Embed Size (px)

DESCRIPTION

Lecture Notes for Macro 2 2001 (first year PhD course in Stockholm), by Paul Söderlind

Citation preview

Lecture Notes for Macro 2 2001 (first year PhDcourse in Stockholm)

Paul Soderlind1

June 2001 (some typos corrected later)

1University of St. Gallen and CEPR. Address: s/bf-HSG, Rosenbergstrasse 52, CH-9000 St.Gallen, Switzerland. E-mail: [email protected]. Document name: MacAll.TeX.

Contents

1 Money Demand (and some Supply) 41.1 Money Supply . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41.2 Overview of Money Demand . . . . . . . . . . . . . . . . . . . . . . 41.3 Money Demand: A General Equilibrium Model with Money in the

Utility Function . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71.4 The Mechanics of Money Supply∗ . . . . . . . . . . . . . . . . . . . 16

2 The Price of Money 242.1 UIP, Fisher Equation, and the Expectations Hypothesis of the Yield

Curve . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 242.2 The Price Level as an Asset Price: Cagan’s (1956) Model with Ratio-

nal Expectations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 252.3 A Simple Model of Exchange Rate Determination . . . . . . . . . . . 31

A Derivations of the Pricing Relations 38A.1 A Real Bond . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40A.2 A Nominal Bond . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40A.3 A Nominal Foreign Bond . . . . . . . . . . . . . . . . . . . . . . . . 41A.4 Real Effects of Money? . . . . . . . . . . . . . . . . . . . . . . . . . 41A.5 Empirical Evidence on the Pricing Relations . . . . . . . . . . . . . . 42

3 Money and Sticky Prices: A First Look 453.1 Basic Models of the Effects of Monetary Policy Surprises . . . . . . . 453.2 “Money and Wage Contracts in an Optimizing Model of the Business

Cycle,” by Benassy . . . . . . . . . . . . . . . . . . . . . . . . . . . 463.3 “Money and the Business Cycle,” by Cooley and Hansen . . . . . . . 56

1

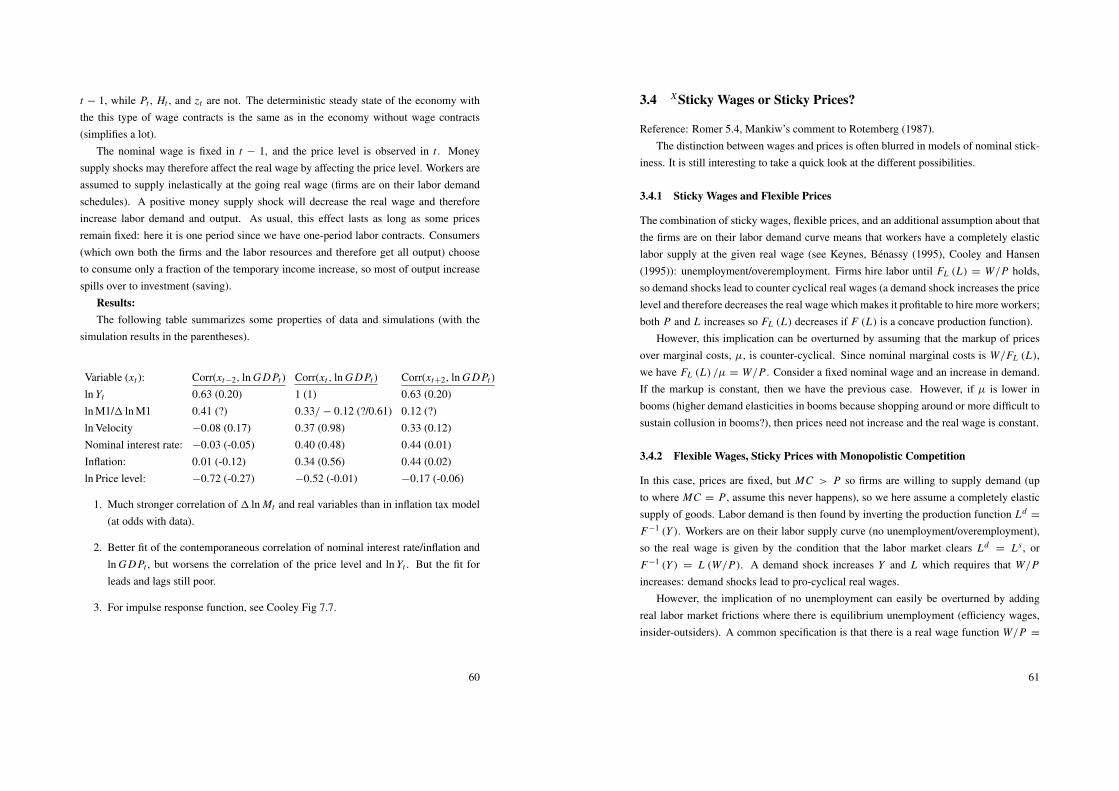

3.4 X Sticky Wages or Sticky Prices? . . . . . . . . . . . . . . . . . . . . 61

4 Money in Models of Monopolistic Competition 634.1 Monopolistic Competition . . . . . . . . . . . . . . . . . . . . . . . 63

5 Money and Price Setting 695.1 Dynamic Models of Sticky Prices . . . . . . . . . . . . . . . . . . . 695.2 Aggregation of One-Sided Ss Rule: A Counter-Example to 1M →

1Y ∗ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

A Summary of Solution Method for Linear RE Models 81A.1 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81A.2 Special Case: Scalar Second Order Equation . . . . . . . . . . . . . . 82A.3 An Alternative for the Scalar Second Order Equation: The Factoriza-

tion Method . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

B Calvo’s Model: An Alternative Derivation 85

6 Monetary Policy 886.1 The IS-LM Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 886.2 The Barro-Gordon Model . . . . . . . . . . . . . . . . . . . . . . . . 916.3 Recent Models for Studying Monetary Policy . . . . . . . . . . . . . 97

A Derivations of the Aggregate Demand Equation 104

7 Empirical Measures of the Effect of Money on Output 1067.1 Some Stylized Facts about Money, Prices, and Exchange Rates . . . . 1067.2 Early Studies of the Effect of Money on Output . . . . . . . . . . . . 1077.3 Early Monetarist Studies of the Effect of Money on Output . . . . . . 1087.4 Unanticipated or Anticipated Money∗ . . . . . . . . . . . . . . . . . 1157.5 VAR Studies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1167.6 Structural Models of Monetary Policy . . . . . . . . . . . . . . . . . 119

0 Reading List 1230.1 Money Supply and Demand . . . . . . . . . . . . . . . . . . . . . . 1230.2 Price Level and Nominal Assets . . . . . . . . . . . . . . . . . . . . 123

2

0.3 Money and Prices in RBC Models . . . . . . . . . . . . . . . . . . . 1240.4 Money and Monopolistic Competition . . . . . . . . . . . . . . . . . 1240.5 Sticky Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1250.6 Monetary Policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1250.7 Empirical Measures of the Effect of Money on Output . . . . . . . . . 1260.8 The Transmission Mechanism from Monetary Policy to Output . . . . 126

3

1 Money Demand (and some Supply)

Main references: Romer (1996) (Romer), Blanchard and Fischer (1989) (BF), Obstfeldtand Rogoff (1996) (OR), and Walsh (1998).

1.1 Money Supply

References: Burda and Wyplosz (1997) 9, OR 8.7.6 and Appendix 8B, and Mishkin(1997).

The really short version: the central bank can control either some monetary aggregateor an interest rate or the exchange rate. How they do that is typically not very importantfor most macroeconomic questions. Still, this is discussed in Section 1.4. Why they do it,that is, the monetary policy, is much more important—and something we will discuss atlength later.

1.2 Overview of Money Demand

1.2.1 Money in Macroeconomics

Roles of money: medium of exchange, unit of account, and storage of value (often domi-nated by other assets).

Money is macro model is typically identified with currency which gives no interest.The liquidity service of money ( medium of exchange) is emphasized, rather than store ofvalue or unit of account.

1.2.2 Traditional money demand equations

References: Romer 5.2, BF 4.5, OR 8.3, Burda and Wyplosz (1997) 8.The standard money demand equation

lnMt

Pt= constant + ψ ln Yt − ωit (1.1)

4

are used in many different models, for instance as the LM curve is IS-LM models. Mt in(1.1) is often a money aggregate like M1 or M3. In most of the models on this course, wewill assume that the central bank have control over this aggregate.

1.2.3 Money Demand and Monetary Policy

There are many different models for why money is used. The common feature of thesemodels is that they all generate something pretty close to (1.1). But why is this broadermoney aggregate related to the monetary base, which the central bank may control? Shortanswer: the central bank creates a demand for narrow money by forcing banks to hold it(reserve requirements) and by prohibiting private substitutes to narrow money (banks arenot allowed to print bills).

The idea behind central bank interventions is to affect the money supply. However,most central banks use short interest rates as their operating target. In effect, the centralbank has monopoly over supply over narrow money which allows it to set the short interestrate, since short debt is a very close substitute to cash. In terms of (1.1), the central bankmay set it , which for a given output and price level determines the money supply as aresidual.

1.2.4 Applied money demand equations

Reference: Goldfeld and Sichel (1990).Applied money demand equations often take the form

lnMt

Pt= b0 + b1 ln Yt + b2it + b3 ln

Mt−1

Pt−1+ b4 ln

Pt

Pt−1+ ut . (1.2)

where Mt is nominal money holdings, Pt the price level, Yt some measure of economicactivity, and it the net nominal interest rate (like 0.07). The inclusion of Mt−1/Pt−1 andPt/Pt−1 is thought to capture partial adjustment effects due to adjustment costs of eithernominal (b4 6= 0) or real money balances (b4 = 0).

