Embed Size (px)

Citation preview

University of Amsterdam

Faculty of Science

Program of Computational Science

Machine Learning Classifications for ThePrediction of Intraday Trading Signal

Wentao Yang

Supervisor: Prof. Dr. Drona Kandhai

Submitted in part fulfillment of the requirements for the degree ofMaster of Science in Computational Science of the University of Amsterdam , November 6,

2017

Abstract

This paper proposes and studies a series of Machine learning methods to make prediction for

intraday trading signal, by using different combinations of stock market technical indicators

as the feature set (the input) into the classier. The main purpose of this paper is to do

research on existing study on application of Machine Learning Classification Algorithms in

automatic quantitative trading, and further uses and combines multiple techniques into one

two-layers filter system to help the automatic trading algorithm in the system with better

financial market information analytical ability and more reliable trading decision making. The

techniques we investigate include famous Machine Learning classifiers such as Artificial Neural

Network, Random Forest, and we also apply re-sampling methods to reduce the imbalanced

problem in the dataset. In total, 1 Year pre-processed dataset from Japanese stock market

(Nikkei) is used to train and test the classification algorithms. As to the evaluation of different

algorithms, the confusion matrix is applied to calculate the evaluation metrics such as accuracy

and precision. Furthermore, due to the imbalanced class problem in the dataset, Kappa and

AUC are employed to measure and compare the performance of the filters based on different

combination of machine learning classification algorithms. Lastly the effect of filter (classier)

on the profitability of trading strategy is also examined.

The findings show that the profitability of momentum trading based strategy/algorithms can

be significantly improved with the help of machine learning applications. With the strong

power of machine learning algorithms in high-dimensional data analysis, the filter can improve

the ability of strategy in better analyzing the trend and relationship in the intraday market by

using the tremendous intraday market data, and improve trading decision making based on the

signal from the filter system.

i

ii

Acknowledgements

This master thesis marks the end of my master study at University of Amsterdam. The work

has at times been challenging, but it has also been very useful and rewarding for my future

career development at the same time. I would like to express my feelings to:

• My colleagues at Algorithmic Trading Group. Thanks to them, I got the opportunity

to do my master project in the firm and gain a lot experience of applying quantitative

techniques in financial algorithmic trading. I appreciate their supports and practical

suggestions regarding the trading strategy during my research.

• My Supervisor and researchers in the Computational Finance Group at UvA. I’d like to

say thanks to them for their kind understandings about my special situation at the last

stage of my study, and of course for their valuable inputs and suggestions during the

writing process.

• Finally, I’d like to say my love and thanks to my girlfriend. Your confidence and support

in me has been a constant in my life, in the meantime your love and patience has been

the foundations of this work.

iii

iv

Contents

Abstract i

Preface iii

1 Introduction 1

1.1 Relevant Studies on Machine learning in Finance . . . . . . . . . . . . . . . . . 2

1.2 Structure of Paper . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

2 Literature Study on Machine Learning 5

2.1 Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2.2 Machine Learning Algorithms . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

2.3 Supervised Learning Classification Algorithms . . . . . . . . . . . . . . . . . . . 7

2.3.1 Support Vector Machine Algorithm (SVM) . . . . . . . . . . . . . . . . . 7

2.3.2 Artificial Neural Network Algorithm (ANN) . . . . . . . . . . . . . . . . 8

2.3.3 Random Forest Algorithm (RF) . . . . . . . . . . . . . . . . . . . . . . . 10

2.3.4 Xgboost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2.3.5 Model Stacking: Combing Classifiers . . . . . . . . . . . . . . . . . . . . 12

