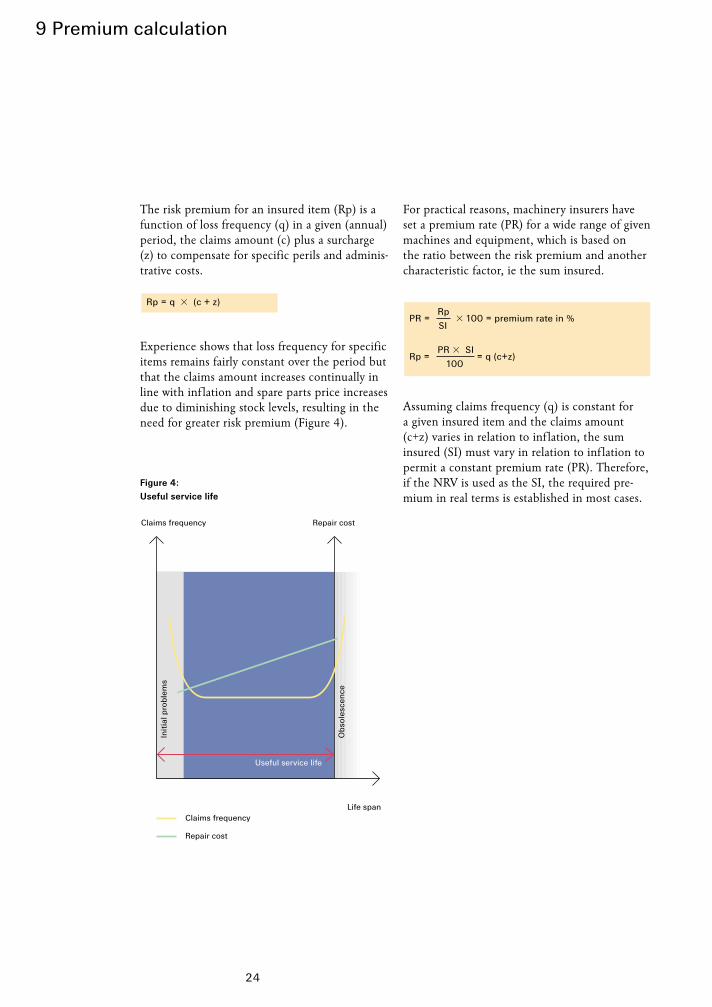

Experience shows that loss frequency for specificitems remains fairly constant over the period butthat the claims amount increases continually inline with inf lation and spare parts price increasesdue to diminishing stock levels, resulting in theneed for greater risk premium (Figure 4).

Figure 4:Useful service life

Claims frequency

Repair cost

Useful service life

Claims frequency

Init

ial p

robl

ems

Obs

oles

cenc

e

Repair cost

Life span

Rp = q � (c + z)

For practical reasons, machinery insurers have set a premium rate (PR) for a wide range of givenmachines and equipment, which is based on the ratio between the risk premium and anothercharacteristic factor, ie the sum insured.

Assuming claims frequency (q) is constant for a given insured item and the claims amount(c+z) varies in relation to inf lation, the suminsured (SI) must vary in relation to inf lation topermit a constant premium rate (PR). Therefore,if the NRV is used as the SI, the required pre-mium in real terms is established in most cases.

Rp PR = � 100 = premium rate in %

SI

PR � SI Rp = = q (c+z)

100

9 Premium calculation

Machinery insurance_e 03.11.2000 8:15 Uhr Seite 24

25

The deductible is an amount carried by theinsured and mutually agreed upon with theinsurers.

Normally, only those losses above a certainamount, and not the first dollar, are covered to maintain the insurance premium at an eco-nomically justifiable level. The insurancecommunity has an interest in ensuring that allmembers keep the loss burden as low as possible.Hence, the policy will not indemnify loss ordamage resulting from an insured event (any oneaccident) until the amount of loss or damageexceeds the deductible and then the policy willpay only the amount of loss or damage exceed-ing the deductible (excess).

The amount of the excess depends on variousparameters, eg type, size and complexity of the machines and equipment, manufacturers’experience, financial strength of the insured, etc.