For instance, the estimate for Germany (69:1-85:4) reported by Goldfeld and Sichel(1990) is {b1, b2, b3, b4} = {0.3,−0.5, 0.7,−0.7}. (They interest rate used in their esti-mation is in percentages, that is, like 7 instead of the 0.07 used here, so I have scaled theirb2 = −0.005 by 100.)

5

In general, this type of equation worked fine until 1975, overpredicted money demandduring the late 1970s, and underpredicted money demand in the early 1980s. Financialinnovations? (1.2) has been refined in various ways. Various disaggregated money mea-sures have been tried, a wealth of different interest rates and alternative costs have beenused, the income variable has been disaggregated, and fairly free adjustment models havebeen tried (error correction models). Single equation estimation of (1.2) presumes thatthis is a true demand function, with monetary authorities setting the interest rate, and withthe other right hand side variables being predetermined.

1.2.5 Different Ways to Introduce Money in Macro Models

Reference: OR 8.3 and Walsh (1998) 2.3 and 3.3.The money in the utility function (MIU) model just postulates that real money balances

enter the utility function, so the consumer’s optimization problem is

max{Ct ,Mt }

∞

t=0

∞∑t=0

β tu(

Ct ,Mt

Pt

). (1.3)

One motivation for having the real balances in the utility function is that having cash maysave time in transactions. The correct utility function would then be u

(Ct , L − Lshopping

t

),

where Lshoppingt is a decreasing function of Mt/Pt .

Cash-in-advance constraint (CIA) means that cash is needed to buy (some) goods, forinstance, consumption goods

PtCt ≤ Mt−1, (1.4)

where Mt−1 was brought over from the end of period t − 1. Without uncertainty, thisrestriction must hold with equality since cash pays no interest: no one would accumulatemore cash than strictly needed for consumption purposes since there are better investmentopportunities. In stochastic economies, this may no longer be true.

The simple CIA constraint implies that “money demand equation” does not includethe nominal interest rate. If the utility function depends on consumption only, then allrates of inflation gives the same steady state utility. This stands in sharp contrast to theMIU model, where the optimal rate of inflation is minus one times the real interest rate(to get zero nominal interest rate). However, this is not longer true if the cash-in-advanceconstraint applies only to a subset of the arguments in the utility function. For instance, if

6

we introduce leisure or credit goods.Shopping-time models typically have a utility function is terms of consumption and

leisure∞∑

s=0

βsU (Ct , 1 − lt − nt) , (1.5)

where lt is hours worked, and nt hours spent on shopping (supposed to give disutility).The latter is typically modelled as some function which is increasing in consumption anddecreasing in cash holdings

1.3 Money Demand: A General Equilibrium Model with Money inthe Utility Function

Reference: BF 4.5; OR 8.3; Walsh (1998) 2.3; and Lucas (2000)

1.3.1 Model Setup

The consumer’s optimization problem is

max{Ct ,Mt }

∞

t=0

∞∑t=0

β tu(

Ct ,Mt

Pt

)(1.6)

subject to the real budget constraint

Kt+1 +Mt

Pt= (1 + rt) Kt +

Mt−1

Pt+ wt − Ct − Tt , (1.7)

where rt is the (net) real interest rate (from investing in t − 1 and receiving the return int), and wt the real wage rate. Labor supply is normalized to one. The consumer rents hiscapital stock to competitive firms in each period. Tt denotes lump sum taxes.

Production is given by a production function with constant returns to scale

Yt = F (Kt , L t) , (1.8)

and there is perfect competition in the product and factor markets. The firms rent capitaland labor from the households and make zero profits.

I assume perfect foresight in order to simply the algebra somewhat. It is straightfor-ward to derive the same results in a stochastic setting, at least if we assume that variances

7

and covariances do not depend on the level of the other variables.

1.3.2 Optimal Consumption and Money Holdings

Use (1.7) in (1.6) to get the unconstrained problem for the consumer

max{Kt+1,Mt}

∞

t=0

∞∑t=0

β tu[(1 + rt) Kt +

Mt−1

Pt+ wt − Tt − Kt+1 −

Mt

Pt,

Mt

Pt

]. (1.9)

The first order condition for Kt+1 is

uC

(Ct ,

Mt

Pt

)= (1 + rt+1) βuC

(Ct+1,

Mt+1

Pt+1

), (1.10)

which is the traditional Euler equation for real bonds (with uncertainty we need to takethe expected value of the right hand side, conditional on the information in t). It wouldalso hold for any other financial asset.

The first order condition for Mt is

uC

(Ct ,

Mt

Pt

)= uM/P

(Ct ,

Mt

Pt

)+ βuC

(Ct+1,

Mt+1

Pt+1

)Pt

Pt+1. (1.11)

If money would not enter the utility function, then this is a special case of (1.10) since thereal gross return on money is Pt/Pt+1. It is not obvious, however, that we get an interiorsolution to money holdings unless money gives direct utility.

The left hand side of (1.11) is the marginal utility lost because some resources aretaken from time t consumption, and the right hand side is the marginal utility gained byhaving more cash today and the extra consumption this allows tomorrow (cash providesutility and is also a form of saving, whose purchasing power depends on the inflation).

Substitute for βuC (Ct+1,Mt+1/Pt+1) from (1.10) in (1.11) and rearrange to get

uC

(Ct ,

Mt

Pt

)(1 −

11 + rt+1

Pt

Pt+1

)= uM/P

(Ct ,

Mt

Pt

). (1.12)

The Fisher equation is

1 + it = Et (1 + rt+1)Pt+1

Pt, (1.13)

where the convention is that the nominal interest rate is dated t since it is known as of t .

8

Under perfect foresight, (1.12) can then be written

it

1 + it= uM/P

(Ct ,

Mt

Pt

)/uC

(Ct ,

Mt

Pt

), (1.14)

which highlights that the nominal interest rate is the relative price of the “money services”we get by holding money one period instead of consuming it. Note that (1.14) is a rela-tion between real money balances, the nominal interest rate, and an activity level (hereconsumption), which is very similar to the LM equation.

Example 1 (Explicit money demand equation from Cobb-Douglas/CRRA.) Let the utility

function be

u(

Ct ,Mt

Pt

)=

11 − γ

[Cα

t

(Mt

Pt

)1−α]1−γ

,

in which case (1.14) can be written

Mt

Pt= Ct

1 − α

α

1 + it

it,

which is decreasing in it and increasing in Ct . This is quite similar to the standard

money demand equation (1.1). Take logs and make a first-order Taylor expansion of

ln [(1 + it) / it ] around iss

lnMt

Pt= constant + ln Ct −

1iss (1 + iss)

it .

Compared with the money demand equation (1.1), ψ ln Yt is replaced by ln Ct and ω =

1/ [iss (1 + iss)]. If iss = 5%, then ω ≈ 20, which appears to be very high compared to

empirical estimates.

Example 2 (Explicit money demand equation from Lucas (2000). Let the utility function

be

u(

Ct ,Mt

Pt

)=

11 − γ

[Ct

(1 + B

Ct

Mt/Pt

)−1]1−γ

,

9

in which case (1.14) can be written

it

1 + it=

(Ct

Mt/Pt

)2

B, or

Mt

Pt= Ct B1/2

(it

1 + it

)−1/2

,

which can be written (approximately) on the same form as (1.1)

lnMt

Pt≈ constant + ln Ct −

12

it

iss (1 + iss).

This gives a value of the ω in the money demand equation (1.1) which is only half of that

in Example 1.

1.3.3 General Equilibrium with MIU

We now add a few equations to close the MIU model in a closed economy. The govern-ment budget is assumed to be in balance in every period (not restrictive since Ricardianequivalence holds in this model)

−Ts =Ms − Ms−1

Ps, (1.15)

so the seigniorage (right hand side) is distributed as lump sum transfers (negative taxes).Note that this is taken as given by each individual agent.

Competitive factor markets, constant returns to scale, and a fixed labor equal to one(recall that is was not part of the utility function) give

rt =∂F (Kt , 1)

∂K, and (1.16)

wt = F (Kt , 1)− Kt∂F (Kt , 1)

∂K.

(This follows from that w = ∂F/∂L and r = ∂F/∂K and that constant returns to scaleimplies F = L∂F/∂L + K∂F/∂K .)

In general, the price level is determined jointly with the rest of the dynamic equilib-rium. In special cases, as with log utility and complete depreciation of capital (as in themodel of Benassy (1995)) there is a closed form solution. However, in most cases, theequilibrium must be computed with numerical methods.

10

1.3.4 Steady State

Two definitions:

• Neutrality of money: the real equilibrium is independent of the money stock.

• Superneutrality of money: the real equilibrium is independent of the money growthrate.

Let the money growth rate be σ , so Mt/Mt−1 = 1 + σ . A steady state impliesthat inflation, consumption, and real money balances are constant: Pt/Pt−1 = 1 + π ,Ct/Ct−1 = 1, and (Mt/Pt) / (Mt−1/Pt−1) = 1. This implies that π = σ .

The first order condition for K , (1.10), can then be simplified as 1 + rss = 1/β.Combining with (1.16) gives that steady state capital stock must solve

FK (Kss, 1) = rss

= 1/β − 1, (1.17)

which depends only on the technology and the real discount rate, not on the money stockor growth. In steady state, the capital stock is constant so Css = F (Kss, 1), so consump-tion in steady state is uniquely determined by the real side of the economy: in the steadystate of this model, money is neutral and superneutral. Note that this is not true for thedynamics around the steady state unless marginal utility of consumption is independentof the real money balances (see Walsh (1998) 2.3 for a textbook treatment).