v

vi CONTENTS

2.4 Evaluation metrics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

2.4.1 Confusion matrix and accuracy . . . . . . . . . . . . . . . . . . . . . . . 13

2.4.2 Precision, Recall and F1-Score . . . . . . . . . . . . . . . . . . . . . . . . 15

2.4.3 Kappa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

2.4.4 ROC and AUC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

2.4.5 Performance of Profitability of the model . . . . . . . . . . . . . . . . . . 17

2.5 Model Validation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

2.5.1 Holdout . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

2.5.2 K-fold Cross-Validation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

2.6 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

3 Project Design and Data Engineering 24

3.1 Project Description . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

3.2 Architecture of the Filter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

3.3 Trading Data Description and Engineering . . . . . . . . . . . . . . . . . . . . . 27

3.3.1 Data Description . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

3.3.2 Data Pre-Processing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

3.3.3 Feature Engineering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

3.3.4 Feature Reduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

3.3.5 Imbalanced Data and Solutions . . . . . . . . . . . . . . . . . . . . . . . 37

3.4 Performance and Efficiency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

4 Experiments and Outputs 41

4.1 Layer 1: Profit Margin Prediction . . . . . . . . . . . . . . . . . . . . . . . . . . 42

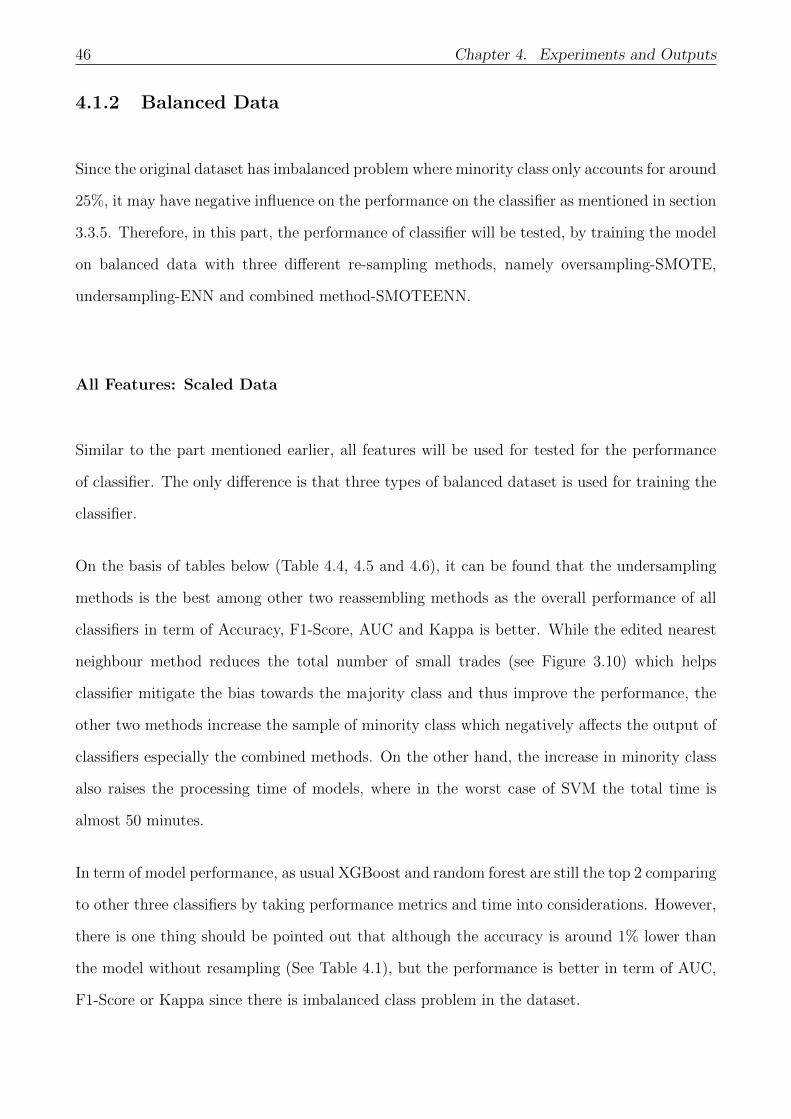

4.1.1 Imbalanced Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

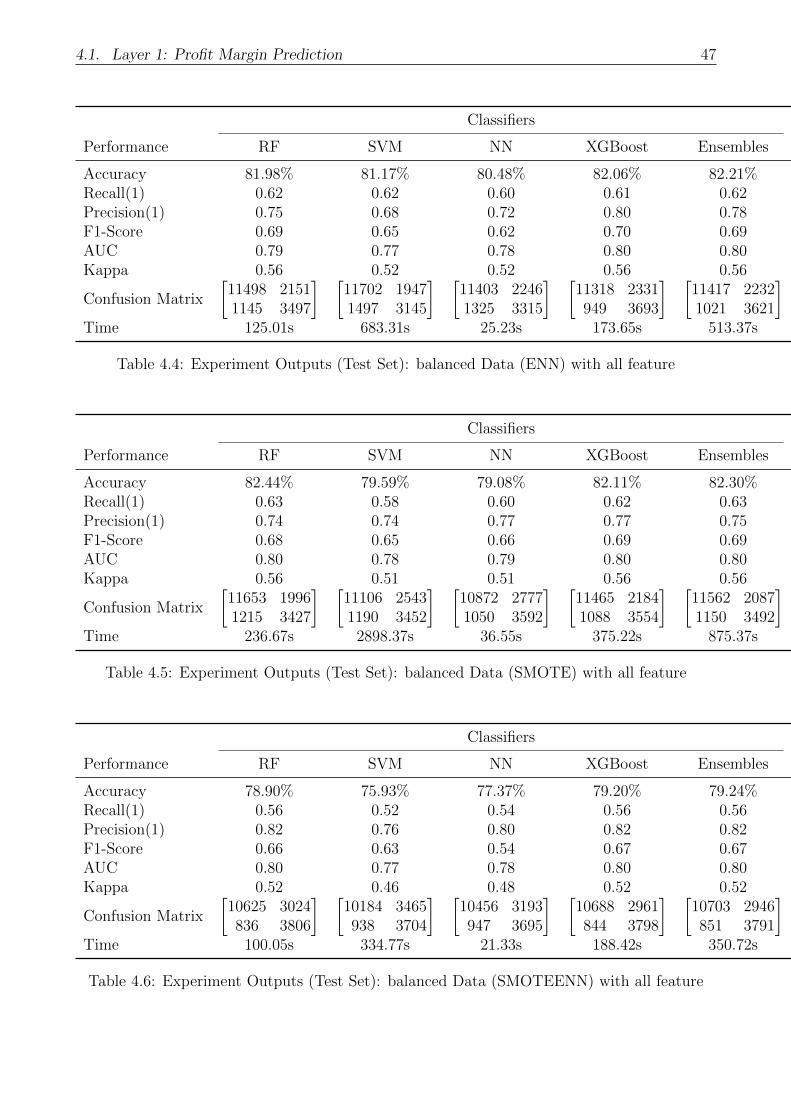

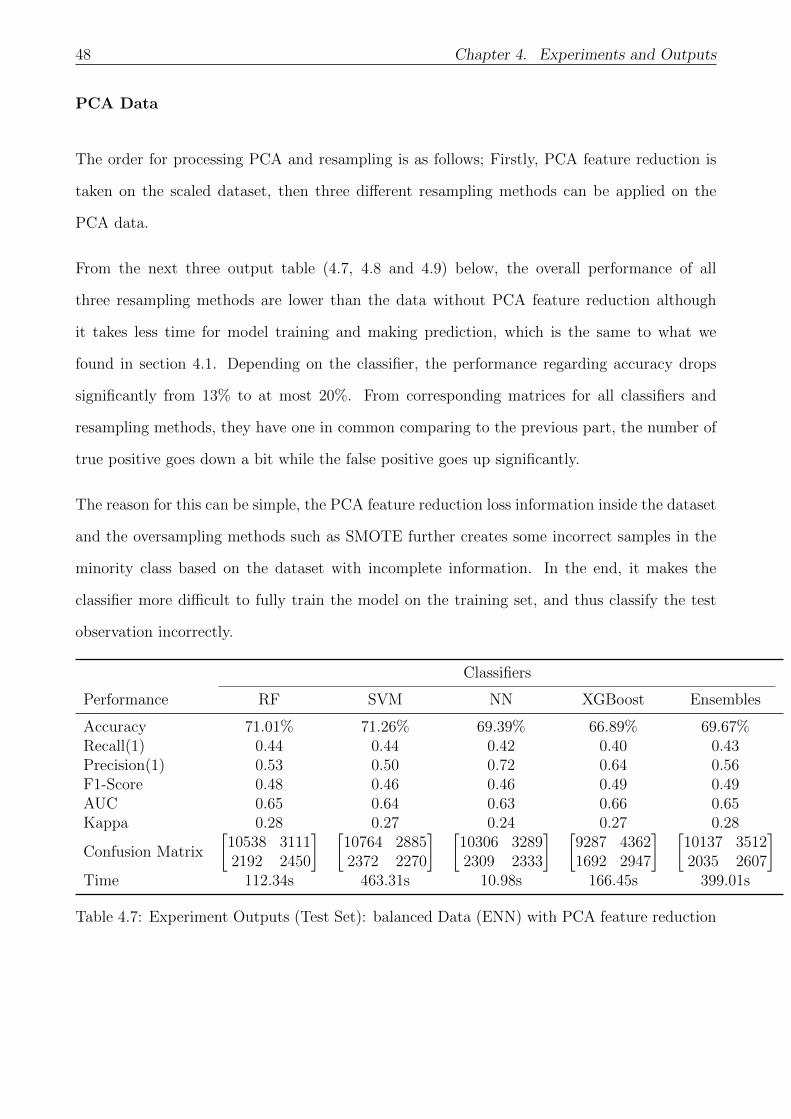

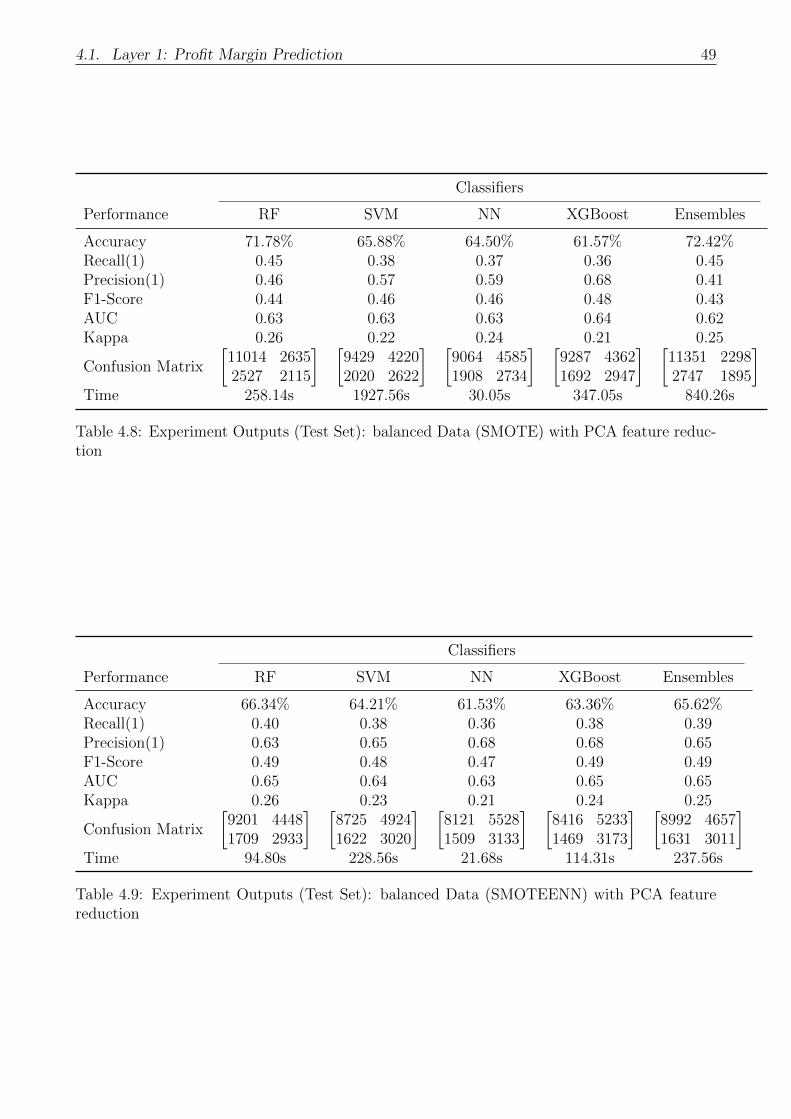

4.1.2 Balanced Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

4.2 Layer 2: Movement Direction Prediction . . . . . . . . . . . . . . . . . . . . . . 52

4.3 Performance of Combining Two Layers . . . . . . . . . . . . . . . . . . . . . . . 53

5 Conclusion 55

5.1 Summary of Thesis Achievements . . . . . . . . . . . . . . . . . . . . . . . . . . 56

5.2 Future Work . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

Bibliography 57

6 Appendix 63

vii

viii

List of Tables

2.1 Confusion Matrix: 2 Classes Problem . . . . . . . . . . . . . . . . . . . . . . . . 14

2.2 Confusion Matrix: Basic Trading Example . . . . . . . . . . . . . . . . . . . . . 16

4.1 Experiment Outputs (Test Set): Imbalanced Data with all features . . . . . . . 43

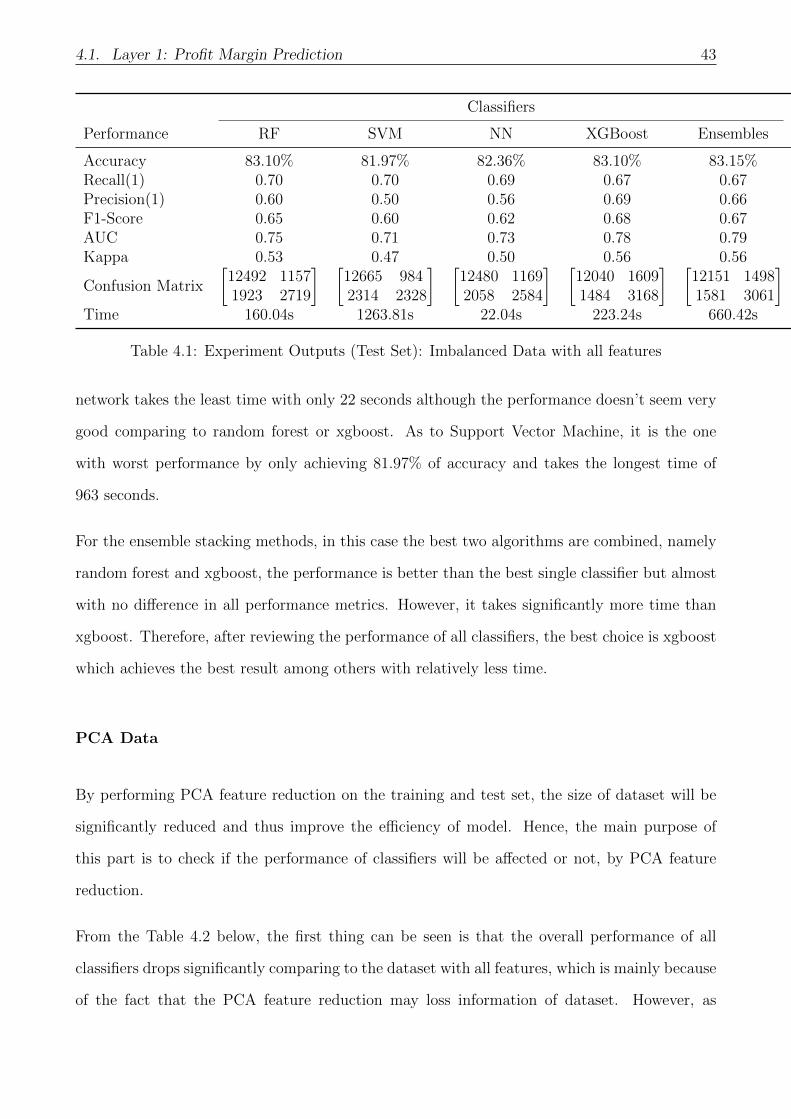

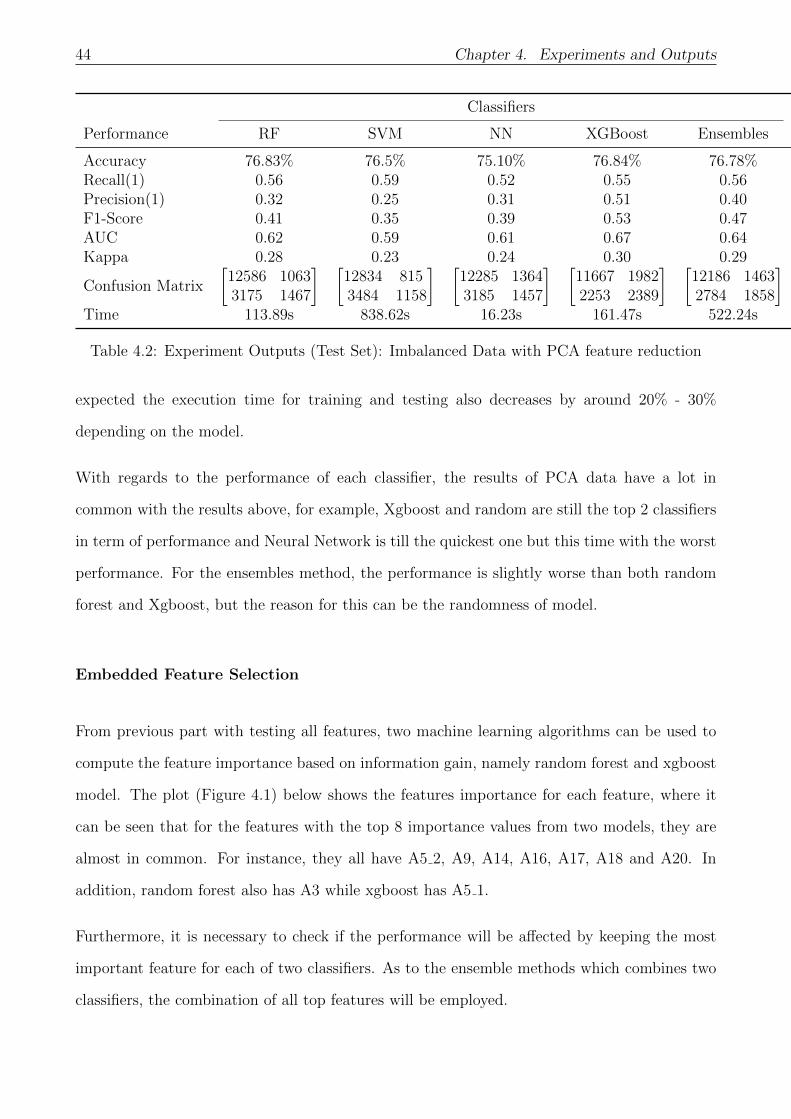

4.2 Experiment Outputs (Test Set): Imbalanced Data with PCA feature reduction . 44

4.3 Experiment Outputs (Test Set): Imbalanced Data with selected Feature . . . . . 45

4.4 Experiment Outputs (Test Set): balanced Data (ENN) with all feature . . . . . 47

4.5 Experiment Outputs (Test Set): balanced Data (SMOTE) with all feature . . . 47

4.6 Experiment Outputs (Test Set): balanced Data (SMOTEENN) with all feature . 47

4.7 Experiment Outputs (Test Set): balanced Data (ENN) with PCA feature reduction 48

4.8 Experiment Outputs (Test Set): balanced Data (SMOTE) with PCA feature

reduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

4.9 Experiment Outputs (Test Set): balanced Data (SMOTEENN) with PCA fea-

ture reduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

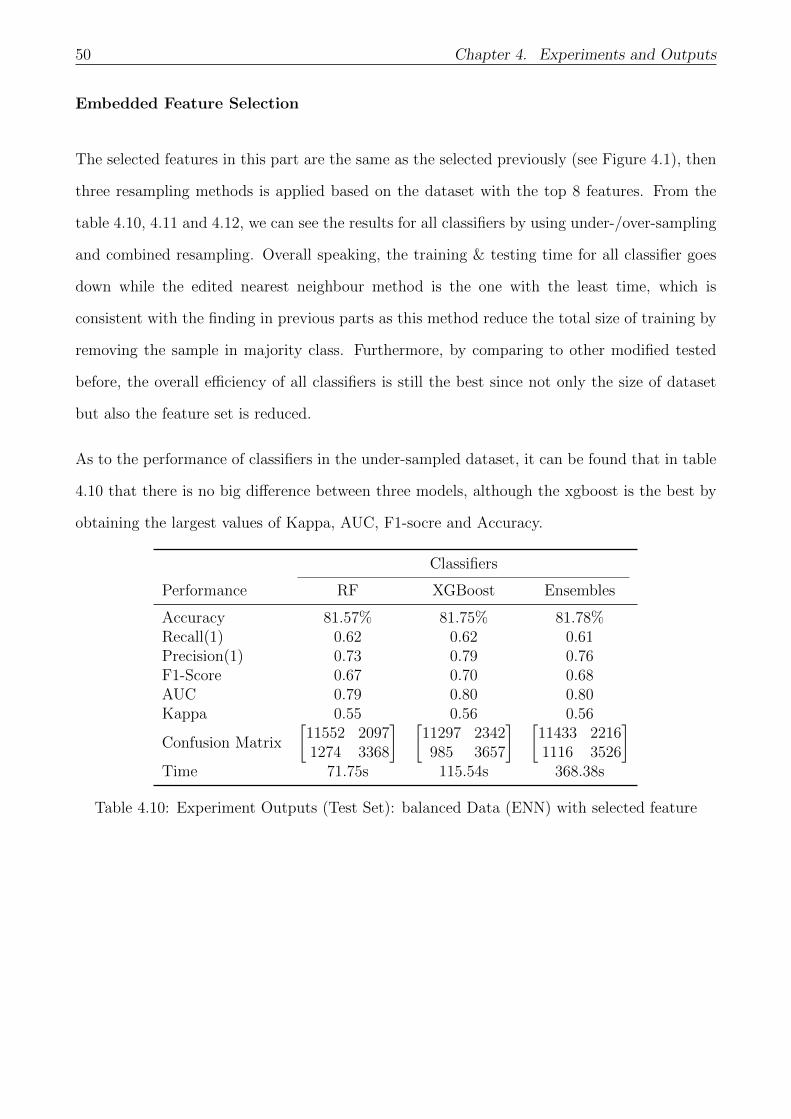

4.10 Experiment Outputs (Test Set): balanced Data (ENN) with selected feature . . 50

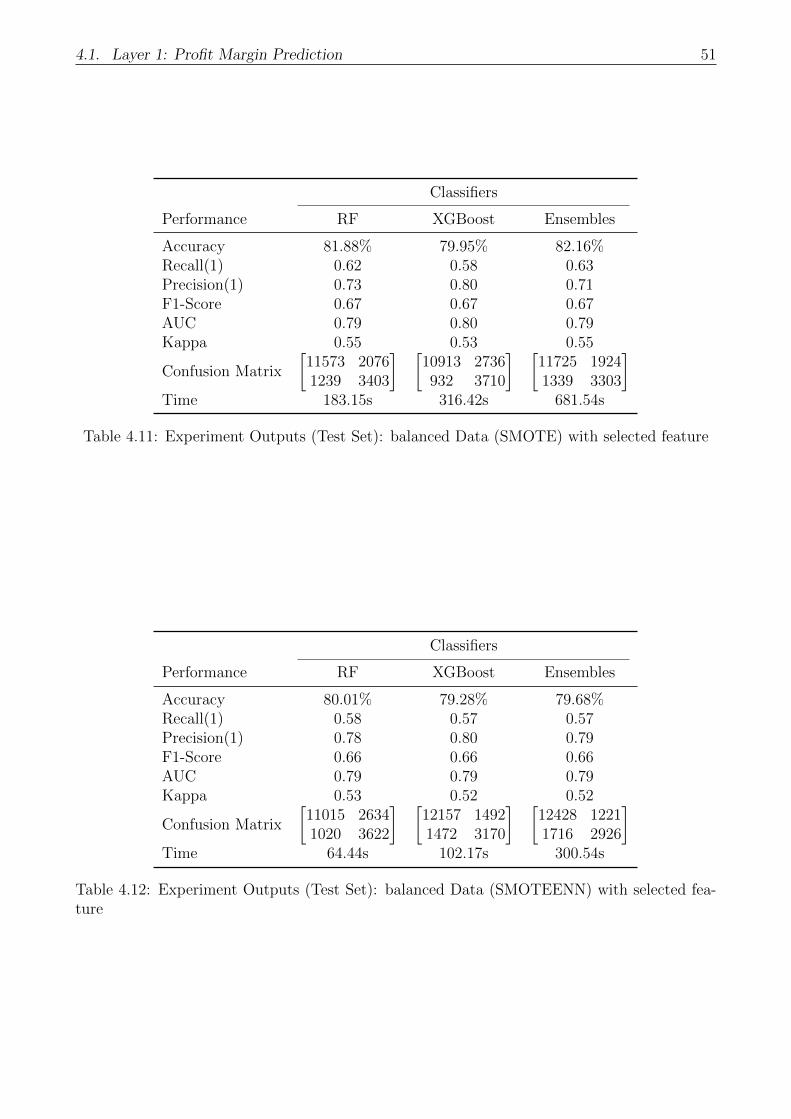

4.11 Experiment Outputs (Test Set): balanced Data (SMOTE) with selected feature 51

ix

4.12 Experiment Outputs (Test Set): balanced Data (SMOTEENN) with selected

feature . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

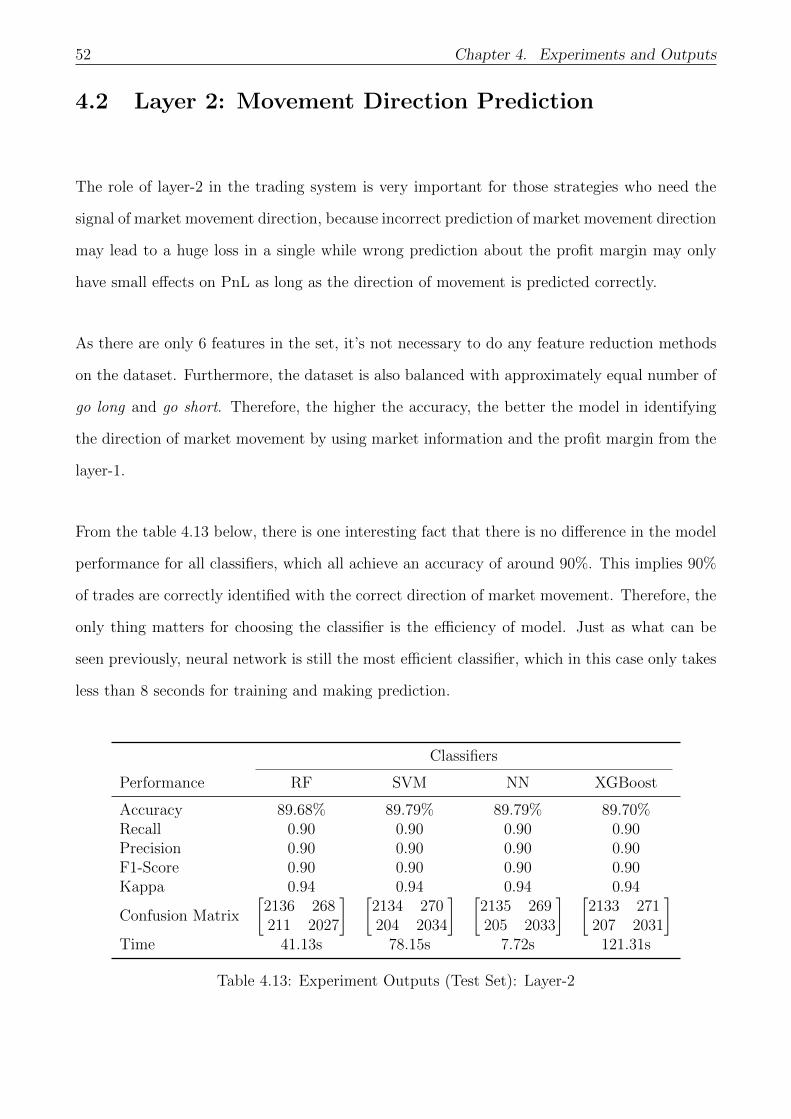

4.13 Experiment Outputs (Test Set): Layer-2 . . . . . . . . . . . . . . . . . . . . . . 52

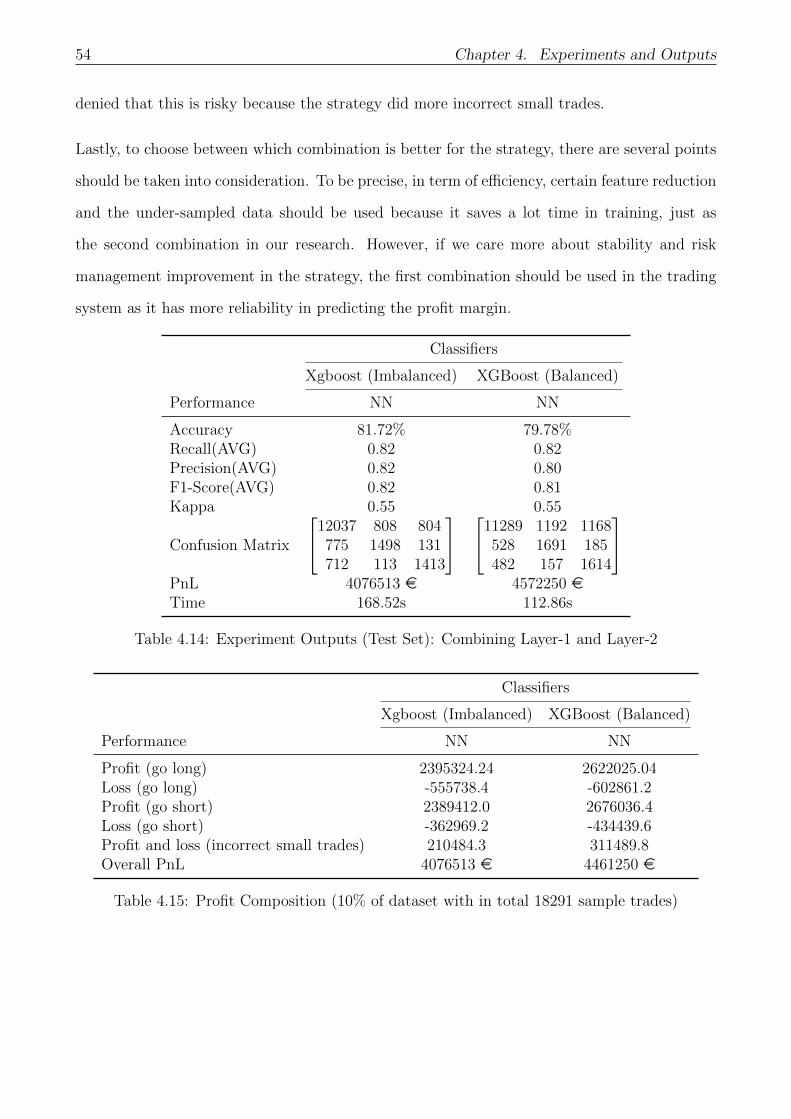

4.14 Experiment Outputs (Test Set): Combining Layer-1 and Layer-2 . . . . . . . . . 54

4.15 Profit Composition (10% of dataset with in total 18291 sample trades) . . . . . 54

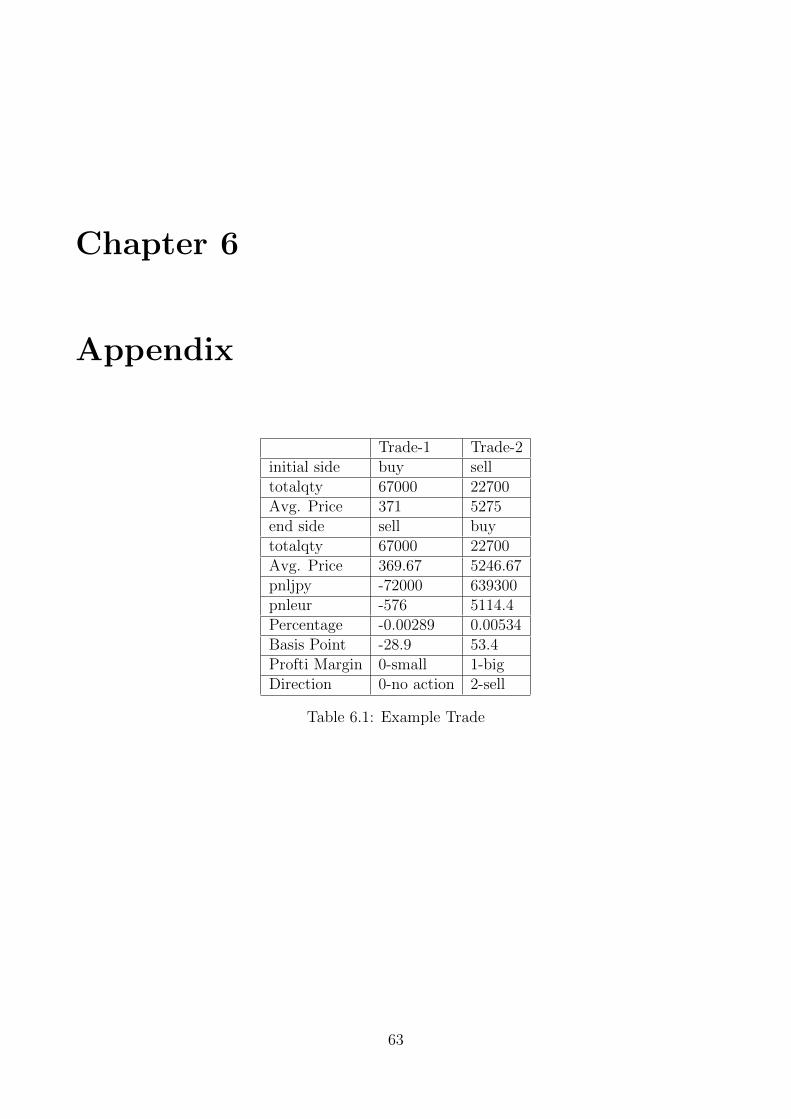

6.1 Example Trade . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

6.2 Feature Table . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

x

List of Figures

2.1 Unsupervised Learning: Clustering . . . . . . . . . . . . . . . . . . . . . . . . . 6

2.2 Example of Support Vector Machine (SVM) Classification . . . . . . . . . . . . 8

2.3 Structure of Artificial Neural Network . . . . . . . . . . . . . . . . . . . . . . . . 9

2.4 A Neural Network node . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2.5 Example of Random Forest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2.6 Structure of Xgboost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2.7 Diagram of Model Stacking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