Insurers will set the minimum deductible basedon technical parameters, and the insured canthen select a higher deductible if desirable,subject to his financial strength and inclinationfor risk. Obviously, the final premium will be adjusted to ref lect the level of the selecteddeductible.

10 Deductible (Excess)

Machinery insurance_e 03.11.2000 8:15 Uhr Seite 25

26

While there is a current trend in many industri-alised countries to waive requirements for com-pulsory inspections required for plant opera-tions, onsite engineering inspection remains akey factor in machinery insurance. Inspectionsare designed principally to safeguard human life and prevent accidents which could have been either mitigated or precluded throughengineering experience and expertise. Further-more, federal and local regulations in manycountries stipulate that operating authorisationfor certain machines and equipment is contin-gent upon inspections, eg boilers and pressurevessels.

These mandatory inspections are performedeither by government agencies or by inspectorsfrom insurance companies licensed by therelevant authorities.

In addition to the assurance offered by regularinspections of boilers and pressure vessels, insur-ers also rely on the feedback from scheduled,governmental inspections of all machines andequipment as a key information source forassessment and pricing of risk.

Detailed information on the following topics is of particular interest to insurers:

Physical condition of the machines and equipment It is best to inspect the physical condition of a machine when dismantled during major over-hauls. Several sophisticated non-destructivediagnostic tests have been developed which alsopermit testing of functional integrity duringmachine operation.

Loss-related problems associated with older machines In this case, the insurer should ascertain that the specific machine type and all required spare parts are still being manufactured prior to granting any cover.

Unconventional features Industry’s ongoing investment in new andunconventional products has led to the use ofmany special purpose machines with unconven-tional features. The risks inherent in operatingsuch equipment warrant prudent evaluation.

Plant configuration All technical machines and equipment in a givenfacility must be overhauled according to speci-fied maintenance schedules. Some type of dam-age often occurs during overhauls, even if allnecessary precautions are observed. Wheneverpossible, inspection of critical components ofmachines and equipment should be performedwithout total disassembly.

If these aspects are not observed, the insurerwould have to increase the premium accordinglyby applying risk aggravating factors.

11 Risk inspection

Machinery insurance_e 03.11.2000 8:15 Uhr Seite 26

27

Loss history The insurer should obtain a copy of the losshistory of the machines and equipment to becovered. A detailed list must cite all majordamage, repairs and modifications during com-missioning, testing and operation. These factorsshould be ref lected in the premium level andmay even raise the question of the basic insura-bility of the machines.

Maintenance Proper and ongoing maintenance is vital for damage prevention.

Repair costs can be reduced by implementingthe manufacturer’s preventive maintenance plansince components would normally be replacedbefore damage occurs. This implies that spareparts inventories can be planned on the basis of the most frequent malfunctions incurred.

Diagnostic checks are employed to obtain anearly warning for repair needs. They can beperformed during normal operation of machinesand equipment or during scheduled and briefshutdowns.

Many diagnostic checks can be made by meansof permanently installed control instruments.Extended range inspection and test equipmentpermits more precise detection of defects andabnormal conditions. For example:

• Infrared imaging for determining local hotspots in transformers and furnaces

• Oil spectrography for analysing the presenceof metal particles in oil

• X-ray inspection of welds• Ultrasonic inspection for detecting f laws

and cracks in shafts and machine casings• Endoscopic inspection of turbine blades• Vibration monitoring, etc.

Machinery insurance_e 03.11.2000 8:15 Uhr Seite 27

Machinery insurance_e 03.11.2000 8:16 Uhr Seite 28

29

12 Clauses/cover extensions

It is often advisable and/or necessary to supple-ment the standard policy form with conditionsspecific to the risk or the machines and equip-ment to be insured. Numerous clauses havealready been drafted and new ones are continu-ally being developed. They are designed tospecify a particular hazard, or to cite acceptanceof technical specifications and regulations orexclusions or cover extensions.

Some of the most frequent clauses are citedbelow:

Pressure plant explosionIn addition to indemnifying the damage to thepressure plant resulting from its own explosion,cover is extended to indemnify damage as adirect result of explosion to the adjacent prop-erty which belongs to the insured or is in theinsured’s custody or control.