With a value for steady state consumption, we can solve for the steady state real moneybalances, Mss/Pss , by combining the first order

iss

1 + iss= uM/P

(Css,

Mss

Pss

)/uC

(Css,

Mss

Pss

), (1.18)

and the Fisher equation

1 + i = (1 + rss) Pt+1/Pt

= (1 + rss) (1 + π) . (1.19)

Using (1.19) in (1.18) gives an equation in Mss/Pss and known model parameters.

11

1.3.5 The Welfare Cost of Inflation

The welfare cost of inflation is typically analyzed for the steady state, since we can thenmake use of the superneutrality of money. The growth rate of money, and therefore theinflation rate and nominal interest rate, can then be changed without affecting the realequilibrium.

The welfare loss from a higher nominal interest rate is often measured as the extraconsumption needed in order to achieve the same utility as in the case with lower interestrate. The approach is typically to find the money demand function which expresses realmoney balances as a function of the consumption level and the nominal interest rate M

P =

f (i,C), and calculate utility as the value of the period utility function u [C, f (i,C)].If C = 1 in steady state, a certain interest rate i0 gives the utility u

[1, f

(i0, 1

)]. The

welfare loss from another nominal interest rate, i1, is the value of C which solves

u[1, f

(i0, 1

)]= u

[C, f

(i1,C

)]. (1.20)

This value of C is the compensation that the consumers need to be as well off with theinterest rate i1 as with i0. Note that C − 1 can be interpreted as the percentage change inconsumption needed to compensate for the higher nominal interest rate.

Example 3 (Welfare loss with Cobb-Douglas/CRRA.) From Example 1, the utility at the

nominal interest rate i is

u [C, f (i,C)] =1

1 − γ

[Cα

(C

1 − α

α

1 + ii

)1−α]1−γ

.

Consider a steady state where C = 1 and suppose that inflation is zero, so i = r . For

instance, to get the same utility as at C = 1 and i = 3%, u [1, f (0.03, 1)], then con-

sumption must be (1.03/ (1 + i)

0.03/ i

)1−α

= C.

Figure 1.1 illustrates the result for α = 0.99.

Example 4 (Welfare loss from Lucas (1994).) From Example 2 we get

u [C, f (i,C)] =1

1 − γ

C

(1 + B1/2

(it

1 + it

)1/2)−1

1−γ

.

12

3 4 5 6 7 8 9 100

0.5

1

1.5

Money in utility function: cost of i>3%

Nominal interest rate, %

Fra

ctio

n o

f co

nsu

mp

tion

, %

Cobb−Douglas, α=0.99

Lucas, B=0.0018

Figure 1.1: Utility loss, in terms of consumption, of inflation in two MIU models.

To get the same utility as with C = 1 and i = 3% consumption must be

1 + B1/2(

i1+i

)1/2

1 + B1/2(0.03

1.03

)1/2 = C.

Figure 1.1 illustrates the result for B = 0.0018 (Lucas’ point estimate).

Also a cash-in-advance model (see, for instance, Cooley and Hansen (1989)) can gen-erate welfare costs of inflation (more precise: of a non-zero nominal interest rate) if thecash-in-advance restriction applies only to a subset of the arguments in the utility func-tion. A positive inflation acts like a tax on those goods that must be paid in cash, andthereby creates a distortion.

Friedman’s Rule for Optimal Money Supply

Reference: Romer 9.8, BF 4.5.Friedman suggested a money rate growth which would set the nominal interest rate to

zero and thereby saturate money demand. The idea is that bills are (virtually) costless toprint and it has a (utility) value for agents, so why not give them as much as they wouldpossibly would like to have?

13

We know that the steady states of the real variables is unaffected by the inflation rate(see above), so if we concentrate attention to the steady state, then (1.14) tells us thatconsumers are satiated with real money balances if uM/P = 0, that is, if i = 0.

By the Fisher equation (1.13) this means that the monetary policy should set (1 + rt) Pt+1/Pt =

1, so the rate of deflation should equal the real interest rate. In this way, holding cash givesthe same return as a real bond, so savers will be happy to keep large real money balancesand to get the utility out of it.

In steady state, inflation equals the money growth rate, so a deflation requires a shrink-ing money supply, which means that seigniorage is negative—see (1.15). In this setting,this is compensated by lump-sum taxes, which highlights the assumption that the gov-ernment revenues from the inflation tax is either wasted or can be raised in other, non-distortive, ways. If, instead, a certain revenue must be raised and the alternative taxes aredistortive, then it may no longer be optimal with a zero inflation rate. See Walsh (1998).

If the utility function is separable in consumption and real money balances, then thisresult hold in general, not just in steady state.

The Welfare Cost of Inflation - Other Arguments

Reference: Fischer (1996), Romer 9.8, Driffil, Mizon, and Ulph (1990), and Walsh (1998)4.5-4.6.

1. Inflation raises the effective capital income tax (subsidy), since the nominal return(loss) is taxed (part of which is just compensation for inflation). The real net of taxreturn is

rnet= (1 − τ) i − π

= (1 − τ) r − τπ, (1.21)

where the Fisher relation gives i = r + Eπ and we assume that π = Eπ . Thisdistorts the savings decision. Some calculation for the US (Feldstein, NBER, 1996)suggest that this effect is large (twice as large as the effect on government revenues).Counter-argument: a lower inflation and therefore lower government revenues fromcapital income taxation is likely to bring higher tax rates.

2. Costs of price adjustments and indexation.

14

3. Some empirical evidence that really high inflation is bad for growth. It is (boththeoretically and empirically) unclear if zero inflation is better for growth than 5%inflation.

4. Seigniorage is low for most OECD countries (less than one percent of GDP, see OR8.2).

5. Low inflation means that it will be hard to drive down the real interest really low tostimulate output. (The nominal interest rates cannot be negative since the nominalreturn on cash is zero.).

6. Variable inflation may lead to large inflation surprises which redistribute wealth,increases uncertainty (affects savings in which way?), and increases the informationcosts.

1.3.6 The Relation to Traditional Macro Models

Equation (1.14) is a money demand equation, which in many cases can be approximatedby

ln Mt − ln Pt = γ1 ln Ct − γ2it , (1.22)

which is a traditional LM equation.When the utility function is separable in consumption and real money balances, then

the optimality condition for consumption (1.10) can often be approximated by

−γ ln Ct = ln (1 + rt+1)+ γ ln Ct+1, (1.23)

where consumption growth is related to the real interest rate. From the Fisher equation,we can replace ln (1 + rt+1) by it−Et (ln Pt+1 − ln Pt). This is clearly reminiscent of anIS equation.

1.3.7 The Price Level

The price level is determined simultaneously with all other variables, and there is typicallyno closed form solution.

In the special case where the utility function in (1.6) is separable, so the Euler equationfor consumption (1.10) is unaffected by real money balances, and where money supply

15

is exogenous is might be possible to arrive at an analytical expression for the price level.In this case, we can solve for the real equilibrium (consumption, real interest rates, etc)without any reference to money supply. The price level can then be found by solving(1.11) and information about money supply. This is an example of a classical dichotomy.

Example 5 (Solving for the price level.) Use the approximate Fisher equation, it =Et ln Pt+1−

ln Pt + rt+1, in the approximate money demand equation in Example 1

ln Mt − ln Pt = a + ln Ct −1

iss (1 + iss)(Et ln Pt+1 − ln Pt + rt+1) ,

and rewrite as

ln Ptiss (1 + iss)+ 1

iss (1 + iss)= −a − ln Ct + ln Mt +

1iss (1 + iss)

rt+1 +1

iss (1 + iss)Et ln Pt+1,

which is a forward looking difference equations for ln Pt in terms of the “exogenous”

variables ln Ct , ln Mt , and rt+1.

1.4 The Mechanics of Money Supply∗

References: Burda and Wyplosz (1997) 9, OR 8.7.6 and Appendix 8B, and Mishkin(1997).

The short version: the central bank can control either some monetary aggregate or aninterest rate or the exchange rate. This section is about how they do that, even if this isnot particularly important for most macroeconomic issues. Why they do it, that is, themonetary policy, is much more important—and something we will return to later.

1.4.1 Operating Procedures of the Central Bank

Suppose demand for the monetary base is decreasing in the nominal interest rate. Supposethe central bank does no interventions at all. Shifts in the demand curve for money willthen lead to movements in the nominal interest rate. Alternatively, suppose the centralbank announces a discount rate where any bank can lend/borrow unlimited amounts. Thiswill fix the interest rate and any shifts in the demand curve leads to movements in themonetary base (as the banks are free to borrow reserves and currency at the fixed rate).Finally, it is possible to strike a compromise between these two extremes letting banks

16

M

i

M

i

M

i

supply

supply

supply

a. Interest rule

b. Money rule

c. Mixture

Figure 1.2: Partial equilibrium on money market

lend at increasing interest rates. This effectively creates an upward sloping supply curvefor the monetary base. This is illustrated in Figure 1.2.

1.4.2 Money Supply and Budget Accounting

Money supply has a direct effect on government finances. Consider the consolidated gov-ernment sector (here interpreted as treasury plus central bank). The real budget identityis

G t +Bt−1

Pt(1 + it−1)+

Mt−1

Pt= Tt +

Bt

Pt+

Mt

Pt, (1.24)

where G t and Tt are real government expenditures revenues, respectively, Bt is nominaldebt, it the nominal interest rate, Mt is the monetary base (the central bank liabilities),and Pt the price level.