2.8 ROC Curve . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2.9 General Trading Structure/Process . . . . . . . . . . . . . . . . . . . . . . . . . 19

2.10 Holdout Validation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

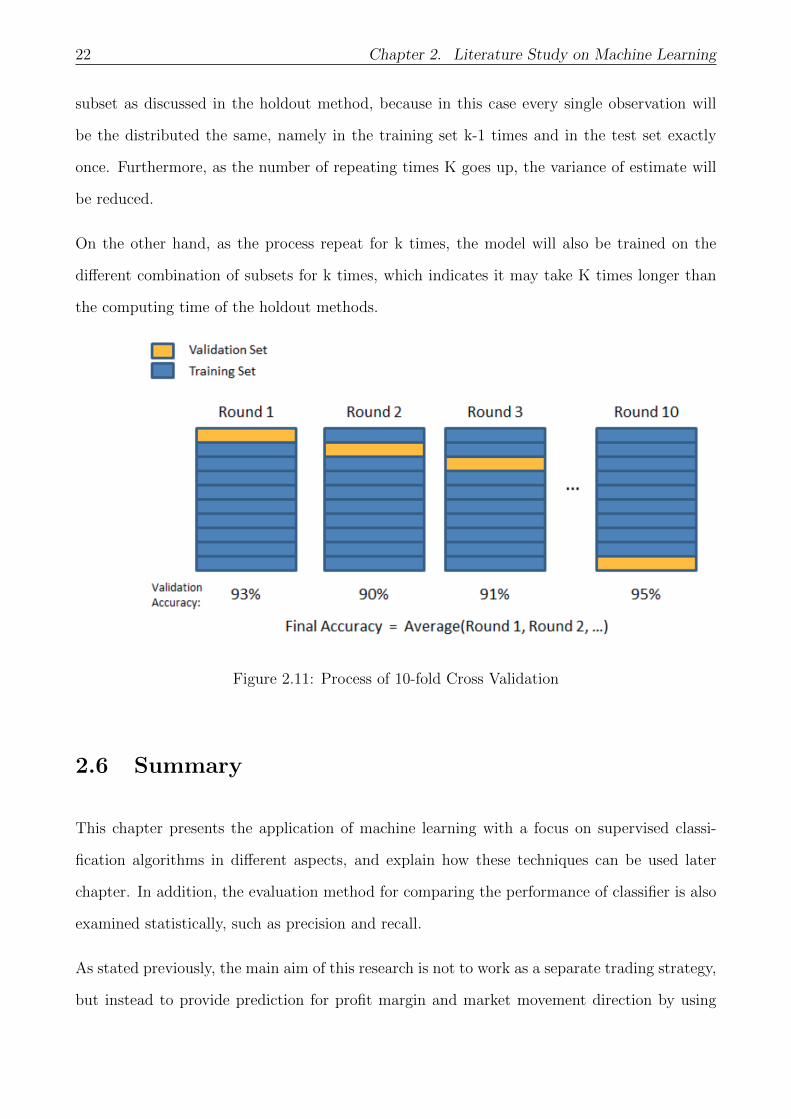

2.11 Process of 10-fold Cross Validation . . . . . . . . . . . . . . . . . . . . . . . . . 22

3.1 Diagram of The Trading System (Example) . . . . . . . . . . . . . . . . . . . . 27

3.2 Histogram of Features . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

3.3 Descriptive Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

3.4 Histogram of Scaled Features . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

xi

3.5 Histogram of Target Variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

3.6 Histogram of New Feature: A20 . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

3.7 Correlations Plot . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

3.8 Principal Component Analysis (PCA) for Group 1(The Layer 1) Plot . . . . . . 36

3.9 Embedded Feature Selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

3.10 Histogram of Target Variable-Size after over-/under-sampling. . . . . . . . . . . 38

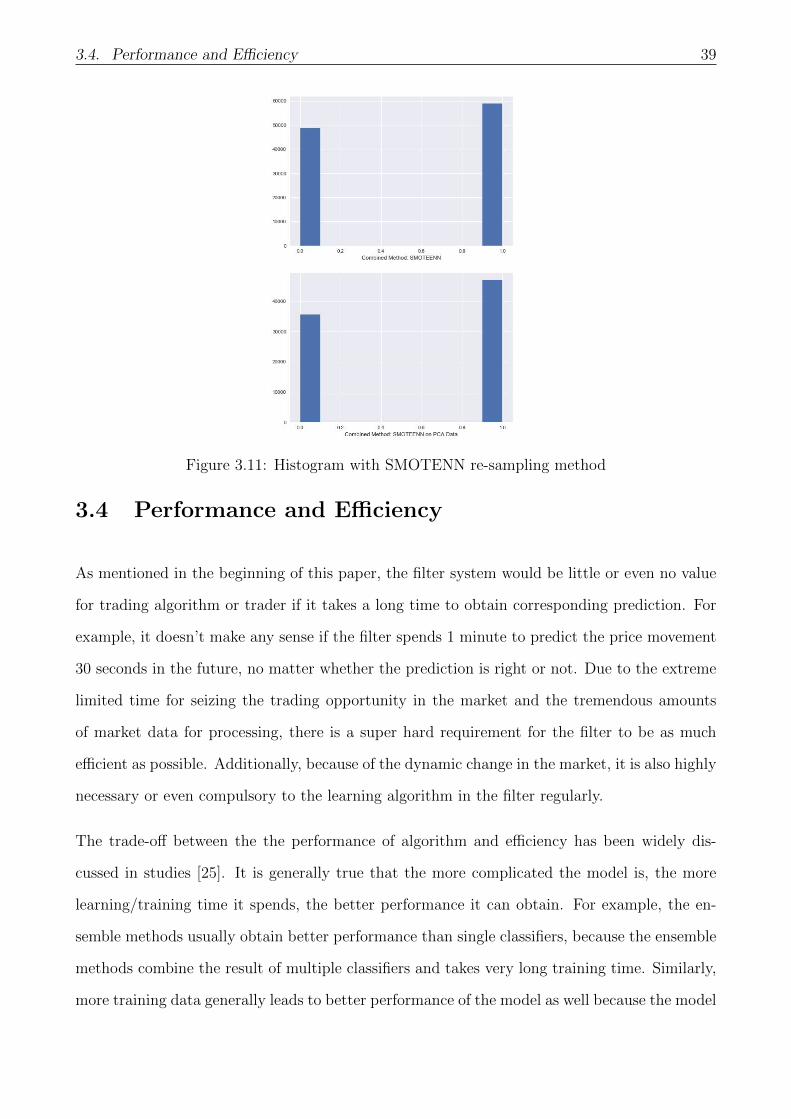

3.11 Histogram with SMOTENN re-sampling method . . . . . . . . . . . . . . . . . . 39

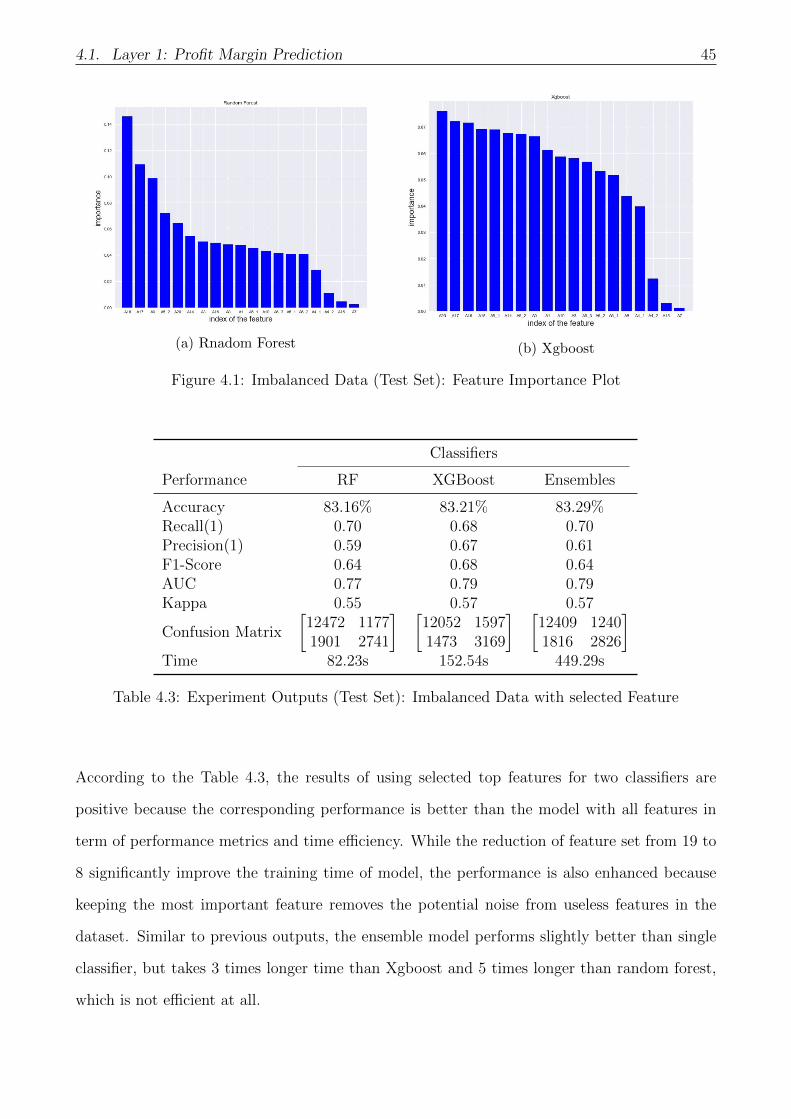

4.1 Imbalanced Data (Test Set): Feature Importance Plot . . . . . . . . . . . . . . . 45

xii

Chapter 1

Introduction

Forecasting the financial securities especially the cash equity, has been widely studied by many

researchers and financial firms in the past decade. Although many results have been published in

books and papers, some of them are rarely applicable and repeatable in real financial problems

for some reasons. Nowadays, as the market has been shifted from traditional (manual) trading

to a more modern and automated electronic trading, recent research now put more and more

focus on the application of different quantitative methods in high-frequency trading (HFT)

data (by seconds/minutes, instead of day or week). However, there might be some difficulties

in dealing with HFT data, for example, extremely large quantities of trading data and relatively

long processing time by the model to compute a prediction comparing to the limited time for

determination a trader has.

When talking about the stock prediction, the first thing comes out is the important theory in

financial economics -Efficient Market Hypothesis (EMH) by Fama in the 1965[1], which states

that the current asset’s price reflects all known information, thus only new information can

lead to a move in the price. As we know, there are three common methods for the stock

market prediction that used by financial industry, namely the fundamental analysis, technical

analysis and quantitative analysis, where both employs relevant information to make movement

prediction although the analytical methods are different.

1

2 Chapter 1. Introduction

The fundamental analysis examines both macroeconomic and microeconomics factors, which in-

cludes elements such as the health of a country economy or global economy, quarterly/annually

company financial report, competitor performance and the corresponding market situation. By

doing fundamental research on these factors, an investor can obtain a general overview of the

company/industry and then determine a fair value (stock price) for the business. For example,

if the company (stock price) is undervalued according to the research result, then we can buy

the stock to make profit.

The idea of traditional technical analysis is to anticipate what other participants in the market

are thinking by using historical market data, mainly based on the stock price and trading

volume. With the help of mathematical/statistical model, we can use historical data to predict

future movements in the stock price, by identifying the trend of price movement and extracting

and inspecting the pattern visually from noisy data. Therefore, trading decision can be made

on the basis of the prediction.

1.1 Relevant Studies on Machine learning in Finance

In the past 10 years, trading gradually became a more and more complex which made the

market keep getting faster and the volumes of trading data keep escalating. Furthermore, the

market also became more volatile, as a result some huge and unexpected shifts may occur in

the market, such as what it could be found in 2007-2009 financial crisis. For old methods as

mentioned above, they have difficulty in processing large volume data and thus not be able to

make quick and correct predictions for those unexpected sudden shifts, but these two factors

are the most important things for high-frequency trading firms.

Recent developments in computing technology and data science has made traditional technical

analysis into a more quantitative approach. Techniques such as machine learning offer the

potential to improve short-term prediction for market movements or key variables, even during

volatile markets, because they can incorporate a much wider range of factors in their models,

1.1. Relevant Studies on Machine learning in Finance 3

and due to their high efficiency in computing. Prediction, as the most commonly used ap-

plication based on machine learning in financial area, there are many existing researches and

literature regarding this topic. Huang and Tsai [3] presents their hybrid-methods by combining

traditional technical analysis and artificial neural network for stock market prediction, where

the neural network classifier is mainly used for feature selection. Similarly, Wu et al.[4] also

use a radial basis function neural network model for stock index prediction, where the model

is optimized heuristically by artificial fish swarm algorithm. In 2013, Menconi and Gori[5]

uses support vector machine to balance recall and precision in stock market predictors, and by

using the selected indicators they make a profitable model with the help of technical analysis.

There are also researches about comparison of performance of different algorithms in stocking

trend prediction, for example Salim, compares between the performance of Probabilistic neural

network (PNN) and SVM and finds out that the PNN performs the best when only technical

indicators are used.

In addition to the prediction task, there are another two types of application based on machine

learning in financial trading, namely finding relationship/association and generating trading

strategies. For instance, Kapoor and Khurana [26] presents their idea about using Genetic

Algorithms in designing and building technical trading system. Wang[22] uses quantitative

methods to find the intraday inefficiency between the heating and natural gas markets.

However, it should be pointed out that none of researchers above claim that their prediction

model can work in real-time settings because their data source are mostly daily data instead

of high-frequency data. For those successful models or applications who can work in real-time

trading environment, there are also no incentive for the researchers or sponsoring firms to pub-

lish results. In fact, quantitative trading firms or researchers do not only use this quantitative

analysis for price prediction, but now also for the area of trading/hedging strategy development,

risk management and portfolio optimization. The example applications of quantitative method

can be algorithmic trading, statistical arbitrage and electrical market marking, where the main

purpose of using the quantitative methods is to replace the human element in trading with a

more technical and automatic way, which are commonly used in HFT firms.

4 Chapter 1. Introduction

1.2 Structure of Paper

The main goal of this research is to build a real-time filter system for trading algorithms that

used in Algorithmic Trading Group (ATG), the Netherlands, in order to improve the overall

performance of the strategy in term of profitability. To be precise, there are two layers in

the filter, where the first layer is to predict the profit margin of potential trade while at the

second layer we explore the predictability of market movement direction of the chosen stock

from previous layer, by employing the machine learning classification algorithms with different

set of technical market features. In this research, we use one-year data from Japanese cash

equity market with in total 23 intraday markets features, such as bid-ask spread, one-minute

trading volume and history volatility.

In the following, Chapter 2 will discuss a literature study of machine learning in general, such

as the introduction to the supervised machine learning algorithms that used in this research,

evaluation metrics for comparing the performance of different classifiers and lastly the model

validation. A description of project, framework of filter system, pre-data engineering and

resampling techniques will be involved in the Chapter 3, The Chapter 4 will present the results

of different classifiers with using different types of modified dataset in term of both statistical

performance, and the one with best performance is selected to further examine its impacts on

the profitability of trading strategy. Lastly, we will summarize and give suggestions for future

improvement.