In this context, explosion is defined as the sud-den and violent bursting of a pressure plant(boiler, pressure vessel, etc) by the force of inter-nal steam or other f luid pressure (other than thepressure of ignited f lue gases), resulting in thephysical destruction of any part in conjunctionwith the forcible ejection of its contents. Thisadditional cover is subject to a liability limit andpremium supplement.

Restricted service lifeThe indemnity provided for components subjectto high and rapid wear and exhibiting limitedservice life is restricted to the value of suchcomponents at the time of the indemnifiableoccurrence, taking into account the length oftheir service lives.

Adjacent propertyAdjacent property is normally not insurableunder the machinery insurance policy. However,for consequential damage arising from an insuredevent, cover up to an aggregate indemnity limitmay be granted against an additional premium.

Debris removalDebris removal costs are covered under themachinery insurance policy and are included inthe total repair costs in the event of an indem-nifiable claim. If experience shows that thesecosts are very high for particular machines orequipment, an indemnity limit should be stipu-lated by special endorsement.

Expediting expensesExpediting costs, comprising extra charges forovertime, nightwork, work on public holidaysand express freight (excluding air freight), may be covered by endorsement and subject to additional premium.

Machinery insurance_e 03.11.2000 8:16 Uhr Seite 29

12 Clauses/cover extensions

30

Machine foundations Machine foundations and other civil engineeringworks or structural elements of a building repre-senting an integral part of an insured machinemay be included in the policy by an endorse-ment to cover damage costs as well as other addi-tional costs required for gaining access to repairthe machine. These items and their new replace-ment values must be listed separately in theendorsement. This extension is subject to addi-tional premium.

Machines and equipment used in subterranean applicationsIt is advisable to include a clause waiving theinsurer’s liability for insured machines andequipment used in subterranean applications for which loss or damage could result from gasexplosions, water ingress, liquefied sand and clay or the collapse of tunnels, shafts and/ortheir support structures.

Air freightAir freight charges may be covered if necessitatedto expedite repairs of an insured item. The pre-mium is calculated on an aggregate indemnitylimit also taking into account the type and loca-tion of the plant and distances from suppliers.

Various job locationsA situation of aggravated risk exists if machinesand equipment are used at various premises andsites. The premium must therefore be increasedand special clauses applied to satisfy this coverrequirement.

Water damageCover may be extended to include water damageonly if it is caused by the breakdown of aninsured item (eg fractured penstocks, valves orturbine casings, etc). Furthermore, this categoryof loss excludes water damage or any otherdamage caused by natural hazards (except wind-storm). This extension is subject to additionalpremium.

Machinery insurance_e 03.11.2000 8:16 Uhr Seite 30

31

Thus far, discussion has focused on insurancewhich indemnifies loss or damage to tangibleproperty (machines and equipment) resultingdirectly from a loss event. In the majority of acci-dents involving boilers and machines, loss is notlimited to the costs of repairing or replacing theproperty damaged or destroyed. Financial lossmay be substantially greater than the loss to the actual machines and equipment in the caseof goods which could not be produced or sold, the spoilage of goods due to inadequate power,heat or refrigeration, or increased operatingexpenses incurred by the use of alternative pro-duction methods.

Indirect damage insurance is not addressed inthis brochure. Since it complements machineryinsurance – either in the form of a separatepolicy or as an endorsement to the relevantmachinery insurance policy – only its mainfeatures will be highlighted. The most frequentlyrequested indirect damage covers are:

Business interruption (BI) Investments in machines and equipment aredesigned solely with the intention of generatingprofit. Business interruption insurance coversfinancial loss resulting from total or partialbusiness downtime caused by the damage ordestruction of insured machines and equipment.For the most part, this insurance is designed to cover net profits, fixed expenses and lossminimisation costs. The cover indemnifies grossprofit (net profit plus fixed expenses) that could have been earned had the loss event notoccurred.

Extra expense insuranceThis insurance covers extra expenses incurred bythe insured to continue his business withoutinterruption while the damage from an insuredloss event is being remedied. It represents a spe-cial form of business interruption cover specifi-cally adapted to service-oriented operationswhich must continue on a daily basis, eg dairies,utilities, newspaper printers, etc.

Payments continue as long as the insured itemsare inoperable, resulting in additional expensesover and above those which would have beeninsured had the accident not occurred.

This cover can be granted only in cases whereother immediate facilities and/or other means are available to the insured to permit operationto continue.