17

Assume the Fisher equation holds, so the nominal interest rate is

1 + it−1 = Et−1 (1 + rt)Pt

Pt−1, (1.25)

where rt is the real interest rate. The convention is that the nominal interest rate is datedt − 1 since it is known as of t − 1. To simplify, assume rt is known in t − 1. We then getfrom (1.25) that the real debt in t is

Bt

Pt= G t − Tt + (1 + rt)

Bt−1

Pt−1

Pt−1

PtEt−1

Pt

Pt−1−

Mt − Mt−1

Pt. (1.26)

Consider the case where real government expenditures and tax revenues are unaffectedby monetary policy (money is neutral), and where the central bank increases money sup-ply, Mt > Mt−1. This drives down the real value of government debt, Bt/Pt in twoways. First, the real revenues from money creation (printing), called seigniorage, is(Mt − Mt−1)/Pt . Second, the money supply increase will probably increase the pricelevel. If this increase is unanticipated, then actual inflation exceeds expected inflation,Pt−1/PtEt−1(Pt/Pt−1) < 1, so the real value of government debt brought over from t −1decreases.

1.4.3 Money Aggregates and the Balance Sheet of the Central Bank

The liabilities of the central bank are currency (Cu) plus banks reserves (Re) depositedin the central bank, the assets are the foreign exchange reserve, the holding of domesticbonds, and perhaps gold

Balance Sheet of Central BankAssets LiabilitiesDomestic bonds Currency (Cu)Foreign currency Reserve deposits (Re)Foreign bonds Net worthGold

18

1.4.4 Reserve Requirements and Deposits

Money stock, M , is currency, Cu, plus deposits, D, (also called “inside money” since it isgenerated inside the private banking system)

M = Cu + D. (1.27)

Suppose that private banks (because of reserve requirements or prudence) hold thefraction r of deposits, D, in reserves, Re. This means that an increase in reserves, 1Re,allows the bank to increase deposits with the reserve multiplier, 1/r ,

1D =1Re

r. (1.28)

These new deposits may be lent to someone (an thereby bring in profits to the bank,assuming the lending rate is above the deposit rate). Note that if r goes to zero, then thecentral bank cannot control the creation of new deposits by affecting the availability ofreserves.

Reserve requirements mean that a private bank must hold a fraction (usually a fewpercentage) of the (checkable) deposits in either cash (in the vault) or as reserves withthe central bank. This fraction is often specified as an average over some period (twoweeks in the US). Suppose a bank needs to get more reserves (maybe depositors withdrewmoney during the preceding week). It can then either sell some assets, borrow from otherbanks (“federal funds” market in the US), or borrow from the central bank (at the Fed’s“discount window” in the US). Note that borrowing from the central bank is effectivelya decrease (as long as the loan lasts) in the reserve requirement. Therefore somethinghas to be done to make the reserve requirements bite in spite of the possibility to borrowfrom the central bank. This is typically a penalty rate for these loans, or some kind ofadministrative rationing of loans.

It is the fact that r < 1 that makes banks different from other financial institutions.To see why, suppose r = 1. Then all deposits would have to be kept as reserves andcouldn’t be used for lending. Consequently, any lending has to be done from the banksown capital. In this sense, the bank is not an intermediary any more and cannot “createmoney.”

The money stock deposits discussed above can be interpreted/measured in differentways. The most common monetary aggregates are: M1 (currency, travellers’ checks,

19

checkable deposits); M2 (M1 plus small denomination time deposits, savings deposits,money market funds, repos, Eurodollars); M3 (M2 plus large denomination time deposits,and money market funds held by institutions)

1.4.5 Interventions and the Money Multiplier

The central bank can typically not control the reserves directly, only the sum of reservesand currency (the private sector can always convert the currency into reserves and viceversa). This sum is called the monetary base (B) (also called high-powered money, M0,central bank money, or outside money since it is generated outside the private bankingsystem), is

B = Cu + Re. (1.29)

The monetary base can be increased by, for instance, an open market operation wherethe central bank buys government bonds and pays by either cash (increases Cu) or cheque(increases Re). The same effect is achieved by a foreign exchange intervention; the centralbank buys a foreign asset and pays by either cash or cheque denominated in the domesticcurrency.

Suppose private agents wants to hold the fraction c of the money stock in currency.We can then write (1.29) and (1.27) as

B = cM + r D (1.30)

M = cM + D.

The money multiplier, M divided by B, can then be written

MB

=M

Cu + Re

=D/ (1 − c)

Dc/ (1 − c)+ r D

=1

c + r (1 − c). (1.31)

The relation between money stock and monetary base is therefore

M =1

c + r (1 − c)B. (1.32)

20

c is often thought of as being determined by bank/households, so the central bank canaffect money supply by either influencing r (reserve requirements) or by changing themonetary base (interventions). The money multiplier is decreasing in fraction of currency,c, since it acts like a “leakage” from the private banking system. At c = 0, that is, whenthere is no currency, then the money multiplier is at a maximum and coincides with thereserve multiplier.

Example 6 (US data 1994, Burda and Wyplosz (1997) 9) For the US 1994 c = 0.29,

M1/M0 = 2.83, which by (1.32) should imply that r = 0.089. The reserve requirements

on demand deposits was (at least in 1995) virtually zero for small demand deposits..

Explanations: voluntary reserves (prudence or transaction purposes) and “leakages”

(deposits in nonbank financial institutions).

Example 7 (The Great Depression.) Private sector decisions can lead to important

changes in both c and r. During the Great Depression, B was not changed much (counter

to the conventional wisdom about a contractionary monetary policy), while savers with-

drew deposits from the banks and the banks increased the voluntary reserves (both c and

r increased substantially), with the result that M decreased some 30%. Fear of banks

going bust?

Example 8 (Money creation.) The central bank makes an open market purchase of

bonds. This increases the monetary base by 1B. Recall Re = r D and Cu = cM,

so according to (1.30)

B =

(c

1 − c+ r

)D.

The increase in the monetary base will therefore be split into increases in reserves and

currency according to

1Re = φ1B where φ =r (1 − c)

c + r (1 − c)

1Cu = δ1B where δ =c

c + r (1 − c).

For concreteness, assume this could happen if the central bank buys the bonds from the

(consolidated) private bank, which in turn buys some of them from savers. The extra

reserves allow the (consolidated) private bank to take extra deposits. This can be done by

21

lending money to a customer by crediting his deposit account. This extra deposit is

1D =φ

r1B

=1 − c

c + r (1 − c)1B.

Clearly,

1M = 1D +1Cu

=1

c + r (1 − c)1B,

as expected and all desired ratios are fulfilled (check this).

1.4.6 More on Interventions

Reference: ORA sterilized foreign exchange intervention is when the effects on the money supply of

a foreign exchange intervention is nullified by an open market operation; the central bankbuys foreign assets, pays with cash, but sell domestic assets (government bonds) to getthe cash back.

An intervention on the forward market is very similar to a sterilized intervention.Suppose the bank enters a forward contract to buy domestic currency tomorrow and tosell foreign currency at the same time. This decreases the supply of “domestic currencytomorrow,” that is, of domestic bonds, while increasing the supply of foreign bonds - justlike in a sterilized intervention.

It seems as if sterilized interventions can have effects on exchange rates and interestrates, but we are not sure why. Portfolio-balance effect (changing supply changes the riskpremium, but what about Ricardian equivalence?) or signalling?

Bibliography

Benassy, J.-P., 1995, “Money and Wage Contracts in an Optimizing Model of the BusinessCycle,” Journal of Monetary Economics, 35, 303–315.

Blanchard, O. J., and S. Fischer, 1989, Lectures on Macroeconomics, MIT Press.

22

Burda, M., and C. Wyplosz, 1997, Macroeconomics - A European Text, Oxford UniversityPress, 2nd edn.

Cooley, T. F., and G. D. Hansen, 1989, “The Inflation Tax in a Real Business CycleModel,” The American Economic Review, 79, 733–748.

Driffil, J., G. E. Mizon, and A. Ulph, 1990, “Costs of Inflation,” in Benjamin M. Friedman,and Frank H. Hahn (ed.), Handbook of Monetary Economics . , vol. 2, North-Holland.

Fischer, S., 1996, “Why Are Central Banks Pursuing Long-Run Price Stability,” inAchieving Price Stability, pp. 7–34. Federal Reserve Bank of Kansas City.

Goldfeld, S. M., and D. E. Sichel, 1990, “The Demand for Money,” in Benjamin M. Fried-mand, and Frank H. Hahn (ed.), Handbook of Monetary Economics, vol. 1, . chap. 8,North-Holland.

Lucas, R. E., 2000, “Inflation and Welfare,” Econometrica, 68, 247–274.

Mishkin, F. S., 1997, The Economics of Money, Banking, and Financial Markets,Addison-Wesley, Reading, Massachusetts, 5th edn.

Obstfeldt, M., and K. Rogoff, 1996, Foundations of International Macroeconomics, MITPress.

Romer, D., 1996, Advanced Macroeconomics, McGraw-Hill.

Walsh, C. E., 1998, Monetary Theory and Policy, MIT Press, Cambridge, Massachusetts.

23

2 The Price of Money

Main references: Romer (1996) (Romer), Blanchard and Fischer (1989) (BF), Obstfeldtand Rogoff (1996) (OR), and Walsh (1998).

2.1 UIP, Fisher Equation, and the Expectations Hypothesis of theYield Curve

Reference: OR 8.7.1-8.7.3

2.1.1 Pricing Relations for Nominal Returns

This section gives three very important relations, which we will use in the subsequentanalysis. These relations can be stated in several different forms, but here we use thelog-linear form which fits nicely into the linear models used in most of this class.