Chapter 2

Literature Study on Machine Learning

2.1 Overview

Because of breakthroughs in both technology and computing algorithms, the trading industry

has shifted from a traditional manual trading to a more technology- and data-driven automated

trading. There are now many different quantitative techniques that can used to predict the

stock market movements, but as noted most of published studies don’t work in real-time setting

with using medium- or high-frequency data. The reason for the lack of published results in real-

time application can be simply be that there is little incentive to publish such (good) methods

in academic literature for either researchers or trading firms. The incentive for researchers to

instead sell them to a trading firm is much greater than publish their findings, monetarily.

Similarly, for those trading firms who build good model to predict the stock movement, they

have no incentive to share the model with other competitors neither. This is the goal of

this research, to explore the application of modern quantitative algorithms, namely Machine

Learning, in predicting the intraday stock movement.

In this chapter, the discussion mainly covers what machine learning is and how we can apply the

algorithm from machine learning to learn from data. In the Section 2.2 and 2.3, an overview of

popular algorithms from machine learning is given, such as Support Vector Machine (SVM) and

5

6 Chapter 2. Literature Study on Machine Learning

Random Forest (RF). Section 2.4 examines different methods for evaluating the performance

of different algorithms by using the confusion metrics. In the section 2.5, a review on model

validation method will be given.

2.2 Machine Learning Algorithms

As part of artificial intelligence, machine learning employs algorithms to explore the pattern

in data and make forecasts about future events. There are two types of Machine Learning

Algorithm, namely the unsupervised learning algorithms and supervised learning algorithms.

The key difference between supervised learning and unsupervised learning is that the output

variable (target) are provided for the supervised one in order to train the machine and desired

output, while in the unsupervised learning modelling it does not include target variable because

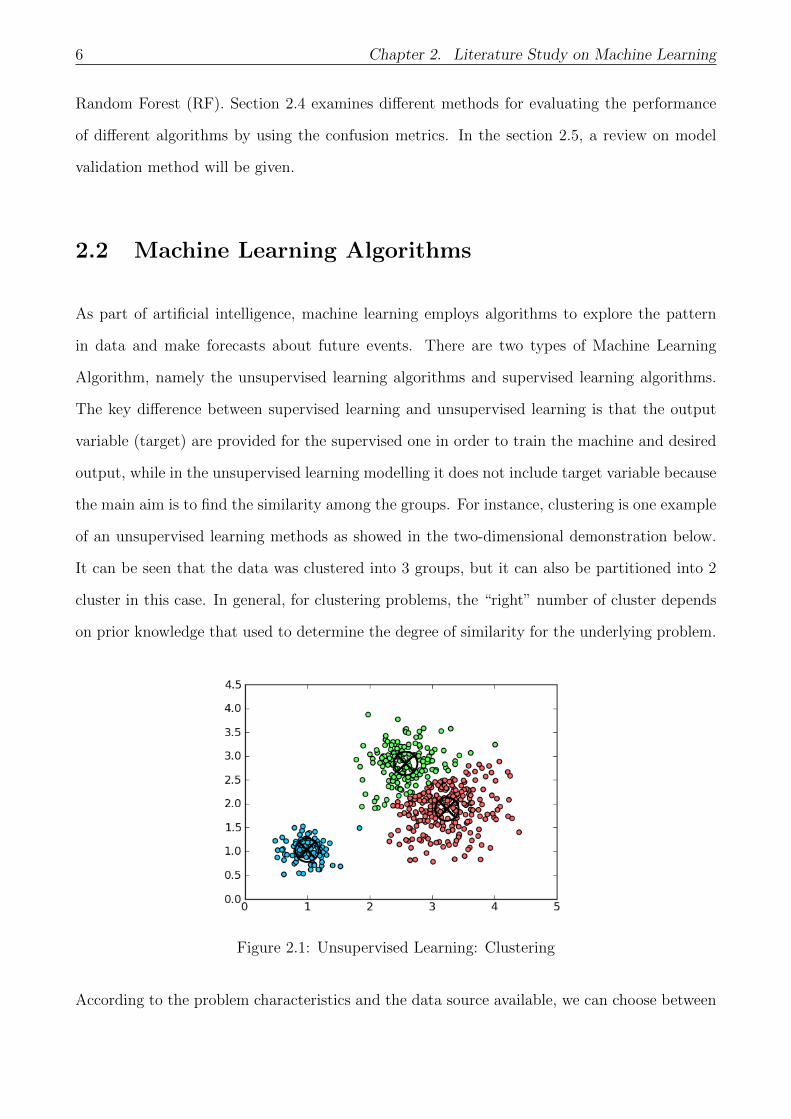

the main aim is to find the similarity among the groups. For instance, clustering is one example

of an unsupervised learning methods as showed in the two-dimensional demonstration below.

It can be seen that the data was clustered into 3 groups, but it can also be partitioned into 2

cluster in this case. In general, for clustering problems, the “right” number of cluster depends

on prior knowledge that used to determine the degree of similarity for the underlying problem.

Figure 2.1: Unsupervised Learning: Clustering

According to the problem characteristics and the data source available, we can choose between

2.3. Supervised Learning Classification Algorithms 7

supervised and unsupervised learning algorithms. In this research, since the target is known

which is the direction of intraday stock movement, namely go long or go short, the supervised

learning algorithm should be used. Furthermore, as the type of target attribute is discrete

instead of continuous, the classification algorithms is applied. Therefore, in the next section

we explore different classification learning algorithms from supervised techniques, since the

performance of different algorithms may differ due to the characteristics of underlying dataset.

2.3 Supervised Learning Classification Algorithms

Classification as one of the Machine Learning techniques, does analysis on a given dataset, then

takes each instance of the dataset, and lastly assigns the instance to a particular class where

the corresponding classification error will be the smallest. As similar to other machine learning

algorithms, the whole process of classification has two steps, at the step one the classification

model is trained based on the training dataset, and then in the next step the training model

is applied to test against the test dataset in order to measure the corresponding performance

and accuracy. The final goal pf classification is to assign class label for the dataset whose class

label is not known.

In the following, a short discussion regarding the classification algorithms that applied in this

research will be given.

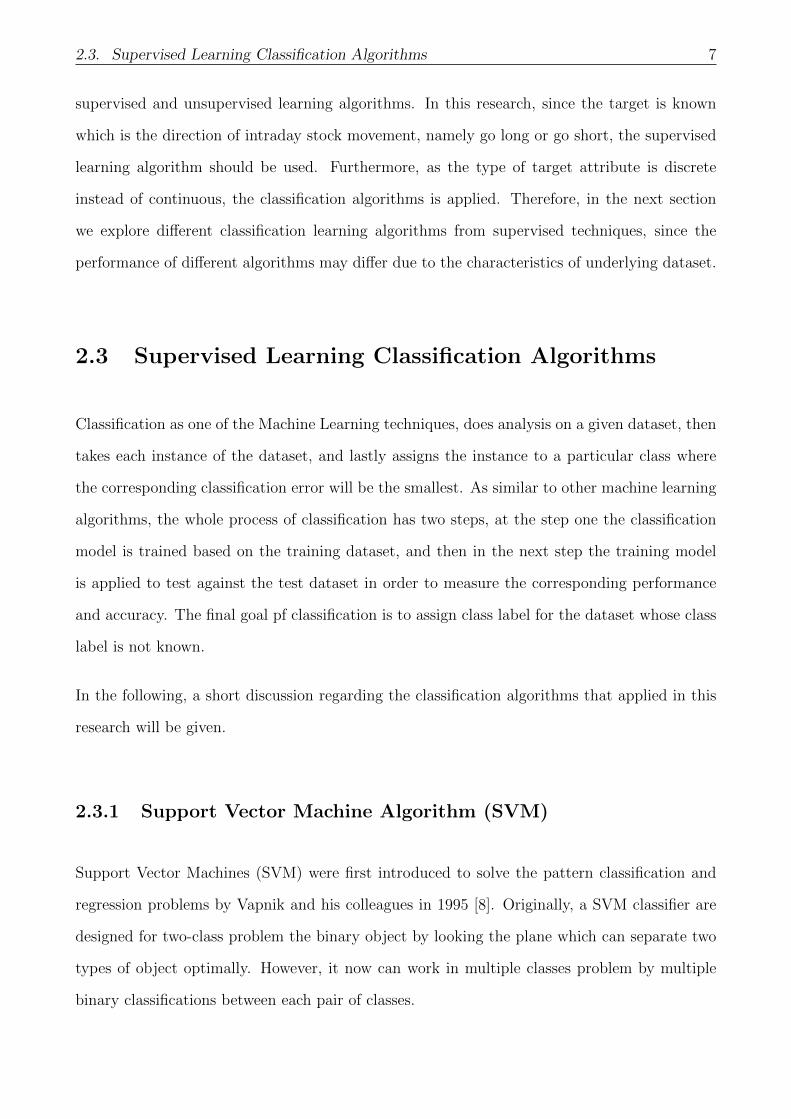

2.3.1 Support Vector Machine Algorithm (SVM)

Support Vector Machines (SVM) were first introduced to solve the pattern classification and

regression problems by Vapnik and his colleagues in 1995 [8]. Originally, a SVM classifier are

designed for two-class problem the binary object by looking the plane which can separate two

types of object optimally. However, it now can work in multiple classes problem by multiple

binary classifications between each pair of classes.

8 Chapter 2. Literature Study on Machine Learning

To be specific, the classifier mostly uses a linear function[8] of the feature to classify the ob-

servation. The margin nearby the linear separation area is computed, which should be as large

as possible. For higher dimensional space, a higher dimensional partition is done by non-linear

function which can be applied with the help of kernel in support vector machine function in

python, such as radial basis function (rbf) and polynomial (’poly’).

Figure 2.2: Example of Support Vector Machine (SVM) Classification

2.3.2 Artificial Neural Network Algorithm (ANN)

Artificial neural network (ANN) (also known as neural nets) is an interconnected network of

nodes, which is inspired from the mechanism of neuron in the brains. This artificial machine

learning methods is widely used in financial studies[10, 11], because its high performance in

learning pattern in complex dataset.

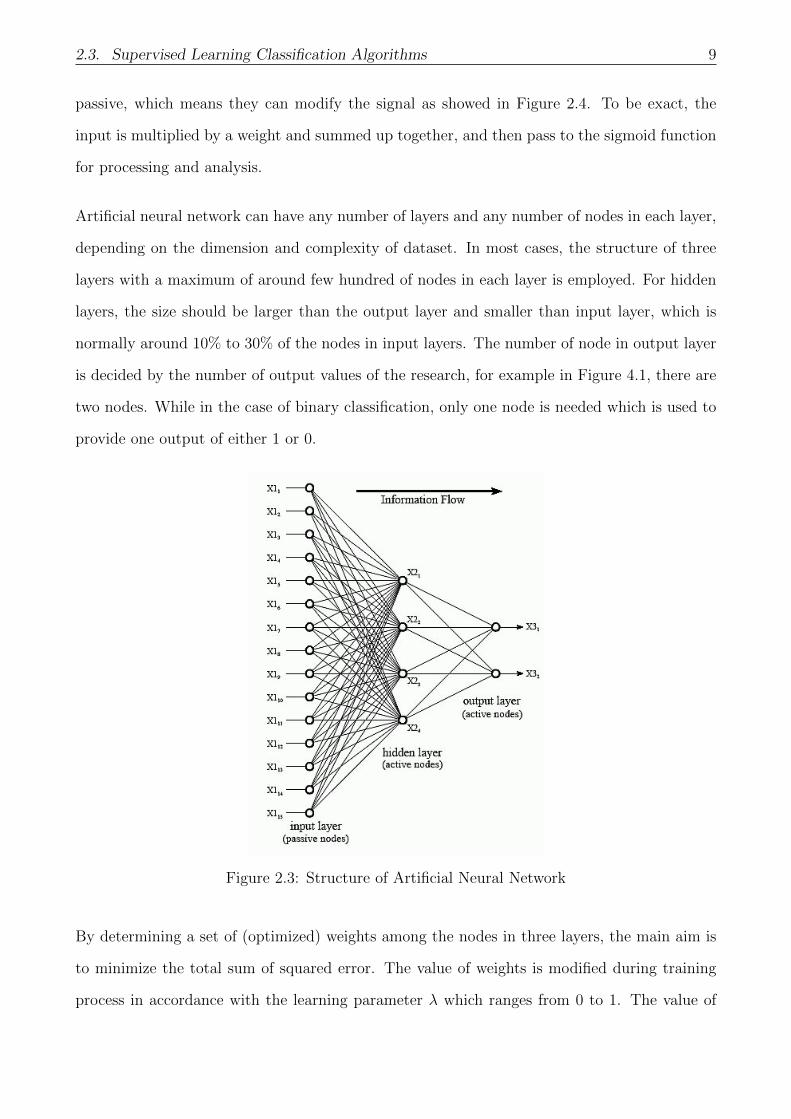

As showed in the graph below (Figure 2.3), an ANN usually consists of three layers, namely

input layer, hidden layers and output layer. The input layer consists of n (equal to the number

of feature) nodes where the nodes in the input are passive indicating they don’t modify the data

but just simply receive the value of data and copy the value to their multiple outputs. The next

part is the hidden layers, but the existence of hidden layer optional. Lastly, the main purpose

of output layer is for transforming the information from previous layers to certain outputs, i.e.,

in binary case 0 and 1. The nodes in hidden layers and output layers are active instead of being

2.3. Supervised Learning Classification Algorithms 9

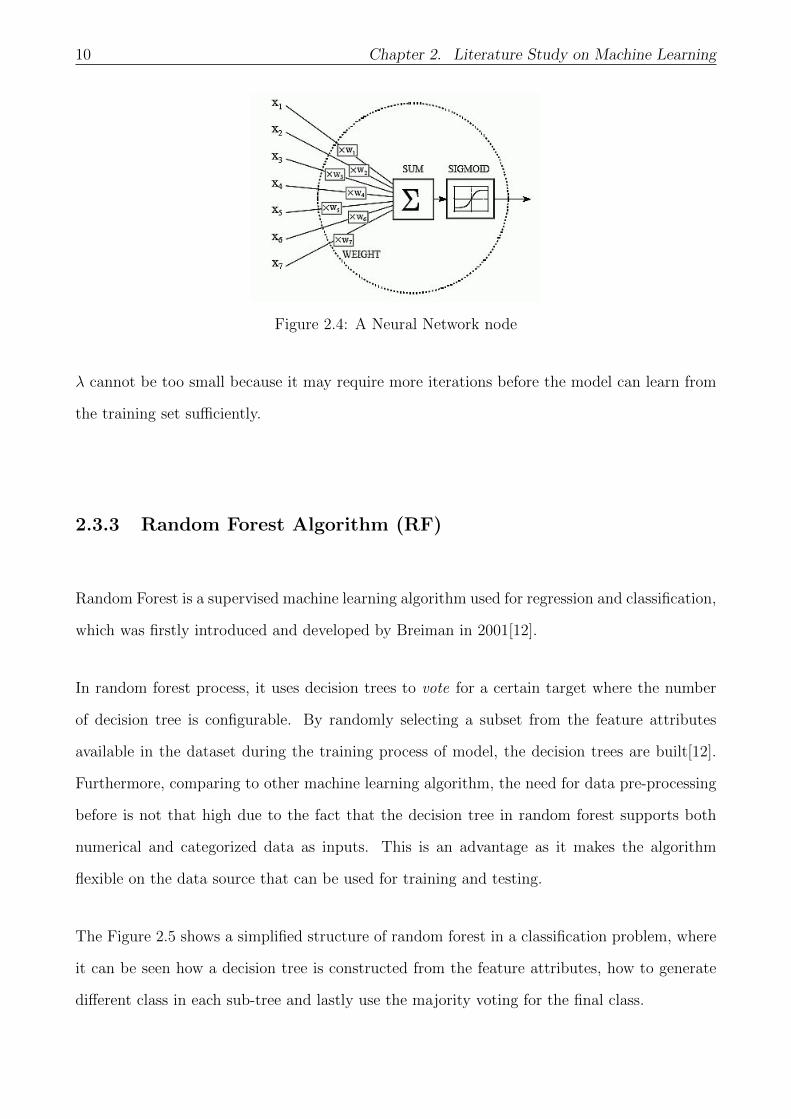

passive, which means they can modify the signal as showed in Figure 2.4. To be exact, the

input is multiplied by a weight and summed up together, and then pass to the sigmoid function

for processing and analysis.

Artificial neural network can have any number of layers and any number of nodes in each layer,

depending on the dimension and complexity of dataset. In most cases, the structure of three

layers with a maximum of around few hundred of nodes in each layer is employed. For hidden

layers, the size should be larger than the output layer and smaller than input layer, which is

normally around 10% to 30% of the nodes in input layers. The number of node in output layer

is decided by the number of output values of the research, for example in Figure 4.1, there are

two nodes. While in the case of binary classification, only one node is needed which is used to

provide one output of either 1 or 0.

Figure 2.3: Structure of Artificial Neural Network

By determining a set of (optimized) weights among the nodes in three layers, the main aim is

to minimize the total sum of squared error. The value of weights is modified during training

process in accordance with the learning parameter λ which ranges from 0 to 1. The value of

10 Chapter 2. Literature Study on Machine Learning

Figure 2.4: A Neural Network node

λ cannot be too small because it may require more iterations before the model can learn from

the training set sufficiently.