Consequential damage insuranceThis insurance covers the indirect loss of perish-able goods spoiled as a result of insufficientpower, light, heat, steam or refrigeration andarising solely from damage to the insuredmachines and equipment.

This cover is required mostly by businesses with the following exposures:– Production processes requiring heat, steam

or refrigeration, eg pharmaceutics, synthetics,processed foods, malt beverages, greenhouses,dairies, etc.

– Production processes dependent upon contin-uous uninterrupted power to avert productdamage, eg synthetic fibres, plastics, smelting,etc.

– Perishable products in cold storage dependenton refrigeration, eg fish, meat, vegetables,frozen foods, etc.

Consequential damage insurance usually coversdamage to the insured’s goods and those whichothers have entrusted to his care and custody.This feature is important to owners of cold storeswhere space is leased to third parties for perish-able goods storage. The indemnity is limited to the actual cash value of the damaged goods.Perishable property subject to spoilage must be specified.

13 Indirect damage insurance

Machinery insurance_e 03.11.2000 8:16 Uhr Seite 31

32

14 Rating

Statistics reveal that losses differ widely in termsof frequency and severity from one industrialbranch to another since perils are determinedlargely by the type of industry and the relevantoperating environment. For example, a steamturboset of the same type and output rating isexposed to far less adverse conditions wheninstalled inside a power generating facility of a public utility than when located in an open-airoil refinery. The nature of these different para-meters has resulted in various risk categories for numerous types of industries, and Swiss Re’sMachinery Breakdown rating guide covers acomprehensive range of industrial groups.

The industrial groups as defined are furthersubdivided into categories of major machinesaccording to different types and output ratings.Other equipment and components are listed as miscellaneous.

The breakdown of rates according to differentmachine and equipment categories necessitatesitemised values at least in the case of largermachine and equipment installations. The moredetailed the itemised values submitted by thepolicyholder, the more accurate the assessmentand rating. This applies particularly to largefactories with a diversity of machines and equip-ment.

Swiss Re has extensive documentation on ratelevels used in many industrialised countries andcan therefore provide relevant rating guides.However, the rates and deductibles (excesses)indicated in such a rating guide are valid only for machines and equipment operating undermoderate exposure, which can be described asfollows:• Plant management and technical staff should

be experienced and well qualified to operatesuch machines and equipment;

• Safety measures, maintenance and lossprevention should be commensurate withmodern standards;

• Machines and equipment must havesuccessfully passed reliability tests in similarinstallations, ie they may not be prototypes;

• The plant should be up to date and notobsolete;

• The political, social and economic environ-ment should be stable.

Rate structures should be adjusted accordingly if these exposure factors are not met. In theworst case, machines and equipment would haveto be declared uninsurable.

The rating guide contains detailed instructionsfor adjusting the premium to ref lect variousfactors which alleviate or aggravate risk.

Machinery insurance_e 03.11.2000 8:16 Uhr Seite 32

Machinery insurance_e 03.11.2000 8:16 Uhr Seite 33

34

15 Claims handling

Any loss event implies impairment for the in-sured and the threat of his economic resources in addition to various attendant problems.Machinery insurance is designed to relieve thepolicyholder of this burden, but the insurancedoes not cover every type of loss event. Aprocedure for establishing prompt proof of the insurer’s liability as well as competent andprofessional handling of claims are vital for both contractual parties.

Policyholder obligationsThe policyholder must proceed as follows in caseof a loss event:• The insurer must be informed as soon as prac-

tically possible.

• The insurer must also be informed in writingabout the possible accident cause, estimatedloss amount, etc. The key points must be cov-ered in the initial loss event report.

• Information must be submitted to substantiatethe claim.

• All efforts must be made during and immedi-ately after the loss event to safeguard theinsured property from further damage. Anyand all instructions from the insurer must be observed.

• The damaged insured items must not be modi-fied in any way which would make it moredifficult or even impossible to determine thecause of the damage. Modification is permissi-ble if it will reduce the loss or is required bypublic authorities.

• Damage repair may begin immediately if vitalfor further plant operation and provided theloss survey is not adversely affected.

• The insurer will not be liable for loss or dam-age unless notice is received within the agreedtime frame stated in the policy.