Let it be a continuously compounded (per period) nominal interest rate on a discountbond (no coupons) traded at t and maturing at t + 1, and let πt+1 = ln(Pt+1/Pt) bethe corresponding inflation rate. The relation between nominal interest rates, real interestrates and expected inflation is

it = Etπt+1 + rrt + ϕπt , (2.1)

where rrt is a real interest rate and ϕπt a risk premium (inflation risk premium). The Fisher

equation assumes that the risk premium is zero or constant, and sometimes also that thereal interest rate is constant.

The relation between domestic interest rates, foreign interest rates (indicated by astar∗), and expected exchange rate depreciation is

it − i∗

t = Et ln (St+1/St)− ϕst , (2.2)

where St is the exchange rate (units of domestic currency per unit of foreign currency,for instance, 8 SEK per USD), and ϕs

t is a risk premium (exchange rate risk premium).

24

(The sign of the risk premium is just a matter of definition. Here ϕst > 0 means that

an investment in foreign bonds require a positive risk premium.) Uncovered interest rateparity, UIP, assumes that the risk premium is zero or constant. Both (2.1) and (2.2) havesimilar forms for multi-period investments.

Finally, let it,t+s be the continuously compounded per period nominal interest rate ona discount bond traded at t and maturing at t + s. The relation between long interest ratesand expected future short interest rates is

it,t+s =1s(Et it + Et it+1 + · · · + Et it+s−1)+ ϕi

t , (2.3)

where ϕit is a risk premium (term premium). The expectations hypothesis of interest rates

(yield curve) assumes that the risk premium is zero or constant.Derivations are given in the Appendix.

2.2 The Price Level as an Asset Price: Cagan’s (1956) Model withRational Expectations

Reference: BF 4.7 and 5.1, Romer 9.7, OR 8.2, Walsh (1998) 4.3.This classic model was first used to discuss hyperinflation. In this case prices are

driven almost entirely by the dynamics of money supply (Phillips effects and other influ-ences of real variables are of minor importance). Many hyperinflation episodes originatein the need to generate government revenues, why we will take a look at seigniorage. Thismodel also allows us to discuss the “asset pricing” aspect of the price level, and how tosolve such models.

The model is an approximation to the general equilibrium model with money in theutility function, where the real side of the economy (output, consumption, real interestrate) is kept constant.

2.2.1 Determination of the Price Level under Rational Expectations

Suppose the money demand function (LM curve) is

ln Mt − ln Pt = ψ ln Yt − ωit , with ω > 0. (2.4)

25

Prices are assumed to be completely flexible. Assume that income and the real interestrate are constant, so by the Fisher equation

it = Et(ln Pt+1 − ln Pt) + constant, (2.5)

and the money demand equation can be normalized as

ln Mt − ln Pt = −ω (Et ln Pt+1 − ln Pt) . (2.6)

These assumptions could either be motivated by that this is a steady state situation (generalequilibrium with MIU) or that we want to look at hyperinflation, where movements in thereal interest rate and output are of trivial importance compared with the movements in themoney stock.

Remark 9 (The price of money) Note that if one unit of the good costs Pt units of money,

then one unit of money costs Ft = 1/Pt units of goods. We can then rewrite (2.6) as

ln Ft = − ln Mt + ω (Et ln Ft+1 − ln Ft) .

This says that the price of money equals a dividend, − ln Mt , and a discounted capital

gain. To see that − ln Mt is like a dividend, suppose utility is U (C,M/P) = u1(C) +

ln M/P, then UM = 1/M. We could therefore think of − ln Mt as an approximation of

the marginal utility of money.

Rewrite (2.6) as

ln Pt = (1 − η) ln Mt + ηEt ln Pt+1, with η = ω/ (1 + ω) < 1. (2.7)

The price level today depend on the money supply, but also on the expected price leveltomorrow. If the price level tomorrow is expected to be very high, then currency willbe worth little tomorrow (the value of money in terms of goods is 1/Pt ). Like any otherasset, the value of money will then decrease already today, which means that Pt increases.

Remark 10 (Law of iterated expectations.) We must have

EtEt+1 ln Pt+2 = Et ln Pt+2,

since the information set in t is a subset of the information set in t + 1. (Senility is not

allowed.)

26

Substituting for Et ln Pt+1 in (2.7) gives

ln Pt = (1 − η) ln Mt + ηEt[(1 − η) ln Mt+1 + ηEt+1 ln Pt+2

]︸ ︷︷ ︸ln Pt+1

, (2.8)

= (1 − η) ln Mt + η (1 − η)Et ln Mt+1 + η2Et ln Pt+2, (2.9)

where we use the law of iterated expectations. By continuing the substitution we end upwith

ln Pt = (1 − η)

K∑s=0

ηsEt ln Mt+s + ηK+1Et ln Pt+K+1. (2.10)

If limK→∞ ηK+1Et ln Pt+K+1 = 0, then we can write

ln P∗

t = (1 − η)

∞∑s=0

ηsEt ln Mt+s, (2.11)

where ln P∗t is the “bubble-free” (or “fundamental”) solution. Note that money is neu-

tral in the sense that changing the level of money supply (Mt ) by a factor γ in eachperiod increases the price level by the same factor. This follows from the fact that(1 − η)

∑∞

s=0 ηs= 1.

Example 11 (Log money supply is random walk plus drift.) Suppose the growth rate of

money is δ plus a (serially uncorrelated) shock, or

ln Mt+1 = δ + ln Mt + εt+1.

Then, the log price level in (2.11) is

ln P∗

t = (1 − η)

∞∑s=0

ηs (ln Mt + sδ) .

Since∑

∞

s=0 ηss = η/ (1 − η)2, the rational expectation equilibrium price level is

ln P∗

t = ln Mt + δη

1 − ηor ln

Mt

P∗t

= −δη

1 − η,

which we can write as (since η = ω/ (1 + ω))

ln P∗

t = ln Mt + δω or lnMt

P∗t

= −δω,

27

so the log real balances are a decreasing function of the growth rate of money. In this

special case, real money balances are not affected by the shocks. (See Romer 391-394 for

a diagrammatic description and a discussion of the case with price inertia.)

Example 12 (Log money supply is random walk plus drift, continued.) From Example

11, inflation is equal to money growth

πt = 1 ln P∗

t = 1 ln Mt = δ + εt .

A higher growth rate of money supply δ drives up the expected inflation and therefore the

nominal interest rate (the real interest rate is assumed to be constant) which decreases

demand for real money balances. With a given money supply Mt , the price level must

increase to keep the money market in equilibrium.

Example 13 (Money supply and the nominal interest rate.) Consider a money demand

equation ln Mt − ln Pt = ψ ln Yt − ωit , and assume that ln Yt is constant. What is the

effect on the nominal interest rate, it , of a shock to money supply? When money supply

is a random walk, then the effect is zero, since ln Pt increases as much as ln Mt . If

ln Mt = ρ ln Mt−1 +εt with |ρ| < 1, then ln Pt = [(1−η)/(1−ηρ)] ln Mt so ln Pt reacts

less than ln Mt to shock. In this case, it must decrease in response to a positive shock

to money growth. To get a positive effect on it , the shock to money supply must be more

persistent than a random walk, for instance, by letting 1 ln Mt be an AR(1).

2.2.2 Bubbles and Saddle Point Properties

Equation (2.11) is not the unique solution, only the unique “fundamental solution.” Letus call it ln P∗

t , and postulate that any solution can be written as a sum of the fundamentalsolution and a “bubble” bt ,

ln Pt = ln P∗

t + bt . (2.12)

Use this in (2.7)

ln P∗

t + bt = (1 − η) ln Mt + ηEt(ln P∗

t+1 + bt+1)

, (2.13)

and use (2.11) to obtain the requirement that any bubble must satisfy

bt = ηEtbt+1 ⇒ Etbt+s = η−sbt . (2.14)

28

Since η < 1, the expected value Etbt+s explodes.Ruling out bubbles, that is, using the solution (2.11), therefore amounts to finding

the unique stable solution of an unstable difference equation, that is, exploiting the sad-dle point property. Equations (2.12)-(2.14) shows that any other solution explodes (inexpectation).

2.2.3 Seigniorage

Seigniorage can be an important source of funds for the government. It has historicallybeen very important during specific episodes, often in conjunction with wars. (Very his-torically, it was the fee the authorities asked for the service of minting your silver or gold.To increase the demand for this service, it was often forbidden to mint your own coins orto use foreign coins or even domestic coins older than a certain number of years.) Theneed for seigniorage is reputed to be the main cause of most hyperinflations.

Real revenues from money creation, seigniorage, is

Seignioraget =Mt − Mt−1

Pt

=Mt

Pt

(1 −

Mt−1

Mt

). (2.15)

This is the real revenues the government get by printing more money. We can think ofMt/Pt as the tax base and 1 − Mt−1/Mt as the tax rate. In fact, seigniorage is oftencalled “inflation tax.” The tax rate is essentially the money growth rate, which is stronglycorrelated with inflation and the nominal interest rate (the Cagan model, they are thesame). We know from the money demand equation that real balances are decreasing inthe nominal interest rate (for a given output level), so increasing the money growth ratetherefore increases the tax rate and decreases the tax base—the result is often a Laffercurve. Mt in (2.15) should be interpreted as the monetary base. Seigniorage is fairlyunimportant for most OECD countries; it is typically less than 1% of GDP.

Example 14 From Example 11 we have

Mt = Mt−1 exp(δ + εt), and Pt = Mt exp (δω) .