2.3.3 Random Forest Algorithm (RF)

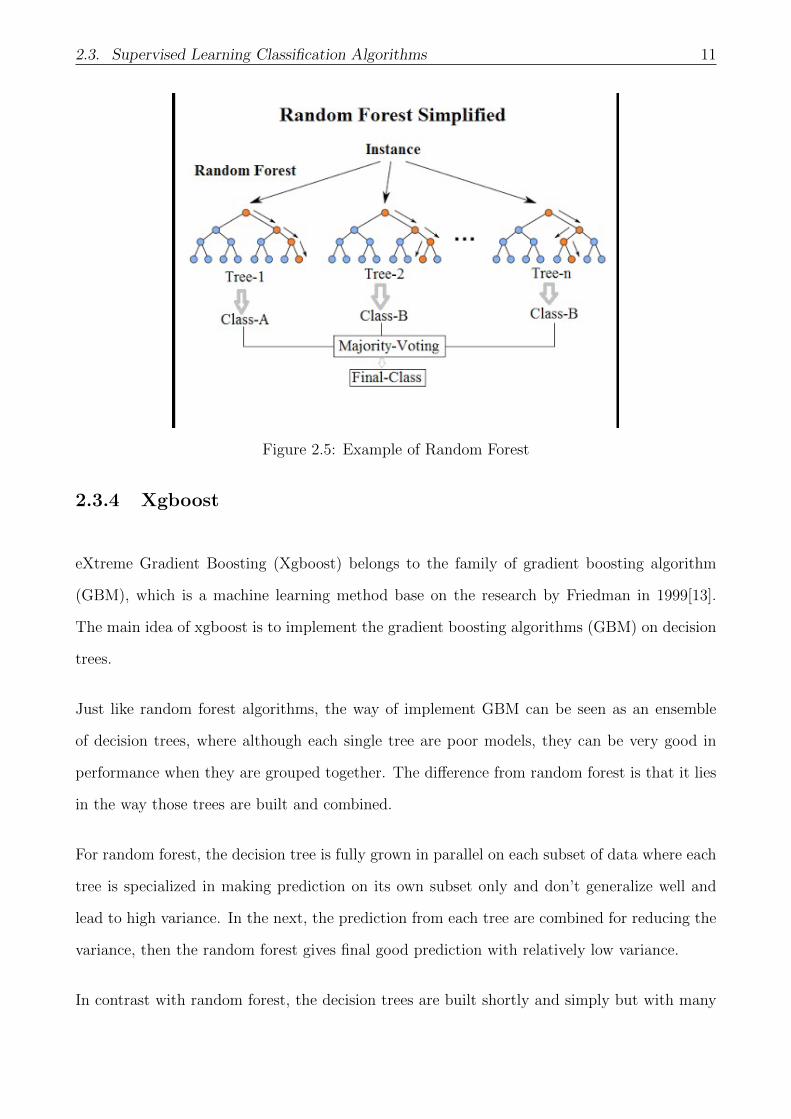

Random Forest is a supervised machine learning algorithm used for regression and classification,

which was firstly introduced and developed by Breiman in 2001[12].

In random forest process, it uses decision trees to vote for a certain target where the number

of decision tree is configurable. By randomly selecting a subset from the feature attributes

available in the dataset during the training process of model, the decision trees are built[12].

Furthermore, comparing to other machine learning algorithm, the need for data pre-processing

before is not that high due to the fact that the decision tree in random forest supports both

numerical and categorized data as inputs. This is an advantage as it makes the algorithm

flexible on the data source that can be used for training and testing.

The Figure 2.5 shows a simplified structure of random forest in a classification problem, where

it can be seen how a decision tree is constructed from the feature attributes, how to generate

different class in each sub-tree and lastly use the majority voting for the final class.

2.3. Supervised Learning Classification Algorithms 11

Figure 2.5: Example of Random Forest

2.3.4 Xgboost

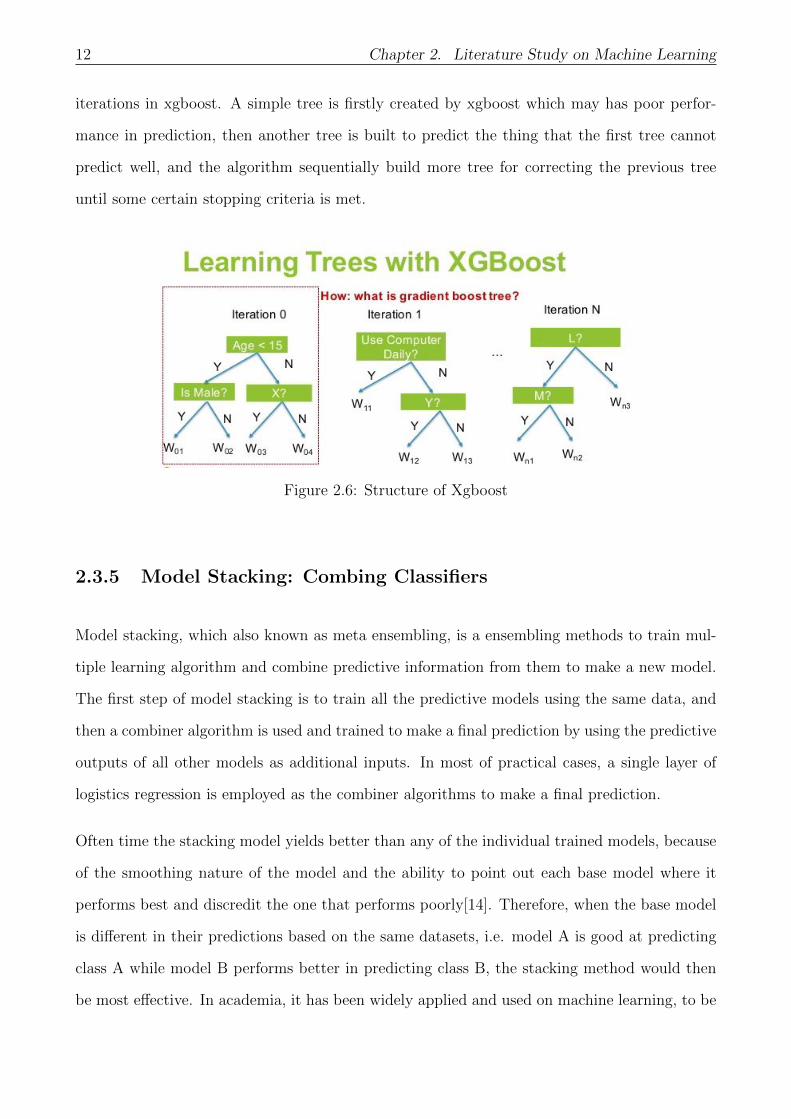

eXtreme Gradient Boosting (Xgboost) belongs to the family of gradient boosting algorithm

(GBM), which is a machine learning method base on the research by Friedman in 1999[13].

The main idea of xgboost is to implement the gradient boosting algorithms (GBM) on decision

trees.

Just like random forest algorithms, the way of implement GBM can be seen as an ensemble

of decision trees, where although each single tree are poor models, they can be very good in

performance when they are grouped together. The difference from random forest is that it lies

in the way those trees are built and combined.

For random forest, the decision tree is fully grown in parallel on each subset of data where each

tree is specialized in making prediction on its own subset only and don’t generalize well and

lead to high variance. In the next, the prediction from each tree are combined for reducing the

variance, then the random forest gives final good prediction with relatively low variance.

In contrast with random forest, the decision trees are built shortly and simply but with many

12 Chapter 2. Literature Study on Machine Learning

iterations in xgboost. A simple tree is firstly created by xgboost which may has poor perfor-

mance in prediction, then another tree is built to predict the thing that the first tree cannot

predict well, and the algorithm sequentially build more tree for correcting the previous tree

until some certain stopping criteria is met.

Figure 2.6: Structure of Xgboost

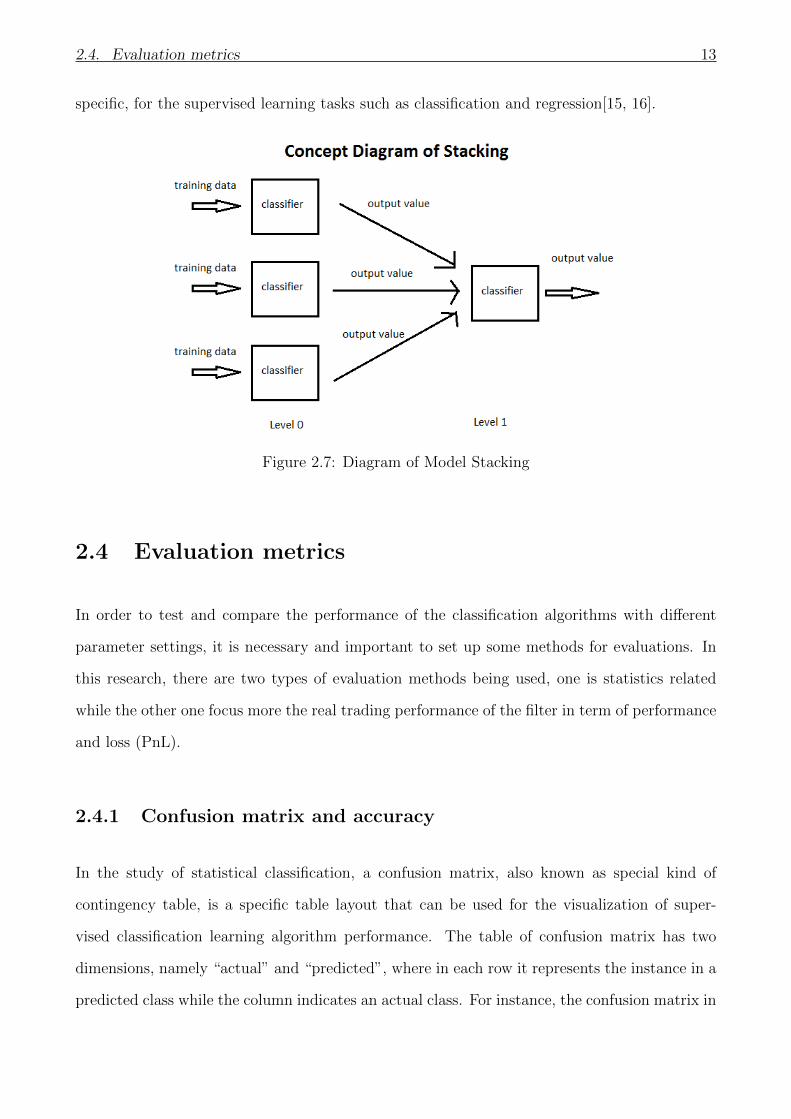

2.3.5 Model Stacking: Combing Classifiers

Model stacking, which also known as meta ensembling, is a ensembling methods to train mul-

tiple learning algorithm and combine predictive information from them to make a new model.

The first step of model stacking is to train all the predictive models using the same data, and

then a combiner algorithm is used and trained to make a final prediction by using the predictive

outputs of all other models as additional inputs. In most of practical cases, a single layer of

logistics regression is employed as the combiner algorithms to make a final prediction.

Often time the stacking model yields better than any of the individual trained models, because

of the smoothing nature of the model and the ability to point out each base model where it

performs best and discredit the one that performs poorly[14]. Therefore, when the base model

is different in their predictions based on the same datasets, i.e. model A is good at predicting

class A while model B performs better in predicting class B, the stacking method would then

be most effective. In academia, it has been widely applied and used on machine learning, to be

2.4. Evaluation metrics 13

specific, for the supervised learning tasks such as classification and regression[15, 16].

Figure 2.7: Diagram of Model Stacking

2.4 Evaluation metrics

In order to test and compare the performance of the classification algorithms with different

parameter settings, it is necessary and important to set up some methods for evaluations. In

this research, there are two types of evaluation methods being used, one is statistics related

while the other one focus more the real trading performance of the filter in term of performance

and loss (PnL).

2.4.1 Confusion matrix and accuracy

In the study of statistical classification, a confusion matrix, also known as special kind of

contingency table, is a specific table layout that can be used for the visualization of super-

vised classification learning algorithm performance. The table of confusion matrix has two

dimensions, namely “actual” and “predicted”, where in each row it represents the instance in a

predicted class while the column indicates an actual class. For instance, the confusion matrix in

14 Chapter 2. Literature Study on Machine Learning

Table 3.1 shows an example of two classes problem where it can be seen that the row represents

the actual class and the column implies the predicted class based on the model. Furthermore,

true positive (TP) in the matrix the total number of positive observation correctly identified

while true negative (TN) is the number of negative observation that correctly identified as neg-

ative. On the other hand, false positive (FP) and false negative are the number of observation

which are incorrectly identified as positive and negative, respectively.

Predicted ClassTrue False

Actual ClassTrue True Positive (TP) False Negative (FN)False False Positive (FP) True Negative (TN)

Table 2.1: Confusion Matrix: 2 Classes Problem

Based on the confusion matrix, several statistical metrics for evaluating the performance of

model can be computed. First of all, the most two commonly used metrics for evaluation are

Accuracy and Error Rate. From equation 2.1 and 2.2, it can be seen that accuracy is the total

number of correct prediction divided by all predictions while error rate is the total number of

incorrect prediction over total predictions (equivalently, 1−Accuracy). Although accuracy is a

very popular and useful evaluation metric in most of statistical analysis, it has some difficulties

in evaluating the performance of model with using a highly imbalanced dataset. It means that

the model may have high level of accuracy in term of overall performance, but it may not obtain

good result for the class that we are interested in for prediction.

Accuracy =TP + TN

TP + TN + FP + FN(2.1)

ErrorRate =FP + FN

TP + TN + FP + FN= 1− Accuracy (2.2)

For instance, assuming that we have imbalanced dataset with 95% (of not trade) as majority

class and 5% (of trade) as minority class, by using most of classifiers we can easily get an

accuracy of around 95% because the model simply predicts almost all the observations as not

trade ignoring the minority class of trade. However, this is not the result as expect, because as

2.4. Evaluation metrics 15

a trading firm the main aim is to do as many trades as possible rather than doing nothing.

In order to measure the performance of model in dealing with the imbalanced dataset better,

another two types of metrics methods are used in this research. The first type is still statistics

related, which is the precision and recall, while the other one is the trading performance in

term of profit and loss (PnL) of the strategy with filter. A more detailed description regarding

these metrics will be given below.

2.4.2 Precision, Recall and F1-Score

In study of machine learning, it is known that precision and recall are both useful evaluation

metrics for measuring the performance of machine learning classifier, especially in processing

imbalanced dataset. Precision is the percentages of correct positive predictions over all positive

predictions (See Eq. 2.3), which is a measurement of how many positive predictions were true

positive observations. Recall is the fraction of all true positive prediction over all true positive

observations (See, Eq. 2.4), which is also known as True Positive Rate (TPR) or Sensitivity.

Recall gives a reflection of how good a model in predicting the positive case because it measures

how many actual positive observations are identified correctly. Similarly, there is also False

Positive Rate (FPR), which is proportion of all negative observation that are predicted wrongly

and gives an impression of how good a model in predicting the negative class (See, Eq. 2.5).

From the imbalanced example with 5% of trade observations as minority class (see Table 2.2),

both precision and recall reflect how good the model in identifying the minority class of trade,

so an ideal model for this case would have both high recall and high precision. In term of FPR,

the False Positive Rate should be as lower as possible since less wrong trades (False Positive)

are desired.

Lastly, with regards to the F1-Score, which is the harmonic mean of precision and recall in a

single measurement and ranges from 0 to 1. (See Eq. 2.6). It can be seen that the value of

F1-score is approximately the average of precision and recall when the two getting closed to

16 Chapter 2. Literature Study on Machine Learning

Predicted ClassNot Trade (Negative) Trade (Positive)

Actual ClassNot Trade (Negative) True Negative (TN) False Negative (FN)Trade (Positive) False Positive (FP) True Positive (TP)

Table 2.2: Confusion Matrix: Basic Trading Example

each other, and the higher the better. For instance, perfect precision and recall would give a

value of 1 for F1-Score.

Precision =TP

TP + FP(2.3)

Recall =TP

TP + FN= TPR (2.4)

FPR =FP

FP + TN(2.5)

F1 =2 ∗ Precision ∗RecallPrecision+Recall

(2.6)

2.4.3 Kappa

Cohen’s Kappa Statistics is another method for measuring the performance of models with using

imbalanced dataset. This metric can be calculated by using the equation 2.7. In this equation,

P0 is the total agreement probability, namely the classifier accuracy in our case calculating by

the equation 2.8 and Pc is the agreement probability due to chance[18].

The Kappa metrics has a range between -1 and 1. When k is equal to 0, it means the per-

formance of model is equal to random chance. And 1 or -1 indicates perfect agreement or

disagreement. Therefore, the higher the kappa is, the better the model is in analyzing imbal-

anced data.

2.4. Evaluation metrics 17

k =P0 − Pc

1− Pc

(2.7)

P0 =n∑

n=1

P (xnn) (2.8)

P1 =n∑

n=1

P (xn.)P (x.n) (2.9)

2.4.4 ROC and AUC

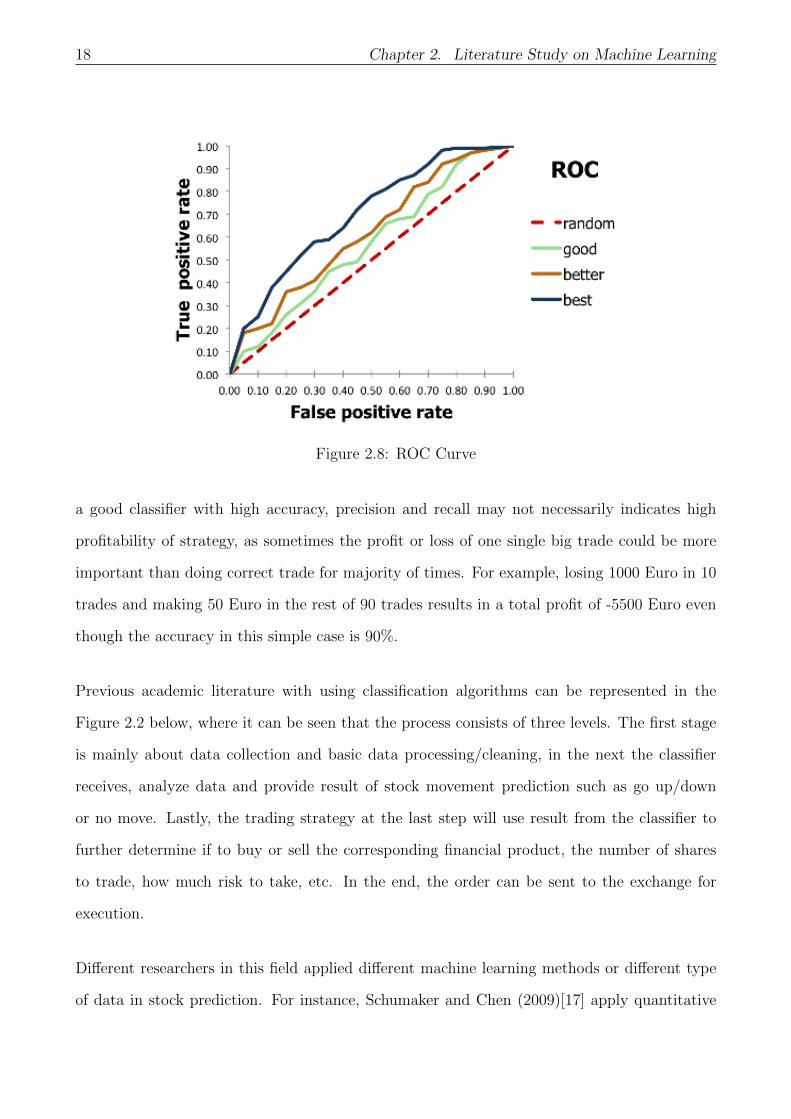

Receiver Operating Characteristic (ROC) curve is the third option for comparing the perfor-

mance of imbalanced data. The figure 2.2 below shows an example of ROC curve where the

x-axis is recall or false positive rate and the y-axis is the true positive rate.