Loss surveyThe insured or the insurer may demand that a loss survey be conducted immediately. Theinsured must prove the indemnity amount. The loss survey may be conducted either by the insured, insurer or by an independent loss adjuster.

Checklist for proving coverage in the event of loss or damage:• Does the plant schedule specify the damaged

item and sum insured?• Did the damage occur within the policy

period?• Did damage arise from defects existing at

policy inception? – Policies will generally not indemnify those

defects known to the insured but notreported to the insurer. The burden of proofrests in establishing that such defects existedbefore policy inception and that they werethe primary cause of any resultant damage.

• Has the premium been paid?• Was the claim reported to the insurer within

the specified time limit?• Is the loss or damage covered by the policy?• How did the loss occur? What were the causes?

Does the damage comply with the criterionsudden and unforeseen?

• What was actually damaged?• Did the loss occur inside or outside the

insured premises?• Did the insured breech certain specifications

or regulations?

Machinery insurance_e 03.11.2000 8:16 Uhr Seite 34

35

Indemnity calculation and loss settlement Unless otherwise agreed, the maximum indem-nifiable amount is either the actual cash value ofthe damaged item or the indemnity limit per lossevent. Generally, a distinction is made betweenpartial losses (PL) and total or constructive totallosses (CTL).

Partial losses are the most frequent type of dam-age. A partial loss results if repair costs (RC) forthe damaged item are less than the actual cashvalue (ACV).

Repair costs are less than the actual cash value (partial loss) (Figure 5).• The indemnifiable amount for these losses

is the same, irrespective of the cover basis, ie the actual cash value basis (A) or repair or replacement basis (B).

• The indemnifiable repair costs are thoserequired to restore machines and equipment to their state immediately prior to the lossevent. Costs are also covered for dismantlingand re-erection, spare parts, transportationand customs duties.

Repair costs are equal to or greater than theactual cash value (constructive total loss) (Figure 6). • A total loss arises if an insured item is so

severely damaged that it can no longer berepaired. A constructive total loss (CTL) ariseswhen the repair costs are equal to or greaterthan the actual cash value of the damageditem.

• The maximum indemnifiable amount deter-mined for the total or constructive total loss is one of the following, depending on the basis on which the policy had been concluded: – actual cash value of the damaged item; – the cost incurred to restore it to the state

immediately prior to the loss event; or – the cost to replace it with a machine similar

in type, capacity, size.

Regardless of whether or not the policy wasconcluded on the repair or replacement basis,the insured is not entitled de facto to a newmachine in case of a constructive total loss. The insurer’s liability is restricted either to the full repair costs, the replacement cost of a second-hand machine (if available) or a newmachine replacement, whichever is less.

Under-insurance (actual cash value basis)The term under-insurance applies if the suminsured of an item is lower than its new replace-ment value. If under-insurance is determined in a loss settlement, full indemnity will not bepaid. Indemnification may be calculated usingthe following formula:

I: IndemnitySI: Sum InsuredNRV: New replacement valueRC: Repair costsD: Deductible

I = ( SI/NRV � RC) – D

Machinery insurance_e 03.11.2000 8:16 Uhr Seite 35

200

180

150

130

100

50

Age

Value in % of IPV

0 2 4 6 8 10 12 14 16 18

0

220

NRV

ACVIndemnity

Indemnity on actual value basis (A)

Repair cost

Indemnity on repair replacement basis (B)

200

180

150

130

100

50

Age

Value in % of IPV

0 2 4 6 8 10 12 14 16 18

0

220

NRV

ACVIndemnity

36

15 Claims handling

Figure 5:Partial loss

Figure 6:Total or constructive total loss

Machinery insurance_e 03.11.2000 8:16 Uhr Seite 36

37

16 Outlook

Monoline machinery cover traditionally under-written by professional engineering insurers iscurrently on the decline. It is generally felt thatthis insurance will be gradually superseded bymultiline covers such as Industrial All Risk or

Property All Risk.

However, the integration of machinery insurancein other insurance forms is not a recent develop-ment. Policyholders have traditionally sought all-inclusive covers for protection against propertyimpairment, irrespective of its cause.