29

Use this in (2.15) to get

Seignioraget =Mt−1 exp(δ + εt)− Mt−1

Mt−1 exp(δ + εt) exp (δω)

= exp(−δω)− exp [−δ(1 + ω)− εt ] .

This is always increasing in the money supply surprises εt , but will typically show a

”Laffer curve” with respect to δ.

Example 15 (Tax smoothing and seigniorage.) Suppose the distortionary effects of taxes

are convex functions of the tax rates. The optimal way to finance government expenditures

is then to keep tax rates more or less constant over time. Temporary changes in govern-

ment consumption should be met by lending/borrowing. Seigniorage is a tax, so this

theory suggests that seigniorage should be relatively constant. In fact, however, seignior-

age seems to much more correlated with government consumption than other taxes. War

financing is a particularly clear case. See, for instance, Walsh (1998) 4.

2.2.4 Causality or Only an Equilibrium Condition?

In Cagan’s model, money supply is exogenous, so (2.11) shows how the expectations formoney supply determine the price level.

This would no longer be true if allowed output to change and to depend on prices(something we will see later in the course), or if we assumed that money supply wasa function of output and inflation (something we will also see later in the course). Inthis case, we could still combine the money demand equation and the Fisher equation toexpress the price level in terms of a discounted sum of expected money supply and output,but it would only be an equilibrium condition.

To demonstrate the last point, suppose both the real interest rate, rt , and log output,ln Yt , vary. Then (2.6) should be

ln Mt − ψ ln Yt + ωrt − ln Pt = −ωEt(ln Pt+1 − Pt). (2.16)

Therefore, if we replace ln Mt in (2.11) with ln Mt −ψ ln Yt +ωrt , we have a solution of(2.16). However, this cannot really be interpreted as the cause of the price level until wehave specified how money supply, output, and the real interest rate are determined—inparticular, if they depend on the price level.

30

2.2.5 Empirical Illustrations

Burda and Wyplosz (1997) Fig 8.9, 8.12, Box 8.5, Table 16.3, and Boxes 16.4-5; WalshFig 4.3.

2.3 A Simple Model of Exchange Rate Determination

Reference: OR 8.2.7, 8.4.1-4, Burda and Wyplosz (1997) 18-21, Isard (1995).

2.3.1 UIP and the Exchange Rate Equation

The traditional monetary model of exchange rates starts out from a money demand equa-tion, which is combined with an UIP condition.

The UIP (uncovered interest rate parity) condition is

Et1 ln St+1 = it − i∗

t , (2.17)

where it and i∗t are the (per period) domestic and foreign currency interest rates, respec-

tively, and St is the number of units of domestic currency per unit of foreign currency(example: 8 SEK per USD). The condition says that the expected returns (measured ina common currency) of lending in the domestic currency or in the foreign currency areequal. This typically requires full capital mobility and risk neutrality.

The money demand equation is

ln Mt − ln Pt = ψ ln Yt − ωit , or

it =1ω(ψ ln Yt − ln Mt + ln Pt) (2.18)

There is a similar demand equation in the foreign country, so the interest rate differentialcan be written

it − i∗

t =1ω

[ψ(ln Yt − ln Y ∗

t)−(ln Mt − ln M∗

t)+(ln Pt − ln P∗

t)]. (2.19)

The real exchange rate is defined as the relative price of foreign goods

Qt =St P∗

t

Pt=

“8 kronor per dollar × 1 dollar per US hamburger”“10 kronor per Swedish hamburger”

. (2.20)

31

You may note that the purchasing power parity (PPP) issue is about whether Qt is constantor not. The flexible-price monetary model of exchange rates would set Qt constant. Wewill not impose that, so the equation for the exchange rate that we will arrive at can onlyby regarded as an equilibrium condition.

Use (2.20) to substitute for ln Pt − ln P∗t = − ln Qt + ln St in (2.19), and then combine

with the UIP condition (2.17) to get

Et1 ln St+1 =1ω

[ψ(ln Yt − ln Y ∗

t)−(ln Mt − ln M∗

t)− ln Qt

]+

1ω

ln St . (2.21)

Collect the “fundamental” driving variable into

vt = −ψ(ln Yt − ln Y ∗

t)+(ln Mt − ln M∗

t)+ ln Qt , (2.22)

and rewrite (2.21)as

Et1 ln St+1 = −vt

ω+

1ω

ln St or

ln St = vt + ωEt1 ln St+1. (2.23)

Note how the exchange rate is like any other asset: the current price is a function of somedividend, vt , plus a discounted capital gain, ωEt1 ln St+1. Note that (2.23) is just anequilibrium condition—it cannot be given a causal interpretations without making furtherassumptions.

2.3.2 A Fixed Exchange Rate (St fixed, Mt variable)

Suppose the central bank pursues a policy of a unilateral fixed exchange rate, and that itmanages to make this policy credible. For instance, let ln St =Et1 ln St+1 = 0 in (2.23),and note that this requires vt = 0. From (2.22), we see that this means that

ln Mt = ln M∗

t + ψ(ln Yt − ln Y ∗

t)+(ln Pt − ln P∗

t). (2.24)

If the money stock is the monetary policy instrument, then this equation shows how thecentral bank must act to keep the exchange rate fixed. In this sense, the central bank hasno control over the money stock in a fixed exchange rate regime. By fixing the exchangerate (or any other financial price) the country looses its monetary policy independence.

The mechanism is the following: suppose we get a temporary shock to ln Yt . This

32

increases money demand according to (2.18); the central bank increases money supplyby either an open market operation (buying bonds, selling domestic currency) or an in-tervention on the foreign exchange market (buying foreign exchange, selling domesticcurrency). This restores money market equilibrium at an unchanged interest rate. By UIP(2.17), this is compatible with a fixed exchange rate.

Instead of a unilateral peg, suppose the home country and one foreign country decideto fix their bilateral exchange rate (for instance, St = 0). According to (2.24), this puts arequirement on the relative money supply, Mt/M∗

t . The level of money supply (“nominalanchor”) can be set to meet some other objective (the exchange rate with a third currency,the price level, or for stabilization purposes). (This is often called the “N-1 problem.”)

Example 16 (Bretton Woods.) The Bretton Woods system was originally based on the

USD being pegged to gold, and the other currencies being pegged to the USD. The fixed

exchange rate forced other countries to behave according to (2.24). As a consequence, the

other countries more or less adopted the US inflation rate, see (2.11). The gold peg meant

that foreign central banks (not private agents) could buy gold per 35 USD per ounce.

It was expected to discipline the US since too fast US money creation would lead other

central banks to convert dollars into gold. However, this did not work as expected during

the 1960s when the US money growth rate increased. Several countries, like Germany

and Japan, had strong anti-inflationary preferences but abstained from converting dollars

into gold, possibly because of the strong political dependence of the US. At the end of the

1960s/beginning of the 1970s a series of speculative attacks toppled the Bretton Woods

regime.

Example 17 (EMS.) Until the mid 1980s EMS was characterized by a series of small

realignments, but thereafter it was very much a system for fixed exchange rates where

most European currencies were effectively pegged to the DM. The boom in Germany after

the unification lead to inflationary pressure, while most other European countries were in

a fairly deep recession with almost deflationary tendencies. Bundesbank wanted to keep

monetary policy tight, which forced other countries to follow (see(2.24)). In the end, the

political pressure for looser monetary policy (for instance, in the UK) undermined the

credibility of the system and a series of speculative attacks forced a number or currencies

to abandon the peg. Why? Central banks should in most cases be able to buy back the

monetary base and thereby restore the exchange rate. However, by (2.18) this would

33

(at unchanged prices and output) lead to very high interest rates, which may disrupt the

economy (especially the banking sector which typically borrows short and lends long).

The Swedish central bank was willing to accept extreme interest rates during the first

attack on the krona in September 1992, but not during the second attack two months later.

2.3.3 A Floating Exchange Rate

Suppose instead that the central bank lets the exchange rate move. In the extreme case,Mt is fixed, but that is clearly not necessary for the exchange rate to move. Rearrange(2.23) to express ln St as a function of vt and Et St+1 on the left hand side

ln St = vt + ωEt ln St+1 − ω ln St

= (1 − η) vt + ηEt ln St+1, with η = ω/ (1 + ω) < 1 (2.25)

because ω > 0. The stable solution (ruling out bubbles) is then

ln St = (1 − η)

∞∑s=0

ηsEtvt+s . (2.26)

This expresses the current exchange rate in terms of the expected values of future “divi-dends.” This is the “asset pricing” view of exchange rate determination. Since we havenot said anything about how vt is determined, this is only an equilibrium condition. Inparticular, there is plenty of evidence that the real exchange rate (which is in vt ) is affectedby the nominal exchange rate, at least in the short to medium run.

Example 18 (AR(1) fundamental.) If vt+1 = ρvt + εt+1 with εt+1 iid, then Etvt+s =

ρsvt , so (2.26) becomes

ln St = vt (1 − η)

∞∑s=0

(ηρ)s

= vt1 − η

1 − ηρ,

where the last term is the effect on 1 ln St+1 of a shock to vt+1. This effect is increasing

in ρ, since a larger ρ means that the shock has a more long lasting effect on vt+s .

We have, once again, nominal neutrality in the sense that increasing Mt in all periodsby the factor γ increases the exchange rate with the same factor. Also note from (2.25)

34

that as ω becomes large, ln St will be very similar to a martingale (for instance, a randomwalk).

(2.26) gives a key role to the expectations formation. An unanticipated increase inthe fundamental will cause a large increase in ln S1, while an anticipated increase in the

fundamental causes the exchange rate to increase already at the date of announcement. Asimple example illustrates that.