As indicated in the plot, the best classifier is the one near the top left corner with small false

positive rate and large true positive rate. And the one on diagonal is purely random classifier.

The Area Under the ROC Curve (AUC) can be calculated by integrating the ROC curve, for

example, the top left one will have the largest AUC because the area under its curve is the

largest. And the random curve will have an area of 0.5. For those classifiers whose performance

is lower than the random one, their AUC will be lower than 0.5 as well. In most cases, AUC is

applied in binary classification problem for measuring the performance.

2.4.5 Performance of Profitability of the model

The reason for employing machine learning techniques in intraday trading is apparently simple

and direct, is to improve the overall profitability of trading strategies. Therefore, instead of

focusing on the statistical metric for evaluation, it is also necessary to check the effect of machine

learning application on the profitability of our algorithmic trading strategy, precisely to what

extent the filter of classifiers can improve the profitability.

Conducting the profitability analysis is necessary in this research, mainly due to the fact that

18 Chapter 2. Literature Study on Machine Learning

Figure 2.8: ROC Curve

a good classifier with high accuracy, precision and recall may not necessarily indicates high

profitability of strategy, as sometimes the profit or loss of one single big trade could be more

important than doing correct trade for majority of times. For example, losing 1000 Euro in 10

trades and making 50 Euro in the rest of 90 trades results in a total profit of -5500 Euro even

though the accuracy in this simple case is 90%.

Previous academic literature with using classification algorithms can be represented in the

Figure 2.2 below, where it can be seen that the process consists of three levels. The first stage

is mainly about data collection and basic data processing/cleaning, in the next the classifier

receives, analyze data and provide result of stock movement prediction such as go up/down

or no move. Lastly, the trading strategy at the last step will use result from the classifier to

further determine if to buy or sell the corresponding financial product, the number of shares

to trade, how much risk to take, etc. In the end, the order can be sent to the exchange for

execution.

Different researchers in this field applied different machine learning methods or different type

of data in stock prediction. For instance, Schumaker and Chen (2009)[17] apply quantitative

2.4. Evaluation metrics 19

Figure 2.9: General Trading Structure/Process

methods based on financial news for stock movement prediction, the general ideas of them is

to automatically follow the signal of model, namely go long at the signal of buy(going up) or

go short at the opposite signal. Furthermore, in 2010 Lamartin and Adriano[20] came up with

a new rule of “stop loss” in his research, which main purpose is to prevent losses in a single

trade from past a certain dollar amount.

The research purpose of this thesis is not to working as a separate trading strategy with

proven profitability, but to work as a filter for the current algorithmic trading strategy for

better market information analysis and trading decision making with the help of machine

learning classification algorithms. It cannot be denied that there are many aspects needed to

be considered, for instance how much to trade, how much risk to take in a position and more

importantly how to find a potential trade/arbitrage opportunity, where each of these topics are

enough for academic dissertations. In practice, an algorithmic trading strategy usually involves

many layers with each layer dealing with different type of task, such as risk management,

sometimes traders need to intervene and override the trading system as well in special extreme

cases. Therefore, the main focus of this thesis will be about building filter for the algorithmic

trading strategy by employing machine learning classifiers, in order to maximize the stability

and profitability of strategies.

20 Chapter 2. Literature Study on Machine Learning

2.5 Model Validation

Model validation is a very important part of machine learning modelling. Once a model has

been trained and built on the training dataset and the corresponding model parameters have

been optimized, the next step is to evaluate the performance of model on an unseen subset

of dataset, namely the test set. It is not appropriate or even not right to use the training set

directly for performance evaluation because the model is biased toward the training set and

thus have a relatively good performance, such as high accuracy and precision. That’s why the

unseen subset (the test set) is applied for performance evaluation of trained model.

In the following subsections, two methods of model validation for measure the performance of

classifiers will be reviewed.

2.5.1 Holdout

The holdout method can be seen as the simplest method of model validation. In this method,

the dataset is randomly split into two sets, usually known as the training set and the test set,

respectively. The size of training set is arbitrary, but in most of cases the training set is larger

than the test set with the ratio ranging from 60%-40% to 90%-10% depending on the size of

whole dataset and the underlying problem. Firstly, the model is trained on the training set

only, and then the trained model is used to predict the target value using the data in the test

set. The main advantage of this simple method for cross validation is that it is efficient and

doesn’t take longer time to compute. However, there are also several problems associated with

this method, which is necessary to be considered.

First of all, as just mentioned the dataset is separated into two parts, this method obviously

reduces the amount of data available for training the model with many observations never being

used by the model. This problem can be mostly mitigated by applying random sub-sampling.

To be precise, the method is repeated for several times in this process with different subsets in

both the training set and the test set. For measuring the performance of model, the average of

2.5. Model Validation 21

performance metrics will be computed.

In addition, there is another potential problem by using the holdout method. The evaluation

metric may heavily depend on distribution of data points end up in both training and test set,

which means the output of evaluation may be significantly different depending on how the split

of dataset is done. For instance, Liu[23] and Steinbach[24] mention in their research that for the

binary class problem if one class dominates in the training set while another class dominates

the test set, the model performance can be not that useful. It is necessary to pay attention to

this problem, because it may happen in our dataset as the financial market is dynamic. Some

methods can be used to deal with this issue, for example, imbalanced processing methods.

Figure 2.10: Holdout Validation

2.5.2 K-fold Cross-Validation

K-fold cross validation is like an enhanced version of the holdout method. To be exact, K-fold

cross validation is the process of dividing the dataset set into K-equal subsets and repeating the

holdout method for K times. At each repeat, the model is trained by using k-1 subset (forming

together) and then test on the remaining one subset, which make sure that each subset is used

as a test set once. The total error is the sum of error obtained in each run, and the performance

metrics such as accuracy and precision can be computed as the average of corresponding values

during all k run[24].

This method can be alleviated mostly from the effect of how the class is distributed in each

22 Chapter 2. Literature Study on Machine Learning

subset as discussed in the holdout method, because in this case every single observation will

be the distributed the same, namely in the training set k-1 times and in the test set exactly

once. Furthermore, as the number of repeating times K goes up, the variance of estimate will

be reduced.

On the other hand, as the process repeat for k times, the model will also be trained on the

different combination of subsets for k times, which indicates it may take K times longer than

the computing time of the holdout methods.

Figure 2.11: Process of 10-fold Cross Validation

2.6 Summary

This chapter presents the application of machine learning with a focus on supervised classi-

fication algorithms in different aspects, and explain how these techniques can be used later

chapter. In addition, the evaluation method for comparing the performance of classifier is also

examined statistically, such as precision and recall.

As stated previously, the main aim of this research is not to work as a separate trading strategy,

but instead to provide prediction for profit margin and market movement direction by using

2.6. Summary 23

machine learning algorithms, which can improve the ability of trading strategy of better market

information processing and trading decision making. As a result, the effect of classifiers (working

as filter) on the profitability of trading strategy will also be compared in term of Profit and

Loss (PnL).

Lastly, this chapter presents two approaches for model validation, namely the holdout meth-

ods and the k-fold cross validation by giving the description about how it works and their

corresponding advantages and disadvantages in model testing.

Chapter 3

Project Design and Data Engineering

3.1 Project Description

As mentioned previously, the main purpose of this project is to create an in-built filter inside

our trading system based on machine learning classifiers to enhance the overall profitability

of the algorithmic trading strategies that currently operating in ATG, in term of improving

intraday market information analysis and systematic trading decision making.

The architecture of this in-built filter plays a very important role in the system. Since the need

from trading strategies are different, the filter is therefore separated into two layers in order to

better meet the requirement from strategies and improve the efficiency of whole trading system,

where some of strategies use both two layers and some use the first layer only. However, for

the academic purpose, this paper focus on the two-layer architecture and thus use the strategy

in the need of two layers for testing and performance comparison. More details regarding the

architecture will be given in the following section 3.2.

With regards to the trading dataset, it is originally from the Japanese Exchange Market-Nikkei

with duration of 1 year from 11/2015 to 11/2016. The dataset has two types of data group

with in total of 1852154 observations where each observation is a single trade. The first group

of data contains around 20 intraday market features that can be used for classification of each

24

3.2. Architecture of the Filter 25

instance (trade), such as moving average in recent short period. In another group, there are

several trade execution related variables, like trade price and trading quantity, which is mainly

used to calculate the corresponding profit and loss (PnL) of one trade, and further determine

and compute the target variable for this research. However, for confidential reasons, it’s not

possible and not allowed to provide any information including definition regarding some of the

market features that used in this research project. In the section 3.3, more details about the

dataset and further data engineering will presented.

Lastly, in the section 3.4, there is a short discussion regarding the trade-off between performance

(i.e. accuracy) and efficiency (time/speed) of the algorithm[25], especially in the case of trading.

Typically, the more complicated the model is, the more time it takes to compute results, the

better results it can achieve. But in high or medium frequency trading (HFT), speed does play

a very important role which the less time the system spends on making decision, the higher

possibility for the strategy to seize the opportunity. If it takes too long, it will miss the chance

although the prediction or decision is correct. Hence, it is very importance to find a balance

between performance and efficiency.

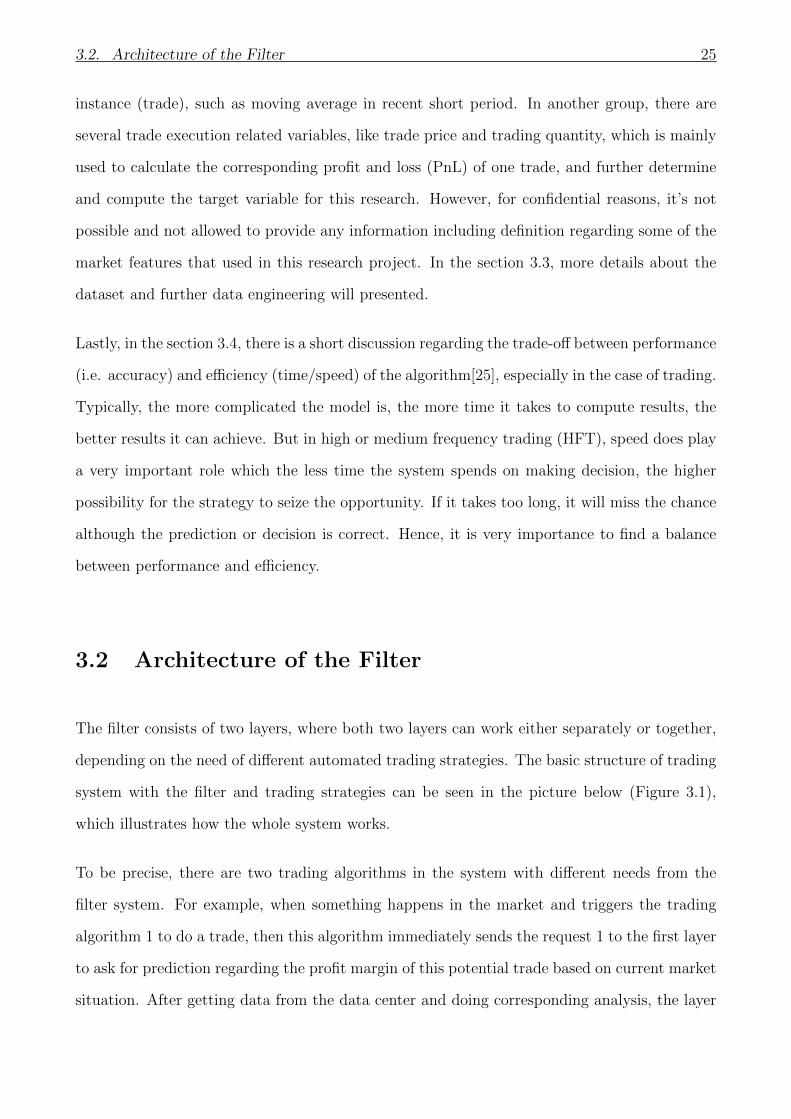

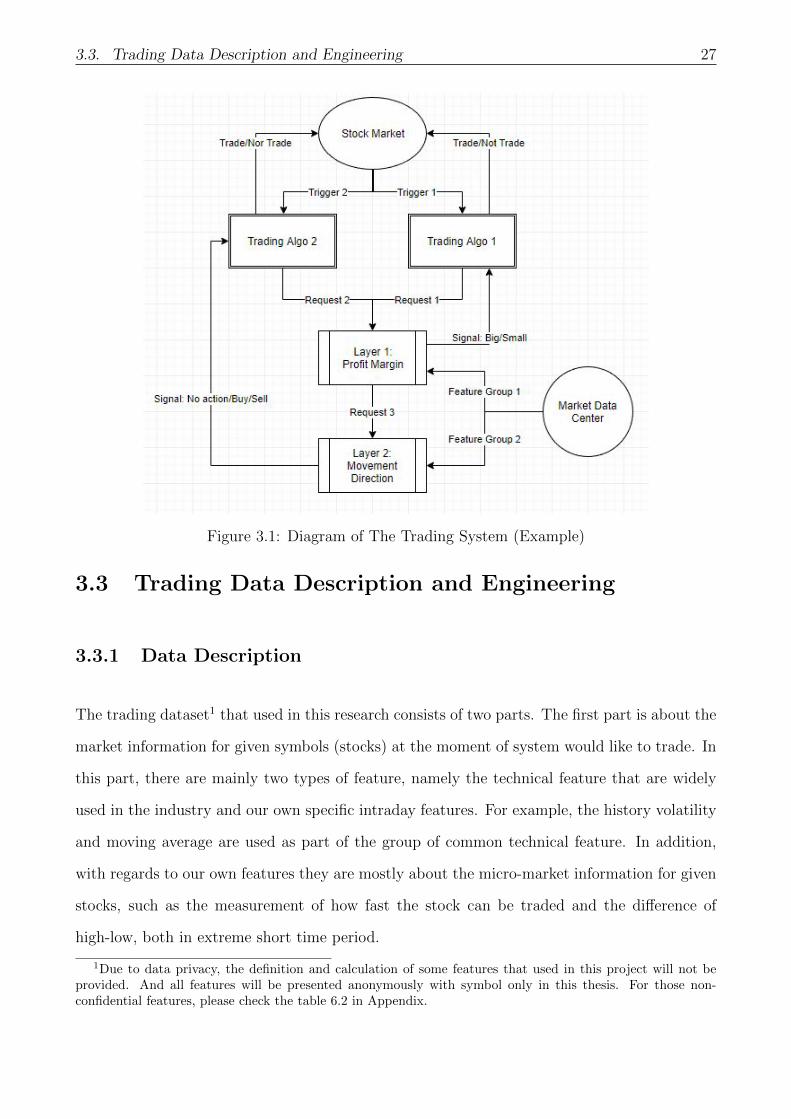

3.2 Architecture of the Filter

The filter consists of two layers, where both two layers can work either separately or together,

depending on the need of different automated trading strategies. The basic structure of trading

system with the filter and trading strategies can be seen in the picture below (Figure 3.1),

which illustrates how the whole system works.

To be precise, there are two trading algorithms in the system with different needs from the

filter system. For example, when something happens in the market and triggers the trading

algorithm 1 to do a trade, then this algorithm immediately sends the request 1 to the first layer

to ask for prediction regarding the profit margin of this potential trade based on current market

situation. After getting data from the data center and doing corresponding analysis, the layer

26 Chapter 3. Project Design and Data Engineering

1 generates a signal about the potential size, then send back the signal to the trading algorithm

1, and lastly the trading algorithm 2 will therefore determine whether trade or not at this

potential moment based on the signal. If the signal shows a big profit margin, the trading algo

1 will thus participate in this trade. In fact, the majority of trading algorithms that currently

running in the system only require information from the first layer, for the purpose of excluding

small trade with low level of potential profit margin.

However, the work structure is bit different for trading algorithms 2 because it requests more

information from the filter including both the profit margin and direction of market movement.

In this case, the layer 2 is employed to make forecast about market movement. To be specific,

as we can see in the plot, the layer 1 send a new request to the second layer with information

about the profit margin, then the layer 2 use the information from both the first layer and

the market data center to make corresponding prediction about movement direction. After

analysis is done, it sends back the signal, namely no action/buy/sell, to the trading algorithm

2. Again, based on the outcome of signal the trading algo 2 will determine if to do a trade

or not, and the direction of trade, short or long. For instance, if at the first layer the profit

margin is predicted as small, the layer 2 will directly send a signal of no action to the trading

algo 2 and thus no order will be sent out. On the other hand, if the profit margin is identified

as big, the layer 2 starts analysis and makes prediction regarding movement direction based on

the market situation. If the market is predicted as going down, the layer 2 sends out a signal

of sell to the trading algo 2, and as a result the algo 2 will send a buy order to the market.