The insured’s primary motives and justificationfor All Risk cover include:• Clear formulation of the policy terms, condi-

tions and restrictive claims adjustment period; • Prevention of cover overlap between different

insurance lines and associated price benefit; • Avoiding coverage gaps: comprehensive insur-

ance cover is offered as a so-called “sleep-easypackage”.

For many years, all-inclusive policies have beenavailable in various countries and incorporatemany individual lines. Such integrated policieshave traditionally comprised an aggregate ofindividual and easily identifiable monolines, with machinery insurance as a component ofsuch integrated packages. Its identification as a distinct monoline has made it possible todefine specific terms and conditions, to acquirestatistics for each line, to provide appropriatetechnical services and to maintain the image of machinery insurance as a special line.

A truly comprehensive blanket all risk cover,however, is not technically justifiable. It isimpossible to assess all known and unknownrisks, and hence such policies would be bur-dened by extensive conditions and exclusions.Conversely, all risk policies with inadequateterms, conditions and exclusions will lead tonumerous losses and ultimately have an adverseeffect on the insurance industry as a whole, which is not in the long-term interests of theinsured parties.

Property All Risk covers are well established andadvantageous for certain industries. While corpo-rate risk managers are potential clients for prop-erty covers, they are also key clients of monolinemachinery insurers. Sophisticated insurancebuyers are also interested in issues beyond thescope of insurance cover and therefore rely onthe special expertise of machinery insurers forfurther developing their safety management programs. Although the concept of Property All

Risk covers may pose a challenge to traditionalmachinery insurers, their expertise will berequired, regardless of whether the policy is aproperty all risk or monoline type.

Many engineering insurers include technical ser-vice as an integrated part of their proposals. Insome markets, legally compulsory inspections areconducted by machinery insurers as a service.Machinery insurers also conduct other loss pre-vention inspections which are normally an inte-grated part in the insurance coverage.

In conclusion, it can be stated that the in-depthand comprehensive technical expertise gained by machinery insurers in this particular field will continue to benefit both clients and theinsurance industry at large.

Machinery insurance_e 03.11.2000 8:16 Uhr Seite 37

38

Actual cash value (ACV) 19

Blanket groups 8Boiler explosion 7Breakdown 7Business interruption (BI) 7

Comprehensive form 8Consequential loss covers 7Constructive total loss (CTL) 35Contractor’s all risks (CAR) 7Contractor’s plant 7Corrosion 14

Delay in start-up 7Deterioration of stock (DOS) 7

Engineering insurance 7Erection all risks (EAR) 7Explosion 14Extra expenses 7

Force majeure (FM) 7

Individual listing 8

Liquidated damage (LD) 7Low voltage & electronic equipment 7

Material damage cover 7

New for old 21New replacement value (NRV) 18

Partial loss 35Pressure plant explosion 29Provisional acceptance certificate (PAC) 8

Ready for use 8Repair or replacement basis 21

Service life 20Sudden and unforeseen/accidental 10

Under-insurance 35

Appendix: Index of terms

Machinery insurance_e 03.11.2000 8:16 Uhr Seite 38

Machinery insurance_e 03.11.2000 8:17 Uhr Seite 39

© 2000Swiss Reinsurance CompanyZurich

Title: Machinery insurance

Author:Max BommeliRE, Reinsurance & Risk division

Published by: Swiss Re Publishing

Editing and production:RK, Corporate CommunicationsReinsurance & Risk division

Graphic design:Galizinski Gestaltung, Zurich

Illustrations:Galizinski Gestaltung, Zurichin cooperation with Meier+Pfister Fotolitho AG, Effretikon

Additional copies and a brochure listing other Swiss Re publications (Swiss Re Publishing–Our expertise for your benefit) can be ordered from:

Swiss Re Mythenquai 50/60P.O. Box CH-8022 ZurichTelephone +411285 21 21Fax +411285 20 23E-mail [email protected]

Swiss Re publications can also be downloaded from our Websitewww.swissre.com

Order no.: 202_00247_en

RR, 10/00, 3000 en

Max Bommeli, dipl. Masch. Ing. HTL,is a retired member of Swiss Re’ssenior management. He joined Swiss Re in 1971. Following initialreinsurance training he worked asunderwriter in the Engineeringdepartment. He has vast experiencein underwriting in all classes ofengineering insurance.

Machinery insurance_e 03.11.2000 8:17 Uhr Seite 40