Example 19 (Anticipated versus unanticipated shocks.) Suppose

v0 = 0vi = 1 for i ≥ 1.

If the change in vi is completely unanticipated, then

ln S0 = 0ln S1 = 1

if E0vi = 0 for i ≥ 1.

In contrast, if the change in vi is anticipated in t = 0, then

ln S0 = 0 + (1 − η)∑

∞

s=1 ηs= η

ln S1 = 1if E0vi = 1 for i ≥ 1.

Is often claimed that the exchange rate depreciation, 1 ln St , and the interest ratedifferential, it − i∗

t , are correlated. However, this depends on which kind of shock thathits the economy. To get a positive correlation between 1 ln St and it − i∗

t , the shockmust create a change in the exchange rate which is expected to be followed by changes inthe future in the same direction.

Example 20 (A mean reverting shock to the fundamental.) When vt is iid, then (2.26)

becomes

ln St = (1 − η) vt ,

so

1 ln St = (1 − η) (vt − vt−1) , and

Et1 ln St+1 = (1 − η)Et (vt+1 − vt) = − (1 − η) vt .

35

Since it − i∗t =Et1 ln St+1 we get

Cov(1 ln St , it − i∗

t ) = − (1 − η)2 Var (vt) ,

which is negative. It is straightforward to show that we get Cov(1 ln St , it − i∗t ) < 0

for any stationary AR(1) specification of vt . In contrast, most empirical estimates of this

covariance are positive.

Example 21 (Permanent shock to the level.) Consider the case when there are permanent

shocks to the level of money supply

vt+1 = vt + εt+1,

so (2.26) is

ln St = vt ,

1 ln St = vt − vt−1 = εt ,

Et ln St+1 = vt , so Et1 ln St+1 = it − i∗

t = 0.

This means that Cov(1 ln St , it − i∗t ) = 0, which is still too low compared with most

empirical estimates.

Example 22 (A more than permanent shock.) Let the fundamental be a sum of a random

walk and the shock to the random walk

vt = ut + θ0εt , where ut = ut−1 + εt and εt is iid.

This means that

Etvt+s = Etut+s + θ0Etεt+s

=

{ut + θ0εt if s = 0

ut if s ≥ 1.

By (2.26) the exchange rate is

ln St = ut + (1 − η) θ0εt

36

The depreciation is then

1 ln St = ut + (1 − η) θ0εt − (ut−1 + (1 − η) θ0εt−1)

= [1 + (1 − η) θ0]εt − (1 − η) θ0εt−1,

since ut − ut−1 = εt . Etεt+1 = 0, so the expected depreciation must be

Et1 ln St+1 = − (1 − η) θ0εt

Combine to get Cov(1 ln St , it − i∗t ) as

Cov(1 ln St ,Et1 ln St+1) = E{[1 + (1 − η) θ0]εt − (1 − η) θ0εt−1}{− (1 − η) θ0εt}

= −[1 + (1 − η) θ0] (1 − η) θ0Var (εt)

which can have either sign. For θ0 = 0 it is zero, since this is the random walk case

discussed above. For θ0 > 0 it is always negative, since εt > 0 shifts the permanent level

of vt up, but also gives a temporary positive blip in t, so1 ln St > 0 but Et1 ln St+1 < 0.

For θ0 < 0, we can get a positive covariance, since εt > 0 gives a temporary negative

blip, that is, the upward permanent shift in vt is not realized until t + 1. For instance, for

θ0 = −1, the covariance is η (1 − η)Var(εt), which is positive. The basic mechanism is

that the expected effect of the shock on the fundamental grows over time.

2.3.4 The Correlation Between Real and Nominal Exchange Rates

A stylized fact is that the real, Qt , and the nominal, St , exchange rates are strongly posi-tively correlated. If we assumed that St does not affect Qt , then the only explanation forCov(Qt , St) > 0 in this setting is that shocks to the real exchange rate is the main drivingforce behind the nominal exchange rate. As seen from (2.22) and (2.23), the nominal ex-change rate is an increasing function of the real exchange rate. Monetary shocks shouldbe small. There is plenty of empirical evidence against this view. The basic mechanismwould then be that monetary shocks drive St which in turn drive Qt , because nominalprices P∗

t /Pt tend to be sticky.

37

2.3.5 Capital Controls and Risk Premia

The preceding discussion shows that the country can chose either fixed exchange rate ormonetary policy independence. It cannot have both, unless there is some way to break theUIP condition (which here serves as the equilibrium condition for the capital market). Onepossibility of doing that is to let the central bank affect risk premia by changing the relativesupplies of different assets. For instance, the portfolio-balance approach emphasizes riskpremia and discusses how sterilized interventions change the risk characteristics of theprivate-sector portfolio and thereby asset prices. Another possibility is to impose capitalcontrols, which make it costly to move capital.

2.3.6 Other Candidate Exchange Rate Equations

There are several other candidate exchange rate equations. Monetary sticky-price models

relaxes the assumption of instantaneous price flexibility, which often adds inflation termsto vt and makes the real exchange rate endogenous. The Dornbusch model (see OR 9.2)is one example.

Structural exchange rate equations, which try to explain exchange rates in terms ofmacro variables often fail to improve upon a simple random walk—at least for relativelyshort horizons.

2.3.7 Empirical Illustrations

Burda and Wyplosz (1997) Figs. 8.9, 13.6, and 19.1; OR Figs. 9.1; Isard (1995) Figs.3.2, 4.2, and 11.1.

A Derivations of the Pricing Relations

Consider an agent who chooses consumption and asset holdings optimally. Let R jt+1 be

the one-period gross return from investing in asset j in t . The first order condition is

1 = Et Rit+1 exp (qt+1) , (A.1)

where qt+1 is the log real discount factor between t and t + 1. For instance, if the utilityfunction is time separable, Et6

∞

s=0βsu(Ct+s,Mt+s/Pt+s), then qt+1 = ln[βuC (Ct+1,Mt+1/Pt+1) /UC (Ct ,Mt/Pt)].

38

Note that the log real discount factor must be decreasing in Ct+1 (and ln Ct+1), since theutility function is concave.

Let r jt+1 = ln R j

t+1 be the log gross return, and rewrite the first order condition as

1 = Et exp(r i

t+1 + qt+1). (A.2)

Assume that q and r j are conditionally normally distributed[qt+1

r jt+1

]=

[Etqt+1

Etrj

t+1

]+

[ε

qt+1

εjt+1

]with

[ε

qt+1

εjt+1

]∼ N

([00

],

[σqq σq j

σq j σ j j

]).

(A.3)

Example 23 (CRRA utility.) The real discount factor, q, would be normally distributed,

for instance, if ln Ct+1 and ln(Mt+1/Pt+1) are normally distributed and the utility func-

tion is isoelastic, so U (Ct ,Mt/Pt) =[Cα

t (Mt/Pt)1−α

]1−γ/ (1 − γ ). In this case,

qt+1 = ln[βuC (Ct+1,Mt+1/Pt+1) /UC (Ct ,Mt/Pt)]

= lnC−αγ

t+1 (Mt+1/Pt+1)(1−α)(1−γ )

C−αγt (Mt/Pt)(1−α)(1−γ )

= −αγ ln (Ct+1/Ct)+ (1 − α) (1 − γ ) ln(Mt+1 Pt/Pt+1Mt).

Remark 24 If x ∼ N (Ex,Var(x)), then

E exp (x) = exp [Ex + Var (x) /2] .

The distribution could be interpreted as a conditional or an unconditional distribution.

Take logs of (A.2), and apply the rule for Eexp (x) when x is normally distributed

0 = Etrj

t+1 + Etqt+1 + Vart

(r j

t+1 + qt+1

)/2. (A.4)

This can be written as

Etrj

t+1 = −Etqt+1 −12

Vart

(r j

t+1 + qt+1

)= −Etqt+1 −

12

Vart

(r j

t+1

)−

12

Vart (qt+1)− Covt

(r j

t+1, qt+1

)(A.5)

39

The variance terms are due to the non-linear transformation (recall Jensen’s inequality)and typically not very interesting. The covariance is more important, since it captures riskaversion.

A.1 A Real Bond

A real bond has a known real interest rate (it is safe), r jt+1 = rr

t . In this case (A.5)simplifies to

rrt = −Etqt+1 −

12

Vart (qt+1) . (A.6)

We can use this equation to rewrite (A.5) as

Etrj

t+1 − rrt = −

12

Vart

(r j

t+1

)− Covt

(r j

t+1, qt+1

)(A.7)

= ϕjt , (A.8)

which shows how the expected return in excess of the safe return depends on a Jensen’sinequality term and the covariance of the return with the stochastic discount factor. Anegative covariance means that the asset tends to have an unexpectedly low return whenmarginal utility is unexpectedly high. This is like a negative insurance, so investors willrequire a positive risk premium, ϕ j

t .

A.2 A Nominal Bond

A nominal bond has an uncertain real return, r jt+1 = it −πt+1, since inflation is uncertain.

In this case (A.7) is

it − Etπt+1 − rrt = −

12

Vart (−πt+1)− Covt (−πt+1, qt+1) , (A.9)

which has the same form as (2.1). Note that it is known, so only −πt+1 enter the varianceand covariance terms. If the covariance is negative, then inflation tend to be unexpectedlyhigh (the real return on the nominal bond is unexpectedly low), when marginal utility isunexpectedly high. Investors will then require a positive inflation risk premium. The signof the inflation risk premium can clearly be different in different economies. It can alsochange over time if the conditional covariance does.