As said previously, this diagram of trading system is not the full version because it doesn’t

include other parts, such as the risk management and post trade analysis. That is to say,

this filter with two layers is more or less working as an advisor for the trading algorithm,

which provides suggestions about the potential trade based on market information and gives

corresponding signal to the algorithms. Again, for the purpose of testing the performance of

two layers, a trading strategy similar to the trading algorithm 1 in the diagram is used in

following research.

3.3. Trading Data Description and Engineering 27

Figure 3.1: Diagram of The Trading System (Example)

3.3 Trading Data Description and Engineering

3.3.1 Data Description

The trading dataset1 that used in this research consists of two parts. The first part is about the

market information for given symbols (stocks) at the moment of system would like to trade. In

this part, there are mainly two types of feature, namely the technical feature that are widely

used in the industry and our own specific intraday features. For example, the history volatility

and moving average are used as part of the group of common technical feature. In addition,

with regards to our own features they are mostly about the micro-market information for given

stocks, such as the measurement of how fast the stock can be traded and the difference of

high-low, both in extreme short time period.

1Due to data privacy, the definition and calculation of some features that used in this project will not beprovided. And all features will be presented anonymously with symbol only in this thesis. For those non-confidential features, please check the table 6.2 in Appendix.

28 Chapter 3. Project Design and Data Engineering

The second part is trade execution data such as trading price including buy and sell price,

trading quantity and holding time, which is the output from the backtesting of trading strategy

that used for checking and comparing the performance of machine learning classifiers.

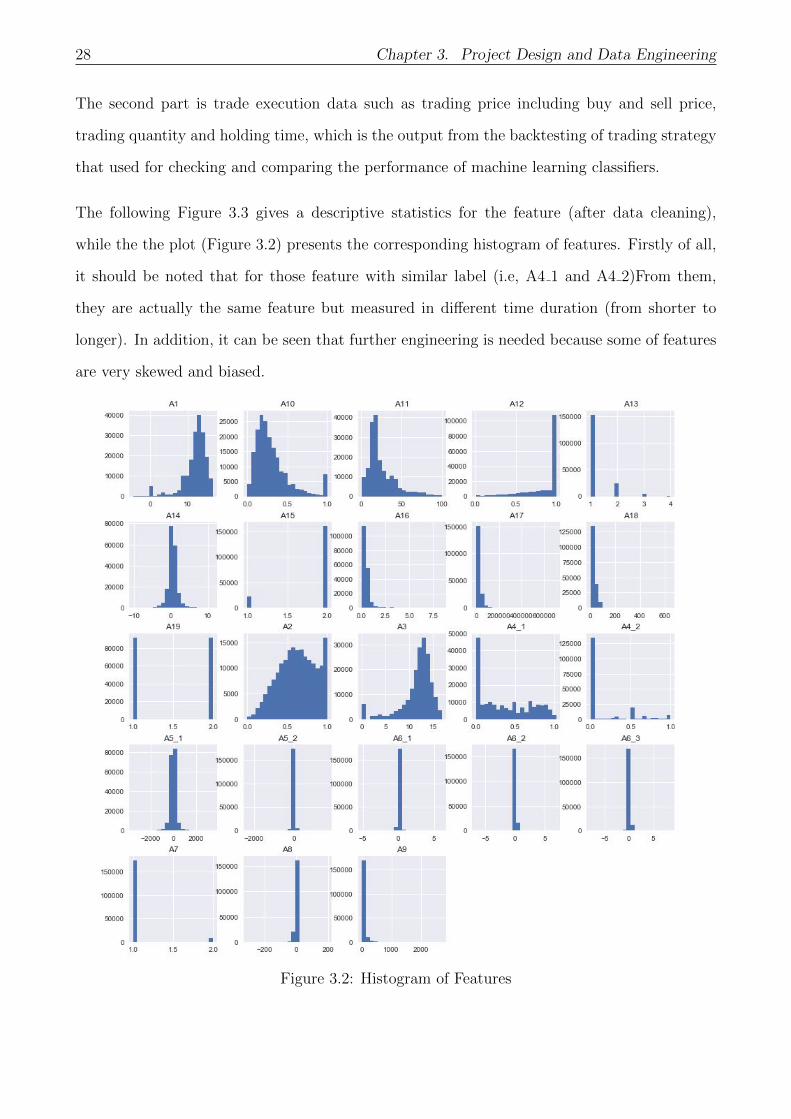

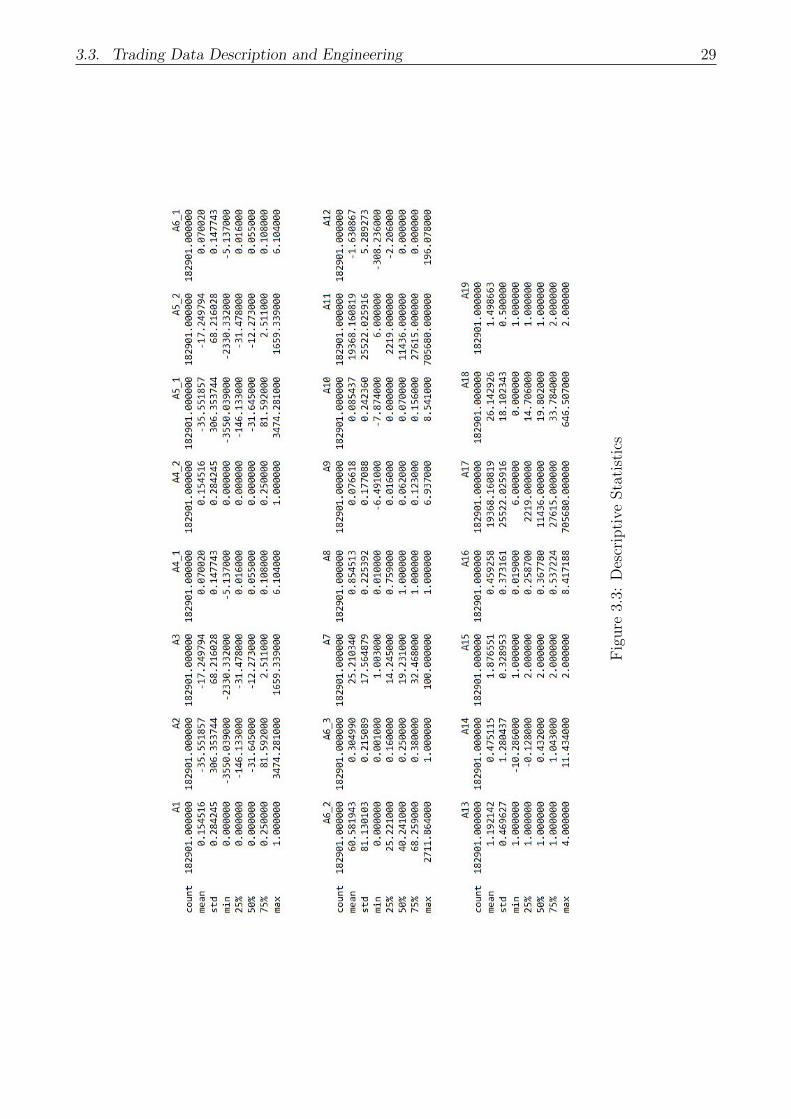

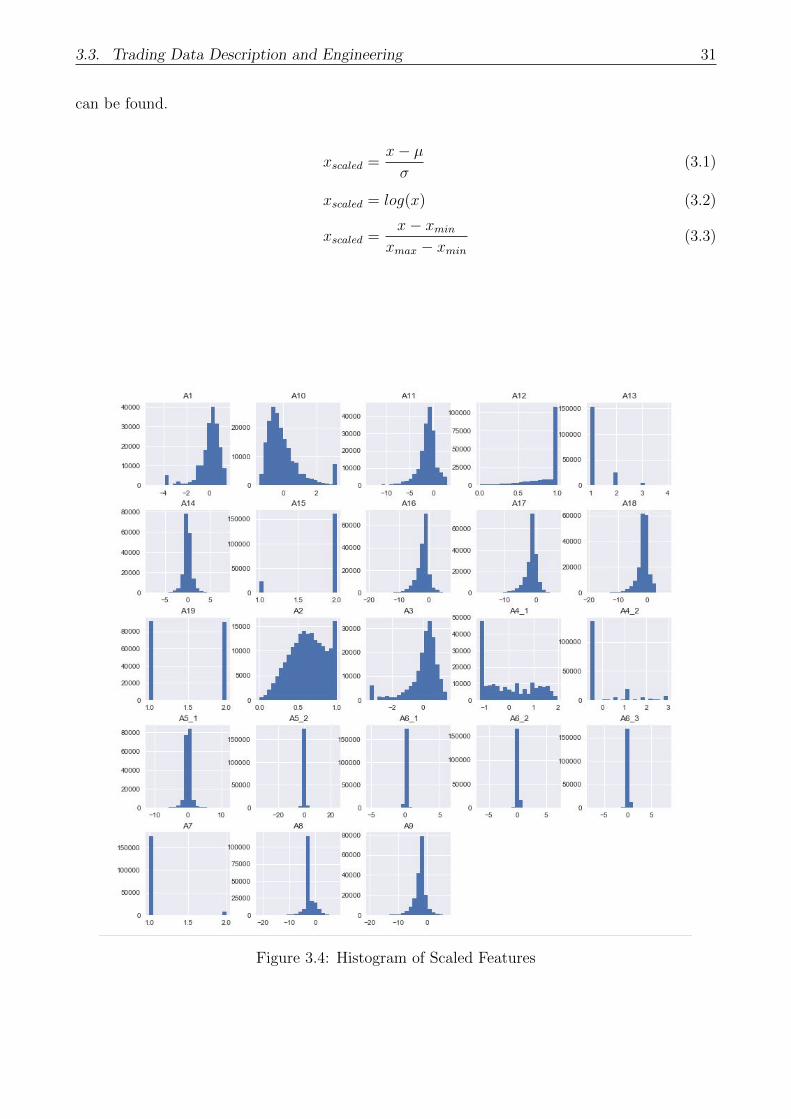

The following Figure 3.3 gives a descriptive statistics for the feature (after data cleaning),

while the the plot (Figure 3.2) presents the corresponding histogram of features. Firstly of all,

it should be noted that for those feature with similar label (i.e, A4 1 and A4 2)From them,

they are actually the same feature but measured in different time duration (from shorter to

longer). In addition, it can be seen that further engineering is needed because some of features

are very skewed and biased.

Figure 3.2: Histogram of Features

3.3. Trading Data Description and Engineering 29

Fig

ure

3.3:

Des

crip

tive

Sta

tist

ics

30 Chapter 3. Project Design and Data Engineering

3.3.2 Data Pre-Processing

Data pre-processing is a very important process before modelling, because it prepares the

data, make it ready for use in a machine learning model and thus make the model more

robust. Although recent development in technology has made the trading data more reliable

comparing to the past, pre-processing is still a necessary step before doing further statistical

analysis because it can guarantee the integrity of the machine learning model built. In general,

data-reprocessing has two main tasks, namely data cleaning and data transformation[27].

After data cleaning by removing invalid observations(values), the total number of observation in

the dataset decreases from 1852154 to 182901 as showed in the descriptive picture above. Then

the next step is data transformation, as it can be found that some of features have different

and relatively large scale.

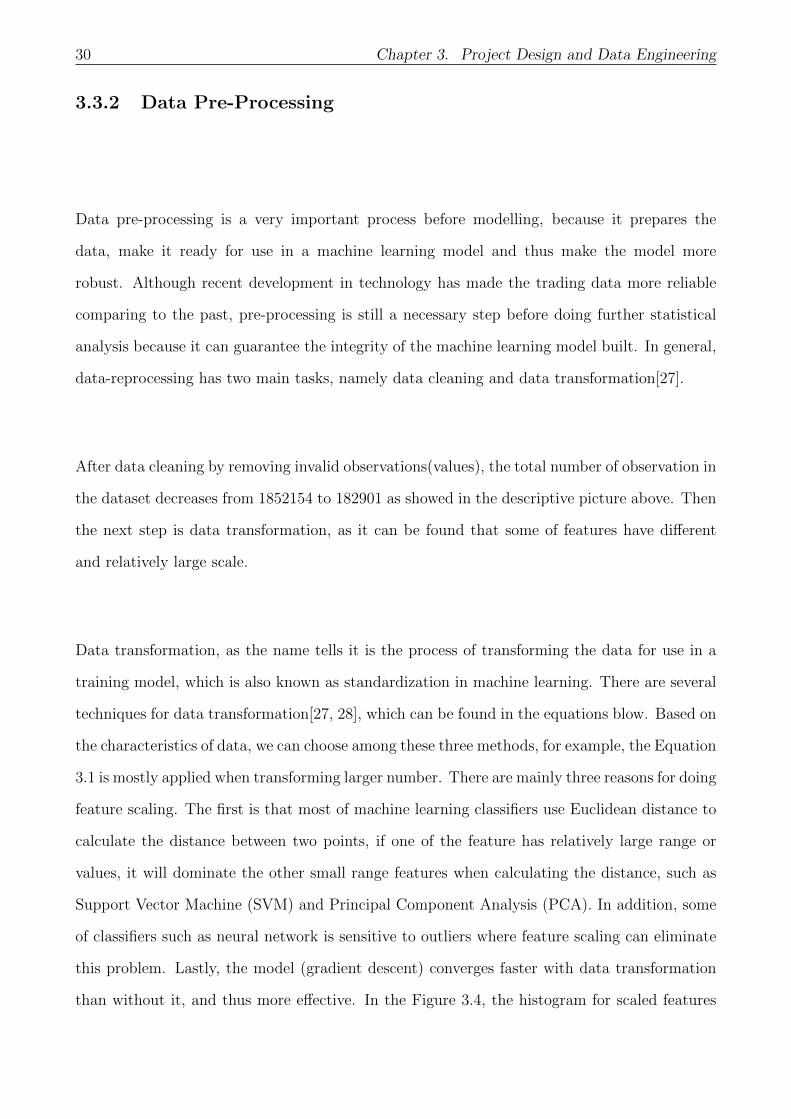

Data transformation, as the name tells it is the process of transforming the data for use in a

training model, which is also known as standardization in machine learning. There are several

techniques for data transformation[27, 28], which can be found in the equations blow. Based on

the characteristics of data, we can choose among these three methods, for example, the Equation

3.1 is mostly applied when transforming larger number. There are mainly three reasons for doing

feature scaling. The first is that most of machine learning classifiers use Euclidean distance to

calculate the distance between two points, if one of the feature has relatively large range or

values, it will dominate the other small range features when calculating the distance, such as

Support Vector Machine (SVM) and Principal Component Analysis (PCA). In addition, some

of classifiers such as neural network is sensitive to outliers where feature scaling can eliminate

this problem. Lastly, the model (gradient descent) converges faster with data transformation

than without it, and thus more effective. In the Figure 3.4, the histogram for scaled features

3.3. Trading Data Description and Engineering 31

can be found.

xscaled =x− µσ

(3.1)

xscaled = log(x) (3.2)

xscaled =x− xmin

xmax − xmin

(3.3)

Figure 3.4: Histogram of Scaled Features

32 Chapter 3. Project Design and Data Engineering

3.3.3 Feature Engineering

Target Variable

As stated previously in chapter 2, the supervised learning algorithm is used in this research

which indicates it is a must to define the target variable. The purpose of two layers in the filter

system is different where the first layer is used to forecast the profit margin of potential trade

in short term while the second layer is to determine the direction of short-term movement of

stock. Hence, we can define the target variable for two layers as follows.

When talking about the stock movement, traders are most interested in the big movement be-

cause big movements can possibly lead to high profit margin while small movements sometimes

cannot even cover the cost, i.e. transaction costs. Therefore, what the first layer is a binary

classifier, to predict the profit margin (size) of a potential trade that the strategy wants to do.

For the computation and measurement of the size, the basis point (BPS) is employed and 1

BPS is equal to 0.01%. The stock price difference in short time term is used and computed

to get percentage change in BPS. According to characteristics of the testing strategy and the

market rule of Nikkei, 30 BPS is defined as the threshold which means for those trades with

more than 30 BPS potential profit margin they are regarded as big trades, labeled as 1. And

for those small trades with profit margin smaller than 30 BPS, it is labeled as 0. Lastly, from

the backtesting results there is one interesting fact that around 80% percent of total profits

come from these big trades we selected, which accounts for 25% of the total number of trades.

This finding is sort of consistent with the famous Pareto principle (also known as 80/20 rule),

which states that for many events, roughly 80% of the effects come from 20% of the causes.

As to the direction of movement, it is then relatively easier. If the price goes down in short

time term we then define it as go short because this is the way to make profit. If it goes up,

then direction is go long. However, there is one need to be added, as we are only interested in

the big movements, so for those small trades that defined in the first layer, no action is taken.

Therefore, there are three classes for the target variable direction, namely go long (1), go short

3.3. Trading Data Description and Engineering 33

(2) and no action (0).