40

A.3 A Nominal Foreign Bond

A nominal foreign bond has also an uncertain real return, i∗t − πt+1 + ln (St+1/St), since

both inflation and the exchange rate depreciation are uncertain. To see that this is thereal return, note that giving up one unit of goods today gives Pt units of domestic cur-rency, and therefore Pt/St units of foreign currency. In t + 1, this gives exp

(i∗t)

Pt/St

units of foreign currency, or exp(i∗t)

Pt St+1/St units of domestic currency, and thereforeexp

(i∗t)(Pt/Pt+1) (St+1/St) units of goods.

In this case (A.7) is

i∗

t − Etπt+1 + Et ln (St+1/St)− rrt = λt , (A.10)

where the variance and covariance terms are collectively denoted λt . We can use (A.9) tosubstitute for Etπt+1 + rr

t to get

i∗

t − it + Et ln (St+1/St) = ϕst , (A.11)

which is the same as (2.2). It is straightforward to show that

ϕst = −

12

Vart[ln (St+1/St)

]− Covt

[−πt+1, ln (St+1/St)

]− Covt

[ln (St+1/St) , qt+1

].

(A.12)If the last covariance term is negative, then the exchange rate tend to unexpectedly ap-preciate (the real return, measured in domestic goods, of the foreign bond is low), whenmarginal utility is unexpectedly high. Investors will then require a positive exchange ratepremium.

A.4 Real Effects of Money?

The derivation of the pricing relations does not rule out real effects of money. In fact, noth-ing has been said about how the conditional distribution (A.3) is determined: it could bethe case that money supply changes affect output and therefore the optimal consumptiondecision. Alternatively, it could be the case that monetary policy cannot affect the averagelevel of output, but it may have an effect on the volatilities. In this case, monetary policyaffects the risk premia for financial assets, which could affect the consumption/savingstrade-off.

41

A.5 Empirical Evidence on the Pricing Relations

Reference: Soderlind and Svensson (1997)

A.5.1 UIP

Several of these relations have been studied by running “ex post” regressions. For in-stance, to test the UIP, we could add the innovation in the log exchange rate, ut+1 =

ln St+1−Et ln St+1, to both sides of (2.2) to get

ln St+1 − ln St = it − i∗

t + ut+1, (A.13)

provided UIP holds, that is, if ϕst = 0. We would test this relation by running the regres-

sionln St+1 − ln St = a + b

(it − i∗

t)+ εt+1, (A.14)

and test the null hypothesis that a = 0 and b = 1. Under the null hypothesis that UIPholds, this regression should give consistent estimates of a and b, since the innovationut+1 must (by definition) be uncorrelated with the regressors, or for that matter, everythingelse in period t or earlier.

This testing approach is a special case of the more general implication of UIP: ln St+1−

ln St − it + i∗t should be unforecastable, and therefore uncorrelated with all information

in period t .The test of the null hypothesis is, of course, a joint test of rational expectations (that

it − i∗t equals Et ln St+1 − ln St rather than some other expectation of the exchange rate

depreciation) and of no risk premia. If a 6= 0 but b = 1, then this might (under RE)be interpreted as constant risk premia, which in (A.11)-(A.12) corresponds to constantsecond moments.

The typical result from a large number of studies is that a 6= 0 but b 6= 1 (oftenb < 0). This could be due to time-varying risk premia (which requires time-varyingvariances and covariances in the theory for risk premia presented above). An alternativeexplanation is that the sample is not long enough for ex post data to produce all thejumps (devaluations) and other features that seems to be part of market expectations ofexchange rates. (The Mexican peso is the classic case, where the interest rate differentialto USD interest rates was positive for many years—and it took a very long time before the

42

realignment eventually came. In many studies, the sample ended before the realignment:the “peso problem.”) Evidence from survey data suggest that this might be the case.

A.5.2 Fisher Equation

The Fisher equation is typically tested in much the same way as UIP: inflation is relatedto the nominal interest rate and the null hypothesis is that the sum of the real interest rateand the inflation risk premium is a constant. Most empirical evidence suggests that this isnot true, in particularly not for short maturities.

A.5.3 Expectations Hypothesis of Interest Rates

The expectations hypothesis of interest rates is also tested in a similar way: future longinterest rates are related to current long interest rates. Most evidence suggest that theexpectations hypothesis of interest rates works fairly well for very short maturities, butperhaps less well for maturities of 6 months up to a couple of years. The empirical evi-dence for really long maturities is very mixed.

A.5.4 Empirical Illustrations

McCallum (1996) Fig 9.1; Soderlind and Svensson (1997) Fig 5; Soderlind (1998) Fig 2.

Bibliography

Blanchard, O. J., and S. Fischer, 1989, Lectures on Macroeconomics, MIT Press.

Burda, M., and C. Wyplosz, 1997, Macroeconomics - A European Text, Oxford UniversityPress, 2nd edn.

Isard, P., 1995, Exchange Rate Economics, Cambridge University Press.

McCallum, B. T., 1996, International Monetary Economics, Oxford University Press,Oxford.

Obstfeldt, M., and K. Rogoff, 1996, Foundations of International Macroeconomics, MITPress.

43

Romer, D., 1996, Advanced Macroeconomics, McGraw-Hill.

Soderlind, P., 1998, “Nominal Interest Rates as Indicators of Inflation Expectations,”Scandinavian Journal of Economics, 100, 457–472.

Soderlind, P., and L. E. O. Svensson, 1997, “New Techniques to Extract Market Expecta-tions from Financial Instruments,” Journal of Monetary Economics, 40, 383–420.

Walsh, C. E., 1998, Monetary Theory and Policy, MIT Press, Cambridge, Massachusetts.

44

3 Money and Sticky Prices: A First Look

Main references: Romer (1996) (Romer), Blanchard and Fischer (1989) (BF), Obstfeldtand Rogoff (1996) (OR), and Walsh (1998).

3.1 Basic Models of the Effects of Monetary Policy Surprises

3.1.1 One-Period Wage Contracts

References: BF 8.2, Romer 6.8, Walsh 5.3.The firm has a Cobb-Douglas production function so log output is

ln Yt = ln Z t + α ln Kt + (1 − α) ln ht , (3.1)

where Z t is the productivity level, Kt capital stock, and ht employment.On a competitive labor market, the log nominal wage would be

lnwt = ln Pt + ln (1 − α)+ ln Yt − ln ht . (3.2)

Instead, nominal wages are here set, one period in advance, equal to the expected valueof the market clearing wage (in logs, to simplify)

lnwt = Et−1 ln Pt + ln (1 − α)+ Et−1 ln Yt − Et−1 ln ht . (3.3)

In period t , shocks are realized and firms employ labor until the nominal marginalproduct of labor equals the nominal wage, that is, until (3.2) holds, but where is lnwt setin t − 1. This implicitly assumes that households have a flat labor supply curve.

Use (3.3) in (3.2) to get

ln ht − Et−1 ln ht = ln Pt − Et−1 ln Pt + ln Yt − Et−1 ln Yt . (3.4)

If Kt = (1 − δ) Kt−1 + It , so Kt is known in t − 1, then the innovation in log output is

ln Yt − Et−1 ln Yt = (ln Z t − Et−1 ln Z t)+ (1 − α) (ln ht − Et−1 ln ht) . (3.5)

45

Now, use (3.4) to substitute for the labor input innovation in (3.5). After rearrangementwe get

ln Yt − Et−1 ln Yt =1α(ln Z t − Et−1 ln Z t)+

(1 − α

α

)(ln Pt − Et−1 ln Pt) . (3.6)

In this model monetary policy surprises can have affect on output by causing a pricesurprise, while anticipated monetary policy cannot. For instance, if monetary policy couldreact to innovations in the productivity level, then it might be possible to stabilize output.

3.1.2 Lucas’s Model of the Phillips Curve

Reference: BF 356-361, Romer 6.1-6.4, .The Lucas model is another way to get one-period effects of monetary supply shocks.

The basic mechanism is that firm i has the supply curve

yi =1φ(pi − Ei p) , (3.7)

where pi is the firm’s price, and Ei p the expectation about the general price level basedon the information set of firm i . It is assumed that firm i observes only pi and yi and usesthese to infer the general price level. The firm cannot distinguish between real shocks(to the relative price, pi − p) and nominal shocks. It therefore reacts, to some extent,to all observed movements in pi : we get real effects of monetary policy as long as thepolicy surprise lasts - the macro implication is very similar to the sticky wage model (3.6).However, the coefficient in front of the innovation in prices here depends on the volatilityof prices, rather than on the production function parameter.

A major criticism against the Lucas model is that the misperception story is weak: theconsumer price index is published with a very short lag.

3.2 “Money and Wage Contracts in an Optimizing Model of the Busi-ness Cycle,” by Benassy

3.2.1 Baseline Model

Reference: Benassy (1995), Walsh 5.3.

46

This model is a general equilibrium model with money in the utility function, butsticky nominal wages.

The key equations are:

Utility function : E0

∞∑t=0

β t[

ln Ct + θ lnMt

Pt+ V

(h − ht

)](3.8)

Real budget constraint : Ct +Mt

Pt+ Kt+1 =

wt

Ptht + rt Kt + µt

Mt−1

Pt(3.9)

Production function : Yt = Z t K αt h1−α

t ⇒wt

Pt= (1 − α)

Yt

ht, rt = α

Yt

Kt. (3.10)

Capital accumulation : complete depreciation, Yt = Ct + Kt+1. (3.11)

This is the same model as in Long and Plosser (1983), but with money in the utilityfunction. The notation is standard, except that the nominal value in the beginning of t