Figure 3.5: Histogram of Target Variables

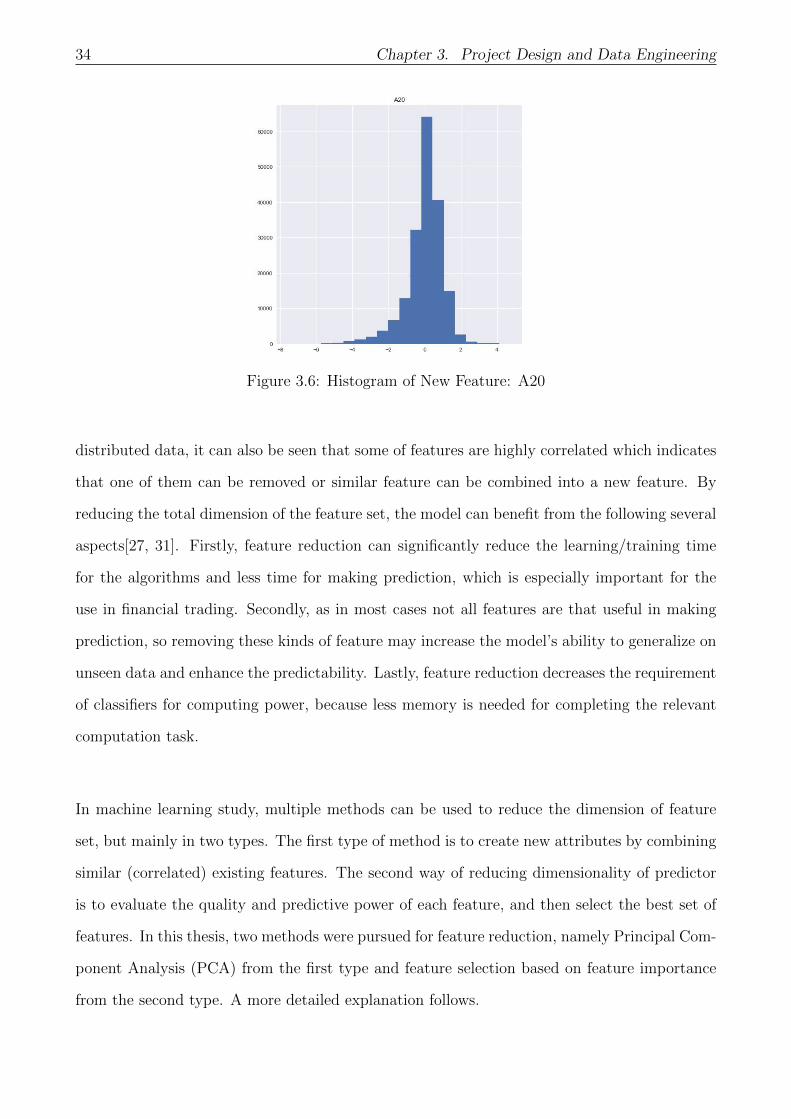

New Attribute

Anything that happens in the market can possibly lead to a change in the stock price, so is

our trade. Therefore, a new feature (A20) is created and added to the input feature set which

measures the relative size of our potential order comparing to open orders in the order book.

For the corresponding histogram, please see Figure 3.6.

3.3.4 Feature Reduction

In this research, there are in total 24 features, but distributed in two groups with one features

in common. The group 1 is used for the first layer with in total of 19 features, while group 2

for the second layer has 6 features only. Therefore, for the first layer there is a potential need

for feature reduction. Since each feature adds another one more dimension to the search space

for the model, the higher the dimension the harder the problem to solve. In addition, from

the correlation plot based on the Spearman Rank Test[30] which is applied on non-normally

34 Chapter 3. Project Design and Data Engineering

Figure 3.6: Histogram of New Feature: A20

distributed data, it can also be seen that some of features are highly correlated which indicates

that one of them can be removed or similar feature can be combined into a new feature. By

reducing the total dimension of the feature set, the model can benefit from the following several

aspects[27, 31]. Firstly, feature reduction can significantly reduce the learning/training time

for the algorithms and less time for making prediction, which is especially important for the

use in financial trading. Secondly, as in most cases not all features are that useful in making

prediction, so removing these kinds of feature may increase the model’s ability to generalize on

unseen data and enhance the predictability. Lastly, feature reduction decreases the requirement

of classifiers for computing power, because less memory is needed for completing the relevant

computation task.

In machine learning study, multiple methods can be used to reduce the dimension of feature

set, but mainly in two types. The first type of method is to create new attributes by combining

similar (correlated) existing features. The second way of reducing dimensionality of predictor

is to evaluate the quality and predictive power of each feature, and then select the best set of

features. In this thesis, two methods were pursued for feature reduction, namely Principal Com-

ponent Analysis (PCA) from the first type and feature selection based on feature importance

from the second type. A more detailed explanation follows.

3.3. Trading Data Description and Engineering 35

Figure 3.7: Correlations Plot

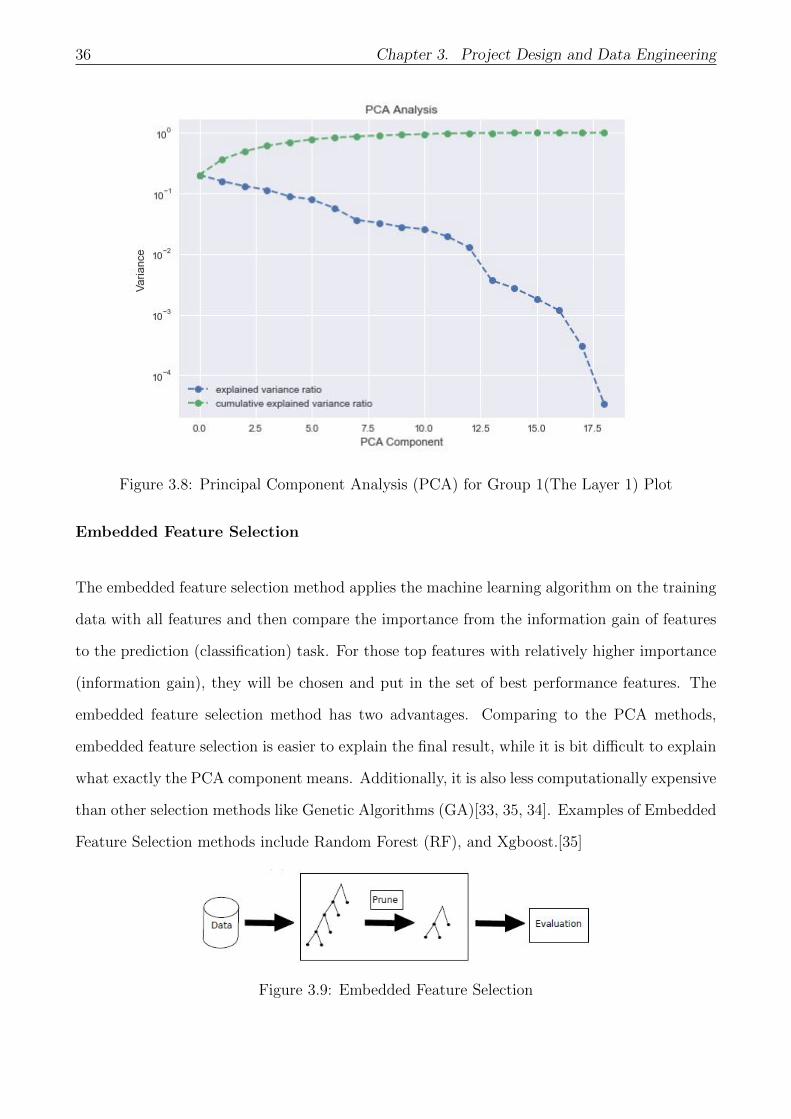

Principal Component Analysis

Principal component analysis (PCA) is a statistical process of converting correlated dataset with

high dimensionality into a dataset of linearly uncorrelated principal components (data) with

lower dimensionality, by implementing an orthogonal transformation[32]. The main purpose

of doing PCA is to reduce the feature dimensionality with keeping as much of information as

possible.

With help of Python Library Sklearn, the following plot is made which explains the relationship

between the number of principal components and (cumulative) variance. By having a look at

the explained variance ratio and its cumulative version, it can be seen that the slope of explained

variance curve drop quickly after 9 components where the corresponding cumulative explained

variance is equal to 90.46%. Therefore, by keeping 9 principal components, around 90% of the

full variance can be explained.

On the other hand, by reducing the size of input space from 19 to 9, which is more than half,

less than 10% of potential information is compromised but may improve the efficiency of model.

36 Chapter 3. Project Design and Data Engineering

Figure 3.8: Principal Component Analysis (PCA) for Group 1(The Layer 1) Plot

Embedded Feature Selection

The embedded feature selection method applies the machine learning algorithm on the training

data with all features and then compare the importance from the information gain of features

to the prediction (classification) task. For those top features with relatively higher importance

(information gain), they will be chosen and put in the set of best performance features. The

embedded feature selection method has two advantages. Comparing to the PCA methods,

embedded feature selection is easier to explain the final result, while it is bit difficult to explain

what exactly the PCA component means. Additionally, it is also less computationally expensive

than other selection methods like Genetic Algorithms (GA)[33, 35, 34]. Examples of Embedded

Feature Selection methods include Random Forest (RF), and Xgboost.[35]

Figure 3.9: Embedded Feature Selection

3.3. Trading Data Description and Engineering 37

3.3.5 Imbalanced Data and Solutions

As can be seen in the Figure 3.5, it is normal to have the class imbalance problem in trading

datasets with more observations of a certain class than the others, i.e. much more small trades

than big trades in term of the profit margin. In general, a machine learning classifier may

have a bias with regards to the majority class and thus identify the minority class wrongly by

training the classifier on imbalanced datasets. This is mainly because identifying the majority

class is in favor of improving accuracy, thus the classifier misclassifies the minority class as

the majority class more often[36]. In the case of dealing with highly imbalanced dataset (i.e

99% majority/ 1% minority), the classifier may obtain a very high accuracy by ignoring and

misclassifying the minority class. This would be a problem for the research if the minority class

is of particular interest.

As to stock trading, traders/trading algorithms are interested in the large movements with

high level of profit margin in which the big movements are mostly the minority class. In order

to improve the performance of identifying the minority class of big trades, certain procedures

need to be taken to deal with imbalanced problem in the training dataset. There are two

types of approaches that can be applied to overcome the issue of imbalance problem, namely

undersampling and oversampling, depending on the size of training set.

To be precise, when the size of dataset is not big, or the number of observation is not that

sufficient, the oversampling method is used to increase the observation of minority class by

using techniques such as random oversampling and Synthetic Minority Oversampling Technique

(SMOTE)[37]. On the contrary, undersampling method balance the ratio between the majority

class and the minority class in the dataset by removing the instance of the abundant class, which

is especially useful when quantity of data is sufficient. There are several techniques in removing

the sample in majority class, for example, Edited Nearest Neighbours Rule[38], neighbourhood

cleaning rule[39], one-sided selection method[40] and removing Tomeks links[41]. In addition,

there is also a hybrid approach that combines oversampling and undersampling together. For

instance, the SMOTEENN method is to perform oversampling using SMOTE and follow by

38 Chapter 3. Project Design and Data Engineering

under-sampling using the Edited Nearest Neighbours[42]. In both two approaches mentioned

above, by either removing the observation in the majority class or increasing the instance of

minority class, a new balanced dataset can be obtained for further training and modelling.

However, in this project, there is a preference for undersampling method over the oversampling

for several reasons. Firstly, the undersampling method is in favor because the size of training

set is sufficiently large for training the model. Secondly, since there is high requirement for

the efficiency of classifiers which will be discussed in the next session, the undersampling is

preferred since it reduces the size of training set by removing the abundant instance in the

majority class and thus saves training time.

The distribution of the target Profit Marin-Size after resampling with methods mentioned above

is presented in the plot below (Figure 3.8 and Figure 3.9), for both data with all features and

data after PCA feature reduction. From the histogram, it can be seen that in oversampling case

the total number of minority grows equally to the majority case, while in the undersampling

and combined method plot the number of majority only drops slightly.

(a) Oversampling Method: SMOTE

(b) Undersampling Method: EditedNearest Neighbours

Figure 3.10: Histogram of Target Variable-Size after over-/under-sampling.

3.4. Performance and Efficiency 39

Figure 3.11: Histogram with SMOTENN re-sampling method

3.4 Performance and Efficiency

As mentioned in the beginning of this paper, the filter system would be little or even no value

for trading algorithm or trader if it takes a long time to obtain corresponding prediction. For

example, it doesn’t make any sense if the filter spends 1 minute to predict the price movement

30 seconds in the future, no matter whether the prediction is right or not. Due to the extreme

limited time for seizing the trading opportunity in the market and the tremendous amounts

of market data for processing, there is a super hard requirement for the filter to be as much

efficient as possible. Additionally, because of the dynamic change in the market, it is also highly

necessary or even compulsory to the learning algorithm in the filter regularly.

The trade-off between the the performance of algorithm and efficiency has been widely dis-

cussed in studies [25]. It is generally true that the more complicated the model is, the more

learning/training time it spends, the better performance it can obtain. For example, the en-

semble methods usually obtain better performance than single classifiers, because the ensemble

methods combine the result of multiple classifiers and takes very long training time. Similarly,

more training data generally leads to better performance of the model as well because the model

40 Chapter 3. Project Design and Data Engineering

have more data to learn the pattern or relationship inside the dataset. However, there is also a

point such that more data (those old data) cannot lead to a better performance of the model,

especially in the study of finance[43], because the predictability in the financial market may

disappear, and the market may constantly evolve.

Increasing the complexity of models does not necessarily improve performance, but on the other

hand negatively affect the efficiency of model. As a result, for this research, the most important

thing is to find a balance point between model efficiency and model performance, instead of

pursuing extreme high performance of the model.

Chapter 4

Experiments and Outputs

The chapter 2 gives a framework of how the machine learning techniques can be applied in

financial prediction (classification) problem, which mainly includes descriptions of different

classification algorithms in machine learning, performance evaluation by using statistical per-

formance metrics and profitability analysis, and lastly model validation/testing with help of the

holdout method and k-fold cross-validation. The first part chapter 3 presents an introduction

to the framework of filters and their connections with trading algorithms and other parts in the

trading system. The rest of chapter 3 mainly focuses on the data engineering process which

should be done before training the model including data cleaning and standardization, feature

engineering such as defining and calculating the target variable and creating new attributes,

feature reduction by using principal component analysis(PCA) & embedded feature selection

method and the imbalanced data processing.

In this chapter, the purpose is to present the experiment performance of the classification

filter on the test dataset with respect to different algorithms and different data engineering

methodologies. To make it clearer to understand the whole architecture of the filter system,

the outputs is presented in the following order. In the beginning, results correspond to the first

layer with purpose of identifying the size of potential profit margin will be given. Secondly, the

test performance of the layer-2 for predicting the direction of market movement will be showed.

41

42 Chapter 4. Experiments and Outputs

Lastly, as the main idea of this project is to connect two layers together to improve the overall

profitability of trading strategy, the experiment outcomes of combined system are of interest,

in term of statistical performance and the profitability.

4.1 Layer 1: Profit Margin Prediction

The first layer is regarded as the most important filter in the trading system, as it not only

serves all running trading strategies in the system but also generates information/signal for

the second layer. The main aim of this layer is to build a classification model for predicting

whether the profit margin of a potential trade is big or not, by using market information such

as 10-minutes trading volumes. As to the target variable, it is defined as follows; if the profit

margin is larger than 30 BPS, it is then labeled as big trades otherwise small.

The experiment outputs for this classifier will be separated into two main parts, with or with-

out using imbalanced data. In each part, the outputs correspond to different classification

algorithms and different features set will be presented.

4.1.1 Imbalanced Data

All Features: Scaled Data

In this part, the scaled dataset with all features will be used for training and testing. From the

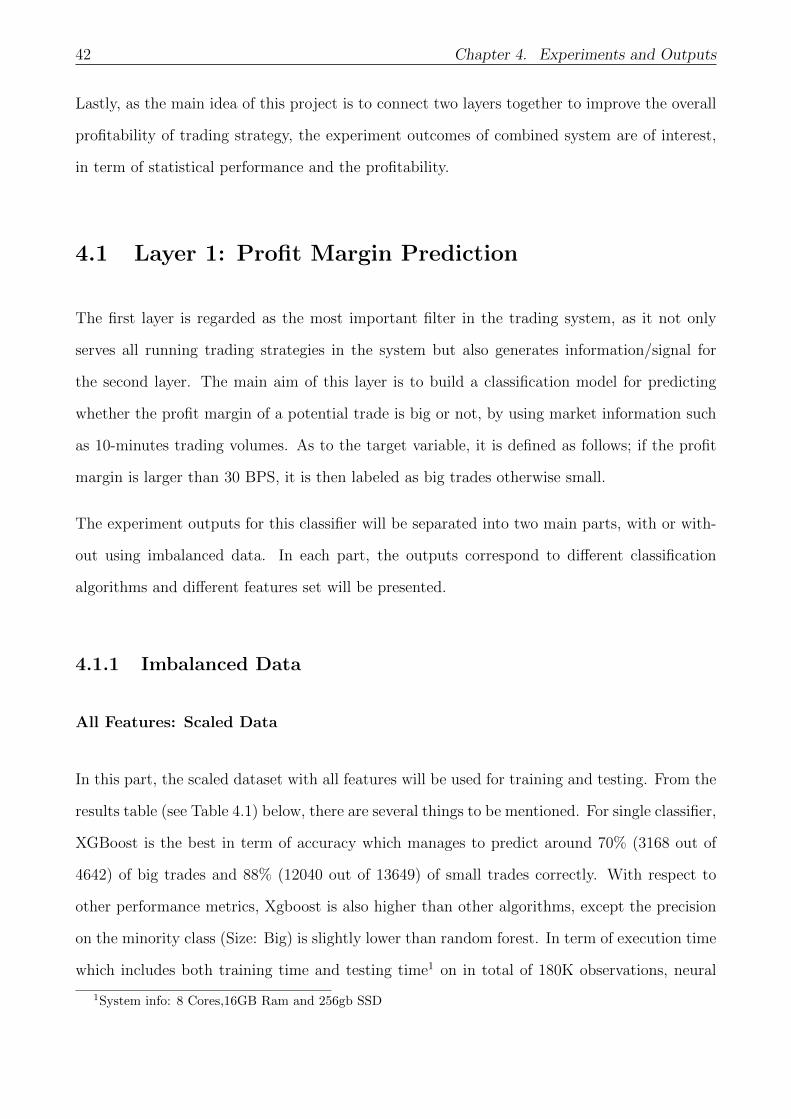

results table (see Table 4.1) below, there are several things to be mentioned. For single classifier,

XGBoost is the best in term of accuracy which manages to predict around 70% (3168 out of

4642) of big trades and 88% (12040 out of 13649) of small trades correctly. With respect to

other performance metrics, Xgboost is also higher than other algorithms, except the precision

on the minority class (Size: Big) is slightly lower than random forest. In term of execution time

which includes both training time and testing time1 on in total of 180K observations, neural

1System info: 8 Cores,16GB Ram and 256gb SSD

4.1. Layer 1: Profit Margin Prediction 43